dcc newsletter 2015 quarter 1

DESCRIPTION

Durban Chemicals Cluster quarterly newsletter for the period January to March 2015TRANSCRIPT

NewsletterJan - Mar 2015

About the Durban Chemicals ClusterThe Durban Chemicals Cluster (DCC) is a Public-Private Partnership between the eThekwini Municipality and local chemicals firms that focuses on developing the competitiveness of the chemicals manufacturing industry in KwaZulu-Natal. This not for profit organisation is an industry driven initiative, drawing on the leadership and expertise of individuals from a broad range of member firms.

For more information on the Durban Chemicals Cluster please visit www.durbanchemicalscluster.org.za.

About the eThekwini MunicipalityFunding for the DCC is overseen by the Economic Development Unit (EDU) of the eThekwini Municipality, which is mandated to promote economic development, job creation, economic transformation and economic intelligence within the municipal region.The EDU is guided by policies established by National and Provincial Government and articulates the approach to economic development through the Municipality’s Integrated Development Plan (IDP) and an Economic Development Strategy (EDS) from which all activities are guided by, but not restricted to, as the Unit also responds to the broader challenges facing the greater region by endorsing other initiatives such as the Millennium Development Goals.

For more information on the eThekwini Municipality please visit www.durban.gov.za.

Powered by B&M AnalystsCluster facilitation services are provided by Benchmarking & Manufacturing Analysts SA (Pty) Ltd (B&M An-alysts), an organisation that provides specialised services to enhance sustainable industry development.

For more information on B&M Analysts please visit www.bmanalysts.com.

ABOUT US

JAN - MAR 2015 DCC NEWSLETTER 2

CONTENTS

The Race for Africa is On – Opportunities for the Chemicals Sector

Recent Events

Health and Safety Tour

Upcoming Events

Become a member

...13

...19

...3

...28...30

The DCC has identified exports as a vital lever for growth of the chemicals manufacturing industry. The close proximity of South Africa to the rapidly develop-ing African market has meant that this is increasingly viewed by our manufacturers as a key target market for exports. This article will unpack the specific oppor-tunities for the chemicals sector in Africa.

IntroductionA few years ago Africa was dubbed by the Economist as the Hopeless Continent. This has changed dramati-cally in recent years, with global markets taking note of the rapid economic growth that is being experi-enced across Africa. This rapid growth has contrasted significantly with the sluggish growth being experi-enced in many of the world’s markets. Positively, the business climate in many African countries has im-proved.

Ashley Peterson, from the Africa Desk of the Industrial Development Corporation (IDC), reported the fol-lowing improvements in the business environment in Africa at the Durban Chemicals Cluster Annual General Meeting (AGM) held in November 2014:

• Many countries have improved their business environment

• Greater predictability and increased reliability of policy and regulatory framework

• Increased transparency and improved decision-making

• Reduced corruption

• Investment protection & promotion

• Intra- and inter-regional initiatives

• Restored and maintained macro-economic stability

Looking ahead, Africa’s overall growth momentum is set to continue, with Gross Domestic Product (GDP) growth expected to accelerate from 3.5 per cent in 2014 to 4.6 per cent in 2015 and 4.9 per cent in 2016. Growth in private consumption and investment are expected to remain the key drivers of GDP growth across all the five sub-regions. This is underpinned by increasing consumer

By Michele Arde

DCC NEWSLETTER JAN - MAR 2015

THE RACE FOR AFRICA IS ON – OPPORTUNITIES FOR THE CHEMICALS SECTOR

“Every morning, a springbok wakes up, it knows it must run faster than the fastest lion or it will be killed, every morning a lion wakes up, it knows it must outrun the slowest springbok or it will starve to death. It doesn’t matter whether you’re a lion or a springbok, when the sun comes up, you better be running.” - African Proverb

3

Projected per region growth in Africa

North Africa

Southern Africa

Central Africa

West Africa

East Africa

2.7 %

2.9 %

5.9%

6.5 %

4.3 %

2014 2015

3.6 %

3.6 %

4.7 %

6.2 %

6.8 %

Source: www.un.org

confi dence, the expanding middle class, improvements in the business environment and the reduction in the cost of doing business. Government consumption will remain high, due mainly to increased spending on infra-structure (KPMG, 2014).

