deere & company investor relations · recent earnings release and conference call ......

TRANSCRIPT

John DeereCommitted to Those Linked to the Land

Deere & CompanyJuly 2012

| Deere & Company | July 2012

Safe Harbor Statement & Disclosures

This presentation includes forward-looking comments subject to important risks and uncertainties. It may also contain financial measures that are not in conformance with accounting principles generally accepted in the United States of America (GAAP).

Refer to Deere’s reports filed on Forms 8-K (current), 10-Q (quarterly), and 10-K (annual) for information on factors that could cause actual results to differ materially from information in this presentation and for information reconciling financial measures to GAAP.

Guidance noted in the following slides was effective as of the company’s most recent earnings release and conference call (16 May 2012). Nothing in this presentation should be construed as reaffirming or disaffirming such guidance.

This presentation is not an offer to sell or a solicitation of offers to buy any of Deere’s securities.

2

|

Table of Contents

Slide #John Deere Strategy 4

Macroeconomic Tailwinds 19

Foundational Success Factors 26

Global Markets and Opportunities 38

John Deere Financial Services 69

John Deere Power Systems 75

Farm Fundamentals 78

Market and Currency Volatility 87

Appendix 90

Deere & Company | July 20123

John Deere Strategy

|5 Deere & Company | July 2012

| Deere & Company | July 2012

The John Deere StrategyOur Purpose: Committed to those linked to the land

6

– Global macro-trends present significant opportunities for John Deere

– Global population and income growth– Global infrastructure needs

– New customer segments

– Technology advances

No longer “business as usual”

744K Wheel Loader

460E Articulated Dump Truck

8360R Tractor

S690 Combine

X728 Riding Mower843K Wheeled Feller Buncher

|

Sustainable SVA growth is delivered by distinctively serving our customers, employees, and investors

Extend and enhance our financial and operating achievements of recent years

Our challenge: to capture anticipated tailwinds by attracting more customers to the John Deere Experience across our six key geographies (US/Canada, EU 27, Brazil, CIS/Russia, India, China) in a manner that meets local needs while leveraging our global scale

7 Deere & Company | July 2012

The John Deere StrategyRealizing Sustainable Growth Through Global Expansion

|

Agricultural Equipment Solutions Strategy– Defend and grow market share in

developed markets– Grow market share in developing

markets

Construction Equipment Solutions Strategy– Continue to grow strong #2 position in

North America– Globalize the business

8 Deere & Company | July 2012

The John Deere StrategyAgricultural and Construction Equipment Aspirations

6488 Combine - China

755K Crawler Loader - USA

9530T Tractor - USA

435 Backhoe Loader - India

|

Sales

– Enterprise net sales of $50 billion at mid-cycle by 2018

Profitability

– Operating margins of no less than 12% at mid-cycle by 2014

Asset Efficiency

– Asset turns of 2.5 times at mid-cycle by 2018

2010 Normal Volume$25 billion

2018 Normal Volume$50 billion

U.S. & Canada

BRIC

Rest of World

6.6%12.3% 13.0%

2009 2010 2011

1.9 2.2 2.3

2009 2010 2011

9 Deere & Company | July 2012

The John Deere StrategyPerformance Target Aspirations

Equi

pmen

tO

pera

tions

Equi

pmen

tO

pera

tions

|

The John Deere StrategyIntegrated Enterprise

Integrated portfolio of businesses, each with a vital and specific role

10 Deere & Company | July 2012

Global Growth BusinessesAgricultural and Construction Equipment Solutions– Invest in global expansion for profitable growth by

capitalizing on macro-trends

Complementary Businesses

Turf and Forestry Equipment Solutions– Defend and grow share, enhance SVA, strengthen the

channel of the Global Growth Businesses

Supporting Businesses

Financial Services, Power Systems, Worldwide Parts, and Intelligent Solutions Group– Strengthen and further differentiate our Global

Growth and Complementary Businesses

S660i Combine 310SJ Backhoe Loader

XUV 550 Gator 1170E Wheeled Harvester

Financial Services

Power Systems

Worldwide Parts

Intelligent Solutions

|

The John Deere StrategyFoundational and Critical Success Factors

Both Foundational and Critical Success Factors necessary…

…to ensure that Deere is the provider of choice across the

world

FOUNDATIONAL SUCCESS FACTORSBuilding on the core strengths that have guided our success

Exceptional Operating Performance

Disciplined SVA Growth

Aligned High-Performance Teamwork

CRITICAL SUCCESS FACTORSDeveloping the capabilities essential to reaching our goals

Deep Customer Understanding

Deliver Customer Value

World-Class Distribution System

Grow Extraordinary Talent

11 Deere & Company | July 2012

| Deere & Company | July 2012

*Excludes fiscal 2009 expenses related to goodwill impairment and voluntary employee-separation, for reconciliation to GAAP see “2009 OROA Reconciliation to GAAP” slide in Appendix.

The John Deere StrategyFoundational Success Factors

Exceptional Operating Performance - Equipment Operations29.8% OROA in 2011, a record high for the company

12%

20%

28%

2001

2002

2003

2004

20052006

20072008

2009

2009, adjusted*

20102011

0%

5%

10%

15%

20%

25%

30%

35%

% of Normal Volume

80%Low

100%Normal

120%High

12% OROA (SVA Neutral)

12

| Deere & Company | July 2012

Exceptional Operating Performance - Equipment OperationsSVA Model: Higher Net Cash Flow, More Consistently

The John Deere StrategyFoundational Success Factors

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

$ M

illio

ns

Sale of Trade Receivables to Credit

Adoption of SVA Model

Over $7 billion in Pension/OPEB contributions, 2001-2011

13

| Deere & Company | July 2012

SVA

($ m

illio

ns)

Note: For reconciliation of SVA to GAAP, please see “Equipment Ops SVA Reconciliation to GAAP” slide in Appendix

Disciplined SVA Growth - Equipment OperationsSVA Journey, 1991 - 2011

-1,600

-1,200

-800

-400

0

400

800

1,200

1,600

2,000

2,400

2,800

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

14

The John Deere StrategyFoundational Success Factors

| Deere & Company | July 2012

SVA

($ m

illio

ns)

Note: For reconciliation of SVA to GAAP, please see “Equipment Ops SVA Reconciliation to GAAP” slide in Appendix

Disciplined SVA Growth - EnterpriseSVA Journey, 2002 - 2011SVA in 2011 was ~ $2.5 billion – a record high for the company

-800

-400

0

400

800

1,200

1,600

2,000

2,400

2,800

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

15

The John Deere StrategyFoundational Success Factors

| Deere & Company | July 2012

Aligned High-Performance TeamworkIntegral part of strategy, reinforced with compensationGlobal Performance Management reinforces alignment Base pay changes linked to achieving goals

STI: Short-Term Incentive – Bonus focuses on OROA/ROECovers most worldwide salaried employeesApplies one enterprise-wide bonus metric

MTI: Mid-Term Incentive – Bonus driven by sustained SVA creationAbout 8,200 management employees eligible

LTI: Long-Term Incentive – Primarily stock options Top 900 employees eligibleMinimum stock holding requirements for senior management (~ top 125)

16

The John Deere StrategyFoundational Success Factors

|

Commitment to execute and monitor all initiatives critical to our successPerformance measures

– Traditional financial measures based on what we are delivering today to our stakeholders

Health measures – The qualities, attributes and actions being introduced to ensure the sustainability of our

performance over time

Deere & Company | July 2012

The John Deere StrategyMeasures

Metric Target

Sales Net Sales Growth Target $50B* (2018, at mid-cycle)

Profitability Return on Sales (Operating Margin) 12% (2014, at mid-cycle)

Asset Efficiency Asset Turns 2.5x (2018, at mid-cycle)

*Implies a CAGR of ~ 9% (2010 – 2018) vs. historical CAGR of 7-8%

17

Metric Target

Exceptional Operating Performance Quality % JDQPS certification

Disciplined SVA Growth Sales/SVA Mix by Geography % Non- U.S. & Canada

Aligned High- Performance Teamwork Employee Engagement Employee Survey’s

Engagement Index

| Deere & Company | July 2012

Accelerated emphasis on global growth –$50 billion mid-cycle sales by 2018–Approximately 50% outside of U.S. & Canada–Capitalize on increased global demand for food, shelter and infrastructure

