daily grind case daily grind, inc. (“daily grind”), a public company, manufactures and...

TRANSCRIPT

Daily Grind Case

Daily Grind, Inc. (“Daily Grind”), a public company, manufactures and distributes branded personal organizers for sale in its company-operated retail stores. Daily Grind also sells its products to wholesalers through various royalty and license arrangements.

Daily Grind negotiated a License Agreement with Pacific Paper Products (“Pacific”), a major manufacturer and distributor of office supplies.

Pacific will have the right to distribute Daily Grind products to a specified retail channel in the United States. Based on the current demand for Daily Grind’s products, Pacific believes that inclusion of certain Daily Grind organizers in its product mix will increase the awareness of, and hence the value of, other Pacific products.

As consideration under the terms of the License Agreement, Pacific will pay Daily Grind a license fee of approximately $12 million for the right to use the Daily Grind trademarks for an indefinite term. Termination of the separate Supply and Royalty Agreement (see below) or execution of licensing or distribution agreements with competitors of Daily Grind constitutes a material breach that would cause the License Agreement to terminate.

Daily Grind Case

The License Agreement specifies that the license fee is earned, payable, and contractually non-refundable as of the date of execution of the License Agreement.

Daily Grind and Pacific also entered into a separate Supply and Royalty Agreement. Based on this agreement, Daily Grind will allow Pacific to distribute personal organizers manufactured by Daily Grind to a specified retail channel in the United States. As part of the Supply and Royalty Agreement, Pacific agreed to pay Daily Grind quarterly royalty payments based upon a predetermined royalty schedule. If Daily Grind cannot or does not provide the amount of product Pacific requires under the Supply and Royalty Agreement, Pacific maintains the right to enter into a separate manufacturing contract that would allow Pacific to use certain of Daily Grind’s proprietary production methods.

The sales terms (e.g., price, discounts) under the Supply and Royalty Agreement do not differ from the terms of other arrangements Daily Grind has with third parties to sell its products. The Supply and Royalty Agreement will expire ten years from the date of its execution and will renew automatically for successive ten-year terms thereafter, unless a material breach of contract occurs. Termination of the License Agreement (see above), non-payment of royalties due, or failure to meet sales performance goals would constitute a material breach under the terms of the Supply and Royalty Agreement. An independent party has evaluated the sales performance goals and has deemed them to be substantive.

Daily Grind Case

Daily Grind has experience in both license and royalty arrangements and believes that both the License Agreement and the Supply and Royalty Agreement are priced at their respective fair values. Further supporting their conclusions, Daily Grind plans to engage an independent valuation expert to verify that the terms of the agreements are at fair value.

Required: Is it appropriate for Daily Grind to recognize the $12 million payment from Pacific under the terms of the License Agreement as revenue upon execution of the License Agreement?

Daily Grind Case

An assessment must be made to determine if, in essence, the $12 million nonrefundable fee was to obtain the on-going right to obtain and sell Daily Grind’s products or if Pacific places a separate value on the License Agreement.

With regard to loan origination fees that are assessed by a creditor for the origination of a loan, paragraph 37 of FASB Statement No. 91, states the following: “The Board concluded that loan origination fees and direct loan origination costs should be accounted for as components of a loan's acquisition cost and recognized as an adjustment to the yield of the related loan. The Board considered and rejected the argument that loan origination is a separate revenue-producing activity and concluded that originating loans is but one means of acquiring a loan.”

Daily Grind Case

SAB No. 101 states, “unless the up-front fee is in exchange for products delivered or services performed that represent the culmination of the earnings process, the deferral of revenue is appropriate.”

Daily Grind Case--Conclusion

1. Given that termination of the License Agreement or the Supply and Royalty Agreement would result in termination of the other corresponding agreement, signing the License Agreement was not a discrete event for which the earnings process had been culminated.

2. Further, as the License Agreement has an indefinite term and the Supply and Royalty Agreement has an initial ten-year term that renews automatically for successive ten-year terms, revenue from the License Agreement should be recognized over the initial contract period (or longer if the relationship with Pacific is expected to extend beyond the initial term and Pacific continues to benefit from the payment of the up-front fee).

Revenue Recognition Over Time

Completed Contract Method

Completed Contract Method

Percentage-of-Completion

Method

Percentage-of-Completion

Method

Long-term Construction

Contracts

Long-term Construction

Contracts

Percentage-of-Completion Method

Cost incurred to dateCost incurred to date

Gross profit estimateGross profit estimate

Measuring Progress Toward Completion

Estimate of project’s total cost

Estimate of project’s total cost

Percentage-of-Completion Method

Total costs incurred to date Percent complete = Most recent estimate of total project cost

Let’s look at an example.

