credit card sector deck (private life of mail)

TRANSCRIPT

MAIL’S EVOLVING ROLE

IN TODAY’S

CREDIT CARD MARKETPLACE

Date

Audience

Credit card marketing and the role of mail

The new news about mail

Why use mail now

Our products and services

WHAT WE WOULD LIKE TO

TALK ABOUT TODAY

2

CREDIT CARDS

AND THE ROLE OF MAIL

3

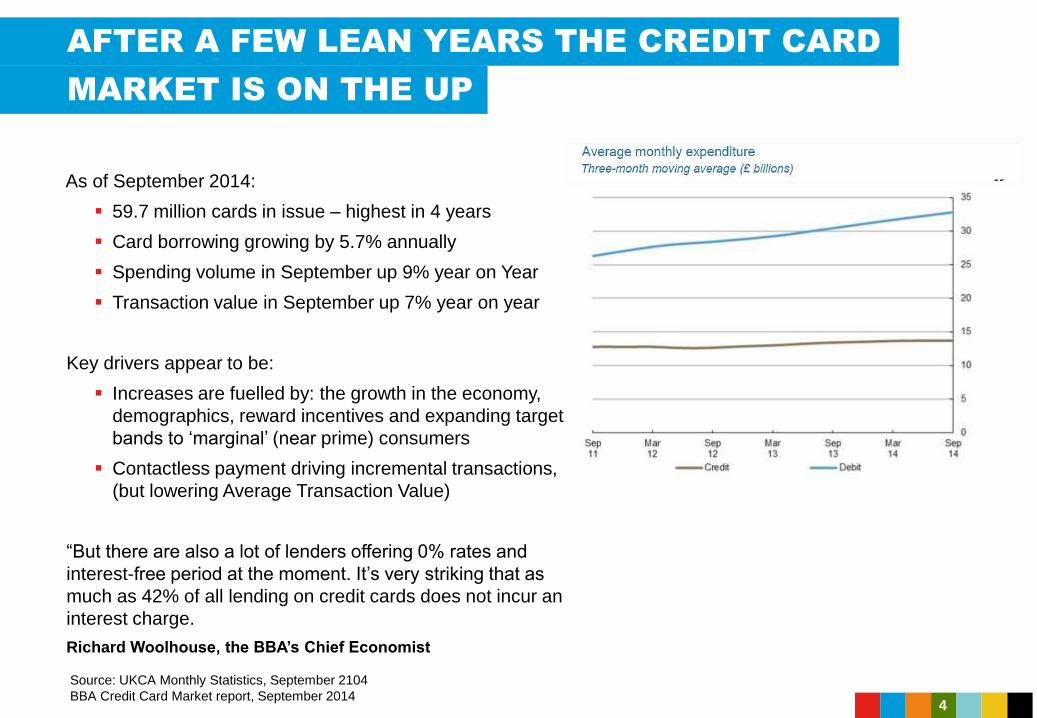

AFTER A FEW LEAN YEARS THE CREDIT CARD

As of September 2014:

59.7 million cards in issue – highest in 4 years

Card borrowing growing by 5.7% annually

Spending volume in September up 9% year on Year

Transaction value in September up 7% year on year

Key drivers appear to be:

Increases are fuelled by: the growth in the economy,

demographics, reward incentives and expanding target

bands to ‘marginal’ (near prime) consumers

Contactless payment driving incremental transactions,

(but lowering Average Transaction Value)

“But there are also a lot of lenders offering 0% rates and

interest-free period at the moment. It’s very striking that as

much as 42% of all lending on credit cards does not incur an

interest charge.

Richard Woolhouse, the BBA’s Chief Economist

Source: UKCA Monthly Statistics, September 2104

BBA Credit Card Market report, September 2014

MARKET IS ON THE UP

4

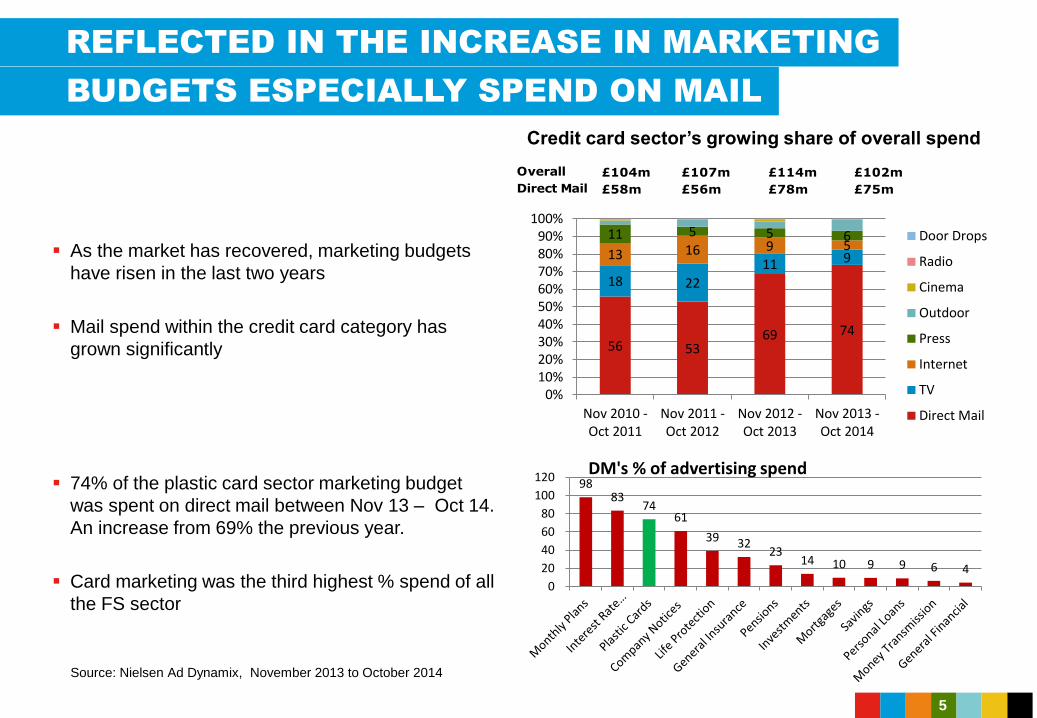

REFLECTED IN THE INCREASE IN MARKETING

As the market has recovered, marketing budgets

have risen in the last two years

Mail spend within the credit card category has

grown significantly

74% of the plastic card sector marketing budget

was spent on direct mail between Nov 13 – Oct 14.

An increase from 69% the previous year.

Card marketing was the third highest % spend of all

the FS sector

Source: Nielsen Ad Dynamix, November 2013 to October 2014

BUDGETS ESPECIALLY SPEND ON MAIL

56 53 69 74

18 22

11 9 13 16 9 5 11 5 5 6

0%10%20%30%40%50%60%70%80%90%

100%

Nov 2010 -Oct 2011

Nov 2011 -Oct 2012

Nov 2012 -Oct 2013

Nov 2013 -Oct 2014

Door Drops

Radio

Cinema

Outdoor

Press

Internet

TV

Direct Mail

Credit card sector’s growing share of overall spend

Overall £104m £107m £114m £102m

Direct Mail £58m £56m £78m £75m

98 83

74 61

39 32 23

14 10 9 9 6 4

0

20

40

60

80

100

120DM's % of advertising spend

5

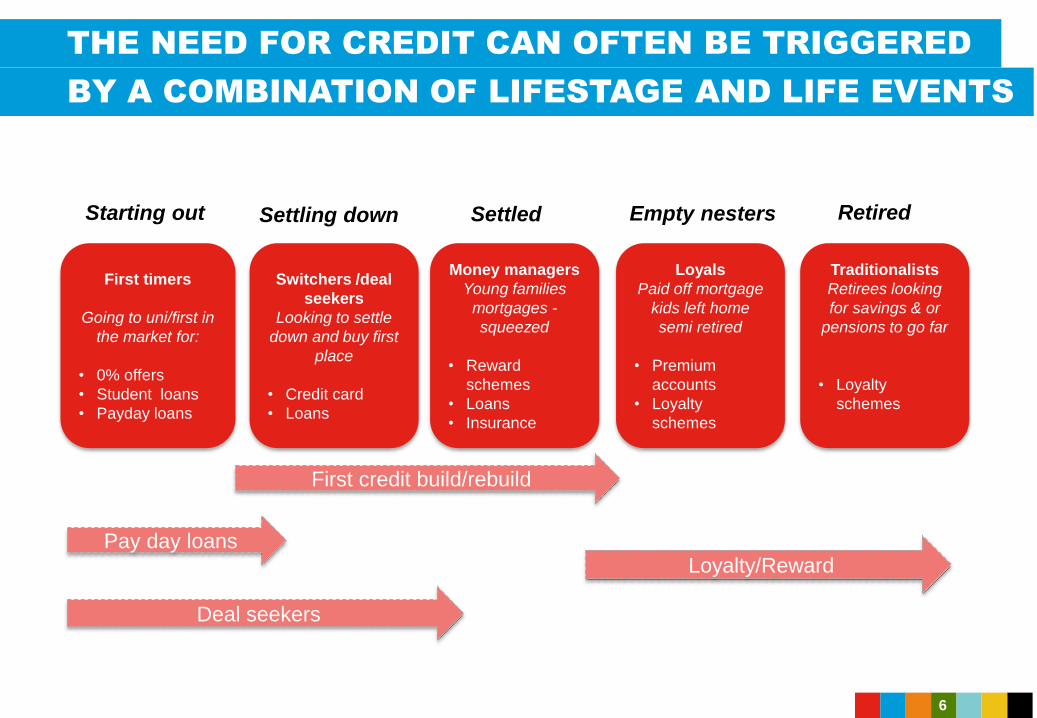

THE NEED FOR CREDIT CAN OFTEN BE TRIGGERED

First timers

Going to uni/first in

the market for:

• 0% offers

• Student loans

• Payday loans

Starting out Settling down

Switchers /deal

seekers

Looking to settle

down and buy first

place

• Credit card

• Loans

Money managers

Young families

mortgages -

squeezed

• Reward

schemes

• Loans

• Insurance

Loyals

Paid off mortgage

kids left home

semi retired

• Premium

accounts

• Loyalty

schemes

Settled Empty nesters

Traditionalists

Retirees looking

for savings & or

pensions to go far

• Loyalty

schemes

Retired

First credit build/rebuild

Deal seekers

Loyalty/RewardPay day loans

BY A COMBINATION OF LIFESTAGE AND LIFE EVENTS

6

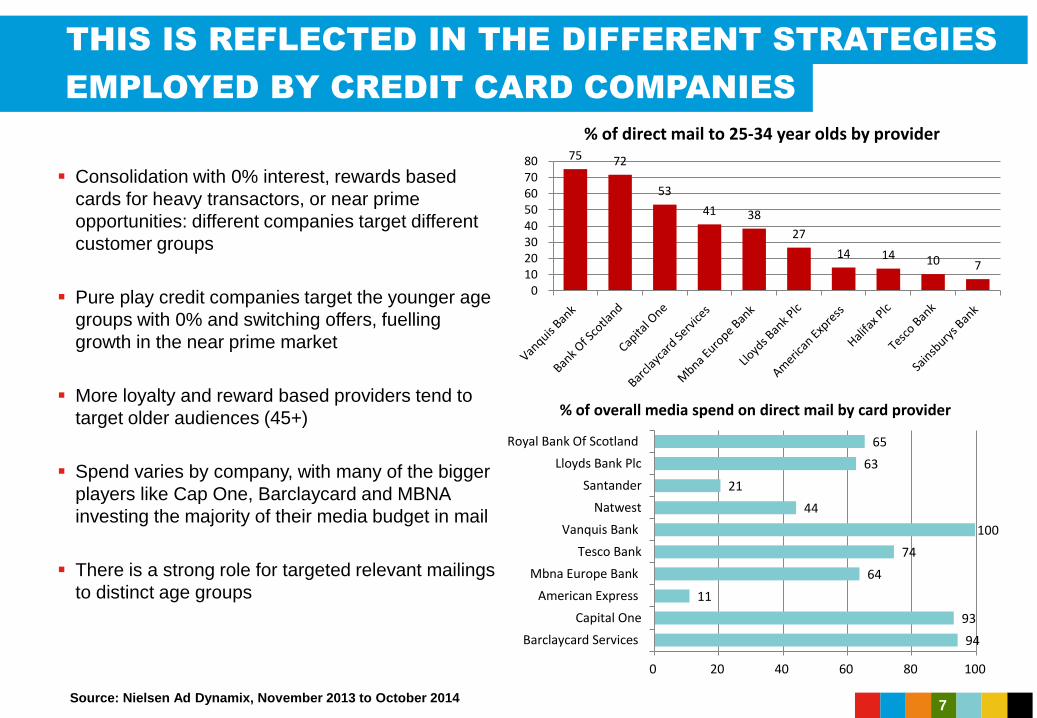

THIS IS REFLECTED IN THE DIFFERENT STRATEGIES

Consolidation with 0% interest, rewards based

cards for heavy transactors, or near prime

opportunities: different companies target different

customer groups

Pure play credit companies target the younger age

groups with 0% and switching offers, fuelling

growth in the near prime market

More loyalty and reward based providers tend to

target older audiences (45+)

