deep dive: gen z and beauty—the social media symbiosis · 68 72 tinder linkedin whatsapp google...

TRANSCRIPT

1

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Thisreportispartofournewseries,TheNewBeautyConsumer,whichlooksatvariousaspectsofbeautyretailingandconsumption.

1) GenZisthefirstgenerationtousesocialmediaintheirformativeyears,anditispressuringteenstolookgood.AccordingtoasurveybytheAmericanPsychologicalAssociation,nearlyone-thirdofUSteengirlsfeelbadwhencomparingthemselveswithotherstheyseeonsocialmedia,andotherstudieshavefoundlinksbetweensocialmediausageandlowself-esteem.

2) Wethinkthesekindsofpressureswilldriveupspendingonbeautyproductsandservicesandfitnessservices.USteensarealreadygrowingtheirspendingonbeauty;thecategory’sshareofspendingamongupper-incomefemaleteensgrewtoitshighestleveleverinfall2016.

3) Whenshoppingforbeautyproducts,youngconsumersturntosocialmedia,andespeciallyvideocontent,foradvice.ThevolumeofbeautycontentonYouTuberocketedby200%between2015and2016,andfemaleconsumersages13–24makeupfully47%oftheaudienceforthesevideos.

4) GenZ’soldestmembersareonthecuspofadulthood,andweexpectthisgeneration’sdemandstobeafactorinfuturebeautyindustrymergersandacquisitions(M&A).Large,establishedmultibrandcompaniesarelikelytoacquirebeautybrandsthatresonatewithGenZersasthegeneration’sspendingpoweraccelerates.

Deep Dive: Gen Z and

Beauty—the Social Media

Symbiosis

Deborah Weinswig

Managing Director,

Fung Global Retail & Technology

US: 917.655.6790

HK: 852.6119.1779

CN: 86.186.1420.3016

2

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

TableofContentsExecutiveSummary..................................................................................................................................................3

Introduction..............................................................................................................................................................5

DefiningGenZ......................................................................................................................................................5

NotJustSocial...Visual..............................................................................................................................................6

SocialMediaFuelsImageConcerns..........................................................................................................................7

USTeensAreGrowingTheirBeautySpending.........................................................................................................8

SocialMediaDrivesBeautyandBeautyDrivesSocialMedia.................................................................................10

USFemaleTeensSpentanEstimated$2.3BilliononBeautyCategoriesLastYear...............................................12

GenZ’sFavoriteBrands..........................................................................................................................................13

GenZLikelytoImpactBeautyM&A.......................................................................................................................16

KeyTakeways…………………………………………………………………………………………………………………………………………………….17

3

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

ExecutiveSummaryWedefinethemembersofGenerationZasthosebornafter2000,whichmeansthegroupisboththenextgenerationofconsumersandonewhosemembershavenotallbeenbornyet.

WehaveidentifiedthreemainthemeswithintheGenZbeautymarket:

Imagepressuresfromsocialmediaarefuelingbeautydemand.GenZersarethefirstgenerationtobothdocumenttheiryearsgrowinguponsocialmediawebsitesandbeexposedonlinetoaspirationalimagesofcelebritiesandself-madesocialmediastars.Consequently,nearlyone-thirdofUSteengirlsfeelbadwhencomparingthemselveswithotherstheyseeonsocialmedia,accordingtoasurveybytheAmericanPsychologicalAssociation.Andacademicresearchstudieshavefoundlinksbetweensocialmediausageandlowself-esteem.Wethinkthesepressuresarelikelytofuelteenspendingonbeautyproducts.

BeautyspendingisagrowingpriorityforUSteengirls.AccordingtoaPiperJaffraysurvey,upper-incomefemaleteens’shareofspendingonthebeautycategorygrewtoitshighestleveleverinthefallof2016.Reflectingthistrend,usageoffacialcosmeticsishighamonggirlsages12–14:accordingtoMinteldata,roughlyhalfofthisagegroupusesmascara,foundationorconcealer.Reflectingtheimpactofsocialmedia,lastyear,brandownersEstéeLauderandL’Oréalattributedstrongdemandforcosmeticstotheselfieculture.

GenZturnstosocialmediaforbeautyadvice.Notonlydoessocialmediaheightenpressuresonyoungpeopleregardingpersonalappearance,butalsoservesasasourceofbeautyinformationandexpertiseforthem.Manyyoungconsumersturntosocialmedia,andespeciallyvideocontent,whenshoppingforbeautyproducts.Mintelfoundthatthree-quartersofUSfemaleteenshadlookedtoYouTubefortutorialsonnewstylesornewproducts.Moreover,theamountofbeautycontentonYouTubesurgedby200%between2015and2016,accordingtoanalyticsfirmPixability,andthefirmfoundthatfemaleconsumersages13–24makeupfully47%oftheaudienceforthesevideos.BrandsseekingtoengagewithGenZmustofferengaging,authenticcontentonvisual-drivensocialmediasites.

Figure1.TheSocialMedia-BeautySymbiosis

Source:FungGlobalRetail&Technology

TeensTurntoSocialMediaforBeautyAdvice

SocialMediaAddstoImagePressures

Lastyear,EstéeLauderandL’Oréalattributedstrongdemandforcosmeticstotheselfieculture.

4

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Source:Shutterstock

WeestimatethatUSfemaleteensages12–17spentapproximately$2.3billiononthecorebeautycategoriesofskincare,cosmeticsandfragrancesin2016.IntheUS,MAC,CoverGirl,MaybellineandUrbanDecayarethefavoredbrandsoffemaleteens,accordingtoPiperJaffray,whileUlta,Sephora,WalmartandTargetaretheirfavoredretailers.

Inthecomingyears,weexpectthedemandsofGenZconsumerstobeadriverofbeautyindustryM&A.LegacymultibrandgiantsarelikelytoseektostrengthentheirpositionwithGenZasthedemographic’sspendingpoweraccelerates.WebelieveGenZersplaceheightenedimportanceonthefollowingwhenshoppingforbeautyproducts,andthatthesepreferenceswillimpactbeautyM&Ainfutureyears:

• Formulatedwithpureandnaturalingredients.

• Celebrity-brandedand/orformulatedby“star”skincareandhaircareexperts.

