data analysis and interpretation -...

TRANSCRIPT

Chapter-5: Data Analysis and Interpretation

112 | P a g e

DATA ANALYSIS AND INTERPRETATION

The previous chapter reviewed the growth structure of Retail Banking in India and

found that various products like Home loans, Consumer loan, Educational loan, Retail

deposits, ATMs facilities etc. have been expanding at an appreciable rate in India. It

discussed the working of retail banking in India and provided an insight into the

management of various retail products both in public sector banks and private sector

banks. A clear picture of the performance of public sector banks and private sector

banks in recent years came to fore highlighting that retail banking in private sector

banks grows at a faster rate than in public sector banks.

The present chapter analyses the data and, with the application of statistical

tools, interprets the facts and figures to test the set hypotheses in order to derive

logical inferences. Since the test of hypotheses involves measurement of the customer

perceptions of Service Quality of retail banking in public and private sector banks,

setting the dimensions of service quality to serve as benchmarks for measurement and

test of hypotheses becomes imperative. Accordingly, the present chapter is split into

two parts. Section-I presents a detailed view of the concept of Service Quality and

also lays down the various dimensions of the SERVQUAL Model applied to survey

and garner data about perceptions of customer satisfaction with retail banking services

in banks of both the sectors-public and private. Section-II on the other hand, is

devoted to the collection of data, its analysis and interpretation as well as to critically

test the hypotheses constructed on the service quality dimensions in retail banking in

India and draw conclusions.

Chapter-5: Data Analysis and Interpretation

113 | P a g e

SECTION-I

Quality of service is an intangible and multi-dimensional feature. Ascertainment of it

requires taking all of its conceivable dimensions into consideration. This section

identifies and delineates the different dimensions of “service quality”. The significant

attributes that can reflect the customer’s perception with regard to service quality in

retail banking are discussed here. An elaborate explanation of each attribute of

Service Quality dimension is also presented in this section.

Prior to proceeding to deal with the dimensions of service quality, a

conceptual discussion of ‘Quality’ and ‘Service’ and the ‘Service Quality’

significance in relation to banks will be pertinent.

A. CONCEPT OF “SERVICE QUALITY”

5.1. Quality

Quality is the foremost key requirement that influences the formation of perception

and level of satisfaction of the customer with regard to any product and service. In

terms of banking growth, quality plays an important role. The basic concept of quality

can be defined as, “meeting to the need of customer”. In most generalized way the

quality term can be defined as “the inclusion of all specified features and

characteristics as defined for product or service and its ability to satisfy the given

needs as per the requirement of user while using it.” Edward Deming (1999) define

Quality as, “A predictable degree of uniformity & dependability to low cost and

suited to the market”

Phillips Crosby (1980) defined quality as, “Quality is conformance to

requirements”.

Chapter-5: Data Analysis and Interpretation

114 | P a g e

Quality is a degree to which a set of inherent characteristics fulfills the requirements.

5.2. Service

Service is a patch up activity to fulfill someone’s need in the market. Service is

something, which can be experienced but cannot be touched or seen. Services offered

by service providers cannot be seen & touched, as they are intangible activities. Some

of the basic and comprehensive definitions of service as given by different authors

are:

1. “A service is any activity or benefit that one party can offer to another which

is essentially intangible and does not result in the ownership of anything.”

---Kotler, Armstrong, Saunders & Wong

2. “Services are the production of essentially intangible benefits and experience,

either alone or as part of a tangible product through some form of exchange,

with the intention of satisfying the needs, wants and desires of the consumers.”

--- C. Bhattachargee

Customer wants to avail different services offered to them by service

providers. Delivered service will become as the quality service if it meets the

customer’s expectation. But customer expectation depends upon the customer

perception, which may differ from person to person.

5.3. Service Quality

Service quality is a critical determinant of competitiveness of establishing and

sustaining satisfying relationships with customers. Service quality by its nature is an

exclusive and abstract concept, which has been defined from different perspective and

orientation. Groonroos (1984) has defined service quality as,” the outcome of an

Chapter-5: Data Analysis and Interpretation

115 | P a g e

evaluation process, where the customers compare their expectations with the services

they have received”.

Persuraman, Zeithaml and Berry (1985) defined service quality as the

customer’s comparison between service expectation and service performance.

Cronin & Taylor (1992) argued that conceptualization of service quality is a

gap between expectations and performance. According to them service quality should

be based on customers attitude towards the service.

Fogli (2006) define service quality as, “a global judgment or attitude relating

to a particular service, the customer’s overall impression of the relative inferiority or

superiority of the organization and its services. Service quality is a cognitive

judgment”.

Service quality is nothing but the difference between the service expectation &

service actually received by the customer. Customer has certain expectation about the

service. If the customers experiences the same service as they expect then this

difference will be zero and we can say that the service quality is very good.

Ostrowski et.al (1993) observed that service quality is a way of thinking about

how to satisfy customers so that they hold positive attitude towards the services they

have received.

5.4. Service Quality in Banks

Service quality is one of the critical success factors that influence the competitiveness

of an organization. A bank can differentiate itself from competitors by providing high

quality service. Service quality is one of the most attractive areas for researches over

the last decade in the retail banking sector. This study investigates the factors that

enable banks to attract and maintain their customers. In India, customers in the

Chapter-5: Data Analysis and Interpretation

116 | P a g e

banking sector are in a strong bargaining position due to the significant growth of

banks. Therefore banks have to provide, service carefully because of the cut throat

competition among the banks. Banks have to improve the service level continuously.

There is no guarantee that what is excellent service today is also applicable for

tomorrow. To survive in the competitive banking industry, banks have to develop new

strategies which will satisfy their customer. That is why in this competitive banking

environment, customer satisfaction is considered as the essence of success. High

customer satisfaction is important in maintaining a loyal customer base. High quality

of service will result in high customer satisfaction and increase customer loyalty.

Customer satisfaction is the outcome of service quality.

Many of the researches on service quality have been in the developed

countries even though service is among the fastest growing sectors in emerging

countries. The bulk of the researches on service quality in banks has been in the

context of US and European banking institution. However with India now at the path

of growth and aiming global integration has become a source of learning for many

other economies.

Banking sector in India has made remarkable progress since independence. It

has undergone a major transformation from class banking to mass banking. The

banking endeavors to provide effective customer service at lowest costs have been

further facilitated through innovation and communication aided by information

technology. IT based services such as automated teller machines (ATM), electronic

fund transfer, anywhere-anytime banking, smart cards, net banking, swift etc are no

longer alien concepts to Indian banking customers. As India continues to move

towards greater economic liberalization, meeting the expectations of the customers in

Chapter-5: Data Analysis and Interpretation

117 | P a g e

all areas relating to customer service has been of prime importance for the banking

sector in India. Global competition has forced Indian bankers to enter the trade-off

between winning new customers and retain old ones.

Issues concerning service quality in Indian Banking sectors have to be studied

extensively, so that they could sustain and grow on the face of stiff competition, by

learning from their counterparts in developed economics like the USA and Europe.

A successful banker must have the ability to anticipate and satisfy customer needs. To

provide faster and more efficient services the Indian banking sector has to realize the

importance of customer care and satisfaction.

Service quality and customer satisfaction are two closely related terms. Service

quality can be assessed in two ways:

1. Is it conforming to standard? and

2. Is it satisfying the customers?

Oliver (1999) states as, “Satisfaction is the consumer’s fulfillment response. It

is a judgment that a product or service feature, or the product or service itself,

provides a pleasurable level of consumption – related fulfillment”. Customer

satisfaction is related with the type of service quality. If the quality of service

provided by the service provider is good then this leads to higher customer

satisfaction.

Service quality management and improvement is the constant endeavor of

service-conscious organizations. Metric application serves as a tool for measuring

service quality and bringing about improvement in areas of deficiency. Large

organization introduce the quality metrics for improving the quality management

processes. They generally collect metrics on several attributes and defects. The

Chapter-5: Data Analysis and Interpretation

118 | P a g e

Metrics help to identify the strong and weak attributes. Improving upon the weak

areas, several organization are able to make their service quality better, efficient and

meeting the customer satisfaction.

B. MEASUREMENT OF SERVICE QUALITY

Measurement of quality of a service can be a very difficult exercise. Unlike

product where there is particular specification such as length, depth, width, weight,

colour etc. a service can have numerous intangibles or qualitative specification. In

addition there is expectation of the customer with regard to the service, which can

vary considerably based on a range of factors such as prior experience, personal needs

and what other people may have told them.

5.5. SERVQUAL

As a way of trying to measure service quality, researchers have developed a

methodology known as SERVQUAL – a perceived service quality questionnaire

survey methodology. SERVQUAL provides a technology for measuring and

managing service quality (SQ) developed by Parsuraman, Zaithaml and Berry in

1985.

Servqual is founded on the view that the customer’s assessment of Service

Quality is paramount. This assessment has been conceptualized as a gap between

what the customers expect by way of SQ from a class of service providers and their

own evaluation of the performance of a particular service provider.

The model is employed as a generic instrument for measuring Service Quality

across different service sectors. It is regarded as the most appropriate tool to measure

and assess service quality in industrial & commercial sectors like banking, telecom,

Chapter-5: Data Analysis and Interpretation

119 | P a g e

hospitals, and healthcare, hotels and fast food chain, travel &tourism, education and

hospitality etc.

Though not devoid of criticism whether the SERVQUAL dimensions for

assessment of service quality are applicable equally well to all sorts of industrial

sectors, yet the instrument has been developed for use in various service settings and

yields results which are most representative of the factual ascertainment of service

quality. Several academic researchers and practitioners worldwide have extensively

adopted the SERVQUAL instrument to measure service quality. Accordingly, the

SERVQUAL Model is being made use of by this study to assess and measure the

Service Quality in retail banking services rendered by public and private sector banks

in India.

C. SERVICE QUALITY DIMENSIONS

SERVQUAL is a multi-dimensional construct. It consists of five most important

dimensions. These dimensions are most representative and eliciting of the customer

satisfaction from the quality of a particular service. The relationship between service

quality and customer satisfaction based on SERVQUAL is depicted in the figure 5.1

below

Chapter-5: Data Analysis and Interpretation

120 | P a g e

TANGIBLES

RELIABILITY

RESPONSIVENESS

ASSURANCE

EMPATHY

Service Quality

Dimensions SERVQUAL

Customer Satisfaction in Retail Banking

in India

Fig.5.1. Service Quality Dimensions

The above diagram brings to fore the five components of the SERVQUAL

dimensions. These are Tangibles, Reliability, Responsiveness, Assurance and

Empathy. The perception of customers obtained on these five dimensions would

provide the measure of service quality. A brief description of each of these five

dimensions of SERVQUAL is presented below:

5.6. TANGIBLES

Tangibles refer to the factors which represents the physical features of the bank. They

are important for banking business as tangibles make the indelible first impression

during face to face contact between the customer and the bank. Impressive tangibles

fill the customers with confidence that they are dealing with the bank where their

financial interests are safe and secure. Examples of tangible factors are the use of

cutting –edge technology and equipment, modern amenities and physical facilities for

customers within bank premises, appearance and deportment of bank personnel, and

above all the physical features of bank building and inner layout which presents an

Chapter-5: Data Analysis and Interpretation

121 | P a g e

ambience attractive and appealing to customers. Pamphlets and brochures giving out

important information about product and services offered by bank also make an

important category of tangibles. The elegance and get up of the published material,

the clarity and articulation of information themselves imprint in customers’ mind an

everlasting impression of goodwill and pride to do business with such an standard

banking organization.

Thus, tangibles are always appealing in the banking sector. They form an

important dimension in the perception of customers with regard to the service quality

availed by them from the banks.

5.7. RELIABILITY

Reliability refers to the customers’ perception with regard to the redemption of

commitment by bank to render the service honestly, sincerely, timely, and

satisfactorily as envisioned by the customer. Factors included in the reliability

dimensions are such as, ‘performing what is promised’ and doing it ‘at the promised

time’ by the bank. Most importantly, reliability perception aims at inculcating in

customers’ mind the belief that the financial records and statements as maintained and

presented to customers by bank are error free, accurate and dependable. Customers

trust in the bank reflects the level of customer satisfaction with regard to reliability of

its service quality.

5.8. RESPONSIVENESS

The ‘Responsiveness’ dimension of service quality includes factors conditioning the

customers’ perception with regard to banks’ attention and action to issues related to

customers. Factors reflecting to responsiveness are rendering instant services,

quickness in attending to problems, promptness in taking action, sagaciousness in

Chapter-5: Data Analysis and Interpretation

122 | P a g e

decision making, disposition of grievance within committed time etc. With the

advancement of technology, customers expect that their problems will be responded

as soon as possible. Lack of responsiveness would make the customers switch over to

the other banks. This underscores the significance of responsiveness as a service

quality dimension.

5.9. ASSURANCE

Assurance refers to the service quality dimension that makes the customer sure that

the transaction dealings are fair and safe with the bank. Assurance involves factors

like trust on the bank employees, keeping privacy of customers’ transactions,

providing access to information to genuine customers etc. An overall feeling of

confidence in customers that bank employees have professional knowledge and

experience and render answer to customers queries which are genuine and trustworthy

is also an important attribute of assurance.

5.10. EMPATHY

The service quality represented by Empathy indicates the ability of the bank to

understand customers’ feelings and the situations they are in for help and assistance.

The attribute of empathy demands an inclination in the attitude of bank personnel to

give personal consideration and priority attention to customers. It deals with the

quality of personal interaction of the employees with their customers as well as

sympathetic response to their queries and complaints.

Chapter-5: Data Analysis and Interpretation

123 | P a g e

SECTION-II

The foregoing Section-I presented conceptual explanation of the service quality and

delineated on its nature and scope. Also the attributes of service quality and their

respective dimensions have been diagrammatically represented and textually

explained at length. The various factors included in each attribute that capture and

reflect the customer perception of the service quality have been identified for use in

the collection of data for the purpose of this study.

