current investment trends in azerbaijan’s gas sector · 3. i. motivation • nuclear phase-out in...

TRANSCRIPT

Current Investment Trends in Azerbaijan’s Gas SectorSevinj Amirova &Tina Flegel16th Meeting of the REFORM GroupSalzburg 2011

2Titel, Datum

outlineI. motivationII. gas sector – backgroundIII. current trends in national supply

1)

demand2)

infrstructure investments (in national supply)

IV. golden age of Azerbaijan‘s gas sector 1)

Shah Deniz gas field devolopment

V. current trends in legal regulations1)

Shah Deniz PSA

2)

law on export oil and gasVI. current trends in export

1)

southern gas corridor2)

pipeline projects

VII. conclusion

3

I. motivation•

Nuclear phase-out in Germany coupled with climate policy goals likely to create additional gas demand of 5bcm.

•

Depending on decisions regarding climate policy & nuclear as well as pace of development of renewables, European gas demand might increase even more.

•

LNG cheap right now, but tanker transportation is not necessarily commercially competitive. •

LNG regasification capacity of ca. 145bcm in Europe in 2010 stood against 94bcm imports (ca. 65% usage), none yet located in Eastern Europenatural gas from the Caspian region to supply (South &) Eastern Europe

•

The amount of gas Europe can get from the Caspian region as alternative to Russia and (unstable) North African states depends on three factors: •

the Caspian countries’

credible decision to export to Europe,

•

the amount of gas available for export, and •

the Caspian countries’

cooperation as transit states.

Peisser 2011: 5; E.On 2010 Strategy & Key Figures: 62; ERGEG 2011: 37; California Energy Commission 2010.

4

II. gas sector – background Iconventional natural gas (bcm)

Sources: BRG 2009 Energierohstoffe; BRG 2010 Kurzstudie; WoodMac

2010; BP 2011; *SOCAR 2011

Year 1990 2000 2005 2007 2009 2010*Reserves 70 1000 1371 1340 1900 2230

Year 1993 1997 2001 2007 2009 2010*Resources 700 1500 1900 1900 1900 2230

(projected) natural gas production (bcm) excluding gas flared or re-injected

•

reserves & resources have increased thanks to investment

•

the 2006 hike in natural gas production marks the 1st

phase and the 2016 hike the planned 2nd

phase of Shah Deniz development

•

ACG produces more gas than SD P1 (10 -12 bcm), but it is mostly re-injected or flared

5

II. gas sector – background II

IEA 2011; BP 2011; Mammadov 2009

•

2004: Gas bought by Gazprom from Turkmenistan & Kazakhstan apparently labeled Russian

•

Azerbaijan became a natural gas net exporter in 2007/08•

2010: 4,35bcm to Turkey; 1,03bcm to Georgia; 0,72bcm to Russia

•

since the 90s: swap with Iran to supply Nakhichevan enclave, 15%

transit fee

6

II. gas sector – background III

IEA 2011, 2006, 2002, 2000;

7

III. demand I•

annual electricity consumption to grow 2010 to 2020 by 50% (22TWh to 33TWh)

•

thermal power plant generation capacity to increase from 5.000 to 6.000 Mwe between 2011 and 2020

•

metering and billing of gas supply to all consumers expected to improve, in

connection with cost covering tariffs relative demand p.p. expected to

decrease by 15-20%•

renewables (hydro power) 15% in 2015

•

min. wage and pensions at 75AZN in 2005what is to expect here?

IEA 2011, EUI 2011; **gas re-injected and flared not included

primary energy demand (Mtoe)

2015 2025 2035

Production** 18,2 31,5 ?

Consumption 6,8 8 8,5

For export 11,4 23,5 ?

8

III. infrastructure investments II•

gas supply to 90% of the country 2012 envisaged (90% because remote areas not economical)•

some regions had been (re-)connected to the national gas grid by 2008

•

district heating is being rehabilitated and expanded•

current policies do not foresee investments in energy efficiency, but in•

new power plants (also for power export)

•

upgrade of transmission lines (secure and widen supply)•

development of conventional and renewable energy sources

Investments in Absheron peninsula: 900 mln USD 2012 – 2022 (with E.ON)

Ministry of Econoic Development of Azerbaijan 2009;

9

IV. golden age of Azerbaijan‘s gas sector I

Ministry of Econoic Development of Azerbaijan 2009;

10

•Reserves 1.31 tcm •Overall investment 25 billion USD• Gas production for: - Shah Deniz I - 8.6 bcm/a (from 2007) - Shah Deniz II - 25 bcm/a (from 2017)

•Shah Deniz Gas consumers- Turkey- Georgia- Greece- EU (2017)

IV. Shah Deniz gas field development II

11

V. gas sector - Legal regulation I

Strong foreign investment promotion through legislation:•

Production Sharing Agreements (PSA) and Intergovernmental Export Sharing Agreements (ESAs)

•

Law of the Azerbaijani Republic on Utilization of Energy Resources •

Law of the Azerbaijani Republic on Subsoil

•

Law on the Special Economic Regime for Export Oil andGas Activity

12

V. Shah Deniz PSA I

Shah Deniz PSA defines:-

Rights and obligations of SOCAR and contracting parties

-

Contractors’

participating interest shares-

Taxation

Grants “exclusive rights”

to the contractor to conduct operation with the respect to “contract area”

Exploration and Production Period -

starts from the date of noticed discovery and lasts for 30 years

and

can be expanded for 5 years. (was expanded till 2036)

13

V. Shah Deniz PSA II

Contractor parties except for the profit tax obligation shall not be subject to any taxes of any nature whatsoever arising from or related, directly or indirectly, to Hydrocarbon Activities.

