crowdfunding industry report · crowdfunding platforms (cfps) that explains their functionality and...

TRANSCRIPT

CROWDFUNDING INDUSTRY REPORTMarket Trends, Composition and Crowdfunding Platforms

THE INDUSTRY WEBSITE TM

May 2012

Research Report

PAGE 2© 2012 Crowdsourcing, LLC | [email protected]

TABLE OF CONTENTS

About this Research 3

Research Sponsors 4

Participating Crowdfunding Platforms 6

Key Messages 11

1. Introduction and Methodology 12

2. Market Growth and Composition 17

3. Crowdfunding Models 31

4. CFPs Value Proposition, Functionality and Approach 36

Appendices 47

Acknowledgements 49

THE INDUSTRY WEBSITE TM

PAGE 3© 2012 Crowdsourcing, LLC | [email protected]

ABOUT THIS RESEARCH

This research report provides an in-depth analysis of crowdfunding market trends and composition, and an overview of Crowdfunding Platforms (CFPs) that explains their functionality and the different models at play.

The report is based on two sources of data; the Crowdfunding ,QGXVWU\�6XUYH\��FRQGXFWHG�LQ�WKH�ȴUVW�TXDUWHU�RI������E\�Crowdsourcing.org with analyses conducted by Crowdsourcing LLC’s research and advisory business, massolution; and VLJQLȴFDQW�UHVHDUFK�FRQGXFWHG�YLD�RWKHU�UHOLDEOH�VRXUFHV�WR�FRPSOHWH�WKH�SURȴOLQJ�RI�WKH�JOREDO�FURZGIXQGLQJ�LQGXVWU\��7KLV�UHVHDUFK�LV�WKH�ȴUVW�LQ�D�VHULHV�RI�UHSRUWV�DLPHG�DW�providing reliable and factual information on the global crowdfunding industry.

We received over 170 responses to our industry survey where we selected participants from Crowdsourcing.org’s Directory of

Crowdfunding Sites which contained 452 active crowdfunding platforms at the time the survey was conducted. As the basis for the analyses, we selected 135 submissions from CFPs that we determined were comprehensive and of high-integrity. The 135 submissions provided extensive data relating to CFPs crowdfunding volumes, operations and key constituents (e.g., Funders and Fundraisers) for the calendar years 2009, 2010 and 2011. Our analyses of this rich data set has resulted in this research report on the crowdfunding industry.

1. An overview of massolution’s methodology for data gathering and analysis.2. An analysis of market growth, composition and key statistics.3. An overview and categorization of crowdfunding models.4. An analysis of the value proposition, functionality and approach.

THE REPORT CONTAINS FOUR SECTIONS:

THE INDUSTRY WEBSITE TM

PAGE 4© 2012 Crowdsourcing, LLC | [email protected]

FOUNDING RESEARCH SPONSOR

(OOHQRII�*URVVPDQ��6FKROH�//3�LV�D�1HZ�<RUN�&LW\�EDVHG�ODZ�ȴUP�FRQVLVWLQJ�RI����SURIHVVLRQDOV�����RI�ZKLFK�DUH�6HFXULWLHV�/DZ\HUV���We represent nearly 50 public companies and numerous private companies in various industries. We are proud to be the Founding Sponsor of Crowdsourcing.org and are institutionally committed to the Crowdfunding industry and being part of its success.

EG&S offers its clients legal services in a broad range of business related matters. Currently celebrating its 20th year, the Firm specializes in many areas of commercial law, including corporate and securities – ‘33 Act and ‘34 Act representation, reverse mergers, 3,3(V��63$&V��JRLQJ�SULYDWH�DQG�PHUJHUV�DQG�DFTXLVLWLRQV��

Over the history of the Firm, we have developed an expertise in establishing novel securities programs (like SPACs, Registered Directs, PIPEs and Reverse Mergers) and we expect to make a similar impact on Crowdfunding.

Our industry expertise includes: information technology, software GHYHORSPHQW��ELRWHFKQRORJ\��PHGLFDO�GHYLFHV��ȴQDQFLDO�VHUYLFHV��

alternative energy, consumer products, and business services throughout the world. We represent portals and entrepreneurs, investment managers, broker dealers, hedge funds, investment EDQNV��UHDO�HVWDWH�GHYHORSHUV��OHDVLQJ��ȴQDQFLQJ��DQG�EX\�VHOO��DQG�work on numerous corporate and partnership tax issues. The Firm also has a strong commercial litigation department that supplements our other practice areas. The Firm has clients throughout the world including Greece, England, the Netherlands, China and India and Israel.

,Q�������(*6�ZDV�UDQNHG����LQ�3,3(V�5HJLVWHUHG�'LUHFWV��DJHQWȇV�counsel); #1 in SPAC Practice (total offerings and business combination representations) and #4 for IPOs (issuer counsel).

150 East 42nd Street New York New York 10017Tel:212 370 1300Fax:212 370 7889

Contact: Douglas S. [email protected]

KWWS���ZZZ�HJVOOS�FRP�5HVRXUFH�&HQWHU�&URZGIXQGLQJ����KWPO

THE INDUSTRY WEBSITE TM

PAGE 5© 2012 Crowdsourcing, LLC | [email protected]

RESEARCH SPONSOR

GATE Technologies, LLC is an innovative technology company that creates new market infrastructure to deliver fully integrated HOHFWURQLF�PDUNHWSODFHV�IRU�WKH�ȴQDQFLDO�VHUYLFH�LQGXVWU\�

GATE Technologies, LLC is an innovative technology company that FUHDWHV�QHZ�PDUNHW�LQIUDVWUXFWXUH�IRU�WKH�ȴQDQFLDO�VHUYLFH�LQGXVWU\��By developing fully integrated electronic marketplaces, GATE has created a complete end to end solution by combining a regulatory compliant transactional platform, settlement and clearing services with global connectivity, enabling investors and institutions to trade WKH�PRVW�FRPSOH[�DOWHUQDWLYH�DVVHWV�ZLWK�FRQȴGHQFH��*$7(�VHHNV�to improve capital formation for lower middle market issuers and social enterprises while bringing a broad range of market participants access to impact investments and information.

GATE Technologies gives market participants the transparency, HɝFLHQF\�DQG�OLTXLGLW\�WKH\�QHHG�WR�YLHZ�DOO�PDUNHW�DFWLYLW\��HQVXULQJ�regulatory oversight while standardizing processes in which transactions and settlement occur. www.gatetechnologies.com

GATE Impact LLC is the impact investing-focused subsidiary of GATE Technologies, LLC. GATE Impact offers utility and infrastructure to the rapidly emerging crowdfunding industry, providing market infrastructure and related services for the emerging impact investment industry – public and private investments with a VXEVWDQWLDO�VRFLDO�DQG�RU�HQYLURQPHQWDO�FRPSRQHQW�WKDW�DOVR�JHQHUDWH�D�KHDOWK\�UDWH�RI�ȴQDQFLDO�UHWXUQ��*$7(�,PSDFW�EXLOGV�on the technology foundation of the GATE Platform, a regulatory-compliant market infrastructure for the transacting of restricted, LOOLTXLG�DQG�DOWHUQDWLYH�DVVHWV��7KH�WHFKQRORJ\�ZDV�GHYHORSHG�WR�PHHW�or exceed all regulatory standards and is easily adapted to handle both primary and secondary transactions in new asset classes. www.gateimpact.com

The GATE Platform is a sophisticated yet user friendly technology WKDW�LV�XQLTXHO\�SRVLWLRQHG�WR�H[SORLW�WKH�UDSLGO\�HPHUJLQJ�RSSRUWXQLW\�WR�EULQJ�WUDQVSDUHQF\��SULFH�GLVFRYHU\��DQG�OLTXLGLW\�WR�LOOLTXLG�DOWHUQDWLYH�DVVHW�FODVVHV�JOREDOO\�

GATE Technologies

5 Penn Plaza, Suite 2301New York, NY 10001

212.896.3983

THE INDUSTRY WEBSITE TM

PAGE 6© 2012 Crowdsourcing, LLC | [email protected]

RESEARCH SPONSOR

J.H. Cohn has been actively monitoring the marketplace’s reaction to the 2012 Jumpstart Our Business Startups Act (“JOBS Act”), including Crowdfunding. Through the progression of the JOBS Act, the Firm has participated in dialogue with market innovators and interested investors. For companies following this migration with interest, we offer updates, insight on how companies can prepare to take advantage of all aspects of the JOBS Act, and access to organizations and market leaders spearheading the movement to develop this alternative capital source.

2QH�RI�WKH�OHDGLQJ�DFFRXQWLQJ�DQG�FRQVXOWLQJ�ȴUPV�LQ�WKH�8QLWHG�States, J.H. Cohn LLP specializes in audit, accounting, tax, and business consulting services for public and private companies and QRW�IRU�SURȴW�RUJDQL]DWLRQV��6LQFH�������WKH�)LUPȇV�SKLORVRSK\�KDV�remained constant: to provide a highly personalized approach to each client, with intelligent guidance and solutions driven by technical and industry expertise that positively affect client SURȴWDELOLW\�DQG�JURZWK��-�+��&RKQ�KDV�FXOWLYDWHG�D�UHSXWDWLRQ�IRU�strategic insight, proactive leadership, unwavering integrity, and a genuine concern for clients and their businesses.

To help clients think and act across national boundaries, J.H. Cohn is an independent member of Nexia International, a global network of independent accountancy, tax, and business advisors and the tenth largest provider of audit and advisory services worldwide. The Firm KDV�RɝFHV�LQ�1HZ�<RUN��1HZ�-HUVH\��&RQQHFWLFXW��0DVVDFKXVHWWV��DQG�California.

For more information, visit our website at www.jhcohn.com.

New York Contact info: J.H. Cohn LLP1212 Avenue of the Americas7th FloorNew York, New York 10036-1602212-297-0400www.jhcohn.com

Contact: Richard Salute, [email protected]

THE INDUSTRY WEBSITE TM

PAGE 7© 2012 Crowdsourcing, LLC | [email protected]

PARTICIPATING CFPs

We would like to thank the participating companies for an unprecedented response and for providing extensive data.

THE INDUSTRY WEBSITE TM

PAGE 8© 2012 Crowdsourcing, LLC | [email protected]

PARTICIPATING CFPs

We would like to thank the participating companies for an unprecedented response and for providing extensive data.

THE INDUSTRY WEBSITE TM

PAGE 9© 2012 Crowdsourcing, LLC | [email protected]

PARTICIPATING CFPs

We would like to thank the participating companies for an unprecedented response and for providing extensive data.

THE INDUSTRY WEBSITE TM

PAGE 10© 2012 Crowdsourcing, LLC | [email protected]

PARTICIPATING CFPs

We would like to thank the participating companies for an unprecedented response and for providing extensive data.

