creative dc/db plan design & case studies

TRANSCRIPT

STRONGER

Strategies for success

2015 Partner Conference

together

Creative DB Plan Designs and Case

StudiesMaryann Geary, EVP, BPAS Plan Administration & Recordkeeping

Vince Spina, President, Harbridge Consulting Group, a BPAS Company

2015 Partner ConferenceStronger Together

Agenda

• Why Save in a Tax-Qualified Plan?• Basic Cash Balance Plan• BPAS WRAP Design (“Worker Retirement Accumulation Plan”)• The Future of DB/DC Combo Plans

2015 Partner ConferenceStronger Together

Why Save in a Tax-Qualified Plan?

The “on-the street” question……why not just save outside a plan where there is favorable capital gains treatment?

2015 Partner ConferenceStronger Together

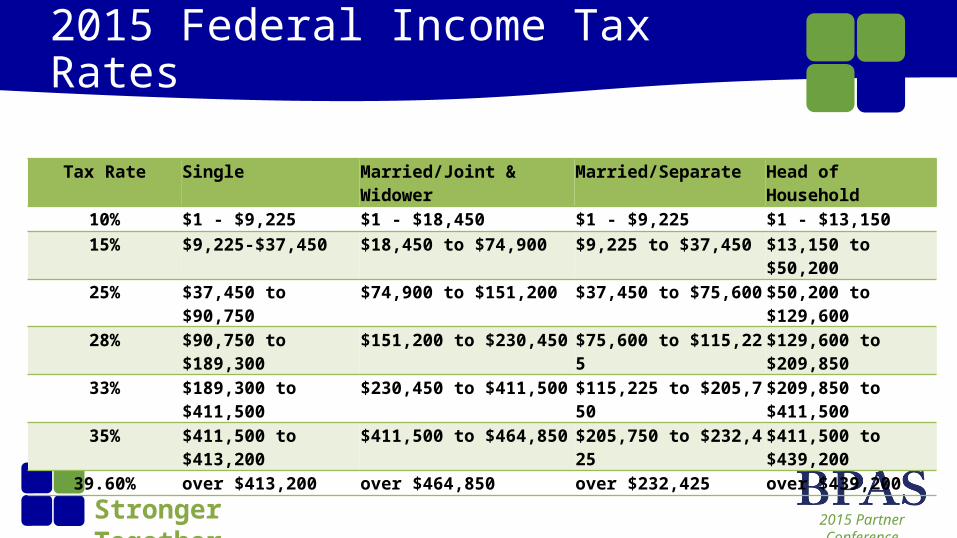

2015 Federal Income Tax Rates

Tax Rate Single Married/Joint & Widower Married/Separate Head of Household

10% $1 - $9,225 $1 - $18,450 $1 - $9,225 $1 - $13,15015% $9,225-$37,450 $18,450 to $74,900 $9,225 to $37,450 $13,150 to $50,20025% $37,450 to $90,750 $74,900 to $151,200 $37,450 to $75,600 $50,200 to $129,60028% $90,750 to $189,300 $151,200 to $230,450 $75,600 to $115,225 $129,600 to $209,85033% $189,300 to $411,500 $230,450 to $411,500 $115,225 to $205,750 $209,850 to $411,50035% $411,500 to $413,200 $411,500 to $464,850 $205,750 to $232,425 $411,500 to $439,200

39.60% over $413,200 over $464,850 over $232,425 over $439,200

2015 Partner ConferenceStronger Together

Why Save in a Tax-Qualified Plan?

One Example: Fact SetAnnual Contribution $ 100,000 Federal Income Tax Rate during savings period 39.60%State Income Tax Rate during savings period 6.85%

Tax Rate for Investments Outside Qualified Plans 21.85%Tax Rate on Income in Retirement 28.00%Investment Return in Qualified Plan 3.00%Investment Return Outside Qualified Plan 7.00%Years Saving in Qualified Plan 5

2015 Partner ConferenceStronger Together

Why Save in a Tax-Qualified Plan?

One Example: OutcomeValue After Five Years in Qualified Plan $530,914

Taxes in Retirement if Paid all at Once (148,656)

Balance After-Tax $382,258

Balance if Saving Outside Plan $298,691

Advantage of Saving in Tax Qualified Plan $ 83,567

2015 Partner ConferenceStronger Together

Why Save in a Tax-Qualified Plan?

• In this example, saving for only five years AND in a much more conservative manner AND paying the tax immediately at the end of five years, one ends up with nearly 30% more spendable dollars than if saving outside of a qualified plan.• Results are more dramatic if money is rolled over to an

IRA and withdrawn over a retirement lifetime--which is what everyone does.

2015 Partner ConferenceStronger Together

2015 DB Plan Contribution LimitsMaximum Maximum Maximum Maximum

Age Contribution Age Contribution Age Contribution Age Contribution31 $ 56,000 41 $ 92,000 51 $151,000 61 $249,000 32 $ 59,000 42 $ 97,000 52 $159,000 62 $262,000 33 $ 62,000 43 $102,000 53 $167,000 63 $256,000 34 $ 65,000 44 $107,000 54 $176,000 64 $250,000 35 $ 68,000 45 $112,000 55 $185,000 65 $244,000 36 $ 72,000 46 $118,000 56 $194,000 66 $257,000 37 $ 75,000 47 $124,000 57 $204,000 67 $270,000 38 $ 79,000 48 $130,000 58 $214,000 68 $280,000 39 $ 83,000 49 $137,000 59 $225,000 69 $267,000 40 $ 88,000 50 $144,000 60 $237,000 70 $260,000

2015 Partner ConferenceStronger Together

Cash Balance Plans

Participants have notional account balances• Service Credits (e.g., 2.5% of pay or a flat amount such as $100,000)

and Interest Credits — A fixed amount (e.g., 3%)— Tied to an index (e.g., 5- or 10-year Treasury yields) that changes year to

year, or— The actual return on plan assets— If the actual return on plan assets is used, there is a minimum floor of 0%

return over a participant’s career (but can have a negative return for a particular year)

2015 Partner ConferenceStronger Together

Cash Balance Plans

• What makes a Cash Balance Plan a Defined Benefit Plan?