Spend varies by company, with many of the bigger

players like Cap One, Barclaycard and MBNA

investing the majority of their media budget in mail

There is a strong role for targeted relevant mailings

to distinct age groups

EMPLOYED BY CREDIT CARD COMPANIES

Source: Nielsen Ad Dynamix, November 2013 to October 2014

75 72

53

41 38

27

14 14 10 7

01020304050607080

% of direct mail to 25-34 year olds by provider

94

93

11

64

74

100

44

21

63

65

0 20 40 60 80 100

Barclaycard Services

Capital One

American Express

Mbna Europe Bank

Tesco Bank

Vanquis Bank

Natwest

Santander

Lloyds Bank Plc

Royal Bank Of Scotland

% of overall media spend on direct mail by card provider

7

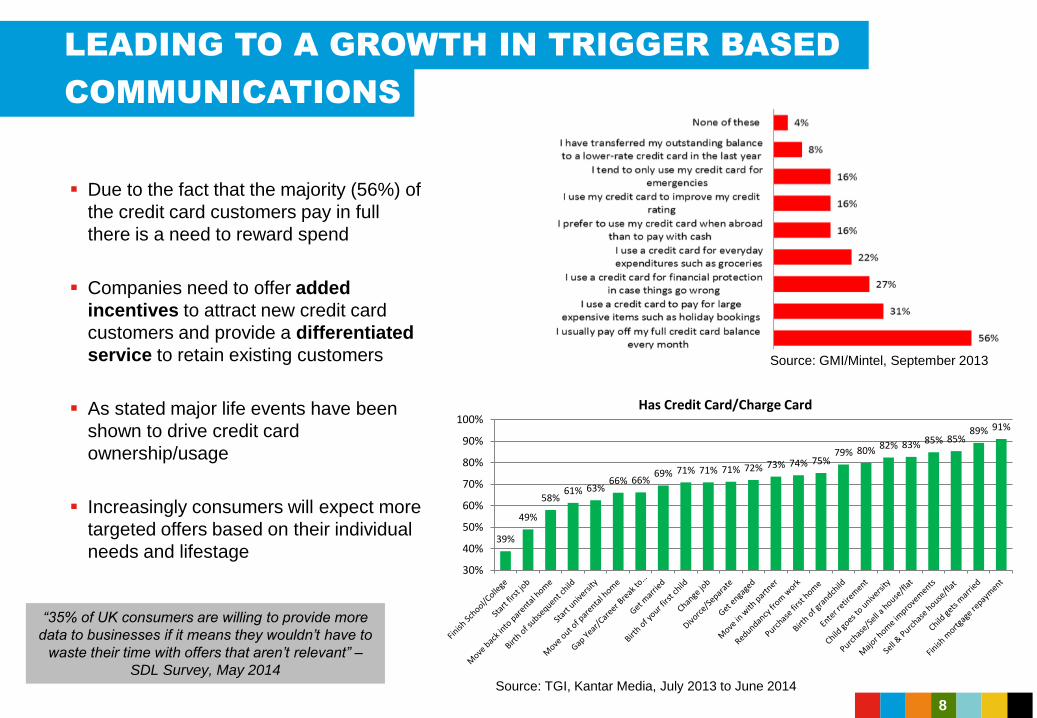

LEADING TO A GROWTH IN TRIGGER BASED

Due to the fact that the majority (56%) of

the credit card customers pay in full

there is a need to reward spend

Companies need to offer added

incentives to attract new credit card

customers and provide a differentiated

service to retain existing customers

As stated major life events have been

shown to drive credit card

ownership/usage

Increasingly consumers will expect more

targeted offers based on their individual

needs and lifestage

“35% of UK consumers are willing to provide more

data to businesses if it means they wouldn’t have to

waste their time with offers that aren’t relevant” –

SDL Survey, May 2014

COMMUNICATIONS

Source: GMI/Mintel, September 2013

Source: TGI, Kantar Media, July 2013 to June 2014

39%

49%

58%61% 63%

66% 66%69% 71% 71% 71% 72% 73% 74% 75%

79% 80% 82% 83% 85% 85%89% 91%

30%

40%

50%

60%

70%

80%

90%

100%Has Credit Card/Charge Card

8

THE MARKET DYNAMICS AND TARGETING

Source: Ebiquity, August 2014

Big growth in pre-authorised and personal targeted mail, as well as in loyalty and value added products/messaging

Pre-authorisation / Personalised Offers Loyalty / Value AddedO% Offers

STRATEGIES ARE REFLECTED IN THE DIFFERENT

MESSAGING APPROACHES

9

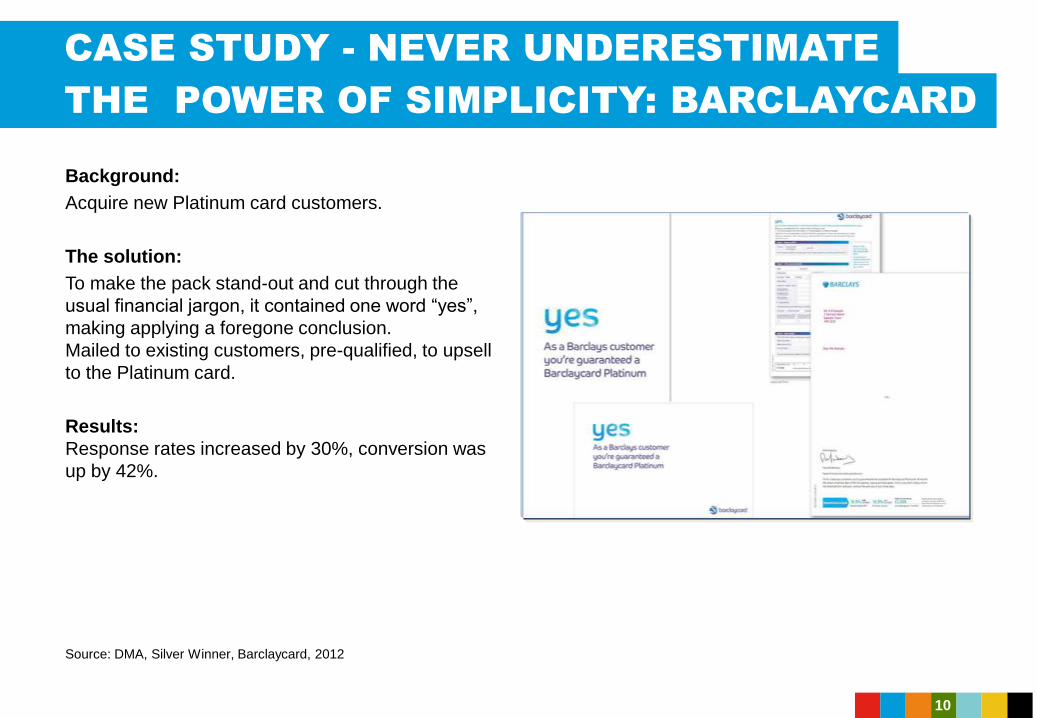

CASE STUDY - NEVER UNDERESTIMATE

Background:

Acquire new Platinum card customers.

The solution:

To make the pack stand-out and cut through the

usual financial jargon, it contained one word “yes”,

making applying a foregone conclusion.

Mailed to existing customers, pre-qualified, to upsell

to the Platinum card.

Results:

Response rates increased by 30%, conversion was

up by 42%.

Source: DMA, Silver Winner, Barclaycard, 2012

THE POWER OF SIMPLICITY: BARCLAYCARD

10

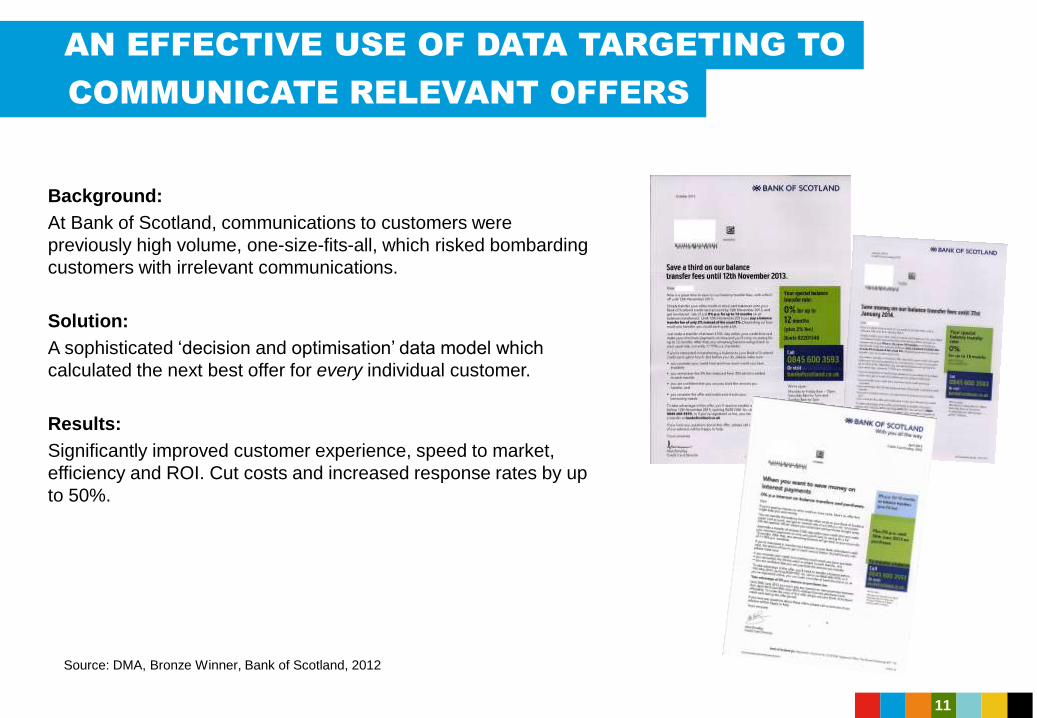

AN EFFECTIVE USE OF DATA TARGETING TO

Background:

At Bank of Scotland, communications to customers were

previously high volume, one-size-fits-all, which risked bombarding

customers with irrelevant communications.

Solution:

A sophisticated ‘decision and optimisation’ data model which

calculated the next best offer for every individual customer.

Results:

Significantly improved customer experience, speed to market,

efficiency and ROI. Cut costs and increased response rates by up

to 50%.

COMMUNICATE RELEVANT OFFERS

Source: DMA, Bronze Winner, Bank of Scotland, 2012

11

HALIFAX ‘NO BULL’: HOW TO LAUNCH A NEW

Source: DMA, Gold Winner, Halifax, 2010

Background:

Clarity was a new credit card with no charges.

The campaign needed to get Halifax branch staff fired up because there was no

commission to staff on the product.

Solution:

For staff - ‘live animal transport box’, with breathing holes (and bull’s eyes

peeping through), which contained Clive the Prize Bull (who didn’t charge).

There were 1,250 boxes in all, with Clarity information and a staff competition.

For prospects – mailed to over 500,000 people (260,000 warm, 250,000 cold).

Brochures and in-branch posters were developed with the same strong identity,

that looked Halifax but was distinct.

Results:

94,297 applications in just 8 weeks - a Halifax record. Since launch, results beat

every single target set. Over 59,000 cards were issued despite there being no TV

or billboard advertising. ROI for the campaign was at 4.2:1 at time of entry and

improving.

