dated 20 january 2021 - slough

TRANSCRIPT

64214407.1

Dated 20 January 2021

INQUIRY INTO THE SLOUGH BOROUGH COUNCIL (TOWER AND ASHBOURNE) COMPULSORY PURCHASE ORDER 2020

PROOF OF EVIDENCE OF NEALE COOPER COMMERCIAL AND HOUSING DEVELOPMENT

FINANCE MANAGER, SLOUGH BOROUGH COUNCIL

64214407.1 i

TABLE OF CONTENTS

No. Heading Page 1. INTRODUCTION 1

2. SCOPE OF EVIDENCE 2

3. GOVERNMENT GUIDANCE 3

4. THE COUNCIL’S FUNDING STRATEGY FOR THE SCHEME 4

5. OBJECTIONS 13

6. SUMMARY AND CONCLUSIONS 16

7. Declaration 17

64214407.1 1

1. INTRODUCTION

1.1 My name is Neale Cooper and I am the Commercial and Housing Development Finance

Manager for Slough Borough Council (the Council), a role I have held since August 2019. I

have worked for the Council since August 2012.

1.2 I am a fellow of the Chartered Institute of Public Finance and Accountancy and have almost

30 years of Local Government Finance experience.

1.3 I have been involved in the Tower & Ashbourne project since at least 2017. My role has

involved working with the Housing team and the Council’s external consultants, Savills, to

progress and secure funding for the comprehensive redevelopment of the site to create 193

new residential units (the Scheme) and to review the financial viability of the Scheme so as

to ensure that it will be delivered. References to the Scheme Land refer to the land shown

on the Scheme Plan at CD 2.1 (the Scheme Land).

64214407.1 2

2. SCOPE OF EVIDENCE

2.1 In my evidence, I explain the Council’s funding strategy for the Scheme, including the

commitments that the Council has already made through funding from the Housing

Revenue Account (the HRA) to meet the costs of the Scheme to date, including land

acquisition costs. I also explain the forward strategy for the delivery of the Scheme and its

operation. In doing so, I refer to and explain the decisions that the Council’s Cabinet has

made in order to ensure that the Scheme will be delivered so as to secure significant

wellbeing benefits including the 193 new, high quality affordable homes for the community.

2.2 My evidence also responds to objections insofar as they relate to areas within my expertise.

2.3 The Council has received independent advice from Savills on the funding strategy for the

Scheme and indeed in respect of options for its HRA housing stock more generally over a

number of years. My evidence should be read alongside that of Steve Partridge, of Savills,

who will explain the process for the financing of the redevelopment of the property.

64214407.1 3

3. GOVERNMENT GUIDANCE

3.1 In preparing this proof of evidence I have had regard to the Government's Guidance on

Compulsory Purchase Process and The Crichel Down Rules (the Guidance). Particular

regard has been had to those parts of the Guidance that are of relevance to funding and

delivery matters, specifically:

3.1.1 Paragraph 13, tier 1: Demonstrating that all the necessary resources are likely

to be available to achieve the Council’s intended use of the land within a

reasonable time-scale, in order to justify that the compulsory acquisition of the

land included in the order is justified in the public interest.

3.1.2 Paragraph 14, tier 1: Providing substantive information regarding the sources of

funding for acquiring the land and implementing the scheme. Where the scheme is

not intended to be independently financially viable or the details cannot be finalised

until there is certainty that the necessary land will be required, providing an

indication as to how potential shortfalls are intended to be ,et.

3.1.3 Paragraph 14, tier 1: Providing detail regarding the timing of funding and that it

is available now or will be available early in the process of delivering the scheme.

3.1.4 Paragraph 106, tier 2: Providing information about the potential financial

viability of the Scheme where a general indication of funding intentions, and of any

commitment from third parties, will usually suffice to reassure the Secretary of

State that there is a reasonable prospect that the scheme will proceed.

3.2 I consider that the funding arrangements that the Council has put in place for the

redevelopment of Tower House and Ashbourne House to deliver the Scheme meet all of

the above criteria and I will explain this in further detail in my evidence below.

64214407.1 4

4. THE COUNCIL’S FUNDING STRATEGY FOR THE SCHEME

The Council’s Financial Commitments to the Scheme to Date

4.1 The redevelopment of the two residential blocks known as Tower House & Ashbourne

House (the Existing Blocks) on the Scheme Land has been a major ambition and

commitment of the Council for a number of years. A number of key decisions have been

made by the Council’s Cabinet in recent years regarding the funding of the Scheme, a

summary of which is provided at Appendix 1 to my evidence.

4.2 The Council has funded the progress of the Scheme to date from the HRA. This account is

separate, and ‘ring-fenced’ from the Council's General Fund, and is the Council’s 'Landlord

Account' for its social housing stock. Slough’s HRA has over 6,000 properties and is

financially healthy with over £13m in general reserves as at 31st March 2020 plus £4m in

retained 1-4-1 Right to Buy receipts and a small amount of s106 funds. The HRA receives

its funding from the rental income and service charges from its housing, sale of council

houses, s106 monies and Government grants, but it can also borrow funds to build new

homes, repair existing housing, or redevelop its housing stock. Whereas there was

previously a borrowing cap set by the Government on HRA borrowing, this was lifted in

October 2018.

4.3 The Council initially identified funding for the Scheme in February 2016 (8th February

Cabinet) as part of its funding for major schemes from its HRA capital programme. The

HRA capital programme identifies funding for expenditure on the acquisition, construction,

major refurbishment, preparation, enhancement or replacement of its buildings and other

assets. The HRA capital programme funding for the Scheme has so far included paying for

the emptying of the blocks and the rehousing of tenants, and the design, planning,

consultation and demolition aspects of the Scheme to enable the replacement of the two

tower blocks.

4.4 Over £9m has been spent on the scheme by the HRA so far which indicates the Council’s

commitment to the delivery of the Scheme.

4.5 Of the £9m spent on the scheme by the HRA, the Council has spent over £3m to-date on

acquisition and associated costs for leaseholders at Tower and Ashbourne Houses, and this

has been funded from the HRA capital programme for this scheme. Similarly, the acquisition

costs associated with purchasing the leasehold interest in no. 54 Ashbourne House, the sole

remaining leasehold interest, will also be met by the HRA capital programme for this

scheme, as will any compensation associated with rights of light.

64214407.1 5

The Funding Strategy for the Delivery of the Scheme – Construction and

Operation

4.6 In this section of my evidence, I will explain the sources of funding available to implement

the Scheme and the timing of that funding. It is my view, in accordance with the CPO

Guidance, that the necessary resources are likely to be available within a reasonable

timescale and that there is every likelihood that the Scheme will proceed.

4.7 The Council has been planning the funding strategy of the Scheme for a considerable time,

and has taken advice throughout the process from Savills. As I have already explained, the

Council’s Cabinet has made consideration of the funding arrangements on a series of

occasions, including in particular at the following meetings – please see the table at

Appendix 1.

4.8 At the Cabinet meeting on 22 January 2018, having had regard to a detailed Housing

Options Appraisal report prepared by Savills, the Council’s Cabinet resolved to pursue the

option to raise private finance through a pension fund or institutional investment to deliver

new affordable rented housing in the borough, and in particular for the remodelling of the

Tower and Ashbourne site. On the same date, the Council’s Cabinet also approved “that

the Director for Finance & Resources, Neighbourhood Services Lead and Cabinet Member

for Corporate Finance & Housing, in conjunction with the recommendations of the Housing

Option Appraisal, determine the funding for the remodelling of the site”.

