credit rating agencies in india

TRANSCRIPT

CREDIT RATING AGENCIES IN INDIA

CRISIL

TYPES OF RATINGS

Credit Ratings

A CRISIL rating reflects CRISIL's current opinion on the relative likelihood of timely payment of interest and principal on the rated obligation. It is an unbiased, objective, and independent opinion as to the issuer's capacity to meet its financial obligations. So far, CRISIL has rated 30,000 debt instruments, covering the entire debt market.

The debt obligations rated by CRISIL include:

Non-convertible debentures/bonds/preference shares

Commercial papers/certificates of deposits/short-term debt

Fixed deposits

Loans

Structured debt

CRISIL Ratings' clientele includes all the industry majors - 23 of the BSE Sensex constituent

companies and 39 of the NSE Nifty constituent companies, accounting for 80 per cent of the

equity market capitalization , are CRISIL's clients.

CRISIL's credit ratings are

An opinion on probability of default on the rated obligation

Forward looking

Specific to the obligation being rated

CRISIL ratings are based on a robust and clearly articulated analytical framework, which ensures

comprehensiveness, standardisation, comparability, and effective communication of the ratings

assigned and of every timely rating action. The assessment is based on the highest standards of

independence and analytical rigour.

CRISIL rates a wide range of entities, including:

Industrial companies

Banks

Non-banking financial companies (NBFCs)

Infrastructure entities

Microfinance institutions

Insurance companies

Mutual funds

State governments

Urban local bodies

CRISIL REAL ESTATE STAR RATINGS

CRISIL Real Estate Star Ratings provide city specific all-round assessment of real estate projects

and help buyers benchmark and identify quality projects within their city. CRISIL Real Estate

Star Ratings address two critical needs in the realty sector: improved transparency and objective

benchmarking of projects.

The key factors evaluated in the Star Ratings process are

quality of legal documentation,

construction related risks,

financial flexibility/viability of the project besides the background, and

track record of the project sponsor.

Star Ratings is based on an eight-point scale that is specific to the city— from ‘City 7-Star’, the

highest, to ‘City 1-Star’, the lowest being 'Non-Deliverable Project'.

Services

Irevna's services complement the onshore financial research teams of some of the world's largest

financial institutions and insurance companies. Its associates possess research expertise in a

variety of asset classes. Irevna also provides comprehensive consulting and finance outsourcing

services with solutions customised to meet the needs of various clients. Furthermore, insurance

companies and consultants have benefited from Irevna's services based on the foundation of

reduced costs and value-added analysis.

Equity Research Irevna provides a full spectrum of equity research services, from searching

and aggregating data to building models, generating ideas for onshore analysts and writing in-

depth reports. Irevna pioneered outsourced equity research and analytics in 2001 and retains this

vanguard position with over 50 of the world's leading buy- and sell-side financial institutions as

clients.

Credit Research Irevna provides valuable credit research and credit sourcing services to its

clients with capabilities across industries, lending types and geographies. Irevna has closely

worked with financial institutions such as banks, thrifts, asset management firms, private equity

firms and insurance companies. The credit research services offered include:

Credit Sourcing

Economic/Sector Assessments

Financial Modeling

Credit Risk Assessments

Legal Due Diligence

Credit Risk Monitoring

Portfolio Monitoring

Retail Brokerage Research Irevna's retail research services include end-to-end stock initiation

reports, financial performance projections, publishing (industry, market and thematic) research

reports, conducting comprehensive fundamental credit research, performing sovereign and

economics research, drafting mutual/hedge fund performance reports, and creating newsletters,

periodicals, and marketing presentations.

Derivatives Outsourcing Irevna is at the forefront of derivatives research outsourcing. Clients

depend on its deep knowledge of various derivative classes, including equity, credit,

commodities, interest rate, and foreign exchange (FX) products, as well as structured and exotic

offerings. Irevna's high-caliber associates allow it to offer an array of middle-office, product

control, and derivatives IT solutions.

Financial Technology Irevna's extensive experience is used to implement and maintain

complex financial technologies and systems through an amalgamation of technology, domain,

and project management. This enables Irevna to deliver solutions of the highest quality and

efficiency on deliverables such as:

FX and Economics In order to negotiate and work within the highly volatile FX markets clients

require partners who have a deep understanding of macroeconomics and that's where Irevna

offers its full support. Irevna is highly skilled in creating quantitative models for FX forecasting,

back testing and new product development. It also supports traders with trade book migration, IT

and application support for algorithmic trading projects, and structured trade reviews of exotic

fixed-income derivatives trades.

Quantitative Analytics In a fast-changing and complex business environment, companies face

many challenges. Irevna's quantitative analytics research team uses specialised statistical and

pricing tools to help financial institutions assess risk and make well-informed decisions to

maximise returns. Some of its services include derivatives pricing, index construction and

maintenance, product development and research monetization.

Commodities Research With the nature of commodity markets being highly volatile, in-depth

commodities research is critical. Through Irevna, market participants are supported through

comprehensive commodities research services such as price discovery using quantitative models,

performance and volatility analytics.

