cred trans

DESCRIPTION

gTRANSCRIPT

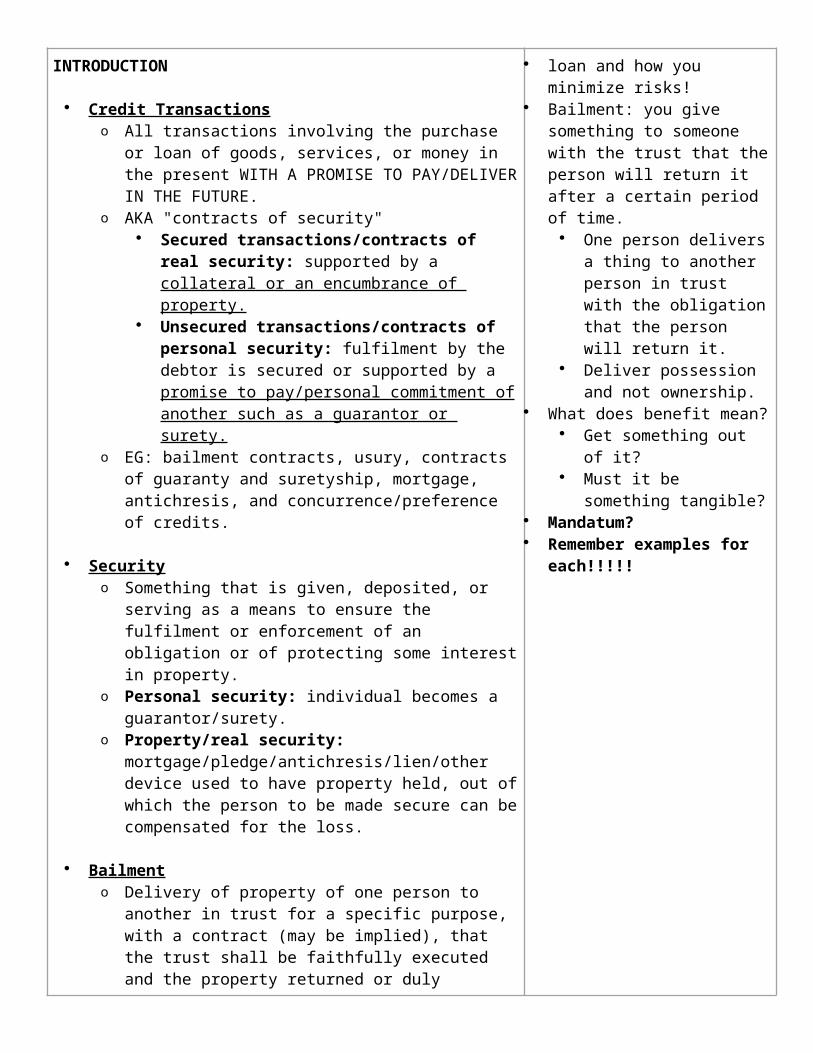

INTRODUCTION

Credit Transactions o All transactions involving the purchase or loan of goods,

services, or money in the present WITH A PROMISE TO PAY/DELIVER IN THE FUTURE.

o AKA "contracts of security" Secured transactions/contracts of real security:

supported by a collateral or an encumbrance of property.

Unsecured transactions/contracts of personal security: fulfilment by the debtor is secured or supported by a promise to pay/personal commitment of another such as a guarantor or surety.

o EG: bailment contracts, usury, contracts of guaranty and suretyship, mortgage, antichresis, and concurrence/preference of credits.

Security o Something that is given, deposited, or serving as a means to

ensure the fulfilment or enforcement of an obligation or of protecting some interest in property.

o Personal security: individual becomes a guarantor/surety.o Property/real security:

mortgage/pledge/antichresis/lien/other device used to have property held, out of which the person to be made secure can be compensated for the loss.

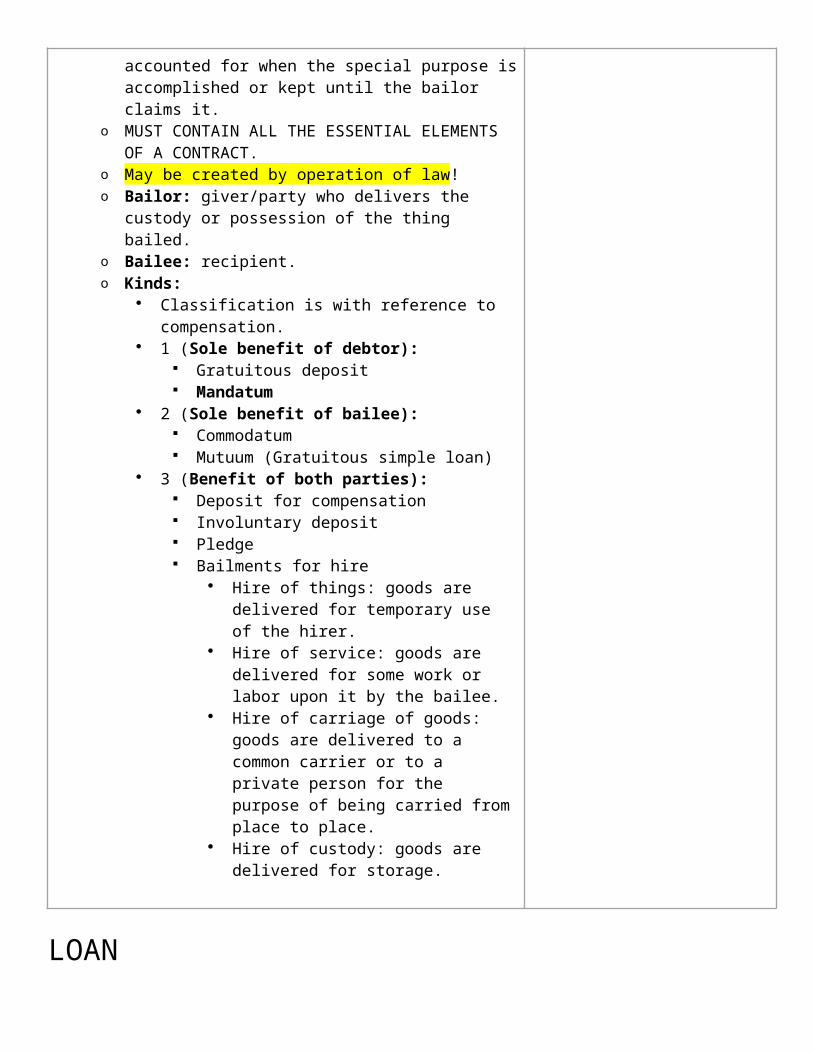

Bailment o Delivery of property of one person to another in trust for a

specific purpose, with a contract (may be implied), that the trust shall be faithfully executed and the property returned or duly accounted for when the special purpose is accomplished or kept until the bailor claims it.

o MUST CONTAIN ALL THE ESSENTIAL ELEMENTS OF A CONTRACT.

o May be created by operation of law!o Bailor: giver/party who delivers the custody or possession of

the thing bailed.o Bailee: recipient.o Kinds:

Classification is with reference to compensation. 1 (Sole benefit of debtor):

Gratuitous deposit Mandatum

2 (Sole benefit of bailee): Commodatum Mutuum (Gratuitous simple loan)

3 (Benefit of both parties): Deposit for compensation Involuntary deposit

loan and how you minimize risks! Bailment: you give something to

someone with the trust that the person will return it after a certain period of time.

One person delivers a thing to another person in trust with the obligation that the person will return it.

Deliver possession and not ownership.

What does benefit mean? Get something out of it? Must it be something

tangible? Mandatum? Remember examples for

each!!!!!

Pledge Bailments for hire

Hire of things: goods are delivered for temporary use of the hirer.

Hire of service: goods are delivered for some work or labor upon it by the bailee.

Hire of carriage of goods: goods are delivered to a common carrier or to a private person for the purpose of being carried from place to place.

Hire of custody: goods are delivered for storage.

LOAN GENERAL PROVISIONS

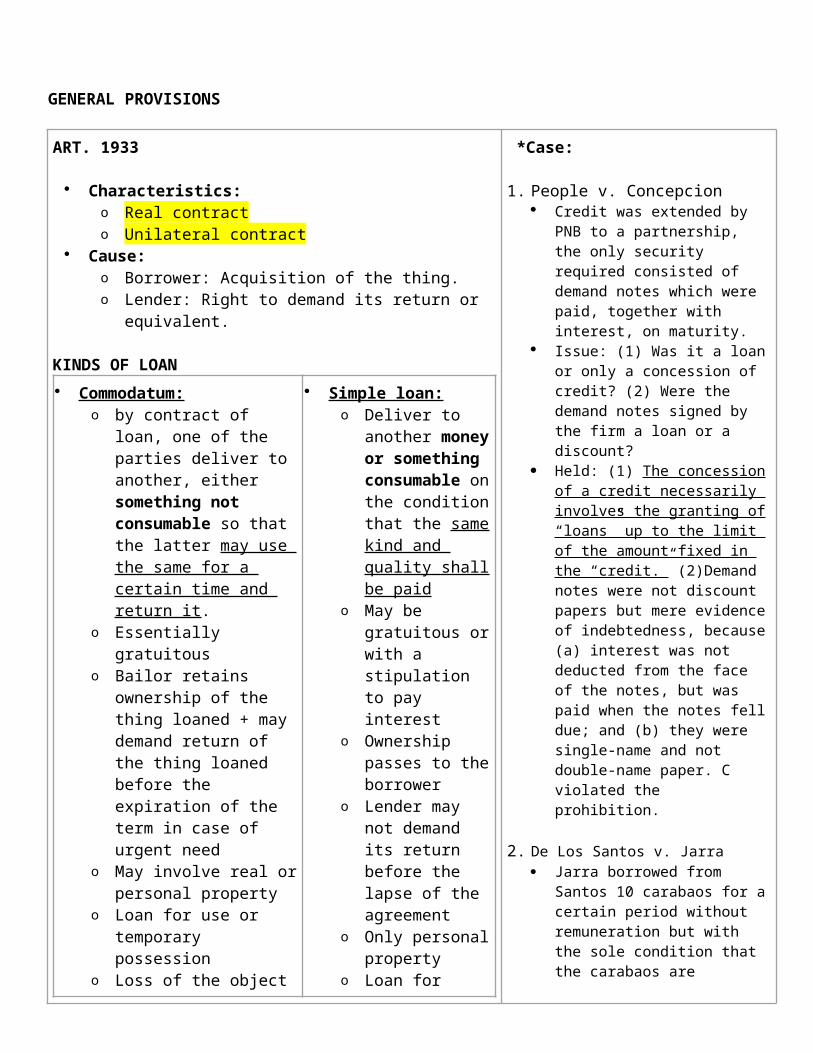

ART. 1933

Characteristics:o Real contracto Unilateral contract

Cause:o Borrower: Acquisition of the thing.o Lender: Right to demand its return or equivalent.

KINDS OF LOAN

Commodatum: o by contract of loan, one of

the parties deliver to another, either something not consumable so that the latter may use the same for a certain time and return it.

o Essentially gratuitouso Bailor retains ownership of

the thing loaned + may demand return of the thing loaned before the expiration of the term in case of urgent need

o May involve real or personal property

o Loan for use or temporary possession

o Loss of the object is suffered by the bailor

Simple loan: o Deliver to another

money or something consumable on the condition that the same kind and quality shall be paid

o May be gratuitous or with a stipulation to pay interest

o Ownership passes to the borrower

o Lender may not demand its return before the lapse of the agreement

o Only personal

*Case:

1. People v. Concepcion Credit was extended by PNB to a

partnership, the only security required consisted of demand notes which were paid, together with interest, on maturity.

Issue: (1) Was it a loan or only a concession of credit? (2) Were the demand notes signed by the firm a loan or a discount?

Held: (1) The concession of a credit necessarily involves the granting of “loans” up to the limit of the amount fixed in the “credit.” (2)Demand notes were not discount papers but mere evidence of indebtedness, because (a) interest was not deducted from the face of the notes, but was paid when the notes fell due; and (b) they were single-name and not double-name paper. C violated the prohibition.

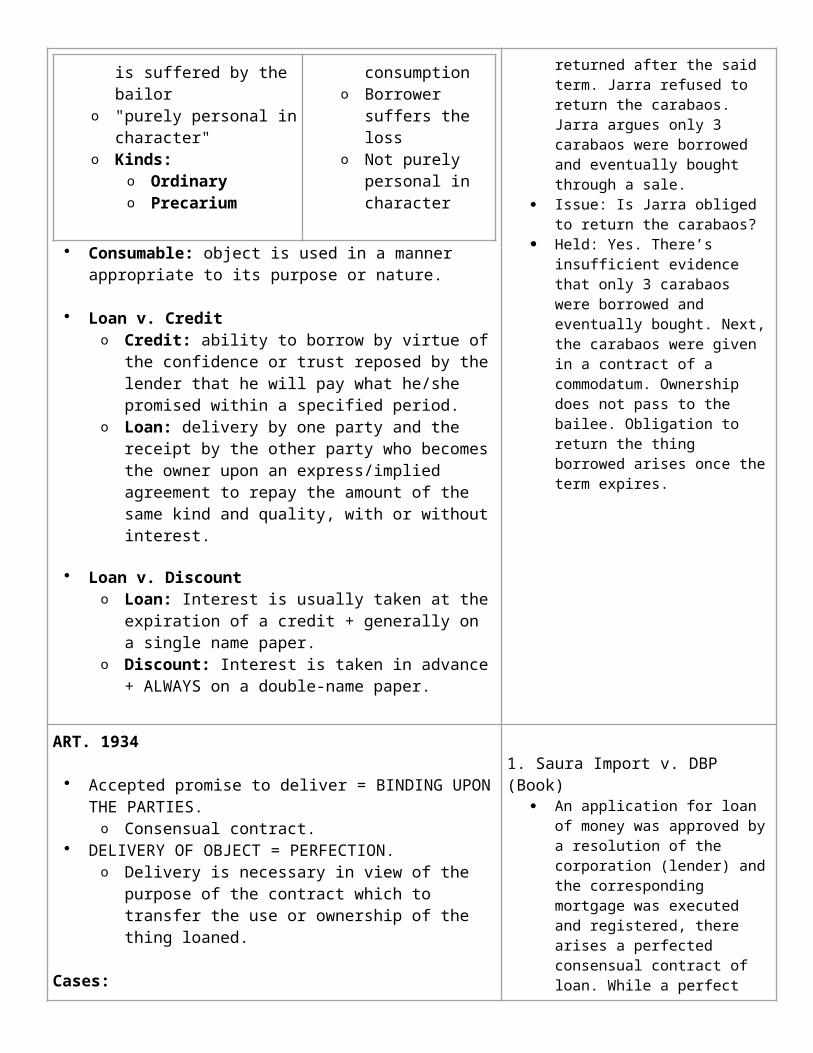

2. De Los Santos v. Jarra Jarra borrowed from Santos 10

carabaos for a certain period without remuneration but with the sole condition that the carabaos are returned after the said term. Jarra refused to return the carabaos. Jarra argues only 3 carabaos were

o "purely personal in character"

o Kinds:o Ordinaryo Precarium

propertyo Loan for

consumptiono Borrower suffers

the losso Not purely

personal in character

Consumable: object is used in a manner appropriate to its purpose or nature.

