credit suisse 20th annual asian investment conference ... · pdf filecredit suisse 20th annual...

TRANSCRIPT

Credit Suisse 20th Annual Asian Investment Conference

MARCH 2017

Information contained in our presentation is intended solely for your personal

reference and is strictly confidential. Such information is subject to change without

notice, its accuracy is not guaranteed and it may not contain all material

information concerning the Company. Neither we nor our advisors make any

representation regarding, and assumes no responsibility or liability for, the

accuracy or completeness of, or any errors or omissions in, any information

contained herein.

In addition, the information contains projections and forward-looking statements

that reflect the Company’s current views with respect to future events and

financial performance. These views are based on current assumptions which are

subject to various risks and which may change over time. No assurance can be

given that future events will occur, that projections will be achieved, or that the

Company’s assumptions are correct. Actual results may differ materially from

those projected.

This presentation is strictly not to be distributed without the explicit consent of

Company’s management under any circumstances.

DISCLAIMER

2

3

1. Growth, Growth, GROWTH!

2. Strong Earnings and Performance

3. Founders Capital Injection - RM1 billion

4. Dividend Policy

5. Value in the Balance Sheet

6. World’s Lowest Cost Airline

7. Ancillary Target of RM60 per pax

8. The Digital Airline

WHY AIRASIA?

• Built Asean Powerhouse.

• All associates performing excellently, not just Malaysia.

[1] Includes two aircraft leased to a 3rd party

Group fleet as at end-2016:

174

A320neo deliveries:

+19

3rd party leases:

+10[1]

Lease retirements:

-3

Group fleet at end-2017:

203

4

A320ceo deliveries:

+3

169 179 176 173 170 157

524 57 84 109 141

614

25

174203

233263

293323

2016 2017 2018 2019 2020 2021

A320ceo A320neo A321neo

[2] AA Msia– 14 (including for replacement of older acft), AA Thailand - 5

ESTIMATED AIRASIA GROUP FLEET IN

THE NEXT 5 YEARS

2017 NET AIRCRAFT ADDITION

STRONG LOAD FACTOR TREND TO

CONTINUE

1. GROWTH, GROWTH , GROWTHTo Cater to the Underserved Market – ASEAN +2

90 89

82

928890

8386 88 87

AAB AAT IAA AAP AAI

1Q17 2Q17

+5ppts

YoY+3ppts

YoY+2ppts

YoYFlat

YoY

-3ppts

YoY

+5ppts

YoY+3ppts

YoY+2ppts

YoY

Flat

YoY

+1ppts

YoY

[1][2]

29Aircraft for

growth

• Malaysia – 7• Thailand – 6• Indonesia – 2• Philippines – 5• India – 6• Japan – 3

WHAT WORRIES THE MARKET?COMPETITION.

World’s lowest-cost airline. Lowest CASK in the industry allows AirAsia to focus on generating revenue, regardless of the yield trend.

Ancillary income machine. Additional stream of income other competitors don’t have and can’t scale up as quickly.

Long track record of profitability. Able to turn a profit in lean times and when oil was over US$100/barrel.

Unbeatable frequencies.

Route thickness is a barrier to entry and gives AirAsia the privilege as the price setter.

Low expansion cost. Operating to over 125 destinations in Asia. Able to start new routes fast with low set-up costs.

Strong brand in all home markets. Built up a strong brand over the years, a key to success that other LCCs neglect.

First mover advantage. The first LCC to new markets in ASEAN and operating 66 unique city pairs system-wide, more than any other competitor in the region.

ASEAN advantage. Operate as one airline with a network spread over 18 hubs across a potential market of 625 million people.

Only Malaysian LCC. Malindo has upgraded to a full-service carrier leaving the LCC space in Malaysia wide open for AirAsia.

Profitable and competitive. Profitable in Indonesia despite small market share. Lower CASK in India than the “giant” Indigo despite a small fleet.

Digital Airline. Investing heavily in digitalisation and the future of aviation and travel – ahead of the rest!

