debt structure, private equity reputation, and performance...

TRANSCRIPT

Debt Structure, Private Equity Reputation, and

Performance in Leveraged Buyouts

Chen Liu

September 20, 2013

Abstract

This paper provides a comprehensive study of deal characteristics and participants’

involvement in leveraged buyouts (LBOs) and their impact on target firms’ performance.

Using a sample of 501 U.S. LBOs completed between 1986 and 2011, I find that higher

industry-adjusted changes in return on assets and return on sales are associated with larger

amount of leverage added during the buyout process, tighter LBO loan covenants, and

equity contribution of target firms’ management. LBOs are more likely to exit through an

IPO or a sale if they use more bank debt with tighter covenants and are sponsored by

private equity firms of high reputation. These relations are robust to credit market

conditions and aggregated LBO activities. The evidence suggests that the main source of

value creation in LBOs is the reduced agency costs through the disciplining effect of debt,

closer monitoring by lenders, and the better aligned management incentives. Private equity

firms’ reputation is also important in ensuring successful deal outcomes. My findings also

suggest that the poor performance observed in recent LBOs is a result of less leverage,

fewer bank loans, and less restrictive covenants used in these deals.

Key Words: leveraged buyout, private equity, debt structure, covenants

Queen’s School of Business, Queen’s University, Kingston, Ontario, Canada. K7L3N6. Email:

[email protected]. I am grateful to my supervisor Lynnette Purda for comments that substantially

improved this paper. I also thank Edwin Neave and Wei Wang for helpful comments. I am responsible for all

remaining errors.

- 1 -

1. Introduction

In a leveraged buyout (LBO),1 a company is acquired using a relatively small portion

of equity and a relatively large portion of outside debt financing. Jensen (1989) argued that

the LBO structure of highly leveraged capital structures, active corporate governance,

concentrated ownership stakes, and well-aligned managerial incentives make the LBO form

superior to widely held public corporations. Early empirical work supported the merits of

this structure with papers by Kaplan (1989a) and Smith (1990) finding improvements in

performance for firms undergoing an LBO in the 1980s. However, more recent studies by

Guo, Hotchkiss, Song (2011) and Cohn, Mills, and Towery (2011) find few performance

improvements to target firms of LBOs completed in the 1990s and first half of the 2000s.

Therefore, I am motivated to examine how recent LBO deals differ from the earlier ones

and whether these differences are responsible for smaller performance enhancements in

these later deals. To do this, I seek to identify the primary drivers of LBO success with a

particular focus on leverage, LBO debt structure and terms, and the changing role of banks

and private equity investors in the resulting firms. I also examine whether performance is

related to different credit market and LBO market conditions or premium paid in the

buyout transaction.

Figure 1 presents the structure of a typical LBO transaction. Equity investors in LBOs

are mainly private equity (PE) firms, management of the target firms, or another

corporation. Financiers of these transactions include banks, institutional investors, and

public debt holders, whereas institutional investors are principally structured investment

vehicles and loan participation mutual funds (Miller 2012). Traditionally, banks were

heavily involved in financing LBO deals. However, the function of banks have changed

significantly as more and more banks move to securitize loans that they previously would

have held (Bord and Santos, 2012). In addition, PE firms have becoming more important in

sponsoring LBO deals and the 2000s has observed an increase in club deal LBOs, where

two or more PE firms conduct a buyout together As a result, I am motivated to begin my

examination of LBO performance drivers by investigating how the structure of these deals 1 A management buyout (MBO) is a form of LBO when incumbent management team takes over the firm. This

paper includes MBOs in the sample and uses the general term “LBO”.

- 2 -

and the participants involved have changed over time.

To undertake this examination, I construct a comprehensive dataset of 501

public-to-private U.S. LBO transactions completed between January 1, 1986 and December

31, 2011 from Capital IQ and the SDC. I require all transactions to have financing details

from LPC’s Dealscan and pre- and post-buyout financial data from Compustat or Capital

IQ, and missing data are filled from SEC filings. This dataset has the following merits. First,

it is to my knowledge the most comprehensive U.S. LBO sample with large number of

deals that have post-buyout data available. As the target firms become private with the

buyout, LBO studies on performance improvement are restricted by data availability. For

example, Kaplan (1989a)’s sample contains 76 management buyouts between 1980 and

1986 and Guo et al. (2011)’s study of LBOs between 1990 and 2006 has 196 observations,

96 of which have post-buyout data available. By hand-collecting financial information of

target firms that have publicly traded debt or subsequently file an IPO, I am able to

construct a larger LBO sample than those used in previous studies. This large sample

allows me to explore the heterogeneity among these LBO deals and generate results with

better statistical properties in the cross-sectional analysis. Second, the sample period covers

the cyclicality of LBOs starting from its first wave of the late 1980s and early 1990s, the

slight recovery and decline in the 1990s, and the most recent boom and bust in the 2000s.

This sample period makes this paper one of the first studies that directly compares how

LBO deal characteristics, performance, and their relation have changed over time.2

Moreover, this paper presents the most up-to-date sample that includes LBOs completed by

December 31st, 2011. This allows me to examine LBOs completed during and after the

2007-08 credit crisis, while most other studies use deals completed before the crisis.

Using this data, I first measure post-buyout operating performance. Following Kaplan

(1989a) and Guo et al. (2011), I calculate the percentage changes in EBITDA and net cash

flows scaled by total assets or sales from the last fiscal year before the LBO to the first

three years after the buyout completion, adjusted by industry medians. I find that

performance change is largely positive for LBOs in the 1980s and 1990s but almost

2 Guo et al. (2011) studies deal characteristics and performance changes by comparing the deal pricing and

financing details calculated in their paper with the results presented in Kaplan and Stein (1993).

- 3 -

insignificant for the deals in the 2000s. For example, during the period of 1986-1993, the

median industry-adjusted percentage increases in net cash flow to sales are significant at

32.7%, 28.2%, and 31.5% in the first three years after the buyout. Between 1994 and 2011,

these increases are still significant, but by a lesser extent at 18.5%, 13.7%, and 29.8%.

However, from 2002 to 2011, only the increase in the first year after the buyout is

significant at 13.3%, while changes in the second and third years become insignificant.

I next examine how LBO deal characteristics have varied over time that may be

responsible for the decreasing performance based on Jensen (1989). I find three important

changes. First, LBOs in the 1990s and 2000s do not borrow as much as the ones in the

1980s. For the deals in the late 1980s, leverage increased by a median of 45% to a

post-buyout debt-to-asset ratio of 74% in the first full year after the buyout completion.

However, the median leverage increase was only 22% and post-buyout leverage was 57%

for deals in the 2000s. Second, there is a structural change in the composition of the LBO

debt. The proportion of bank debt in total LBO debt has decreased from a median of 85%

in the late 1980s to a median of 34% in the 2000s. In the meanwhile, institutional investors

have become more important in the LBO market with institutional loans financing a

median of 63% of total LBO debt in the 2000s. In addition, covenants within the LBO

loans have become less restrictive. Third, PE firms have become more important players in

LBO transactions. The proportion of deals sponsored by PE firms increased from 68% in

the late 1980s to 96% in the second half of the 2000s. In addition, there are more club deals

in recent years, leading to mega LBOs with large transaction values between 2005 and

2007.

Having documented a decline in post-buyout operating performance and a shift in

deal structure and participants, the second part of the paper seeks to identify what aspects

of a deal’s structure and the role of participants are associated with its performance.

Possible drivers of performance that I consider are (1) change in leverage, (2) monitoring

by lenders, (3) involvement of PE firms, and (4) better aligned management incentives. I

control for pre-buyout characteristics of target firms, credit market and LBO market

conditions, LBO loan spread for each deal, and the premium paid for the target firm, and

other deal characteristics in examining these performance drivers.

- 4 -

Regression results show that target firms have better performance when leverage is

increased by a larger amount through the buyout, LBO loan covenants are more restrictive,

and when managers of the target firms contribute equity and participate in the buyout. PE

reputation, however, is not related with changes in operating performance. In addition, I do

not find evidence that links performance to credit market conditions, LBO loan spreads, or

the buyout price. Overall, these results suggest that the main source of value creation is the

reduced agency costs in the post-buyout firms through the discipline effect of debt, closer

monitoring by lenders, and the better aligned management incentives. These results help us

to understand the observed reduced performance enhancement in the more recent LBOs as

they use less leverage and less restrictive loan covenant, which are important drivers for

performance improvement.

Another way to examine LBO success is to look at the outcome of each

deal—whether it goes bankrupt, exits through an IPO or a sale to financial or strategic

buyer. Using an IPO and a sale as indicator of LBO success, I find that LBOs are more

likely to succeed if they use more bank debt and tighter covenants, experience no CEO

change, and are sponsored by highly reputable PE firms. LBOs are more likely to fail if the

buyers are subsidiary of banks that are also financiers of the deals. These results are

consistent with the lenders’ monitoring and PE firms’ reputation as sources of value

creation in LBOs. I also find that LBOs completed during the time when interest rates are

lower than their historical average are less likely to succeed, providing some evidence for

the market timing behavior of LBO buyers that they overinvest in unprofitable deals under

times of favorable credit market conditions.