THE INDUSTRY WEBSITE TM

PAGE 11© 2012 Crowdsourcing, LLC | [email protected]

PARTICIPATING CFPs

We would like to thank the participating companies for an unprecedented response and for providing extensive data.

THE INDUSTRY WEBSITE TM

PAGE 12© 2012 Crowdsourcing, LLC | [email protected]

KEY MESSAGES

1. INTRODUCTION AND METHODOLOGY

:H�DQDO\]HG�D�VWDWLVWLFDOO\�VLJQLȴFDQW�GDWD�VHW�EDVHG�RQ�GLUHFW�VXEPLVVLRQV�IURP�����&)3V��HTXDWLQJ�WR�����RI�WKH�market on a funds-raised basis. Secondary research provided DQ�DGGLWLRQDO�����RI�WKH�PDUNHW�HVWLPDWH�DQG�IXUWKHU�H[WUDSRODWLRQV�RI�WKH�UHPDLQLQJ����SURYLGHG�WKH�WRWDO�PDUNHW�estimate.

2. MARKET GROWTH AND COMPOSITION

As of April 2012, based on Crowdsourcing.org’s Directory of Sites, the most complete database of crowdfunding sites, there were 452 crowdfunding platforms active worldwide. The majority of them are in North America and Western Europe. Together, these platforms raised almost $1.5 billion and successfully funded more than one million campaigns in 2011.

3. CROWDFUNDING MODELS

(TXLW\�EDVHG�DQG�OHQGLQJ�EDVHG�FURZGIXQGLQJ��L�H���IRU�ȴQDQFLDO�UHWXUQ��LV�PRVW�HIIHFWLYH�IRU�GLJLWDO�JRRGV��H�J���VRIWZDUH��ȴOP�DQG�PXVLF���7KHVH�FDWHJRULHV��RQ�DYHUDJH���UDLVHG�the largest sum of money per campaign.

Donation-based and reward-based crowdfunding for cause-based campaigns that appeal to funders’ personal beliefs and passions perform best (e.g., environment).

4. CFPs VALUE PROPOSITION, FUNCTIONALITY & APPROACH

The primary revenue model for crowdfunding platforms is percentage based commission on funds paid out to entrepreneurs. A few also generate income by offering white label solutions and cash management by maintaining responsibility for netting and settlements.

Our research shows that campaign metrics such as launch to fund (L2F) differ greatly between crowdfunding models.

THE INDUSTRY WEBSITE TM

PAGE 13© 2012 Crowdsourcing, LLC | [email protected]

CATEGORIZATION OF CROWDFUNDING PLATFORMS

0DVVROXWLRQ�GHȴQHV�IRXU�FDWHJRULHV�RI�FURZGIXQGLQJ�SODWIRUPV��&)3V��

ȏ� (TXLW\�EDVHG�FURZGIXQGLQJ

ȏ� /HQGLQJ�EDVHG�FURZGIXQGLQJ

ȏ� 5HZDUG�EDVHG�FURZGIXQGLQJ

ȏ� 'RQDWLRQ�EDVHG�FURZGIXQGLQJ

Our survey respondents were asked more than 30 detailed TXHVWLRQV�UHODWLQJ�WR�WKH�SDUWLFLSDQWV�RQ�WKHLU�SODWIRUPV��WKH�functionality of their platforms and their fundraising activities for the calendar years 2009, 2010 and 2011. Further data was gathered via direct communications with 135 CFPs and VLJQLȴFDQW�VHFRQGDU\�UHVHDUFK��7KH�VXUYH\�ZDV�FRQGXFWHG�under strict non-disclosure rules; hence all the data in this report is aggregated or averaged.

2XU�UHVHDUFK�LGHQWLȴHG�WKDW�QHDUO\�86����%�ZDV�UDLVHG�E\�crowdfunding platforms globally in 2011. The participating CFPs UHSUHVHQW�D�VLJQLȴFDQW�SRUWLRQ�RI�WKH�FURZGIXQGLQJ�PDUNHW��

collectively accounting for more than US$575 million of funds UDLVHG��)XUWKHU�VHFRQGDU\�UHVHDUFK�LGHQWLȴHG�DQRWKHU�86�����from additional sources. Finally, to complete our estimate of the overall size of the market, we developed a forecasting methodology to identify an additional US$68 million of funds raised via crowdfunding platforms.

The sample of participating CFPs survey respondents is very diverse and therefore we are able to compare and contrast the characteristics of the different types of crowdfunding models and compare each individually by region. The data set represents all four categories of crowdfunding across all regions of the world. Although our sample is robust and VWDWLVWLFDOO\�VLJQLȴFDQW��ZH�DOVR�XVHG�DGGLWLRQDO�VRXUFHV�WR�present a holistic view of the crowdfunding market.

We ensured the accuracy of our analyses by excluding TXHVWLRQDEOH�GDWD�DQG�LQFRPSOHWH�UHVSRQVHV��:KHUH�applicable, this is indicated alongside the charts by showing the sample size of respondents used for each element of analysis.

1. INTRODUCTION ANDMETHODOLOGY

2. MARKET GROWTHAND COMPOSITION

3. CROWDFUNDINGMODELS

4. CFPs VALUE PROPOSITION, FUNCTIONALITY & APPROACH

1. INTRODUCTION AND METHODOLOGY THE INDUSTRY WEBSITE TM

PAGE 14© 2012 Crowdsourcing, LLC | [email protected]

THERE WILL BE OVER 530 CFPs BY DECEMBER 2012

NUMBER OF CFPs WORLDWIDE (Based on a sample of 348 CFPs),QGH[HG�SHUFHQWDJH�������LV�����

1 Based on Crowdsourcing.org Directory of Sites as of April 2012.2 Estimates are based on historical market projections and do not take into account extraordinary events, (e.g., passing of US Crowdfunding legislation) which are, based on available data, unpredictable.Source: Based on Crowdsourcing.org Directory of Sites as of April 2012

536Estimated number of CFPs as of Dec 2012

452The total number of CFPs as of Apr 2012

1. INTRODUCTION AND METHODOLOGY

2007

100%

2008 2009 2010 2011 2012 (Est.)

138%

200%

294%

452%

557%

470%

1

2

38% 45% 47% 54% 60%GROWTH

THE INDUSTRY WEBSITE TM

PAGE 15© 2012 Crowdsourcing, LLC | [email protected]

)285�7<3(6�2)�&52:')81',1*�3/$7)2506�(;,67��(48,7<�%$6('��/(1',1*�%$6('��5(:$5'�BASED, AND DONATION-BASED

7KHUH�DUH�IRXU�PDMRU�W\SHV�RI�FURZGIXQGLQJ�SODWIRUPV��HTXLW\�EDVHG��OHQGLQJ�EDVHG��UHZDUG�EDVHG��DQG�GRQDWLRQ�EDVHG��2XU�FODVVLȴFDWLRQ�LV�EDVHG�RQ�WKH�IXQGHUVȇ�SULPDU\�PRWLYDWLRQ�IRU�HQJDJLQJ�LQ�FURZGIXQGLQJ�

:H�FODVVLI\�HTXLW\�EDVHG�FURZGIXQGLQJ�DV�D�PRGHO�LQ�ZKLFK�IXQGHUV�UHFHLYH�DQ�LQWHUHVW�LQ�WKH�IRUP�RI�HTXLW\�LQ�WKH�YHQWXUH�WKH\�IXQG�RU��DOWHUQDWLYHO\��UHYHQXH�RU�SURȴW�VKDUH�arrangements.

We classify lending-based as a crowdfunding model in which IXQGHUV�RIWHQ�UHFHLYH�ȴ[HG�SHULRGLF�LQFRPH�DQG�H[SHFW�repayment of the original principal investment.

,Q�VWDUN�FRQWUDVW�WR�HTXLW\�EDVHG�DQG�OHQGLQJ�EDVHG�PRGHOV��reward-based and donation-based models are characterized by QRQ�ȴQDQFLDO�PRWLYDWLRQV�IRU�HQJDJLQJ�LQ�FURZGIXQGLQJ��

Reward-based crowdfunding allows funders to gain a QRQ�ȴQDQFLDO�EHQHȴW�LQ�UHWXUQ�IRU�ȴQDQFLDO�FRQWULEXWLRQV��Non-monetary rewards often take the form of a token of appreciation or the pre-purchasing of products or services.

Donation-based crowdfunding provides funders with a way to donate to causes that they want to support, with no expected compensation (i.e., philanthropic or sponsorship based incentive).

(48,7<�%$6(' LENDING-BASEDREWARD-BASED DONATION-BASED(Includes revenue and�SURȴW�

sharing models)(P2P lending, P2B lending and

social lending)

)RU�ȴQDQFLDO�UHWXUQ )RU�ȴQDQFLDO�UHWXUQ For non-monetary rewards For philanthropy or sponsorship

1. INTRODUCTION AND METHODOLOGY THE INDUSTRY WEBSITE TM

PAGE 16© 2012 Crowdsourcing, LLC | [email protected]

CFPs THAT PARTICIPATED IN THIS RESEARCH REPRESENT ALL KEY REGIONS AND ALL CATEGORIES OF THE CROWDFUNDING MARKET

5HȵHFWLQJ�UDWLRV�FRQVLVWHQW�ZLWK�WKH�RYHUDOO�FRPSRVLWLRQ�RI�WKH�FURZGIXQGLQJ�PDUNHWSODFH�IURP�D�FDWHJRU\�SHUVSHFWLYH������RI�RXU�VXUYH\�SDUWLFLSDQWV�UHSUHVHQWHG�UHZDUG�EDVHG�SODWIRUPV�

*HRJUDSKLFDOO\��MXVW�RYHU�����RI�RXU�VXUYH\�SDUWLFLSDQWV�UHSUHVHQWHG�(XURSHDQ�SODWIRUPV��ZLWK�����UHSUHVHQWLQJ�North American platforms. While this over represents European platforms when compared to the overall composition of the crowdfunding marketplace from a regional perspective, the size of our sample is still statistically relevant.

