critical challenges for the global economy icrier new delhi, india april 20, 2007

TRANSCRIPT

Critical Challenges Critical Challenges for the Global Economyfor the Global Economy

ICRIERICRIERNew Delhi, IndiaNew Delhi, IndiaApril 20, 2007April 20, 2007

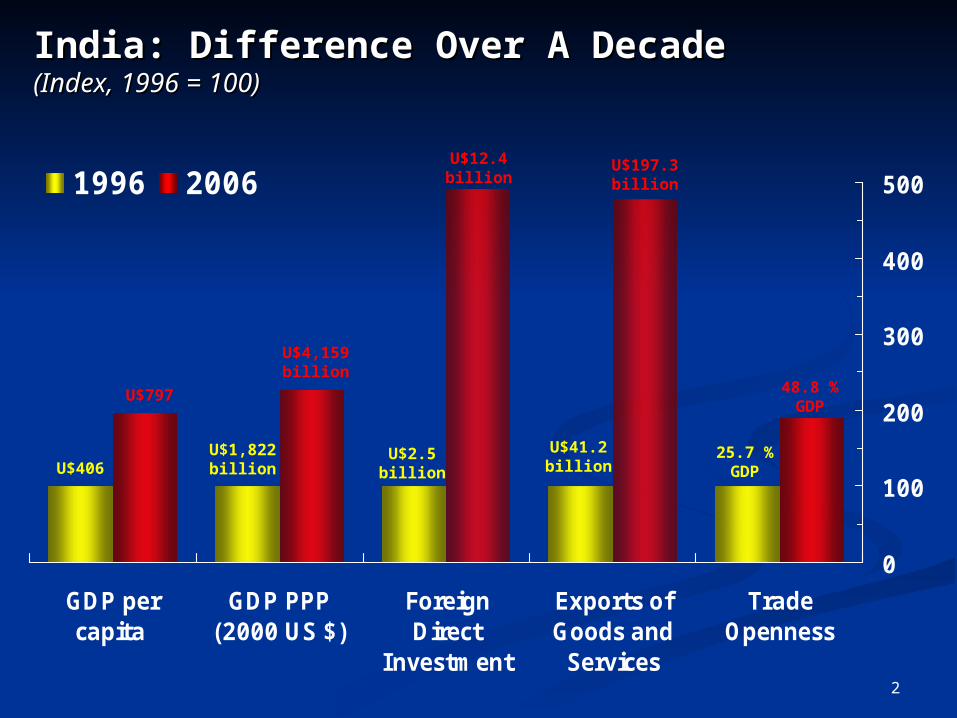

2

0

100

200

300

400

500

GDP percapita

GDP PPP(2000 US $)

ForeignDirect

Investment

Exports ofGoods andServices

TradeOpenness

1996 2006

India: Difference Over A DecadeIndia: Difference Over A Decade(Index, 1996 = 100)(Index, 1996 = 100)

U$406

U$797

U$4,159 billion

U$1,822 billion

U$2.5 billion

U$12.4 billion

U$41.2 billion

U$197.3 billion

25.7 % GDP

48.8 % GDP

3

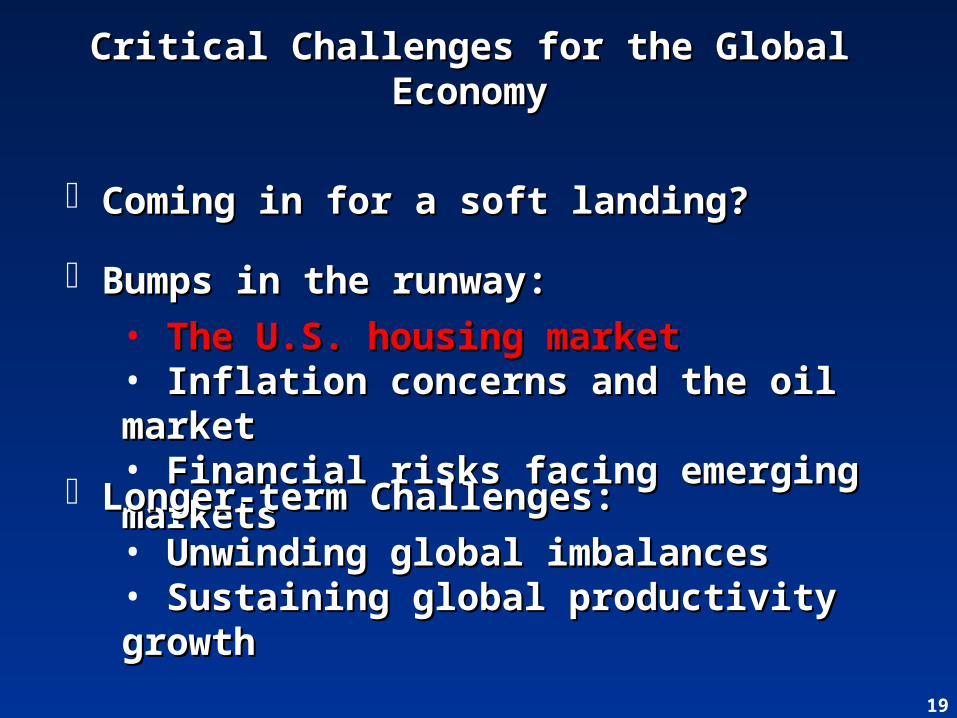

Critical Challenges for the Global Critical Challenges for the Global EconomyEconomy

Coming in for a soft landing?Coming in for a soft landing?

Bumps in the runway:Bumps in the runway:• The U.S. housing marketThe U.S. housing market• Inflation concerns and the oil Inflation concerns and the oil marketmarket• Financial risks facing emerging Financial risks facing emerging marketsmarkets

Longer-term Challenges:Longer-term Challenges:• Unwinding global imbalancesUnwinding global imbalances• Sustaining global productivity Sustaining global productivity growthgrowth

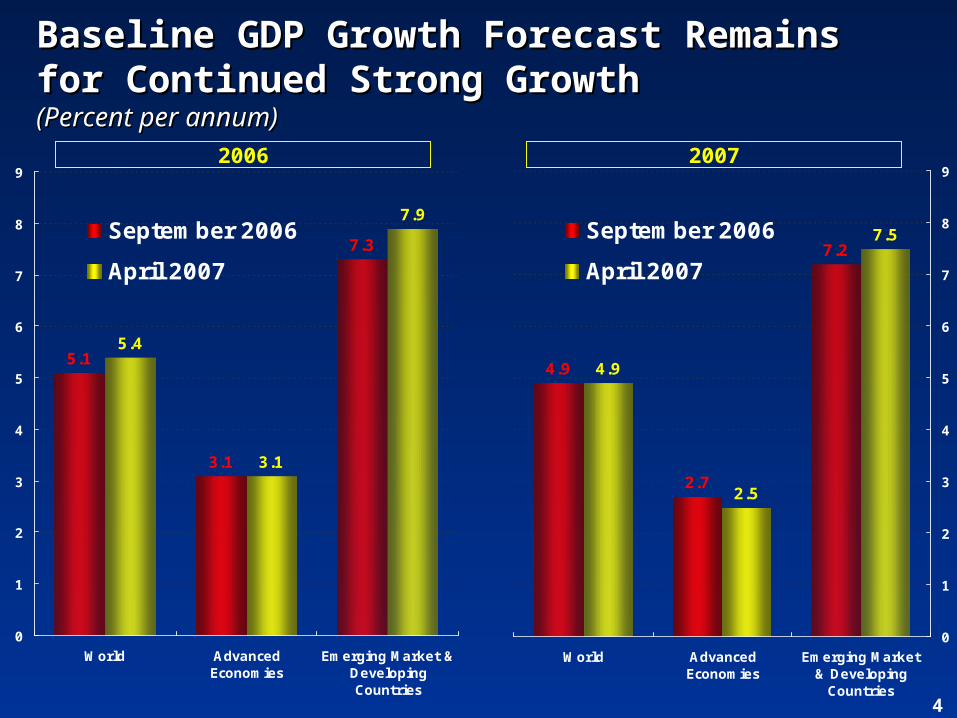

4

5.1

3.1

7.3

3.1

7.9

5.4

0

1

2

3

4

5

6

7

8

9

World AdvancedEconomies

Emerging Market &DevelopingCountries

September 2006

April 2007

4.9

2.7

7.2

4.9

2.5

7.5

0

1

2

3

4

5

6

7

8

9

World AdvancedEconomies

Emerging Market& Developing

Countries

September 2006

April 2007

2006 2007

Baseline GDP Growth Forecast Remains Baseline GDP Growth Forecast Remains for Continued Strong Growthfor Continued Strong Growth(Percent per annum)(Percent per annum)

5

-15

-10

-5

0

5

10

15

2003Q1 2004Q1 2005Q1 2006Q1-2

0

2

4

6

8

10

12

2003Q1 2004Q1 2005Q1 2006Q1

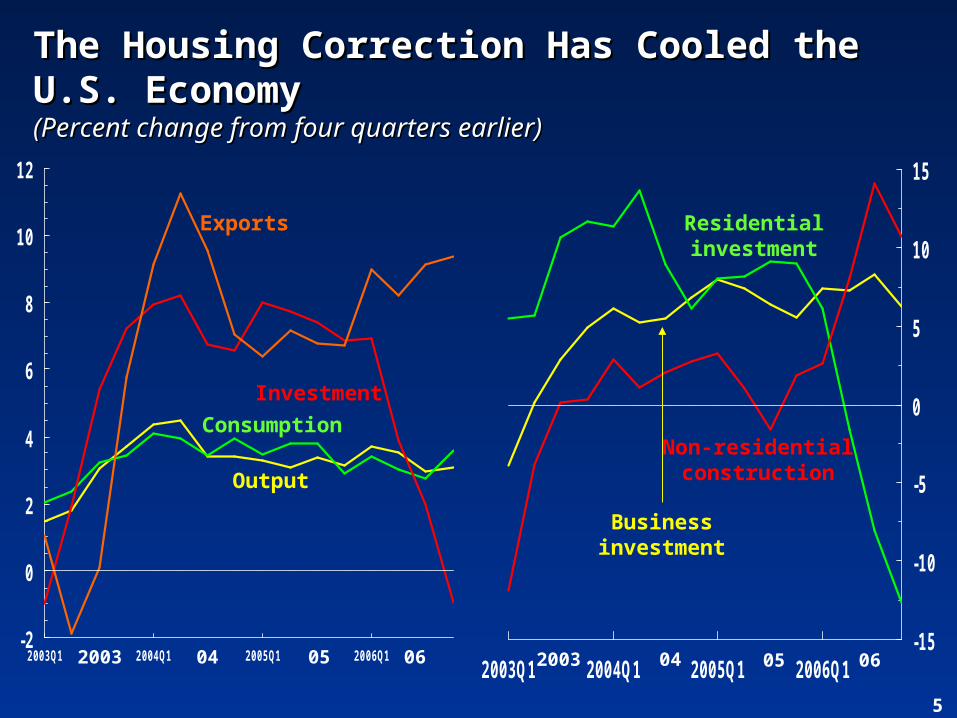

The Housing Correction Has Cooled the The Housing Correction Has Cooled the U.S. EconomyU.S. Economy(Percent change from four quarters earlier)(Percent change from four quarters earlier)

Output

Investment

Consumption

Business investment

Residential investment

Non-residential construction

2003 04 05 06 2003 04 05 06

Exports

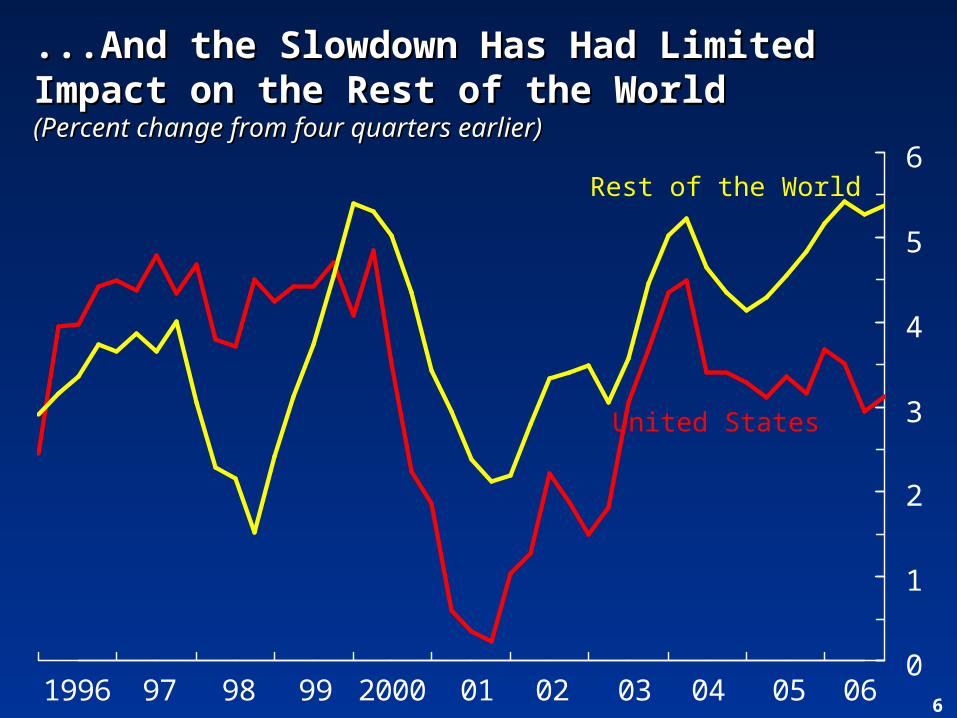

606050403020120009998971996

0

1

2

3

4

5

6

United States

Rest of the World

...And the Slowdown Has Had Limited ...And the Slowdown Has Had Limited Impact on the Rest of the WorldImpact on the Rest of the World(Percent change from four quarters earlier)(Percent change from four quarters earlier)

7

-4

-3

-2

-1

0

1

2

3

4

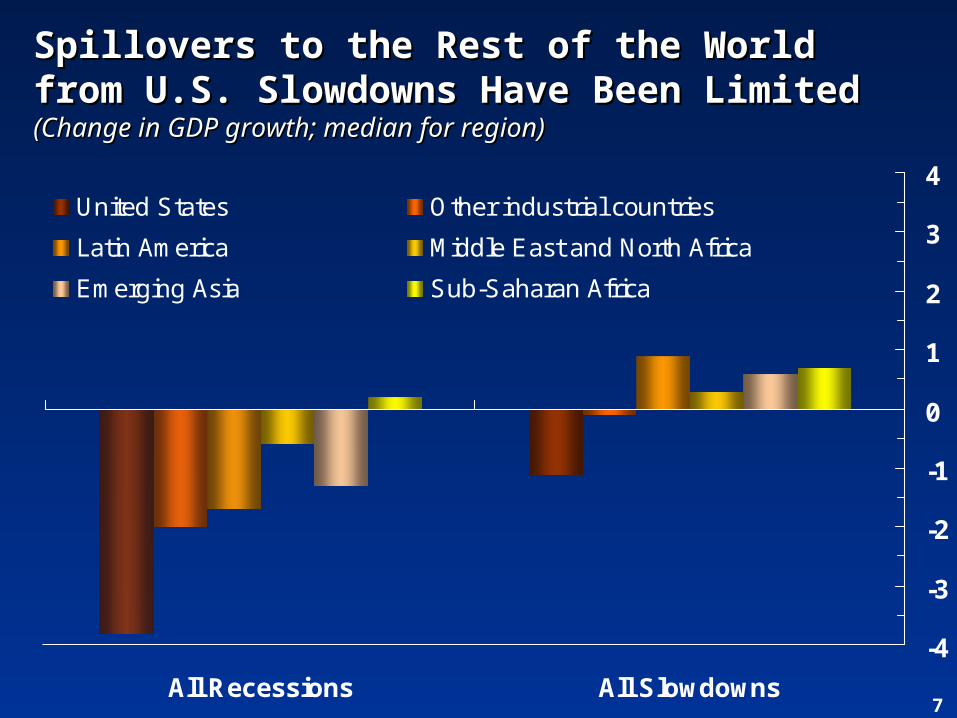

All Recessions All Slowdowns

United States Other industrial countries

Latin America Middle East and North Africa

Emerging Asia Sub-Saharan Africa

Spillovers to the Rest of the World from Spillovers to the Rest of the World from U.S. Slowdowns Have Been LimitedU.S. Slowdowns Have Been Limited(Change in GDP growth; median for region)(Change in GDP growth; median for region)

8

Impact of Growth Declines in the U.S. and Impact of Growth Declines in the U.S. and Japan Japan (Shading denotes one standard error confidence interval)(Shading denotes one standard error confidence interval)

-0.8

-0.6

-0.4

-0.2

0.0

0.2

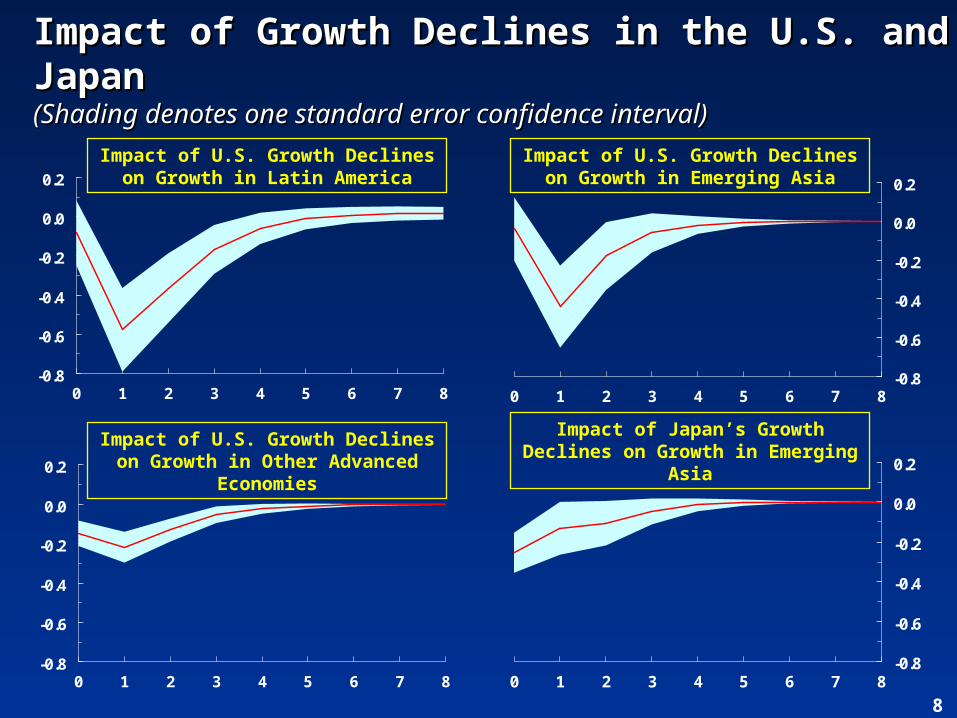

0 1 2 3 4 5 6 7 8

Impact of U.S. Growth Declines on Growth in Latin America

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0 1 2 3 4 5 6 7 8

Impact of U.S. Growth Declines on Growth in Emerging Asia

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0 1 2 3 4 5 6 7 8-0.8

-0.6

-0.4

-0.2

0.0

0.2

0 1 2 3 4 5 6 7 8

Impact of U.S. Growth Declines on Growth in Other Advanced

Economies

Impact of Japan’s Growth Declines on Growth in Emerging

Asia

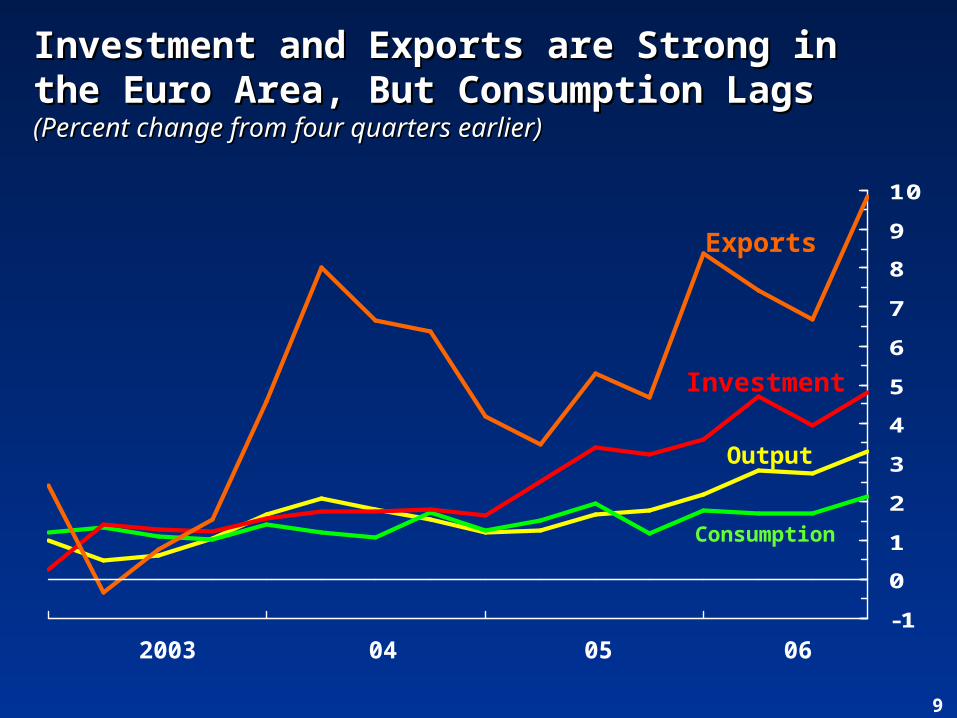

9

-1

0

1

2

3

4

5

6

7

8

9

10

Investment and Exports are Strong in the Investment and Exports are Strong in the Euro Area, But Consumption LagsEuro Area, But Consumption Lags(Percent change from four quarters earlier)(Percent change from four quarters earlier)

Output

Investment

Consumption

2003 04 05 06

Exports

10

-3

-2

-1

0

1

2

3

4

5

6

0

4

8

12

16

20

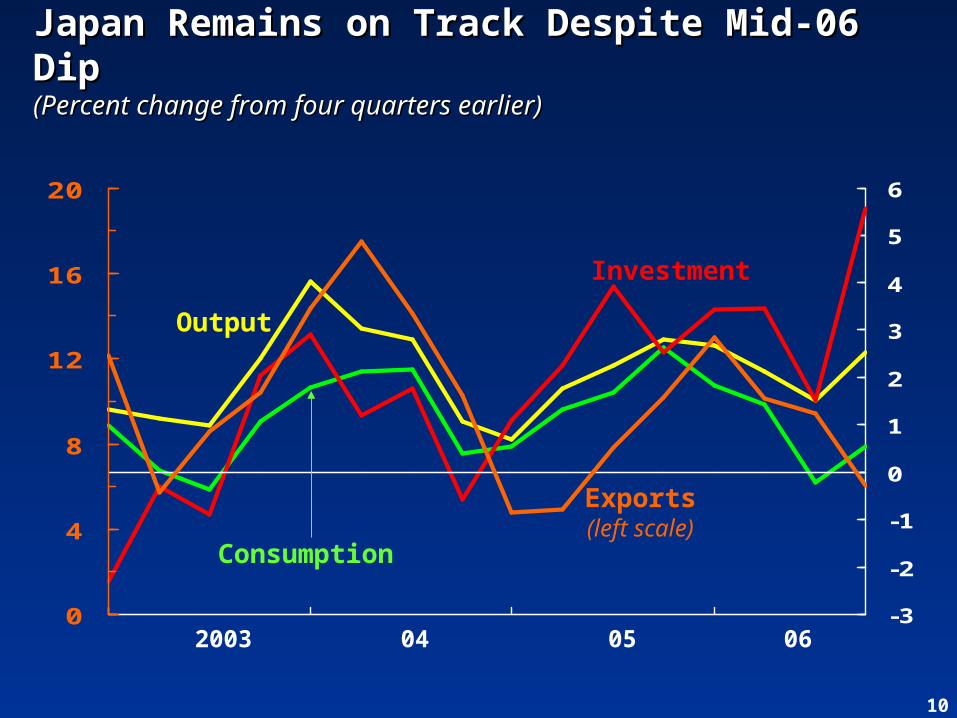

Japan Remains on Track Despite Mid-06 Japan Remains on Track Despite Mid-06 DipDip(Percent change from four quarters earlier)(Percent change from four quarters earlier)

Output

Consumption

Investment

2003 04 05 06

Exports(left scale)