Loan v. Credito Credit: ability to borrow by virtue of the confidence or

trust reposed by the lender that he will pay what he/she promised within a specified period.

o Loan: delivery by one party and the receipt by the other party who becomes the owner upon an express/implied agreement to repay the amount of the same kind and quality, with or without interest.

Loan v. Discounto Loan: Interest is usually taken at the expiration of a

credit + generally on a single name paper.o Discount: Interest is taken in advance + ALWAYS on a

double-name paper.

borrowed and eventually bought through a sale.

Issue: Is Jarra obliged to return the carabaos?

Held: Yes. There’s insufficient evidence that only 3 carabaos were borrowed and eventually bought. Next, the carabaos were given in a contract of a commodatum. Ownership does not pass to the bailee. Obligation to return the thing borrowed arises once the term expires.

ART. 1934

Accepted promise to deliver = BINDING UPON THE PARTIES.o Consensual contract.

DELIVERY OF OBJECT = PERFECTION.o Delivery is necessary in view of the purpose of the

contract which to transfer the use or ownership of the thing loaned.

Cases:

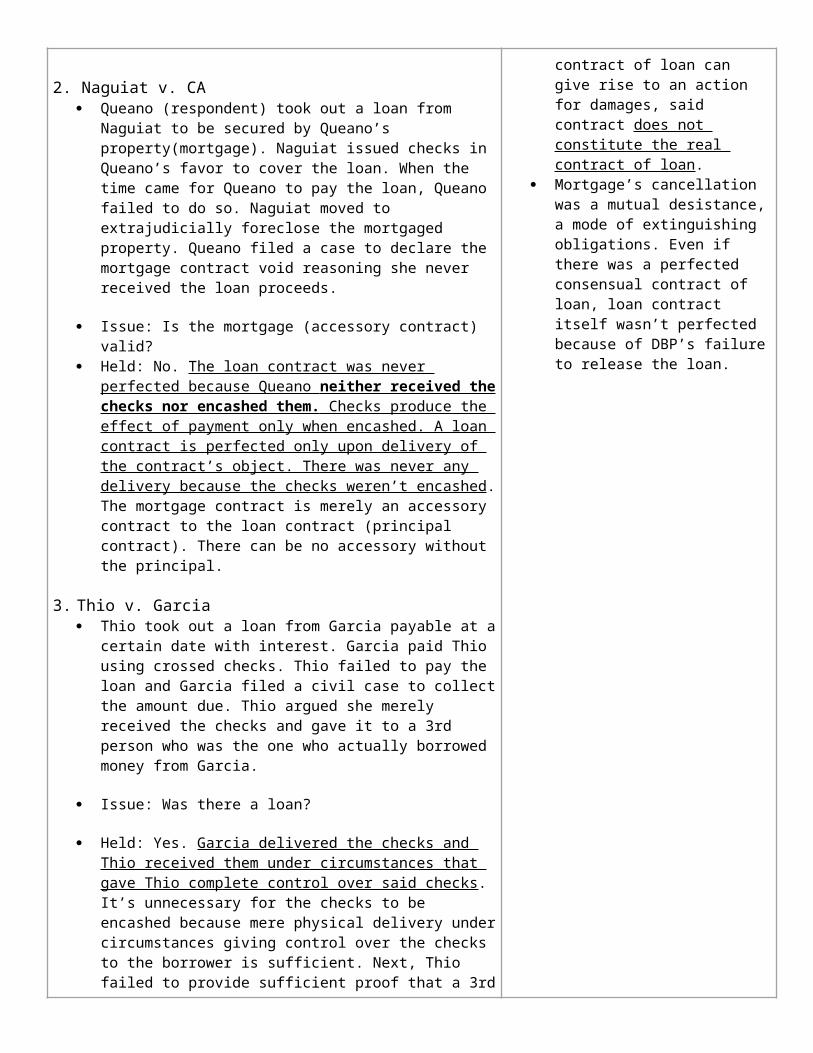

2. Naguiat v. CA Queano (respondent) took out a loan from Naguiat to be secured by

Queano’s property(mortgage). Naguiat issued checks in Queano’s favor to cover the loan. When the time came for Queano to pay the loan, Queano failed to do so. Naguiat moved to extrajudicially foreclose the mortgaged property. Queano filed a case to declare the mortgage contract void reasoning she never received the loan proceeds.

Issue: Is the mortgage (accessory contract) valid? Held: No. The loan contract was never perfected because Queano

neither received the checks nor encashed them. Checks produce

1. Saura Import v. DBP (Book) An application for loan of money

was approved by a resolution of the corporation (lender) and the corresponding mortgage was executed and registered, there arises a perfected consensual contract of loan. While a perfect contract of loan can give rise to an action for damages, said contract does not constitute the real contract of loan.

Mortgage’s cancellation was a mutual desistance, a mode of extinguishing obligations. Even if there was a perfected consensual contract of loan, loan contract itself wasn’t perfected because of DBP’s failure to release the loan.

the effect of payment only when encashed. A loan contract is perfected only upon delivery of the contract’s object. There was never any delivery because the checks weren’t encashed. The mortgage contract is merely an accessory contract to the loan contract (principal contract). There can be no accessory without the principal.

3. Thio v. Garcia Thio took out a loan from Garcia payable at a certain date with

interest. Garcia paid Thio using crossed checks. Thio failed to pay the loan and Garcia filed a civil case to collect the amount due. Thio argued she merely received the checks and gave it to a 3rd person who was the one who actually borrowed money from Garcia.

Issue: Was there a loan?

Held: Yes. Garcia delivered the checks and Thio received them under circumstances that gave Thio complete control over said checks. It’s unnecessary for the checks to be encashed because mere physical delivery under circumstances giving control over the checks to the borrower is sufficient. Next, Thio failed to provide sufficient proof that a 3rd person entered into the loan agreement and not Thio.

COMMODATUM Sec. 1 Nature of a Commodatum

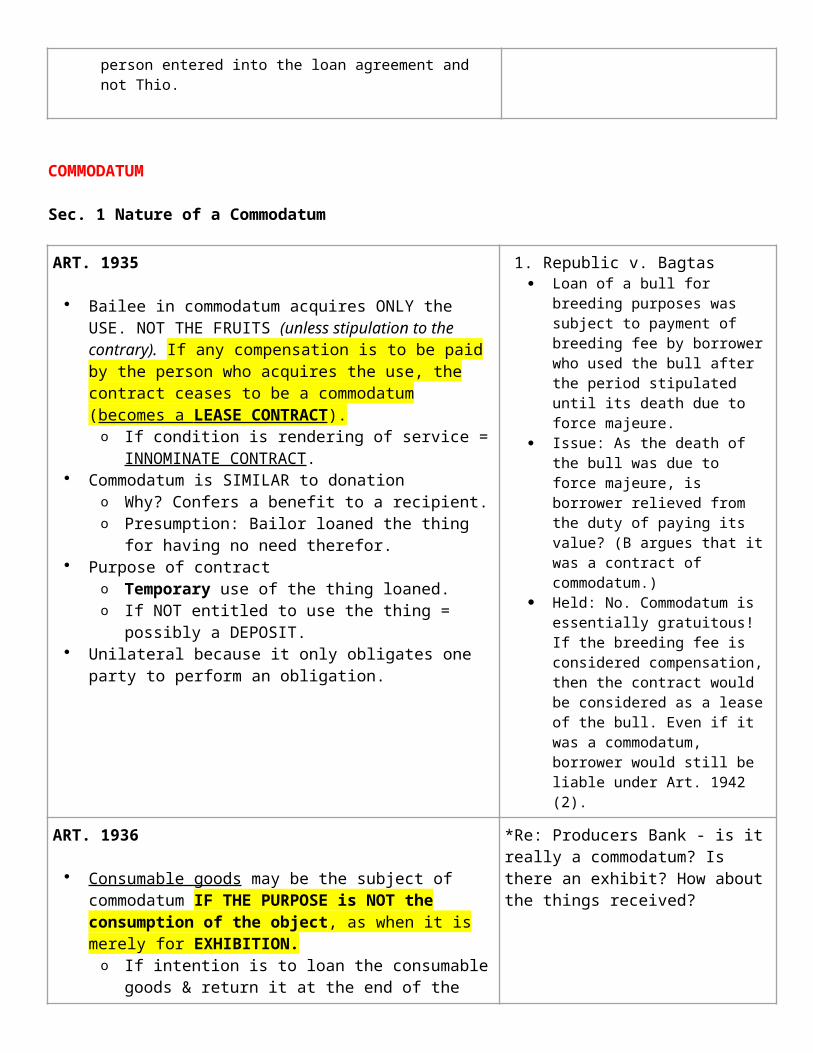

ART. 1935

Bailee in commodatum acquires ONLY the USE. NOT THE FRUITS (unless stipulation to the contrary). If any compensation is to be paid by the person who acquires the use, the contract ceases to be a commodatum (becomes a LEASE CONTRACT).o If condition is rendering of service = INNOMINATE

CONTRACT. Commodatum is SIMILAR to donation

o Why? Confers a benefit to a recipient.o Presumption: Bailor loaned the thing for having no need

therefor. Purpose of contract

o Temporary use of the thing loaned.o If NOT entitled to use the thing = possibly a DEPOSIT.

Unilateral because it only obligates one party to perform an obligation.

1. Republic v. Bagtas Loan of a bull for breeding purposes

was subject to payment of breeding fee by borrower who used the bull after the period stipulated until its death due to force majeure.

Issue: As the death of the bull was due to force majeure, is borrower relieved from the duty of paying its value? (B argues that it was a contract of commodatum.)

Held: No. Commodatum is essentially gratuitous! If the breeding fee is considered compensation, then the contract would be considered as a lease of the bull. Even if it was a commodatum, borrower would still be liable under Art. 1942 (2).

ART. 1936 *Re: Producers Bank - is it really a commodatum? Is there an exhibit? How

Consumable goods may be the subject of commodatum IF THE PURPOSE is NOT the consumption of the object, as when it is merely for EXHIBITION.o If intention is to loan the consumable goods & return it at

the end of the period agreed upon = commodatum. (always remember)

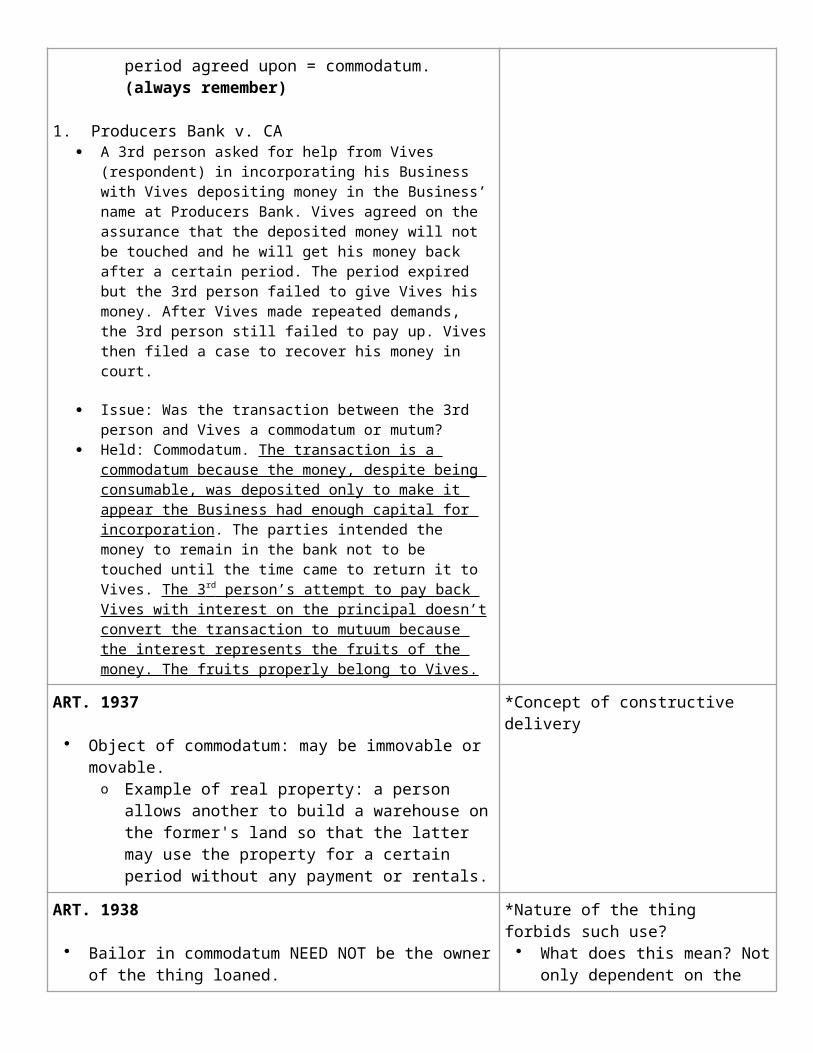

1. Producers Bank v. CA A 3rd person asked for help from Vives (respondent) in

incorporating his Business with Vives depositing money in the Business’ name at Producers Bank. Vives agreed on the assurance that the deposited money will not be touched and he will get his money back after a certain period. The period expired but the 3rd person failed to give Vives his money. After Vives made repeated demands, the 3rd person still failed to pay up. Vives then filed a case to recover his money in court.

Issue: Was the transaction between the 3rd person and Vives a commodatum or mutum?

Held: Commodatum. The transaction is a commodatum because the money, despite being consumable, was deposited only to make it appear the Business had enough capital for incorporation. The parties intended the money to remain in the bank not to be touched until the time came to return it to Vives. The 3 rd person’s attempt to pay back Vives with interest on the principal doesn’t convert the transaction to mutuum because the interest represents the fruits of the money. The fruits properly belong to Vives.

about the things received?

ART. 1937

Object of commodatum: may be immovable or movable.o Example of real property: a person allows another to

build a warehouse on the former's land so that the latter may use the property for a certain period without any payment or rentals.