Note: When we refer to Other Regions our research does not include a data set from CFPs in Asia (e.g., China) were non-English language versions of platforms prohibited us from analyzing this market. Source: Massolution

COMPOSITION OF PARTICIPATING CFPsPercentage of the 135 total participating CFPs

1. INTRODUCTION AND METHODOLOGY

Composition by category

Composition by region

DONATION-BASED27%

47%REWARD-BASED

11%LENDING-

BASED

EQUITY-BASED15%

OTHERREGIONS

14%

NORTHAMERICA

30%

EUROPE56%

THE INDUSTRY WEBSITE TM

PAGE 17© 2012 Crowdsourcing, LLC | [email protected]

CFPs THAT DIRECTLY PARTICIPATED IN THIS RESEARCH ACCOUNT FOR A SIGNIFICANT PORTION OF THE MARKET IN TERMS OF TOTAL FUNDS RAISED

7KH�SDUWLFLSDWLQJ�&)3V�UHSUHVHQW�D�VLJQLȴFDQW�SRUWLRQ�RI�WKH�FURZGIXQGLQJ�PDUNHW�LQ�WHUPV�RI�WRWDO�IXQGV�UDLVHG��FROOHFWLYHO\�DFFRXQWLQJ�IRU�PRUH�WKDQ�86�����PLOOLRQ�RU�����RI�IXQGV�UDLVHG�LQ�������7KLV�VDPSOH�DORQH�DGGUHVVHV�PRUH�WKDQ�RQH�WKLUG�RI�WKH�WRWDO�DPRXQW�RI�IXQGV�UDLVHG�ZRUOGZLGH�LQ�������

Although our survey data is, in its own right, statistically VLJQLȴFDQW��DGGLWLRQDO�UHOLDEOH�VRXUFHV�LGHQWLȴHG�D�IXUWKHU�����RI�WKH�WRWDO�PDUNHW�DQG�D�YDOLG�PHWKRGRORJ\�ZDV�XVHG�IRU�HVWLPDWLQJ�WKH�UHPDLQLQJ����RI�WKH�PDUNHW��7KLV�KDV�enabled massolution to present the most complete view, to date, of the total crowdfunding market.

Source: Massolution

COMPOSITION OF FUNDS RAISED BY PARTICIPATING CFPs 3HUFHQWDJH������� ������PLOOLRQ

1. INTRODUCTION AND METHODOLOGY

Composition by category

Composition by region

DONATION-BASED49%

11%REWARD-BASED

22%LENDING-

BASED

EQUITY-BASED18%

OTHER REGIONS 8%

NORTH AMERICA 82%

EUROPE 10%

THE INDUSTRY WEBSITE TM

PAGE 18© 2012 Crowdsourcing, LLC | [email protected]

MARKET GROWTH AND COMPOSITION

0DUNHW�JURZWK�DQG�FRPSRVLWLRQ�E\�IXQGV�UDLVHG�

ȏ� Almost $1.5 billion was raised by CFPs world-wide in 2011.

ȏ� North America was the largest market for fundraising DW�������P�ZKLFK�HTXDWHG�WR�PRUH�WKDQ�KDOI�RI�DOO�WKH�funds raised globally.

ȏ� )XQGV�UDLVHG�JUHZ�DW�D�����&$*5�RYHU�WKH�ODVW���\HDUV��primarily driven by donation-based and lending-based platforms. Reward-based platforms are growing at a rate RI������EXW�IURP�D�VPDOOHU�EDVH������P�IXQGV�UDLVHG�LQ�2009).

ȏ� While the CFPs formed some years ago are still growing in terms of funds raised, new market entrants are securing a larger relative percentage of new funds raised, consistent with a high growth, early stage industry.

ȏ� Funds pledged to funds paid-out in aggregate has declined slightly over time; donation-based CFPs pay-out a much higher percentage of funds pledged.

3. CROWDFUNDINGMODELS

4. CFPs VALUE PROPOSITION, FUNCTIONALITY & APPROACH

1. INTRODUCTION ANDMETHODOLOGY

0DUNHW�JURZWK�DQG�FRPSRVLWLRQ�E\�QXPEHU�RI�&)3V�

ȏ� As of April 2012, 452 CFPs were operating globally.

ȏ� Market composition in each category YDULHV�VLJQLȴFDQWO\�E\�UHJLRQ��H�J���UHZDUG�EDVHG�DQG�HTXLW\�EDVHG�platforms are higher in numbers in Europe than in North America).

ȏ� Reward-based is the largest category in terms of overall number of CFPs, while HTXLW\�EDVHG�LV�WKH�IDVWHVW�JURZLQJ�category by net year-on-year growth.

ȏ� North America leads other regions in terms of the total number of crowdfunding platforms; however Europe, based on a higher rate of regional growth, is gaining percentage share within the market in aggregate.

0DUNHW�JURZWK�DQG�FRPSRVLWLRQ�E\�QXPEHU�RI�FDPSDLJQV�

ȏ� More than 1 million successful campaigns were run by CFPs in 2011.

ȏ� The majority of these campaigns were in the donation-based category totaling 1067 PLOOLRQ��EXW�HTXLW\�based campaigns were, on average, much larger in size in terms of funds raised.

2. MARKET GROWTH AND COMPOSITION

2. MARKET GROWTH AND COMPOSITION

THE INDUSTRY WEBSITE TM

PAGE 19© 2012 Crowdsourcing, LLC | [email protected]

$/0267������%,//,21�:$6�5$,6('�7+528*+�&)3V�,1������:,7+�29(5�����5$,6('�,1�1257+�AMERICA

TOTAL FUNDS RAISEDMillions of US dollars, 2011

Source: Massolution

2. MARKET GROWTH AND COMPOSITION

WORLDWIDE

NORTHAMERICA

EUROPE

OTHERREGIONS$1,469.9M

$837.2M $583.9M

$48.8M

THE INDUSTRY WEBSITE TM

PAGE 20© 2012 Crowdsourcing, LLC | [email protected]

727$/�)81'6�5$,6('�*5(:�$7�����&$*5��PRIMARILY DRIVEN BY THE DONATION-BASED AND LENDING-BASED CATEGORIES

7KH�FURZGIXQGLQJ�PDUNHW�LV�JURZLQJ�DW�WKH�UDWH�RI�����&$*5�

Donation-based platforms are responsible for the largest source of funds raised through crowdfunding, but they are also the slowest-growing category.

5HZDUG�EDVHG�SODWIRUPV�VKRZ�YHU\�KLJK�JURZWK�DW�������but from a very low base of close to $1.6m in 2009.

(TXLW\�EDVHG�SODWIRUPV�DUH�JURZLQJ�DW�D�UDWH�RI�������primarily in Europe.

Source: Massolution

GROWTH IN FUNDS RAISED BY CATEGORYMillions of dollars, based on a sample of 92 CFPs which HTXDWHV�WR�����RI�WKH�WRWDO�PDUNHW

2. MARKET GROWTH AND COMPOSITION

2011

1,401

2010

854

2009

530

43% CAGRDONATION-BASED

524% CAGRREWARD-BASED

78% CAGRLENDING-BASED

114% CAGREQUITY-BASED

63% CAGR

675.7

61.5

552.0

112.661.5

316.5

15.7

460.4

328.9

1.6

175.1

24.6

THE INDUSTRY WEBSITE TM

PAGE 21© 2012 Crowdsourcing, LLC | [email protected]

TOTAL FUNDING VOLUME IS EXPECTED TO DOUBLE IN 2012, DRIVEN BY ABOVE-$9(5$*(�*52:7+�,1�(48,7<�%$6('�$1'�REWARD-BASED CROWDFUNDING

�������PLOOLRQ

Estimated total funding volume for 2011.

�������PLOOLRQ�YHULȴHG�E\�primary and secondary research.

Additional $68 million estimated on the basis of our crowdfunding site database.

�������PLOOLRQ

Estimated total funding volume for 2012. Our IRUHFDVWV�HTXDWH�WR��

ȏ� �����JURZWK�LQ�HTXLW\�based and reward-based crowdfunding

ȏ� ����JURZWK�LQ�OHQGLQJ�based

ȏ� ����JURZWK�LQ�donation-based crowdfunding.

Source: Massolution

GROWTH IN WORLDWIDE FUNDING VOLUME(millions of dollars) Research based estimate

2. MARKET GROWTH AND COMPOSITION

2009 2010 2011 2012 (Est.)

530

854

1,470

2,806

61% 72% 91%GROWTH

1,063

258

1,013

472

DONATION-BASED

REWARD-BASED

LENDING-BASED

EQUITY-BASED

THE INDUSTRY WEBSITE TM

PAGE 22© 2012 Crowdsourcing, LLC | [email protected]

NORTH AMERICA IS THE REGION THAT RAISED THE LARGEST AMOUNT OF FUNDS AND CONTINUES TO SHOW THE FASTEST GROWTH

1RUWK�$PHULFD�LV�WKH�UHJLRQ�WKDW�UDLVHG�WKH�ODUJHVW�DPRXQW�RI�IXQGV�DW�������P�LQ�������1RUWK�$PHULFD�LV�DOVR�VKRZLQJ�WKH�IDVWHVW�JURZWK�RXW�RI�DOO�WKH�UHJLRQV��RYHUWDNLQJ�(XURSH�LQ�WKH�WRWDO�DPRXQW�RI�IXQGV�UDLVHG�in 2010.

(XURSHDQ�&)3V��WKRXJK�QRW�VLJQLȴFDQWO\�EHKLQG�WKHLU�1RUWK�American counterparts, are growing in terms of funds UDLVHG�DW�WKH�VORZHU�UDWH�RI�����

Source: Massolution

GROWTH IN FUNDS RAISED BY REGIONMillions of dollars, based on a sample of 92 CFPs which HTXDWHV�WR�����RI�WKH�WRWDO�PDUNHW

2. MARKET GROWTH AND COMPOSITION

53% CAGROTHER REGIONS

40% CAGREUROPE

90% CAGRNORTHAMERICA

2009 20112010

530

854

1,40146.8

571.5

783.5

422.3

401.1

30.7

218.1

292.2

19.9

THE INDUSTRY WEBSITE TM

PAGE 23© 2012 Crowdsourcing, LLC | [email protected]

1(:(5�0$5.(7�(175$176�+2/'�����2)�MARKET SHARE

(DUO\�HQWUDQWV�WR�WKH�FURZGIXQGLQJ�LQGXVWU\��GHȴQHG�DV�PDWXUH�SODWIRUPV�ZKLFK�DUH�PRUH�WKDQ�IRXU�\HDUV�ROG��ZHUH�WKH�NH\�VRXUFHV�RI�JURZWK�DQG�YROXPH�DQG�DFFRXQW�IRU�MXVW�RYHU�����RI�WKH�WRWDO�PDUNHW�LQ������

Newer-entrants (between two and four years old) now DFFRXQW�IRU�DSSUR[LPDWHO\�D�TXDUWHU�RI�WKH�WRWDO�IXQGV�UDLVHG��6WDUWXSV�KRZHYHU��GHȴQHG�DV�FRPSDQLHV�OHVV�WKDQ�two years old) contribute a very limited amount of the WRWDO�IXQGV�UDLVHG�GXULQJ�WKHLU�ȴUVW�WZR�\HDUV�LQ�RSHUDWLRQ�

Source: Massolution

TOTAL FUNDS RAISED BY CFP MATURITYMillions of dollars, based on a sample of 92 CFPs, 2011

