dangote sugar h1 2015 presentation

TRANSCRIPT

Dangote Sugar Refinery Plc

Investor Presentation

Unaudited Results for the six-months ended 30-06-2015

4 August 2015

Disclaimer

This presentation contains forward looking statements which revealManagement’s recent views and estimates. The forward looking statementscontain certain risks and uncertainties that could cause actual results to varymaterially from those contained in the forward looking statements. Potentialrisks and uncertainties include factors such as general economic conditions,foreign exchange fluctuations, pricing pressures and regulatory developments.

2

Overview of Operations

Apapa Refinery

• Located at the Apapa Wharf in Lagos with a dedicated jetty that berths 40,000MT shipments of raw sugar from Brazil

• Produces quality sugar to customer specification making it the refinery of choice for Nigeria’s leading industrial companies

• Refinery is powered efficiently with gas and/or LPFO (back up) with 16MW of in house generating capacity

• Refining operations supported with strategically located warehouses and 450 trucks for efficient distribution

Savannah Sugar

• Located on 32,000ha of land in Numan, Adamawa State, with annual production capacity of 50,000MT factory

• Over 6,750 ha of land currently under cane, still undergoing rehabilitation and expansion

• Expansion project to increase sugar production to 260,000 MT of refined sugar p.a. on 25,000ha of cultivated land

• Land development & planting to continue over the next 2-3 years

• 700 full time staff and 4800 seasonal workers currently

3

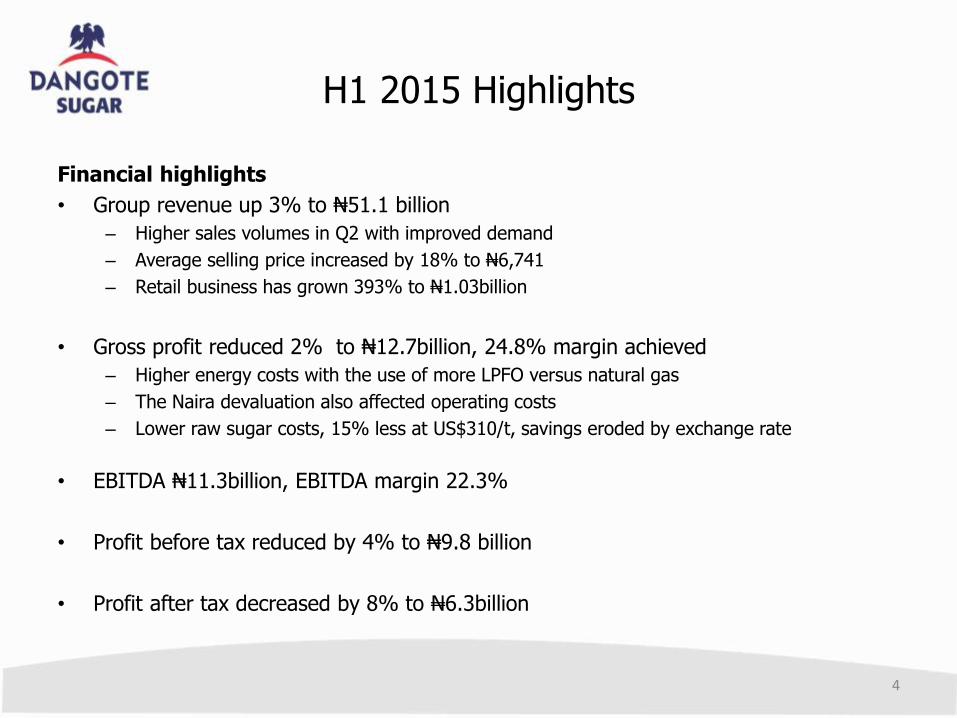

H1 2015 Highlights

Financial highlights

• Group revenue up 3% to ₦51.1 billion

– Higher sales volumes in Q2 with improved demand

– Average selling price increased by 18% to N6,741

– Retail business has grown 393% to N1.03billion

• Gross profit reduced 2% to ₦12.7billion, 24.8% margin achieved

– Higher energy costs with the use of more LPFO versus natural gas

– The Naira devaluation also affected operating costs

– Lower raw sugar costs, 15% less at US$310/t, savings eroded by exchange rate

• EBITDA ₦11.3billion, EBITDA margin 22.3%

• Profit before tax reduced by 4% to ₦9.8 billion

• Profit after tax decreased by 8% to N6.3billion

4

H1 2015 HighlightsOperating highlights

• Demand increase in the second quarter compared to Q1 2015

– Group Sugar sales volume for the period 368,026 tonnes

– Sales in Q2 up 12% to 195,322 tonnes

• Refinery production at Apapa 361,083 tonnes (2014: 417,362)

– Production at Apapa constrained due to traffic grid lock in the Apapa area

– Despite increasing demand, trucks unavailable for delivery

– Escalated by Fuel Crisis

– Disruptions to supply of Natural Gas resulting in higher energy costs with switch to LPFO