Contributions of this paper are as follows. First, this is one of the first large sample

LBO studies with a sample period that covers the entire cyclicality of the LBO history.

Second, this paper contributes to the literature on value creation of LBOs by examining the

primary drivers of performance improvement and successful deal outcomes. To the best of

my knowledge, this is the first paper that studies the effects of detailed LBO financing

structure and its contractual features, and PE reputation on post-buyout operation

performance. Results of this paper will further our understanding of when and how an LBO

may be successfully employed to improve firm performance. By doing so, it facilitates our

- 5 -

understanding as to why recent LBOs seem to be less successful than previous transactions.

Third, this paper contributes to the literature of private equity reputation by being one

of the first studies that investigate how PE reputation affects performance. The finding that,

controlling for target and deal characteristics, PE reputation is not related to operating

performance in the first three years after the buyout but is important in ensuring successful

deal outcomes provides some indirect evidence that PE firms create value through later

stage of LBOs. Findings of this paper will motivate future studies in investigating when

and how PE firms create value in LBOs.

Forth, this paper contributes to the literature on debt structure and debt contracting in

the setting of LBOs. This paper finds that loan covenants are important drivers of operating

performance and instrumental to ensure successful outcomes. This result has important

implications for practitioners as well as policy makers that they should focus on covenant

to reduce risks and to improve performance of target firms. The proportion of bank debt is

also important for LBOs to exit through an IPO or a sale, suggesting that composition of

LBO debt needs to be carefully structured.

The rest of the paper proceeds as follows. Section 2 reviews related literature and

develops hypotheses. Section 3 describes the sample and provides evidence on post-buyout

operating performance. Section 4 presents the changing characteristics and participants of

LBO deals over time. Section 5 examines the drivers of post-buyout performance. Section

6 conducts robustness analyses. Section 7 concludes.

2. Literature review and hypotheses

2.1 Measuring value creation in LBOs

Previous studies have examined value creation in LBOs in two ways: returns to

LBO investors and post-buyout performance improvement in LBO target firms. In the first

approach, value creation is measured as the returns to invested debt and equity capital from

the time of buyout to a subsequent IPO, sale of the firm, or bankruptcy. Studies on LBO

deal level returns suggest significant value creation through LBOs as evidenced by positive

returns to investors. For example, Kaplan (1989a) estimates a median market-adjusted

- 6 -

return of 28% (mean 42%) for investors in 25 MBOs in the 1980s that went public after an

average of 2.7 years. Also, Guo et al. (2011) finds a median market- and risk-adjusted

return to pre-buyout capital of 68.7% (mean 94.7%) for a sample of 70 LBOs completed

from 1990 to 2006.

On the LBO fund level, literature provides mixed evidence. Kaplan and Schoar (2005)

investigate returns for 160 LBO funds between 1980 and 2001 and find that the median

fund underperformed stock market index, generating only 80% of the return on the S&P

500. Higson and Stucke (2012) find that the buyout funds in their sample have significantly

outperformed the S&P 500, with funds liquidated in the period 1980-2000 generating

excess returns of on average 4.5% per year. The different results of these two studies are

mainly due to sample selections as both studies find large heterogeneity in returns across

funds. Higson and Stucke (2012) find just over 60% of the funds in their sample

outperform the S&P500 and Kaplan and Schoar (2005) show that for the subset of funds

that have been around for at least five years, the median performance exceeds the S&P500

by 50% (mean 80%). They also show that this performance is persistent and suggest that

different LBO sponsors may have different skills in managing their portfolio companies.

The heterogeneity in fund returns and performance persistence motivate me to examine

characteristics of PE firms to determine whether and how they are associated with the

performance of target firms.

The second way to examine value creation in LBOs is to focus on the post-buyout

operating performance of target firms.3 Kaplan (1989a) studies 48 management buyouts

from 1980 to 1986 and finds that industry-adjusted ratios of EBITDA to sales increased by

21.3%, cash flow to sales increased by 28.3%, and capital expenditure to sales decreased

by 25.6% during a three-year period following the buyout. Smith (1990) reports a

significant increase in operating cash flow per employee and per dollar of operating assets

from the year prior to the buyout to one year post-buyout for 58 MBOs between 1977 and

1986. Lichtenberg and Siegel (1990) study 193 LBOs between 1981 and 1986 with a total

of 1,132 plants and show that plant total factor productivity increases more than the

3 Some studies, for example Guo et al. (2011), use changes in operating perofrmance as an explanation for

returns to investors.

- 7 -

industry average in the years following a buyout. In contrast to the significant performance

enhancement documented in the early studies, using this approach, the evidence of

performance improvement is weaker for more recent LBOs. Guo et al. (2011) find a

median of only 2.25% industry-adjusted increase in operating margins and a 12.54%

decrease in cash flow margins for 94 LBOs completed between 1990 and 2006. Cohn et al.

(2011) also find little evidence of performance enhancement using corporate tax return data

for 317 LBOs from 1995 to 2007.

This paper follows the second approach and examines post-buyout operating

performance for the following reasons. First, this paper defines value creation as the real

effects of buyouts, such as increased efficiency and reduced costs, rather than purely

financial returns.4 For this purpose, operating performance is a cleaner measure of value

creation compared with the returns to investors. This is because returns to investors do not

necessarily reflect the real value creation as they are usually calculated upon the exit of the

deal, therefore depending on market conditions and investors’ market timing ability.

Second, one of the goals of this paper is to construct a comprehensive and up-to-date LBO

database that includes deals completed during and after the 2007-09 credit crunch. Most of

these deals have not reached their outcome yet so no returns to investors are available for

these deals. However, I can still examine the value creation and its drivers through

operating performance change. One problem with measuring performance using cash flow

variables from target firms’ financial statements, as mentioned in Cumming, Siegel, and

Wright (2007), is that they are in general subject to managerial manipulation. However, as

all the performance ratios in the paper are industry-adjusted, and assuming all firms in the

same industry are subject to managerial manipulation in the similar ways, I expect the

effect from manipulation to be small although the incentives for LBOs to show improved

performance are probably greater than the average firms.

4 According to KKR founder Henry Kravis, private equity firms create value in LBOs over the long-term as

managers, not merely as financial engineers. Kravis said that “We only make money because we improve the

operations of the newly acquired company”. Source: “Merger Talk - LBO firms rush to exits with quick flips.”

Reuters News, December 30, 2004.

- 8 -

2.2 How LBOs create value: hypotheses

In this subsection, I develop hypotheses on the sources of post-buyout performance

changes of LBO target firms. I hypothesize that performance is positively influenced by the

disciplining effect of increased leverage, better monitoring by lenders, active involvement

of PE firms, and better aligned management incentives.

2.2.1 The disciplining and monitoring effect of debt

The first key ingredient in a buyout transaction is leverage. Jensen (1986, p325) states

that “many of the benefits in going-private and leveraged buyout transactions seem to be

due to the control function of debt”. Leverage creates pressure on managers not to waste

money, because they must make interest and principal payments. This pressure reduces the

free cash flow problem described in Jensen (1986) where entrenched managers dissipate

the free cash flows and overinvest in negative-NPV projects. Also, the increased risk of

financial distress associated with higher leverage motivates managers to operate the firm

efficiently and to increase profit. Therefore, I expect that target firms that have increased

their leverage by a greater amount through the buyout have better performance.

Hypothesis 1.1(Debt Disciplining Hypothesis): Firms with higher level of leverage

increase have better post-buyout performance.

In addition to the disciplining effect of debt, I examine whether the monitoring by

lenders lead to better performance of target firms. At the center of this examination is the

conflict of interest between shareholders and bondholders that has negative impact on the

value of the firm’s outstanding debt as well as the total value of the firm (Bradley and

Roberts, 2004). Lenders’ monitoring on managers’ behavior can help to mitigate these

conflicts and reduce the attendant agency costs.

To study the monitoring effect, I first examine the proportion of bank debt in total

LBO loans. This is because banks are generally thought to have more incentives and

comparative advantages in monitoring borrowers (Diamond 1984, 1993; Park 2000).

Therefore, traditional thinking suggests that LBOs that are funded with a larger proportion

of bank debt to have better performance as these deals are more closely monitored by

banks.

- 9 -

Another way to examine the monitoring effect is through the investigation of LBO

loan covenants. Chava and Roberts (2008) suggest that covenants increase firm value in

two ways. First, covenants that monitor and control managers’ behavior mitigate the

reduction in firm value from the conflicts of interest between shareholders and debtholders

and managers acting on behalf of shareholders to expropriate bondholders’ wealth.

Specifically, covenants can restrict borrowers’ use of cash flows and require them to repay

with proceeds of excess cash flow, asset sale, or debt and equity issuance. Based on Miller

(2012), in a typical syndicated loan contract, 100% of net proceeds from asset sales and

debt issuance and 50% to 75% of excess cash flow are required to prepay the loans. These

requirements mitigate the free cash flow problems described in Jensen (1986). In addition,

covenants specify the maximum level of different categories of debt to be used by the

borrowing firms, therefore reducing the risk of post-buyout financial distress. Second,

covenants define the circumstances under which creditors are permitted to intervene in

management. This threat of transfer of control rights from borrowers to creditors serves as

a discipline mechanism for managers. In particular, covenants enforce minimum financial

performance measures against the borrowers, therefore motivating managers of the LBO

target firms to increase revenue.