• Madebycompaniesthatrecognizeanddemonstratesocialconsciousness,whichmayincludeafocusondiversityandequalityandcruelty-freeprocessesandgoods.

Weincludeatableofrecent,relevantbeautyindustryM&Aactivitytoconcludethereport.

5

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

IntroductionBornafter2000,GenZwillformthenextgenerationofconsumers.Itsoldestmembersareonthecuspofadulthood,andsoarebeginningtodrawtheattentionofmass-marketretailers.InAugust2016,wepublisheda20-pageoverviewofGenZanditspreferencesandbehaviorsasaconsumergroup:readerscanfindthatreportatbit.ly/FungGenZ

Inthisreport,weturntothebeautycategoryinmoredetailanddiscusshowsocialmediainparticularfuelsbeautydemandamongteens.Wealsolookathow,inturn,theseconsumerslooktosocialmediaforadviceandrecommendationswhenshoppingforbeautyproducts.ThefollowingsectionsalsoexplorewhichbrandsandretailersarepreferredbyUSteensandthelikelihoodthatGenZdemandswillimpactfutureM&Ainthebeautyindustry.

Thisreportispartofournewseries,TheNewBeautyConsumer,whichlooksatvariousaspectsofbeautyretailingandconsumption.SomeofthedatacitedinthisreportareglobalornotspecifictotheUS,butourfocusisontheAmericanmarket.

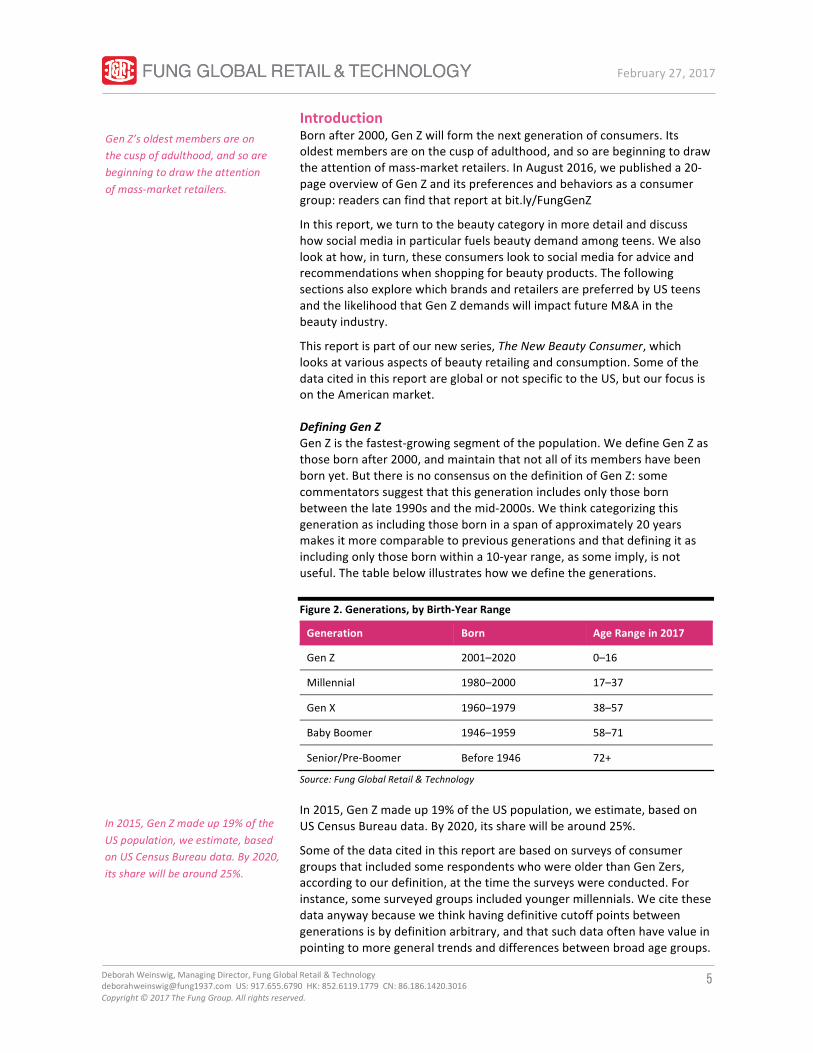

DefiningGenZGenZisthefastest-growingsegmentofthepopulation.WedefineGenZasthosebornafter2000,andmaintainthatnotallofitsmembershavebeenbornyet.ButthereisnoconsensusonthedefinitionofGenZ:somecommentatorssuggestthatthisgenerationincludesonlythosebornbetweenthelate1990sandthemid-2000s.Wethinkcategorizingthisgenerationasincludingthoseborninaspanofapproximately20yearsmakesitmorecomparabletopreviousgenerationsandthatdefiningitasincludingonlythosebornwithina10-yearrange,assomeimply,isnotuseful.Thetablebelowillustrateshowwedefinethegenerations.

Figure2.Generations,byBirth-YearRange

Generation Born AgeRangein2017

GenZ 2001–2020 0–16

Millennial 1980–2000 17–37

GenX 1960–1979 38–57

BabyBoomer 1946–1959 58–71

Senior/Pre-Boomer Before1946 72+

Source:FungGlobalRetail&Technology

In2015,GenZmadeup19%oftheUSpopulation,weestimate,basedonUSCensusBureaudata.By2020,itssharewillbearound25%.

SomeofthedatacitedinthisreportarebasedonsurveysofconsumergroupsthatincludedsomerespondentswhowereolderthanGenZers,accordingtoourdefinition,atthetimethesurveyswereconducted.Forinstance,somesurveyedgroupsincludedyoungermillennials.Wecitethesedataanywaybecausewethinkhavingdefinitivecutoffpointsbetweengenerationsisbydefinitionarbitrary,andthatsuchdataoftenhavevalueinpointingtomoregeneraltrendsanddifferencesbetweenbroadagegroups.

GenZ’soldestmembersareonthecuspofadulthood,andsoarebeginningtodrawtheattentionofmass-marketretailers.

In2015,GenZmadeup19%oftheUSpopulation,weestimate,basedonUSCensusBureaudata.By2020,itssharewillbearound25%.