Percentage-of-Completion Method

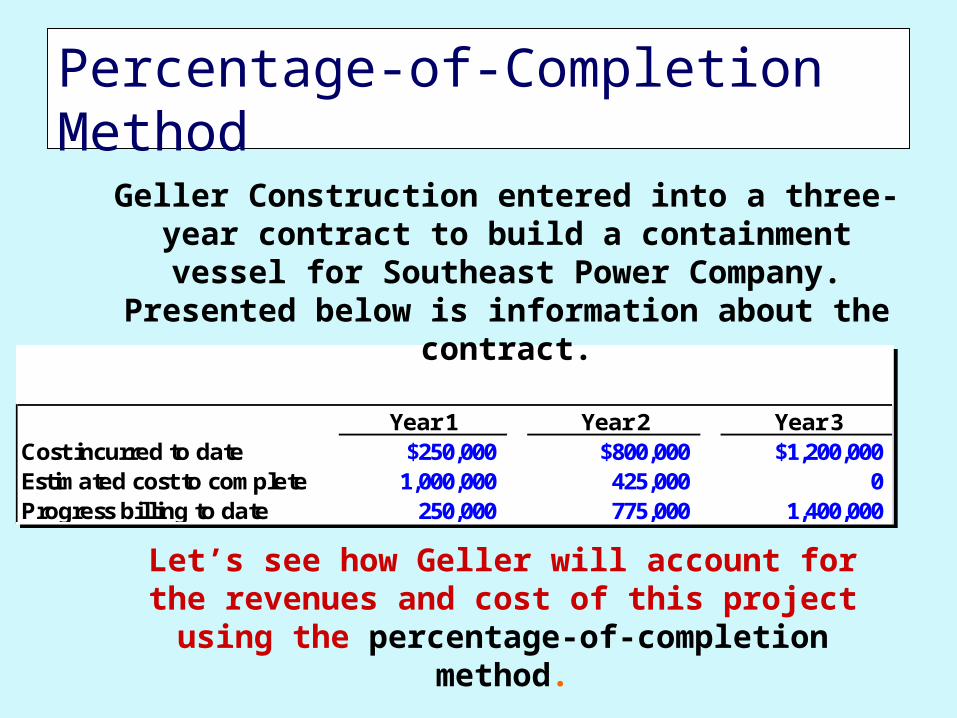

Year 1 Year 2 Year 3Cost incurred to date $250,000 $800,000 $1,200,000Estimated cost to complete 1,000,000 425,000 0Progress billing to date 250,000 775,000 1,400,000

Year 1 Year 2 Year 3Cost incurred to date $250,000 $800,000 $1,200,000Estimated cost to complete 1,000,000 425,000 0Progress billing to date 250,000 775,000 1,400,000

Geller Construction entered into a three-year contract to build a containment vessel for Southeast Power Company. Presented below is information about the contract.

Let’s see how Geller will account for the revenues and cost of this project using the percentage-of-completion

method.

Percentage-of-Completion Method

$250,000 ÷ $1,250,000 = 20%$250,000 ÷ $1,250,000 = 20%

Percentage-of-Completion Method

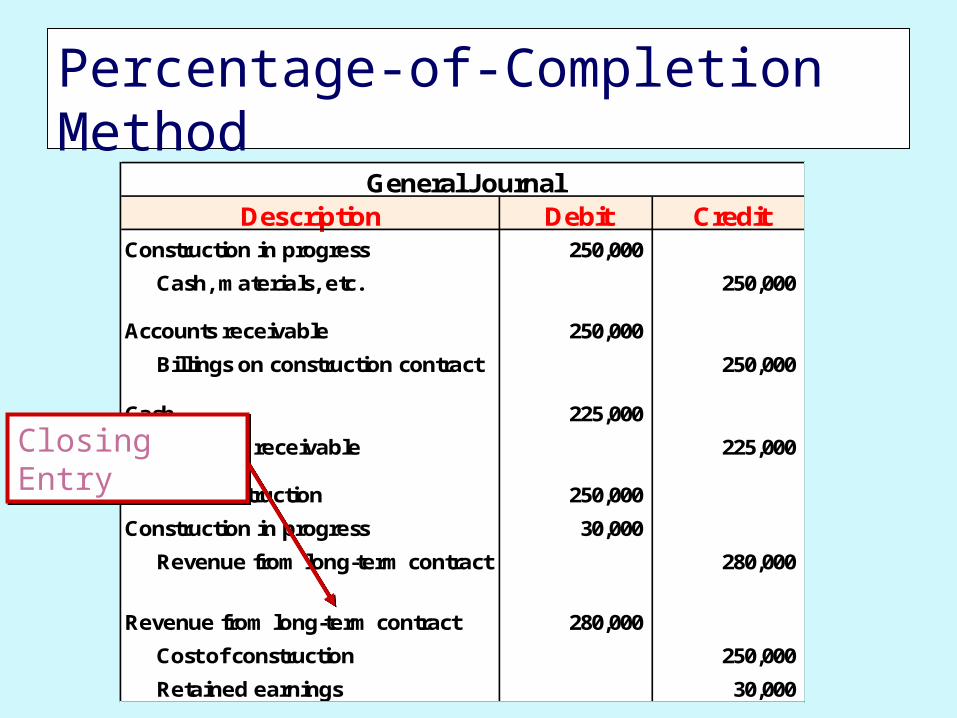

Description Debit CreditConstruction in progress 250,000

Cash, materials, etc. 250,000

Accounts receivable 250,000

Billings on construction contract 250,000

Cash 225,000

Accounts receivable 225,000

General Journal

Percentage-of-Completion Method

Contra account to CIP

Description Debit CreditConstruction in progress 250,000

Cash, materials, etc. 250,000

Accounts receivable 250,000

Billings on construction contract 250,000

Cash 225,000

Accounts receivable 225,000

General Journal

Percentage-of-Completion Method

Construction in Progress

- Billings on Construction ContractDebit Balance (Unbilled Receivable)

Classified as an asset

Construction in Progress

- Billings on Construction ContractCredit Balance (Overbilled Receivable)