While positive growth is projected, it is expected to vary substantially across Africa’s fi ve sub-regions, as outlined in the table below, with East Africa projected to be the fastest growing region in 2015, closely followed by West Africa. North and Southern Africa are projected to display the lowest growth.

JAN - MAR 2015 DCC NEWSLETTER 4

Enhanced growth prospects for North Africa are un-derpinned by improving political stability in Egypt and Tunisia. In the Southern African sub-region, although Angola, Mozambique and Zambia are expected to continue to be the fastest-growing economies, the growth in 2015 is expected to be mainly driven by investments in the non-diamond sector in Botswana, a recovery in private consumption in South Africa and increased investment in mining and natural gas exploration in Mozambique. Increased political insta-bility, the Ebola outbreak and terrorism in some of the countries in this region (e.g. Central African Republic, Mali and Nigeria) are preventing an even stronger expansion. Regional integration in the East African Community is expected to continue to boost the GDP growth of this sub-region, from 6.5 per cent in 2014 to 6.8 per cent in 2015, making it the fastest-growing African sub-region. Kenya and Uganda will be the key drivers of growth between 2014 and 2015. Kenya’s growth will benefit from the rapid expansion in bank-ing and telecommunications services, the rise of the middle class, urbanisation and investment in infra-structure, particularly railways, while Uganda’s growth will be supported by increased activity in sectors such as construction, financial services, transport and tel-ecommunications (Retrieved from www.un.org).

Chemical demand in Africa will emanate from five key areas which will each be unpacked in this article. These are agriculture, consumer products, infra-structure development and construction, natural resources and water treatment.

Agriculture

The agricultural subsector in Africa is expected to grow significantly in the future. Africa is the world’s second largest continent and has over 1/5th of the world’s arable land. With over 30 million square kilo-metres, Africa is actually bigger in size than China, the US, Western Europe, India, Argentina and the Brit-

ish Isles combined. Approximately 25 per cent of the world’s arable land is in Africa and 60 per cent of the world’s uncultivated arable land is in Africa. Despite this, Africa remains a net importer of foodstuffs. The current low crop yield per hectare is a major opportu-nity for increased food production (KPMG, 2014). The growth of the agricultural value chain will be associ-ated with significant opportunities for chemical manu-facturers, with these mainly centred on fertilisers.

Consumer products It is estimated that a third of the growth in Africa is from consumer facing sectors or at least partially con-sumption faced sectors. The African consumer prod-uct opportunity is concentrated in 10 African countries including Algeria, Angola, Egypt, Ghana, Kenya, Mo-rocco, Nigeria, South Africa, Sudan and Tunisia. In 2011, these countries accounted for 81% of Africa’s private consumption. From 2012 to 2020 the consumer prod-ucts industry is expected to grow a further $410 billion. Apparel, consumer goods and food are expected to be 45 per cent of this amount (Mckinsey, 2012). Im-portant macro trends that influence the consumption market include:

• Africa has the youngest population in the world – 2/3rd of the population are under 25

• Africa, like the rest of the world, is undergoing major urbanisation

• Africa has a burgeoning middle class with more disposable income

The growth in consumption will result in an increased demand for chemicals as they are required inputs in the value chains as more and more products are pro-duced in Africa.