— “Defined” interest credits— Ability to annuitize account balances at retirement

within the plan— As a result, DB plan limits apply (i.e. not the

$53,000 DC plan limit)• Plan assets don’t need to equal the sum of account

balances

2015 Partner ConferenceStronger Together

Cash Balance Plans

• Need to satisfy non-discrimination rules— Generally need to provide rank and file a contribution of

7.5% of pay between the 401(k) Plan and Cash Balance Plan

• Assets are in a pooled account— Participants do NOT have individual direction of account

balance— All participants get the same investment return

2015 Partner ConferenceStronger Together

Cash Balance Plans

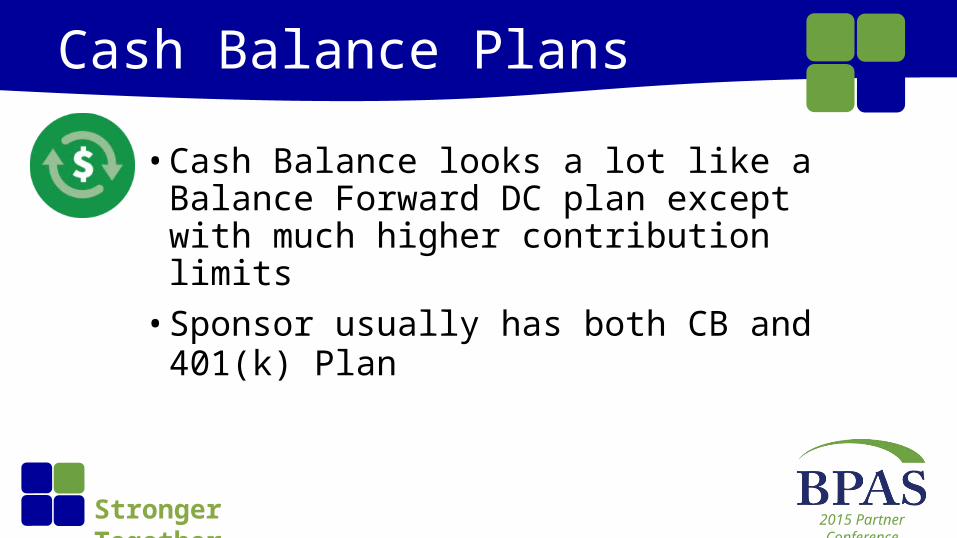

• Cash Balance looks a lot like a Balance Forward DC plan except with much higher contribution limits• Sponsor usually has both CB and 401(k) Plan

2015 Partner ConferenceStronger Together

Cash Balance PlansTypical Plan Design

• 5% of pay for rank and file• Maximum contribution for owners• No matching contribution

401(k) Plan

• 2.5% of pay for rank and file• Contribution for owner based on

Survey Results (up to maximum limit)

CB Plan

2015 Partner ConferenceStronger Together

Cash Balance Plan - Example

Contribution Credit • Owner: $100,000 • Employees: 2.5% of W-2

Interest Credit: 3.0% Compounded Annually

2015 Partner ConferenceStronger Together

Cash Balance Plan - Example

Owner Employee Owner Employee

W-2 Pay $265,000 $40,000 $265,000 $41,000

1/1/2015 Balance $ - $ - 1/1/2016 Balance $ 100,000 $ 1,000

Interest Credit $ - $ - Interest Credit $ 3,000 $ 30 Service Based Credit $ 100,000 $ 1,000 Service Based Credit $ 100,000 $ 1,025

12/31/2015 Balance $ 100,000 $ 1,000 12/31/2016 Balance $ 203,000 $ 2,055

2015 Partner ConferenceStronger Together

Cash Balance Plans – Investments

• Maximum amount that may be accumulated on behalf of an individual in a CB plan is about $2.6M at age 62• Because of this cap, plan assets tend to be

invested more conservatively….taking significant investment risk just gets owner to the maximum lump sum sooner

2015 Partner ConferenceStronger Together

Cash Balance Plans – Investments

2015 Partner ConferenceStronger Together

Potential Medicare Tax Savings

• To the extent contributions to a Qualified Plan result in reduction to owner’s W-2 pay, there may be a significant Medicare tax savings— Applies to corporate sponsors— Not applicable for sole proprietors or partnerships

• In many situations, savings in Medicare tax is more than the cost of administration

2015 Partner ConferenceStronger Together

FICA Tax Savings – Actual BPAS Client Employer CB Plan

Year Contributions2013 $ 1,422,500 2014 $ 1,315,999 2015 $ 1,466,000

Cumulative CB Plan Contributions (2013 -2015) $ 4,204,499

Reduction in Employer Medicare Tax (1.45%) $ 60,965 Reduction in Employee Medicare Tax (2.35%) $ 98,806

Total reduction in Medicare Taxes (2013 - 2015) $ 159,771 BPAS Fees (2013-2015) $ (32,580)

Net Savings to PC Owners (2013-2015) $ 127,191

2015 Partner ConferenceStronger Together

Potential Cash Balance Plan Clients

A Financial Advisor should discuss a Cash Balance Plan with any Company whose top employees earn more than $350,000 annually• Not discussing this will put your relationship