*Concept of constructive delivery

ART. 1938

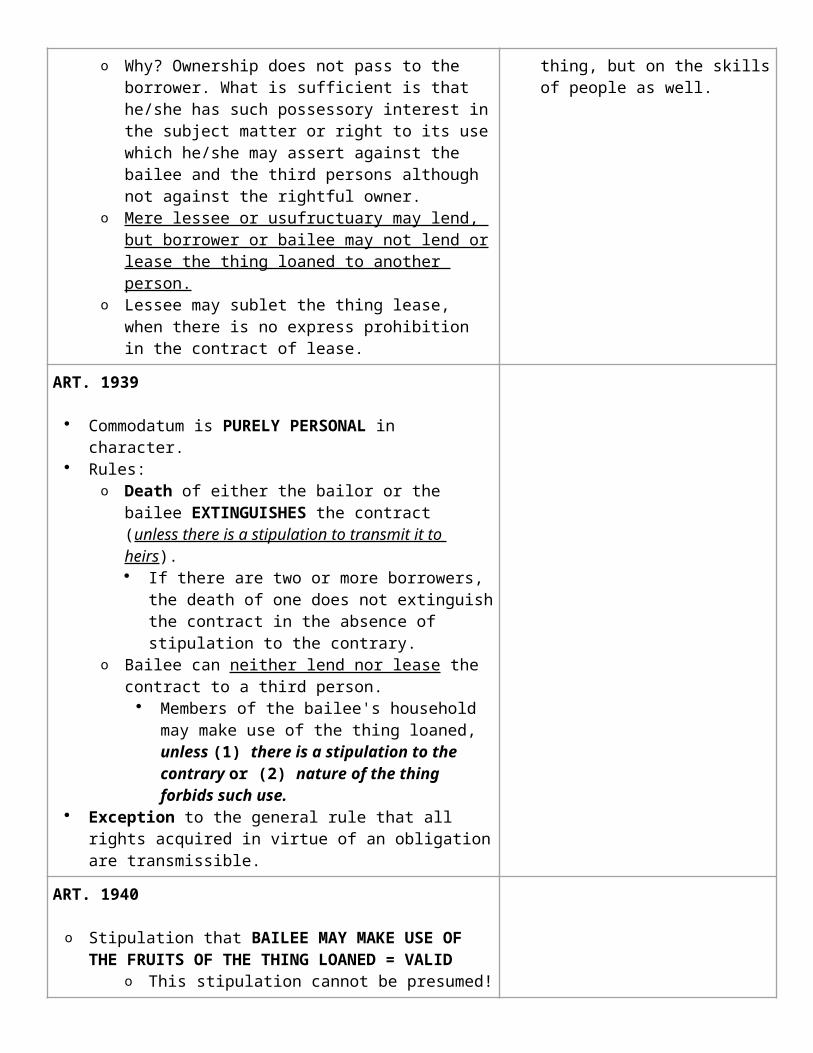

Bailor in commodatum NEED NOT be the owner of the thing loaned.o Why? Ownership does not pass to the borrower. What is

sufficient is that he/she has such possessory interest in the subject matter or right to its use which he/she may assert against the bailee and the third persons although not against the rightful owner.

o Mere lessee or usufructuary may lend, but borrower or bailee may not lend or lease the thing loaned to another person.

o Lessee may sublet the thing lease, when there is no express prohibition in the contract of lease.

*Nature of the thing forbids such use? What does this mean? Not only

dependent on the thing, but on the skills of people as well.

ART. 1939

Commodatum is PURELY PERSONAL in character. Rules:

o Death of either the bailor or the bailee EXTINGUISHES the contract (unless there is a stipulation to transmit it to heirs). If there are two or more borrowers, the death of one

does not extinguish the contract in the absence of stipulation to the contrary.

o Bailee can neither lend nor lease the contract to a third person.

Members of the bailee's household may make use of the thing loaned, unless (1) there is a stipulation to the contrary or (2) nature of the thing forbids such use.

Exception to the general rule that all rights acquired in virtue of an obligation are transmissible.

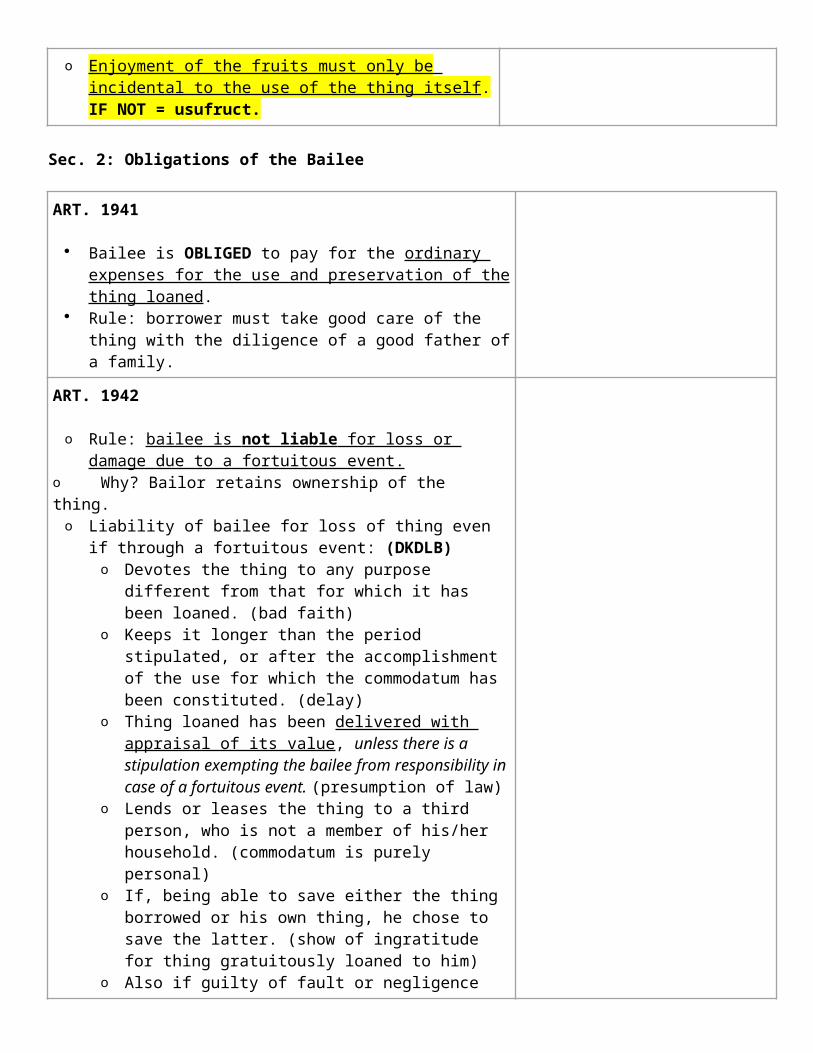

ART. 1940

o Stipulation that BAILEE MAY MAKE USE OF THE FRUITS OF THE THING LOANED = VALID

o This stipulation cannot be presumed!o Enjoyment of the fruits must only be incidental to the use of

the thing itself. IF NOT = usufruct.

Sec. 2: Obligations of the Bailee

ART. 1941

Bailee is OBLIGED to pay for the ordinary expenses for the use and preservation of the thing loaned.

Rule: borrower must take good care of the thing with the diligence of a good father of a family.

ART. 1942

o Rule: bailee is not liable for loss or damage due to a fortuitous event.

o Why? Bailor retains ownership of the thing.o Liability of bailee for loss of thing even if through a fortuitous

event: (DKDLB)o Devotes the thing to any purpose different from that for

which it has been loaned. (bad faith)o Keeps it longer than the period stipulated, or after the

accomplishment of the use for which the commodatum has been constituted. (delay)

o Thing loaned has been delivered with appraisal of its value, unless there is a stipulation exempting the bailee from responsibility in case of a fortuitous event. (presumption of law)

o Lends or leases the thing to a third person, who is not a

member of his/her household. (commodatum is purely personal)

o If, being able to save either the thing borrowed or his own thing, he chose to save the latter. (show of ingratitude for thing gratuitously loaned to him)

o Also if guilty of fault or negligence (not included in this article).

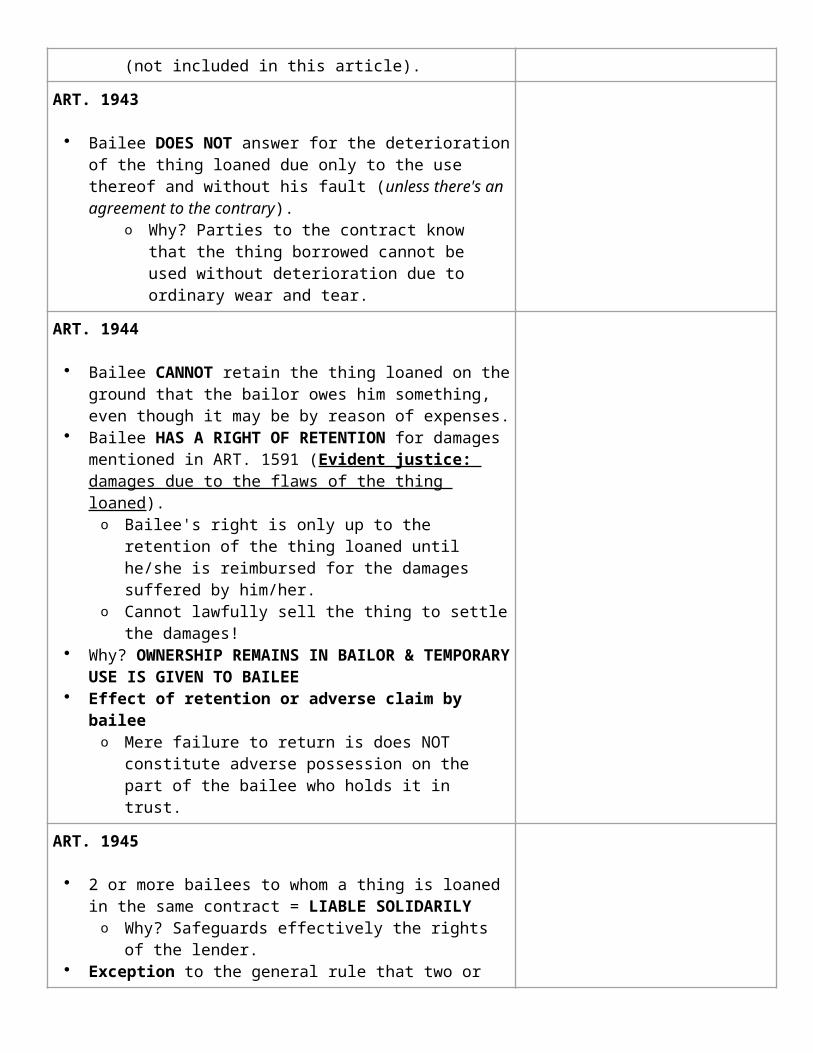

ART. 1943

Bailee DOES NOT answer for the deterioration of the thing loaned due only to the use thereof and without his fault (unless there's an agreement to the contrary).

o Why? Parties to the contract know that the thing borrowed cannot be used without deterioration due to ordinary wear and tear.

ART. 1944

Bailee CANNOT retain the thing loaned on the ground that the bailor owes him something, even though it may be by reason of expenses.

Bailee HAS A RIGHT OF RETENTION for damages mentioned in ART. 1591 (Evident justice: damages due to the flaws of the thing loaned).o Bailee's right is only up to the retention of the thing loaned

until he/she is reimbursed for the damages suffered by him/her.

o Cannot lawfully sell the thing to settle the damages! Why? OWNERSHIP REMAINS IN BAILOR &

TEMPORARY USE IS GIVEN TO BAILEE Effect of retention or adverse claim by bailee

o Mere failure to return is does NOT constitute adverse possession on the part of the bailee who holds it in trust.

ART. 1945

2 or more bailees to whom a thing is loaned in the same contract = LIABLE SOLIDARILYo Why? Safeguards effectively the rights of the lender.

Exception to the general rule that two or more parties in the same obligation gives rise to a joint obligation.

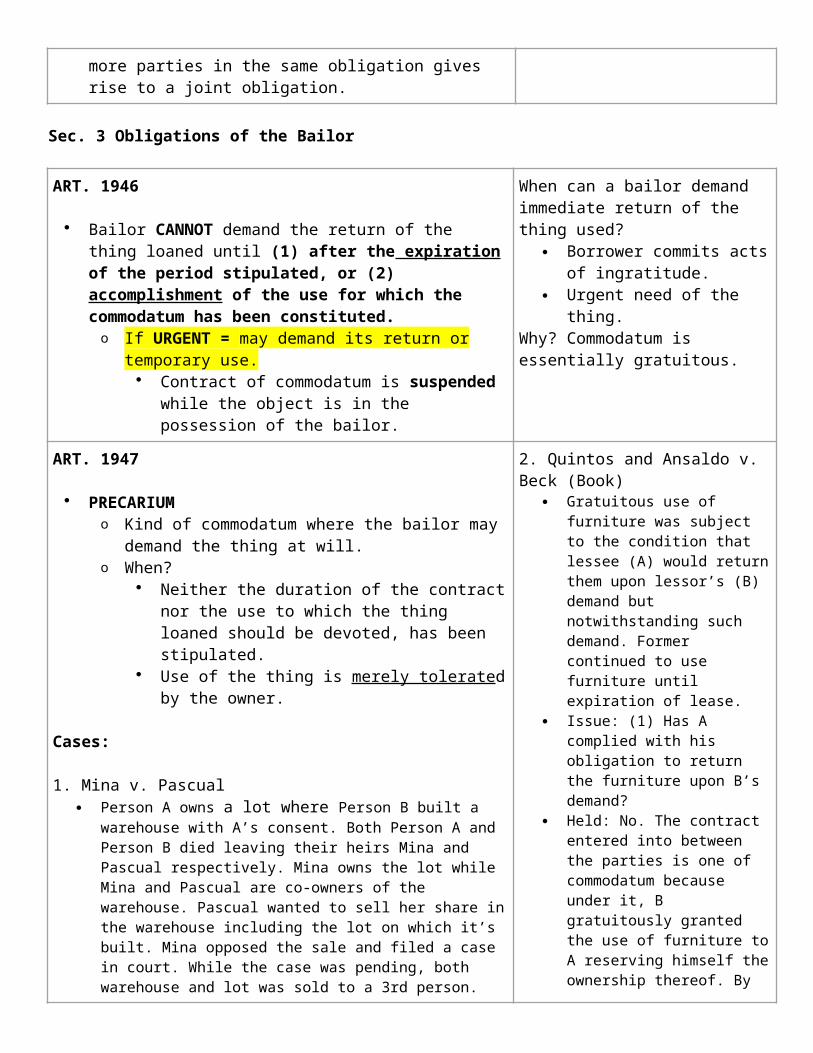

Sec. 3 Obligations of the Bailor

ART. 1946

Bailor CANNOT demand the return of the thing loaned until (1) after the expiration of the period stipulated, or (2) accomplishment of the use for which the commodatum has been constituted.

When can a bailor demand immediate return of the thing used?

Borrower commits acts of ingratitude.

Urgent need of the thing.Why? Commodatum is essentially

o If URGENT = may demand its return or temporary use. Contract of commodatum is suspended while the

object is in the possession of the bailor.

gratuitous.

ART. 1947

PRECARIUMo Kind of commodatum where the bailor may demand the

thing at will.o When?

Neither the duration of the contract nor the use to which the thing loaned should be devoted, has been stipulated.

Use of the thing is merely tolerated by the owner.