11

-2

0

2

4

6

8

10

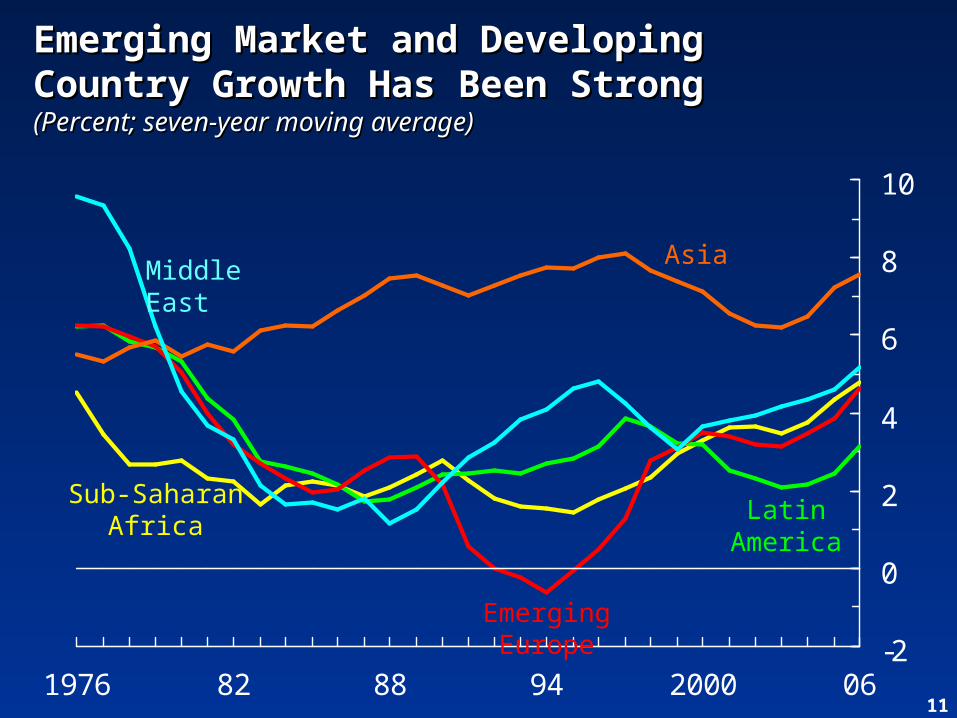

1976 82 88 94 2000 06

Sub-Saharan Africa

Latin America

Emerging Europe

Middle EastAsia

Emerging Market and Developing Emerging Market and Developing Country Growth Has Been StrongCountry Growth Has Been Strong(Percent; seven-year moving average)(Percent; seven-year moving average)

122003 07060504

10

20

30

40

50

60

6

7

8

9

10

11

12

Fixed Asset Investment(6-month m.a.; right scale)

Real GDP Growth(left scale)

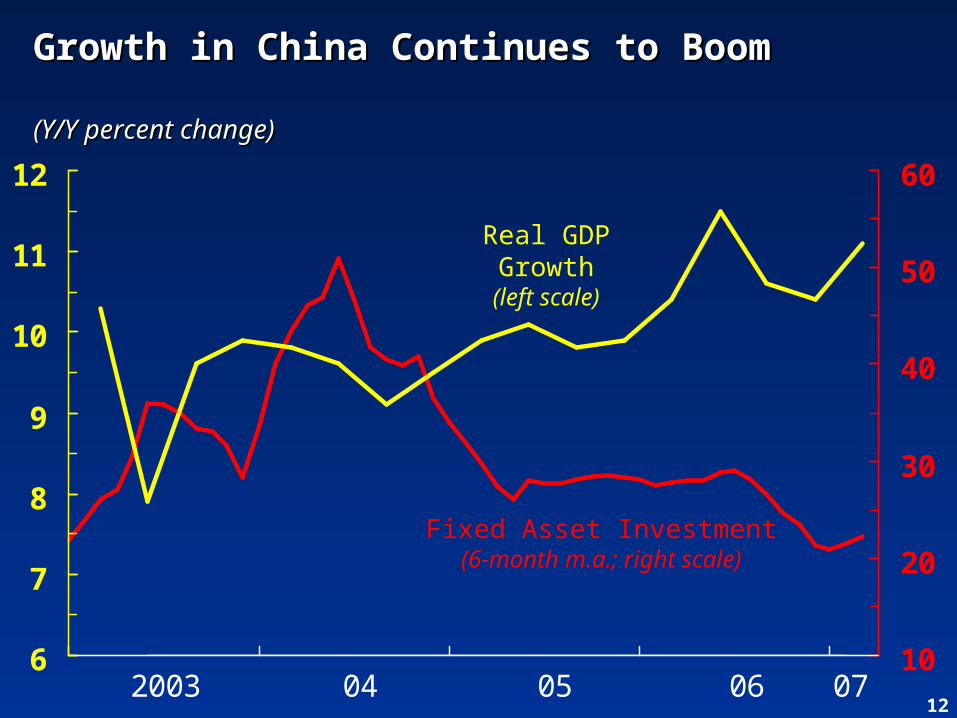

Growth in China Continues to BoomGrowth in China Continues to Boom

(Y/Y percent change)(Y/Y percent change)

132003 04 05 06

0

2

4

6

8

10

12

14

.

Industrial Production Growth

Real GDP Growth

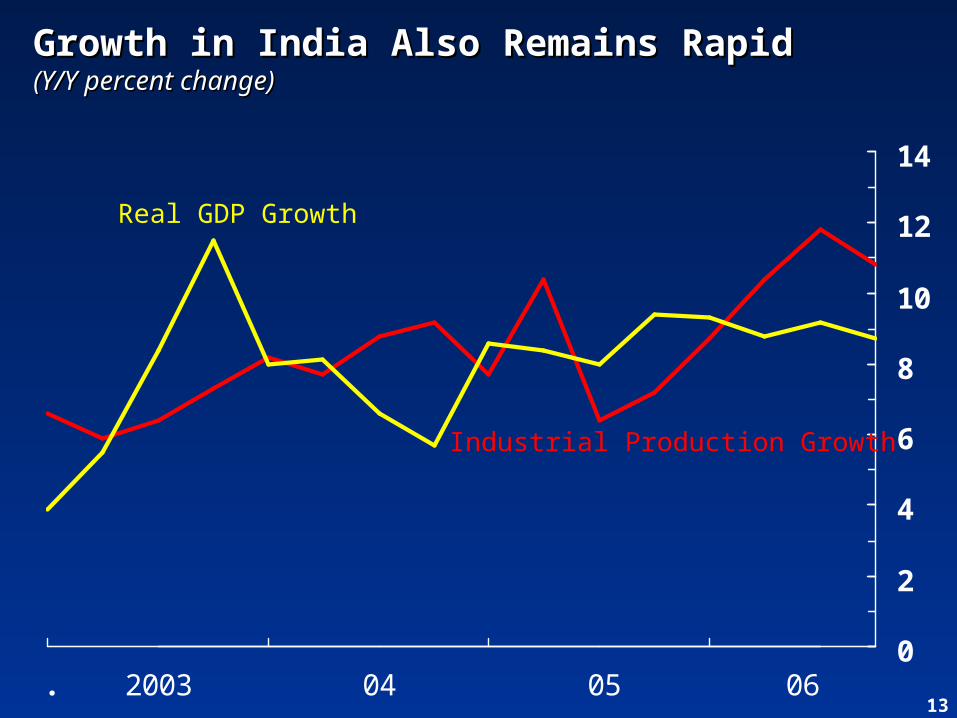

Growth in India Also Remains RapidGrowth in India Also Remains Rapid(Y/Y percent change)(Y/Y percent change)

14

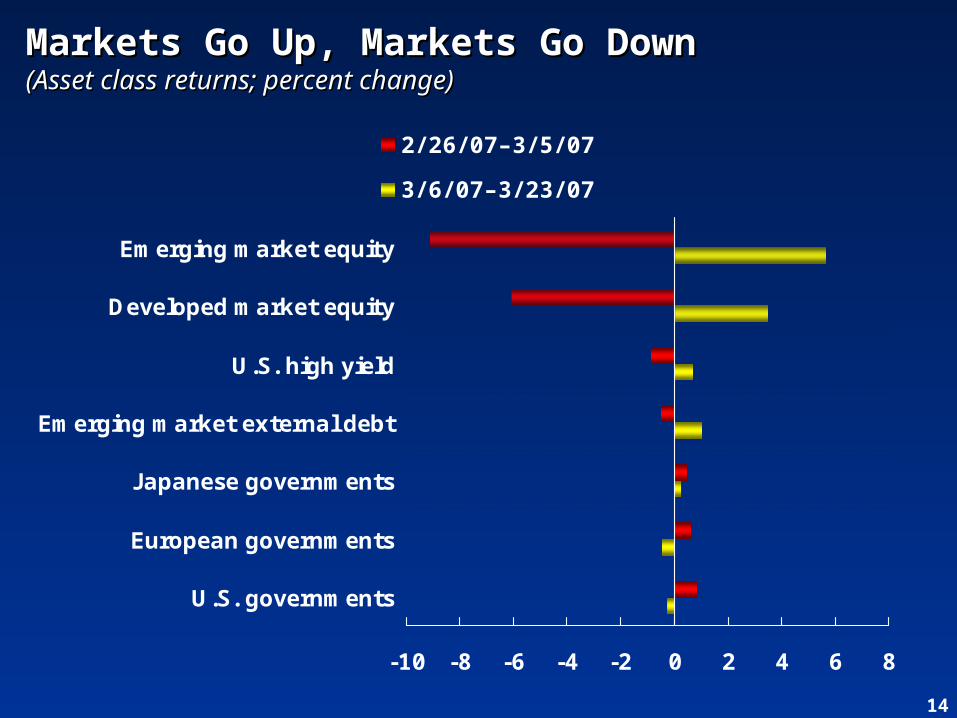

-10 -8 -6 -4 -2 0 2 4 6 8

U.S. governments

European governments

Japanese governments

Emerging market external debt

U.S. high yield

Developed market equity

Emerging market equity

2/ 26/ 07–3/ 5/ 07

3/ 6/ 07–3/ 23/ 07

Markets Go Up, Markets Go DownMarkets Go Up, Markets Go Down(Asset class returns; percent change)(Asset class returns; percent change)

15

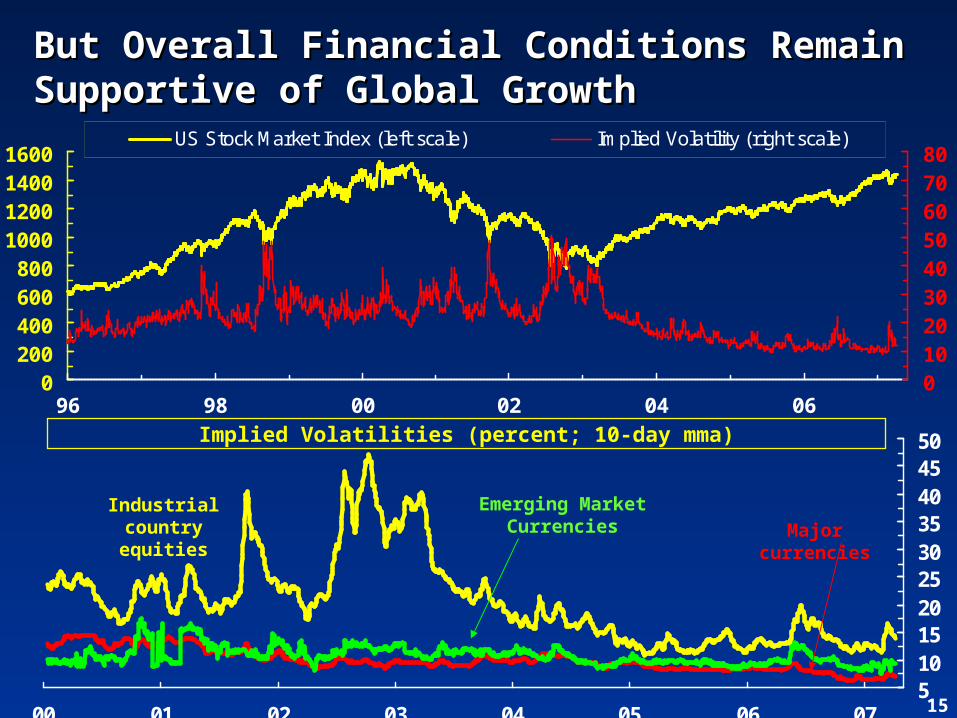

But Overall Financial Conditions Remain But Overall Financial Conditions Remain Supportive of Global GrowthSupportive of Global Growth

0200400600800

1000120014001600

96 98 00 02 04 0601020304050607080

US Stock Market Index (left scale) Implied Volatility (right scale)

5101520253035404550

00 01 02 03 04 05 06 07

Emerging Market

Currencies

Industrialcountryequities

Major currencies

Implied Volatilities (percent; 10-day mma)

16

0

1

2

3

4

5

6

7

01 02 03 04 05 06 07 08

0

1

2

3

4

5

6

7

UnitedStates

Euro area

Japan

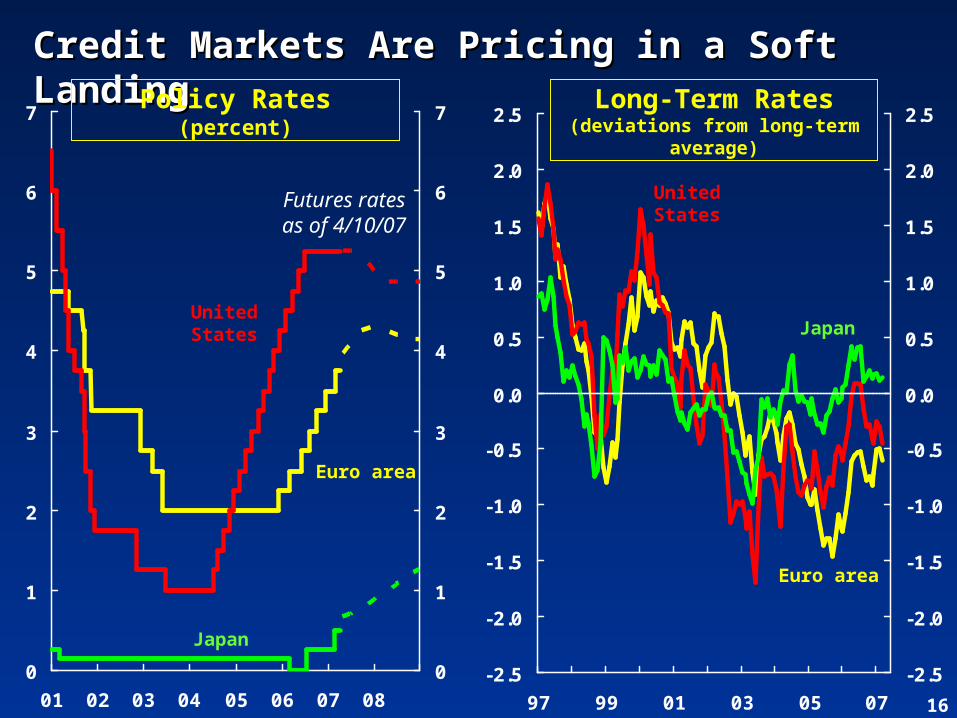

Credit Markets Are Pricing in a Soft Credit Markets Are Pricing in a Soft LandingLanding

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

97 99 01 03 05 07

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

UnitedStates

Euro area

Japan

Policy Rates(percent)

Futures ratesas of 4/10/07

Long-Term Rates(deviations from long-term

average)

17

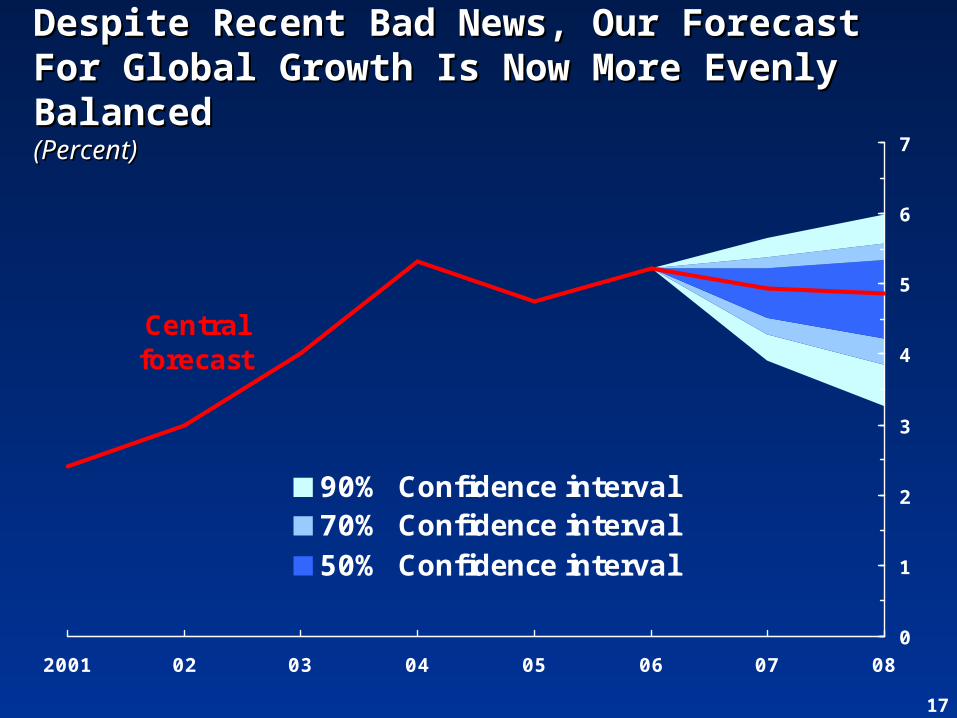

Central forecast

0

1

2

3

4

5

6

7

2001 02 03 04 05 06 07 08

90% Confidence interval70% Confidence interval50% Confidence interval

Despite Recent Bad News, Our Forecast Despite Recent Bad News, Our Forecast For Global Growth Is Now More Evenly For Global Growth Is Now More Evenly BalancedBalanced(Percent)(Percent)

18

-0.10

-0.08

-0.06

-0.04

-0.02

0.00

0.02

0.04

U.S.housing

Domesticdemand inEurope and

Japan

Emergingmarketgrowth

Inflationrisks

Oil supply Disorderlyunwindingof global

imbalances

Financialstability

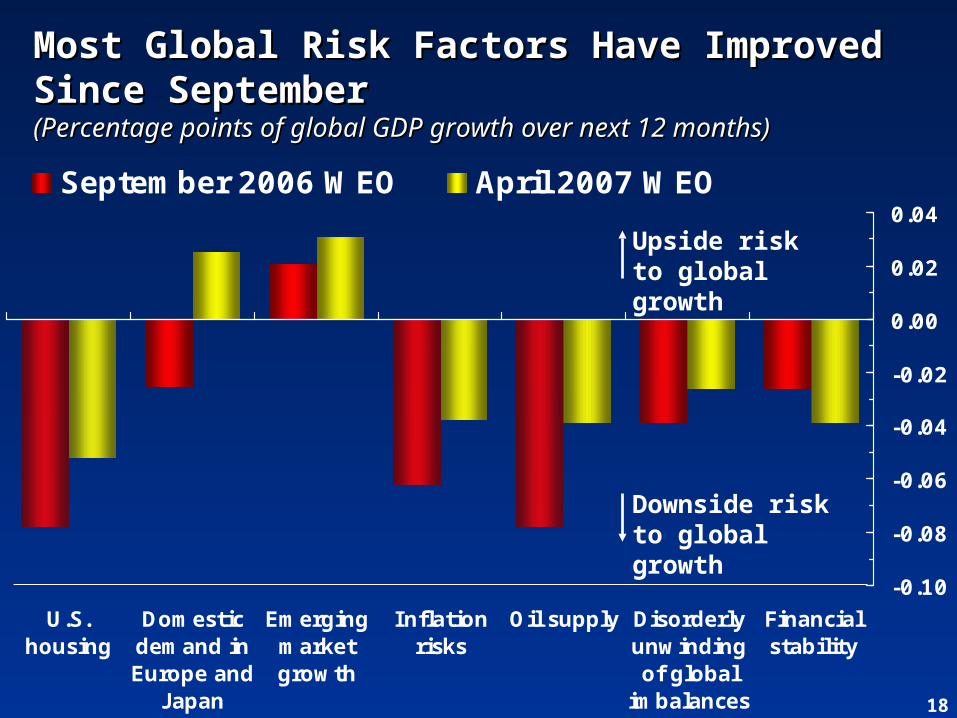

September 2006 WEO April 2007 WEO

Most Global Risk Factors Have Improved Most Global Risk Factors Have Improved Since SeptemberSince September(Percentage points of global GDP growth over next 12 months)(Percentage points of global GDP growth over next 12 months)

Downside risk to global growth

Upside risk to global growth

19

Critical Challenges for the Global Critical Challenges for the Global EconomyEconomy

Coming in for a soft landing?Coming in for a soft landing?

Bumps in the runway:Bumps in the runway:• The U.S. housing marketThe U.S. housing market• Inflation concerns and the oil Inflation concerns and the oil marketmarket• Financial risks facing emerging Financial risks facing emerging marketsmarkets

Longer-term Challenges:Longer-term Challenges:• Unwinding global imbalancesUnwinding global imbalances• Sustaining global productivity Sustaining global productivity growthgrowth

20

-8

-6

-4

-2

0

2

4

6

8

10

12

1978 82 86 90 94 98 2002 06

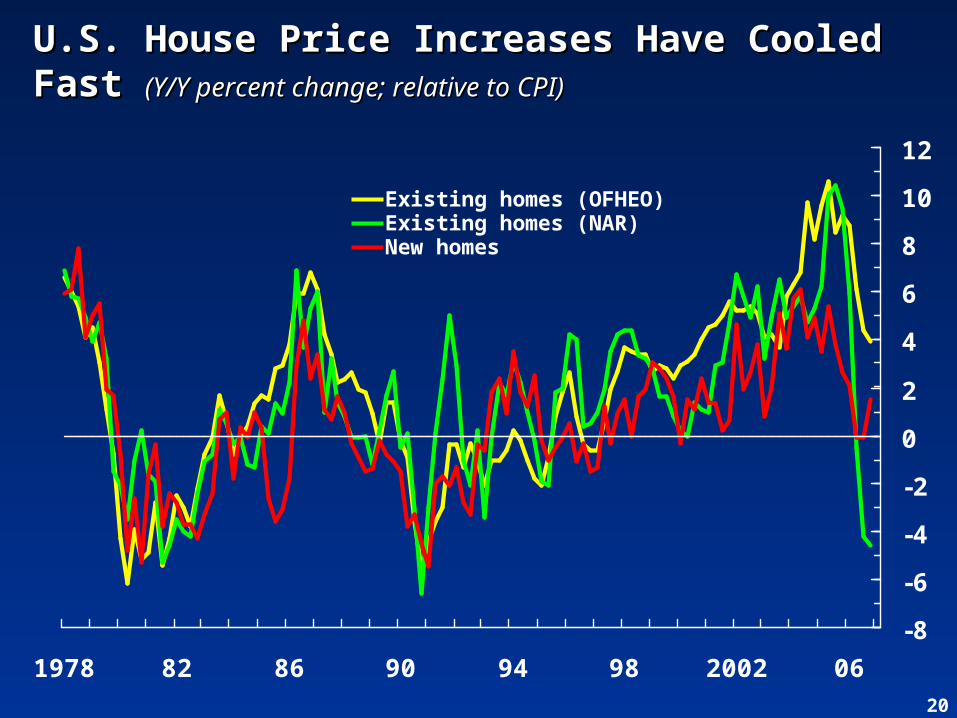

U.S. House Price Increases Have Cooled U.S. House Price Increases Have Cooled Fast Fast (Y/Y percent change; relative to CPI)(Y/Y percent change; relative to CPI)

