critical illness and long term care: why you need a plan

TRANSCRIPT

Critical illness and long term care: why you need a plan

Disclaimer• The following information is being presented on the

understanding that it is for information purposes only. Neither Sun Life Assurance Company of Canada nor the presenter has been engaged for the purpose of providing legal, accounting, taxation or other professional advice.

• No one should act upon the examples/information without a thorough examination of the legal/tax situation with their own professional advisors.

Agenda• An inconvenient truth – Today’s health

care realities• The industry’s response – Basics of

Critical Illness and Long Term Care Insurance

• Why you need a plan – A rational approach to quantifying the risk

• Talking to clients - Making an emotional connection to the need

An Inconvenient Truth

Today’s Health Care Realities

TM and c 2006, Paramount Classics, a division of Paramount Pictures, all rights reserved.

Health care costing “an arm and a leg”• For the last ten years,

health care spending has outpaced both inflation and population growth

• 30% of health care spending ($44 billion in 2006) is funded privately (via insurance and out-of-pocket)

Health care spending to reach $148 billion this year, Canadian Institute for Health Information, Media Release, December 5, 2006.

Health care costing “an arm and a leg”• Government home care

spending reached $3.4 billion in 2003/04, an average annual increase of over 9% from 1994/95

• Even so, 65% of adults who needed help with eating, bathing or dressing did not receive government-subsidized home care

Public-Sector Expenditures and Utilization of Home Care Services in Canada: Exploring the Data, Canadian Institute for Health Information, March 2007.Kathryn Wilkins. "Government-subsidized home care" in Health Reports, Vol. 17, No. 4, October 2006, Statistics Canada. Based on 2003 statistics.

“Ont. bill covers anti-psychotics in nursing homes” Canadian Press, April 11, 2007“Nursing homes with high antipsychotic prescribing rates more likely to dispense drugs to residents who don’t need them”, Institute for Clinical Evaluative Sciences, Media Release, April 09, 2007

Care concerns• Widespread use of anti-psychotic

drugs in nursing homes• Some facilities dispensing the

drugs much more often than others, sometimes without identifying obvious need for them

• Serious adverse events associated with use of anti-psychotics (risk of falls, hip fracture, parkinsonism, death)

Medical advances and increased costs

“Understanding Health Care Cost Drivers and Escalators”, The Conference Board of Canada, March 2004

• Increased prices for newer drugs

• Technological change likely accounts for 25% of health expenditure growth in Canada

Our bottoms are on the line• 3 in 5 Canadian adults

are overweight or obese• More than 1 in 4

Canadian children are overweight or obese

Health Reports, Statistics Canada, Vol. 17, No. 3, August 2006

Cancer incidence• 39% of Canadian women and

44% of Canadian men are expected to develop cancer in their lifetimes

• 30% of new cancer cases will occur in young and middle-aged adults.

• Cancer incidence is rising in young adults ages 20 - 29 and females up to age 39.

• About 1300 Canadian children develop cancer each year

Canadian Cancer Society, National Cancer Institute of Canada: Canadian Cancer Statistics 2007

Cancer incidence ratesAges 0-64

Source: National Cancer Institute- Cases per 100,000- Age-adjusted

190

200

210

220

230

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

Survival rates improving• Mortality rates have declined for

all cancers combined and for most types of cancer in both sexes since 1994 (exceptions are lung cancer in females and liver cancer in males)

• Five year survival rate for breast cancer is 86%

• Five year survival rate for prostate cancer is 92%

Canadian Cancer Society, National Cancer Institute of Canada: Canadian Cancer Statistics 2007

5-year cancer survival rates

45%

50%

55%

60%

65%

70%

1974-76

1977-79

1980-82

1983-85

1986-88

1989-91

1992-94

1995-2001

Source: National Institutes of Health

Mortality rates – heart diseases

0

100

200

300

400

500

600

700

800

900

1000

1100

1950

1970

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

Male, ages 45-54 Male, ages 55-64

Female, ages 45-54 Female, ages 55-64

Source: National Cancer Institute - deaths per 100,000

Who will need care?• At age 65, the lifetime

probability of developing either a need for help with two or more activities of daily living for at least 90 days or a cognitive impairment is 44% for males and 72% for females

Cohen, Marc A., Maurice Weinrobe, Jessica Miller, and Anne Ingoldsby. "Becoming Disabled After Age 65: The Expected Lifetime Costs of Independent Living," AARP (American Association for Retired Persons) Public Policy Institute, 2005.