6

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

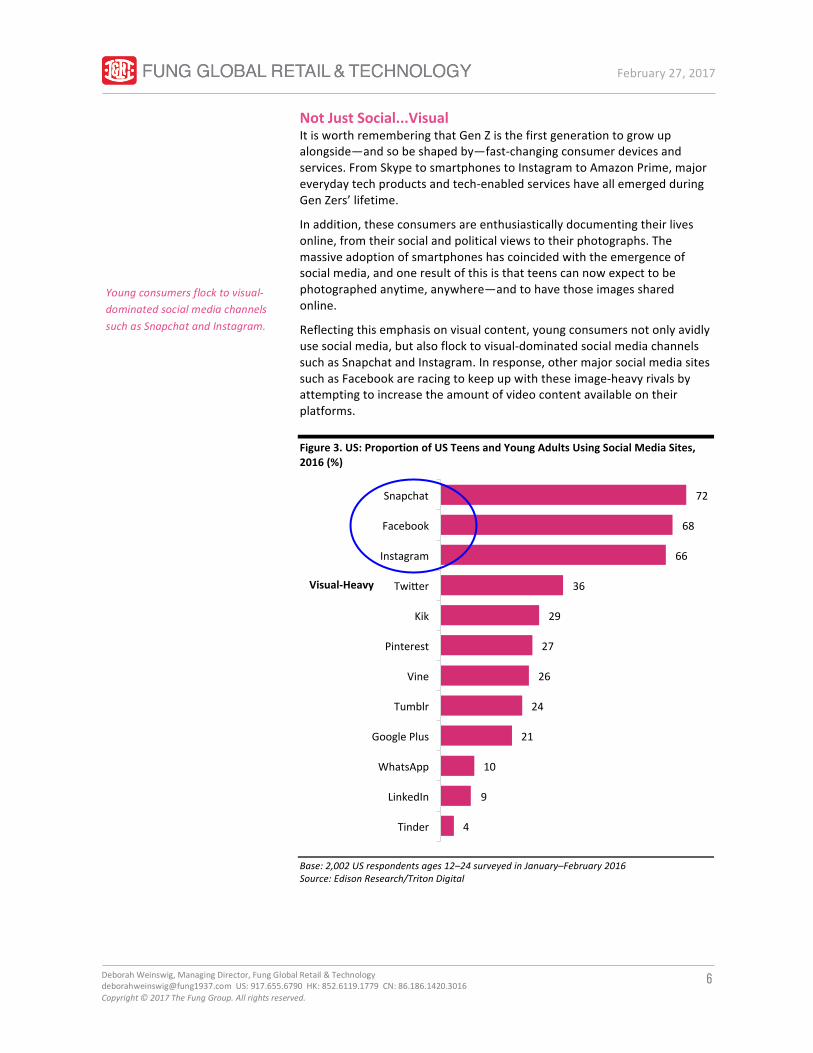

NotJustSocial...VisualItisworthrememberingthatGenZisthefirstgenerationtogrowupalongside—andsobeshapedby—fast-changingconsumerdevicesandservices.FromSkypetosmartphonestoInstagramtoAmazonPrime,majoreverydaytechproductsandtech-enabledserviceshaveallemergedduringGenZers’lifetime.

Inaddition,theseconsumersareenthusiasticallydocumentingtheirlivesonline,fromtheirsocialandpoliticalviewstotheirphotographs.Themassiveadoptionofsmartphoneshascoincidedwiththeemergenceofsocialmedia,andoneresultofthisisthatteenscannowexpecttobephotographedanytime,anywhere—andtohavethoseimagessharedonline.

Reflectingthisemphasisonvisualcontent,youngconsumersnotonlyavidlyusesocialmedia,butalsoflocktovisual-dominatedsocialmediachannelssuchasSnapchatandInstagram.Inresponse,othermajorsocialmediasitessuchasFacebookareracingtokeepupwiththeseimage-heavyrivalsbyattemptingtoincreasetheamountofvideocontentavailableontheirplatforms.

Figure3.US:ProportionofUSTeensandYoungAdultsUsingSocialMediaSites,2016(%)

Base:2,002USrespondentsages12–24surveyedinJanuary–February2016Source:EdisonResearch/TritonDigital

4

9

10

21

24

26

27

29

36

66

68

72

Tinder

GooglePlus

Tumblr

Vine

Kik

Twiser

Snapchat

Visual-Heavy

Youngconsumersflocktovisual-dominatedsocialmediachannelssuchasSnapchatandInstagram.

7

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Weperceivesocialmediaascausingteenstofocusmoreattentionontheirpersonalappearance,andwethinkthatislikelytoboostdemandinthebeautyproductmarket,aswellasadjacentmarketsthatarefocusedonpersonalappearance,suchbeautyservicesandthefitnessindustry.

SocialMediaFuelsImageConcerns

“Everytime[teens]switchontheirphones,they’regettingmessagesaboutpartiestheyhaven’tbeeninvitedto,orthey’reseeingphotosoftheirfriendsdoingthings....Itabsolutelypermeatestheirsenseofself-worth.”

–EmilyCherry,HeadofParticipationatUKchildren’scharityNSPCC

Socialmediauseis“significantlyassociated”withincreasedincidenceofdepression,accordingtoa2016studyofyoungadultsbytheUniversityofPittsburghSchoolofMedicine.A2015reportfromCanada’sCentreforAddictionandMentalHealthsimilarlyfoundmeaningfulassociationsbetweentimespentonsocialmediaandnegativementalhealthindicators:heavysocialmediausersweremorelikelytoreportlowself-esteem,forinstance.

So,itisperhapsnotsurprisingthatnegativesentimentsassociatedwithpersonalimageandbody-consciousnessappeartobewidespreadamongGenZers.AccordingtoasurveybytheAmericanPsychologicalAssociation,nearlyone-thirdofUSteengirlsfeelbadwhencomparingthemselveswithotherstheyseeonsocialmedia,asillustratedinthegraphbelow.Itisworthnotingthatthissurveywasconductedin2013,whenimage-focusedsocialmediachannelssuchasInstagramandSnapchatwerestillintheirinfancy.

Figure4.US:PercentageofTeensWhoAgreedwithStatementonTheirAppearance,2013

Base:1,018USteens,ages13–17Source:AmericanPsychologicalAssociation

13%

30%

55%

68%

Boys

Girls

Feelbadwhencomparingthemselvestoothersonsocialmedia:

Boys

Girls

Someaspectoftheirappearanceisasomewhatorverysignificantsourceof

stress:

AccordingtoasurveybytheAmericanPsychologicalAssociation,nearlyone-thirdofUSteengirlsfeelbadwhencomparingthemselveswithotherstheyseeonsocialmedia.