Existing homes (OFHEO)Existing homes (NAR)New homes

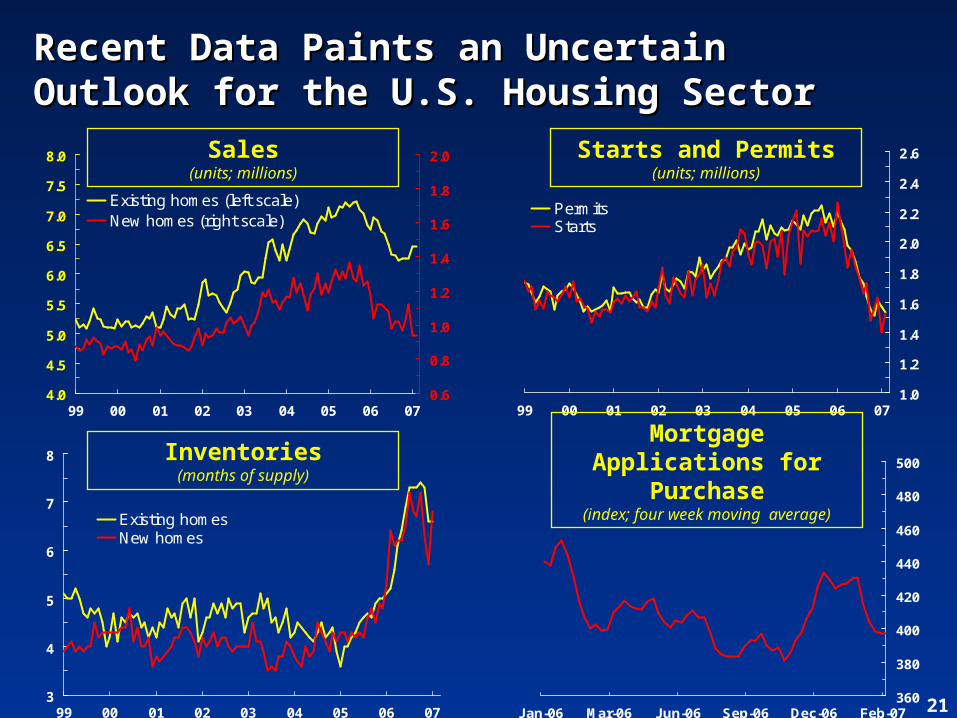

21

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

99 00 01 02 03 04 05 06 070.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Existing homes (left scale)New homes (right scale)

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

99 00 01 02 03 04 05 06 07

PermitsStarts

3

4

5

6

7

8

99 00 01 02 03 04 05 06 07

Existing homesNew homes

Inventories(months of supply)

Mortgage Applications for Purchase

(index; four week moving average)

Starts and Permits(units; millions)

Sales(units; millions)

360

380

400

420

440

460

480

500

Jan-06 Mar-06 Jun-06 Sep-06 Dec-06 Feb-07

Recent Data Paints an Uncertain Recent Data Paints an Uncertain Outlook for the U.S. Housing SectorOutlook for the U.S. Housing Sector

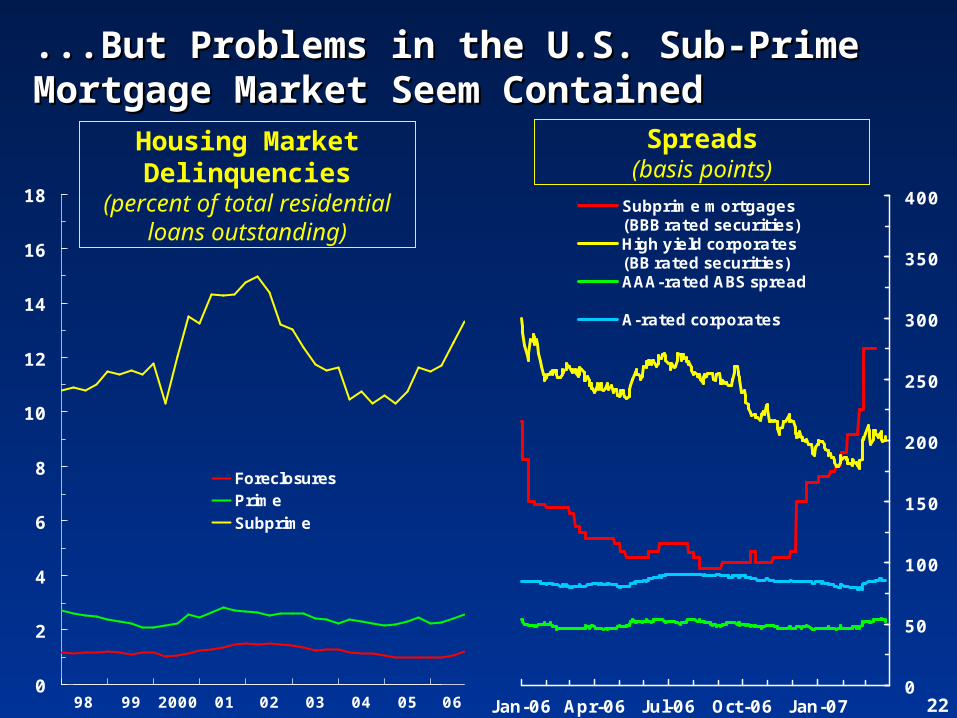

220

50

100

150

200

250

300

350

400

Jan-06 Apr-06 Jul-06 Oct-06 Jan-07

Subprime mortgages(BBB rated securities)High yield corporates(BB rated securities)AAA-rated ABS spread

A-rated corporates

...But Problems in the U.S. Sub-Prime ...But Problems in the U.S. Sub-Prime Mortgage Market Seem ContainedMortgage Market Seem Contained

Spreads(basis points)

Housing Market Delinquencies

(percent of total residential loans outstanding)

060504030201200099980

2

4

6

8

10

12

14

16

18

ForeclosuresPrimeSubprime

23

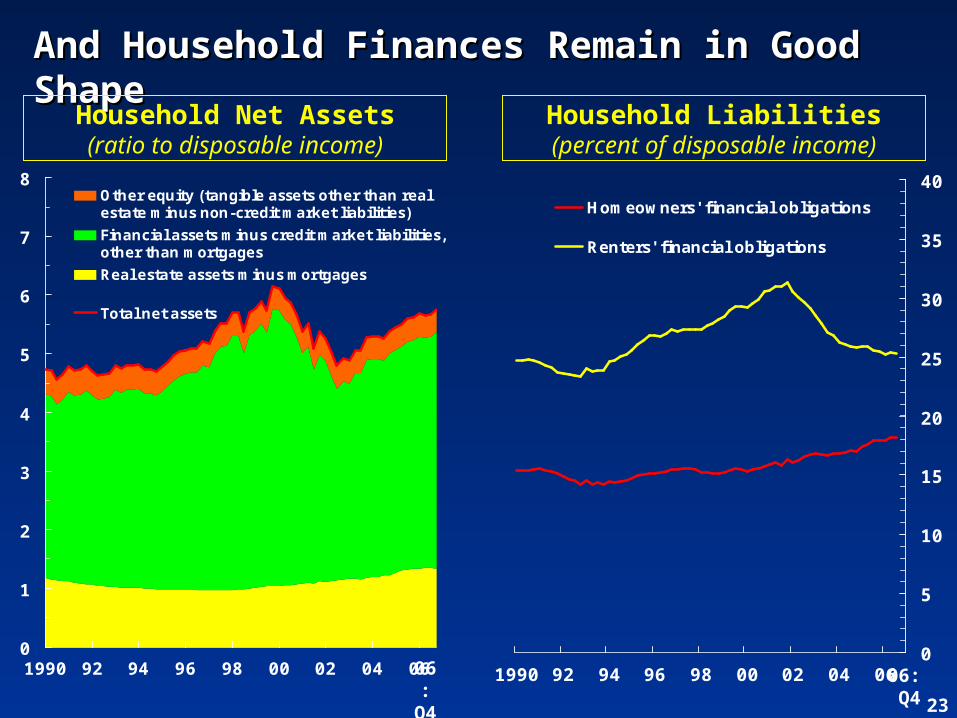

And Household Finances Remain in Good And Household Finances Remain in Good ShapeShape

0

5

10

15

20

25

30

35

40

1990 92 94 96 98 00 02 04 06

Homeowners' financial obligations

Renters' financial obligations

0

1

2

3

4

5

6

7

8

1990 92 94 96 98 00 02 04 06

Other equity (tangible assets other than realestate minus non-credit market liabilities)

Financial assets minus credit market liabilities,other than mortgages

Real estate assets minus mortgages

Total net assets

Household Net Assets(ratio to disposable income)

Household Liabilities(percent of disposable income)

06:Q4

06:

Q4

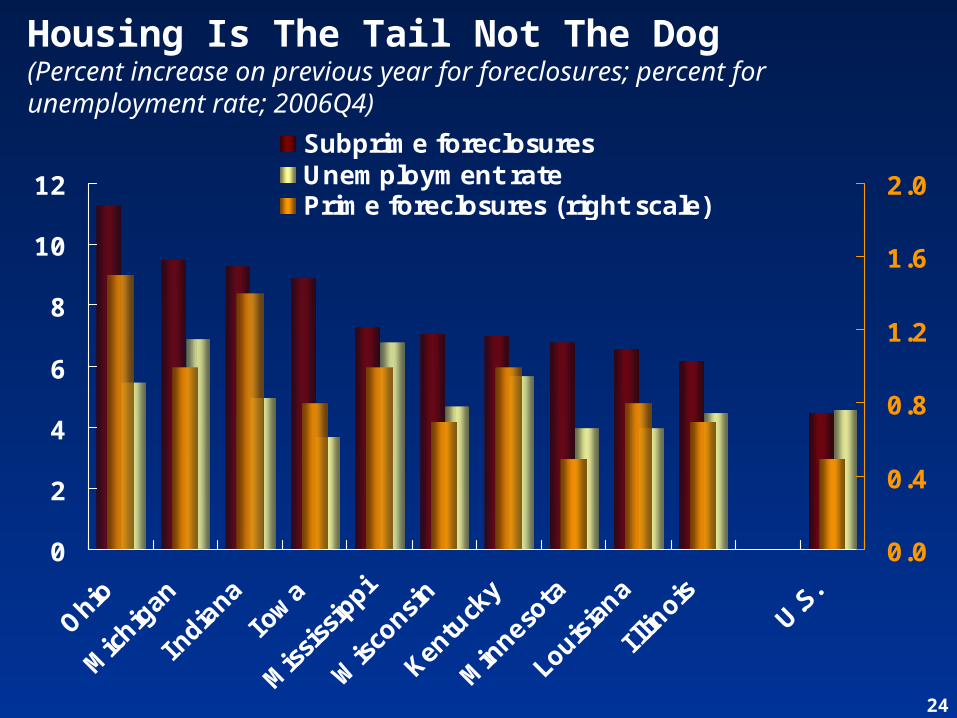

24

0

2

4

6

8

10

12

Ohio

Michiga

n

Indian

aIo

wa

Mississ

ippi

Wisc

onsin

Kent

ucky

Minne

sota

Louisian

a

I llinois

U.S.

0.0

0.4

0.8

1.2

1.6

2.0

Subprime foreclosuresUnemployment ratePrime foreclosures (right scale)

Housing Is The Tail Not The Dog(Percent increase on previous year for foreclosures; percent for unemployment rate; 2006Q4)

25

Critical Challenges for the Global Critical Challenges for the Global EconomyEconomy

Coming in for a soft landing?Coming in for a soft landing?

Bumps in the runway:Bumps in the runway:• The U.S. housing marketThe U.S. housing market• Inflation concerns and the oil Inflation concerns and the oil marketmarket• Financial risks facing emerging Financial risks facing emerging marketsmarkets

Longer-term Challenges:Longer-term Challenges:• Unwinding global imbalancesUnwinding global imbalances• Sustaining global productivity Sustaining global productivity growthgrowth

26

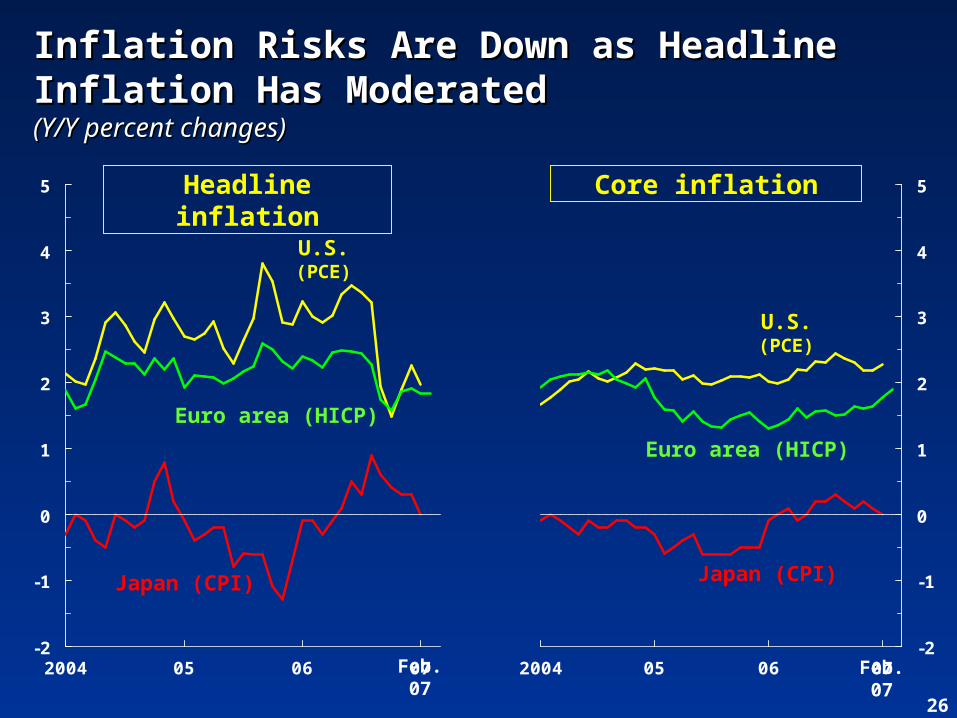

Inflation Risks Are Down as Headline Inflation Risks Are Down as Headline Inflation Has ModeratedInflation Has Moderated(Y/Y percent changes)(Y/Y percent changes)

-2

-1

0

1

2

3

4

5

2004 05 06 07-2

-1

0

1

2

3

4

5

2004 05 06 07

U.S.(PCE)

Euro area (HICP)

Euro area (HICP)

Japan (CPI) Japan (CPI)

U.S.(PCE)

Headline inflation Core inflation

Feb. 07

Feb. 07

27-4

-3

-2

-1

0

1

2

3

4

1980 85 90 95 2000 05

Emergingmarkets

Advancedeconomies

World

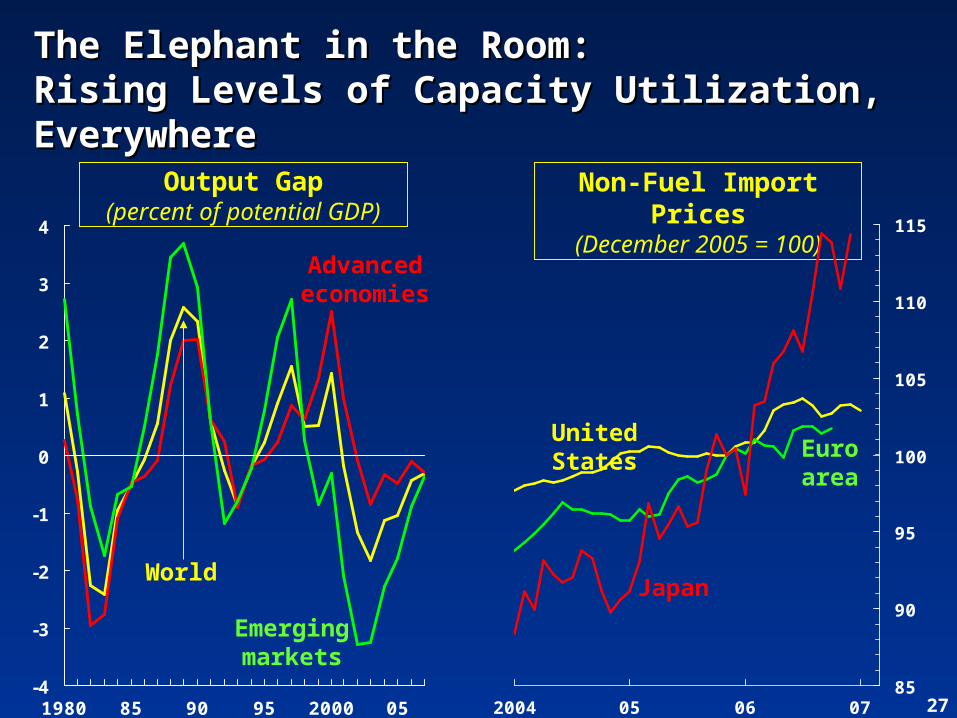

The Elephant in the Room:The Elephant in the Room:Rising Levels of Capacity Utilization, Rising Levels of Capacity Utilization, EverywhereEverywhere

Output Gap(percent of potential GDP)

Non-Fuel Import Prices

(December 2005 = 100)

85

90

95

100

105

110

115

2004 05 06 07

Euro area

Japan

United States

28

-1

0

1

2

3

4

5

6

7

96 98 00 02 04 06

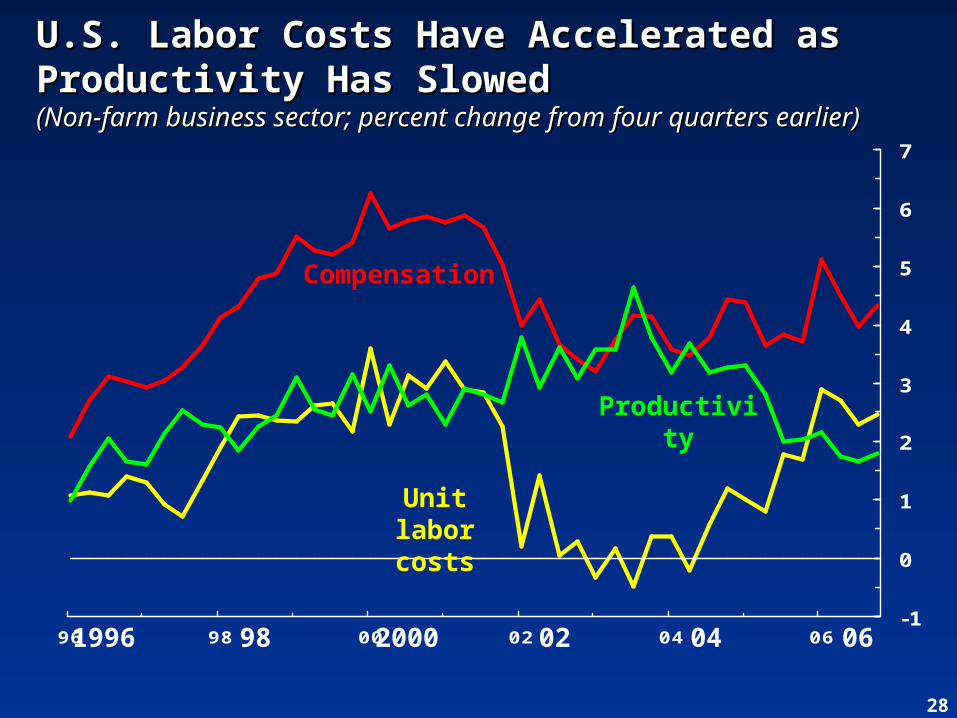

U.S. Labor Costs Have Accelerated as U.S. Labor Costs Have Accelerated as Productivity Has SlowedProductivity Has Slowed(Non-farm business sector; percent change from four quarters (Non-farm business sector; percent change from four quarters earlier)earlier)

Unit labor costs

Compensation

Productivity

1996 2000 04 060298

29

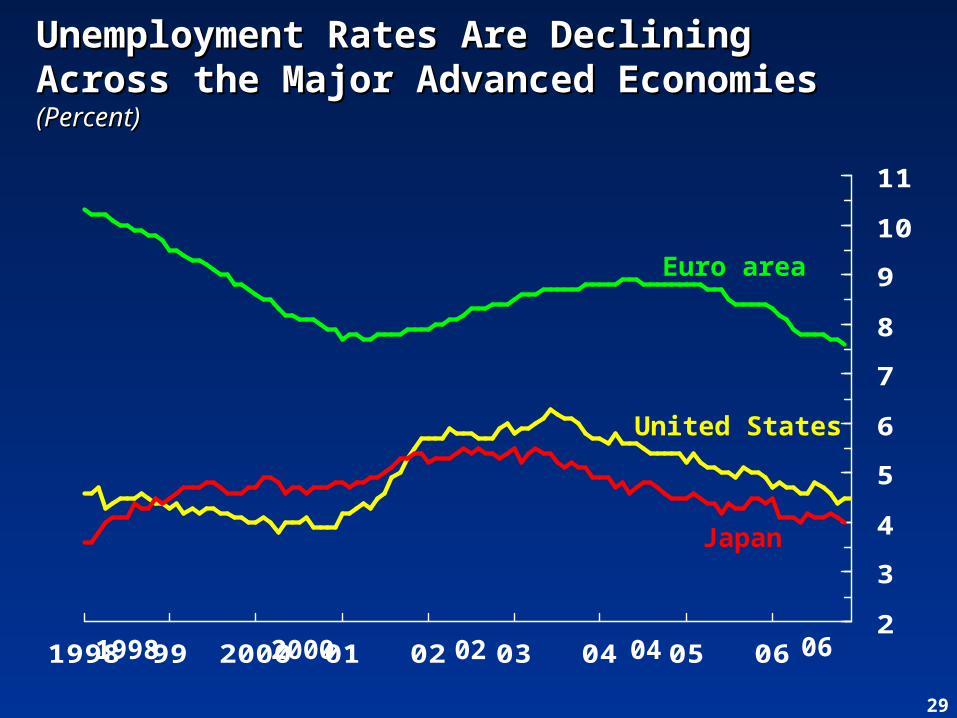

Unemployment Rates Are Declining Unemployment Rates Are Declining Across the Major Advanced EconomiesAcross the Major Advanced Economies(Percent)(Percent)

2

3

4

5

6

7

8

9

10

11

1998 99 2000 01 02 03 04 05 06

United States

Japan

Euro area

1998 02 062000 04

30

-20

-15

-10

-5

0

5

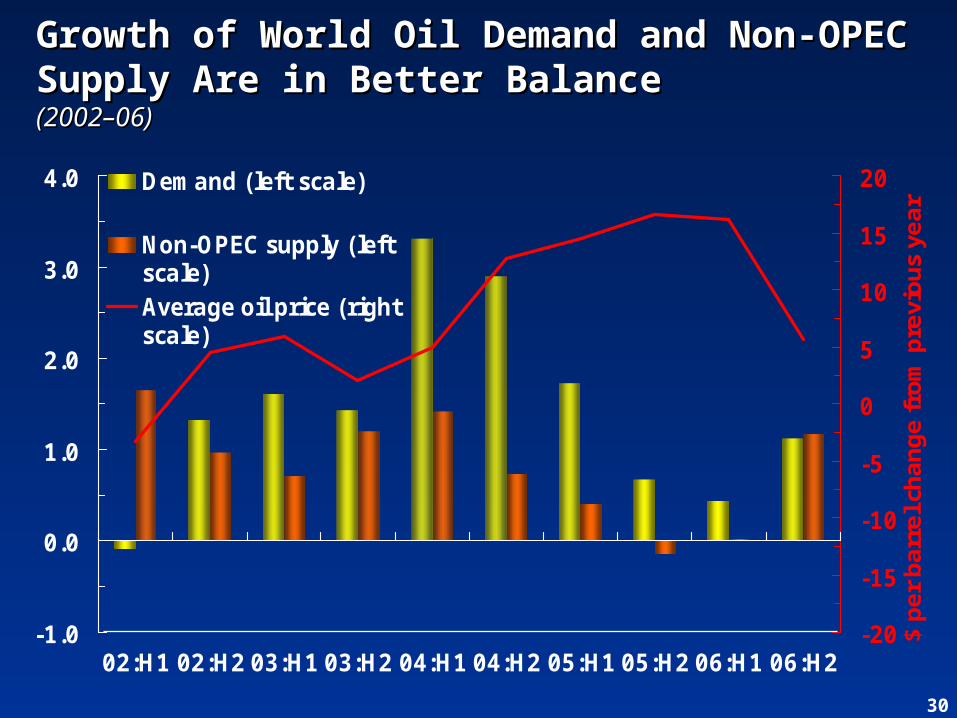

10

15

20

02:H1 02:H203:H103:H2 04:H104:H2 05:H105:H206:H1 06:H2

$ pe

r ba

rrel

cha

nge

from

pre

viou

s ye

ar

-1.0

0.0

1.0

2.0

3.0

4.0 Demand (left scale)

Non-OPEC supply (leftscale)Average oil price (rightscale)

Growth of World Oil Demand and Non-Growth of World Oil Demand and Non-OPEC Supply Are in Better BalanceOPEC Supply Are in Better Balance(2002–06)(2002–06)