����� ��������PLOOLRQ

2. MARKET GROWTH AND COMPOSITION

STARTUPS0.2%

NEWERENTRANTS

22.7%

MATURE77.2%

THE INDUSTRY WEBSITE TM

PAGE 24© 2012 Crowdsourcing, LLC | [email protected]

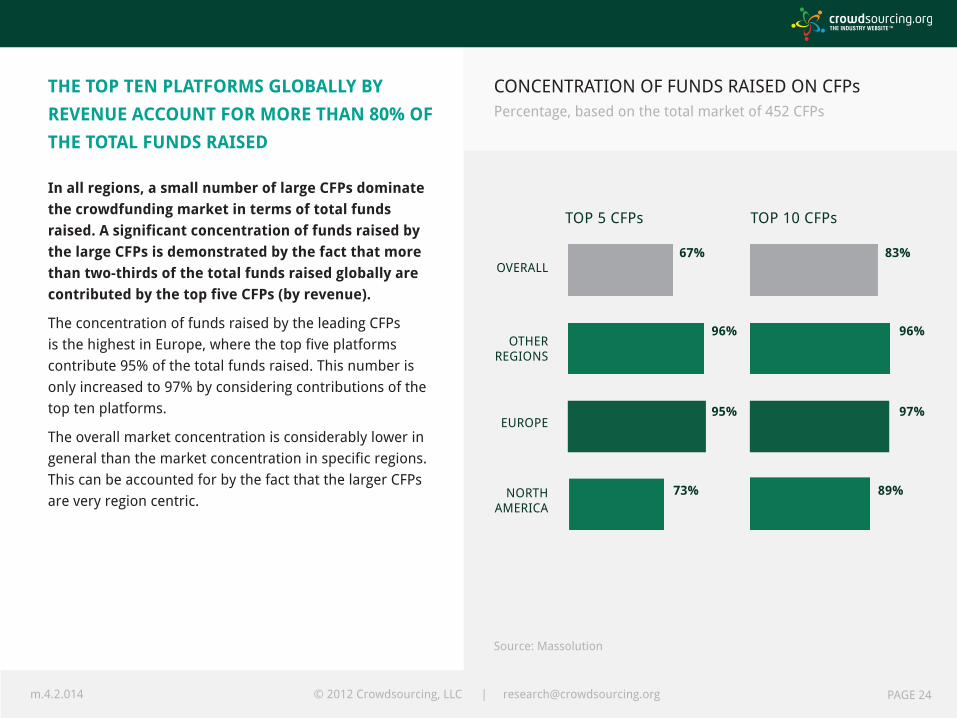

THE TOP TEN PLATFORMS GLOBALLY BY 5(9(18(�$&&2817�)25�025(�7+$1�����2)�THE TOTAL FUNDS RAISED

,Q�DOO�UHJLRQV��D�VPDOO�QXPEHU�RI�ODUJH�&)3V�GRPLQDWH�WKH�FURZGIXQGLQJ�PDUNHW�LQ�WHUPV�RI�WRWDO�IXQGV�UDLVHG��$�VLJQLȴFDQW�FRQFHQWUDWLRQ�RI�IXQGV�UDLVHG�E\�WKH�ODUJH�&)3V�LV�GHPRQVWUDWHG�E\�WKH�IDFW�WKDW�PRUH�WKDQ�WZR�WKLUGV�RI�WKH�WRWDO�IXQGV�UDLVHG�JOREDOO\�DUH�FRQWULEXWHG�E\�WKH�WRS�ȴYH�&)3V��E\�UHYHQXH��

The concentration of funds raised by the leading CFPs LV�WKH�KLJKHVW�LQ�(XURSH��ZKHUH�WKH�WRS�ȴYH�SODWIRUPV�FRQWULEXWH�����RI�WKH�WRWDO�IXQGV�UDLVHG��7KLV�QXPEHU�LV�RQO\�LQFUHDVHG�WR�����E\�FRQVLGHULQJ�FRQWULEXWLRQV�RI�WKH�top ten platforms.

The overall market concentration is considerably lower in JHQHUDO�WKDQ�WKH�PDUNHW�FRQFHQWUDWLRQ�LQ�VSHFLȴF�UHJLRQV��This can be accounted for by the fact that the larger CFPs are very region centric.

Source: Massolution

CONCENTRATION OF FUNDS RAISED ON CFPsPercentage, based on the total market of 452 CFPs

2. MARKET GROWTH AND COMPOSITION

OVERALL

OTHERREGIONS

EUROPE

NORTHAMERICA

67% 83%

96% 96%

95% 97%

73% 89%

TOP 5 CFPs TOP 10 CFPs

THE INDUSTRY WEBSITE TM

PAGE 25© 2012 Crowdsourcing, LLC | [email protected]

FUNDS PLEDGED TO FUNDS PAID OUT DECLINED OVER TIME; DONATION-BASED CFPs HAVE THE HIGHEST PLEDGED TO PAID OUT RATIO

FUNDS PLEDGED AND PAID OUTMillions of dollars, sample of 92 CFPs

2. MARKET GROWTH AND COMPOSITION

7KH�UDWLR�RI�IXQGV�SOHGJHG�WR�IXQGV�UDLVHG�GHFOLQHG�RYHU�WKH�ODVW�WZR�\HDUV��IURP�����WR������7KLV�FDQ�EH�H[SODLQHG�E\�D�VLJQLȴFDQW�HQWU\�RI�QHZ�SODWIRUPV���

Lending-based platforms show the highest funds pledged to funds paid out ratio out of all the categories, while reward-

based platforms show the lowest. North American investments VKRZ�WKH�KLJKHVW�IXQGV�SDLG�RXW�UDWLR�DW�����

2009 20112010 EQUITY-BASED

LENDING-BASED

REWARD-BASED

DONATION-BASED

NORTHAMERICA

EUROPE OTHERREGIONS

593 530

1,015854

1,767

1,402

162113

629552

12361

854

676

961

784744

572

62 47

79%

TOTAL FUNDS FUNDS BY CATEGORY FUNDS BY REGION

83%89% 75% 88% 50% 79% 82% 77% 75%% PAID OUT

PAID OUTPLEDGED

THE INDUSTRY WEBSITE TM

PAGE 26© 2012 Crowdsourcing, LLC | [email protected]

MORE THAN 450 CFPs ARE ACTIVE WORLDWIDE; THE MAJORITY BASED IN NORTH AMERICA AND EUROPE

NUMBER OF CFPs, 2012

Source: Based on Crowdsourcing.org Directory of Sites as of April 2012

2. MARKET GROWTH AND COMPOSITION

H

3 SWEDEN3 DENMARK3 IRELAND3 FINLAND2 CZECH REP.1 AUSTRIA1 ESTONIA1 LATVIA1 NORWAY1 ROMANIA1 HUNGARY

DF

EL

NS

R

CI

RDIFCAELNRH

A44 UNITED KINGDOM

29 NETHERLANDS

28 FRANCE

21 BRAZIL

20 GERMANY

18 SPAIN

17 CANADA

12 AUSTRALIA

6 INDIA

6 ITALY

6 NEW ZEALAND

6 PORTUGAL

6 BELGIUM

5 SWITZERLAND

4 CHINA

3 JAPAN3 SOUTH AFRICA

2 ARGENTINA

2 RUSSIA

2 MEXICO

1 CHILE

1 HONG KONG

1 ISRAEL

1 PHILLIPINES

1 ZAMBIA

1 HAITI

4 POLAND

191 UNITED STATES

THE INDUSTRY WEBSITE TM

PAGE 27© 2012 Crowdsourcing, LLC | [email protected]

IN TERMS OF NUMBER OF CFPs, EUROPE GREW AT APPROXIMATELY TWICE THE COMPOUND ANNUAL GROWTH RATE OF 1257+�$0(5,&$�)520������72�����

:KLOH�1RUWK�$PHULFD�LV�FXUUHQWO\�WKH�ODUJHVW�PDUNHW�LQ�WHUPV�RI�WKH�RYHUDOO�QXPEHU�RI�FURZGIXQGLQJ�SODWIRUPV�ZLWK�DERXW�����PRUH�SODWIRUPV�WKDQ�(XURSH��(XURSH�KDV�DFKLHYHG�D�����FRPSRXQGHG�DQQXDO�JURZWK�UDWH�RYHU�WKH�ODVW�VL[�\HDUV��7KLV�LV�PRUH�WKDQ�WZLFH�WKH�FRPSRXQGHG�DQQXDO�JURZWK�UDWH�LQ�SODWIRUPV�LQ�1RUWK�$PHULFD�

Other regions (primarily Latin America and Australia) showed much slower compounded annual growth over WKH�ODVW�VL[�\HDUV�������

Note: This research was conducted during the active debate in the US Congress over the JOBS Act, which contained a provision for a crowdfunding exemption. The passing of this exemption will likely have a profound effect on growth of CFPs in the HTXLW\�EDVHG�FDWHJRU\�LQ�WKH�8QLWHG�6WDWHV� Source: Crowdsourcing.org Directory of Sites

GROWTH IN NUMBER OF CFPs WORLDWIDEBased on a sample of 348 CFPs

2. MARKET GROWTH AND COMPOSITION

26% CAGROTHER REGIONS

59% CAGREUROPE

29% CAGRNORTHAMERICA

2007 2008 2009 20112010

77106

154

226

348

51

139

158

114

84

28

22

50

82

1825

63

1814

45

THE INDUSTRY WEBSITE TM

PAGE 28© 2012 Crowdsourcing, LLC | [email protected]

REWARD-BASED IS THE LARGEST &52:')81',1*�&$7(*25<��:+,/(�(48,7<��BASED IS THE FASTEST GROWING

7KH�UHZDUG�EDVHG�FDWHJRU\�LV�WKH�ODUJHVW�FURZGIXQGLQJ�FDWHJRU\�LQ�WHUPV�RI�QXPEHU�RI�&)3V��DQG�DOVR�JUHZ�DW�WKH�KLJK�UDWH�RI�����&$*5�

The lending-based category is the smallest in terms of the number of platforms.

Donation-based and lending-based crowdfunding are JURZLQJ�DW�D�VLPLODU�SDFH��VLJQLȴFDQWO\�ORZHU�WKDQ�WKDW�RI�the reward-based category.

7KH�HTXLW\�EDVHG��FDWHJRU\�VKRZV�WKH�IDVWHVW�JURZWK�UDWH��DW�������DQG�LV�PRVWO\�GULYHQ�E\�JURZWK�LQ�WKH�QXPEHU�RI�European platforms.