4.9 As is explained further in the evidence of Mr Partridge, the option adopted by the Council

bore fruit in that there was substantial interest in the financing of the project from

institutional investors, which resulted in the Council agreeing substantive heads of terms

with Legal and General Investment (L&G) in November 2019. L&G were chosen as they

best met the funding requirements of the Scheme, and provided the best funding ‘package’

to ensure the financial viability of the scheme. This was officially sanctioned through a

significant officer decision based upon the 22nd January 2018 Cabinet approval (CD 4.1) as

under the Council’s Constitution, certain decisions can be delegated by the Cabinet to

officers to be made on their behalf.

4.10 The initial arrangement was for the capital costs of the Scheme to be forward funded by

L&G but on 13 July 2020, the Council’s Cabinet gave approval for the Director of Finance

and Resources with the Lead Member to agree the option for the HRA to fund the

construction costs of the Scheme, and once completed, for the development to be re-

64214407.1 6

financed through the option of Institutional Funding to reimburse the HRA to invest in

other projects. These resolutions are recorded at CD 4.8.

4.11 The funding of the construction phase will be provided by the HRA drawing down short

term loans from the Public Works Loans Board (the PWLB) during 2021/22 and 2022/23

to match the construction phases of the project – this will be mirrored in the HRA capital

programme. The Council’s Cabinet on 12 October 2020 (CD 4.9) delegated authority to

the Director of Finance & Resources following consultation with Cabinet Member for

Housing & Community Safety to consent to supporting the Development Initiative for

Slough Homes Registered Provider (the DISH RP) with the provision of a conditional

supporting loan from the HRA, In a comparison between using the PWLB to fund the

construction costs during the construction period, and using Institutional Funding to

forward fund the costs from the start of the construction, it is more cost effective for the

Council to use short term PWLB funding than Institutional Funding.

4.12 The PWLB lending facility is operated by the UK Debt Management Office (the DMO) on

behalf of HM Treasury and provides loans to local authorities, and other specified bodies,

from the National Loans Fund, operating within a policy framework set by HM Treasury.

This borrowing is mainly for capital projects, including the building of affordable housing,

and is at beneficial interest rates that enables local authorities to fund major improvement

schemes e.g. roads, housing, leisure centres etc. without incurring expensive financing costs

for their residents. It is entirely usual for local authorities use PWLB to fund their

capital/major works programmes.

4.13 Providing local authorities follow professional principles, which are contained in the CIPFA1

Prudential Code, under the Prudential Framework, local authorities are able to make their

own judgements as to whether new borrowing is affordable and prudent. For the Council,

this is explained and outlined in the annual Capital Strategy report to Cabinet each February

and constitutes the formal approval basis on which the Council can apply to PWLB for

borrowing in accordance with its approved capital programme. Each February, the

Council’s Cabinet approves the forthcoming capital programme and the sources of funding

including the amount of borrowing from the PWLB; once approved, the Council will

request, and receive, loan funding from the PWLB which is usually paid the same day. In

1CIPFA (Chartered Institute of Public Finance and Accountancy) is a UK based international accountancy membership and standard setting body, and is the primary professional accountancy organisation overseeing accounting and financial matters in public sector organisations.

64214407.1 7

February 2020, Cabinet (Table 1 in the Appendix to the Treasury Management Strategy

202021 report) approved the increase in the HRA’s borrowing limits from the PWLB by

£20m across the next three years to meet initial development costs of new affordable

housing schemes being planned by the HRA, which can include some of the construction

costs of this development. These borrowing limits will now be sought to be revised through

the February 2021 report to Cabinet in order to increase the HRA’s borrowing limits again

to meet the full construction costs of this development. A budget of £55m will be included

in the HRA capital programme over the next two years to meet the construction cost of

this development.

4.14 The Council recently commissioned Savills to review the HRA’s borrowing capacity and

their summary conclusion in early October, based upon the HRA’s 30 Financial Business

Plan, was that Slough’s HRA has the capacity to borrow at least an additional £90m over

the next five years, which would be more than sufficient to meet the Tower and Ashbourne

development costs. On 12th October 2020, Cabinet granted delegated authority to

Director of Finance and Resources following consultation with the Cabinet Member for

Housing and Safety for the provision of up to £90m to be loaned to the DISH RP over the

next five years for the development and/or the delivery of affordable housing including the

Tower & Ashbourne development (CD 4.9). In December 2020, Savills produced their

‘HRA Business Plan and Capacity Review', in the format of a power point presentation, and

in that report they concluded, in the context of the current borrowing capacity of £168m,

that:

• Taken together, the assumptions in the business plan suggest increased capacity to

£250-300m in the next 10 years;

• Based on applying certain assumptions on income and costs, Savills consider that the

debt capacity could increase this capacity to approaching £400m in 10 years and

sustain further increases thereafter.

4.15 The Savills capacity report will be used as the evidence base to justify the updating of the

HRA’s ability to borrow to meet the costs of constructing the Scheme, and will be referred

to and incorporated into the ‘Treasury Management Strategy 2021/22’ and ‘Capital Strategy

2021 to 2025’ reports to Cabinet in February 2021.

4.16 Apart from borrowing from the PWLB, the HRA may also provide other sources of funding

to meet the construction costs such as retained 1-4-1 Right To Buy receipts, s106 funds,

revenue funding and other receipts.

64214407.1 8

4.17 Retained 1-4-1 Right To Buy receipts are the income that the Council receives when a

Council house is sold. Under a Government formula, the Council is allowed to retain a

certain amount of the sale price which it must use to help fund the costs of building new

affordable homes. Certain allowances are made for the cost of administration etc. but then

the remainder of the sale price has to be paid to the Government. These receipts can only

be used to fund up to 30% of the cost of new affordable housing and have to be used within

3 years of the sale of the property.

4.18 On the basis of the above, the Council is confident that the HRA will be able to provide the

resources required to deliver the construction phase of the Scheme at the appropriate

time.

Institutional Funding

4.19 As is explained further in Mr Partridge’s evidence, on completion of the construction phase

of the Scheme, the Council’s intention is that the Institutional Funder will be granted a long

lease (c. 125 years) and will lease back to the Council's nominated lease vehicle, the DISH

RP, for a forty year period on a FRI (full repair and insurance) basis with the lessee

acquiring the scheme for a nominal sum at the end of the lease. This will allow the DISH

RP to use the funding from the institutional funder to reimburse the HRA in respect of

construction costs so that it can invest in other projects for the delivery of affordable

housing within the Council’s area.

4.20 As I have already explained, towards the end of 2019, Heads of Terms were agreed

between the Council and the Institutional Funder. As Mr Partridge explains further, periodic

update meetings have been held to maintain the commitment between the two parties. The

funding arrangements for the construction of the Scheme have changed somewhat since the

end of 2019 in that the construction phase is proposed to be funded by the HRA and not

the Institutional Funder, and this has been reflected in the ongoing discussions with the

Institutional Funder. At the appropriate times, agreements will be put in place between the

Council and DISH RP, and between the DISH RP and the Institutional Funder to ensure the

funding is in place. The Council’s Cabinet gave approval on 12 October 2020 for the

Director of Finance & Resources following consultation with the Cabinet Member for

Housing & Community Safety to facilitate, by means of financial or other guarantees or such

other financial or other support considered to be reasonably necessary and in the best

interests of the Council, the provision of Institutional Finance arrangement to be taken out

by DISH RP (CD 4.9). In my view, relying on the evidence of Mr Partridge, there is every

64214407.1 9

reason to think that the funding from L&G will be forthcoming at the appropriate stage in

the process of delivering this Scheme.

Financial Viability

4.21 In this section of my evidence, I explain the basis upon which the Council considers that the

Scheme will be financially viable. I do this because paragraph 106 of tier 2 of the Guidance

indicates that information about the potential financial viability of the Scheme should be

provided, although it also states that a general indication of funding intentions and any

commitment from third parties should be sufficient to reassure the decision-maker that

there is a reasonable prospect that the Scheme will proceed.

