december, 2016 - liaa · aventis and pfizer have all made acquisitions in this area in brazil....

TRANSCRIPT

December, 2016

ELANbiz is a project financed by the

European Union

2

The pharmaceutical sector in

Latin America

4 LATAM markets within the top 20

The pharmaceutical markets of LATAM

X=Per capita pharmaceutical spending/ Bubble size=Absolute market size in US$ billions

US$87.29bn in 2018

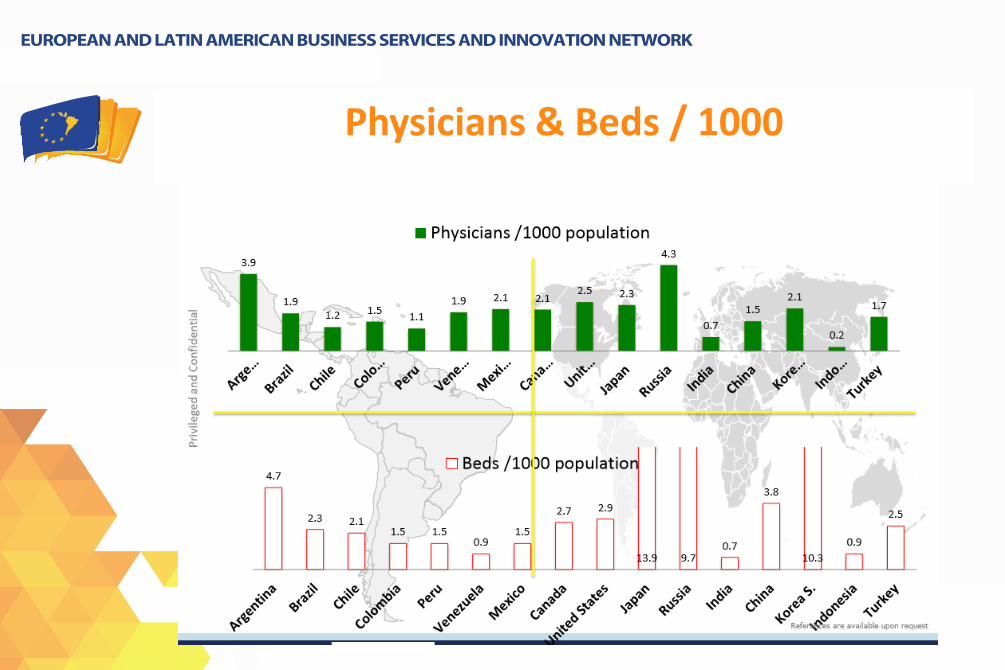

Physicians & Beds / 1000

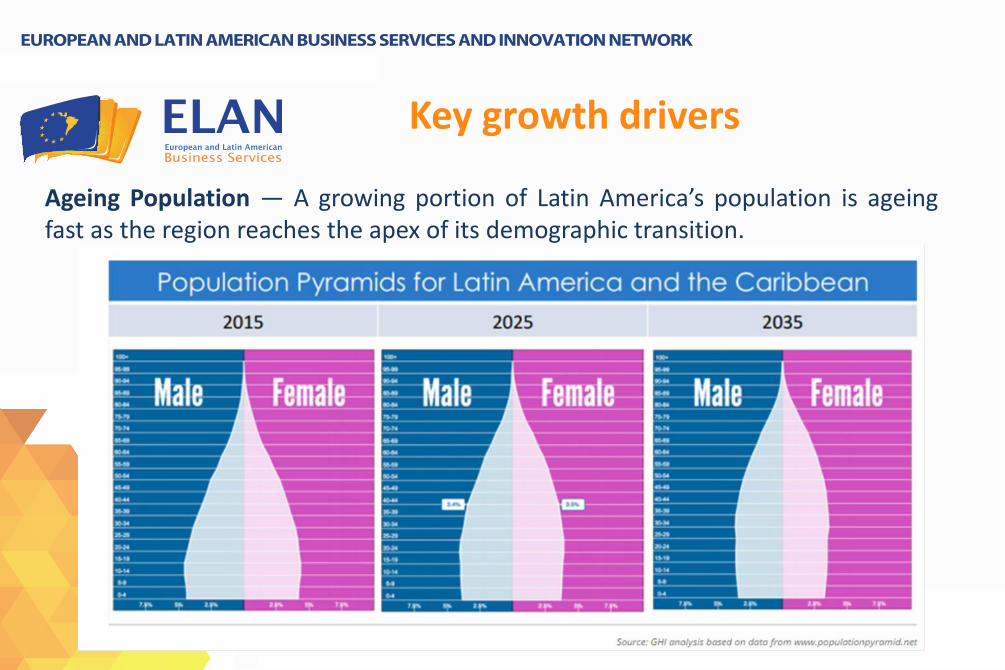

Key growth drivers

Ageing Population — A growing portion of Latin America’s population is ageing fast as the region reaches the apex of its demographic transition.

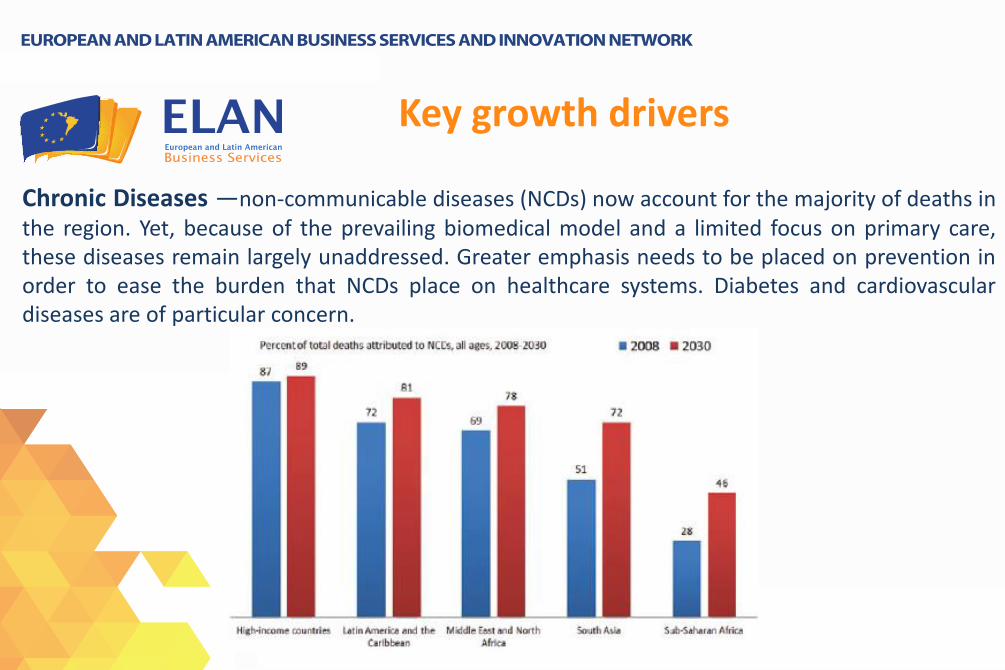

Key growth drivers

Chronic Diseases —non-communicable diseases (NCDs) now account for the majority of deaths in the region. Yet, because of the prevailing biomedical model and a limited focus on primary care, these diseases remain largely unaddressed. Greater emphasis needs to be placed on prevention in order to ease the burden that NCDs place on healthcare systems. Diabetes and cardiovascular diseases are of particular concern.

Key growth drivers

Key growth drivers

Obesity — A risk factor for many of the chronic diseases plaguing LA

Key growth drivers

Manufacture of generic drugs driven by the expiry of a number of key patents during the last few years. This has provided ideal opportunities for the startup of new facilities in the region.

• In Brazil, generics make up the largest segment of drug sales accounting for 22% of the total. Amgen, Sanofi-Aventis and Pfizer have all made acquisitions in this area in Brazil.

Competitive landscape

• 2014 report from GlobalData: approximately $12.7 billion has been invested in Latin America’s pharmaceutical market through mergers and acquisitions in recent years, and this level of investment is expected to continue.