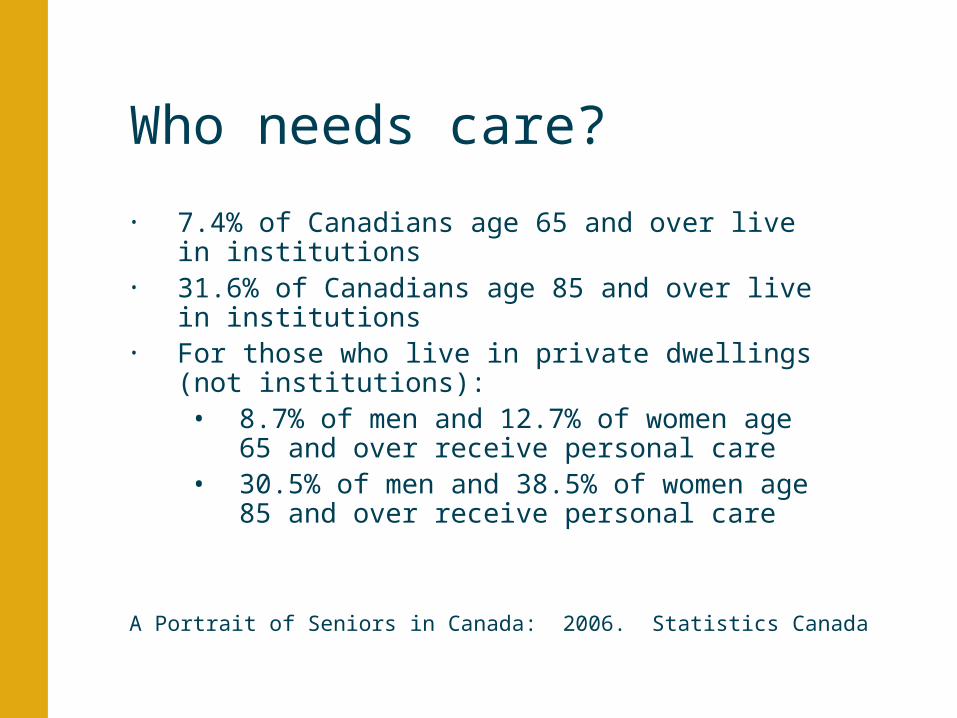

Who needs care?

• 7.4% of Canadians age 65 and over live in institutions

• 31.6% of Canadians age 85 and over live in institutions

• For those who live in private dwellings (not institutions):• 8.7% of men and 12.7% of women age 65 and

over receive personal care• 30.5% of men and 38.5% of women age 85 and

over receive personal care

A Portrait of Seniors in Canada: 2006. Statistics Canada

Proportion of individuals age 65+

0%

5%

10%

15%

20%

25%

1986 1996 2006 2016 2026 2036

Over the last 30 years, the proportion of individuals age 65 and over increased by 23%. Over the next 30 years, it’s expected to increase by 85%.

