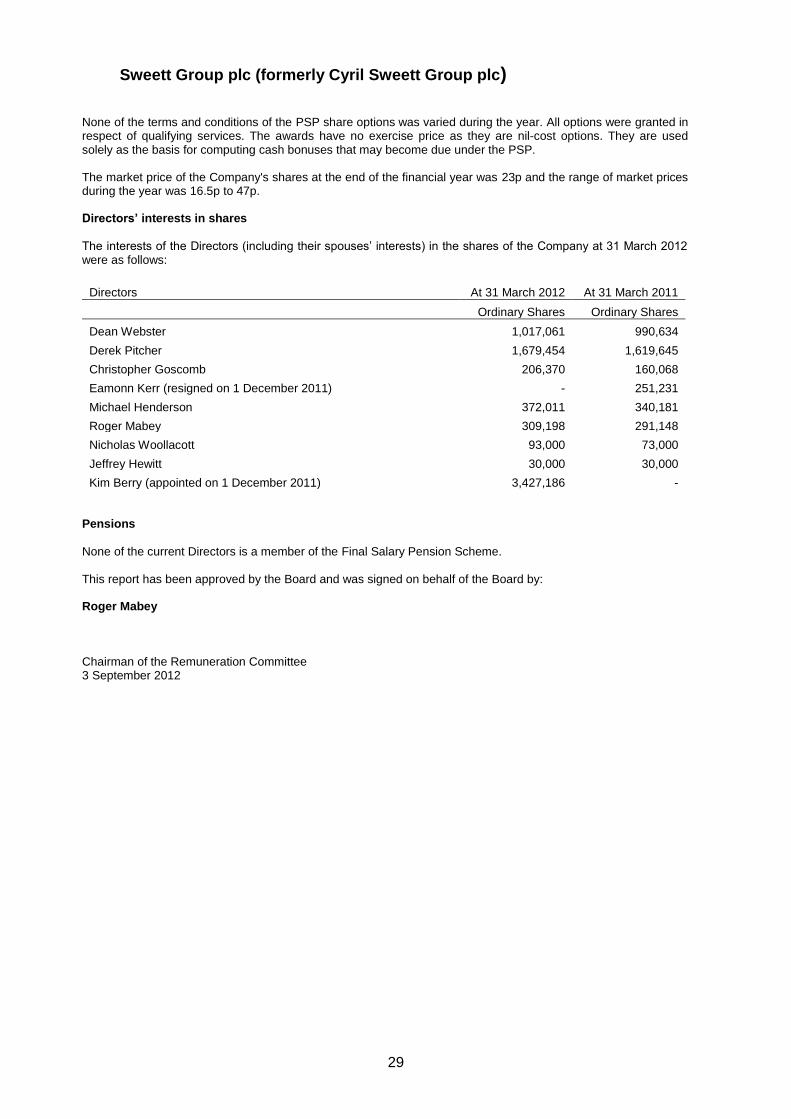

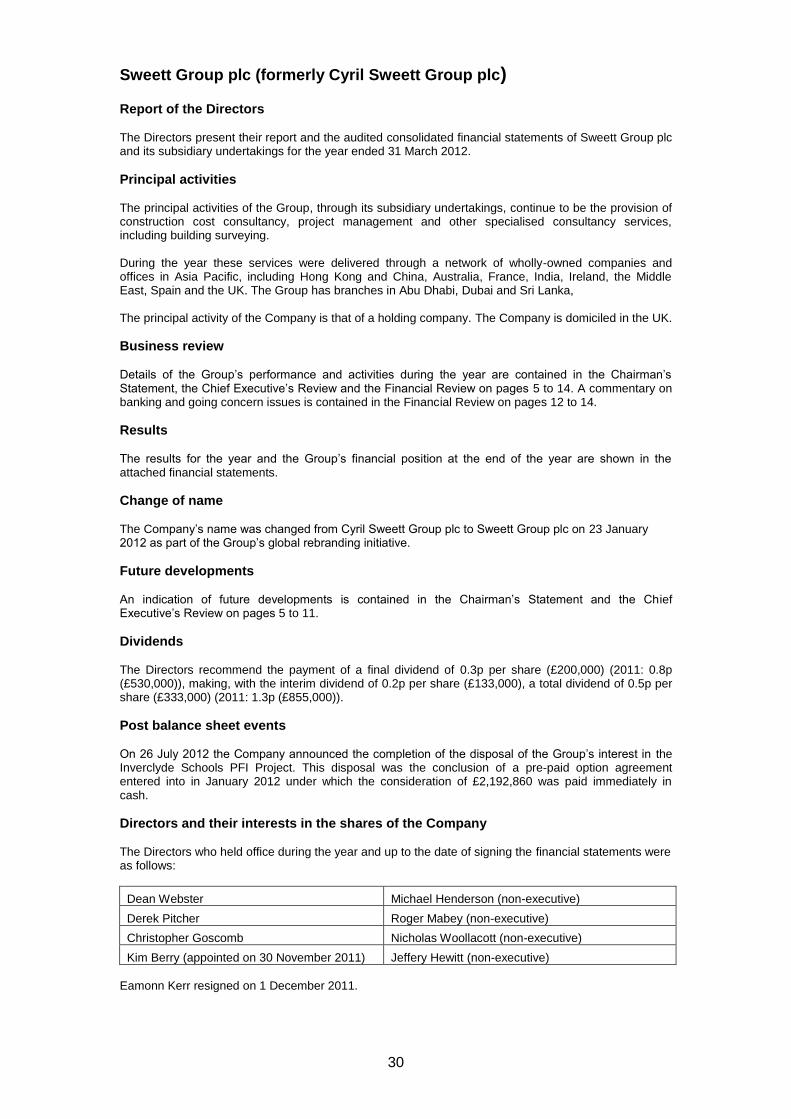

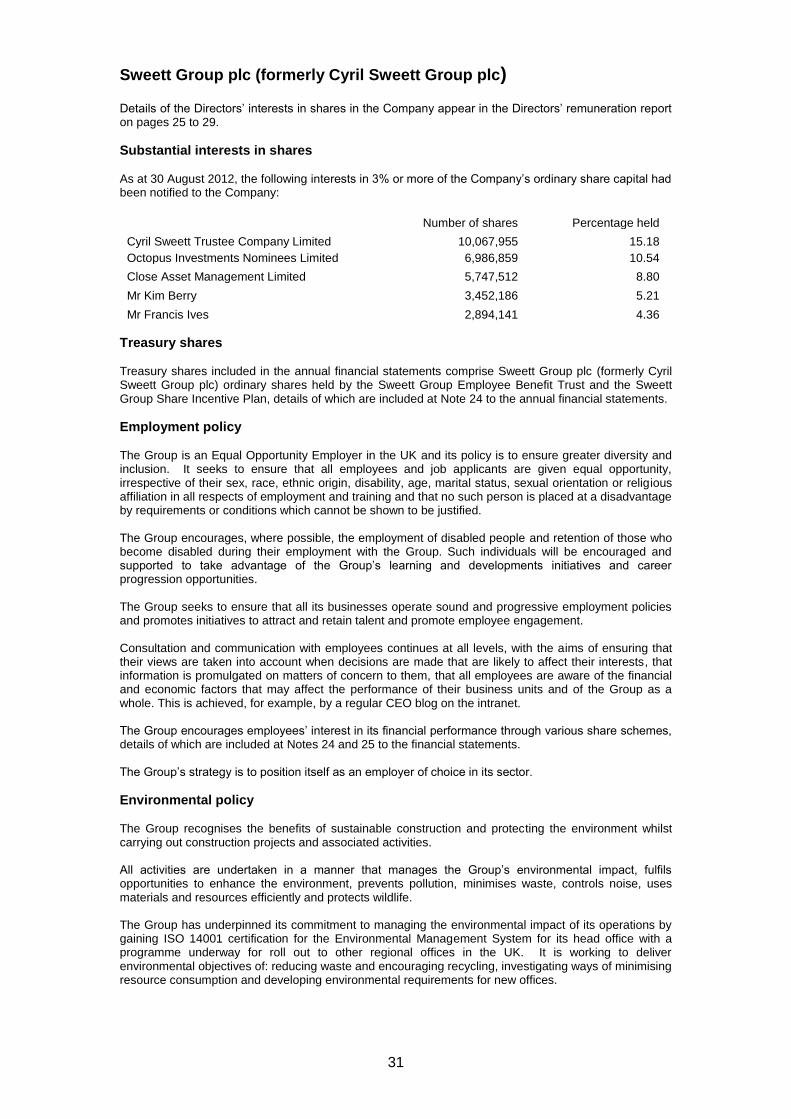

cyril sweett group plc - morningstar, inc

TRANSCRIPT

Sweett Group plc (formerly Cyril Sweett Group plc)

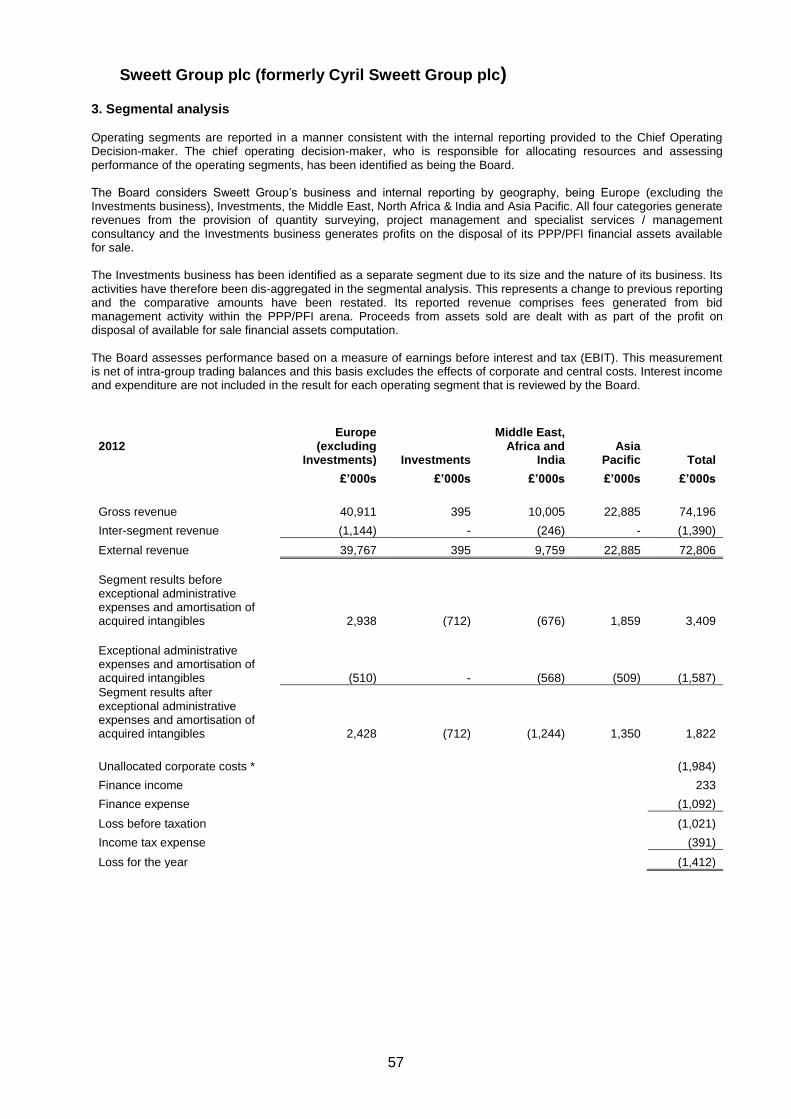

Annual report and financial statements 2012 International construction and property consultancy

Sweett Group plc (formerly Cyril Sweett Group plc)

Who we are Sweett Group is a global business with expertise in property and infrastructure professional services. Our services include cost management, programme and project management, strategic advisory and PPP/PFI investment and consultancy services. Clients tell us that we are experienced, professional and collaborative in our approach. We aim to forge long term, successful relationships with all stakeholders in the property and infrastructure industry. ―Global knowhow, local delivery‖ is the essence of our business and our reach enables us to put global best practice to use in the local markets we serve. For more information about our projects and services: www.sweettgroup.com Connect with us on [Twitter logo] [Facebook logo] [LinkedIn logo]

Sweett Group plc (formerly Cyril Sweett Group plc)