Cases:

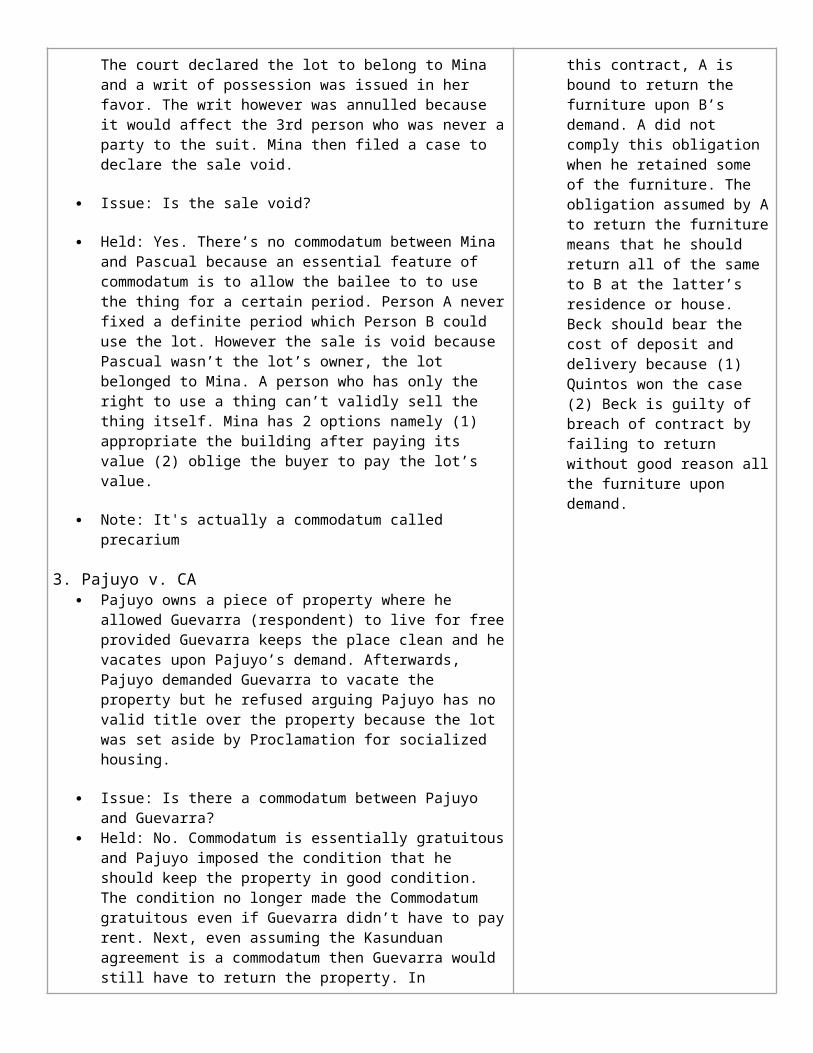

1. Mina v. Pascual Person A owns a lot where Person B built a warehouse with A’s

consent. Both Person A and Person B died leaving their heirs Mina and Pascual respectively. Mina owns the lot while Mina and Pascual are co-owners of the warehouse. Pascual wanted to sell her share in the warehouse including the lot on which it’s built. Mina opposed the sale and filed a case in court. While the case was pending, both warehouse and lot was sold to a 3rd person. The court declared the lot to belong to Mina and a writ of possession was issued in her favor. The writ however was annulled because it would affect the 3rd person who was never a party to the suit. Mina then filed a case to declare the sale void.

Issue: Is the sale void?

Held: Yes. There’s no commodatum between Mina and Pascual because an essential feature of commodatum is to allow the bailee to to use the thing for a certain period. Person A never fixed a definite period which Person B could use the lot. However the sale is void because Pascual wasn’t the lot’s owner, the lot belonged to Mina. A person who has only the right to use a thing can’t validly sell the thing itself. Mina has 2 options namely (1) appropriate the building after paying its value (2) oblige the buyer to pay the lot’s value.

Note: It's actually a commodatum called precarium

3. Pajuyo v. CA Pajuyo owns a piece of property where he allowed Guevarra

(respondent) to live for free provided Guevarra keeps the place clean and he vacates upon Pajuyo’s demand. Afterwards, Pajuyo demanded Guevarra to vacate the property but he refused arguing Pajuyo has no valid title over the property because the lot was set aside by Proclamation for socialized housing.

Issue: Is there a commodatum between Pajuyo and Guevarra? Held: No. Commodatum is essentially gratuitous and Pajuyo

imposed the condition that he should keep the property in good

2. Quintos and Ansaldo v. Beck (Book)

Gratuitous use of furniture was subject to the condition that lessee (A) would return them upon lessor’s (B) demand but notwithstanding such demand. Former continued to use furniture until expiration of lease.

Issue: (1) Has A complied with his obligation to return the furniture upon B’s demand?

Held: No. The contract entered into between the parties is one of commodatum because under it, B gratuitously granted the use of furniture to A reserving himself the ownership thereof. By this contract, A is bound to return the furniture upon B’s demand. A did not comply this obligation when he retained some of the furniture. The obligation assumed by A to return the furniture means that he should return all of the same to B at the latter’s residence or house. Beck should bear the cost of deposit and delivery because (1) Quintos won the case (2) Beck is guilty of breach of contract by failing to return without good reason all the furniture upon demand.

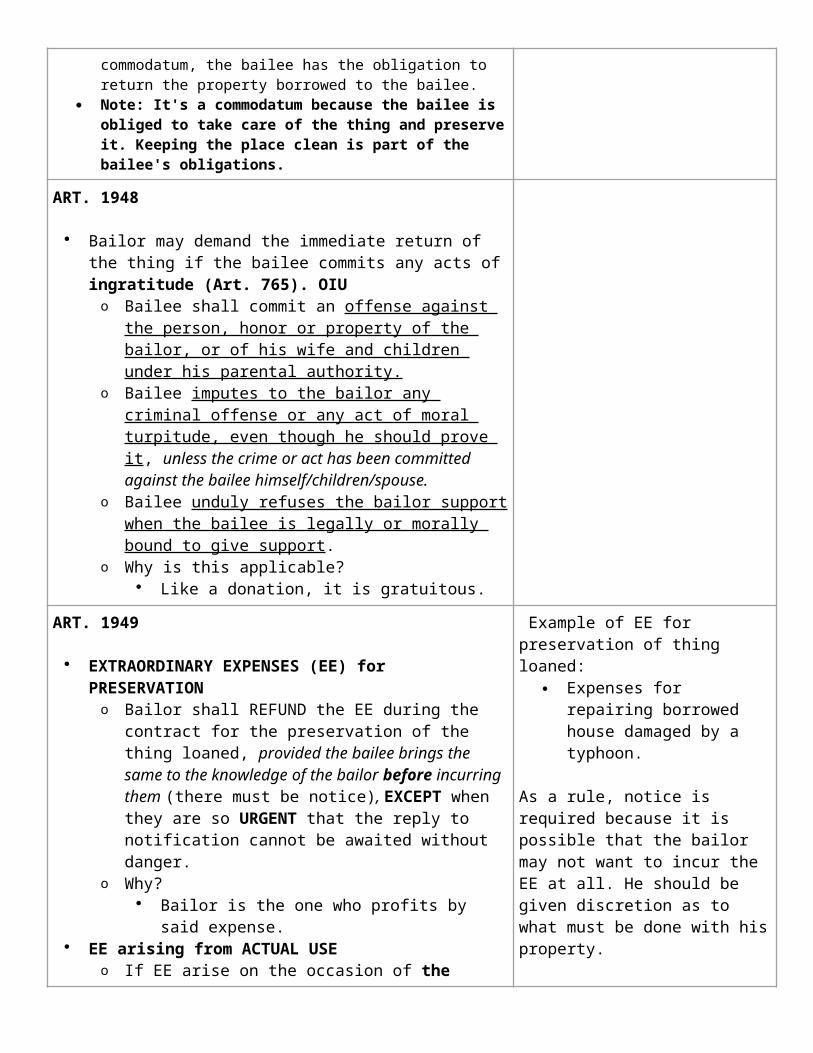

condition. The condition no longer made the Commodatum gratuitous even if Guevarra didn’t have to pay rent. Next, even assuming the Kasunduan agreement is a commodatum then Guevarra would still have to return the property. In commodatum, the bailee has the obligation to return the property borrowed to the bailee.

Note: It's a commodatum because the bailee is obliged to take care of the thing and preserve it. Keeping the place clean is part of the bailee's obligations.

ART. 1948

Bailor may demand the immediate return of the thing if the bailee commits any acts of ingratitude (Art. 765). OIUo Bailee shall commit an offense against the person, honor or

property of the bailor, or of his wife and children under his parental authority.

o Bailee imputes to the bailor any criminal offense or any act of moral turpitude, even though he should prove it, unless the crime or act has been committed against the bailee himself/children/spouse.

o Bailee unduly refuses the bailor support when the bailee is legally or morally bound to give support.

o Why is this applicable? Like a donation, it is gratuitous.

ART. 1949

EXTRAORDINARY EXPENSES (EE) for PRESERVATIONo Bailor shall REFUND the EE during the contract for the

preservation of the thing loaned, provided the bailee brings the same to the knowledge of the bailor before incurring them (there must be notice), EXCEPT when they are so URGENT that the reply to notification cannot be awaited without danger.

o Why? Bailor is the one who profits by said expense.

EE arising from ACTUAL USEo If EE arise on the occasion of the actual use of the thing

by the bailee (even without fault) = borne equally by both bailor and bailee unless there's a stipulation to the contrary.

Parties may, by stipulation, provide for a different apportionment of such expenses, or that they shall be borne by the bailee or bailor only.

Example of EE for preservation of thing loaned:

Expenses for repairing borrowed house damaged by a typhoon.

As a rule, notice is required because it is possible that the bailor may not want to incur the EE at all. He should be given discretion as to what must be done with his property.

Example of EE from actual use: Expenses for repairing a

borrowed jeep damaged in a collision.

ART. 1950

If the purpose of using the thing is not in ART. 1941/1949 = bailee is NOT entitled to reimbursement.

ART. 1951

If the bailor knows the flaws of the thing loaned + does not tell

If flaw is unknown, bailor is not liable because commodatum is gratuitous.

the bailee = bailor will be liable for the damages which the bailee may suffer by reason thereof.

o Why? Bailor is made liable for his bad faith! Requisites for liability : FHADS

o Flaw or defect of the thing loaned.o It is hidden.o Bailor is aware.o Bailor does not tell bailee of the flaw or defect.o Bailee suffers damages by reason of said flaw or defect.

Bailee is given right of retention until he or she is paid damages.

If defect is patent or could have been known by the borrower, lender is not liable.

ART. 1952

Bailor CANNOT exempt himself from the payment of expenses or damages by abandoning the thing to the bailee.o Why? Expenses or damages may exceed the value of the

thing loaned.

SIMPLE LOAN OR MUTUUM

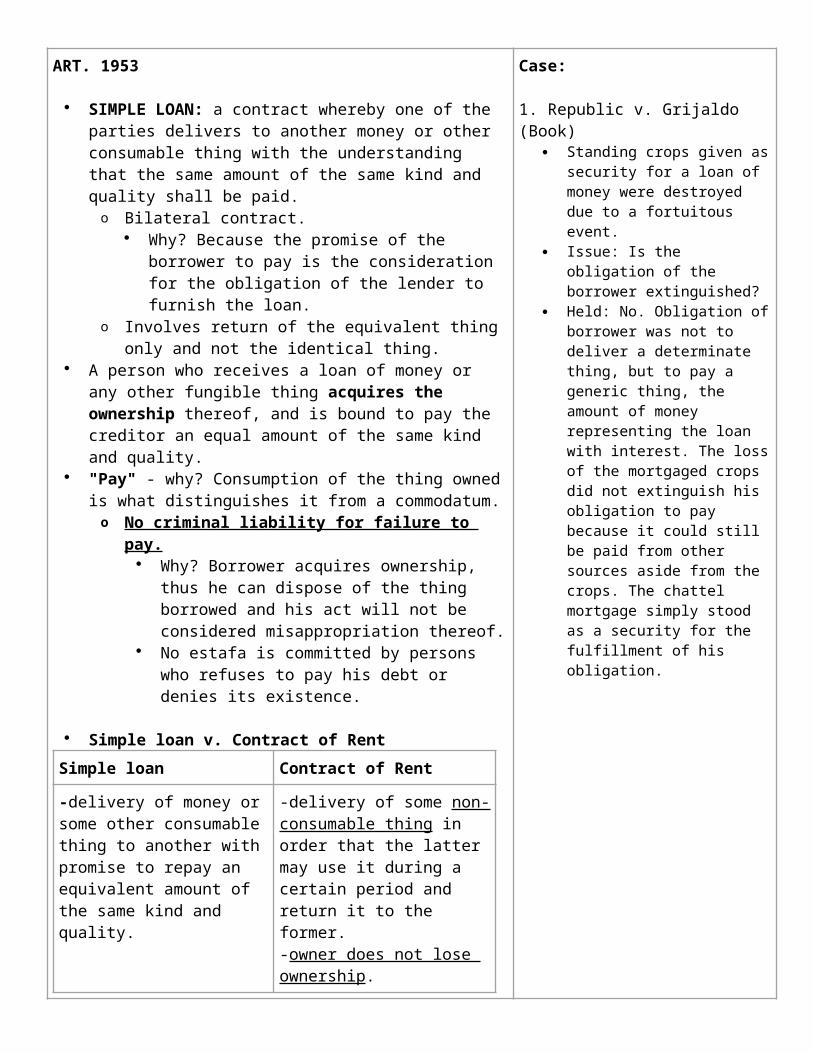

ART. 1953

SIMPLE LOAN: a contract whereby one of the parties delivers to another money or other consumable thing with the understanding that the same amount of the same kind and quality shall be paid.o Bilateral contract.

Why? Because the promise of the borrower to pay is the consideration for the obligation of the lender to furnish the loan.

o Involves return of the equivalent thing only and not the identical thing.

A person who receives a loan of money or any other fungible thing acquires the ownership thereof, and is bound to pay the creditor an equal amount of the same kind and quality.

"Pay" - why? Consumption of the thing owned is what distinguishes it from a commodatum.o No criminal liability for failure to pay.

Why? Borrower acquires ownership, thus he can dispose of the thing borrowed and his act will not be considered misappropriation thereof.

No estafa is committed by persons who refuses to pay his debt or denies its existence.

Simple loan v. Contract of Rent

Simple loan Contract of Rent

-delivery of money or some other consumable thing to another with promise to repay

-delivery of some non-consumable thing in order that the latter may use it during a

Case:

1. Republic v. Grijaldo (Book) Standing crops given as security

for a loan of money were destroyed due to a fortuitous event.

Issue: Is the obligation of the borrower extinguished?

Held: No. Obligation of borrower was not to deliver a determinate thing, but to pay a generic thing, the amount of money representing the loan with interest. The loss of the mortgaged crops did not extinguish his obligation to pay because it could still be paid from other sources aside from the crops. The chattel mortgage simply stood as a security for the fulfillment of his obligation.

an equivalent amount of the same kind and quality.

certain period and return it to the former.-owner does not lose ownership.