PRODUCT USING TARGETED AND CREATIVE MAIL

12

SPECIFIC ROLE FOR MAIL

13

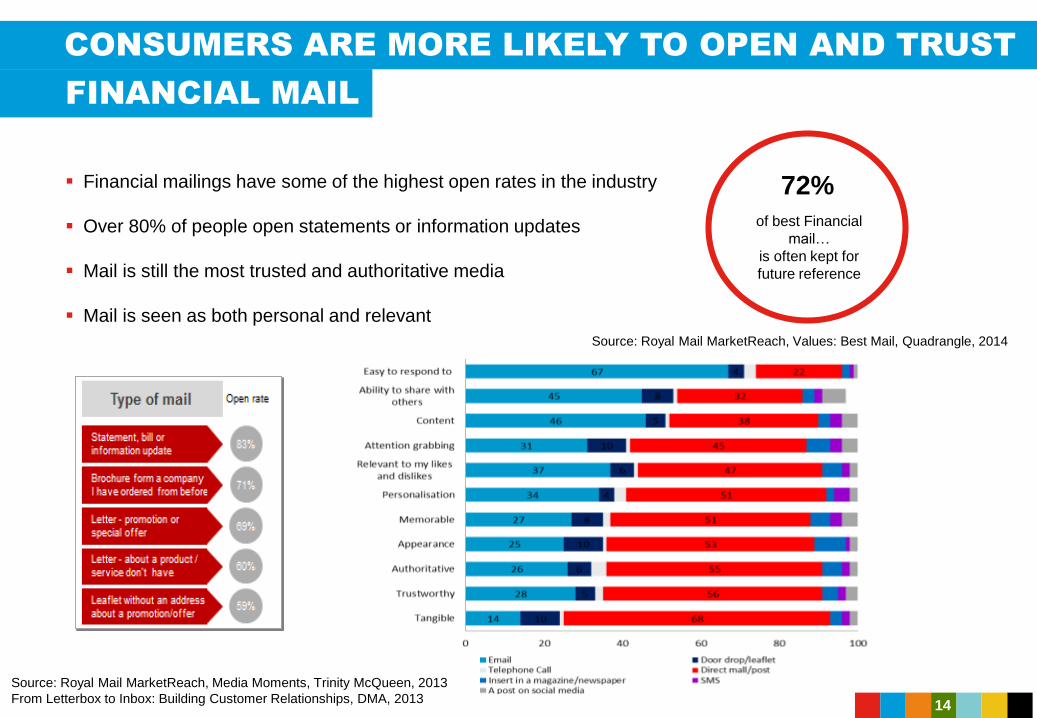

CONSUMERS ARE MORE LIKELY TO OPEN AND TRUST

Financial mailings have some of the highest open rates in the industry

Over 80% of people open statements or information updates

Mail is still the most trusted and authoritative media

Mail is seen as both personal and relevant

Source: Royal Mail MarketReach, Media Moments, Trinity McQueen, 2013

From Letterbox to Inbox: Building Customer Relationships, DMA, 2013

FINANCIAL MAIL

of best Financial

mail…

is often kept for

future reference

72%

14

Source: Royal Mail MarketReach, Values: Best Mail, Quadrangle, 2014

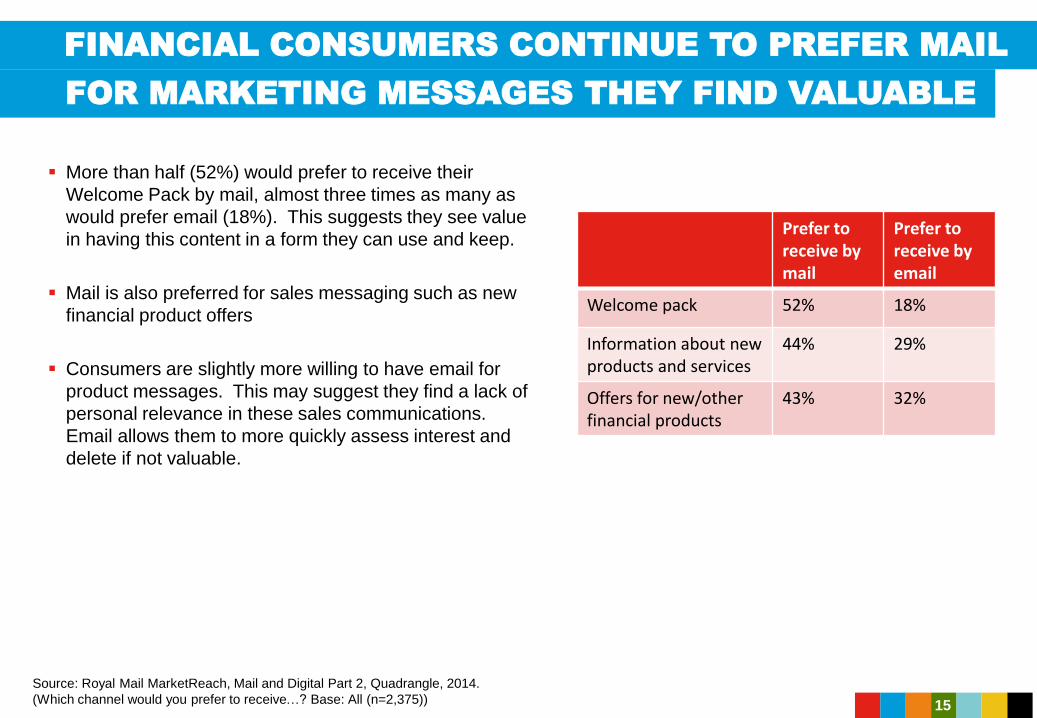

More than half (52%) would prefer to receive their

Welcome Pack by mail, almost three times as many as

would prefer email (18%). This suggests they see value

in having this content in a form they can use and keep.

Mail is also preferred for sales messaging such as new

financial product offers

Consumers are slightly more willing to have email for

product messages. This may suggest they find a lack of

personal relevance in these sales communications.

Email allows them to more quickly assess interest and

delete if not valuable.

FINANCIAL CONSUMERS CONTINUE TO PREFER MAIL

FOR MARKETING MESSAGES THEY FIND VALUABLE

Prefer to receive bymail

Prefer to receive byemail

Welcome pack 52% 18%

Information about new products and services

44% 29%

Offers for new/other financial products

43% 32%

Source: Royal Mail MarketReach, Mail and Digital Part 2, Quadrangle, 2014.

(Which channel would you prefer to receive…? Base: All (n=2,375)) 15

0%

10%

20%

30%

40%

50%

60%

70%

New CardActivation

New Pin Number

Annual Statements

Welcome Packs

Changing Ts & Cs

Monthly statement

Information aboutnew products and

services

Responding tocomplaints

Offers for otherfinancial products

Notifications e.g.account over the

limit

DM

Portal

Channel I would prefer to receive by message

SHOWED A CLEAR PREFERENCE FOR MAIL

THAT HAS CLEAR PERSONAL IMPORTANCE

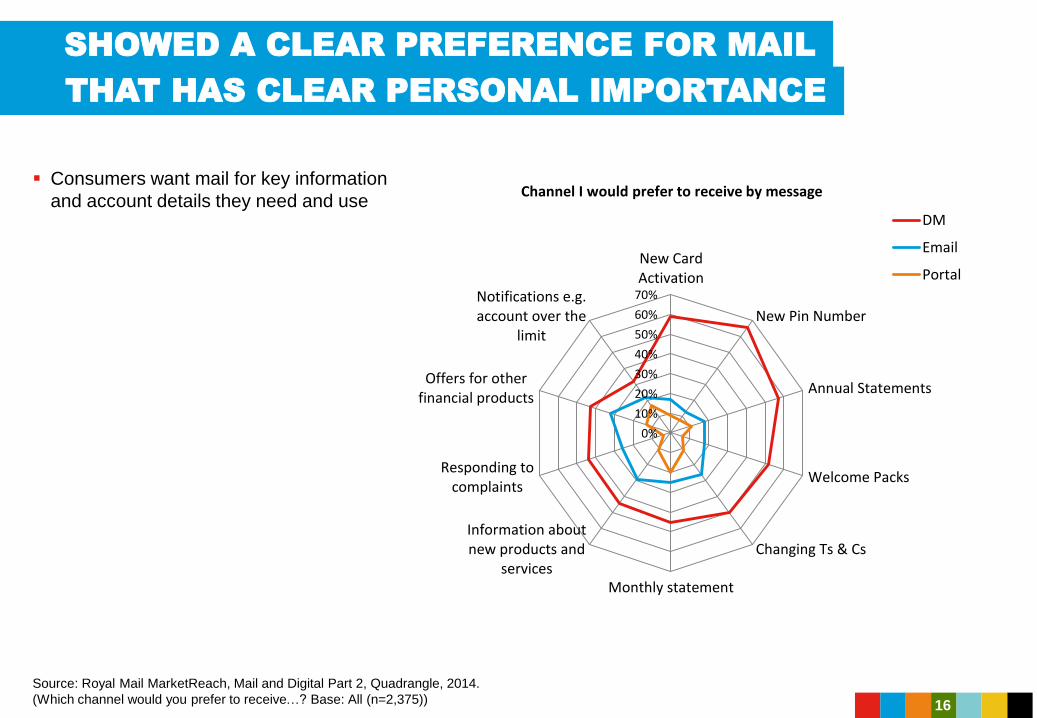

Consumers want mail for key information

and account details they need and use

16

Source: Royal Mail MarketReach, Mail and Digital Part 2, Quadrangle, 2014.

(Which channel would you prefer to receive…? Base: All (n=2,375))

