current status and future of coal mining industry in indonesia · 2013-09-27 · current status and...

TRANSCRIPT

Clean Coal Day in Japan 2008

L-9-1

CURRENT STATUS AND FUTURE OF COAL MINING INDUSTRY IN INDONESIA

Supriatna Suhala

Executive Director, Indonesian Coal Mining Association (ICMA)

OUTLINEOUTLINE1.1. IntroductionIntroduction2.2. The Role of Coal in Indonesian Economic DevelopmentThe Role of Coal in Indonesian Economic Development3.3. Present Status on Coal Reserves and Resources, Production, ExporPresent Status on Coal Reserves and Resources, Production, Export t

and Domestic Sales and Domestic Sales 3.1. Coal Reserves and Resources3.1. Coal Reserves and Resources3.2. Production, Export and Sales3.2. Production, Export and Sales3.3. Coal Players3.3. Coal Players3.4. Domestic Coal Consumers3.4. Domestic Coal Consumers3.5. Coal Quality3.5. Coal Quality

4.4. Energy Mix Blue Print (2006Energy Mix Blue Print (2006--2025)2025)5.5. Long Run Prediction on Coal Domestic UtilizationLong Run Prediction on Coal Domestic Utilization6.6. Key Issues which Require Immediate ImprovementKey Issues which Require Immediate Improvement7.7. Investment Opportunity in upstream and downInvestment Opportunity in upstream and down--stream coal industriesstream coal industries8.8. Conclusion RemarksConclusion Remarks

2

CURRENT STATUS AND FUTURE OF COAL CURRENT STATUS AND FUTURE OF COAL MINING INDUSTRY IN INDONESIAMINING INDUSTRY IN INDONESIA

ByBySupriatnaSupriatna SuhalaSuhala

Executive Director of Indonesian Coal Mining Association (ICMA)Executive Director of Indonesian Coal Mining Association (ICMA)

Presented at Presented at ““Clean Coal Day in Japan 2008Clean Coal Day in Japan 2008””Japan Coal Energy Centre (JCOAL)Japan Coal Energy Centre (JCOAL)

Tokyo, 4 September 2008Tokyo, 4 September 2008

Asosiasi Pertambangan Batubara Indonesia - APBI(Indonesian Coal Mining Association - ICMA)

Clean Coal Day in Japan 2008

L-9-2

INTRODUCTIONINTRODUCTIONIn the last three years, the mining industry both in Indonesia aIn the last three years, the mining industry both in Indonesia and nd globally experienced significantly high performance.globally experienced significantly high performance.

For Indonesia, PricewaterhouseCoopers reported that in 2006:For Indonesia, PricewaterhouseCoopers reported that in 2006:-- EBITDA Margin was 41.2% in averageEBITDA Margin was 41.2% in average-- Net Profit Margin was 22.5% in averageNet Profit Margin was 22.5% in average-- Return on Capital Employed was 26.0% in averageReturn on Capital Employed was 26.0% in average-- Return on Shareholders fund was 39.4% in averageReturn on Shareholders fund was 39.4% in average-- Net Debt to Equity Ratio was 46.5% in averageNet Debt to Equity Ratio was 46.5% in average

Mining Industry in Indonesia:Mining Industry in Indonesia:-- Continue to having strong balance sheets due to strong profitsContinue to having strong balance sheets due to strong profits-- Debt to Equity Ratios having decreasedDebt to Equity Ratios having decreased-- Current Assets have also increased Current Assets have also increased

Investment in Mining Sector is increasing Investment in Mining Sector is increasing ?? however there is still however there is still room for improvement in investment climate.room for improvement in investment climate.

4

3

1.1. INTRODUCTIONINTRODUCTION

Clean Coal Day in Japan 2008

L-9-3

THE ROLE OF COAL IN INDONESIAN ECONOMIC DEVELOPMENT (2006)

The mining industry continues to be an important The mining industry continues to be an important contributor to the Indonesian economic;contributor to the Indonesian economic;

Mining Products accounted for approximately 3% Mining Products accounted for approximately 3% of the total Indonesian GDP in 2006 (up from 2% of the total Indonesian GDP in 2006 (up from 2% in 2005)in 2005)

The industry also continue to make significant The industry also continue to make significant contributions to regional and Community contributions to regional and Community DevelopmentDevelopment

In 2006, Total Growth Revenue (tax, royalties and In 2006, Total Growth Revenue (tax, royalties and other levies) increased 27% to US$ 3.4 billion, a other levies) increased 27% to US$ 3.4 billion, a record for the last 10 years.record for the last 10 years.

5

2. THE ROLE OF COAL IN INDONESIAN ECONOMIC DEVELOPMENT (2006)

Clean Coal Day in Japan 2008

L-9-4

3.3. Present Status on Coal Reserves Present Status on Coal Reserves and Resources, Production, and Resources, Production, Export and Domestic SalesExport and Domestic Sales

THE ROLE OF COAL IN INDONESIAN ECONOMIC DEVELOPMENT (2006)

(continued)

Total number of direct employees has increased by 3% Total number of direct employees has increased by 3% to approximately 38.000 in 2006to approximately 38.000 in 2006

Employee compensation has increased significantly by Employee compensation has increased significantly by approximately 49% overall due to increased benefits approximately 49% overall due to increased benefits received as a result of increased profits and production.received as a result of increased profits and production.