Note: This research was conducted during the active debate in the US Congress over the JOBS Act, which contained a provision for a crowdfunding exemption. The passing of this exemption will likely have a profound effect on growth of CFPs in the HTXLW\�EDVHG�FDWHJRU\�LQ�WKH�8QLWHG�6WDWHV� Source: Massolution

GROWTH IN NUMBER OF CFPs BY CATEGORYBased on a sample of 143 CFPs

2. MARKET GROWTH AND COMPOSITION

41% CAGRDONATION-BASED

79% CAGRREWARD-BASED

50% CAGRLENDING-BASED

2007 2008 2009 20112010

21

36

53

88

143

114% CAGREQUITY-BASED

40

62

20

21

30

25

18

15

23

10

10

10

17

793

1064 1

THE INDUSTRY WEBSITE TM

PAGE 29© 2012 Crowdsourcing, LLC | [email protected]

MARKET COMPOSITION, BY NUMBER OF CFPs, VARIES SIGNIFICANTLY BY CATEGORY ACROSS REGIONS

0DUNHW�FRPSRVLWLRQ��LQ�WHUPV�RI�WKH�QXPEHU�RI�FURZGIXQGLQJ�SODWIRUPV��YDULHV�VLJQLȴFDQWO\�E\�UHJLRQV�

North America, predictably, has a very low proportion RI�HTXLW\�EDVHG��SODWIRUPV�DW�RQO\�����VHH�QRWH���GXH�WR�regulations. The largest number of North American CFPs (almost half) are in the donation-based category.

(XURSHDQ�&)3V�IRFXV�RQ�UHZDUG�EDVHG�SODWIRUPV��������larger than the second and third categories combined with HTXLW\�EDVHG��DQG�OHQGLQJ�EDVHG��SODWIRUPV�FROOHFWLYHO\�WRWDOLQJ�����RI�WKH�(XURSHDQ�PDUNHW��

2WKHU�UHJLRQV�VKRZ�D�VLJQLȴFDQW�SUHIHUHQFH�IRU�UHZDUG�based platforms, with approximately two-thirds of all CFPs in that category.

Note: Participants in our survey included North American CFPs RIIHULQJ�HTXLW\�EDVHG�LQYHVWPHQWV�WR�$FFUHGLWHG�,QYHVWRUV�RU�UHYHQXH�RU�SURȴW�VKDUH�DUUDQJHPHQWV� Source: Massolution

PERCENTAGE BREAKDOWN OF CFPs BY REGION AND CATEGORYBased on a sample of 143 CFPs, 2011

2. MARKET GROWTH AND COMPOSITION

EUROPE OTHERREGIONS

NORTHAMERICA

22%

47%

9%

22%

46%

27%

12%

6%

11%

68%

16%

5%

DONATION-BASED

REWARD-BASED

LENDING-BASED

EQUITY-BASED

THE INDUSTRY WEBSITE TM

PAGE 30© 2012 Crowdsourcing, LLC | [email protected]

MORE THAN 1 MILLION SUCCESSFUL FUND-RAISING CAMPAIGNS WERE RUN BY CFPs IN 2011

TOTAL NUMBER OF CAMPAIGNS, 2011

Source: Massolution

2. MARKET GROWTH AND COMPOSITION

WORLDWIDE

NORTHAMERICA

EUROPE

OTHERREGIONS1,187K

532K 654K

1K

THE INDUSTRY WEBSITE TM

PAGE 31© 2012 Crowdsourcing, LLC | [email protected]

NUMBER OF CAMPAIGNS BY CATEGORYMillions of campaigns, based on a sample of 92 CFPs

THE MAJORITY OF CAMPAIGNS ARE IN THE '21$7,21�%$6('�&$7(*25<��%87�(48,7<�BASED CAMPAIGNS RAISE MUCH LARGER AMOUNTS

'RQDWLRQ�EDVHG�FURZGIXQGLQJ�DFFRXQWV�IRU�WKH�RYHUZKHOPLQJ�PDMRULW\�RI�WKH�FDPSDLJQV��SULPDULO\�GXH�WR�UHODWLYHO\�ORZ�DYHUDJH�VL]H�RI�WKH�GRQDWLRQ�campaign.

The reward-based category shows the fastest growth in terms of the number of campaigns, albeit off a low base.

7KH�HTXLW\�EDVHG�FDWHJRU\�IHDWXUHV�D�ORZ�QXPEHU�RI�campaigns in relative terms, but with a much higher average amount of funds raised per campaign.

Source: Massolution

2. MARKET GROWTH AND COMPOSITION

2011

1,187

2010

754

2009

527

47% CAGRDONATION-BASED

539% CAGRREWARD-BASED

82% CAGRLENDING-BASED

119% CAGREQUITY-BASED

50% CAGR

$84,597

$664 $4,076 $5,587

DONATIONS-BASED

REWARD-BASED

LENDING-BASED

EQUITY-BASED

AVERAGE CAMPAIGN SIZEUS dollars

THE INDUSTRY WEBSITE TM

PAGE 32© 2012 Crowdsourcing, LLC | [email protected]

CROWDFUNDING MODELS

4. CFPs VALUE PROPOSITION, FUNCTIONALITY & APPROACH

1. INTRODUCTION ANDMETHODOLOGY

3. CROWDFUNDING MODELS

3. CROWDFUNDINGMODELS

2. MARKET GROWTHAND COMPOSITION

0DVVROXWLRQ�GHȴQHV�IRXU�W\SHV�RI�FURZGIXQGLQJ�SODWIRUPV��

ȏ� (TXLW\�EDVHG�FURZGIXQGLQJ�

ȏ� /HQGLQJ�EDVHG�FURZGIXQGLQJ�

ȏ� 5HZDUG�EDVHG�FURZGIXQGLQJ��DQG

ȏ� 'RQDWLRQ�EDVHG�FURZGIXQGLQJ�

&URZGIXQGLQJ�IRU�ȴQDQFLDO�UHWXUQ��L�H���FROOHFWLYHO\��HTXLW\�based and lending-based crowdfunding) is most effective for digital goods such as applications or computer games, ȴOPV��PXVLF��RU�OLWHUDWXUH��,W�DOVR�UDLVHV�WKH�ODUJHVW�VXPV�RI�PRQH\�SHU�FDPSDLJQ��0RUH�WKDQ�����RI�WKH�FDPSDLJQV�LQ�WKLV�category raise above $25,000.

Donation-based and reward-based crowdfunding for cause-based campaigns that appeal to funders’ personal beliefs

(e.g., environment, community, faith) and passions perform best. Donation-based and reward-based crowdfunding for art and performing arts projects drive less funding volume than the mainstream media suggests. The campaigns in these categories are much smaller, with two-thirds of them generating less than $5,000.

THE INDUSTRY WEBSITE TM

PAGE 33© 2012 Crowdsourcing, LLC | [email protected]

ALLOCATION OF CAPITALPercentage, based on a sample of 19 CFPs, 2011

CROWDFUNDING FOR FINANCIAL RETURN IS PRIMARILY DIRECTED TOWARD PROJECTS THAT CAN BE EASILY DESCRIBED ON THE INTERNET

(TXLW\�EDVHG�DQG�OHQGLQJ�EDVHG�FURZGIXQGLQJ�SHUIRUPV�ZHOO�IRU�VRIWZDUH��,QWHUQHW��KLJK�WHFK�DQG�media.

We believe this is the case because:

ȏ� Digital projects present well on crowdfunding platforms;

ȏ� They appeal to Internet savvy investors that are drawn to the online social experience of crowdfunding;

ȏ� Investors can easily associate with the content, products and services being funded.

Source: Massolution

3. CROWDFUNDING MODELS

SOFTWARE, INTERNET 43%

COMPUTERS, TELECOM 14%

MEDIA 7%

ENVIRONMENT 6%

CONSUMER PRODUCTS 5%

OTHER 24%

THE INDUSTRY WEBSITE TM

PAGE 34© 2012 Crowdsourcing, LLC | [email protected]

(48,7<�%$6('�&52:')81',1*�5$,6(6�7+(�LARGEST AMOUNT OF FUNDS PER PROJECT

(TXLW\�EDVHG�FURZGIXQGLQJ�SURGXFH�WKH�ODUJHVW�DPRXQW�RI�IXQGV�UDLVHG�RQ�D�SHU�SURMHFW�EDVLV�

2QO\����RI�WKH�IXQGV�UDLVHG�RQ�HTXLW\�EDVHG�FURZGIXQGLQJ�platforms were raised for projects that drew less than ��������RI�IXQGLQJ�LQ�WRWDO��0HDQZKLOH������RI�WKH�IXQGV�UDLVHG�E\�HTXLW\�EDVHG�SODWIRUPV�ZHUH�UDLVHG�IRU�SURMHFWV�that drew $250,000 or more in funding.

/DUJH�VXPV�FDQ�EH�UDLVHG�YLD�HTXLW\�EDVHG�FURZGIXQGLQJ�platforms; crowdfunding shows to be a viable alternative for raising capital to fund small businesses and start-ups.

1RWH���2XU�FDOFXODWLRQV�GR�QRW�UHȵHFW�WKH�QXPEHU�RI�SURMHFWV�IRU�D�VSHFLȴF�IXQGLQJ�UDQJH��EXW�UDWKHU�WKH�WRWDO�QXPEHU�RI�IXQGV�UDLVHG�IRU�SURMHFWV�WKDW�IDOO�ZLWKLQ�D�VSHFLȴF�IXQGLQJ�UDQJH� Source: Massolution

FUNDS PAID OUT PER EQUITY-BASED PROJECTPercentage, based on sample of 10 CFPs, 2011

3. CROWDFUNDING MODELS

>$250,00121%

<$10,0006%

$10,001-$25,00010%

$25,001-$50,000

16%

26%$50,001-$100,000

$100,001-$250,000

21%

THE INDUSTRY WEBSITE TM

PAGE 35© 2012 Crowdsourcing, LLC | [email protected]

DONATION-BASED AND REWARD-BASED CROWDFUNDING PERFORM WELL FOR &$86(6�7+$7�$33($/�72�)81'(56ȇ�%(/,()6�AND PASSIONS

'RQDWLRQ�EDVHG�DQG�UHZDUG�EDVHG�FURZGIXQGLQJ�KDYH�EHHQ�PRVW�VXFFHVVIXO�IRU�FDXVHV�WKDW�DSSHDO�WR�IXQGHUVȇ�SHUVRQDO�EHOLHIV�DQG�SDVVLRQV��H�J���UHOLJLRQ���

While funding for the arts and performing arts receives more attention from the media, these sectors drive less volume. Funding for artists, etc., have raised a lower amount in terms of total dollars than crowdfunding directed towards causes that help people in need, the environment, health, or faith based causes.