5

2. STRONG EARNINGS & PERFORMANCESAirAsia Group Recorded Profit Before Tax RM2.13 Billion in FY2016

• Group Passengers Carried: 56.59 million (+12%)

• Group Load Factor: 86% (+6 ppts)

• Group Revenue: RM12.02 billion (+11%)

• Group Operating Profit: RM2.15 billion (+24%)

• Group Net Operating Profit: RM1.65 billion (+58%)

• Group Profit Before Tax: RM2.13 billion (12.1x)

• Group Cash Position: RM2.97 billion

• Group Net Gearing: 1.30x

6Refer to appendix for segment breakdown

AIRASIA GROUP: FULL YEAR 2016 PRO-FORMA CONSOLIDATED RESULTS

14.81

15.71

12.65

11.70

10.50

11.50

12.50

13.50

14.50

15.50

16.50

4Q15 4Q16

sen/A

SK RASK UP 6%

- Strong demand for air travel

- Load factor up by 2 ppts to 87%

- Higher average fare of RM186 (+5%)

CASK DOWN 8%

- Decrease in average fuel price of

20% to US$59/barrel jet kerosene

- Fuel consumption flat despite 2%

capacity increase

AirAsia Malaysia FY2016

• Passengers Carried: 26.41 million (+9%)

• Load Factor: 87% (+6 ppts)

• Revenue: RM6.92 billion (+10%)

• Operating Profit: RM2.05 billion (+29%)

• Net Operating Profit: RM1.67 billion(+63%)

• Profit After Tax: RM2.03 billion(+276%)

AIRASIA MALAYSIA: 4Q16 & FY2016 PERFORMANCE

2. STRONG EARNINGS & PERFORMANCESAirAsia Malaysia Recorded Profit After Tax RM2.03 Billion in FY2016

7

AIRASIA’S GROWING FOOTPRINT OVER THE LAST 15 YEARS

2001 2010 2013 2016

COUNTRIES 1DESTINATIONS 5ROUTES 5ASK (in Mil) 586

COUNTRIES 18DESTINATIONS 65ROUTES 145ASK (in Mil) 37,935

COUNTRIES 17DESTINATIONS 83ROUTES 182ASK (in Mil) 52,710

COUNTRIES 23DESTINATIONS 125ROUTES 255ASK (in Mil) 103,080

We expanded our footprint extensively into key markets whilst keeping an eye on underserved routes with high yields, enabling us to grow to 23 countries, 125 destinations and 255 routes in just 15 years.

AIRASIA’S FOOTPRINT GROWTH OVER 15 YEARS

Countries +22 + 23% CAGR

Destinations +120 + 24% CAGR

Routes +250 + 30% CAGR

ASK (in Mil) +102,494 + 45% CAGR

IN 9 YEARS IN 3 YEARS IN 3 YEARS

Source: Annual Report, Quarterly Reports and Internal data. 8

2. STRONG EARNINGS & PERFORMANCES

Confidence

• RM1bil injection shows founders confidence and commitment towards AirAsia

growth and expansion.

Increased Shareholdings

• Combined shareholding of 32.3%

Net Gearing

• 4Q2016 - 1.30x down to 1Q2017 – 1.0x (est.)

Continuity of policy since 2013

• Committed to pay dividend up to 20% of the net operating profit p.a.

Dividend payments

• FY2015 - RM0.04 (2.20%) paid on 29 June 2016

• FY2014 - RM0.03 (1.20%) paid on 2 July 2015

• FY2013 - RM0.04 (1.40%) paid on 3 July 2014

9

3. FOUNDERS’ CAPITAL INJECTION

4. DIVIDEND STOCK

INVESTMENTS WORTH RM5.8 BILLION

Monetisation

• Realising approximately

USD900 - USD1.2 billion

from Asia Aviation Capital

• IPO for training centre,

AACE

• Potential full disposal of

AirAsia Expedia (AAE

Travel)

• Ground Team Red (GTR):

Set up ground handling

teams in Indo-China and

China

Asia Aviation Capital -

Updates

• Deadline for final bidding

submission 27 Mar 2017

(indicative)

• SPA & SSA execution to

start 7 April 2017

(indicative)

Note: Refer to appendix for private equity performance FY201610

5. VALUE IN THE BALANCE SHEET

Value of Unwinding Hedges

• If we unwind all hedges, we could

have a net gain of MYR 936 million:

1. FX hedges

• Total gains approx MYR923mil

2. Fuel hedges

• Total gains approx MYR184mil

3. IRS hedges

• Out of the money. Total loss is

MYR 171mil

• However, much smaller than

gains from FX and Fuel hedges

Source: Bloomberg

AirAsia figures based on full year 2016 results, USD/MYR = 4.14 (full year average)