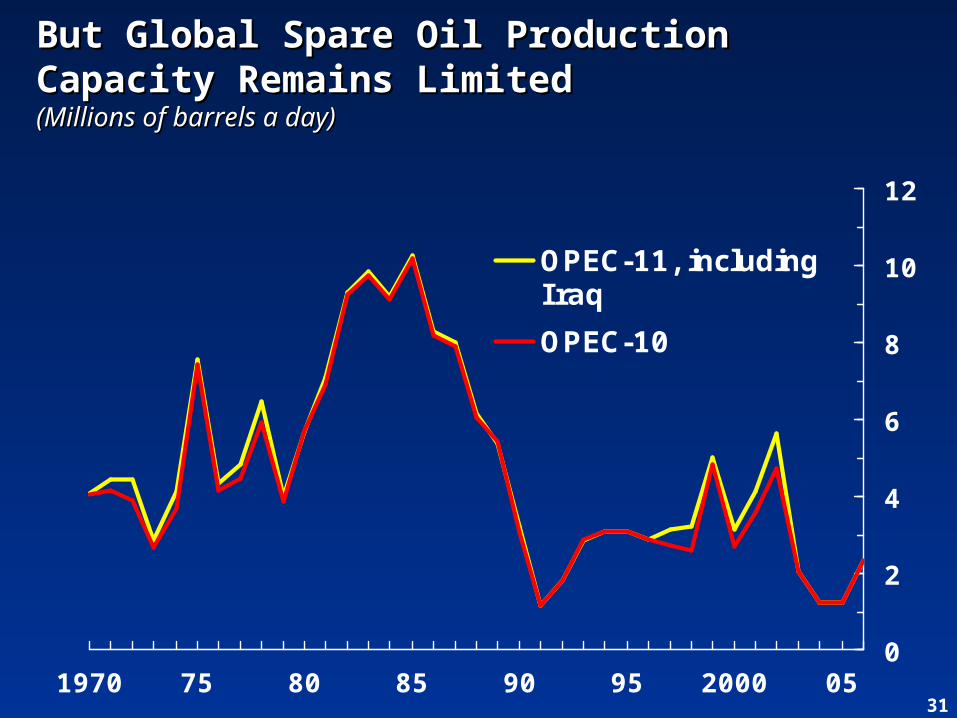

31

0

2

4

6

8

10

12

1970 75 80 85 90 95 2000 05

OPEC-11, includingIraq

OPEC-10

But Global Spare Oil Production Capacity But Global Spare Oil Production Capacity Remains LimitedRemains Limited(Millions of barrels a day)(Millions of barrels a day)

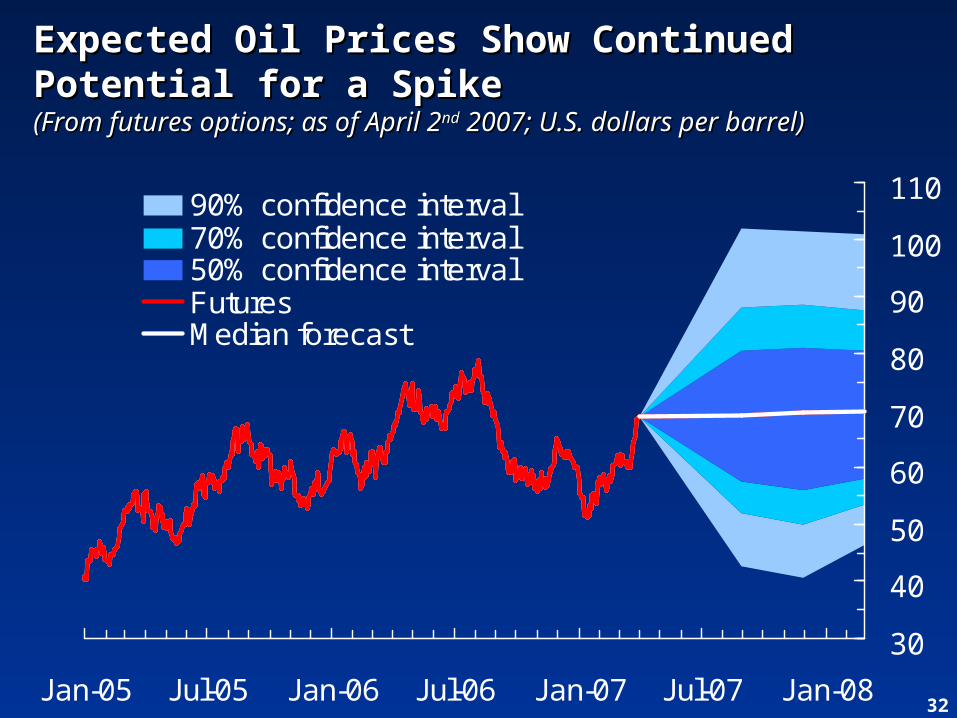

32

30

40

50

60

70

80

90

100

110

Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08

90% confidence interval70% confidence interval50% confidence intervalFuturesMedian forecast

Expected Oil Prices Show Continued Expected Oil Prices Show Continued Potential for a SpikePotential for a Spike(From futures options; as of April 2(From futures options; as of April 2ndnd 2007; U.S. dollars per 2007; U.S. dollars per barrel)barrel)

33

Critical Challenges for the Global Critical Challenges for the Global EconomyEconomy

Coming in for a soft landing?Coming in for a soft landing?

Bumps in the runway:Bumps in the runway:• The U.S. housing marketThe U.S. housing market• Inflation concerns and the oil Inflation concerns and the oil marketmarket• Financial risks facing emerging Financial risks facing emerging marketsmarkets

Longer-term Challenges:Longer-term Challenges:• Unwinding global imbalancesUnwinding global imbalances• Sustaining global productivity Sustaining global productivity growthgrowth

34

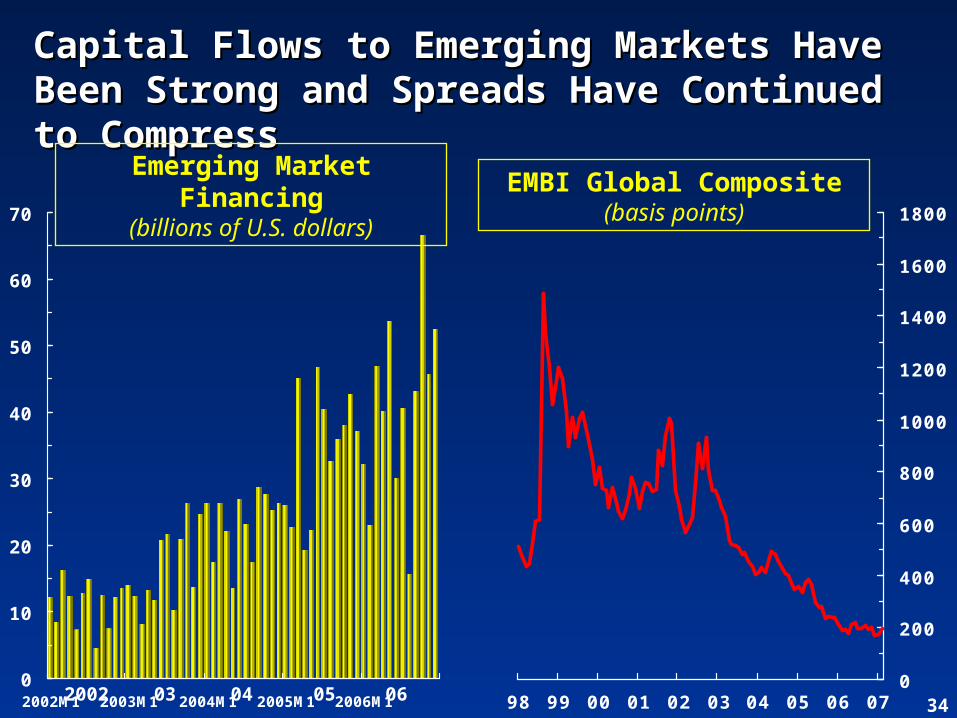

Capital Flows to Emerging Markets Have Capital Flows to Emerging Markets Have Been Strong and Spreads Have Continued Been Strong and Spreads Have Continued to Compressto Compress

0

10

20

30

40

50

60

70

2002M1 2003M1 2004M1 2005M1 2006M12002 0603 04 050

200

400

600

800

1000

1200

1400

1600

1800

98 99 00 01 02 03 04 05 06 07

EMBI Global Composite(basis points)

Emerging Market Financing

(billions of U.S. dollars)

35

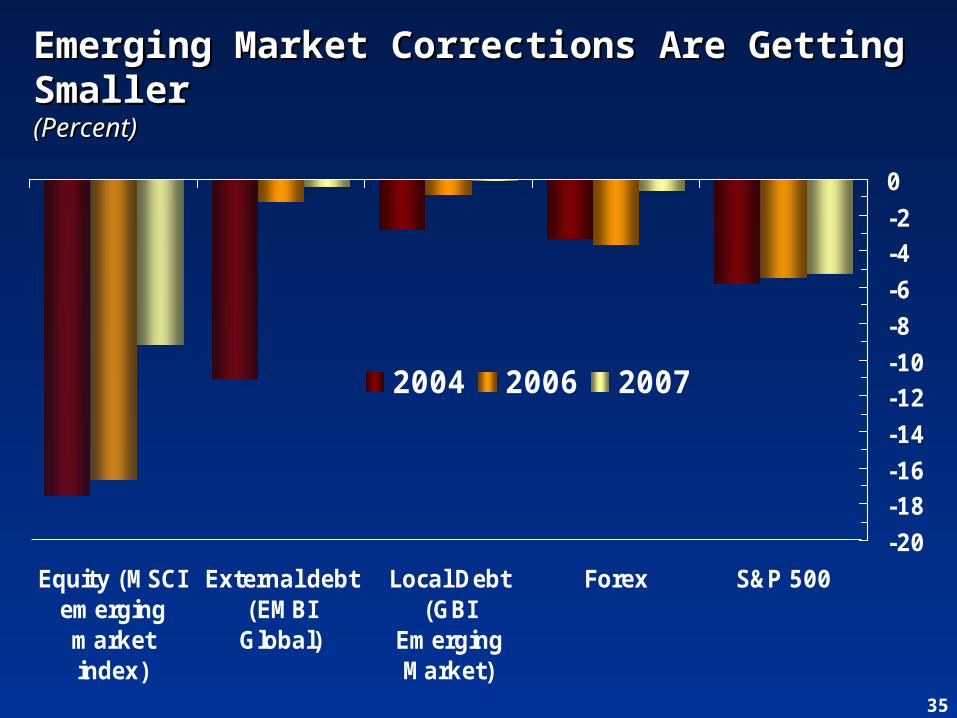

Emerging Market Corrections Are Getting Emerging Market Corrections Are Getting SmallerSmaller(Percent)(Percent)

-20

-18-16

-14

-12-10

-8

-6

-4-2

0

Equity (MSCIemergingmarketindex)

External debt(EMBIGlobal)

Local Debt(GBI

EmergingMarket)

Forex S&P 500

2004 2006 2007

36

-25

0

25

50

75

100

125

150

175

1980 85 90 95 2000 05

FDI

Flows to the public sector

Flows to the private sector excl. FDI

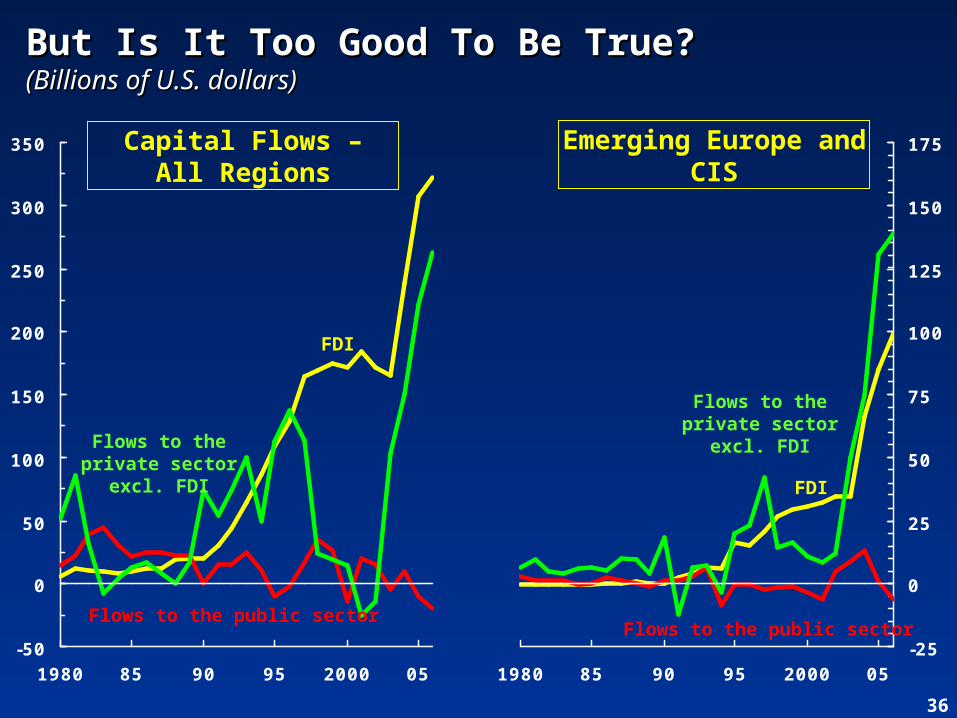

But Is It Too Good To Be True?But Is It Too Good To Be True?(Billions of U.S. dollars)(Billions of U.S. dollars)

-50

0

50

100

150

200

250

300

350

1980 85 90 95 2000 05

FDI

Flows to the public sector

Flows to the private sector

excl. FDI

Capital Flows –All Regions

Emerging Europe and CIS

37

-300

-150

0

150

300

450

600

750

900

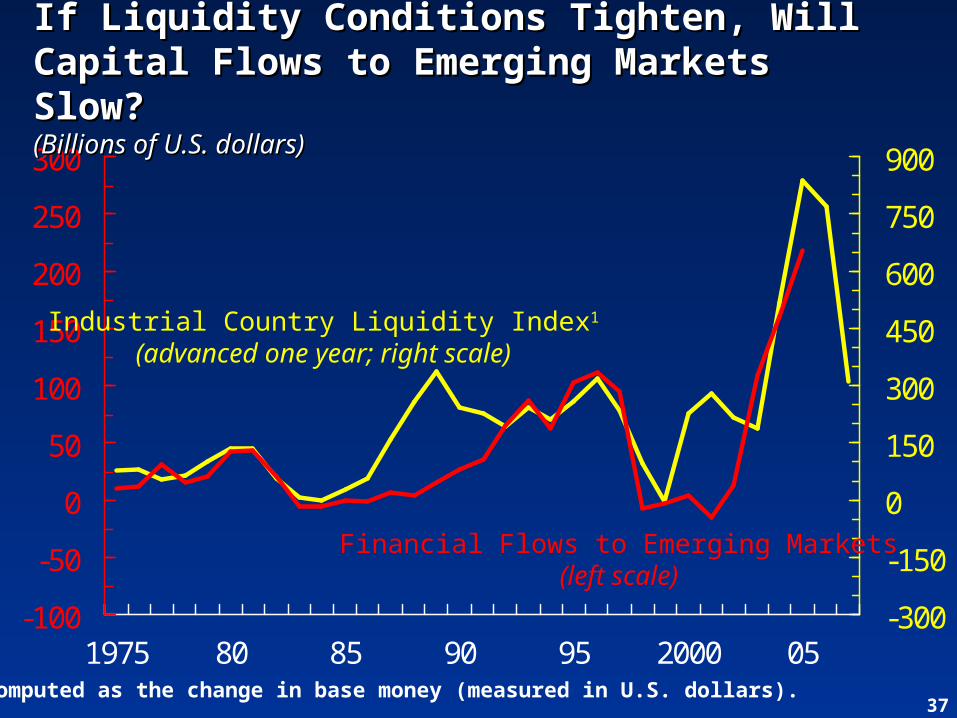

1975 80 85 90 95 2000 05-100

-50

0

50

100

150

200

250

300

Financial Flows to Emerging Markets(left scale)

Industrial Country Liquidity Index1

(advanced one year; right scale)

If Liquidity Conditions Tighten, Will If Liquidity Conditions Tighten, Will Capital Flows to Emerging Markets Capital Flows to Emerging Markets Slow?Slow?(Billions of U.S. dollars)(Billions of U.S. dollars)

1Computed as the change in base money (measured in U.S. dollars).

38

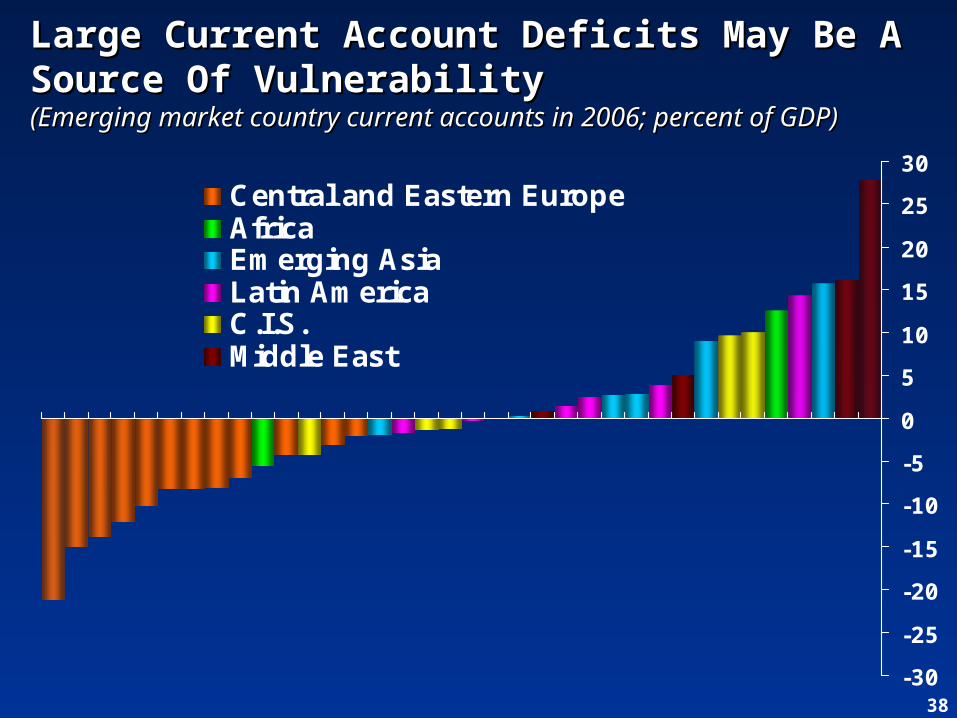

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

Central and Eastern EuropeAfricaEmerging AsiaLatin AmericaC.I.S.Middle East

Large Current Account Deficits May Be A Large Current Account Deficits May Be A Source Of VulnerabilitySource Of Vulnerability(Emerging market country current accounts in 2006; percent of (Emerging market country current accounts in 2006; percent of GDP)GDP)

39

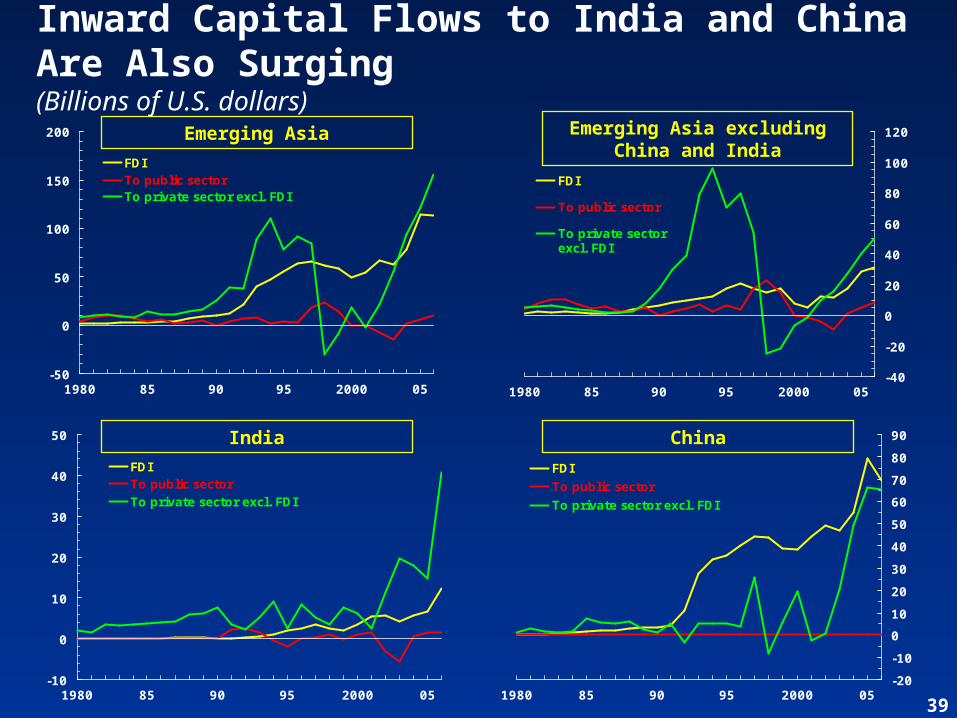

Inward Capital Flows to India and China Are Also Surging(Billions of U.S. dollars)

-50

0

50

100

150

200

1980 85 90 95 2000 05

FDITo public sectorTo private sector excl. FDI

-10

0

10

20

30

40

50

1980 85 90 95 2000 05

FDITo public sectorTo private sector excl. FDI

India

-40

-20

0

20

40

60

80

100

120

1980 85 90 95 2000 05

FDI

To public sector

To private sectorexcl. FDI

Emerging Asia excludingChina and India

-20

-10

0

10

20

30

40

50

60

70

80

90

1980 85 90 95 2000 05

FDI

To public sector

To private sector excl. FDI

China

Emerging Asia

40

Critical Challenges for the Global Critical Challenges for the Global EconomyEconomy

Coming in for a soft landing?Coming in for a soft landing?