Risk Management Analytics As a proficient risk management consultant Irevna's capabilities

in the market, credit and operational domains is unmatched. Irevna's expertise lies in risk

assessment and quantification, the development of tools and frameworks based on Basel II

guidelines, stress testing, risk monitoring and reporting. With an array of services and offerings

Irevna has fast become a leading risk management consultant.

Private Wealth Management In the current market scenario, providers of private wealth

management offshoring services with specialised industry expertise and exposure to multiple

asset classes have a critical role to play. Irevna's experience in diverse domains of financial

outsourcing such as equity, fixed income, derivatives and risk management helps provide

customised services to private wealth management firms.

Insurance Actuarial Services Irevna is a pioneer in insurance actuarial offshoring. Irevna's

actuarial team is a mix of actuaries, student actuaries, CAs, MBAs, and statisticians. Irevna's

clients include general and life insurance, reinsurance, and pension and investment management

firms and provide them with effective problem-solving tools such as sophisticated actuarial

models.

Retail Risk Analytics Irevna's risk analytics team, has experience in building empirical models

(scorecards), strategies and performing data-driven analyses in the risk domain for consumer

banking/finance businesses, across various stages of the consumer's credit life cycle - Product

Planning, Credit Acquisition, Account Maintenance, Collections, and Account-Write-Offs.

RATING SYMBOLS

AAA(Triple A) Highest Safety

Instruments rated 'AAA' are judged to offer the highest degree of safety, with regard to timely payment of financial obligations. Any adverse changes in circumstances are most unlikely to affect the payments on the instrument.

AA(Double A) High Safety

Instruments rated 'AA' are judged to offer a high degree of safety, with regard to timely payment of financial obligations. They differ only marginally in safety from 'AAA' issues.

AAdequate Safety

Instruments rated 'A' are judged to offer an adequate degree of safety, with regard to timely payment of financial obligations. However, changes in circumstances can adversely affect such issues more than those in the higher rating categories.

BBB (Triple B) Moderate Safety

Instruments rated 'BBB' are judged to offer moderate safety, with regard to timely payment of financial obligations for the present; however, changing circumstances are more likely to lead to a weakened capacity to pay interest and repay principal than for instruments in higher rating categories.

BB(Double B) Inadequate Safety

Instruments rated 'BB' are judged to carry inadequate safety, with regard to timely payment of financial obligations; they are less likely to default in the immediate future than instruments in lower rating categories, but an adverse change in circumstances could lead to inadequate capacity to make payment on financial obligations.

BHigh Risk

Instruments rated 'B' are judged to have high likelihood of default; while currently financial obligations are met, adverse business or economic conditions would lead to lack of ability or willingness to pay interest or principal.

CSubstantial Risk

Instruments rated 'C' are judged to have factors present that make them vulnerable to default; timely payment of financial obligations is possible only if favourable circumstances continue.

DDefault

Instruments rated 'D' are in default or are expected to default on scheduled payment dates.

NM Instruments rated 'NM' have factors present in them, which render

Not Meaningful the outstanding rating meaningless. These include reorganisation or liquidation of the issuer, the obligation being under dispute in a court of law or before a statutory authority.

IMPORTANT: 1) CRISIL may apply '+' (plus) or '-' (minus) signs for ratings from 'AA' to 'C' to reflect comparative standing within the category.

2) CRISIL may assign rating outlooks for ratings from 'AAA' to 'B'. Ratings on Rating Watch will not carry outlooks. A rating outlook indicates the direction in which a rating may move over a medium-term horizon of one to two years. A rating outlook can be 'Positive', 'Stable', or 'Negative'. A 'Positive' or 'Negative' rating outlook is not necessarily a precursor of a rating change.

3) The contents within parenthesis are a guide to the pronunciation of the rating symbols.

4) A suffix of 'r' indicates investments carrying non-credit risk.

The 'r' suffix indicates that payments on the rated instrument have significant risks other than credit risk. The terms of the instrument specify that the payments to investors will not be fixed, and could be linked to one or more external variables such as commodity prices, equity indices, or foreign exchange rates. This could result in variability in payments-including possible material loss of principal-because of adverse movement in value of the external variables. The risk of such adverse movement in price/value is not addressed by the rating.

5) A suffix of '(so)' indicates instruments with structured obligation.

A CRISIL rating on a structured obligation reflects CRISIL's opinion on the degree of credit protection provided by the credit enhancement structure.

The assessment takes into consideration any arrangement for payment on the instrument by an entity other than the issuer to fulfill the financial obligations on the instrument. It also takes into account any other means of enhancing the credit quality of the rated obligation.

6) CRISIL assigns ratings to preference shares on its long-term rating scale. For the purpose of these ratings, preference dividend payments are construed as being equivalent to interest payments, and failure to pay the same on time is treated as a default.

ICRA

ICRA Limited (formerly Investment Information and Credit Rating Agency of India Limited)

was set up in 1991 by leading financial/investment institutions, commercial banks and financial

services companies as an independent and professional Investment Information and Credit

Rating Agency. Today, ICRA and its subsidiaries together form the ICRA Group of Companies

(Group ICRA). ICRA is a Public Limited Company, with its shares listed on the Bombay Stock

Exchange and the National Stock Exchange.