4.22 As part of the evaluation of the offers submitted by the various interested institutional

investors in 2019, both Savills and the Council financially modelled the different offer rates

and terms. The conclusion of the financial modelling was that the utilising the funding from

the selected institutional funder, the development was financially viable, meeting all the

costs from the rental revenue and producing a ‘positive’ NPV (Net Present Value – a way of

evaluating the financial value of a scheme over a period of time); the Institutional Funder

offered rates for both funding the construction of the development as well as acquiring the

development upon completion and these were taken into consideration in the financial

modelling.

4.23 The Council, working with Savills, have undertaken analysis to ensure that the development

will be financially manageable over the life of the funding at affordable rents.

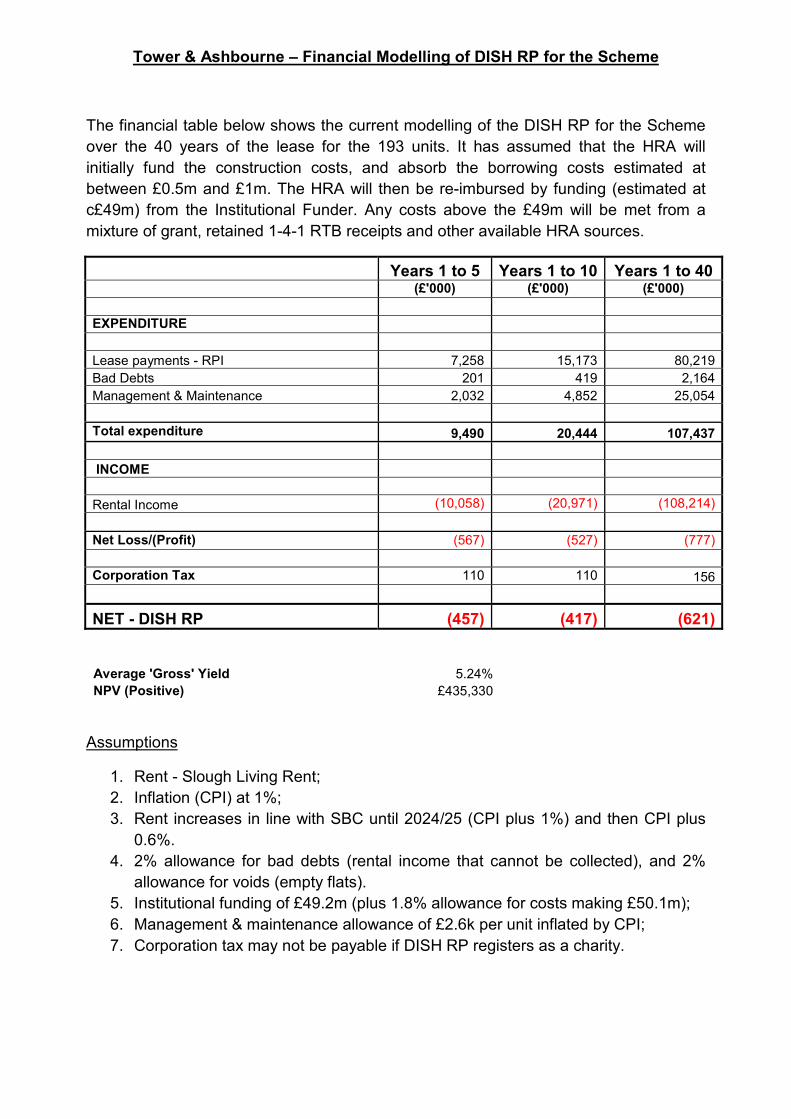

4.24 I have prepared a model (the Model), which can be found at Appendix 2, which

demonstrates that the development will be financially manageable for the DISH RP over the

period of the funding at Slough Living Rents.

4.25 The Model demonstrates that in applying realistic and robust variables the Scheme will

result in a net average gross yield of 5.24% and a total net profit of £621,000 over 40 years,

after repaying the total sum borrowed to funds its initial construction.

4.26 The Model is based on the HRA having funded the construction of the Scheme which is

currently expected to conclude in financial year 2022/23; the borrowing costs for funding

the construction of the Scheme are estimated at between £0.5m and £1m and will be

separately paid for by the HRA. Year one for the purposes of the Model is therefore

financial year 2023/24.

64214407.1 10

4.27 The Institutional Funder has currently valued the scheme at £49.2m. The Institutional

Funders fees estimated at 1.8% of the loan will also be added to the loan bringing the total

amount borrowed to £50.1m. The Model assumes borrowing at this amount.

Addressing the Model on a line by line basis:

Expenditure

Lease Payments – RPI

4.27.1 The lease repayments have been based on the DISH RP repaying the loan over the

term of a 40 year 'FRI (full repair and insurance)' lease. Lease repayments would be

increased on an annual basis by reference to the Retail Prices Index (RPI). For the

purposes of the Model RPI has been estimated at an annual rate of 1.7% which is

reasonable given recent historical trends.

Bad Debts

4.27.2 Bad debt is the total amount of rental income which the Model assumes will be

irrecoverable for various reasons but typically tenant default. The Model applies a

rate of 2% of income for bad debts which is based on advice from Savills on

schemes of this type.

4.27.3 Total bad debt at 2% has the effect of reducing the Scheme’s rental income by

£2,164,000 over the 40 year term of the loan.

Management and Maintenance

4.27.4 On advice from Savills following their consideration of the Scheme and its

specifications, the Model allows for an average £2,600 per unit per year to cover

maintenance and management costs. Maintenance costs have been profiled to be

lower per unit in the initial years but then increasing to allow for the higher costs

of maintaining over time. I consider this to be an adequate amount to meet both

day to day and annual maintenance costs as well as making provision for the larger

much more occasional expenses that may be required such as replacing the roof.

Expenditure

4.27.5 Taking into account the expected costs of managing the Scheme including lease

payments to the Institutional Funder, bad debts, void periods and management and

64214407.1 11

maintenance costs total expenditure is expected to be £9.4m in the first five years,

£20,444,000 in the first ten years and £107,437,000 over the total 40 year term of

the loan. These figures have been indexed by reference to the Consumer Price

Index (CPI) at an anticipated rate of 1% for years 1– 40. CPI has historically

fluctuated and I consider these to be reasonable assumptions for the current

purposes.

Income

4.27.6 The form of income for the Scheme is rental income. Rental Income has been

calculated by applying the current Slough Living Rent with an annual adjustment by

reference to the CPI plus an additional 1% for the first two years of the scheme

(2023/24 to 2024/25); increasing rent levels for units of this tenure in this way

complies with the Ministry for Housing Communities and Local Governments

published Policy Statement on rents for social housing (2020) (CD 8.5). After the

five year period covered in the Government’s Rent Policy (2020/21 to 2024/25),

the rental income has been increased by CPI plus 1% for 2025/26 and CPI plus

0.6% thereafter

4.27.7 The model also builds in a 2% 'void' period to allow for periods when units will not

be let as tenants are between lettings, marketing periods etc.; this is netted off the

rental income figure. Voids at 2% is based on the Council's own experience of

delivering social housing and likely to be much lower during the early part of the

lifecycle due to the desirability of the units and the fact units will typically be let on

assured short hold tenancies (AST's) of several years.

4.27.8 The model expects rental income in the first five years of the Scheme to be

£10,058,000, rental income in the first ten years to be £20,971,000 and total rental

income over the 40 year period to be £108,214,000.

Corporation Tax

4.27.9 Provision has been made for the payment of corporation tax on the rental income

at the amounts shown. However, the DISH RP is considering applying for

charitable status in which case the rental income will be corporation tax free.

