creditors and allowances - weebly · creditors control is credited and the individual creditor is...

TRANSCRIPT

Grade 10 Accounting Notes

SET 3:

CREDITORS

Name: ________________________

2

INTRODUCTION TO CREDITORS – GRADE 10 ACC PROBLEM SOLVING

Merri Stores has two creditors.

The balances at 1 Feb 2009 were as follows:

Moore Distributors R8 400

Moni Wholesales R4 200

Transactions for February 2009 …

5 Purchased trading stock, R1 200 and stationery, R 600 on credit from Moore Distributors.

8 Returned Trading stock, R200 and stationery, R50 to Moore Distributors.

19 Paid Moore Distributors R2 500 by cheque.

27 Settled our account with Moni Wholesales, and paid an amount of R4000 by cheque.

tot ret 250 bal 12600 crs 1200 crs 200 crs 600 crs 50

bank 2500 tot purch 1800

bk 4000

discrec200

bal 7450

14 400 14 400

bal 7450

Creditors Control Trading Stock Stationery

crs 2500 crs 200

crs 4000

Bank Disc Rec

Moore Distributors debit credit Balance Feb 1 Account Rendered b/d 8 400

5 Invoice CJ 1 800 10 200

8 Debit Note CAJ 250 9 950

19 Cheque counterfoil CPJ 2 500 7 450

Moni Distributors

Feb 1 Account Rendered b/d 4 200

27 Cheque counterfoil CPJ 4 000 200

Discount Received CPJ 200 -

3

CREDITORS AND ALLOWANCES

REVIEWING THE CREDITORS JOURNAL

The Creditors Journal A trader purchases stock and other items such as equipment for cash or on credit. Cash purchases are recorded in the CPJ if payment was made with a cheque or PCJ if petty cash funds were used. All credit purchases are recorded in the Creditors Journal (CJ). Any services acquired on credit (e.g. repairs) are also recorded in the CJ. The source document for credit purchases is an invoice, which he receives from his supplier. Credit purchases has the following effect: the item (e.g. trading stock) purchased is debited;

Creditors are credited. Creditors are liabilities (amounts owing to a trader) and increase on the credit side. The triple-entry principle applies:

Creditors control is credited and the individual creditor is credited in the Creditors Ledger.

Trade discounts This is a discount allowed by one dealer to another. Trade discounts are allowed for cash or credit purchases. The reasons for offering trade discounts vary from dealer to dealer. Some offer trade discounts to promote bulk buying; to clear obsolete or slow moving stock; to promote/reward customer loyalty; etc. The trade discount is calculated and subtracted from the invoice price - the dealer records the net amount. No entry is made for the trade discount. Trade discounts should not be confused with discounts that are granted for early settlement of accounts. Example: Bought trading stock on credit from Weaver Wholesalers for R500 less 10% trade discount. The amount recorded in the CJ is R450. The R50 trade discount is not reflected in the books.

WORKED EXAMPLE 1

4

5

WORKED EXAMPLE 2

6

RETURNS TO CREDITORS

(Creditors Allowances)

CREDITORS ALLOWANCES JOURNAL The dealer may have to return items due to inferior quality, damaged goods, etc. He may also claim an allowance on damaged goods or overcharges. Returns and allowances are recorded in the Creditors Allowances Journal (CAJ). The trader sends a Debit Note (DIN) to his supplier indicating the reasons for his claim. The supplier would issue a credit note (C/N) if he approves of the claim. The source document for entries in the CAJ is either the debit note issued or the credit note received. An example of a debit note is shown below:

The triple entry principle applies:

Creditors control is debited with the return/allowance - liabilities decrease; the trader now owes less

to the creditor. Creditors’ accounts in the Creditors Ledger are debited individually - less is now owed to the creditor. The item being returned (e.g. trading stock) or for which an allowance is made is credited - decrease in the respective item.

