creating and delivering value in the asean steel industryab4082e8-b93d-… · ·...

TRANSCRIPT

Creating and delivering value

in the ASEAN steel industry

Edwin Basson, Director General, worldsteel

Disclaimer text

This document is protected by copyright. Distribution to third parties or reproduction

in any format is not permitted without written permission from worldsteel. worldsteel

operates under the strictest antitrust guidelines. Visit worldsteel.org\About us for

detailed antitrust guidelines.

Global framework

Steel industry faces new challenge of low growth

4

474 447300 373 397 389 388 412 413 420

329 332

299348 374 391 406 415 425 442

418 447551

588641 660 735 711 707 704

6.8

0.4

-6.1

13.7

7.9

2.0

6.2

0.6 0.5 1.4

0

500

1 000

1 500

2 000

2 500

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Developed, Mt Developing ex China, Mt

China, Mt World, y-o-y % growth

-40

-30

-20

-10

0

10

20

30

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

China Developing ex China Developed

y-o-y % growth

Apparent Steel Use, finished steel (SRO April 2015)

Regional Summary Apparent Steel Use, finished steel (SRO April 2015)

2014 2015 2016 14/13 15/14 16/152016 as

% of 2007

World 1 537.3 1 544.4 1 565.5 0.6 0.5 1.4 128.2

European Union (28) 146.8 149.9 154.1 4.5 2.1 2.8 76.9

Other Europe 37.0 38.0 38.5 0.2 2.8 1.4 126.6

CIS 56.5 52.4 52.2 -4.9 -7.3 -0.3 92.7

NAFTA 144.6 143.3 145.1 11.3 -0.9 1.3 103.0

Central & South America 48.1 46.5 48.1 -3.9 -3.4 3.4 116.4

Africa 36.9 39.6 41.5 4.2 7.4 4.9 182.4

Middle East 51.9 53.3 55.6 3.7 2.8 4.2 126.7

Asia & Oceania 1 015.6 1 021.5 1 030.4 -1.0 0.6 0.9 150.3

China 710.8 707.2 703.7 -3.3 -0.5 -0.5 168.2

million tonnes (Mt) %

5

ASEAN region

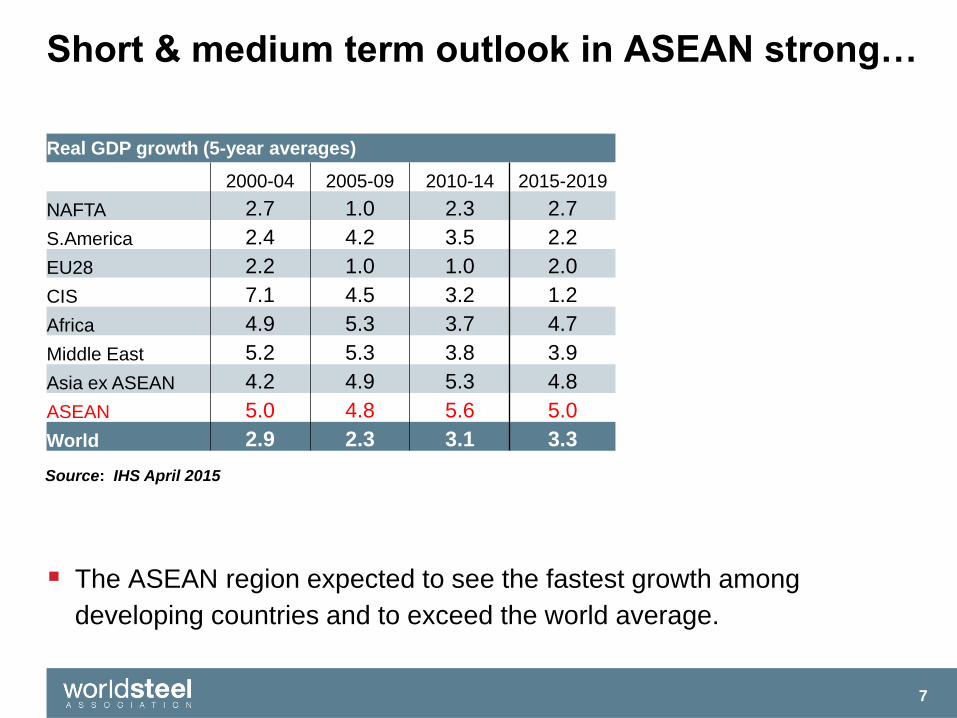

Short & medium term outlook in ASEAN strong…

The ASEAN region expected to see the fastest growth among

developing countries and to exceed the world average.