Jetstar’s CASK breakdown unavailable

CASK (US¢) based on latest available results

11

2.26 2.29 2.21 2.77 3.00 3.41 3.023.82 3.73 3.54

4.52 4.02

5.90 5.750.84 1.07 1.421.36

1.50 1.24 1.671.09 1.38 1.68

1.19 1.79

1.25 1.54

3.11 3.36 3.634.13

4.50 4.64 4.68 4.91 5.02 5.11 5.215.71 5.80

7.15 7.29

Air

Asi

a X

Gro

up

Air

Asi

a (G

rou

p)

Rya

nai

r

Ceb

u

Cit

ilin

k

Spir

it A

irlin

es

Ind

iGo

No

rweg

ian

Air

JetS

tar

Alle

gian

t

Spic

e Je

t

Ala

ska

Go

l Lin

has

No

k

Sou

thw

est

CASK ex fuel CASK Fuel

6. WORLD’S LOWEST COST AIRLINE

THE POWER OF ONEDRIVE GROWTH & REDUCE COST FURTHER

• ASEAN Holding Co to be listed

• Branding by sending consistent messaging across the Group

• Culture cultivated by more internal marketing: One Voice, One Vision, One with our People

• Centralisation of functions and processes to extract group synergy, leverage scale & reduce cost

• Regionalisation of more departments at Group

• Standardisation and Streamlining SOPs, Standardise Document Control Management System and Station

Audit Checklists across the Group, implementing best practices across stations, One Pricing for inflight meals

Total Cost Saving Initiatives ~ USD23m annuallyShared Service

Savings of ~US$3m annually

AGSS & Treasury

AGSS (savings of US$2m)

• Automation

–Improve system & workflow

• Centralize Payment release–

payment below RM 1.5 M approve

by AGSS, strengthen and

empowered AGSS

Treasury - Cash Pooling (savings of

US$1m)

• Cash & Liquidity Optimization

• Cash centralization

• Optimize Returns

RegionalisationSavings of ~US$5m annually

Control Center + Localised Coordination

• Legal

• CFO

• Procurement

• People Department

• Internal Audit

• Corp Finance

• ICT

• Network Planning

• Engineering

• Customer Care

Best practices sharing

Share resources

Eliminate duplication work

Consolidation

• CapEx Group purchase, ICT, GSE,

Inflight

• Consolidate media purchase –

Commercial

• Group sourcing Lowest costs

through scale benefits – Inflight,

crew, GS

Procurement Savings of ~US$15m annually

12

Baggage45.1%

Cargo9.6%

F&B6.9%

Assigned seat6.1%

Connecting fees5.7%

Insurance5.6%

Duty free & merchandise

1.6%

Others19.4%

7. ANCILLARY RM50 per pax; Onward to RM60

Ancillary

Revenueper pax

FY2016 – AirAsia Malaysia

• Total ancillary revenue increased +10.4%

• ancillary income per pax +1.4%; RM47.02 to RM47.68

(approx. revenue RM118.9mil)

• Biggest contributors:

• Baggage up 16% (contributes 45% of total ancillary

revenue) and

• Cargo (9.6% of total ancillary revenue)

• Highest growth:

• Assigned seat (+13.6%), Flythru (+34%)

• Inflight merchandise (+82.7%), Inflight Duty Free

(+116%) and Aircraft Advertising (+191%)

• Core ancillary – FY2016 vs FY2015 achievements:

F&B

• Revenue +10%. Introduced Santan combo meals for RM10.

• Bought over T&CO (Barista in the sky for LCC).

Baggage

• Revenue +16% (RM24.4mil)

Fly-thru

• Connecting fee +34%. AA Grp recorded 2.2mil FlyThru traffic for FY2016 (+36% vs FY2015).

• AAB FY16 connecting fees +RM0.78 per pax from RM1.95 to RM2.73 (+40%) revenue of RM72.1m vs RM47.3m

• Top 3 Routes: S’pore–Tiruchirappalli (+19%), Incheon–S’pore (+88%), Jeddah–Surabaya (pilgrimage route) (+72%)