Bumps in the runway:Bumps in the runway:• The U.S. housing marketThe U.S. housing market• Inflation concerns and the oil Inflation concerns and the oil marketmarket• Financial risks facing emerging Financial risks facing emerging marketsmarkets

Longer-term Challenges:Longer-term Challenges:• Unwinding global imbalancesUnwinding global imbalances• Sustaining global productivity Sustaining global productivity growthgrowth

41-4

-2

0

2

4

6

8

10

12

14

2000 01 02 03 04 05 06-4

-3

-2

-1

0

1

2

3

4

5

2000 01 02 03 04 05 06

-40

-30

-20

-10

0

10

20

30

40

50

60

70

2000 01 02 03 04 05 06-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

2000 01 02 03 04 05 06

China

Saudi Arabia

Euro Area

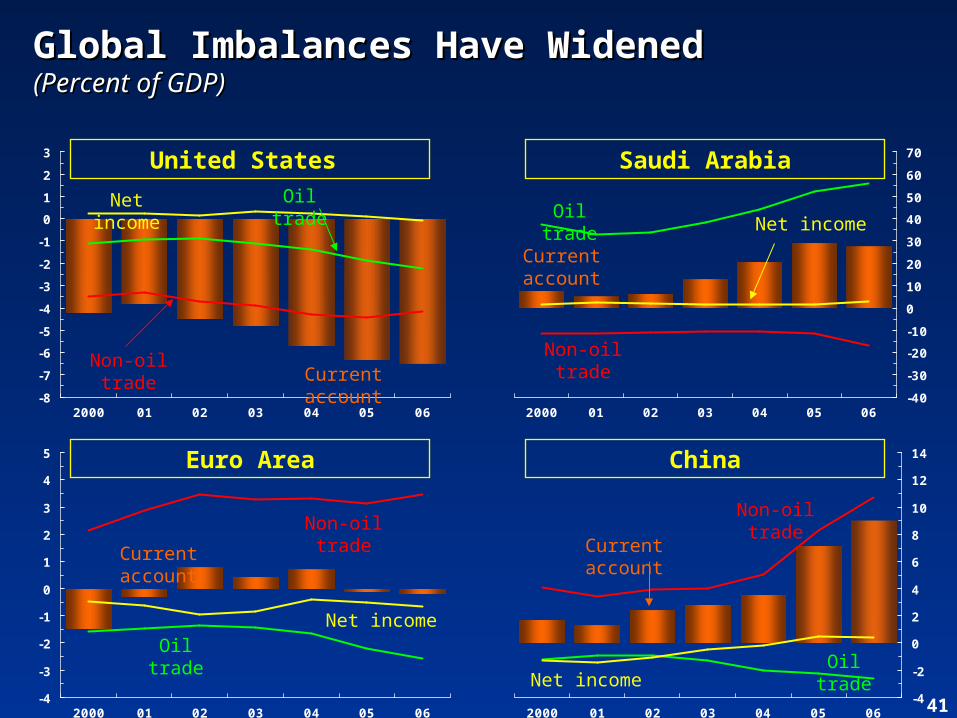

Global Imbalances Have WidenedGlobal Imbalances Have Widened(Percent of GDP)(Percent of GDP)

Oil tradeNet income

Non-oil trade

Oil tradeNet income

Non-oil trade

United States

Current account

Current account

Non-oil trade

Oil tradeNet income

Current account

Oil tradeNet income

Non-oil trade

Current account

42

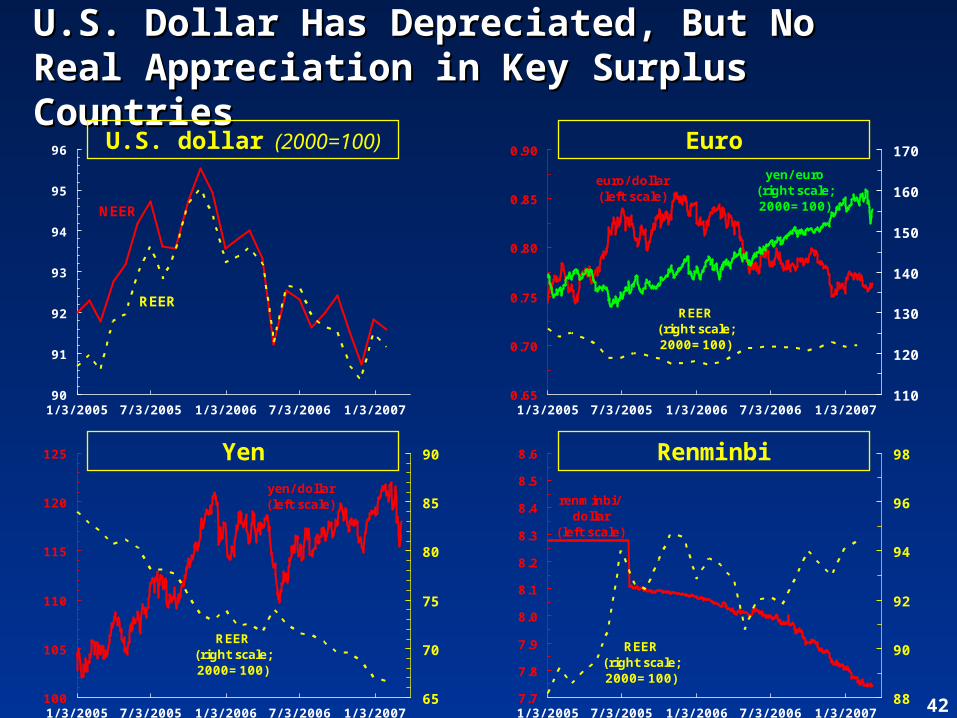

yen/ dollar (left scale)

REER(right scale; 2000=100)

100

105

110

115

120

125

1/ 3/ 2005 7/ 3/ 2005 1/ 3/ 2006 7/ 3/ 2006 1/ 3/ 200765

70

75

80

85

90

euro/ dollar (left scale)

REER(right scale; 2000=100)

yen/ euro (right scale; 2000=100)

0.65

0.70

0.75

0.80

0.85

0.90

1/ 3/ 2005 7/ 3/ 2005 1/ 3/ 2006 7/ 3/ 2006 1/ 3/ 2007110

120

130

140

150

160

170

renminbi/dollar

(left scale)

REER(right scale; 2000=100)

7.7

7.8

7.9

8.0

8.1

8.2

8.3

8.4

8.5

8.6

1/ 3/ 2005 7/ 3/ 2005 1/ 3/ 2006 7/ 3/ 2006 1/ 3/ 200788

90

92

94

96

98

NEER

REER

90

91

92

93

94

95

96

1/ 3/ 2005 7/ 3/ 2005 1/ 3/ 2006 7/ 3/ 2006 1/ 3/ 2007

U.S. Dollar Has Depreciated, But No Real U.S. Dollar Has Depreciated, But No Real Appreciation in Key Surplus CountriesAppreciation in Key Surplus Countries

Yen Renminbi

EuroU.S. dollar (2000=100)

43

-40

-30

-20

-10

0

10

20

30

40

50

60

70

2000 01 02 03 04 05 06 07 08 09 10 11 12

-4

-2

0

2

4

6

8

10

12

14

2000 01 02 03 04 05 06 07 08 09 10 11 12-4

-3

-2

-1

0

1

2

3

4

5

2000 01 02 03 04 05 06 07 08 09 10 11 12

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

2000 01 02 03 04 05 06 07 08 09 10 11 12

China

Saudi Arabia

Euro Area

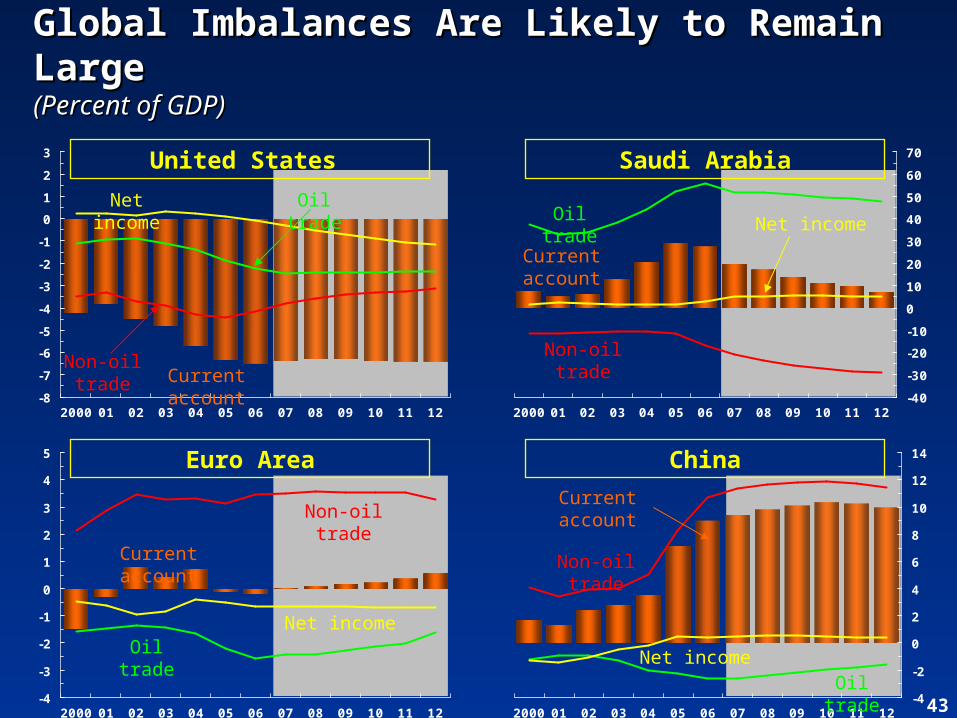

Global Imbalances Are Likely to Remain Global Imbalances Are Likely to Remain LargeLarge(Percent of GDP)(Percent of GDP)

Oil tradeNet income

Non-oil trade

Oil trade Net income

Non-oil trade

United States

Current account

Current account

Non-oil trade

Oil tradeNet income

Current account

Oil tradeNet income

Non-oil trade

Current account

44

-15

-10

-5

0

5

10

199798 99 200001 02 03 04 05 06 07 08 09 10 11 12

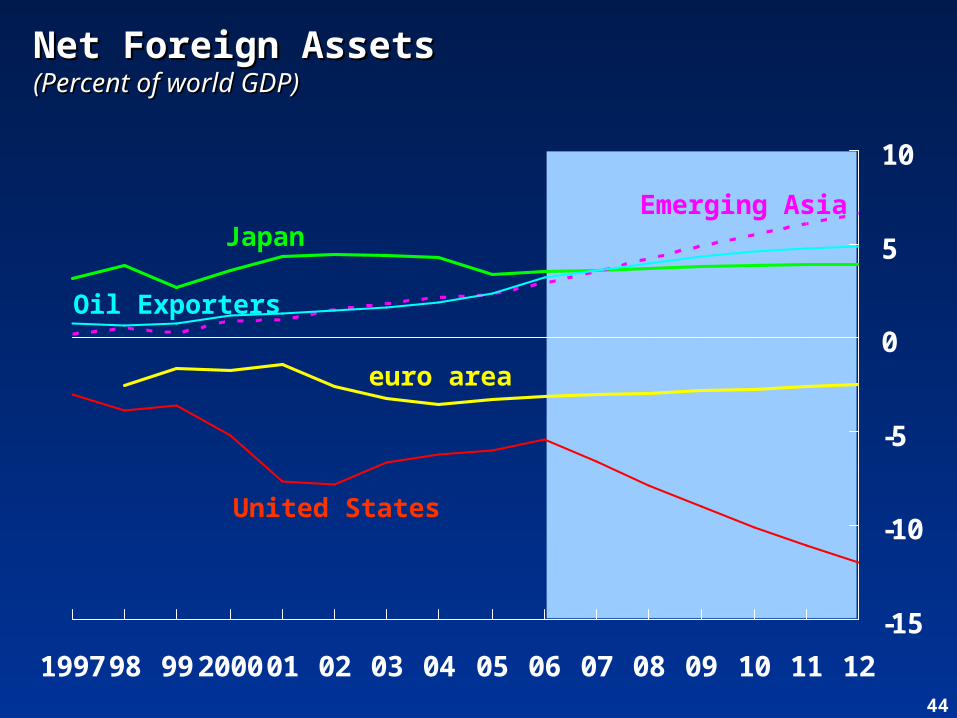

Net Foreign AssetsNet Foreign Assets(Percent of world GDP)(Percent of world GDP)

United States

Japan

euro area

Oil Exporters

Emerging Asia

45

-1

0

1

2

3

4

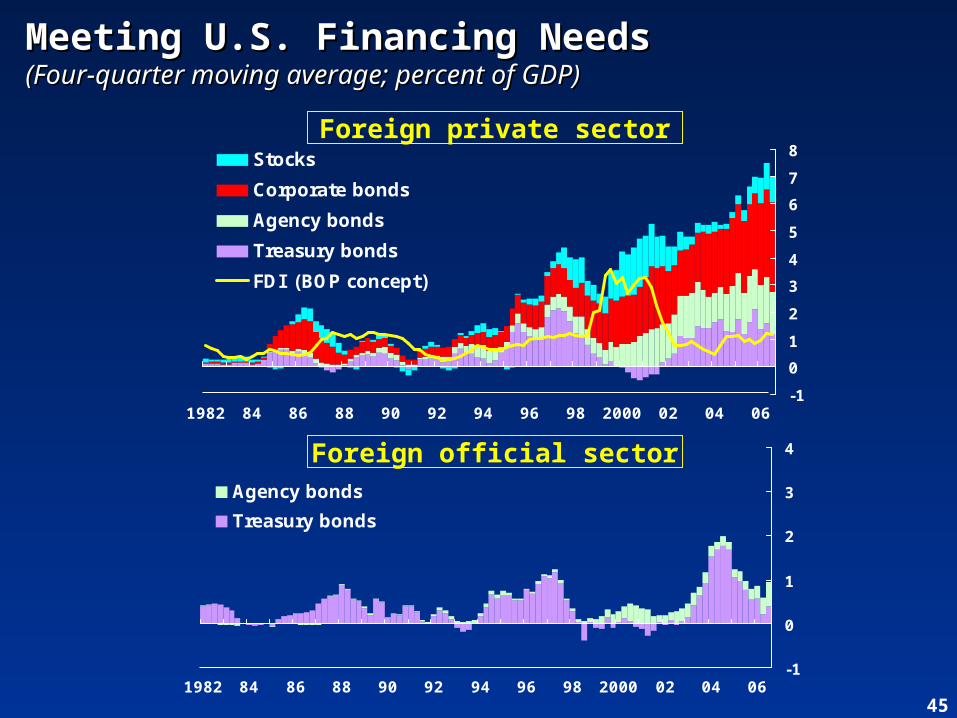

1982 84 86 88 90 92 94 96 98 2000 02 04 06

Agency bonds

Treasury bonds

Foreign official sector

Meeting U.S. Financing NeedsMeeting U.S. Financing Needs(Four-quarter moving average; percent of GDP)(Four-quarter moving average; percent of GDP)

-1

0

1

2

3

4

5

6

7

8

1982 84 86 88 90 92 94 96 98 2000 02 04 06

Stocks

Corporate bonds

Agency bonds

Treasury bonds

FDI (BOP concept)

Foreign private sector

46

Adjustment of Global Imbalances—Adjustment of Global Imbalances—How Could India Be Affected?How Could India Be Affected?

Smooth unwinding led by Smooth unwinding led by rebalancing of domestic demand rebalancing of domestic demand remains the most likely outcome remains the most likely outcome

Potential for “disorderly Potential for “disorderly adjustment”—rapid movement in adjustment”—rapid movement in exchange rates worldwide, volatile exchange rates worldwide, volatile financial conditionsfinancial conditions

Demand rebalancing in the United Demand rebalancing in the United States could imply a prolonged period States could imply a prolonged period of sub-par global growthof sub-par global growth

Risk of rising protectionist pressuresRisk of rising protectionist pressures

47

Critical Challenges for the Global Critical Challenges for the Global EconomyEconomy

Coming in for a soft landing?Coming in for a soft landing?

Bumps in the runway:Bumps in the runway:• The U.S. housing marketThe U.S. housing market• Inflation concerns and the oil Inflation concerns and the oil marketmarket• Financial risks facing emerging Financial risks facing emerging marketsmarkets

Longer-term Challenges:Longer-term Challenges:• Unwinding global imbalancesUnwinding global imbalances• Sustaining global productivity Sustaining global productivity growthgrowth

48

0

2

4

6

8

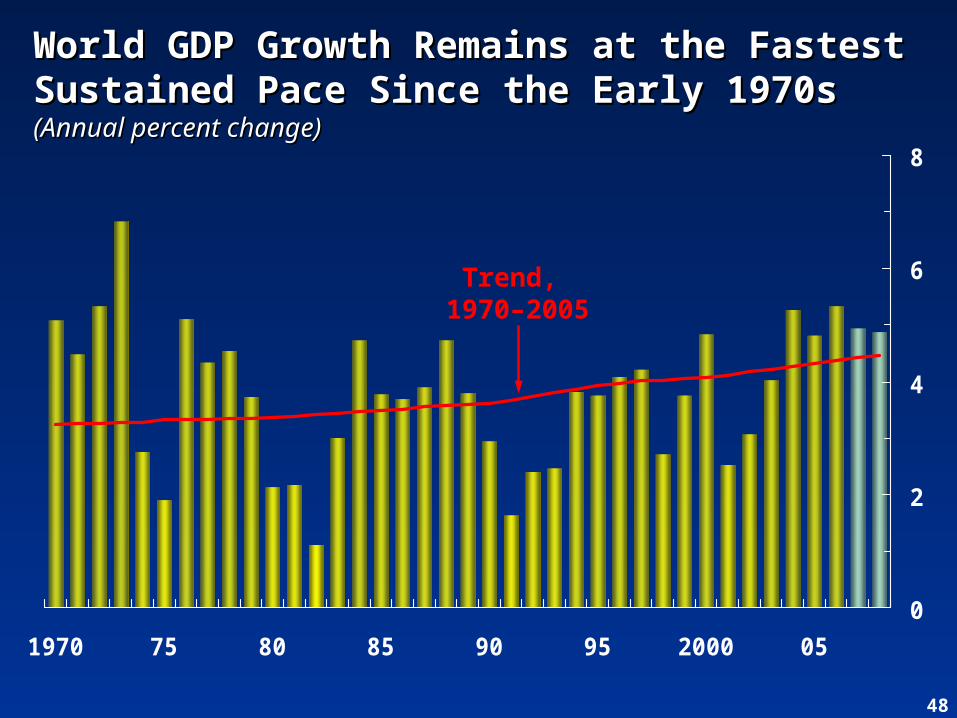

1970 75 80 85 90 95 2000 05

Trend, 1970–2005

World GDP Growth Remains at the Fastest World GDP Growth Remains at the Fastest Sustained Pace Since the Early 1970sSustained Pace Since the Early 1970s(Annual percent change)(Annual percent change)

49

-2

-1

0

1

2

3

4

5

6

1990 92 94 96 98 2000 02 04 06

World

Advanced economies

Emerging markets and developing countries

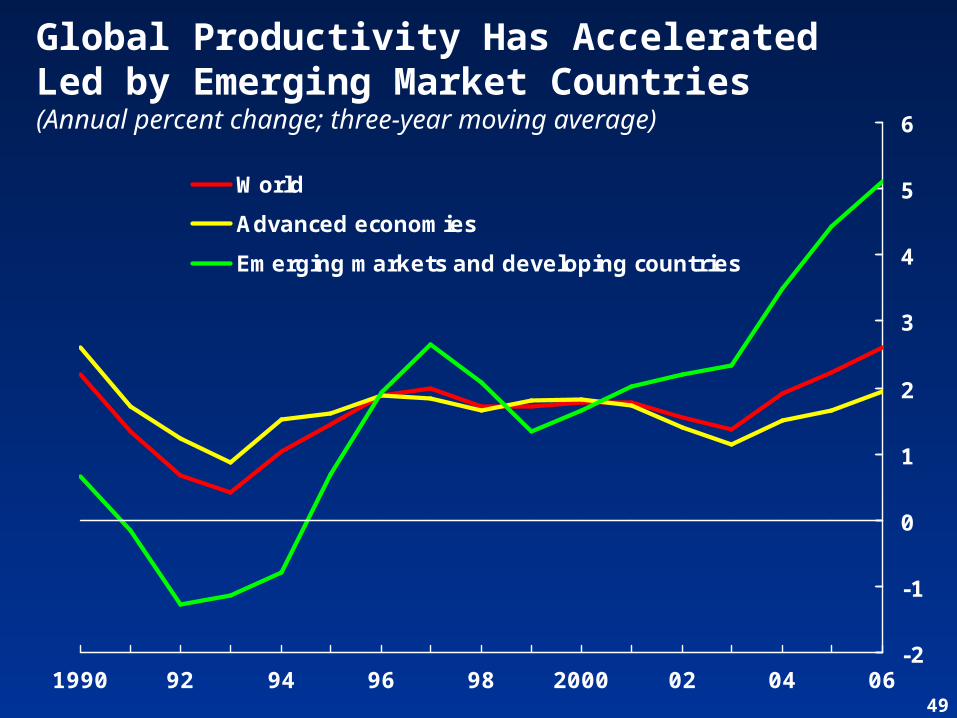

Global Productivity Has Accelerated Led by Emerging Market Countries(Annual percent change; three-year moving average)

50

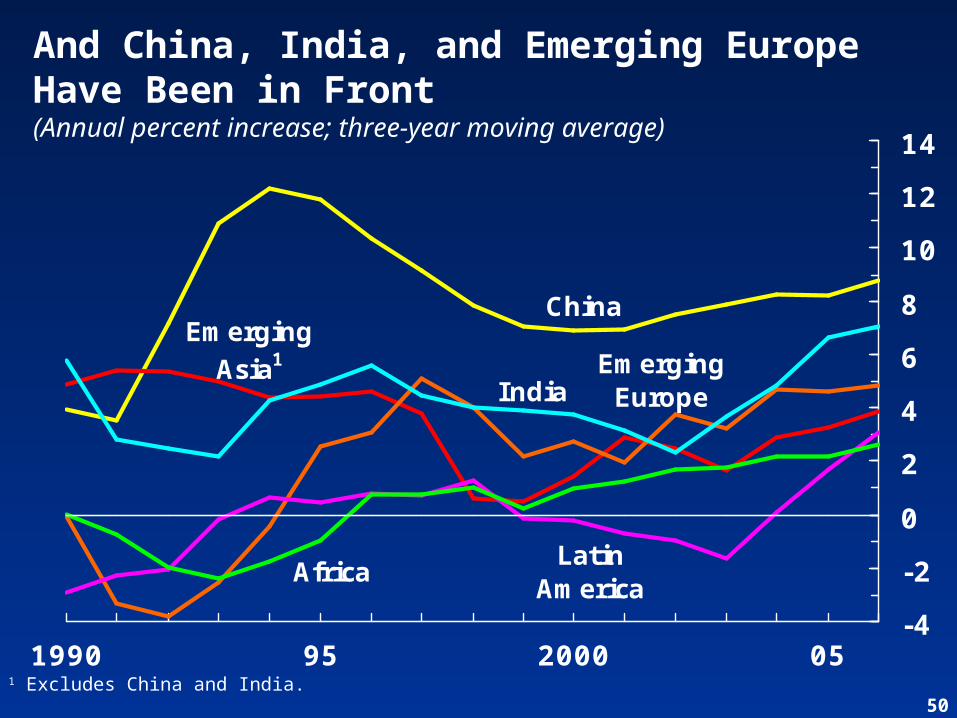

ChinaEmerging

Asia1 Emerging Europe

Latin America

Africa

India

-4

-2

0

2

4

6

8

10

12

14

1990 95 2000 05

And China, India, and Emerging Europe Have Been in Front(Annual percent increase; three-year moving average)

1 Excludes China and India.

51

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Asia Advancedeconomiesexcl. Asia

LatinAmerica andCaribbean

Physical capital accumulationHuman capital accumulationTFP growth

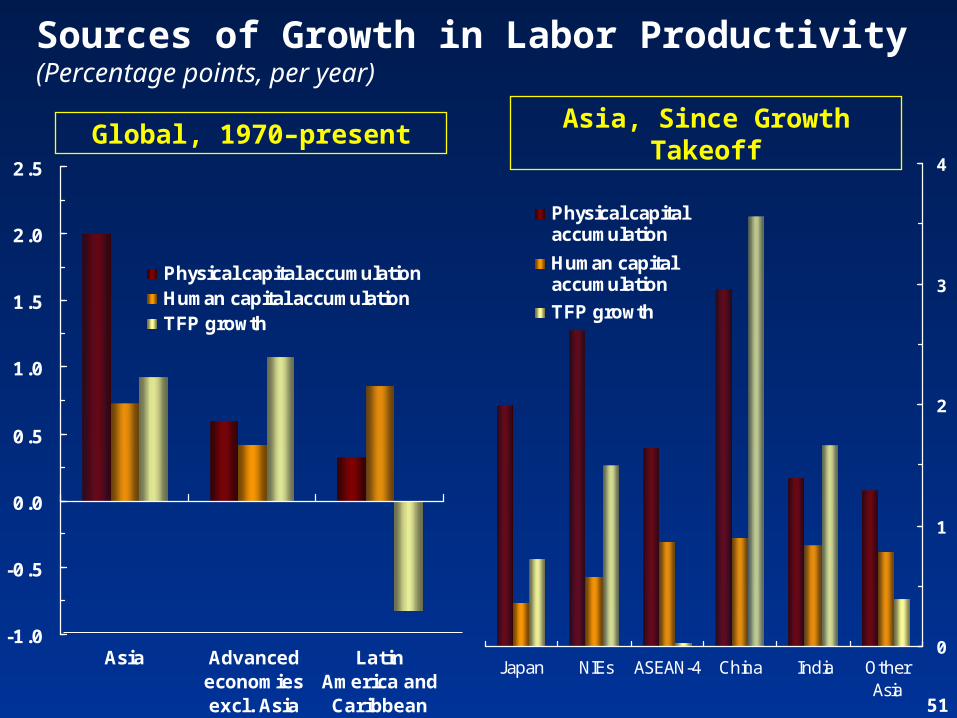

Sources of Growth in Labor Productivity(Percentage points, per year)

0

1

2

3

4

Japan NIEs ASEAN-4 China India OtherAsia

Physical capitalaccumulation

Human capitalaccumulation

TFP growth

Global, 1970–presentAsia, Since Growth

Takeoff

52

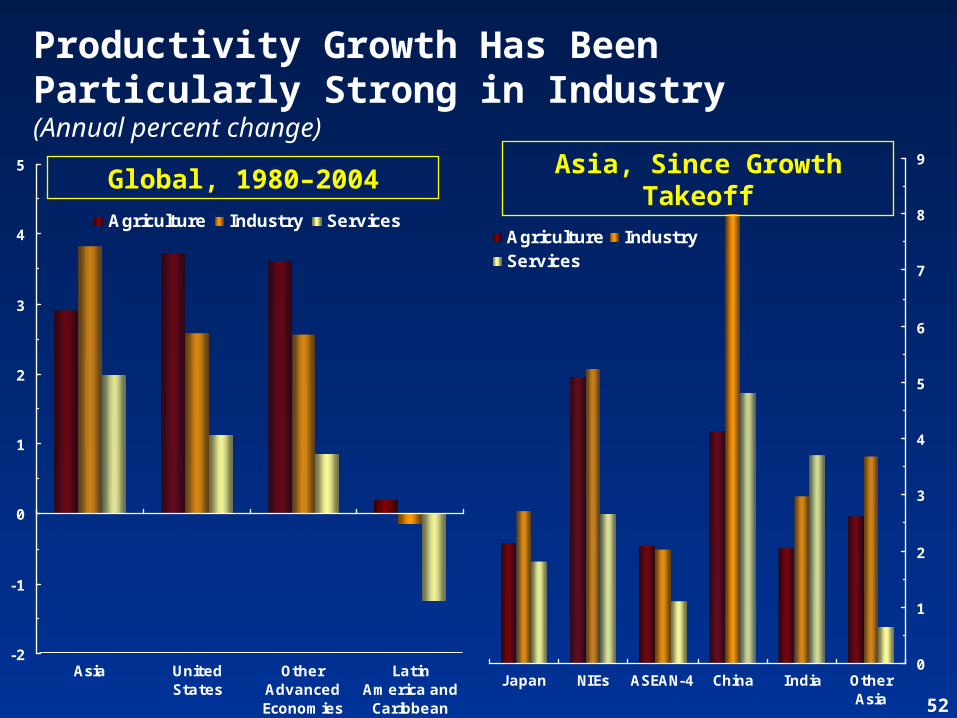

Productivity Growth Has Been Particularly Strong in Industry(Annual percent change)

