credit suisse: capital structure & legal entity transformation · low-trigger capital...

TRANSCRIPT

Credit Suisse: Capital Structure & Legal Entity

Transformation

2016 Credit Suisse European Banks Conference

David Mathers, Chief Financial Officer

London, March 3, 2016

Disclaimer

March 3, 2016

Cautionary statement regarding forward-looking statements

This presentation contains forward-looking statements that involve inherent risks and uncertainties, and we might not be able to achieve the predictions, forecasts, projections and other outcomes we describe or imply in forward-looking statements. A number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions we express in

these forward-looking statements, including those we identify in "Risk Factors" in our Annual Report on Form 20-F for the fiscal year ended December 31, 2014 and in "Cautionary statement regarding forward-looking information" in our fourth quarter earnings release 2015 filed with the US Securities and Exchange Commission, and in other public filings and press releases. We do not intend to update

these forward-looking statements except as may be required by applicable law.

We may not achieve the benefits of our strategic initiatives

We may not achieve all of the expected benefits of our strategic initiatives. Factors beyond our control, including but not limited to the market and economic conditions, changes in laws, rules or

regulations and other challenges discussed in our public filings, could limit our ability to achieve some or all of the expected benefits of these initiatives.

Statement regarding purpose and basis of presentation

This presentation contains certain historical information that has been re-segmented to approximate what our results under our new structure would have been, had it been in place from January 1, 2014.

In addition, "Illustrative,“ “Ambition” and “Goal” presentations are not intended to be viewed as targets or projections, nor are they considered to be Key Performance Indicators. All such presentations are subject to a large number of inherent risks, assumptions and uncertainties, many of which are outside of our control. Accordingly, this information should not be relied on for any purpose. In preparing this

presentation, management has made estimates and assumptions which affect the reported numbers. Actual results may differ. Figures throughout presentation may also be subject to rounding

adjustments.

Statement regarding capital, liquidity and leverage

As of January 1, 2013, Basel 3 was implemented in Switzerland along with the Swiss “Too Big to Fail” legislation and regulations thereunder. As of January 1, 2015, the Bank for International

Settlements (BIS) leverage ratio framework, as issued by the Basel Committee on Banking Supervision (BCBS), was implemented in Switzerland by FINMA. Our related disclosures are in accordance with

our interpretation of such requirements, including relevant assumptions. Changes in the interpretation of these requirements in Switzerland or in any of our assumptions or estimates could result in different numbers from those shown in this presentation. Capital and ratio numbers for periods prior to 2013 are based on estimates, which are calculated as if the Basel 3 framework had been in place in Switzerland during such periods. Unless otherwise noted, leverage exposure is based on the BIS leverage ratio framework and consists of period-end balance sheet assets and prescribed regulatory adjustments. Leverage amounts for 4Q14, which are presented in order to show meaningful comparative information, are based on estimates which are calculated as if the BIS leverage ratio framework

had been implemented in Switzerland at such time. Beginning in 2015, the Swiss leverage ratio is calculated as Swiss total capital, divided by period-end leverage exposure. The look-through BIS tier 1

leverage ratio and CET1 leverage ratio are calculated as look-through BIS tier 1 capital and CET1 capital, respectively, divided by end-period leverage exposure.

Cautionary statement regarding this presentation

This presentation does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire securities of Credit Suisse Group AG or Credit Suisse AG (together, the “Company”) in any jurisdiction or an inducement to enter into investment activity. No part of this document, nor the fact of its distribution, should form the basis of, or be relied on

in connection with, any contract or commitment or investment decision whatsoever. No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or the opinions contained herein. None of the Company or any of its affiliates, advisors or representatives shall have any liability

whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with the document.