DCC NEWSLETTER JAN - MAR 20155

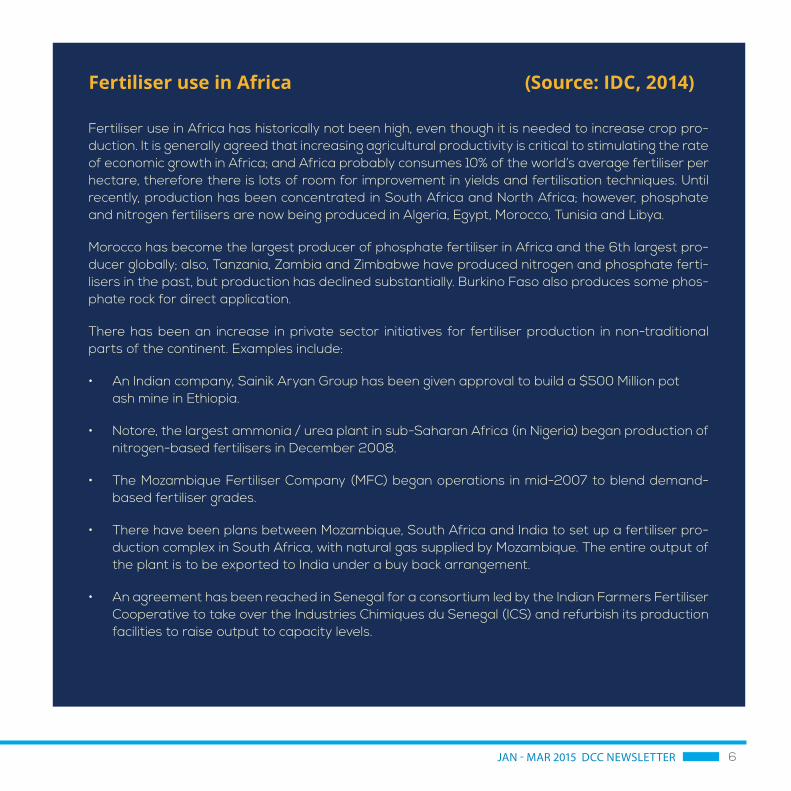

Fertiliser use in Africa (Source: IDC, 2014)

Fertiliser use in Africa has historically not been high, even though it is needed to increase crop pro-duction. It is generally agreed that increasing agricultural productivity is critical to stimulating the rate of economic growth in Africa; and Africa probably consumes 10% of the world’s average fertiliser per hectare, therefore there is lots of room for improvement in yields and fertilisation techniques. Until recently, production has been concentrated in South Africa and North Africa; however, phosphate and nitrogen fertilisers are now being produced in Algeria, Egypt, Morocco, Tunisia and Libya.

Morocco has become the largest producer of phosphate fertiliser in Africa and the 6th largest pro-ducer globally; also, Tanzania, Zambia and Zimbabwe have produced nitrogen and phosphate ferti-lisers in the past, but production has declined substantially. Burkino Faso also produces some phos-phate rock for direct application.

There has been an increase in private sector initiatives for fertiliser production in non-traditional parts of the continent. Examples include:

• An Indian company, Sainik Aryan Group has been given approval to build a $500 Million pot ash mine in Ethiopia.

• Notore, the largest ammonia / urea plant in sub-Saharan Africa (in Nigeria) began production of nitrogen-based fertilisers in December 2008.

• The Mozambique Fertiliser Company (MFC) began operations in mid-2007 to blend demand-based fertiliser grades.

• There have been plans between Mozambique, South Africa and India to set up a fertiliser pro-duction complex in South Africa, with natural gas supplied by Mozambique. The entire output of the plant is to be exported to India under a buy back arrangement.

• An agreement has been reached in Senegal for a consortium led by the Indian Farmers Fertiliser Cooperative to take over the Industries Chimiques du Senegal (ICS) and refurbish its production facilities to raise output to capacity levels.

JAN - MAR 2015 DCC NEWSLETTER 6

Infrastructure and ConstructionThe infrastructure and construction demands of Africa are immense at every level of the economy. For in-stance, Nigeria, with a population of 150 million, has the same power capacity as Hungary, with a population of less than 10 million (EIU, 2012). In order to meet the demand, it would need to spend at least $93 billion. Similarly, because of the poor transport network, transport costs are amongst the highest in the world for some African countries (REF). Infrastructure and construction is demanded in three key areas in Africa:

• Energy

• Information and Communications Technology

• Transport

As a result, this area is receiving more attention by many government organisations and private investors and poses a major opportunity for the chemicals sector.