-2

-1

0

1

2

3

4

5

Asia UnitedStates

OtherAdvancedEconomies

LatinAmerica andCaribbean

Agriculture Industry Services

0

1

2

3

4

5

6

7

8

9

Japan NIEs ASEAN-4 China India OtherAsia

Agriculture IndustryServices

Global, 1980–2004 Asia, Since Growth Takeoff

53

-1

0

1

2

3

4

5

6

7

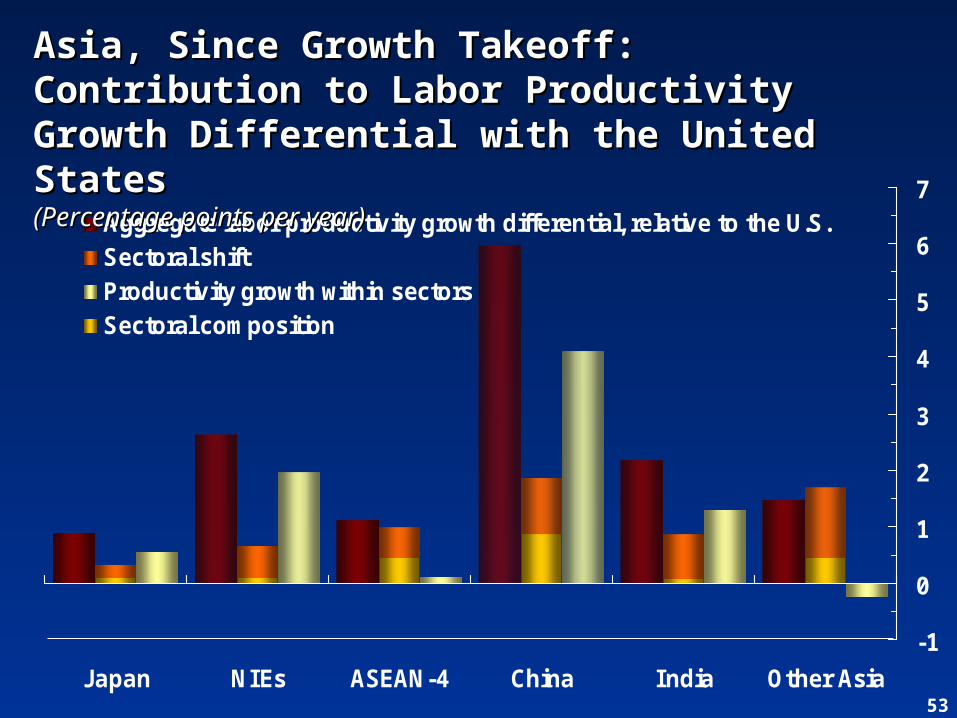

Japan NIEs ASEAN-4 China India Other Asia

Aggregate labor productivity growth differential, relative to the U.S.Sectoral shiftProductivity growth within sectorsSectoral composition

Asia, Since Growth Takeoff: Contribution Asia, Since Growth Takeoff: Contribution to Labor Productivity Growth Differential to Labor Productivity Growth Differential with the United Stateswith the United States(Percentage points per year)(Percentage points per year)

54

Industry

Services

Agriculture

10

20

30

40

50

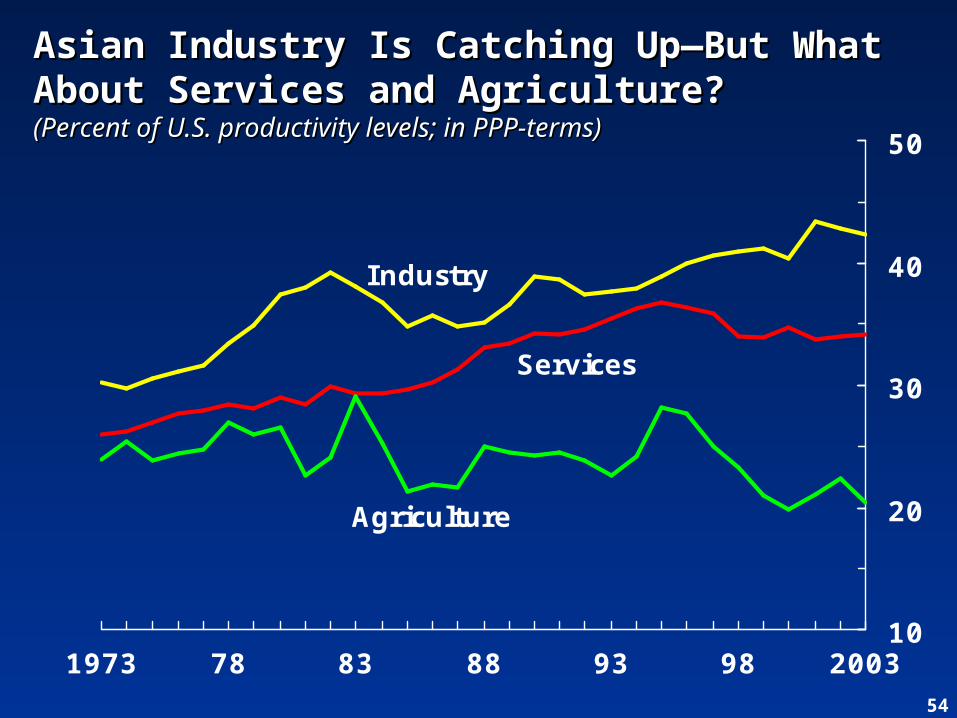

1973 78 83 88 93 98 2003

Asian Industry Is Catching Up—But What Asian Industry Is Catching Up—But What About Services and Agriculture?About Services and Agriculture?(Percent of U.S. productivity levels; in PPP-terms)(Percent of U.S. productivity levels; in PPP-terms)

55

1 2 3 4 50

2

4

6

8

10

12

1 2 3 4 50

2

4

6

8

10

12

1 2 3 4 5

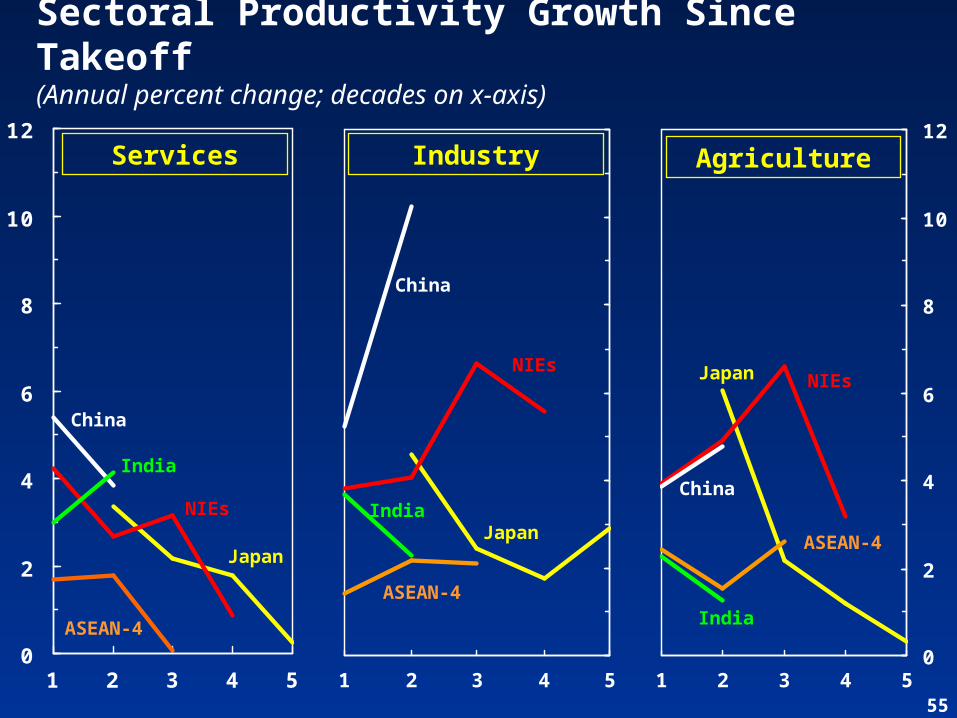

Sectoral Productivity Growth Since Takeoff(Annual percent change; decades on x-axis)

AgricultureIndustryServices

Japan

NIEs

ASEAN-4

China

India

Japan

ASEAN-4

NIEs

China

India

Japan NIEs

ASEAN-4

India

China

56

High growth countries

World

20

30

40

50

60

70

80

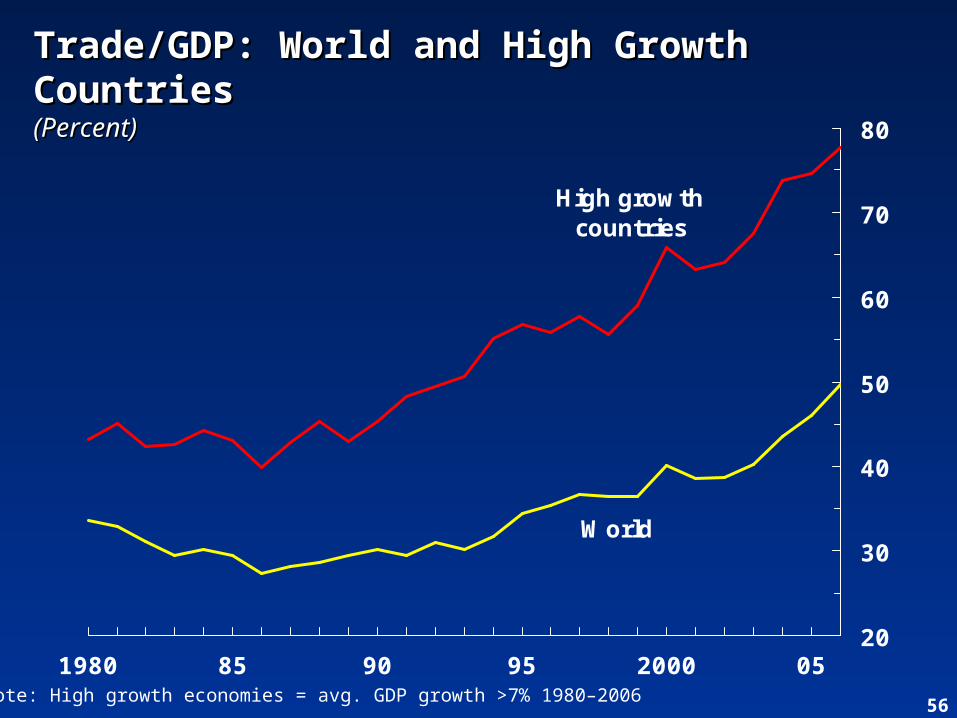

1980 85 90 95 2000 05Note: High growth economies = avg. GDP growth >7% 1980–2006

Trade/GDP: World and High Growth Trade/GDP: World and High Growth CountriesCountries(Percent)(Percent)

57

Sustaining Global Productivity GrowthSustaining Global Productivity Growth

Domestic market reforms can help to Domestic market reforms can help to sustain rapid productivity growth in sustain rapid productivity growth in emerging market and developing emerging market and developing countriescountries

Further steps to remove trade Further steps to remove trade barriers—both unilateral and barriers—both unilateral and multilateral—are also crucialmultilateral—are also crucial

But greater attention must be paid But greater attention must be paid both in advanced and developing both in advanced and developing countries to make sure that the fruits countries to make sure that the fruits of globalization are well distributedof globalization are well distributed

58

Notwithstanding recent volatility Notwithstanding recent volatility and U.S. slowdown, continued robust and U.S. slowdown, continued robust global growth still looks the most global growth still looks the most likely outcome.likely outcome.

Policy makers and financial markets Policy makers and financial markets around the world need to be ready for around the world need to be ready for surprises.surprises.

Take advantage of good times to Take advantage of good times to tackle structural impediments to tackle structural impediments to sustained growth.sustained growth.

In Conclusion:In Conclusion:

Download the WEODownload the WEO

http://www.imf.org/weohttp://www.imf.org/weo

60

Working-age

population

Total labor force

Export-weighted

labor

force1

0

50

100

150

200

250

300

350

400

1980 85 90 95 2000 05

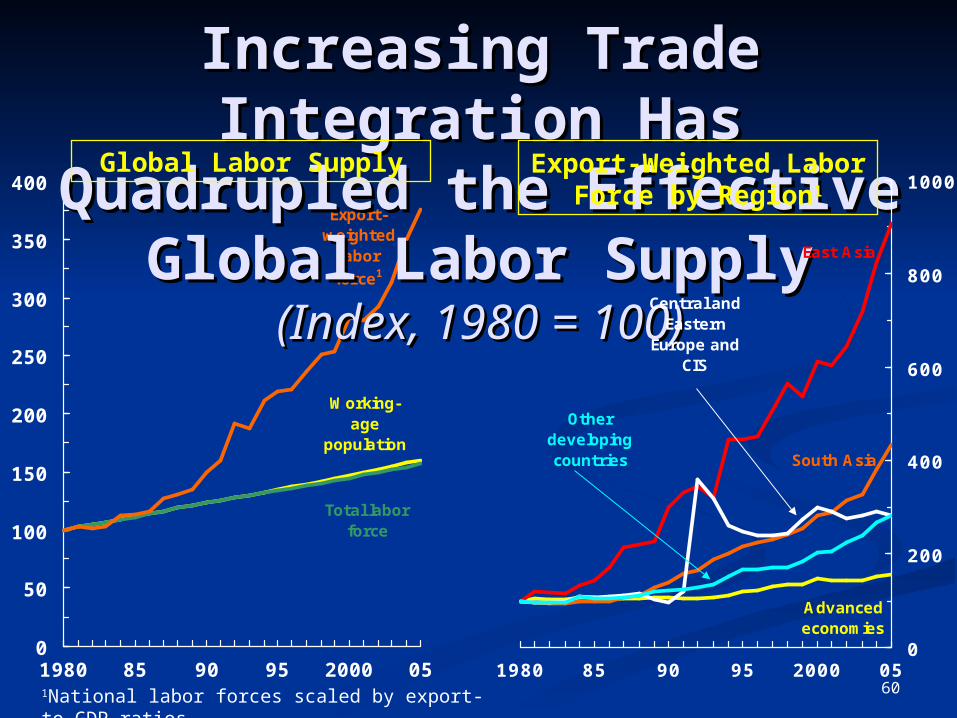

Increasing Trade Increasing Trade Integration Has Integration Has

Quadrupled the Effective Quadrupled the Effective Global Labor SupplyGlobal Labor Supply

(Index, 1980 = 100)(Index, 1980 = 100)

Global Labor Supply

Advanced economies

East Asia

South Asia

Central and Eastern

Europe and CIS

Other developing countries

0

200

400

600

800

1000

1980 85 90 95 2000 05

Export-Weighted Labor Force by

Region1

1National labor forces scaled by export-to-GDP ratios.

61

0

2

4

6

8

10

Latin America EmergingEurope

Asia Middle East Africa

2005 2006 2007 2008

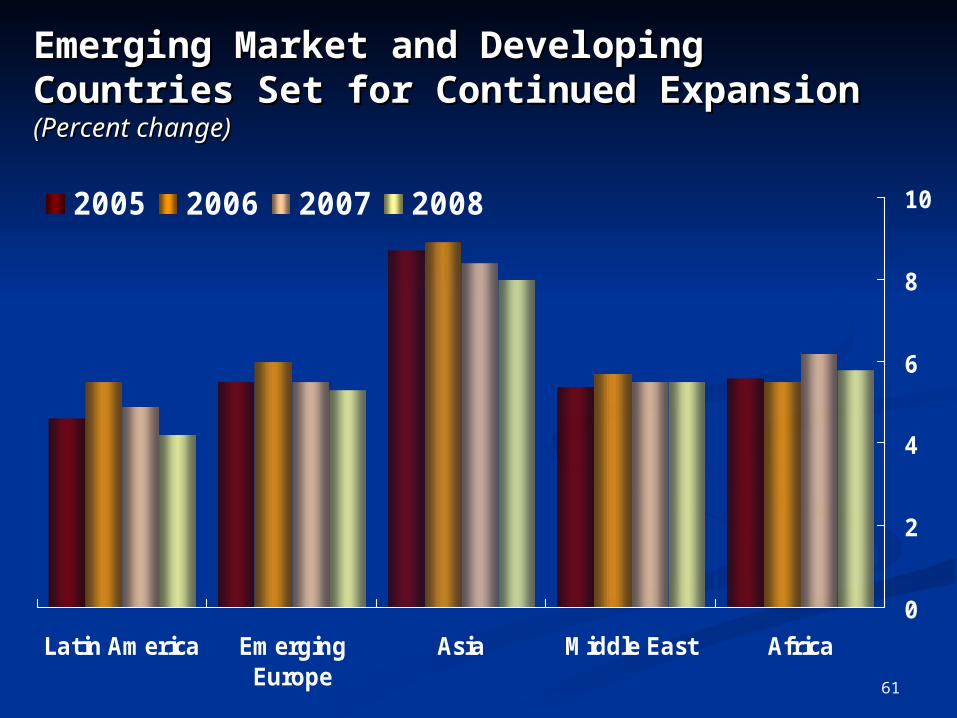

Emerging Market and Developing Emerging Market and Developing Countries Set for Continued ExpansionCountries Set for Continued Expansion(Percent change)(Percent change)

62

Saving

Investment

20

21

22

23

24

25

26

1970 75 80 85 90 95 2000 05

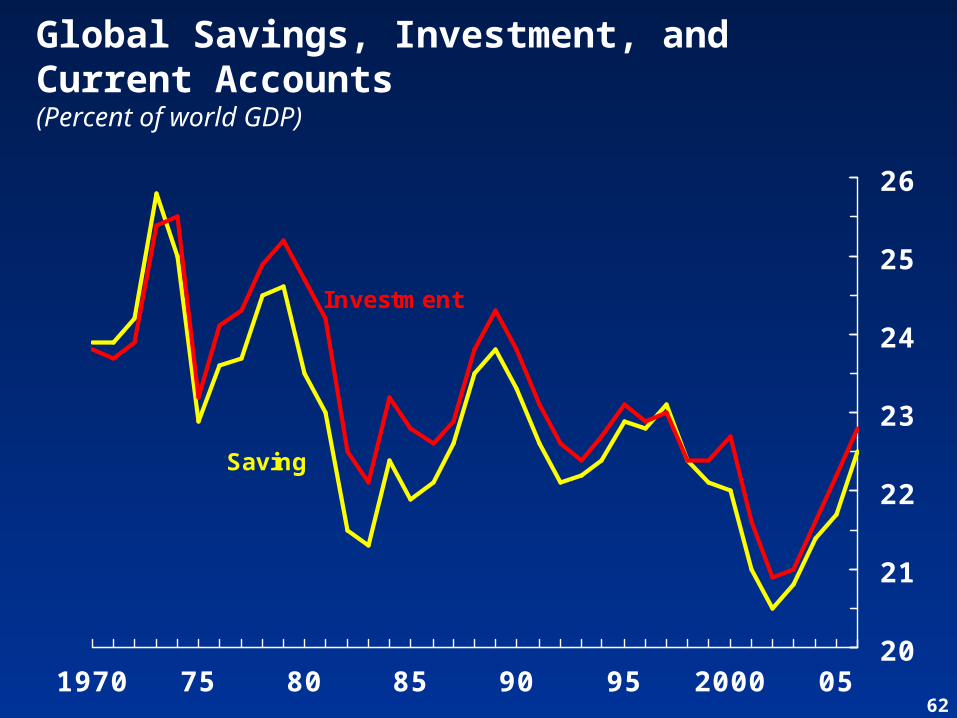

Global Savings, Investment, and Current Accounts(Percent of world GDP)

63

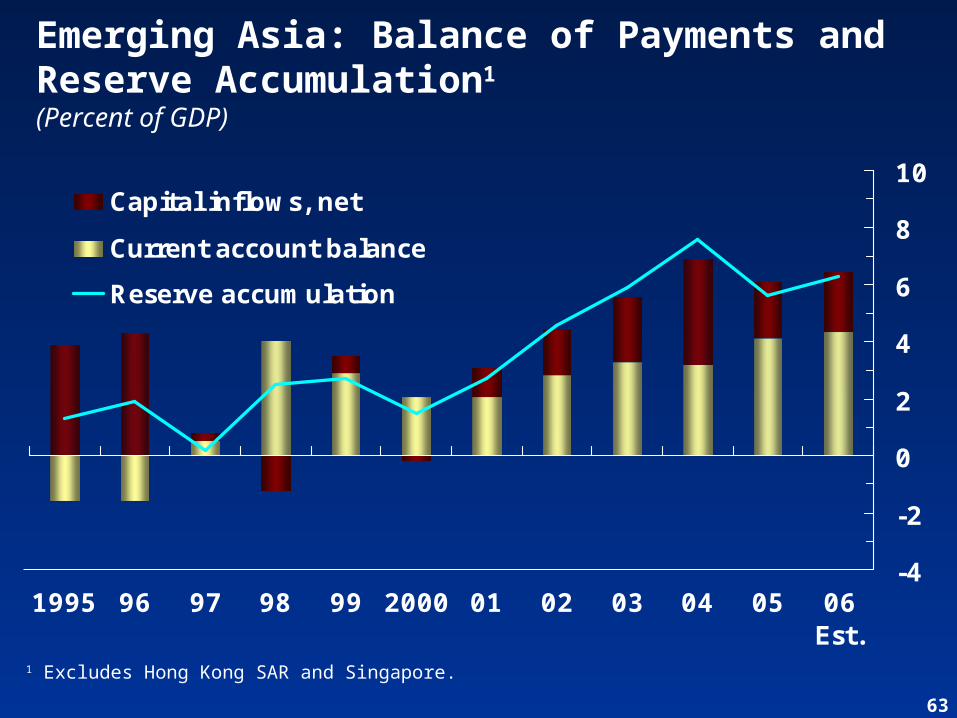

Emerging Asia: Balance of Payments and Reserve Accumulation1

(Percent of GDP)

-4

-2

0

2

4

6

8

10

1995 96 97 98 99 2000 01 02 03 04 05 06Est.