Focus on improved profitability–12% mid-cycle margin by 2014

Continued adherence to OROA/SVA model–30% OROA at mid-cycle sales (12% at trough) with improved asset turns

Focus on two growth platforms–Global pre-eminence in agricultural-equipment solutions–Global construction-equipment operations (with presence in China)–Complementary/supporting businesses to help drive performance of global growth platforms

Revised metrics reflect strategic direction–“Performance” metrics align compensation to strategy–“Health” metrics introduced to monitor underlying factors (e.g., market share, quality) to ensure performance is sustainable

18

The John Deere StrategyIn Summary

Macroeconomic Tailwinds

Support John Deere’sGlobal Growth Businesses

|

Population growing in size and affluence• By 2050, world population will reach 9 billion, up from ~7 billion today, with

most of population growth in Asia and Africa• Large middle class developing in China and India

Opportunity #1: Feeding the world• Agricultural output must double by 2050• Gross output must increase 3.4% annually in the next 10 years vs. 2.4%

annual growth in past 10 years• Natural resources under strain, especially water

Opportunity #2: Massive urbanization• Migration from rural areas creates need for infrastructure development• 2010: For the first time in history, more than half the world population lives

in cities• 2050: More than 70 percent will live in cities

20 Deere & Company | July 2012

Long-Term Macroeconomic TailwindsSupport Global Growth Opportunities

|

17%

24%

26%

34%

34%

36%

36%

39%

46%

49%

58%

58%

61%

71%

71%

Health and Social Services

Real Estate and Business Activities

Social and Personal Services

Hotels and Restaurants

Education

Public Administration and Defense, Compulsory Social Security

Financial Intermediation

Wholesale and Retail Trade

Construction

Transport, Storage and Telecommunication

Utilities

Manufacturing

Mining

Agriculture

Private Household Services

88

289

321

331

351

381

462

575

647

757

1,052

1,315

1,805

2,301

Private Household Services

Hotels and Restaurants

Mining

Utilities

Social and Personal Services

Agriculture

Education

Public Administration and Defense, Compulsory Social Security

Health and Social Services

Construction

Financial Intermediation

Transport, Storage and Telecommunication

Wholesale and Retail Trade

Real Estate and Business Activities

Manufacturing

Deere & Company | July 2012

Sector

Agriculture and Construction amongst the Top 10 industry sectors in the G-20 countries . . .

Absolute increase in real value added 2009-18, $ Billions

CAGR 2009-18 Percent

3.1

2.3

5.3

2.9

5.2

4.0

4.1

3.0

3.2

3.4

2.9

2.7

4.8

3.8

3.8

. . . Significant growth in Agriculture and Construction between 2009-2018 will happen in the BRIC countries

Share of growth from BRIC1Sector

Note: G20 countries account for 73% and 89% of agriculture and construction segments respectively.Total global growth for agriculture is $520B and construction is $854B

1Brazil, Russia, India, ChinaSource: Global Insight World Industry Service

Real value-added 2005 USD

Strong Global Tailwinds in Ag & Construction Significant Growth from Developing Economies

3,625

21

|

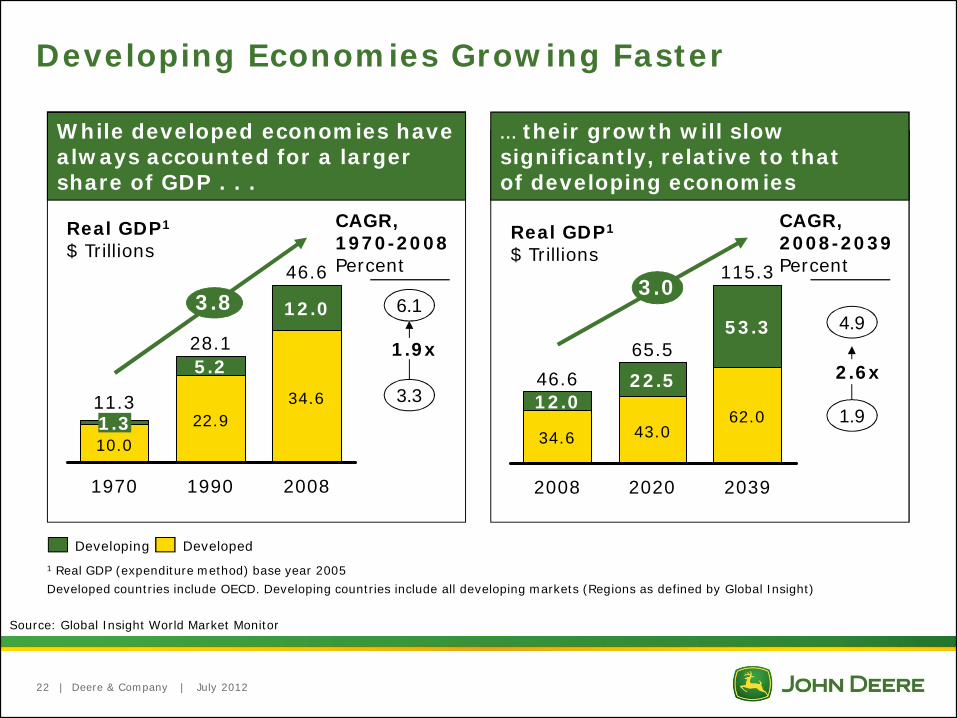

Developing Economies Growing Faster

While developed economies have always accounted for a larger share of GDP . . .

10.022.9

34.61.3

12.0

28.1

1990

5.2

11.3

1970

46.63.8

2008

Real GDP1

$ Trillions

6.1

CAGR,1970-2008Percent

3.3

34.6 43.062.0

12.0

3.0

203920202008

65.5

115.3

53.3

22.546.6

Real GDP1

$ Trillions

4.9

CAGR,2008-2039Percent

... their growth will slow significantly, relative to that of developing economies

1 Real GDP (expenditure method) base year 2005Developed countries include OECD. Developing countries include all developing markets (Regions as defined by Global Insight)

1.9x2.6x

1.9

Developing Developed

Deere & Company | July 2012

Source: Global Insight World Market Monitor

22

| Deere & Company | July 2012

Dynamics of Food Demand

Source: World Bank 2008

>$10 per day

27% of world’s population(Most hunger problems solved at

$2.50 threshold)

Services

Processed Products

Livestock Products

Commodities

Per CapitaIncome

20% of world’s population(2/3rds experience hunger &

malnutrition)

$2.50-10 per day

$1.25-2.50 per day

<$1.25 per day

23

| Deere & Company | July 2012

Global Construction and Infrastructure Needs

2,266

2,356

1,888

6,509

2008

2,998

3,555

3,361

9,915

2020

3.6%

Infrastructure is expected to be the fastest growing segment of construction

Estimated gross spending as a percent of 2008 global GDP

2.4

3.5

4.9

ResidentialNon-residentialInfrastructure

CAGR2008-2020Percent

WW Construction spendingGross output, $ 2008 Billions

Construction12%

Mining & Quarrying7% Ag, Hunting,

Forestry & Fishing7%

All Other74%

*Note: Construction and Mines & Quarries account for ~5% and ~4% of 2008 value-added WW GDP, respectivelySource: IHS Global Insight, March 2009; Off Highway Research; AEM; CCMA; Yengst; Deere analysis

24

|

Infrastructure

Non-residential

Residential

All Construction

Construction spending 2020 absolute, Top 10 (Billions of 2009 $s)

2,049

1,508

751

592

432

365

302

299

267

257

China

U.S. & Canada

India

Japan

U.K.

France

Germany

Brazil

Russia

Italy

China + U.S. & Canada 36% of 2020 absolute, compared to 30% todayChina + U.S. & Canada + Brazil, Russia, India 50% of 2020 absolute, compared to 40% today

Construction spending 2010-2020 change, Top 10 (Billions of 2009 $s)

1,128

534

437

168

106

103

95

92

60

57

China

U.S. & Canada

India

Brazil

Russia

U.K.