7

Source: IHS April 2015

Real GDP growth (5-year averages)

2000-04 2005-09 2010-14 2015-2019

NAFTA 2.7 1.0 2.3 2.7

S.America 2.4 4.2 3.5 2.2

EU28 2.2 1.0 1.0 2.0

CIS 7.1 4.5 3.2 1.2

Africa 4.9 5.3 3.7 4.7

Middle East 5.2 5.3 3.8 3.9

Asia ex ASEAN 4.2 4.9 5.3 4.8

ASEAN 5.0 4.8 5.6 5.0

World 2.9 2.3 3.1 3.3

…Supporting the convergence of income levels

to developed world levels

Economic development supporting income growth and gradual

convergence to the developed world.

8

GDP per capita (000’s real USD 2010 PPP)

Source: IHS April 2015

GDP per capita (000’s real USD 2010 PPP)

Developed world average: 40k USD

0

5

10

15

20

25Philippines Indonesia

Malaysia Thailand

Vietnam

2

4

6

8

10

12

14

16

18

ASEAN India China

…and helping the urbanisation process

9

Urbanisation (% of total population) ASEAN urbanisation (% of total population)

Urbanisation will continue to increase in ASEAN but at different degrees

among countries.

Source: United Nations

15

20

25

30

35

40

45

50

55

60

65ASEAN China India

15

25

35

45

55

65

75

85Philippines Malaysia

Thailand Vietnam

Indonesia

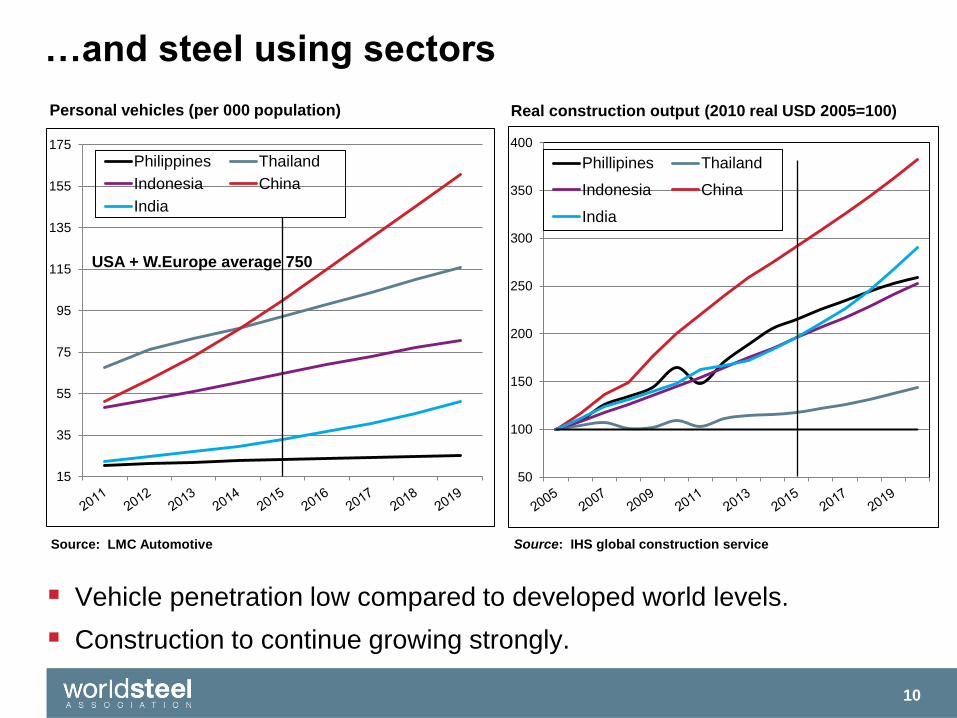

…and steel using sectors

10

Personal vehicles (per 000 population)

Vehicle penetration low compared to developed world levels.