The outlook for the job market in the mining industry is The outlook for the job market in the mining industry is extremely positive due to the potential for new projects extremely positive due to the potential for new projects and expansions in coming years.and expansions in coming years.

Because of the indirect multiplier effect the total Because of the indirect multiplier effect the total economic benefit to Indonesia is significantly greater economic benefit to Indonesia is significantly greater than data reported.than data reported.

Source: PricewaterhouseCoopers

Clean Coal Day in Japan 2008

L-9-5

RIAURESOURCES = 2,057.22MINEABLE = 15.15

NANGROE ACEH DARUSALAMRESOURCES = 450.15MINEABLE = n.a.

WEST KALIMANTANRESOURCES = 527.52MINEABLE = n.a

CENTRAL KALIMANTANRESOURCES = 1,399.21MINEABLE = 48.59

EAST KALIMANTANRESOURCES = 19,567.79MINEABLE = 2,410.33

PAPUARESOURCES = 138.30MINEABLE = n.a.

WEST SUMATRARESOURCES = 719.09MINEABLE = 36.07

BENGKULURESOURCES = 198.37MINEABLE = 21.12

SOUTH KALIMANTANRESOURCES = 8,674.56MINEABLE = 1,787.32

SOUTH SULAWESIRESOURCES = 132.01MINEABLE = 0.06

SOUTH SUMATRARESOURCES = 22,240.40MINEABLE = 2,653.98

COAL RESOURCES AND RESERVES COAL RESOURCES AND RESERVES DISTRIBUTION BY PROVINCE (M.TONS) DISTRIBUTION BY PROVINCE (M.TONS)

20062006

10

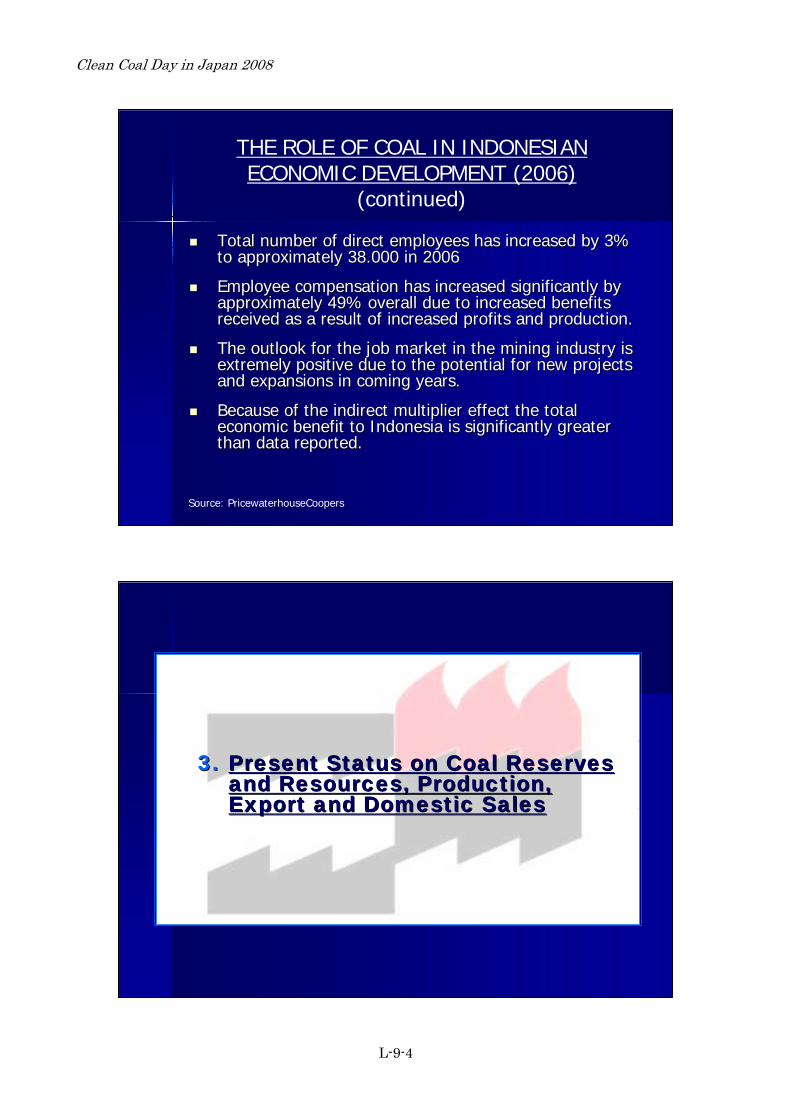

COAL RESOURCES, RESERVES AND QUALITY(2006)

6.758,9061.273,99TOTAL RESOURCES IN 2006

0,000,0030,9130,916100 6100 -- 71007100High High –– Very HighVery High

0,000,00120,35120,35< 5100 < 5100 -- 61006100Low Low –– MediumMediumPapuaPapua6.6.