Japan

Indonesia

Mexico

Korea

Infrastructure

Non-residential

Residential

All Construction

Global Construction Spending in 2020Concentrated in a Small Number of Markets

Deere & Company | July 2012

Source: IHS Global Insight, Deere Analysis, August 2011

25

FoundationalSuccess Factors

Building on Core Strengths That Have Guided Our Success

| Deere & Company | July 2012

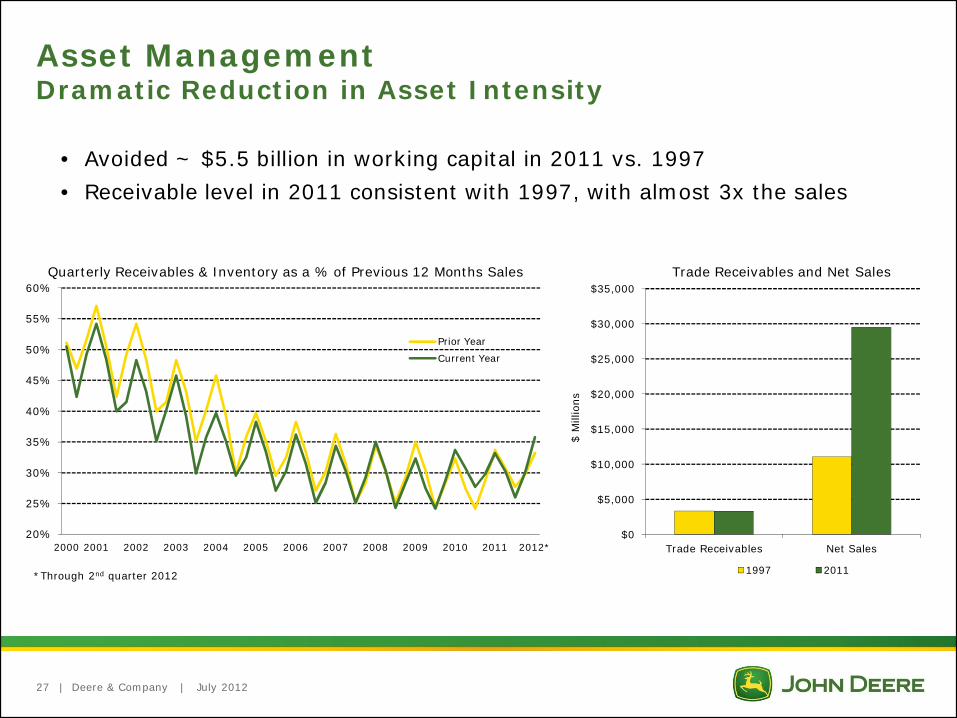

Asset Management Dramatic Reduction in Asset Intensity

20%

25%

30%

35%

40%

45%

50%

55%

60%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012*

Prior Year

Current Year

Trade Receivables and Net Sales

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

Trade Receivables Net Sales

$ M

illio

ns1997 2011

• Avoided ~ $5.5 billion in working capital in 2011 vs. 1997• Receivable level in 2011 consistent with 1997, with almost 3x the sales

Quarterly Receivables & Inventory as a % of Previous 12 Months Sales

27

*Through 2nd quarter 2012

| Deere & Company | July 2012

Productivity Improvement ~ 6% CAGR over 30 Years

• Deere’s net sales and revenues per employee have increased at a CAGR of ~ 6% over last 30 years

Net Sales and Revenues per Employee

$0

$100

$200

$300

$400

$500

$600

1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

$ Th

ousa

nds

28

| Deere & Company | July 2012

Manufacturing Efficiencies – Waterloo, IAJourney to a 6-Day Drive Train

Prod

uctio

n D

ays

0

5

10

15

20

25

30

35

40

45

50

Prior to 2005 2005 2006 2007 2008

Relocation of 412 machinesEliminated 155 machines

Total evacuation of multi-story buildingsNew heat treat fully operationalSet-up improvementOn-site forging storageInsourcing of core processes

Machining departments based on part familiesArranged machines using cellular conceptsStarted evacuation of multi-story buildings

Run size optimization and set-up improvementDaily run size parametersOutsourcing non-core processes

-12 Days

-2 Days

-10 Days

-14 Days

29

| Deere & Company | July 2012

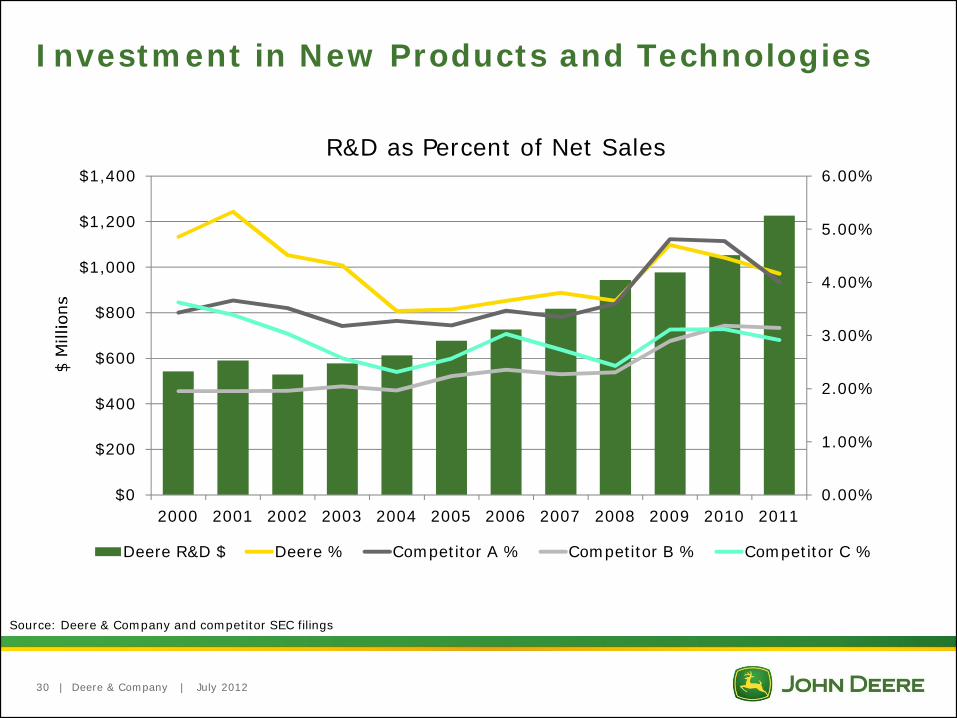

Investment in New Products and Technologies

R&D as Percent of Net Sales

Source: Deere & Company and competitor SEC filings

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Deere R&D $ Deere % Competitor A % Competitor B % Competitor C %

30

|

Net Sales by Product CategoryEquipment Operations - Fiscal Year 2011

Deere & Company | July 2012

Agriculture & Turf – $24.1B Construction & Forestry – $5.4B

Construction

Forestry

CWPOther

Large Ag

Small Ag

Turf

Other

31

| Deere & Company | July 2012

Committed Bank Group Supports Credit Facility• Average length of continuous relationship = ~29 Years• $5.00 billion credit facility supporting commercial paper

– $1.50 billion 61-month facility expiring in 2017– $2.75 billion 49-month facility expiring in 2015– $750 million 364-day facility expiring in 2013– Have not drawn on facility– $2.7 billion incremental capacity as of 30 April 2012

Credit Facility Size & Commercial Paper Outstanding

$ M

illio

ns

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Total Facility CP Outstanding as of October 31

32

| Deere & Company | July 2012

Deere Use-of-Cash Priorities

Manage the balance sheet, including liquidity, to support a rating that provides access to low-cost and readily available short- and long-term funding mechanisms

Reflects the strategic nature of our financial services operation

Committed to “A” Rating

Cash from Operations

Fund Operating and Growth Needs

Common Stock Dividend

Share Repurchase

Fund value-creating investments in our businesses

Consistently and moderately raise dividend targeting a 25%-35% payout ratio of mid-cycle earnings

Consider share repurchase as a means to deploy excess cash to shareholders, once above requirements are met and repurchase is viewed as value-enhancing