8

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Source:Shutterstock

Asthedataabovesuggest,thisisnotanissueconfinedtogirls.A2016surveysponsoredbyadvertisingthinktankCredosintheUKfoundthatmorethanhalfofyoungmalerespondentsrankedsocialmediaasasourceofpressuretolookgood.Socialmediarankedhigherinimportanceoverallthaneitheradvertisingorcelebritiesdidasaperceivedsourceofpressureamongrespondents.

Figure5.UK:PercentageofMaleRespondentsAges8–18WhoNamedFactorasOneoftheBiggestSourcesofPressuretoLookGood,20

Base:1,005UKmales,ages8–18Source:Credos

USTeensAreGrowingTheirBeautySpendingSo,youngpeopleappeartofeelgreaterpressurethaneverbeforetospendontheirpersonalappearance.WenotethattheimpactthispressurehasonGenZers’consumerbehaviormaychangeasthegenerationgrowsolder,but,fornow,beautyspendingisagrowingpriority,particularlyforUSteengirls.

49%

53%

57%

68%

Celebriues

Adverusing

SocialMedia

Friends

SpendingonbeautyisagrowingpriorityforUSteengirls.

InaUKsurvey,morethanhalfofyoungmalerespondentsrankedsocialmediaasasourceofpressuretolookgood.

9

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

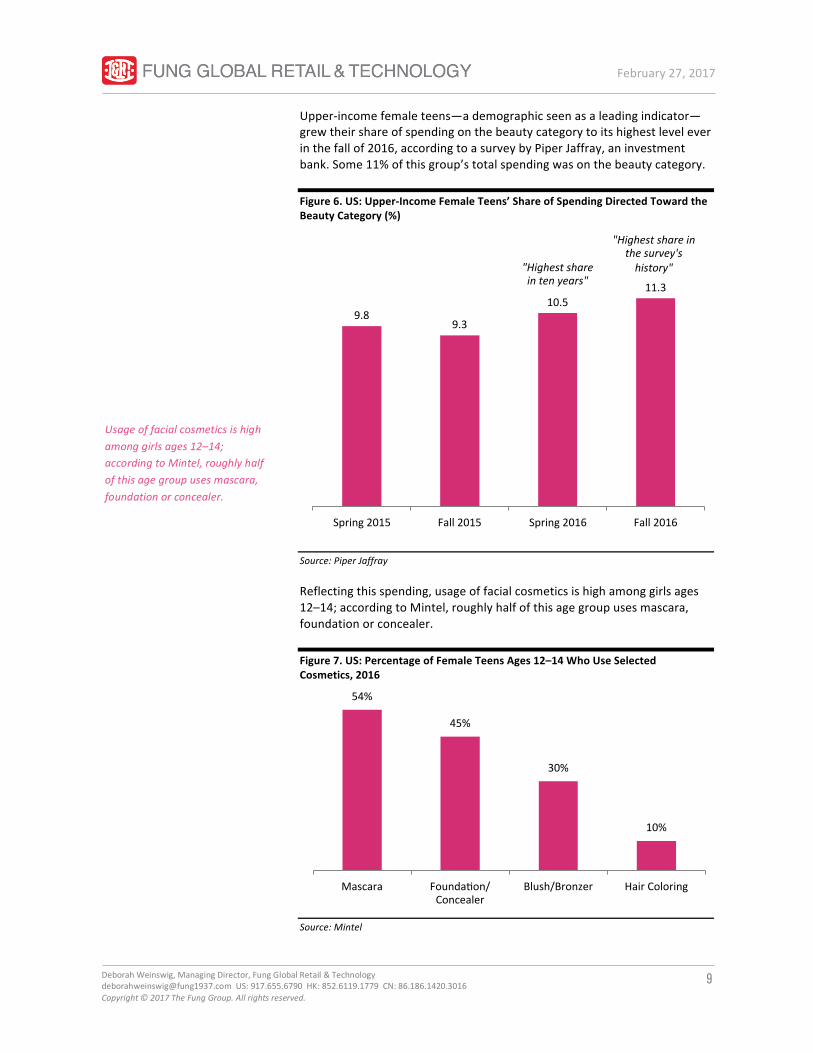

Upper-incomefemaleteens—ademographicseenasaleadingindicator—grewtheirshareofspendingonthebeautycategorytoitshighestleveleverinthefallof2016,accordingtoasurveybyPiperJaffray,aninvestmentbank.Some11%ofthisgroup’stotalspendingwasonthebeautycategory.

Figure6.US:Upper-IncomeFemaleTeens’ShareofSpendingDirectedTowardtheBeautyCategory(%)

Source:PiperJaffray

Reflectingthisspending,usageoffacialcosmeticsishighamonggirlsages12–14;accordingtoMintel,roughlyhalfofthisagegroupusesmascara,foundationorconcealer.

Figure7.US:PercentageofFemaleTeensAges12–14WhoUseSelectedCosmetics,2016

Source:Mintel

9.89.3

10.511.3

Spring2015 Fall2015 Spring2016 Fall2016

"Highestshareintenyears"

"Highestshareinthesurvey'shistory"

54%

45%

30%

10%

Mascara Foundauon/Concealer

Blush/Bronzer HairColoring

Usageoffacialcosmeticsishighamonggirlsages12–14;accordingtoMintel,roughlyhalfofthisagegroupusesmascara,foundationorconcealer.

10

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

AccordingtoMintel,beautyandgroomingproductusagebymaleteensisalsohigh,withfourin10maleteensages12–17usingfragranceorlip-careproducts.

Figure8.US:PercentageofMaleTeensAges12–17WhoUseSelectedBeauty/GroomingProducts,2016

Source:Mintel

Beautybrandsarereportingstrengtheneddemandasaresultofsocialmedia.In2016,bothEstéeLauderandL’Oréalsaidtheselfieculturehadcontributedtostronggrowthintheircosmeticssales.Andtheparticulartrendforgymselfiesisfuelingyoungconsumers’demandforgym-friendlymakeupfrombrandssuchasTarteCosmetics,BirchboxandCultBeauty,accordingtoTheTimes.