The present Section-II is accordingly ear-marked for collection of data on the

basis of SERVQUAL Dimensions and benchmarks set in the foregoing section to

ascertain service quality in retail banking rendered by public and private sector banks.

The analysis and interpretation of data with the help of statistical tools has also been

carried out in this section. On the basis of logical inferences drawn from the analysis

and interpretation of facts and figures, the hypotheses formulated for the study have

been tested at the end.

A. DATA COLLECTION

The study bases itself on primary data collected by using the SERVQUAL model for

ascertaining the service quality of retail banking in India. The information has been

elicited through a field survey by means of a well designed questionnaire comprising

of queries on the various service quality attributes and their dimensions as identified

and contained in the SERVQUAL. One additional attribute has been added to the

original SERVQUAL. This relates to ascertainment of ATM Service Quality which is

one of the most important factors that reflects the service quality of banks in retail

segment. The questionnaire has been administered on a randomly selected sample of

Chapter-5: Data Analysis and Interpretation

124 | P a g e

customers availing retail banking services from the private and public sector Indian

banks. The spread of survey covers nine districts of the State of Uttar Pradesh,

Uttarakhand and Delhi

A blow-up of the methodology adopted for primary data collection is

presented below.

5.11. UNIVERSE

The universe or population represents the entire group of units concerned with the

particular study. Thus, the population could consist of all the living and non-living

units in the country, or those in a particular geographical location, or a special ethnic

or economic group, depending on the purpose and coverage of the study.

In the present study all the customers of banks in India are considered as

Universe. These are the customers who have their accounts in different banks of the

country whether it is Public Sector Banks or Private Sector Banks. The universe of

this study is specifically concerned with those customers of banks in India who are

availing services of the retail banking segment.

As the collection of complete data from all the customers in the universe is not

possible, a select sample of geographical areas as well as of customers is chosen for

data collection for this study.

5.12. SAMPLE

Sample represents the subset of population. A sample is a finite part of a statistical

population whose properties are studied to gain information about the whole. When

dealing with people it can be defined as a set of respondents (people) selected from a

large population for the purpose of a survey.

Chapter-5: Data Analysis and Interpretation

125 | P a g e

For this research, samples have to be taken since it is not possible to cover

such a vast country as India on account of impediments of time, finance and other

resources required for the purpose. Hence, the geographical area for the survey as

well as the bank customers (respondents) to the questionnaire have been selected in

such a manner that the whole country is represented and the conduct of research work

gets convenient in handling and possible for completion.

As regards the geographical coverage, the Northern Region, which stands out

as the biggest region of India, has been chosen. Since this region consists of large

number of cities spread over different States and Union Territory, necessity arose to

further abridge the geographical area selecting a few important cities from the

Northern Region of India. Accordingly, nine big cities with huge banking population

have been taken as sample for survey under this study. These nine cities are spread

over three northern Indian States, namely, Uttar Pradesh, Uttarkhand and Delhi. The

city of Delhi also happens to be the Capital of India. Being a metropolitan and

cosmopolitan city, Delhi alone represents the whole of India and hence makes this

study more representative and reliable. Other selected cities besides Delhi are: Agra,

Aligarh, Lucknow, Mathura, Dehradun Moradabad, Kanpur, and Noida.

Respondents have been drawn from the nine cities to a manageable handling

limit of 500, of which 497 responded. The selection of these respondents is at random.

This mode of selection rules out any bias creeping into the opinion survey and lends

lot of credence to the outcome of the study.

Chapter-5: Data Analysis and Interpretation

126 | P a g e

5.13. QUESTIONNAIRE

Descriptive research has been conducted to gain an insight into consumers perceived

service quality, offered by banks with respect to five dimensions of SERVQUAL

scale. A structured questionnaire based on SERVQUAL scale (Persuraman et.al.

1985) has been used for data collection for this research with some modification. The

modified questionnaire maintains the number of dimensions of SERVQUAL to five,

but substitutes the dimension of ‘Empathy’ by ‘ATM Service Quality’. Thus, the five

dimensions of questionnaire comprise Tangibles, Reliability, Responsiveness,

Assurance and ATM Service Quality.

The design and structure of the questionnaire is simple, study specific

unambiguous and capable of seeking objective type of answers through marking a tick

only. The queries that elicit information about the perception of customers under five

dimensions have a direct bearing as the hypotheses of this study. Each of the five

dimensions asks questions specifically related to the dimensions. The customers have

been requested to rate the service quality variables at five point scale on the basis of

their perceived service quality and their satisfaction level towards the banks. Against

every question in each statement, five options of answers are given, i.e ‘Strongly

Agree’; ‘Agree’; ‘Neutral’; ‘Disagree’ and ‘Strongly Disagree’. Each respondent is

advised to tick the option that represents the perception most truly and faithfully.

5.14. ADMINISTRATION OF QUESTIONNAIRE

The universe for collection of data consists of the customers of private and public

sector banks spread all over India. Their full coverage being not possible on account

of restraints by a host of factors, a representative sample of respondents as well as the

geographical area as explained under ‘Sample’ technique has been taken for

Chapter-5: Data Analysis and Interpretation

127 | P a g e

administrating the questionnaire. The sample consists of 500 respondents (bank

customers) and the geographical area covered comprised of nine big cities of three

States in the Northern Region of India and includes the Capital city of Delhi which

alone represents the respondents from all parts of India. Besides Delhi, the other cities

are Aligarh, Agra, Lucknow, Moradabad, Mathura, Noida, Dehradun and Kanpur.

The mode of administration of questionnaire on respondents is through direct

personal investigation. It is blended with ‘Convenience’ of respondents. Since the

sample population of bank customers comprised of educated persons who could read,

understand and tick their perceptions in the boxes provided for answers in the

questionnaire at their convenient time, they were handed over questionnaire to be

collected from them at the pre-fixed time and date. Yet, while getting back the

questionnaire discussions and clarification were made to help get the perceptions

expressed by the respondents as they really felt. Larger number of respondents

approached, however, obliged by filling the questionnaire face to face. Thus, the

direct investigation method adopted for this study reassures that the information

collected is more accurate, reliable, and trustworthy in reflecting the results of this

research.

5.15. RESPONSE

Customers of the banks gave a highly encouraging response. About 600

questionnaires have been distributed out to cover the sample size of 500 out of which

497 completely filled questionnaire have been received from the different customers

of the banks. The response has, thus been more than 80 percent. Moreover, the

respondents took very cooperative and sincere interest and care of appropriately

ticking their perceptions on the scale of preference provided in the questionnaire and

Chapter-5: Data Analysis and Interpretation

128 | P a g e

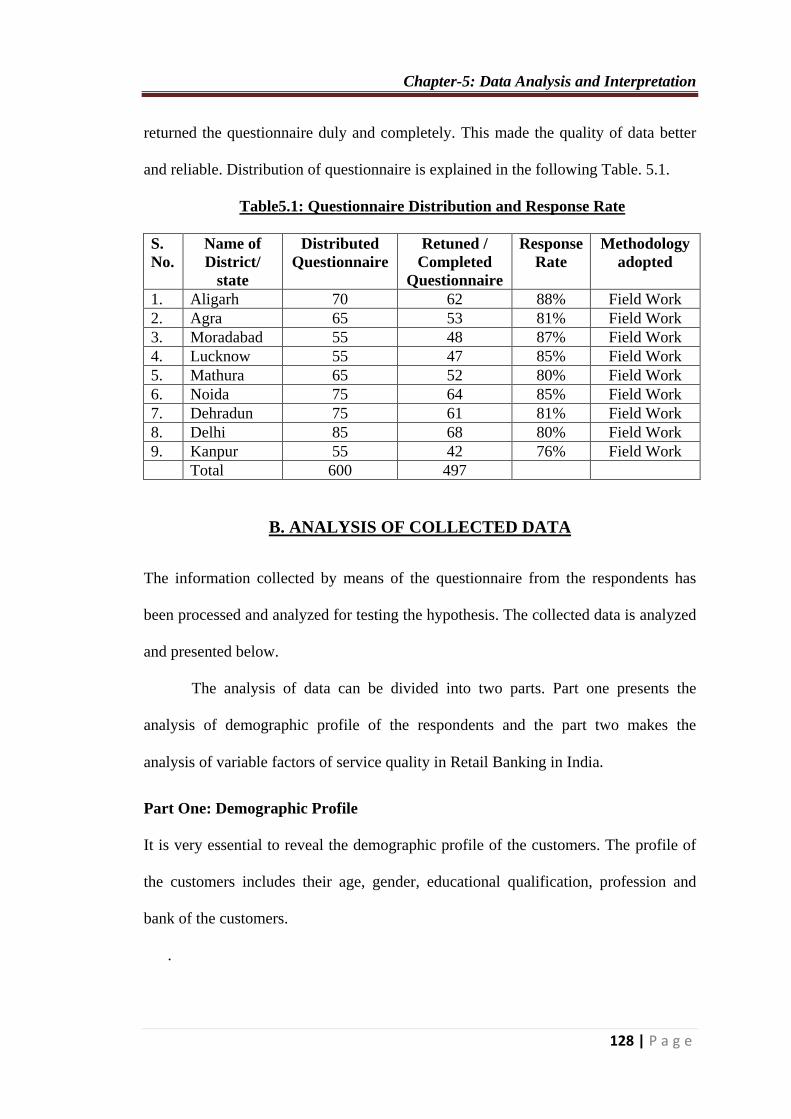

returned the questionnaire duly and completely. This made the quality of data better

and reliable. Distribution of questionnaire is explained in the following Table. 5.1.

Table5.1: Questionnaire Distribution and Response Rate

S.

No.

Name of

District/

state

Distributed

Questionnaire

Retuned /

Completed

Questionnaire

Response

Rate

Methodology

adopted

1. Aligarh 70 62 88% Field Work

2. Agra 65 53 81% Field Work

3. Moradabad 55 48 87% Field Work

4. Lucknow 55 47 85% Field Work

5. Mathura 65 52 80% Field Work

6. Noida 75 64 85% Field Work

7. Dehradun 75 61 81% Field Work

8. Delhi 85 68 80% Field Work

9. Kanpur 55 42 76% Field Work

Total 600 497

B. ANALYSIS OF COLLECTED DATA

The information collected by means of the questionnaire from the respondents has

been processed and analyzed for testing the hypothesis. The collected data is analyzed

and presented below.

The analysis of data can be divided into two parts. Part one presents the

analysis of demographic profile of the respondents and the part two makes the

analysis of variable factors of service quality in Retail Banking in India.

Part One: Demographic Profile

It is very essential to reveal the demographic profile of the customers. The profile of

the customers includes their age, gender, educational qualification, profession and

bank of the customers.

.

Chapter-5: Data Analysis and Interpretation

129 | P a g e

5.16. Age of the Respondents

Age of the customers is one of the important profile variables of the customers. It

shows their level of experience and maturity. In the banking industry, age plays a

predominant role in their level of satisfaction on the service quality of the banks. In

general the youngsters expect more than the elders who are highly experienced and

emotional. The age of the customers in the present study is confined to below 25

years, 25-35, 35-45, 45-55 and above 55. The distribution of the customers on the

basis of their age is given in Table 5.2

Table 5.2: Age Wise Distribution of Customers

Age (in years) Number of Customers Total

Number Public Sector Banks

(PSBs)

Private Sector Banks

(Prv. SBs)

Number Percentage Number Percentage

Below 25 134 26.96 0 0

25 – 35 109 21.93 104 20.93 213

35 – 45 42 8.45 30 6.04 72

45 – 55 42 8.45 15 3.02 57

Above 55 13 2.61 8 1.61 21

Total 340 68.4 157 31.6 497

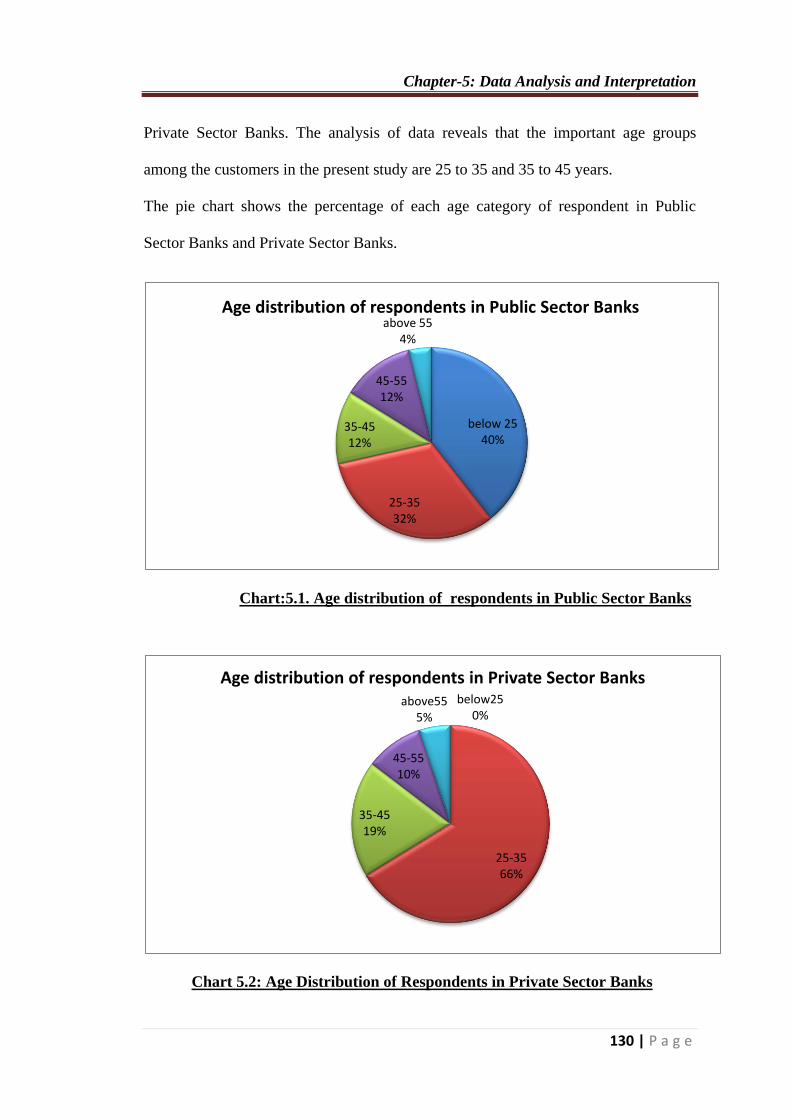

From the above table it is clear that the important age group among the

customers is 25 to 35 years which constitute 21.93 percent in Public Sector Banks and

20.93 percent in Private Sector Banks The age group of below 25 years constitutes the

highest number of 134 customer or 26.96 percent in the Public Sector Banks while in

Private Sector Banks the age group below 25 years constitute the zero. The age group

of 35-45 years constitutes 42 respondents in Public Sector Bank and 30 respondents in

Private Sector Banks yielding a percentage of 8.45 and 6.04 respectively. The age

group above 55 which reveals the senior citizens customer of the banks constitutes 13

with a percentage of 2.61 in Public Sector Bank and 8 with the percentage of 1.61 in

Chapter-5: Data Analysis and Interpretation

130 | P a g e

Private Sector Banks. The analysis of data reveals that the important age groups

among the customers in the present study are 25 to 35 and 35 to 45 years.