Besides covenants, the maturity structures of LBO loans are also important. When

LBOs are financed with short-term loans, the incentive effects of debt described by Jensen

(1986) tend to be stronger. In particular, a shorter maturity increases required debt service

payments, thus increasing the incentives for mangers to work harder to generate cash and

avoid wasting resources in the earlier stages of the LBOs. In combination, these LBO loan

characteristics form Hypothesis 1.2.

Hypothesis 1.2 (Lenders’ Monitoring Hypothesis): LBOs with more bank loans,

tighter loan covenants, and shorter loan maturity are associated with better post-buyout

performance.

2.2.2 Private equity involvement

Another possible source of value creation in LBOs may be the involvement of PE

firms. As equity investors in LBOs, PE firms are incentivized to actively engage in the

- 10 -

target firms’ management. Also, general partners (GPs) of PE funds are paid a management

fee of 2% on the fund’s capital and receive a carried interest of 20% of the profits above a

certain benchmark realized by the fund. Therefore, GPs have incentives to closely monitor

their portfolio firms. As described by KKR’s founder Henry Kravis, PE firms “generally

aren’t board members who show up once a month... Most of us in the industry live with

these companies on a day-to-day basis”.5

However, it is hard to directly observe PE firms’ involvement in management, as

target firms become private after the buyouts and therefore not required to disclose

corporate governance information.6 As a result, I use PE firms’ reputation as a proxy for

their experience and skills to manage the target firms, where reputation of each PE firm is

calculated as its years of experience or its market share based on all buyout deals it

sponsored in history or in the past 36 months. The idea to use PE firms’ past experience as

a proxy for their current skills is based on Kaplan and Schoar (2005)’s finding of

performance persistence of PE funds. Specifically, they find that performance of PE funds

persists over time and that larger and older funds perform better than the new ones. The

observed performance persistence can be attributed to PE firms’ experience and skills in

selecting, restructuring, and monitoring target firms. Better-performing PE firms gain

experience through their experiential learning from previous deals and PEs with lower

returns cannot get funds from investors and fail to exist. In addition, Axelson, Stromberg,

and Weisbach (2009) argue that highly reputable PE firms are less susceptible to risk

shifting as they have incentives to pursue relatively more conservative investment

strategies in order to maintain their reputation. Therefore, using PE firms’ reputations as an

indicator of their ability and skills, I hypothesize that LBOs sponsored by highly reputable

PE firms perform better.

Hypothesis 2.1 (Private Equity Reputation Hypothesis): LBO deals sponsored by PE

5 Source: “Merger Talk - LBO firms rush to exits with quick flips.” Reuters News, December 30, 2004.

6 Some studies look at the board composition of target firms using the Dash dataset that’s only available for

U.K. firms. For example, Cornelli and Karakas (2011) examine the board structure for 88 U.K. LBOs from

1998 to 2003 and find significant changes in board size and composition when a firm goes private. Board size

generally decreases and the presence of outside directors is drastically reduced, as they are replaced by

individuals employed by the LBO sponsors.

- 11 -

firms of high reputation experience higher performance improvement.

A recent trend in LBOs is club deals, where two or more PE firms pool their assets to

acquire target firms and manage them collectively. Club deals can be beneficial as each PE

firm may bring different expertise to target firms. For example, when KKR teamed up with

Bain Capital and Vornado Realty Trust to acquire Toys "R" Us, the New York Times stated

that “it was clear what each firm brought to the table. Kohlberg Kravis has a good

reputation in the retail business, Bain has a good record doing turnarounds, and Vornado

clearly knows real estate”.7 However, as the number of PE firms in the club gets larger, it

is harder to make timely operational and management decisions. For example, Jeffrey

Walker, a managing partner of CCMP Capital, argued that it was difficult to manage an

LBO that has more than two or three investors.8 Also, based on the experience of the

venture capital industry, which is closely similar to the private equity industry, the ideal

size of the consortium is two PE firms. To sum up, anecdotal evidence suggests that club

deals may improve performance through each PE firm offering valuable management

advice. However, as the size of the club gets larger, this benefit may decrease.

Hypothesis 2.2: Club Deals perform better than LBOs sponsored by a single PE firm.

However, this advantage tends to decrease as the number of PE firms participating in a

deal gets larger.

Recent studies in LBOs have investigated the relationship between banks and PE

firms and how it affects returns to PE investors at the exit of LBOs. Fang, Ivashina, and

Lerner (2012) find that LBOs sponsored by PE firms that are subsidiaries of banks (the

bank-affiliated deals) exhibit worse equity returns if the deal is completed during the peaks

of the credit market. Ivashina and Kovner (2012) find that bank relationship formed

through repeated interactions between banks and PE firms lead to more favorable loan

terms and higher equity return to the PE firms. Empirical results on the effect of banking

relation on returns to PE firms are mixed, depending on the nature of the relation and the

motivation behind it. I follow Fang et al. (2012) and examine bank-affiliated deals, as there

may be some distinct features of these deals. First, as banks are in general less willing to

7 Source: “Do Too Many Cooks Spoil the Takeover Deal”, the New York Times, April 3, 2005 8 Source: “Buyout Veterans Have Questions about Club Deals”, Dow Jones Newswires, January 24, 2007.

- 12 -

take risks than other investors, I expect that bank-affiliated PEs choose to sponsor deals

with lower risks, therefore generating lower returns. Second, bank-affiliated deals provide

parent banks with cross-selling opportunities (such as potential M&A advisory work,

cash-management services, etc.) that increase their fee income. As a result, buyout

decisions may not be based on PE’s expectation on efficiency improvement of target firms,

but only to take advantage of these cross-selling opportunities.

Hypothesis 2.3: Bank-affiliated LBOs perform worse than stand-alone deals.

2.2.3 Management participation

When incumbent managers of target firms participate in a buyout, they become the

equity investors and their incentives are well-aligned with other shareholders. As a result,

agency costs are minimized.

Hypothesis 3.1 (Management Participation Hypothesis): Management-participated

LBOs tend to have better performance due to better-aligned management incentives that

reduce agency costs.

Some studies look at management turnover and consider it as a way to measure PE

firms’ control over target firms. Gong and Wu (2011) find that 51% of incumbent CEOs are

replaced within two years of the LBO announcement. Acharya and Kohoe (2008) find that

for U.K. LBOs, one third of the CEOs are replaced within the first 100 days and two-thirds

are replaced over a four-year period. However, management turnover can be a noisy

measure. First, it may not be clear that the management change is due to PE firms unless it

is explicitly indicated in the proxy statement. Second, even it is confirmed that PE firms

replace the CEO or CFO, management change may not necessarily indicate increased

control from the PE firms. On the one hand, management turnover can be consistent with

replacing bad managers by the good ones. On the other hand, the same managers running

the company before and after the buyout may indicate low pre-buyout agency problem and

therefore there is no need to replace managers. As a result, I expect the effect of

management turnover on performance to be ambiguous.

Hypothesis 3.2 (Management Turnover Hypothesis): The effect of management

change on performance is ambiguous.

- 13 -

3. Data and post-buyout performance

3.1. The Buyout Sample

LBO sample of this paper is constructed from the Standard and Poor’s Capital IQ and

the Securities Data Company’s (SDC) U.S. Mergers and Acquisitions Database. I manually

combine LBO deals from the above two sources and eliminate duplicate observations.

Compared with the SDC dataset, Capital IQ has an advantage as it allows me to link the

LBO transaction details to target firms’ financials and information on LBO buyers (private

equity firms, management teams, or another corporation). However, one possible problem

with Capital IQ is its limited coverage of earlier deals. Stromberg (2008) compares the

1980s’ LBOs from Capital IQ and other data sources and estimates that Capital IQ covers

between 70% and 85% of the LBO sample for this period. As one of the goals of this paper

is to compare deal characteristics of LBOs during the period of 1986 to 2011, I also collect

LBO transactions from SDC which has better coverage of deals in the late 1980s and early

1990s.

Each LBO transaction in my sample meets the following criteria: (1) the transaction

is flagged as an LBO, MBO, or secondary LBO and completed between January 1, 19869

and December 31, 2011; (2) the target is a publicly traded U.S. company; and (3) the

transaction value is $10 million or larger. The minimum deal value of $10 million is lower

than that in some other studies, such as Kaplan (1989a) and Guo et al. (2011). It is chosen

to avoid biasing against earlier time periods when small deals were more common. This

initial screening yields a total of 1,586 LBO transactions. To reconstruct the financial

structure of each deal accurately, I require that all transactions have financing details

available from Reuter’s LPC Dealscan loan database.10 I match the Dealscan data with the

buyout sample by borrower names and time of the transactions. I then reconstruct the

financial structure for each deal using the tranche level data of LBO loans from Dealscan

and the mezzanine debt from Capital IQ. This reduces the sample to 885 observations. In

9 My sample starts from 1986 because the loan information from Dealscan starts from 1986. 10 Restructuring LBO deals across databases requires matching by names of target firms. Target firms mostly

appear under their old names in SDC, Dealscan, and Compustat, while Capital IQ uses only the most recent

names. I keep track of all name changes using a text search in Company Tearsheet of CapitalIQ. I also use the

Wall Street Journal for name changes if the Tearsheet is ambiguous.