0,000,002,132,13< 5100< 5100Low Low –– MediumMediumMalukuMaluku5.5.

0,000,0014,6814,686100 6100 -- 71007100High High –– Very HighVery High

0,060,06218,42218,42< 5100 < 5100 -- 61006100Low Low –– MediumMediumSulawesiSulawesi4.4.

1.219,101.219,106.844,446.844,446100 6100 -- 71007100High High –– Very HighVery High

2.769,012.769,0125.375,6925.375,69< 5100 < 5100 -- 61006100Low Low –– MediumMediumKalimantanKalimantan3.3.

134,11134,111.780,661.780,666100 6100 -- 71007100High High –– Very HighVery High

2.636,622.636,6226.872,526.872,5< 5100 < 5100 -- 61006100Low Low –– MediumMediumSumatraSumatra2.2.

0,000,002,972,976100 6100 -- 71007100High High –– Very HighVery High

0,000,0019,2419,24< 5100 < 5100 -- 61006100Low Low –– MediumMediumJavaJava1.1.

VALUE OF CALORIE(gr/cal)

CRITERIARESERVES(M. Ton)

RESOURCES(M. Ton)

QUALITY (CALORIE)

ISLANDNO

9

Clean Coal Day in Japan 2008

L-9-6

62.5

45.541.3

37.135.7429.227.3

22.11915.413.210.98.9

158.6

148

110.79

93.7685.3

73.463.457.253.9

46.740.935.330.3

212193.5

153.2

132.4

114.3102.5

91.575.672.2

60.653.9

48.840.1

0

20

40

60

80

100

120

140

160

180

200

220

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

DomesticExportProduction

Growth Production 1997 – 2007144.4 M.tons/Year or 15.81 %

Growth Export 1997 - 200711.3 M.tons/Year or 11.77 %

Growth Domestic Sales 1997 - 20073.4 M.tons/Year or 4.93 %

Source: - Directorate of Mineral and Coal Enterprise – “Indonesia Mineral and Coal Statistic 2005”- APBI-ICMA

M.T

ons

INDONESIAN COAL PRODUCTION, EXPORT AND INDONESIAN COAL PRODUCTION, EXPORT AND DOMESTIC SALES GROWTH (1995 DOMESTIC SALES GROWTH (1995 -- 2007)2007)

12

INDONESIA’SCOAL PLAYER

GROUP

COAL CONTRACTS OF WORK (CCOW HOLDERS)

**)

MINING AUTHORIZATION (MA HOLDERS)

***)

STATE OWNEDCOMPANY (PTBA)

*)

Contribute 4.8% of national coal production

Contribute 83.9% of national coal production

Contribute 11.3% of national coal production

*) 1 Company in production**) 34 Companies in production

40 Companies not yet in production***) 169 Companies in production

COAL MINING COAL MINING PLAYERS/GROUP (2006)PLAYERS/GROUP (2006)

