cut income tax rates or cut national territory and bureaucracies

TRANSCRIPT

Cut income tax rates or cut national territory and bureaucracies

TAX Exchange: Tax Reform in the Philippines Organized by Ateneo IGNITE Movement,

Ateneo Econ. Association, UPSE Student Council, Center for Strategic Reform of the Philippines,

Tax Reform Philippines Escaler Hall, AdeMU, QC, 29 March 2016

Bienvenido Oplas, Jr. Pres., Minimal Government Thinkers

Fellow, SEANET and ADRi

Outline

I. Comparative taxation data in Asia

II. Proposal 1: Cut income tax rate

III. Proposal 2: Disintegrate the country, tax competition among new island-countries

IV. Proposal 3: National income tax is zero, allow provinces to impose income tax, have provincial tax competition

V. Concluding notes

Source: WB-PWC, Paying Taxes 2016, Figure A2.4

Philippines 42.9

I. Comparative taxation data in Asia Total tax rate, % of commercial profit

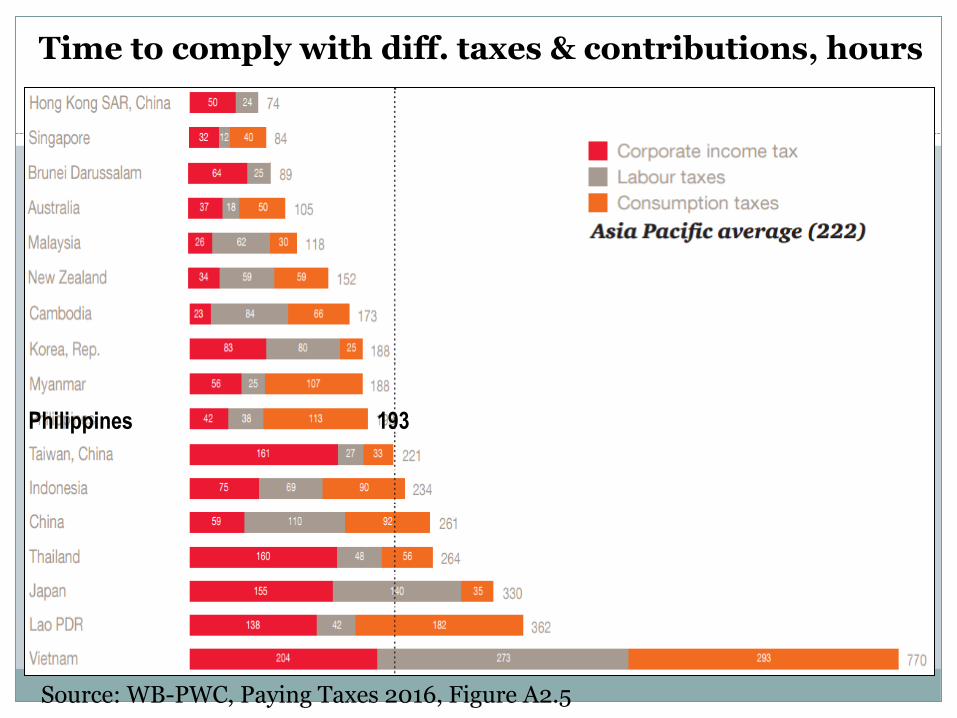

Source: WB-PWC, Paying Taxes 2016, Figure A2.5

Time to comply with diff. taxes & contributions, hours

Philippines 193

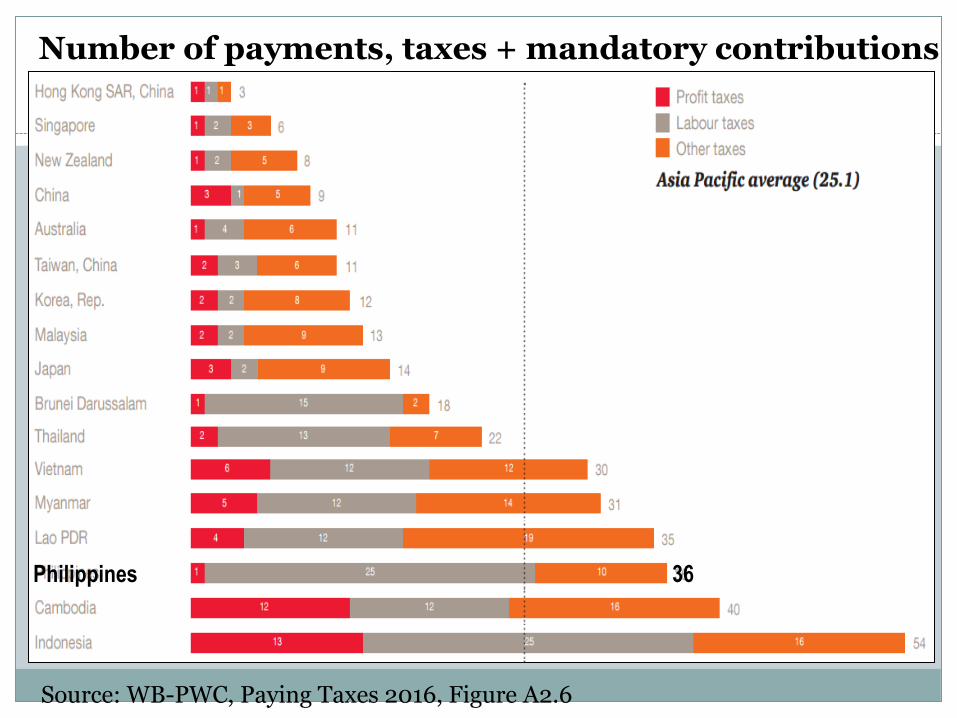

Source: WB-PWC, Paying Taxes 2016, Figure A2.6