Capital inflows, net

Current account balance

Reserve accumulation

1 Excludes Hong Kong SAR and Singapore.

64

10

20

30

40

50

60

70

1970 75 80 85 90 95 2000 05-10

-8

-6

-4

-2

0

2

4

6

8

10

10

20

30

40

50

60

70

1970 75 80 85 90 95 2000 05-10

-8

-6

-4

-2

0

2

4

6

8

10

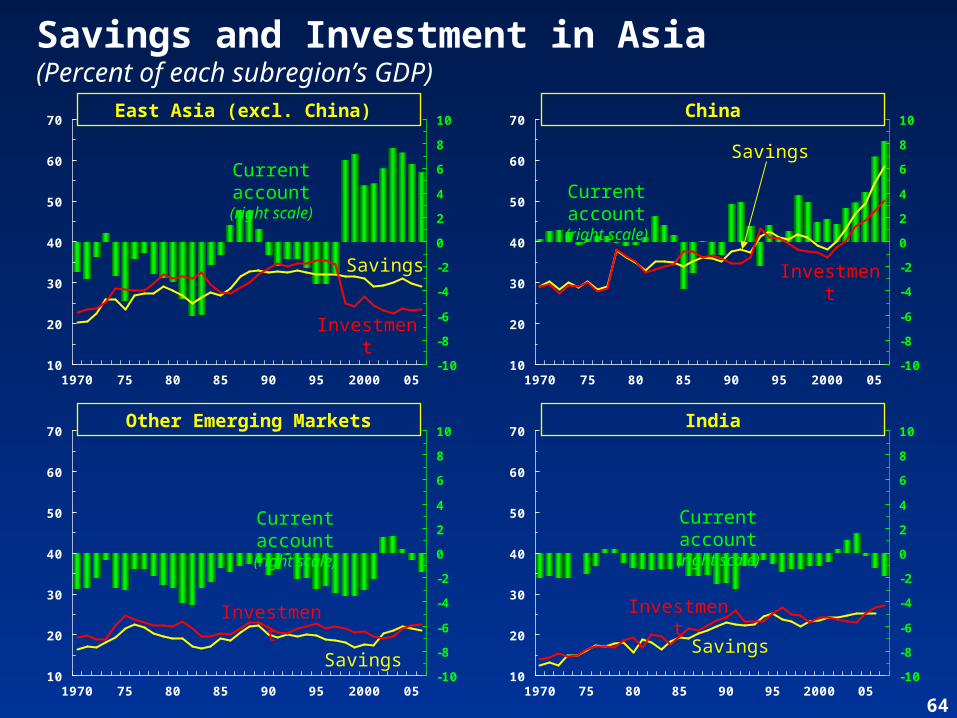

Savings and Investment in Asia(Percent of each subregion’s GDP)

Savings

Investment

IndiaOther Emerging Markets

ChinaEast Asia (excl. China)

Current account

(right scale)

Savings

Investment

Current account

(right scale)

10

20

30

40

50

60

70

1970 75 80 85 90 95 2000 05-10

-8

-6

-4

-2

0

2

4

6

8

10

10

20

30

40

50

60

70

1970 75 80 85 90 95 2000 05-10

-8

-6

-4

-2

0

2

4

6

8

10

Savings

Investment

Current account

(right scale)

Savings

Current account

(right scale)

Investment

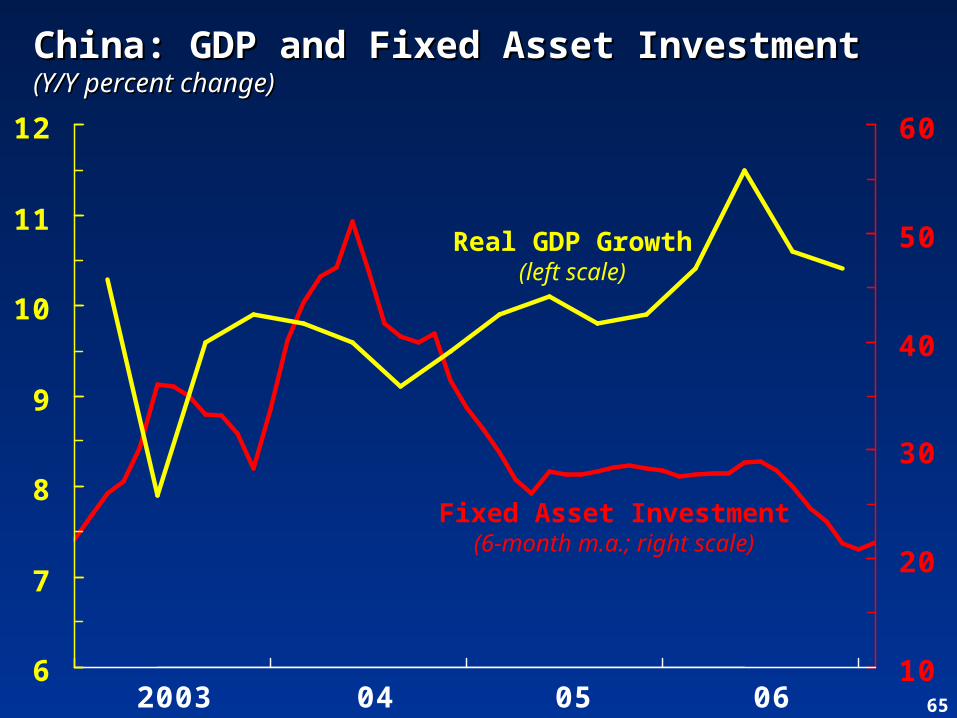

65060504200310

20

30

40

50

60

6

7

8

9

10

11

12

China: GDP and Fixed Asset InvestmentChina: GDP and Fixed Asset Investment(Y/Y percent change)(Y/Y percent change)

Fixed Asset Investment(6-month m.a.; right scale)

Real GDP Growth(left scale)

66

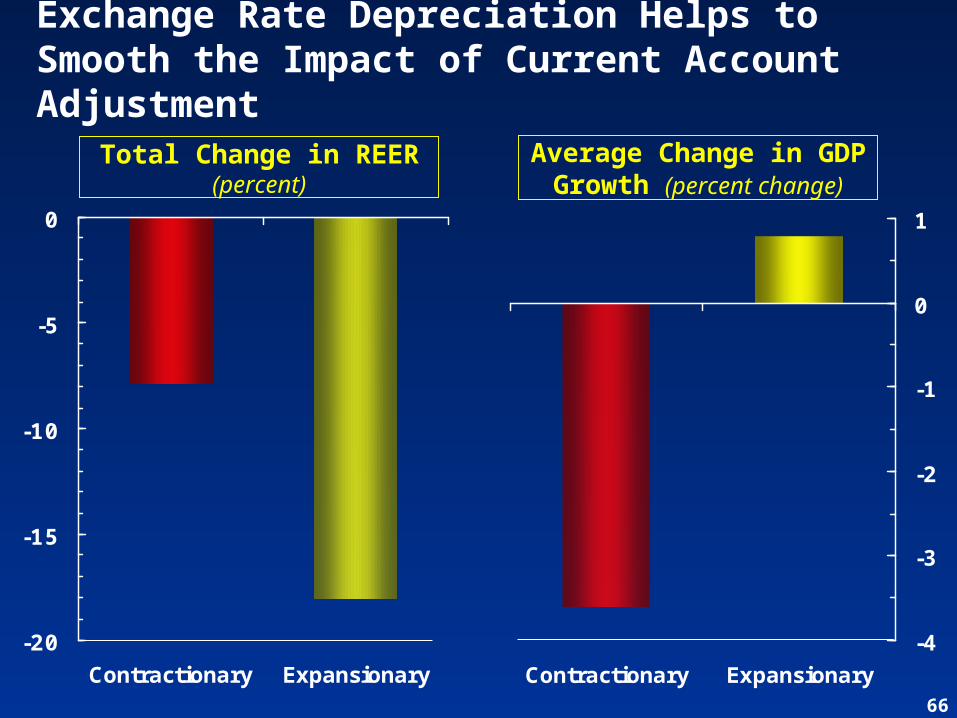

Exchange Rate Depreciation Helps to Smooth the Impact of Current Account Adjustment

-20

-15

-10

-5

0

Contractionary Expansionary

Total Change in REER(percent)

Average Change in GDP Growth (percent change)

-4

-3

-2

-1

0

1

Contractionary Expansionary

67

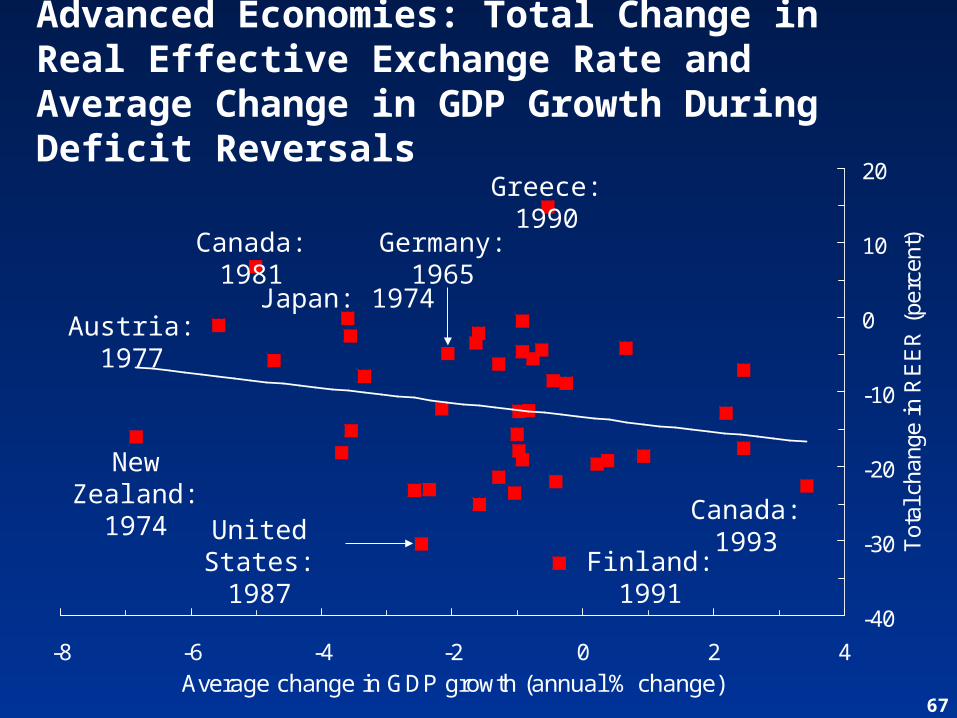

Advanced Economies: Total Change in Real Effective Exchange Rate and Average Change in GDP Growth During Deficit Reversals

-40

-30

-20

-10

0

10

20

-8 -6 -4 -2 0 2 4Average change in GDP growth (annual % change)

Tot

al c

hang

e in

RE

ER

(pe

rcen

t)

Greece: 1990

Germany: 1965

Japan: 1974

Canada: 1981

Austria: 1977

New Zealand:

1974 United States: 1987 Finland:

1991

Canada: 1993

68

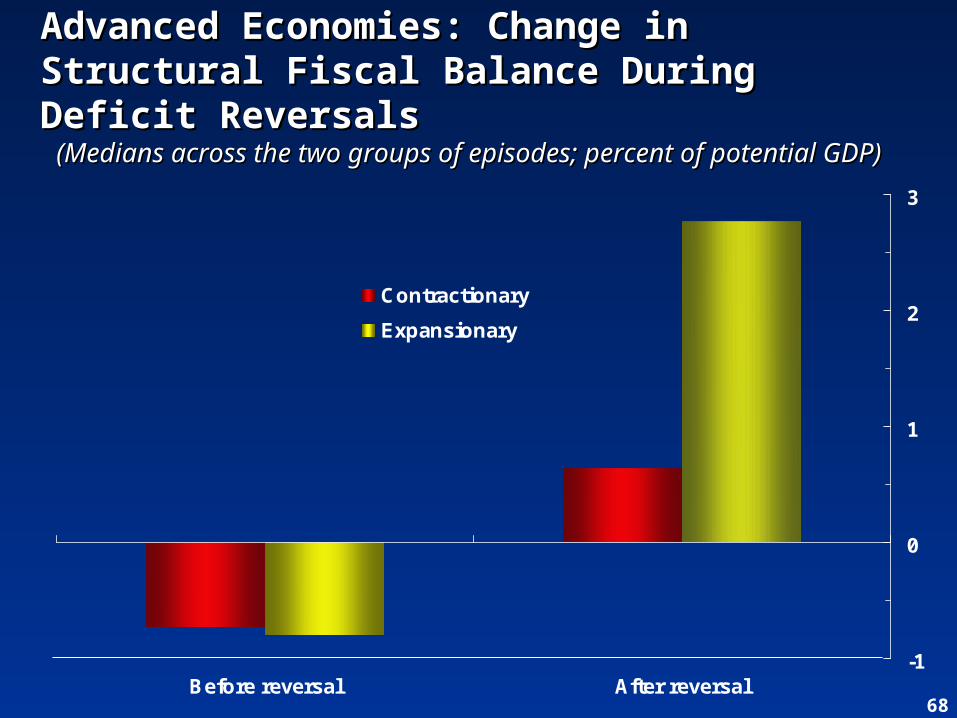

Advanced Economies: Change in Advanced Economies: Change in Structural Fiscal Balance During Deficit Structural Fiscal Balance During Deficit ReversalsReversals (Medians across the two groups of episodes; percent of (Medians across the two groups of episodes; percent of potential GDP)potential GDP)

-1

0

1

2

3

Before reversal After reversal

Contractionary

Expansionary

69

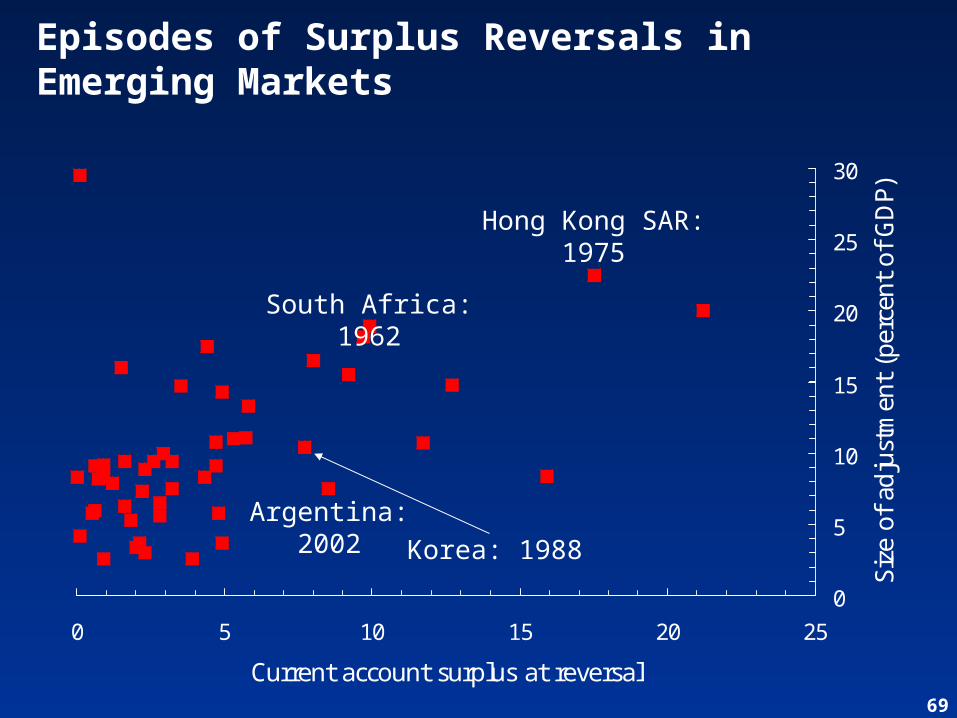

Episodes of Surplus Reversals in Emerging Markets

0

5

10

15

20

25

30

0 5 10 15 20 25

Current account surplus at reversal

Size

of ad

just

men

t (p

erce

nt o

f G

DP)

Hong Kong SAR: 1975

South Africa: 1962

Korea: 1988Argentina:

2002

70

95

100

105

110

115

-5 -4 -3 -2 -1 0 +1 +2 +3 +4 +5

0

4

8

12

16

20

24

-5 -4 -3 -2 -1 0 +1 +2 +3 +4 +5

4

6

8

10

12

-5 -4 -3 -2 -1 0 +1 +2 +3 +4 +5

2

3

4

5

6

7

8

-5 -4 -3 -2 -1 0 +1 +2 +3 +4 +5

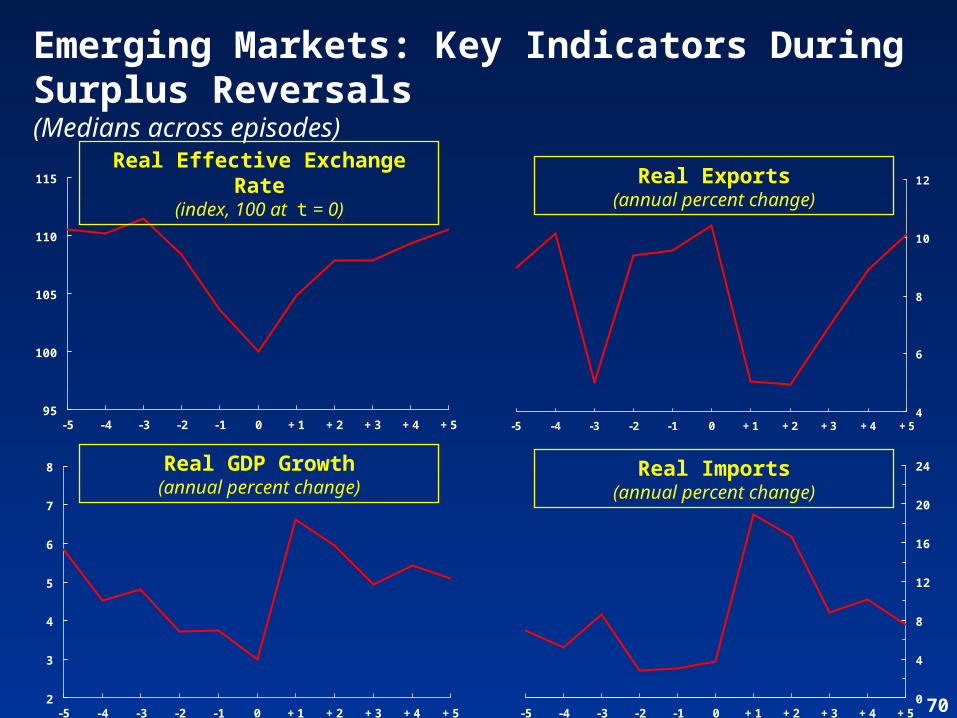

Emerging Markets: Key Indicators During Surplus Reversals(Medians across episodes)

Real GDP Growth(annual percent change)

Real Effective Exchange Rate

(index, 100 at t = 0)

Real Exports(annual percent change)

Real Imports(annual percent change)

71

-0.6

-0.3

0.0

0.3

0.6

0.9

1.2

t - 4 t = 0 t + 4 t + 8

Current cycle

Mid-cycle pauses

Recessions

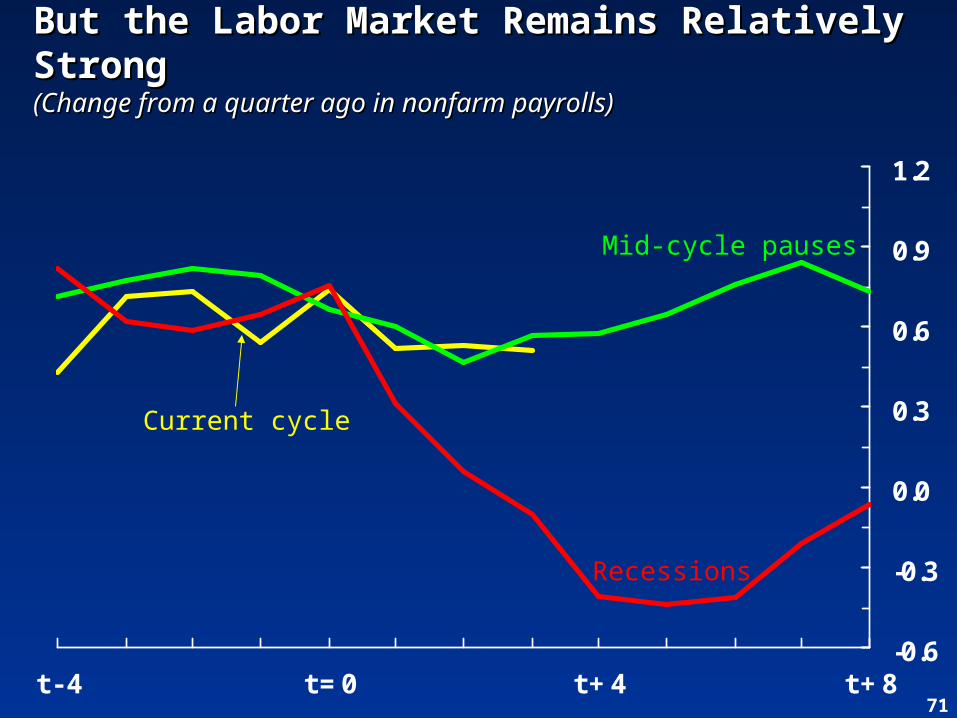

But the Labor Market Remains Relatively But the Labor Market Remains Relatively StrongStrong(Change from a quarter ago in nonfarm payrolls)(Change from a quarter ago in nonfarm payrolls)

72

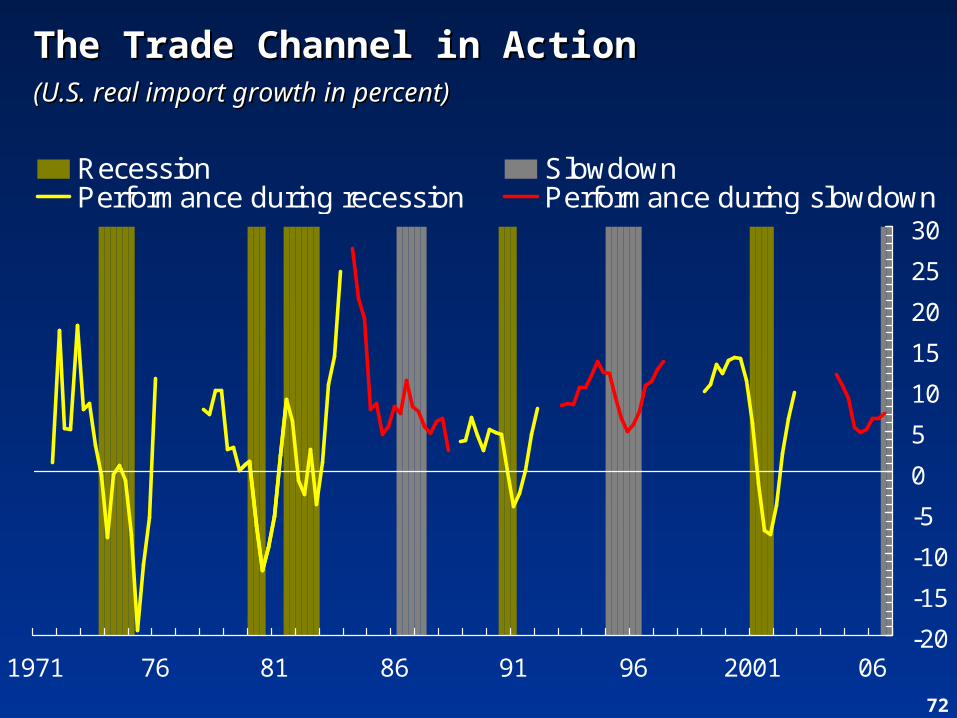

The Trade Channel in ActionThe Trade Channel in Action(U.S. real import growth in percent)(U.S. real import growth in percent)

-20

-15

-10

-5

0

5

10

15

20

25

30

1971 76 81 86 91 96 2001 06

Recession SlowdownPerformance during recession Performance during slowdown

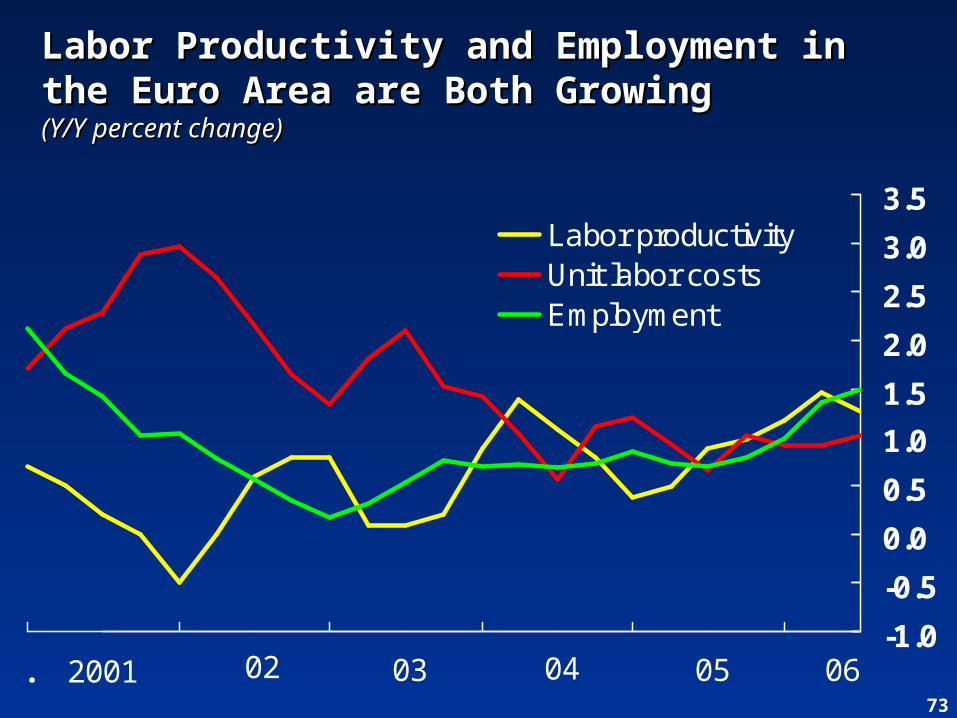

73

Labor Productivity and Employment in Labor Productivity and Employment in the Euro Area are Both Growingthe Euro Area are Both Growing(Y/Y percent change)(Y/Y percent change)

2001 02 03 04 05 06-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

.