Construction to continue growing strongly.

Real construction output (2010 real USD 2005=100)

Source: LMC Automotive Source: IHS global construction service

15

35

55

75

95

115

135

155

175

Philippines Thailand

Indonesia China

India

USA + W.Europe average 750

50

100

150

200

250

300

350

400

Phillipines Thailand

Indonesia China

India

Income and urbanisation underpin steel demand

11

ASU/capita (kg) vs Urbanisation (% of total population)

1980-2014

ASU/capita (kg) vs Urbanisation (% of total population)

1980 -2014

Source: United Nations & worldsteel

A generally strong correlation between urbanisation and apparent steel

use per capita in ASEAN countries

0

100

200

300

400

500

600

15 25 35 45 55

AS

U p

er

ca

pit

a

Urbanisation (%)

ASEAN China India

0

50

100

150

200

250

300

350

400

15 35 55 75 95A

SU

pe

r c

ap

ita

Urbanisation (%)

Philippines Malaysia

Thailand Vietnam

Indonesia

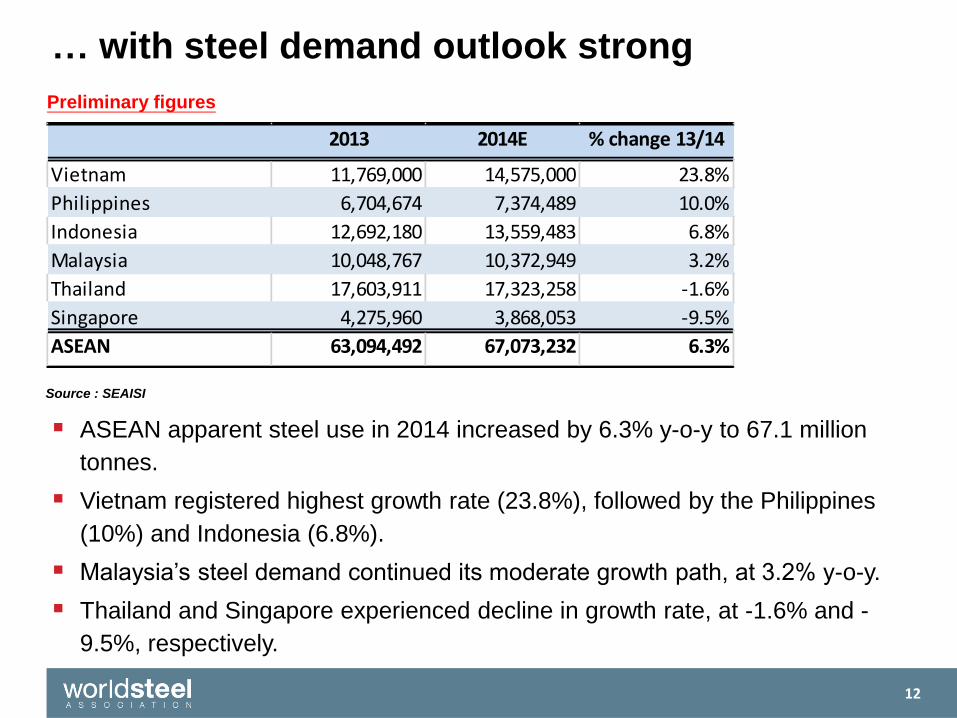

… with steel demand outlook strong

Source : SEAISI

Preliminary figures

ASEAN apparent steel use in 2014 increased by 6.3% y-o-y to 67.1 million

tonnes.

Vietnam registered highest growth rate (23.8%), followed by the Philippines

(10%) and Indonesia (6.8%).

Malaysia’s steel demand continued its moderate growth path, at 3.2% y-o-y.

Thailand and Singapore experienced decline in growth rate, at -1.6% and -

9.5%, respectively.