The pie chart shows the percentage of each age category of respondent in Public

Sector Banks and Private Sector Banks.

Chart:5.1. Age distribution of respondents in Public Sector Banks

Chart 5.2: Age Distribution of Respondents in Private Sector Banks

below 25 40%

25-35 32%

35-45 12%

45-55 12%

above 55 4%

Age distribution of respondents in Public Sector Banks

below25 0%

25-35 66%

35-45 19%

45-55 10%

above55 5%

Age distribution of respondents in Private Sector Banks

Chapter-5: Data Analysis and Interpretation

131 | P a g e

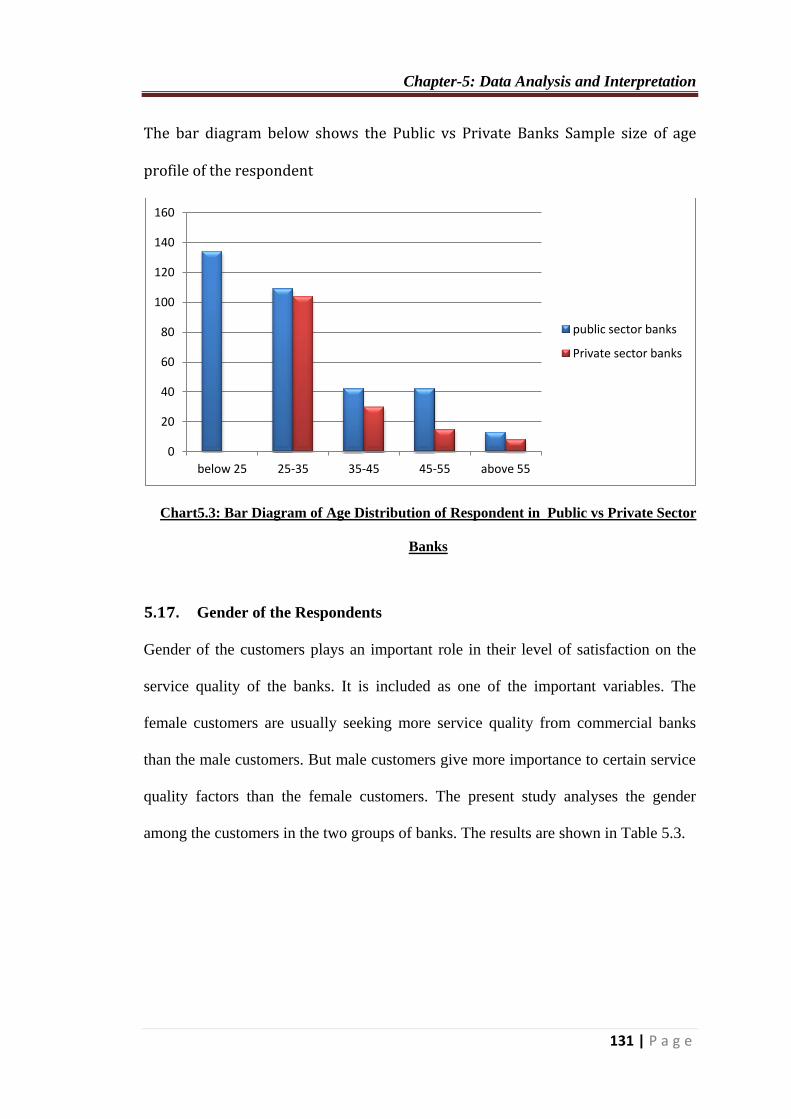

The bar diagram below shows the Public vs Private Banks Sample size of age

profile of the respondent

Chart5.3: Bar Diagram of Age Distribution of Respondent in Public vs Private Sector

Banks

5.17. Gender of the Respondents

Gender of the customers plays an important role in their level of satisfaction on the

service quality of the banks. It is included as one of the important variables. The

female customers are usually seeking more service quality from commercial banks

than the male customers. But male customers give more importance to certain service

quality factors than the female customers. The present study analyses the gender

among the customers in the two groups of banks. The results are shown in Table 5.3.

0

20

40

60

80

100

120

140

160

below 25 25-35 35-45 45-55 above 55

public sector banks

Private sector banks

Chapter-5: Data Analysis and Interpretation

132 | P a g e

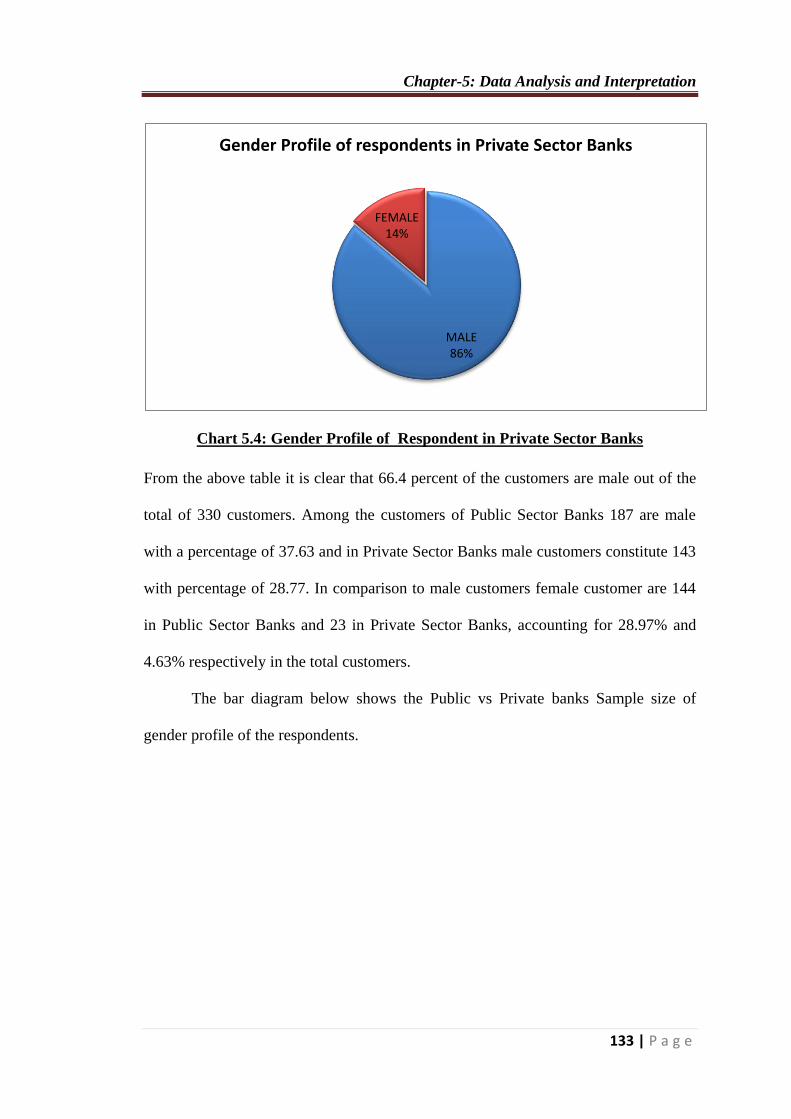

Table 5.3: Distribution of the customers based on Gender

S.

No.

Gender Public Sector Banks Private Sector Banks Total

Number Percentage Number Percentage Number Percentage

1. Male 187 37.63 143 28.77 330 66.40

2. Female 144 28.97 23 4.63 167 33.60

Total 331 65.60 166 33.40 497 100.00

The pie chart shows the percentage of each gender category of respondent in Public

Sector Banks and Private Sector Banks.

Chart 5.4: Gender Profile of Respondent in Public Sector Banks

MALE 56%

FEMALE 44%

Gender profile of respondents in Public Sector Banks

Chapter-5: Data Analysis and Interpretation

133 | P a g e

Chart 5.4: Gender Profile of Respondent in Private Sector Banks

From the above table it is clear that 66.4 percent of the customers are male out of the

total of 330 customers. Among the customers of Public Sector Banks 187 are male

with a percentage of 37.63 and in Private Sector Banks male customers constitute 143

with percentage of 28.77. In comparison to male customers female customer are 144

in Public Sector Banks and 23 in Private Sector Banks, accounting for 28.97% and

4.63% respectively in the total customers.

The bar diagram below shows the Public vs Private banks Sample size of

gender profile of the respondents.

MALE 86%

FEMALE 14%

Gender Profile of respondents in Private Sector Banks

Chapter-5: Data Analysis and Interpretation

134 | P a g e

5.5: Bar Diagram of Gender profile of Public vs Private Sector Banks

5.18. Level of Education of the Respondents

The level of education provides more knowledge and exposure on the competitive

service offered by the commercial banks with globalised scenario. Hence the level of

education of the customers is included as one of the profile variable. The highly

educated customers may be more aware of competitive service and expect more from

their banks as compared to uneducated customers. The education level of the

customers is confined to Under Graduate, Graduate, Post Graduate, Ph.D and others

(including less than Under Graduates). The data is computed in Table 5.4.

0

20

40

60

80

100

120

140

160

180

200

PUBLIC SECTOR BANKS PRIVATE SECTOR BANKS

Publis Vs Private Sector Banks

MALE

FEMALE

Chapter-5: Data Analysis and Interpretation

135 | P a g e

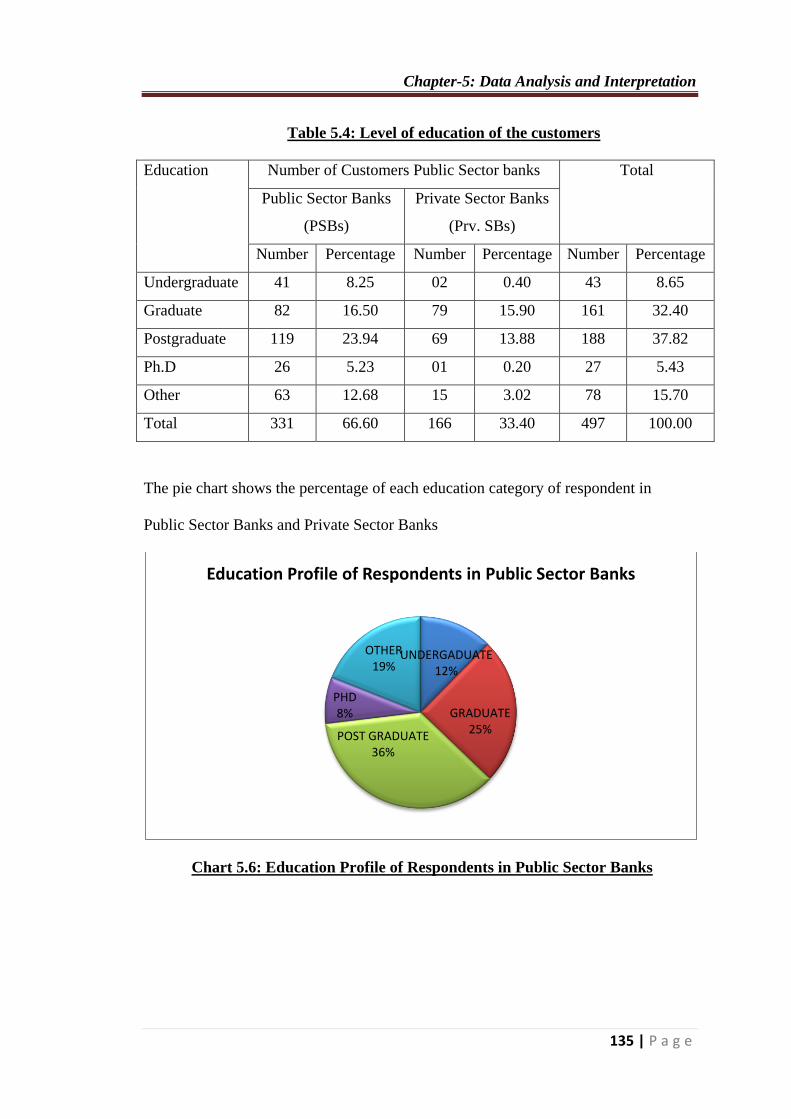

Table 5.4: Level of education of the customers

Education Number of Customers Public Sector banks Total

Public Sector Banks

(PSBs)

Private Sector Banks

(Prv. SBs)

Number Percentage Number Percentage Number Percentage

Undergraduate 41 8.25 02 0.40 43 8.65

Graduate 82 16.50 79 15.90 161 32.40

Postgraduate 119 23.94 69 13.88 188 37.82

Ph.D 26 5.23 01 0.20 27 5.43

Other 63 12.68 15 3.02 78 15.70

Total 331 66.60 166 33.40 497 100.00

The pie chart shows the percentage of each education category of respondent in

Public Sector Banks and Private Sector Banks

Chart 5.6: Education Profile of Respondents in Public Sector Banks

UNDERGADUATE 12%

GRADUATE 25%

POST GRADUATE 36%

PHD 8%

OTHER 19%

Education Profile of Respondents in Public Sector Banks

Chapter-5: Data Analysis and Interpretation

136 | P a g e

Chart 5.7: Education Profile of Respondents in Private Sector Banks

Table 5.4 explains the distribution of customer on the basis of their level of education.