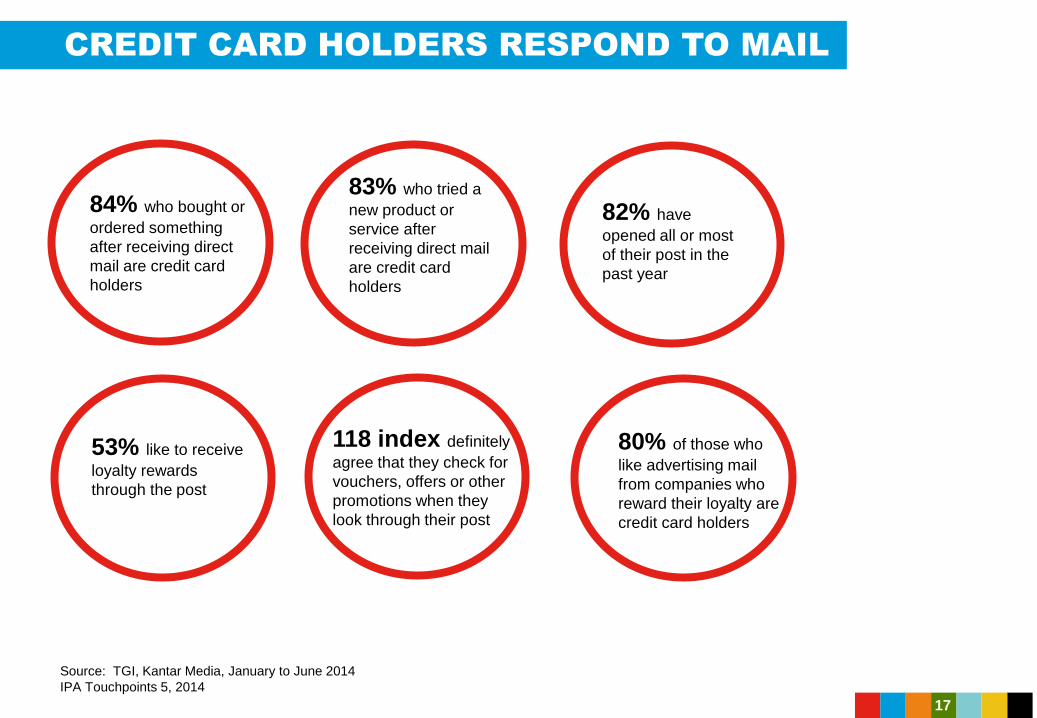

CREDIT CARD HOLDERS RESPOND TO MAIL

82% have

opened all or most

of their post in the

past year

118 index definitely

agree that they check for

vouchers, offers or other

promotions when they

look through their post

53% like to receive

loyalty rewards

through the post

83% who tried a

new product or

service after

receiving direct mail

are credit card

holders

84% who bought or

ordered something

after receiving direct

mail are credit card

holders

Source: TGI, Kantar Media, January to June 2014

IPA Touchpoints 5, 2014

80% of those who

like advertising mail

from companies who

reward their loyalty are

credit card holders

17

It’s been proven to be the most emotionally engaging media

People still enjoy receiving it

It has increasing standout in a digital world

It is highly valued by people

It is omnipresent in people houses

It helps uplift other channels and create value

NEW NEWS ABOUT MAIL

18

THE PRIVATE LIFE OF MAIL

MAIL IN THE HOME,

HEART AND HEAD

20

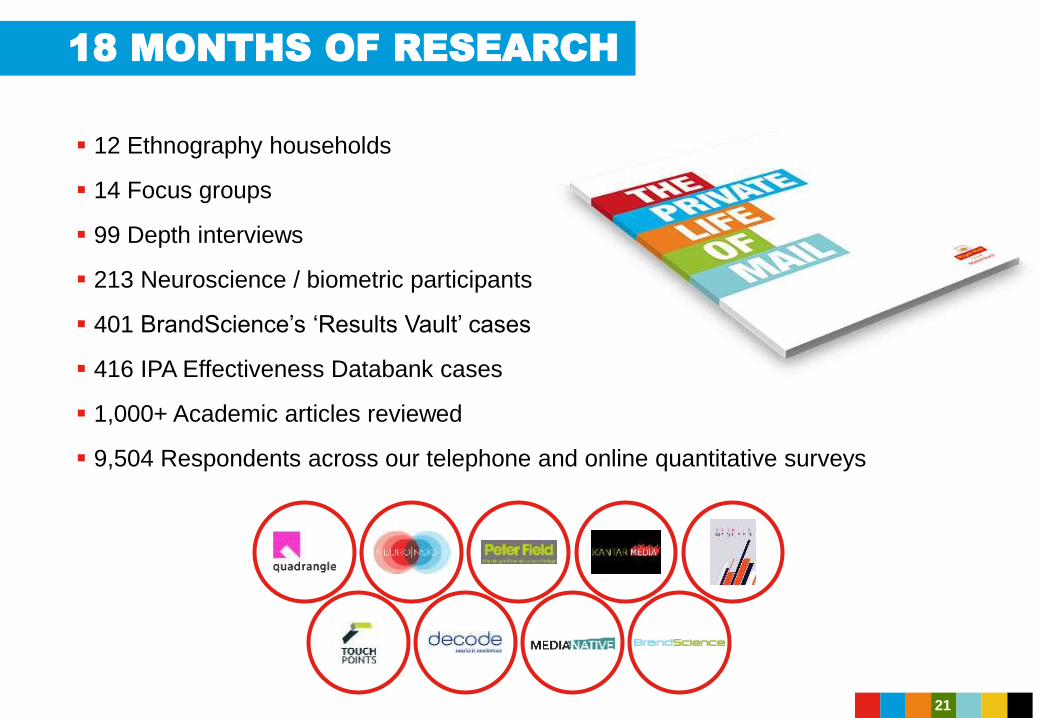

12 Ethnography households

14 Focus groups

99 Depth interviews

213 Neuroscience / biometric participants

401 BrandScience’s ‘Results Vault’ cases

416 IPA Effectiveness Databank cases

1,000+ Academic articles reviewed

9,504 Respondents across our telephone and online quantitative surveys

18 MONTHS OF RESEARCH

21

DEVELOPED IN 8 STRANDS

Ethnography

Post ethnography survey

Multisensory Communications: review of academic literature

Tactility

Values: Best Mail

Mail and Digital 1 & 2

Neuroscience

ROI/Effectiveness metrics

22

MAIL IN THE HOME

LIFE BEYOND THE LETTERBOX

23

24

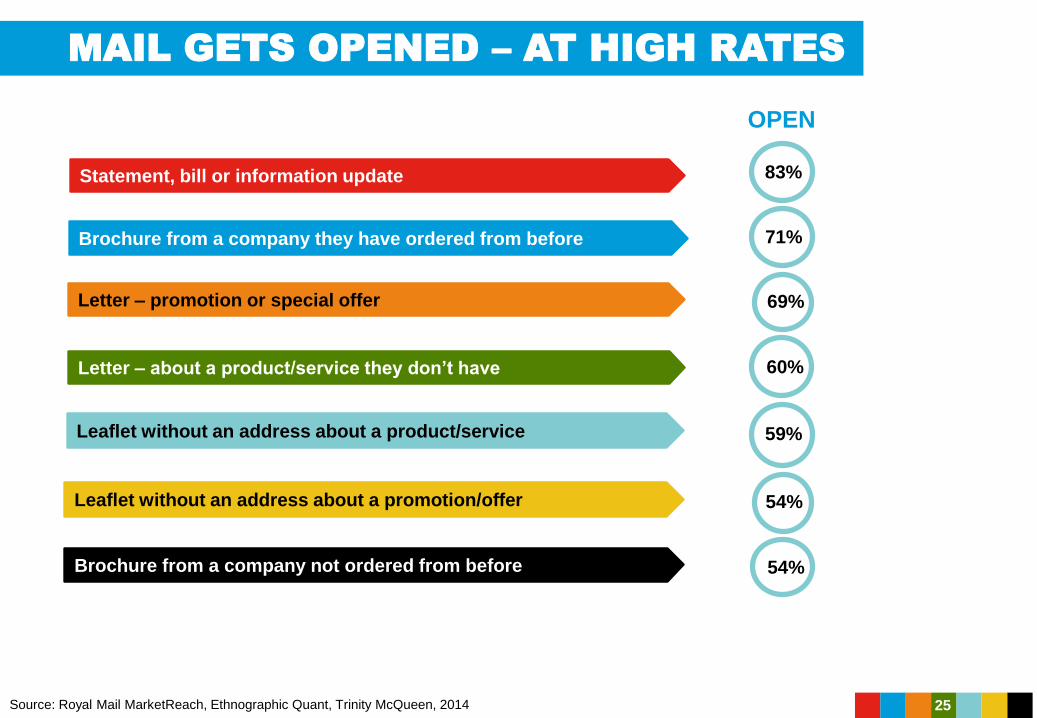

MAIL GETS OPENED – AT HIGH RATES

Statement, bill or information update

Brochure from a company they have ordered from before

Letter – promotion or special offer

Letter – about a product/service they don’t have

Leaflet without an address about a product/service

Leaflet without an address about a promotion/offer

Brochure from a company not ordered from before

83%

71%

69%

60%

59%

54%

54%

OPEN

Source: Royal Mail MarketReach, Ethnographic Quant, Trinity McQueen, 2014 25

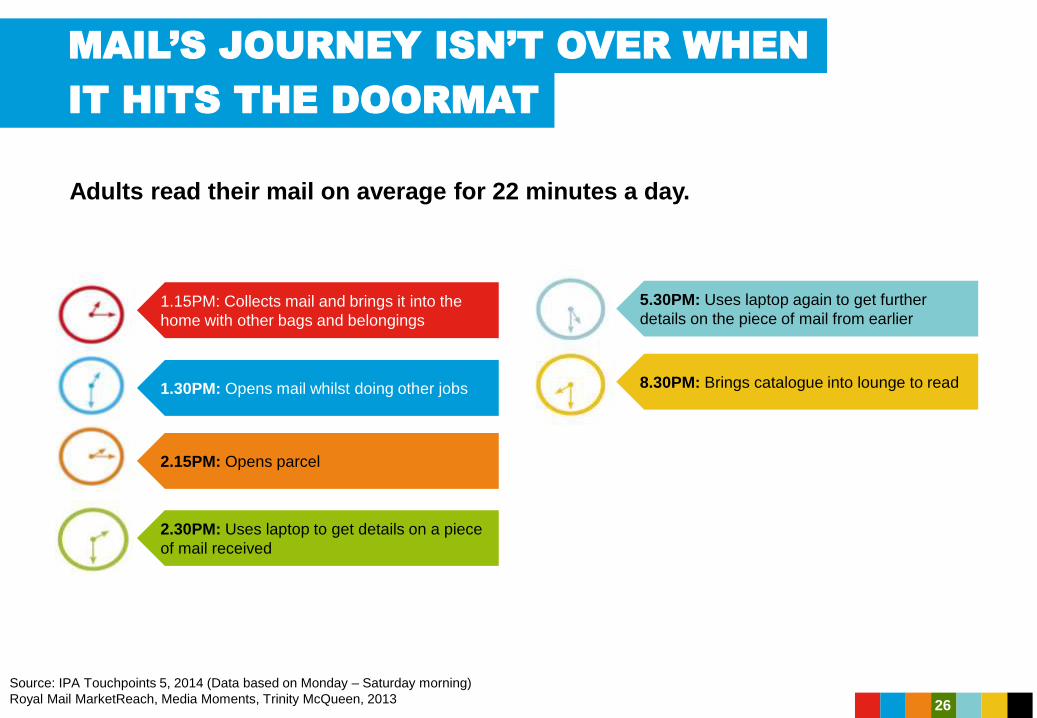

MAIL’S JOURNEY ISN’T OVER WHEN

Adults read their mail on average for 22 minutes a day.

IT HITS THE DOORMAT

1.15PM: Collects mail and brings it into the

home with other bags and belongings

1.30PM: Opens mail whilst doing other jobs

2.15PM: Opens parcel

2.30PM: Uses laptop to get details on a piece

of mail received

5.30PM: Uses laptop again to get further

details on the piece of mail from earlier

8.30PM: Brings catalogue into lounge to read

26

Source: IPA Touchpoints 5, 2014 (Data based on Monday – Saturday morning)

Royal Mail MarketReach, Media Moments, Trinity McQueen, 2013

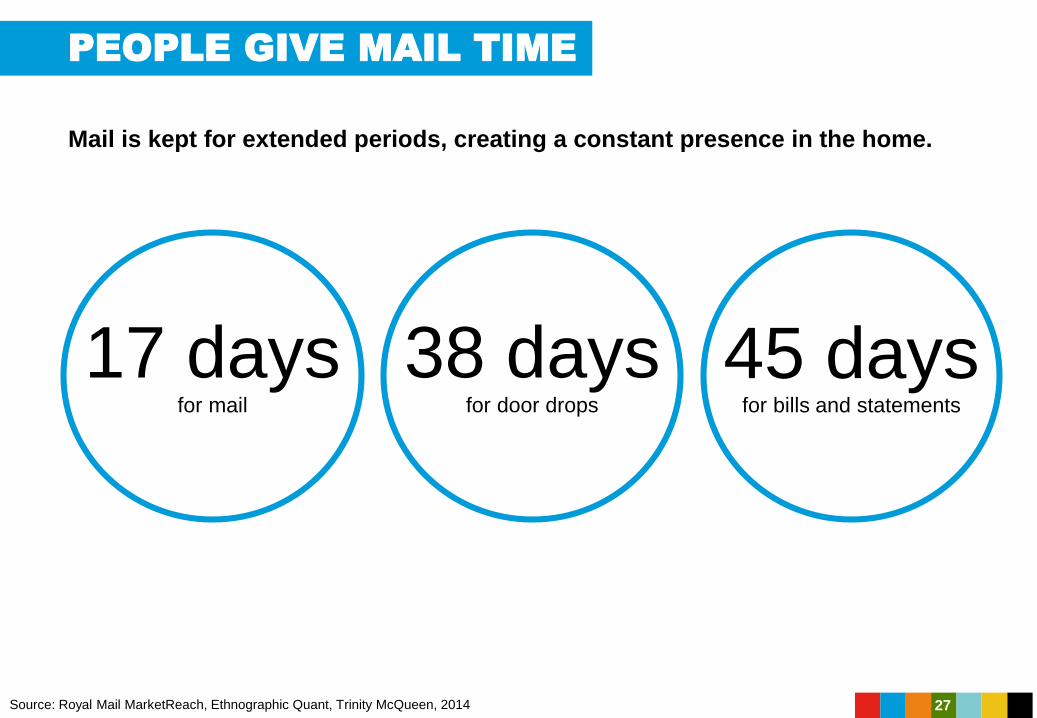

PEOPLE GIVE MAIL TIME

Mail is kept for extended periods, creating a constant presence in the home.

17 daysfor mail

38 daysfor door drops

45 daysfor bills and statements

Source: Royal Mail MarketReach, Ethnographic Quant, Trinity McQueen, 2014 27

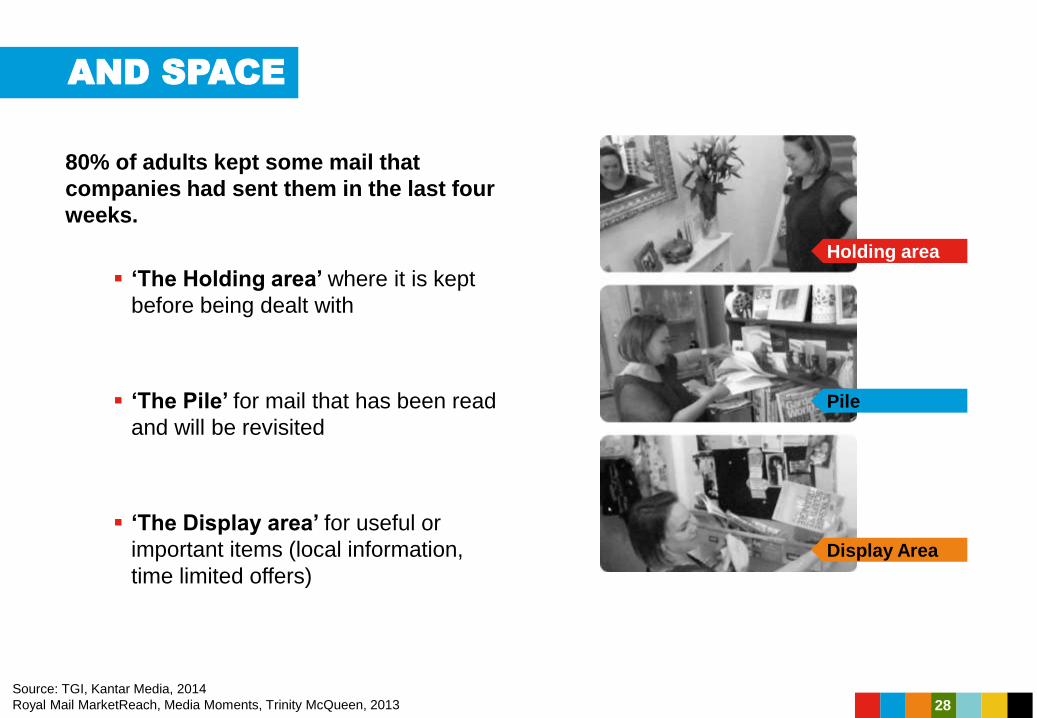

AND SPACE

80% of adults kept some mail that

companies had sent them in the last four

weeks.

‘The Holding area’ where it is kept

before being dealt with

‘The Pile’ for mail that has been read

and will be revisited

‘The Display area’ for useful or

important items (local information,

time limited offers)