Life expectancy

55

65

75

85

1920-22

1930-32

1940-42

1950-52

1960-62

1970-72

1980-82

1990-92

Male Female

Source: Statistics Canada

A shift in risk

Current age

Inci

denc

e ra

te

Critical illness in males

Death in females

Critical illness in females

Death in males

Incidence of death vs. critical illness

before age 75

Source: Munich Reinsurance Co., 2003

Source of financial risk

Before Today

Dying Surviving

Risk

Solution

Life InsuranceCritical Illness

& LTC Insurance

The Industry’s Response

Basics of Critical Illness and Long Term Care

Insurance

Critical illness insurance• Provides a tax free lump sum benefit upon

diagnosis of a covered condition• 30 day survival period• Used at the client’s discretion • Optional ‘cost-recovery’ benefits: return of

premium on cancellation/expiry; return of premium on death

Critical Illness Insurance

Definition• No specific provisions in the Income Tax Act• Critical illness insurance is NOT Life or Disability

insurance• Can be illness or accident insurance – CRA

technical interpretation (2003-0026385)

CII – Individual Ownership

Premiums• Are not tax deductible• Are considered to be personal in nature• Will not give rise to a credit for medical expensesBenefits• Received are non-taxableReturn of Premiums• Non-taxable, both during lifetime and at death

CII – Corporate Ownership• Employee as benefit payee - Premium is taxable

benefit for employee, employer deduct premium, benefits non-taxable for employee

• Shareholder as benefit payee – may not deduct premium

• Company as benefit payee – premium is capital expenditure not a current expense, no deduction

Key Fact: CII benefits will not give rise to a credit to the capital dividend account

Standard Critical Illness OfferingFeature Options

Plan types • T10, T20, T65, T75, T100

# of illnesses • Range from 3 to 25+

Partial payouts • Usually 3-4 illnesses• 10% to 25% of base, typically to a max. of $50,000

Child Plans • Either as a rider or stand alone• Additional child hood illnesses

Return of Premium • At death (attachment)• Expiry, and cancellation (attachment). value is guaranteed

Convertibility • T10 can convert to T75 or T100

Return of Premium

ROP $39,150

Base Premium

Alternative

Investment $18,624

40, MNS, $150,000, end of 15 years

5%

$1,788ROPC

Premium $822

Benefit

$150,000

+

13.5%

Note: Based on Sun T75, with ROPC at 15 years. Base premium includes annual ROPD premium of $106.50. Interest rate calculations done on beginning of period basis.

Guaranteed

Target Market

All that qualify!

“Primary market”Ages 30-55

Ages 2-65

• Business owners / Professionals• Families / Singles• Mortgage protection• Women

• Business owners / Professionals• Families / Singles / Children• Mortgage protection• Women

SLF placement rates, 2006

Placed77.5%

Declined/ postponed

11%

Not proceeded w ith*11.5%

*Not proceeded with includes: incomplete medicals, offers not accepted by the client, no reply, and clients choosing not to proceed with the application.

2005 Industry placement rates ranged from 60% to 76%. Source: Munich Re’s Critical Illness Survey 2006

Claims Since Inception - % Paid

Coronary Artery Bypass Surgery

4%

Multiple Sclerosis2%

Cancer70%

Heart Attack14%

Others5%

Stroke5%

Munich Re’s Critical Illness Survey, 2006

Long term care insurance• Provides a tax free benefit if you are unable to take

care of yourself (need another person to help you perform two or more activities of daily living – e.g. bathing, dressing or require continual supervision due to mental deterioration)

Product details: three plan styles• Reimbursement: reimburse expenses for eligible

services* received on a given day, up to a pre-determined maximum

• Indemnity: pay a pre-determined daily benefit if the insured person receives any eligible service(s)* on that day (even if the service(s) cost more or less than the pre-determined daily benefit amount)

• Income: provide an income when the insured person requires care, without requiring a plan of care or proof of service

*An individual plan of care is created for each claimant. The plan specifies the types and frequency (hours per day, days per week) of eligible services.

Customized plan design• Benefit type(s) - comprehensive benefit, facility care

benefit• Benefit amount - from $150 - $2000 per week with or

without inflation protection• Benefit duration - 100, 150, 250, or unlimited weeks)• Waiting period - 30 day, 90 day (option of 0 day for facility

care if both benefit types selected)• Optional return of premium on death benefit• Payment period:

– Longer of 20 years or to age 55– Lifetime

Primary question to determine whether someone is eligible to claim:

Is the person dependent on another person for care?