Number of payments, taxes + mandatory contributions

Philippines 36

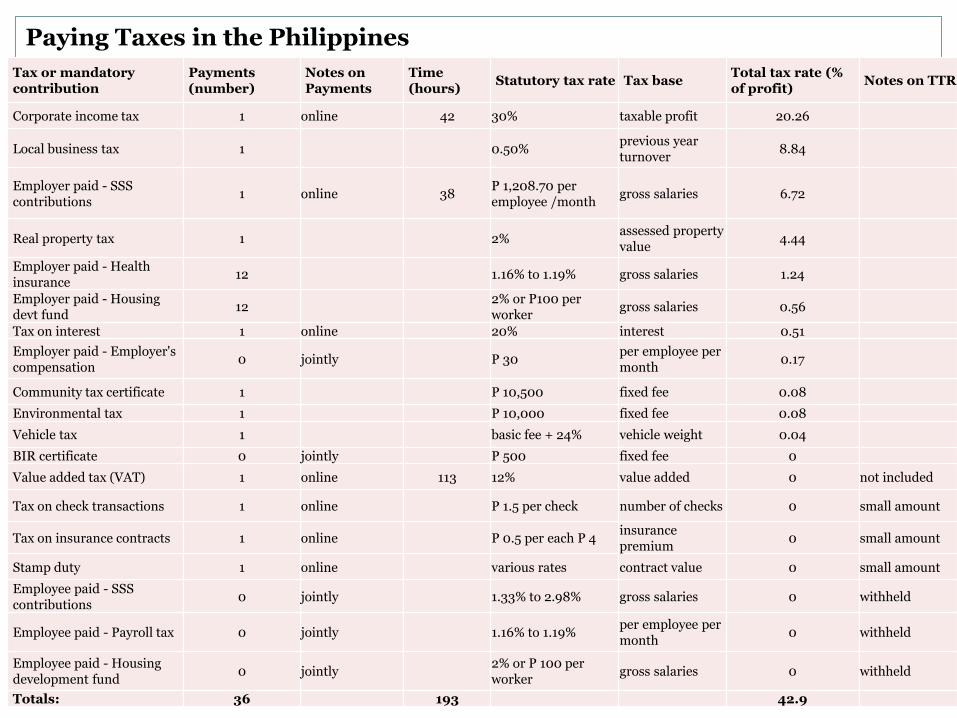

Tax or mandatory contribution

Payments (number)

Notes on Payments

Time (hours)

Statutory tax rate Tax base Total tax rate (% of profit)

Notes on TTR

Corporate income tax 1 online 42 30% taxable profit 20.26

Local business tax 1 0.50% previous year turnover

8.84

Employer paid - SSS contributions

1 online 38 P 1,208.70 per employee /month

gross salaries 6.72

Real property tax 1 2% assessed property value

4.44

Employer paid - Health insurance

12 1.16% to 1.19% gross salaries 1.24

Employer paid - Housing devt fund

12 2% or P100 per worker

gross salaries 0.56

Tax on interest 1 online 20% interest 0.51

Employer paid - Employer's compensation

0 jointly P 30 per employee per month

0.17

Community tax certificate 1 P 10,500 fixed fee 0.08

Environmental tax 1 P 10,000 fixed fee 0.08

Vehicle tax 1 basic fee + 24% vehicle weight 0.04

BIR certificate 0 jointly P 500 fixed fee 0

Value added tax (VAT) 1 online 113 12% value added 0 not included

Tax on check transactions 1 online P 1.5 per check number of checks 0 small amount