SocialMediaDrivesBeautyandBeautyDrivesSocialMediaVisual-focusedsocialmediaandthebeautymarketexistinakindofsymbiosis:notonlydoessocialmediaheightenpressuresonyoungconsumersregardingtheirpersonalappearance,butalsoservesasasourceofinformationandexpertiseforthemwhentheyareshoppingforbeautyproducts.Manyyoungconsumersturntosocialmedia,andespeciallyvideocontent,forinformationwhendecidingwhatbeautyitemstobuy.

Figure9.US:PercentageofFemaleTeensAges12–17WhoUseSocialMediaforSelectedBeauty-RelatedPurposes,2016

Source:Mintel

29%

41%

42%

44%

Hair-StylingProducts

Lip-CareProducts

Perfume/Cologne

Facial-CleansingProducts

45%

56%

65%

HavePostedAboutBrandsonSocialMedia

FollowBeauty/PersonalCareBrandsonSocialMedia

UseYouTubetoLearnHowtoCreateaNewStyleorUseaNewProduct

Manyyoungconsumersturntosocialmedia,andespeciallyvideocontent,whenshoppingforbeautyproducts.

11

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

BeautycontenthasballoonedonYouTubeandcontinuestogrowapace.AccordingtoPixability,thenumberofbeauty-relatedvideoshostedonYouTubemorethantripled,to5.3million,inthe16monthsendedJune2016.

Figure10.NumberofBeauty-RelatedVideosonYouTube(Mil.)

Source:Pixability

GenZersaretheleadingconsumersofthiscontent.AccordingtoPixability,femaleviewersages13–24makeupfully47%oftheYouTubebeautyaudience.ThiskindofdemandhasmadestarsofvloggerssuchasZoella,whosetargetaudienceisyoungfemaleteens.PixabilitysaysthatZoellaleadsbynumberofbeautysubscribers,with10.9millionsigneduptofollowheronYouTube.

Source:YouTube

1.8

5.3

March2015 June2016

+200%

12

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

OnYouTube,beautyvideosgarnerfarmoreviewsthandovideosinrivallifestylecategories,Pixabilitysays.AsofJune2016,beautyvideosonthesitehadbeenviewed125billiontimes.Meanwhile,onFacebook,thetop200beautybrandshadnotchedsome850millionvideoviewsbyJune2016.

Figure11.YouTube:TotalViewsofLifestyleCategoryVideosasofJune2016(Bil.)

Source:Pixability

USFemaleTeensSpentanEstimated$2.3BilliononBeautyCategoriesLastYearWeestimatethatAmericanfemalesages12–17spentapproximately$2.3billiononthecorebeautycategoriesofskincare,cosmeticsandfragrancesin2016.ThisestimateisforspendingbyteensthemselvesandexcludesspendingbyyoungerGenZers.Thetablebelowshowshowourestimatebreaksdownbysubcategory.

Figure12.US:EstimatedSpendingonCoreBeautyCategoriesbyFemaleConsumersAges12–17,2016(USDBil.)

TotalSpend

TotalCoreBeauty $2.3

Skincare $1.1

Cosmetics $0.8

Fragrances $0.4

Source:PiperJaffray/USCensusBureau/FungGlobalRetail&Technology

Thefollowingdatapointsinformedandcontextualizedourestimates:

• PiperJaffray’sfall2016USteensurveyfoundthatupper-incomefemaleteensspentanaverageof$395acrossskincare,cosmeticsandfragrancesperyear.Basedontheratioofupper-incomehouseholdincometoaverage-incomehouseholdincomeinthePiperJaffraysurvey,weestimatethataverage-incomefemaleteens’

125

0

20

40

60

80

100

120

140

Beauty Fitness Food Travel Fashion

OnYouTube,beautyvideoshadnotched125billionviewsasofJune2016.

13

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Source:Shutterstock

annualspendingwasabout$192acrossskincare,cosmeticsandfragrancesin2016.

• Populationestimatesofaround12millionfemaleteensages12–17intheUSleadtoaballparkspendingfigureof$2.3billionacrossthesethreebeautycategories.

• Ourestimateequatesto3%ofthetotalUSbeautyandpersonalcaremarketsizeasrecordedbyEuromonitorInternationalfor2016(andwenotethatEuromonitor’stotalincludestoiletriesandpersonalcarecategoriesthatextendbeyondskincare,cosmeticsandfragrances).Ourestimatesuggeststhatfemaleteensaccountedforaround7%oftheUSskincaremarketrecordedbyEuromonitorand6%ofthecosmeticsmarket.

• USfamiliesspent$24billionon“miscellaneous”categories—whichincludebeautyproductsandservices—forthoseages12–17in2015,weestimate,basedonUSDepartmentofAgriculturesurveydata.Ourestimatedfigureof$2.3billionforcorebeautycategoriesequatestojustunder10%ofthismiscellaneousspendingtotal.