Source: Massolution

ALLOCATION OF CAPITALPercentage, based on sample of 33 CFPs, 2011

3. CROWDFUNDING MODELS

HEALTH, ENVIRONMENT 30%

RELIGION 16%

FILMS, MUSIC, ETC 9%

COMMUNITY 8%

EDUCATION 7%

OTHER 30%

THE INDUSTRY WEBSITE TM

PAGE 36© 2012 Crowdsourcing, LLC | [email protected]

DONATION-BASED AND REWARD-BASED CROWDFUNDING DRAW LOWER LEVELS OF FUNDING PER PROJECT THAN LENDING-%$6('�$1'�(48,7<�%$6('�352-(&76

'RQDWLRQ�EDVHG�DQG�UHZDUG�EDVHG�FURZGIXQGLQJ�JHQHUDOO\�DWWUDFW�OHVV�IXQGLQJ�SHU�SURMHFW�WKDQ�HTXLW\�EDVHG�RU�OHQGLQJ�EDVHG�FURZGIXQGLQJ�

Of the funds raised on donation-based and reward-based FURZGIXQGLQJ�SODWIRUPV������DUH�SDLG�RXW�WR�SURMHFWV�WKDW�GUDZ�OHVV�WKDQ��������LQ�IXQGLQJ��2QO\�����DUH�SDLG�RXW�to projects that draw more than $10,000 in funding. The UHPDLQLQJ�����RI�DOO�IXQGV�UDLVHG�E\�GRQDWLRQ�EDVHG�DQG�reward-based crowdfunding platforms are paid out to projects that raise between $5,000 and $10,000.

Source: Massolution

FUNDS PAID OUT PER PROJECT FOR DONATION-BASED AND REWARD-BASED PROJECTSPercentage, based on a sample of 25 CFPs, 2011

3. CROWDFUNDING MODELS

$7,501-$10,0009%

>$10,00110%

<$2,50035%

28%$2,501-$5,000

$5,001-$7,500

18%

THE INDUSTRY WEBSITE TM

PAGE 37© 2012 Crowdsourcing, LLC | [email protected]

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

1. INTRODUCTION ANDMETHODOLOGY

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

3. CROWDFUNDINGMODELS

2. MARKET GROWTHAND COMPOSITION

0RVW�FURZGIXQGLQJ�SODWIRUPV�JHQHUDWH�UHYHQXH�E\�FKDUJLQJ�D�SHUFHQWDJH�FRPPLVVLRQ�RQ�IXQGV�SDLG�RXW�WR�IXQGUDLVHUVȇ��7KLV�FRPPLVVLRQ�LV�W\SLFDOO\�FDOFXODWHG�IURP�WKH�WRWDO�IXQGV�UDLVHG��DQG�RU�EDVHG�RQ�DFKLHYLQJ�D�ȊIXOO\�IXQGHGȋ�JRDO�

Commissions are generally lower in North America compared ZLWK�RWKHU�UHJLRQV�DQG�(XURSH��OLNHO\�UHȵHFWLQJ�D�KLJKHU�GHJUHH�of competition.

:KLOH�WHFKQRORJ\�OLFHQVLQJ�LV�D�OHVV�IUHTXHQW�VRXUFH�RI�UHYHQXH��a number of platforms generate additional income by offering ZKLWH�ODEHO�VROXWLRQV�IRU�ZKLFK�WKH\�FKDUJH�D�ȴ[HG�OLFHQVH�IHH�and maintenance fee.

,Q�FRQWUDVW�WR�SRSXODU�EHOLHI�WKDW�WKH�ȴUVW�����RI�IXQGV�WDNH�ORQJHU�WR�UDLVH�WKDQ�WKH�ODVW������RXU�GDWD�VKRZV�LW�WDNHV������

ZHHNV�RQ�DYHUDJH��DFURVV�DOO�FDWHJRULHV��WR�UDLVH�WKH�ȴUVW�����of the funding goal and 3.18 weeks on average to raise the ODVW�����RI�WKH�IXQGLQJ�JRDO��/HQGLQJ�EDVHG�FDPSDLJQV�WDNH�DSSUR[LPDWHO\�����OHVV�WLPH�WR�FRPSOHWH�WKDQ�HTXLW\�EDVHG�RU�donation-based campaigns.

$SSUR[LPDWHO\�����RI�DOO�&)3V�UHTXLUH�LQYHVWRUV�WR�GHSRVLW�PRQH\�LQ�HVFURZ�DFFRXQWV������XVH�3D\3DO�DV�D�SD\PHQW�method.

Platform reliability (i.e., up-time) is a differentiating factor of FKRLFH�IRU�UHZDUG�EDVHG�&)3V��(TXLW\�EDVHG�DQG�OHQGLQJ�EDVHG�SODWIRUPV�IRFXV�RQ�UHSXWDWLRQ��7KH�DELOLW\�WR�UHTXHVW�RU�DFFHSW�funds from countries, other than the home country of the CFPs is an important differentiating factor for donation-based and reward-based CFPs.

4. CFPs VALUE PROPOSITION, FUNCTIONALITY & APPROACH

THE INDUSTRY WEBSITE TM

PAGE 38© 2012 Crowdsourcing, LLC | [email protected]

29(5�����2)�&)3V�&+$5*(�$�75$16$&7,21�FEE BASED ON A PERCENTAGE COMMISSION OF FUNDS PAID OUT

&)3V�JHQHUDWH�UHYHQXH�E\�FKDUJLQJ�D�WUDQVDFWLRQ�IHH��GHWHUPLQHG�DV�D�SHUFHQWDJH�FRPPLVVLRQ�RQ�IXQGV�SDLG�RXW�WR�IXQGUDLVHUV��&RPPLVVLRQV�UDQJH�IURP����RQ�WKH�ORZHU�HQG�WR�D�PD[LPXP�RI�����RQ�WKH�XSSHU�HQG��$�FRPPLVVLRQ�LV�FDOFXODWHG�IURP�WKH�WRWDO�IXQGV�UDLVHG��DQG�RU�EDVHG�RQ�DFKLHYLQJ�D�ȊIXOO\�IXQGHGȋ�JRDO�

Commissions are generally lower in North America and (XURSH��DYHUDJH�����WKDQ�LQ�RWKHU�FRXQWULHV��DYHUDJH������:H�EHOLHYH�WKDW�WKLV�UHȵHFWV�D�KLJKHU�GHJUHH�RI�competition in North America and Europe compared with other countries. We did not observe notable differences between different types of platforms, or between recently founded and older platforms.

$Q�DGGLWLRQDO�VRXUFH�RI�LQFRPH�ZLWK�VRPH�&)3V������RI�RXU�VXUYH\�UHVSRQGHQWV��LV�WR�FKDUJH�IXQGHUV�D�ȴ[HG�IHH��LQ�the region of $15 (median), per campaign.

Source: Massolution

COMMISSIONS EARNED BY CFPsPercentage, based on a sample of 60 CFPs

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

ALL 42%

NORTH AMERICA 60%

EUROPE 36%

OTHER REGIONS 33%

ALL 63%

NORTH AMERICA 47%

EUROPE 67%

OTHER REGIONS 78%

58%

40%

64%

67%

37%

53%

33%

22%

Based on funds raised

Based on a fully-funded goal

YES NO

1RWH��,Q�WKH�DFFRPSDQ\LQJ�FKDUW��WRWDOV�GR�QRW�DGG�XS�WR������for each geographic area, as CFPs were able to present their approach to both partially-funded and fully-funded campaigns. For instance, a number of platforms charge higher commissions for partially-funded campaigns, but still pay-out funds raised to fundraisers even if a funding goal is not reached.

THE INDUSTRY WEBSITE TM

PAGE 39© 2012 Crowdsourcing, LLC | [email protected]

$3352;,0$7(/<�����2)�&)3V�2))(5�:+,7(�LABEL CROWDFUNDING SOLUTIONS

$ERXW�D�TXDUWHU�RI�DOO�&)3V�RIIHU�ZKLWH�ODEHO�VROXWLRQV�WR�JHQHUDWH�DGGLWLRQDO�UHYHQXH��VRPHWLPHV�UHWDLQLQJ�UHVSRQVLELOLW\�IRU�EDFN�RɝFH�QHWWLQJ�DQG�VHWWOHPHQWV�

The one-off setup fee for white label solutions ranges from $3,500 (reward-based platform solution) to above ����������HTXLW\�EDVHG�SODWIRUP�VROXWLRQ��EDVHG�RQ�D�sample of 12 survey respondents. The median of all responses was $15,000.

Furthermore, 11 survey respondents indicated that they FKDUJHG�D�ȴ[HG�PRQWKO\�PDLQWHQDQFH�IHH�IRU�ZKLWH�ODEHO�solutions. This fee ranged from $150 on the lower end (reward-based platform solution) to above $10,000 on the XSSHU�HQG��HTXLW\�EDVHG�SODWIRUP�VROXWLRQ���7KH�PHGLDQ�RI�all responses was $1,500.

WHITE LABEL OFFERINGS BY CFPsPercentage, based on a sample of 77 CFPs

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

Source: Massolution

YES NO

NORTH AMERICA

EUROPE

OTHER REGIONS

26%74%

0%100%

30%70%

REWARD-BASED

DONATION-BASED20%

80%

15%85%

EQUITY-BASED

LENDING-BASED42%

58%

36%64%

ALL25%

75%

THE INDUSTRY WEBSITE TM

PAGE 40© 2012 Crowdsourcing, LLC | [email protected]

THE ROLE CROWDFUNDING PLATFORMS PLAY IN THE TRANSACTION BETWEEN FUNDERS AND FUNDRAISERS IS DIFFERENT ACROSS REGIONS

7KH�PDMRULW\�RI�SODWIRUPV�LQ�RXU�VDPSOH�UHTXLUH�SDUWLHV�WR�HQWHU�LQWR�D�FRQWUDFW�EXW�GR�QRW�EHFRPH�D�FRQWUDFW�SDUW\�WKHPVHOYHV��,Q�(XURSH������RI�SODWIRUPV�UHTXLUH�FRQWUDFWV�EHWZHHQ�WKH�SDUWLHV�DQG�����RI�SODWIRUPV�LQ�RWKHU�UHJLRQV�UHTXLUH�FRQWUDFWV��

There are notable differences among regions and with GLIIHUHQW�W\SHV�RI�SODWIRUPV��,Q�1RUWK�$PHULFD��RQO\�����RI�SODWIRUPV�LQGLFDWH�WKDW�WKH\�UHTXLUH�FRQWUDFWV�EHWZHHQ�funders and fundraisers.

A minority of platforms become a party to the contract ZLWK�����RI�(XURSHDQ�SODWIRUPV�DQG�����RI�SODWIRUPV�from other regions becoming a contract party. In contrast, LQ�1RUWK�$PHULFD��RQO\�����RI�SODWIRUPV�EHFRPH�D�contract party if funding occurs.