2

Agenda 2016 Credit Suisse European Banks Conference

March 3, 2016 3

Agenda 1. Existing Credit Suisse Capital Instruments

2. Draft New Swiss TBTF Rules and TLAC

3. Q&A Session

2019

2020

2010

TBTF development since 2010

March 3, 2016 4

Final Swiss TBTF report

from

Commission

of Experts (Group

“Siegenthaler”)

2011

2012

2013

2014

2015

2016

Entry into force of

TBTF

legislation

Development from initial Swiss discussion to revised Swiss TBTF rules

FSB consultative document on

TLAC published

Group of Experts (Brunetti Commission) publishes proposals for amendments to

initial Swiss TBTF regime

Expected entry into force of revised Swiss TBTF rules (2H16)

Final FSB TLAC

rules published

Federal Council adopts revised

TBTF regulation

End of phase-in for initial Swiss

TBTF rules

Proposed end of phase-in for

revised Swiss

TBTF rules

Low-

trigger

write-down issuances

Further low-trigger write-down issuance

Initial

TLAC

bonds

issuance

Public

high-

trigger

Tier 2 convertible issuances

Q&O

exchange

into high-trigger AT1 instruments

TBTF = Too Big to Fail. FSB = Financial Stability Board. TLAC = Total loss-absorbing capacity. Q&O = Qatar Investment Authority and The Olayan Group.

Public consultation on revised Swiss TBTF rules (December 2015 to February 2016)

Further high-trigger

issuances

Credit Suisse capital instrument philosophy

March 3, 2016 5

Design and implementation have been driven by the differentiation between concepts of going and gone concern capital

− Generally, equity and high-trigger capital instruments are considered going concern, while low-trigger

capital instruments are considered gone concern

Credit Suisse has favored equity conversion structures for high-trigger capital instruments in order to provide recovery value and preserve equity subordination

− Have a preference for high-trigger conversion formats, but may also look to issue high-trigger write-down instruments (also aligns with employee Contingent Capital Awards)

Low-trigger capital instruments were generally viewed as gone concern capital, given the likely limited

recovery value at the specified trigger point. As such, all low-trigger capital instruments have been issued

with write-down structures

− Note that the revised TBTF rules do not require any trigger-based gone concern capital

We have designed our issuance structure in coordination with the rules to align various stakeholder groups:

− Dividend stopper aligns the interests of equity and AT1 investors

− High-trigger write-down AT1 employee Contingent Capital Awards aligns the interests of employees with fixed income investors