7

WORKED EXAMPLE 3

8

9

TRY THESE …

ACTIVITY 1 The following are some of the transactions of Sonja’s Cafe during June 2010. Required Record the following transactions in the correct columns, of Sonja’s Cafe for June 2010. Transactions 09 Bought merchandise on credit from Sparky & Co. R400. (Inv. X4) 10 Sonja’s Café complained to Sparky & Co. that the trade discount of R40 was not deducted

on the invoice issued on the 09th. Sent them D/N (J9) for this amount. 15 Received the equipment R1 200 and stationery R800 ordered on credit from Mako Supplies.

(lnv. B2) 17 Returned R150 worth of stationery to Mako Supplies as it was unsuitable. Issued a D/N.

(J10) 24 AIco Services undertook repairs to the refrigerators for Sonja’s Café R1 90.

Received a credit invoice from them. (Inv. V12)

ACTIVITY 1

SONJA’S CAFÉ

No Document Journal Acc Debit Acc Credit A = O + L 09 Invoice CJ Trading Stock Creditors Control +400 0 +400

10 Debit note CAJ Creditors Control Trading Stock -40 0 -40

15 Invoice CJ Equipment;

Creditors Control +1200 0 +1200

Stationery Creditors Control 0 -800 +2000 +800

17 Debit note CAJ Creditors Control Stationery 0 +150 -150

24 Invoice CJ Repairs Creditors Control 0 -190 +190

10

ACTIVITY 2 The following information was extracted from the accounting records of Molepo Stores (owner Mr L. Molepo). Record the transactions in the CJ and CAJ for September 2008. Use your own document numbers. Required 2.1 Provide for the following additional columns in both journals:

Trading stock; Equipment; Stationery 2.2 Post to the ledger (both the General and Creditors Ledger). 2.3 Extract a Creditors List on 30 September 2008. Information Creditors List on 31 August 2008:

Yeng Fui CC CL1 R12 450 Naidoo’s Cash & Carry CL2 14 570 Plop Wholesalers CL3 8 330

Balances/totals on 01 September 2008

Equipment R46 790 Trading stock 18 870 Creditors control ? Stationery 3 310

Transactions during September 2008 03 Bought the following on credit from Naidoo’s Cash & Carry:

stock R8 760; stationery R450 05 Bought trading stock on credit from Yeng Fui CC, R4 210. 06 Returned stock R390 and stationery R40 to Naidoo’s Cash & Carry as they were not up to

standard. Sent them a D/N. 11 Plop Wholesalers delivered stock that had been ordered on credit R3 450. 13 Took delivery of stock that was ordered on credit from Yeng Fui CC R1 980 (a 10% trade

discount has been deducted). 14 Some of the stock that had been delivered on the 11th was damaged during unloading. A

D/N for R380 was sent to the supplier. 15 Bought a new cash register from on credit from Naidoo’s Cash & Carry for R6 510 subject to

a trade discount of 33⅓%

16 Some of the stock that was bought on the 13th was stale. A D/N for R1 20 was sent to the supplier.

17 The sales staff informed the owner Mr Molepo that almost all of the stock purchased on the 11th was of sub-standard quality. Mr Molepo was furious - he sent all the stock back to the supplier together with a D/N.

24 Received a credit invoice from The Printshop for printing letterheads R220. 29 During an audit it was discovered that the addition of the invoice dated 3rd was incorrect.

The trading stock figure should have been R8 670 instead of R8 760. A D/N was delivered to them.