Tax on insurance contracts 1 online P 0.5 per each P 4 insurance premium

0 small amount

Stamp duty 1 online various rates contract value 0 small amount

Employee paid - SSS contributions

0 jointly 1.33% to 2.98% gross salaries 0 withheld

Employee paid - Payroll tax 0 jointly 1.16% to 1.19% per employee per month

0 withheld

Employee paid - Housing development fund

0 jointly 2% or P 100 per worker

gross salaries 0 withheld

Totals: 36 193 42.9

Paying Taxes in the Philippines

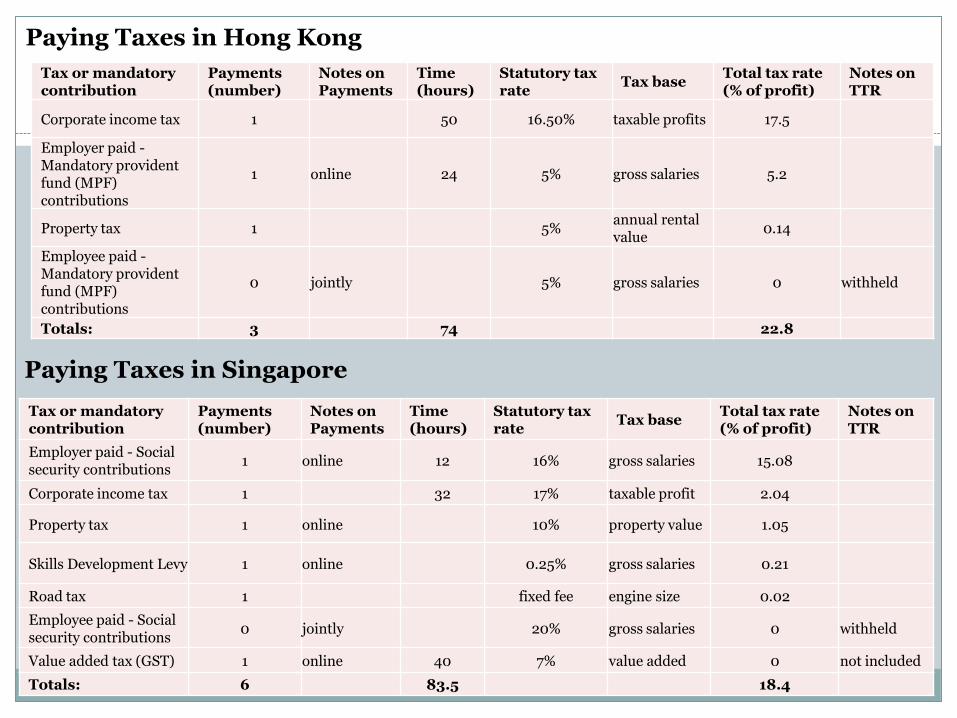

Paying Taxes in Hong Kong

Tax or mandatory contribution

Payments (number)

Notes on Payments

Time (hours)

Statutory tax rate

Tax base Total tax rate (% of profit)

Notes on TTR

Corporate income tax 1 50 16.50% taxable profits 17.5

Employer paid - Mandatory provident fund (MPF) contributions

1 online 24 5% gross salaries 5.2

Property tax 1 5% annual rental value

0.14

Employee paid - Mandatory provident fund (MPF) contributions

0 jointly 5% gross salaries 0 withheld

Totals: 3 74 22.8

Paying Taxes in Singapore

Tax or mandatory contribution

Payments (number)

Notes on Payments

Time (hours)

Statutory tax rate

Tax base Total tax rate (% of profit)

Notes on TTR

Employer paid - Social security contributions

1 online 12 16% gross salaries 15.08

Corporate income tax 1 32 17% taxable profit 2.04

Property tax 1 online 10% property value 1.05

Skills Development Levy 1 online 0.25% gross salaries 0.21

Road tax 1 fixed fee engine size 0.02

Employee paid - Social security contributions

0 jointly 20% gross salaries 0 withheld

Value added tax (GST) 1 online 40 7% value added 0 not included

Totals: 6 83.5 18.4

A gas station in QC. Permits & more permits before one can start or continue a business

Source: PWC, Paying Taxes (annual reports) • http://www.pwc.com/gx/en/paying-taxes/assets/paying-taxes-2009.pdf • http://www.pwc.com/gx/en/paying-taxes/assets/paying-taxes-2012.pdf • http://www.pwc.com/gx/en/paying-taxes/pdf/pwc-paying-taxes-2015-low-resolution.pdf

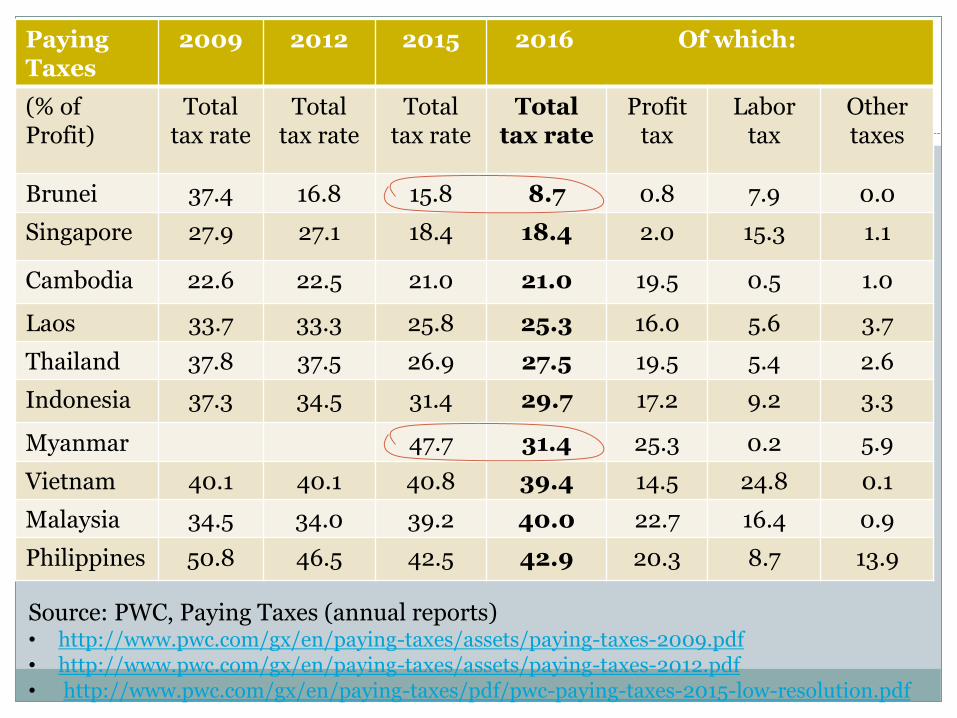

Paying Taxes

2009 2012 2015 2016 Of which:

(% of Profit)