- 14 -

addition, I require that all target firms have pre- and post- buyout financial information

from COMPUSTAT or Capital IQ,11 and missing data are filled from SEC filings. This

drops 384 transactions, the majority of which are the buyouts in the 1980s, as Capital IQ

mainly provides financial statement information for the 1990s and the 2000s. My final

sample consists of 501 LBO transactions.

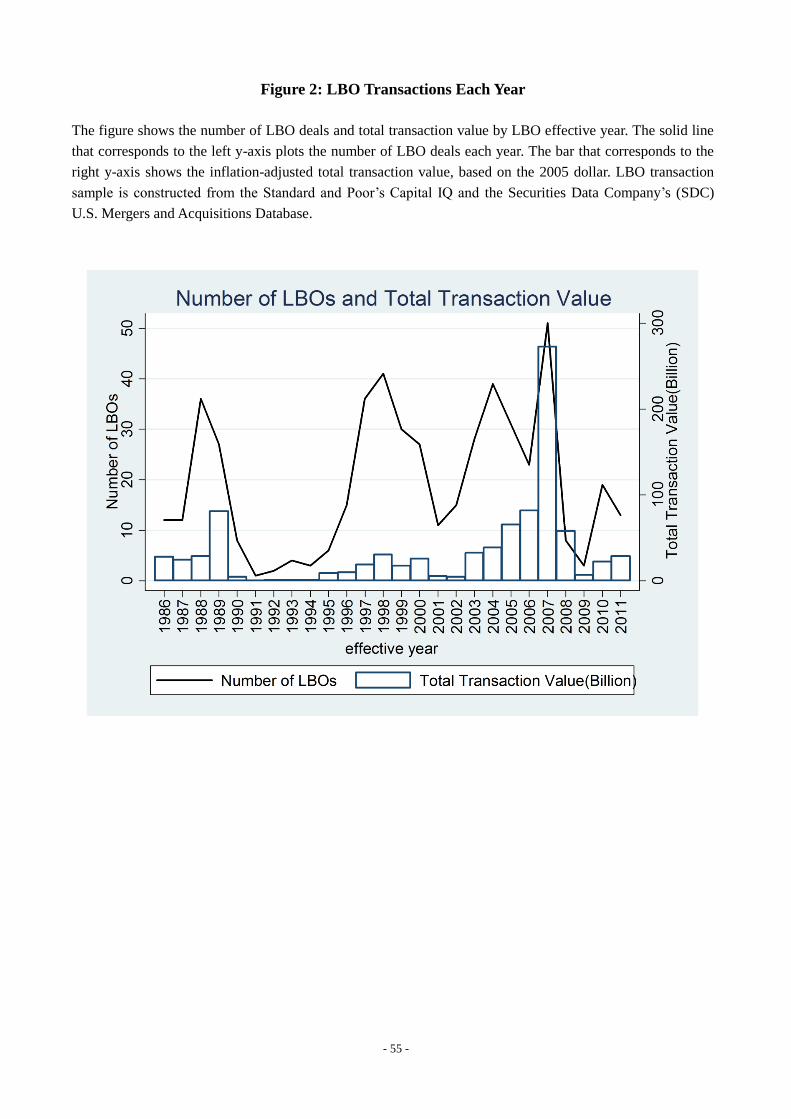

Figure 2 presents the total number of LBO deals (left y-axis, solid line) and the

inflation-adjusted12 total transaction values (right y-axis, bar) by LBO effective year.13

The first LBO boom occurred in the late 1980s, with a total transaction value increasing

from $24 billion in 1987 to a peak of $81 billion in 1989. The largest deal during the time

was KKR’s buyout of RJR Nabisco in 1989 with a transaction value of $39 billion. This

first wave of LBOs ended with the recession in 1990-1991 when the high yield bond

market collapsed. The buyout market started to resume in 1996 but crashed with the

bursting of the tech bubble in 2001. In the mid-2000s, LBOs reappeared in a third buyout

boom. Total transaction value increased sharply from $5.4 billion in 2002 to $65 billion in

2005 and reached a historical high of $273 billion in 2007. The years 2006 and 2007

observed the surge of the mega-buyouts, including the acquisitions of TXU ($42 billion,

later renamed as “Energy Future Holdings Corp”), HCA Holdings, Inc ($33 billion), Kinder

Morgan ($28 billion), and First Data ($27 billion).

Table 1 breaks down the sample by industry grouping based on SIC codes. Target

firms are from eight broad industries but are concentrated in the manufacturing sector with

approximately 44.5% of the sample coming from this sector. Firms in the service industry

and the wholesale and retail industry are the next biggest grouping. In the late 1980s and

early 1990s, almost 50% of the buyout transactions were from the manufacturing sector.

Since the year 1997, relatively more firms come from the service and the wholesale/retail

industries. Overall, the sample shows an increased industry scope for LBOs over time.

11 Capital IQ provides financials for private companies that belong to one of the following categories: (1).

Private companies with publicly traded debt, (2). M.A. targets filing financials in 8-K/A SEC forms; (3). D&B

Financials; (4). U.S. bank subsidiaries filing with various regulatory bodies in the U.S., such as FFIEC, CUA,

OTS. My sample contains samples of cases (1) and (2). 12 In the rest of the paper, unless specified, all values are inflation adjusted with 2005 as the base year. 13 LBO effective year is the year an LBO is complete. This is shown as the deal closed date or effective date in

Capital IQ and SDC.

- 15 -

I next examine how buyout price have varied over time. Following Kaplan and Stein

(1993), I measure the buyout price, referred to as “total capital”, as the sum of the market

value paid for the target firm’s equity, the value of the firm’s outstanding debt, and the fees

paid in the transaction, minus any cash removed from the firm to finance the buyout.

Column (1) of Table 2 presents the sample medians of total capital by LBO effective year.

For the full sample of 501 transactions, the median buyout price is $ 620.97 million. There

is a trend towards larger deals in later years, significant at 1% level based on the

nonparametric trend test. The median capital for LBOs in the 1990s is $382 million. It

increased to $1,956 million in 2007 due to the mega club deals and reached $2,223 million

in 2011 after the LBO markets recovered from the crisis.

I describe the buyout price relative to fundamentals using two primary measures of

cash flows: EBITDA and the net cash flow (NCF) in the last full year prior to the buyout

completion, where NCF is calculated as EBITDA minus capital expenditures. Columns (2)

and (3) present the median ratios of EBITDA and NCF to total capital by LBO effective

year. The nonparametric trend test shows that both ratios have been decreasing significantly

at 5% level, suggesting a trend of increased buyout price over time.

The decline in buyout cash flow to price ratios may not necessarily reflect anything

unique to the buyout market. To control for overall market trends and macroeconomic

factors, I follow Kaplan and Stein (1993) and calculate the market-adjusted measures that

subtract the earnings to price ratio of the S&P 50014 from the buyout ratios of EBITDA

and NCF to total capital for the quarter in which the deal was priced. Columns (4) and (5)

show that market-adjusted measures still exhibit a significant downward trend, indicating

an increase in buyout prices relative to fundamentals over time.

Another way to look at the extent of a buyout-specific trend in prices is to examine

the premium paid in the buyout transactions, calculated as the percentage difference

between the price paid for a firm’s equity and the firm’s stock price 1 month before the first

announcement of buyout.15 Column (7) presents the annual median premiums paid to

14 The S&P 500 earnings data are downloaded from the S&P Index Data Platforms. 15 I also calculate the premium using stock 1 day and 1 week before the buyout announcement, the results are

robust.

- 16 -

shareholders. The median premiums show no significant time trend over the entire sample

periods. The difference between the trend of buyout premium and that of market-adjusted

ratios of buyout price to fundamentals may be due to the missing data in calculating buyout

premium, as some of the stock prices are missing for the sample firms. As a result, the rest

of this paper will use price relative to fundamentals instead of buyout premiums.

3.2. Evidence on post-buyout operating cash flows

In this subsection, I calculate measures of post-buyout operating performance and

examine how they have changed over time.

3.2.1 Methodology

To document the post-buyout operating performance, I use the operating income as

measured by EBITDA and net cash flow (NCF). Operating income measures the cash

generated from buyout firms’ operations before depreciation, interest, or taxes, and the

calculations do not include gains or losses from sales of divisions or assets. NCF is the

primary component of the numerator in a net present value analysis to value a buyout

company. A permanent increase in NCF, therefore, should lead to an increase in value.

EBITDA and NCF are scaled by sales and average assets for each fiscal year. Performance

change is calculated as the percentage changes of these cash flow measures in the first three

full years after the year of LBO completion (year +1, +2, and +3) compared to the last

fiscal year before the buyout completion (year -1).

In order to evaluate the economic and statistical significance of pre- to post-buyout

changes in performance, I follow Kaplan (1989a) and Guo et al. (2011) and calculate the

industry-adjusted performance measures. The industry-adjusted change equals the

percentage change in the cash flow variables for the target firms minus the median

percentage change over the relevant period for all Compustat firms in the same industry.