Display Area

Pile

Holding area

28Source: TGI, Kantar Media, 2014

Royal Mail MarketReach, Media Moments, Trinity McQueen, 2013

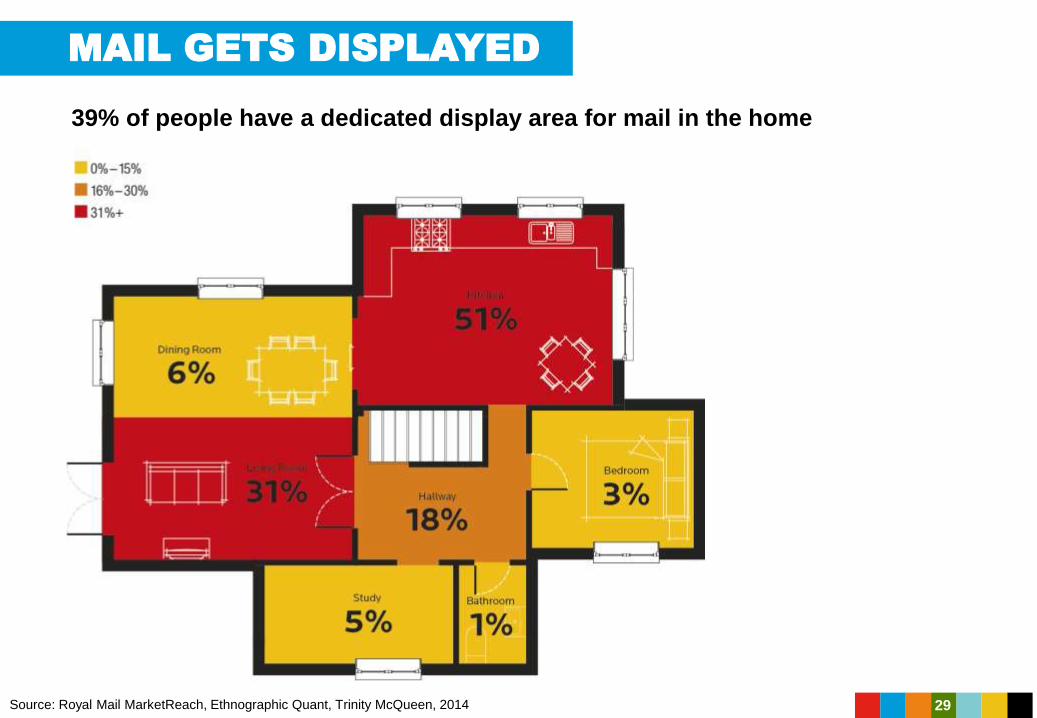

MAIL GETS DISPLAYED

39% of people have a dedicated display area for mail in the home

Source: Royal Mail MarketReach, Ethnographic Quant, Trinity McQueen, 2014 29

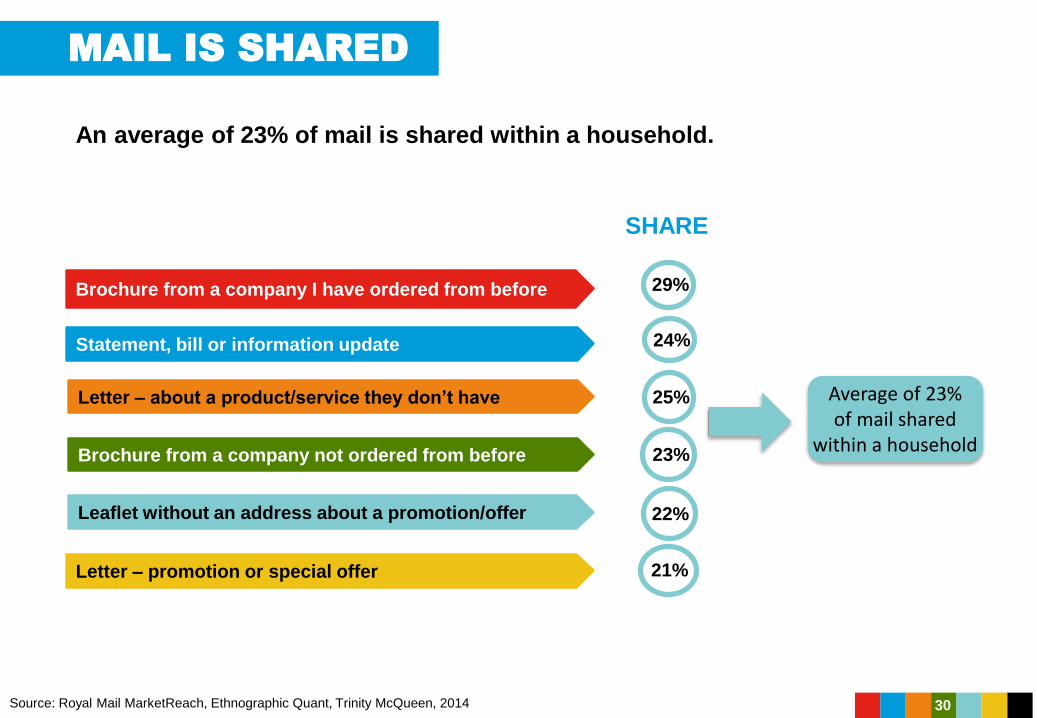

MAIL IS SHARED

An average of 23% of mail is shared within a household.

Brochure from a company I have ordered from before

Statement, bill or information update

Letter – about a product/service they don’t have

Brochure from a company not ordered from before

Leaflet without an address about a promotion/offer

Letter – promotion or special offer

29%

24%

25%

23%

22%

21%

SHARE

Average of 23% of mail shared

within a household

Source: Royal Mail MarketReach, Ethnographic Quant, Trinity McQueen, 2014 30

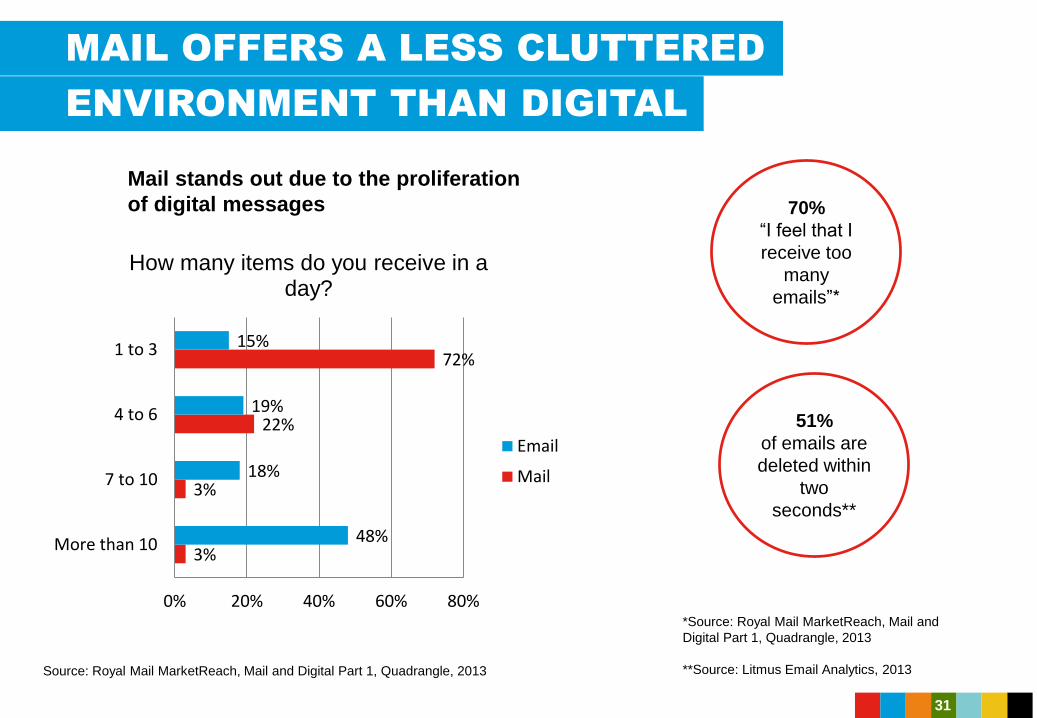

MAIL OFFERS A LESS CLUTTERED

ENVIRONMENT THAN DIGITAL

70%

“I feel that I

receive too

many

emails”*

Mail stands out due to the proliferation

of digital messages

3%

3%

22%

72%

48%

18%

19%

15%

0% 20% 40% 60% 80%

More than 10

7 to 10

4 to 6

1 to 3

How many items do you receive in a day?

51%

of emails are

deleted within

two

seconds**

31

Source: Royal Mail MarketReach, Mail and Digital Part 1, Quadrangle, 2013

*Source: Royal Mail MarketReach, Mail and

Digital Part 1, Quadrangle, 2013

**Source: Litmus Email Analytics, 2013

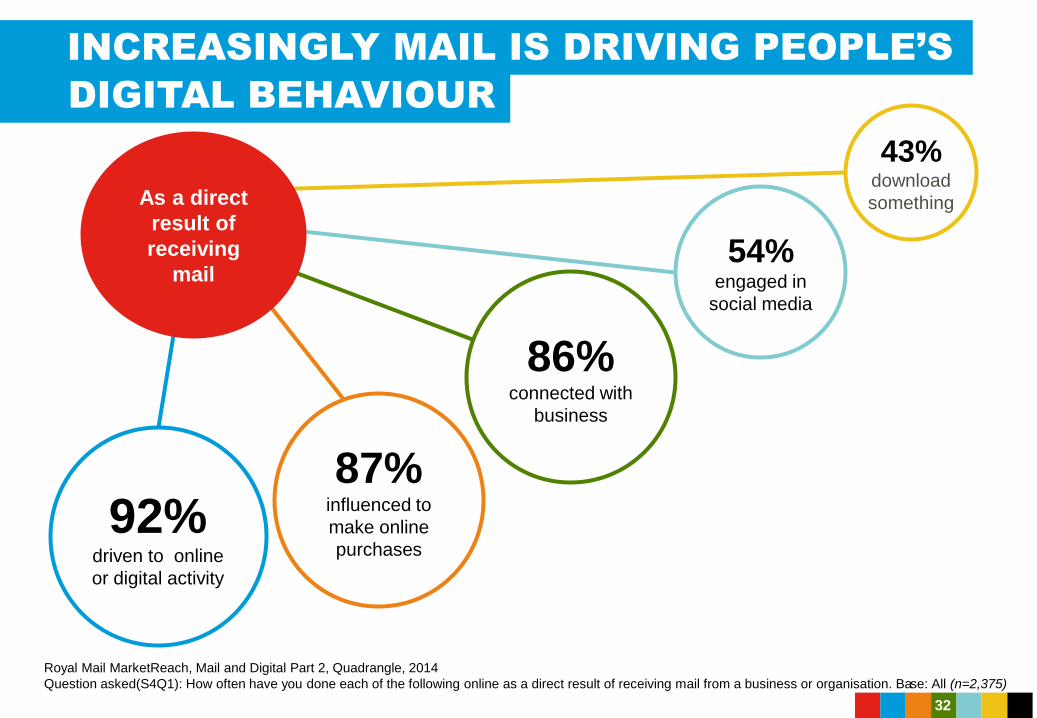

INCREASINGLY MAIL IS DRIVING PEOPLE’S

43%download

something

54%engaged in

social media

87%influenced to

make online

purchases

92%driven to online

or digital activity

86%connected with

business

DIGITAL BEHAVIOUR

As a direct

result of

receiving

32

Royal Mail MarketReach, Mail and Digital Part 2, Quadrangle, 2014

Question asked(S4Q1): How often have you done each of the following online as a direct result of receiving mail from a business or organisation. Base: All (n=2,375)

MAIL IN THE HEART

CREATING AN EMOTIONAL

RESPONSE

33

34

35

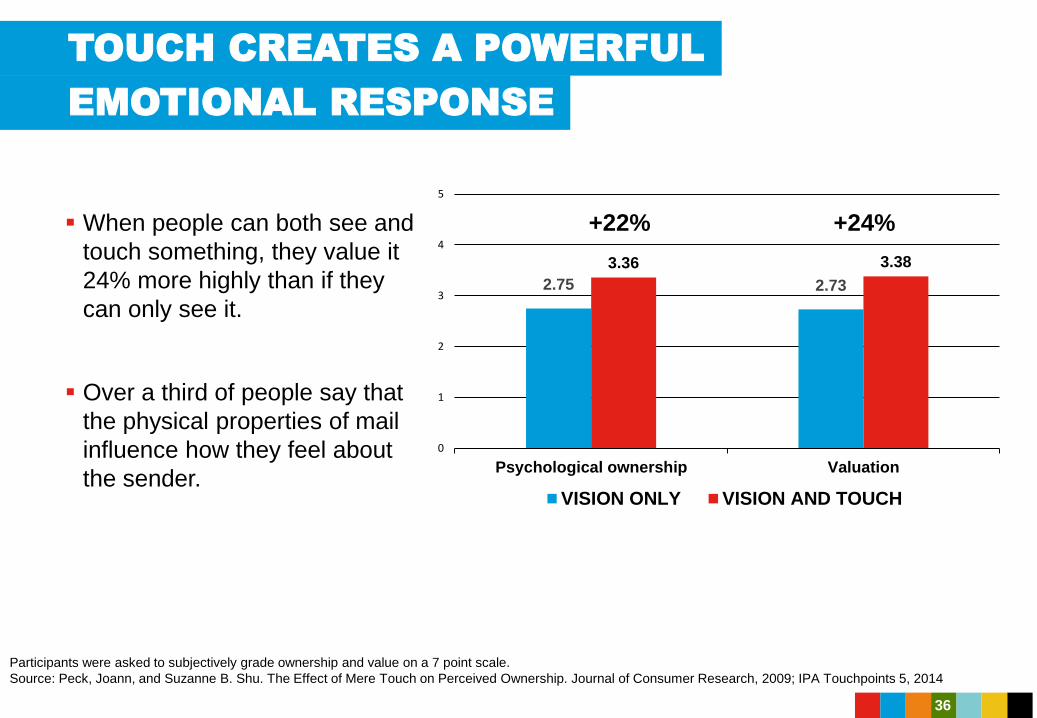

TOUCH CREATES A POWERFUL

When people can both see and

touch something, they value it

24% more highly than if they

can only see it.

Over a third of people say that

the physical properties of mail

influence how they feel about

the sender.

EMOTIONAL RESPONSE

+22% +24%

2.75 2.73

3.36 3.38

0

1

2

3

4

5

Psychological ownership Valuation

VISION ONLY VISION AND TOUCH

36

Participants were asked to subjectively grade ownership and value on a 7 point scale.