• According to the report, the number of pharma-related M&As in the region increased by 214% between 2008 and 2012, and accounted for 70% of the region’s total deals during this period.

Competitive landscape

M&As have come from global pharmaceutical firms acquiring local companies

• US-based UnitedHealth’s acquired Brazil’s Amil Particapacoes in 2012 at a cost of US$4.9 billion.

• Merck Inc announced joint venture agreement with Supera Farma Laboratórios,

• US drugstore chain CVS Caremark made its first overseas acquisition of Drogaria Onofre, Brazil’s eighth largest pharmacy chain.

• 2014 GSK, Pfizer, Novartis and Abbott were reported to be bidding for Aché Laboratorios Farmaceuticos, fourth largest drugmaker in Brazil

Competitive landscape

• 2014, the Mexican Association of Industrial and Pharmaceutical Research (AMIIF) reported that six more international pharmaceutical companies, Mundipharma, Menarini, Eisai, Innovare, Celgene and Alexion have joined the association to expand their presence in Mexico’s patented medicine sector.

• Mundipharma announced plans to invest US$40m in Mexico, including US$20m to buy local drugmaker Eticare Pharmaceutical

• Having already established operations in Brazil and Colombia, Mundipharma is also looking to enter the pharmaceutical markets in Venezuela, Argentina, Chile, Ecuador, Peru and Central America

Competitive landscape

As well as M&A activity there are innovative licensing and expertise sharing arrangements being established.

• For instance, at the beginning of 2014 Reckitt Benckiser of the UK agreed a US$482m license deal with the US’s Bristol-Myers Squibb to sell a number of BMS’s over the counter drugs in Brazil and Mexico.

Investing in the pharma sector in LATAM?

• Market growth is significantly greater than in the developed world and these so called “pharmerging” countries provide an ideal opportunity for continued business growth.

• Manufacturing costs are lower than in developed countries.

• The region is becoming an increasingly attractive area in which to conduct clinical trials.

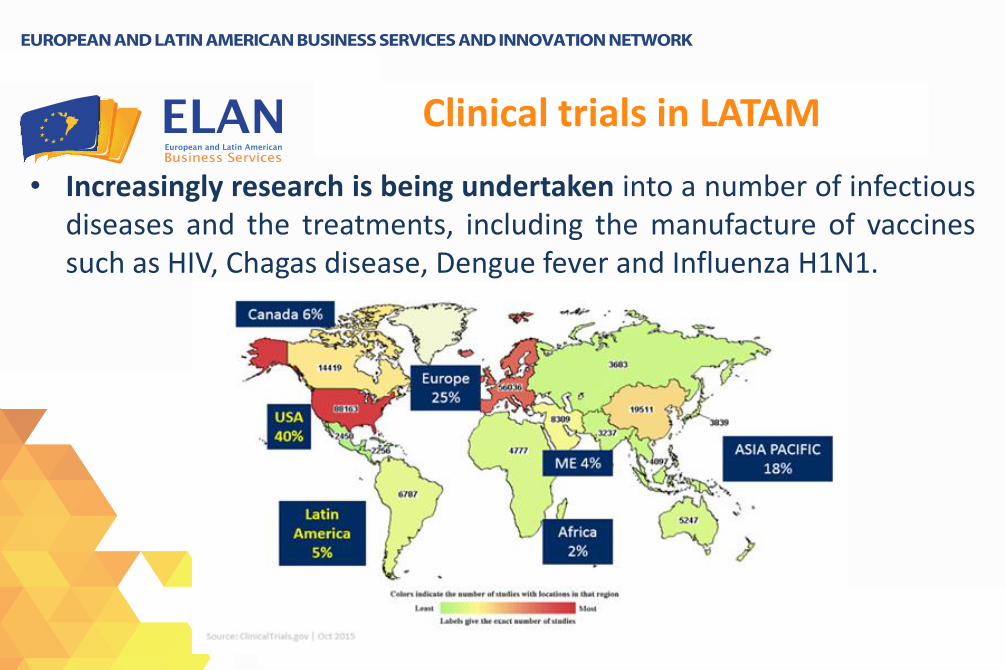

Clinical trials in LATAM

• Increasingly research is being undertaken into a number of infectious diseases and the treatments, including the manufacture of vaccines such as HIV, Chagas disease, Dengue fever and Influenza H1N1.