Classified as a liability

Description Debit CreditConstruction in progress 250,000

Cash, materials, etc. 250,000

Accounts receivable 250,000

Billings on construction contract 250,000

Cash 225,000

Accounts receivable 225,000

Cost of construction 250,000

Construction in progress 30,000

Revenue from long-term contract 280,000

General Journal

Percentage-of-Completion Method

Percentage-of-Completion Method

Description Debit CreditConstruction in progress 250,000

Cash, materials, etc. 250,000

Accounts receivable 250,000

Billings on construction contract 250,000

Cash 225,000

Accounts receivable 225,000

Cost of construction 250,000

Construction in progress 30,000

Revenue from long-term contract 280,000

Revenue from long-term contract 280,000

Cost of construction 250,000

Retained earnings 30,000

General Journal

Closing EntryClosing Entry

Percentage-of-Completion Method

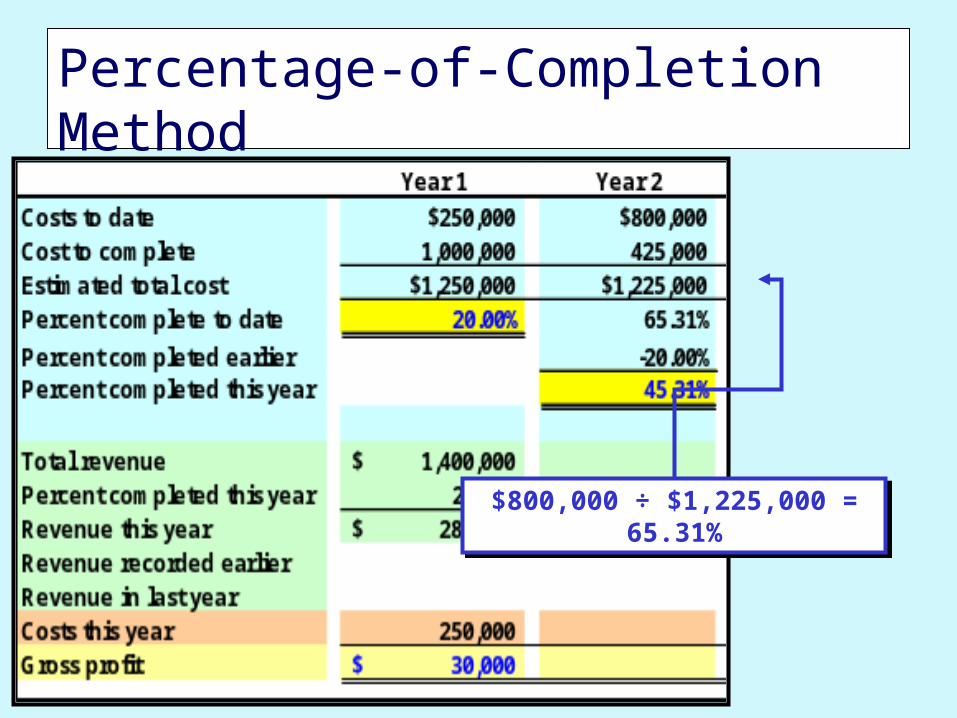

$800,000 ÷ $1,225,000 = 65.31%$800,000 ÷ $1,225,000 = 65.31%

Percentage-of-Completion Method

Description Debit CreditConstruction in progress 550,000

Cash, materials, etc. 550,000

General Journal

Percentage-of-Completion Method

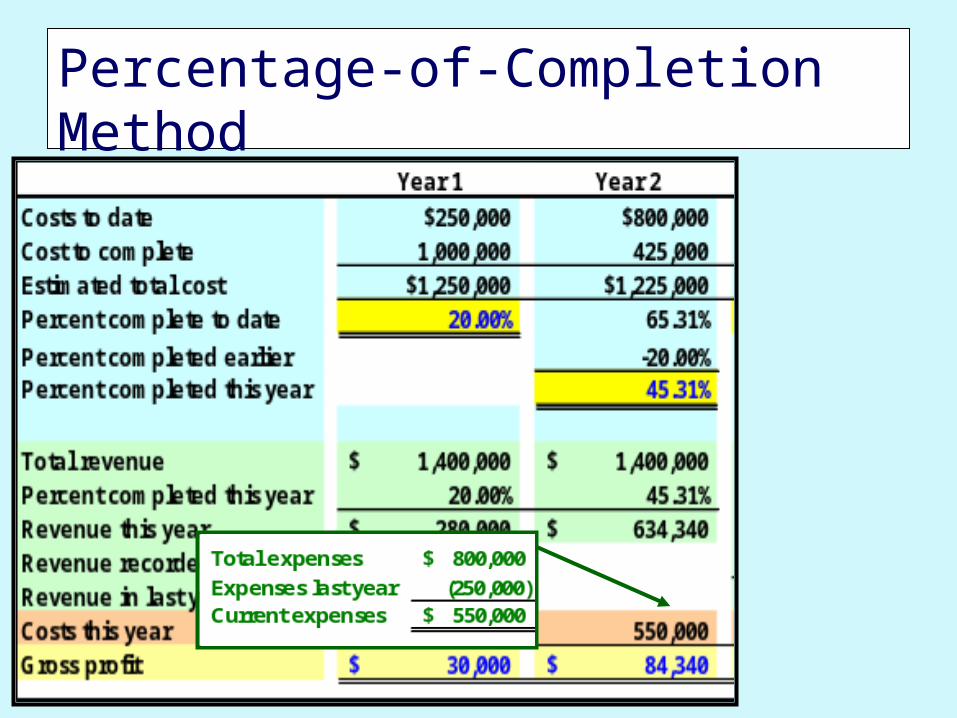

$800,000 - $250,000 last year = $550,000

Description Debit CreditConstruction in progress 550,000

Cash, materials, etc. 550,000

Accounts receivable 525,000

Billings on construction contract 525,000

General Journal

Percentage-of-Completion Method

$775,000 - $250,000 last year = $525,000

Description Debit CreditConstruction in progress 550,000

Cash, materials, etc. 550,000

Accounts receivable 525,000

Billings on construction contract 525,000

Cash 470,000

Accounts receivable 470,000

General Journal

Percentage-of-Completion Method

$695,000 - $225,000 last year = $470,000

Description Debit CreditConstruction in progress 550,000

Cash, materials, etc. 550,000

Accounts receivable 525,000

Billings on construction contract 525,000

Cash 470,000

Accounts receivable 470,000

Cost of construction 550,000

Construction in progress 84,340

Revenue from long-term contract 634,340

General Journal

Percentage-of-Completion Method

Percentage-of-Completion Method

Description Debit CreditConstruction in progress 550,000