Gone

Concern

Going

Concern

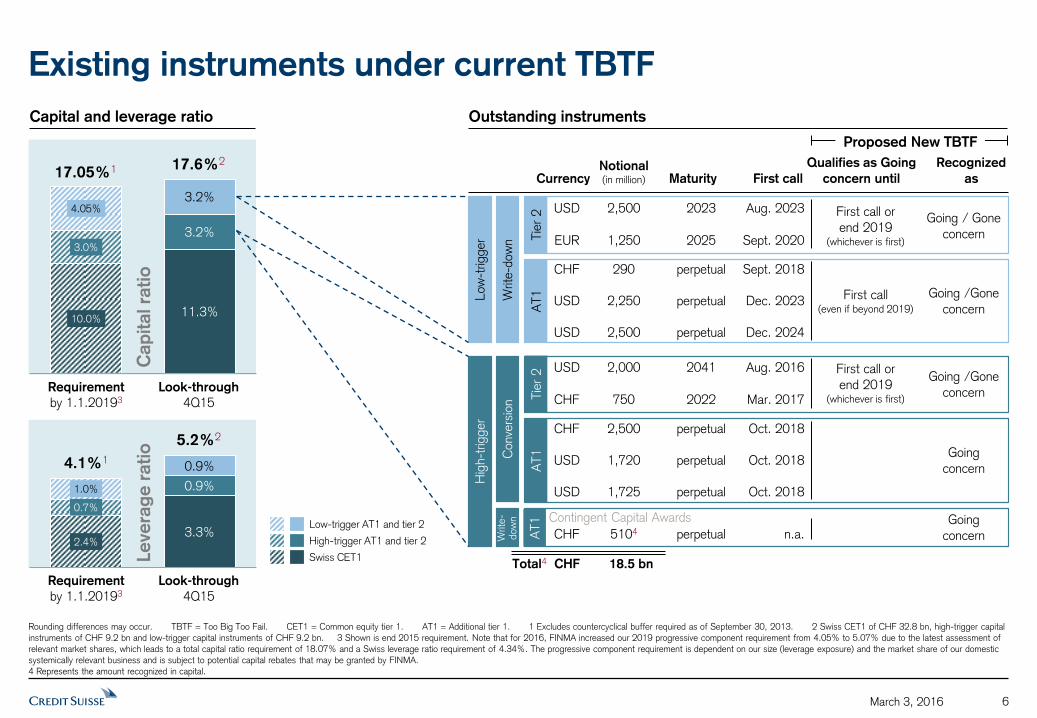

Existing instruments under current TBTF

March 3, 2016 6

10.0% 11.3%

3.0%

3.2%

4.05% 3.2%

17.05%1

Le

vera

ge

rati

o

Capital and leverage ratio

Rounding differences may occur. TBTF = Too Big Too Fail. CET1 = Common equity tier 1. AT1 = Additional tier 1. 1 Excludes countercyclical buffer required as of September 30, 2013. 2 Swiss CET1 of CHF 32.8 bn, high-trigger capital

instruments of CHF 9.2 bn and low-trigger capital instruments of CHF 9.2 bn. 3 Shown is end 2015 requirement. Note that for 2016, FINMA increased our 2019 progressive component requirement from 4.05% to 5.07% due to the latest assessment of

relevant market shares, which leads to a total capital ratio requirement of 18.07% and a Swiss leverage ratio requirement of 4.34%. The progressive component requirement is dependent on our size (leverage exposure) and the market share of our domestic

systemically relevant business and is subject to potential capital rebates that may be granted by FINMA.

4 Represents the amount recognized in capital.

17.6%2

Outstanding instruments

USD 2,500 2023 Aug. 2023

Going / Gone

concern

Currency Notional (in million) Maturity First call

Recognized

as

First call or

end 2019 (whichever is first)

Qualifies as Going

concern until

Proposed New TBTF

Low

-trig

ger T

ier

2

AT1

EUR 1,250 2025 Sept. 2020

CHF 290 perpetual Sept. 2018

Going /Gone

concern First call

(even if beyond 2019) USD 2,250 perpetual Dec. 2023

USD 2,500 perpetual Dec. 2024

USD 2,000 2041 Aug. 2016 First call or

end 2019 (whichever is first)

Hig

h-t

rigger

Tie

r 2

A

T1

CHF 750 2022 Mar. 2017

CHF 2,500 perpetual Oct. 2018

Going

concern USD 1,720 perpetual Oct. 2018

USD 1,725 perpetual Oct. 2018

Going /Gone

concern

Cap

ital ra

tio

Swiss CET1

High-trigger AT1 and tier 2

Low-trigger AT1 and tier 2

Write

-dow

n

Conve

rsio

n

AT1

CHF 5104 perpetual n.a. Going

concern Writ

e-

dow

n Contingent Capital Awards

4.1%1

5.2%2

2.4% 3.3%

0.7%

0.9% 1.0%

0.9%

Requirement

by 1.1.20193

Look-through

4Q15

Requirement

by 1.1.20193

Look-through

4Q15

Total4 CHF 18.5 bn

CET1

capital 4Q15

7 March 3, 2016

14.3% 42.1

20.6

CHF

21.4 bn CET1 buffer1

4Q151

CET1

capital ratio

Note: For presentation purposes the CET1 buffer for the 5.125% low-trigger capital instrument is not shown. Rounding differences may occur. CET1 = Common equity Tier 1. 1 Based on year-end 2015 phase-in risk-weighted

assets of CHF 295 bn. 2 Conversion into equity upon Credit Suisse Group AG’s (the “Group”) reported phase-in CET1 ratio falling below 7%, or a determination by FINMA that conversion is necessary, or that the Group requires public sector capital

support, to prevent it from becoming insolvent, bankrupt or unable to pay a material amount of debts, or other similar circumstances. 3 The principal amount of the instrument would be written-down to zero and canceled if the following trigger events were

to occur: A) the Group’s reported phase-in CET1 ratio falls below 5%; or B) FINMA determines that cancellation of the instrument and other similar contingent capital instruments is necessary, or that the Group requires public sector capital support, in either

case to prevent it from becoming insolvent or otherwise failing (“Customary Non-Viability Scenarios”). 4 Assumes the full application of a five-year (20% per annum) phase-in of goodwill, other intangible assets and other capital deductions (e.g., certain

deferred tax assets) and the phase-out of an adjustment for the accounting treatment of pension plans and certain capital instruments. 5 Based on year-end 2015 look-though risk-weighted assets of CHF 290 bn. 6 Based on year-end 2018 look-

though RWA target of CHF 315 bn.