Net Profit

64214407.1 12

4.27.10 The model expects net profit to be £457,000 in the first five years of the scheme,

£417,000 in the first ten years (the slight dip is due to the higher maintenance

costs expected after the initial years), and £621,000 over the 40 year period. If

DISH RP registers as a charity, net profits are expected to be higher as the rental

income will be exempt from corporation tax.

4.28 As part of the sensitivity testing, modelling has included construction costs up to a

maximum of £54.6m, increases in management & maintenance costs by up to 10%, lower

collection rates for rental income, and higher funder costs e.g. legal, SDLT etc. These all

showed that the Scheme is still viable at affordable rents.

I consider that the assumptions used in the model are prudent and reasonable, and that it,

along with the sensitivity testing that I have undertaken, demonstrates that the Scheme will

be financially viable.

64214407.1 13

5. OBJECTIONS

Objection: Mr Iftakhar of 54 Ashbourne House

5.1 Mr Iftakhar has made an objection on the basis that the Council has failed to provide

substantive information as to the sources of the funding available for both implementing the

development of the site and for acquiring the objector's interest in the land required and to

meet compensation claims from those affected by construction of the development. Mr

Iftakhar also suggests that information about the funding of the Scheme has not been put

into the public domain.

5.2 Further, Mr Iftakhar questions the Council’s financial position on the basis that he considers

that the Council is not able to ‘afford’ further borrowing, he thus questions the ability to

deliver the Scheme. He also refers to the potential for the Council to provide a subsidy

from its capital resources and questions whether this has been taken account of.

5.3 Mr Iftakhar also refers to the wholly owned subsidiary not yet having been identified by the

Council.

Response to the Objection

5.4 I do not consider that Mr Iftakhar’s concerns as to funding are justified. In relation to

sources of funding for implementing the Scheme and for compensation payments, I have

provided detailed information regarding the commitments already made to the Scheme

through the HRA capital funding, which will also cover compensation payments. I have also

explained the funding strategy for the delivery of the Scheme once vacant possession has

been gained. I believe that the information provided by the Council and the strategy that it

has adopted accords entirely with the expectations of the CPO Guidance.

5.5 Information about the funding has been in the public domain through a number of Cabinet

reports since 2016 which have provided substantive information as to the proposed funding

arrangements. It is not accurate for Mr Iftakhar to say that this information has not been

put in the public domain.

5.6 With regard to the Council’s financial position, Mr Iftakhar refers to a Cabinet meeting that

took place on the 3rd February 2020, where a forecast overspend was referred to. That

forecast overspend related to the Council’s General Fund and not the HRA. The healthy

financial position of the HRA is addressed in paragraph 4.2 above and the HRA’s ability to

‘afford’ further borrowing is explained in paragraphs 4.10 to 4.19. Should a subsidy be

64214407.1 14

required from the HRA, this can be met from its retained 1-4-1 RTB receipts (£2.5m in

2021/22 and £2m estimated in 2022/23), s106 funds or revenue contributions.

5.7 With regard to the identification of a subsidiary, the DISH RP has been identified as the

body that will take forward the Scheme.

Objection: Mr Fajurally

5.8 Mr Fajurally, a non-qualifying objector, made an objection on the grounds that he considers

that the Council most likely has not allocated funding for the development because it is

‘£750m in debt’. Mr Fajurally also refers to a section of the Savills Housing Options

Appraisal Report within the January 2018 Cabinet papers, where it was stated that the

Council would not be able to deliver the Tower and Ashbourne House Scheme by relying

on the HRA due to the borrowing cap that was then in place.

Response to the Objection

5.9 I have explained in detail the funding arrangements that the Council has put in place for the

delivery of the Scheme and it is therefore not accurate for Mr Fajurally to suggest that the

Council has not allocated funding for the development.

5.10 Further, it is not clear the basis upon which Mr Fajurally considers that the Council is

‘£750m in debt’. In any event, it is wrong for Mr Fajurally to suggest that Council borrowing

may act as an impediment to the funding of the Scheme. As at 31st December 2019, the

Council had £569.133m borrowing (of which £125.841m was HRA Government approved

self-financing borrowing from 2012) and £32.075m investments. A Local Authority’s need

to borrow is measured by its Capital Finance Requirement (CFR). CIPFA’s prudential code

for Capital Finance in Local Authorities recommends that the Authority’s total debt should

be lower than its highest forecast CFR over the next three years. The highest forecast of

the Council’s CFR over the three year period 2020/21 to 2022/23 is £833m. The total debt

over this period is expected to be £732m and so the Council’s position complies with the

nationally recommended borrowing guidance (‘Treasury Management Strategy 2020/21’ to

3rd February 2020 Cabinet meeting at CD 4.7).

5.11 As I have explained above, HRA funding for the development has been included since 2016

in the annual capital budget reports to Cabinet. In February 2020, Cabinet approved the

HRA’s ability to borrow an additional £20m, and this will be further adjusted in the

February 2021 Treasury Management report to Cabinet to include the borrowing in the

HRA’s capital programme to fully meet the costs of the Scheme. As well as borrowing, the

64214407.1 15

HRA also has access to 1-4-1 Right To Buy receipts, s106 monies, and reserves should this

be required.

5.12 Finally, Mr Fajurally’s reference to the January 2018 Savills Housing Option Appraisal Report

is taken out of context. In that report, Savills’s recommendation to the Council was that it

look to pursue institutional funding to deliver the Scheme. Savills did not conclude that due

to the HRA borrowing cap then in place, the development could not be delivered; quite the

contrary in that the Savills report put forward a deliverable option for the Scheme that the

Council has successfully pursued.

64214407.1 16

6. SUMMARY AND CONCLUSIONS

6.1 The Council has thought carefully about the funding arrangements for the Scheme over a

number of years and has been advised by Savills throughout the process. The Scheme has

been independently assessed as financially deliverable and funding sources identified and

approved. It has adopted an approach that is in my view robust, considered and will, in all

likelihood, lead to the successful delivery and operation of the Scheme for the benefit of the

community.

6.2 I consider that the Council has demonstrated that all relevant aspects of the CPO Guidance

are met. As I have explained above, the objections that have been made that relate to my

area of expertise are not correct or justified.

64214407.1 17

7. Declaration

7.1 As a member of the Chartered Institute of Public Finance and Accountancy (CIPFA), I am

required to comply with the International Ethics Standards Board’s International Code of

Ethics for Professional Accountants, which has been adopted by CIPFA as its Standard of

Professional Practice.

7.2 I confirm that I am acting in the capacity of a Finance Witness for Slough Borough Council

in providing the following evidence to the Inquiry and have done so in compliance with the

International Code of Ethics for Professional Accountants and make the declaration below

to the effect that:

• I confirm that my replies have drawn attention to all material facts which are relevant

and have affected my professional opinion.

• I confirm that I understand and have complied with my duty to the Inquiry as a finance

witness which overrides any duty to those instructing or paying me, that I have given my

evidence impartially and objectively, and that I will continue to comply with that duty as

required.

• I confirm that I am not instructed under any conditional or other success-based fee

arrangement.

• I confirm that I have no conflicts of interest.

.........................................