Total tax rate

Total tax rate

Total tax rate

Total tax rate

Profit tax

Labor tax

Other taxes

Brunei 37.4 16.8 15.8 8.7 0.8 7.9 0.0

Singapore 27.9 27.1 18.4 18.4 2.0 15.3 1.1

Cambodia 22.6 22.5 21.0 21.0 19.5 0.5 1.0

Laos 33.7 33.3 25.8 25.3 16.0 5.6 3.7

Thailand 37.8 37.5 26.9 27.5 19.5 5.4 2.6

Indonesia 37.3 34.5 31.4 29.7 17.2 9.2 3.3

Myanmar 47.7 31.4 25.3 0.2 5.9

Vietnam 40.1 40.1 40.8 39.4 14.5 24.8 0.1

Malaysia 34.5 34.0 39.2 40.0 22.7 16.4 0.9

Philippines 50.8 46.5 42.5 42.9 20.3 8.7 13.9

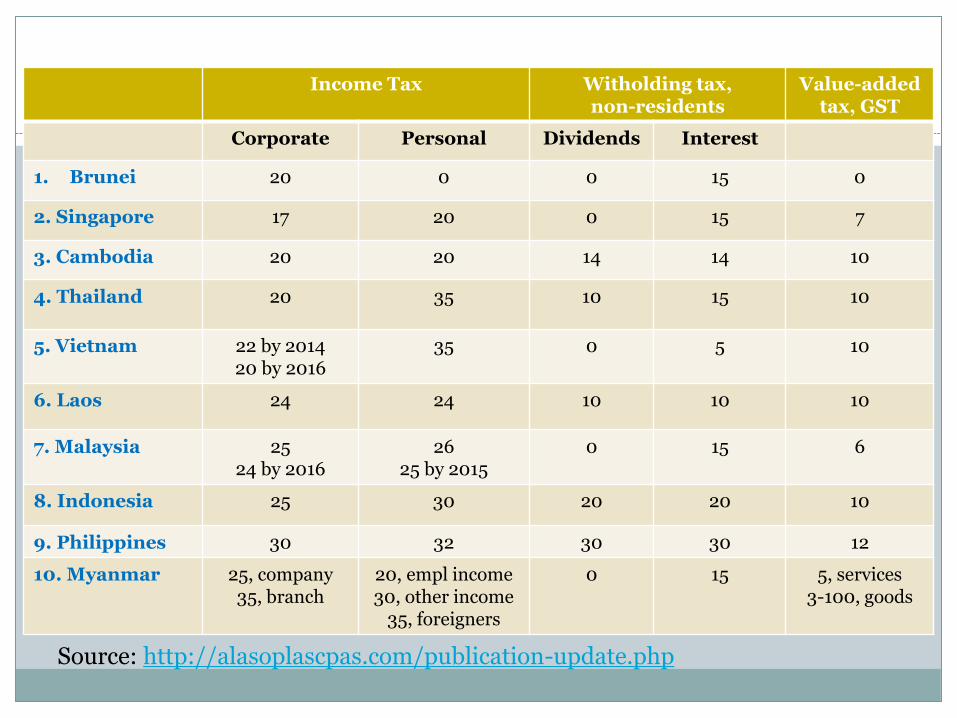

Source: http://alasoplascpas.com/publication-update.php

Income Tax Witholding tax, non-residents

Value-added tax, GST

Corporate Personal Dividends Interest

1. Brunei 20 0 0 15 0

2. Singapore 17 20 0 15 7

3. Cambodia 20 20 14 14 10

4. Thailand 20 35 10 15 10

5. Vietnam 22 by 2014 20 by 2016

35 0 5 10

6. Laos 24 24 10 10 10

7. Malaysia 25 24 by 2016

26 25 by 2015

0 15 6

8. Indonesia 25 30 20 20 10

9. Philippines 30 32 30 30 12

10. Myanmar 25, company 35, branch

20, empl income 30, other income

35, foreigners

0 15 5, services 3-100, goods

the above tables mean…

• Tax wise, PH is NOT an attractive place to do business in the ASEAN. Highest total tax rate (TTR) in the region plus complicated and bureaucratic procedures. Only developed welfare countries Australia and Japan, and socialist China have higher TTR than PH.

• Although in number of hours, VN proves it is indeed a socialist and bureaucratic state; in number of payments, ID’s bureaucracies are most notable.

• Tax competition among ASEAN countries is happening. BR, SG and CM keeping their low TTR, MM significantly cut its TTR last year. Only MY is dueling with PH in high TTR.

• The time to cut the PH’s (a) number of taxes and forced contributions,

and (b) income tax rates, was yesterday. So we need to move fast today and tomorrow.

II. Proposal 1: Cut income tax rates

Both personal and corporate income taxes, to be compensated by (a) expanded tax base and (b) higher revenues from consumption-based taxes.

(1) TR = t x Q. Tax revenues (TR) is a product of tax rate (t) multiplied by the quantity (Q) or number of taxpayers, individuals and corporate. If there is only one form of tax, the income tax, then 2 ways to raise TR: (i) raise t or keep it at a high rate and wait for Q to expand due to

increases in population and number of private enterprises; or

(ii) reduce t and watch Q to expand faster than the decline in t.

But there are many types of taxes other than income tax: (a) consumption-based taxes (VAT, excise tax, travel tax, amusement tax, …) (b) property-based taxes (real property tax or RPT by LGUs, vehicle registration tax, franchise tax, …) (c) indirect income taxes (bank interests withholding tax, capital gains tax, estate tax, documentary stamp tax, …) (d) product-based taxes (royalties and excise tax for extractive industries – mining, natural gas, geothermal, coal, petroleum, etc., …) (e) LGU taxes (barangays, business permit taxes, community tax, …) (f) others And there are many types of mandatory fees and permits: (a) National: drivers license fee (LTO-DOTC), passport fee (DFA), terminal fee (airports-DOTC), NBI clearance (NBI-DOJ), police clearance (PNP-DILG), professional clearance (PRC-OP),… (b) LGUs: residence tax/cedula, barangays, city/municipality/provincial permits and fees. Even if income tax is zero, nada, government can remain BIG and bloated.