Conversion

trigger2

CET1 capital

at conversion trigger

Phase-in BIS CET1 ratio and capital in CHF bn

7.0%

Look-through impact4:

Assuming CET1 capital ratio of 11.4%5 (as of end 4Q15)

CHF

12.6 bn CET1 buffer

14.7

Write-down

trigger3

5.0%

CET1 capital

at write-down trigger

CHF

27.3 bn CET1 buffer1

7.0%

CHF

18.4 bn CET1 buffer

5.0%

Assuming a targeted CET1 capital ratio

of 13%6 (as end 2018 target)

CHF

18.9 bn CET1 buffer

7.0%

CHF

25.2 bn CET1 buffer

5.0%

Large capital buffer to capital instrument triggers

Strong capacity for AT1 coupon payments Credit Suisse has been a consistent dividend payer, not only throughout the financial crisis but since the bank was

founded in 1856

March 3, 2016 8

Recent market volatility in USD low-trigger AT1 capital instruments

Price (%)

70

80

90

100

110

Aug 15 Okt 15 Dez 15 Feb 16

CS

UBS

DB

Aug 15 Oct 15 Dec 15 Feb 16

Source: Bloomberg. “Distributable Profits” = aggregate of i) net profits carried forward and ii) freely available reserves (other than reserves for own shares), in each case, less any amounts that must be contributed to legal reserves under applicable law, all

as appearing in the Relevant Accounts (i.e., the audited unconsolidated financial statements of the issuer for the previous financial year). 1 As of the end of 2014, the distributable profits of Credit Suisse Group AG, under the terms of our capital

instruments, consisted of retained earnings brought forward of CHF 5.2 bn and free reserves of CHF 10.5 bn.

Credit Suisse will be prohibited from making any AT1 interest payment if:

– Distributable profits are less than the aggregate amount of AT1 interest payments

– FINMA prohibited such interest payment

– Minimum regulatory requirements are not met

Distributable profits1 of CHF 15.7 bn Provides significant coverage for AT1 coupon payments of ~CHF 1bn (2016)

AT1 instruments include a contractual dividend stopper (unlike EU under CRD4)

Agenda 2016 Credit Suisse European Banks Conference

March 3, 2016 9

1. Existing Credit Suisse Capital Instruments

2. Draft New Swiss TBTF Rules and TLAC

Agenda

3. Q&A Session

Expected key changes of new Swiss TBTF capital requirements

March 3, 2016 10

Formalization of FSB

TLAC proposals

Streamlining of capital

instruments into only

high-trigger AT1

Extensive

grandfathering

proposals for existing high-trigger Tier 2 and

low-trigger capital Recalibration of the

leverage regime and

associated RWA

requirements

Swiss law

requirements for TLAC

Withholding tax

exemption

Key

Changes

FSB = Financial Stability Board. TLAC = Total loss-absorbing capacity.

Proposed new Swiss TBTF capital requirements

March 3, 2016 11

TBTF = Too Big to Fail. SIBs = Systemically important banks. CET1 = Common Equity Tier 1. AT1 = Additional Tier 1. 1 In percentage of leverage exposure. 2 In percentage of risk-weighted assets (RWA). 3 Based on year-end

2015 look-through Swiss leverage exposure of CHF 988 bn. 4 Based on year-end 2015 look-through Swiss RWA of CHF 291 bn. 5 Including CHF 15.0 bn of senior unsecured HoldCo debt and CHF 4.1 bn of low-trigger Tier 2 capital instruments.

6 Based on end-2018 leverage exposure target of CHF 1,000 bn. 7 Based on end-2018 RWA target of CHF 315 bn. Note: On December 22, 2015, the Swiss Federal Council published the planned ordinance amendments to the Swiss TBTF regime,

which will be phased in by the end of 2019. It is expected that draft ordinances implementing this new framework into Swiss law will be approved by the Swiss Federal Council in 2Q16 and implemented shortly thereafter. Note: Going concern adequacy

ratios dependent on size (leverage ratio exposure) and market share of our domestic systemically relevant business and is subject to potential capital rebates that may be granted by FINMA.