13

7. ANCILLARY TARGET – RM60 PER PAX

Separate branding and

drive pre-book

Enable ROKKI at all

AOCs

Maximize take up

rate

Enforcement and demand

based pricing to optimize

revenue

Focus on dynamic pricing,

product innovation and

bundling

Product innovation and

demand based pricing to

optimize revenue

To increase number of

users and online

conversion via one-click

payment solution

Centralization, rationalize

catalogue and drive

ecommerce conversion

14

Priority By Category

Enforcement

Seamless user experience

Maximize touch points

Revenue management

Technology & Data

Awareness & product education

Ancillary Revenue Growth 2017

Strategies

Cabin baggage and checked baggage

Self-service kiosks, simplified booking, BIG Pay for one click payment solution

Cabin crew as sales agents, kiosk, MMB for anonymous booking

Demand based pricing for seats and baggage

EPOS, Big data for personalized marketing

Initiatives

Set product value proposition, drive pre-book & standardise branding

Timelines

On-going

Q2 2017 onwards

Q3 2017

On-going

On-going

Q2 onwards

15

7. ANCILLARY – KEY STRATEGIES

Buying

Perfumes & Cosmetics

Watches

Liquor

Jewellery & Gifts

Strategic Focus

Buy Direct from Brand Principals

Margin Optimization

Increase Product Range by Customers Profiling

Introducing Major Brands In All Categories

Health & Gadgets

Cigarettes

CATEGORIES

New catalogue differentiator

Desirable but non-mainstream counter brands

16

Duty Free Buying Strategy

7. ANCILLARY – KEY STRATEGIES

Think of our plane as a thing, a big part of our information network.

Building a platform so all data

related to aircraft is in one place.

Guests Operations Maintenance Cabin• experience

• interests

• profiling

• Experience

• Communication

• Fuel management

• Crewing

• Ground & Flight Ops

Info

• AIMS

• aircraft servicing

• Response

management

• in-flight sales

• time

management

8. THE INTERNET WAY OF AIRASIA

17

8. THE DIGITAL AIRLINE

Improve performance Reduce Costs

Create Innovative ServicesNew Revenue Stream

• BigPay’s e-Wallet – cashless/ hassle free travel

• Mobile facilitates seamless travel

• Platform for future development of e-commerce

travel

• Big Duty Free

• BigPay - Fx wallet with 5 foreign currencies (USD,

GBP, SGD, EUR, AUD)

• Reduction of distribution cost/ channels by direct

customer acquisition

• Increase share of sales through mobile device

• Paperless travel

• Increase productivity with automation

• Offer personalised services to customer’s travel

needs at no additional cost

• Increase conversion by 2ppt equals to approx.

RM2bil in sales (FY2016 5%)

• Increase ancillary sales through target marketing

18

19

20

WHY AIRASIA?

ASEAN POWERHOUSE

THANK YOU

0.03 1 25 7

1215

1924

2832

37

4650

5457

2 3 717

2742

6578 84

101 108127

169

196 201 204

-50

0

50

100

150

200

10.00

20.00

30.00

40.00

50.00

60.00

70.00

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016F

Passengers Flown (in mil)

No. of Aircraft

21

AIRASIA’S GROWTH STORY

FROM MALAYSIA TO ASEAN TO ASIA

All figures refer to AAB, AAT, IAA, AAP, AAI, AAX1 As of end-2016 AAB, AAT, IAA, AAP, AAI, AAX

225 202143

108 84 78 75 60 47 46 35 30 23

Lion Air AirAsia Group GarudaIndonesia

SingaporeAirlines

VietnamAirlines

MalaysiaAirlines

Thai Airways PhilippineAirlines

Cebu Pacific Citilink VietJet Air Nok Air Tigerair

LARGEST LCC IN ASIA BY PASSENGERS

((million))

Source: Airlines’ Financials and CAPA

AirAsia fleet notes: Includes AAX, excludes two aircraft leased to PIA and two aircraft delivered to AirAsia Japan but yet to commence operations

SECOND LARGEST AIRCRAFT FLEET IN ASEAN

22

51 ATR turboprops

114.6 101.7 96.6

61.3 47.4 41.1 40.7 35.0 34.3 31.2

19.1 18.2 14.7 13.5 5.1

ChinaSouthern

ChinaEastern

Air ChinaAirAsiaGroup

All NipponAirways

IndigoJapanAirlines

GarudaIndonesia

CathayPacific

SingaporeAirlines

CebuPacific

THAIChinaAirlines

PhilippineAirlines

Tigerair

*includes AirAsia X

FROM ASEAN TO ASIAAssociate Structure

AirAsia INDIA (Associate Co - 49% owned)

• Population base: 1.3b

• Years in Operation : 2

MALAYSIA AirAsia• Population base: 32m

• Years in Operation: 15

• Listed on Bursa Malaysia (AirAsia Bhd)