1

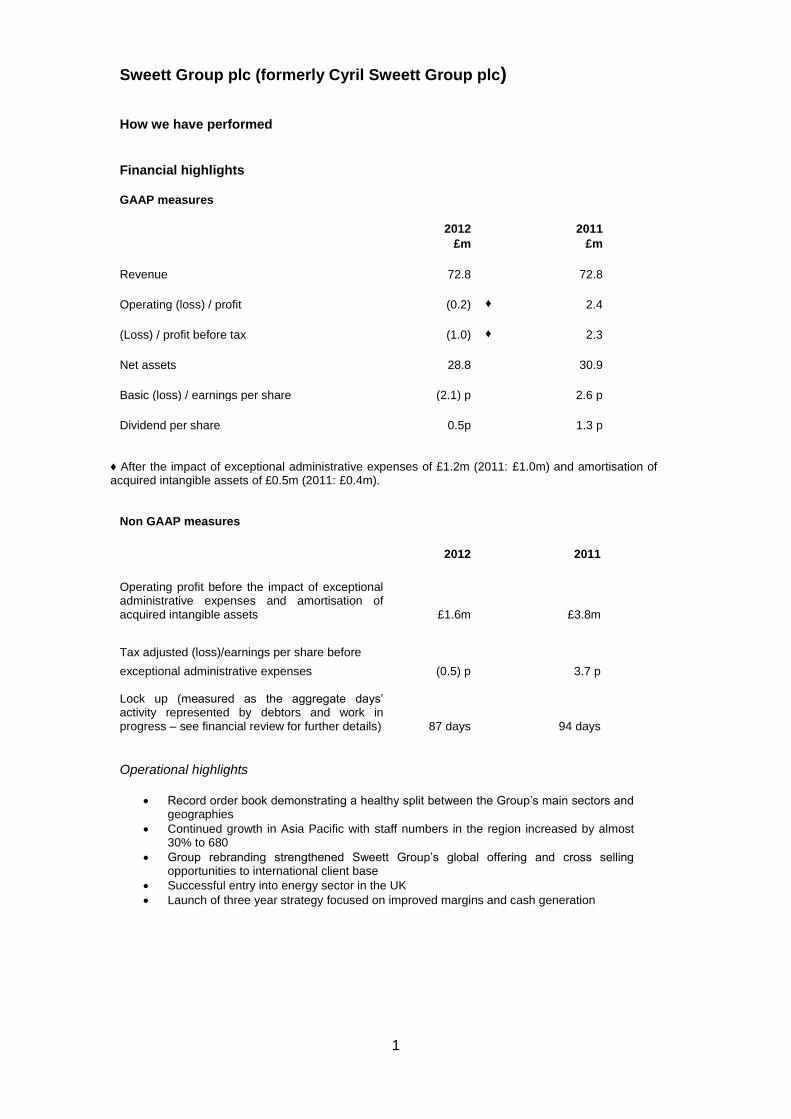

How we have performed Financial highlights GAAP measures

2012 2011

£m £m

Revenue 72.8 72.8

Operating (loss) / profit (0.2) ♦ 2.4

(Loss) / profit before tax (1.0) ♦ 2.3

Net assets 28.8 30.9

Basic (loss) / earnings per share (2.1) p 2.6 p

Dividend per share 0.5p 1.3 p

♦ After the impact of exceptional administrative expenses of £1.2m (2011: £1.0m) and amortisation of acquired intangible assets of £0.5m (2011: £0.4m).

Non GAAP measures

2012 2011

Operating profit before the impact of exceptional administrative expenses and amortisation of acquired intangible assets £1.6m

£3.8m

Tax adjusted (loss)/earnings per share before

exceptional administrative expenses (0.5) p 3.7 p

Lock up (measured as the aggregate days‘ activity represented by debtors and work in progress – see financial review for further details) 87 days

94 days

Operational highlights

Record order book demonstrating a healthy split between the Group‘s main sectors and geographies

Continued growth in Asia Pacific with staff numbers in the region increased by almost 30% to 680

Group rebranding strengthened Sweett Group‘s global offering and cross selling opportunities to international client base

Successful entry into energy sector in the UK

Launch of three year strategy focused on improved margins and cash generation

Sweett Group plc (formerly Cyril Sweett Group plc)

2

What we do Why us?

Sweett Group understands that clients select a company with a reputation for delivering quality advice, open communication, sector knowledge and value for money. When you work with Sweett Group you can expect: Credibility

We have a history and reputation for service delivery. Expertise We have people experienced in applying expert knowledge. We use our 'global knowhow' to deliver local, sustainable solutions. Assurance We deliver every time, accurately and in a professional, independent way.

Value We optimise our clients' ideas, budget and time. Our values

Our values define everything we do. From the manner in which we engage with clients and stakeholders, through to the methodologies we employ and the way we deliver success. The values that form the foundation of our business are: Client success We optimise our clients' investment by understanding their business. We want our clients to succeed.

Collaboration We collaborate across disciplines, across territories, with our clients, with our partners and within our territories.

Professionalism We undertake our work with professionalism. We approach each other with integrity and trust. Our professionalism, knowledge and creativity are critical to success. Our people

Sweett Group employs the best talent the industry has to offer. In addition we employ individuals who are aligned with our organisational values and demonstrate a professionalism that our clients expect from us. We take a strategic approach to selecting and developing our team. We first seek to identify the skills, experience, capability and passion of each individual. We then harness and develop these attributes to strengthen the skills of the group as a whole and provide further value to clients through a broader service offering.

Sweett Group plc (formerly Cyril Sweett Group plc)

3

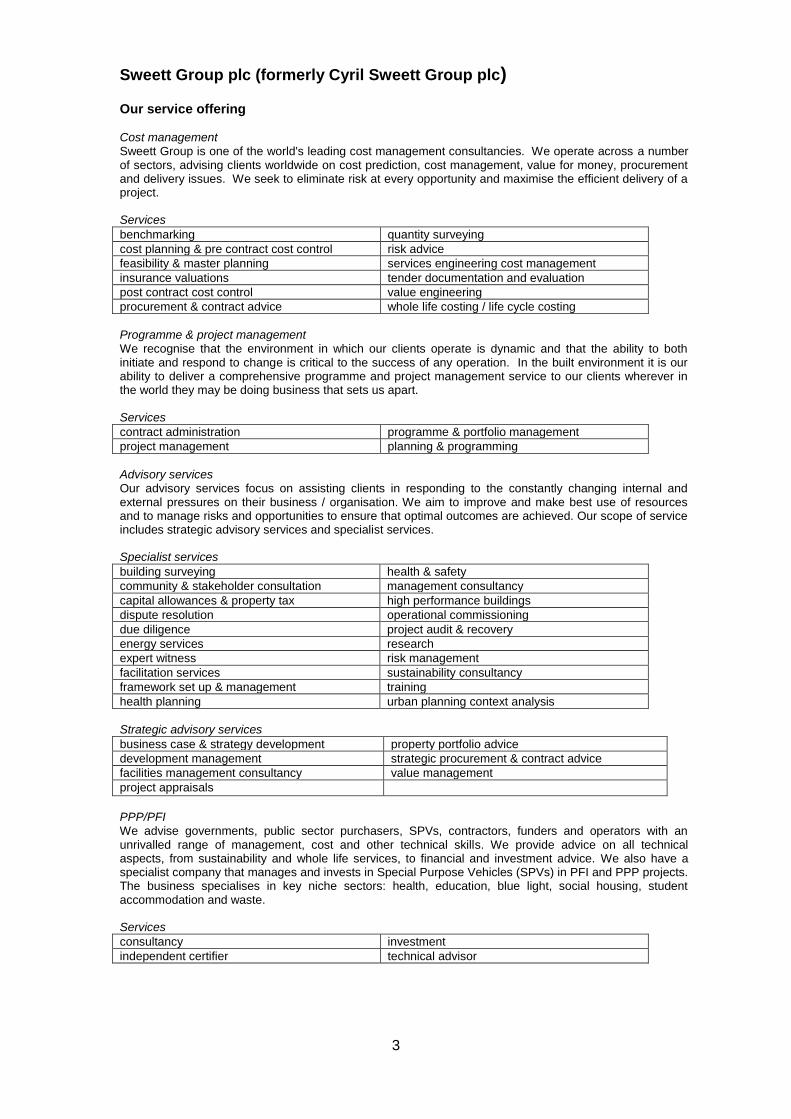

Our service offering Cost management Sweett Group is one of the world's leading cost management consultancies. We operate across a number of sectors, advising clients worldwide on cost prediction, cost management, value for money, procurement and delivery issues. We seek to eliminate risk at every opportunity and maximise the efficient delivery of a project. Services

Programme & project management We recognise that the environment in which our clients operate is dynamic and that the ability to both initiate and respond to change is critical to the success of any operation. In the built environment it is our ability to deliver a comprehensive programme and project management service to our clients wherever in the world they may be doing business that sets us apart. Services

contract administration programme & portfolio management

project management planning & programming

Advisory services Our advisory services focus on assisting clients in responding to the constantly changing internal and external pressures on their business / organisation. We aim to improve and make best use of resources and to manage risks and opportunities to ensure that optimal outcomes are achieved. Our scope of service includes strategic advisory services and specialist services. Specialist services

building surveying health & safety

community & stakeholder consultation management consultancy

capital allowances & property tax high performance buildings

dispute resolution operational commissioning

due diligence project audit & recovery

energy services research

expert witness risk management

facilitation services sustainability consultancy

framework set up & management training

health planning urban planning context analysis

Strategic advisory services

business case & strategy development property portfolio advice

development management strategic procurement & contract advice

facilities management consultancy value management

project appraisals PPP/PFI We advise governments, public sector purchasers, SPVs, contractors, funders and operators with an unrivalled range of management, cost and other technical skills. We provide advice on all technical aspects, from sustainability and whole life services, to financial and investment advice. We also have a specialist company that manages and invests in Special Purpose Vehicles (SPVs) in PFI and PPP projects. The business specialises in key niche sectors: health, education, blue light, social housing, student accommodation and waste. Services

consultancy investment

independent certifier technical advisor

benchmarking quantity surveying

cost planning & pre contract cost control risk advice

feasibility & master planning services engineering cost management

insurance valuations tender documentation and evaluation

post contract cost control value engineering

procurement & contract advice whole life costing / life cycle costing

Sweett Group plc (formerly Cyril Sweett Group plc)

4

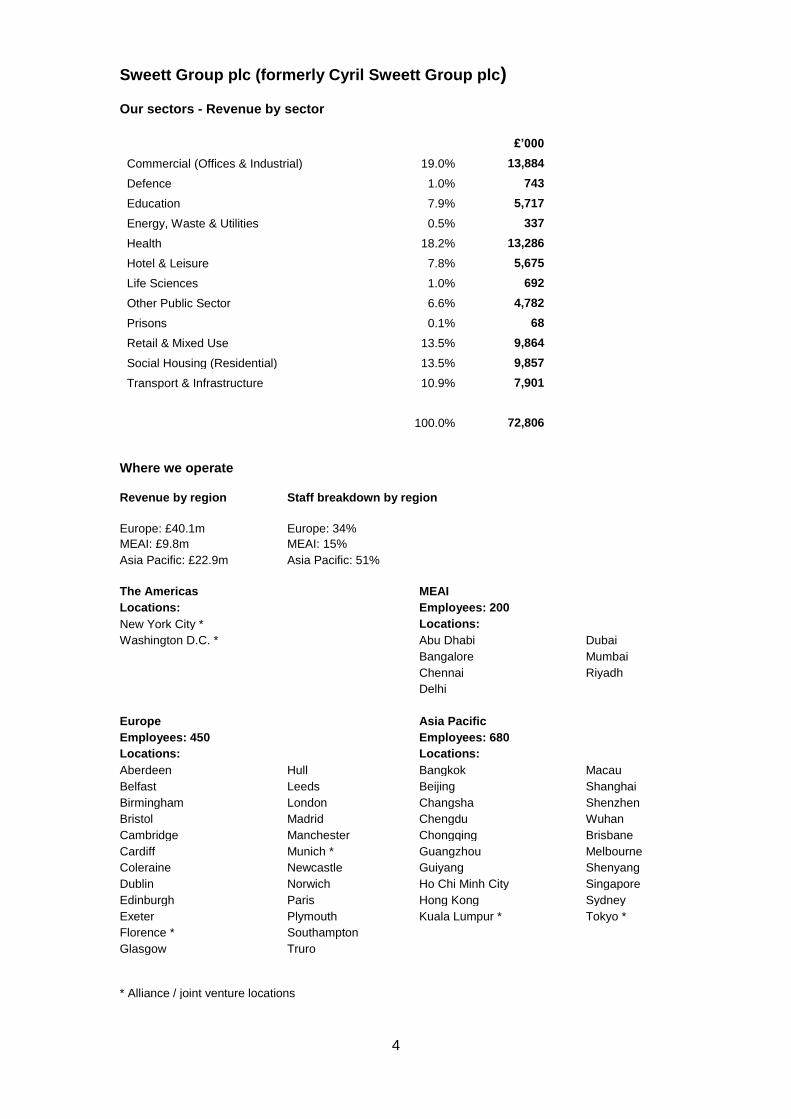

Our sectors - Revenue by sector

£’000

Commercial (Offices & Industrial) 19.0% 13,884

Defence 1.0% 743

Education 7.9% 5,717

Energy, Waste & Utilities 0.5% 337

Health 18.2% 13,286

Hotel & Leisure 7.8% 5,675

Life Sciences 1.0% 692

Other Public Sector 6.6% 4,782

Prisons 0.1% 68

Retail & Mixed Use 13.5% 9,864

Social Housing (Residential) 13.5% 9,857

Transport & Infrastructure 10.9% 7,901

100.0% 72,806

Where we operate

Revenue by region Staff breakdown by region

Europe: £40.1m Europe: 34%

MEAI: £9.8m MEAI: 15%

Asia Pacific: £22.9m Asia Pacific: 51%

The Americas MEAI

Locations: Employees: 200

New York City * Locations:

Washington D.C. * Abu Dhabi Dubai

Bangalore Mumbai

Chennai Riyadh

Delhi

Europe Asia Pacific

Employees: 450 Employees: 680

Locations: Locations:

Aberdeen Hull Bangkok Macau

Belfast Leeds Beijing Shanghai

Birmingham London Changsha Shenzhen

Bristol Madrid Chengdu Wuhan

Cambridge Manchester Chongqing Brisbane

Cardiff Munich * Guangzhou Melbourne

Coleraine Newcastle Guiyang Shenyang

Dublin Norwich Ho Chi Minh City Singapore

Edinburgh Paris Hong Kong Sydney

Exeter Plymouth Kuala Lumpur * Tokyo *

Florence * Southampton

Glasgow Truro

* Alliance / joint venture locations

Sweett Group plc (formerly Cyril Sweett Group plc)