• The cost of conducting such trials is cheaper than in the developed world and there is a large and varied supply of trial patients with about half of the dropout rate seen in Europe.

• For firms based in the northern hemisphere, the season reversal in the southern hemisphere can be advantageous when researching into seasonal illness.

Clinical trials: LATAM advantages

Clinical trials: LATAM advantages

• Large, urban patient populations in all therapeutic indications enables faster enrollment and f/up

• Large drug naïve patient populations with common and special disease profiles

• Rapid compliant patient recruitment

• Highly involved and experienced investigators

• Ready and professional supply of research facilities and contract research organizations (CROs) offering professional services for partnering solutions in clinical trial conduction

• In 2014, the French pharmaceutical company Sanofi announced results of tests on the first ever vaccine for Dengue fever. Sanofi has invested US$1.7bn in the project over two decades and the final study was conducted on 20,875 children aged 9-16 in Brazil, Colombia, Mexico, Honduras and Puerto Rico

• Marken, the multinational specialist clinical logistics company, has just opened clinical trials warehouse in Argentina, Brazil, Peru and Chile in 2015

Clinical trials growth in LATAM

Challenges

Commodities low prices and currency Devaluations will continue to put pressure on manufacturers profit margins —

Challenges

LATIN AMERICA’S BOOMING PHARMA INDUSTRY IS A LOCAL AFFAIR

• The real winners are Latin American generic drug makers and locally owned retailers.

• Local producers are growing at 28% per year enabling generics to be sold in domestic markets 70% more economically than their patented counterparts

• Brazilian, Argentine and Cuban generics producers already export their goods to other emerging markets in Asia, Africa and the mid-East

Challenges

PHARMACY SECTOR CONSOLIDATION AND PRIVATE BRANDING GROWTH

• Growing demand for generic drugs and the pharmacy retail sector is quickly evolving to meet demand. Chile was the first to modernize and consolidate its pharmacies. Farmacias Ahumada S.A. (Fasa), based in Santiago, is the largest drugstore chain in Latin America and one of the largest in the world in number of outlets, with a network of nearly 1,000 pharmacies in Chile, Peru, Brazil, and Mexico.

Challenges

PHARMACY SECTOR CONSOLIDATION AND PRIVATE BRANDING GROWTH

• Pharmacy chains and supermarkets in Mexico went from controlling 69% of pharmaceutical sales in 2007 to 88% in 2014

• Wal-Mart’s entry in the pharmacy market in Mexico and Femsa’s acquisition of Mexican local pharmacy chains Farmacias Yza and Farmacias FM Moderna are testimony to how modern retail chains are taking control of pharmaceuticals in Latin America.