Firms in the same industry as the target firms are those that have the same four-digit SIC

code. Comparisons are made at the three-digit level and then at the two-digit level if fewer

than five industry matches are found.

- 17 -

3.2.2. Evidence on changes in operating performance

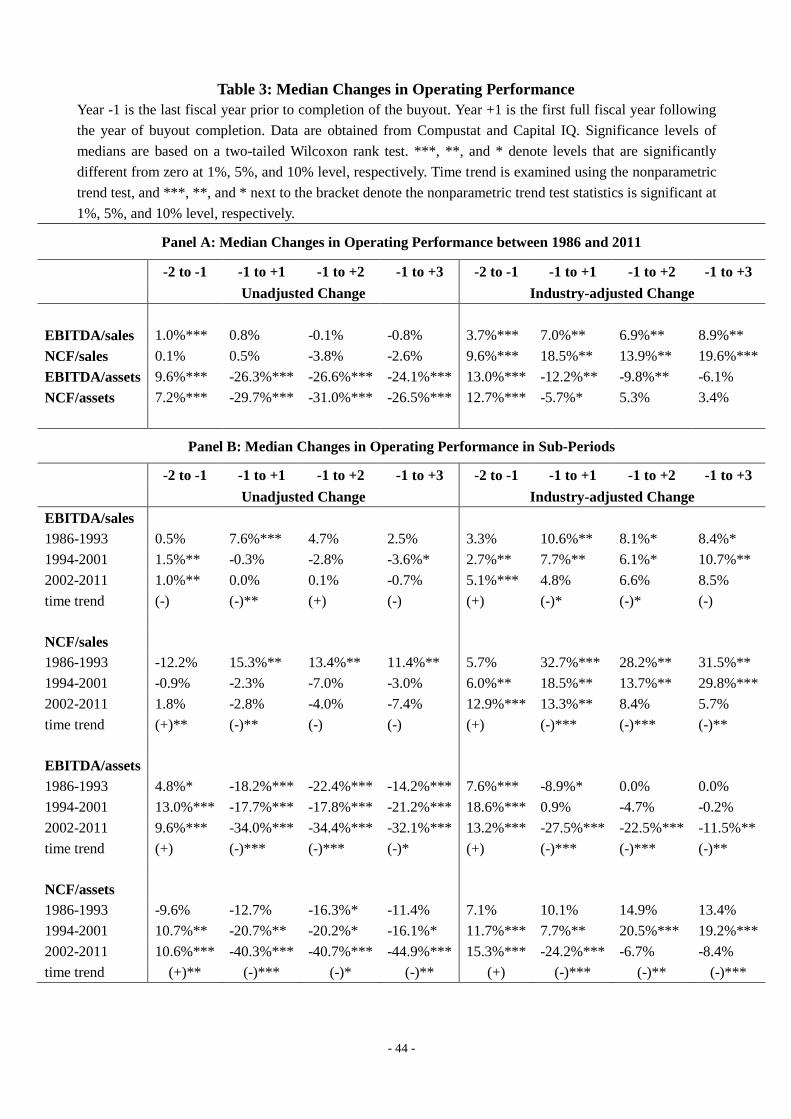

Table 3 summarizes the medians of unadjusted and market-adjusted percentage

changes in operating performance for the last full year prior to completion of the buyout

year (year -2 to year -1) and from year -1 to up to 3 years after the buyout completion.

Panel A shows the median changes over the entire sample period and Panel B presents the

medians in each LBO wave and their time trend. As shown in Panel A, industry-adjusted

percentage increases in EBITDA to sales are significant at 7.0%, 6.9%, and 8.9% in years

+1, +2, and +3 relative to year -1. Changes in NCF to sales adjusted by industry medians

are also positive and significant, with medians of 18.5%, 13.9%, and 19.6% in years +1, +2,

and +3.

In contrast to the increased cash flow variables that are scaled by sales, there are 12.2%

and 9.8% significant decreases in EBITDA over average assets in year +1 and +2 relative

to year -1. The median changes become insignificant in year +3. The significant decrease in

the first year after buyout can be explained by the fact that most LBO firms write up the

book value of their inventories at the time of the buyout (Kaplan, 1989b). According to

Kaplan (1989b), this “paper” inventory write-up is expensed in the first full year after the

buyout. As a result, cost of goods sold is artificially high and the measured change in

operating income as a ratio of average assets during the period underestimates the true

change. Also, as argued by Kaplan (1989b), for most of the buyouts, buyout accounting

leads to a change (usually an increase) in the book value of the assets, representing the

difference between the market value of equity and the book value. This may also lead to an

underestimates of operating improvement or an overestimate of performance declining.

The industry-adjusted changes in the net cash flow as a proportion of average assets

decreased by 5.7% in the first year after the buyout (significant at 10%), the median

changes then become insignificant in year +2 and +3. Overall, the evidence in operating

performance for the whole sample period suggests industry-adjusted performance

improvement after the buyouts.

According to Kaplan (1989a) who finds a significant increase in operating

performance for the management buyout in the 1980s and Guo et al. (2011) that documents

little performance improvement for LBOs in the 1990s and early 2000s, there may be a

- 18 -

fundamental change in the performance of LBOs during the sample periods. Therefore, I

divide the sample period into three sub-periods, 1986-1993, 1994-2001, and 2002-2011,

based on the cyclicality of the LBO market presented by Figure 2. Panel B of Table 3

shows the median changes of performance in each sub-period and the time trend. The

nonparametric trend test results show that there is less performance improvement in the

more recent deals for all four measures. For example, during the period of 1986-1993, the

industry-adjusted percentage increases in NCF to sales are significant at 32.7%, 28.2%, and

31.5% in the first three years after the buyout. The increases between 1994 and 2011 are

still significant, but by a lesser extent at 18.5%, 13.7%, and 29.8%. From 2002 to 2011, only

the increase in the first year after buyout is significant at 13.3% and the changes in years +2

and +3 are insignificant.

To conclude, results in this section show some evidence of performance improvement

after the buyout. However, this is mainly driven by LBOs in the early years, as there is a

significant trend of decreased post-buyout performance improvement in the more recent

deals.

4. LBO deal characteristics and participants involvement

Having documented a decreasing trend of improvements to operating performance,

this section studies factors that are expected to be important drivers for performance based

on the debt disciplining, lenders’ monitoring, private equity reputation, and management

participation hypotheses developed in section 2.2. Specifically, I focus on the pre- and

post-buyout leverage and its change, the composition of LBO debt and its contractual

features, the reputation and bank affiliation of private equity firms, and the trend in club

deals.

4.1. Leverage, debt structure, and contractual features

The debt disciplining hypothesis and the lenders’ monitoring hypothesis state that

firms that have larger amount of leverage added during the LBOs and are more closely

monitored by lenders will experience more improvement to operating performance. Having

- 19 -

documented a decreasing trend of performance improvement, I now examine whether and

how leverage, bank debt proportion, loan covenants and maturity structure have changed

over time.

4.1.1. Leverage

Panel A of Table 4 reports the capital structure change from the buyout. Columns

(1)-(3) show the sample median of the pre- and post-buyout leverage and leverage changes,

calculated using the financial data from Compustat and Capital IQ. Prior to the buyout,

firms have a median leverage ratio of 31.92%. Leverage increased significantly to a sample

median of 64.35% after buyout, with a median percentage increase in leverage of 30.55%.

Column (4) shows the median leverage change of all Compustat firms. Comparing the

LBO sample and the Compustat population, I find that the leverage increase is unique to

LBO firms. Over time, both the leverage change and the post-buyout leverage ratio have

been decreasing. Column (5) shows that equity ratio has a significant increasing trend over

time. The decreasing trend of leverage change, in combination with the declined

post-buyout performance, provides some preliminary evidence for the debt disciplining

hypothesis.

4.1.2. LBO debt structure

I next study the composition of LBO debt and its contractual features, using tranche

(or “facility”) level data constructed from Dealscan and Capital IQ. LBO debt is syndicated

through different tranche. According to Miller (2012), revolving credit facility and

amortizing term loan (term A loan, or TLa) are usually packaged together and syndicated to

banks.16 The term B, C, and D loans are structured specifically for institutional investors,

such as structured investment vehicles, loan participation mutual funds, hedge funds,

pension funds, insurance companies, and other proprietary investors (Miller, 2012).

Therefore, I consider the revolving credit facility and the term A loan tranche in a loan

package as bank debt and term B, C, and D loans as institutional debt. I also consider notes

16 A revolving credit facility allows borrowers to draw down, repay, and re-borrow capital over time. A term

loan is an installment loan that requires a complete withdrawal of funds at inception.