Capital adequacy ratios, Swiss look-through

Requirements

by 1.1.2020

Credit Suisse

end 4Q153

Going concern

Gone concern

Leverage ratio1

6.7%

10.0%

Requirements

by 1.1.2020

Credit Suisse

end 4Q154

Capital ratio2

22.8%

28.6%

1.9%

1.5%

3.3%

5.0%

1.5%

3.5%

6.6%

4.9%

11.3%

14.3%

4.3%

10.0%

CET1

High-trigger AT1

(incl. high-trigger Tier 2 and

low-trigger Tier 1)

Bail-in instruments

(incl. low-trigger Tier 2)

Bail-in shortfall:

~ CHF 30 bn

Bail-in (TLAC) shortfall:

Based on 4Q15 leverage exposure and RWA, the

look-through gone concern5 shortfall is:

– ~ CHF 30 bn on a leverage basis3

– ~ CHF 22 bn on an RWA basis4

Based on end-2018 leverage exposure and RWA

targets, the look-through gone concern5 shortfall

would be:

− ~ CHF 31 bn on a leverage basis6

− ~ CHF 26 bn on an RWA basis7

Bail-in shortfall:

~ CHF 22 bn

Leverage ratio requirement currently most

binding:

– determines optimal level of high-trigger AT1

– determines gone concern requirement

Capital instrument issuance requirements

March 3, 2016 12

CET1 = Common Equity Tier 1. AT1 = Additional Tier 1. 1 Based on year-end 2015 look-through Swiss leverage exposure of CHF 988 bn. 2 Including CHF 15.0 bn of senior unsecured HoldCo debt and CHF 4.1 bn of low-trigger Tier 2 capital

instruments. Note: On December 22, 2015, the Swiss Federal Council published the planned ordinance amendments to the Swiss TBTF regime, which will be phased in by the end of 2019. It is expected that draft ordinances implementing this new

framework into Swiss law will be approved by the Swiss Federal Council in 2Q16 and implemented shortly thereafter. Note: Going concern adequacy ratios dependent on size (leverage ratio exposure) and market share of our domestic systemically relevant

business and is subject to potential capital rebates that may be granted by FINMA.

Capital adequacy amounts, Swiss look-through in CHF bn

32.8 34.6

14.3 14.8

19.1

49.4

Requirements1

by 1.1.2020

Credit Suisse

end 4Q15

66.3

98.8

CET1

High-trigger AT1

(incl. high-trigger Tier 2 and

low-trigger Tier 1)

Bail-in instruments2

(incl. low-trigger Tier 2)

Through 2019 we will replace existing callable capital instruments with fully compliant going concern AT1 capital

We will replace a portion of maturing Bank (OpCo) instruments through 2019 with ~CHF 30 bn of TLAC instruments to reach our estimated gone concern requirement

Going concern

Gone concern

Shortfall

30.2

0.5

1.8

March 3, 2016 13

Designed to meet future requirements for global recovery and resolution planning

Possibility of limited reduction in capital requirements provided for under Swiss banking law if resolvability is improved

In support of FINMA’s “single point of entry” bail-in strategy we commenced issuing long-term senior debt from

Credit Suisse Group AG3 in 2015. We also expect to continue issuing long-term senior debt from Credit Suisse AG

Better aligns the booking of Investment Banking business on a regional basis, from a client and risk management perspective

Less complex and more efficient operating infrastructure for the bank

1 Org structure shows main operating entities only; This program has been approved by the Board of Directors of Credit Suisse Group AG, but is subject to final regulatory approval. Implementation of the program is well underway, with a number of key

components to be implemented through to 2017. 2 Proposed hub for Asia Pacific Investment Banking business in Singapore branch. 3 Funding may be issued either at the holding company level or at the level of an entity that will be substituted by the

holding company in a restructuring event. 4 Subject to US regulatory approvals, the US derivatives businesses, currently booked in London in Credit Suisse International, are anticipated to be transferred to the US broker-dealer. US Service Co activities will

also be housed here. 5 Credit Suisse is planning that its two principal UK operating subsidiaries (Credit Suisse Securities (Europe) Limited and Credit Suisse International) will be consolidated into one single subsidiary. 6 In Switzerland, Credit Suisse will

create a subsidiary for its Swiss-booked business (primarily wealth management, retail and corporate and institutional clients as well as the product and sales hub in Switzerland).