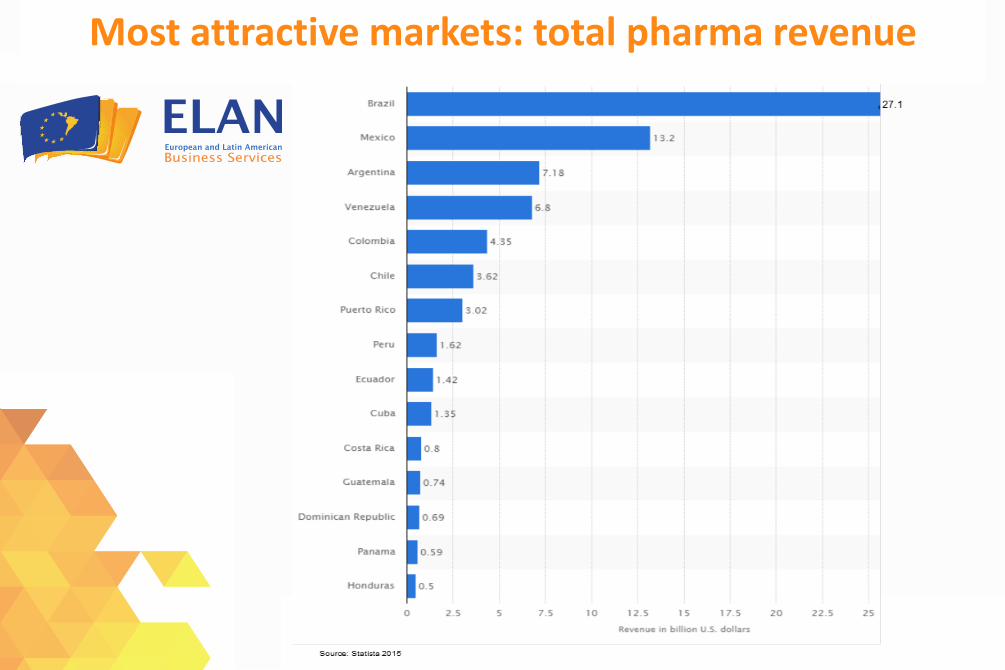

Most attractive markets: total pharma revenue

Most attractive markets

• Brazil will continue to be the primary driver of healthcare expenditure in the region, accounting for ~43% of the region’s pharmaceutical sales between 2013-2017

• Followed by Mexico as the region’s second largest market with ~17% of the region’s sales. Brazil is expected to become the world’s fifth largest pharmaceutical market by 2016.

Most attractive markets

• Colombia and Peru present strong growth prospects, albeit from a small base.

• Chile maintains the characteristics of a more mature market, with consistent and stable growth.

• In contrast, the economic woes and inflationary pressures currently besetting countries such as Argentina and Venezuela are causing varying degrees of distortion to the market values, pricing and margins in these countries. As a result, it is difficult to predict how these markets will fare, though the picture looks grimmer than for their neighbours

Risk/rewards rating (BMI)

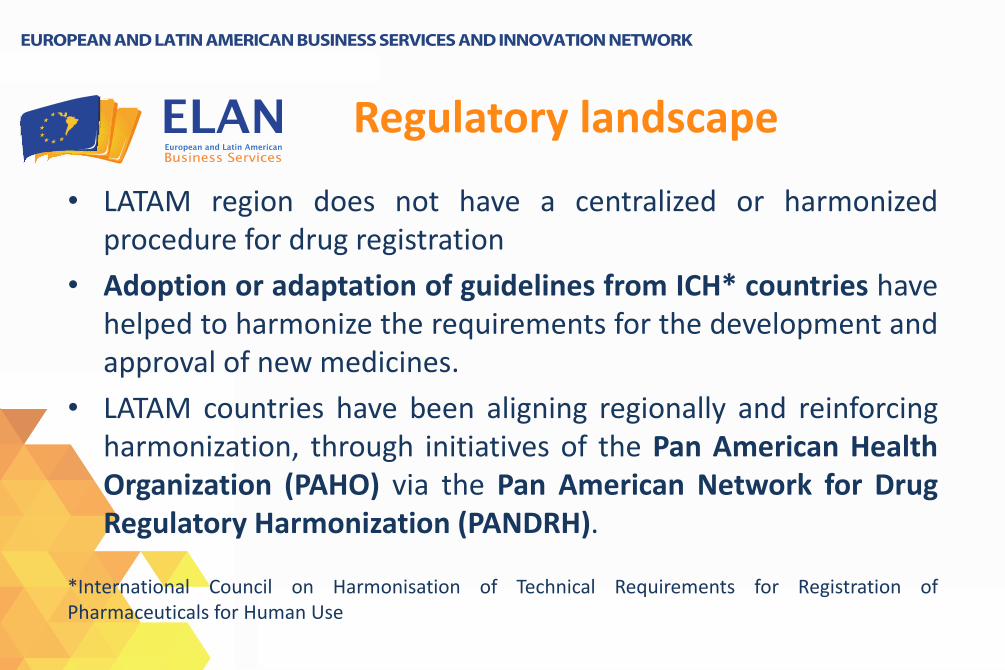

Regulatory landscape

• LATAM region does not have a centralized or harmonized procedure for drug registration

• Adoption or adaptation of guidelines from ICH* countries have helped to harmonize the requirements for the development and approval of new medicines.