Source: Peck, Joann, and Suzanne B. Shu. The Effect of Mere Touch on Perceived Ownership. Journal of Consumer Research, 2009; IPA Touchpoints 5, 2014

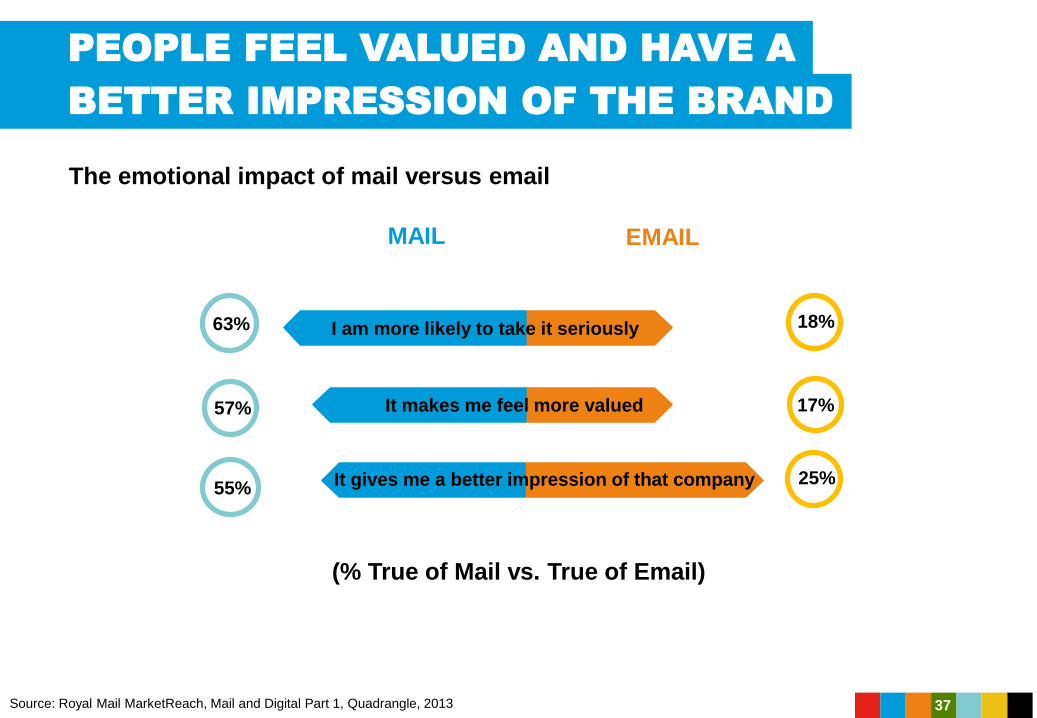

PEOPLE FEEL VALUED AND HAVE A

BETTER IMPRESSION OF THE BRAND

The emotional impact of mail versus email

I am more likely to take it seriously

It gives me a better impression of that company

It makes me feel more valued

63%

57%

55%

18%

17%

25%

(% True of Mail vs. True of Email)

MAIL EMAIL

Source: Royal Mail MarketReach, Mail and Digital Part 1, Quadrangle, 2013 37

MAIL IN THE HEAD

HOW MAIL IMPACTS THE BRAIN

38

39

40

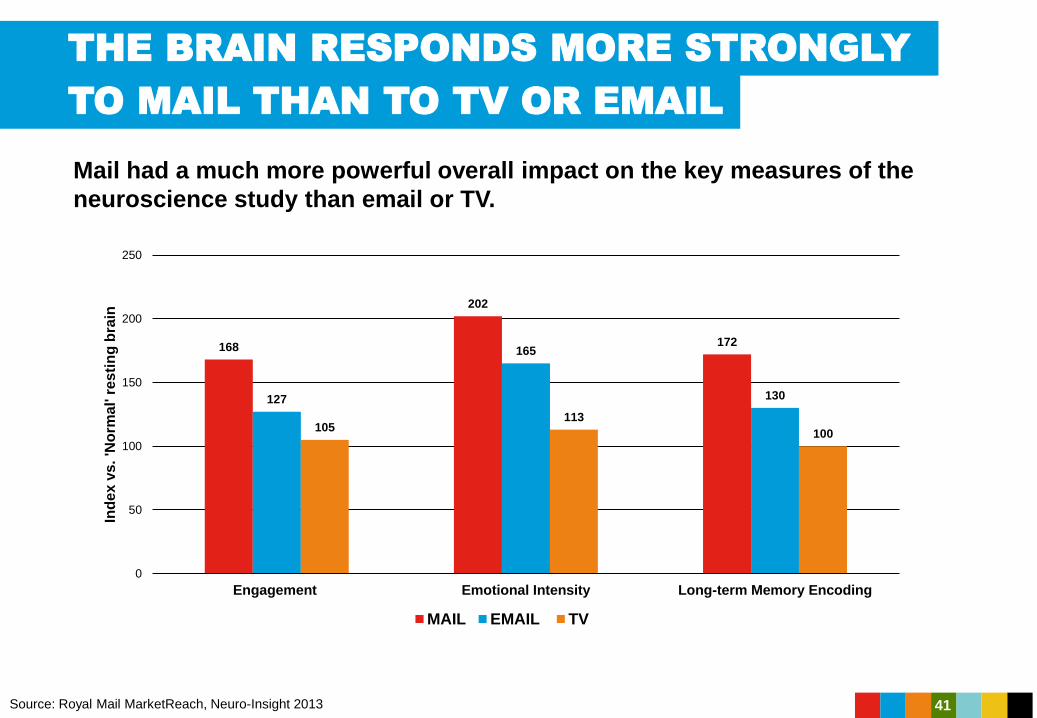

THE BRAIN RESPONDS MORE STRONGLY

Mail had a much more powerful overall impact on the key measures of the

neuroscience study than email or TV.

TO MAIL THAN TO TV OR EMAIL

Source: Royal Mail MarketReach, Neuro-Insight 2013

168

202

172

127

165

130

105113

100

0

50

100

150

200

250

Engagement Emotional Intensity Long-term Memory Encoding

Ind

ex v

s.

'No

rma

l' r

es

tin

g b

rain

MAIL EMAIL TV

41

IN A MULTI MEDIA CAMPAIGN

SEQUENCING MAIL LAST MAXIMISES IMPACT

Source: Royal Mail MarketReach, Neuro-Insight, 2013

Mail after TV and email

100 100 100

112

101

106

126

121

110

80

90

100

110

120

130

140

Engagment Emotional Intensity Long-term MemoryEncoding

Ind

ex v

s.

resp

on

se

fro

m first e

xp

osu

re

MAIL SEEN FIRST MAIL SEEN SECOND MAIL SEEN THIRD

Engagement

42

MAIL IN THE WALLET

HOW MAIL MAKES MONEY

43

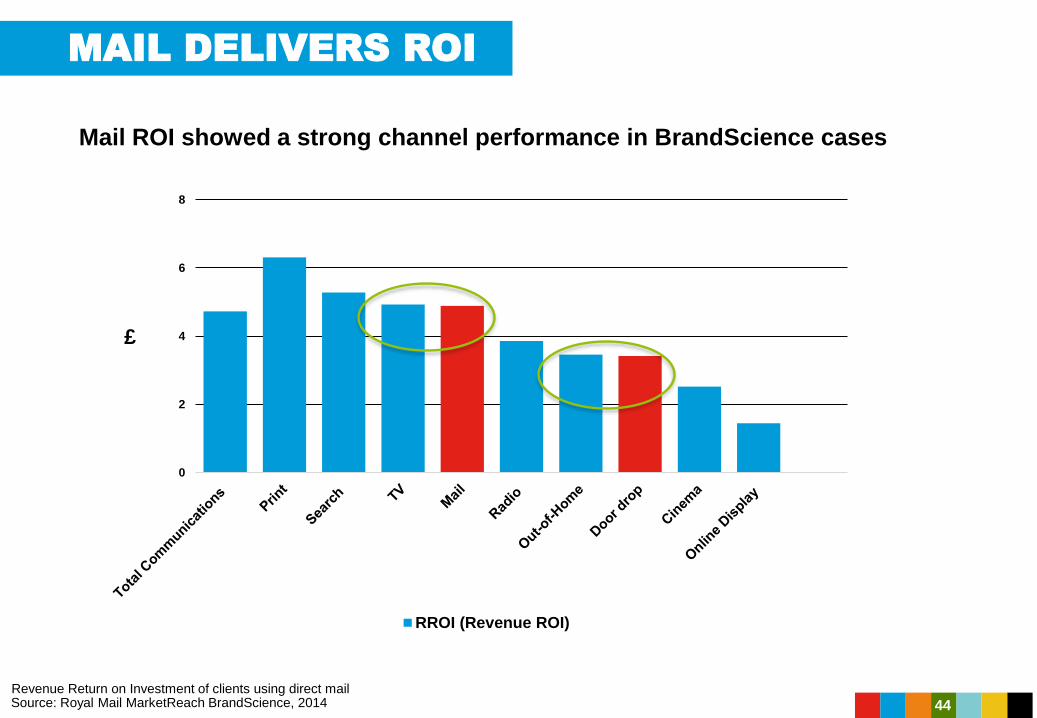

MAIL DELIVERS ROI

Mail ROI showed a strong channel performance in BrandScience cases

Revenue Return on Investment of clients using direct mailSource: Royal Mail MarketReach BrandScience, 2014

0

2

4

6

8

£

RROI (Revenue ROI)

44

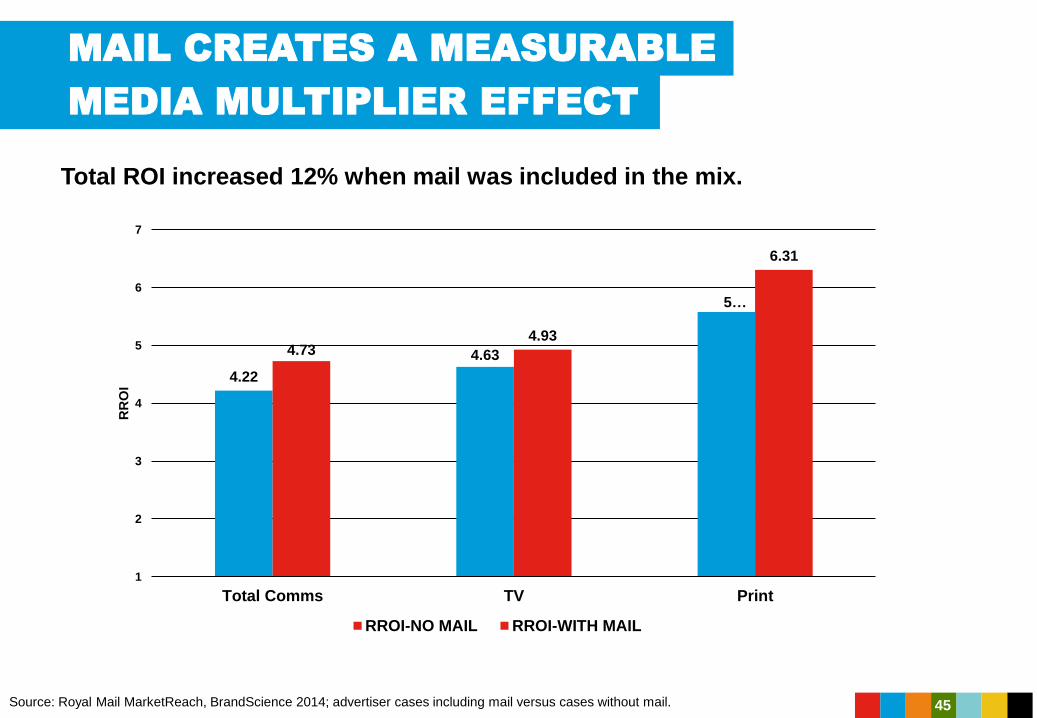

Total ROI increased 12% when mail was included in the mix.

MEDIA MULTIPLIER EFFECT

MAIL CREATES A MEASURABLE

Source: Royal Mail MarketReach, BrandScience 2014; advertiser cases including mail versus cases without mail.