CFPs LEVEL OF INVOLVEMENT IN CONTRACTSPercentage, based on sample of 70 CFPs

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

Source: Massolution

YES NO

ALL 66%

NORTH AMERICA 39%

EUROPE 73%

OTHER REGIONS 87%

ALL 29%

NORTH AMERICA 12%

EUROPE 37%

OTHER REGIONS 29%

34%

61%

27%

13%

71%

88%

63%

71%

THE INDUSTRY WEBSITE TM

PAGE 41© 2012 Crowdsourcing, LLC | [email protected]

AVERAGE CROWDFUNDING CAMPAIGN TIMEFRAMESWeeks, based on sample of 83 CFPs

LAUNCH TO COMPLETION TIME OF LENDING-BASED CAMPAIGNS IS ON AVERAGE HALF 7+$7�2)�(48,7<�%$6('�$1'�'21$7,21�BASED CAMPAIGNS

7KH�WLPH�IURP�ODXQFK�WR�FRPSOHWLRQ�LV�DERXW�KDOI�DV�ORQJ�IRU�SURMHFWV�SRVWHG�RQ�OHQGLQJ�EDVHG�SODWIRUPV�DV�LW�LV�IRU�SURMHFWV�SRVWHG�RQ�HTXLW\�EDVHG��DQG�GRQDWLRQ�EDVHG�SODWIRUPV��3URMHFWV�SRVWHG�RQ�UHZDUG�EDVHG�FURZGIXQGLQJ�SODWIRUPV�WDNH�RQ�DYHUDJH��DSSUR[LPDWHO\����ZHHNV�IURP�ODXQFK�WR�FRPSOHWLRQ�

,QWHUHVWLQJO\��UHDFKLQJ�WKH�ȴUVW�����PLOHVWRQH�DQG�WKH�ODVW�����PLOHVWRQH�XVXDOO\�WDNHV�D�VLPLODU�DPRXQW�RI�WLPH�IRU�DOO�W\SHV�RI�SODWIRUPV��,Q�IDFW��WKH�ȴQDO�����RQ�DYHUDJH�WDNHV�VOLJKWO\�ORQJHU�WKDQ�WKH�ȴUVW�����RQ�DOO�types of platforms. These statistics lead us to believe that campaigns on average do not accelerate after certain PLOHVWRQHV��7KLV�ȴQGLQJ�FRQWUDGLFWV�SUHYLRXV�VWXGLHV��DQG�VRPH�KLJK�SURȴOH�QRWDEOH�H[FHSWLRQV��WKDW�IRXQG�WKDW�funding accelerates toward the end of a project.

Source: Massolution

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

EQUITY-BASED

LENDING-BASED

REWARD-BASED

DONATION-BASED

ALL

LAUNCH TO COMPLETION

9.1

FIRST 25% MILESTONE

LAST 25% MILESTONE

8.24.8

10.010.2

2.0

2.52.3

2.93.6

3.3 3.1

2.63.6 3.3

THE INDUSTRY WEBSITE TM

PAGE 42© 2012 Crowdsourcing, LLC | [email protected]

FUNDER AND FUNDRAISER ACTIVITYPercentage based on sample of 57 and 47 CFPs, respectively

MOST FUNDERS PARTICIPATE IN NO MORE THAN ONE OR TWO CAMPAIGNS

1HDUO\�����RI�IXQGHUV�KDYH�SDUWLFLSDWHG�LQ�RQO\�RQH�RU�WZR�FURZGIXQGLQJ�FDPSDLJQV��2QO\����RI�IXQGHUV�KDYH�SDUWLFLSDWHG�LQ�EHWZHHQ�WKUHH�DQG�ȴYH�FDPSDLJQV��DQG�RQO\����KDYH�SDUWLFLSDWHG�LQ�PRUH�WKDQ�ȴYH�campaigns.

As the majority of funders have participated in two or less crowdfunding campaigns, it is reasonable to conclude that:

ȏ� 7KH�PDMRULW\�RI�IXQGHUV�DUH�LQ�IDFW��QRQ�SUROLȴF��RU

ȏ� Funders do not express a preference towards a particular crowdfunding platform.

1HDUO\�����RI�IXQGUDLVHUV�KDYH�UDLVHG�PRQH\�YLD�WKH�same platform more than twice. Furthermore, survey UHVSRQGHQWV�LQGLFDWHG�WKDW����RI�WKHLU�IXQGUDLVHUV�KDYH�raised money via their platform in excess of three times.

Fundraisers that are going to crowdfund for a second time or more seem to be more willing to use the same CFP. Funders on the other hand either engage in crowdfunding only once or show less loyalty towards a particular platform.

Source: Massolution

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

FUNDERS FUNDRAISERS

89%

69%

7%26%

4% 5%

1-2 CAMPAIGNS

3-5 CAMPAIGNS

>5 CAMPAIGNS

THE INDUSTRY WEBSITE TM

PAGE 43© 2012 Crowdsourcing, LLC | [email protected]

PAYMENT METHODS OFFEREDPercentage, based on sample of 36 CFPs

DEPOSITS IN ESCROW ACCOUNT REQUIREDPercentage, based on sample of 75 CFPs

OTHER FINANCIALINSTITUTIONS

67%

DIRECTLYESTABLISHED

PAYPAL

33%41%

59%

30%

70%

$3352;,0$7(/<�����2)�$//�&)3V�5(48,5(�INVESTORS TO DEPOSIT MONEY IN ESCROW ACCOUNTS

$SSUR[LPDWHO\�����RI�FURZGIXQGLQJ�SODWIRUPV�UHTXLUH�LQYHVWRUV�WR�GHSRVLW�PRQH\�LQ�HVFURZ�DFFRXQWV��7KHUH�DUH�QR�QRWDEOH�GLIIHUHQFHV�EHWZHHQ�GLIIHUHQW�FDWHJRULHV�RI�FURZGIXQGLQJ�SODWIRUPV�RU�EHWZHHQ�GLIIHUHQW�UHJLRQV�

7KH�PDMRULW\�RI�SODWIRUPV�WKDW�UHTXLUH�HQWUHSUHQHXUV�to deposit money use PayPal as a payment method. 0HDQZKLOH������RIIHU�RWKHU�IRUPV�RI�SD\PHQW�VHUYLFHV��DQG�����RI�SODWIRUPV�GLUHFWO\�HVWDEOLVK�DQ�HVFURZ�DFFRXQW�

Escrow accounts are particularly popular for “all-or-nothing” crowdfunding models that only pay out funds for projects surpassing a minimum funding threshold. By establishing an escrow account, platforms can make sure that funders live up to their funding commitment, and that investees are not able to access funds before target funding thresholds are reached.

At current rates, it is unlikely that interest earned from HVFURZ�DFFRXQWV�VLJQLȴFDQWO\�DGGV�WR�&)3V�HDUQLQJV�

Source: Massolution

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

YES NO

NO55%

YES45%

THE INDUSTRY WEBSITE TM

PAGE 44© 2012 Crowdsourcing, LLC | [email protected]

FINANCIAL PARAMETERS GUIDING CAMPAIGNS DIFFER ACROSS CFP CATEGORIES

CAMPAIGN PARAMETERSPercentage of CFPs which impose minimum or maximum thresholds (based on a sample of 68 CFPs)

3ODWIRUPV�IURP�DOO�FDWHJRULHV�WHQG�WR�UHTXLUH�PLQLPXP�SOHGJHV�IURP�IXQGHUV��7KH�PLQLPXP�DPRXQW�DFFHSWHG�GLIIHUV�JUHDWO\�EHWZHHQ�FDWHJRULHV��DSSUR[LPDWHO\�����IRU�HTXLW\�EDVHG�DQG�OHQGLQJ�EDVHG�SODWIRUPV��EDVHG�RQ�D�VDPSOH�RI����&)3V������IRU�UHZDUG�EDVHG�SODWIRUPV��EDVHG�RQ�D�VDPSOH�RI����&)3V���DQG����IRU�GRQDWLRQ�EDVHG�SODWIRUPV��EDVHG�RQ�D�VDPSOH�RI���&)3V��

,Q�WRWDO�KRZHYHU��RQO\�����RI�GRQDWLRQ�EDVHG�SODWIRUPV�impose a minimum threshold on the amount to be raised by IXQGUDLVHUV��ZKHUHDV�ZLWK�HTXLW\�EDVHG�DQG�OHQGLQJ�EDVHG�SODWIRUPV������DQG�����UHVSHFWLYHO\�UHTXLUH�D�PLQLPXP�

DPRXQW��)RU�HTXLW\�EDVHG�SODWIRUPV��WKLV�DPRXQW�LV�W\SLFDOO\�in the region of $100,000 (based on a sample of 5 CFPs). For lending-based platforms, it is about $1,000 (based on a VDPSOH�RI���&)3V���$ERXW�����RI�UHZDUG�EDVHG�FURZGIXQGLQJ�SODWIRUPV�UHTXLUH�D�PLQLPXP��ZKLFK�LV�DURXQG�������EDVHG�RQ�a sample of 10 CFPs).

Donation-based platforms are most likely to set maximum levels of borrowing by the fundraiser.

Many lending-based platforms also set minimum level of interest for funders.

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

EQUITY-BASED LENDING-BASED REWARD-BASED DONATION-BASEDALL

Source: Massolution

MIN. PLEDGE MIN. REQUEST MAX. REQUEST MIN. RETURN

57%89%

73%48% 50% 47% 67% 70%

52%

13% 22% 22%0%

28%0%

14% 22% 40%7%

0%

40%

THE INDUSTRY WEBSITE TM

PAGE 45© 2012 Crowdsourcing, LLC | [email protected]

)81'5$,6(56�$5(�7<3,&$//<�5(48,5('�72�'(9(/23�$�Ȇ%86,1(66�3/$1ȇ�$1'�'(6&5,%(�3(5621$/AND COMPANY BACKGROUND

REQUIREMENTS FOR ENTREPRENEURSPercentage, based on sample of 101 CFPs

0RVW�FURZGIXQGLQJ�SODWIRUPV�DVN�HQWUHSUHQHXUV�WR�GHVFULEH�WKHLU�SHUVRQDO�DQG�FRPSDQ\�EDFNJURXQG��7KLV�LV�WKH�PRVW�FRPPRQ�UHTXLUHPHQW�HQWUHSUHQHXUV�QHHG�WR�FRPSO\�ZLWK�ZKHQ�SLWFKLQJ�D�SURMHFW�RQ�D�FURZGIXQGLQJ�SODWIRUP�

7KH�VHFRQG�PRVW�LPSRUWDQW�UHTXLUHPHQW�LV�WR�SURYLGH�D�plan for how funds will be used (a business plan). Counter-

intuitively, fewer lending-based platforms than donation-based platforms ask investees for this information. This may be the case because donation-based platforms are more concerned with fraud. Knowing how the money will be allocated is the only motivation for funders to donate.