Two ways to be considered ‘physically dependent’

1. Needs continual supervision by another person for protection from threats to their physical health and safety as the result of deterioration in mental ability from an organic brain disorder*

*Organic brain disorders cause physical changes in the brain – Alzheimer’s, other forms of senile dementia, and brain injuries (from accidents or from strokes) are examples of organic brain disorders

2. Always needs substantial physical assistance or stand-by assistance* from another person to safely and completely perform 2 or more of the “activities of daily living” – with or without the aid of assistive devices

Two ways to be considered ‘physically dependent’

*Stand-by assistance means the other person must be within arms reach of the insured person each time the relevant activity of daily living is performed

Activities of daily living• Bathing – washing oneself in a bathtub or shower

(including getting in and out of the bathtub or shower) or by sponge bath

• Dressing – putting on, taking off, fastening and unfastening clothing and medically necessary braces or artificial limbs

• Feeding – ability to get food into the body through the mouth or by a feeding tube

Activities of daily living• Toileting – getting to and from and on and off the

toilet and performing associated personal hygiene• Transferring – moving into or out of a bed, chair or

wheelchair• Continence – ability to control both bowel and

bladder functions, or maintain a reasonable level of personal hygiene (including caring for catheter or colostomy bag)

Use of assistive devices• An assistive device is a device or tool that assists users in

accomplishing day-to-day tasks• Home renovations (significant removal or replacement of

any part of an existing residence) are not assistive devices• Examples of assistive devices to aid with bathing and

dressing (most often, these are the first two activities of daily living that are lost):

– grab bar, bath stool, hand-held shower head, long-handled brush, long-handled shoe horn, sock puller

Use of assistive devices• If insured person can independently use an assistive

device to safely and completely perform an activity of daily living, then she/he is not dependent on another person for that activity

• If insured person uses an assistive device but also remains dependent on another person, she/he is still considered dependent for that activity

• No specific income tax laws for long term care insurance

• The following information is what we believe based on current tax laws and current CRA interpretation

Tax treatment

Can premiums be used when calculating the medical expense tax credit?

• Only if the plan qualifies as a private health services plan (PHSP)

• Income- and indemnity-style long term care insurance plans do not qualify as PHSPs

• Reimbursement-style long term care insurance plans may or may not qualify as PHSPs

Tax treatment – individual ownership

Tax treatment – individual ownership

Are benefits taxable?

• Cash benefits from income- or indemnity-style long term care insurance plans should not be taxed

• Reimbursements made from LTCI plans are not are not taxed

Tax treatment – individual ownership

Are actual medical expenses eligible for the medical expense tax credit?

• With income- and indemnity-style plans, actual medical expenses may still be used when calculating the medical expense tax credit

• With reimbursement-style plans, only expenses that are not reimbursed are eligible

Placement rate and target market

0%10%20%30%40%50%60%70%80%90%

<30 31-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75+

Age

Pla

cem

ent

rate

(p

oli

cies

) Target Market

Source: Sun Life

Why you Need a Plan

A Rational Approach to Quantifying the Risk

Cost of care• Facility care:

– Waiting lists can be long (one or two years)– Is this where you want to live?

• Retirement homes:– Accommodation can cost over $5,000 a month– Personal care services may be in addition

• Home care:– Depends on level of care required– Example:

• 2 hours nursing care 3 days / week at $40 / hour• 2 hours personal care 7 days / week at $20 / hour• 3 hours homemaking 4 days / week at $20 / hour

Total = $3,293 / month

The bottom line for your client

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

0 2 4 6 8 10 Years

• Today’s care cost: $3,293/month• Monthly cost of care starting in 25 years (2% inflation):

$5,403• Taking lost interest of 7% into account, 5-year care

need would cost over $400,000• 10-year care need would cost over $1 million

Sample lost wealth trailersdue to long term care withdrawals

Average assets under management $100,000

Number of clients 100

Per cent of clients withdrawing each year 3.5%

Average number of years withdrawing 2.5

Average monthly withdrawal $3,293

Inflation rate 2.0%

Investment return 7.0%

Average trailer rate 0.375%

Amount of lost trail $583,018

Percentage of trail lost 31%

Total difference had lost trail been invested $896,751

Asset or ‘stop loss’ protection with critical illness insurance

• Do you have an asset protection strategy for your investments?