Natural resources Africa represents 10 per cent of the world’s natural reserves and also has a wealth of additional reserves of gold, copper, diamonds, chromium and platinum. Along with this wealth, Africa contains 10 per cent of the world’s oil reserves. African countries now make up 11 out of the top 50 countries in terms of proven oil reserves. Nigeria and Angola are amongst the top 20 oil producers in the world. Africa also accounts for 20 per cent of the world’s total exports of crude and the region is recognised by Western and Asian markets as a way to mitigate their dependence on Middle Eastern oil. Energy analysts’ project that Africa will increase its production of oil from 9.4 million barrels per day (BPD) in 2011 to 12 million by 2020. In East Africa, new discoveries of onshore oil in Uganda and offshore gas in Tanzania have encouraged new de-velopment initiatives. In West Africa, the Gulf of Guinea remains a significant producer of hydrocarbons, supplying European and American markets. The Organisation for Economic Co-operation and Develop-ment (OECD) estimates that $1.25 trillion will be invested from 2001-30 in African energy, with upstream exploration and investment remaining the focus for both the oil and gas sectors. Africa’s abundant natural resources in the areas of oil and gas provide major opportunities for a range of chemical manufacturers.

DCC NEWSLETTER JAN - MAR 20157

8JAN - MAR 2015 DCC NEWSLETTER

Natural gas demand Africa (Source: IDC, 2014)In January 2012, Africa had proved natural gas reserves of 14 trillion cubic meters, 7.33% of the world and equivalent to 71.7 years of current production. Natural gas is used as feedstock in chemical processes which have high economies of scale and is a significant catalyst for the development of a petrochemicals industry. Gas can be used as the main feedstock for:

• Ammonia for fertilizers;

• Through a Gas-to-Liquid (GTL) process for fuel as a source of energy.

• Methanol for formaldehyde, fuel additives, fuel cells, Olefins, Propylene;

• Acetic acid;

• Dimethyl terephthalate;

• Methyl chloride; and Fuel like diesel, Jet fuel,

According to the IDC (2014), barriers to entry in these countries are high especially giv-en that they are dominated by the large established global petrochemicals companies of the world. They view possible investment opportunities to lie in the following regions:

• Angola;

• Cameroon;

• Mozambique;

• Congo (Brazzaville); and

• Sudan.

World Ranking Country Natural Gas Proven Reserves (m3 in millions)

% Of Global Total

9

10

21

22

Nigeria

Algeria

Egypt

Libya

5,246,000

4,502,000

1,656,000

1,539,000

2.75%

2.37%

0.87%

0.81%

9 DCC NEWSLETTER JAN - MAR 2015

According to the IDC (2014), barriers to entry in these countries are high especially giv-en that they are dominated by the large established global petrochemicals companies of the world. They view possible investment opportunities to lie in the following regions:

• Angola;

• Cameroon;

• Mozambique;

• Congo (Brazzaville); and

• Sudan.

These markets represent an opportunity because:

• New discoveries are continuously being made in some of these countries;

• Some are newly discovered reserves and not yet developed;

• Many of these countries do not have an established petrochemicals industry to fully benefit from the gas reserves; and

• Many of these countries have expressed a clear objective to develop the mid- and downstream component of the sector as part of their national development strategies.

Source: IDC, 2014

Water TreatmentThe rapid urbanisation and economic development in Africa has led to a surge in economic develop-ment and water treatment. Specific opportunities for growth exist in Nigeria, Ghana, Democratic Re-public of Congo and Zambia. The need is propelled by the treatment of tap water and sewerage by municipalities. Other opportunities in the water treatment sector exist with the expansion of the manufacturing industry including the mining, petrochemical and food and beverage industries.

10JAN - MAR 2015 DCC NEWSLETTER

11 DCC NEWSLETTER JAN - MAR 2015

ConclusionAs outlined, definite opportunities for the expansion of the chemicals industry into Africa are evident. These relate to the areas of agriculture, consumer products, infrastruc-ture development and construction, natural resources and water treatment. If member firms of the Durban Chemi-cals Cluster are to leverage growth opportunities in Afri-ca, a focus on these areas must be viewed as a priority. It is thus clear that the race for Africa is on, with South Afri-can industries and thus the Durban Chemicals Cluster ide-ally positioned to benefit from the identified growth areas.

To better support its member firms, the DCC is hosting anImbizo that will focus on providing market linkages with busi-nesses in Africa in May 2015. For more information please contact the DCC.

How can the DCC assist with market linkages into Africa?