33

| Deere & Company | July 2012

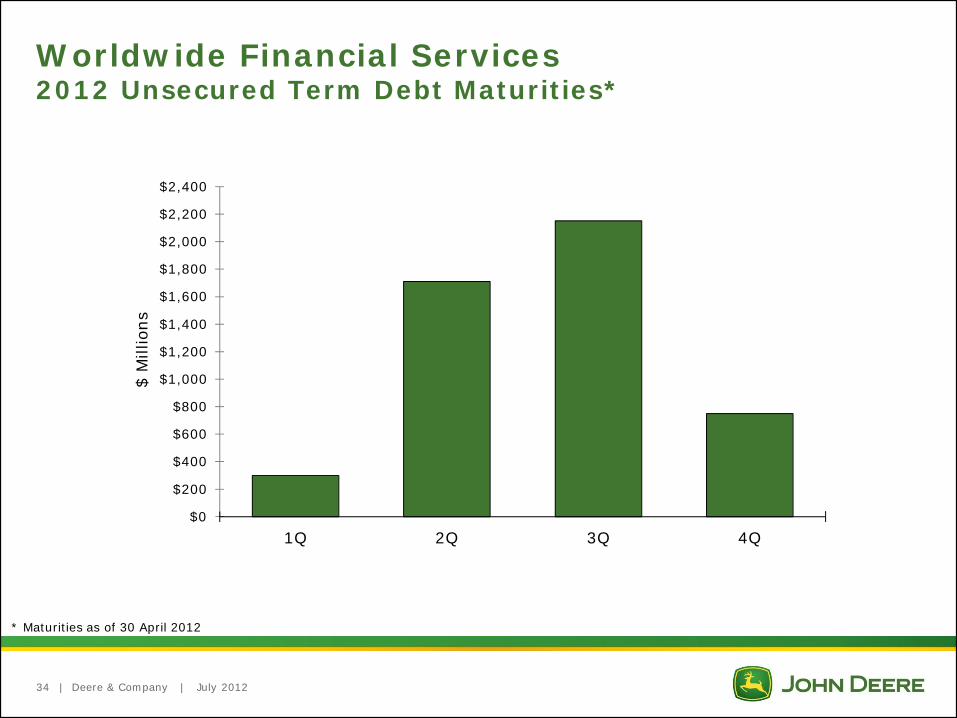

Worldwide Financial Services2012 Unsecured Term Debt Maturities*

* Maturities as of 30 April 2012

34

$ M

illio

ns

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

$2,400

1Q 2Q 3Q 4Q

| Deere & Company | July 2012

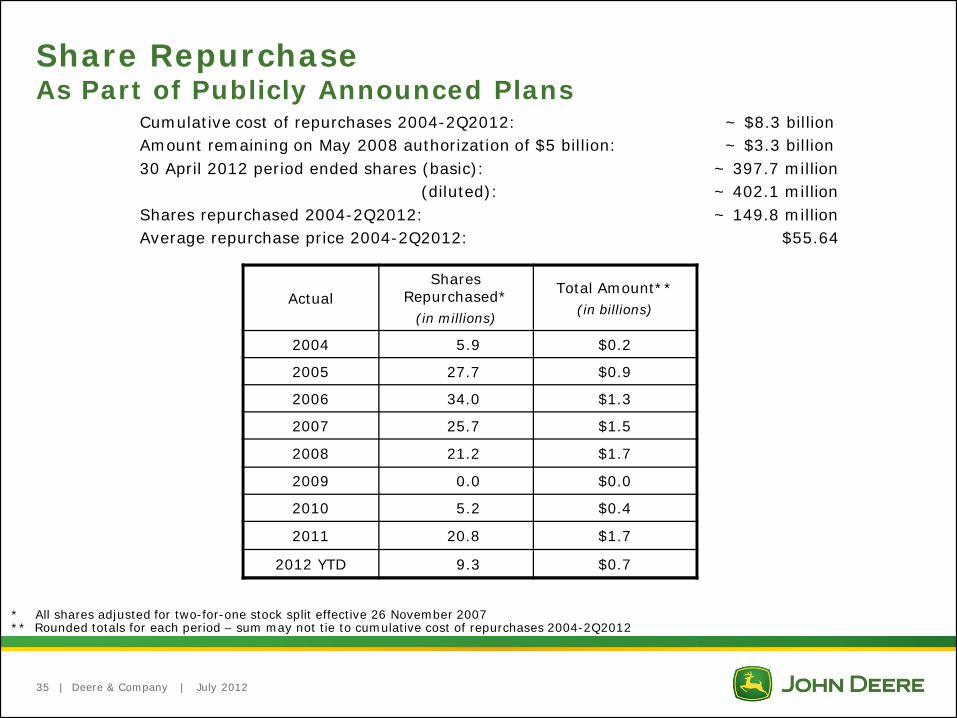

Share RepurchaseAs Part of Publicly Announced Plans

35

Actual Shares

Repurchased*(in millions)

Total Amount**(in billions)

2004 5.9 $0.2

2005 27.7 $0.9

2006 34.0 $1.3

2007 25.7 $1.5

2008 21.2 $1.7

2009 0.0 $0.0

2010 5.2 $0.4

2011 20.8 $1.7

2012 YTD 9.3 $0.7

Cumulative cost of repurchases 2004-2Q2012: ~ $8.3 billionAmount remaining on May 2008 authorization of $5 billion: ~ $3.3 billion 30 April 2012 period ended shares (basic): ~ 397.7 million

(diluted): ~ 402.1 millionShares repurchased 2004-2Q2012: ~ 149.8 millionAverage repurchase price 2004-2Q2012: $55.64

* All shares adjusted for two-for-one stock split effective 26 November 2007** Rounded totals for each period – sum may not tie to cumulative cost of repurchases 2004-2Q2012

|

$0.11$0.14

$0.16

$0.20$0.22

$0.25$0.28

$0.30

$0.35

$0.41

$0.46

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

$0.45

$0.50

'03

Q1

Q2

Q3

Q4

'04

Q1

Q2

Q3

Q4

'05

Q1

Q2

Q3

Q4

'06

Q1

Q2

Q3

Q4

'07

Q1

Q2

Q3

Q4

'08

Q1

Q2

Q3

Q4

'09

Q1

Q2

Q3

Q4

'10

Q1

Q2

Q3

Q4

'11

Q1

Q2

Q3

Q4

'12

Q1

Q2

Q3

Deere & Company | July 2012

Deere Quarterly Dividends Declared* Q1 2003 – Q3 2012

* Adjusted for 2 for 1 stock split on 26 November 2007** See slide 5 for revised John Deere Strategy

36

Dividend raised 64% since launch of the revised John Deere Strategy in 2010**

| Deere & Company | July 2012

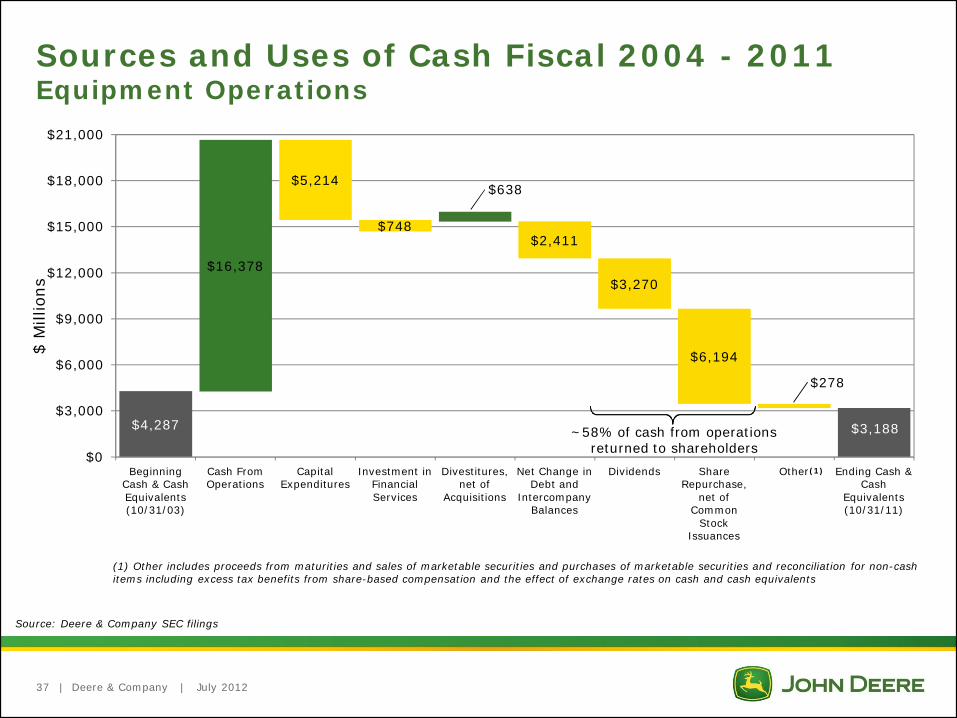

Sources and Uses of Cash Fiscal 2004 - 2011 Equipment Operations

(1) Other includes proceeds from maturities and sales of marketable securities and purchases of marketable securities and reconciliation for non-cash items including excess tax benefits from share-based compensation and the effect of exchange rates on cash and cash equivalents