Labor productivityUnit labor costsEmployment

74

0

1

2

3

4

5

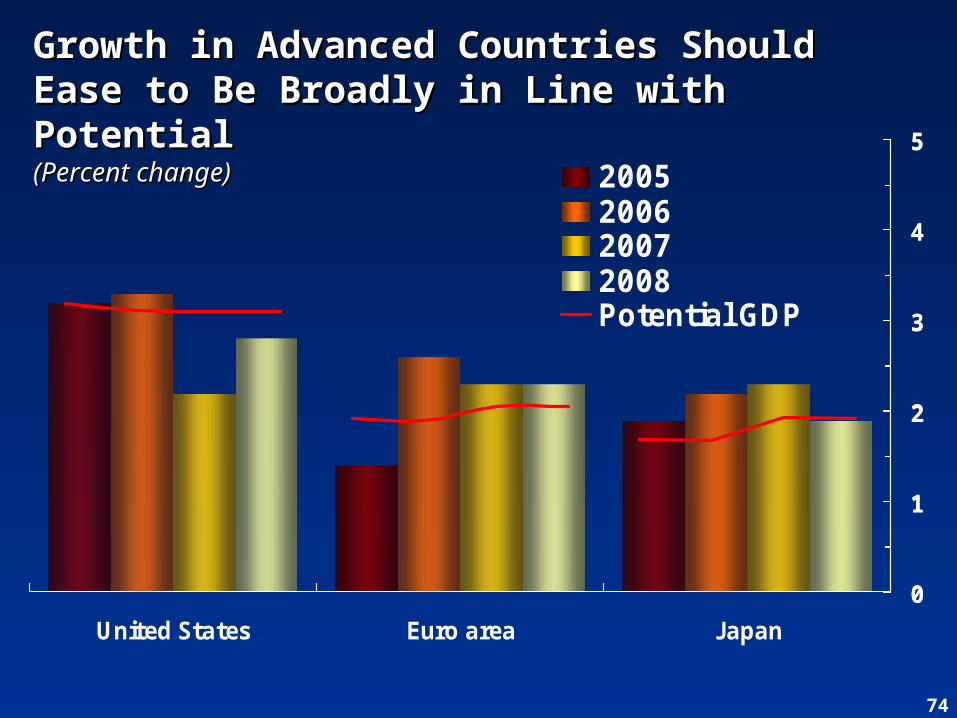

United States Euro area Japan

2005200620072008Potential GDP

0

1

2

3

4

5

Growth in Advanced Countries Should Growth in Advanced Countries Should Ease to Be Broadly in Line with PotentialEase to Be Broadly in Line with Potential(Percent change)(Percent change)

752002 03 04 05 06 07 08

50

100

150

200

250

300

350

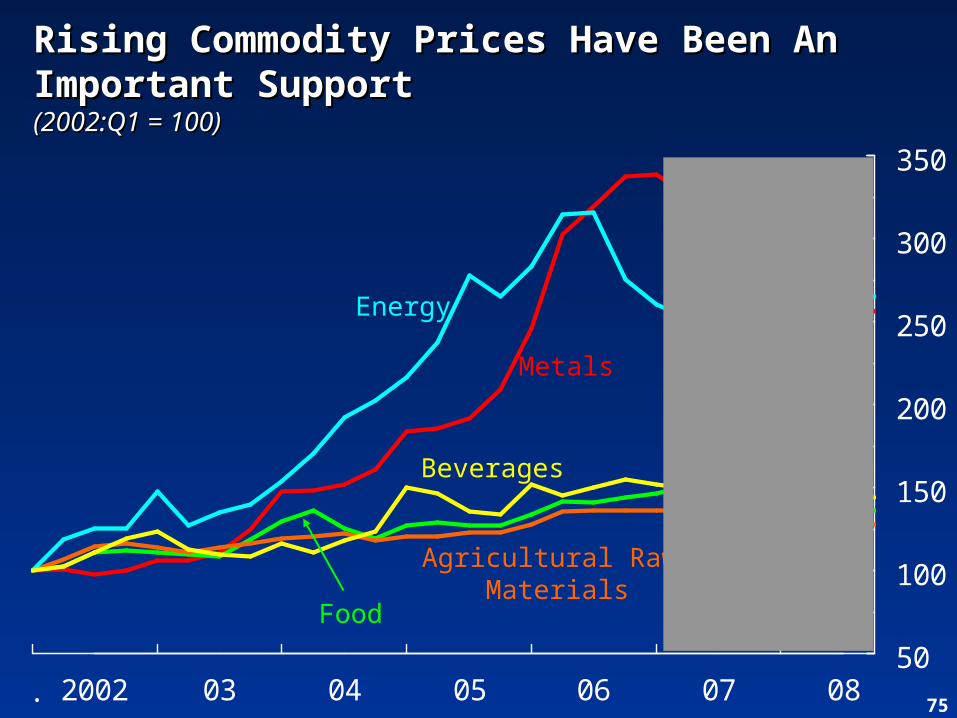

.

Metals

Beverages

Energy

Food

Agricultural Raw Materials

Rising Commodity Prices Have Been An Rising Commodity Prices Have Been An Important SupportImportant Support(2002:Q1 = 100)(2002:Q1 = 100)

76

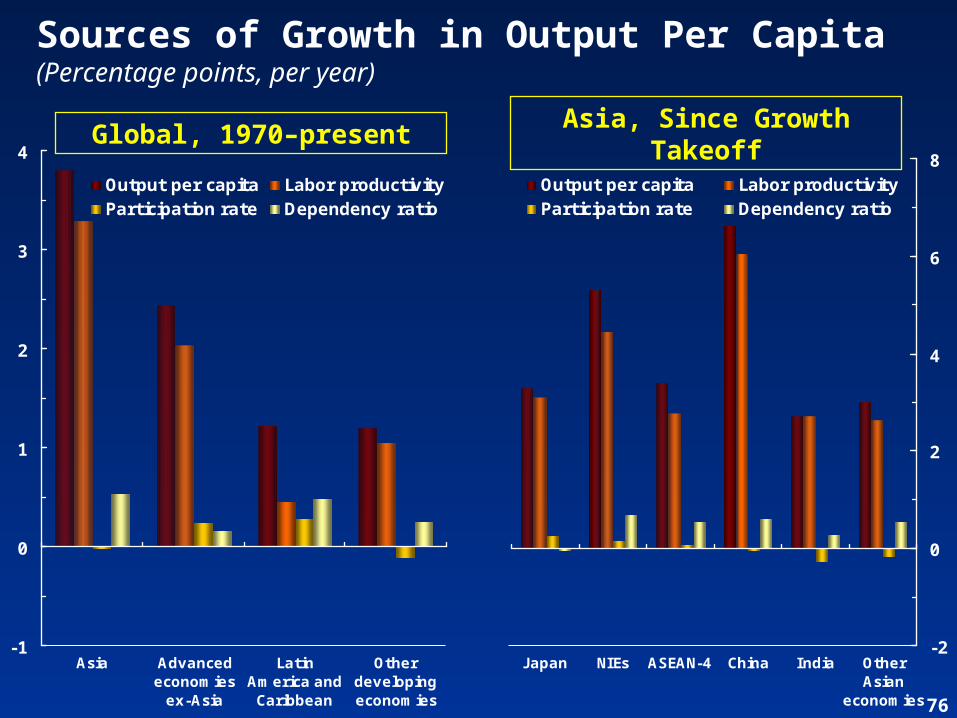

Sources of Growth in Output Per Capita(Percentage points, per year)

-1

0

1

2

3

4

Asia Advancedeconomies

ex-Asia

LatinAmerica andCaribbean

Otherdevelopingeconomies

Output per capita Labor productivityParticipation rate Dependency ratio

-2

0

2

4

6

8

J apan NIEs ASEAN-4 China India OtherAsian

economies

Output per capita Labor productivityParticipation rate Dependency ratio

Global, 1970–presentAsia, Since Growth

Takeoff

77

-40

-30

-20

-10

0

10

20

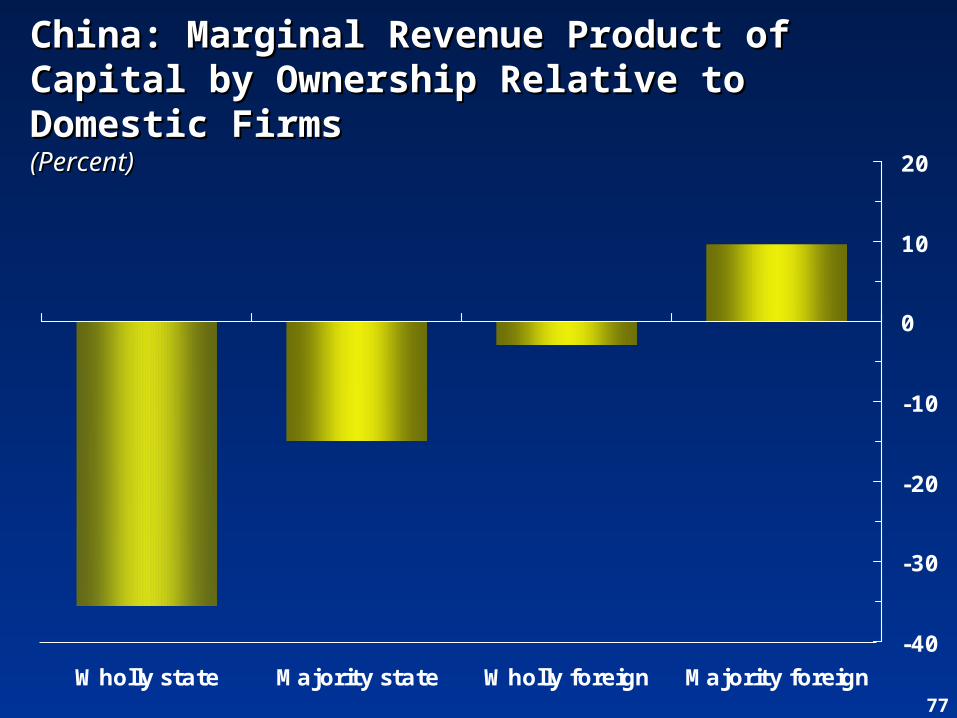

Wholly state Majority state Wholly foreign Majority foreign

China: Marginal Revenue Product of China: Marginal Revenue Product of Capital by Ownership Relative to Capital by Ownership Relative to Domestic FirmsDomestic Firms(Percent)(Percent)

78

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

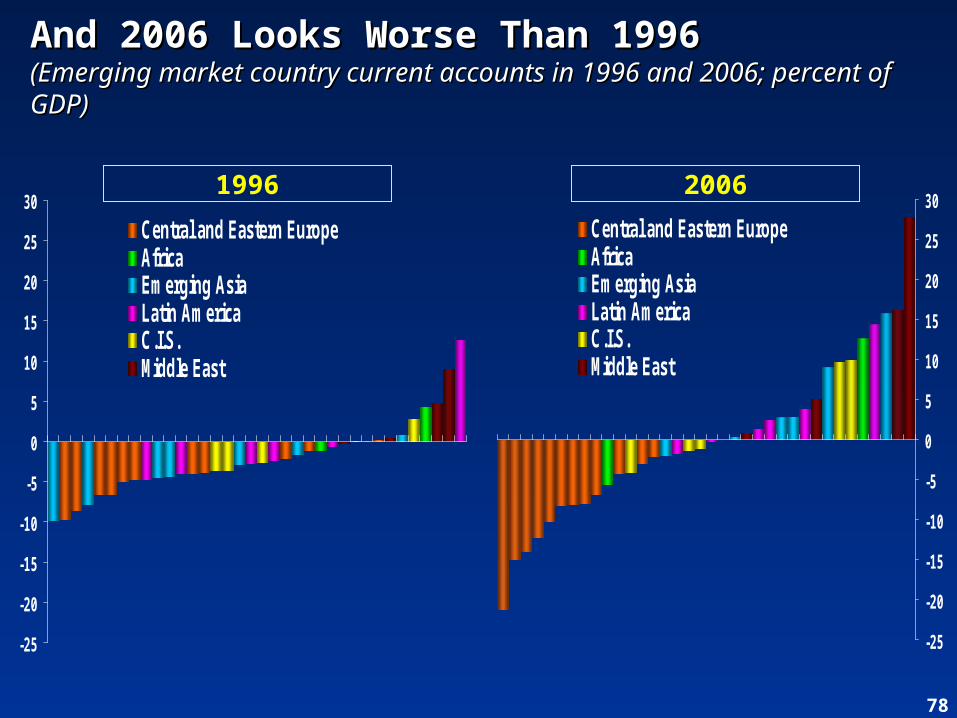

Central and Eastern EuropeAfricaEmerging AsiaLatin AmericaC.I.S.Middle East

And 2006 Looks Worse Than 1996And 2006 Looks Worse Than 1996(Emerging market country current accounts in 1996 and 2006; (Emerging market country current accounts in 1996 and 2006; percent of GDP)percent of GDP)

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

Central and Eastern EuropeAfricaEmerging AsiaLatin AmericaC.I.S.Middle East

1996 2006

79

80

100

120

140

160

180

200

1980 85 90 95 2000 05

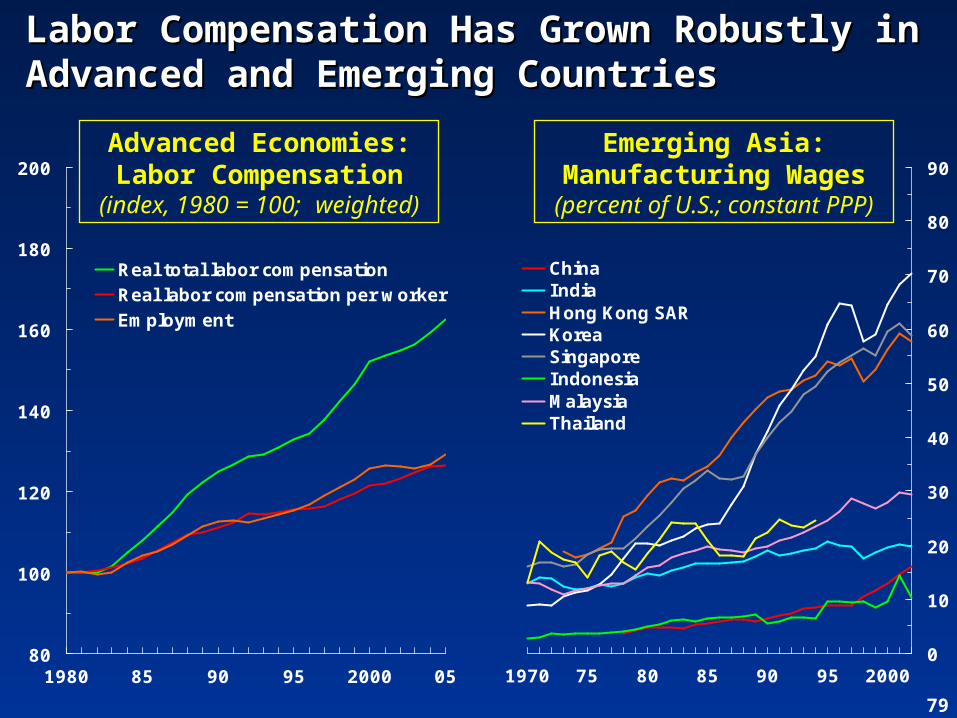

Real total labor compensationReal labor compensation per workerEmployment

Labor Compensation Has Grown Robustly Labor Compensation Has Grown Robustly in Advanced and Emerging Countriesin Advanced and Emerging Countries

0

10

20

30

40

50

60

70

80

90

1970 75 80 85 90 95 2000

ChinaIndiaHong Kong SARKoreaSingaporeIndonesiaMalaysiaThailand

Emerging Asia: Manufacturing Wages(percent of U.S.; constant

PPP)

Advanced Economies: Labor Compensation

(index, 1980 = 100; weighted)

80

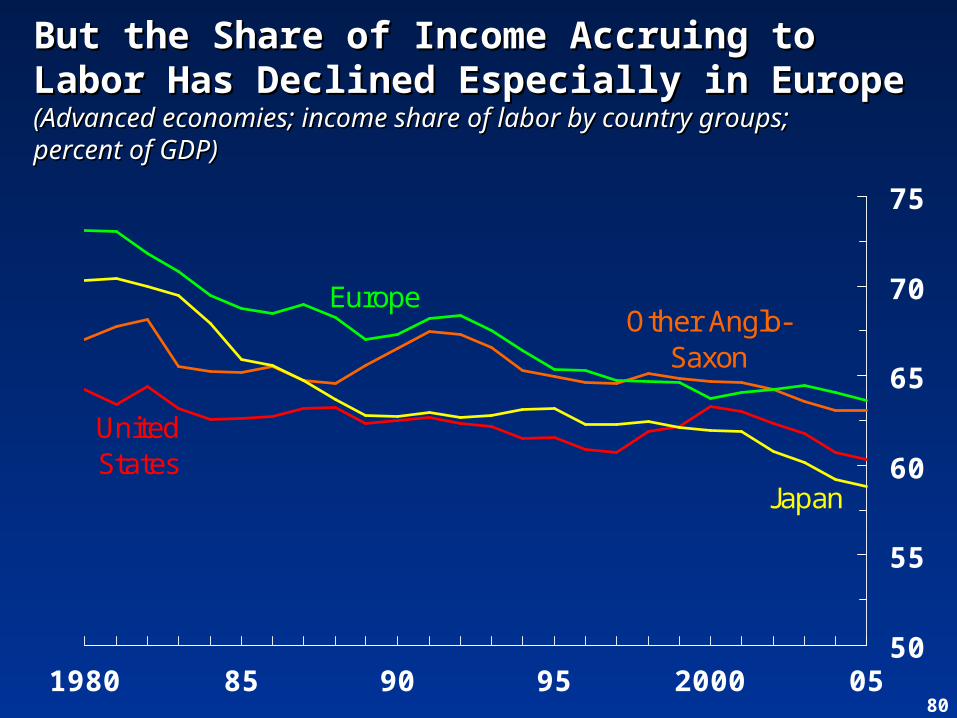

But the Share of Income Accruing to Labor But the Share of Income Accruing to Labor Has Declined Especially in EuropeHas Declined Especially in Europe(Advanced economies; income share of labor by country groups;(Advanced economies; income share of labor by country groups;percent of GDP)percent of GDP)

United States

Other Anglo-Saxon

Europe

Japan

50

55

60

65

70

75

1980 85 90 95 2000 05

81

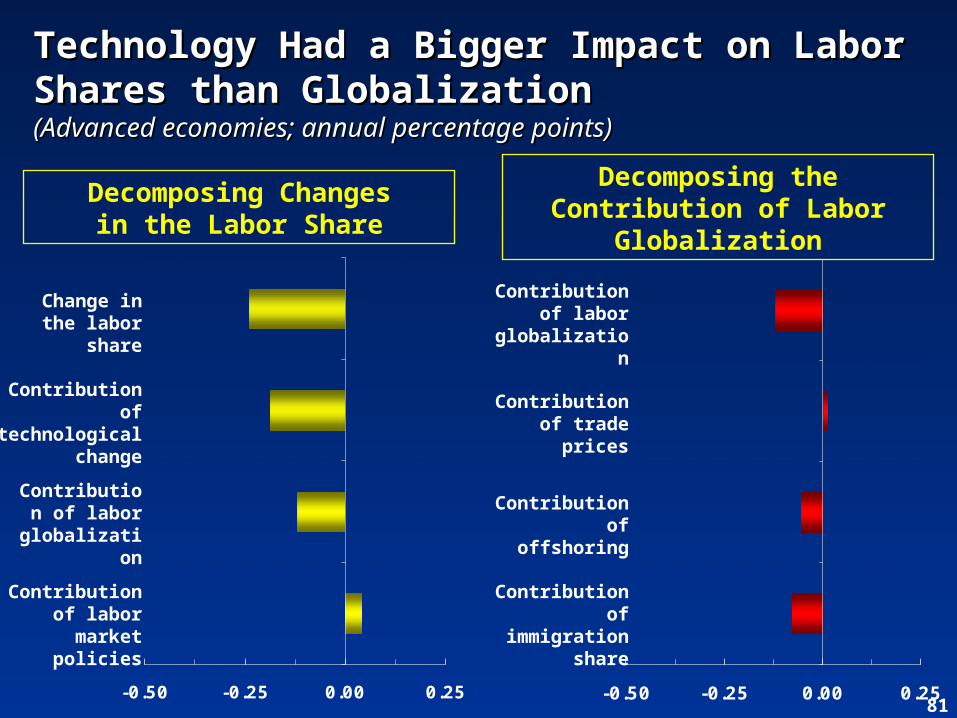

Technology Had a Bigger Impact on Labor Technology Had a Bigger Impact on Labor Shares than GlobalizationShares than Globalization(Advanced economies; annual percentage points)(Advanced economies; annual percentage points)

-0.50 -0.25 0.00 0.25

Decomposing Changesin the Labor Share

Change in the labor

share

Contribution of

technological change

Contribution of labor market policies

-0.50 -0.25 0.00 0.25

Decomposing the Contribution of Labor Globalization

Contribution of labor

globalization

Contribution of trade

prices

Contribution of offshoring

Contribution of

immigration share

Contribution of labor

globalization

82

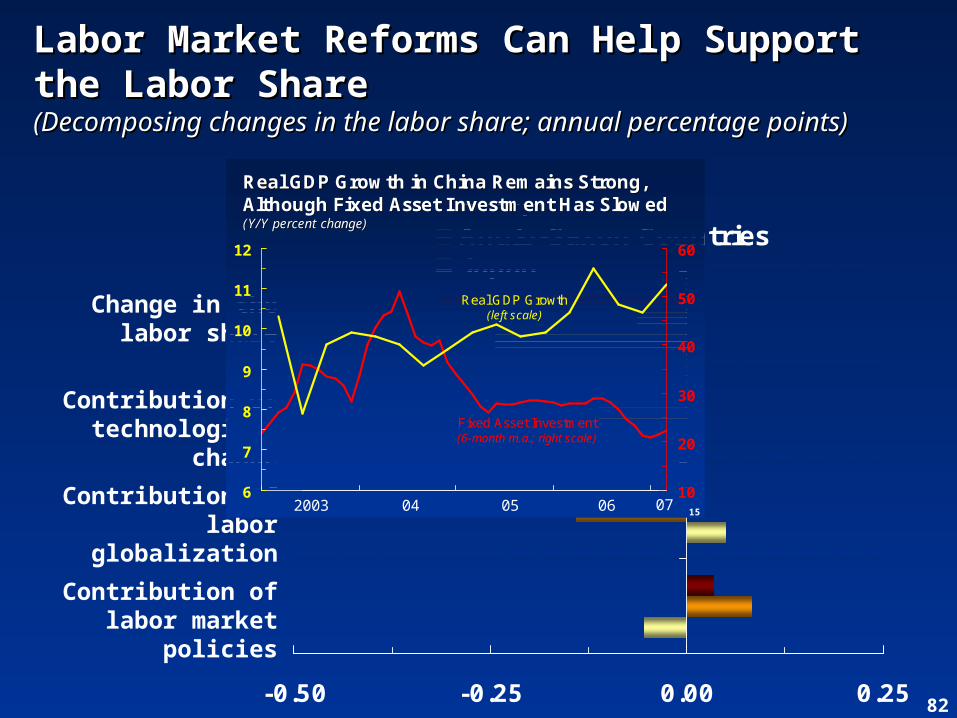

Labor Market Reforms Can Help Support Labor Market Reforms Can Help Support the Labor Share the Labor Share (Decomposing changes in the labor share; annual percentage (Decomposing changes in the labor share; annual percentage points)points)

-0.50 -0.25 0.00 0.25

EuropeAnglo-Saxon CountriesJapan

Change in the labor share

Contribution of technological

change

Contribution of labor globalization

Contribution of labor market

policies

152003 07060504

10

20

30

40

50

60

6

7

8

9

10

11

12

Fixed Asset Investment(6-month m.a.; right scale)

Real GDP Growth(left scale)

Real GDP Growth in China Remains Strong, Real GDP Growth in China Remains Strong, Although Fixed Asset Investment Has SlowedAlthough Fixed Asset Investment Has Slowed(Y/Y percent change)(Y/Y percent change)