THAI AirAsia (Associate Co - 45% owned)• Population base: 68m

• Years in Operation: 12

• Listed on SET under Asia Aviation PCL

INDONESIA AirAsia (Associate Co - 49% owned)• Population base: 261m

• Years in Operation : 12

PHILIPPINES AirAsia (Associate Co - 40% owned)

• Population base: 102m

• Years in Operation : 4

AirAsia JAPAN (Associate Co - 49% owned)

• Population base: 126m

• Years in Operation : To start in 2017

Note: AirAsia Berhad owns 13% of AirAsia X Berhad (long-haul operations) which is listed on

Bursa Malaysia 23

Single ClassOne Class Configuration

Same specification on all aircraft

Point to Point Point to point routes

Single Aircraft

Type

All Airbus A320 (AirAsia)

Single pool of professionals training, spare parts inventory,

tools

Modern & Efficient

Fleet with Good

Maintenance

Young fleet with average age of 5 yrs

Sharklets (4% more fuel efficient) A320neo (15%)

Long term engine programme with GE

Operational

Excellence25 minutes turnaround time (AirAsia)

Interest

Rate Low interest rate on all aircraft financing

PeopleNo Unions

High productivity and deep management

High Aircraft

Utilisation12.5 hours a day (AirAsia)

Low Distribution Cost 70% sales via internet

Favorable termsDiscount on aircraft and engine purchase

Tax incentives on purchase of aircraft

Economies of scale Cost Savings among AOC when operating same destination

Simplified Model No dedicated cargo fleet, catering, MRO, etc.

THE AIRASIA BUSINESS MODEL

24

Network• 125 destinations

• 27 countries

• 258 routes

• 60 unique routes

• 28 new routes

introduced in 2016

• 5 new routes

introduced so far in

2017

Allstars• 16,067k

Allstars

comprising

44

nationalities

Key Milestones• Voted The World’s Best Low-

Cost Airline for the eighth

consecutive year (Skytrax

World Airline Awards 2016)

• Voted Asia’s Leading Cabin

Crew (World Travel Awards)

• Largest LCC in Asia – 57 million

guests carried in 2016

174 Airbus A320’s

AirAsia Malaysia– 77 (+2 leased to PIA)

AirAsia Thailand - 51

AirAsia Indonesia – 22 (+5 A320 under IAAX)

AirAsia Philippines - 14

AirAsia India - 8

AirAsia Japan- 2

21 hubs

5 : KUL, JHB, BKI, KCH, PEN

6 : DMK, HKT, CNX, KBV, UTP, HDY

4 : CGK, SUB, KNO, DPS

3 : MNL, CEB, KLO

2 : BLR, DEL

1 : NGO

25

4Q16 load factor

87%

82%

83%

85%

86%

Market ShareDOM INT

Malaysia 48% 45%

Thailand 29% 14%

Indonesia 3% 24%

Philippines 13% 5%

India 2% 3%

-

Aircraft as of 28h Feb ’17. Network as of Dec ’16. Allstars as of Dec’ 16. Market share as of Dec’ 2016.

AIRASIA – FACTS AT A GLANCE

UNDERSERVED MARKETFOR ASEAN, INDIA, CHINA & THE REST OF ASIA

Source: World Bank, IEMS, Kharas and Gertz, 2010

North America

pop. 357 mil.

2.5 flights per capita

European Union

pop. 509 mil.

1.3 flights per capitaASEAN +2

pop. 3.3 billion

0.3 flights per capita

2009 2020 2030

Rest of World

North America & Europe

Asia-Pacific

Expanding global middle class

28% 54% 66%

26

Note: All provided figures based on latest reported quarter of4QCY16, unless otherwise stated.1 Malaysia Airlines figures based on the latest available auditedfinancial statement as at 31 December 20132 Nok Air figures based on latest reported financials for FY20163 Garuda Indonesia figures based on latest reported financials for9M16

COST ADVANTAGE OVER PEERSAirAsia

Malaysia

Malaysia

Airlines1 Ryanair AirAsia

ThailandNok Air2

Staff costs 0.66 0.97 0.44 0.67 0.86

Depreciation 0.28 0.36 0.36 0.17 0.04

Aircraft fuel expenses 0.93 2.44 1.29 1.14 1.24

Aircraft operating lease expense 0.05 0.48 0.06 0.66 1.63

Maintenance and overhaul 0.16 0.84 0.11 0.37 1.74

User charges and related expenses 0.54 0.56 1.06 0.71 0.71

Other operating expenses 0.18 0.55 0.22 0.26 0.84

Finance costs 0.20 0.18 0.04 0.07 0.05

Finance income (0.12) (0.05) 0.00 (0.02) (0.02)