Cash, materials, etc. 550,000

Accounts receivable 525,000

Billings on construction contract 525,000

Cash 470,000

Accounts receivable 470,000

Cost of construction 550,000

Construction in progress 84,340

Revenue from long-term contract 634,340

Revenue from long-term contract 634,340

Cost of construction 550,000

Retained earnings 84,340

General Journal

Closing EntryClosing Entry

Percentage-of-Completion Method

Year 1 Year 2 Year 3Costs to date $250,000 $800,000 $1,200,000Cost to complete 1,000,000 425,000 0Estimated total cost $1,250,000 $1,225,000 $1,200,000Percent complete to date 20.00% 65.31% 100.00%

Percent completed earlier -20.00%Percent completed this year 45.31%

Total revenue 1,400,000$ 1,400,000$ Percent completed this year 20.00% 45.31%Revenue this year 280,000$ 634,340$ Revenue recorded earlierRevenue in last yearCosts this year 250,000 550,000 Gross profit 30,000$ 84,340$

Percentage-of-Completion Method

Year 1 Year 2 Year 3Costs to date $250,000 $800,000 $1,200,000Cost to complete 1,000,000 425,000 0Estimated total cost $1,250,000 $1,225,000 $1,200,000Percent complete to date 20.00% 65.31% 100.00%

Percent completed earlier -20.00%Percent completed this year 45.31%

Total revenue 1,400,000$ 1,400,000$ 1,400,000$ Percent completed this year 20.00% 45.31%Revenue this year 280,000$ 634,340$ Revenue recorded earlier 914,340 Revenue in last year 485,660$ Costs this year 250,000 550,000 400,000 Gross profit 30,000$ 84,340$ 85,660$

Percentage-of-Completion Method

Description Debit CreditConstruction in progress 400,000

Cash, materials, etc. 400,000

Accounts receivable 625,000

Billings on construction contract 625,000

Cash 405,000

Accounts receivable 405,000

Cost of construction 400,000

Construction in progress 85,660

Revenue from long-term contract 485,660

Revenue from long-term contract 485,660

Cost of construction 400,000

Retained earnings 85,660

General Journal

Percentage-of-Completion Method

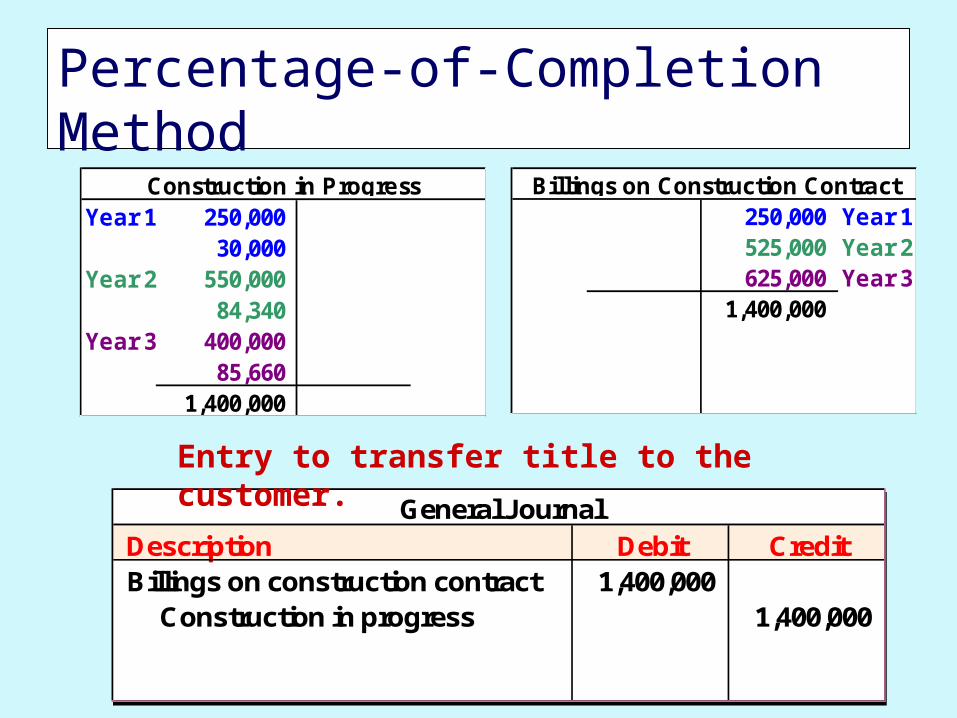

Description Debit CreditBillings on construction contract 1,400,000 Construction in progress 1,400,000

General JournalDescription Debit CreditBillings on construction contract 1,400,000 Construction in progress 1,400,000

General Journal

Entry to transfer title to the customer.