5

Chairman’s Statement “I remain heartened by the continued support, collaboration and professionalism exhibited on a daily basis by our colleagues across the world, which will continue to set us apart from our peers as we build a stronger Sweett Group.” It is my pleasure to present Sweett Group plc's annual report and accounts for 2012. The last twelve months have seen the shape and size of our business evolve as we have continued to deliver on our strategy of creating a more diversified, global Group. We entered 2012 having already been through a significant period of difficult market conditions in our traditional home markets. In the UK and UAE, these conditions continued throughout the year, impacting both revenues and margins. Our Asia Pacific business, buoyed by increasing revenues in China, was negatively impacted by losses in Australia during the first half of the year. The need to defer revenue recognition from two PFI asset divestments and the accounting treatment for a forward foreign exchange contract contributed to the Group missing its internal profit target for the year by over £2m, which was disappointing. However, we are confident, following the completion of the Inverclyde divestment in July of this year, that we have moved into the next year in a stronger position, having built a solid platform for the future, The Board believes it is appropriate to prepare the financial statements on a going concern basis and is confident that it has the right strategy and action plan to operate within the requirements of the Group‘s bank covenants (see Note 1 to the financial statements). Our net debt levels at March 2011 were £5m and having reached nearly £11m at September 2011 were reduced to just over £8m at March 2012. Construction markets in Europe continue to be affected by low levels of economic activity and the impact of the Eurozone crisis and related austerity measures. Although our European order book has fallen by some 47% since 2008, it has remained at a consistent level for the last 15 months, a sign that we are competing well and gaining market share, despite challenging conditions. Our operations in the Middle East, Africa and India (MEAI) were drastically impacted by the Arab Spring. By adjusting our cost base and focusing on winning work in new markets such as Saudi Arabia and Oman we are seeing a pick-up in activity in the region. Expanding our presence in Asia Pacific has been one of our key focus areas in the last 12 months, resulting in staff numbers growing by almost 30% to approximately 680. Our global capability, built on successfully developing a critical mass in key trade and industrial hubs around the world, has and will continue to benefit the Group greatly. Our outstanding reputation has been strengthened further during the year through the launch of a global brand, with all of our entities now operating under the Sweett Group identity. Having a brand that reflects the integrated, independent service offering that our global, corporate clients expect is one of our key strengths. During the year Eamonn Kerr resigned from the Group and I would like to thank Eamonn on behalf of the Board of Directors for his work in pioneering Sweett Group's international expansion. In November 2011 the Board of Directors invited Kim Berry, Managing Director, Asia Pacific, to join the Board as an Executive Director and in only a short space of time his presence within our senior management team has been a great help in accelerating our global expansion and integration strategies. We remain cautious of construction markets generally but our strong geographical spread gives confidence in our successfully providing high quality services to our clients around the world to maintain our position as a leading independent provider. I also remain heartened by the continued support, collaboration and professionalism exhibited on a daily basis by our colleagues across the world, which will continue to set us apart from our peers as we build a stronger Sweett Group.

Michael Henderson, Chairman

Sweett Group plc (formerly Cyril Sweett Group plc)

6

Business Review Contents

Three year strategy

Review of operations Europe (excluding Investments)

Investment activities

Middle East, Africa, India (MEAI)

Asia Pacific

Developments in North America

Rebrand

Outlook

Sweett Group plc (formerly Cyril Sweett Group plc)

7

Chief Executive’s Review Business Review

“Despite challenging market conditions across Europe and the Middle East our staff have worked relentlessly to ensure we continue to gain market share in our traditional home markets, whilst growing our presence in the Asia Pacific region, a testament to our ability to provide our clients with exceptional levels of service.” After a difficult start to the financial year, as a result of well documented challenging trading conditions in Europe and operational losses in the Middle East, we took action to de-centralise our administrative functions, reducing costs in both regions. The second half of the year saw an improvement in the Group‘s trading activities, as well as a reduction in our debt levels. We had planned for earnings to be realised from the divestment of two PFI assets during the year. Due to prolonged negotiations, together with the deferral of the profit attribution from these, our overall profit for the current year has fallen below expectations. The requirement to defer profits was a large setback as was the crystallisation under IAS39 of exchange rate losses which are shown as finance costs. The result of these adjustments meant that our performance in the year was a reversal in fortune as we report a loss before tax of £1.0m after the impact of £1.7m of exceptional and amortisation of acquired intangibles. This is clearly a disappointment; however our cost-cutting actions mean that we have started the current financial year in a much stronger position. During the year, the vision and expertise of our staff have made our investments in international expansion and diversification across new sectors and services a success, building a stronger, more diversified Sweett Group. Our order book now shows a healthy split between our main sectors, as does our revenue generation, which stands at 55% in Europe and 45% in the rest of the world. The growth of our Asia Pacific business, driven largely by the successful integration of our operations in China, and our ability to capitalise on a seamless regional presence, has continued at a substantial pace during the year. We have now almost doubled our staff numbers in China from around 300 in 2010, with revenues increasing by approximately 21% during the same period. Whilst our growth in Asia Pacific has been a key component of our improved performance, it has been very encouraging to see momentum returning to some of our core UK markets as well as the success the Group has had in entering new sectors such as energy and utilities, as a result of the significant investment over the last two years. Our ability to combine our global presence with local knowhow is what sets us apart from many of our competitors. Our clients come back to us as a result of the independent advice we provide them with, which is reflected in the success of their projects. Across the Group we are driving greater collaboration, which combined with our greater global footprint, is attracting a wider range of clients. The commitment exhibited by our staff, both towards our clients and in support of each other is something I am very proud of.

Three year strategy Having successfully built a globally diversified business operating under a single, unified brand, the Group‘s strategy moving forward will focus on a three year programme of organic growth, aimed at consolidating the global footprint we have developed whilst at the same time improving our margins and cash generation. The strategy plans to grow the business largely through organic means, with recruitment of key personnel in sectors or locations where our plan has identified additional expertise is required to fully develop the opportunity. We will focus on extending our sector expertise in Europe, diversifying our presence and service offering in Asia Pacific and further developing our presence in North America. We will carefully target any investment in the Middle East, North Africa and India, but will aim to be flexible by operating in new territories as and when our clients need support. As much of our strategy relies on using existing systems and resources, we aim to adopt a flexible approach to the pace of our expansion, should the economic environment deteriorate. The Group‘s increased revenue is predominantly expected to come from continued investment in Asia Pacific, where our progress in geographic expansion across mainland China and Southeast Asia, as well as diversifying our service offering by building a project management and strategic advisory expertise, is expected to deliver encouraging levels of growth over the next three years.

Sweett Group plc (formerly Cyril Sweett Group plc)

8

In Europe, the Group has invested in growth sectors such as energy and infrastructure and has secured framework appointments in both. Continuing to win work in these new sectors, combined with increasing market share in our existing areas of expertise, downsizing our PPP/PFI investment exposure and keeping overhead costs under tight control, are expected to result in improved cash generation and operating profit over the period. Growth in our international operations will also bring inward investment into our European operations, as we capitalise on opportunities to cross-sell our services to an increasingly large base of corporate clients, hoteliers and retailers. Improvements in the Group‘s margins will be driven by the reductions in the Group‘s cost base achieved during 2011/2012, which will result in cost savings of some £2m being realised in the current year. As the Group‘s operations in China mature, this will also contribute improved operating margins. In terms of cash flow, we have made some good progress in reducing our lock up (debtors and work in progress). However we have also been financing growth and additional working capital in developing our global footprint. With this footprint now in place we see that the next phase of our development can be focused more sharply on delivering improved margins and cash generation.