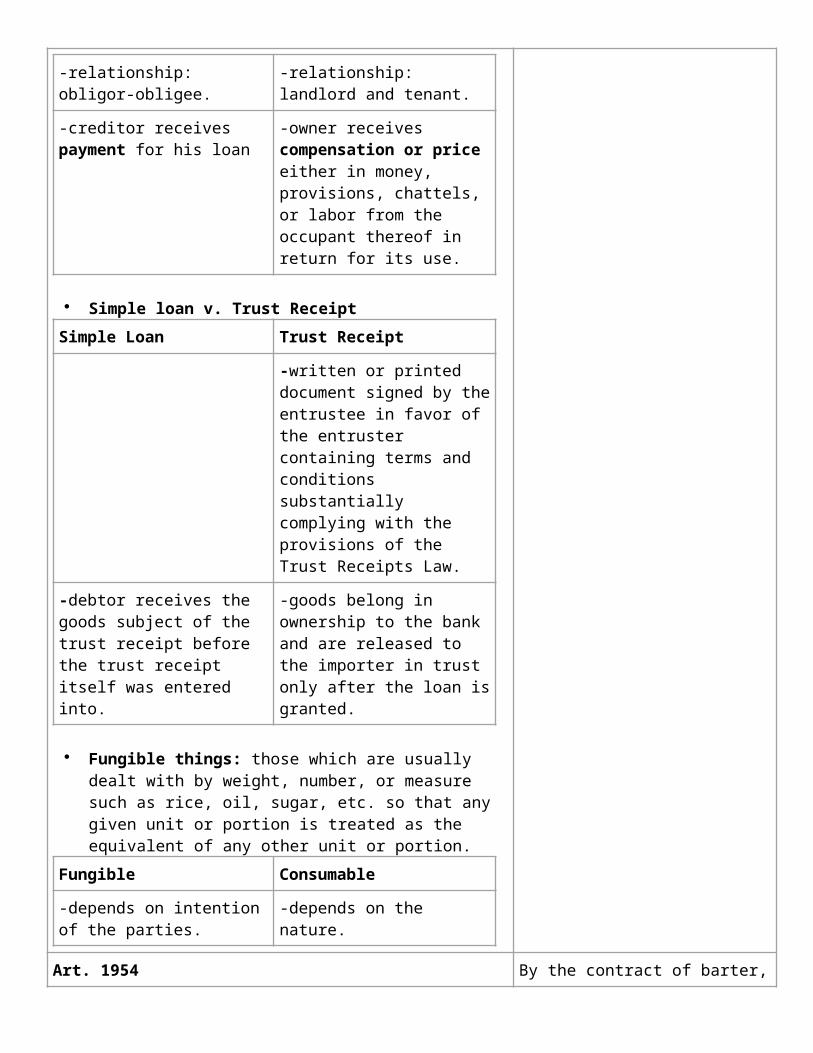

-relationship: obligor-obligee. -relationship: landlord and tenant.

-creditor receives payment for his loan

-owner receives compensation or price either in money, provisions, chattels, or labor from the occupant thereof in return for its use.

Simple loan v. Trust Receipt

Simple Loan Trust Receipt

-written or printed document signed by the entrustee in favor of the entruster containing terms and conditions substantially complying with the provisions of the Trust Receipts Law.

-debtor receives the goods subject of the trust receipt before the trust receipt itself was entered into.

-goods belong in ownership to the bank and are released to the importer in trust only after the loan is granted.

Fungible things: those which are usually dealt with by weight, number, or measure such as rice, oil, sugar, etc. so that any given unit or portion is treated as the equivalent of any other unit or portion.

Fungible Consumable

-depends on intention of the parties.

-depends on the nature.

Art. 1954

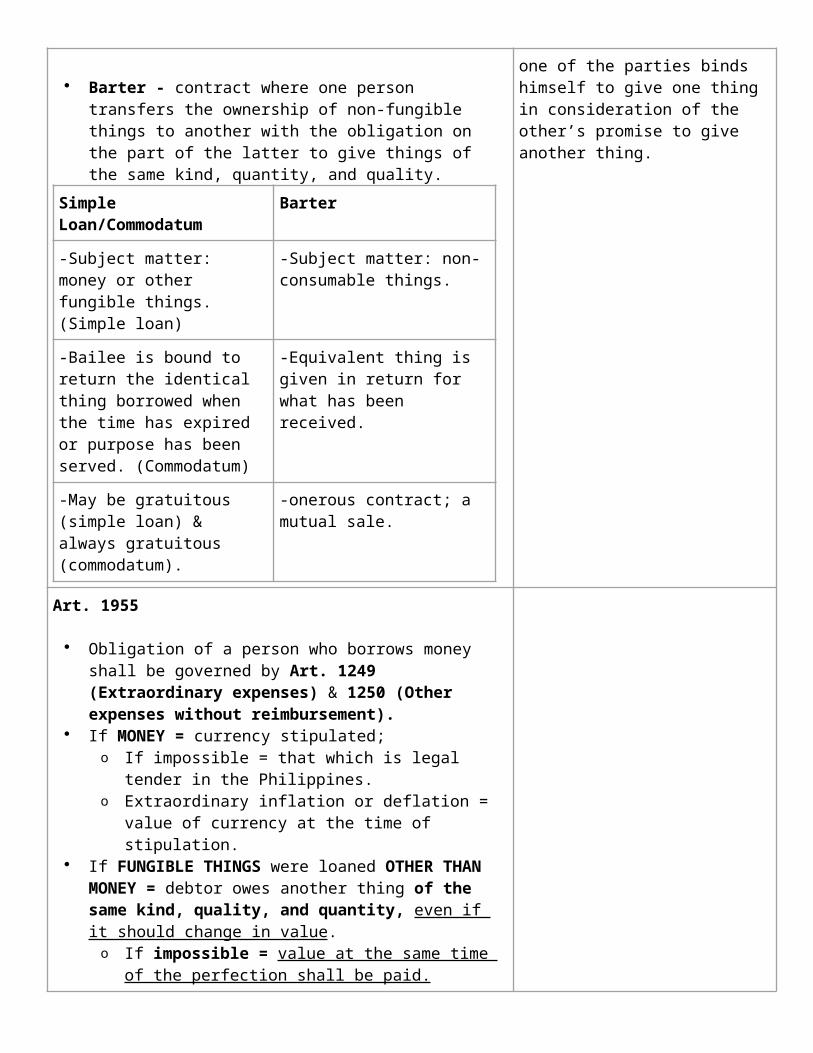

Barter - contract where one person transfers the ownership of non-fungible things to another with the obligation on the part of the latter to give things of the same kind, quantity, and quality.

Simple Loan/Commodatum Barter

-Subject matter: money or other fungible things. (Simple loan)

-Subject matter: non-consumable things.

-Bailee is bound to return the identical thing borrowed when the time has expired or purpose has been served.

-Equivalent thing is given in return for what has been received.

By the contract of barter, one of the parties binds himself to give one thing in consideration of the other’s promise to give another thing.

(Commodatum)

-May be gratuitous (simple loan) & always gratuitous (commodatum).

-onerous contract; a mutual sale.

Art. 1955

Obligation of a person who borrows money shall be governed by Art. 1249 (Extraordinary expenses) & 1250 (Other expenses without reimbursement).

If MONEY = currency stipulated;o If impossible = that which is legal tender in the Philippines.o Extraordinary inflation or deflation = value of currency at

the time of stipulation. If FUNGIBLE THINGS were loaned OTHER THAN

MONEY = debtor owes another thing of the same kind, quality, and quantity, even if it should change in value.o If impossible = value at the same time of the perfection

shall be paid.

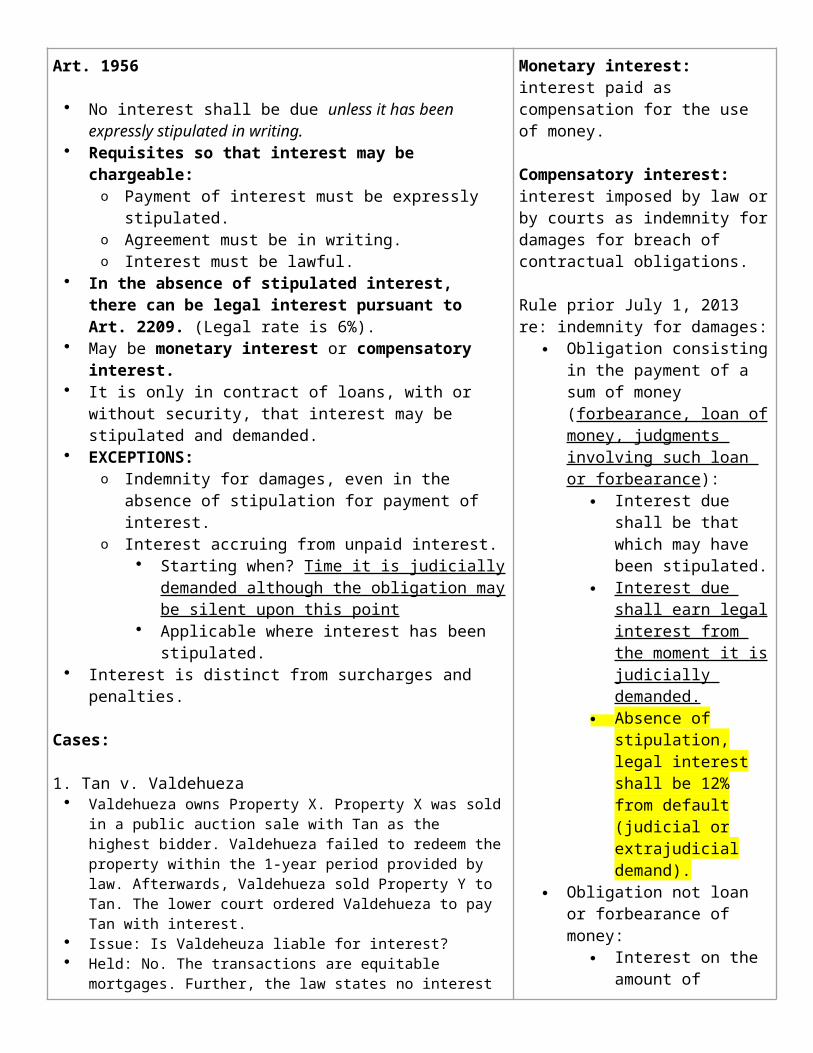

Art. 1956

No interest shall be due unless it has been expressly stipulated in writing.

Requisites so that interest may be chargeable:o Payment of interest must be expressly stipulated.o Agreement must be in writing.o Interest must be lawful.

In the absence of stipulated interest, there can be legal interest pursuant to Art. 2209. (Legal rate is 6%).

May be monetary interest or compensatory interest. It is only in contract of loans, with or without security, that

interest may be stipulated and demanded. EXCEPTIONS:

o Indemnity for damages, even in the absence of stipulation for payment of interest.

o Interest accruing from unpaid interest. Starting when? Time it is judicially demanded

although the obligation may be silent upon this point Applicable where interest has been stipulated.

Interest is distinct from surcharges and penalties.

Cases:

1. Tan v. Valdehueza Valdehueza owns Property X. Property X was sold in a public auction

sale with Tan as the highest bidder. Valdehueza failed to redeem the property within the 1-year period provided by law. Afterwards, Valdehueza sold Property Y to Tan. The lower court ordered Valdehueza to pay Tan with interest.

Issue: Is Valdeheuza liable for interest?

Monetary interest: interest paid as compensation for the use of money.

Compensatory interest: interest imposed by law or by courts as indemnity for damages for breach of contractual obligations.

Rule prior July 1, 2013 re: indemnity for damages:

Obligation consisting in the payment of a sum of money (forbearance, loan of money, judgments involving such loan or forbearance):

Interest due shall be that which may have been stipulated.

Interest due shall earn legal interest from the moment it is judicially demanded.

Absence of stipulation, legal interest shall be 12% from default (judicial or extrajudicial demand).

Obligation not loan or forbearance of money:

Interest on the amount

Held: No. The transactions are equitable mortgages. Further, the law states no interest shall be due unless expressly stipulated in writing. The contract provided stipulated no interest in writing. Further, Tan herself didn’t ask for such interest and she merely wanted a consolidation of ownership of Property X and Y.

2. Jardenil v. Solas Solas took out a loan from Jardenil with interest. Issue: Is Solas bound to pay interest up to the date of maturity or up

to the date payment is effected? Held: Solas must pay interest up to the date of maturity and legal

interest from judicial demand. Interest shall be due only when it has been expressly stipulated. In this case, the contract mentions no interest during the 1-year grace period after maturity.

3. Frias v. San Diego Frias owns Property X. Frias entered into an Agreement with San

Diego-Sison for the latter to buy Property X at P6 million. San Diego-Sison gave Frias P3 million as consideration for the Agreement. The Agreement gave San Diego-Sison 6 months to decide if it will buy the property. Once San Diego-Sison decides to buy the property, it has another 6 months to pay the P6 million purchase price. However, if San Diego decides not to purchase the property, the P3 million consideration will be treated as loan and Property X as security. Further, the loan will earn compounded bank interest for the last 6 months only. San Diego-Sison decided not to purchase the property and demanded the return of the P3 millionplus interest. Frias failed to pay back the P3 million and San Diego-Sison filed a case before the RTC for a sum of money with preliminary attachment against Frias.

Issue: Is Frias liable to pay interest on the loan even after the 2nd 6-month period?

Held: Yes. Regular interest constitutes the cost of using money and the debtor must pay such interest until the principal sum is returned to the creditor. It’s unjust enrichment for the debtor to continue possessing the principal and use it after the loan has matured without paying interest. In this case, the phrase ‘for the last 6 months only’ should be taken in context of the entire Agreement. The Agreement speaks of two 6 month periods with the second 6 month period given to Frias to pay the P3 million in case San Diego-Sison decides not to buy the property. Consequently, the Agreement, in using the phrase ‘for the last 6 months only’ meant no interest shall be paid during the 1st 6 months while San Diego-Sison was still making up its mind. The Agreement logically presumed the loan plus interest shall be fully paid within the second 6 month period. The Agreement doesn’t suggests at all that interest will be charged for the second 6 month period only even if it takes Frias an eternity to pay the loan.

4. Arwood Industries v. DM-Consunji Arwood Industries entered into an Agreement with DM Consunji.

DM Consunji would build Condominum X while Arwood would pay DM Consunji a sum certain of money. DM Consunji finished Condominum X but Arwood failed to fully pay the contract price upon maturity. Consequently, DM Consunji filed a civil case to collect the unpaid amount plus damages against Arwood. The RTC

of damages awarded may be imposed at the discretion of the court at the rate of 6% per annum.

If date of demand is not clear, interest shall only run from judgment.

Actual base for the computation is the amount finally adjudged.

When judgment of the court awarding a sum of money becomes final and executory, rate of legal interest, regardless of whether obligation involves a loan or forbearance, shall be 12% from such finality until its satisfaction. This interim period being deemed to be by then an equivalent to a forbearance or credit.

ruled in DM Consunji’s favor and ordered Arwood to pay the remaining balance with 2% monthly interest.

Issue: Was the RTC’s imposition of 2% monthly interest correct? Held: Yes. The Agreement between Arwood and DM Consunji

provides for 2 options in case of delay in monthly payments namely (1) suspend work on the project until the owner remits payment (2) continue the work but the owner shall be required to pay 2% monthly interest. In this case, DM Consunji chose the latter option. Further, Arwood can’t impugn the Agreement because it willingly gave consent to such Agreement. Further, even if the Agreement failed to stipulate any interest, DM Consunji can still recover under the Civil Code Art. 2209. Art. 2209 provides the appropriate measure of damages if the obligation breached consists in the payment of money. The damages shall be the payment of penalty interest at the rate agreed upon, and if there’s no penalty interest then the regular interest agreed upon. If there’s no stipulation on both penalty and regular interest, then legal interest shall be the basis.

5. Soncuya v. Azarraga It is only in contracts of loans, with or without security, that

interest may be stipulated and demanded.

6. Royal Shirt v. Co Bon Tic Royal Shirt entered into a contract of sale with Co Bon Tic with the

latter selling the former’s shoes. Co Bon Tic sold part of the shoes but failed to fully return the value of the shoes sold causing Royal Shirt to file a case to recover the deficiency. The CFI ordered Co Bon Tic to pay the remaining balance with interest at 12% per annum from the date of the complaint’s filing, to return the unsold shoes unless Co Bon Tic preferred to retain them by paying their value, and attorney’s fees. The order slips and invoice indicated Co Bon Tic will pay 12% interest per annum and 25% attorney’s fees. Co Bon Tic never signed either the order slips or invoice.