Range of Services

Rating Services

As an early entrant in the Credit Rating business, ICRA Limited (ICRA) is one of the most

experienced Credit Rating Agencies in the country today. ICRA rates rupee denominated debt

instruments issued by manufacturing companies, commercial banks, non-banking finance

companies, financial institutions, public sector undertakings and municipalities, among others.

ICRA also rates structured obligations and sector-specific debt obligations such as instruments

issued by Power, Telecom and Infrastructure companies. The other services offered include

Corporate Governance Rating, Stakeholder Value and Governance Rating, Credit Risk Rating of

Debt Mutual Funds, Rating of Claims Paying Ability of Insurance Companies, Project Finance

Rating, and Line of Credit Rating.

Grading Services

The Grading Services offered by ICRA employ pioneering concepts and methodologies, and

include Grading of: Initial Public Offers (IPOs); Microfinance Institutions (MFIs); Construction

Entities; Real Estate Developers and Projects; Healthcare Entities; and Maritime Training

Institutes. In IPO Grading, an ICRA-assigned IPO Grade represents a relative assessment of the

“fundamentals” of the issue graded in relation to the universe of other listed equity securities in

India. In MFI Grading, the focus of ICRA’s grading exercise is on evaluating the candidate

institution’s business and financial risks. The Grading of Construction Entities seeks to provide

an independent opinion on the quality of performance of the entities graded. Similarly, the

Grading of Real Estate Developers and Projects seeks to make property buyers aware of the risks

associated with real estate projects, and with the developers’ ability to deliver in accordance with

the terms agreed. ICRA’s Healthcare Gradings present an independent opinion on the quality of

care provided by healthcare entities. In the education sector, ICRA offers the innovative service

of Grading of Maritime Training Institutes in India.

Consulting Services

ICRA Management Consulting Services Limited (IMaCS), a wholly-owned subsidiary of

ICRA Limited, is a multi-line management and development consulting firm with a global

operating footprint. IMaCS offers Consulting Services in Strategy, Risk Management,

Regulation & Reform, Transaction Advisory, Development Consulting and Process Re-

engineering. IMaCS’ clientele includes Banks and Financial Service Companies, Corporate

Entities, Institutional Investors, Governments, Regulators, and Multilateral Agencies. Besides

India, IMaCS has consulting experience across 35 countries in South East Asia, Northern Asia,

West Asia, Africa, Western Europe, and North America.

Software Development, Business Intelligence and Analytics and Engineering Services

ICRA Techno Analytics Limited (ICTEAS), a wholly-owned subsidiary of ICRA Limited,

offers a complete portfolio of Information Technology (IT) solutions to meet the dynamic needs

of present-day businesses. The services range from the traditional development of client-server,

web-centric and mobile application

The Engineering Division of ICTEAS offers multidisciplinary computer aided engineering

design services. The activities cover design and drawing in the mechanical, civil/structural,

electrical and instrumentation space. ICTEAS engineers and designers are well-versed in

AutoCAD, MicroStation, PDS and Staad pro with experience in the Oil & Gas, Petrochemical

and Power Sectors. The services range from providing Engineering Design Services to CAD

Vectorisation and Conversion ServicesICTEAS has two subsidiaries, ICRA Sapphire Inc.

(ICSAP) and Axiom Technologies Limited (AXIOM). ICSAP is based in Connecticut, USA,

while AXIOM operates out of Kolkata, India.

ICSAP, a wholly-owned subsidiary of ICTEAS, offers US clients a full array of leading edge

Business Analytics and Software Development services backed by offshore teams, which work

out of ICTEAS, Kolkata. This hybrid engagement model of onsite and offshore teams allows for

seamless project management, execution and rapid offshore scaling of teams while bringing

down development costs.

AXIOM, a wholly-owned subsidiary of ICTEAS, specialises in customisation and

implementation services on the Oracle E-Business Suite. Its services include process study,

fitment analysis, customisation, implementation and post-implementation maintenance services.

AXIOM focuses on the Financial Modules of the Oracle E-Business Suite, which include Order

Management, General Ledger, Accounts Payable, Accounts Receivable, Cash Management,

Purchasing and Inventory, Fixed Assets and Global Consolidation.