• LATAM countries have been aligning regionally and reinforcing harmonization, through initiatives of the Pan American Health Organization (PAHO) via the Pan American Network for Drug Regulatory Harmonization (PANDRH).

*International Council on Harmonisation of Technical Requirements for Registration of Pharmaceuticals for Human Use

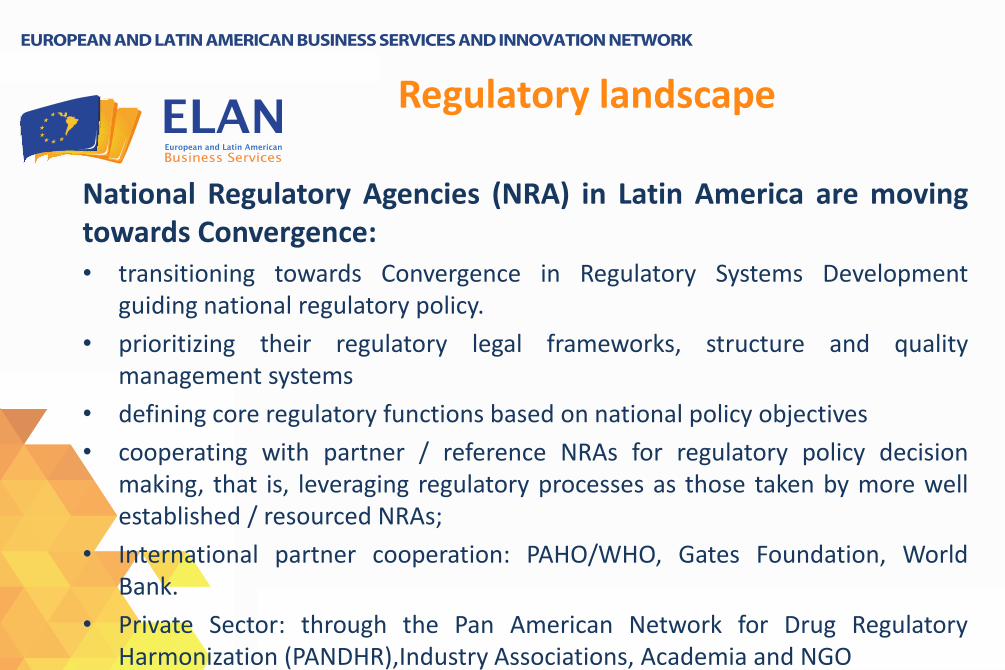

Regulatory landscape

National Regulatory Agencies (NRA) in Latin America are moving towards Convergence: • transitioning towards Convergence in Regulatory Systems Development

guiding national regulatory policy.

• prioritizing their regulatory legal frameworks, structure and quality management systems

• defining core regulatory functions based on national policy objectives

• cooperating with partner / reference NRAs for regulatory policy decision making, that is, leveraging regulatory processes as those taken by more well established / resourced NRAs;

• International partner cooperation: PAHO/WHO, Gates Foundation, World Bank.

• Private Sector: through the Pan American Network for Drug Regulatory Harmonization (PANDHR),Industry Associations, Academia and NGO

Regulatory landscape

Regulatory Convergence - Function Strengthening across Latin America

• Key topics for alignment have included sharing safety data, developing a common pharmacopeia, recognizing reciprocal acknowledgement of clinical site and GMP inspections.

• On-going Institutional development plans in process for: Costa Rica, Chile, Dominican Republic, Ecuador, El Salvador, Guatemala, Honduras, Panamá, Paraguay, Trinidad & Tobago.

Regulatory landscape

LATAM – Individual Regulatory Requirements

• Local presence/direct representation/distributor

• Market Authorization approval ownership

• Language

• Patent, trademarks, Intellectual Property

• Need for a local clinical trial or international trials accepted

• GMP* Inspection requirements

• Packaging and Labeling/country specific

*Good Manufacturing Practices

Regulatory landscape

GMP Certification – Inspection Requirements

• Most LATAM countries follow the WHO GMP requirements.