12

2013 2014E % change 13/14

Vietnam 11,769,000 14,575,000 23.8%

Philippines 6,704,674 7,374,489 10.0%

Indonesia 12,692,180 13,559,483 6.8%

Malaysia 10,048,767 10,372,949 3.2%

Thailand 17,603,911 17,323,258 -1.6%

Singapore 4,275,960 3,868,053 -9.5%

ASEAN 63,094,492 67,073,232 6.3%

Apparent Steel Consumption in ASEAN (million tonnes)

Source : SEAISI

30

40

50

60

70

80

90

2004

2006

2008

2010

2012

2014

E

2016

F

2018

F

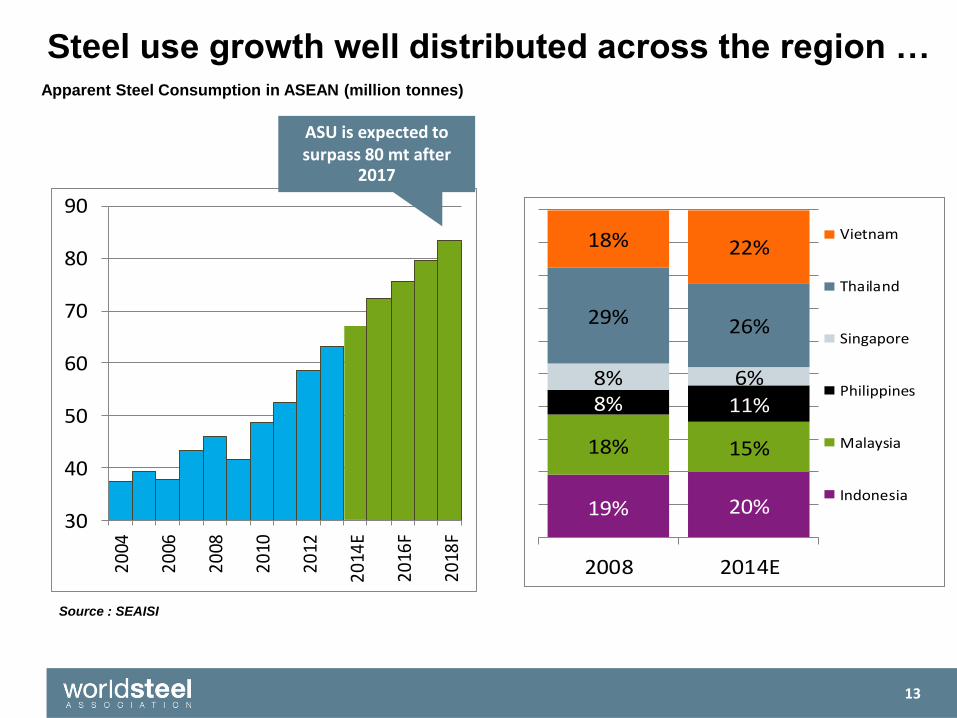

Steel use growth well distributed across the region …

ASU is expected to surpass 80 mt after

2017

19% 20%

18% 15%

8% 11%8% 6%

29% 26%

18% 22%

2008 2014E

Vietnam

Thailand

Singapore

Philippines

Malaysia

Indonesia

13

Construction, 66%

Automotive, 18%

Ship building & repair, 1%

E&E, 4%

Machinery & Industry, 3%

Packaging, 2%

Oil & Gas, 3%

Others, 3%

Construction Sector – a Major driver of steel demand in ASEAN

66% of total steel used in the region comes from construction sector

Share of steel used in construction sector in each country

14

…With construction the largest steel user

Source: SEASI

% of Construction

Contribution

Philippines 81%

Singapore 75%

Malaysia 69%

Indonesia 66%

Vietnam 60%

Thailand 60%

Steel demand outpaces capacity

Present characteristics suggests the region to remain a net importer for

some time

15

ASEAN(6): crude steel capacity vs crude ASU, Mt

Source : OECD & worldsteel

20

30

40

50

60

70

80

90

2000 2002 2004 2006 2008 2010 2012 2014 2016

Crude capacity Apparent demand

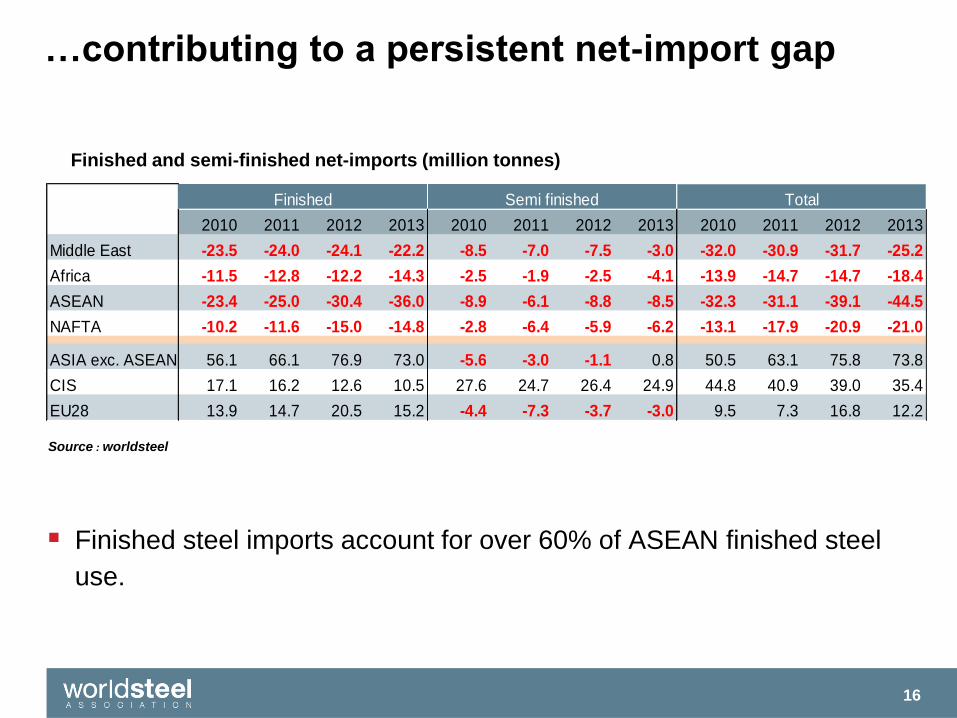