RATING SYMBOLS

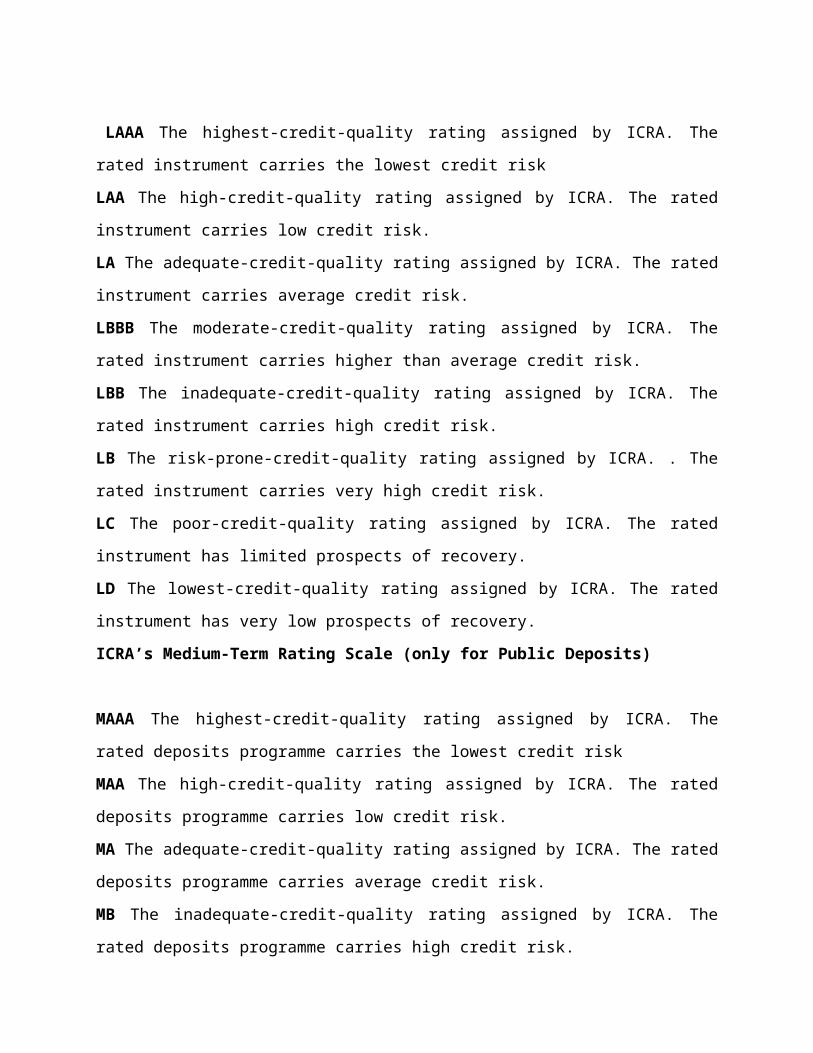

LAAA The highest-credit-quality rating assigned by ICRA. The rated instrument carries the

lowest credit risk

LAA The high-credit-quality rating assigned by ICRA. The rated instrument carries low credit

risk.

LA The adequate-credit-quality rating assigned by ICRA. The rated instrument carries average

credit risk.

LBBB The moderate-credit-quality rating assigned by ICRA. The rated instrument carries higher

than average credit risk.

LBB The inadequate-credit-quality rating assigned by ICRA. The rated instrument carries high

credit risk.

LB The risk-prone-credit-quality rating assigned by ICRA. . The rated instrument carries very

high credit risk.

LC The poor-credit-quality rating assigned by ICRA. The rated instrument has limited prospects

of recovery.

LD The lowest-credit-quality rating assigned by ICRA. The rated instrument has very low

prospects of recovery.

ICRA’s Medium-Term Rating Scale (only for Public Deposits)

MAAA The highest-credit-quality rating assigned by ICRA. The rated deposits programme

carries the lowest credit risk

MAA The high-credit-quality rating assigned by ICRA. The rated deposits programme carries

low credit risk.

MA The adequate-credit-quality rating assigned by ICRA. The rated deposits programme carries

average credit risk.

MB The inadequate-credit-quality rating assigned by ICRA. The rated deposits programme

carries high credit risk.