The dominant level of education among the customers is Graduation and Post

Graduation which constitute 32.4 percent and 37.82 percent to their respective total.

The number of customers who are Undergraduate is 41 or 8.25 percent in Public

Sector Banks and 2 or 0.40 percent in Private Sector Banks. The prominent level of

education among the customers is of graduates and Postgraduates which constitute

16.5 percent and 23.94 percent in Public Sector Banks and 15.9and 13.88 percent in

Private Sector Banks respectively. The number of customers with education upto

Ph.D. is 26 or 5.23 percent in Public Sector Banks and 1 or 0.20 percent in Private

Sector Banks respectively. The number of customer with the education level below

the undergraduate in ‘others’ category is 63 and constitute 12.68 percent in Public

Sector Banks and 15 or 3.02 percent in Private Sector Banks.

The bar diagram below shows the Public vs Private banks Sample size of education

profile of the respondent.

U.GADUATE 0%

GRADUATE 1%

POST GRADUATE

52%

PHD 46%

OTHER 1%

Education Profile of Respondents in Private Sector Banks

Chapter-5: Data Analysis and Interpretation

137 | P a g e

Dig.5.8: Education Profile of Respondents Public vs Private Sector Banks

5.19. Occupation of the Respondents

The occupation of the customer reveals the nature of work done by the customers.

Occupation of the customers influences their level of satisfaction on the perceived

service quality of Retail Banking. It includes as one of the profile variable. The

occupation of the customers is confined to government service, Private Services,

students, professionals and other jobs. The occupation of the customers is illustrated

in Table 5.5

0

20

40

60

80

100

120

140

PUBLIC SECTOR BANKS

PRIVATE SECTOR BANKS

Chapter-5: Data Analysis and Interpretation

138 | P a g e

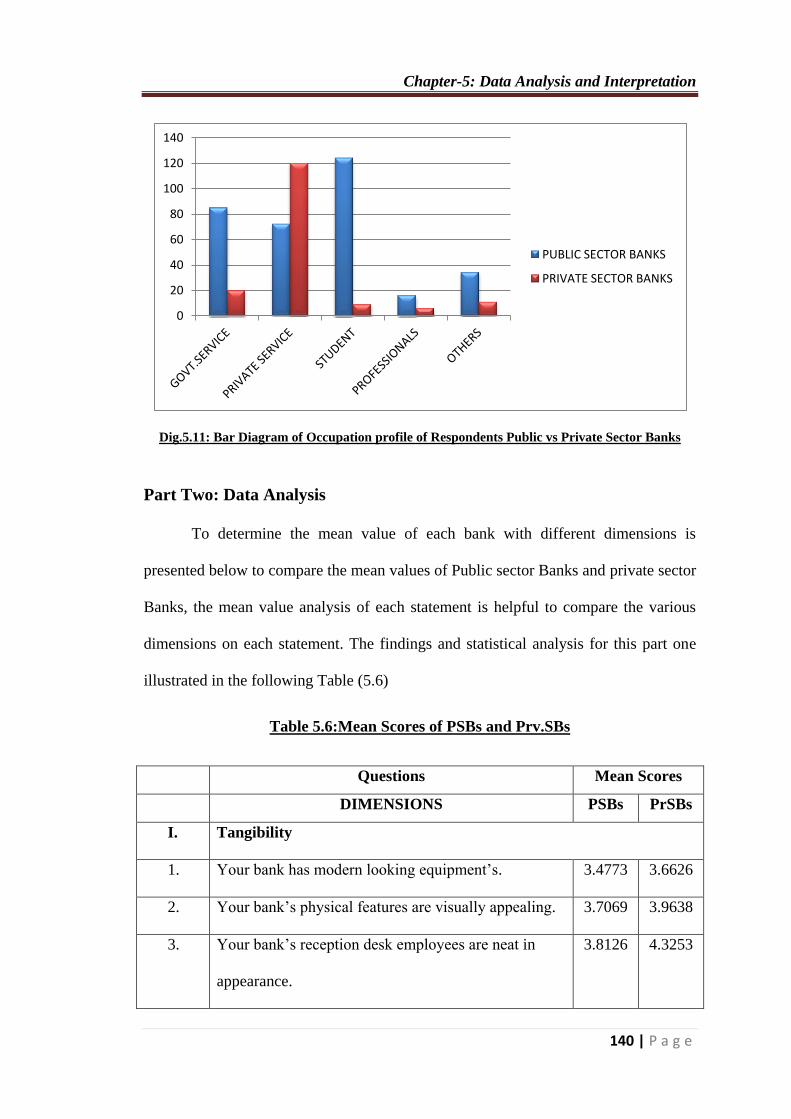

Table 5.5: Occupation Profile of the Customers

Occupation Number of Customers Public Sector banks Total

Public Sector Banks

(PSBs)

Private Sector Banks

(Prv. SBs)

Number Percentage Number Percentage Number Percentage

Government

services

85 17.10 20 4.02 105 21.12

Private

Services

72 14.49 120 24.14 192 38.63

Students 124 24.95 09 1.82 133 26.77

Profession 16 3.22 06 1.21 22 4.43

Other 34 6.84 11 2.21 45 9.05

Total 331 66.60 166 33.40 497 100.00

The pie chart shows the percentage of each occupation category of respondents in

Public Sector Banks and Private Sector Banks.

Chart 5.9: Occupation Profile of Respondents in Public Sector Banks

GOVT.SERVICE 26%

PRIVATE SERVICE

22%

STUDENT 37%

PROFESSIONAL 5%

OTHERS 10%

Occupation profile of respondents in Public Sector Banks

Chapter-5: Data Analysis and Interpretation

139 | P a g e

Chart 5.10: Occupation Profile of Respondents In Private Sector Banks

The important occupations among the customers are Government Service, Private

Service and Students which constitute 21.12 percent 38.63 percent and 26.77 percent

respectively. The important occupation among the customers of PSBs is government

services and students which constitute 17.10 percent and 24.95 percent to their

respective total. In the Pr.SBs, the two important occupations are Private Services and

Government services which constitute 4.02 percent and 24.14 percent respectively. In

case of Public Sector Banks, Private Services constitutes 14.49, professional jobs

constitute 3.32 percent and others which include business constitute 6.84 percent. In

case of Private Sector Banks Government Services constitute 4.02 percent, students

1.82 percent, Professional Jobs constitutes 1.25 percent and others constitute 2.21

percent.

The bar diagram below shows the Public vs Private banks Sample size of occupation

profile of the respondents.

GOVT.SERVICE 12%

PRIVATE SERVICE 72%

STUDENT 5%

PROFESSIONAL 4%

OTHERS 7%

Occupation Profile of Customers in Private Sector Banks

Chapter-5: Data Analysis and Interpretation

140 | P a g e

Dig.5.11: Bar Diagram of Occupation profile of Respondents Public vs Private Sector Banks

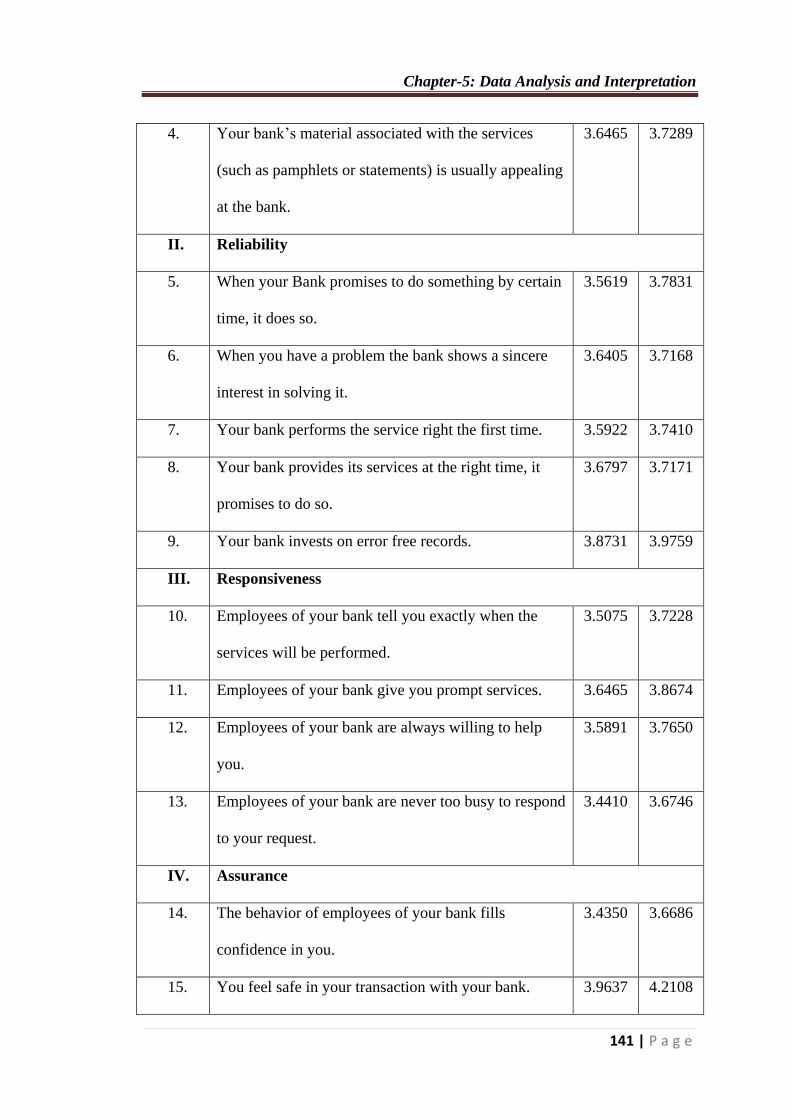

Part Two: Data Analysis

To determine the mean value of each bank with different dimensions is

presented below to compare the mean values of Public sector Banks and private sector

Banks, the mean value analysis of each statement is helpful to compare the various

dimensions on each statement. The findings and statistical analysis for this part one

illustrated in the following Table (5.6)

Table 5.6:Mean Scores of PSBs and Prv.SBs

Questions Mean Scores

DIMENSIONS PSBs PrSBs

I. Tangibility

1. Your bank has modern looking equipment’s. 3.4773 3.6626

2. Your bank’s physical features are visually appealing. 3.7069 3.9638

3. Your bank’s reception desk employees are neat in

appearance.

3.8126 4.3253

0

20

40

60

80

100

120

140

PUBLIC SECTOR BANKS

PRIVATE SECTOR BANKS

Chapter-5: Data Analysis and Interpretation

141 | P a g e

4. Your bank’s material associated with the services

(such as pamphlets or statements) is usually appealing

at the bank.

3.6465 3.7289

II. Reliability

5. When your Bank promises to do something by certain

time, it does so.

3.5619 3.7831

6. When you have a problem the bank shows a sincere

interest in solving it.

3.6405 3.7168

7. Your bank performs the service right the first time. 3.5922 3.7410

8. Your bank provides its services at the right time, it

promises to do so.

3.6797 3.7171

9. Your bank invests on error free records. 3.8731 3.9759

III. Responsiveness

10. Employees of your bank tell you exactly when the

services will be performed.

3.5075 3.7228

11. Employees of your bank give you prompt services. 3.6465 3.8674

12. Employees of your bank are always willing to help

you.

3.5891 3.7650

13. Employees of your bank are never too busy to respond

to your request.

3.4410 3.6746

IV. Assurance

14. The behavior of employees of your bank fills

confidence in you.

3.4350 3.6686

15. You feel safe in your transaction with your bank. 3.9637 4.2108

Chapter-5: Data Analysis and Interpretation

142 | P a g e

16. Employees of your Bank are polite with you. 3.6555 3.8975

17. Employees of your Bank have the knowledge to

answer your questions.

3.8701 3.9337

V. ATM Service Quality

18. Your Bank has quick cash withdrawal through ATM. 4.1359 4.0421

19. Your bank has suitable ATM location. 3.8489 3.5000

20. Your bank has safe and secure ATM transaction. 4.0604 4.3253

21. Your Bank ATM machine is user friendly. 3.9425 4.0180

22. Your bank has attractive appearance of ATM. 3.8489 3.7108

23. Your Bank has excellent quality of currency. 3.8429 3.8072

As shown in table (5.6) it is found that there is positive attitude towards all question

but with different mean values in public sector Banks and private sector Bank.

Chapter-5: Data Analysis and Interpretation

143 | P a g e

5.20. Dimension-I Tangibles

As shown in Table (5.6) the dimension tangible has positive attitude in the

respondents towards private sector Bank. Their mean values were greater than Public

Sector banks with different mean values.

The statement with the high mean in this dimensions is number (3) which

says, “your bank’s reception desk employees are neat in appearance” where its mean

is (4.3253) in private sector Banks in comparison to public sector banks where it is

(3.8126), whereas the lowest mean noted is (3.6626) in private sector banks and

3.4773) in Public Sector Banks in statement number (1) which said “your Bank has

modern looking equipments”.