Source: Deere & Company SEC filings

$4,287

$16,378

$5,214

$748

$638

$2,411

$3,270

$6,194

$278

$0

$3,000

$6,000

$9,000

$12,000

$15,000

$18,000

$21,000

Beginning Cash & Cash Equivalents (10/31/03)

Cash From Operations

Capital Expenditures

Investment in Financial Services

Divestitures, net of

Acquisitions

Net Change in Debt and

Intercompany Balances

Dividends Share Repurchase,

net of Common

Stock Issuances

Other Ending Cash & Cash

Equivalents (10/31/11)

~58% of cash from operations returned to shareholders

(1)

$ M

illio

ns

$3,188

37

Global Markets and Opportunities

| Deere & Company | July 2012

Growing Global Presence

• FY 2011 equipment net sales outside U.S. & Canada over 4x the level in FY 2000

20%

25%

30%

35%

40%

45%

50%

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

• FY 2011 equipment net sales outside U.S. & Canada over 4x the level in FY 2000

$ M

illio

ns

Net Sales Outside U.S. and Canada

Net Sales Outside U.S. & Canada % of Total Net Sales

39

| Deere & Company | July 2012

Net Sales by Major MarketsFiscal Years 2011, 2010, 2009, 2008

(in millions of dollars) 2011 2010%

Change 2009 2008

United States 15,029 13,026 +15% 11,568 13,166

Canada 2,329 1,767 +32% 1,454 1,902

Western Europe 4,382 3,360 +30% 3,427 4,610

Central Europe & CIS 1,407 746 +89% 749 1,874

Central & South America 3,612 2,623 +38% 1,787 2,577

Asia, Africa & Middle East 1,930 1,431 +35% 1,166 1,062

Asia Pacific, Australia & New Zealand 777 620 +25% 605 612

Total 29,466 23,573 +25% 20,756 25,803

40

|

U.S. and CanadaFactory Locations

Deere & Company | July 201241

Iowa, USA• Cotton Harvesting Equipment• Planting Equipment• Spraying Equipment• Tillage Equipment• Ag Tractors• Components• Foundry• Engines• Hay & Forage Equipment• Articulated Dump Trucks• 4WD Loaders• Motor Graders• Skidders• Wheeled Feller Bunchers• Backhoes• Compact Tracked Loaders• Crawler Dozers• High-Speed Dozers• Knuckleboom Loaders• Skid Steer Loaders• Tracked Feller Bunchers• Tracked Harvesters

Illinois, USA• Combine Harvesters• Headers• Planting Equipment• Hydraulic Cylinders

North Dakota, USA• Air Seeding Equipment• Electronics

North Carolina, USA• Commercial Mowers• Golf & Turf Mowers• Utility Vehicles• Hydraulic Excavators

Alberta, Canada• Remanufactured ComponentsBritish Columbia, Canada

• Log Loaders & Specialty Products

California, USA• Satellite Receivers

Kansas, USA• Power Transmission Equipment

Missouri, USA• Remanufactured Components

Louisiana, USA• Sugarcane Harvesting Equipment• Tractor Loaders• Scrapers• Cotton Strippers

Georgia, USA• Utility Tractors• Compact Utility Tractors

Tennessee, USA• Lawn Tractors

Wisconsin, USA• Lawn & Garden Equipment• Utility Vehicles• Golf & Turf Reel Mowers

| Deere & Company | July 2012

U.S. and CanadaRecent Announcements

• June 2012 – $47 million investment at Moline, IL cylinder operations to expand manufacturing capacity

• March 2012 – Final Tier 4/Stage IV solution to combine proven EGR Interim Tier 4 platform with customized selective catalytic reduction (SCR) system

• March 2012 – $70 million investment at Waterloo, IA factory to expand production of large farm tractors by 10%

• January 2012 – Strategic agreement with MacDon to manufacture self-propelled windrowers

• December 2011 – $85 million in capital improvements at Des Moines, IA factory to expand production of self-propelled sprayers

• August 2011 – Largest, most significant product introduction in the company’s history

42

2008-2010

2010-2012

2012-2013

25%

15%

10%

Waterloo Works Capacity Expansion

2008 to 2013

Deere & Company Forecast as of 16 May 2012

| Deere & Company | July 2012

EU 27Factory Locations

Joensuu, Finland• Wheel Forwarders• Wheel Harvesters• Forestry Attachments

Bruchsal, Germany• Tractor, Harvesting & Forestry Cabs

Mannheim, Germany• Tractors

Zweibrücken, Germany• Combine & Forage Harvesters• Material Handling Equipment

Arc-les-Gray, France• Forage Equipment• Balers• Material Handling Equipment

Saran, France• Engines

Madrid, Spain• Components

Horst, The Netherlands• Spraying Equipment

Stadtlohn, Germany• Forage Harvesters• Headers

Gummersbach, Germany• Walk-Behind Mowers

43

|

EU 27Economic Data

Deere & Company | July 2012

PPP: Purchasing Power ParitySource: FAO, Global Insight, The World Factbook

1.8%

25.0%

73.2%

GDP Composition

Agriculture Industry ServicesSource: The World Factbook, 2011 est.

4.7%

28.7%

66.6%

Labor Composition

Agriculture Industry ServicesSource: The World Factbook, 2010 est.

Production Net ExportsTotal Grains 15% 4%Wheat 20% 7%Barley 39% 39%Pork Meat 22% 30%Cow Milk 27% 22%

Source: USDA, 2011

• General (2010)• Population ~ 516 million• GDP (PPP) ~ $13.77 trillion• Top four economies based on GDP:

• Germany, UK, France, Italy

• Agricultural (2009)• Utilized agricultural area ~ 192 million hectares• Arable land ~ 111 million hectares

• Approximately 70 million hectares of permanent crop or grassland

• Share of the world market:

44

|

EU 27Economic Update

Deere & Company | July 2012

Deere & Company Forecast as of 16 May 2012

45

Optimism continues in the Agricultural sector• Farm business climate and mood remain at high levels

Farm income expected to be above long-term average levels• Grain, beef and milk prices at attractive levels

Demand for agricultural equipment remains strong• Sovereign debt and fiscal issues concentrated in Southern Europe

• Not key agricultural markets

Low levels of used equipment

|

• November 2011 – Awards received at Agritechnica 2011• 7280R – “Tractor of the Year 2012”• 6R tractor – “Machine of the Year”• Five silver medals

• June 2011 – Largest new product introduction for Region 2*• Over 100 new products

• 80% of large tractor and combine models new or updated

• Focus on Dealer of Tomorrow strategy

• May 2011 – John Deere and Kuhn Group sign strategic cooperation

• Provides large square balers into Region 2* in 2012

Deere & Company | July 2012

EU 27Recent Announcements

* Region 2: EU 27, CIS (including Russia), Mediterranean countries in Africa, and the Near and Middle East

46

|

0

10

20

30

40

50

60

70

1990 1995 2000 2005 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

EUR

bn

(nom

inal

pric

es)

Pillar I (Direct Payments + Market Expenditures) Pillar II (Rural Development)

2007-2013 2014-2020

Deere & Company | July 2012

EU 27Government Support of Agriculture

• Common Agricultural Policy proposed budget 2014-2020 frozen at 2007-2013 nominal levels• Rules generally known, eliminating uncertainty• Redistribution of direct payments in favor of new member states