at risk

2015 Partner ConferenceStronger Together

Potential Cash Balance Plan Clients

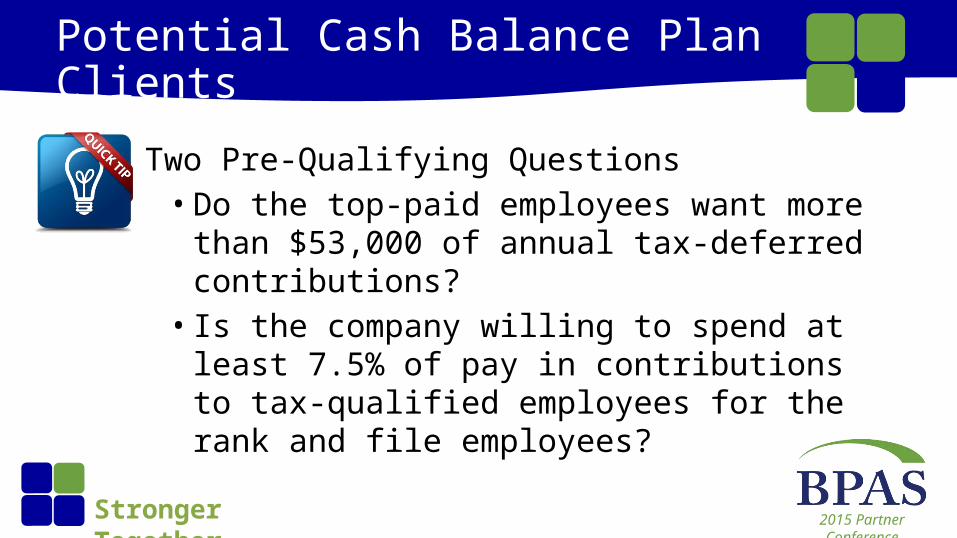

Two Pre-Qualifying Questions• Do the top-paid employees want more than $53,000

of annual tax-deferred contributions?• Is the company willing to spend at least 7.5% of pay

in contributions to tax-qualified employees for the rank and file employees?

2015 Partner ConferenceStronger Together

BPAS WRAP Design

• BPAS WRAP Design (“Worker Retirement Accumulation Plan”)—a Second Generation Cash Balance Plan Design• Basic Cash Balance Plan with one difference

—interest credit in Cash Balance Plan is replaced with a contribution to the 401(k) Plan

2015 Partner ConferenceStronger Together

WRAP Plan - Example

Cash Balance PlanContribution Credit:

5.0% of W-2

Interest Credit: 3.0% of Beginning of YearBalance in Cash Balance Plan made as a contribution to the 401(k) Plan

2015 Partner ConferenceStronger Together

WRAP Plan - Example

401(k) 401(k)WRAP WRAP

CB Plan Account CB Plan AccountW-2 Pay of Participant $ 50,000 $ 50,000 $ 51,000 $ 51,000 1/1/2015 Balance $ - $ - 1/1/2016 Balance $ 2,500 $ - Interest Credit $ - $ - Interest Credit $ - $ 75 Service Based Credit $ 2,500 $ - Service Based Credit $ 2,550 $ -

12/31/2015 Balance $ 2,500 $ - 12/31/2016 Balance $ 5,050 $ 75

2015 Partner ConferenceStronger Together

BPAS WRAP Design – Why?

• For the same contribution credit (e.g., 5% of pay), 401(k) Expense > Traditional CB Expense > WRAP Expense• For some BPAS clients, resulting book expense savings

can be more than $.03 per share*

* Anything more than $.01 per share gets a CFO’s attention

2015 Partner ConferenceStronger Together

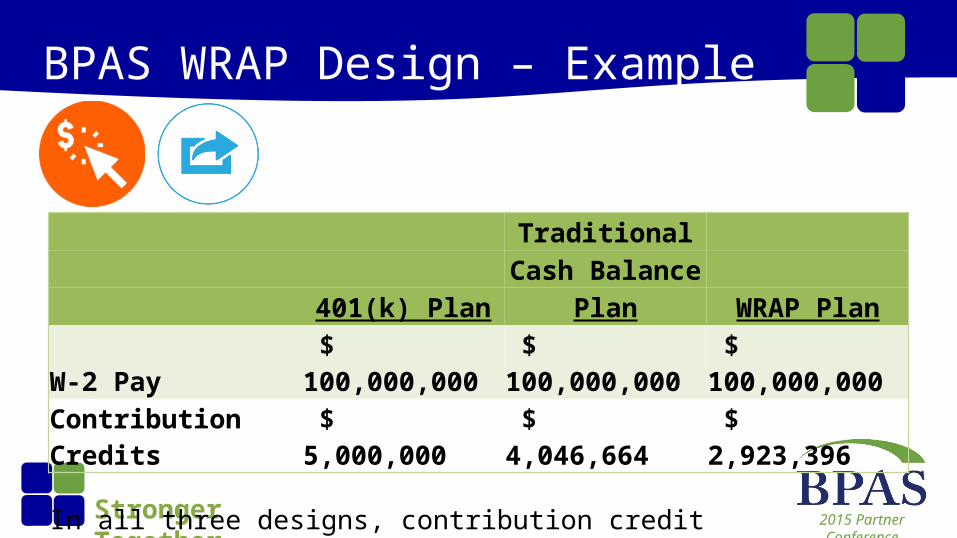

BPAS WRAP Design – Example

TraditionalCash Balance

401(k) Plan Plan WRAP PlanW-2 Pay $ 100,000,000 $ 100,000,000 $ 100,000,000 Contribution Credits $ 5,000,000 $ 4,046,664 $ 2,923,396

In all three designs, contribution credit is 5% of pay

2015 Partner ConferenceStronger Together

BPAS WRAP Design – Who?

Who would be interested in a WRAP Plan Design?• Public companies where book expense is a primary

issue• Any sponsor of a DB plan that was already

converted into a Cash Balance Plan

2015 Partner ConferenceStronger Together

DB/DC Combo Plans

• What is the Current State of these plans?• Generally at Retirement:• DC Plan, take rollover distribution to IRA

• DC industry has been focused on “catching the rollover”• DB Plan, make one time election of an annuity

from plan

2015 Partner ConferenceStronger Together

DB/DC Combo Plans

Suppose someone earning $50,000 has done everything right and accumulated $500,000 (i.e., 10 x pay) at age 65• What do they do? Rollover to IRA and draw

down over their retirement?• Does this maximize their lifestyle in retirement?• What about a guaranteed life annuity?

