ctc 475 review gradient series –find p given g –find a given g rules: 1.p occurs two periods...

TRANSCRIPT

CTC 475 Review CTC 475 Review Gradient Series

– Find P given G– Find A given GRules:1. P occurs two periods before the first G2. n equals the number of cash flows + 13. First cash flow is G

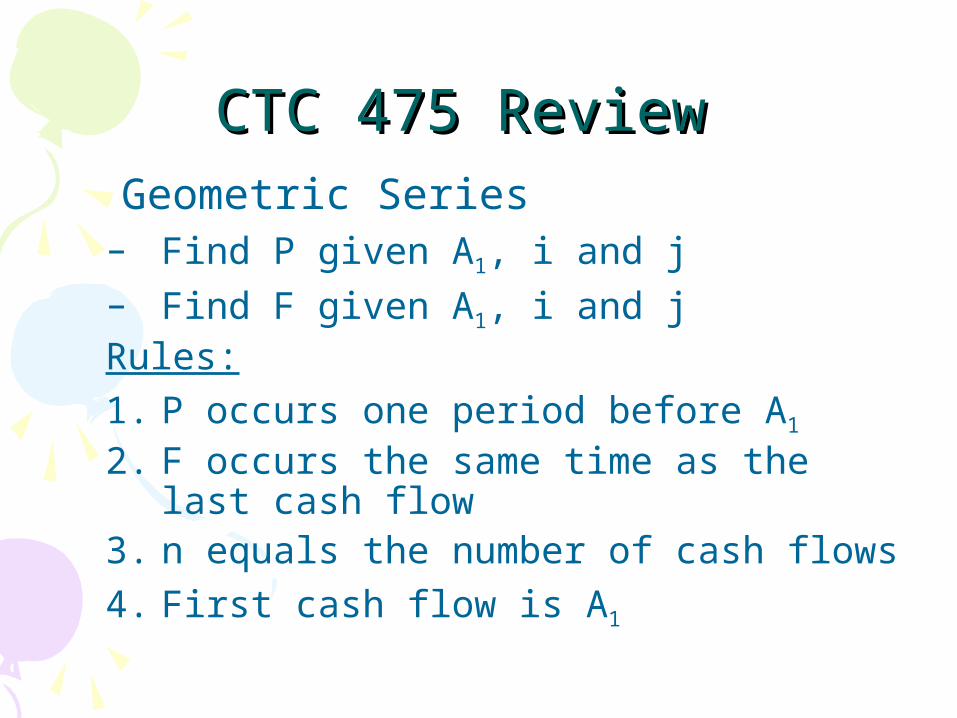

CTC 475 Review CTC 475 Review Geometric Series

– Find P given A1, i and j– Find F given A1, i and jRules:1. P occurs one period before A1

2. F occurs the same time as the last cash flow

3. n equals the number of cash flows4. First cash flow is A1

CTC 475 CTC 475 Interest/equity, Changing Interest/equity, Changing

interest rates and interest rates and

Effective interest ratesEffective interest rates

ObjectivesObjectives• Know how to determine equity

(principal) and interest on borrowed money

• Know how to recognize and solve problems when interest rates change

• Know how to calculate effective interest rates

Principle and Interest Principle and Interest

• An individual borrows $10,000 and agrees to pay it back in 5 equal payments at an interest rate of 6% per year compounded yearly.

• A=P(A/P6,5)

• A=$10,000(.2374)• A=$2,374• Total=$11,870

EOY Cash Flow

0 -$10,000

1 $2,374

2 $2,374

3 $2,374

4 $2,374

5 $2,374

Interest/EquityInterest/Equity

EOY Calculate Interest Int. Calculate Equity

Equity Sum. Equity

1 .06*$10K= $600 $2374-$600= $1774 $1774

2 .06*(10K-1774)= $494 $2374-$494= $1880 $3654

3 .06*(10K-3654)= $381 $2374-$381= $1993 $5647

4 .06*(10K-5647)= $261 $2374-$261= $2113 $7760

5 .06*(10K-7760)= $134 $2374-$134= $2240 $10K

Methods for borrowing Methods for borrowing moneymoney

1. Periodic payment of interest with all principle being repaid at end of repayment period.

2. Uniform payment of principle. 3. Uniform payment (principle and

interest). 4. Pay nothing until end of repayment

period.