Issue: Is Co Bon Tic liable to pay the 12 % interest per annum indicated in the order slips and invoice?

Held: No. Co Bon Tic isn’t bound by either the order slip or invoice because he never signed them. Sales invoices or slips issued by a store to its customers, stating interest and attorney’s fees in the usual printed forms as terms and conditions, without the signature of the obligor, do not constitute the express stipulation required by Art. 1956. Co Bon Tic isn’t liable to pay attorney’s fees and the 12% interest per annum as indicated in the order slips and invoice. However, he’s still liable to pay the legal interest of 6% because of the absence of any stipulated interest from the date of the complaint’s filing.

7. Overseas v. Cordero Cordero opened a time deposit account worth P80 thousand with 6%

interest per annum at Overseas Bank. The time deposit matured but Overseas Bank, due to financial distress, was unable to pay the time deposit plus interest. Consequently, Cordero filed a civil case before the CFI to recover the amount deposited.

Issue: Is Cordero entitled to interest on his time deposit during the period that Overseas Bank was closed?

Held: No. A bank is able to pay interest on the money deposited with

it thru other aspects of its operations. Consequently, once such operations cease the bank has no way of paying interest on its deposits . It’s deemed read into every contract of deposit with a bank that the obligation to pay interest on the deposit ceases the moment the bank’s operation is completely suspended by duly constituted authority. Further, this decision is applicable to all other obligations which Overseas Bank couldn’t pay during the period of its actual complete closure.

8. Ramos v. Central Bank Central Bank granted loans to respondent Commercial Bank of

Manila (formerly Overseas Bank of Manila). The Central Bank suspended Commercial Bank’s operations because of financial distress. According to a previous Supreme Court decision, Commercial Bank is not obliged to pay interest on deposits and loans during the period of its suspension.

Issue: Is Commercial Bank of Manila liable to pay interest on Central Bank’s loans and advances?

Held: No. The parties have failed to provide any cogent reason for the SC not to apply its previous decision in this case, particularly on the Central Bank loans. Further, GSIS has acquired 99% of Commercial Bank’s outstanding stock and the previous SC decision will manifestly redound to the benefit of another government institution.

9. Lirag v. SSS Lirag and SSS entered into a Purchase Agreement with the latter

buying stock from the former. The agreement also states Lirag must repurchase the stock at regular intervals. Lirag’s President constituted himself as surety in SSS’ favor for the repurchase of stocks and payment of stock dividends. The agreement further states the entire obligation shall become due and demandable if Lirag fails to repurchase the stocks; further, Lirag will be liable for 12% of the amount then outstanding as liquidated damages. Afterwards, Lirag failed to pay the stock dividends and repurchase the stocks due to financial distress. Lirag’s President likewise failed his obligation as surety. Consequently, SSS filed a civil case before the CFI to enforce payment of the obligation plus liquidated damages equivalent to 12% of the amount then outstanding.

Issue: Is Lirag liable to pay the unliquidated damages plus interest on the unredeemed shares and unpaid dividends?

Held: Yes. The award of P146 thousand representing liquidated damages of 12% of the amount then outstanding is correct. Because Lirag admitted having failed to fulfill its obligation under the Purchase Agreement. Such liquidated damages are expressly provided for in the Purchase Agreement in case of contractual breach. Further, the CFI’s order for Lirag to pay interest on both the unredeemed shares and unpaid dividends is also correct. Lirag’s failure to perform under the Purchase Agreement involve sums of money which are overdue, therefore they’re bound to earn legal interest from the time of demand. In this case, there was judicial demand when the complaint was filed in court.

Art. 1957 Case:

Contracts and stipulations, UNDER ANY CLOAK OR DEVICE WHATEVER, intended to circumvent the laws against usury shall be VOID.o Borrower may recover in accordance with laws on usury.

Usurious contracts declared voido Form of contract is not conclusive.o Contract void only as to interest involved .o Right of debtor: the amount paid as interest under a

usurious agreement is recoverable by him, since the payment is deemed to have been made under restraint, rather than voluntarily.

Note: Interest rates are no longer subject to any ceiling. The rate will depend on the agreement of the parties.

Instances of contracts disguised to cover usurious loanso Credit sale of property at exorbitant price to loan applicant.o Purchase of lender's property at an exorbitant price to be

taken from loan.o Price of sale with right to repurchase clearly inadequate.o Pretended lease by borrower at usurious rental.o Rent free by lender of borrower's property in addition to

interest on loans.o Date for repayment of loan with interest ante-dates actual

transaction.o Payment by borrower for lender's services as additional

compensation.

1. Angel Jose Warehousing v. Chelda Enterprises

Angel Warehousing granted a loan to Childa Enterprises which upon maturity Childa Enterprises failed to pay. Angel Warehousing then filed a civil case to recover the loan’s unpaid balance with legal interest from the date of the complaint’s filing. Childa countered stating the loan’s interest is usurious and shouldn’t be permitted recovery.

Issue: Can Angel Warehousing recover the principal loan?

Held: Yes. In loans with interest there are actually 2 stipulations, the principal stipulation as to the loan itself and accessory stipulations as to the interest. These 2 stipulations are divisible and the illegality of the accessory stipulation won't render the principal stipulation likewise void. In loans with usurious interest, only the entire interest is void. The loan becomes one without interest. In this case, Childa Enterprises must pay the loan with legal interest. The legal interest arises not due to stipulation but because when the debtor incurs delay he’s liable to pay damages. Further, the New Civil Code merely adds that usurious interest paid can be recovered with interest as of the date of payment. The New Civil Code doesn't render both the interest and principal void.

Art. 1958

In the determination of the interest, if it is payable in kind, its value shall be appraised at the current price of the products or goods at the time and place of payment.

o Purpose: to make usury harder to perpetrate.

Art. 1959

General Rule: Interest due and unpaid shall not earn interest.o Exception:

Art. 2212 (When judicially demanded.) Express stipulation made by parties. Interest due an

unpaid balance shall be added to the principal obligation and the resulting total amount shall earn interest. (COMPOUNDING INTEREST)

Compounding of both monetary interest and the penalty charged is allowed. Hence, borrower may be held liable for the total amount of principal, monetary, and penalty interest.

Cases:

1. Co-Unjieng v. Mabalacat Mabalacat took out a loan with interest from Co Unjien but when the

loan matured Mabalacat failed to pay. Co Unjieng then filed a civil case to recover the amount due and the RTC ruled in Co-Unieng's favor. The RTC ordered Mabalacat to pay the unpaid balance on the loan plus compounded interest.

Issue: Is Mabalacat liable for compounded interest? Held: No. The parties may stipulate that interest shall be

compounded provided there is an express stipulation to that effect. In the absence of stipulation, no interest can be collected on interest until the debt is judicially claimed, and then only at the rate of 6% per annum. In this case, the contract’s language doesn’t justify charging of interest upon interest. The contract merely requires Mabalacat to pay monthly interest at the end of each month computed based on the unpaid principal loan. Nothing in it provides for the compounding of interest. Mabalacat is only liable for interest of the unpaid interest at the rate of 6% per annum from the action’s institution (judicial demand).

2. David v. CA The dispute centers on the RTC’s decision. The RTC ordered

respondent Afable to pay David a sum certain in money plus interest. The sum certain in money was computed based on simple interest but David argues the basis should be compounded interest.

Issue: Should the interest be simple or compounded?

Held: No. David’s argument that Art. 2212 should apply because of Art. 2209 which provides for legal interest in the absence of stipulation is wrong. Art. 2212 contemplates the presence of stipulated interest which has accrued upon judicial demand. If there’s no stipulated interest, Art. 2212 doesn’t apply. In this case, the parties never stipulated any interest.

Art. 1960

If the borrower pays interest when there has been no stipulation therefor, the provisions of this Code concerning solutio indebti, or natural obligations, shall be applied, as the case may be.o If unstipulated interest is paid by mistake, the debtor may

recover as this would be a case of solutio indebti or undue payment.

o If paid voluntarily + not in writing, there can be no recovery as in the case of natural obligations.

1. Velez v. Balzarra Velez filed a complaint for the return of Property X which she

alleged Balzarza sold to her deceased husband. She alleged that in distributing her dead husband’s estate, Property X was adjudicated to her. Balzarza countered however the real agreement was a loan for P2,000 secured by a mortgage on Property X. Balzarza alleged he paid P4,000 and prayed for the return of the excess. At trial, the parties agreed the case involved the collection of a debt secured by Property X, and not for conveyance of Property X.

Issue: Were the excess payments made by Balzarza intended to be applied to the principal or were interests.

Held: Payments applied to the principal. No interest is due unless expressly stipulated. When the borrower pays interest when there has been no stipulation for it, the provisions on solutio indebiti or natural obligations shall apply as the case may be. In this case, the lender was allowed to possess Property X and reap its fruits. The parties must have thought it unfair for the borrower to pay interest in addition to this. Further, if the payments are construed as interests, then the lender would’ve committed usury outright. Velez argued her husband was known publicly as a money lender and the parties must have contemplated paying interest. However, such fact didn’t comply with the requisite that interest must be expressly stipulated. Having concluded the payments were to be applied only to the principal, Velez must return the excess paid. The requirements for solutio indebiti are present in this case which requires (1) a person receives something by mistake (2) there’s no right to collect. In this case namely (1) the parties never intended interest to be paid (2) Balzarza paid only for the principal but he overpaid.

Art. 1961

Usurious contracts shall be governed by the Usury Law and other special laws, so far as they are not inconsistent with this code.

Usury is now legally non-existent. The interest legally chargeable depends upon the agreement between the lender and the borrower.

USURY LAW

Usury: contracting for or receiving something in excess of the amount allowed by law for the loan or forbearance of money, goods,

*check the different types of interest (eg. Lawful interest etc)

or chattels. Purely a statutory creation.

Elements of usury A loan or forbearance. An understanding between the parties that the loan shall or may

be returned. An unlawful intent to make more than the legal rate for the use

of money or its equivalent. The taking or agreeing to take for the use of the loan of

something in excess of what is allowed by law. When the Usury Law applies

An act fixing rates of interest upon loans and declaring he effect of receiving or taking usurious rates, and for other purposes.

Two transactions:o Loan (mutuum)o Forbearance of a debt signifies the contractual obligation

of the creditor to forbear during a given period to require the debtor, payment of an existing debt then due and payable.

No loan or forbearance = no usury. Usury law is only suspended by Circular Bank No. 905. Only a

law can repeal another law.

Interest - compensation allowed by law or fixed by the parties for the loan or forbearance of money, goods, or credits.

Kinds of interest: Simple interest: that which is paid for the principal at a certain

rate fixed or stipulated by parties. Compound interest: that which is imposed upon interest due

and unpaid.o Accrued interest is added to the principal sum. The whole

(principal + accrued interest) is treated as a new principal upon which the interest for the next period is calculated.

Legal interest: that which the law directs to be charged in the absence of any agreements as to the rate between parties.o 6% should be computed from the date of the rendition of

the judgment and not from the filing of the complaint. Lawful interest: that which the law allows or does not prohibit,

that is, the rate of interest within the maximum prescribed by the law.

Unlawful/usurious interest: that which is paid or stipulated to be paid beyond the maximum fixed by the law.

Old rule: CB circular: 12% if loan or forbearance + judgment involving

such loan or forbearance.o Payment of unliquidated cash advances to an employee by

her employer.o Return of the money paid by the buyer of a leasehold right

but which contract was voided due to the fault of the seller.

*BPI v.Makalingaw

READ THE USURIOUS LAW PROPERLY

o May be imposed even though there is no loan or forbearance, in cases of delay in the payment of the sums adjudged in a final judgment, and not as part of the judgment for damages.

Interim period from finality of judgment awarding a monetary claim and until payment= forbearance of credit.

Article 2209: payment of indemnities as damages in the form of interest.

Interest rates (under usury law): Legal rate: 12% per annum Maximum rate (Usury law)

o 12% per annum: loan is secured by a mortgage upon real estate with Torrens title; or agreement conveying such real estate or an interest therein. (Other secured loans: treasury bills, Central Bank certificate of indebtedness)

o 14% per annum: loan is not secured. Maximum rate (Central Bank Circular, July 21, 1981):

o 16%: secured loans of 365 days or less (commissions, fees, and other charges are included).

o 18%: unsecuredo More than 365 days: not subject to any ceiling.

When is it a penalty? When an excessive rate of interest is made payable only in case

of default in payment of the principal. Higher rate is imposed not as an interest but as a penalty for non-performance. No stipulation preventing this (other than the power of the courts to modify unconscionable ones).o Available only to section 3.

Attorney's fees to cover costs of collection = NOT INTEREST. If excessive, subject to equitable reduction.

Determination of existence of usury: Corrupt agreement must be present! Where consideration of loan is property or services of uncertain

value. -> not necessarily usurious. Form of contract is not conclusive.

o Check pacto de retro contracts.

When Usury Law is not applicable: Check examples in the book + cases!

Rules on interests:1. When an obligation, regardless of its source, is breached, the contravenor can be held liable for damages.2. If obligation consists in the payment of a sum of money (loan, forbearance of money, judgment money)

a. Interest due is what has been stipulated by the parties

b. The interest shall earn legal interest from the time of judicial demand.c. If there’s no stipulation, the rate is 12% from default (judicial or extrajudicial demand).

3. If obligation is not a loan or forbearance of moneya. Interest on the amount of damages awarded may be imposed at the discretion of the court at 6%.b. No interest shall be adjudged on unliquidated claims or damages, except when or until the amount can be established with reasonable certainty.c. Where the amount is established with reasonable certainty, the interest shall begin from the time the claim is made judicially or extrajudicially.d. But when such certainty cannot be so reasonably established the time the demand is made, the interest shall begin to run only from the date the judgment of the court is made.e. The actual base (principal) for the computation of the legal interest shall, in any case, be on the amount finally adjudged.