11

Clean Coal Day in Japan 2008

L-9-7

14

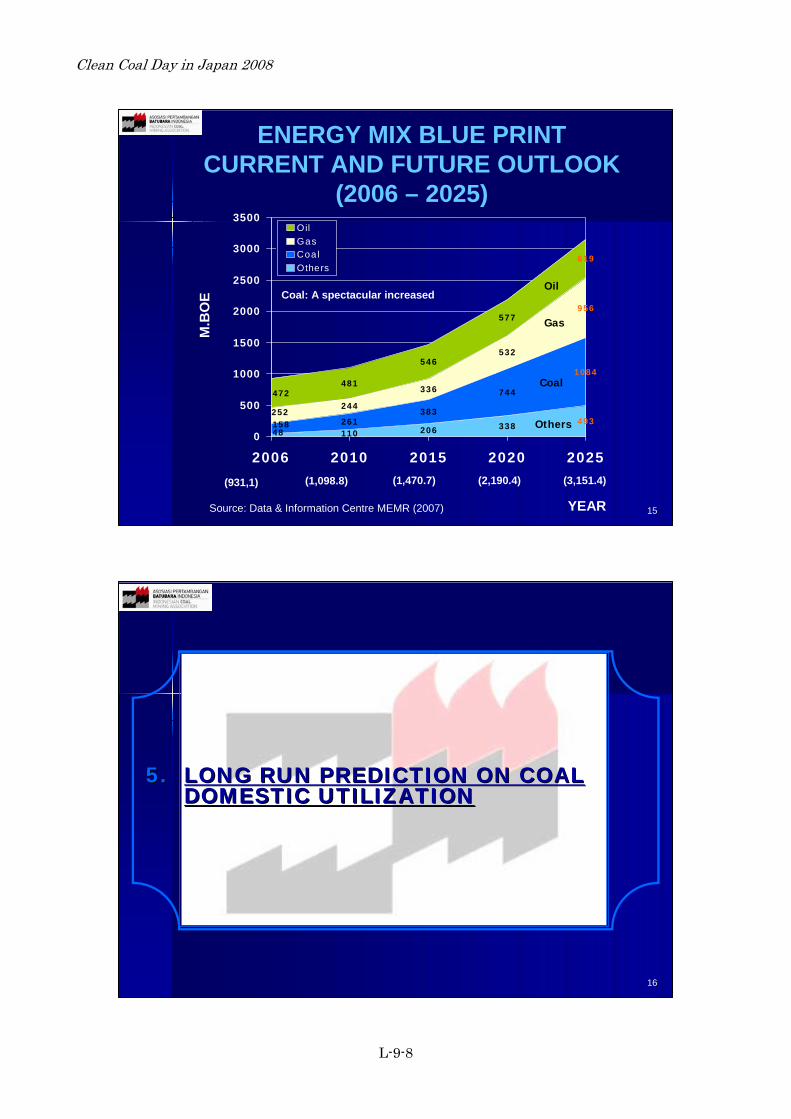

4.4. ENERGY MIX BLUE PRINT ENERGY MIX BLUE PRINT (2006 (2006 –– 2025)2025)

INDONESIA COAL QUALITY BASED ONTHE SPECIFIC ENERGY (KCAL/KG)

62%

13%

24%

1%

Medium Quality

Low QualityHigh Quality

Very High Quality

(6100-7100 kcal/kg)

(>7100 kcal/kg)

(< 5100 kcal/kg)

(5100-6100 kcal/kg)

13

Clean Coal Day in Japan 2008

L-9-8

16

5.5. LONG RUN PREDICTION ON COAL LONG RUN PREDICTION ON COAL DOMESTIC UTILIZATIONDOMESTIC UTILIZATION

110 206 338261383

744244

336

532

481

546

577

49348

1084

158

956

252

472

619

0

500

1000

1500

2000

2500

3000

3500

2006 2010 2015 2020 2025

OilGasCoalOthers

M.B

OE

YEAR

(931,1) (1,098.8) (1,470.7) (2,190.4) (3,151.4)

Source: Data & Information Centre MEMR (2007)

ENERGY MIX BLUE PRINTCURRENT AND FUTURE OUTLOOK

(2006 – 2025)

Coal: A spectacular increasedOil

Gas

Coal

Others

15

Clean Coal Day in Japan 2008

L-9-9

18

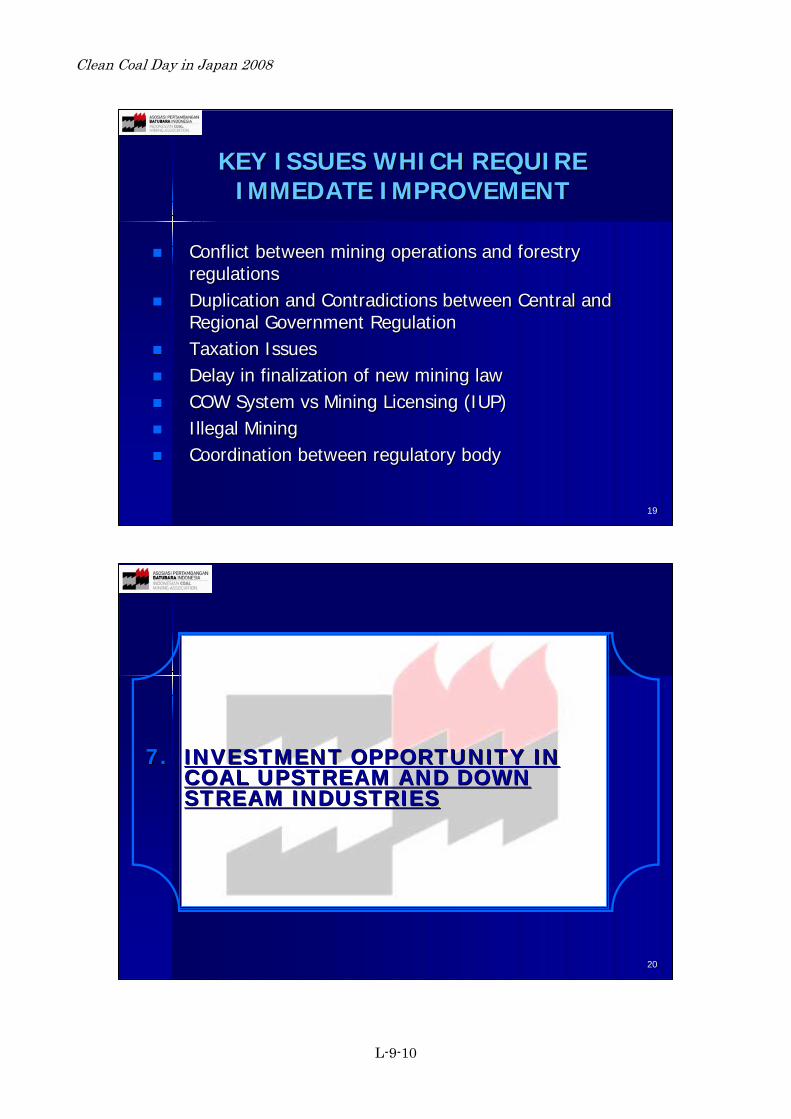

6.6. KEY ISSUES WHICH REQUIRE KEY ISSUES WHICH REQUIRE IMMEDIATE IMPROVEMENTIMMEDIATE IMPROVEMENT

LONG RUN PREDICTION ON INDONESIAN COAL PRODUCTION, EXPORT AND DOMESTIC

CONSUMPTION (2007 - 2025)