- 20 -

that are sold to institutional investors as institutional debt. The bridge loan tranche from

Dealscan and the mezzanine debt from Capital IQ that are subordinated to bank and

institutional debt are considered the junior debt.17

Panel B of Table 4 presents the structure of LBO debt over the years. For each

category of debt, I calculate the ratio of the amount of debt to total LBO debt and the

percentage of LBO deals that use this type of debt. Columns (1) and (2) demonstrate the

use of revolving credit facilities and term A loans in financing LBO debt. The ratio of

revolving credit facilities to total LBO debt has decreased over time, from 61% in 1986 to

13.7% in 2011. The ratio of term A loans to total LBO debt has also declined, from its peak

of 76.9% in 1993 to 1.2% in 2011. Although most LBOs continue to use revolving credit

facilities, the proportion of LBOs that use A-term loans significantly declined from 47.1%

in 1993 to 5.7% in 2011. As a result, the ratio of bank debt to total LBO debt and the

percentage of LBO deals that use bank debt have decreased significantly, as shown in

Column (3). All of these time trends are consistent with the declining importance of banks

in financing LBO deals. With the decrease of bank debt, there has been an increasing use of

institutional debt, as presented in Column (4). The proportion of institutional debt has

increased from 1.2% in 1989 to 58.4% in 2011 and the nonparametric trend test shows a

significant increase in the proportion at 1% level. Since 1998, the proportion of institutional

debt in total LBO debt has exceeded that of bank debt, suggesting that institutional

investors have become more important in the LBO market.

The last column of Panel A demonstrates the use of junior debt. The use of junior debt

is mainly concentrated in the late 1980s and the 2000s. The large proportion of junior debt

in the total LBO debt in the late 1980s corresponded to the use of high yield junk bond

whereas since 2002 the use of mezzanine debt in LBO financing has increased

dramatically.

In summary, analysis of this subsection shows that the importance of banks as

financiers of LBO transactions has been decreasing and that institution debt has become

17 I follow Shivdasani and Wang (2011) and record bridge loans as high-yield bond/note and mezzanine finance.

Mezzanine debt is a committed financing with individually negotiated terms. All or part of the interest expense

of the mezzanine debt is often in the form of additional securities rather than cash. Investors of the mezzanine

debt are typically insurance companies and the mezzanine funds.

- 21 -

more important in financing LBOs. These trends may provide some explanations for the

decreasing performance of post-buyout firms as bank monitoring has been considered as

instrumental in reducing agency costs of debt and therefore creating value in LBOs

(Diamond 1984, 1993; Park 2000). This relation will be tested in the multivariate analysis

in the next section.

4.1.3. LBO loan spread, maturity, and covenants

I next examine the spread, maturity, and covenants of bank debt verses institutional

debt. Columns (1)-(3) of Table 4 Panel C present medians of the all-in-drawn interest

spread of bank debt, institutional debt, and their differences. All-in-drawn spreads (over

6-month London Interbank Offered Rate (LIBOR) for each tranche are from Dealscan and

include both the interest cost and fees associated with borrowing. Column (1) shows a

significant increasing trend over time for spreads of bank debt. Institutional debt spreads

are higher than bank debt spreads but the institutional-bank difference reported in Column

(3) narrows with the increased usage of institutional debt in LBO financing. This is

consistent with Miller’s (2012) argument that the spread difference between institutional

loans and bank loans narrows when the institutional demand for syndicated loans is high.

I expect that the maturity structure of LBO loans is related to performance as shorter

maturity increase required debt service payment in the earlier stage of the LBOs and

therefore increasing the incentives for managers to work hard to generate cash and to avoid

wasting resources. Columns (4)-(6) show the median maturity (in months). There is no

significant change in the maturity of bank debt. However, the maturity of institutional debt

has decreased throughout the sample period, from 120 months in 1992 to 79 months in

2011, suggesting better monitoring of institutional investors in the more recent LBOs.

I also examine the covenants of LBO debt as they provide specific requirements and

restrictions on management behavior that reduce the agency costs associated with the

conflict of interests between shareholders and debt holders. Covenant information is

obtained from Dealscan. To measure the tightness of covenant restrictions, I use the

covenant intensity index developed by Bradley and Roberts (2004). This index indicates

whether each loan package contains the following six specific covenants—asset sale sweep,

- 22 -

debt issuance sweep, equity issuance sweep, financial covenant, dividend covenant, and

secured debt covenant—and counts the number these covenants in each package. The first

three covenants, also referred to as the “sweeps”, specify the percentage of net proceeds

from an asset sale, debt issuance, or equity issuance that the borrowers must use to pay

down any outstanding debt. Financial covenant enforces minimum financial performance

measures that the borrowers must maintain. Bradley and Roberts (2004) define a binary

variable that is equal to 1 if the loan contract contains more than two restrictions on

financial ratios and zero otherwise. Dividend covenant restricts the ability of the borrowers

to distribute cash to shareholders and secured debt covenant requires the debt to be secured.

The covenant intensity index counts the number of covenants included in each loan

package and the index ranges from 0 through 6. Covenants are unique to packages, so that

every tranche in a package is covered by all of the covenants. If an LBO uses multiple loan

packages, I use the index of the most covenant-heavy package as the covenant index of the

deal. Column (7) presents the median covenant intensity index each year for loans with

non-missing covenant information. The number in the bracket shows the proportion of

LBOs with non-missing loan covenant information of total LBOs each year. As information

on covenants is fairly limited prior to 1994, loans syndicated before 1994 only have

secured debt covenant reported. During the period of 1995-2011, LBO loans have a median

of 5 covenants based on the measure of Bradley and Roberts (2004) and there is a

significant decrease in covenant tightness. In 2002, the median number of covenants was 6;

however, the number dropped to 1 for LBO loans syndicated in the late 2000s.

The Bradley and Roberts (2004)’s index only considers the presence of financial

covenants. It does not take into account the number or different types of financial

covenants used in a debt contract. However, there is large variation in the use of financial

covenants in my sample and the number of financial covenants included in the LBO loan

packages ranges from 0 through 6. Therefore, I modify the index by including the number

of financial covenants used in each package. Specifically, the modified covenant intensity

index is the sum of (1) number of financial covenants (up to 6), (2) number of sweeps

(asset sales sweep, debt issue sweep, equity issue sweep, excess cash flow sweep, insurance

- 23 -

proceeds sweep18), (3) dividend covenant (0/1 variable), and (4) secured debt covenant (0/1

variable).19 The modified index is presented by Column (8). LBO loans constructed

between 1998 and 2002 used more covenants, with a median of 8-10 covenants. The

number of covenants decreased in the second half of the 2000s with only 1 or 2 covenants

for LBO loans in 2010 and 2011.

Column (9) shows the proportion of LBO loans with no financial maintenance

covenants (the covenant-lite loans).20 There is a general trend towards more covenant-lite

loans over time. In summary, results from Columns (7)-(9) show declining tightness of

covenant restrictions of LBO loans, suggesting weaker monitoring by lenders that may lead

to worse post-buyout performance.

4.2. Private Equity in LBOs

4.2.1 Private Equity Involvement

The private equity reputation hypothesis on LBO value creation states that LBOs

sponsored by PE firms of high reputation tend to perform better as these PEs have better

skills to improve performance and to reduce risks of target firms (Kaplan and Schoar, 2005;

Axelson, et al., 2009). Therefore, I examine the changing characteristics of PE firms that

are expected to be instrumental to LBO success. To identify PE firms, I download all

private equity funds (PE funds) from Capital IQ. For each LBO transaction that is collected

from Capital IQ, I merge the buyer Excel Company ID of the LBO to the PE funds Excel

Company ID. For the buyout sample from SDC, I run a text search for the names of PE

firms in the transaction synopses and hand match with the PE funds from Capital IQ. As

18 The excess cash flow sweep and the insurance proceeds sweep specify the percentage amount of net proceeds

a borrower receive from excess cash flows or insurance settlements that must be used to pay down any

outstanding loan balance. Including the two sweeps ensure that all sweep covenants are considered in the

modified intensity index. 19 Covenant intensity measures used in this paper indicate the presence of certain covenants in the loan contract,

not the actual threshold of each covenant. This is because the thresholds for financial covenants and sweeps are

related to many factors, such as the credit market conditions and the borrowers’ specific characteristics.

Therefore, it is hard to compare the threshold directly. 20 According to Bavaria and Lai (2007), S&P define covenant-lite loans as those with no maintenance financial

covenants that have to be maintained quarterly through the term of the loan. Instead, covenant-lite loans have

only incurrence covenants that do not have to be met on an ongoing basis as maintenance covenants do.

Incurrence covenants only restrict the borrower’s ability to issue new debt, make acquisitions, or take other

action that would breach the covenants.

- 24 -

this paper is to look at private equity involvement at firm level, I consolidate PE funds to

PE firm level. So if one PE firm has multiple active PE funds, I use the Excel Company ID

at the PE firm level for the analysis. For example, both Lehman Brothers Mezzanine Fund

and Lehman Brothers Capital Partners IV are identified at the PE firm level as the Lehman

Brothers, Private Equity Division. I also track the name changes of the PE firms. Of the

501 LBO deals in the sample, 448 deals have at least one PE firm involved. The remaining

transactions are either management buyouts or buyouts by another corporations with no PE

firm involved. There are in total 234 PE firms sponsoring the 448 deals. Appendix A

presents the top 25 PE firms of these 234 PE firms by the number of deals and total

transaction values of buyouts they sponsored. The most frequent PE firms are Kohlberg

Kravis Roberts & Co (27 deals), TPG Capital (26 deals), The Blackstone Group, (22 deals),

Goldman Sachs Capital Partners (21 deals), and Bain Capital Private Equity (20 deals).