2015 Partner ConferenceStronger Together

Comparison of Annual Income from$500K Accumulated at Age 65

Purchase Transfer toLife Annuity DB Plan &

Keep in Plan Keep in Plan From Purchase4% Drawdown 5% Drawdown Insurer Annuity

Female $ 20,000 $ 25,000 $ 30,900 $ 35,997 Male $ 20,000 $ 25,000 $ 33,000 $ 35,997

Insurance company annuity rates generated from www.immediateannuities.com

DB Plan annuities based on IRC 417(e) rates for 2015

2015 Partner ConferenceStronger Together

The Future of DB/DC Combo Plans

What about a very flexible structure, using DB plan for lifetime income, and DC plan for structured payments for fixed period with ability to access remaining account balance if needed?

2015 Partner ConferenceStronger Together

The Future of DB/DC Combo Plans

Example: Age 65 Retiree has accumulated $200,000 in Cash Balance Plan, $800,000 in 401(k) Plan, $1,000,000 in totalWhat is available….and what could be available?

2015 Partner ConferenceStronger Together

The Future of DB/DC Combo Plans

$1,000,000 $200,000 $800,000 in Qualified

CB Balance 401(k) Balance Plan BalancesTake Rollovers and then take 5% Drawdown $10,000 $40,000 $50,000 CB Plan: Life Annuity/DC Plan: 5% Drawdown $14,399 $40,000 $54,399 Transfer DC to DB and take all as a life annuity $71,994 $0 $71,994 Transfer $494,500 from DC to DB to generate $50,000 $35,814 $85,814 for 10 years$50,000 in lifetime income, drawdown remainder for 10 years $50,000 thereafterfrom DC plan in 10 annual payments(assume 3% annual earnings in DC Plan)

2015 Partner ConferenceStronger Together

The Future of DB/DC Combo Plans

Historic DB/DC combo plans have had distribution options that have been too rigid; technology will make the type of options illustrated easily accessible

2015 Partner ConferenceStronger Together

Questions

Thank you

2015 Partner ConferenceStronger Together

BPAS DB Plan Contacts

Vince Spina [email protected] (315) 703-8999Ken Prell [email protected] (315) 703-8993Jason Disco [email protected] (315) 703-8916

STRONGER

Strategies for success

2015 Partner Conference

together

Creative DC/DB Plan Design & Case

Studies

Maryann Geary, EVP, BPAS Plan Administration

& Recordkeeping

Vince Spina, President, Harbridge Consulting

Group, a BPAS Company

2015 Partner ConferenceStronger Together

Things to Consider• Plan Sponsor’s Needs

—Flexibility—Desired Contributions—Administrative Complexity and Expenses

• Employer and Employee Demographics—Entity Type—Employee Demographics—Plan Features

2015 Partner ConferenceStronger Together

Traditional 401(k)

Advantages• Elective Deferrals• Catch-up contributions• Discretionary employer

contributions• Employer contributions can be

subject to vesting schedule

• Employees working less than 1,000 hours can be excluded as well as employees under 21 or who have been employed less than one year

• Loans and hardships can be offered

2015 Partner ConferenceStronger Together

Traditional 401(k)

Disadvantages• ADP/ACP test can limit HCE contributions• Fiduciary responsibilities• Adds an administrative burden with payroll complexity,

frequent plan deposits, testing and reporting costs

2015 Partner ConferenceStronger Together

Traditional 401(k)

Best for companies that:• Don’t want to commit to employer contributions• Have HCEs that are willing to accept contribution

limitations• Expect good NHCE participation• Have payroll systems in place to handle withholding

and are able to provide data in a timely manner

2015 Partner ConferenceStronger Together

401(k) — Automatic Contribution

Advantages• Increased NHCE participation

improves ADP• Possible extension of ADP refund

deadline to 6 months

• Increases savings of the employee population increasing the likelihood that employees will have sufficient funds at retirement

2015 Partner ConferenceStronger Together

401(k) — Automatic Contribution

Disadvantages• Still possible that testing will fail even

with increased participation• Administrative burden of application

of automatic contributions and notices to employees

• An EACA can not be started mid-year• May result in small account balances• Matching contributions will likely be

higher with increased participation

2015 Partner ConferenceStronger Together

401(k) — Automatic Contribution

Best for companies that:• Don’t want to commit to employer contributions• Want to increase participation among NHCEs, but

can’t afford a safe harbor plan• Want to encourage a culture of saving• Have payroll systems in place to handle withholding,

track enrollment amounts and dates and provide data in a timely manner

2015 Partner ConferenceStronger Together

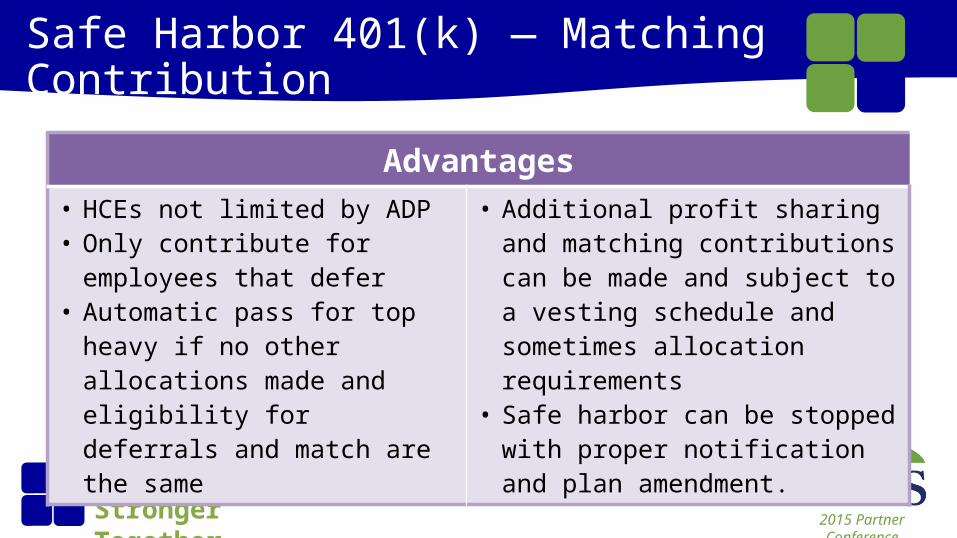

Safe Harbor 401(k) — Matching Contribution

Advantages• HCEs not limited by ADP• Only contribute for employees that

defer• Automatic pass for top heavy if no

other allocations made and eligibility for deferrals and match are the same

• Additional profit sharing and matching contributions can be made and subject to a vesting schedule and sometimes allocation requirements

• Safe harbor can be stopped with proper notification and plan amendment.