Neale Cooper FCPFA, BCom(Hons)

20 January 2021

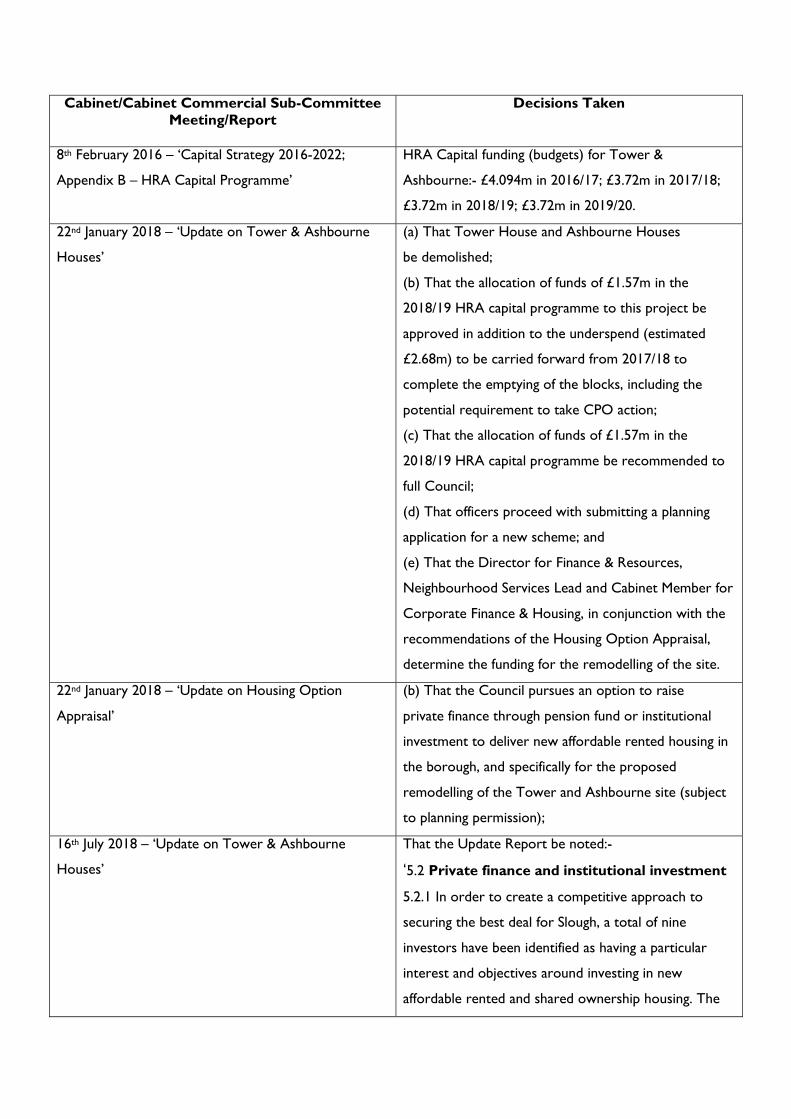

Cabinet/Cabinet Commercial Sub-Committee Meeting/Report

Decisions Taken

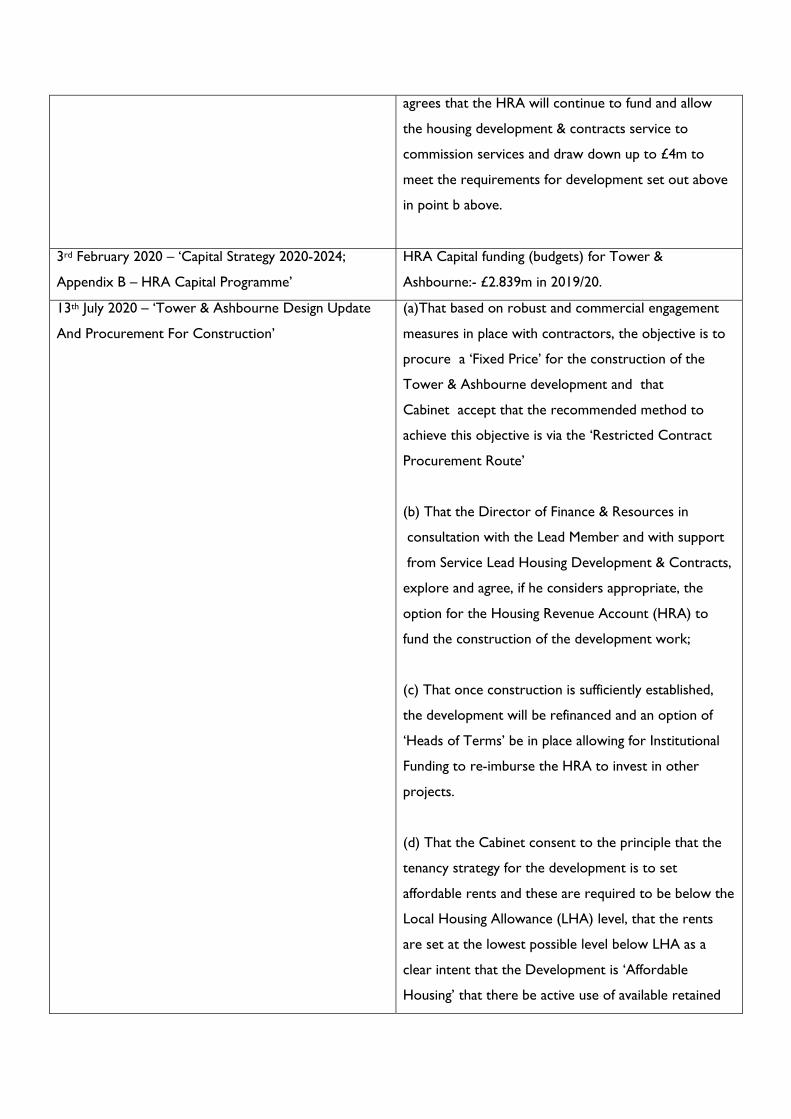

8th February 2016 – ‘Capital Strategy 2016-2022;

Appendix B – HRA Capital Programme’

HRA Capital funding (budgets) for Tower &

Ashbourne:- £4.094m in 2016/17; £3.72m in 2017/18;

£3.72m in 2018/19; £3.72m in 2019/20.

22nd January 2018 – ‘Update on Tower & Ashbourne

Houses’

(a) That Tower House and Ashbourne Houses

be demolished;

(b) That the allocation of funds of £1.57m in the

2018/19 HRA capital programme to this project be

approved in addition to the underspend (estimated

£2.68m) to be carried forward from 2017/18 to

complete the emptying of the blocks, including the

potential requirement to take CPO action;

(c) That the allocation of funds of £1.57m in the

2018/19 HRA capital programme be recommended to

full Council;

(d) That officers proceed with submitting a planning

application for a new scheme; and

(e) That the Director for Finance & Resources,

Neighbourhood Services Lead and Cabinet Member for

Corporate Finance & Housing, in conjunction with the

recommendations of the Housing Option Appraisal,

determine the funding for the remodelling of the site.

22nd January 2018 – ‘Update on Housing Option

Appraisal’

(b) That the Council pursues an option to raise

private finance through pension fund or institutional

investment to deliver new affordable rented housing in

the borough, and specifically for the proposed

remodelling of the Tower and Ashbourne site (subject

to planning permission);

16th July 2018 – ‘Update on Tower & Ashbourne

Houses’

That the Update Report be noted:-

‘5.2 Private finance and institutional investment

5.2.1 In order to create a competitive approach to

securing the best deal for Slough, a total of nine

investors have been identified as having a particular

interest and objectives around investing in new

affordable rented and shared ownership housing. The

investors range from pension funds, institutions

managing insurance and private pension funds, together

with ethical investors operating funds with a social

purpose.

5.2.2 These investors have been approached with a

"teaser" inviting investment into the

proposed Tower and Ashbourne redevelopment

scheme for 195 new homes with an estimated cost of

between £30-35million. The investors are being invited

to discuss terms for the provision for both

Development Funding (to ensure that the scheme can

be built) and Investment Funding - long-term finance for

the scheme. investors have responded very positively

to date and all nine have entered into Non-Disclosure

Agreements with Savills within a matter of days of the

scheme being presented to them.