4.22

4.63

5…

4.734.93

6.31

1

2

3

4

5

6

7

Total Comms TV Print

RR

OI

RROI-NO MAIL RROI-WITH MAIL

45

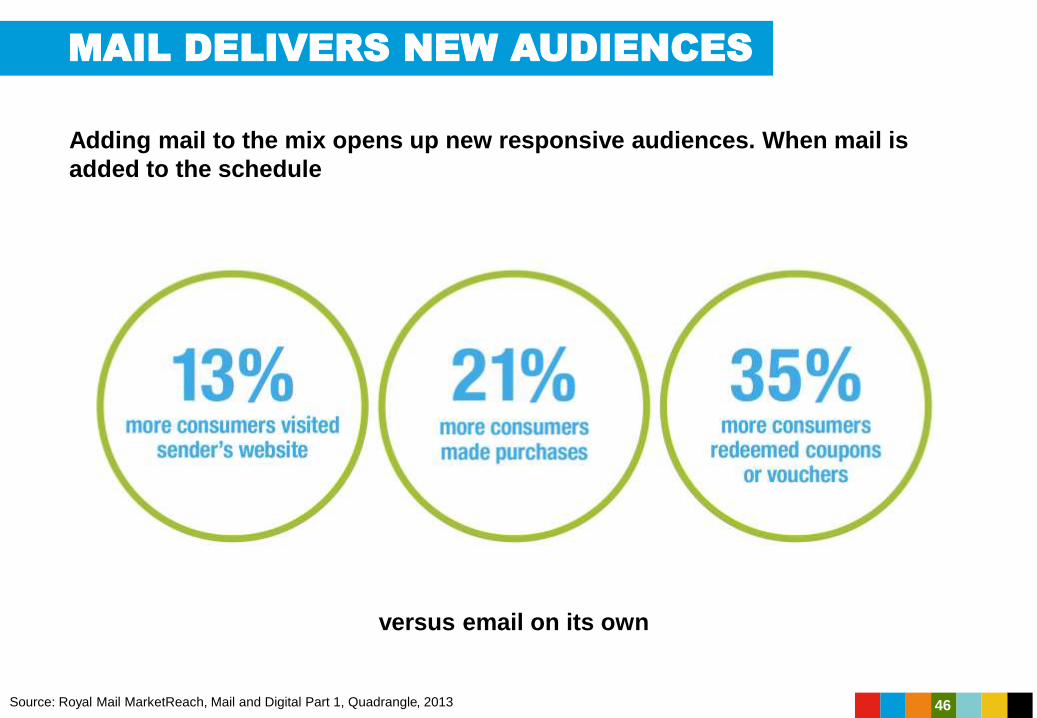

MAIL DELIVERS NEW AUDIENCES

Adding mail to the mix opens up new responsive audiences. When mail is

added to the schedule

versus email on its own

Source: Royal Mail MarketReach, Mail and Digital Part 1, Quadrangle, 2013 46

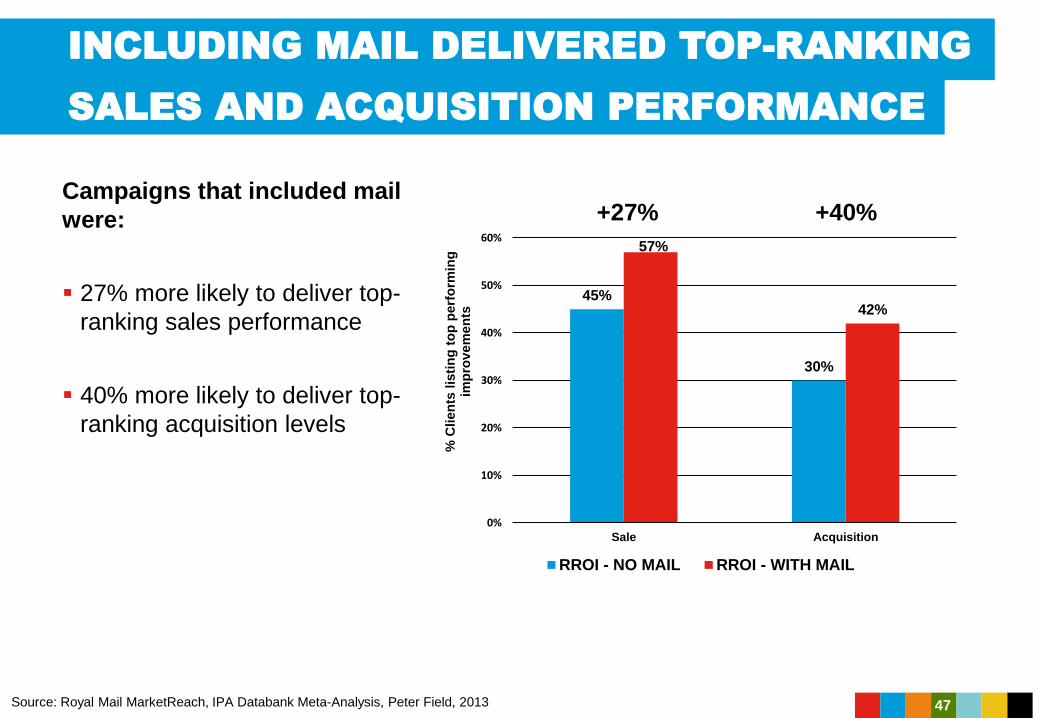

INCLUDING MAIL DELIVERED TOP-RANKING

Campaigns that included mail

were:

27% more likely to deliver top-

ranking sales performance

40% more likely to deliver top-

ranking acquisition levels

SALES AND ACQUISITION PERFORMANCE

Source: Royal Mail MarketReach, IPA Databank Meta-Analysis, Peter Field, 2013

+27% +40%

45%

30%

57%

42%

0%

10%

20%

30%

40%

50%

60%

Sale Acquisition

% C

lien

ts l

isti

ng

to

p p

erf

orm

ing

im

pro

vem

en

ts

RROI - NO MAIL RROI - WITH MAIL

47

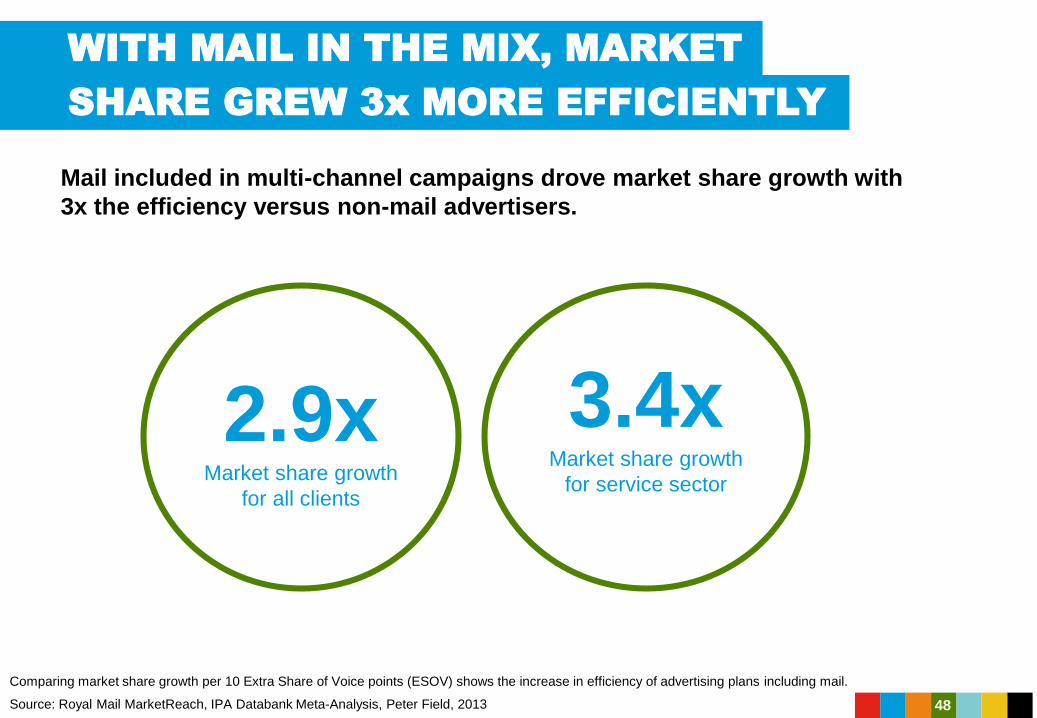

WITH MAIL IN THE MIX, MARKET

SHARE GREW 3x MORE EFFICIENTLY

Mail included in multi-channel campaigns drove market share growth with

3x the efficiency versus non-mail advertisers.

2.9xMarket share growth

for all clients

3.4x Market share growth

for service sector

48

Comparing market share growth per 10 Extra Share of Voice points (ESOV) shows the increase in efficiency of advertising plans including mail.

Source: Royal Mail MarketReach, IPA Databank Meta-Analysis, Peter Field, 2013

MAIL IN ACTION

EDF

49

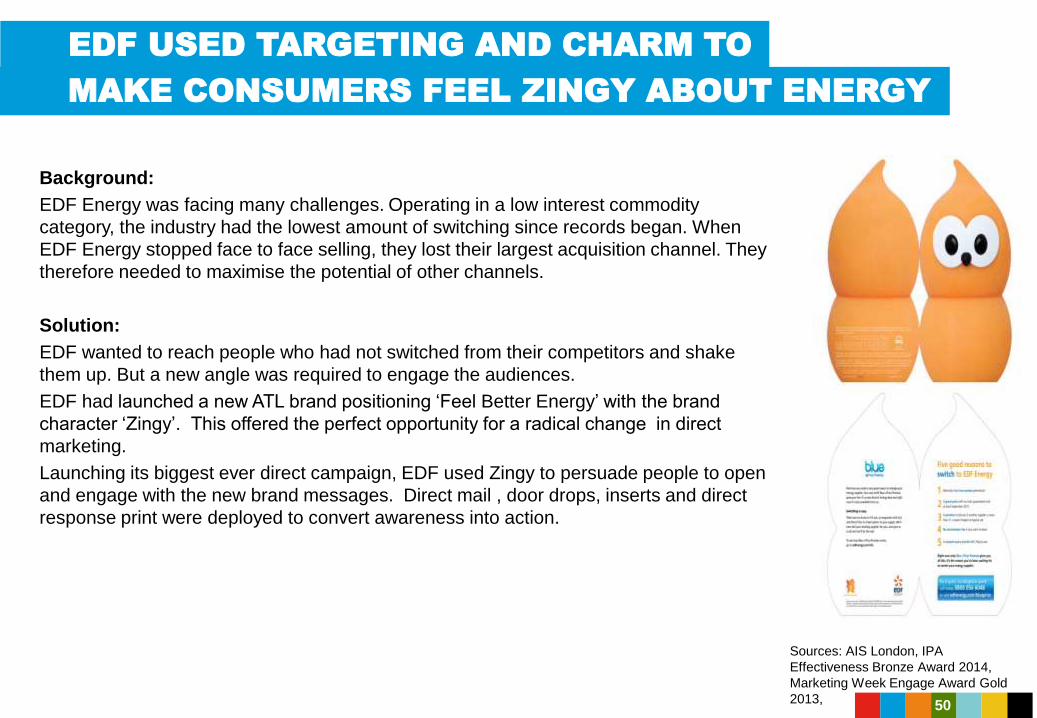

EDF USED TARGETING AND CHARM TO

MAKE CONSUMERS FEEL ZINGY ABOUT ENERGY

Background:

EDF Energy was facing many challenges. Operating in a low interest commodity

category, the industry had the lowest amount of switching since records began. When

EDF Energy stopped face to face selling, they lost their largest acquisition channel. They

therefore needed to maximise the potential of other channels.

Solution:

EDF wanted to reach people who had not switched from their competitors and shake

them up. But a new angle was required to engage the audiences.

EDF had launched a new ATL brand positioning ‘Feel Better Energy’ with the brand

character ‘Zingy’. This offered the perfect opportunity for a radical change in direct

marketing.

Launching its biggest ever direct campaign, EDF used Zingy to persuade people to open

and engage with the new brand messages. Direct mail , door drops, inserts and direct

response print were deployed to convert awareness into action.

Sources: AIS London, IPA

Effectiveness Bronze Award 2014,

Marketing Week Engage Award Gold

2013, 50

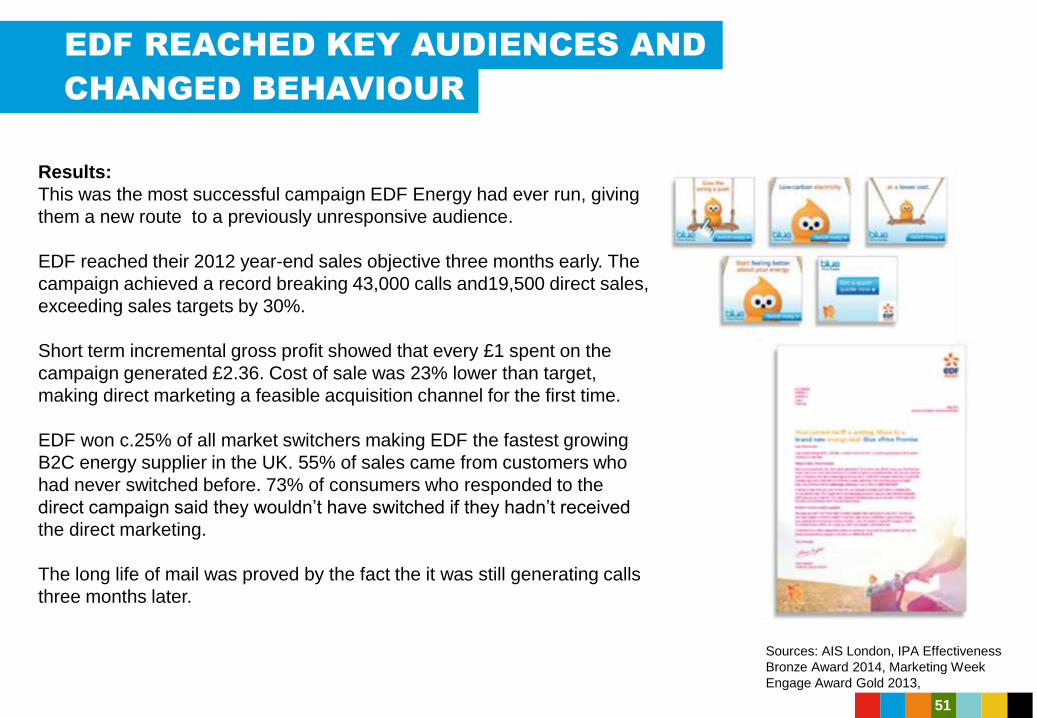

EDF REACHED KEY AUDIENCES AND

Results:

This was the most successful campaign EDF Energy had ever run, giving

them a new route to a previously unresponsive audience.

EDF reached their 2012 year-end sales objective three months early. The

campaign achieved a record breaking 43,000 calls and19,500 direct sales,

exceeding sales targets by 30%.

Short term incremental gross profit showed that every £1 spent on the

campaign generated £2.36. Cost of sale was 23% lower than target,

making direct marketing a feasible acquisition channel for the first time.

EDF won c.25% of all market switchers making EDF the fastest growing

B2C energy supplier in the UK. 55% of sales came from customers who

had never switched before. 73% of consumers who responded to the

direct campaign said they wouldn’t have switched if they hadn’t received

the direct marketing.

The long life of mail was proved by the fact the it was still generating calls

three months later.