5.21. Dimension II- Reliability

As shown in Table (5.6) there exist a positive attitude in the respondents towards the

Private Sector Banks because their means are greater than the Public sector Banks.

The statement with the high mean in this dimension is number (9) which says,

“Your bank invests on error free records”. The mean value of private sector banks

being (3.9759) is greater in comparison to (3.8731) in Public Sector Banks.

Whereas the lowest mean was (3.5619) in statement number (5) in Public

sector banks and (3.7831) in Private Sector Banks which said “when your Bank

promises to do something by certain time, it does so”.

5.22. Dimension III- Responsiveness

As shown in Table (5.6) in the dimension Responsiveness, there exists a positive

attitude in the respondents towards the Private Sector Banks in comparison to Public

sector Banks with different mean scores.

Chapter-5: Data Analysis and Interpretation

144 | P a g e

The statement with the highest mean in this dimension is number (11) which

says, “Employees of your Bank give you prompt services”. Its mean is (3.6465) in

Public Sector Banks and (3.8674) in Private Sector Bank.

Whereas the lowest mean of (3.4410) in Public Sector Banks and (3.6746) in

Private Sector Banks is in case of statement number (13) which said “Employees of

your bank are never too busy to respond to your request”.

5.23. Dimension IV- Assurance:

As shown in Table (5.6) there exists a positive attitude in the respondents towards the

Private Sector Banks because the mean scores of private sector Banks are greater than

the Public Sector Bank in all the questions under this dimension.

The statement with the high mean in this dimension is number (15) which

says, “You feel safe in your transactions with your Bank” where its mean has reached

(4.2108) in Private Sector Banks and (3.9637) in Public Sector Banks.

Whereas the lowest mean is (3.4350) in Public sector banks and (3.6686) in

Private Sector Banks in statement number (14) which said, “The behavior of your

employees fills confidence in you”.

Chapter-5: Data Analysis and Interpretation

145 | P a g e

5.24. Dimension V- ATM Service Quality

As shown in Table (5.6) there exists a positive attitude in the respondents towards the

Public Sector Banks as is evident from their means which are greater than the Private

Sector Banks having the different mean scores.

The statement with the high mean in this dimension ATM Service Quality is

number (18) which says, “Your bank has quick cash withdrawal through ATM”.

Where the mean values is (4.1359) in Public Sector Banks which is greater than in

Private Sector Banks where it is (4.0421).

Whereas the lowest mean was (3.8429) in Private Sector Bank and (3.8072) in

Public Sector Bank in statement number (23) which said “Your Bank has excellent

quality of Currency”.

The following Table 5.7 shows the mean values of five service quality

dimension used in analysis of data for this research. The highest mean score of 3.94 is

of ‘ATM Service Quality’ in Public Sector Banks and 3.90 in Private Sector Banks.

There is small variation in the mean score of reliability, responsiveness & assurance.

Table 5.7: Shows The Overall Mean In Each Dimension

Table 5.7: Item Statistics

Dimension Mean Score

Public Sector Banks Private Sector Banks

Tangibles 3.66 3.91

Reliability 3.66 3.80

Responsiveness 3.54 3.76

Assurance 3.73 3.92

ATM Service Quality 3.94 3.90

Total number of respondents: 497

The following diagram represents the mean values of all the five dimensions through

the graphs between Public Sector Banks and Private Sector Banks.

Chapter-5: Data Analysis and Interpretation

146 | P a g e

Dig.5.12: Mean Scores of Service Quality Dimensions in Public vs Private Sector Banks

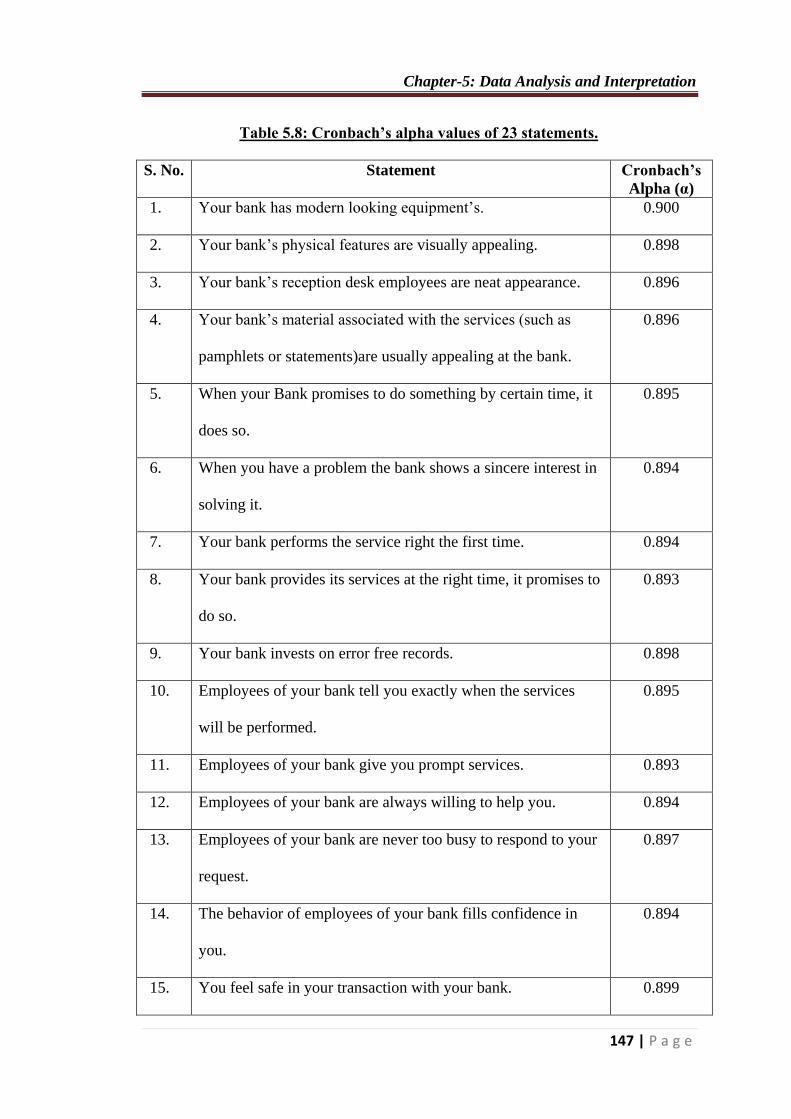

5.25. Reliability and Validity Test

5.25.1. Reliability Test

Reliability is the consistency of the measurement; or the degree to which an

instrument measures the same way each time it is used under the same condition with

the same subject. In the present study Cronbach’s alpha (α) is used to measure the

reliability of data. Cronbach (1951) gave a measure to that which is loosely equivalent

to splitting data in two in every possible way and computing the correlation

coefficient for each split. The average of these values is equivalent to Cronbach’s

alpha (α) which is the most common measure of scale reliability. Kline (1999)

indicates that interpretation of Cronbach’s alpha is estimated such that a value of 0.7-

0.8 is an acceptable value for Cronbach’s alpha. Values substantially lower indicate

an unreliable scale. Following Table 5.8 shows the statement-wise reliability of 23

statements.

3.3

3.4

3.5

3.6

3.7

3.8

3.9

4

Mean Score Public Sector Banks

Mean Score Private Sector Banks

Chapter-5: Data Analysis and Interpretation

147 | P a g e

Table 5.8: Cronbach’s alpha values of 23 statements.

S. No. Statement Cronbach’s

Alpha (α)

1. Your bank has modern looking equipment’s. 0.900

2. Your bank’s physical features are visually appealing. 0.898

3. Your bank’s reception desk employees are neat appearance. 0.896

4. Your bank’s material associated with the services (such as

pamphlets or statements)are usually appealing at the bank.

0.896

5. When your Bank promises to do something by certain time, it

does so.

0.895

6. When you have a problem the bank shows a sincere interest in

solving it.

0.894

7. Your bank performs the service right the first time. 0.894

8. Your bank provides its services at the right time, it promises to

do so.

0.893

9. Your bank invests on error free records. 0.898

10. Employees of your bank tell you exactly when the services

will be performed.

0.895

11. Employees of your bank give you prompt services. 0.893

12. Employees of your bank are always willing to help you. 0.894

13. Employees of your bank are never too busy to respond to your

request.

0.897

14. The behavior of employees of your bank fills confidence in

you.

0.894

15. You feel safe in your transaction with your bank. 0.899

Chapter-5: Data Analysis and Interpretation

148 | P a g e

16. Employees of your Bank are polite with you. 0.895

17. Employees of your Bank have the knowledge to answer your

questions.

0.895

18. Your Bank has quick cash withdrawal through ATM. 0.896

19. Your bank has suitable ATM location. 0.899

20. Your bank has safe and secure ATM transaction. 0.897

21. Your Bank ATM machine is user friendly. 0.896

22. Your bank has attractive appearance of ATM. 0.894

23. Your Bank has excellent quality of currency. 0.892

The above table indicates the reliability of scale by calculating Cronbach’s

alpha. The items where the value of alpha is more than 0.7 are considered significant

for this research. The reliability table shows the statement wise values of alpha, which

is more than 0.7 in each statement.

Chapter-5: Data Analysis and Interpretation

149 | P a g e

The Cronbach’s alpha (α) values of the 23 items are narrated into five dimensions

namely Tangibles, Reliability, Responsiveness, Assurance and ATM Service quality.

These result of Cronbach’s alpha for five dimensions are given in Table (5.9)

Table 5.9: Reliability Analysis

S. NO. Dimensions No. of Item Cronbach’s

Alpha(α)

1. Tangibles 4 0.825

2. Reliability 5 0.842

3. Responsiveness 4 0.865

4. Assurance 4 0.807

5. ATM Service Quality 6 0.871

Overall Reliability 23 0.900

The reliability of five dimensions gets confirmed from the above table since

the reliability coefficients are higher than the standard minimum of 0.70 in each

dimension. The overall composite reliability of the variables is also higher than the

minimum threshold of 0.7 that is 0.900.

5.25.2. Validity of test:

Validity is the strength of our conclusions, inferences or propositions. Cook and

Campbell (1979) define it as the “best available approximation to the truth or falsity

of a given inference, proposition or conclusion”.

The test of validity of data for factor analysis has been conducted with the help

of KMO measure and Bartlett’s test of Sphericity.

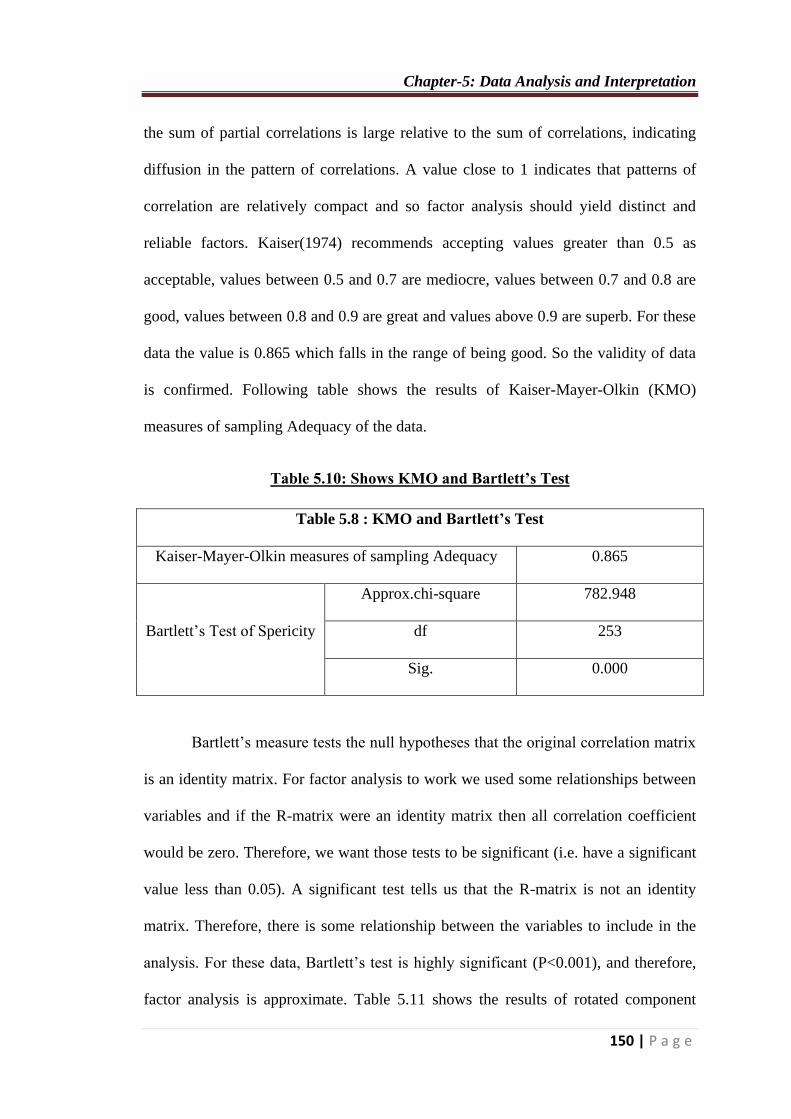

The Kaiser-Meyer-Olkin (KMO) measures the validity of the dimensions for

factor analysis. The KMO statistics varies between 0 and 1. A value 0 indicates that

Chapter-5: Data Analysis and Interpretation

150 | P a g e

the sum of partial correlations is large relative to the sum of correlations, indicating

diffusion in the pattern of correlations. A value close to 1 indicates that patterns of

correlation are relatively compact and so factor analysis should yield distinct and

reliable factors. Kaiser(1974) recommends accepting values greater than 0.5 as

acceptable, values between 0.5 and 0.7 are mediocre, values between 0.7 and 0.8 are

good, values between 0.8 and 0.9 are great and values above 0.9 are superb. For these

data the value is 0.865 which falls in the range of being good. So the validity of data

is confirmed. Following table shows the results of Kaiser-Mayer-Olkin (KMO)

measures of sampling Adequacy of the data.