2015 Partner ConferenceStronger Together

Safe Harbor 401(k) — Matching Contribution

Disadvantages• Matching contributions required• Additional notices must be provided• Safe harbor contribution must be 100% vested• No allocation requirements permitted on safe harbor

contribution

2015 Partner ConferenceStronger Together

Best for companies that:• Have HCEs that want to maximize deferrals• Can afford to make required contributions• Don’t mind contributing to employees who defer• Expect poor NHCE participation• May want to make additional contributions in good years• Are concerned about top heavy and don’t want to

contribute to employees who don’t defer

Safe Harbor 401(k) — Matching Contribution

2015 Partner ConferenceStronger Together

Safe Harbor — Non-elective

Advantages• HCEs are not limited by ADP• Provide savings for all employees• Non-elective acts as a base for

additional profit sharing, top heavy or new comparability allocation

• Additional profit sharing or match can be made and can be subject to a vesting schedule and sometimes allocation requirements• A maybe notice can be issued to

delay final decision until closer to plan-year end

2015 Partner ConferenceStronger Together

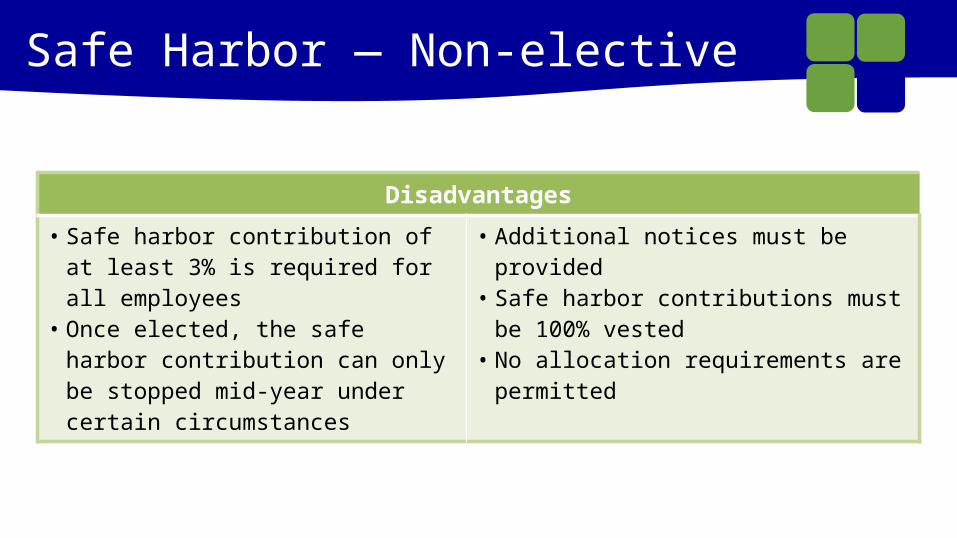

Safe Harbor — Non-elective

Disadvantages

• Safe harbor contribution of at least 3% is required for all employees

• Once elected, the safe harbor contribution can only be stopped mid-year under certain circumstances

• Additional notices must be provided• Safe harbor contributions must be 100%

vested• No allocation requirements are permitted

2015 Partner ConferenceStronger Together

Safe Harbor — Non-elective

Best for companies that:• Have HCEs that want to maximize deferrals• Can afford to make the required contribution• Want to contribute something for each employee• Expect poor employee participation• Do not have high turnover after one year or service• Likely to make additional contributions in good years

2015 Partner ConferenceStronger Together

QACA Safe Harbor 401(k) — Match

Advantages• HCEs not limited by ADP• NHCE participation higher in plans

with automatic enrollment• Only contribute to employees that

participate• Automatic pass for top heavy if no

other contributions are made

• Can be subject to a vesting schedule as long as contributions are 100% vested after 2 years• Maximum match is 3.5% compared

to 4% for traditional safe harbor• Additional profit sharing

contribution can be made and subject to a vesting schedule and sometimes allocation requirements

2015 Partner ConferenceStronger Together

QACA Safe Harbor 401(k) — Match

Disadvantages• Matching contribution required• Additional notices must be provided• Increased participation due to automatic enrollment may increase

administrative burden• No allocation requirements on safe harbor contribution

2015 Partner ConferenceStronger Together

QACA Safe Harbor 401(k) — Match

Best for companies that:• Have HCEs that want to maximize deferrals• Can afford to make required contributions• Don’t mind contributing to employees who defer• Want to encourage saving by their employees • May want to make additional contributions in good years• Are concerned about top heavy and don’t want to

contribute for employees that don't defer

2015 Partner ConferenceStronger Together

QACA Safe Harbor 401(k) — Non-Elective

Advantages• HCEs not limited by ADP• NHCE participation higher in plans

with automatic enrollment• Some savings for all employees

through non-elective contributions and encourages employees to contribute to retirement

• Non-elective contributions act as a base for additional profit sharing, top heavy or new comparability • Two-year cliff vesting can save a lot if

employer has high turnover in the first two years of employee’s employment• Additional profit sharing contribution

can be made and subject to vesting schedule and sometimes allocation requirements

2015 Partner ConferenceStronger Together

QACA Safe Harbor 401(k) — Non-Elective

Disadvantages• Safe Harbor contribution is required• Additional notices must be provided• No allocation requirements on safe harbor contribution• A Maybe notice is not available• Contribution are required even for employees that do not defer