• Bolivia, Chile, Costa Rica, Dominican Republic, Guatemala, Nicaragua, Panama, Peru, Puerto Rico, Venezuela and others accept foreign GMP certifications.

• Argentina, Brazil, Colombia and Mexico enforce their own inspection and GMP certification regimes

• Brazilian GMP certification is mandatory for registration approval.

• Argentina, Colombia and Mexico accept GMP certifications from high vigilance countries (i.e. USA, Europe, etc.).

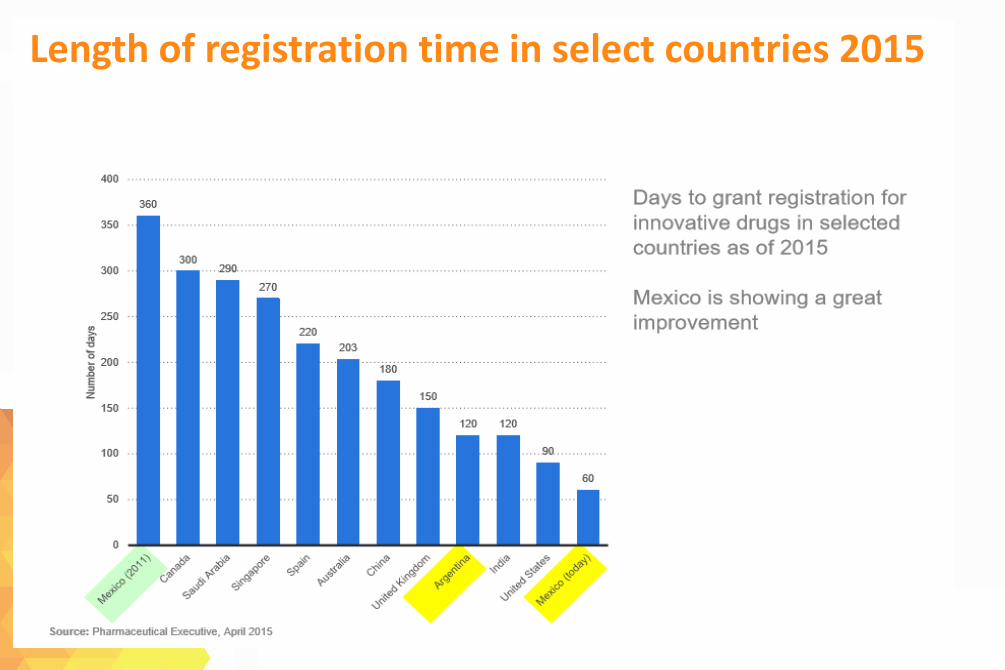

Length of registration time in select countries 2015

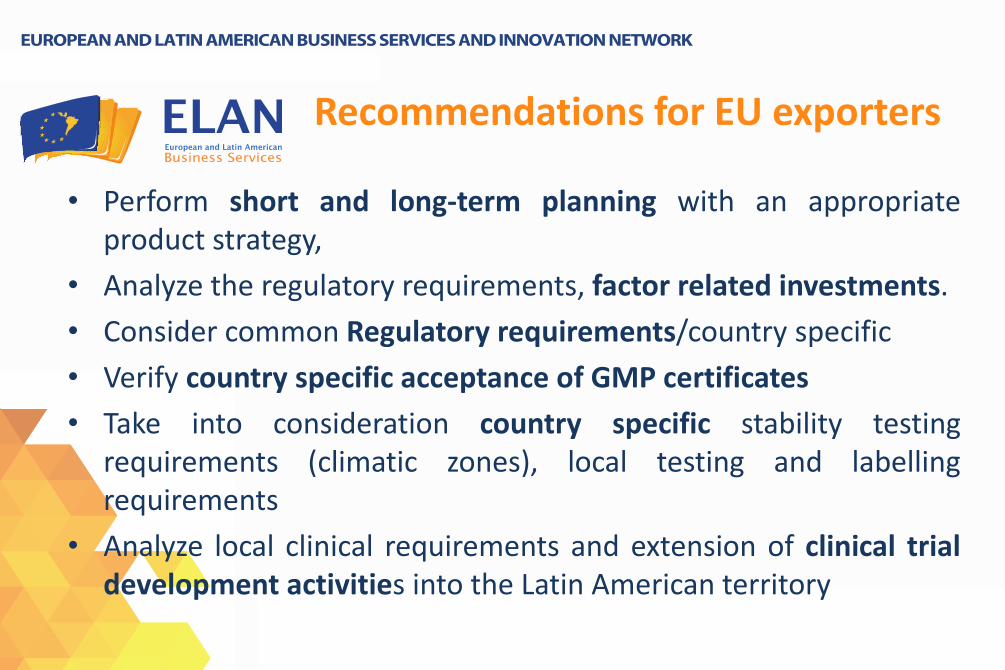

Recommendations for EU exporters

• Perform short and long-term planning with an appropriate product strategy,

• Analyze the regulatory requirements, factor related investments.

• Consider common Regulatory requirements/country specific

• Verify country specific acceptance of GMP certificates