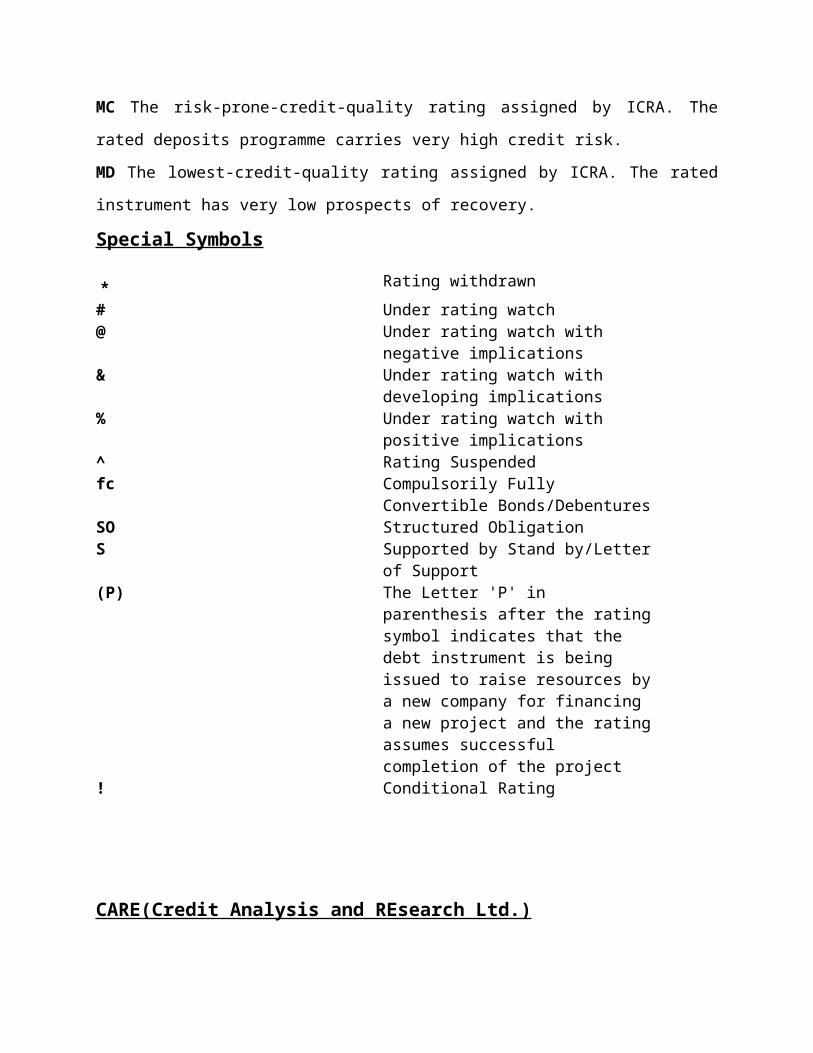

MC The risk-prone-credit-quality rating assigned by ICRA. The rated deposits programme

carries very high credit risk.

MD The lowest-credit-quality rating assigned by ICRA. The rated instrument has very low

prospects of recovery.

Special Symbols

* Rating withdrawn

# Under rating watch @ Under rating watch with negative

implications & Under rating watch with developing

implications % Under rating watch with positive

implications ^ Rating Suspended fc Compulsorily Fully Convertible

Bonds/Debentures

SO Structured Obligation S Supported by Stand by/Letter of Support (P) The Letter 'P' in parenthesis after the

rating symbol indicates that the debt instrument is being issued to raise resources by a new company for financing a new project and the rating assumes successful completion of the project

! Conditional Rating

CARE(Credit Analysis and REsearch Ltd.)

Credit Analysis & Research Ltd. (CARE Ratings) is a full service rating company that offers a

wide range of rating and grading services across sectors. CARE has an unparallel depth of

expertise. CARE Ratings methodologies are in line with the best international practices. CARE

Ratings has completed over 8488 rating assignments having aggregate value of about Rs.26609

bn (as at Sep 30, 2010), since its inception in April 1993. CARE is recognised by Securities and

Exchange Board of India (Sebi), Government of India (GoI) and Reserve Bank of India (RBI)

etc.

RATING SERVICES

CARE's Credit Rating is an opinion on the relative ability and willingness of an issuer to make

timely payments on specific debt or related obligations over the life of the instrument. CARE

rates rupee denominated debt of Indian companies and Indian subsidiaries of multinational

companies.

CARE undertakes credit rating of all types of debt and related obligations. These include all

types of medium and long term debt securities such as debentures, bonds and convertible bonds

and all types of short term debt and deposit obligations such as commercial paper, inter-

corporate deposits, fixed deposits and certificates of deposit.

CARE also rates quasi-debt obligations such as the ability of insurance companies to meet

policyholders’ obligations. CARE's preference share ratings measure the relative ability of a

company to meet its dividend and redemption commitments.

CARE has a strong structured finance team and has been instrumental in developing rating

methodologies for innovative asset backed securities in the Indian capital market. The term

'structured financing' refers to securities where the servicing of debt and related obligations is

backed by some sort of financial assets and/ or credit support from a third party to the

transaction.

CARE’s credit ratings consider a medium to long term horizon which is typically defined as

three to five years. While the time horizon of a short term instrument is up to one year.

ONICRA(

Onicra Credit Rating Agency is an active player in the Credit and Performance Assessment

space. It provides scoring and rating services to Individuals, Corporates and MSMEs. These

ratings enable the lender or service provider to make smart, value based decisions on the

individuals, corporates or the MSME by arming them with essential information that includes

financial, operational, productivity and 3-Dimensional analysis that provides a holistic view

about the entity.

TYPES OF RATINGS

MICRO, SMALL AND MEDIUM ENTERPRISE RATING

The changes in the industrial climate world over and the liberalization of economic environment

have thrown up many opportunities and challenges to the Micro, Small and Medium Enterprises

(MSME). Therefore, there is a need to create awareness amongst MSMEs about the strengths

and weaknesses of their existing operations and to provide them with an opportunity to enhance

their organizational strength in terms of Finance, Marketing, Production, Corporate Governance

and Operations.

EDUCATION RATING

A well-developed and organized education sector is crucial for bringing socio-economic

transformation in the country. We provide an assessment, rating and grading model for

educational institutions that complies with government laid down regulations. Through the rating

report, institutions can reassess their areas of expertise and aim towards identifying, validating

and improving the quality and standard of education. We have experience in conducting SWOT

and Training Needs Analysis (TNA) for engineering colleges to apply for TEQIP-II funds.