Source: EU Commission, Agra Europe

47

|

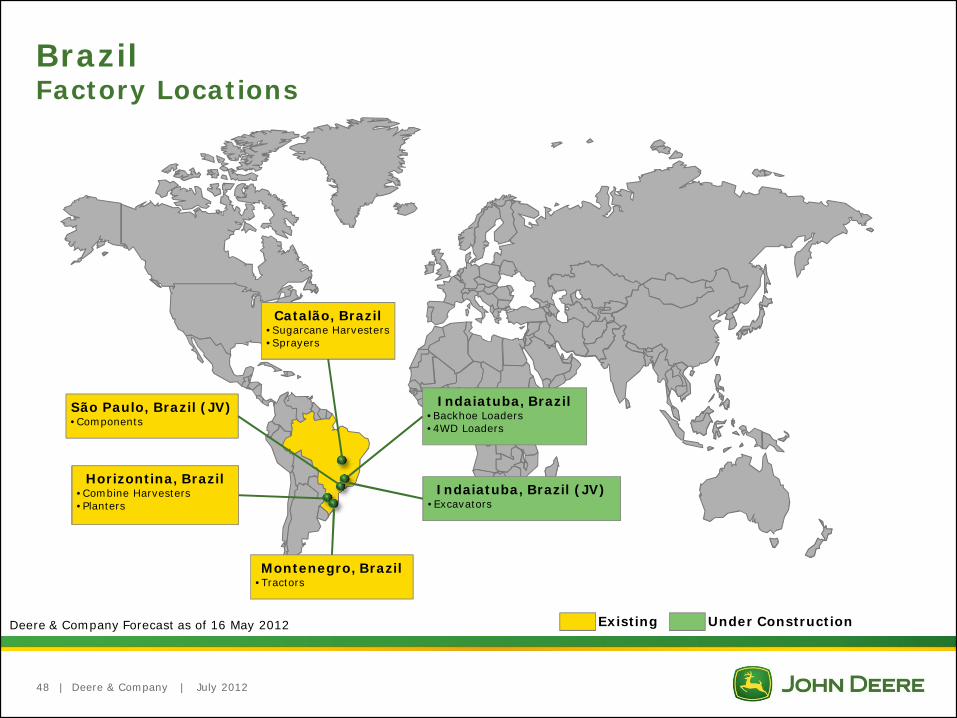

BrazilFactory Locations

Deere & Company | July 2012

São Paulo, Brazil (JV)• Components

Catalão, Brazil• Sugarcane Harvesters• Sprayers

Montenegro, Brazil• Tractors

Horizontina, Brazil• Combine Harvesters• Planters

Indaiatuba, Brazil• Backhoe Loaders• 4WD Loaders

Indaiatuba, Brazil (JV)• Excavators

Deere & Company Forecast as of 16 May 2012

48

Existing Under Construction

|

BrazilEconomic Data

Deere & Company | July 2012

• General (2010)• Population ~ 193 million• GDP (PPP) ~ $2.172 trillion• Top four cities based on population:

• São Paulo, Rio de Janeiro, Salvador and Brasília

• Agricultural• Brazil converted ~ 13 million hectares from pasture land into

crop land in the last 10 years• Soybean, Corn, Sorghum, Cotton, and Sugarcane

• Deere projects ~20 million hectares will be brought into production in the next decade

• Soybeans and corn• Deere projects ~5% CAGR in industry equipment sales through

the end of this decade

5.8%

26.8%

67.4%

GDP Composition

Agriculture Industry ServicesSource: Brazilian Institute of Geography and Statistics (IBGE), 2010

18%

24%58%

Labor Composition

Agriculture Industry ServicesSource: Brazilian Institute of Applied Economic Research (IPEA), 2008

PPP: Purchasing Power ParitySource: Brazilian Institute of Geography and Statistics (IBGE), The World Fact BookDeere & Company Forecast as of 16 May 2012

49

| Deere & Company | July 2012

BrazilRecent Announcements

• October 2011 – Two new factories in São Paulo to manufacture construction equipment• Solely-owned Deere factory

• Backhoe and four-wheel-drive loaders• Partner with Hitachi in second factory

• Excavators• Expect production to begin in 2013

Deere & Company Forecast as of 16 May 20121 Carta da Anfavea, November 2011

• Agriculture portfolio and dealer expansion• 50 new or updated products• Dealer locations roughly doubled since 2007• Achieved 4 points of tractor market share in

FY 20111

50

| Deere & Company | July 2012

BrazilGross Value of Production

Source: MAPA (Brazilian Ministry of Agriculture), May 2012

51

Gross Value of Agricultural Production*

* In Brazilian Real

Expected to increase 2.7% in 2012 over last season

2011 Mix by Crop

1997

1999

2001

2003

2005

2007

2009

2011

49%

16%

35%

Grains Sugarcane Other

| Deere & Company | July 2012

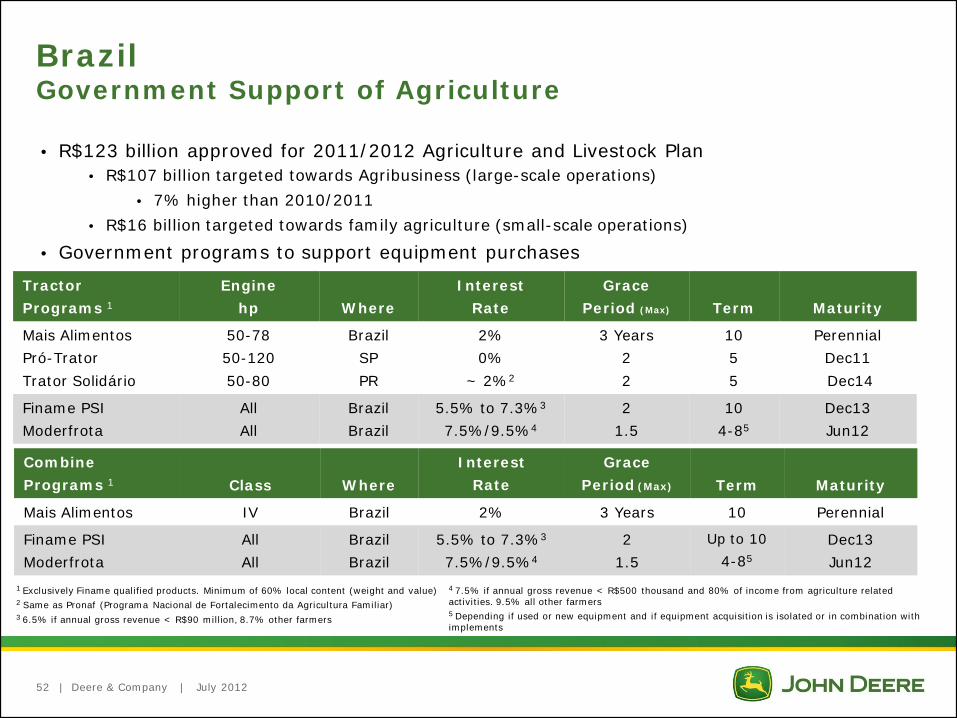

• R$123 billion approved for 2011/2012 Agriculture and Livestock Plan• R$107 billion targeted towards Agribusiness (large-scale operations)

• 7% higher than 2010/2011• R$16 billion targeted towards family agriculture (small-scale operations)

• Government programs to support equipment purchases

BrazilGovernment Support of Agriculture

52

Tractor Programs 1

Enginehp Where

InterestRate

GracePeriod (Max) Term Maturity

Mais AlimentosPró-TratorTrator Solidário

50-7850-12050-80

BrazilSPPR

2%0%

~ 2%2

3 Years22

1055

PerennialDec11Dec14

Finame PSIModerfrota

AllAll

BrazilBrazil

5.5% to 7.3%3

7.5%/9.5%4

2 1.5

104-85

Dec13Jun12

CombinePrograms 1 Class Where

InterestRate

GracePeriod (Max) Term Maturity

Mais Alimentos IV Brazil 2% 3 Years 10 Perennial

Finame PSIModerfrota

AllAll

BrazilBrazil

5.5% to 7.3%3

7.5%/9.5%4

2 1.5

Up to 104-85

Dec13Jun12

1 Exclusively Finame qualified products. Minimum of 60% local content (weight and value)2 Same as Pronaf (Programa Nacional de Fortalecimento da Agricultura Familiar)3 6.5% if annual gross revenue < R$90 million, 8.7% other farmers