14

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

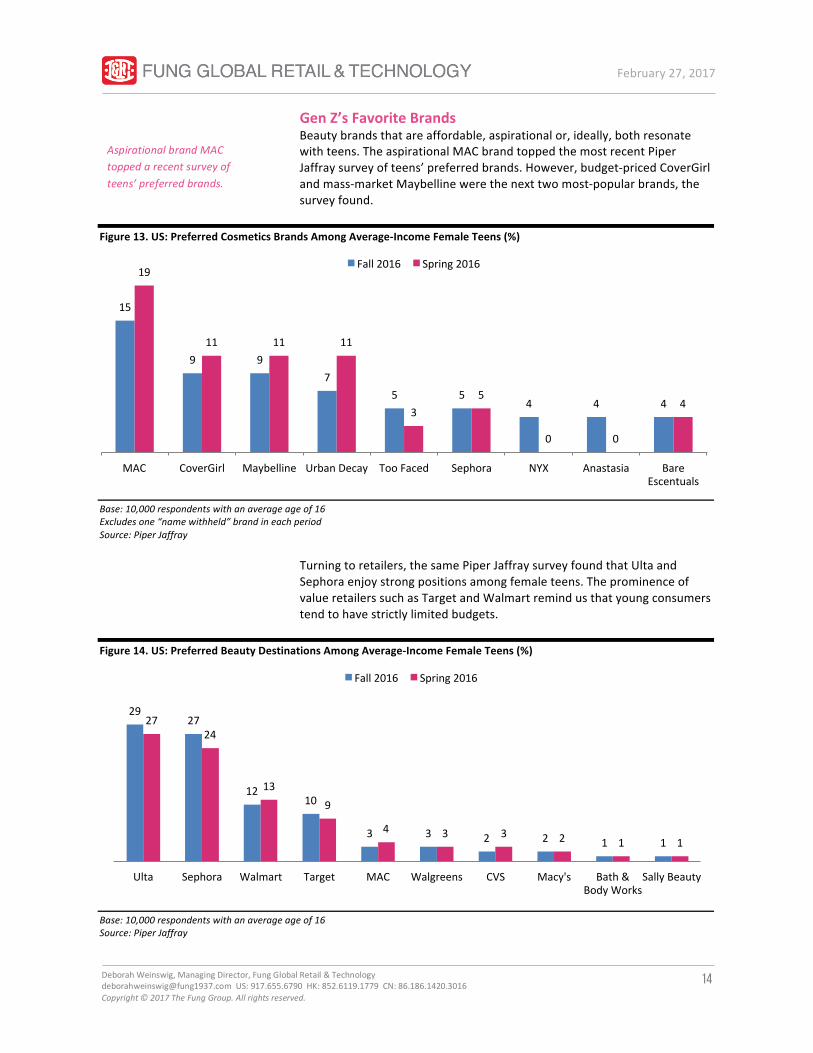

GenZ’sFavoriteBrandsBeautybrandsthatareaffordable,aspirationalor,ideally,bothresonatewithteens.TheaspirationalMACbrandtoppedthemostrecentPiperJaffraysurveyofteens’preferredbrands.However,budget-pricedCoverGirlandmass-marketMaybellinewerethenexttwomost-popularbrands,thesurveyfound.

Figure13.US:PreferredCosmeticsBrandsAmongAverage-IncomeFemaleTeens(%)

Base:10,000respondentswithanaverageageof16Excludesone“namewithheld”brandineachperiodSource:PiperJaffray

Turningtoretailers,thesamePiperJaffraysurveyfoundthatUltaandSephoraenjoystrongpositionsamongfemaleteens.TheprominenceofvalueretailerssuchasTargetandWalmartremindusthatyoungconsumerstendtohavestrictlylimitedbudgets.

Figure14.US:PreferredBeautyDestinationsAmongAverage-IncomeFemaleTeens(%)

Base:10,000respondentswithanaverageageof16Source:PiperJaffray

AspirationalbrandMACtoppedarecentsurveyofteens’preferredbrands.

15

9 97

5 54 4 4

19

11 11 11

35

0 0

4

MAC CoverGirl Maybelline UrbanDecay TooFaced Sephora NYX Anastasia BareEscentuals

Fall2016 Spring2016

2927

1210

3 3 2 2 1 1

2724

139

4 3 3 2 1 1

Ulta Sephora Walmart Target MAC Walgreens CVS Macy's Bath&BodyWorks

SallyBeauty

Fall2016 Spring2016

15

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

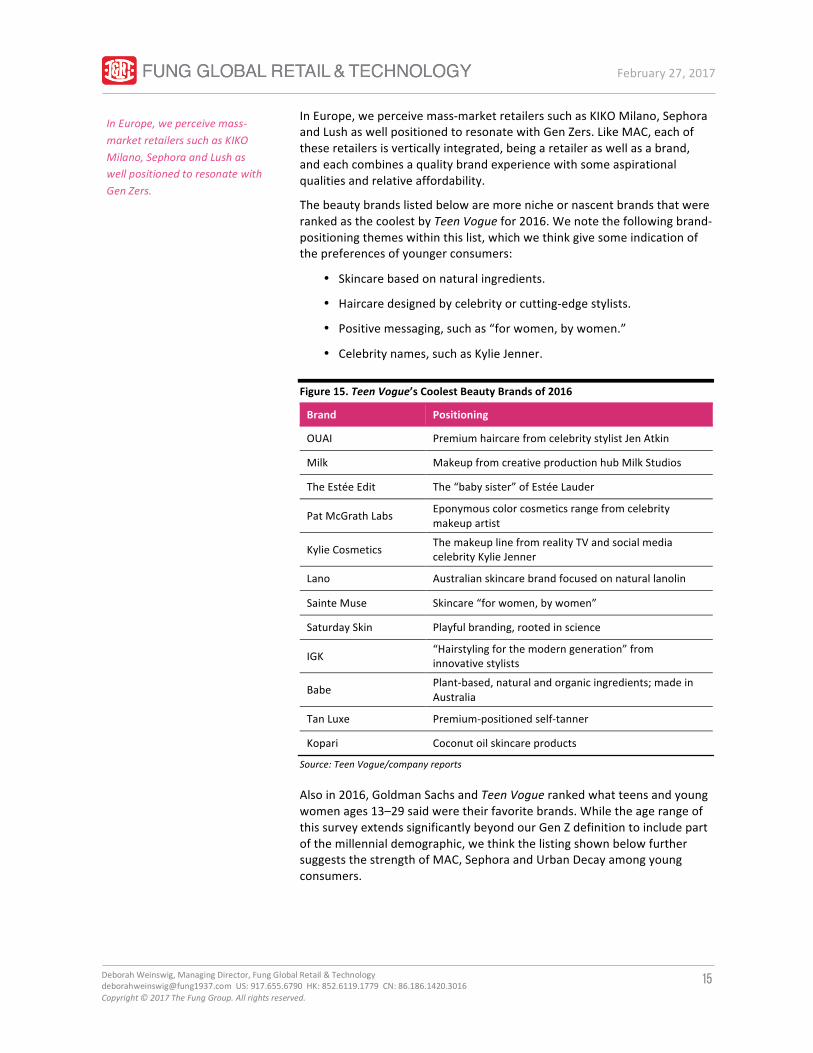

InEurope,weperceivemass-marketretailerssuchasKIKOMilano,SephoraandLushaswellpositionedtoresonatewithGenZers.LikeMAC,eachoftheseretailersisverticallyintegrated,beingaretaileraswellasabrand,andeachcombinesaqualitybrandexperiencewithsomeaspirationalqualitiesandrelativeaffordability.