12JAN - MAR 2015 DCC NEWSLETTER

Amendments to the Employ-ment Equity Amendment Act The Employment Equity Amendment Act of 2013 came into effect on 01 August 2014. There is no transitional period for compliance with the amendments. These amendments have created much interest and contro-versy. The cluster hosted Shepstone and Wylie Associ-ate, Raoul J Kissun on 02 December 2014 at the Protea Hotel Edward in Durban to allow members to come to grips with the meaning of these changes to mem-ber firms. The objectives of the Act are to; promote equality, eliminate discrimination, redress the effects of discrimination, achieve a diverse workforce and promote economic development and efficiency in the workplace. The Department of Labour is likely to be very active in assessing the employer’s compliance in the months to come. Companies need to ensure that they comply with the new provisions of the legislation to ensure that they meet the requirements of law, are not fined and, most importantly, that they embrace the spirit of transformation.

The following are some of the key amendments:

• Unfair Discrimination

• Burden of Proof

• Equal Pay for Work Of Equal Value

• Medical and Psychometric Testing

• Designated Groups and Designated Employers

• Duties of Employer

• Compliance

If your firm is struggling to grapple with the changes to the legislation, don’t hesitate to contact the DCC for assistance.

DCC Annual General Meeting The Durban Chemicals Cluster (DCC) Annual General Meeting (AGM) brought together public and private sector players from the manufacturing sector to net-work and promote the growth of South Africa’s chemi-cals manufacturing industry. The chemicals manu-facturing sector is a vitally important manufacturing sector in KwaZulu-Natal and therefore this specific gathering of industry, Government and labour stake-holders was useful to facilitate increased dialogue in relation to the critical issues of increasing manufac-turing competitiveness. The AGM, that took place on 11 November 2014, served a number of purposes, the most important of which were to:

• Reflect on key cluster experiences and successes from the previous year;

RECENT EVENTS

13 DCC NEWSLETTER JAN - MAR 2015

• Review Cluster priorities for the medium term; and

• Comply with important corporate governance requirements such as presenting the DCC’s audited financial statements.

Highlights of the event included addresses by Professor Simon Roberts (Professor of Economics at the Univer-sity of Johannesburg and Director of the Centre for Competition Economics) who shared South Africa’s Industrial policy in Economic Development and Ashley Petersen (Senior Development Manager, Africa Desk: IDC) who enlightened attendees on the growth opportunities in Africa for chemical manufacturers.

14JAN - MAR 2015 DCC NEWSLETTER

15 DCC NEWSLETTER JAN - MAR 2015

Highlights of the event included ad-dresses by Professor Simon Roberts (Professor of Economics at the Universi-ty of Johannesburg and Director of the Centre for Competition Economics) who shared South Africa’s Industrial policy in Economic Development and Ashley Pe-tersen (Senior Development Manager, Africa Desk: IDC) who enlightened at-tendees on the growth opportunities in Africa for chemical manufacturers.

16JAN - MAR 2015 DCC NEWSLETTER

A G M

17 DCC NEWSLETTER JAN - MAR 2015

Industrial land available for chemical use

The perception of manufacturing industries in the eThekwini area is that there is limited industrial land available, specifically for the chemicals industry. The eThekwini Municipality have conducted a study that resulted in the Spatial Development Plan for the mu-nicipality. This development plan includes a report on industrial land use in the municipality which includes various opportunities for the industry. Cathy Dale (The Planning Initiative) was the head of the team that conducted the study to develop the plan; she shared the specifics of the plan and tools that chemical firms can utilise to identify investment opportunities in the eThekwini region.

Incentive Opportunities There are several incentives available to firms operat-ing in the local chemicals sector, as well as those look-ing at establishing new operations. These can be cat-egorised under four categories, namely, 1) Logistics, 2) Utilities and Facilities, 3) Training and 4) Equipment. By effectively accessing the benefits associated with the incentives available, firms are able to derive benefits from around five to almost ten percent of sales. Doug-las Comrie (Chief Facilitator: DCC) explored investment and incentive support mechanisms in the eThekwini municipality at an Investment and Growth workshop hosted by the DCC.