• Take into consideration country specific stability testing requirements (climatic zones), local testing and labelling requirements

• Analyze local clinical requirements and extension of clinical trial development activities into the Latin American territory

Recommendations for EU exporters

• Engage early on in the product development phase with well established, reputable, international professional teams with sound expertise and global mindset.

• Keep current with regulatory changes, developments and evolving requirements per individual country across the region.

• Mastering the countries‘ local language and understanding local idiosyncrasies is helpful increasing perspectives of successful market access

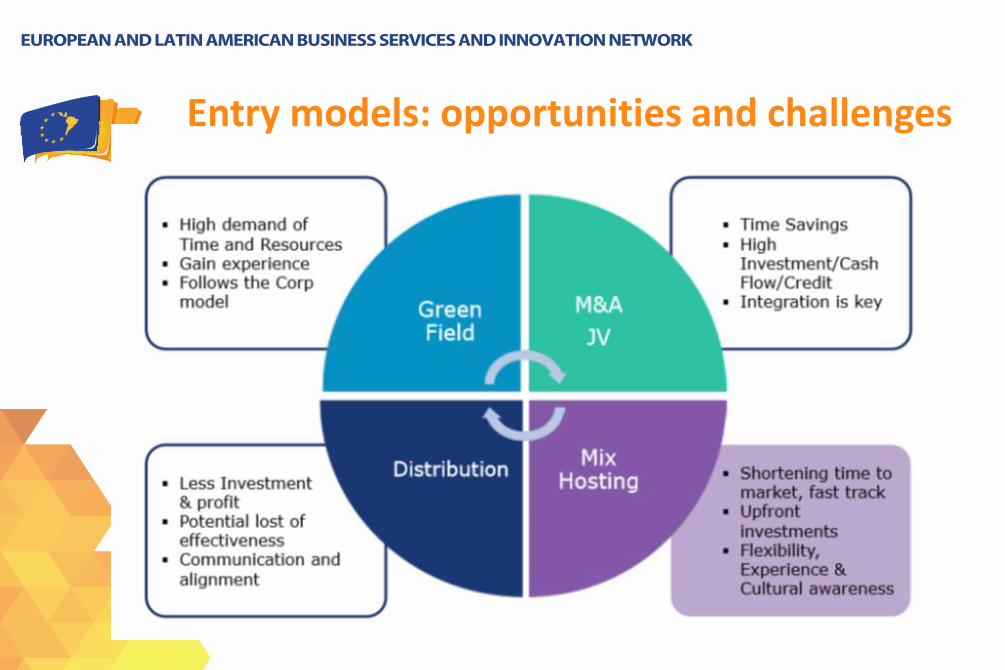

Entry models: opportunities and challenges

Thank you

for your attention!

Javier Sanchez, LAC Expert

Coordination office in Lima:

Katelyne Ghémar, ELANbiz Coordinator

ELANbiz is a project financed by the

European Union