Review of operations Group financial performance

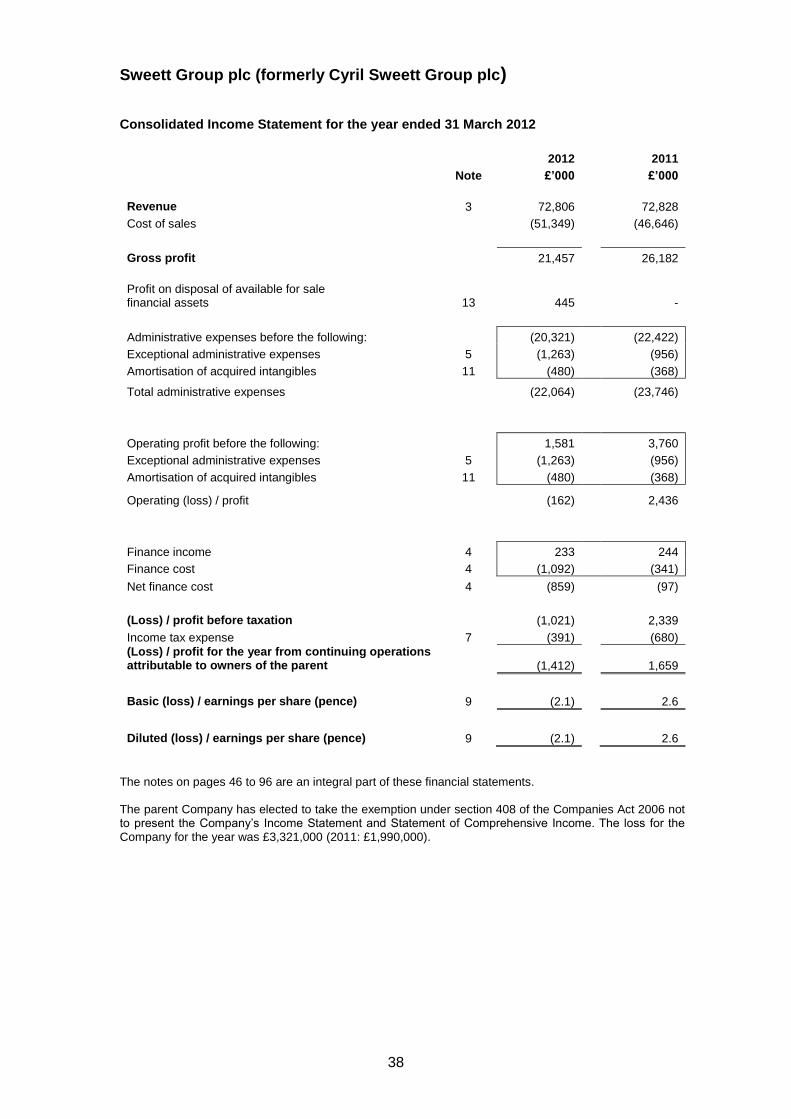

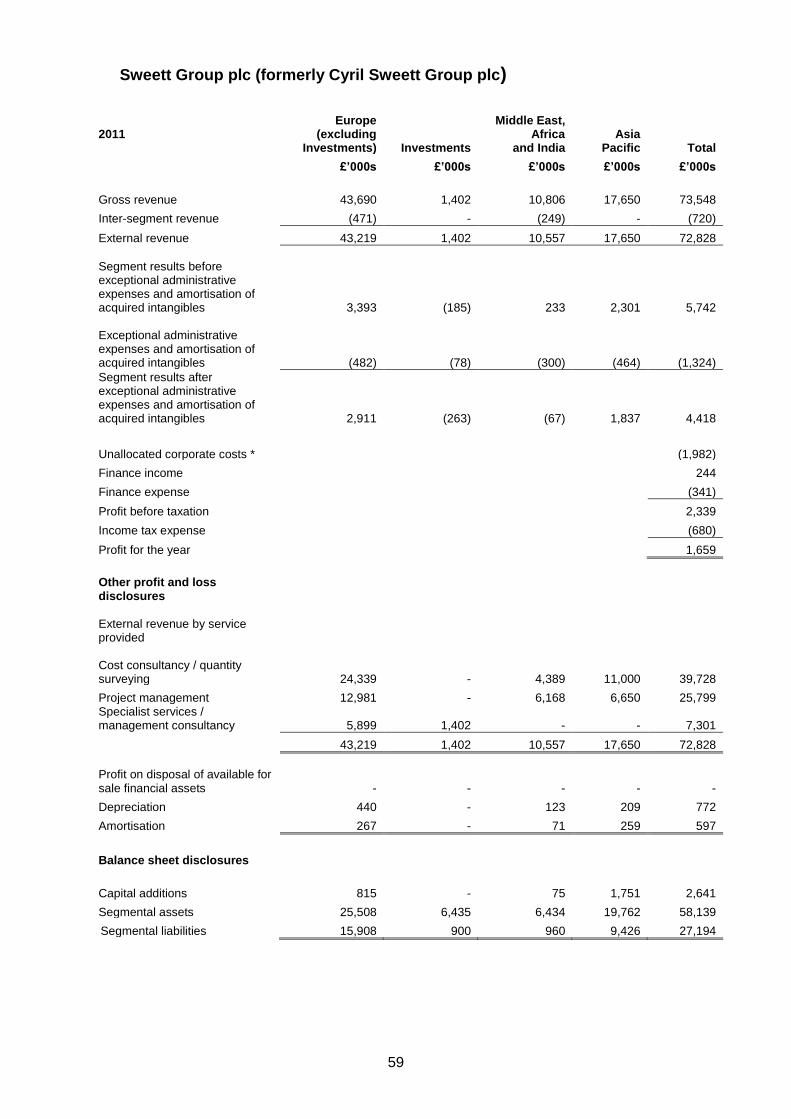

Revenue for the year was £72.8m (2011: £72.8m). The pre-tax loss (2011: profit of £2.3m) was £1.0m after exceptional expenses, amortisation of acquired intangibles and net finance costs. The results were severely affected by first half losses in Australia and the Middle East and during the second half, delays in reaching financial close on a major PFI project, the deferral of asset disposals and finance costs relating to Australia. Basic (loss) / earnings per share were (2.1) pence (2011: 2.6 pence) and operating margins were (0.2)% (2011: 3.3%). Our current order book is approximately £90m, a increase from last year‘s reporting date of 6% (2011: £84m). The Board has proposed a final dividend in respect of the year of 0.3p per share which, together with the interim dividend, totals 0.5p per share for the year. The final dividend will be paid on 12 October 2012 to shareholders on the register on 14 September 2012. Europe (excluding Investments) Revenue from Europe, which includes the Group‘s operations in the UK, Ireland and Continental Europe was down to £39.8m (2011: £43.2m), accounting for 55% of the Group‘s revenue. In overall terms Europe profits were £2.4m (2011: £2.9m). The order book stands at £33m (2011: £37m). Performance of our core activities was weak in the first half of the year with profit after exceptional items of £0.3m (2011:£1.5m). Following the restructuring actions announced in the first half of the year, the second half was a significant improvement and delivered £1.6m in operating profit. The operating margin on a pre-exceptional basis was 7.6% (2011:7.9%) as a result of the stronger second half performance. The full effect of the restructuring actions will be realised increasingly during the current year. Our European order book continues to reflect the short-term nature of contracts across the region. An increasing proportion of UK turnover is being achieved from frameworks which, with the exception of contracted projects, are not included in our order book projections. Our investment in the energy sector has been rewarded with our appointment on the NNB Genco (part of EDF Energy) framework for their new build nuclear programme, initially for the reactors at Hinkley C, Somerset. Further framework appointments in the energy and utilities sectors for Babcock, Dounreay Site decommissioning, Northern Gas Networks and United Utilities will provide the group with long term opportunities in the infrastructure market. Despite cuts in UK public sector spending, we continue to win work across the central government and local authority sectors around the country. During the past 12 months we have secured over 15 major framework appointments, including the North London Strategic Alliance and North West Construction Hub. In the health sector, we have secured framework appointments with a number of NHS Trusts, including Imperial Healthcare, Central & Northwest London and NHS Shared Business Services across England. Our sustainability team was recently appointed on the new pan-government three-year environmental and sustainability consultancy framework agreement by the Government Procurement Service (GPS), a significant win for the Group and evidence of our strength in the environmental arena.

Sweett Group plc (formerly Cyril Sweett Group plc)

9

Although activity levels across Europe continue to be suppressed by uncertainty surrounding the Euro zone crisis, we are capitalising on pockets of activity across the private sector, both in the UK and across Continental Europe. We continue to maintain our strong market position in the retail sector with appointments from Land Securities, Hammerson and Stanhope on major retail schemes in addition to working with blue chip retail clients such as Primark and Tesco and a predominance of high end retailers such as Selfridges, Jimmy Choo, Louis Vuitton and Shanghai Tang. Our commercial sector team has also won a number of commissions across the UK, including a regional programme and fit-out framework with Royal Bank of Scotland across northern England and Scotland and a framework appointment with Jaguar Land Rover. In Southern Europe, the Group has secured a commission for the Milan Hilton, further strengthening our hospitality sector portfolio. Investment activities Revenue from the Group‘s PFI/PPP business totalled £0.4m (2011: £1.4m). Segment losses were £0.7m (2011: £0.3m) and were offset by a gain of £0.44m on the sale of our interest in the South Ayrshire Schools PFI project. This activity has continued to develop new opportunities, despite a delay in reaching financial close on the Leeds Social Housing PFI project. The process of recycling existing investments has also taken longer than expected, though our investment in the South Ayrshire Schools PFI project for a total consideration of £787,500 was completed in the first half-year. In January 2012, we announced an agreement to dispose of our investment in the Inverclyde Schools PFI project for a total consideration of £2,192,860. The latter completed in July 2012 and therefore the profits were deferred into the current year. In April 2012, we announced the conditional sale of our investment in the Dumfries & Galloway Schools PFI project. However the Group has since withdrawn from this sale and will seek alternative divestment routes during the current financial year. Middle East, Africa, India (MEAI) Revenue from MEAI accounted for 13.4% of Group revenues at £9.8m (2011: £10.6m). Segment losses were £1.2m (2011: break even) and the order book is £6m (2011: £7m). Our performance in the Middle East was lower than expected, as a result of project postponements and cancellations resulting from the Arab Spring and continued depressed market conditions and investor sentiment across the region. Losses in the first half of the year were £0.7m. Whilst losses in the second half were £0.5m this included a £0.3m charge for exceptional costs. Conditions in the region are reflected in our order book, which stood at £13m 24 months ago and fell to as low as £4m, before rising to its current level. Following a reorganisation of our management team in the region and a reduction in both operational and overhead costs, we are now experiencing a pick-up in bidding activity across the region. The increased bidding activity has resulted in a number of recent project commissions and extensions, including the 90-storey Capital Market Authority Tower in Riyadh. In the health sector we have secured a high-profile commission from the Khalifa bin Zayed Foundation to provide cost and project management services on a new-build hospital in Sharjah and in the aviation sector we have secured commissions with Etihad Airways and the Dubai Aviation City Corporation. The hospitality sector remains one of our strongest in the Middle East, with current commissions with Raffles Hotel, Le Meridien, Grand Hyatt and developers such as Kingdom Hotel Investments. Following our cost reduction actions the region has returned to profitability during the first quarter of the current year. In India, the Group is benefiting from buoyant markets in Delhi and Bangalore, whilst conditions in Chennai and Mumbai remain challenging. With a regional management team across its four offices now in place, the Group aims to continue to grow its presence across India. Asia Pacific Revenue from Asia Pacific accounted for 32% of Group revenues at £22.9m (2011: £17.6m). Segment profits were £1.3m (2011: £1.8m) and the order book stands at £51m (2011: £40m). The Group‘s operations in China and Hong Kong (previously Widnell Limited) continue to perform better than expected at the time of its acquisition both in terms of revenues and profits, contributing approximately £15m of revenues and £1.5m of net profit. The segment‘s operating margin on a pre exceptional basis for the entire region was 8.1% (2011:13.0%) weighed down by our performance in Australia.

Sweett Group plc (formerly Cyril Sweett Group plc)

10

Our performance in North Asia was very strong with first half profits of £1.2m (2011; £0.4m). Second half performance was still satisfactory at £0.7 (2011:£1.2m) although the results were beginning to reflect a slow-down in the China construction markets. Nevertheless, the operating margin for the year on a pre-exceptional basis was 13.7% (2011:20.0%), encouraging given the levels of investment in new resources that are being dedicated to the region. The performance of the Australian business was particularly disappointing with £0.6m of operational losses in the year, which was sustained substantially in the first half of the year as the result of weak trading, issues with two contracts and re-assessment of long service and annual leave provisions. The growth of our presence in China and Hong Kong is one of the main contributors to the Group‘s increased diversification during the year. We now employ over 600 staff across China, with a further 80 staff across Southeast Asia and Australia. With an experienced Asia Pacific management team now in place, we are focusing considerable efforts on cross-selling services and sector expertise throughout North Asia, Southeast Asia and Australia, including the development of full project management dispute resolution and programme management services to complement our well established cost management offering in China. In China, the Group enjoys a large blue-chip client base which includes numerous listed Hong Kong and Chinese developers, international businesses investing in the country and multi-national corporates and retailers. The Group has mature and sizeable offices in the first tier cities of Shanghai, Beijing and Guangzhou and established and expanding offices in the fast-growing second tier cities of Shenzhen, Chengdu, Chongqing, Tianjin, Wuhan, Changsha and Shenyang. While we anticipate some fluctuations in the Chinese economy, we believe that it will continue to grow significantly over the long term and will enable the Group to benefit from cross-selling opportunities with existing international clients as they invest in the country's growing domestic market, as has already been the case with clients such as Nike, Merlin Entertainments, Tesco and Blackrock. Similarly, we are able to capitalise on the flow of outward investment from China by supporting existing clients such as Shanghai Tang, Shangri-la Hotels and Huawei as they develop their global presence. In Southeast Asia our expansion is being led out of our established offices in Singapore and Hong Kong together with the investment we have made in our office in Thailand, recent registration in Vietnam and joint ventures established in Malaysia and Japan. Operations in the region are now benefitting from the adoption of the single brand and the integrated approach of the Asia Pacific management team resulting in new commissions in the corporate real estate, hospitality and leisure sectors. As indicated, the Group‘s progress in the Asia Pacific region as a whole was held back by losses in Australia during the first half of the year. However, our Australian business is benefiting from growth across other parts of Asia Pacific, as a result of cross-selling opportunities and returned to profitability during the second half of the year. This recovery was complemented with a number of significant wins including a framework appointment with the Australian Department of Defence and successful investments in developing our cost management service offering. Developments in North America The successful progression of the Group‘s alliance partnership with VVA LCC, a New York based project management consultancy, has resulted in the signing of a joint venture agreement in May, 2012. The joint venture company, VVA Sweett, is incorporated in the State of New York, with each party owning 50% of the joint venture company‘s shares. Through the joint venture, the Group will market its cost management services to North American corporate clients, as well as offer existing clients project management and cost management services across North America. Rebrand In order to further strengthen its leading position and help integrate its acquisitions, the Group embarked on a global rebrand during the year at a cost of approximately £100,000. The process, which saw the consolidation of four brands into one, was completed in April 2012. All wholly-owned businesses in the Group are now operating under the Sweett Group brand with most of the entities renamed. Cyril Sweett Group plc was renamed Sweett Group plc on 23 January 2012.

Sweett Group plc (formerly Cyril Sweett Group plc)

11

Outlook The last four years, during which time the global economy and construction industry in particular has experienced significant challenges, have been transformational for Sweett Group. The impact of the global economic recession, financial turmoil in the euro-zone and political instability in parts of the Middle East have necessitated difficult decisions to adjust the size and structure of our business, resulting in annualised savings of £2m being realised in the current year. Having implemented these, whilst diversifying our presence and expertise, the Group now has a solid platform from which to deal with lower levels of activity in the developed world, whilst having the ability to expand in growth markets. The outlook for the construction sector across the regions in which we operate varies considerably. In Asia Pacific, the Group‘s main growth market, we will benefit from an encouraging order book but are also mindful of the slowing growth currently being experienced in the region. In Europe, the economic recession and instability across the euro-zone, together with further planned reductions to UK spending, will continue to have a negative impact on public sector spending and construction activity as a whole. We do not anticipate this gap will be filled by the private sector in the short term and we expect market volumes and pricing levels to continue to be challenging. However, the Group‘s entry into new markets such as energy and infrastructure and our success in securing framework appointments across a variety of sectors does provide encouragement. We remain cautious about construction markets in the Middle East, Africa and India. We are encouraged by increased levels of bidding, in particular in the UAE and are focusing on developing new business opportunities in growth markets such as Saudi Arabia, Oman and Qatar. Our business in India continues to benefit from private sector investments across the country‘s main business and trade hubs. In North America, where we now have a joint venture company with VVA, a leading New York based project management firm, we are seeing some initial cross-selling opportunities, as well as opportunities to provide cost management services to our JV partner‘s existing clients. Trading during the first four months of the current financial year has been in line with Management‘s expectation, with each reporting region seeing significant increases in profits compared to the same period last year. Our order book currently stands at £90m, with a healthy split across Europe, MEAI and Asia Pacific. I am confident that the dedication of our staff and quality of service that they provide to our clients will continue to contribute to building a stronger Sweett Group.

Dean Webster, Chief Executive Sweett Group plc

Sweett Group plc (formerly Cyril Sweett Group plc)