Various types of tax rates to be noted as: t1 – direct income taxes t2 – consumption based taxes t3 – property based taxes t4 – indirect income taxes t5 – product-based taxes, and so on. Q1, Q2, Q3,… are the respective tax base for each type of taxes. So government’s TR goal can be summarized as: (2) TR = ∑ [(t1 x Q1) + (t2 x Q2) + t3 x Q3) + …] For the income tax cut campaign, it can be shown that reducing t1 from 32% (individual) and 30% (corporate) to only 20% or 10%, will result in: Q1 can increase by ___% Q2 can increase by ___% even if t2 will remain the same, or raise the VAT from 12% to 14% Q3 can increase by ___%, and so on.

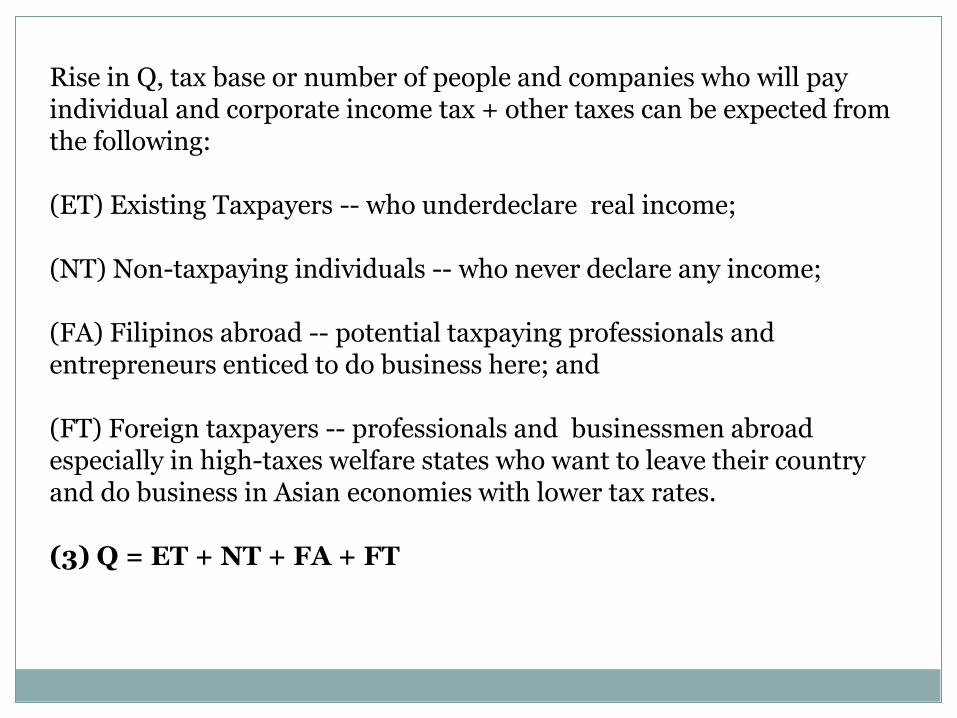

Rise in Q, tax base or number of people and companies who will pay individual and corporate income tax + other taxes can be expected from the following: (ET) Existing Taxpayers -- who underdeclare real income; (NT) Non-taxpaying individuals -- who never declare any income; (FA) Filipinos abroad -- potential taxpaying professionals and entrepreneurs enticed to do business here; and (FT) Foreign taxpayers -- professionals and businessmen abroad especially in high-taxes welfare states who want to leave their country and do business in Asian economies with lower tax rates. (3) Q = ET + NT + FA + FT