…contributing to a persistent net-import gap

16

Source : worldsteel

Finished steel imports account for over 60% of ASEAN finished steel

use.

Finished and semi-finished net-imports (million tonnes)

2010 2011 2012 2013 2010 2011 2012 2013 2010 2011 2012 2013

Middle East -23.5 -24.0 -24.1 -22.2 -8.5 -7.0 -7.5 -3.0 -32.0 -30.9 -31.7 -25.2

Africa -11.5 -12.8 -12.2 -14.3 -2.5 -1.9 -2.5 -4.1 -13.9 -14.7 -14.7 -18.4

ASEAN -23.4 -25.0 -30.4 -36.0 -8.9 -6.1 -8.8 -8.5 -32.3 -31.1 -39.1 -44.5

NAFTA -10.2 -11.6 -15.0 -14.8 -2.8 -6.4 -5.9 -6.2 -13.1 -17.9 -20.9 -21.0

ASIA exc. ASEAN 56.1 66.1 76.9 73.0 -5.6 -3.0 -1.1 0.8 50.5 63.1 75.8 73.8

CIS 17.1 16.2 12.6 10.5 27.6 24.7 26.4 24.9 44.8 40.9 39.0 35.4

EU28 13.9 14.7 20.5 15.2 -4.4 -7.3 -3.7 -3.0 9.5 7.3 16.8 12.2

Finished Semi finished Total

The future

Future regional strategy could focus on creating

and delivering value

Using steel in downstream activities can be equally value-adding than

steelmaking strategies.

Substantial regional steel supply sources create interesting development

opportunities.

Focus on delivering service

Large population with many and diverse requirements

Value chain focus could deliver sustainable returns, but require

appropriate focus on:

Training & development

Building collaborative producer relationships

Ensuring stable supply relationships

18

19

Thank you for your attention.

For further information contact:

Edwin Basson | Director General

World Steel Association [email protected] | T: +32 (0)2 702 81 87 | worldsteel.org

worldsteel.org