Year 1 250,000 30,000

Year 2 550,000 84,340

Year 3 400,000 85,660

1,400,000

Construction in Progress250,000 Year 1525,000 Year 2625,000 Year 3

1,400,000

Billings on Construction Contract

A Thought Exercise E5-11

A Thought Exercise E5-11

Requirement 1Construction in progress = Costs

incurred + Profit recognized $100,000 = ? + $20,000

Actual costs incurred in 2003 = $80,000

A Thought Exercise E5-11

Requirement 2Billings = Cash collections + Acc. Rec.$94,000 = ? + $30,000

Cash collections in 2003 = $64,000

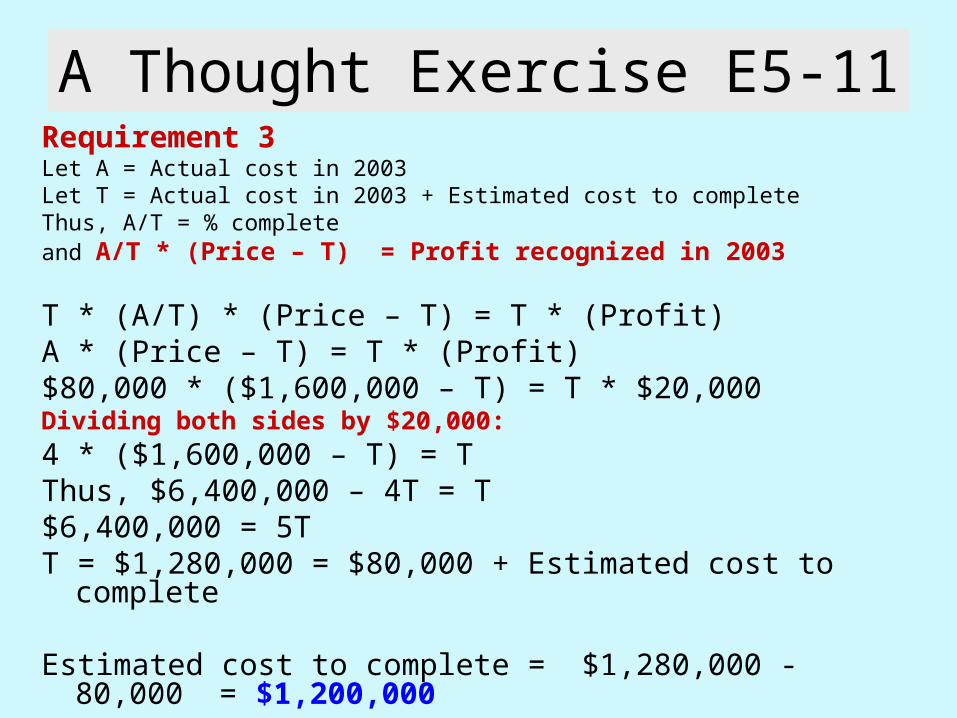

A Thought Exercise E5-11Requirement 3Let A = Actual cost in 2003Let T = Actual cost in 2003 + Estimated cost to completeThus, A/T = % complete and A/T * (Price – T) = Profit recognized in 2003

T * (A/T) * (Price – T) = T * (Profit)A * (Price – T) = T * (Profit)$80,000 * ($1,600,000 – T) = T * $20,000Dividing both sides by $20,000:4 * ($1,600,000 – T) = TThus, $6,400,000 – 4T = T$6,400,000 = 5TT = $1,280,000 = $80,000 + Estimated cost to

complete

Estimated cost to complete = $1,280,000 - 80,000 = $1,200,000

A Thought Exercise E5-11

Requirement 4

$80,000 = X * $1,280,000

X = 6.25%

Completed Contract Method

Year 1 Year 2 Year 3Cost incurred to date $250,000 $800,000 $1,200,000Estimated cost to complete 1,000,000 425,000 0Progress billing to date 250,000 775,000 1,400,000Cash collections to date 225,000 695,000 1,100,000Contract price $1,400,000

Year 1 Year 2 Year 3Cost incurred to date $250,000 $800,000 $1,200,000Estimated cost to complete 1,000,000 425,000 0Progress billing to date 250,000 775,000 1,400,000Cash collections to date 225,000 695,000 1,100,000Contract price $1,400,000

Geller Construction entered into a three-year contract to build a containment vessel for Southeast Power Company. Presented below is information about the contract.

Let’s see how Geller will account for the revenues and cost of this project

using the completed contract method.

Description Debit CreditConstruction in progress 250,000

Cash, materials, etc. 250,000

Accounts receivable 250,000

Billings on construction contract 250,000

Cash 225,000

Accounts receivable 225,000

General Journal

Completed Contract Method

Entries are identical to the entries for

percentage of completion.

Gross profit is

not recognized

until project is complete.

Description Debit CreditConstruction in progress 550,000

Cash, materials, etc. 550,000

Accounts receivable 525,000

Billings on construction contract 525,000

Cash 470,000

Accounts receivable 470,000

General Journal

Completed Contract Method

Entries are identical to the

entries for percentage of completion.

Gross profit is

not recognized

until project is complete.

Completed Contract Method

Description Debit CreditConstruction in progress 400,000

Cash, materials, etc. 400,000

Accounts receivable 625,000

Billings on construction contract 625,000

Cash 405,000

Accounts receivable 405,000

Cost of construction 1,200,000

Construction in progress 200,000

Revenue from long-term contract 1,400,000

Revenue from long-term contract 1,400,000

Cost of construction 1,200,000

Retained earnings 200,000

General JournalGross

profit is recognized in year 3

since project is complete.