Source APBI - ICMA

ProductionRealization

Year

Production

Export

Pro

duct

ion

(M

illio

n T

ons)

Domestic Sales (Base on

17

Clean Coal Day in Japan 2008

L-9-10

20

7.7. INVESTMENT OPPORTUNITY IN INVESTMENT OPPORTUNITY IN COAL UPSTREAM AND DOWN COAL UPSTREAM AND DOWN STREAM INDUSTRIESSTREAM INDUSTRIES

KEY ISSUES WHICH REQUIRE KEY ISSUES WHICH REQUIRE IMMEDATE IMPROVEMENTIMMEDATE IMPROVEMENT

Conflict between mining operations and forestry Conflict between mining operations and forestry regulationsregulationsDuplication and Contradictions between Central and Duplication and Contradictions between Central and Regional Government RegulationRegional Government RegulationTaxation IssuesTaxation IssuesDelay in finalization of new mining lawDelay in finalization of new mining lawCOW System COW System vsvs Mining Licensing (IUP)Mining Licensing (IUP)Illegal MiningIllegal MiningCoordination between regulatory bodyCoordination between regulatory body

19

Clean Coal Day in Japan 2008

L-9-11

INVESTMENT OPPORTUNITY IN INVESTMENT OPPORTUNITY IN COAL DOWN STREAM INDUSTRIESCOAL DOWN STREAM INDUSTRIES

Coal Supplier, Exporter/ Trader.Coal Supplier, Exporter/ Trader.Energy Conversion Plant.Energy Conversion Plant.Upgrading Brown Coal.Upgrading Brown Coal.

GasificationGasification..BriquettingBriquetting. . Liquefactions.Liquefactions.

22

INVESTMENT OPPORTUNITY IN INVESTMENT OPPORTUNITY IN COAL UPSTREAM INDUSTRIESCOAL UPSTREAM INDUSTRIES

The development of green field/ Grass Root.The development of green field/ Grass Root.Joint Venture/ Joint Operation/ Acquisition.Joint Venture/ Joint Operation/ Acquisition.Mining Contractor.Mining Contractor.Transportation (River, inland, sea Transportation (River, inland, sea transportation)transportation)Coal Terminal.Coal Terminal.Washing Plant/ Blending Plant.Washing Plant/ Blending Plant.The development of Coal Bed Methane.The development of Coal Bed Methane.Post Mining Contractor.Post Mining Contractor.

21

Clean Coal Day in Japan 2008

L-9-12

CONCLUSION

1. The role of coal in Indonesian economic development will increase furthermore in the next twenty years as stated in the energy mixblue print.

2. Strong coal prices continue to drive production and exports levels.

3. To secure domestic energy supply GOI will implement DMO to coal producers at market price.

4. There are a lot of opportunity for investment in upstream and downstream coal industries.

5. There are still rooms for improvement in attracting new investors.

24

23

8.8. CONCLUSIONCONCLUSION

Clean Coal Day in Japan 2008

L-9-13

Asosiasi Pertambangan Batubara Indonesia(Indonesian Coal Mining Association)

Email: Email: [email protected]@indo.net.idMenaraMenara KuninganKuningan Building, 1Building, 1thth Floor, Suite AFloor, Suite A

JlJl. H. R. . H. R. RasunaRasuna Said Blok XSaid Blok X--7 Kav.57 Kav.5Jakarta 12940 Jakarta 12940 -- INDONESIAINDONESIA

Phone/Fax : 021Phone/Fax : 021--30015935, 30015936, 3001567430015935, 30015936, 30015674Website : Website : www.apbiwww.apbi--icma.comicma.com

THANK YOU Supriatna Suhala, Executive Director APBI-ICMA

Email : [email protected]

Clean Coal Day in Japan 2008

L-9-14

Clean Coal Day in Japan 2008

L-9-15

インドネシアにおける石炭産業の現状および将来

Supriatna Suhala

インドネシア石炭鉱山協会(ICMA)事務局長

概要概要

1.1. はじめにはじめに2.2. インドネシアの経済発展における石炭の役割インドネシアの経済発展における石炭の役割3.3. 石炭の埋蔵量と資源量、生産量、輸出量、国内販売量の現状石炭の埋蔵量と資源量、生産量、輸出量、国内販売量の現状