Panel A of Table 5 presents the PE firms’ involvement in LBOs over the sample

period. Column (1) shows the number of buyouts that have PE firms involved and its

proportion in all LBOs in the year (in the brackets). There is an overall trend of increased

PE involvement. In the late 1980s, the average proportion of LBOs with PE firms involved

is around 73%. In the 1990s, almost all LBOs have PE firms. Following Officer, Ozbas,

and Sensoy (2010), I categorize a PE firm as a prominent PE if it is listed as the 50 largest

PE firms by the Private Equity International (PEI) magazine from the year 2007 to 2013.

Starting 2007, the PEI magazine ranks PE firms based on the capital raised over the

previous five-year period. I add the PE firms that are listed as the top 25 PEs in my sample

from Appendix A to this list of prominent PE firms if they are not already included in the

prominent list. The PE firms added are mainly those that are subsidiaries of banks (the

bank-affiliated PEs), as these firms may not be on the PEI list because they may use

internal capital rather than relying on external fundraising. Following Officer et al. (2010) I

also add Forstmann Little and HM Capital Partners (formerly Hicks, Muse, Tate, and Furst)

because they are historically prominent PE firms that have been less active in recent

fundraising. Column (2) shows that 52% of the LBOs in my sample have prominent PE

firms and there is a trend of more prominent PEs involved in LBOs over time.

Fang et al. (2012) argue that it is important to look at bank-affiliated LBOs where the

- 25 -

PE firms are subsidiaries of major banks as these deals may have different characteristics

than LBOs sponsored by the stand-alone PE firms. First, bank-affiliated PEs may have

better access to funds provided by their parent banks should an LBO opportunity rise and

these PE firms are better able to take advantage of the favorable credit market conditions.

Second, these bank-affiliated deals provide the parent banks with cross-selling

opportunities (such as potential M&A advisory work, cash-management services, etc.) that

increase parent banks’ fee income. As a result, buyout decisions may not be based on PE’s

expectation on efficiency improvement of target firms, but only to take advantage of these

cross-selling opportunities.

To confirm bank affiliation, I check whether a PE firm is a subsidiary of a bank at the

LBO announcement day.21 I further require that the parent bank provides loans for the deal.

There are in total 103 bank-affiliated deals (21% of 501 LBOs) in the sample and the total

transaction value of these deals is 35% of the sum of transaction value of all 501 LBOs.

This is similar to the findings of Fang et al. (2012) that bank-affiliated groups account for

nearly 30% of the overall private equity market, and the findings reported by

Lopez-de-Silanes, Phalippou, and Gottschalg (2011) that roughly one-third of the

investment in the global private equity dataset are done by PE groups that are subsidiaries

of banking and finance companies. Column (3) presents the number of bank-affiliated deals

by year. Bank-affiliated deals exhibits cyclicality corresponding to the LBO market

activities. In the years 1989, 1998, and 2007, when the LBO activities were at the peak of

the cycle, the proportions of bank-affiliated deals in total LBOs was higher. This is

consistent with Fang et al. (2012) that PE firms time the market and bank affiliations allow

these PE firms to take advantage of favorable credit market conditions.

I then look at the club deals, where a consortium of two or more PE firms are

involved in an LBO deal. Column (4) shows the number of club deals and its percentage

over total LBOs each year and Column (5) presents the sum of transaction values of club

deals each year and its ratio over the total transaction values of the 501 LBOs. 30% of the

LBOs in my sample are club deals and the total transaction values of these deals are 50% of

21 Some PE firms started as subsidiaries of major banks but later became independent. I only consider an LBO

as bank-affiliated if it is announced during the time the PE firm is subsidiary of a major bank.

- 26 -

all deals. This is consistent with PE firms pooling their assets to acquire large targets.

Column (6) shows the maximum number of PE firms in a club deal consortium by year.

Club deals are very rare in the late 1980s and early 1990s and they start to become

important in the late 1990s. During 2005-2008, club deals reached their peak—almost 50%

of LBOs were club deals and the total transaction value of these deals was around 80% of

all LBOs during the time. The largest-ever LBO, the buyout of TXU in 2007 with a

transaction value of $44.5 billion was conducted by a consortium including KKR, the TPG

Capital, and Goldman Sachs Capital Partners. As shown by Column (6), there is a general

trend of more PE firms cooperating in a club deal. During the whole sample period, there

are on average 2.6 PE firms in the consortium of the club deals (not tabulated). The deal

that has the largest number of PE firms involved is the buyout of SunGard Data Systems

sponsored by seven PE firms and completed in 2005 with a transaction value of $11.5

billion.22

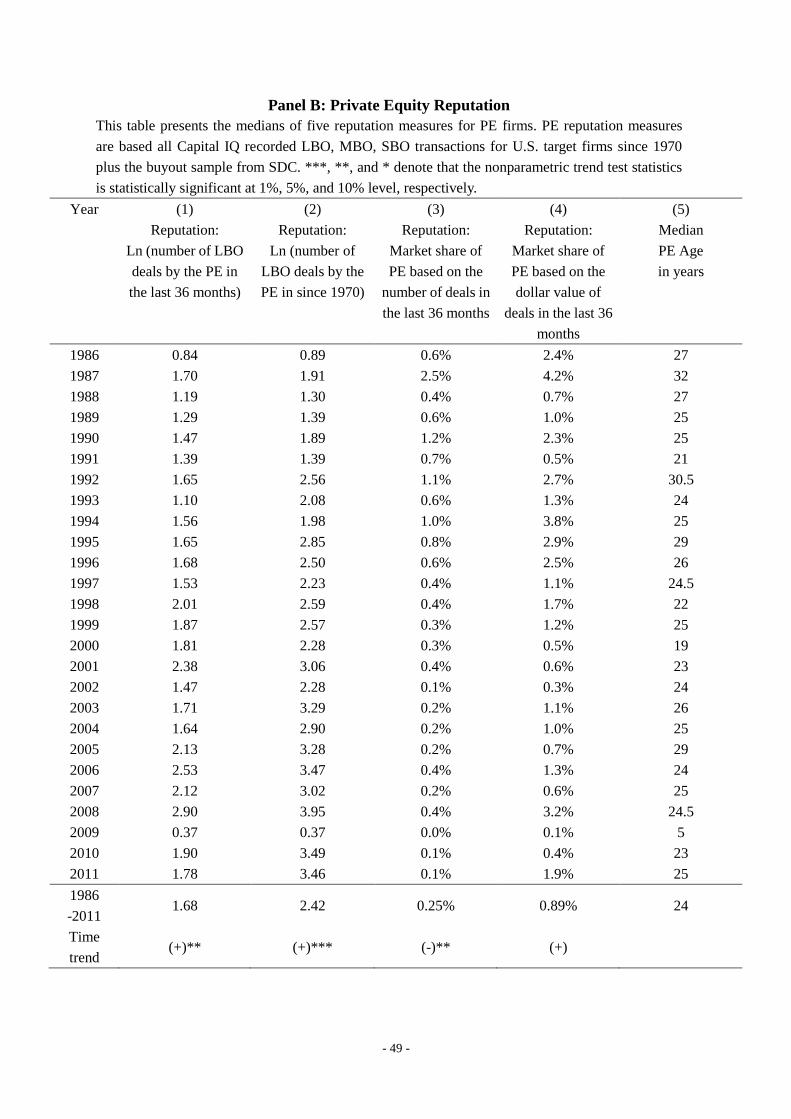

4.2.2. Private Equity Reputation

Having documented the time trend of PE firms’ involvement in LBOs, I construct

measures for private equity reputation that capture PE firms’ past experience and skills.

Previous empirical studies measure PE fund reputation in a number of different ways that

include fund size, its market share, the number of recent LBO transactions, and the number

of previous fund raisings23. As the PEs in my sample are at the firm level, I use reputation

measures that can be constructed for each PE firm. I follow Demiroglu and James (2010)

and construct reputation measures based on the number of LBOs sponsored by the PE firm

and the total transaction values of these deals in the past 36 months or since 1970.24 In

order to get the LBO transaction history, I use all Capital IQ recorded LBO, MBO, SBO

transactions for U.S. target firms since 1970 plus the buyout sample from SDC—a total of

19,014 deals. In the case of club deals, I consider the buyout as a full deal for each PE firm.

When calculating LBO deal-level PE firm reputation, I use the reputation score of the PE

22 The seven PE firms were Silver Lake, Bain Capital, the Blackstone Group, Goldman Sachs Capital

Partners, KKR, Providence Equity Partners, and the TPG Capital. 23 See Demiroglu and James (2010) for discussions on strengths and weaknesses of each reputation measures. 24 The earliest LBO deal documented by Capital IQ is in 1970.

- 27 -

firm with the highest reputation if the deal has multiple PE firms. The reputation score is

set to zero if there are no PE firms involved in the buyout deal.

Panel B of Table 5 presents the PE reputation measures. The first reputation measure

is based on the number of deals. Columns (1) and (2) show the medians of the reputation

measures calculated as the natural logarithm of the total number of deals completed by a

certain PE firm during the past 36 months and since 1970, respectively. Both reputation

measures have shown an increasing trend, suggesting that PE firms are more involved in

LBO deals now than before.