Other income (0.21) (0.24) (0.00) (0.03) (0.29)

ASK (million) 10,275 14,983 37,236 5,208 1,566

CASK (US cents) 2.67 6.09 3.59 4.00 6.82

AirAsia

Indonesia

Garuda

Indonesia3AirAsia

Philippines

Cebu

Pacific

AirAsia

IndiaIndiGo

Staff costs 0.43 0.24 0.69 0.37 0.70 0.54

Depreciation 0.06 0.11 0.08 0.50 0.02 0.12

Aircraft fuel expenses 1.06 1.84 1.28 1.61 1.06 1.72

Aircraft operating lease expense 0.60 1.50 0.63 0.33 0.35 0.84

Maintenance and overhaul 0.47 0.63 0.88 0.47 0.32 0.15

User charges and related expenses 0.63 1.04 0.47 0.53 0.59 0.52

Other operating expenses 0.19 0.97 0.48 0.12 0.23 0.69

Finance costs 0.09 0.12 0.08 0.09 0.14 0.08

Finance income - (0.01) 0.00 -0.01 -0.07 -

Other income (0.08) (0.07) 0.56 0.00 -0.08 (0.18)

ASK (million) 2,661 14,638 1,473 6,399 990 14,390

CASK (US cents) 3.45 6.37 5.15 4.02 3.26 4.48

Cost reduction initiatives

- New A320neo & A321neo

• Added 5 A320neo in 2016 and a further 17 planned for 2017

• A321neo to be introduced in 2019

• 15% - 20% fuel burn reduction

- Fuel saving

• One engine taxi

• Required Navigation Performance

• Engine wash & tyre pressure check

- Innovation

• Self Bag drop & e-boarding pass

• Enhanced mobile and web booking

• Digitalisation and One AirAsia

- Others

• Renegotiating lower airport charges

AirAsia X Berhad Tune Protect Group Berhad

• Est Valuation: RM 234m (Our Stake 13.76%)

• FY2016 vs FY2015Rev: RM4.0b (+31%)Net Op Profit: RM250.9m (vs net op. loss - RM101.7mil)PAT: RM230.5m vs LAT -RM349.6m

• Est Valuation: RM 149m(Our Stake: 13.65%)

• FY2016 vs FY2015: Rev: RM126.08mPAT: RM15.34m

roKKi.com

• Est Valuation: RM 29m(Our Stake: 73%)

• FY2016 vs FY2015: Rev RM22m (-18%)PAT RM2.6m (+392.5%)Margins: EBIT = 12.8%, EBITDAR = 12.8%

BIG Loyalty

• Est Valuation: RM 292m(Our stake: 69.33%)

• FY2016 vs FY2015: Rev RM50.4m (+37%)LAT –RM10.3m (vs -RM15.5m)

• Active members increased to 5.5m from 31.m.

Asian Aviation Centre of Excellence

• Est Valuation: RM 355m(Our Stake 50%)

• FY2016 vs FY2015: Rev RM130.7m (+21%)EBITDA RM78.9m (+22%)PAT RM48.6m (+46% against budget)Margins: EBIT 44%, EBITDA 60%10 Full Flight Simulators (FFS)

AirAsia Expedia

• Est Valuation: RM 354m(Our Stake 25%)

• FY2016 vs FY2015 Rev USD208.9m (+30%)PAT USD27.8m (+35%)Margins: EBIT 13.9% EBITDAR 14.2%

T & Co.

• Est Valuation: RM 914k (Our stake: 80%)

• FY2016 vs FY2015:Rev RM3.1m (+12%)

INVESTMENTS WORTH RM5.8 BILLION

Asia Aviation Capital

• Est Valuation: RM 4.5 bil• (Our Stake 100%)• FY2016 vs FY2015:

Revenue: US223.96m ( +140%)EBITDAR: USD57.2mPAT: USD70.9m (+515%)Normalised Profit Margin for