(A World Bank and Ministry of HRD initiative)

BUSINESS ASSOCIATE RATING

The Indian economy is gathering momentum and many corporates are finding it difficult to

identify the right mix of business associates to work with. We provide an assessment, rating and

grading model that enables corporates to gain valuable insights into the sales, operational and

financial architecture of their associates. The service captures, records and analyses vital data

pertaining to an existing or potential business associate, including current and past performance,

to minimize risk exposure while formulating a partnership

EMPLOYEE BACKGROUND ASSESSMENT & PROFILING

Onicra is a National Skills Registry (NSR) empanelled Background Screening Company . Our

services provide comprehensive results that help employers reduce workplace violence , theft ,

substance abuse and negligent hiring abilities . Details such as employment history , educational

qualifications and several other personal and behavioral information are captured . We fully

understand the complexity and criticality that employers face to select the right candidate. We

give you the insight you need to uncover unknown facts quickly . Our employee background

screening services are provided to international and national companies in the IT/ITES,

Hospitality, FMCG, Telecom and Financial sectors. The success of any organization depends on

its employees.The success rate of companies is high where there is a mutual trust between the

employer and the employee. Employee Background Screening is a way to develop that mutual

trust.

VENDOR RATING

Onicra’s vendor ratings provide insight, analysis and advice on the key indicators of a vendor’s

overall status such as strategy, organization goals, products, marketing and financials. Vendors

are given standing, according to their attainment of some level of performance, such as delivery,

lead time, quality, price and credit standing.

RATING FRAMEWORK

The basic methodology followed to formulate and plan the mathematical model for rating is

consistent across individuals and corporates. It follows a five step process.

The first step is the definition of the objective- which is the entity that needs to be rated.

This is followed by collation of all the high level parameters that affect the entity. This

high level parameter collation is done using a mix of market analysis, in-house expertise,

primary and secondary research.

Once the parameters are identified, Onicra follows a top-down approach of parameter

decomposition. This simply entails decomposing the parameters into the sub-parameters

upon which they are dependent at several levels, until we reach independent and

quantifiable parameters.

These parameters are input into a mathematical model and analyzed to ensure that the

results are in line with actual behavior.

Simultaneously, the organization’s research groups are constantly monitoring and

keeping checks on various other parameters, both environmental and economic to keep

the model being worked on, relevant, fresh and up-to-date with the fast changing

financial and economic scene.

STANDARDS & POOR’S

Standard & Poor’s is a leading provider of financial market intelligence. The world’s

foremost source of credit ratings, indices, investment research, risk evaluation and data,

Standard & Poor’s provides financial decision-makers with the intelligence they need to

feel confident about their decisions.

Standard & Poor’s Ratings Services’ mission is to provide high-quality, objective,

independent, and rigorous analytical information to the marketplace. In order to achieve

its mission, Ratings Services strives for analytic excellence at all times; evaluates its

rating criteria, methodologies, and procedures on a regular basis; and modifies or

enhances them as necessary to respond to the needs of the global capital markets. Ratings

Services endeavors to conduct the rating and surveillance processes in a manner that is

transparent and credible and that also maintains the integrity and independence of such

processes in order to avoid any compromise by conflicts of interest, abuse of confidential

information, or other undue influences.

RATING SYMBOLS

Ratings Services continues to utilize a global ratings scale and traditional rating symbols.

Ratings Services has not adopted separate ratings or identifiers for ratings of structured

finance products. In our view, the use of separate rating symbols or identifiers for

structured finance products ratings would not provide any additional information about

the meaning and limitations of ratings. Ratings Services believes that the capital markets

are better served by initiatives to enhance the rating process and increase transparency

about the rating process. In addition, adopting separate ratings or identifiers for structured

finance product ratings may have the unintended consequence of imposing substantial

administrative burdens and operational difficulties on, and increasing the costs for,

market participants. Finally, in response to a request for comment conducted by Ratings

Services this year, a substantial majority of the respondents were against a proposal to

adopt a subscript or identifier for structured finance product ratings.

Long-term issuer credit ratings

AAA: An obligor rated 'AAA' has extremely strong capacity to meet its financial

commitments. 'AAA' is the highest issuer credit rating assigned by Standard & Poor's.

AA: An obligor rated 'AA' has very strong capacity to meet its financial commitments. It

differs from the highest-rated obligors only to a small degree.

A: An obligor rated 'A' has strong capacity to meet its financial commitments but is

somewhat more susceptible to the adverse effects of changes in circumstances and

economic conditions than obligors in higher-rated categories.

BBB: An obligor rated 'BBB' has adequate capacity to meet its financial commitments.

BB, B, CCC, and CC: Obligors rated 'BB', 'B', 'CCC', and 'CC' are regarded as having

significant speculative characteristics. 'BB' indicates the least degree of speculation and

'CC' the highest. While such obligors will likely have some quality and protective

characteristics, these may be outweighed by large uncertainties or major exposures

to adverse conditions.

BB: An obligor rated 'BB' is less vulnerable in the near term than other lower-rated

obligors. However, it faces major

ongoing uncertainties and exposure to adverse business, financial, or economic

conditions, which could lead to the obligor's inadequate capacity to meet its financial

commitments.

B: An obligor rated 'B' is more vulnerable than the obligors rated 'BB', but the obligor

currently has the capacity to meet its financial commitments. Adverse business, financial,

or economic conditions will likely impair the obligor's capacity or willingness to meet its

financial commitments.

CCC: An obligor rated 'CCC' is currently vulnerable, and is dependent upon favorable

business, financial, and economic conditions to meet its financial commitments.