Example ProblemExample ProblemMethod 1-4Method 1-4

• Borrowed amount = $40K • 18% per year compounded annually• Repayment period-5 years

Method 1-Pay Interest Method 1-Pay Interest PeriodicallyPeriodically

EOYEOY Interest Interest PaymentPayment

Principle Principle PaymentPayment

Total Total PaymentPayment

00

11 18%*40K=18%*40K= $7,200 $7,200 00 $7,200$7,200

22 $7,200$7,200 00 $7,200$7,200

33 $7,200$7,200 00 $7,200$7,200

44 $7,200$7,200 00 $7,200$7,200

55 $7,200$7,200 $40,000$40,000 $47,200$47,200

Method 2-Pay Principal Method 2-Pay Principal PeriodicallyPeriodically

EOEOYY

Interest Interest PaymentPayment

Principle Principle PaymentPayment

Remaining Remaining PrinciplePrinciple

Total Total PaymentPayment

00 $40,000$40,000

11 $7,200$7,200 $8,000$8,000 $32,000$32,000 $15,200$15,200

22 $5,760$5,760 $8,000$8,000 $24,000$24,000 $13,760$13,760

33 $4,320$4,320 $8,000 $8,000 $16,000$16,000 $12,320$12,320

44 $2,880$2,880 $8,000$8,000 $8,000$8,000 $10,880$10,880

55 $1,440$1,440 $8,000$8,000 $0$0 $9,440$9,440

Method 3-Uniform PaymentMethod 3-Uniform PaymentEOEO

YYInterest Interest

PaymentPaymentPrinciple Principle PaymentPayment

Remaining Remaining PrinciplePrinciple

Total Total PaymentPayment

00 $40,000$40,000

11 $7,200$7,200 $5,591$5,591 $34,409$34,409 $12,791$12,791

22 $6,194$6,194 $6,598$6,598 $27,811$27,811 $12,791$12,791

33 $5,006$5,006 $7,785 $7,785 $20,026$20,026 $12,791$12,791

44 $3,605$3,605 $9,186$9,186 $10,840$10,840 $12,791$12,791

55 $1,951$1,951 $10,840$10,840 $0$0 $12,791$12,791

Method 4-Pay All at EndMethod 4-Pay All at EndEOYEOY Interest Interest

PaymentPaymentPrinciple Principle PaymentPayment

Total PaymentTotal Payment

00

11 $0$0 $0$0 $0$0

22 $0$0 $0$0 $0$0

33 $0$0 $0$0 $0$0

44 $0$0 $0$0 $0$0

55 $51,510$51,510 $40,000$40,000 40K(F/P18,5)=40K(F/P18,5)= $91,510 $91,510

Changing Interest Rates Changing Interest Rates • $1000 is deposited into an account.

The account pays 4% per year for 3 years and 5% per year for 4 years. How much is the account worth at the end of year 7?

F (3)=1,000(1.04)3=$1,124.86

F(7) =$1,124.86(1.05)4=$1,367orF=$1,000(1.04)3(1.05)4=$1,367

Multiple Compounding Periods Multiple Compounding Periods in a Year in a Year

• 12% compounded quarterly is equivalent to 3% every 3 months

• 12% is the nominal interest rate (r-mixed)• 3% is the interest rate per interest period

(i-not mixed)• 3 months is the duration period • m is the number of compounding periods

per year (m=4 quarters per year)

• i = r/m =12%/4=3%

RememberRememberCan only use tools if all periods match

3% per quarter compounded quarterly for 20 quarters

ExampleExampleIf $1000 is borrowed at an interest rate of 12% compounded quarterly then what is the amount owed after 5 years?Change nominal rate:

12/4=3% per quarter comp. quarterlyChange periods to quarters:

5yrs=20 quarters

F=$1,000(1.03)20=$1806Not: $1,000(1.12)5=$1762

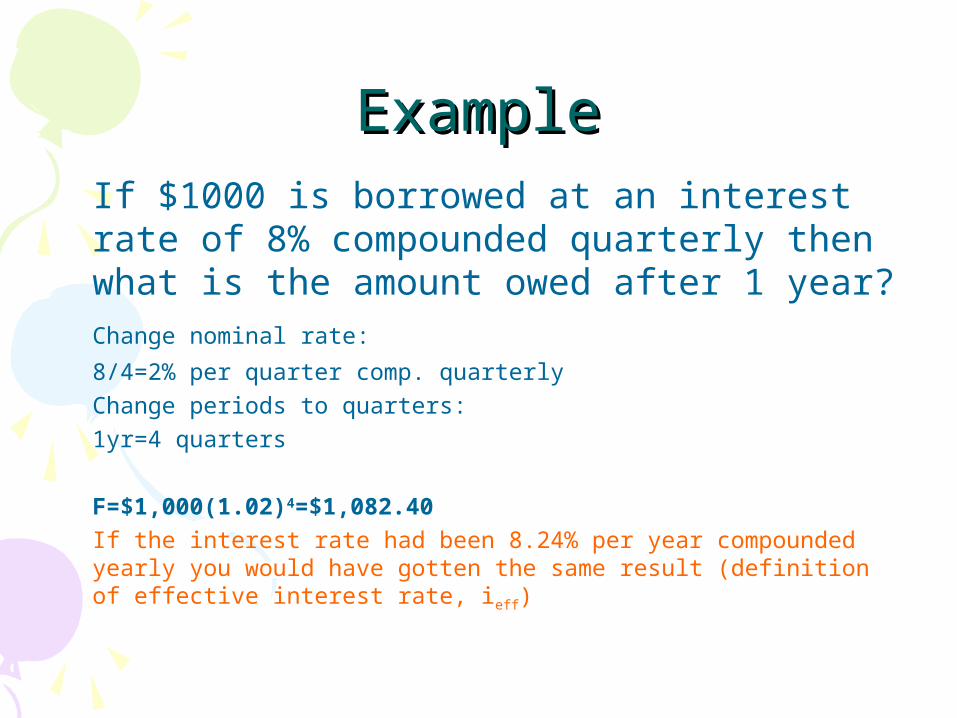

ExampleExampleIf $1000 is borrowed at an interest rate of 8% compounded quarterly then what is the amount owed after 1 year?Change nominal rate:

8/4=2% per quarter comp. quarterlyChange periods to quarters:

1yr=4 quarters

F=$1,000(1.02)4=$1,082.40If the interest rate had been 8.24% per year compounded yearly you would have gotten the same result (definition of effective interest rate, ieff)

Effective Interest RateEffective Interest Rate

• ieff=(1+r/m)m-1• ieff=(1+i)m-1

• ieff=(1+.08/4)4-1=.0824 (8.24%)• ieff=(1+.02)4-1 = .0824 (8.24%)

ExampleExample• An individual borrowed $1,000 and paid off the loan with

interest after 4.5 years. The amount paid was $1500. What was the effective annual interest rate for this transaction?

• i=?• ieff=?• n=4.5 years• m=9 (half-year increments)• $1500=$1000(1+i)9

• i=4.6% per 6 months compounded every 6 months =9.2% per year compounded every 6 months

• ieff=(1.046)2-1• ieff=9.43% per year compounded yearly

Next lectureNext lecture• What to do when

your cash flow interval doesn’t occur at the same time as the compound interval

• 3% per yr compounded qtrly; cash flows are monthly

PracticePracticeDetermine the effective annual

interest rate:6%/year, compounded monthly (6.17%)

6%/year, comp. hourly (6.18%)

2%/year, comp. semiannually (2.01%)

1%/month, comp. monthly (12.68%)

5%/year, comp. daily (5.13%)

2%/quarter, comp. monthly (8.30%)