Table 5.10: Shows KMO and Bartlett’s Test

Table 5.8 : KMO and Bartlett’s Test

Kaiser-Mayer-Olkin measures of sampling Adequacy 0.865

Bartlett’s Test of Spericity

Approx.chi-square 782.948

df 253

Sig. 0.000

Bartlett’s measure tests the null hypotheses that the original correlation matrix

is an identity matrix. For factor analysis to work we used some relationships between

variables and if the R-matrix were an identity matrix then all correlation coefficient

would be zero. Therefore, we want those tests to be significant (i.e. have a significant

value less than 0.05). A significant test tells us that the R-matrix is not an identity

matrix. Therefore, there is some relationship between the variables to include in the

analysis. For these data, Bartlett’s test is highly significant (P<0.001), and therefore,

factor analysis is approximate. Table 5.11 shows the results of rotated component

Chapter-5: Data Analysis and Interpretation

151 | P a g e

matrix. All the values of extraction are more than 0.40. Therefore, the data is found

suitable for further analysis.

Table 5.11: Rotated Component Matrix

Component Matrix

Statement Extraction

1. Your banks physical features equipment. 0.630

2. Your bank’s physical features are visually appealing. 0.658

3. Your bank’s reception desk employees are neat in

appearance.

0.648

4. Your bank’s material associated with the services (such as

pamphlets or statements) is usually appealing at the bank.

0.521

5. When your Bank promises to do something by certain time,

it does so.

0.687

6. When you have a problem the bank shows a sincere

interesting in solving it.

0.581

7. Your bank performs the service right the first time 0.589

8. Your bank provides its services at the right time, it promises

to do so.

0.542

9. Your bank invests on error free records. 0.606

10. Employees of your bank tell you exactly when the services

will be performed.

0.528

11. Employees of your bank give you prompt services. 0.593

12. Employees of your bank are always willing to help you. 0.522

13. Employees of your bank are never too busy to respond to 0.631

Chapter-5: Data Analysis and Interpretation

152 | P a g e

your request.

14. The behavior of employees of your bank fills confidence in

you.

0.549

15. You feel safe in your transaction with your bank. 0.671

16. Employees of your Bank are polite with you. 0.626

17. Employees of your Bank have the knowledge to answer

your questions.

0.697

18. Your Bank has quick cash withdrawal through ATM. 0.607

19. Your bank has suitable ATM location. 0.707

20. Your bank has safe and secure ATM transaction. 0.774

21. Your Bank ATM machine is user friendly. 0.749

22. Your bank has alternative appearance of ATM. 0.640

23. Your Bank has excellent quality of currency. 0.620

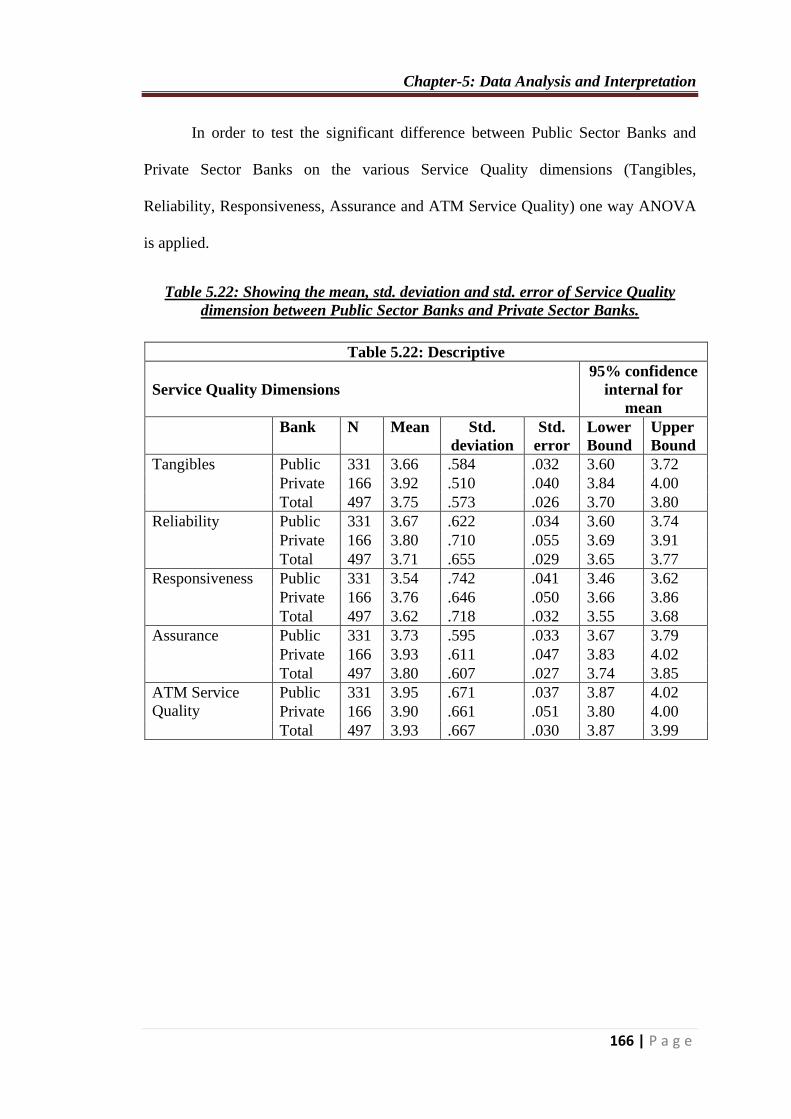

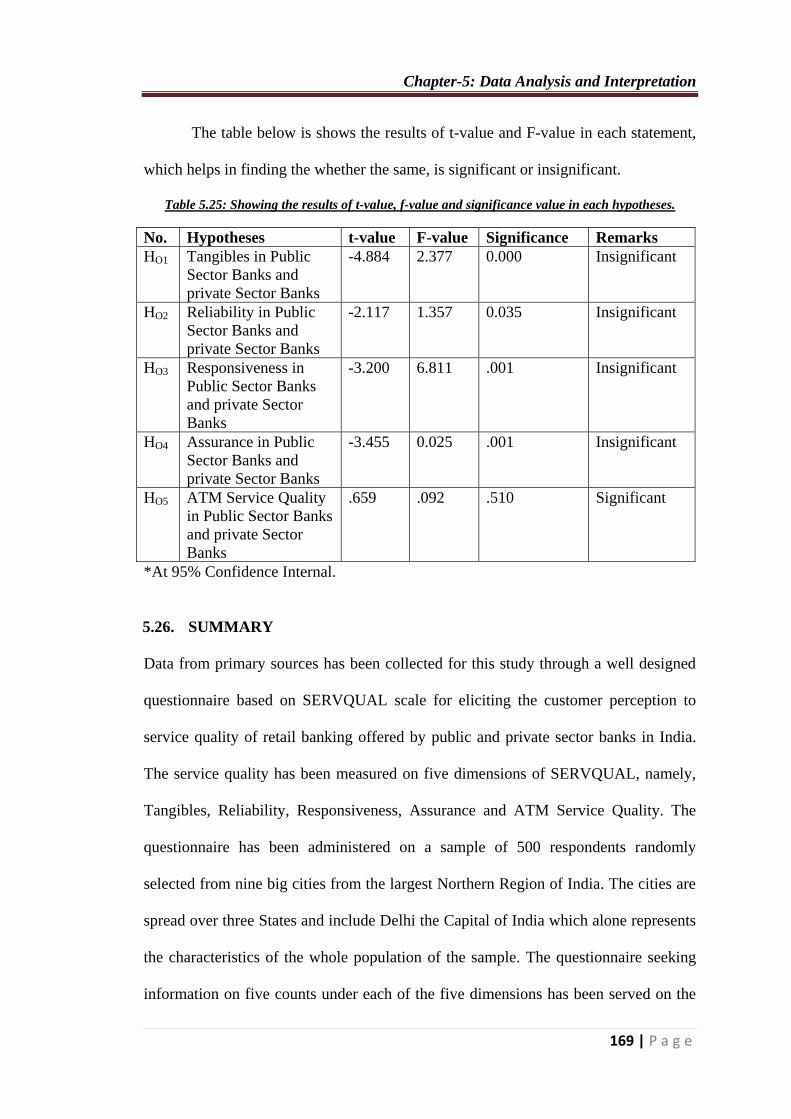

C. TESTING OF HYPOTHESES

Hypotheses testing are very important phase of the research process which determines

the results of the analysis. The primary data collected has been tabulated and

transferred to SPSS (Statistical package for Social Science) from Microsoft Excel

File. SPSS software has been used to analyze the primary data to test the hypotheses

of the study. Necessary statistical tools have been applied for the analysis of this

research while using SPSS software. The mean, One-Way ANOVA (analysis of

variance) and other statistical tests were used to compute the result.

Chapter-5: Data Analysis and Interpretation

153 | P a g e

For hypothesis testing mostly independent t-test and one way analysis of

variance (ANOVA) has been used for the analysis of data. In the present study

hypothesis were tested with the help of these two statistical tools.

Independent Samples t-test:

Independent samples t-test is used on the data if there are two independent samples

(or groups). It is used to compare the values of the means from two samples and test

whether it is likely that the samples are from populations having different mean

values. The independent t-test also called unpaired or the two samples t-test or

student’s t-test is an inferential statistical test that determines whether there is a

statistically significant difference between the mean in two groups (Cohen, 1998).

Independent t-test is used to compare the mean of a normally distributed

internal independent variable for two independent groups. When the two samples are

taken from the same population, it is very unlikely that the mean of the two samples

will be identical. When two samples are taken from two groups with different mean

scores, it is likely that the means of the two samples will differ.

For the present study comparing the mean values of the Public Sector banks

and Private Sector Banks on the different service quality dimensions of Retail

Banking in India. Independent t-test is used to signify the Hypothesis testing. When

reporting the result of an independent t-test, it is necessary to include the t-statistic

value, the degree of freedom and the significance value of the test (P-value).

The test result is computed as t (df)=t-statistic, P= significance value.

For computing the results statistical packages like SPSS is used. The data are

transferred to SPSS package and then compared the results. Statistical tests are

available to assess whether the two sample variance are significantly different. All

Chapter-5: Data Analysis and Interpretation

154 | P a g e

statistical tests produce a p-value and this is equal to the probability of obtaining the

observed difference, or one more extreme, if the null hypothesis is true. To put it

another way- if the null hypothesis is true, the p-value is the probability of obtaining a

difference at least as large as that observed due to sampling variation.

Consequently, if the p-value is small, the data support the alternative

hypothesis, if the p-value is large the data support the null hypothesis. A p-value of

0.05(5%) is generally regarded as sufficiently small to reject the null hypothesis. If

the p-value is larger than 0.01 then the null hypothesis is accepted. The significance

value considered for the present statistical test is 0.05(5%). The 1% value is also

commonly used in research to test the hypothesis.

In the present study there are only two levels of the independent variables (e.g.

Public Sector Banks and Private Sector Banks). If the data contains more than two

variables then t-test is inappropriate. For that purpose another statistical tool of

analysis of variance (ANOVA) is used.

One way analysis of variance(ANOVA)

One way analysis of variance (ANOVA) is used to determine whether there are any

significant differences between the means of three or more independent (unrelated)

groups. So it is used where there are more than two groups (Onwnegbuzie, 2002).

ANOVA determines the relationship of mean scores of more than two

variables. An ANOVA produces t-statistic or t-ratio, which is similar to the t-static in

that it compares the amount of systematic variances in the data to the amount of

unsystematic variance.

ANOVA is used to compare the variance (variability in scores) between the

different groups with the variability within each group. An ‘F’ ratio is calculated

Chapter-5: Data Analysis and Interpretation

155 | P a g e

which represents the variation between groups, divided by within the groups. A large

‘F’ ratio indicates that there is more variability between the groups.

To achieve the objects of the study, the following hypothesis were developed

for statistical testing.

Chapter-5: Data Analysis and Interpretation

156 | P a g e

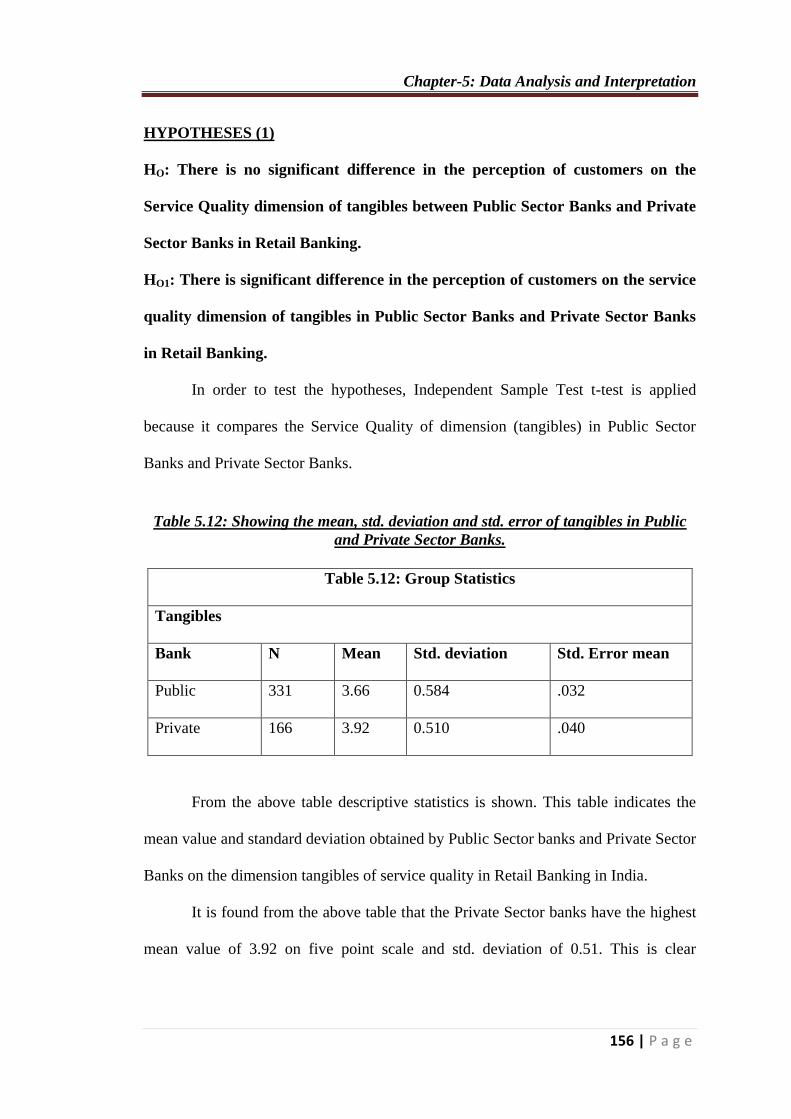

HYPOTHESES (1)

HO: There is no significant difference in the perception of customers on the

Service Quality dimension of tangibles between Public Sector Banks and Private

Sector Banks in Retail Banking.