4Q2016: EBIT 27% Total acft:63

28

PRIVATE EQUITY PERFORMANCE FY2016

2017 FLEET STATISTICS

[1] Includes aircraft operating under IAAX flight code

Owned Op. Lease Owned Op. Lease Owned Op. Lease

Malaysia 2 2 71 2 - - 7

Thailand 12 16 2 - 16 5 6

Indonesia1 9 7 - - 5 1 2

Philippines 2 6 2 - - 4 3

India 2 1 5 - - - 6

Japan - 2 - - - - 3

Pakisan 2 - - - - - -

TOTAL 29 34 80 2 21 10 27

Net

growth in

2017

OperatorAAC MAA TAA / IAA / PAA

29

5

29

DURABLE COMPETITIVE ADVANTAGECURRENCY, HEDGING & COST

USD borrowings Associates' a/c,natural hedged

MAA a/cunhedged

MAA a/c hedged

Only 35% of

USD

borrowings

is totally

unhedged:

35%

50%

• Loans by currency: USD (90%), MYR (7%), SGD (2%) and EUR (1%)

15%

Bought planes at low cost. Negotiated best prices for

aircraft by ordering early and ordering big.

Fixed interest rates. All loans are either fixed rate

loans or have fixed interest rates via interest rate

swaps.

Most of fuel for 2017 is fixed. Hedged 75% of FY2017 fuel requirements at

USD59 per barrel.

Currency hedges. USD operating expenditure 50% hedged up to May 2017.

Able to pass on currency risk to passengers via increasing average fare.

30

OUR PERFORMING ASEAN AIRLINES FULL YEAR 2016 RESULTS

Malaysia Thailand Indonesia Philippines

+10% +10%+18%

Malaysia Thailand Indonesia Philippines

REVENUE

RM6.92

bilTHB32.5

bil

IDR3,854

bilPHP10.8

bil

Malaysia Thailand Indonesia Philippines

OPERATING

PROFIT +29%+35%

+125%Reduced

operating loss to 188%1

RM2.05

bil

THB3.8

bilIDR190

bil

-PHP0.9 bil2

planned capacity

reduction

1 Reported2 Less one-off charges

31

4Q2016 SEGMENT PERFORMANCEAIRASIA GROUP: PRO-FORMA CONSOLIDATED RESULTS

-23%

Elimination

Malaysia Thailand Indonesia Philippines India Japan Adjustments Total

RM'000 RM'000 RM'000 RM'000 RM'000 RM'000 RM'000 RM'000

Segment results

Revenue 1,936,769 933,122 318,813 276,280 174,412 - (401,048) 3,238,348

Operating expenses - - - - - - -

- Staff costs (314,032) (152,818) (50,148) (44,595) (30,460) (17,567) - (609,619)

- Depreciation of property, plant and equipment (192,431) (38,085) (7,359) (5,207) (985) 634 - (243,432)

- Aircraft fuel expenses (420,484) (261,671) (83,832) (82,922) (69,128) (1,622) - (919,659)

- Maintenance and overhaul (72,369) (85,754) (48,104) (56,850) (18,926) (1,775) 126,489 (157,290)

- User charges and other related expenses (245,473) (161,704) (63,949) (30,263) (24,669) (4,504) - (530,562)

- Aircraft operating lease expenses (135,519) (151,463) (47,165) (40,563) (29,689) (8,264) 271,798 (140,865)

- Other operating expenses (109,570) (60,110) (22,175) (30,675) (10,885) (5,622) 18,500 (220,538)

Other income 143,549 6,857 33,642 (36,442) 3,706 59 (15,739) 135,633

Operating profit/(loss) 590,440 28,375 29,723 (51,236) (6,625) (38,661) 0 552,016

Finance income 80,940 3,693 399 14 919 0 - 85,964

Finance costs (126,792) (16,473) (11,257) (4,886) (111) (16) - (159,535)

Net operating profit/(loss) 544,588 15,594 18,866 (56,108) (5,817) (38,677) 0 478,446

Foreign exchange (losses)/gains 54,120 (17,857) (95,285) (68,981) (4,063) (4,117) - (136,184)

Impairment of investment in associate (163,750) - - - - - - (163,750)

Share of results of joint ventures 6,108 - - - - - - 6,108

Share of results of associates (91,870) - - - - - 103,985 12,115

Profit/(loss) before taxation 349,196 (2,263) (76,420) (125,089) (9,881) (42,794) 103,985 196,735

32

AIRASIA BERHAD: 4Q16 and FY2016 PERFORMANCEAIRASIA MALAYSIA: INCOME STATEMENT AND PERFORMANCE INDICATORS

4Q15 4Q16

MRF adj. +0.12+0.11 1.94

REVENUE(RM billion)

Passenger

seat sales

Other

revenue

Topline revenue declined year-on-year due to recognition of one-off Maintenance

Reserve Fund (MRF) adjustment in 4Q15 of RM457 million. Leaving out the one-off gain,

revenue increased by 15%.