2015 Partner ConferenceStronger Together

QACA Safe Harbor 401(k) — Non-Elective

Best for companies that:• Have HCEs that want to maximize deferrals• Can afford to make required contributions• Don’t mind contributing to employees who defer• Want to encourage saving by their employees • May want to make additional contributions in good years• Are concerned about top heavy and don’t want to

contribute for employees that don't defer

2015 Partner ConferenceStronger Together

Profit Sharing Only Plan

Advantages• Less administrative complexity

and cost compared to plan with deferrals

• Contributions are discretionary• Contributions can be subject to a

vesting schedule

• Can have allocation conditions• Several types of allocation formulas

available• Can require 2 years of service to

participate

2015 Partner ConferenceStronger Together

Profit Sharing Only Plan

Disadvantages• Depending on demographics, it might be significantly more expensive

to maximize the HCES• Employees aren’t able to contribute to their own retirement

2015 Partner ConferenceStronger Together

Pro Rata AllocationBest for companies that:• Want to keep the plan simple• Are okay with contributing the same percentage of

compensation to HCEs as to NHCEs

2015 Partner ConferenceStronger Together

Integrated AllocationBest for companies that:• Want to provide a greater benefit to employees with

higher compensation without additional testing• Have HCE compensation that is quite a bit higher than

NHCE compensation• Have owners with high compensation that are younger

than some or most of the NHCEs

2015 Partner ConferenceStronger Together

New Comparability AllocationBest for companies that:• Have HCEs who are older than at least a few of the NHCEs• Have a fairly stable workforce demographic• Have HCEs that want to receive the maximum contribution

while contributing as little as possible to the NHCEs• Don’t mind making the gateway contribution of the lesser of 5%

or 1/3 of the highest HCE contribution percentage• Want flexibility to provide different contribution levels to

different employees

2015 Partner ConferenceStronger Together

Age-Weighted AllocationBest for companies that:• Have all HCEs who are older than all of the NHCEs• Have a very stable workforce• Have HCEs that want to maximize contributions for

themselves while contributing as little as possible for NHCEs• Have demographics to support contributions of less

than the gateway to NHCEs

2015 Partner ConferenceStronger Together

Defined Benefit Plan

Advantages

• Can have higher deductible contribution than DC plan

• Older employees can accumulate large benefits more quickly than in a DC plan

• Can have contributions in excess of the §415 limit for DC plans

• Provides a predictable benefit to employees

• Provides larger benefits for older/longer service employees

• Generally insured by PBGC

2015 Partner ConferenceStronger Together

Defined Benefit PlanDisadvantages

• Can be hard to understand and may not be appreciated by employees

• Required contributions must be made annually and can fluctuate each year based on investment performance and demographic changes

• The employer bears the investment risk• Employees generally cannot contribute to

their own retirement• Administrative cost and complexity is higher

than many other plan types

2015 Partner ConferenceStronger Together

Defined Benefit PlanBest for Companies that:• Have stable long-term profits, can afford to make required

contributions• Have HCEs who are older with more years of service than

NHCEs• Want to fund a large benefit for older owners in a short

period of time• Want to make sure employees are able to retire

2015 Partner ConferenceStronger Together

Defined Benefit PlanBest for Companies that:• Want to make deductible contributions in excess of 25%

of eligible compensation• Want to contribute more than the maximum contribution

available under a DC plan for some employees

2015 Partner ConferenceStronger Together

Employee Stock Ownership Plan

Advantages• Provides ownership mentality for

employees• Possible business succession tool• Can provide tax advantages to the

selling owner• Can be leveraged

• Creates a market for the stock of a closely held corporation

• Interest and dividends in excess of the 25% of compensation limitation may be deductible

2015 Partner ConferenceStronger Together

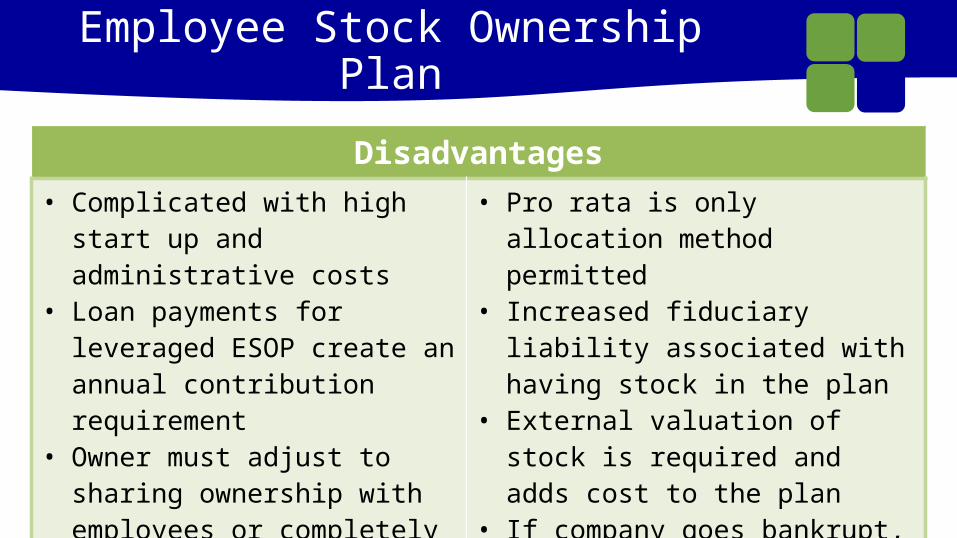

Employee Stock Ownership Plan

Disadvantages• Complicated with high start up and

administrative costs• Loan payments for leveraged ESOP

create an annual contribution requirement

• Owner must adjust to sharing ownership with employees or completely transferring ownership to employees

• Pro rata is only allocation method permitted

• Increased fiduciary liability associated with having stock in the plan

• External valuation of stock is required and adds cost to the plan

• If company goes bankrupt, ESOP accounts may become worthless

2015 Partner ConferenceStronger Together

Employee Stock Ownership Plan

Best for companies that:• Have stable long-term profits• Want to transfer ownership to employees• Want to create a market for shares of a closely held

company• Want to deduct more than 25% of eligible

compensation

2015 Partner ConferenceStronger Together

Case Study #1• Dr. Jalil contacts you about a retirement plan. He and his partner want

to start saving $50,000 each per year for retirement. Dr. Jalil’s wife acts as the office manager and comes into the office bi-weekly to process payroll.