CC: An obligor rated 'CC' is currently highly vulnerable.

R: An obligor rated 'R' is under regulatory supervision owing to its financial condition.

During the pendency of the regulatory supervision, the regulators may have the power to

favor one class of obligations over others or pay some obligations and not others. Please

see Standard & Poor's issue credit ratings for a more detailed description of the effects of

regulatory supervision on specific issues or classes of obligations.

SD and D: An obligor rated 'SD' (selective default) or 'D' has failed to pay one or more of

its financial obligations (rated or unrated) when it came due. A 'D' rating is assigned

when Standard & Poor's believes that the default will be a general default and that the

obligor will fail to pay all or substantially all of its obligations as they come due.

An 'SD' rating is assigned when Standard & Poor's believes that the obligor has

selectively defaulted on a specific issue or class of obligations but it will continue to meet

its payment obligations on other issues or classes of obligations in a timely manner. A

selective default includes the completion of a distressed exchange offer, whereby

one or more financial obligation is either repurchased for an amount of cash or replaced

by other instruments

MOODY’S

Moody's is an essential component of the global capital markets, providing credit ratings,

research, tools and analysis that contribute to transparent and integrated financial

markets. Moody's Corporation (NYSE: MCO) is the parent company of Moody's

Investors Service, which provides credit ratings and research covering debt instruments

and securities, and Moody's Analytics, which offers leading-edge software, advisory

services and research for credit analysis, economic research and financial risk

management. The Corporation, which reported revenue of $2 billion in 2010, employs

approximately 4,500 people worldwide and maintains a presence in 26 countries.

Moody’s Long-Term Rating Definitions:

Aaa Obligations rated Aaa are judged to be of the highest quality, with minimal credit

risk.

Aa Obligations rated Aa are judged to be of high quality and are subject to very low

credit risk.

A Obligations rated A are considered upper-medium grade and are subject to low credit

risk.

Baa Obligations rated Baa are subject to moderate credit risk. They are considered

medium-grade and as such may possess certain speculative characteristics.

Ba Obligations rated Ba are judged to have speculative elements and are subject to

substantial credit risk.

B Obligations rated B are considered speculative and are subject to high credit risk.

Caa Obligations rated Caa are judged to be of poor standing and are subject to very

high credit risk.

Ca Obligations rated Ca are highly speculative and are likely in, or very near, default,

with some prospect of recovery of principal and interest.

C Obligations rated C are the lowest rated class of bonds and are typically in default,

with little prospect for recovery of principal or interest.

Moody’s employs the following designations to indicate the relative repayment ability of

rated issuers:

P-1 Issuers (or supporting institutions) rated Prime-1 have a superior ability to repay

short-term debt obligations.

P-2 Issuers (or supporting institutions) rated Prime-2 have a strong ability to repay short-

term debt obligations.

P-3 Issuers (or supporting institutions) rated Prime-3 have an acceptable ability to repay

short-term obligations.

NP Issuers (or supporting institutions) rated Not Prime do not fall within any of the

Prime rating categories.

MARC(MALAYSIAN RATING CORPORATION)

Malaysian Rating Corporation (MARC) is a domestic credit rating institution in

Malaysia. MARC was incorporated in October 1995. We commenced operations on 17

June 1996, and were officially launched on 5th September 1996 by the Deputy Prime

Minister and Minister of Finance, Malaysia.

Services

All ratings completed by MARC are kept under continuous surveillance. The ratings are formally reviewed at least once a year. Due to positive or adverse developments, ratings may be placed on MARCWatch for upgrading, affirmation or downgrading.

Rating Products, Symbols & Definitions

Corporate Debt Ratings Assess the likelihood of timely repayment of principal and payment of interest over the term to maturity of such debts.

Issuer Ratings Are applied to a company's debt securities provided they are homogeneous, senior debt or where debts rank pari passu, under a scenario whereby the company may be intending to issue multiple debts within a short time frame.[

Islamic Capital Market Instrument Ratings

Assess the likelihood of timely repayment of the instruments issued under the various Islamic financing contract(s).

Asset-Backed Securities (ABS)

Assess the likelihood of timely repayment of principal and payment of interest on debt securities issued by a corporate, usually a single purpose vehicle, against stable income-generating assets, e.g. hire purchase receivables, toll collections, rental income, etc.

Financial Institution Ratings

Assess the creditworthiness of financial institutions, i.e. commercial and investment banks, finance companies and discount houses.

Corporate Credit Ratings

Are a measure of a corporate's intrinsic ability and overall capacity for timely repayment of its financial obligations. These are voluntary ratings that may be sought by companies to enhance corporate governance and transparency.

Insurer Financial Strength Ratings

Essentially assess the financial security characteristics of an insurance company on its ability

to meet its policyholder obligations in accordance with the terms of their insurance contracts.

Islamic Financial Institution Governance Ratings

Assess the corporate governance of an Islamic Financial Institution (IFI). IFI governance ratings are an assessment of how the IFI promotes sound governance transparency and accountability and institutional capacity-building for improved governance.