ThebeautybrandslistedbelowaremorenicheornascentbrandsthatwererankedasthecoolestbyTeenVoguefor2016.Wenotethefollowingbrand-positioningthemeswithinthislist,whichwethinkgivesomeindicationofthepreferencesofyoungerconsumers:

• Skincarebasedonnaturalingredients.

• Haircaredesignedbycelebrityorcutting-edgestylists.

• Positivemessaging,suchas“forwomen,bywomen.”

• Celebritynames,suchasKylieJenner.

Figure15.TeenVogue’sCoolestBeautyBrandsof2016

Brand Positioning

OUAI PremiumhaircarefromcelebritystylistJenAtkin

Milk MakeupfromcreativeproductionhubMilkStudios

TheEstéeEdit The“babysister”ofEstéeLauder

PatMcGrathLabs Eponymouscolorcosmeticsrangefromcelebritymakeupartist

KylieCosmetics ThemakeuplinefromrealityTVandsocialmediacelebrityKylieJenner

Lano Australianskincarebrandfocusedonnaturallanolin

SainteMuse Skincare“forwomen,bywomen”

SaturdaySkin Playfulbranding,rootedinscience

IGK “Hairstylingforthemoderngeneration”frominnovativestylists

Babe Plant-based,naturalandorganicingredients;madeinAustralia

TanLuxe Premium-positionedself-tanner

Kopari Coconutoilskincareproducts

Source:TeenVogue/companyreports

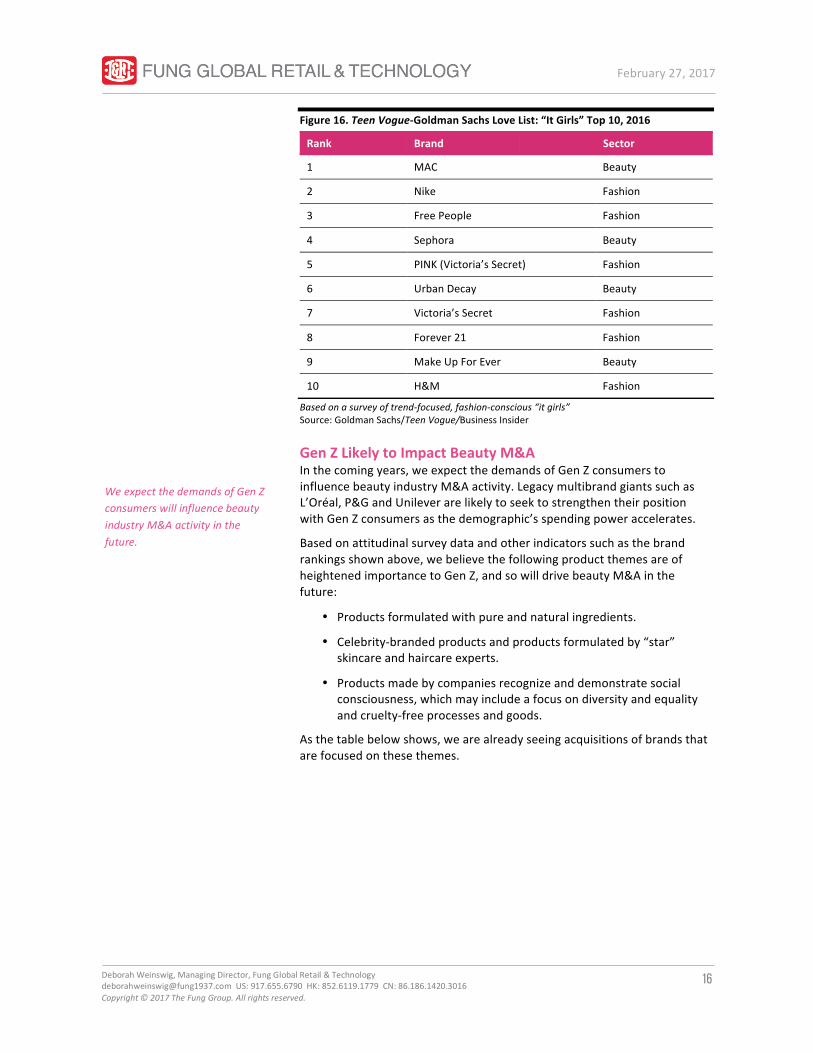

Alsoin2016,GoldmanSachsandTeenVoguerankedwhatteensandyoungwomenages13–29saidweretheirfavoritebrands.WhiletheagerangeofthissurveyextendssignificantlybeyondourGenZdefinitiontoincludepartofthemillennialdemographic,wethinkthelistingshownbelowfurthersuggeststhestrengthofMAC,SephoraandUrbanDecayamongyoungconsumers.

InEurope,weperceivemass-marketretailerssuchasKIKOMilano,SephoraandLushaswellpositionedtoresonatewithGenZers.

16

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Figure16.TeenVogue-GoldmanSachsLoveList:“ItGirls”Top10,2016

Rank Brand Sector

1 MAC Beauty

2 Nike Fashion

3 FreePeople Fashion

4 Sephora Beauty

5 PINK(Victoria’sSecret) Fashion

6 UrbanDecay Beauty

7 Victoria’sSecret Fashion

8 Forever21 Fashion

9 MakeUpForEver Beauty

10 H&M Fashion

Basedonasurveyoftrend-focused,fashion-conscious“itgirls”Source:GoldmanSachs/TeenVogue/BusinessInsider

GenZLikelytoImpactBeautyM&AInthecomingyears,weexpectthedemandsofGenZconsumerstoinfluencebeautyindustryM&Aactivity.LegacymultibrandgiantssuchasL’Oréal,P&GandUnileverarelikelytoseektostrengthentheirpositionwithGenZconsumersasthedemographic’sspendingpoweraccelerates.

Basedonattitudinalsurveydataandotherindicatorssuchasthebrandrankingsshownabove,webelievethefollowingproductthemesareofheightenedimportancetoGenZ,andsowilldrivebeautyM&Ainthefuture:

• Productsformulatedwithpureandnaturalingredients.

• Celebrity-brandedproductsandproductsformulatedby“star”skincareandhaircareexperts.