4. When judgment of court awarding a sum of money becomes final and executory, 12% interest from such until its payment.

DEPOSITCHAPTER 1: DEPOSIT IN GENERAL AND ITS DIFFERENT KINDS

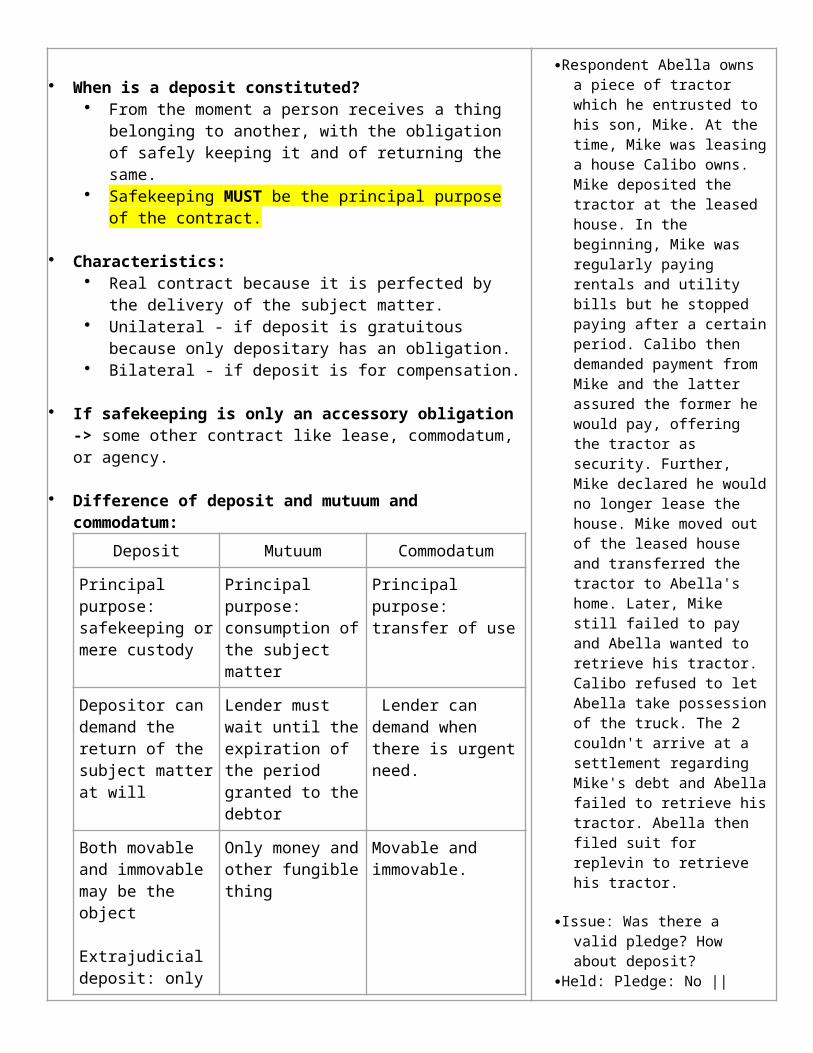

Art. 1962 (Deposit)

When is a deposit constituted? From the moment a person receives a thing belonging to another,

with the obligation of safely keeping it and of returning the same.

Safekeeping MUST be the principal purpose of the contract.

Characteristics: Real contract because it is perfected by the delivery of the

subject matter. Unilateral - if deposit is gratuitous because only depositary has

an obligation. Bilateral - if deposit is for compensation.

If safekeeping is only an accessory obligation -> some other contract like lease, commodatum, or agency.

Difference of deposit and mutuum and commodatum:

Deposit Mutuum Commodatum

Principal purpose: Principal purpose: Principal purpose:

1. Calibo v. CARespondent Abella owns a piece of

tractor which he entrusted to his son, Mike. At the time, Mike was leasing a house Calibo owns. Mike deposited the tractor at the leased house. In the beginning, Mike was regularly paying rentals and utility bills but he stopped paying after a certain period. Calibo then demanded payment from Mike and the latter assured the former he would pay, offering the tractor as security. Further, Mike declared he would no longer lease the house. Mike moved out of the leased house and transferred the tractor to Abella's home. Later, Mike still failed to pay and Abella wanted to retrieve his tractor. Calibo refused to let Abella take possession of the truck. The 2 couldn't arrive at a settlement

safekeeping or mere custody

consumption of the subject matter

transfer of use

Depositor can demand the return of the subject matter at will

Lender must wait until the expiration of the period granted to the debtor

Lender can demand when there is urgent need.

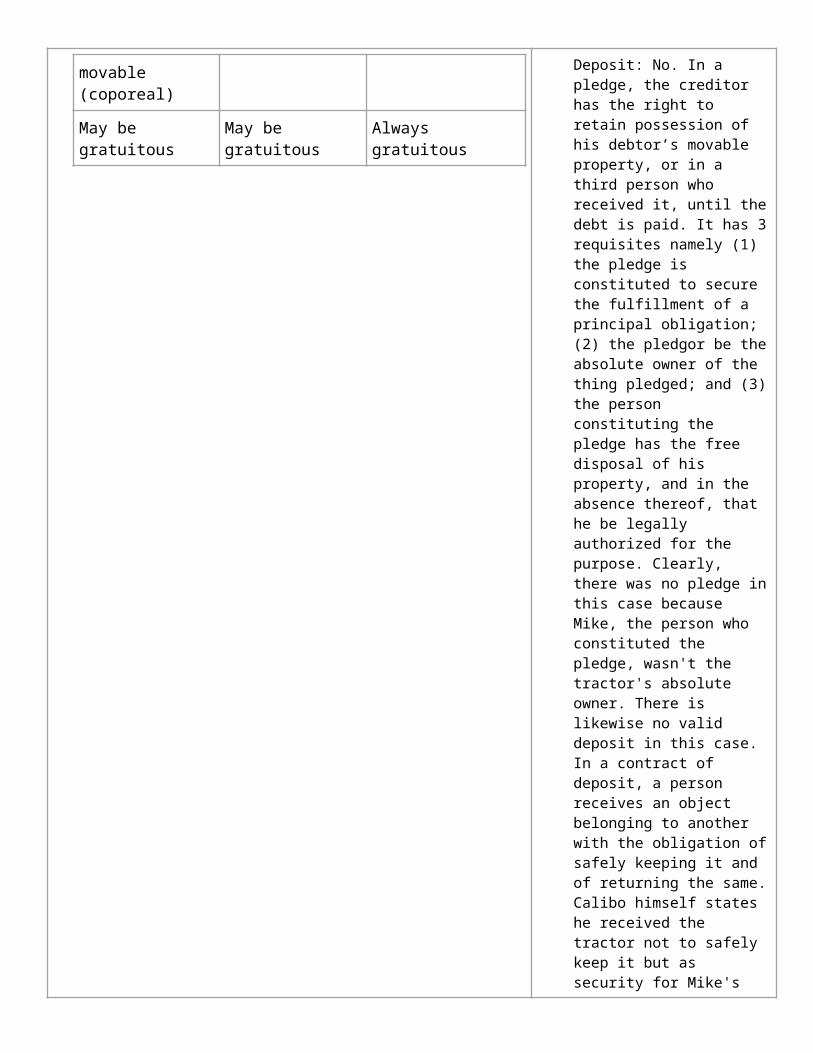

Both movable and immovable may be the object

Extrajudicial deposit: only movable (coporeal)

Only money and other fungible thing

Movable and immovable.

May be gratuitous May be gratuitous Always gratuitous

regarding Mike's debt and Abella failed to retrieve his tractor. Abella then filed suit for replevin to retrieve his tractor.

Issue: Was there a valid pledge? How about deposit?

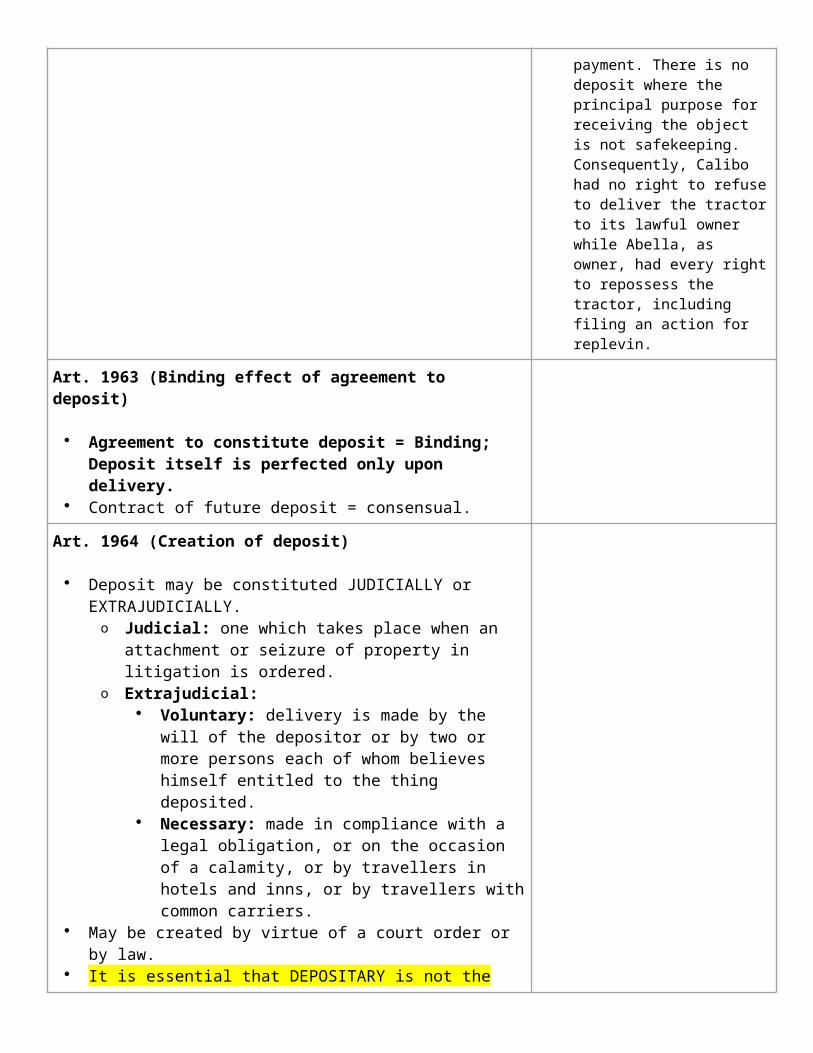

Held: Pledge: No || Deposit: No. In a pledge, the creditor has the right to retain possession of his debtor’s movable property, or in a third person who received it, until the debt is paid. It has 3 requisites namely (1) the pledge is constituted to secure the fulfillment of a principal obligation; (2) the pledgor be the absolute owner of the thing pledged; and (3) the person constituting the pledge has the free disposal of his property, and in the absence thereof, that he be legally authorized for the purpose. Clearly, there was no pledge in this case because Mike, the person who constituted the pledge, wasn't the tractor's absolute owner. There is likewise no valid deposit in this case. In a contract of deposit, a person receives an object belonging to another with the obligation of safely keeping it and of returning the same. Calibo himself states he received the tractor not to safely keep it but as security for Mike's payment. There is no deposit where the principal purpose for receiving the object is not safekeeping. Consequently, Calibo had no right to refuse to deliver the tractor to its lawful owner while Abella, as owner, had every right to repossess the tractor, including filing an action for replevin.

Art. 1963 (Binding effect of agreement to deposit)

Agreement to constitute deposit = Binding; Deposit itself is perfected only upon delivery.

Contract of future deposit = consensual.

Art. 1964 (Creation of deposit)

Deposit may be constituted JUDICIALLY or EXTRAJUDICIALLY.o Judicial: one which takes place when an attachment or

seizure of property in litigation is ordered.o Extrajudicial:

Voluntary: delivery is made by the will of the depositor or by two or more persons each of whom believes himself entitled to the thing deposited.

Necessary: made in compliance with a legal obligation, or on the occasion of a calamity, or by travellers in hotels and inns, or by travellers with common carriers.

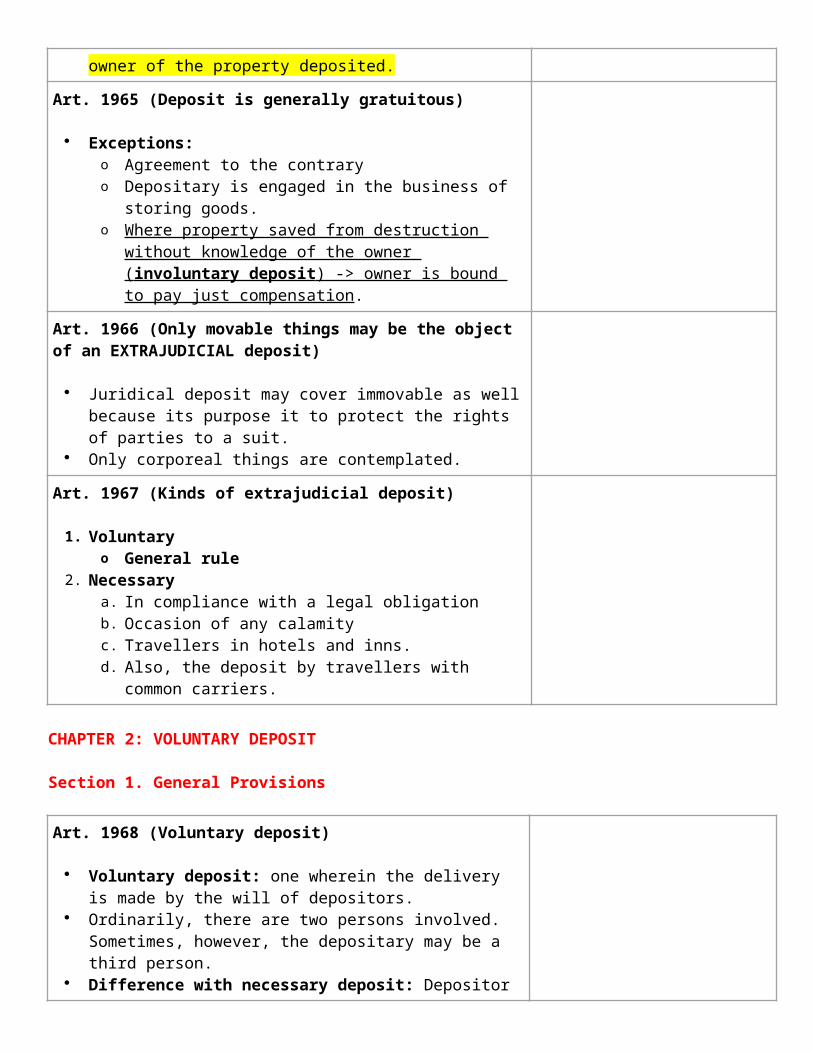

May be created by virtue of a court order or by law. It is essential that DEPOSITARY is not the owner of the property

deposited.

Art. 1965 (Deposit is generally gratuitous)

Exceptions:o Agreement to the contraryo Depositary is engaged in the business of storing goods.o Where property saved from destruction without knowledge of

the owner ( involuntary deposit ) -> owner is bound to pay just compensation.

Art. 1966 (Only movable things may be the object of an EXTRAJUDICIAL deposit)

Juridical deposit may cover immovable as well because its purpose it to protect the rights of parties to a suit.

Only corporeal things are contemplated.

Art. 1967 (Kinds of extrajudicial deposit)

1. Voluntaryo General rule

2. Necessarya. In compliance with a legal obligationb. Occasion of any calamityc. Travellers in hotels and inns.d. Also, the deposit by travellers with common carriers.

CHAPTER 2: VOLUNTARY DEPOSIT Section 1. General Provisions

Art. 1968 (Voluntary deposit)

Voluntary deposit: one wherein the delivery is made by the will of depositors.

Ordinarily, there are two persons involved. Sometimes, however, the depositary may be a third person.

Difference with necessary deposit: Depositor has complete freedom in choosing the depositary (voluntary).

General Rule: Depositor must be the owner of the thing deposited.o Exceptions: carrier, commission agent, lessee, etc. may

deposit goods temporarily in his possession considering that the contract does not involve the transfer of ownership.

Where there are several depositors:o Two or more persons claiming to be entitled to a thing may

deposit the same to a third person. Third person assumes the obligation to deliver to the one

to whom it belongs.o INTERPLEADER - action to compel the depositors to settle

their conflicting claims among themselves.

Art. 1969 (Form of contract of deposit)

May be oral or in writing. Only thing required: delivery of the thing.