4 7.5% if annual gross revenue < R$500 thousand and 80% of income from agriculture related activities. 9.5% all other farmers5 Depending if used or new equipment and if equipment acquisition is isolated or in combination with implements

|

CISFactory Locations

Orenburg, Russia• Seeding Equipment• Tillage Equipment• Spraying Equipment

Deere & Company | July 201253

Orenburg, Russia• Seeding Equipment• Tillage Equipment• Spraying Equipment

Domodedovo, Russia• Tractors• Combine Harvesters• Combine Front-End Equipment• Backhoes, Loaders, Graders• Log Forwarders, Skidders

Existing Under ConstructionDeere & Company Forecast as of 16 May 2012

|

CISEconomic Data

Deere & Company | July 2012

• General (2010)• Population ~ 279 million• GDP (PPP) ~ $2.81 trillion• Top four economies based on GDP:

• Russia, Ukraine, Kazakhstan and Belarus

• Agricultural (2009)• Utilized agricultural area ~ 560 million hectares• Arable land ~ 196 million hectares• Deere estimates “western-style” equipment used

<25% of farmed hectares

• Share of the world market:

PPP: Purchasing Power ParitySource: FAO, Global Insight, The World FactbookDeere & Company Forecast as of 16 May 2012

4.2%

37.0%58.8%

GDP Composition

Agriculture Industry ServicesSource: The World Factbook, 2011 est.

9.8%

27.5%62.7%

Labor Composition

Agriculture Industry ServicesSource: The World Factbook, 2010 est.

Production Net ExportsTotal Grains 10% 19%Wheat 16% 21%Barley 23% 15%Rapeseed 5% 14%Sunflower 49% 51%

Source: USDA, 2011

(Russia)

(Russia)

54

| Deere & Company | July 2012

CISRecent Announcements

• November 2011 – Orenburg, Russia• Move existing operations to a new, larger facility• Increase available manufacturing space by ~ 600 percent• Expand product offering from four to fifteen models

• March 2011 – Domodedovo, Russia• Double manufacturing space at the factory• Expand capacity for existing products• Enable addition of new products such as log

forwarders and front-end equipment

55

| Deere & Company | July 2012

CISGovernment Support of Agriculture

• Export barriers lifted• Russian grain export ban ended in July 2011• Ukraine’s wheat and corn export duty ended in October 2011

• Barley export duty ended in January 2012

• Russian Ag funding is expected to increase in 2012 by ~ 7% in nominal terms

• Annual Ag support in the Russian National Ag Program for 2013 - 2020 expected to more than double by 2020 in nominal terms, but can be shortened and/or restructured due to WTO requirements

• Ag modernization support, including machinery investments, expected to be $4.2 billion over 8 year period

• Loan interest rate subsidies may decline in favor of direct payments

56

|

IndiaFactory Locations

Deere & Company | July 2012

Gummidipoondi, India (JV)• Side-Shift Backhoes• 4WD Loaders (planned production 2013)

Pune, India• Engines• Transmissions• Tractors (36-75 hp)

Sirhind, India• Combine Harvesters

Dewas, India• Tractors (36-50 hp)

Deere & Company Forecast as of 16 May 2012

57

Existing Under Construction

|

IndiaEconomic Data

Deere & Company | July 2012

• General• Population ~ 1.205 billion (July 2012 est.)• GDP (PPP) ~ $4.463 trillion (2011 est.)• Top four cities based on population (2011 est.):

• Mumbai, Delhi, Bangalore and Hyderabad

• Agricultural• Total land area ~ 3.0 million sq km• Arable land ~ 1.5 million sq km (2005 est.)• Annual industry tractor sales >500,000 units• High interest rates• Commodity prices expected to soften against 2011 but remain

elevated due to strong demand• Increased focus from government for farm mechanization

• Infrastructure investment projected to be ~ 9% of GDP by 2012 (~5% in 2007)

18.9%

18.2%62.8%

GDP Composition

Agriculture Industry ServicesSource: IHS Global Insight, 2010 est.

52.0%

14.0%

34.0%

Labor Composition

Agriculture Industry ServicesSource: The World Factbook, 2009 est.

PPP: Purchasing Power ParitySource: The World Fact Book, Censusindia, Tractor Manufacturers Association of India

58

|

• January 2011 – New tractor factory in Dewas and expand current tractor facility in Pune

• ~ $100 million investment

• Expect production in Dewas to begin in 2013

• October 2010 – Ashok Leyland John Deere Construction Equipment Company inauguration

• Production of backhoes commenced in 2011

• Four-wheel-drive loader production expected in 2013

• September 2010 – New combine factory in Sirhind• Production commenced February 2012

• John Deere has been the largest exporter of tractors from India for past 8 years

Deere & Company | July 2012

IndiaRecent Announcements

Deere & Company Forecast as of 16 May 2012

59

| Deere & Company | July 2012

IndiaGovernment Support of Agriculture

159

185

262

325

766

530

623

672

610

258

231

240

313

438

560

638

728

750

35

40

60

123

143

170

195

237

180

194

197

207

275

36

56

48151

332

0 500 1,000 1,500 2,000 2,500

2004

2005

2006

2007

2008

2009

2010

2011

2012F

Rupees (in billions)

Fertilizer Subsidy

Food Subsidy (for households)

Interest Rate Subsidy (for farmers)

Irrigation Subsidy

Electricity Subsidy

Other Subsidies (mainly for seeds)

Source: India Ministry of Agriculture (2004-2009), India Ministry of Finance (2010-2012)

756

809

917

1,191

2,048

1,090

1,296

1,440

60

1,420

|

ChinaFactory Locations

Deere & Company | July 2012

Xuzhou, China (JV)• Excavators

Ningbo, China• Tractors (28-70 hp)• Small Combine Harvesters

Tianjin, China (JV)• Tractors (75-135 hp)

Tianjin (TEDA), China• Transmissions

Jiamusi, China• Large Combine Harvesters• Corn Pickers

Harbin, China• Combine Front-End Equipment• Tractors (150+ hp)• Planters• Sprayers• Irrigation Products

Tianjin (TEDA), China• 4WD Loaders• Excavators

Tianjin (TEDA), China• Engines

Deere & Company Forecast as of 16 May 2012

61

Existing Under Construction

|

ChinaEconomic Data

Deere & Company | July 2012

• General• Population ~ 1.343 billion (July 2012 est.)• GDP (PPP) ~ $11.3 trillion (2011 est.)• Top four cities based on population (2009):

• Shanghai, Beijing, Chongqing and Shenzhen

• Agricultural• Total land area ~ 9.6 million sq km• Arable land ~ 1.4 million sq km (2005 est.)

• Share of the world market:

10.1%

46.8%

43.1%

GDP Composition

Agriculture Industry ServicesSource: The World Factbook, 2011 est.

36.7%

28.7%

34.6%

Labor Composition

Agriculture Industry ServicesSource: The World Factbook, 2008 est.