• Dr. Jalil wants flexibility in contributions as he and his partner have children entering college and they may need cash. He does not want to add an administrative burden for his wife. His staff is older than he and his partner. He does not object to making contributions for his staff as long as he can subject them to a vesting schedule. He anticipates that his staff will remain at the current level for at least three years.

2015 Partner ConferenceStronger Together

Case Study #2

In a conversation with Jewel, owner of the gym you frequent, she mentions that she would like to purchase some new gym equipment. However, the equipment is expensive and the financing would require increased net profits after paying corporate taxes. Jewel is also interested in establishing a retirement plan and wants to know if there is a plan type that can help her achieve both goals.

2015 Partner ConferenceStronger Together

Case Study #3Jeffrey owns a fitness company and wants to encourage employees to increase productivity and decrease expenses. He is also looking for a higher return on his investments and would like to save taxes and corporate cash flow. His key executives would like ownership in the company. Many of his employees have significant longevity and he would like to reward them with a piece of the profitability they helped to create.

2015 Partner ConferenceStronger Together

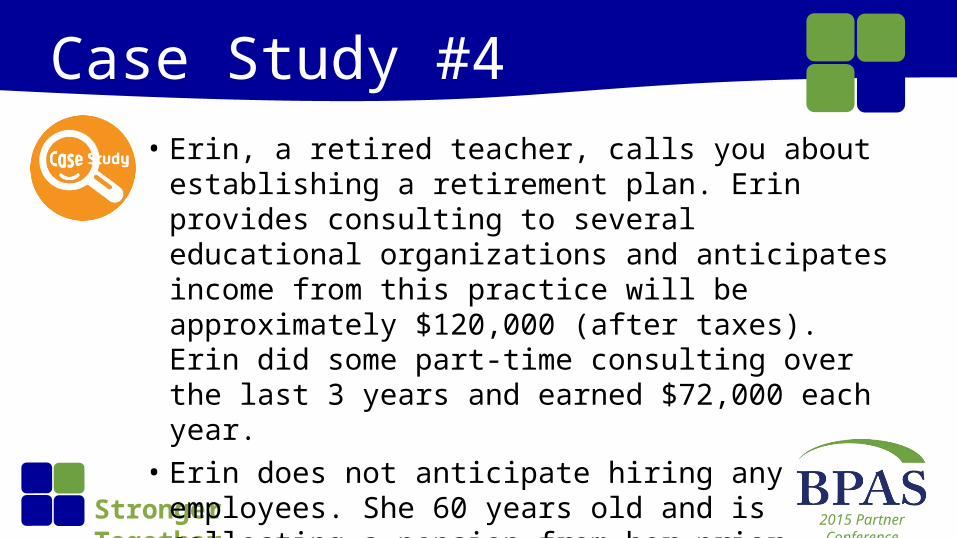

Case Study #4• Erin, a retired teacher, calls you about establishing a

retirement plan. Erin provides consulting to several educational organizations and anticipates income from this practice will be approximately $120,000 (after taxes). Erin did some part-time consulting over the last 3 years and earned $72,000 each year.

• Erin does not anticipate hiring any employees. She 60 years old and is collecting a pension from her prior employer’s plan. She plans to continue her consulting services for another 5 years

2015 Partner ConferenceStronger Together

Case Study #5• You meet Dr. Baker, sole owner of Lakeside Dental. Her husband works

at Lakeside Dental as the Office Manager and processes payroll in QuickBooks.

• Dr. Baker wants flexibility in contributions because she plans to buy equipment in the next few years.

• She wants to minimize administration for her husband.• She has two employees in addition to her husband and herself – a

hygienist and a receptionist. • Most of her staff is older than she and she’d like to make a contribution

for them. She does want to retain her current staff and does not anticipate any new hires for the next five years

2015 Partner ConferenceStronger Together

Case Study #6• During a round of golf, your friend, Jim, tells you he wants to begin saving

for retirement. Jim has a small business and his mother works for him as an assistant doing payroll and HR.

• Jim would like flexibility in contributions and he is concerned about the administrative burden on his mother; payroll takes her away from her other duties.

• Jim has one staff member, Jack, who is younger than he. Jim wants to provide Jack with a substantial benefit. He would also like to maximize the benefit to his mother. He would like to subject the contributions to a vesting schedule. One of his goals is to retain Jack as an employee.