NET OPERATING

PROFIT (RM million)

EBITDAR

MARGIN

EBIT

MARGINLOAD

FACTORAVERAGE

FARE

47% 30%

4Q16

87%(+2 ppts)

544.6

724.5RM186

(+5%)

Total passengers carried at 6.76 mil for 4Q16, up 5%, exceeding capacity growth of 2%

year-on-year.

Net Operating Profit down 25% by due to payout of staff bonuses and wet-lease

charges

Ancillary income per passenger of RM47.

4Q16

1.71

0.46

4Q15 4Q16

-25%

33

157

90

4Q15 4Q16

Operating Profit

1,091971

4Q15 4Q16

Revenue

34

4Q16 – ASSOCIATES’ PERFORMANCE

AIRASIA THAILAND (THB MIL)

7,678 7,559

4Q15 4Q16

Revenue

585

229

4Q15 4Q16

Operating profit

-2%

-61%

Revenue held steady at THB7.56

bil. Lower operating profit from

tour operator crackdown and

national mourning period

AIRASIA INDONESIA (IDR BIL)

-11%

-43%

Revenue 11% lower due to planned

capacity reduction as part of the

turnaround plan

Load factor up 3 ppts to 83%.

CASK down by 25%

Second consecutive profitable

quarter with operating profit of

IDR90.6 million

-110

-576

Operating loss

35

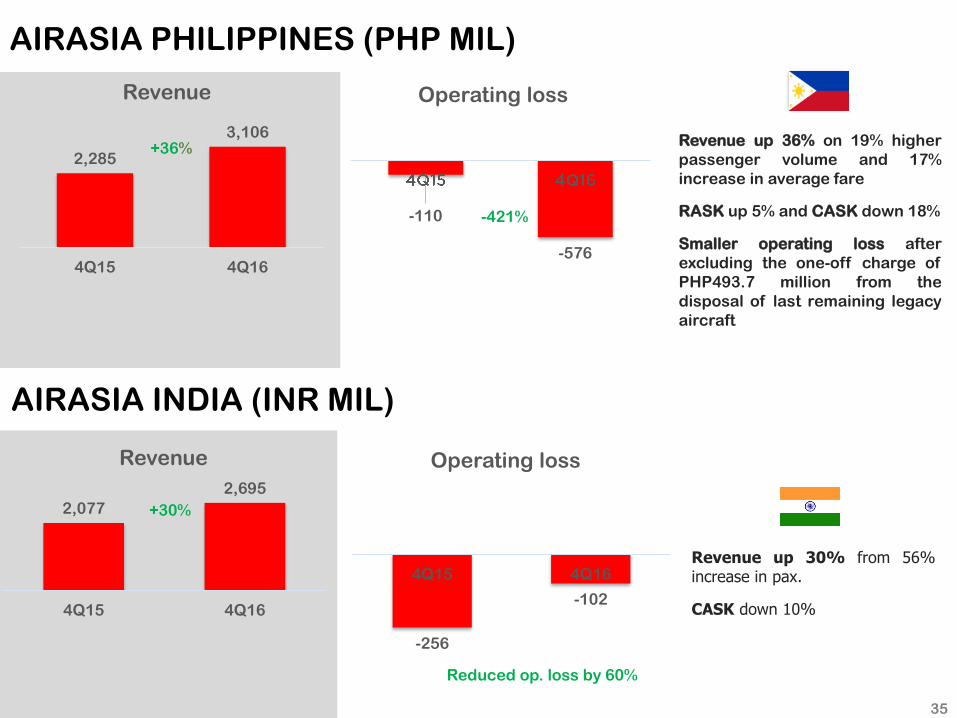

AIRASIA INDIA (INR MIL)

2,077

2,695

4Q15 4Q16

Revenue

-256

-102

4Q15 4Q16

Operating loss

+30%

Reduced op. loss by 60%

Revenue up 30% from 56%increase in pax.

CASK down 10%

2,285

3,106

4Q15 4Q16

Revenue

+36%

-421%

Revenue up 36% on 19% higher

passenger volume and 17%

increase in average fare

RASK up 5% and CASK down 18%

Smaller operating loss after

excluding the one-off charge of

PHP493.7 million from the

disposal of last remaining legacy

aircraft

AIRASIA PHILIPPINES (PHP MIL)