CHANGED BEHAVIOUR

Sources: AIS London, IPA Effectiveness

Bronze Award 2014, Marketing Week

Engage Award Gold 2013,

51

MAIL IN ACTION

HOMEBASE

52

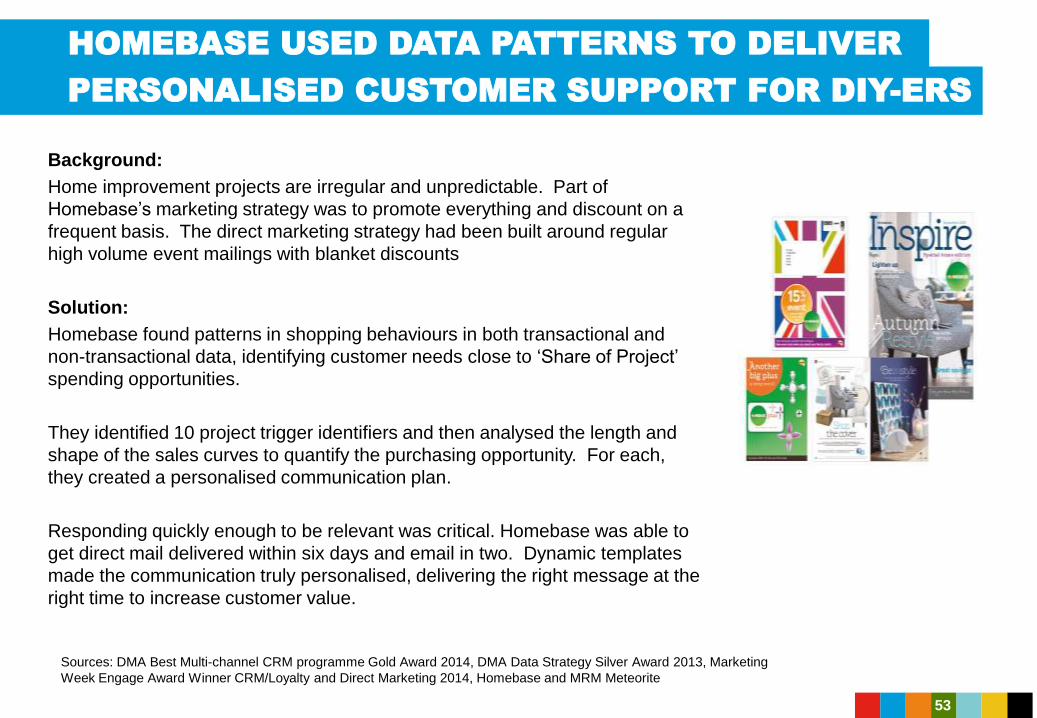

Background:

Home improvement projects are irregular and unpredictable. Part of

Homebase’s marketing strategy was to promote everything and discount on a

frequent basis. The direct marketing strategy had been built around regular

high volume event mailings with blanket discounts

Solution:

Homebase found patterns in shopping behaviours in both transactional and

non-transactional data, identifying customer needs close to ‘Share of Project’

spending opportunities.

They identified 10 project trigger identifiers and then analysed the length and

shape of the sales curves to quantify the purchasing opportunity. For each,

they created a personalised communication plan.

Responding quickly enough to be relevant was critical. Homebase was able to

get direct mail delivered within six days and email in two. Dynamic templates

made the communication truly personalised, delivering the right message at the

right time to increase customer value.

HOMEBASE USED DATA PATTERNS TO DELIVER

Sources: DMA Best Multi-channel CRM programme Gold Award 2014, DMA Data Strategy Silver Award 2013, Marketing

Week Engage Award Winner CRM/Loyalty and Direct Marketing 2014, Homebase and MRM Meteorite

PERSONALISED CUSTOMER SUPPORT FOR DIY-ERS

53

Solution:

The programme used highly responsive direct mail, magazines, emails, at till

communications and inspiring shareable content to increase customer value,

using a hierarchy to determine customer inclusion to suit their interest or

project.

Results:

The strategy has been transformational. The evolved CRM programme has

delivered incremental sales four times greater than three years ago - ROI up

350% to 4.3:1. It also smashed its profit target by +48% creating a

demonstrably more engaged and valuable customer in terms of both total

spend and activity – mail response increased from an average of 9% to a

maximum of 46%, up 500%, ATV increased by 13.5% and repeat visits up 6%.

TARGETING AND PERSONALISATION COMBINED

Sources: DMA Best Multi-channel CRM programme Gold Award 2014, DMA Data Strategy Silver Award 2013, Marketing

Week Engage Award Winner CRM/Loyalty and Direct Marketing 2014, Homebase and MRM Meteorite

WITH FAST REPONSE DELIVERED DRAMATIC GROWTH

54

IN SUMMARY

Mail brings a brand into the home where it is kept, displayed, and/or shared

Its tactile qualities have powerful emotional and rational impact that can be identified

and proven

Mail makes your message more memorable

Mail drives successful return on investment

When used in integrated campaigns, it can provide a measurable media multiplier effect

Mail delivers top-ranking sales and acquisition growth and efficient market share growth

The newly transformed Royal Mail is a credible, motivated and connected partner to you and your

marketing agencies.

Media and Data

Planning

Bespoke Research

and Insight

Data Provision

Distribution

55

56

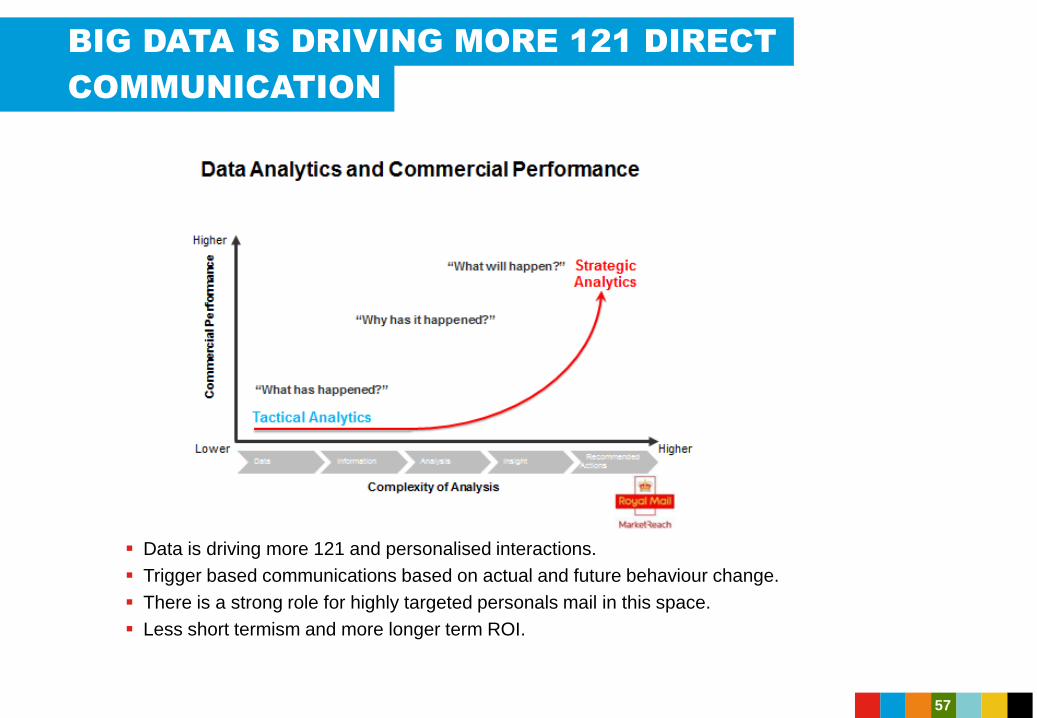

BIG DATA IS DRIVING MORE 121 DIRECT

Data is driving more 121 and personalised interactions.

Trigger based communications based on actual and future behaviour change.

There is a strong role for highly targeted personals mail in this space.

Less short termism and more longer term ROI.

COMMUNICATION

57

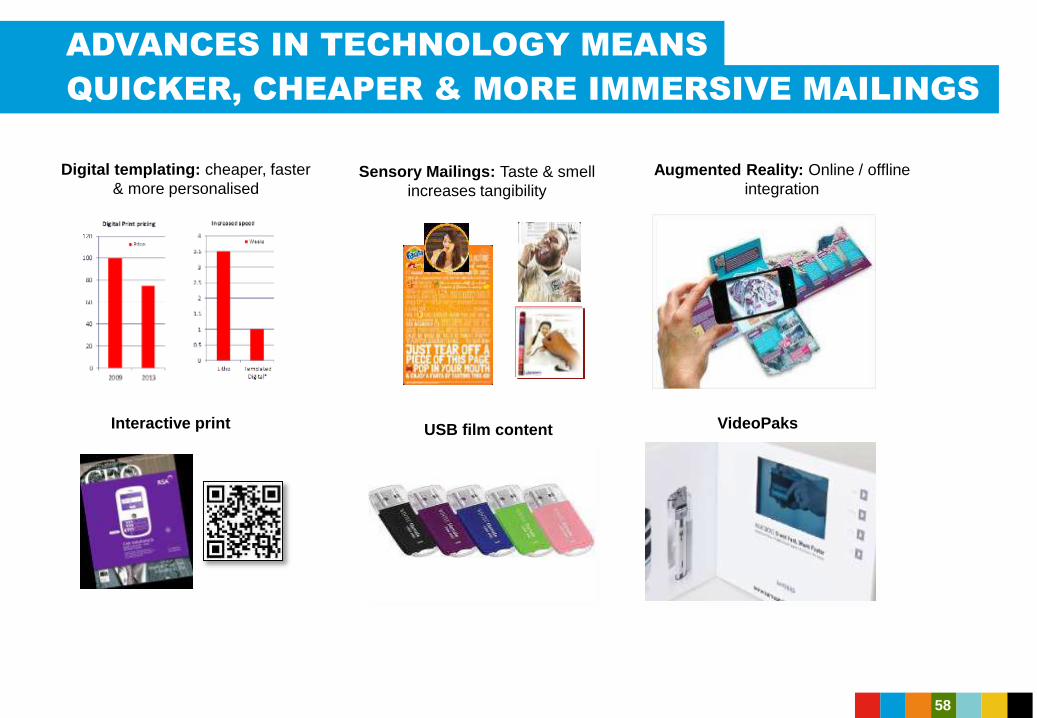

ADVANCES IN TECHNOLOGY MEANS

USB film content

Augmented Reality: Online / offline

integration

VideoPaks

Sensory Mailings: Taste & smell

increases tangibility

Interactive print

Digital templating: cheaper, faster

& more personalised

QUICKER, CHEAPER & MORE IMMERSIVE MAILINGS

58

NEW DEVELOPMENTS FOR MAIL

Barcode

A new barcode standard for machine readable Business, Advertising and Publishing Mail

Technology

Sorting machines that read the new barcode and collect mail data

Reporting

Mail Analytics that reports on volume, compliance, predicted delivery and overall performance

Ultimately generating more efficiency, greater transparency and

measurement for your mail campaigns

59

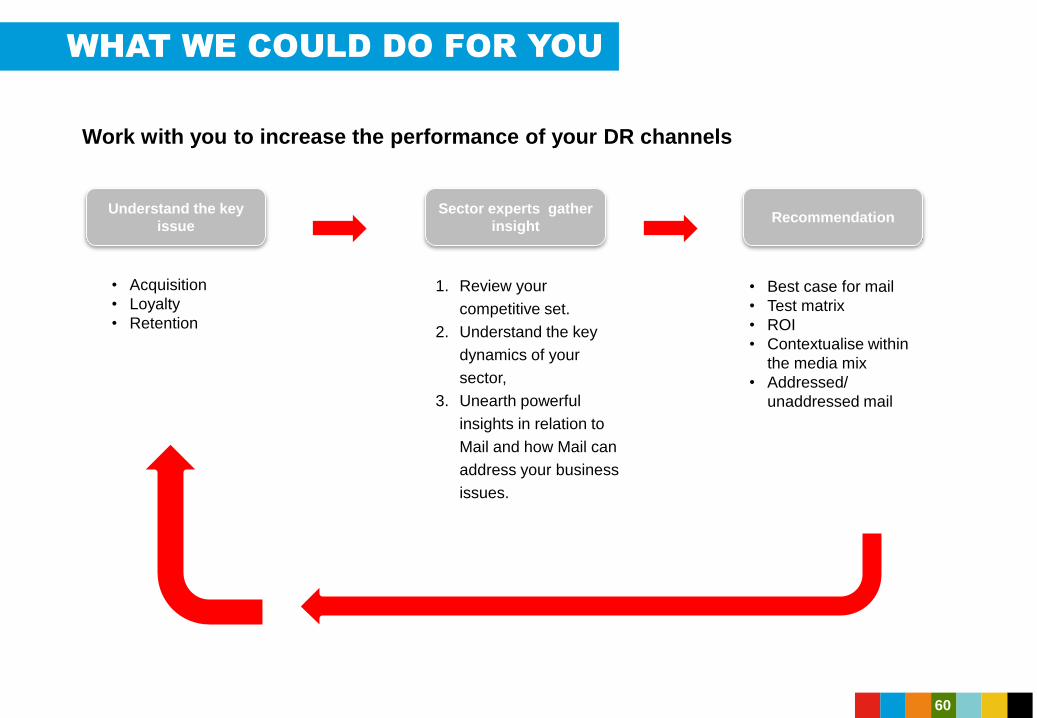

WHAT WE COULD DO FOR YOU

Work with you to increase the performance of your DR channels

• Best case for mail

• Test matrix

• ROI

• Contextualise within

the media mix

• Addressed/

unaddressed mail

1. Review your

competitive set.

2. Understand the key

dynamics of your

sector,

3. Unearth powerful

insights in relation to

Mail and how Mail can

address your business

issues.

• Acquisition

• Loyalty

• Retention

Understand the key

issue

Sector experts gather

insight Recommendation

60

Royal Mail, the cruciform and all marks indicated with ® are registered trade marks of Royal Mail Group Ltd.

Royal Mail Group Ltd 2014. Registered Office: 100 Victoria Embankment, London EC4Y 0HQ.© Royal Mail Group Ltd 2014. All rights reserved.

THANK YOU

61