11

ACTIVITY 2 CJ9

Fol Details

1 3Naidoo's Cash and

Carry 9210 0 8760 0 450 0

2 5 Yeng Fui CC 4210 0 4210 0

3 11 Plop Wholesalers 3450 0 3450 0

4 13 Yeng Fui CC 1980 0 1980 0

5 15Naidoo's Cash and

Carry 4340 0 4340 0

6 24 The Printshop 220 0 220 0

23410 0 18400 0 4340 0 670 0

B3 B2 B1 N1

CAJ9

Fol Details

1 6Naidoo's Cash and

Carry 430 0 390 0 40 0

2 14 Plop Wholesalers 380 0 380 0

3 16 Yeng Fui CC 120 0 120 0

4 17 Plop Wholesalers 3070 0 3070 0

5 29

Naidoo's Cash and

Carry 90 0 90 0

4090 0 4050 0 40 0

B3 B2 N1

Creditors Journal of Molepe Stores for September 2008

Creditors Allowances Journal of Molepe Stores for September 2008

Doc Date Creditor Fol

Doc Date Creditor

Amount

Sundry Accounts

Creditors

Control

Trading

Inventory

Sundry Accounts

Creditors

Control

Trading

Inventory Stationery

Equipment StationeryFol Amount

12

2008

Sept 1 Balance b/d 46790 0

2008

Sept 30 Balance c/d 51130 0

30 Creditors Control CJ9 4340 0

51130 0 51130 0

2008

Oct 1 Balance b/d 51130 0

2008

Sept 1 Balance b/d 18870 0

2008

Sept 30 Creditors ControlCAJ

9 4050 0

30 Creditors Control CJ9 18400 0 Balance c/d 33220 0

37270 0 37270 0

2008

Oct 1 Balance b/d 33220 0

2008

Sept 30 Total AllowancesCAJ

9 4090 0

2008

Sept 1 Balance b/d 35350 0

Balance c/d 54670 0 30 Total Purchases CJ9 23410 0

58760 0 58760 0

2008

Oct 1 Balance b/d 54670 0

2008

Sept 1 Balance b/d 3310 0

2008

Sept 30 Creditors ControlCAJ

9 40 0

30 Creditors Control CJ9 670 0 Balance c/d 3940 0

3980 0 3980 0

2008

Oct 1 Balance b/d 3940 0

General Ledger of Molepo Stores

Trading Stock

Equipment

Creditors Control

NOMINAL SECTIONStationery

BALANCE SHEET SECTION

13

CREDITORS LEDGER OF MOLEPO STORES – SEPTEMBER 2008

Date Code Details/ Document Fol

2008 Sep 1 Balance 12450 0

5 Invoice CJ 4210 0 16660 0

13 Invoice CJ 1980 0 18640 0

16 Debit Note CAJ 120 0 18520 0

2008 Sept 1 Balance 14570 0

3 Invoice CJ 9210 0 23780 0

6 Debit note CAJ 430 0 23350 0

15 Invoice CJ 4340 0 27690 0

29 Debit note CAJ 90 0 27600 0

2008 Sept 1 Balance 8330 0

11 Invoice CJ 3450 0 11780 0

14 Debit note CAJ 380 0 11400 0

17 Debit note CAJ 3070 0 8330 0

2008 Sept 24 Invoice 220 0

The Printshop

Yeng Fui CC

Naidoo' Cash and Carry

Plop Wholesalers

Debit Credit Balance

CREDITORS LEDGER OF

2.3 CREDITORS LIST ON 30 SEPTEMBER 208

Yeng Fui CC

Naidoo’s Cash and Carry

Plop Wholesalers

The Printshop

18520

27600

8330

220

54670

14

ACTIVITY 3 Problem Solving Phillip’s Plumbing is a sole proprietorship. It is owned by Phillippa Howe. The following transactions relate to her creditors for the month of August 20.4. Her bookkeeper went on long leave, and so failed to capture the creditors for the month. Ms Howe needs to know how much she owes her creditors, so that she can calculate the monthly payments she needs to make. She was able to ascertain the following from the previous months’ records:

Transactions for August 20.4 4 Bought service material (e.g., washers and screws) on credit from Plumbers for Africa, R1 087. 7 Issued a debit note to Plumbers for Africa for material that was damaged, R187. 9 Received an invoice from General Motors for new tyres fitted for R800. 12 General Motors had forgotten to process a 2% discount promotion that was being given on

the new tyres that were fitted. 14 Purchased cleaning material from Handy Dealers, as per invoice X898, R120. 17 An invoice was received from General Motors for a new vehicle purchased for R13 900. 19 Bought service material for R14 760 and cleaning material for R230 on credit from Plumbers

for Africa. An invoice was received. 25 Plumbers for Africa forgot to deduct a 10% trade discount on the service material purchased

on 19 August 20.4. A debit note was issued. Calculate the payment that needs to be made to each creditor and the total amount that must be subtracted from Creditors control, Show only the calculation by taking each balance and adding or subtracting the appropriate transactions.