A second measure for PE firm’s reputation is based on its market share. Market share

of each PE firm at the time of a new LBO deal is calculated as the ratio of the number of

deals completed by the PE firm in the prior 36 months over the total number of deals

(based on the 19014 deals) during the same 36 months. I also calculate PE firm’s market

share as the ratio of the total transaction value of LBOs by the PE firm in the prior 36

months over the total transaction value of all LBOs during the 36 months. Column (3) and

(4) shows the median reputation score based on market share. The median PE firm in my

LBO sample has about 0.25% (mean 0.44%) market share by number of deals and 0.89%

(mean 2.1%) market share by deal value in the LBO market.

Another reputation measure is years of experience, which is calculated as the number

of years based on the first ever LBO deals sponsored by the PE firm and the last LBO deals

in the sample. Overall, the median PE firm in the sample has 24 years (mean: 21 years) of

experience and has invested in 15 LBOs (mean: 22 LBOs) since 1970 (not tabulated).

In summary, analyses of this subsection show that PE firms have become more

involved in LBO deals, as evidenced by the increasing proportion of LBOs sponsored by

PE firms in the more recent years and the increasing importance of club deals.

Bank-affiliated LBOs have shown some cyclicality that corresponds to the credit market

condition, suggesting some market timing of these deals. The reputation score for PE firms

based on their market share has been decreasing. The next section will examine how these

PE reputation and involvement are related to performance.

- 28 -

5. Explanations for post-buyout operating performance

In this section, I examine the relationship between operating performance and the

LBO deal characteristics that are expected to be related to performance change. My goal is

to test the different hypotheses developed in Section 2.2 to determine factors that contribute

to value creation in LBOs. The analysis will also help to understand whether the

documented changing characteristics of LBOs can be used to explain the reduced

performance improvement observed in the more recent LBO deals.

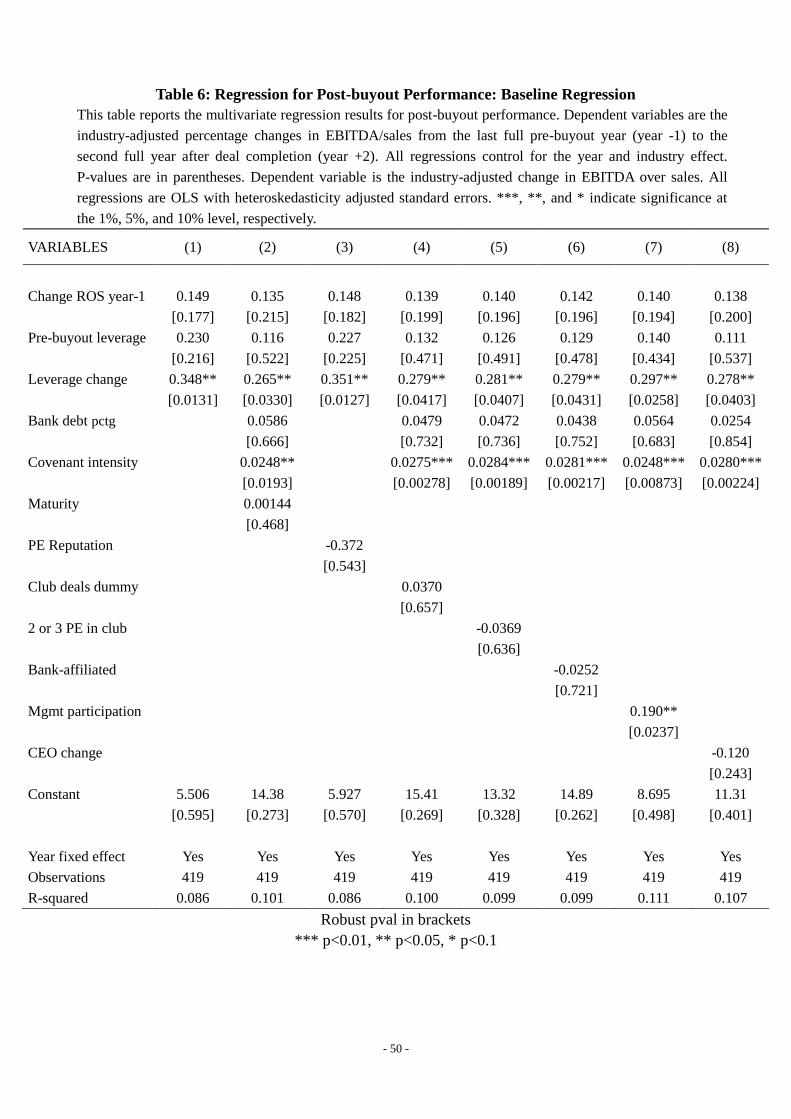

Table 6 reports the multivariate regression results for post-buyout operating

performance and its drivers. The dependent variables are the industry-adjusted percentage

changes in EBITDA/sales from the last full pre-buyout year (year -1) to the second full

year after deal completion (year +2). This allows me to include LBO deals completed by

the end of 2010 to look at the performance of LBOs during and after the 2007-09 financial

crisis. Also, I use EBITDA scaled by sales, instead of total assets, to avoid the inventory

write-up problems related to total assets as described in Kaplan (1989b). To control for

pre-buyout characteristics of target firms, all regressions include leverage ratios at the end

of year -1 and the industry-adjusted change in EBITDA/sales from year -2 to year -1. All

regressions control for year and industry effect.

First, I look at the disciplining effect of leverage. Column (1) shows that the effect of

leverage change on performance is significantly positive. That is, firms with greater amount

of leverage added during the LBOs show more post-buyout performance improvement,

supporting the debt disciplining hypothesis. I next examine whether and how performance

is related to the monitoring by lenders. I include the proportion of LBO debt that is funded

by banks, with the expectations that banks have more incentives and advantages to monitor

the borrowing firms and that the percentage of bank debt is proportional to banks’

monitoring effort. I also include the modified covenant intensity index that measures the

presence of different covenants in LBO loans. The maturity structures of LBO debt are also

used in the regression, with the expectation that shorter maturities indicate better

monitoring by lenders therefore leading to better performance.25

25 For robustness, I replace the maturity of the whole LBO loans with maturity of bank loans and maturity of

- 29 -

Column (2) demonstrates a significantly positive coefficient for covenant intensity,

suggesting that controlling for the leverage effect, tighter covenants further improves the

post-buyout performance. These covenants generally put restrictions on the target firms’

use of cash flow, therefore further reducing the agency costs of the free cash flow problems.

Covenants also require target firms’ to maintain certain financial ratios and restrict them

from using more debt, possibly motivating managers to improve efficiency and to increase

earnings. However, bank debt proportion and maturity are insignificant drivers for

performance.

I then examine the effects of PE firms’ reputation and involvement on performance. I

use different PE reputation measures constructed in the last section as independent

variables in the regression. However, none of these reputation measures is significantly

related to performance (Column (3)). Column (4) shows result for a regression that

includes the club deal dummy that takes the value 1 if an LBO has more than two PE firms

involved and 0 otherwise. It has been argued that in a club deal, different PE firms bring

different expertise to the target firm’s management, therefore providing another source of

value creation.26 However, the result in Column (4) does not support this argument.

Another view on club deal is that as the size of the consortium of PE firms gets bigger, it is

harder to make timely operational and management decisions. Experts of the private equity

industry suggested that the optimal size of the consortium is two or three PE firms.27 I

construct an optimal consortium size dummy variable that takes the value of 1 if there are

two or three PE firms in a club, and 0 other wise. However, regression result presented by

Column (5) shows no evidence that the optimal consortium size is related with performance.

In column (6), I include a dummy variable that indicates whether an LBO is bank-affiliated

deal, where bank affiliation is defined as (1) the PE sponsoring the deal is a subsidiary of a

institutional loans, the results are similar.

26 For example, New York Times commented on KKR, Bain, and Vornado Realty Trust’s buyout of Toys "R"

Us that “it was clear what each firm brought to the table. Kohlberg Kravis has a good reputation in the retail

business, Bain has a good record doing turnarounds and Vornado clearly knows real estate”. Source: “Do Too

Many Cooks Spoil the Takeover Deal”, the New York Times, April 3, 2005. 27 For example, Jeffrey Walker, a managing partner of CCMP Capital, said that “I find it very difficult

managing a deal that has more than two or three investors”. Source: “Buyout Veterans Have Questions about

Club Deals”, Dow Jones Newswires, January 24, 2007.

- 30 -

bank and (2) the parent bank provides loans for the deal. I find that bank affiliation has no

significant effect on performance. In sum, regression results presented in Columns (3)-(6)

provide no evidence that PE firms’ involvement or reputation is related to performance of

target firms.

I test the management participation hypothesis that LBOs tend to perform better when

managers of target firms contribute equity and participate in the buyout as their incentives

are better aligned with other shareholders. I use a dummy variable that indicates management

participation. Specifically, the dummy variable equals 1 if Capital IQ labels a transaction as

“management buyout”, “management participated”, “individual investor participated”

when the individual investor is confirmed to be board member or management of the target

firm, or the firm is bought out through an employee stock ownership plan (ESOP). If a

transaction is from the SDC database, the dummy is equal to 1 if the SDC synopsis

describes the deal as “management led” or “management participated”. Results in column