Completed Contract Method

Description Debit CreditBillings on construction contract 1,400,000 Construction in progress 1,400,000

General JournalDescription Debit CreditBillings on construction contract 1,400,000 Construction in progress 1,400,000

General Journal

Entry to transfer title to the customer.

Year 1 250,000 Year 2 550,000 Year 3 400,000 Year 3 200,000

1,400,000

Construction in Progress250,000 Year 1525,000 Year 2625,000 Year 3

1,400,000

Billings on Construction Contract

Significant Uncertainty of Collectibility

1. Installment Sales Method

2. Cost Recovery

1. Installment Sales Method

2. Cost Recovery

When uncertainties about collectibility exist, revenue

recognition is delayed.

When uncertainties about collectibility exist, revenue

recognition is delayed.

Sale and cost of sale recorded as usual.

Compute gross margin rate on the installment sales.

Recognize gross margin as cash is received.

Gross margin not realized is deferred until a future period.

Installment Sales Method

2003 2004 2005Installment sales $200,000 $250,000 $275,000Cost of sales 155,000 190,000 220,000Gross profit $45,000 $60,000 $55,000

Gross profit percentage 22.50% 24.00% 20.00%

Installment Sales Method

Clarke, Inc. had the following installment sales in addition to its regular sales.

$45,000 ÷ $200,000 = 22.50%$45,000 ÷ $200,000 = 22.50%

Installment Sales Method

2003 2004 2005Installment sales $200,000 $250,000 $275,000Cost of sales 155,000 190,000 220,000Gross profit $45,000 $60,000 $55,000

Gross profit percentage 22.50% 24.00% 20.00%

Clarke, Inc. had the following installment sales in addition to its regular sales.

2003 2004 2005Installment sales 200,000$ 250,000$ 275,000$ Cash Collected:From 2003 Sales (100,000) (50,000) (50,000) From 2004 Sales (195,000) (25,000) From 2005 Sales (200,000)

Cash Collections At Dec. 31, 2005, Clarke, Inc. is still

owed $30,000 from the 2004

sales and $75,000 from the 2005

sales.

Installment Sales Method

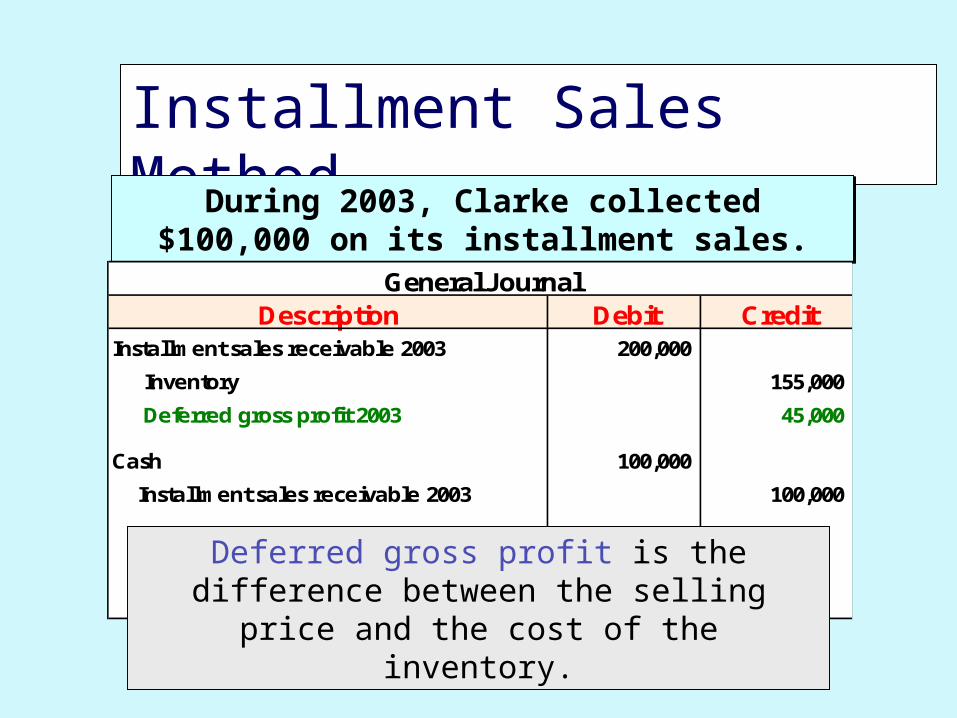

During 2003, Clarke collected $100,000 on its installment sales.

During 2003, Clarke collected $100,000 on its installment sales.

Description Debit CreditInstallment sales receivable 2003 200,000

Inventory 155,000

Deferred gross profit 2003 45,000

Cash 100,000

Installment sales receivable 2003 100,000

General Journal

Deferred gross profit is the difference between the selling price and the cost of

the inventory.

Installment Sales Method

Description Debit CreditInstallment sales receivable 2003 200,000

Inventory 155,000

Deferred gross profit 2003 45,000

Cash 100,000

Installment sales receivable 2003 100,000

Deferred gross profit 2003 22,500

Realized gross profit 22,500

($100,000 collected x 22.50%)

General Journal

This entry records the Realized Gross Profit by adjusting the Deferred Gross

Profit account.

Installment Sales Method Deferred gross profit 2004

Cash 245,000

Installment sales receivable 2003

Installment sales receivable 2004

Deferred gross profit 2003 11,250

Deferred gross profit 2004 46,800

Realized gross profit

During 2004, Clarke collected $50,000 on its 2003 installment sales and $195,000 on its 2004 installment sales.