Taxation:• Profit Tax –

25%

• Income Tax –

6.25%• Employee Taxes (Lohnsteuer) • No VAT

75%

14

V. Law on Export Oil and Gas Activity I

•

Special tax, customs, currency and other benefits for local contractors and their local or foreign sub-contractors

� Carrying out oil and gas activities (including the exploration for and the sale and purchase of oil and natural gas)

� Oriented towards exports (e.g., the supply of equipments, work and services in connection with oil and gas operations)

� In connection with oil and gas activities conducted

outside of Azerbaijan

•

Does NOT apply to activities under PSAs/ESAs •

Law to lose force after 15 years (unless extended)

15

V. Law on Export Oil and Gas Activity IITaxation regime •

Local contractors -

chose between: -

20% corporate income tax

-

5% gross amount of profit tax•

Foreign subcontractors –

the 5% profit tax

Benefits:•

No tax on dividends•

No branch tax for foreign subcontractors•

No property tax•

No land taxes•

NO VAT •

No customs duties

16

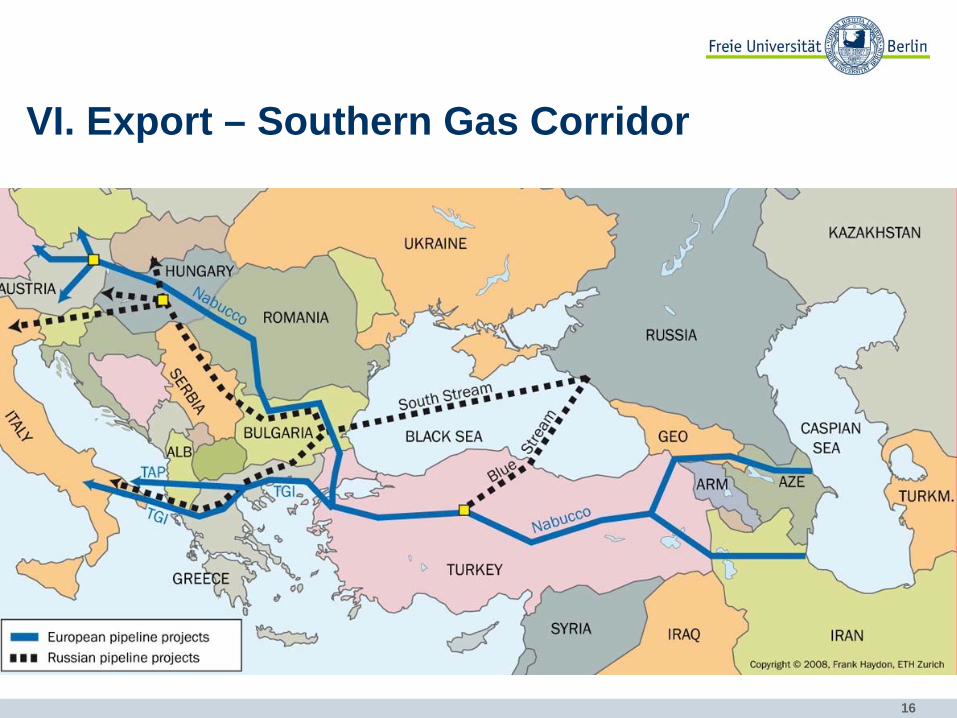

VI. Export – Southern Gas Corridor

17

VI. Export – NABUCCO I

Shareholders:OMV, MOL, RWE, BEH, Transgas, BotasCapacity: 25.5 – 31 bcm/aCAPEX: 8 bn + 4 bn?Length: 3300kmSources: AZ, TUR and North IraqMarkets: Central and Eastern Europe

18

VI. Export – ITGI II

Shareholders: Edison/DEPACapacity: 8-12 bcm/aCAPEX: 1.4 bnLength: 800 kmSources: AzerbaijanMarkets: Balkans and Italy (EU)

19

VI. Export – Trans Adriatic Pipeline III

Shareholders: EGL, Statoil, E.ON Ruhrgas Capacity: 10-20 bcm/aCAPEX: 1.5 bnLength: 520 kmSources: AzerbaijanMarkets: Western Balkans and Italy (EU)

20

VII. Conclusion

•

Market oriented competition•

Market determines commercial viability of the pipeline project

•

Reliability of the partners involved in long term projects•

Availability of the sources

•

Risks:1.

High level of interdependence

2.

Political vulnerability formed by long-term linkages of the pipeline 3.

Disruptive role of transit countries

The following principles will be used during the process for selection of an export route:

Tina Flegel & Sevinj AmirovaBerlin Center for Caspian Region Studies

Thank you for your attention!!!

Titel, Datum