ACTIVITY 3

34100 – 20150 – 5125 = 8825 Plumbing for Africa opening balance General Motors: 20 150 +800 -16 +13 900 = 34 834 Handy Dealers: 5 125 +120 = 5 245 Plumbing for Africa: 8 825 +1 087 -187 +14 760 +230 – 1 476 = 23 239 Total creditors: 34 834 + 5245 + 23239 = 63318

15

DISCOUNT We all know what discount means and that it is a good thing if you are the consumer. For those who are not all that familiar with the terminology, it is when you pay less than the regular price for a product, or service you are paying for. Discount is almost the same, if not the same as something you would see at a sale; in which case you are getting a certain percentage off of the purchase price of your purchases because you bought from a particular store. Therefore a discount is a kind of reward, in some cases it is for shopping at a given store, or you may even get a reward for paying cash, this reward will be in the form of a discount. Many shops prefer to receive cash, rather than dealing with accounts, cards and so on. In this case they may offer a discount if you pay by cash to encourage you to do so. Furthermore, some shops may offer a discount if you pay your account a few days earlier, thus encouraging swift payment, whereby everyone wins. Discount is a clever way for companies to attract people’s attention and to get what they want out of their customers. You may be thinking that the shops are losing out on money, but by offering a discount in order to receive cash, they are saving on other charges, such as bank charges. They may even be losing out on interest from the bank when people have accounts. This is because they do not have the money in their bank account, therefore they prefer to receive the cash as soon as possible. How do you work out discount?

Now wasn’t that easy!

16

Time to try it on your own:

1. You are told that if you pay your account 3 days early you will receive a 15% discount. Your account is sitting at R 5500.00. What was the discount received and how much did you end up paying?

825 discount 4 675 paid

2. While analyzing a client’s books you spot that some discount was not taken into account.

Therefore this amount must be calculated so that the money that was written off can be re-accounted for. You are told that you received a discount of 6% off your purchase, however the accountant recorded the full amount of R 4673.00 in the client’s books.

4673 280.38 discount 4392.62 paid

A challenge for you: 3. You are told that you were given a discount of R 28 on your R 560 account. What was the

percentage of the discount? (Tip: start with R 28).

28/ 560 x100/1 = 5%

4. Try this one:

You are told that you received 5% off your account. The discount you received came to R 7.50. How much was your account before the discount?

100/5 x 7.50 R150

17

DISCOUNT RECEIVED FROM CREDITORS In order to encourage prompt payment, a creditor will grant a business a discount when settling an account. This discount received from the creditor is an income to the business. E.G. Ace Traders owe creditors, ALL Distributors R820. Issue a cheque no.221 for R800 in

full settlement of the account.