3.1. 3.1. 石炭の埋蔵量と資源量石炭の埋蔵量と資源量3.2. 3.2. 生産量、輸出量、販売量生産量、輸出量、販売量3.3. 3.3. 石炭産業のプレーヤー石炭産業のプレーヤー3.4. 3.4. 国内の石炭消費者国内の石炭消費者3.5. 3.5. 石炭の品質石炭の品質

4.4. エネルギーミックス計画(エネルギーミックス計画(20062006--20252025年)年)

5.5. 石炭の国内利用に関する長期予測石炭の国内利用に関する長期予測6.6. 改善を要する主要課題改善を要する主要課題7.7. 石炭産業の上流および下流における投資チャンス石炭産業の上流および下流における投資チャンス8.8. 結論結論

2

インドネシアにおける石炭産業の現状および将来インドネシアにおける石炭産業の現状および将来

ByBySupriatna SuhalaSupriatna Suhala

インドネシア石炭鉱山協会インドネシア石炭鉱山協会 (ICMA) (ICMA) 事務局長事務局長

““Clean Coal Day in Japan 2008Clean Coal Day in Japan 2008””発表発表

財団法人財団法人 石炭エネルギーセンター石炭エネルギーセンター (JCOAL)(JCOAL)東京 東京 20082008年年99月月44日日

Asosiasi Pertambangan Batubara Indonesia - APBI(インドネシア石炭鉱山協会 - ICMA)

Clean Coal Day in Japan 2008

L-9-16

3

1.1. はじめにはじめに

はじめにはじめに過去過去33年にわたり、インドネシアおよび世界の石炭鉱業は著しく高い伸び年にわたり、インドネシアおよび世界の石炭鉱業は著しく高い伸びを示した。を示した。

インドネシアについて、インドネシアについて、 20062006年にプライスウォーター・ハウス・クーパー年にプライスウォーター・ハウス・クーパース(ス(PwCPwC)は以下を報告した:)は以下を報告した:-- EBITDAEBITDAマージンは平均マージンは平均 41.2%41.2%であったであった-- 純利益率は平均純利益率は平均 22.5%22.5%であったであった-- 使用総資本利益率は平均使用総資本利益率は平均 26.0%26.0%であったであった-- 株主資本利益率は平均株主資本利益率は平均 39.4%39.4%であったであった-- Net D/E Net D/E レシオは平均レシオは平均 46.5%46.5%であったであった

インドネシアにおける石炭鉱業:インドネシアにおける石炭鉱業:-- 強い収益により強力なバランスシートを持続強い収益により強力なバランスシートを持続-- D/E D/E レシオ減少レシオ減少-- 流動資産も増加流動資産も増加

鉱業部門に対する投資は増加している鉱業部門に対する投資は増加している ?? しかし投資環境にはまだ改しかし投資環境にはまだ改善の余地がある。善の余地がある。

4

Clean Coal Day in Japan 2008

L-9-17

5

2. インドネシアの 経済発展における石炭の役割( 2006年)

インドネシアの経済発展における石炭の役割(2006年)

石炭鉱業はインドネシア経済に大きく貢献し続けている;石炭鉱業はインドネシア経済に大きく貢献し続けている;

2006 2006 年に石炭鉱業製品はインドネシアの総年に石炭鉱業製品はインドネシアの総GDPGDPのおよ のおよ そそ 3% 3% を占めた(を占めた(20052005年の年の 2%2%から増加)から増加)

石炭鉱業は地域および地域共同体の発展にも大きく貢 石炭鉱業は地域および地域共同体の発展にも大きく貢 献し続けている献し続けている

2006 2006 年の総収益成長率(税金やロイヤルティおよび他年の総収益成長率(税金やロイヤルティおよび他の賦課金)は の賦課金)は 27%27%増加し、増加し、 過去過去1010年間で最高の 年間で最高の 3434億 億 米ドルを記録した。米ドルを記録した。

インドネシアの経済発展における石炭の役割(2006年)

(続き)

20062006 年における直接雇用の総従業員数は年における直接雇用の総従業員数は3%3%増加し、お増加し、およそよそ 38,000 38,000人であった。人であった。

収益および生産量の増加に伴う利益の増大により、従業員収益および生産量の増加に伴う利益の増大により、従業員 に対する報酬は全体としておよそに対する報酬は全体としておよそ49%49%と著しく増加した。と著しく増加した。

将来の新しいプロジェクトや設備拡張の見込みにより、石将来の新しいプロジェクトや設備拡張の見込みにより、石炭鉱業界における求人市場の見通しは非常に明るい。炭鉱業界における求人市場の見通しは非常に明るい。

間接的な相乗効果により、インドネシアの経済的利益は報間接的な相乗効果により、インドネシアの経済的利益は報告されたデータよりはるかに大きい。告されたデータよりはるかに大きい。

出所:プライスウォーターハウスクーパース

Clean Coal Day in Japan 2008

L-9-18

石炭の埋蔵量、資源量、および品質(2006年)