During 2004, Clarke collected $50,000 on its 2003 installment sales and $195,000 on its 2004 installment sales.

Installment Sales Method Deferred gross profit 2004 60,000

Cash 245,000

Installment sales receivable 2003 50,000

Installment sales receivable 2004 195,000

Deferred gross profit 2003 11,250

Deferred gross profit 2004 46,800

Realized gross profit 58,050

During 2004, Clarke collected $50,000 on its 2003 installment sales and $195,000 on its 2004 installment sales.

During 2004, Clarke collected $50,000 on its 2003 installment sales and $195,000 on its 2004 installment sales.

Cash collections - 2004 195,000 24.00% 46,800 58,050$

Cash collections - 2004 195,000 24.00% 46,800 58,050$

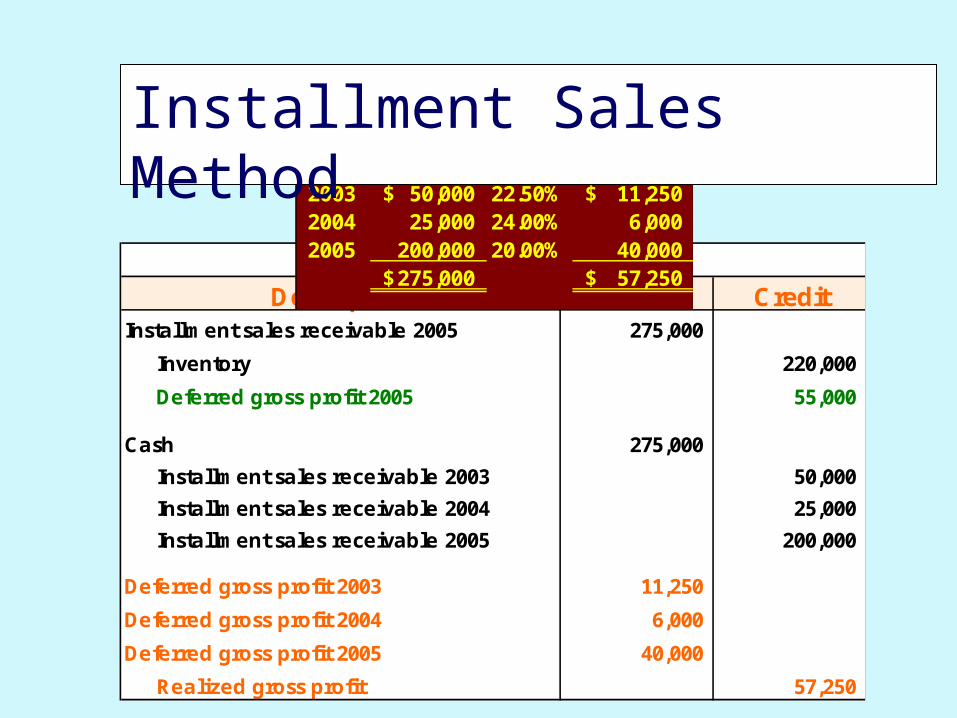

Description Debit CreditInstallment sales receivable 2005 275,000

Inventory 220,000

Deferred gross profit 2005 55,000

Cash 275,000

Installment sales receivable 2003 50,000

Installment sales receivable 2004 25,000

Installment sales receivable 2005 200,000

Deferred gross profit 2003 11,250

Deferred gross profit 2004 6,000

Deferred gross profit 2005 40,000

Realized gross profit 57,250

General Journal

Cash Collection on Installment Sales in 2005

2003 50,000$ 22.50% 11,250$ 2004 25,000 24.00% 6,000 2005 200,000 20.00% 40,000

275,000$ 57,250$

Installment Sales Method

Installment Sales Method

Installment Sales MethodBalance Sheet

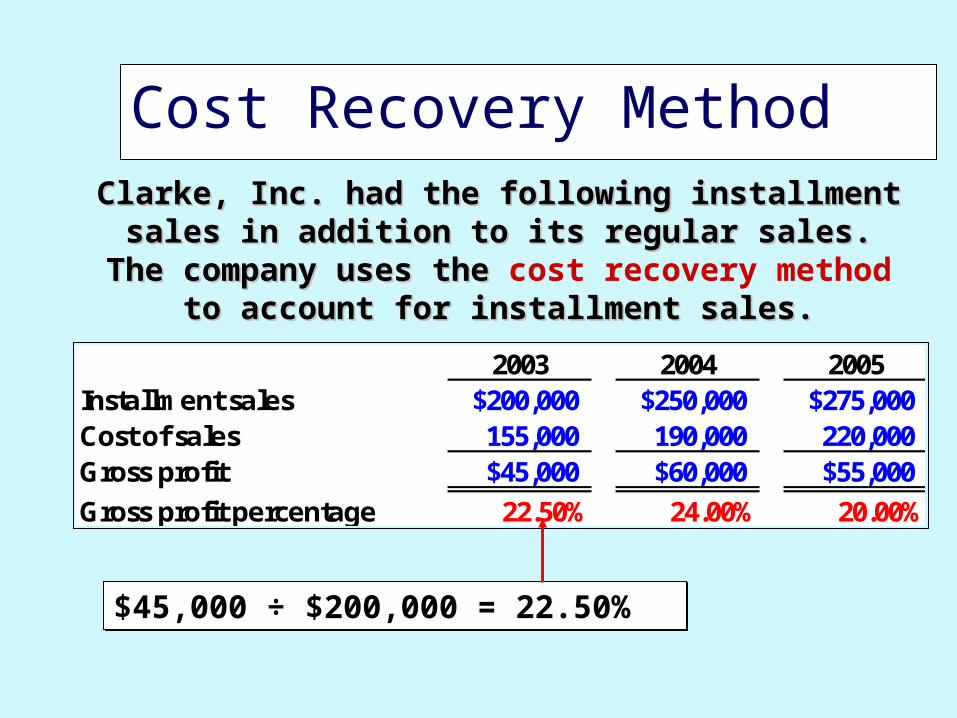

Cost Recovery Method

2003 2004 2005Installment sales $200,000 $250,000 $275,000Cost of sales 155,000 190,000 220,000Gross profit $45,000 $60,000 $55,000