12

Financial Review Trading performance

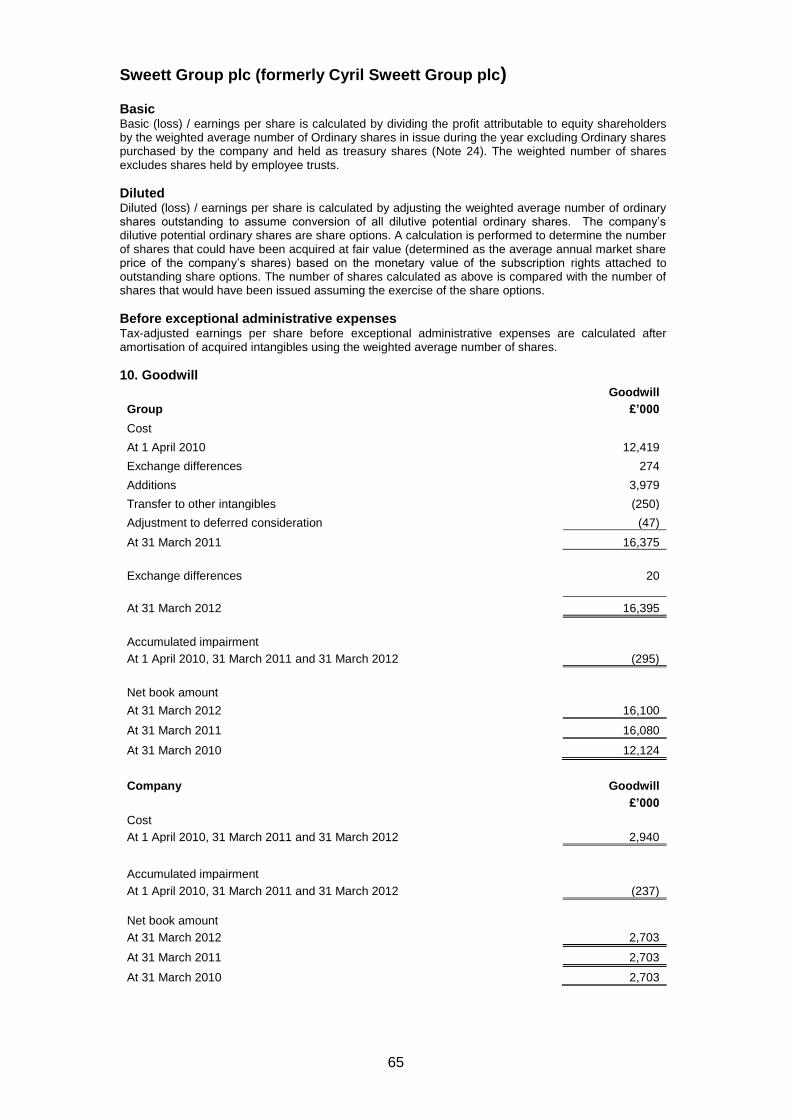

The year to 31 March 2012 was a further year of consolidation for Sweett Group in the UK, where revenues decreased, whilst activity levels overseas increased overall following the acquisition of Widnell Limited in the previous year. Group revenue was £72.8m (2011: £72.8m). There was a loss before taxation, after the impact of £1.2m of exceptional expenses and £0.5m of amortisation of acquired intangibles as described in Note 5 to the financial statements, of £1.0m (2011: profit of £2.3m). This loss was exacerbated by profit recognition on two non-concluded PFI asset sales being deferred. The Inverclyde Schools disposal completed in July 2012 such that the gain has already been recognised in the current year. The Dumfries & Galloway Schools disposal is being pursued under a revised structure with the intention of concluding a transaction in the current year also. Furthermore, there was a charge to finance costs of £0.6m relating to the change in fair value of a derivative financial instrument under IAS39. This is covered in more detail below. The primary segmental analysis in Note 3 to the financial statements details the segmental revenue and result. In aggregate the Group‘s gross margin decreased from 35.9% to 29.5%, with segmental margins affected mainly by continued competitive pressure in the UK, losses arising in France, contract issues in the Middle East and Australia and staff retention issues in Hong Kong and China. Despite reductions in administrative expenses, the segment results are each affected by these issues. An increase at the half year in work in progress on achievement of preferred bidder status on the Leeds Social Housing project of £362,000 has been de-recognised in the full year operating loss, due to the continued delay in financial close of the project. Details of exceptional costs and other items affecting the result for the year are provided at Note 5 to the financial statements. Exceptional costs of £1,263,000 (2011: £956,000) comprised in the main restructuring costs of £1,193,000 (2011: £694,000). Other items which are material to an understanding of the results, also detailed in Note 5 to the financial statements, totalled £500,000 (2011: a credit of £400,000) of which £602,000 related to the change in fair value of a derivative financial instrument under IAS39. There was little change in the exchange rates to sterling of our major trading currencies and little impact on either revenues or profits at the pre-interest level.

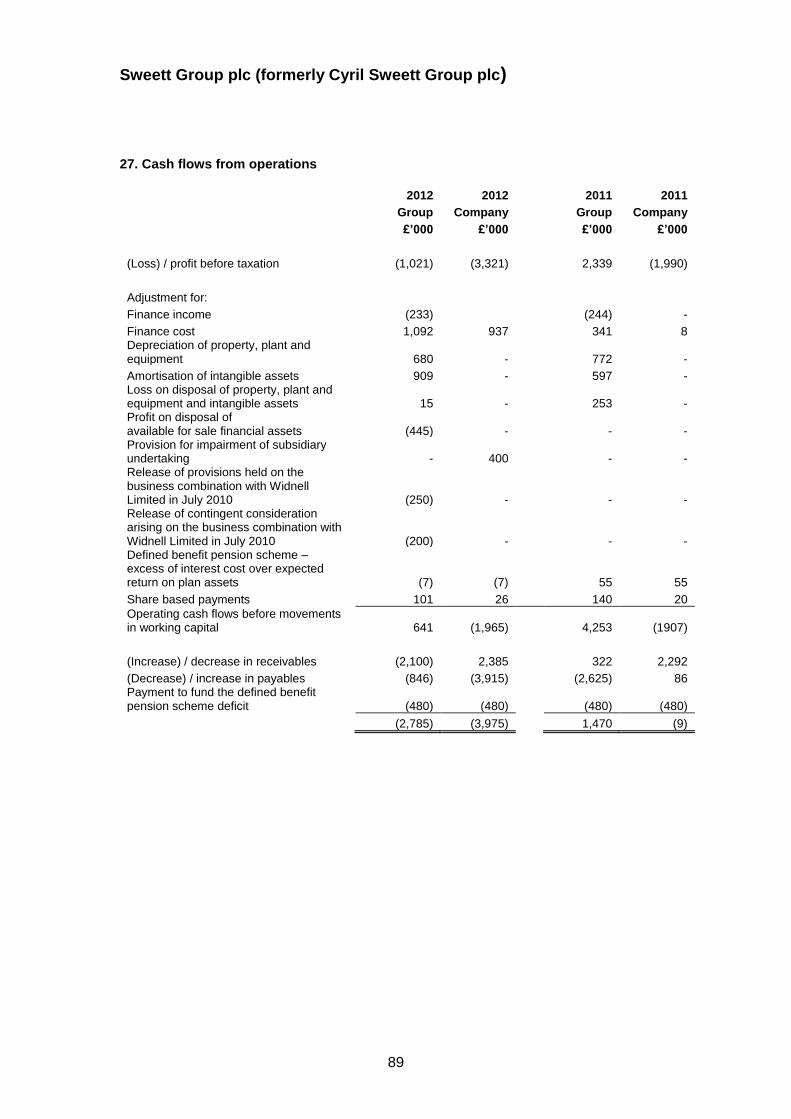

Cash performance

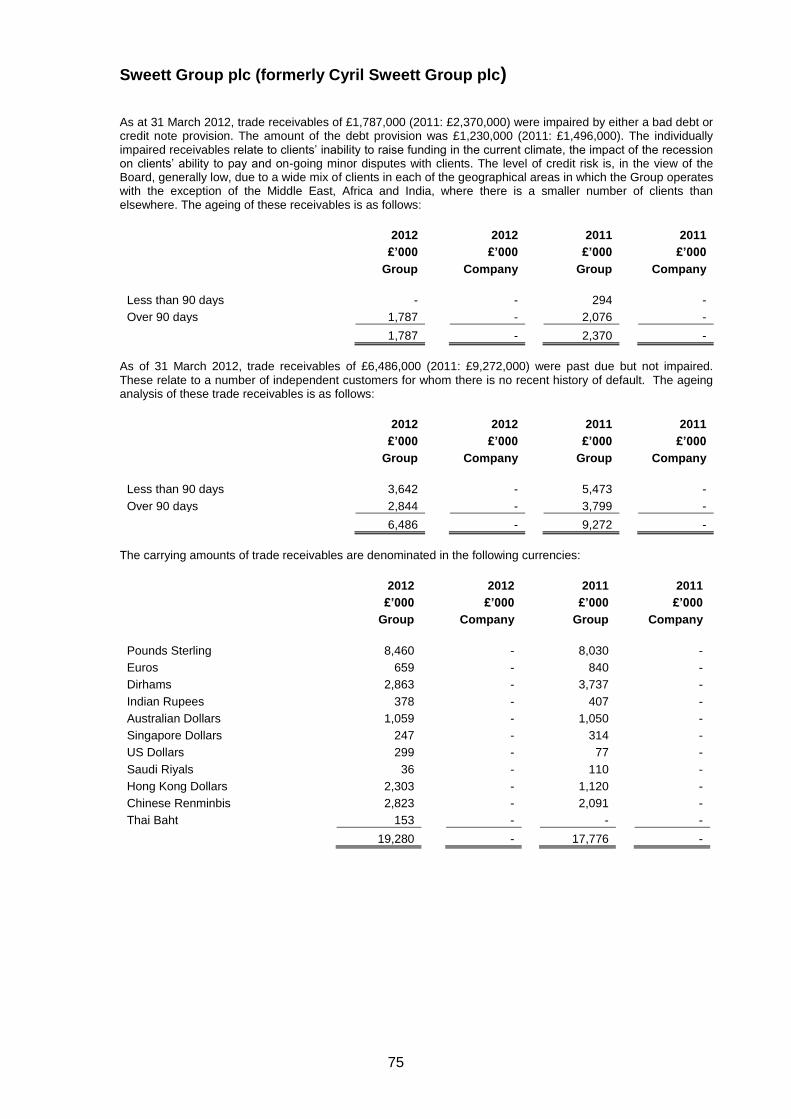

Cash (used by) / generated from operations was £(2.8m) (2011: £1.5m). Note 27 to the financial statements analyses this usage, which arises largely through working capital outflows. In particular, the Group‘s work in progress net of fees in advance increased to £5,766,000 (2011: £4,149,000) and gross receivables to £20,510,000 (2011: £19,272,000), though overdue amounts reduced to £6,486,000 (2011: £9,272,000) and there was a reduction in the impairment provision to £1,787,000 (2011: £2,370,000). The lock-up calculation, which measures the number of days‘ activity included within work in progress and debtors, incorporates an annualisation of revenues based on the last three months‘ revenues. Management of working capital is a key issue as the Group expands, particularly in the Asia Pacific region, and steps are being taken to improve its management such that operating cash flows are expected to improve.

Key Performance Indicators

A number of metrics are used to monitor financial performance. These include turnover, operating profit, cash collection, pre-exceptional administration costs, earnings per share and lock-up. Most of these Key Performance Indicators remained stable in the last year. The pre-exceptional administration expenses (loss) / earnings per share were (0.5)p (2011: 3.7p) and the average number of lock-up days for the final quarter was 87 (2011: 94). These have been covered in more detail in the business review. The financial performance by segment is reported in Note 3 to the financial statements.

Underlying profit margins

The gross profit margin was 29.5% (2011: 35.9%) and the operating profit margin was 0% (2011: 3.3%). The operating profit margin before exceptional administrative expenses was 1.5% (2011: 4.7%). Internal forecasts for the current year indicate a recovery in the gross margin, in part through the full-year impact of cost savings made in late 2011 and better trading profiles in Australia and the Middle East, Africa and India region.

Sweett Group plc (formerly Cyril Sweett Group plc)

13

Finance costs

Note 4 to the financial statements discloses a cost of £0.6m relating to the change in fair value of a derivative financial instrument under IAS39. The circumstances were that a forward foreign exchange contract valued at AUD$11.1m to hedge advances in Australian dollars to a subsidiary company, the bulk of which were capitalised in September 2011, was rolled into a replacement instrument on maturity in March 2012 and is being accounted for as a derivative rather than a hedge. The hedge is effective for AUD8.5m, being the Group‘s net asset exposure to Australia, from 1 April 2012 having failed the stringent IAS39 documentation requirements for the year ended 31 March 2012. The balance of the contract is hedging advances to Australia.

Tax

The charge for the year of £391,000 on a reported loss of £1,021,000 arises predominantly through the impact of expenses not deductible for tax purposes and deferred tax relief not recognised. The 2011 charge of £680,000 was affected by lower tax rates on overseas earnings and the reversal of expenditure disallowed in previous periods, net of the determination of prior year liabilities.

Earnings per share

Basic (loss) / earnings per share decreased to (2.1) p (2011: 2.6 p) and fully diluted (loss) / earnings per share decreased to (2.1) p (2011: 2.6 p). Tax-adjusted (loss) / earnings per share prior to exceptional administrative expenses was (0.5) p (2011: 3.7 p).

Balance sheet

The Group ended the year with:

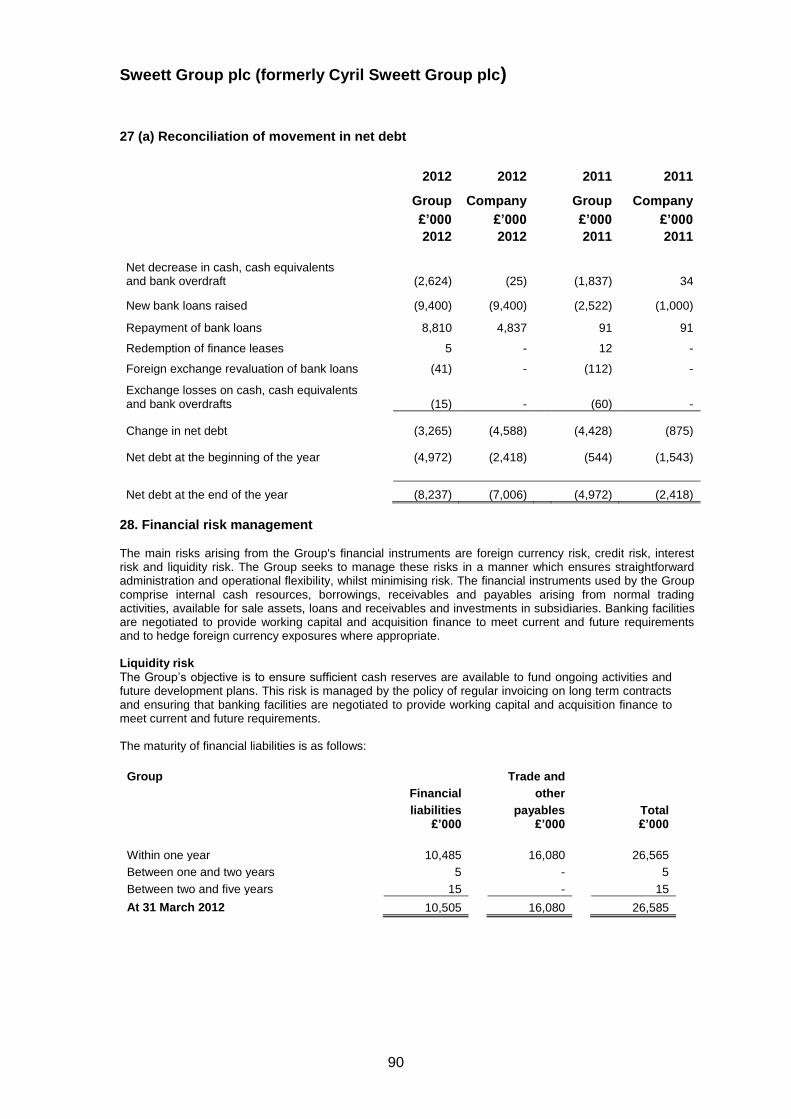

- Net borrowings of £8.2m, compared with £4.9m at 31 March 2011; - Net assets of £28.8m, which compared with net assets of £30.9m at 31 March 2011; - Work in progress (net of fees in advance) of £5.8m compared with £4.1m at 31 March 2011;

and - Trade receivables of £19.3m compared with £17.8m at 31 March 2011.