• Savannah harvesting season commenced in January 2015

– Better cane quality following new area planted and improved cane husbandry

– 124,723 tonnes harvested (2014: 122,452)

– Sugar production, 6,610 tonnes (2014:6245)

– Harvesting to recommence in October/November 2015 after the rains

• Technical evaluation and design activities for new projects progressed (Details on slide 10)

• Graham Clark resigns as Group Managing Director, mutual decision with BOD

5

H1 2015 Highlights

30-06-2015 30-06-2014 % change

Refined Sugar Produced (MT) 367,693 423,608 -13.2%

Refined Sugar Sold (MT) 368,026 420,862 -12.6%

Average C&F Raw Sugar/MT ($) 310 365 -15%

Average Price per 50kg bag (N) 6,741 5,685 18%

N’000,000 N’000,000

Revenue 51,120 49,601 3%

Gross Profit 5,464 7,187 -2%

Gross margin (%) 24.8% 26.1%

EBITDA 11,384 11,063 3%

EBITDA margin (%) 22.3% 22.3%

PBT 9,802 10,263 -4%

PAT 6,312 6,835 -8%

EPS 105 114 -8%

6

H1 2015 Highlights

30-06-2015N’000,000

30-06-2014N’000,000

Non-Current Assets 56,047 42,892

Current Assets 44,386 45,919

Total Assets 100,433 88,812

Total Equity 52,925 46,839

Long-Term Debts - 312

Non-Current Liabilities 4,611 6,382

Total Liabilities 47,508 41,972

Total Equity and Liabilities 100,433 88,812

7

Sugar for NigeriaThe Dangote Sugar Master Plan

5 large sugar factories

150,000 Ha of land under cultivation

1.5 million MT of refined sugar from cane p.a.

Production cost at around 16USc/lb

130 million litres of ethanol potential across all sites

Animal feed and surplus power generation capacity to be sourced from cane fiber

Generate over 100,000 jobs

8

10 year Target

Sugar for NigeriaThe Dangote Sugar Master Plan

Phase 1: Year 1 – Year 5

Site Type of Development Acreage (Ha) Refined Sugar (mt) State

Savannah Rehabilitate and Expand 25,000 260,000 Adamawa

Lau / Tau Greenfield 23,000 250,000 Taraba

Hadejia Greenfield 21,500 235,000 Jigawa

Total 69,500 745,000

Phase 2: Year 6 – Year 10

Site Type of Development Acreage (Ha) Refined Sugar (mt) State

Zaria Greenfield 60,000 660,000 Kebbi

Kpada Greenfield 36,000 396,000 Kwara / Kogi

Total 96,000 1,056,000

9

Sugar for NigeriaProjects Update

Savannah Sugar

• Agricultural and factory rehabilitation ongoing

• A further 1,500ha redeveloped in Q1 2015

• Plant, equipment and field machinery deployed

• Redevelopment area to increase to 2,735ha in 2015

• Progress rapidly to produce target of 260,000 ha per annum

Lau/Tau

• Commenced site evaluation and technical design work

• Soil and topographic surveys concluded

• Verification of irrigation water availability underway

• Environmental and social impact assessment in progress

• Concluded development timetable

• Seed cane nursery established

Hadejia

• Commenced site evaluation and technical design work

• Environmental and social impact assessment in progress

• Concluded development timetable

Kebbi• Site evaluation and technical analysis underway• Site approval obtained• Soil and topographical surveys concluded• Finalising Land acquisition

Kwara• Site evaluation and technical analysis underway• Site approval obtained• Soil and topographical surveys concluded• Finalising Land acquisition

Kogi• Site evaluation and technical analysis underway• Site approval obtained• Soil and topographical surveys concluded• Finalising Land acquisition

10

Phase 1 Phase 2

Sugar from CaneValue Chain

11

From 1 hectare of land, we will produce…

Timelines to production at full capacity

1•Develop Seed Cane Area Begin factory design

2•Plant out seed cane and develop additional seed cane area Begin factory construction

3•Plant out largest area for harvesting Complete factory construction

4•Crushing and final planting Commission factory

5•Full area planted and crushed Produce at full capacity

Year Agriculture Industrial Complex

Sugar Cane

1tonne

130KwH Power

Mill Mud0.03tonne

Bagasse0.3tonne

Raw Sugar Juice

0.7tonne

Clarified Sugar Juice0.5tonne

Molasses0.05tonne

Sugar Crystals0.1tonne

11.25lEthanol

Animal Feed

20% sugar in juice

Outlook

Outlook for 2015 has improved as market conditions turn more positive

• Activity following peaceful elections and transition to new Government May 29

• Continued pressure for the Naira devaluation, offset by lower raw sugar prices

• Raw sugar prices expected to remain volatile but remain around 2014 levels

• Increased harvest to refined sugar from Savannah Sugar

• Continue to implement Phase 1 of the “Sugar for Nigeria” project

12

Investor Relations

For further information:

Ayeesha Aliyu

Investor Relations Lead

Dangote Industries Limited

+234 1 448 0815

www.Dangote.com

13