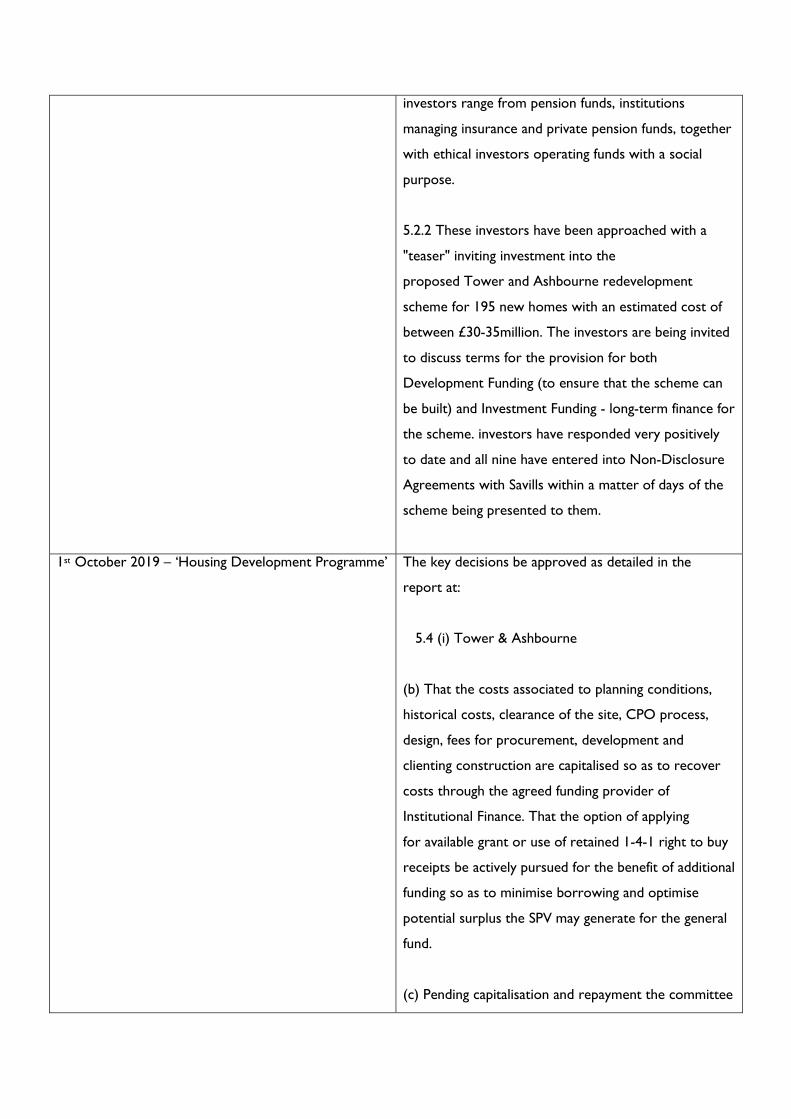

1st October 2019 – ‘Housing Development Programme’ The key decisions be approved as detailed in the

report at:

5.4 (i) Tower & Ashbourne

(b) That the costs associated to planning conditions,

historical costs, clearance of the site, CPO process,

design, fees for procurement, development and

clienting construction are capitalised so as to recover

costs through the agreed funding provider of

Institutional Finance. That the option of applying

for available grant or use of retained 1-4-1 right to buy

receipts be actively pursued for the benefit of additional

funding so as to minimise borrowing and optimise

potential surplus the SPV may generate for the general

fund.

(c) Pending capitalisation and repayment the committee

agrees that the HRA will continue to fund and allow

the housing development & contracts service to

commission services and draw down up to £4m to

meet the requirements for development set out above

in point b above.

3rd February 2020 – ‘Capital Strategy 2020-2024;

Appendix B – HRA Capital Programme’

HRA Capital funding (budgets) for Tower &

Ashbourne:- £2.839m in 2019/20.

13th July 2020 – ‘Tower & Ashbourne Design Update

And Procurement For Construction’

(a)That based on robust and commercial engagement

measures in place with contractors, the objective is to

procure a ‘Fixed Price’ for the construction of the

Tower & Ashbourne development and that

Cabinet accept that the recommended method to

achieve this objective is via the ‘Restricted Contract

Procurement Route’

(b) That the Director of Finance & Resources in

consultation with the Lead Member and with support

from Service Lead Housing Development & Contracts,

explore and agree, if he considers appropriate, the

option for the Housing Revenue Account (HRA) to

fund the construction of the development work;

(c) That once construction is sufficiently established,

the development will be refinanced and an option of

‘Heads of Terms’ be in place allowing for Institutional

Funding to re-imburse the HRA to invest in other

projects.

(d) That the Cabinet consent to the principle that the

tenancy strategy for the development is to set

affordable rents and these are required to be below the

Local Housing Allowance (LHA) level, that the rents

are set at the lowest possible level below LHA as a

clear intent that the Development is ‘Affordable

Housing’ that there be active use of available retained

1-4-1 RTB Receipts and s106 Housing funding or

successful application for Homes England Grant to

reduce further the rent levels to lowest possible viable

level;

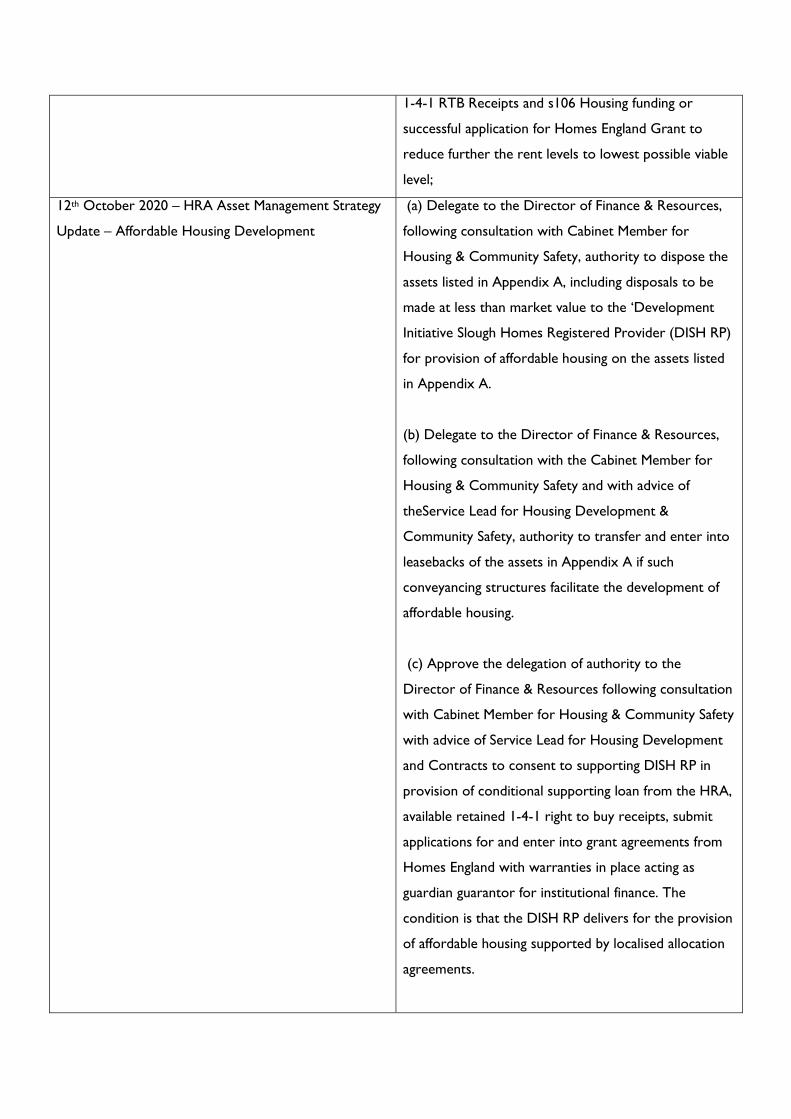

12th October 2020 – HRA Asset Management Strategy

Update – Affordable Housing Development

(a) Delegate to the Director of Finance & Resources,

following consultation with Cabinet Member for

Housing & Community Safety, authority to dispose the

assets listed in Appendix A, including disposals to be

made at less than market value to the ‘Development

Initiative Slough Homes Registered Provider (DISH RP)

for provision of affordable housing on the assets listed

in Appendix A.