NO 島名

品質(熱量)資源量

(百万トン)埋蔵量

(百万トン)分類発熱量

(gr/cal)

1.1. ジャワジャワ 低低 –– 中中 < 5100 < 5100 -- 61006100 19,2419,24 0,000,00

高高 –– 非常に高非常に高 6100 6100 -- 71007100 2,972,97 0,000,00

2.2. スマトラスマトラ 低低 –– 中中 < 5100 < 5100 -- 61006100 26.872,526.872,5 2.636,622.636,62

高高 –– 非常に高非常に高 6100 6100 -- 71007100 1.780,661.780,66 134,11134,11

3.3. カリマンタンカリマンタン 低低 –– 中中 < 5100 < 5100 -- 61006100 25.375,6925.375,69 2.769,012.769,01

高高 –– 非常に高非常に高 6100 6100 -- 71007100 6.844,446.844,44 1.219,101.219,10

4.4. スラウェシスラウェシ 低低 –– 中中 < 5100 < 5100 -- 61006100 218,42218,42 0,060,06

高高 –– 非常に高非常に高 6100 6100 -- 71007100 14,6814,68 0,000,00

5.5. マルクマルク 低低 –– 中中 < 5100< 5100 2,132,13 0,000,00

6.6. パプアパプア 低低 –– 中中 < 5100 < 5100 -- 61006100 120,35120,35 0,000,00

高高 –– 非常に高非常に高 6100 6100 -- 71007100 30,9130,91 0,000,00

2006年総資源量 61.273,99 6.758,90

9

3.3. 石炭の埋蔵量と資源量、石炭の埋蔵量と資源量、 生産量、輸出量、および生産量、輸出量、および 国内販売量の現状国内販売量の現状

Clean Coal Day in Japan 2008

L-9-19

インドネシアの石炭産業プレーヤー/

グループ

石炭事業契約(CCOW 保有者)

**)

鉱業権(MA 保有者)

***)

国営会社(PTBA)*)

全国石炭生産量の 4.8% のシェア

全国石炭生産量の 83.9% のシェア

全国石炭生産量の 11.3% のシェア

*) 生産中 1 社**) 生産中 34 社

生産予定 40 社***) 生産中 169 社

石炭鉱業石炭鉱業プレーヤープレーヤー//グループグループ

((20062006年)年)

11

リアウ州資源量 = 2,057.22可採量 = 15.15

ナングル・アチェ・ダルサラム州資源量 = 450.15可採量 = n.a.

西カリマンタン州資源量 = 527.52可採量 = n.a

中央カリマンタン州資源量 = 1,399.21可採量 = 48.59

東カリマンタン州資源量 = 19,567.79可採量 = 2,410.33

パプア州資源量 = 138.30可採量 = n.a.

西スマトラ州資源量 = 719.09可採量 = 36.07

ブンクル州資源量 = 198.37可採量 = 21.12

南カリマンタン州資源量 = 8,674.56可採量 = 1,787.32

南スラウェシ州資源量 = 132.01可採量 = 0.06

南スマトラ州資源量 = 22,240.40可採量 = 2,653.98

州ごとの州ごとの石炭資源量・埋蔵量分布(百万トン)石炭資源量・埋蔵量分布(百万トン)

20062006年年

10

Clean Coal Day in Japan 2008

L-9-20

比エネルギー(KCAL/KG)によるインドネシアの炭質

62%

13%

24%

1%

中品質

低品質高品質 非常に高品質

(6100-7100 kcal/kg)(>7100 kcal/kg)

(< 5100 kcal/kg)

(5100-6100 kcal/kg)

13

62.5

45.541.3

37.135.7429.227.3

22.11915.413.210.98.9

158.6

148

110.79

93.7685.3

73.463.457.253.9

46.740.935.330.3

212193.5

153.2

132.4

114.3102.5

91.575.672.2

60.653.9

48.840.1

0

20

40

60

80

100

120

140

160

180

200

220

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

国内

輸出

生産量

生産成長率 1997 – 2007年144.4 M.tons/年 即ち 15.81 %

輸出成長率 1997 - 2007年11.3 M.tons/年 即ち 11.77 %

国内販売成長率 1997 - 2007年3.4 M.tons/年 即ち 4.93 %

出所: - Directorate of Mineral and Coal Enterprise – “Indonesia Mineral and Coal Statistic 2005”- APBI-ICMA

百万トン

インドネシアの石炭生産量、輸出量、国内販売量の伸びインドネシアの石炭生産量、輸出量、国内販売量の伸び((19951995年年 -- 20072007年)年)

12

Clean Coal Day in Japan 2008

L-9-21

110 206 338261383

744244

336

532

481

546

577

49348

1084

158

956

252

472

619

0

500

1000

1500

2000

2500

3000

3500

2006 2010 2015 2020 2025

石油

ガス

石炭

その他

百万

BO

E

年

(931,1) (1,098.8) (1,470.7) (2,190.4) (3,151.4)

出所: Data & Information Centre MEMR (2007)