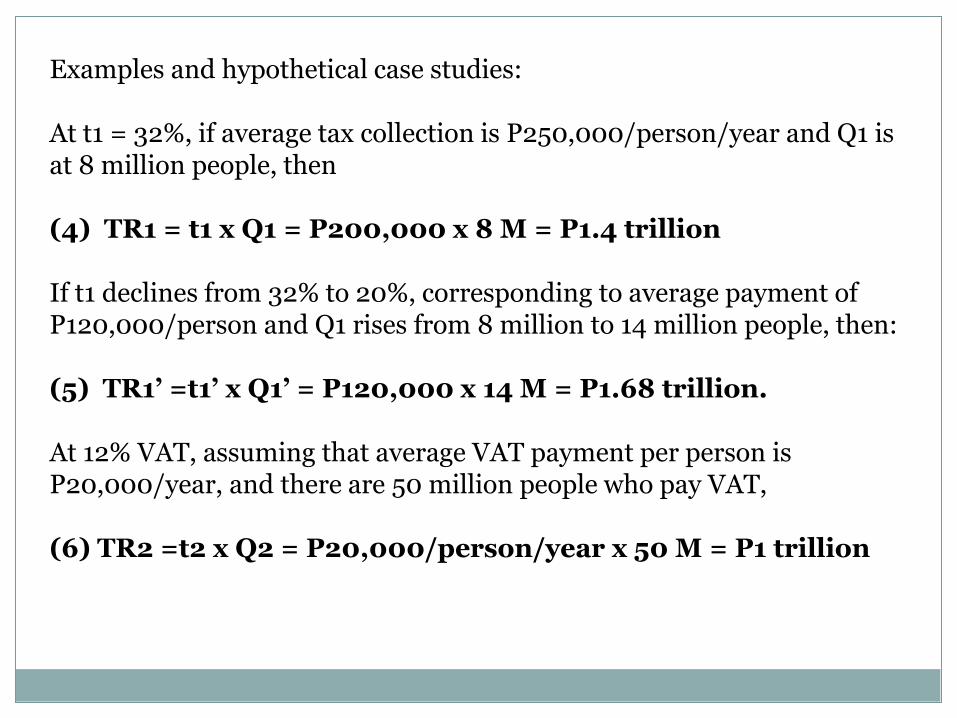

Examples and hypothetical case studies: At t1 = 32%, if average tax collection is P250,000/person/year and Q1 is at 8 million people, then (4) TR1 = t1 x Q1 = P200,000 x 8 M = P1.4 trillion If t1 declines from 32% to 20%, corresponding to average payment of P120,000/person and Q1 rises from 8 million to 14 million people, then: (5) TR1’ =t1’ x Q1’ = P120,000 x 14 M = P1.68 trillion. At 12% VAT, assuming that average VAT payment per person is P20,000/year, and there are 50 million people who pay VAT, (6) TR2 =t2 x Q2 = P20,000/person/year x 50 M = P1 trillion

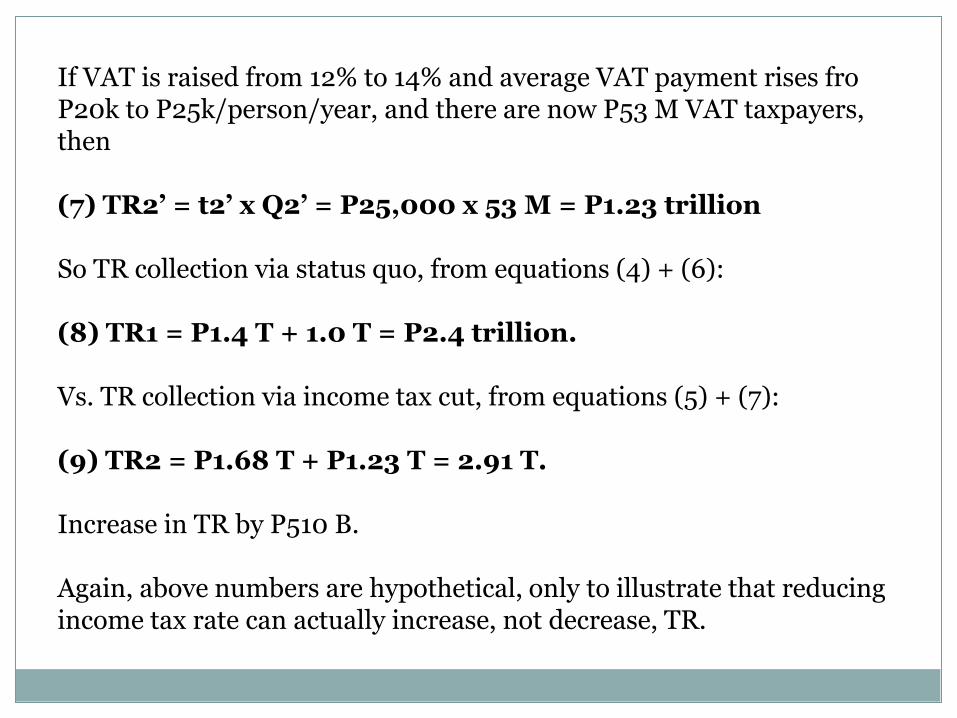

If VAT is raised from 12% to 14% and average VAT payment rises fro P20k to P25k/person/year, and there are now P53 M VAT taxpayers, then (7) TR2’ = t2’ x Q2’ = P25,000 x 53 M = P1.23 trillion So TR collection via status quo, from equations (4) + (6): (8) TR1 = P1.4 T + 1.0 T = P2.4 trillion. Vs. TR collection via income tax cut, from equations (5) + (7): (9) TR2 = P1.68 T + P1.23 T = 2.91 T. Increase in TR by P510 B. Again, above numbers are hypothetical, only to illustrate that reducing income tax rate can actually increase, not decrease, TR.

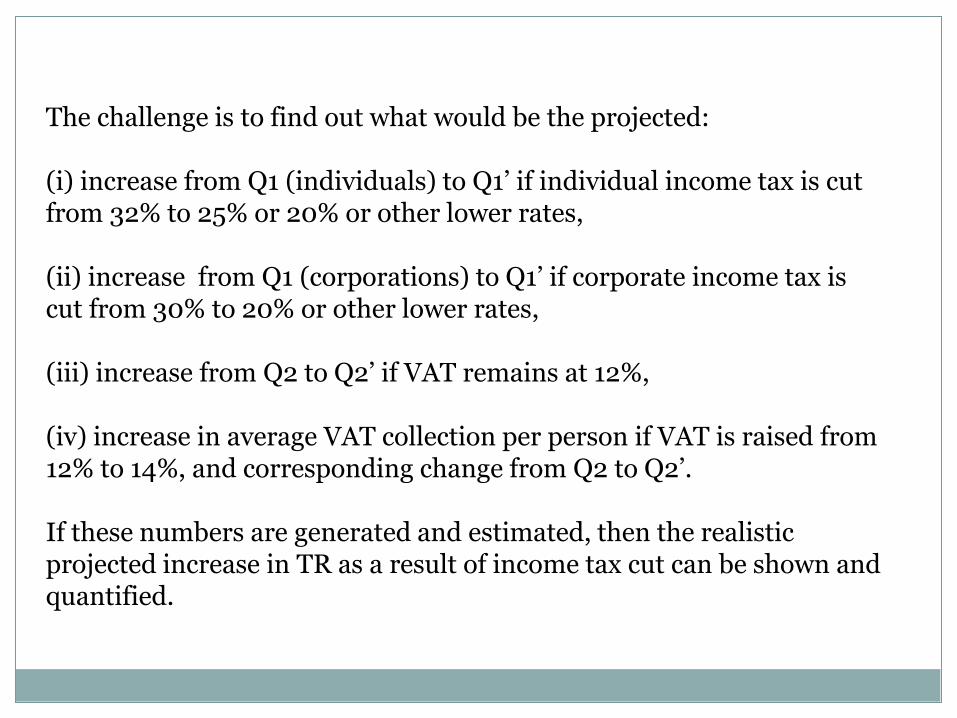

The challenge is to find out what would be the projected: (i) increase from Q1 (individuals) to Q1’ if individual income tax is cut from 32% to 25% or 20% or other lower rates,