18JAN - MAR 2015 DCC NEWSLETTER

Health & Safety

At Engen Refinery & SAB Miller

19 DCC NEWSLETTER JAN - MAR 2015

20JAN - MAR 2015 DCC NEWSLETTER

If you would like additional information on any of the events above, or have missed a presentation that you would like to receive electronically, please contact the DCC at [email protected]

Fostering Lean Thinking on the

Shop FloorMember firms were invited to send employees that work specifically on the shop floor to attend a session focusing on World Class Manufacturing. The session took place over a two-day period which included both theory and practical work for attendees. The session enabled individuals to deepen their knowledge of key functions in relation to World Class Manufacturing (WCM), Just-In-Time (JIT), Total Quality Management (TQM) and Continuous Improvement (CI) Processes. The second day of the session included a plant visit to two local manufacturing facilities, Gelvenor Textiles and PFE Extrusions, which allowed attendees to relate the theory covered to a practical environment. Attendees were able to identify losses more effectively, understand the importance of teams and become more knowledgeable in terms of processes and standardised working methods. The cluster will continue with oper-ator training sessions in 2015 which will focus on the specific training needs of member firms.

21 DCC NEWSLETTER JAN - MAR 2015

If you would like additional information on any of the events above, or have missed a presentation that you would like to receive electronically, please contact the DCC at [email protected]

22JAN - MAR 2015 DCC NEWSLETTER

Developing Scarce Skills in KZN through the GDPThe Graduate Development programme (GDP) is designed to support the development of scarce skills in the chemicals industry in KwaZulu-Natal. This programme is aimed at Graduates with degrees and/or Diplomas in the relevant fields in the Chemicals Industry. The programme is a cluster-based initiative involving multiple firms so as to leverage synergies in areas such as recruit-ment of talent, development of common modules and standards for Graduates in training, common evaluation mechanisms, Graduate exchanges between firms to enhance transfer of skills, in-creased number of total skilled engineers enter-ing the industry, and potentially improved access to funding subsidies. It is envisaged that the Programme will produce experienced, and voca-tion specifically trained employees each year for the chemicals industry in KwaZulu-Natal. The DCC will be providing an external, experienced individ-ual to be the mentor for all the Graduates enrolled in the programme. The programme kicked off on 13 March 2015 at the Premier Hotel in Pinetown with an Introduction to the Programme as well as the theoretical aspect for Module 1.

23 DCC NEWSLETTER JAN - MAR 2015

24JAN - MAR 2015 DCC NEWSLETTER

Get Lean ChallengeThe Durban Chemicals Cluster is challenging member firms to become increasingly competitive by taking part in the Get Lean Challenge. The aim of this challenge is to assist member firms to upgrade their manufacturing competitiveness by focusing on reducing waste within the operations of the firm.

The Challenge will run for six months with the goal of reducing 10% waste within each individual firm and par-ticipants will take part in this challenge through following a “continuous improvement network”.

Firm level benchmarking

A 6 Month Programme Overview

Strategy Development & Support

Expert Training

Lean Challenge

A Firm level, objective assessment or relative competitiveness.

The alignment of strategic goals and operational priorities to ultimately improve competitiveness, profitability and sustainability

The DCC will provide executive level, lean trainingto memer firms, to build capacity to achieveoperational performance improvement.

Firms will monitor their operational wastereduction monthly, striving towards the ultimategoal of an overall waste reduction of 10% over a 6 month period. Firms will be placed amongstlikeminded operational leaders and undergo bimonthly peer review sessions. An award willbe presented to the firm who has made thegreatest improvement.

Bimonthly

Every 2 months

February- June

January -February

25 DCC NEWSLETTER JAN - MAR 2015

Would you like to improve the operational competitivness of your firm?

Join the Lean Challenge and receive a firm-level benchmark, strategy development and expert training & learning sessions. Contact the DCC at [email protected]

10% OperationalWaste Reduction

SET THE TARGETAND MAKE LEANA PART OF YOUR EVERYDAYMANUFACTURINGPROCESS

26JAN - MAR 2015 DCC NEWSLETTER

New Generation ISO Standards

The new year brings amendments and the introduction of a number of ISO Standards for the Chemicals Manu-facturing Industry. These standards are strategic tools that reduce costs by minimising waste and increasing productivity.