• Productsmadebycompaniesrecognizeanddemonstratesocialconsciousness,whichmayincludeafocusondiversityandequalityandcruelty-freeprocessesandgoods.

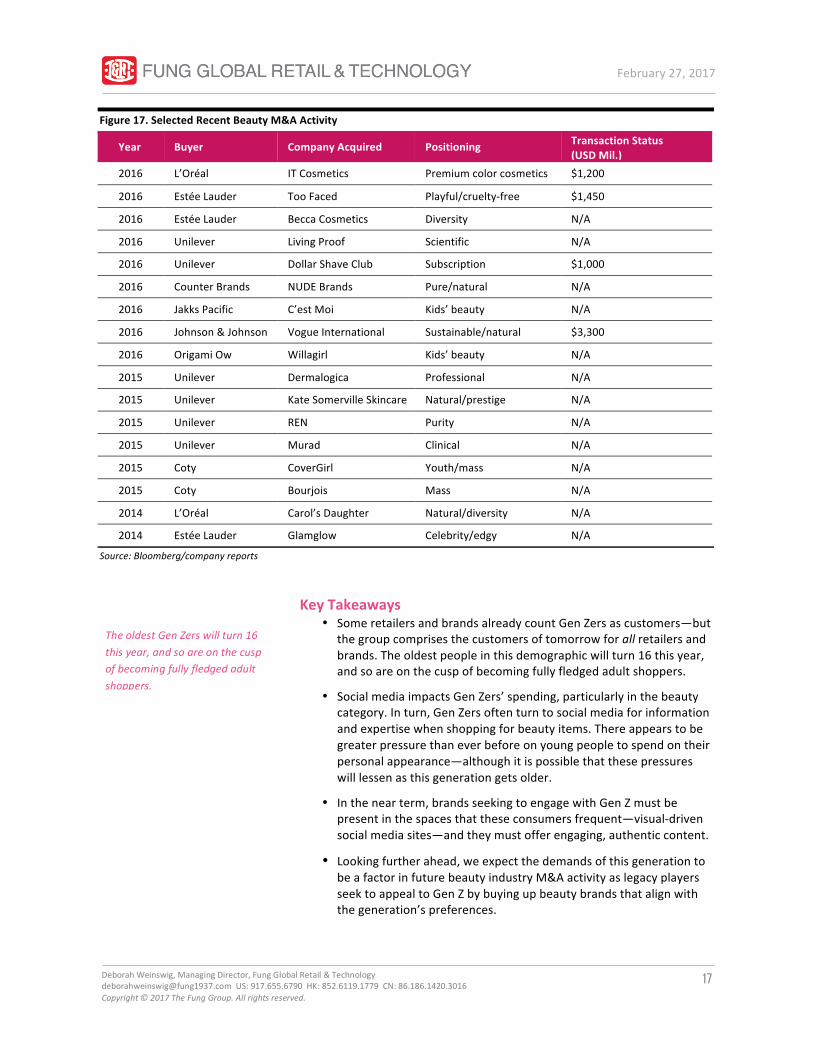

Asthetablebelowshows,wearealreadyseeingacquisitionsofbrandsthatarefocusedonthesethemes.

WeexpectthedemandsofGenZconsumerswillinfluencebeautyindustryM&Aactivityinthefuture.

17

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

TheoldestGenZerswillturn16thisyear,andsoareonthecuspofbecomingfullyfledgedadultshoppers.

Figure17.SelectedRecentBeautyM&AActivity

Year Buyer CompanyAcquired Positioning TransactionStatus(USDMil.)

2016 L’Oréal ITCosmetics Premiumcolorcosmetics $1,200

2016 EstéeLauder TooFaced Playful/cruelty-free $1,450

2016 EstéeLauder BeccaCosmetics Diversity N/A

2016 Unilever LivingProof Scientific N/A

2016 Unilever DollarShaveClub Subscription $1,000

2016 CounterBrands NUDEBrands Pure/natural N/A

2016 JakksPacific C’estMoi Kids’beauty N/A

2016 Johnson&Johnson VogueInternational Sustainable/natural $3,300

2016 OrigamiOw Willagirl Kids’beauty N/A

2015 Unilever Dermalogica Professional N/A

2015 Unilever KateSomervilleSkincare Natural/prestige N/A

2015 Unilever REN Purity N/A

2015 Unilever Murad Clinical N/A

2015 Coty CoverGirl Youth/mass N/A

2015 Coty Bourjois Mass N/A

2014 L’Oréal Carol’sDaughter Natural/diversity N/A

2014 EstéeLauder Glamglow Celebrity/edgy N/A

Source:Bloomberg/companyreports

KeyTakeaways• SomeretailersandbrandsalreadycountGenZersascustomers—but

thegroupcomprisesthecustomersoftomorrowforallretailersandbrands.Theoldestpeopleinthisdemographicwillturn16thisyear,andsoareonthecuspofbecomingfullyfledgedadultshoppers.

• SocialmediaimpactsGenZers’spending,particularlyinthebeautycategory.Inturn,GenZersoftenturntosocialmediaforinformationandexpertisewhenshoppingforbeautyitems.Thereappearstobegreaterpressurethaneverbeforeonyoungpeopletospendontheirpersonalappearance—althoughitispossiblethatthesepressureswilllessenasthisgenerationgetsolder.

• Inthenearterm,brandsseekingtoengagewithGenZmustbepresentinthespacesthattheseconsumersfrequent—visual-drivensocialmediasites—andtheymustofferengaging,authenticcontent.

• Lookingfurtherahead,weexpectthedemandsofthisgenerationtobeafactorinfuturebeautyindustryM&AactivityaslegacyplayersseektoappealtoGenZbybuyingupbeautybrandsthatalignwiththegeneration’spreferences.

18

February27,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

DeborahWeinswig,CPAManagingDirectorFungGlobalRetail&TechnologyNewYork:917.655.6790HongKong:852.6119.1779China:86.186.1420.3016deborahweinswig@fung1937.comJohnMercerSeniorAnalyst

HongKong:8thFloor,LiFungTower888CheungShaWanRoad,KowloonHongKongTel:85223004406London:242-246MaryleboneRoadLondon,NW16JQUnitedKingdomTel:44(0)2076168988NewYork:1359Broadway,9thFloorNewYork,NY10018Tel:6468397017

FungGlobalRetailTech.com