(ii) increase from Q1 (corporations) to Q1’ if corporate income tax is cut from 30% to 20% or other lower rates, (iii) increase from Q2 to Q2’ if VAT remains at 12%, (iv) increase in average VAT collection per person if VAT is raised from 12% to 14%, and corresponding change from Q2 to Q2’. If these numbers are generated and estimated, then the realistic projected increase in TR as a result of income tax cut can be shown and quantified.

Do not force t at 32% (indiv.) and 30% (corp.)

Move at lower t, higher TR

As t goes up, many people will leave/migrate, or stop working and wait for state welfare, or keep working but understate output and income. And TR declines.

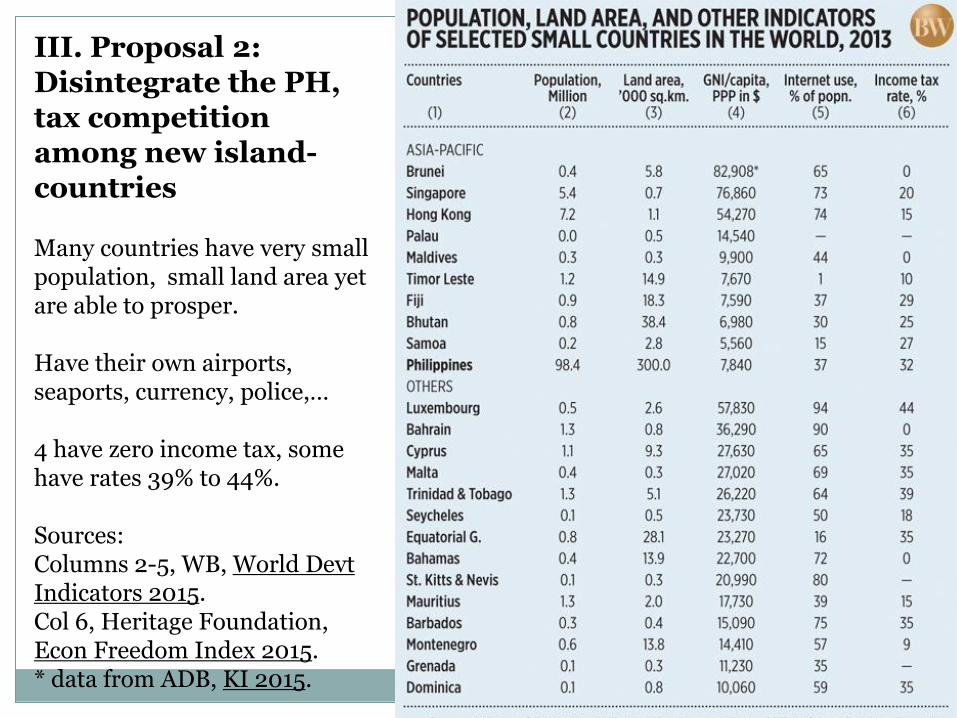

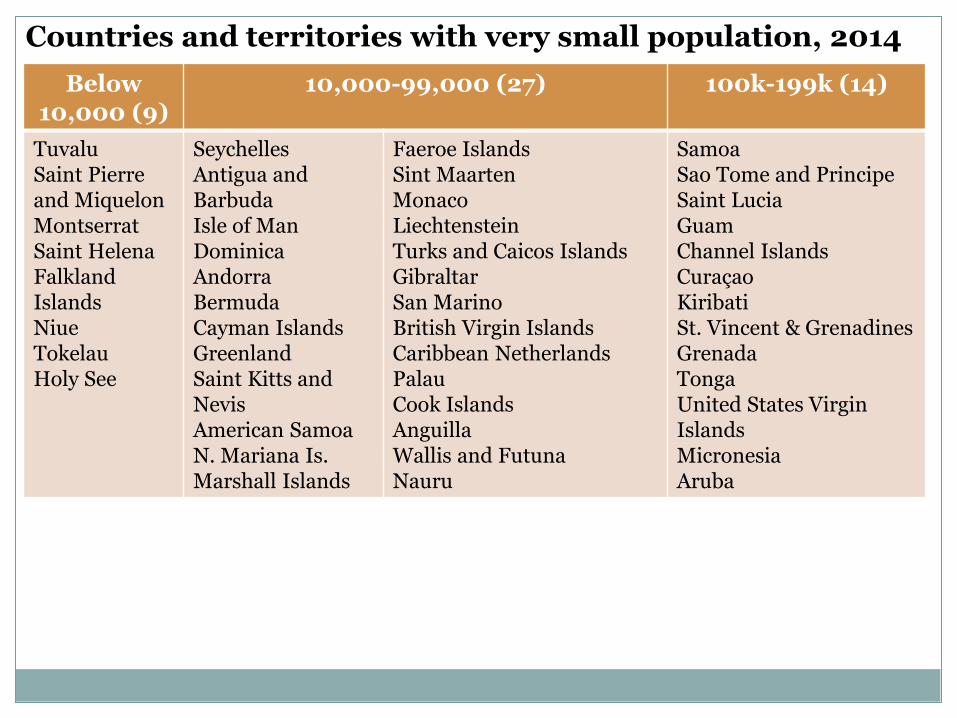

III. Proposal 2: Disintegrate the PH, tax competition among new island-countries Many countries have very small population, small land area yet are able to prosper. Have their own airports, seaports, currency, police,… 4 have zero income tax, some have rates 39% to 44%. Sources: Columns 2-5, WB, World Devt Indicators 2015. Col 6, Heritage Foundation, Econ Freedom Index 2015. * data from ADB, KI 2015.

Below 10,000 (9)

10,000-99,000 (27) 100k-199k (14)

Tuvalu Saint Pierre and Miquelon Montserrat Saint Helena Falkland Islands Niue Tokelau Holy See

Seychelles Antigua and Barbuda Isle of Man Dominica Andorra Bermuda Cayman Islands Greenland Saint Kitts and Nevis American Samoa N. Mariana Is. Marshall Islands

Faeroe Islands Sint Maarten Monaco Liechtenstein Turks and Caicos Islands Gibraltar San Marino British Virgin Islands Caribbean Netherlands Palau Cook Islands Anguilla Wallis and Futuna Nauru

Samoa Sao Tome and Principe Saint Lucia Guam Channel Islands Curaçao Kiribati St. Vincent & Grenadines Grenada Tonga United States Virgin Islands Micronesia Aruba

Countries and territories with very small population, 2014