HO1: There is significant difference in the perception of customers on the service

quality dimension of tangibles in Public Sector Banks and Private Sector Banks

in Retail Banking.

In order to test the hypotheses, Independent Sample Test t-test is applied

because it compares the Service Quality of dimension (tangibles) in Public Sector

Banks and Private Sector Banks.

Table 5.12: Showing the mean, std. deviation and std. error of tangibles in Public

and Private Sector Banks.

Table 5.12: Group Statistics

Tangibles

Bank N Mean Std. deviation Std. Error mean

Public 331 3.66 0.584 .032

Private 166 3.92 0.510 .040

From the above table descriptive statistics is shown. This table indicates the

mean value and standard deviation obtained by Public Sector banks and Private Sector

Banks on the dimension tangibles of service quality in Retail Banking in India.

It is found from the above table that the Private Sector banks have the highest

mean value of 3.92 on five point scale and std. deviation of 0.51. This is clear

Chapter-5: Data Analysis and Interpretation

157 | P a g e

indication that the customers of Private Sector Banks have a positive perception on

the dimension of tangible in comparison to Public Sector Banks.

Table 5.13: Showing the F-value and sig. value of Tangibles between Public and

Private Sector Banks.

Table 5.13: Independent Samples Test

Tangibles

Levene’s Test

for equality of

variances

T-test for equality of means

F Sig. t Df Sig. (2

tailed)

Mean

difference

Std. Error

difference

Equal

variance

assumed

2.377 0.124

-4.884 494 .000 -. 260 .053

Equal

variance

not

assumed

-5.107 373.082 .000 -. 260 0.051

Table 5.13 shows the results of independent samples test used to access the

difference with perception of customers towards the dimension of tangibles on the

ground of Service Quality in Public Sector Banks and Private Sector Banks.

The t-value is -4.884 and sig. value is 0.000 which is less than 0.05 (95

Percent Confidence Internal), which indicates that there exists difference in the

perception of customer in the Service Quality factor of Tangibles between Public

Sector Banks and Private Sector Banks.

Hence, the hypotheses that there is no significant difference in the perception

of customers on the service quality dimension of Tangibles in Public Sector Banks

and Private Sector Banks stands rejected and alternative hypotheses is accepted.

Chapter-5: Data Analysis and Interpretation

158 | P a g e

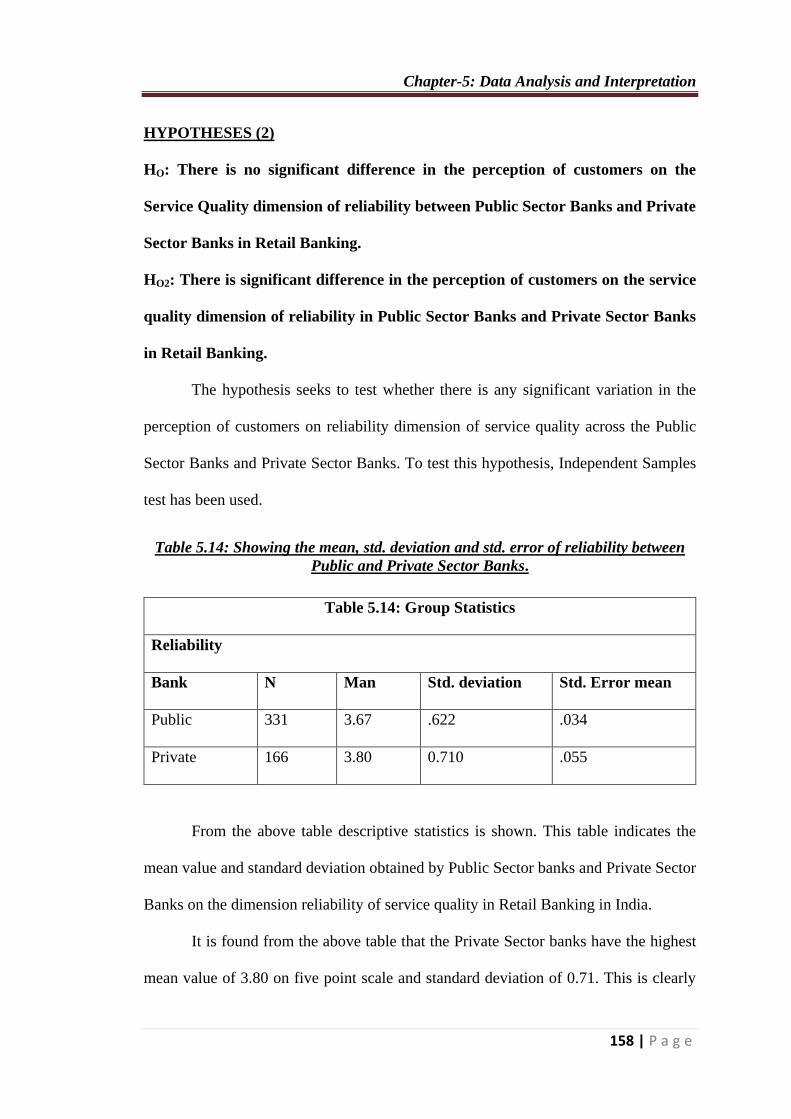

HYPOTHESES (2)

HO: There is no significant difference in the perception of customers on the

Service Quality dimension of reliability between Public Sector Banks and Private

Sector Banks in Retail Banking.

HO2: There is significant difference in the perception of customers on the service

quality dimension of reliability in Public Sector Banks and Private Sector Banks

in Retail Banking.

The hypothesis seeks to test whether there is any significant variation in the

perception of customers on reliability dimension of service quality across the Public

Sector Banks and Private Sector Banks. To test this hypothesis, Independent Samples

test has been used.

Table 5.14: Showing the mean, std. deviation and std. error of reliability between

Public and Private Sector Banks.

Table 5.14: Group Statistics

Reliability

Bank N Man Std. deviation Std. Error mean

Public 331 3.67 .622 .034

Private 166 3.80 0.710 .055

From the above table descriptive statistics is shown. This table indicates the

mean value and standard deviation obtained by Public Sector banks and Private Sector

Banks on the dimension reliability of service quality in Retail Banking in India.

It is found from the above table that the Private Sector banks have the highest

mean value of 3.80 on five point scale and standard deviation of 0.71. This is clearly

Chapter-5: Data Analysis and Interpretation

159 | P a g e

an indication that the customers of Private Sector Banks have a positive perception on

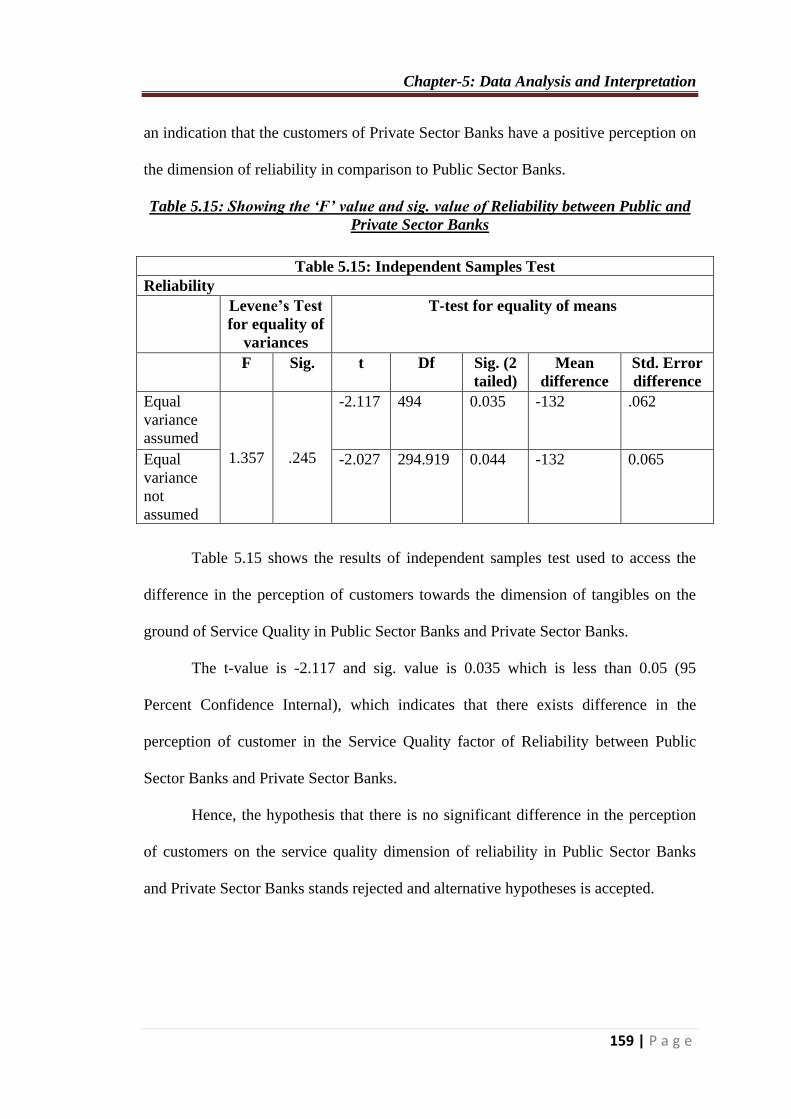

the dimension of reliability in comparison to Public Sector Banks.

Table 5.15: Showing the ‘F’ value and sig. value of Reliability between Public and

Private Sector Banks

Table 5.15: Independent Samples Test

Reliability

Levene’s Test

for equality of

variances

T-test for equality of means

F Sig. t Df Sig. (2

tailed)

Mean

difference

Std. Error

difference

Equal

variance

assumed

1.357 .245

-2.117 494 0.035 -132 .062

Equal

variance

not

assumed

-2.027 294.919 0.044 -132 0.065

Table 5.15 shows the results of independent samples test used to access the

difference in the perception of customers towards the dimension of tangibles on the

ground of Service Quality in Public Sector Banks and Private Sector Banks.

The t-value is -2.117 and sig. value is 0.035 which is less than 0.05 (95

Percent Confidence Internal), which indicates that there exists difference in the

perception of customer in the Service Quality factor of Reliability between Public

Sector Banks and Private Sector Banks.

Hence, the hypothesis that there is no significant difference in the perception

of customers on the service quality dimension of reliability in Public Sector Banks

and Private Sector Banks stands rejected and alternative hypotheses is accepted.

Chapter-5: Data Analysis and Interpretation

160 | P a g e

HYPOTHESES (3)

HO: There is no significant difference in the perception of customers on the

service quality dimension of Responsiveness between Public Sector Banks and

Private Sector Banks in Retail Banking.

HO3: There is significant difference in the perception of customers on the Service

Quality dimension of Responsiveness between Public Sector Banks and Private

Sector Banks in Retail Banking.

The hypothesis seeks to test whether there is any significant variation in the

perception of customers on responsiveness dimension of service quality across the

Public Sector Banks and Private Sector Banks. To test this hypothesis, Independent

Samples test has been used.

Table 5.16: Showing the mean, std. deviation and std. error of Responsiveness

between Public and Private Sector Banks.

Table 5.16: Group Statistics

Responsiveness

Bank N Mean Std. deviation Std. Error mean

Public 331 3.54 .742 .041

Private 166 3.76 .646 .050

From the above table descriptive statistics is shown. This table indicates the

mean value and standard deviation obtained by Public Sector banks and Private Sector

Banks on the dimension responsiveness of service quality in Retail Banking in India.

It is found from the above table that the Private Sector banks have the highest

mean value of 3.76 on five point scale and standard deviation of 0.64. This is a clear

Chapter-5: Data Analysis and Interpretation

161 | P a g e

indication that the customers of Private Sector Banks have a positive perception on

the service quality dimension of responsiveness in comparison to Public Sector

Banks.