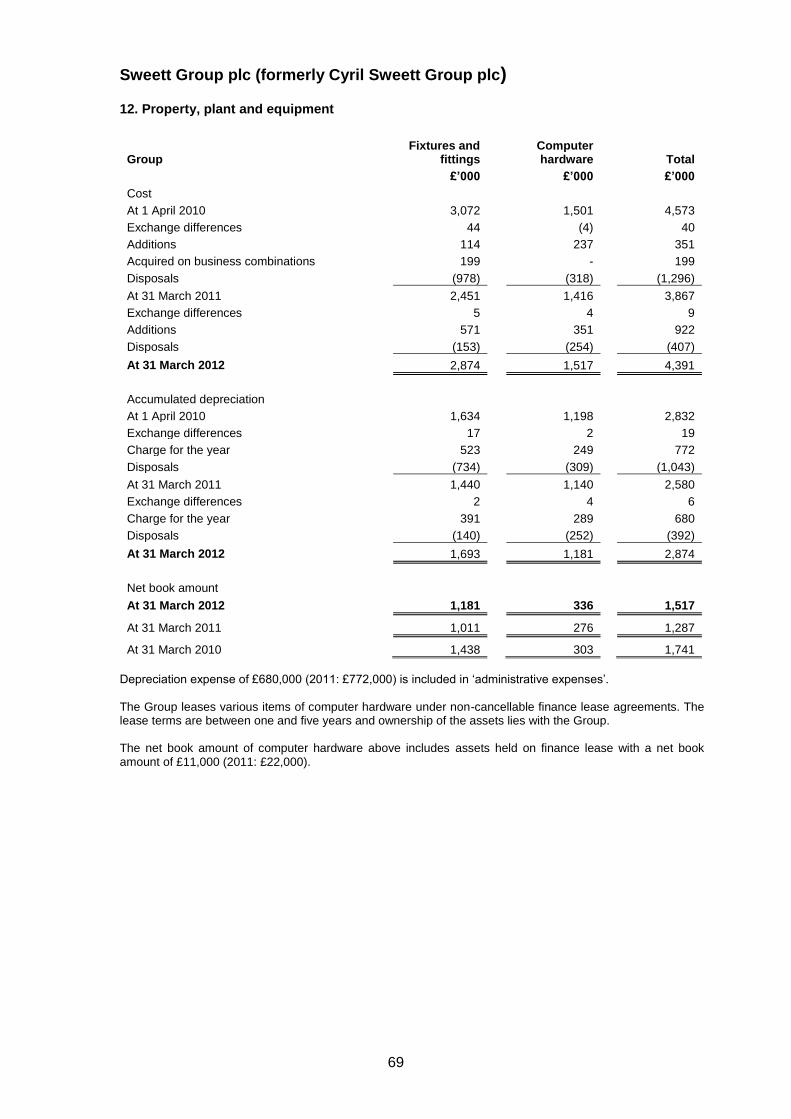

We continue to invest in property, plant and equipment and computer software to ensure that, as the business environment becomes more complex and technology evolves, the Group‘s IT systems and equipment are kept up-to-date and properly serve the business.

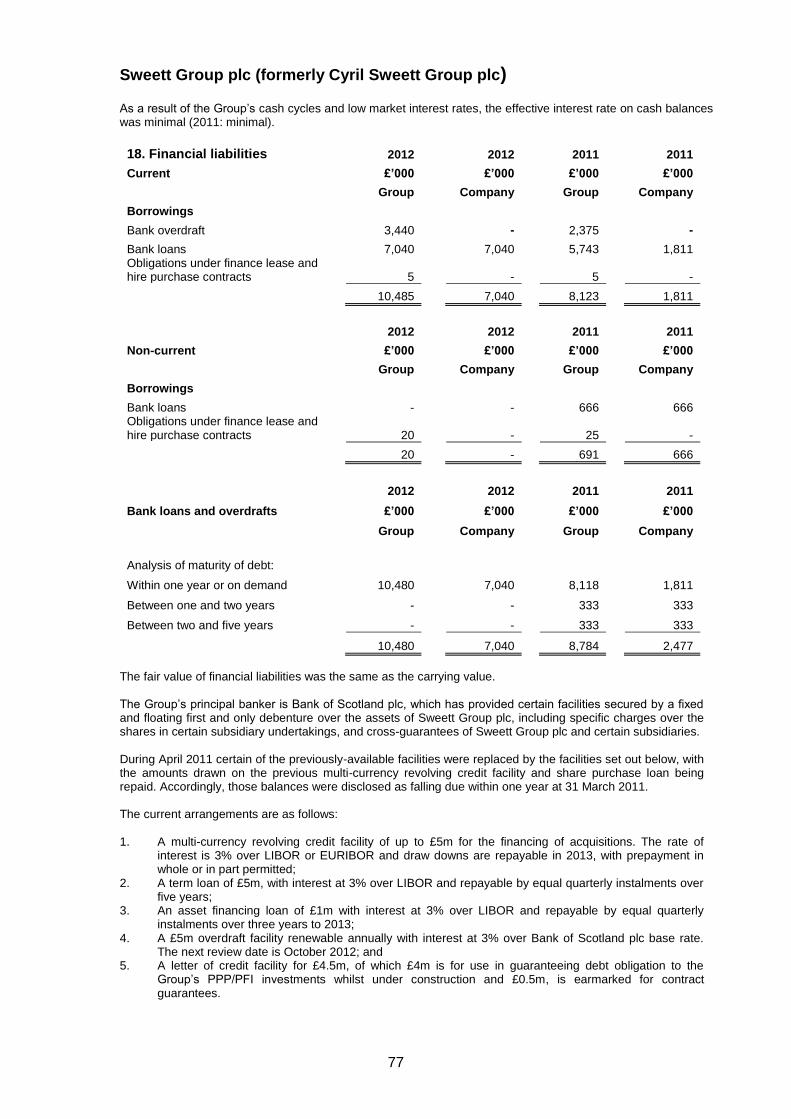

Banking facilities

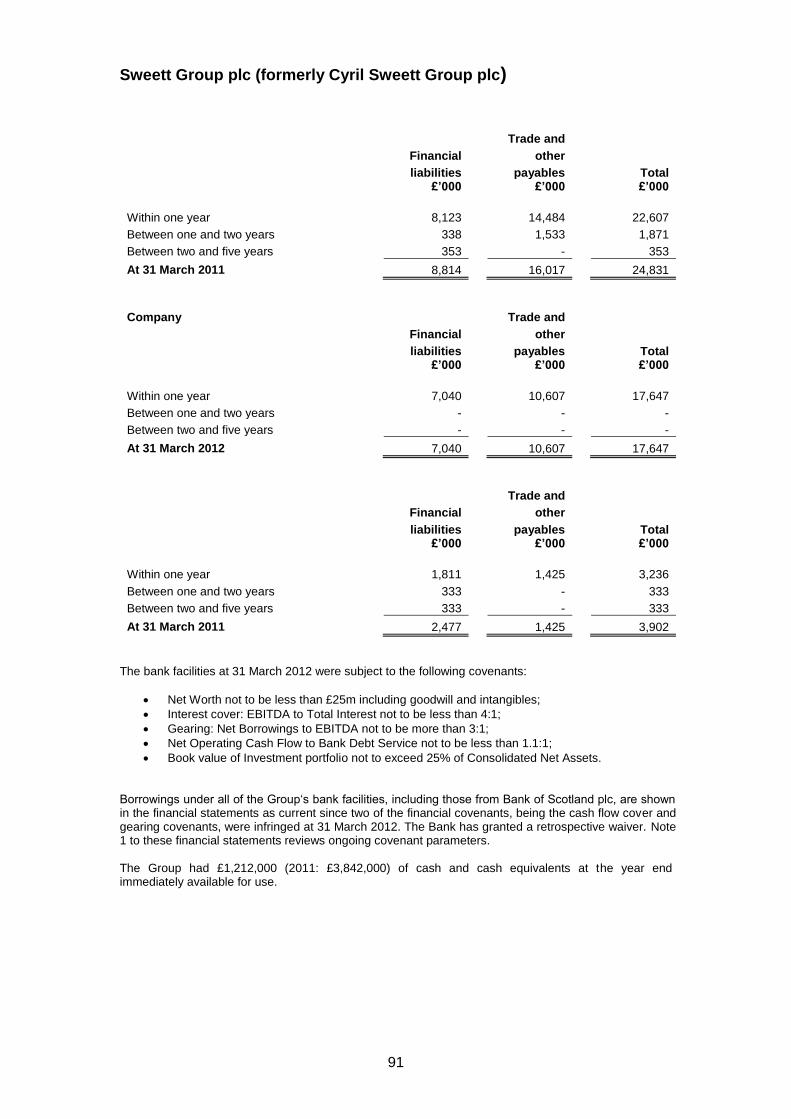

The Group funds its activities through cash generated from operations and supplemented, where necessary and appropriate, with bank borrowings and asset funding. The Group‘s principal banker is Bank of Scotland plc, part of the Lloyds Bank group, which provides Sweett Group with overdraft, revolving credit, loan and contract guarantee facilities as well as a letter of credit facility in relation to the ongoing equity and debt obligations of the Group‘s PPP investment projects. At 31 March 2012, the amount undrawn under the Group‘s credit lines was £7m (2011: £7m). All of the borrowings under the Group‗s credit lines are shown in the financial statements as current liabilities. The reason for this is that two of the financial covenants, being the cash flow cover and gearing covenants, were infringed at 31 March 2012. Bank of Scotland plc has subsequently granted a waiver. The Bank of Scotland plc facility agreements contain five separate financial covenants being:

Net worth shall not at any time be less than £25m

The ratio of EBITDA to Total Interest shall not at any time be less than 4:1

The ratio of Net Operating Cash flow to Bank Debt Service on each test date shall not be less than 1.1:1

The ratio of Total Net Debt to EBITDA shall not at any time exceed 3:1

The value of CS Investments PPP investment portfolio as detailed in the annual audited accounts shall be no greater than 25% of the consolidated net assets

Sweett Group plc (formerly Cyril Sweett Group plc)

14

Going concern

A detailed examination of the Group‘s cash flow and trading forecasts has been undertaken to enable the board to conclude that the Group can operate within its banking covenants such that it could be established that the Group should continue to prepare its financial statements on the going concern basis. Further information on going concern appears within Note 1 to the financial statements.

Internal Controls

In the established parts of the Group there are well developed policies and procedures to support a sound internal control environment. These policies are being rolled out across the enlarged Group but this standardisation is not yet complete. Systems enhancements over the next two years, based on the roll-out of the UK‘s Agresso ERP system across the group‘s overseas businesses, will further strengthen internal controls. Meanwhile more intense management review processes are in operation and it is intended to form a treasury committee to oversee matters of treasury control in an international environment. The corporate governance section of this Report outlines further issues of internal control within the Group.

Dividends

An interim dividend for the year to 31 March 2012 of 0.2 pence per share at a cost of £133,000 (2011: 0.5 pence per share at a cost of £325,000) was paid on 16 January 2012 to all shareholders on the register on 16 December 2011. The directors are recommending a final dividend of 0.3p per share at a cost, assuming no issues of shares in the intervening period, of £200,000 (2011: 0.8 pence at a cost of £530,000) which, if approved by the shareholders at the AGM, will be paid on 12 October 2012 to all shareholders on the register on 14 September 2012. A dividend reinvestment service is available through the Registrar.

Employee Benefit Trust

The Group‘s Employee Benefit Trust (EBT) is a separately administered discretionary trust in Jersey for the benefit of employees. Shares owned by the EBT are shown as a reduction in capital and reserves as Treasury shares. Periodically, payments are made by Sweett Group to the EBT to reimburse the EBT for awarding shares or transferring shares to employees on the exercise of options.

Share Incentive Plan

The Share Incentive Plan (SIP), originally launched in February 2001, enables UK resident employees to acquire shares in the Group out of untaxed income and provides a tax-efficient means of awarding shares to employees. Dividends received by the plan in cash are used to purchase additional shares on behalf of employees. Free shares may be awarded to qualifying employees based on remuneration. Shares held in the plan which have not been allocated to individual employees are shown as a reduction in capital and reserves as Treasury shares. The granting of matching shares whereby individuals‘ purchases of SIP shares were matched on a 4 for 5 basis was withdrawn with effect from 31 December 2010.