Go

als

US Holding Co4

Simplified view1

Funding Entity3

UK Subsidiary5

Credit Suisse AG Operating Bank with branches2

Credit Suisse Group AG Holding Company

Swiss Legal Entity6

Credit Suisse legal entity structure

Withholding tax

Paying agent principle to be refrained for now and tax exemption for bail-in bonds expected beginning of 2017

March 3, 2016 14

Bail-in debt – loss absorbency FSB Standard, but different national solutions

FSB: Subordination can have three forms:

Structural

1 Switzerland

HoldCo issuance United Kingdom

United States

Germany Subordination by law and retrospective outstanding bonds

France Contractual subordination plus new category of non-preferred debt instruments in insolvency law

Statutory

Contractual

3

2

FSB = Financial Stability Board.

Further solutions developing in Italy, Spain, Canada and other countries, which all fall into the broad categories listed above, but have nuanced national differences

March 3, 2016 15

Multiple “buffer” layers1 for senior creditors

42

33

9

9

9

9

Phase-in Look-through

61

CET1

High-trigger capital instruments3

Low-trigger capital instruments2

CET1 = Common equity tier 1. AT1 = Additional tier 1. RWA = Risk-weighted assets. 1 Basel 3 Credit Suisse Group AG consolidated figures. 2 Consists of CHF 5.1 bn additional tier 1 instruments and CHF 4.1 bn tier 2 instruments.

3 Consists of CHF 6.6 bn additional tier 1 instruments and CHF 2.7 bn tier 2 instruments. 4 Trigger of regulatory capital instruments with PONV conversion/write-down feature. 5 Bank Insolvency Ordinance (BIO-FINMA). References to phase-in

and look-through refer to Basel 3 capital requirements. Phase-in reflects that, for the years 2014 – 2018, there will be a five-year (20% per annum) phase-in of goodwill, other intangible assets and other capital deductions (e.g., certain deferred tax assets and

participations in financial institutions) and the phase-out of an adjustment for the accounting treatment of pension plans and, for the years 2013 – 2022, there will be a phase-out of certain capital instruments. Look-through assumes the full phase-in of goodwill

and other intangible assets and other regulatory adjustments and the phase-out of certain capital instruments.

51

Resolution (restructuring by FINMA)5

Poin

t of

non-v

iability

4

Bail-in hierarchy in Switzerland

as of 4Q15, in CHF bn

Common equity tier 1

Low-trigger AT1 capital instruments

High-trigger capital instruments

Common equity tier 1

Common equity tier 1

Loss

abso

rptio

n w

ate

rfall

Deposits, in so far as not privileged

AT1 and tier 2 instruments

Common equity tier 1

Low-trigger tier 2 capital instruments

Equity capital

Subordinated debt without capital adequacy eligibility (e.g. HoldCo senior unsecured bonds)

Other claims not excluded from conversion/write-down (e.g. OpCo senior unsecured bonds), with the exception of deposits

insofar as not converted/written-

off, prior to restructuring based on terms

< 5%

≤ 5.125%

≤ 7%

> 7%

between 7% and 5.125%

between 5.125% and 5%

≤ 5%

CET1/RWA levels:

Large capital buffers supporting senior creditors with clear

credit hierarchy

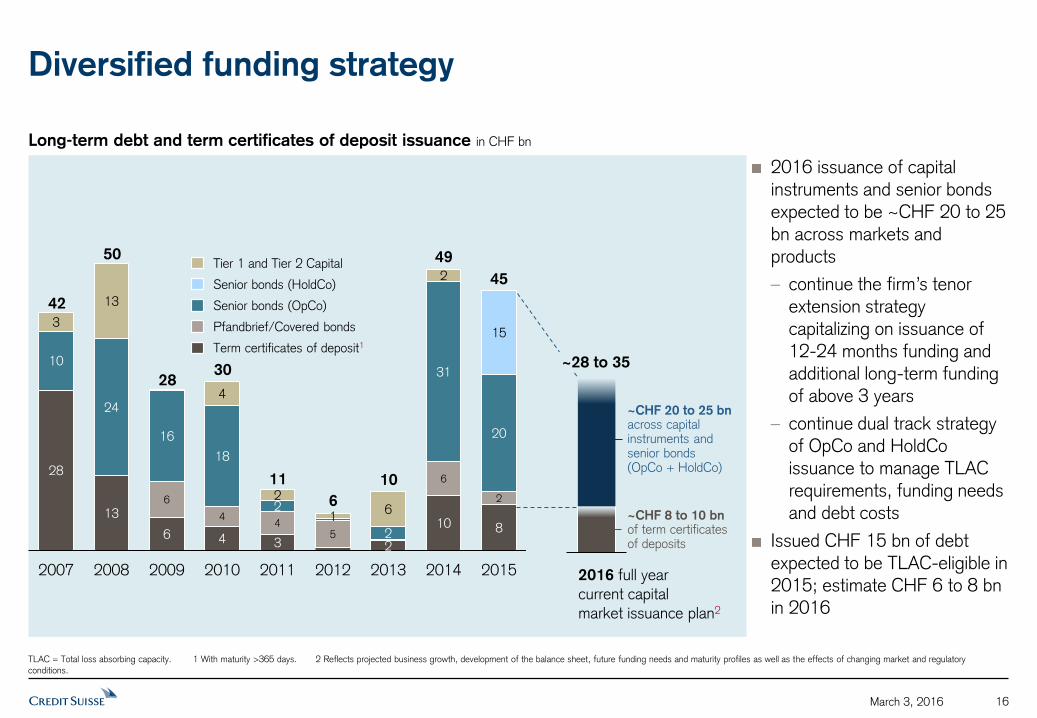

March 3, 2016 16

Long-term debt and term certificates of deposit issuance in CHF bn

TLAC = Total loss absorbing capacity. 1 With maturity >365 days. 2 Reflects projected business growth, development of the balance sheet, future funding needs and maturity profiles as well as the effects of changing market and regulatory

conditions.

2016 full year current capital market issuance plan2

~CHF 20 to 25 bn across capital instruments and senior bonds (OpCo + HoldCo) 28

13

6 4 3 2

10 8

6

4 4

5

6

2

10

24

16

18

2

2

31

20

15 3

13

4

2

1 6

2

2007 2008 2009 2010 2011 2012 2013 2014 2015

45

42

50

28 30

11

6

49 Tier 1 and Tier 2 Capital

Senior bonds (OpCo)

Pfandbrief/Covered bonds

Term certificates of deposit1

Senior bonds (HoldCo)

2016 issuance of capital instruments and senior bonds expected to be ~CHF 20 to 25 bn across markets and products

– continue the firm’s tenor extension strategy capitalizing on issuance of 12-24 months funding and additional long-term funding of above 3 years

– continue dual track strategy of OpCo and HoldCo issuance to manage TLAC requirements, funding needs and debt costs

Issued CHF 15 bn of debt expected to be TLAC-eligible in 2015; estimate CHF 6 to 8 bn in 2016