A session on 17 February 2015 will provide both prac-tical and theoretical understandings of the new ISO (high level) structures which are being applied to new management systems in 2015 and 2016.The majority of the chemicals industry comply to ISO standards and thus the new additions and amendments contained within the new international standards will have an impact on member firms. If the South African Chemical Industry is able to comply with these standards, local companies will be able to access more new markets, thus increasing competition.

What plan does the Transnet Ports Authority have for Southern Africa’s busiest Port?The chemicals industry relies heavily on the port of Durban as majority of raw materials are imported through the port, which impacts on the DCC firms’ manufacturing reliability and flexibility. The port of Durban is undergoing various developments includ-ing the new Dig Out port, which will have a significant impact on the chemicals manufacturing industry. The Acting Manager, Planning and Development of the

Transnet Ports Authority, Khulekani Xaba, shared the development plan and port activities for 2015 at a Quarterly Investment and Growth session on 12 Febru-ary 2015.

How eThekwini manages load shedding

The chemicals industry is impacted heavily due to load shedding and is facing many challenges as a result of the pressure on South Africa’s power grid. EThekwini Electricity works closely with industry to re-duce the impact of load shedding on the manufactur-ing industry in eThekwini. Vijay Batohi (Senior Manager: HV Network Control, eThekwini Electricity) presented the municipality’s plan for load shedding and the impact this will have on industry at B&M Analysts on 12 February 2015.

27 DCC NEWSLETTER JAN - MAR 2015

Waste Management PracticesDolphin Coast Landfill Management (DCLM) is a spe-cialised environmental waste management company involved in the provision of general and Hazardous waste services. The DCLM Group owns and operates its waste services at the Kwadukuza H:H Landfill Site. Improper waste management in the past has resulted in costly clean-up operations. In order to remedy past problems caused by hazardous waste and to prevent future problems, waste management practices should include source reduction, recycling, treatment and proper disposal of hazardous waste. The cluster mem-bers will have an opportunity to visit this world class site in April 2015 and gain knowledge in effective waste management practices.

Enterprise Development OpportunitiesEnterprise development has become increasingly important for our firms given the changes to the BBBEE legislation. Join the DCC on 31 March 2015 where Paul Vermaak (HR Director: Smiths Manufacturing) will be sharing their experience with dealing with Enterprise Development and will also present on the Enterprise Development Programme currently run by Smiths Manufacturing.

Local Chemical SME developmentThe DCC commenced the CHIETA Phase 3 SME De-velopment Programme in June 2014 with the aim of developing chemical manufacturing SMEs for long

term growth and improved competitiveness. This programme constituted the development of 15 local chemical manufacturers in the KZN region. The Pro-gramme will come to a close on 31 March 2015 with an exhibition by those firms who have participated where-by they will showcase their products and services to existing cluster members.

Stay Abreast of the Amended Labour Laws The recently updated Labour Law will give employees more protection in the workplace and put specified obligations on employers from 01 April 2015. Les Owen (Owen, Adendorff & Associates) is a Management Con-sultant and Training Facilitator specialising in Business Management, Negotiations and Conflict Resolution. Les will explore the amendments to the Labour Rela-tions Act (Act 66 of 1995) as it came into effect on 01 January.

UPCOMING EVENTS

28JAN - MAR 2015 DCC NEWSLETTER

Bringing the chemicals industry together The Chemicals sector is one of the primary manufacturing sectors in KZN. The chemicals sec-tor is being constrained by high imports, volatile exchange rate and sluggish demand. It is for this reason that the DCC is launching a Chemicals Industry Imbizo to bring together the indus-try, increase local demand and promote exports into Africa. The Imbizo will take place in July 2015.

IMBIZO 2015

Would your firm like to increase your domestic footprint or grow exports into Africa? [email protected] about participating in the meet and greets at the DCC Imbizo.

29 DCC NEWSLETTER JAN - MAR 2015

BECOME A MEMBER!

We welcome membership enquiries from chemical manufacturing compa-nies with operations in KwaZulu-Natal.

For further information please either call +27 (0) 31 764 6100 or email the DCC [email protected].

30JAN - MAR 2015 DCC NEWSLETTER

+27 (0) 31 764 6100 www.durbanchemicalscluster.org.za