Summary

Sweett Group‘s underlying trading performance is expected to improve as the result of past cost reduction programmes and attention to consolidating its present global operations.

Chris Goscomb

Chief Financial Officer

Sweett Group plc (formerly Cyril Sweett Group plc)

15

Governance

Although not required to do so by the AIM Rules, the directors have chosen to give selected disclosures on the main principles of the UK Corporate Governance Code 2010 (“the Code”) in so far as is practicable for a business of its size and nature. The Board is committed to high standards of Corporate Governance and considers sound governance and transparency to be fundamental to achieving its objective of enhancing shareholder value. Michael Henderson Non-executive Chairman

Sweett Group plc (formerly Cyril Sweett Group plc)

16

Board of Directors

Michael Henderson FCA, FRSA, KHS

Non-Executive Chairman

Date Appointed: Appointed as Non-Executive Director in 1998 and Chairman in 2010. Committee Membership: Nominations Committee, Remuneration Committee, Audit Committee Skills & Experience: Michael enjoys a long standing reputation for his expertise and network in industrial

and financial management. Other Appointments: At present Michael is also Chairman of the Advisory Board of Quexco Inc., the

largest lead producer in the world. Past Appointments: He was Managing Director and Chief Executive of Cookson Group plc (a former

FTSE 100 company) for 12 years and has also been a Director of Guinness Mahon Holdings PLC and Tioxide Group PLC. He was also Chairman of Henderson Crosthwaite Ltd.

Age: 73

Dean Webster MBA, BSc, FRICS, MAPM

Chief Executive Officer

Date Appointed: Joined the Board in 2000 and was appointed CEO in 2005. Skills & Experience: Dean joined the Company in 1980, qualified as a member of the RICS in 1986, is a

member of the Association of Project Managers and has a Henley MBA. Between 1995 and 2004 Dean was responsible for steering the Company‘s project management business. Dean now drives the Group's overall strategy and the performance of the Group‘s overall business operations.

Age: 52

Chris Goscomb FCA

Chief Financial Officer

Date Appointed: January 2009. Skills & Experience: Chris‘ construction industry background brings valuable experience to Sweett Group

in both its UK and international business. Past Appointments: Prior to joining the board, Chris had worked as the Group Treasurer for nearly 2

years. Before he joined Sweett Group, Chris was Finance Director of EMCOR (UK) Limited and previously Group Finance Director of Biwater plc.

Age: 60

Derek Pitcher BSc, FRICS Dip.Proj.Man

Director of European Operations

Date Appointed: Derek joined Sweett Group in 1978, became a Partner at the age of 30 and Managing Director of the Quantity Surveying business in 1996. He joined the Board in 2000.

Skills & Experience: Derek is a managing Director with responsibility for the Group‘s operations in Europe, the Middle East and India. He is a Board Director of VVA Sweett joint venture in America, is responsible for a number of key accounts in the commercial and retail sectors and has led the Group‘s move into the nuclear and manufacturing sectors.

Other Appointments: Derek is the Honorary Treasurer of the British Council of Shopping Centres and an active member of BCO, Design and Build Foundation and also the RICS Procurement panel.

Age: 53

Sweett Group plc (formerly Cyril Sweett Group plc)

17

Kim Berry LLB (HONS), MRICS, MHKIS, MCIarb, RPS (QS), F.PFM

Managing Director of Asia Pacific

Date Appointed: November 2011. Skills & Experience: Kim joined the Company in 1982 and became Managing Director of the Group‘s

operations in China and Hong Kong in 1987, building it into a business with over 500 staff across 12 offices. Kim is responsible for operations across the Asia Pacific region. Kim is a member of the RICS, HKIS, CIArb and holds an Honours Degree in Law. Kim serves on the RICS Hong Kong QS Faculty Committee and is a past member of the HKIS QS Divisional Council and a past Chairman of the HK Association of Consultant Quantity Surveyors.

Age: 58

Roger Mabey CMG, FCIOB, FRSA

Non-Executive Director

Date Appointed: September 2003. Committee Memberships: Chairman of the Remuneration Committee, Member of Nomination Committee and

Audit Committee. Skills & Experience: Roger has a wealth of knowledge of operating in international and UK construction

markets. He has 40 years‘ experience in the construction and property industry. He is currently, a Fellow of the Chartered Institute of Building and a Fellow of the Royal Society of Arts.

Other Appointments: Roger is the Chairman for Housing Solutions Limited and in 1997 was made a CMG (Companion of the Order of St Michael and St George) in recognition for export achievement and services to the construction industry.

Past Appointments: Managing Director at Bovis International Ltd and as Director at Bovis Lendlease Ltd. Aged: 67

Paul Nicholas Woollacott, BSc, CIGEM

Non-Executive Director - Senior Independent Director

Date Appointed: November 2007. Committee Membership: Chairman of the Nomination Committee, Member of Audit Committee and

Remuneration Committee. Skills & Experience: A former FTSE 100 Executive Director who has wide experience of developing,

acquiring and disposing of businesses in the UK and overseas. He has also had direct responsibility for running a workforce of over 15,000 people with still more contractors. As Senior Independent Director of Enterprise plc he was involved in its move from the AIM market to a full listing and then later, as Chairman, he oversaw its move into private-equity ownership. Subsequently, he was similarly involved in the transition of Goldshield plc from public to private-equity ownership.

Past Appointments: Senior Independent Director Goldshield plc, Chairman Enterprise plc, Board Member University of Hertfordshire, Group Managing Director Lattice plc and over 20 more national and international directorships.

Age: 64

Jeffrey Hewitt, FCA, MA, MBA

Non-Executive Director

Date Appointed: August 2010. Committee Membership: Chairman of the Audit Committee, Member of Nomination Committee and

Remuneration Committee. Skills & Experience: Jeff is a chartered accountant and has substantial experience as a Director of listed

companies, latterly in non-executive roles. He holds an Oxford MA in Chemistry and an MBA emphasising Finance and Marketing from Stanford, California.

Other Appointments: At present Jeff is also Director and Chairman of the Audit Committee of Cookson Group Plc, Director and Chairman of the Audit and Management Engagement Committee of Foreign & Colonial Investment Trust plc, Director and Chairman of the Audit Committee of Cenkos Securities plc and Chairman of Electrocomponents Pension Trustees.

Past Appointments: Jeff's past appointments are External Chairman of the Audit and Risk Committee of John Lewis Partnership and Executive Director of Electrocomponents Plc, Unitech Plc and Coats Plc.

Age: 64

Sweett Group plc (formerly Cyril Sweett Group plc)

18

Corporate Governance Details are provided below of how the Company applies those parts of the Code which it believes to be appropriate.

Leadership

The Chairman is responsible for leadership of the Board and for ensuring effectiveness of the Board as a whole. The Board‘s role is to determine the strategic direction of the Group within a framework of best practice corporate governance and prudent and effective controls, which enables risks to be assessed and managed. It sets the Group's values and standards, including matters relating to corporate social responsibility, and ensures that its obligations to its shareholders and others are understood and met. The roles of the Chairman and Chief Executive are separate and clearly defined and a Senior Independent Director has been appointed. The role of the Non-executive Directors is to challenge constructively and review executive proposals, including the development of strategy. The Board‘s annual two day strategy retreat was held in March, which all Directors attended, and which gave the Board the opportunity to work in a very focussed way on the Group‘s strategy for the coming year. All Directors are expected to attend all meetings of the Board, and of those Committees on which they serve, and to devote sufficient time to the Company‘s affairs to enable them to fulfil their duties as Directors. The table below details the attendance of Directors at Board and Committee meetings they were eligible to attend in the year: Board Executive

Dean Webster 8/8 Derek Pitcher 7/8 Chris Goscomb 8/8 Eamonn Kerr 5/6 Kim Berry 2/2 Board Audit Remuneration Nomination Non-executive

Michael Henderson 8/8 3/3 3/3 4/4 Roger Mabey 8/8 3/3 3/3 4/4 Nicholas Woollacott 8/8 3/3 3/3 4/4 Jeff Hewitt 8/8 3/3 3/3 4/4

Specific responsibilities reserved to the Board include:

The acquisition or disposal of a business or of shares in a company;

The establishment of a new business or closure of an existing business;

The annual budget and strategic plan;

Significant capital expenditure, IT equipment and leasing arrangements;

Proposed contracts satisfying specific criteria;

Changes to the organisational structure or management structure; and

Dividend policy.

Effectiveness

The Board comprises four executive and four non-executive Directors, meeting every other month and additionally when necessary. In the reporting period there were 8 formal Board meetings and also a 2-day strategic planning workshop dealing with shorter term budgeting and longer term planning issues. Sub-committees of the Board meet as required. The Executive directors have long and deep experience of business in the sectors in which the company operates. This is complemented by the expertise of the Non-executive directors who have strong track records of running both large and smaller companies in diverse sectors both nationally and internationally. This collective mix of skills and experience is a major contribution to the proper functioning of the Board, ensuring matters are constructively challenged and fully debated and that no individual or group dominates the Board‘s decision-taking process.

Sweett Group plc (formerly Cyril Sweett Group plc)

19

Directors are appointed by the Board on the recommendation of the Nomination Committee, for specified terms. They are subject to periodic re-appointment by shareholders and statutory provisions regarding removal. This applies equally to Non-executive directors and, because the non-executive Chairman of the Company has served on the Board in excess of nine years, with effect from 10 September 2010 he is subject to annual re-election at the Company‘s Annual General Meeting. The Board has determined that the Chairman continues to be independent in character and judgement and that the Company is fortunate to have someone of his calibre and expertise to lead it. Each non-executive Director has significant external commercial experience and brings this experience and judgement to the Board. The Board considers that all of the non-executive Directors are independent of management and have no business or other relationships which could materially interfere with or affect the exercise of their independent judgement. None has previously been involved in the management of the Company. Nicholas Woollacott was appointed Senior Independent Director on 30 November 2010. When required he presides at meetings of the Board and shareholders in the absence of the Chairman and is available should occasion arise where there is a need to convey concerns to the Board other than through the Chairman, the Chief executive and the other executive Directors. All Directors have access to the advice and services of the Company Secretary and there is a procedure for Directors to seek independent professional advice, in furtherance of their duties, at the Company‘s expense. The Company Secretary is responsible for advising the Board, through the Chairman, on all governance matters. Under the direction of the Chairman, the Company Secretary ensures that the information presented to the Board is timely and of sufficient quality to enable members to make informed decisions and ensures good information flows within the Board and its Committees and between Senior Management and non-Executive Directors. The Board is committed to evaluating its own performance, that of its Committees and its individual Directors. Individual Board members (executive and non-executive) are evaluated annually on similar timing to the Company-wide appraisal system. This is led by the Chairman of the Board generally and by the Senior Independent Director in relation to the Chairman. The Board conducted its last effectiveness review in 2009 and although the Code recommends a review be conducted every year, the Board considers it to be more reasonable to hold the effectiveness review when required rather than every year. The Board will be conducting an effectiveness review in 2013. Nominations Committee The members of the Nominations Committee are the non-executive Directors. It meets at least twice a year and is responsible for reviewing the Board‘s structure, size, composition, balance of skills, experience, independence and knowledge. During the period the Nominations Committee advised the Board on appointments and resignations to and from the Board, succession planning, as well as reviewing the position of Chairman. A new executive Director was appointed to the Board in November 2011. As the candidate had a proven and impressive track record of achievement in the Asia Pacific Region and proved to be an ideal candidate for the role, no search agents were used on this occasion. The candidate‘s knowledge and abilities in running the Group‘s Far Eastern operations were seen as a valuable addition to the Board and an important step given the Group‘s ambitions in that region. When considering a new candidate the Nominations Committee takes into consideration relevant experience, knowledge, skills and suitability for the Board and the Company to ensure the best possible leadership and strength on the Board. Succession planning for the Group, Senior Management and the Board are in place and are continually updated as part of a Company-wide succession planning programme. The Nominations Committee leads this process for the Board. During the year the Nominations Committee assessed the appropriateness of the non-executive Chairman and concluded that although he had served in excess of nine years, he remains fully independent in character and judgement and continues to be an ideal leader for the Board, bearing in mind his very extensive business experience and expertise.

Sweett Group plc (formerly Cyril Sweett Group plc)

20

Accountability

The Board is responsible for establishing, reviewing and maintaining the Group‘s systems of internal control and risk management and ensuring that these systems are effective for managing the business risk within the Group. The Group has established a framework for identifying, evaluating and managing significant risks faced by the Group. It is the responsibility of the management to ensure that the controls and procedures that operate within the framework are followed and that the Board is kept fully appraised of any risks and control issues, both operational and financial. The Board recognises that any system of internal control exists to minimise the risk of failure rather than eliminate it and that any system of internal control can only provide reasonable, not absolute, assurance against material misstatement or loss. Work to reduce operational and financial risks and to improve the control environment is ongoing across the Group and will include the formation of a treasury committee in the current year. The risk management of joint ventures and strategic partnerships is agreed between the parties and periodic reviews carried out where appropriate. The Group reviews the effectiveness of the risk management system and its internal controls annually. Following on from the assignments performed last year in the UK and overseas by KPMG LLP, the internal auditors, an Internal Control Self Assessment Review has recently been introduced by them in respect of all of the Group‘s trading entities. This has supported the directors in assessing the effectiveness of the group‘s system of internal control. The outputs are being used to identify future internal audit priorities and assignments. This exercise is part of the ongoing process for identifying, evaluating and managing the significant risks faced by the group. The roll-out of a standardised Agresso ERP system, already embedded in the UK, across the group is expected to improve significantly the internal control environment. The UK product has been improved during the year and implementation in the overseas businesses is scheduled to commence later in the financial year. Audit Committee The Company‘s Audit Committee comprises the non-executive Directors and meets not less than three times per year. Jeff Hewitt, a qualified accountant, is Chairman of the Committee. The Board is satisfied that Mr Hewitt has the necessary recent and relevant experience to meet the requirement in the Code. The Company‘s Chief Executive Officer, Chief Financial Officer and the Company‘s auditors, PricewaterhouseCoopers LLP and internal audit providers KPMG LLP, are normally invited to attend Audit Committee meetings and other executives are invited to attend as and when appropriate. The Audit Committee operates under formal terms of reference that were reviewed in the year. The terms of reference authorise the Committee to obtain external professional advice as necessary. The main role and responsibilities of the Audit Committee are:

To review the half-year and annual financial statements and reports thereon, of the Company before their submission to the Board;

To review the process whereby the Board assesses the effectiveness of the Group‘s internal control and risk management systems;

To consider other topics, as defined by the Board, such as the Company‘s policies for preventing or detecting fraud, its code of corporate conduct/business ethics, or the policies for ensuring that the company complies with relevant regulatory and legal requirements;

To review the performance of the Company‘s external and internal auditing functions;

To review the results and cost effectiveness of the audit and the independence and objectivity of the external auditors;

To make recommendations to the Board on the appointment of the external auditors, the audit fee and any questions of resignation or dismissal relating to the auditors; and

To strengthen the independent position of the Company‘s external auditors by providing channels of communication between them and the non-executive Directors.