Gross profit percentage 22.50% 24.00% 20.00%

Clarke, Inc. had the following installment Clarke, Inc. had the following installment sales in addition to its regular sales. The sales in addition to its regular sales. The

company uses the company uses the cost recovery method to to account for installment sales.account for installment sales.

$45,000 ÷ $200,000 = 22.50%$45,000 ÷ $200,000 = 22.50%

Cost Recovery Method

The following schedule shows the pattern of cash collections for the three year period.

Year of Sale 2003 2004 20052003 $100,000 $50,000 $50,0002004 195,000 25,0002005 200,000

COGS 155,000$ 190,000$ 220,000$

Year of CollectionYear of Sale 2003 2004 2005

2003 $100,000 $50,000 $50,0002004 195,000 25,0002005 200,000

COGS 155,000$ 190,000$ 220,000$

Year of Collection

Under the cost recovery method profit is not recognized until the

seller has recovered all of the cost of the goods sold.

Cost Recovery Method

Description Debit CreditInstallment receivable 2003 200,000

Inventory 155,000

Deferred gross profit 2003 45,000

Cash 100,000

Installment receivable 2003 100,000

General Journal

The entries are exactly the same as under the Installment Method—EXCEPT that there is not an entry to realize gross profit. Since we have not

collected cash in excess of COGS, no gross profit is recognized in 2003.

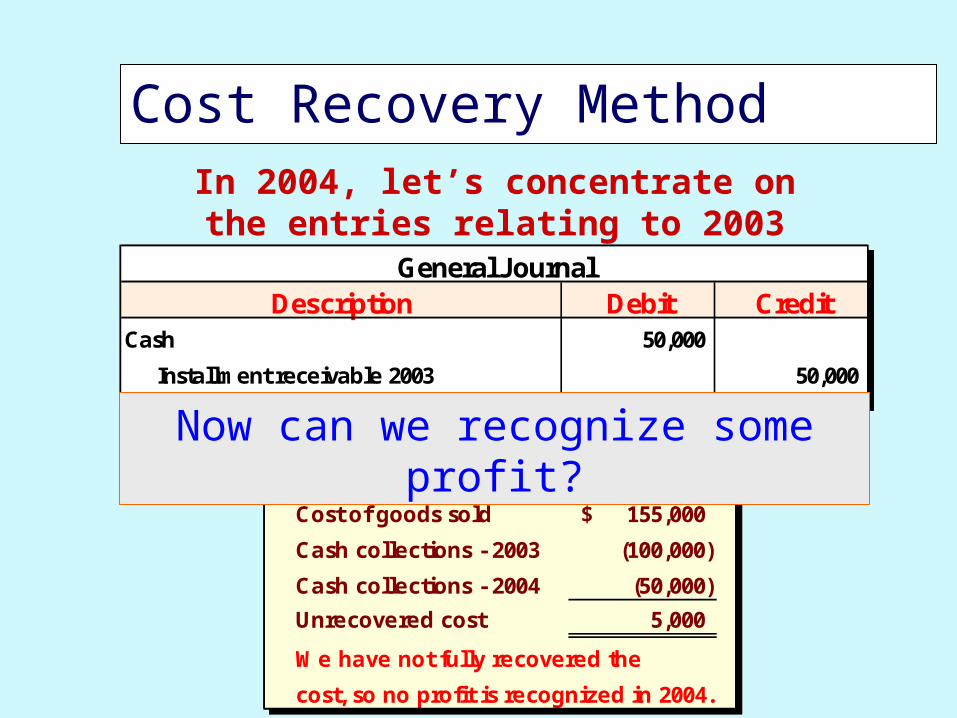

Cost Recovery MethodIn 2004, let’s concentrate on the

entries relating to 2003 sales only.

Description Debit CreditCash 50,000

Installment receivable 2003 50,000

General JournalDescription Debit Credit

Cash 50,000

Installment receivable 2003 50,000

General Journal

2003

Cost of goods sold 155,000$

Cash collections - 2003 (100,000)

Cash collections - 2004 (50,000)

Unrecovered cost 5,000

We have not fully recovered the

cost, so no profit is recognized in 2004.

2003

Cost of goods sold 155,000$

Cash collections - 2003 (100,000)

Cash collections - 2004 (50,000)

Unrecovered cost 5,000

We have not fully recovered the

cost, so no profit is recognized in 2004.

Now can we recognize some profit?

Cost Recovery MethodHere are the entries we would make in

2005 relating to 2003 sales.

Description Debit CreditCash 50,000

Installment receivable 2003 50,000

Deferred gross profit 45,000

Realized gross profit 45,000

General Journal

We have fully recovered the $155,000 cost during 2005, so the entire deferred gross

profit will be recognized.