(b) Delegate to the Director of Finance & Resources,

following consultation with the Cabinet Member for

Housing & Community Safety and with advice of

theService Lead for Housing Development &

Community Safety, authority to transfer and enter into

leasebacks of the assets in Appendix A if such

conveyancing structures facilitate the development of

affordable housing.

(c) Approve the delegation of authority to the

Director of Finance & Resources following consultation

with Cabinet Member for Housing & Community Safety

with advice of Service Lead for Housing Development

and Contracts to consent to supporting DISH RP in

provision of conditional supporting loan from the HRA,

available retained 1-4-1 right to buy receipts, submit

applications for and enter into grant agreements from

Homes England with warranties in place acting as

guardian guarantor for institutional finance. The

condition is that the DISH RP delivers for the provision

of affordable housing supported by localised allocation

agreements.

(d) Delegate authority to the Director of Finance &

Resources following consultation with the Cabinet

Member for Housing & Community Safety to make all

necessary arrangements (including the entry into loan

and other financing agreements) for up to £90m to be

loaned to the DISH RP over the next 5 years on terms

that require the DISH RP to develop and/or deliver the

affordable housing as set out in appendix D.

(e) Delegate authority to the Director of Finance &

Resources following consultation with the Cabinet

Member for Housing & Community Safety to facilitate,

by means of financial or other guarantees or such other

financial or other support considered to be reasonably

necessary and in the best interests of the Council, the

provision of Institutional Finance arrangement to be

taken out by DISH RP.

Tower & Ashbourne – Financial Modelling of DISH RP for the Scheme

The financial table below shows the current modelling of the DISH RP for the Scheme over the 40 years of the lease for the 193 units. It has assumed that the HRA will initially fund the construction costs, and absorb the borrowing costs estimated at between £0.5m and £1m. The HRA will then be re-imbursed by funding (estimated at c£49m) from the Institutional Funder. Any costs above the £49m will be met from a mixture of grant, retained 1-4-1 RTB receipts and other available HRA sources.

Years 1 to 5 Years 1 to 10 Years 1 to 40 (£'000) (£'000) (£'000) EXPENDITURE Lease payments - RPI 7,258 15,173 80,219Bad Debts 201 419 2,164Management & Maintenance 2,032 4,852 25,054 Total expenditure 9,490 20,444 107,437 INCOME Rental Income (10,058) (20,971) (108,214) Net Loss/(Profit) (567) (527) (777) Corporation Tax 110 110 156

NET - DISH RP (457) (417) (621)

Average 'Gross' Yield 5.24% NPV (Positive) £435,330

Assumptions

1. Rent - Slough Living Rent; 2. Inflation (CPI) at 1%; 3. Rent increases in line with SBC until 2024/25 (CPI plus 1%) and then CPI plus

0.6%. 4. 2% allowance for bad debts (rental income that cannot be collected), and 2%

allowance for voids (empty flats). 5. Institutional funding of £49.2m (plus 1.8% allowance for costs making £50.1m); 6. Management & maintenance allowance of £2.6k per unit inflated by CPI; 7. Corporation tax may not be payable if DISH RP registers as a charity.

�

����������� ��

��������������� ��������� �������������

��� ��� ���������������������� �� � � ������ ��������������������� ���� ����!�������

�������"���#������$���������������%�������� �&'������������ �������������(�������)�*����

�� ��+��,���"���������������������(�������)����

��� ��� ���"����+��"��������������������������"�-�.����!�����������(���������������� ���� ����

/)�������"�0�����1� ��� ����!��������2����������

��/ ���� ��.������ �� ����������3�+���4�(��.���������5���� ����������������)��������������

�� �� ���+��,����+������������������� ����������������6���2������������������'�#� ����'����

��������������������"�������"��������� �������� ������ ���� �����"���������������������*/�

��+�������������������%����������&���������� ��+�����"��������� ��.������"�����#��� ��������

������������������+����.������ ������7�"���������������#��� ��0������"������������������+��

�������#��� ��-��������������%���������������&�

�

�

�

����������� ��

�� ������������������

��� ��� � � ������'� �� �2������ ���� �������6�� "������� �������� "��� ���� #��� �'� ���������� ����

�� �� ����� ����� ���� �������� ���� ������� ���� �������� "������� "�� � ���� ��������

7� ����� (������� %������ &� ��� ���� ���� �������"� ����#��� �� ��� ����'� ���������������

��8������������������������2����������"��+������������"����������� ����"�����#��� ����������

����������������������'�����"�����������2������������������������������������6����.���������

������������� ��� ������� ����� ����#��� ��+����.�� ���� ����� ��� ��� ��� ������� �����"������

+���.�����.���"�������������������*/���+'������8�������""����.����� ���"��������� ������

��� �� �������������������������.5������������"��������������������������+������ ��2����������

��/ �� ��������������.�����������������������"�#�� ��-��������'��"�#� ����'�+���+�����2����������

��������"�������"����������"��������� ���� �����"��������������

�

����������� /�

/� !�����"����!��� ����

/�� ����������������������"��"�� ������� �� �� ������������� ��� ����1� ��� ���9��1�����������

�� �������-��������-������� ���� 3�������������+��7����� %����!� �����&��-����������

�����������.�������� ����������������"�����1������������� �����"����� ����� ���"�����������

���� ��� ��������

/�� �� ��������� ����� ���� "������� ������� ����� ����� ���� �������� ���� ���� ��� ������ "��� ����

���� ���� �����"�3�+�������������(��.������������������� �������#��� �� ���������"�

�����.� �����������������+�����2��������������"����������������� �� �������.���+��

�

����������� ��

�� �����������#��������!���� ��!$�������������"��

�������� �#%�� ���� ������ &���&%�&�&����������&���&��

��� 3������� ���� �����"� ���� �+��������������.���,��,��+����� 3�+���������4�(��.������

������ %���� �' %& �(� )��*%&� ��� ���� #��� �� 0���� ���� .���� �� �5��� � .������ ����

�� �� �����"�������������"������� .����"�������(��� .����"�,�������������� ��.����

����.� �����������6����.������������������������������ ����"��������"� ����#��� �'� ��

�� ����"�+����������� ��������(������2������ �����"��"�� ��������

��� 3���������������"��������������������"�����#��� ����������"�� ������7(��3���������������

��������'�����:����;"�����6�"�� ������������9��1�������!���'�������������������6��90��������

(������9� "��� ���� ������� �������� ����,�� #�����6�� �7(� ���� � ��� �')))� ����������� ���� ���

"�����������������+����� ���<�/ ����������������� ���������/����������)�)������<� ����

����������;�;��7��������$������������������ ����� ������"���)��"�������

��/ 3��� �������� ��������� ������"���� "������� "��� ���� #��� �� ��� !�.����� �)��� %���� !�.�����

��.����&����������"�����"�������"��� �5������� ���"�� ������7(��������������� �'��������

/���!�.������)�)���.������������ :��������#������=��)�)� ��� �)��6� %������)&�� 3����7(�

�������������� ��������"����"�������"����2�������������������8��������'�������������'� �5���

��"��.��� ���'������������'�������� �������������� �����"�����.���������������������������

3����7(� �������������� ��"�������"��� ����#��� �� ���� ���"������������������"��� ����

� �������"�����.���,���������������������"��������'���������������'���������'��������������

������ �����������������"�����#��� ��������.�������������� �����"������+����+���.���,���

���� ���� �(� �&��&�(�� �� &��� ��� ����� � &��� ������� +� ��%&���& �� ����

�,���& ��

��� ��� �� ������'���+�����2�������������������"�"�������� ����.������� ��� ��������#��� ������

���� �� �����"������"�������������� � ��+'���������������+���� �����->�1�������'� ����� ����

�������������������������,������.��� ����.���+���������������.����� �������������������������

� �����,�����������������#��� ��+��������������

��? �� ���������������������������6����.����9�����������������"�����"�������������� ��������

���� ��.��� ��� (������2� �� ���������� ���� ���������� ��� �������� �������� "���� ��� ��������������

�� ��� ���� ������� �����+��""����.�������������������������.������'�������������������"���

������ ����������"�����3�+�������(��.�������������

�

����������� ?�

��� ��+�����������'�������5��������+���� ���� � ��������"���-��������'� ��+� �������������������

��.������ ���������"���� ��+����0���������1��������� ��� ���� %041&������ � .����)�*��

041�+������������������.���� �������"���������8���� ������"�����#��� �'�������� �����

����.����"�������:���,���6���������������"��������� ��.������"��������� ���3����+����""�������

��������������������������"�������""��������������.�������������������@�������)�����.�����

����� ���%������&��

��� �� ������� �2���������+� ����"��������"����� �������������������+����.����� �����.� ����

�7(����+������+�������� ��� �������"�� �����-�.����A��,��0�����$����� %�����-�)&�

��������)��B��������)��B�/���� ������������������������������"��������5����C������+����.��

����������������7(��������������� ���3����������6����.�����������>���.����)�)�%���

��*&�������������������������������������"�!�������4�7����������������������������������

������ ���� ������������ ��"���#�������� ���7����������-�� �����%�����������&�+��������

��� �������"�������������������������������"�� ������7(' ��

��� -�� ������������������������"����+����"�������������������������������������������.������ �,��

�������+��5���� ����� ��� ���+���������+�.����+������� �""����.��� �������������!��� ����

�������'����������2�������������������������������������������#�������������������.����������

!�.����� ���� ������������ ����"�� ��� ����� ���.��������+����� ������������ ���� ����� ���

-A0$�"���.����+������������������+������������� ����������������� ����D����!�.����'�

�����������6����.����� ����� ��� ����"������ ���� �������������� �� ���� ���� ���������"�

"����������������� ���� � ������"�.����+����"�� � ����-A0$��� � ������� �2������� ��+�

������.����+������ ����+������+�.�� ������� ���.���� ����� ���� ��.�������"�<?? �+����.��

�����������������7(��������������� ��� ���������2���+���������� ���������������������

������"�������� ���� ������

��* 3������������������� �� ���������#� ����� ����� ��+� �����7(6��.����+������������ ����

�������� ����������������������>���.��'�.���������������7(6�� /)�!���������$��������

-���'�+��� �����#�����6���7(����� ���������������.����+������������������������<*) �� ���

������2��"� ������'�+�����+�����.�� �����������""���������� ��������3�+�������(��.������

�� ���� ���� ������� >�� ����� >���.��� �)�)'� ��.����� �������� ���������� ��������� ���

����������"�!������� ����7���������"����+���� �������������+���� ������.������ .���"���

������������#�"���"���������� �������"�������<*) ����.������������������#��7-�� �������

��2��"� �������"��������� ���� �������B����������� ����"��""����.�������������������������

3�+���4�(��.�������� ���� ����%�����*&���

���) (� �������� ������� ��������� .� #� ����� +���� .�� ����� ��� ���� � ������� .���� ��� 5����"� ����

����������"������7(6���.��������.����+���� ���������������"������������������#��� �'�����

�

����������� ��

+����.����"�����������������������������������:3������������ ����#��������)��B��6�����

:��������#��������)�������)�?6��������������.��������!�.������)����

���� >������.������"������.� �'�������������������"����������������7(�+����.���.��������� ��������

������������8������ ��� ���� ��� ���� ��������������������"� ����#��� �� ��� ���� ������������

�� ���

��%& &�& �������� �(�

���� (������2��������"������������-��������6��� ������'������ ���������"������������������������

�"�����#��� �'������������6��������������������������������������!������+����.�����������������

������%�����?�����&�����+����������.��,���������������9���� ������������� ������'�������#��

7-'� "��� �� "���� ���� ������� ��� �� !7�� %"���� ������� ���� ���������&� .����� +���� ���� �������

��8��������������� ��"������� ������� �������������"�������������3����+��������+�������#��

7-� ������� ����"�������"�� � ������������������"������ ������ .����� �����7(�������������"�

������������� ������ ��� ����� ��� ������ ����������������5�����"��� ���� ���� ����"� �""����.���

��������+�����������������6���������

���/ (�� �� +���� �2�����'� ��+����� ���� �����"� �)�*'��������"� 3�� ��+���� �������.��+���� ����

���������������� ��������������!�������(�� ���������������� �� ��'� ����� �����+����.���������

������.��+����������������������#��7-'�����.��+����������#��7-��������� ��������������

!������ ��� ������� ���� "������� ��� ��� ������� 3��� �������6�� ��.����� �� �� ����� ��� ��� ���

>���.��� �)�)�"��� ��������������"�!�������4�7���������"����+���� �������������+���� ����

��.������ .���"�����������4��� �����#�"��� ���"���������'�.� ������"�"������������

�������������������� �����������"������������������ �������� ����������� ���.���������.��

���������������� ����.���������������"� �����������'� ������� �������"� ��������������!�������

������� �������.����,�������.���#��7-�%�����*&����� � ��+'���������������� ��������"�

��-��������'����������� �����������������,����������"�������"�� �041�+����.��"������ ����

�����������������������������������������"����� �����������#��� ����

� ���� ���� �. � &��

���� ��� �� ����������2����������.����������+������������������������������������#��� ��+����.��

"���������� ��.�����

���? (��������"� ���� � ����������"� �����""���� ��. ������.� ���� ��������������������������������

�� �����������)�*'�.����#� ���������������������"���������� ��������������""�������""���������

������� ���3���������������"�����"��������� ���������+��������������������������"�������"�� �

���� ��������� ��������������"�����'� ���� �� ���� ����+��� "���������� ��.��'� ������� ���� ����

�

����������� ��

������"�� �������������� ���������������������:������ �6��-E�%����-�������E�����C���+���"�

� �������������"��������� ������"������� ��� �������������"��� �&��

���� �� �� �� ��������� �� ����� %���� "���&'� +����� ���� .�� "����� ��� (������2� �'� +�����

�� ��������������������� ���� ����+����.��"���������� ������.���"���������#��7-�� �������

������� �"� ���� "������� ��� #������ 0� ���� 7������ ��� � � ������� �� ���� ���� ��� ������� ����

���� ���������+�����������������.������

���� ������������������������ ������������������� ����������������������������.��'������������'�

������+��������������� �������������������� ���������,��'��� �������������������#��� ��+����

.��"���������� ��.����

�

����������� ��

?� �)/��������

?�� �� ���������������� ����.5�������� ����.��� �"��,����������!�5���������������� ����

���8�����"������������9��"�������"�������#��� ����

�

����������� *�

�� ��"" �$� ���������������

��� �������������������������������������������������� ����������������������� �������������"�����

�->�1������������ ������������ �����.5�������� ���� ������������ ��� �������"��2��������

�������������������5����"������