IV. Proposal 3: National income tax is zero, allow provinces to impose income tax.

• “No tax on work.” Survival and prosperity of societies are based on work of people. Work should not be penalized and discouraged with taxes, the way governments discourage smoking and drinking with more taxes.

• National income tax is zero, or 5% max. National government to keep collecting consumption-based taxes (VAT, excise, franchise, vehicle registration, other taxes) and regulatory fees, while devolving more functions to provincial governments.

• Provinces can impose income tax. Let there be tax competition, governance competition among them.

• Professionals and entrepreneurs, local and foreign, will be voting with their feet. Provinces that offer the lowest income and other taxes and/or have good peace and order will attract the bulk of those entrepreneurs.

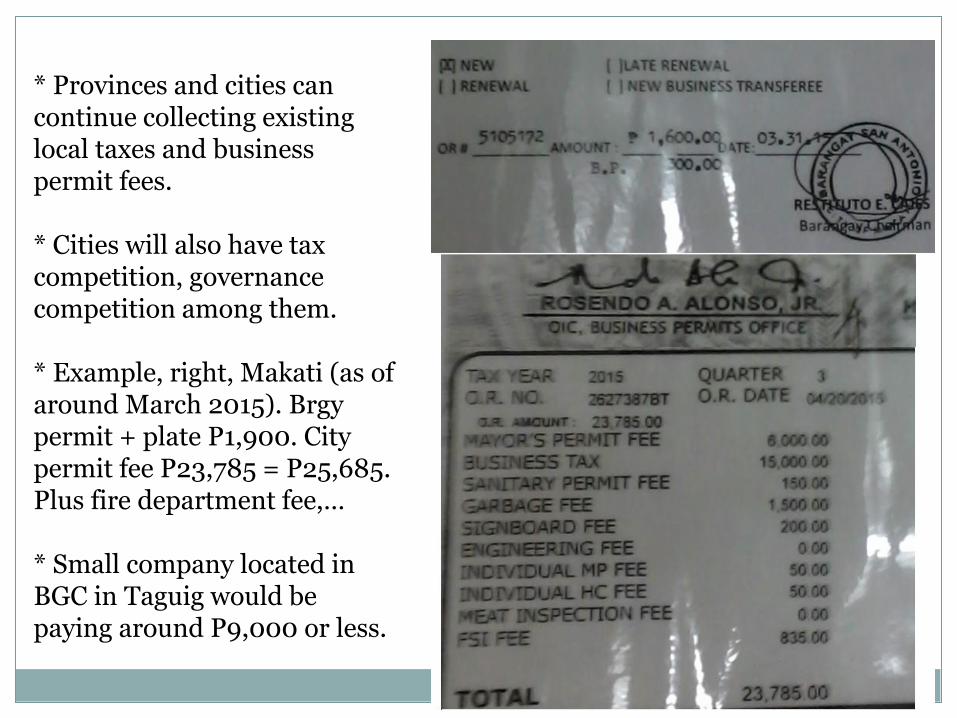

* Provinces and cities can continue collecting existing local taxes and business permit fees.

* Cities will also have tax competition, governance competition among them. * Example, right, Makati (as of around March 2015). Brgy permit + plate P1,900. City permit fee P23,785 = P25,685. Plus fire department fee,… * Small company located in BGC in Taguig would be paying around P9,000 or less.

V. Concluding Notes • Tax and governance competition, infrastructure and security

competition among provinces will empower the people and companies to vote with their feet.

• Of 3 proposals, most feasible is #1, cut income tax rates to 20% or lower. Higher Q, wider tax base, will compensate for the reduction and propel higher TR.

• Proposal #3 will attract the advocates of federalism and more decentralization and denationalization.

• Proposal #2 will attract the more daring politicians, business and civil society leaders. Long-term view.

• All 3 proposals can lead to more individual freedom, freer markets and limited government.