Sweett Group plc (formerly Cyril Sweett Group plc)

21

The main responsibilities of the Audit committee as discharged during the period were as follows:

At its meetings in June and November 2011, the Audit Committee reviewed the Company‘s Half-Yearly Report and Annual Results Announcement/Annual Report and Accounts, respectively. On both occasions, the Committee received reports from management on significant aspects of the Group‘s financial statements and reports from the Auditors identifying any accounting or judgemental issues requiring its attention;

At each of the three meetings held during the year, the Committee received reports from the internal auditor, KPMG, which considered, among other things, the ongoing internal audit programme, which included an Internal Control Self Assessment Questionnaire; and

The Committee also reviewed the External Auditors‘ control findings and monitored the updating of the risk register by management.

The Audit Committee is responsible for making recommendations to the Board in relation to the appointment, reappointment and removal of the Auditors. The Committee takes into consideration a number of factors including the quality of reports provided by the auditors and of advice given, the level of understanding demonstrated of the Company‘s businesses, the objectivity of the auditors‘ views on the controls throughout the Company, ability to co-ordinate a global audit, the cost competitiveness of the auditors, the tenure of incumbent auditors and the periodic rotation of the senior audit management assigned to the audit of the Company. Having considered these factors the Committee agreed to recommend the auditors for reappointment. As PwC has a long standing tenure as the Company‘s Auditor, the rotation of the senior audit partner was made at the commencement of the year. Where the auditors have provided non-audit services, the committee has ensured protection of their objectivity and independence taking account of relevant ethical guidance. Details of all fees paid to the auditors are included within Note 5 to the financial statements. The outsourced internal auditors, KPMG LLP, report to the Committee, which reviews and approves the internal audit work programme each year. An Internal Control Self Assessment Questionnaire was rolled out towards the end of the period on a global basis. The purpose of the control self assessment was to improve control consciousness amongst Sweett Group entities and give the Group comfort that the minimum standard of controls is in place across the key financial and IT processes within each entity, as well as identify gaps or weaknesses in the existing control framework against which to put action plans. It forms an important part of the Group approach to ensuring effective compliance with good corporate governance practice and will assist in setting priorities for the coming year. The Group has established a whistleblowing policy as part of its ethical guidelines to encourage openness and an environment where any relevant matter can be reported to management. The policy was rolled out across the Group during the year. A helpline is operated 24 hours a day, seven days a week, by an external organisation that specialises in these services. The policy was rolled out in English and Chinese and the facility is available to all group employees. An Anti Bribery and Corruption policy was developed during the year and training was rolled out to all employees globally. The training was conducted through an e-learning module and further information on Anti Bribery and Corruption is available to all staff on the intranet. The Board applies a zero tolerance approach to any breach of the Anti Bribery and Corruption Policy.

Remuneration

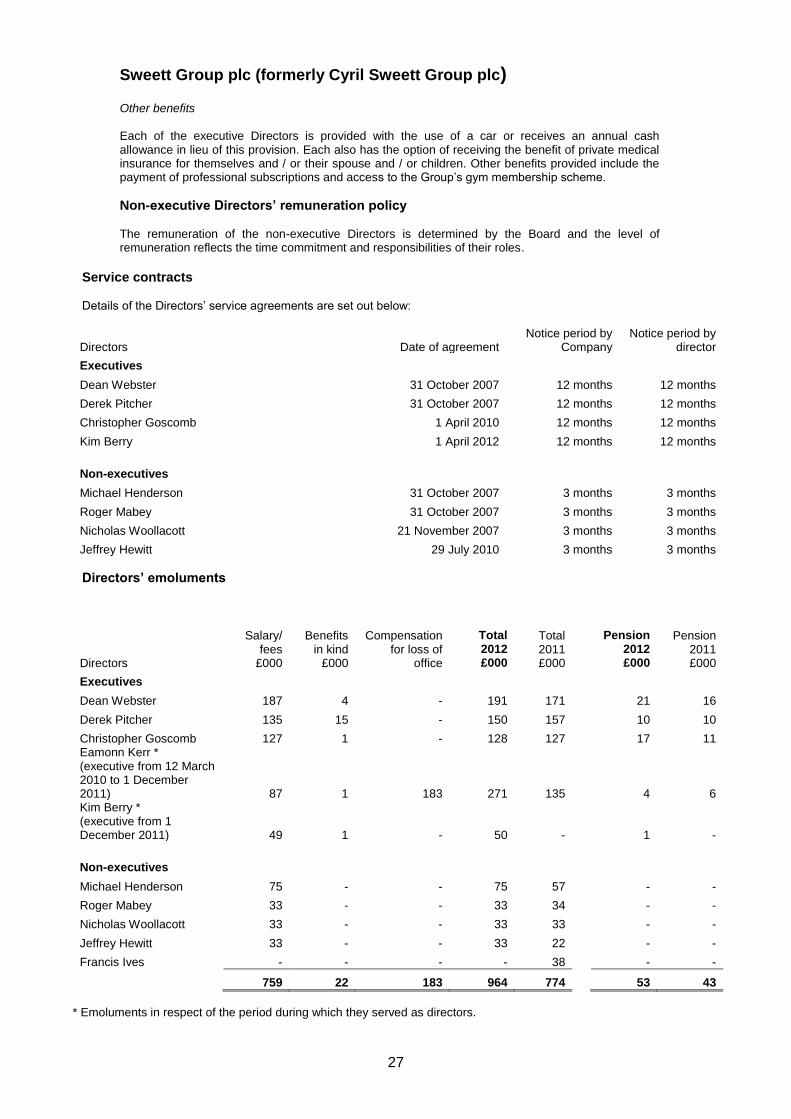

The Board has established a Remuneration Committee which meets at least twice a year and in the past year met 3 times. It reviews the performance of the executive Directors and sets the scale and structure of their remuneration and the basis of their service agreements with due regard to the interest of shareholders. During the year the Committee implemented the PSP approved by shareholders at the last General Meeting. Options were granted to Executive Directors Dean Webster, Derek Pitcher and Chris Goscomb. The PSP was designed by external consultants, with performance conditions that are stretching and promote the long-term success of the Company. Further details on the PSP can be found in the Directors‘ remuneration report on pages 25 to 29.

Relations with shareholders

The Board is committed to a continuing dialogue with its shareholders. The Chairman ensures that the views of shareholders are communicated to the Board as a whole.

Sweett Group plc (formerly Cyril Sweett Group plc)

22

Following the announcement and presentation of the interim and year end results, there is a series of formal meetings with institutional shareholders. These meetings enable the executive Directors to appraise the investors of the Group‘s business and future plans and the shareholders can communicate any concerns they may have. The Group‘s brokers and financial PR advisors provide feedback from the shareholder and analyst meetings and present the results to the Board. The Group‘s investor relations section on its website contains information on the Group‘s financial results and its stock exchange announcements. Additionally, the AGM provides a useful interface with shareholders. All shareholders are invited to attend the AGM and all members of the Board will be available at the meeting to answer questions. Full Interim and Annual Reports are made available to all shareholders. For and on behalf of the Board Danielle Pass Company Secretary 3 September 2012

Sweett Group plc (formerly Cyril Sweett Group plc)

23

Risk management and principal risks and uncertainties

Risk management

Risk management involves identifying the principal risks relating to the Group and its business objectives, establishing appropriate controls to manage those risks and ensuring that associated monitoring and reporting systems are in place. The Group‘s risk management process balances the cost of mitigation or elimination against the perceived risk exposure and is consistent with the prudent management of a diverse professional organisation. As with internal controls, risk and its management vary in some of our international operations for reasons of scale and, for companies acquired, in the immediate post-acquisition period. The Group is exposed to a range of risks and uncertainties, the principal ones of which are:

Market conditions

Changes in the prevailing general market conditions present a risk to operations, in particular because construction spend can vary significantly depending on the economic outlook. Some of the market sectors in which the Group operates are funded and regulated by government bodies. These sectors are subject to changes in government policy, spending, regulation and procurement practices. The Group is also at risk, particularly in developed markets from continuing static or reducing spend in the private sector, which is a function of changing demand patterns and lack of funding availability. Further, there is a risk posed by the ongoing global financial crisis, recently exacerbated by instability in the Euro zone.

We mitigate these risks by continuing to diversify across a broad spectrum of sectors and geographies, regularly monitoring public sector spending patterns and ensuring that our resource levels are aligned to market activity with key employees retained within the business.

Growth and integration

The Group‘s policy is to spread its risks by developing overseas. This brings its own risks in terms of control of the targets and their integration into the Group, its systems and business practices.

These risks are mitigated by thorough due diligence reviews of potential targets, particularly of their finances and human resources, by internal and external means and also through a prompt and structured introduction of the Group‘s policies, procedures, standards and management control systems.

Financial

Financial risks are inherent in the Group‘s business, mainly in respect of liquidity and covenant compliance, which could affect considerations of going concern as highlighted in Note 1 to the financial statements, foreign currency, interest rates, credit and capital. The Board reviews and agrees policies for managing each of these risks and they are summarised at Note 28 to the financial statements. The principal foreign exchange exposures in the group relate to net assets in overseas subsidiary undertakings and cross-border inter-company loans from the UK. The bulk of the latter were capitalised during the year. The Australian dollar exposure continues to be hedged. It is the Group‘s policy that no speculative trading in financial instruments shall be undertaken.

Systems and IT

In common with most businesses, the Group is dependent on its operational and IT systems and their reliability for the protection of its intellectual capital, service delivery and the availability of timely management information. There is a latent risk of downtime, data loss, insufficient capacity and disparity in the manner in which the core systems are operated. Management is mitigating these risks by moving all of the Group‘s businesses onto a common ERP system with consistent operating criteria, infrastructure, back-up and disaster recovery. Work to fully integrate recent overseas acquisitions into the standard Group IT infrastructure configuration continues as well as constant review and upgrade of local processing and data transfer capacity.

Sweett Group plc (formerly Cyril Sweett Group plc)

24

Reputation

The Board considers reputational risk to be one of the most significant risks in a professional service organisation. Our reputation for being able to deliver large projects to a high technical standard is critical to how our clients perceive the business, how we are portrayed in the public arena and thus our ability to secure new commissions. Awareness of the importance of the Group‘s reputation and individual integrity underpins our business ethics and culture. Management mitigates this risk by ensuring that robust cost and project management systems are linked to internal quality processes, which are regularly audited by independent consultants against industry standards. These delivery processes are supported by policies and procedures which reinforce the importance of high ethical standards.

People

The Board is proud of the dedication and commitment of the people who work for the Group and grateful for their continued contribution despite challenging market conditions. The Group aims to provide clients with excellence in service delivery based on trust, continuity and understanding of each client‘s business objectives. Attracting and retaining talented professionals therefore remains a key objective of the Group. To mitigate the risk of staff attrition, the Group maintains a number of staff awards and recognition programmes, a clear, transparent career structure with promotion based on merit and a comprehensive ongoing programme of training and educational support. Staff are regularly updated on progress in the business and invited to put forward their suggestions and opinions for improvements in the overall performance of the business. Individual development needs and career aspirations are discussed as part of the annual performance review and the regular ―one to one‖ processes.

Health, safety and the environment The Group‘s business is concerned with the built environment and this presents risks and impacts in terms of health, safety and the environment. Should the Group‘s policy or practice in this area prove inadequate there is a consequent risk to employees, clients, contractors and third parties. In mitigation, given that the Group takes its health, safety and environmental responsibilities very seriously, policies are in place setting out its approach to these matters. The Group‘s policies are supported by a range of more detailed guidance and documentation, which have now been standardised across the regions of operation and are subject to audit checks. In addition, the company has specialist teams engaged in the delivery of specialist external professional services in both Health & Safety and Sustainability. The experience and knowledge of these teams is drawn upon to inform our own internal processes.

Sweett Group plc (formerly Cyril Sweett Group plc)

25

Directors’ remuneration report

Unaudited information The following disclosures are sufficient to meet the AIM rules requirements.

Remuneration Committee

The Remuneration Committee comprises the non-executive Directors of the Company and is chaired by Roger Mabey.

Executive Directors’ remuneration policy