Sovereign Issuer Credit Ratings

Are intended to be assessments of the ability and willingness of a sovereign government to repay its debt obligations in a full and timely manner.

FITCH

Fitch Solutions, a division of the Fitch Group, focuses on the development of fixed-

income products and services bringing to market a wide range of data, analytical tools

and related services, and is the distribution channel for Fitch Ratings content. Fitch

Solutions products and services provide market participants with greater insight into the

growing complexity of the credit markets to enable more timely and informed business

decisions.

SERVICES

Research Services Credit research, ratings and analytical tools offered via an online

platform and as a data feed.

Structured Finance Solutions Surveillance, performance data, models and analytics for

structured finance portfolio management.

Risk & Performance Analytics Ratings, implied ratings, and company financials

distributed via single and integrated data feeds and an analytical platform.

Pricing & Valuation Services Independent pricing and valuation data for structured

finance and fixed-income derivatives.

Training Credit and corporate finance training services for bankers, fixed income

professionals and regulators.

Quantitative Analytics Academic-quality research and analytics delivered by Fitch

Solutions quantitative analysts.

RATING SYMBOLS

AAA: Highest credit quality.

‘AAA’ ratings denote the lowest expectation of default risk. They are assigned only in

cases of exceptionally strong capacity for payment of financial commitments. This

capacity is highly unlikely to be adversely affected by foreseeable events.

AA: Very high credit quality.

‘AA’ ratings denote expectations of very low default risk. They indicate very strong

capacity for payment of financial commitments. This capacity is not significantly

vulnerable to foreseeable events.

A: High credit quality.

‘A’ ratings denote expectations of low default risk. The capacity for payment of financial

commitments is considered strong. This capacity may, nevertheless, be more vulnerable

to adverse business or economic conditions than is the case for higher ratings.

BBB: Good credit quality.

‘BBB’ ratings indicate that expectations of default risk are currently low. The capacity

for payment of financial commitments is considered adequate but adverse business or

economic conditions are more likely to impair this capacity.

BB: Speculative.

‘BB’ ratings indicate an elevated vulnerability to default risk, particularly in the event of

adverse changes in business or economic conditions over time; however, business or

financial flexibility exists which supports the servicing of financial commitments.

B: Highly speculative.

‘B’ ratings indicate that material default risk is present, but a limited margin of safety

remains. Financial commitments are currently being met; however, capacity for

continued payment is vulnerable to deterioration in the business and economic

environment.

CCC: Substantial credit risk.

Default is a real possibility.

CC: Very high levels of credit risk.

Default of some kind appears probable.

C: Exceptionally high levels of credit risk

Default is imminent or inevitable, or the issuer is in standstill. Conditions that are

indicative of a ‘C’ category rating for an issuer include:

a. the issuer has entered into a grace or cure period following non-payment of a material

financial obligation;

b. the issuer has entered into a temporary negotiated waiver or standstill agreement

following a payment default on a material financial obligation; or

c. Fitch Ratings otherwise believes a condition of ‘RD’ or ‘D’ to be imminent or

inevitable, including through the formal announcement of a coercive debt exchange.

RD: Restricted default.

‘RD’ ratings indicate an issuer that in Fitch Ratings’ opinion has experienced an uncured

payment default on a bond, loan or other material financial obligation but which has not

entered into bankruptcy filings, administration, receivership, liquidation or other formal

winding-up procedure, and which has not otherwise ceased business. This would include:

a. the selective payment default on a specific class or currency of debt;

b. the uncured expiry of any applicable grace period, cure period or default forbearance

period following a payment

default on a bank loan, capital markets security or other material financial obligation;

c. the extension of multiple waivers or forbearance periods upon a payment default on

one or more material financial

obligations, either in series or in parallel; or

d. execution of a coercive debt exchange on one or more material financial obligations.

D: Default.

‘D’ ratings indicate an issuer that in Fitch Ratings’ opinion has entered into bankruptcy

filings, administration, receivership, liquidation or other formal winding-up procedure, or

which has otherwise ceased business.

Default ratings are not assigned prospectively to entities or their obligations; within this

context, non-payment on an instrument that contains a deferral feature or grace period

will generally not be considered a default until after the expiration of the deferral or grace

period, unless a default is otherwise driven by bankruptcy or other similar circumstance,

or by a coercive debt exchange.

“Imminent” default typically refers to the occasion where a payment default has been

intimated by the issuer, and is all but inevitable. This may, for example, be where an

issuer has missed a scheduled payment, but (as is typical) has a grace period during

which it may cure the payment default. Another alternative would be where an issuer has

formally announced a coercive debt exchange, but the date of the exchange still lies

several days or weeks in the immediate future.

In all cases, the assignment of a default rating reflects the agency’s opinion as to the most

appropriate rating category consistent with the rest of its universe of ratings, and may

differ from the definition of default under the terms of an issuer’s financial obligations or

local commercial practice.

MANAGEMENT OF FINANCIAL SERVICES

ASSIGNMENT

ON

“CREDIT RATING AGENCIES”

SUBMITTED BY: SUBMITTED TO:

RICHA DHAWAN DR. SHELLY

GLOBAL INSTITUTE OF MANAGEMENT

(2009-11)