820 800 20

Creditors Bank Discount Received

Source Document: Cheque counterfoil

Journal: _CPJ__

A O L

-800 20 -820

18

19

CPJ

Fol Details

100 5

Tricon Shop

Supplies 3000 0 3150 0 150 0

101 7 Cash 24000 0 24000 0 wages

102 BLT & Co 1500 0 1500 0

103 21 Cash 24000 0 24000 0 wages

104 23

BZK

Development 7000 0 7000 0 Rent expense

105 25

Owens

Shopfitters 2800 0 2800 0 Equipment

106 30

Moosa

Wholesalers 1400 0 1400 0

107 31 BLT & Co 5058 0 5620 0 562 0

68758 0 1500 0 0 0 10170 0 712 0 57800

Discount

Received Doc Bank

Trading

Inventory Stationery

Cash Payments Journal of Owen Traders - May 2008

Date Details Fol

Creditors

Control

Sundry Accounts

Amount

20

CJ

Fol Details

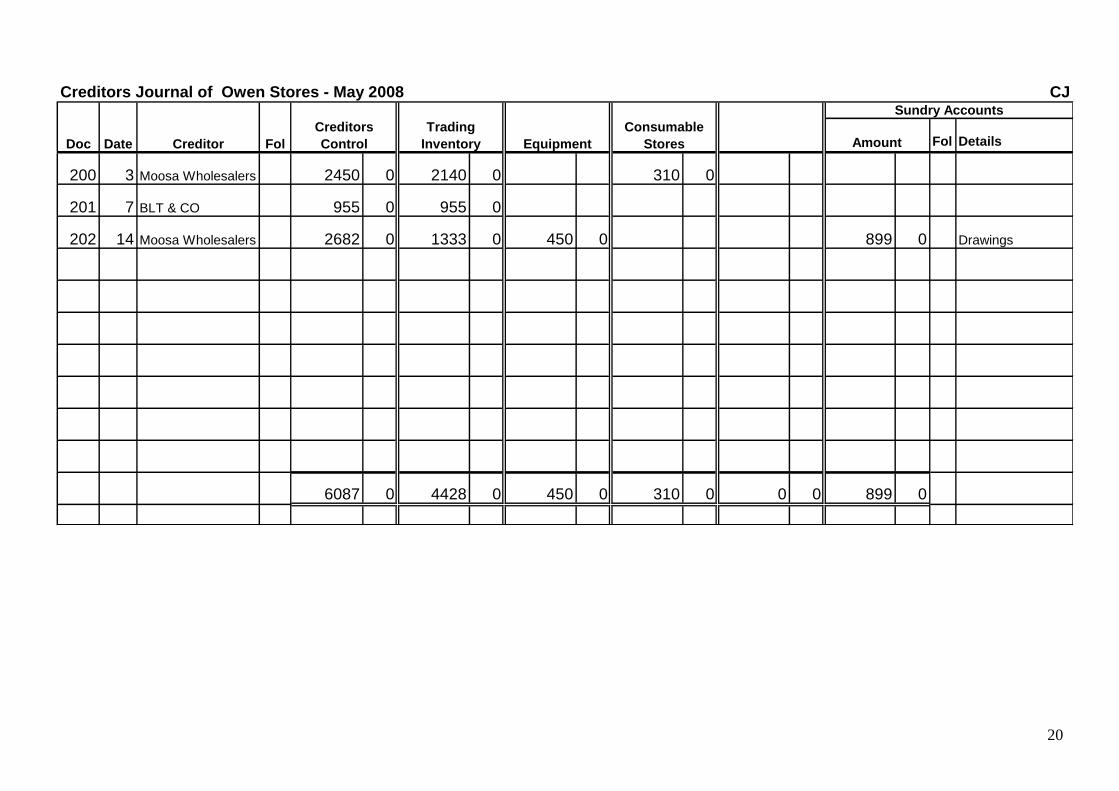

200 3 Moosa Wholesalers 2450 0 2140 0 310 0

201 7 BLT & CO 955 0 955 0

202 14 Moosa Wholesalers 2682 0 1333 0 450 0 899 0 Drawings

6087 0 4428 0 450 0 310 0 0 0 899 0

Creditors Journal of Owen Stores - May 2008

Doc Date Creditor Fol

Creditors

Control

Trading

Inventory Amount

Sundry Accounts

Consumable

StoresEquipment

21

22

Date Code Details/ Document Fol Date Code Details/ Document Fol

Date Code Details/ Document Fol Date Code Details/ Document Fol

Debit Credit Balance

Debit Credit Balance

Debit Credit Balance

Debit Credit Balance

23

24

25

26

27