• He does not anticipate any staff increases in the foreseeable future

2015 Partner ConferenceStronger Together

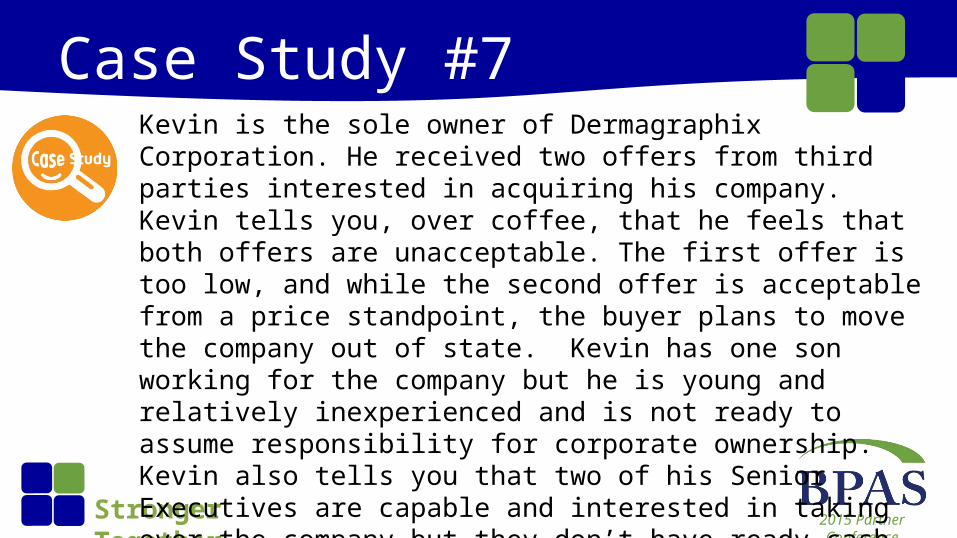

Case Study #7Kevin is the sole owner of Dermagraphix Corporation. He received two offers from third parties interested in acquiring his company. Kevin tells you, over coffee, that he feels that both offers are unacceptable. The first offer is too low, and while the second offer is acceptable from a price standpoint, the buyer plans to move the company out of state. Kevin has one son working for the company but he is young and relatively inexperienced and is not ready to assume responsibility for corporate ownership. Kevin also tells you that two of his Senior Executives are capable and interested in taking over the company but they don’t have ready cash to buy Kevin out. Kevin asks you if he should accept one of the offers or if you have another option that he should consider

2015 Partner ConferenceStronger Together

Case Study #8A few years later, you get another call from Kevin. The ESOP that you helped him establish is working very well. However, Kevin is concerned he won’t have enough money saved for retirement. He has 25 employees now, including himself and his wife. Everyone is under the age of 30, except Kevin and his wife. Kevin uses an outside payroll vendor and has an office manager that is extremely computer savvy. Kevin suspects that many of his employees are not saving for their retirement outside of the ESOP and he wants to help them achieve a comfortable retirement. He also wants to make the maximum contribution for himself and his wife, which he has determined to be $50,000+ per year

2015 Partner ConferenceStronger Together

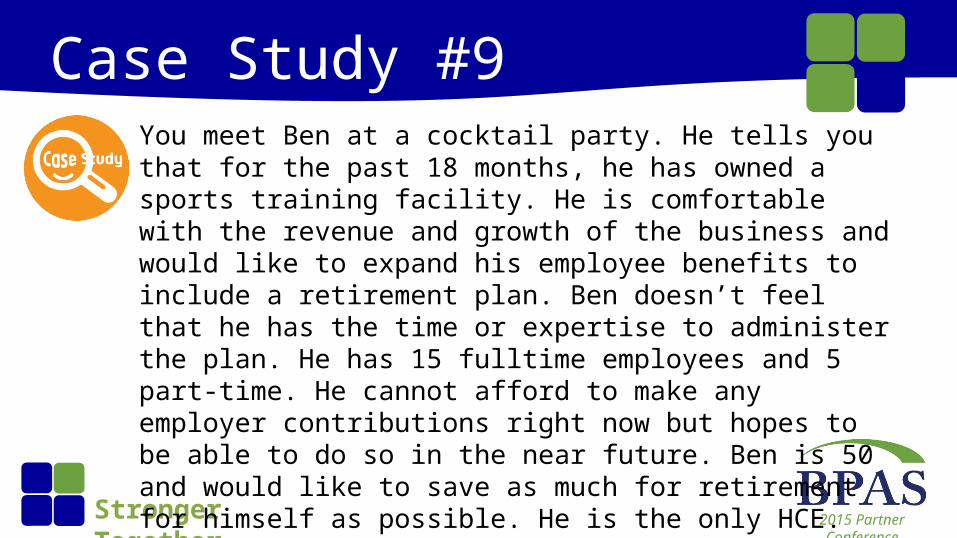

Case Study #9You meet Ben at a cocktail party. He tells you that for the past 18 months, he has owned a sports training facility. He is comfortable with the revenue and growth of the business and would like to expand his employee benefits to include a retirement plan. Ben doesn’t feel that he has the time or expertise to administer the plan. He has 15 fulltime employees and 5 part-time. He cannot afford to make any employer contributions right now but hopes to be able to do so in the near future. Ben is 50 and would like to save as much for retirement for himself as possible. He is the only HCE. He currently uses an outside payroll vendor that also provides a platform for their health benefits.

2015 Partner ConferenceStronger Together

Case Study #10• You get a call from Ryan who is interested in establishing a

retirement plan. He heard about a plan that allows him to accumulate substantial dollars for his retirement while providing modest benefits for his employees. He tells you that he is a dentist with 8 employees. He wants to start saving for retirement and wants his contributions to be pre-tax.

• Ryan purchased the practice 20 years ago after having worked for the prior owner for several years. The practice is now incorporated and has elected Sub-chapter S status. 7 employees have worked with Ryan for more that 2 years. The practice has a solid client base and income is fairly steady.

2015 Partner ConferenceStronger Together

Case Study #10• Ryan would like to see proposals that would provide him with a

contribution of $150,000 while keeping contributions to employees in the 5-10% of compensation range. Ryan does not want to provide different contribution percentages for different employees as he fears this may lead to personnel problems.

• Ryan currently sponsors a safe harbor 401(k) plan with a new comparability formula.

• There are several employees the same age or older than Ryan.

2015 Partner ConferenceStronger Together

Case Study #11• During 2014, you get a call from George who is interested in establishing a

retirement plan. George is an independent insurance agent with no employees and no plans to ever hire another person. He is 50 years old and has not really made any plans for retirement other than annual contributions to a traditional IRA. He would like to retire at age 62 and wants to be able to continue his current standard of living. He is also very interested in reducing his tax burden.

• George explains that he has built up a substantial group of clients that are very loyal to him. His income has grown over the last 20 years at an annual rate of 7%-10% and he foresees this continuing into the future. His net Schedule C was $350,000 and he has a high 3-year average of over $255,000.

2015 Partner ConferenceStronger Together

QuestionsMaryann Geary, SVP, Plan

Administration and Recordkeeping Services, BPAS

Vince Spina, President, Harbridge Consulting Group, a BPAS Company

Thank you