• A personal financial health credit line?*• Have you been shown a way to protect your financial

health if you were diagnosed with cancer, a heart attack or stroke?*

* Alphonso Franco 2005 MDRT Speech

Asset protection with critical illness insurance

$2,505,673

40 yrs 45 yrs 50 yrs 55 yrs 60 yrs 65

$2,108,273

B) Invest yearly $50,000 *Less CI yearly Premium $ 7,930 Net Yearly Investment $42,070

*Sun Critical Illness Plan Level T75 – $500,000, AIB/ROPD/ROPC/E – 15 years

In 13 yrs $500,000 is required to cover expenses incurredDue to a Critical Illness

$1,468,566

Plus $198,250

ROP

A) Invest $50,000 yearlyAssume 5% annually

Stop Loss Protection Needs Analysis and Data Entry

Actual Age Smoking Status

Name of Client: 40 m no

Annual Income: $80,000

3.0%

Return of Premium C/E: 15

Registered assets Non-Registered assets

Starting balance: $125,000 $35,000

Annual deposit: $5,000 $0

Years of deposit: 25

Growth rate: 6.00% 6.00%

Tax Rate: 45.00%

CI Need

Illness at age: 55

No of Months Inc needed: 6

Health care: $15,000

Home care: $2,000

Health Care Inflation Rate: 6.0%

Need Calculated: $ 104,000

Gender

Salary Increase:

Impact of Illness

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

40 45 45.1 50 55 60 65

Age

Asset

Valu

e

No w/d

$50k w/d

$100k w/d

$150k w/d

1,000,000

831,000

670,000

505,000

Assumptions: • $160,000 in assets at age 40• $5,000 annual contribution• withdrawal at age 45 due to illness

FACT: • 85% of CI claims have occurred in the first 5 yearsSource: Munich Re’s Critical Illness Survey 2006

Portfolio Adjustment

Rate to Meet Original $1,000,000 Goal

Withdrawal New Yield % Increase

$ (50,000.00) 7.2% 18%

$(100,000.00) 8.5% 39%

$(150,000.00) 10.3% 69%

Original plan assumed 6.1% rate of return to meet retirement target of $1,000,000 at age 65.

Talking to Clients

Making an Emotional Connection to their

Need

The Myth…

It won’t happen to me!

The Reality…• Each day in Canada, more

than: – 400 are diagnosed with

cancer– 190 have heart attacks– 140 suffer strokes

Daily averages derived from the following sources:Canadian Cancer Society, 2006 (http://www.cancer.ca/ccs/internet/standard/0,2283,3172_14423__langId-en,00.html)Heart and Stroke Foundation, 2001Heart and Stroke Foundation of Canada, Annual Report 2004Multiple Sclerosis Society of Canada, 2006

• Do you know someone who has had…?

• Did they plan it? • Did the illness result in

emotional or financial strain on the household or business?

• Would extra cash have helped?

Talking to clients about critical illness insurance: questions you should ask

“Her husband is still not working. John lost his job in downsizing not long before Amy got pregnant and was diagnosed with cancer. Since then, it’s been difficult to concentrate on the job hunt…”

Talking to clients about long term care insurance: what to ask

• What do you want to have happen when you can no longer take care of yourself?

• What quality of care do you want to receive?

• Where do you want to receive care? • How will your family cope, financially and

emotionally, with care-giving?• Do you want to use your savings and

investments for care?

Public awareness Advisor training Cost Need Underwriting Standardized Definitions

Top 6 Industry Challenges

Tyler’s story