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

EQUITY-BASED LENDING-BASED REWARD-BASED DONATION-BASEDALL

Source: Massolution

DEVELOP BUSINESS PLAN DESCRIBE PERSONAL BACKGROUND DEVELOP VIDEO PITCH

80%94% 96% 90%92%85% 81%60%

91% 91% 92% 94%60%

100% 95%

THE INDUSTRY WEBSITE TM

PAGE 46© 2012 Crowdsourcing, LLC | [email protected]

3/$7)250�5(/,$%,/,7<�,6�&5,7,&$/�)25�5(:$5'�%$6('�3/$7)2506��(48,7<�%$6('�$1'�/(1',1*�BASED PLATFORMS FOCUS ON REPUTATION

MOST COMMON DIFFERENTIATING FACTORS FOR CFPs (1 OF 2)Percentage answering ‘Yes’, based on a sample of 59 CFPs

'LIIHUHQW�W\SHV�RI�FURZGIXQGLQJ�SODWIRUPV�IRFXV�RQ�GLIIHUHQW�GLVWLQJXLVKLQJ�IDFWRUV��:H�DVNHG�VXUYH\�SDUWLFLSDQWV�WR�UDQN�HLJKW�SRVVLEOH�GLIIHUHQWLDWLQJ�IDFWRUV�IURP����KLJKHVW��WR����ORZHVW���7KH�FKDUW�VKRZV�ZKDW�SHUFHQWDJH�RI�DQVZHUV�UDQNHG�WKH�KLJKHVW�

Access to investors was not consistently ranked as a top differentiating factor and was ranked as one of the least LPSRUWDQW�IDFWRUV�E\�HTXLW\�EDVHG�DQG�OHQGLQJ�EDVHG�VLWHV��

Success ratio (i.e., percentage of campaigns that achieved their funding goal) also did not rank high.

Reputation, however, scored consistently high. Combining this result with the score of “access to investors” leads us to believe that reputation is primarily important for fundraisers but not for funders. Platform reliability is a particularly important differentiating factor for lending-based and reward-based platforms.

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

EQUITY-BASED LENDING-BASED REWARD-BASED DONATION-BASEDALL

Source: Massolution

ACCESS TO INVESTORS RELIABILITY SUCCESS RATIO REPUTATION

34%17%

0%

33% 38% 32%17%

38% 46%

13% 14%33%

0%21%

6%

34%50% 54%

25% 25%

THE INDUSTRY WEBSITE TM

PAGE 47© 2012 Crowdsourcing, LLC | [email protected]

DONATION-BASED AND REWARD-BASED CFPs OFTEN PROMOTE THEIR GEOGRAPHIC REACH

MOST COMMON DIFFERENTIATING FACTORS FOR CFPs (2 OF 2)Percentage answering ‘Yes’, based on a sample of 59 CFPs

/RZ�WUDQVDFWLRQ�FRVWV�DUH�DQ�LPSRUWDQW�VWDWHG�GLIIHUHQWLDWLQJ�IDFWRU�IRU�OHQGLQJ�EDVHG�DQG�UHZDUG�EDVHG�SODWIRUPV��/RZ�FRVWV�DUH�UDQNHG�OHVV�KLJKO\�IRU�HTXLW\�EDVHG�SODWIRUPV��7KLV�FDQ�EH�H[SODLQHG�E\�WKH�LPSRUWDQFH�RI�KLJK�WRXFK�VXSSRUW�IRU�HQWUHSUHQHXUV�DQG�OLPLWHG�FKRLFH�RI�SODWIRUPV��,W�VXJJHVWV�WKDW�HTXLW\�EDVHG�SODWIRUPV�FXUUHQWO\�DUH�QRW�DW�WKH�SRLQW�RI�QHHGLQJ�WR�VWDQGDUGL]H�LQ�RUGHU�WR�VFDOH�EH\RQG�VWDQGDUG�SODWIRUP�IXQFWLRQDOLW\�DQG�WKHUHIRUH�FDQ�FXUUHQWO\�GHPDQG�D�SULFH�SUHPLXP�IRU�D�GLIIHUHQWLDWHG�VHUYLFH��

3ODWIRUP�IRFXV��L�H���FRQFHQWUDWLRQ�ZLWKLQ�D�VSHFLȴF�QLFKH��LV�

very important for all types of platforms. Given that access to investors did not score very high as a differentiated value-add, IRFXVLQJ�RQ�D�VSHFLȴF�QLFKH�PD\�EH�DQ�LPSRUWDQW�HOHPHQW�RI�the CFPs value proposition when appealing to fundraisers.

Finally, geographic reach is an important differentiating factor for donation-based and reward-based platforms, but is less LPSRUWDQW�IRU�HTXLW\�EDVHG�DQG�OHQGLQJ�EDVHG�SODWIRUPV�ZKLFK�RIWHQ�RSHUDWH�ZLWKLQ�OHJDOO\�GHȴQHG�MXULVGLFWLRQV�WRJHWKHU�with an investor bias towards investing in ventures in familiar markets and regions.

4. CFPs VALUE PROPOSITION, FUNCTIONALITY AND APPROACH

EQUITY-BASED LENDING-BASED REWARD-BASED DONATION-BASEDALL

Source: Massolution

LOW COSTS ADVANCED SUPPORT GEOGRAPHIC REACH FOCUS

32%17%

46%25% 38% 39%

50%46%

38% 31% 42%

17%

50% 56%42%

50%

31%46% 44%

23%

THE INDUSTRY WEBSITE TM

PAGE 48© 2012 Crowdsourcing, LLC | [email protected]

$33(1',;����*/266$5<

TERM DEFINITION

CAGR Compound Annual Growth

Crowdfunding platform (CFP) An operator of a funding platform that facilitates monetary exchange between funders and fundraisers.

Crowdfunding campaign An initiative to raise funds via a CFP.

Donation-based crowdfunding Crowdfunding model where funders donate to causes that they want to support, with no expected compensation (i.e., philanthropic or sponsorship based incentive).

(TXLW\�EDVHG�FURZGIXQGLQJ &URZGIXQGLQJ�PRGHO�LQ�ZKLFK�IXQGHUV�UHFHLYH�FRPSHQVDWLRQ�LQ�WKH�IRUP�RI�IXQGUDLVHUȇV�HTXLW\�EDVHG�RU�UHYHQXH�RU�SURȴW�VKDUH�DUUDQJHPHQWV��

Funded campaign A crowdfunding campaign that has achieved its funding goal and completed distribution of funds.

Lending-based crowdfunding &URZGIXQGLQJ�PRGHO�LQ�ZKLFK�IXQGHUV�UHFHLYH�ȴ[HG�SHULRGLF�LQFRPH�DQG�H[SHFW�UHSD\PHQW�RI�WKH�RULJLQDO�principal investment.

Pledged funds Amount of money that has been committed by funders to crowdfunding campaigns. Pledged funds may turn into raised funds if a campaign is successful.

Posted campaign A crowdfunding campaign that has a stated funding goal, posted on a CFP and open for fundraising.

Raised funds Amount of money that has been distributed through a CFP within a stated period of time.

Reward-based crowdfunding &URZGIXQGLQJ�PRGHO�LQ�ZKLFK�IXQGHUVȇ�SULPDU\�REMHFWLYH�IRU�IXQGLQJ�LV�WR�JDLQ�D�QRQ�ȴQDQFLDO�UHZDUG�VXFK�DV�D�WRNHQ�RU�LQ�WKH�FDVH�RI�D�PDQXIDFWXUHG�SURGXFW��D�ȴUVW�HGLWLRQ�UHOHDVH�

THE INDUSTRY WEBSITE TM

PAGE 49© 2012 Crowdsourcing, LLC | [email protected]

$33(1',;����&52:')81',1*�0$5.(7�6,=(�(67,0$7,21�0(7+2'2/2*<�

$575

$827

$68������In millions of US dollars

CFPs that provided their total raised funds in the

survey, or reported it publicly. This number

is factual; it was reported without any

PRGLȴFDWLRQ�

SURVEY RESPONDENTS LARGE CFPs

Each CFP was modelled individually based on key metrics, market

growth dynamics and other characteristics for a number of large CFPs

that did not provide data in order to estimate the

total funds.

SMALL CFPs

The average amount of funds raised by small platforms by category and by geography was

calculated and multiplied by the number of

small CFPs that did not participate in the survey.

TOTAL MARKET

)LQDO�UHSRUWHG�QXPEHU�IRU�����&)3V

THE INDUSTRY WEBSITE TM

PAGE 50© 2012 Crowdsourcing, LLC | [email protected]

ACKNOWLEDGEMENTS

We would like to thank the participating CFPs for an unprecedented response and for providing extensive data. We would like to express a special thanks to the following CFPs for their participation in the survey.

*HUULW�$KOHUV�who is currently enrolled as a dual degree student at McCombs School of Business (MBA, The University of Texas at Austin) and WHU – Otto Beisheim School of Management in Vallendar, Germany (MSc). Gerrit joined the massolution research team in December 2011 and assisted in the data collection and analysis. ([email protected])

A special thanks to our Founding Research Sponsor, EG&S, and our Research Sponsors, GATE and J.H. Cohn, who, with their support, have enabled the broad distribution of this report.

&URZGIXQGLQJ�3URIHVVLRQDO�$VVRFLDWLRQ�(CfPA) for the dedication to the facilitation of a vibrant, credible and growing crowdfunding community and the mission to advocate on behalf of the industry. Uniting a broad-based coalition of industry participants, the association is committed to supporting research essential to the credible development of the industry and to establishing the highest ethical standards. The association’s collaborations and insights DUH�VKDUHG�EURDGO\�WR�DYRLG�RQHURXV��VWLȵLQJ�bureaucracy that can endanger innovation, idea generation and job creation.

FUTURE RESEARCH

If you would like to apply to participate in future research initiatives as an analyst or sponsor, please contact us.

www.crowdfundingprofessional.org

THE INDUSTRY WEBSITE TM

Crowdsourcing.org is an initiative by massolution. This research has been produced by massolution, a unique research and advisory firm specializing in the crowdsourcing and crowdfunding industries. As an industry analyst, massolution tracks both the supply and demand side of each segment.

CROWDSOURCING, LLCEmail: [email protected] www.massolution.com

Twitter: @Crowdsourcing_ www.crowdsourcing.org

For crowdsourcing, massolution provides research and analysis covering Crowdsourcing Service Providers (CSPs), use cases and the adoption of crowdsourcing by enterprises.

For crowdfunding, massolution provides research and analysis covering Crowdfunding Platforms (CFPs), fundraisers or entrepreneurs, and funders or investors.

ABOUT MASSOLUTION

massolution’s unique data assets, fact-based research and proprietary intellectual property, drive forward-looking and actionable insights that inform the strategies and operations of business leaders and market stakeholders.