10

~CHF 8 to 10 bn of term certificates of deposits

~28 to 35

Diversified funding strategy

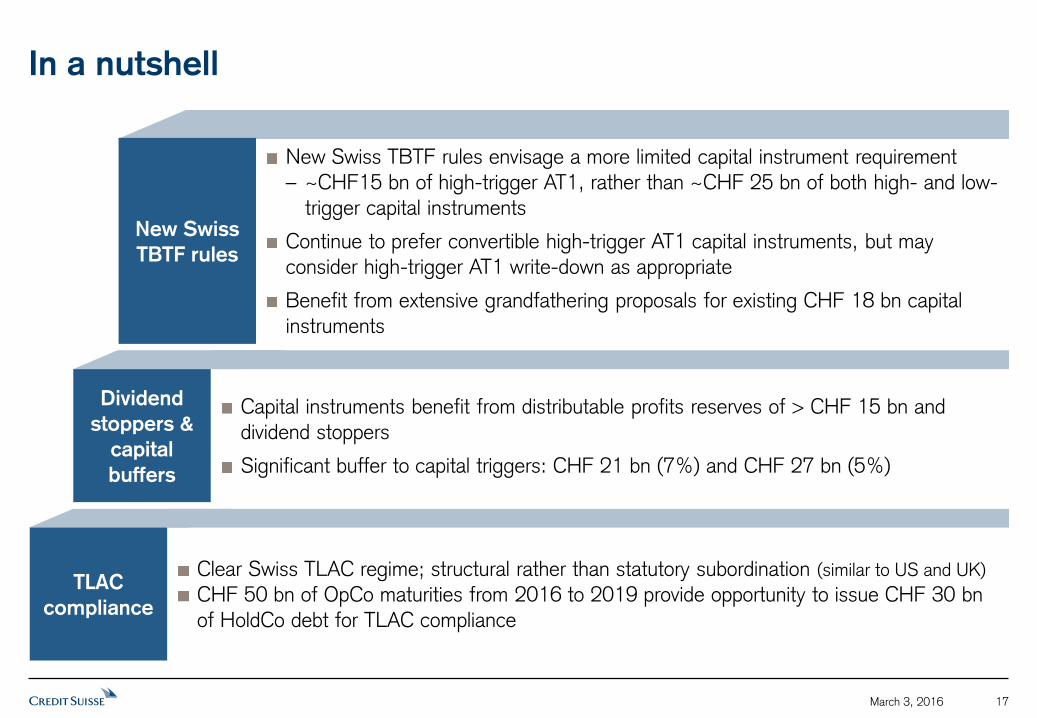

In a nutshell

March 3, 2016 17

Clear Swiss TLAC regime; structural rather than statutory subordination (similar to US and UK)

CHF 50 bn of OpCo maturities from 2016 to 2019 provide opportunity to issue CHF 30 bn

of HoldCo debt for TLAC compliance

TLAC

compliance

Capital instruments benefit from distributable profits reserves of > CHF 15 bn and

dividend stoppers

Significant buffer to capital triggers: CHF 21 bn (7%) and CHF 27 bn (5%)

Dividend

stoppers &

capital

buffers

New Swiss TBTF rules envisage a more limited capital instrument requirement

– ~CHF15 bn of high-trigger AT1, rather than ~CHF 25 bn of both high- and low-

trigger capital instruments

Continue to prefer convertible high-trigger AT1 capital instruments, but may

consider high-trigger AT1 write-down as appropriate

Benefit from extensive grandfathering proposals for existing CHF 18 bn capital

instruments

New Swiss

TBTF rules

Questions

?

March 3, 2016 18

Appendix

Down-streaming of HoldCo senior financing

March 3, 2016 20

CSG AG = Credit Suisse Group AG. CS AG = Credit Suisse AG TLAC = Total loss absorbing capacity. FSB = Financial Stability Board. HoldCo = Holding Company.

OpCo = Operating Company . 1 Funding may be issued either at the holding company level or at the level of an entity that will be substituted by the holding company in a restructuring event. Current funding entity: Credit Suisse Group Funding (Guernsey)

Ltd.

1 Funding entity issues senior unsecured notes (“Notes”) expected to qualify for FSB’s proposed TLAC rules by way of “structural subordination” and Swiss TBTF Gone concern capital

2 Notes are guaranteed by CSG AG. The guarantee is a traditional direct, unconditional, unsecured and unsubordinated contingent liability of CSG AG, thereby placing investors in an equivalent position against CSG AG as holding senior debt issued directly by CSG AG

3 The internal notes will be senior unsecured debt aligned to the external notes (maturity, interest rate and currency)

Proceeds

– Proceeds are down-streamed initially to CS AG, acting through a non-Swiss branch (“OpCo”) as unsecured notes

– Investors have no direct recourse to this intercompany instrument

Hierarchy

– HoldCo senior notes (external) structurally subordinated to OpCo liabilities

– Internal notes:

– subordinated to OpCo senior liabilities in restructuring

– pari passu with OpCo senior liabilities in liquidation

Guarantee

2

Credit Suisse AG Operating Bank

Credit Suisse

Group AG Holding Company

Investors

HoldCo senior notes (external)

Proceeds

Internal notes Proceeds

1

3

Funding entity1

Investors

OpCo senior liabilities

Proceeds 100%

100%