エネルギーミックス計画現状と将来の見通し(2006 – 2025年)

石炭:目覚ましい増加Oil

Gas

Coal

Others

15

14

4.4. エネルギーミックス計画エネルギーミックス計画((2006 2006 –– 20252025年)年)

Clean Coal Day in Japan 2008

L-9-22

インドネシアの石炭生産量、輸出量、および国内消費量に関する長期予測(2007 - 2025年)

出所:APBI - ICMA

予測実績

年

生産量

輸出量

生産

量(百

万トン)

国内販売量(根拠:

17

16

5.5. 石炭の国内使用に関する長期予測石炭の国内使用に関する長期予測

Clean Coal Day in Japan 2008

L-9-23

改善を要する主要課題改善を要する主要課題

採炭活動と森林規制との間に横たわる溝採炭活動と森林規制との間に横たわる溝

中央政府と地方行政による規制の間に存在する重複と矛中央政府と地方行政による規制の間に存在する重複と矛盾盾

税制問題税制問題

新たな鉱業法を確定させる上での遅延新たな鉱業法を確定させる上での遅延

COWCOWシステム対鉱業ライセンス(システム対鉱業ライセンス(IUPIUP))不法採炭不法採炭

規制機関との協調規制機関との協調

19

18

6.6. 改善を要する主要課題改善を要する主要課題

Clean Coal Day in Japan 2008

L-9-24

石炭産業の上流における投資チャンス石炭産業の上流における投資チャンス

未開発地域未開発地域/ / 新規鉱山の開発新規鉱山の開発

合弁合弁/ / 合同操業合同操業/ / 買収買収

採炭契約業者採炭契約業者

輸送(河川、輸送(河川、 内陸、内陸、 海上輸送)海上輸送)

石炭ターミナル石炭ターミナル

選炭プラント選炭プラント/ / ブレンドプラントブレンドプラント

炭層メタンの開発炭層メタンの開発

採炭後処理契約業者採炭後処理契約業者

21

20

7.7. 石炭産業の上流と下流における投資チャンス石炭産業の上流と下流における投資チャンス

Clean Coal Day in Japan 2008

L-9-25

23

8.8. 結論結論

石炭産業の下流における投資チャンス石炭産業の下流における投資チャンス

石炭供給業者、輸出者石炭供給業者、輸出者/ / トレーダートレーダー

エネルギー変換プラントエネルギー変換プラント

褐炭の改質・高品質化褐炭の改質・高品質化

ガス化ガス化

ブリケット化ブリケット化

液化液化

22

Clean Coal Day in Japan 2008

L-9-26

結論

1. インドネシアの経済発展における石炭の役割は、エネルギーミックス計画で述べたように、向こう20年の間さらに増大するであろう。

2. 高い石炭価格が生産量と輸出量を推進し続ける。

3. 国内のエネルギー供給を確保するため、GOIは石炭生産者に対して市場価格でDMOを課すであろう。

4. 石炭産業の上流と下流には多くの商機がある。

5. 新たな投資家を引きつけるためにはまだ改善の余地がある。

24

Clean Coal Day in Japan 2008

L-9-27

氏名: Supriatna Suhala Education: First Degree: Mining Engineering Bandung Institute of Technology, Indonesia (1975) Second Degree: School of Mining Engineering The University of New South Wales, Sydney, Australia (1986) Professional Career: 1975 – 1995 Researcher in the Mineral Technology Development Centre (MTDC) in Bandung 1995 – 1997 Director of MTDC 1997 – 1998 Director of Mining Engineering (Chief Mining Inspector) Directorate General of Mines, DEMR 1999 – 2001 Head of International Cooperation Bureau – DEMR 2002 – 2004 Inspector to the Inspectorate Generale of DEMR 2004 – 2006 Director of Energy & Electricity Research Center, DEMR 2006 – 2007 Head of General Affairs Bureau - DEMR 1998 – 2008 Member of ANTAM Tbk.’s Board of Commissioners (State Owned Mining Company) 2008 – Present Executive Director to the APBI – ICMA Supriatna Suhala 学歴: 第一学位:鉱山工学 バンドン工科大学(インドネシア)1975 年 第二学位:鉱山工学部 ニューサウスウェールズ大学(豪州シドニー)1986 年 職歴: 1975 – 1995 鉱物技術開発センター(MTDC)(バンドン)研究員 1995 – 1997 MTDC 所長 1997 – 1998 エネルギー・鉱物資源省(DEMR)鉱山総局 鉱山技術局長(主席鉱山

保安監督官) 1999 – 2001 DEMR 国際協力局長 2002 – 2004 DEMR 総合検査団検査官 2004 – 2006 DEMR エネルギー・電力研究センター長 2006 – 2007 DEMR 総務局長 1998 – 2008 アンタム社(ANTAM Tbk:インドネシア国営鉱山会社) 理事会メンバー

Clean Coal Day in Japan 2008

L-9-28

2008 – 現在 APBI/ICMA(インドネシア石炭鉱山協会)事務局長