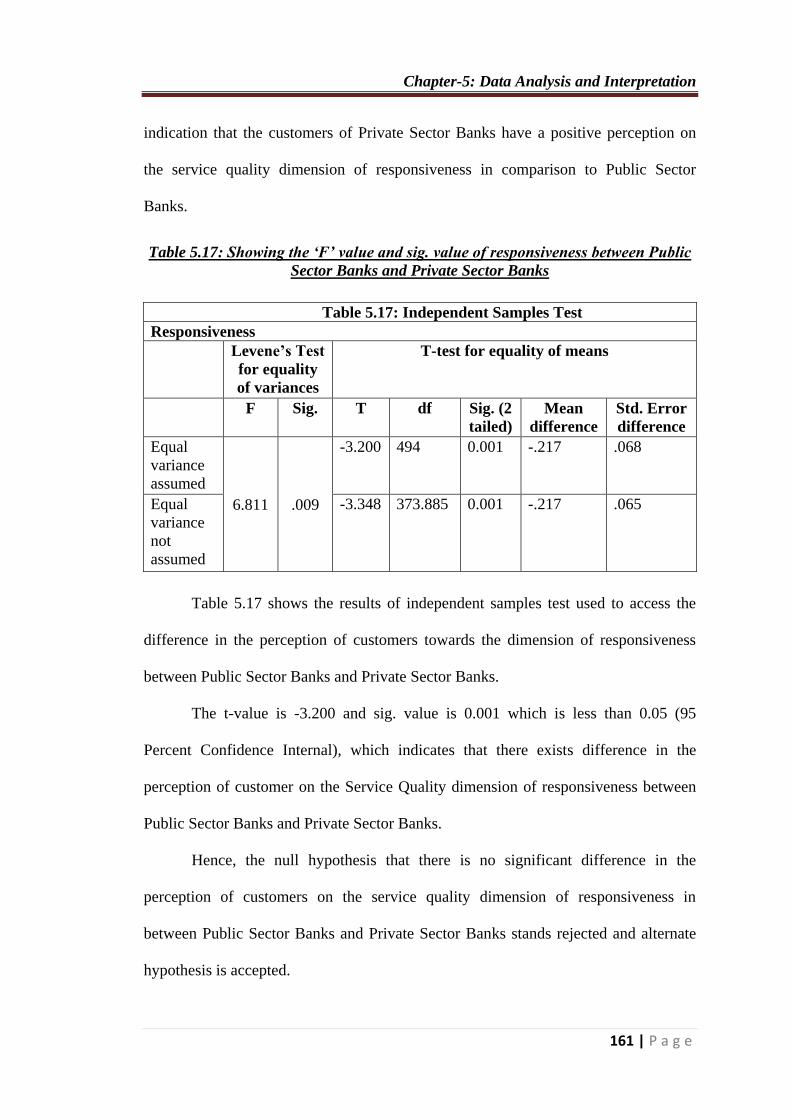

Table 5.17: Showing the ‘F’ value and sig. value of responsiveness between Public

Sector Banks and Private Sector Banks

Table 5.17: Independent Samples Test

Responsiveness

Levene’s Test

for equality

of variances

T-test for equality of means

F Sig. T df Sig. (2

tailed)

Mean

difference

Std. Error

difference

Equal

variance

assumed

6.811 .009

-3.200 494 0.001 -.217 .068

Equal

variance

not

assumed

-3.348 373.885 0.001 -.217 .065

Table 5.17 shows the results of independent samples test used to access the

difference in the perception of customers towards the dimension of responsiveness

between Public Sector Banks and Private Sector Banks.

The t-value is -3.200 and sig. value is 0.001 which is less than 0.05 (95

Percent Confidence Internal), which indicates that there exists difference in the

perception of customer on the Service Quality dimension of responsiveness between

Public Sector Banks and Private Sector Banks.

Hence, the null hypothesis that there is no significant difference in the

perception of customers on the service quality dimension of responsiveness in

between Public Sector Banks and Private Sector Banks stands rejected and alternate

hypothesis is accepted.

Chapter-5: Data Analysis and Interpretation

162 | P a g e

HYPOTHESES (4)

HO: There is no significant difference in the perception of customers on the

Service Quality dimension of Assurance between Public Sector Banks and

Private Sector Banks in Retail Banking.

HO4: There is significant difference in the perception of customers on the Service

Quality dimension of Assurance between Public Sector Banks and Private Sector

Banks in Retail Banking.

The hypothesis seeks to test whether there is any significant variation in the

perception of customers on the Service Quality dimension of assurance between the

Public Sector Banks and Private Sector Banks. To test this hypothesis, Independent

Samples test has been used.

Table 5.18: Showing the mean, std. deviation and std. error of Assurance between

Public Sector Banks and Private Sector Banks.

Table 5.18: Group Statistics

Assurance

Bank N Man Std. deviation Std. Error mean

Public 331 3.73 .595 .033

Private 166 3.93 .611 .047

From the above table descriptive statistics is shown. This table indicates the

mean value and standard deviation obtained by Public Sector Banks and Private

Sector Banks on the dimension assurance of Service Quality in Retail Banking in

India.

It has been found from the above table that Private Sector Banks have highest

mean value of 3.93 on five point scale and standard deviation of 0.61. This is a clear

Chapter-5: Data Analysis and Interpretation

163 | P a g e

indication that the customers of Private Sector Banks have a positive perception on

the Service Quality dimension of assurance in comparison to Public Sector Banks.

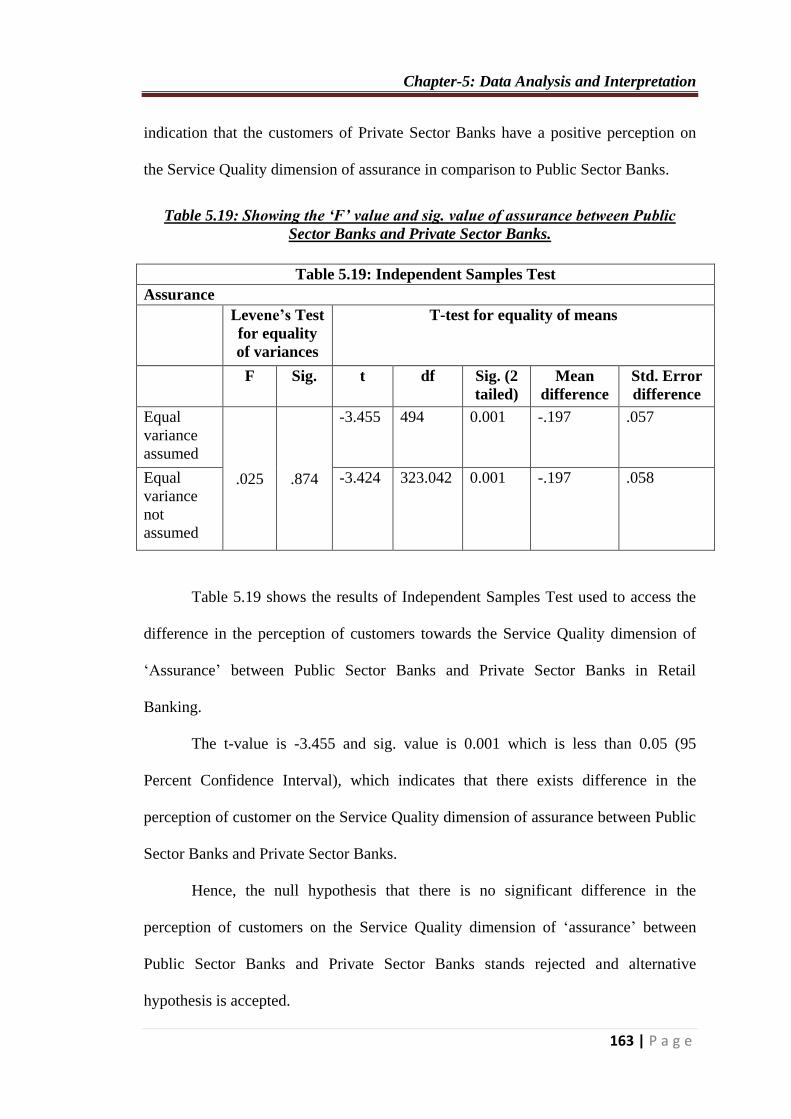

Table 5.19: Showing the ‘F’ value and sig. value of assurance between Public

Sector Banks and Private Sector Banks.

Table 5.19: Independent Samples Test

Assurance

Levene’s Test

for equality

of variances

T-test for equality of means

F Sig. t df Sig. (2

tailed)

Mean

difference

Std. Error

difference

Equal

variance

assumed

.025 .874

-3.455 494 0.001 -.197 .057

Equal

variance

not

assumed

-3.424 323.042 0.001 -.197 .058

Table 5.19 shows the results of Independent Samples Test used to access the

difference in the perception of customers towards the Service Quality dimension of

‘Assurance’ between Public Sector Banks and Private Sector Banks in Retail

Banking.

The t-value is -3.455 and sig. value is 0.001 which is less than 0.05 (95

Percent Confidence Interval), which indicates that there exists difference in the

perception of customer on the Service Quality dimension of assurance between Public

Sector Banks and Private Sector Banks.

Hence, the null hypothesis that there is no significant difference in the

perception of customers on the Service Quality dimension of ‘assurance’ between

Public Sector Banks and Private Sector Banks stands rejected and alternative

hypothesis is accepted.

Chapter-5: Data Analysis and Interpretation

164 | P a g e

HYPOTHESES (5)

HO: There is no significant difference in the perception of customers on the

Service Quality dimension of ATM Service Quality between Public Sector Banks

and Private Sector Banks in Retail Banking.

HO5: There is significant difference in the perception of customers on the Service

Quality dimension of ATM Service Quality between Public Sector Banks and

Private Sector Banks in Retail Banking.

The hypothesis seeks to test whether there is any significant variation in the

perception of customers on the Service Quality dimension of assurance between the

Public Sector Banks and Private Sector Banks.

To test this hypothesis, Independent Samples test has been used.

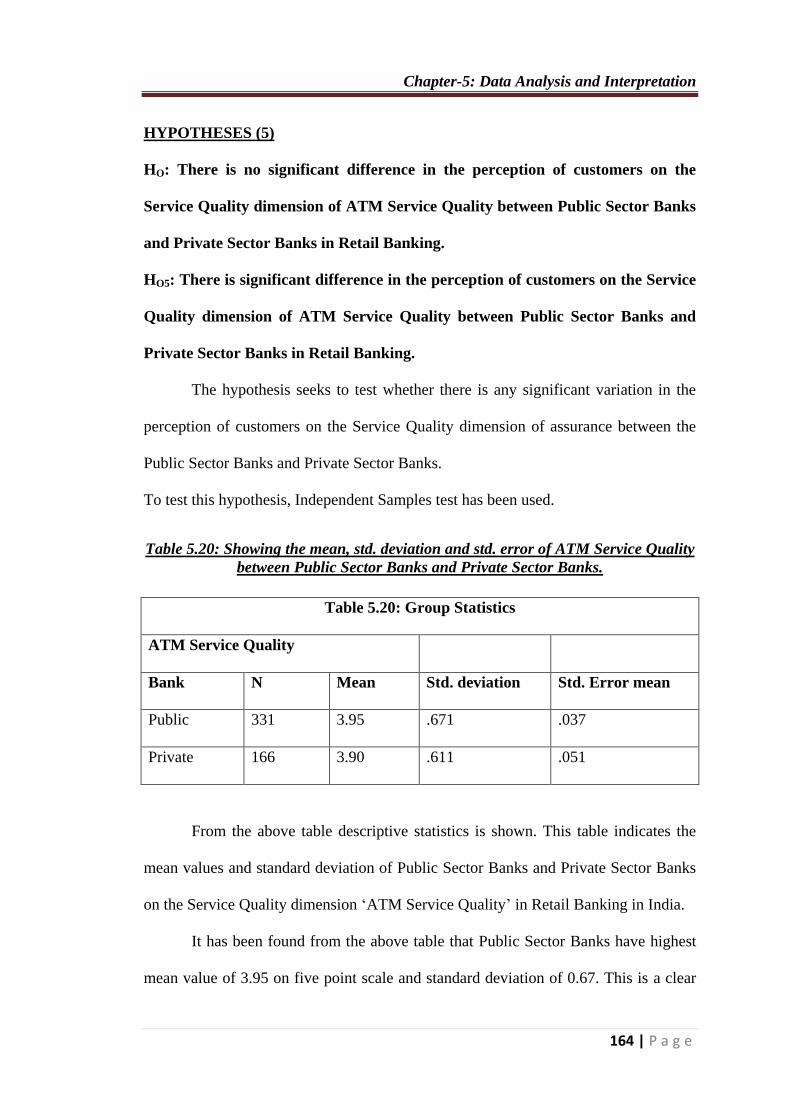

Table 5.20: Showing the mean, std. deviation and std. error of ATM Service Quality

between Public Sector Banks and Private Sector Banks.

Table 5.20: Group Statistics

ATM Service Quality

Bank N Mean Std. deviation Std. Error mean

Public 331 3.95 .671 .037

Private 166 3.90 .611 .051

From the above table descriptive statistics is shown. This table indicates the

mean values and standard deviation of Public Sector Banks and Private Sector Banks

on the Service Quality dimension ‘ATM Service Quality’ in Retail Banking in India.

It has been found from the above table that Public Sector Banks have highest

mean value of 3.95 on five point scale and standard deviation of 0.67. This is a clear

Chapter-5: Data Analysis and Interpretation

165 | P a g e

indication that the customers of Public Sector Banks have a positive perception on the

Service Quality dimension of ATM Service Quality in comparison to Private Sector

Banks.

Table 5.21: Showing the ‘F’ value and sig. value of ATM Service Quality between

Public Sector Banks and Private Sector Banks

Table 5.21: Independent Samples Test

ATM Service Quality

Levene’s Test

for equality of

variances

T-test for equality of means

F Sig. t Df Sig. (2

tailed)

Mean

difference

Std. Error

difference

Equal

variance

assumed

.092 .762

-.659 494 .510 .042 .064

Equal

variance

not

assumed

-.662 335.158 .508 .042 .063

Table 5.21 shows the results of Independent Samples Test used to assess the

difference in the perception of customers towards the Service Quality dimension of