Art. 1970 (Incapacitated Depositor)

If Depositary is CAPACITATED:o Subject to all obligations of a depositary whether the

depositor is capacitated or not.o Depositary may be compelled to return the property to the

legal representative of the incapacitated person or to the depositor himself if he should acquire responsibility.

Art. 1971 (Incapacitated Depositary)

Incapacitated depositary does NOT incur the obligation of a depositary.o Liable to (aka Depositor's action):

Return the thing deposited while still in his/her possession.

Pay the depositor the amount by which he may have benefited himself with the thing or its price subject to the right of any third person who acquired the thing in good faith.

If a third person who acquired the thing is in bad faith, depositor can bring an action against him for its recovery.

*What does it mean to be "benefited?" some tangible benefit! Depositor can perhaps recover from parents of minors (?).

*Take note: not the actual value of the thing, but the amount by which the depositary may have been benefited.

Section 2. Obligations of the Depositary

Art. 1972 (Obligation to keep the thing deposited and return it)

Depositary is obliged to (1) keep the thing safely, and (2)

Bishop of Jaro v. Dela Pena Trust fund which trustee mixed with his

own and deposited in a bank to his personal account was lost through force

return it, when required. Degree of care must be the same as the diligence that he

would exercise over his property.o Why?

Essential requisite of the juridical relation which involves the depositor's confidence in the depositary's good faith and trustworthiness.

Presumption that depositor picked the depositary for his/her diligence.

Depositary CANNOT excuse himself in the event of loss by claiming that he exercised the same amount of care toward the thing deposited as he would toward his own, IF SUCH CARE IS LESS THAN THAT REQUIRED BY THE CIRCUMSTANCES.

Rules applicable:o Liability of the depositary for the care and delivery of

the thing loaned is governed by the rules on obligations!

Liable if the loss occurs through his fault or negligence, even if the thing was insured.

Loss of the thing while in his possession, ordinarily raises a presumption of fault on his part.

Required degree of care is greater if the deposit is for compensation!

Return before specified term:o Must be returned to depositor whenever he claims it,

even though a specified term or time for such may have been stipulated in the contract.

majeure (Trustee was arrested by the military authorities and the entire deposit was confiscated by the government).

Issue: Is trustee liable? Held: Trustee is not liable. By placing

money in the bank and mixing it with his personal funds, trustee did not assume an obligation different from that under which he would have lain if such deposit had not been made nor did he thereby make himself liable to repay the money at all hazards. The fact that he placed the trust funds in his personal account did not add to the responsibility.

Dissenting: When trustee mixed his funds with the trust fund, he stamped on the said funds his own private marks and unclothed it of all the protection that it had. If this was deposited in the name of the depositor, military would not have confiscated it.

Art. 1973 (Obligation not to transfer deposit)

General Rule: Depositary CANNOT deposit the thing with a third person.o Exception: If authorized by EXPRESS stipulation.

Depositary is liable for the deposit to a third person, when?o No authorityo Authorized, but deposited it to a third person who is

manifestly careless or unfit.o Lost through negligence of his employees.

What could be the indication that a person is manifestly unfit or careless?

Art. 1974 (Obligation not to change way of deposit)

Depositary may change the way or manner of deposit if there are circumstances indicating that the depositor would consent to the change if he knew of the facts of the situation.

Before the depositary may make the change, HE SHALL NOTIFY THE DEPOSITOR thereof and wait for his

decision, unless delay would cause danger.

Art. 1975 (Obligation to collect interest)

If a thing (certificates, bonds, securities or instruments) deposited should earn interest, depositary is under the obligation:1. Collect interest as it becomes due (capital itself also

when due). Does not apply to a depositary of certificates,

bonds, securities, or instruments which earn interest if such documents are kept in a rented safety deposit box.

2. Take such steps as may be necessary to preserve their value and rights corresponding them according to the law.

Contract for rent of safety deposit boxes.o Not an ordinary contract of lease of things but a

special kind of deposit; hence, it is not to be strictly governed by provisions on deposit.

o Prevailing rule in US: bailor-bailee relationship!o Possession of the contents should reasonably be

considered to be in the bank since the bank is, by nature of the contract, given absolute control of access to the property and the depositor cannot gain access thereto without the consent and active participation of the bank.

CA Agro-Industrial Devpt. Corp. v. CA The contents of a safety deposit which can

be opened only with the use of 1 of 2 renter's keys given to the joint renter and by a guard key in the possession of the bank were missing. (Contract of lease was signed)

Issue: Was the contract that of bailee-bailor or lessor-lessee?

Held: Petition is partly meritorious.o Contract is not an ordinary contract

of lease but a special kind of deposit. Not a lease because the full

and absolute possession and control of the safety deposit box was not given to the joint renters.

o Relation created is that of bailor and bailee.

Bailment is for hire and mutual benefit.

o Contract 13 & 14 are void. Any stipulation exempting the

depositary from liability arising from the loss of the thing deposited on account of fraud, negligence or delay would be void for being contrary to law and public policy.

o Bank was unaware of the agreement between joint renters.

Art. 1976 (Obligation not to commingle things deposited if so stipulated)

General Rule: Depositary may commingle grain or other articles of the same kind and quality.o Exception: stipulation to the contrary.o Depositors shall own or have proportionate interest in

the mass.

Art. 1977 (Obligation not to make use of thing deposited unless authorized)

General Rule: Depositary cannot make use of the thing deposited without the express permission of the depositor.o If not, LIABLE FOR DAMAGES.o However, when preservation of the thing deposited

requires its use, it MUST BE USED BUT ONLY FOR THAT PURPOSE. (no need for express permission)

Javellana v. Lim After failing to "return" money received as

a "deposit without interest," debtors bound themselves to pay interest until refund is made.

Issue: Was the contract a loan or a deposit?

Held: The second document was a real loan of money with interest, notwithstanding that in the original document it was called a deposit.

Art. 1978 (Effect if permission is given to make use of the thing)

Contract loses the concept of a deposit and becomes a loan (if money or consumable thing) or commodatum (if real property).o Exception: if safekeeping is still the purpose of a

contract. (IRREGULAR DEPOSITS) Permission is not presumed. Its existence must be proven

by the depositary.

Irregular deposit distinguished from mutuum

Irregular deposit Mutuum

Consumable thing deposited may be demanded at will by the irregular depositor for whose benefit the deposit has been constituted.

Lender is bound by the provisions of the contract and cannot seek restitution until time of payment as stated in the contract.

Only benefit is that which accrues to the depositor.

Essential cause for the transaction is the necessity of the borrower.

Depositor has preference over other creditors with respect to the thing deposited, while common creditors enjoy no preference in the distribution of the debtor's property.

No special preference (?).

Gavieres v. Tavera Amount is received "as a deposit" but debtor

binds himself to pay interest. Issue: Is it a deposit or a loan? Held: Although in the document a deposit is

spoken nevertheless, it clearly appears that the contract was a loan and that was the intention of the parties. Obligation of the debtor to pay interest suffices to cause the obligation to be considered a loan and makes it likewise evident that it was the intention of the parties that the debtor shall have a right to make use of the amount deposited, since it was stipulated that the amount should be collected after notice of 2 months in advance.

Note: If there’s a stipulation to pay interest, “deposit” becomes a loan.

Baron v. David Depositary was allowed to mill the palay

deposited and had milled and appropriated it to his own use before his rice mill was burned.

Issue: Is the depositary bound to account for its value?

Held: Yes. Even supposing that the palay may have been delivered in the character of a deposit, subject to future sale or withdrawal at the depositor's election, nevertheless, it was understood that the depositary might mill the palay and he has, in fact, appropriated it to his own use, he is of course, bound to account for its value. The contract loses the concept of a deposit and becomes a loan!

US v. Igpaura Depositary appropriated to his personal

benefit money deposited which depositor failed to claim at once.

Issue: Did this failure or delay imply permission to use the money?

Held: No. Failure to claim at once or delay for some time in demanding restitution of the thing deposited, which was immediately due, does not imply permission to use the thing deposited as would convert the deposit into loan. Permission is not presumed except in certain cases.

Art. 1979 (Depositary's liability for loss of thing through a fortuitous event)

When? SUDAo If stipulated;o Uses the thing without depositor's permission;

Palacio v. Sudario

Important because it tells you how to prove the cause of the loss. (Take note of this case)

o Delays its return;o Allows others to use it, even though he himself may

have been authorized to use the same.

Art. 1980 (Relation between bank and depositor)

Deposits of money in banks and similar institutions (whether fixed, savings, and current deposits of money) are really loans to a bank.o Why? Because the bank can use the same for its

ordinary transactions and for the banking business in which it is engaged.

Bank has the obligation to return the amount deposited, but not the same money that was actually deposited.

Relationship between depositor and a bank = creditor & debtor.o Deposit agreement between the bank and the

depositor determines the rights and obligations of the parties.

Bank's failure to honor a deposit = failure to pay an obligation and not a breach of trust arising from a depositary's failure to return the subject matter of the deposit. It will not constitute estafa through misappropriation.

Payment by a bank of the amount of a depositor's check = extinguishes obligation.

General Rule: Bank can compensate or set off the deposit in its hands for the payment of any indebtedness to it on the part of the depositor.o In a true deposit, compensation is not allowed.

In the performance of its obligations, drawee bank is bound by its internal banking rules and regulations and is liable to the depositor for fraud, negligence, or delay.o Exemplary damages = when there is malice, bad faith

or gross negligence.o Moral damages = may be awarded even if negligence

was not attended by bad faith or malice.

A bank is imbued with public interest, hence it should exercise extraordinary diligence to negate its liability to its depositors.

A bank is not excused from its obligations to depositors when it was suspended by Central Bank.o However, they are not liable to pay interest on the

deposit during the suspension.

Gullas v. PNB

Serrano v. Central Bank

Art. 1981 (When thing deposited is delivered closed and sealed)

Depositary must return it in the same condition.o Liable for damages should the seal or lock be broken

through his fault.o Fault on the part of the depositary is presumed, unless

proof to the contrary. When the seal or lock is broken, with or without his fault,

depositary must keep the secret of the deposit. As regards the value of the thing deposited, statement of

the depositor shall be accepted when the forcible opening is imputable to the depositary, should there be no proof to the contrary.o However, the courts may pass upon the credibility of

the depositor with respect to the value claimed by him.

Art. 1982 (When depositary justified to open)

1. Presumed authority (if key has been delivered to him or when instructions of the depositor cannot be executed without opening the box)

2. Necessity

Art. 1983 (Obligation to return products, accessories, and accessions)

Depositary must return thing + all its products, accessories, and accessions which are a consequence of ownership.

If what has been deposited is money -> depositary has no right to make use thereof, and therefore, he is not liable to pay interest.o If depositary is in delay or has used the money

without permission -> liable for interest as indemnity. Interest will be counted from the day when he

first applied to his own use the deposit + those which he still owes after the extinguishment of the deposit.

Art. 1984 (Depositor need not prove his ownership)

Depositary who receives the thing in deposit cannot require that the depositor prove his ownership.o Why? (1) not essential that the depositor be the owner

of the thing, (2) may open the door to fraud and bad faith, for the depositary, on the pretense of requiring proof of ownership, may be able to retain the thing.

Where third person appears to be the owner:a. Reasonable ground to believe that the thing has not

been lawfully acquired by the depositor.b. Depositary discovers the thing stolen.

Requisites: Depositary must know (1) that the thing

have been stolen, and (2) who the true owner is.

o Steps: Advise true owner of the deposit. If true owner does not claim it within one

month, depositary shall be relieved of all responsibility by returning the thing deposited to the depositor.

True owner may still claim it after one month through other legal processes.

Art. 1985 (Right of two or more depositors)

Two or more debtors + not solidary + thing admits of division = one cannot demand more than his/her share.

Two more + solidary or thing does not admit of division = rules on solidarity among creditors shall apply, to the effect that each one of the solidary debtors may do whatever may be useful to the others but not anything which may be prejudicial to the latter, and the depositary may return the thing to any one of the solidary depositors unless a demand, judicial or extrajudicial, for its return has been made by one of them in which case delivery should be made to him.o If there is a stipulation that the thing be returned to

one of the depositors, depositary shall return it only to the person designated.

Art. 1986 (Person to whom return must be made)

Depositor is obliged to return the thing deposited, when required, to the depositor, to his heirs and successors, or to the person who may have been designated in the contract.

If depositor becomes incapacitated after having made the deposit, thing cannot be returned except to the persons who may have administration of his property and rights.

Art. 1987 (Place of return)

Where?a. Place agreed upon by the parties. (Expenses for

transportation are borne by the depositor)b. Absent a stipulation, place where thing deposited

might be even if it should not be the same where the original deposit was made provided the transfer was accomplished without malice on the part of the depositary.

Art. 1988 (Time of return)

General Rule: Depositor can demand the return of the thing deposited at will and this is whether there is a period or not.o Exception (depositary is not obliged, but must inform

Sesbreno v. CA

the depositor immediately of the opposition or attachment):

When the thing is judicially attached while in the depositary's possession. (judicial order of attachment)

He have been notified of the opposition of a third person to return or the removal of the thing deposited.

Better thing to do is to allow depositary to consign the thing in court through an action of interpleader.

Art. 1989 (Right of depositary to return thing deposited)

Depositary may return the thing deposit if it was GRATUITOUS and for JUSTIFIABLE REASONS.o If depositor refuses, depositary may consign the

thing. If depositary is for a VALUABLE CONSIDERATION =

no right to return it. Bound by the period and restitution before its expiration constitutes a breach of obligation.

Art. 1990 (Liability for loss by force majeure or government order)

If depositary receives no money for it = no liability. If depositary receives money or another thing in its place =

duty to deliver to the depositor what he has received otherwise, he would enrich himself at the expense of the depositor.

Art. 1991 (Alienation in good faith by depositary's heir)

If depositary's heir, in good faith, sold the thing which he did not know was deposited => he shall only be bound (1) to return the price received or (2) to assign the right to collect the same if it has not been paid.

If third person is in bad faith = depositor may recover the thing.

If heir is in bad faith = liable for damages. The sale or appropriation constitutes estafa.

Section 3. Obligations of the Depositor

Art. 1992 (Obligation to pay expenses of preservation)

If deposit is GRATUITOUS = depositor is obliged to reimburse the depositary for the expense he may have incurred for the preservation of the thing deposited.o Right to reimbursement covers all types of expenses!

If deposit is for COMPENSATION = expense for

Take note on whether it is gratuitous or not.

preservation are borne by the depositary because they are deemed to be included in the compensation.o However, there can be a contrary stipulation.

Art. 1993 (Obligation to pay losses incurred due to character of thing deposited)

General Rule: Depositor shall reimburse the depositary for any loss arising from the character of the thing deposited.o Exception:

At the time of the constitution of the deposit, the depositor was not aware of the dangerous character of the thing.

At the time of the constitution of the deposit, the depositor was not expected to know of the dangerous character of the thing.

Notified the depositary of the same. Depositary was aware of it without advice from

the depositor.

Art. 1994 (Depositary's right of retention)

Depositary may retain the thing until full payment of what may be due him by reason of the deposit.

Example of a pledge created by law. Thing retained serves as security for the payment.

Difference between deposit and commodatum:Right of retention: Deposit – until full payment of what may be due him by reason of the deposit. Commodatum – damages in Art. 1951 (flaws of the thing loaned).

Art. 1995 (Deposit's extinguishment)