PPP: Purchasing Power ParitySource: The World Factbook

ProductionTotal Grains 17%Wheat 17%Corn 22%Rice 30%Cotton 27%

62

Source: USDA, 2011

| Deere & Company | July 2012

ChinaRecent Announcements

Deere & Company Forecast as of 16 May 2012

Construction Equipment (New)

Engines (New)

ProductTest (PV&V)

Office (New)

Tianjin Economic-Technological Development Area (TEDA) Site

Drivetrain

• May 2011 – New engine facility in Tianjin• ~ $60 million investment

• Expect production to begin in 2013

• May 2011 – New factory in Harbin• ~ $80 million initial outlay

• Mid- and large-sized tractors

• Harvesting front-end equipment

• Planters and sprayers

• Irrigation products

• Expect production to begin in 2013

• December 2010 – New construction equipment factory in Tianjin• ~ $50 million investment

• Expect production to begin in 2013

63

| Deere & Company | July 2012

Source: China Ministry of Agriculture

ChinaGovernment Support of Agriculture

12

28

72

75

72

86

108

12

13

14

15

15

19

15

15

15

3

4

4

7

12

20

20

22

22

1

2

4

13

16

18

20

0 25 50 75 100 125 150 175

2004

2005

2006

2007

2008

2009

2010

2011

2012F

RMB (in billions)

Material Subsidy (basic subsidy for purchase of inputs)Grain Direct Subsidy (for growing encouraged crops)Seed Subsidy (for purchasing high-performing seed)Equipment Subsidy (for purchasing encouraged equipment)

141

15

17

31

52

103

127

123

64

165

|

Other RegionsFactory Locations

Deere & Company | July 201265

Kibbutz Beit Hashita, Israel• Cotton Picker Components

Rosario, Argentina• Engines• Tractors (planned)• Combines (planned)

Monterrey, Mexico• Rotary Cutters• Implements• Components

Ramos, Mexico• Ag Loaders• Compact Utility Tractor Loaders• Utility Tractor Cabs

Saltillo, Mexico• Ag Tractors• Transaxles

Torreon, Mexico• Axles• Engines• Electronics

Richards Bay, South Africa• Articulated Dump Trucks• Loaders

Tokoroa, New Zealand• Forestry Harvester Heads

Deere & Company Forecast as of 16 May 2012

|

Recent announcements:November 2011 – Bruchsal, Germany

Inauguration of new deconsolidation & packaging facility within European Parts Distribution Center

September 2011 – Rosario, ArgentinaConstruction of new, larger parts facility

Worldwide Parts ServicesSupporting the Global Growth of Our Equipment Operations

Deere & Company | July 2012

3 largest Parts Distribution CentersOther Parts Distribution locations

66

| Deere & Company | July 2012

Integrated wireless technology linking the equipment, owners, operators, dealers, and agricultural consultants to provide more productivity to a farm or business.

Machine OptimizationSolutions that get the most out of machineryUse of precision technology and wireless data networks Higher levels of productivity and increased uptime

Logistics Optimization Manage logistics and machinery from remote locationsFleet management solutions Increased machine-to-machine communication

Ag Decision Support User-friendly monitors, sensors, wireless networksEasy access to machinery and agronomic dataEnable proactive management decisions

John Deere FarmSightTM

67

| Deere & Company | July 2012

John Deere WaterLeveraging our leadership in global agriculture to provide innovative and efficient agricultural water management solutions, and increase agricultural productivity

Innovative solutionsEfficient irrigation and water managementSuperior channel partners

Integration of machinery and technologyConsistent application of the right amount of water at the right timeEnable increased yields and higher quality cropsImprove water use efficiency and reduce input costs

Partnering with our customersOptimize operations and outputEnable good stewardship of water resources

68

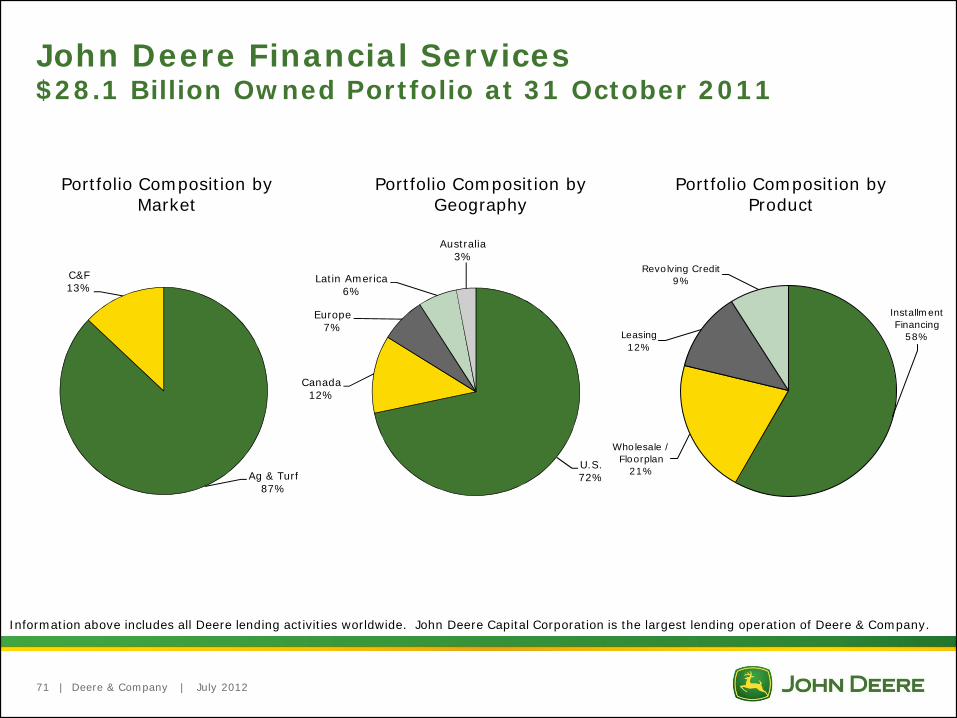

John Deere Financial Services

| Deere & Company | July 2012

John Deere Financial ServicesSupporting the Global Growth of Our Equipment Operations

Deere & Company Forecast as of 16 May 2012

New locations announced:China … began operations 4Q 2011

Russia … began operations 2Q 2012

Chile … operations expected to begin 2H 2012

India … operations expected to begin 2H 2012

Thailand … operations expected to begin 2H 2012

70

| Deere & Company | July 2012

Portfolio Composition by Market

John Deere Financial Services$28.1 Billion Owned Portfolio at 31 October 2011

Portfolio Composition by Geography

Portfolio Composition by Product

Information above includes all Deere lending activities worldwide. John Deere Capital Corporation is the largest lending operation of Deere & Company.

Ag & Turf87%

C&F13%

U.S.72%

Canada12%

Europe7%

Latin America6%

Australia3%

Revolving Credit9%

Leasing12%

Installment Financing

58%

Wholesale / Floorplan

21%

71

| Deere & Company | July 2012

John Deere Capital CorporationProfitability and Growth

271 275 291 311282

149

319364

2004 2005 2006 2007 2008 2009 2010 2011

Net Income ($ Millions)

2004 2005 2006 2007 2008 2009 2010 2011

0.28% 0.16% 0.22% 0.29% 0.33%

0.70%

0.48%

0.12%

Write-offs/Average Owned Portfolio

2004 2005 2006 2007 2008 2009 2010 2011

16.417.7 18.6 19.0 19.1 19.3

21.123.3

Administered Portfolio Growth ($ Billions)

72

| Deere & Company | July 2012

John Deere Capital Corporation Retail Notes60+ Days Past Due vs. Write-offs

Agriculture & Turf1

• Extremely low write-offs; average less than 5 bps over last 10 years

• Even in severe Ag market of the 1980s, losses were comparatively low

Construction & Forestry• The performance and quality

of portfolio improved during 2011

-0.05%

0.45%

0.95%

1.45%

1.95%

2.45%

2.95%

3.45%

3.95%

'83 '86 '89 '92 '95 '98 '01 '04 '07 '10Net Write-offs (Ag) Installments 60+DPD (Ag)

-0.05%

0.45%

0.95%

1.45%

1.95%

2.45%

2.95%

3.45%

3.95%

'95 '98 '01 '04 '07 '10Net Write-offs (C&F) Installments 60+DPD (C&F)

(1) 1982 – 1985 includes Construction; 1986 - 1994 includes Lawn & Grounds Care; beginning in 2009 includes both Ag and Turf equipment; As % of Owned Losses After Dealer Reserve Charges

Source: 1982 – 1994 internal reporting, 1995 - 2010 JDCC 10-K filings, 2011 Deere & Company 8-K filed with SEC 23 November 2011

73

|

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Res

ale

Valu

e as

a %

of

Origi

nal

List

Price

Time Since Origination

2010 2009 2008 2007 2006 2005

Deere & Company | July 2012

U.S. Resale Value vs. Loan Balance7830 Tractor and 9670 Combine

(1) Model 7810 was replaced with Model 7820 in 2004. In 2007 the 7830 series was introduced to the market. Loan balance assumes a 30% down payment on the highest list price financed for 5 years with annual payments at a rate of 6.50%.

(2) Model 9650 was replaced with Model 9660 in 2004. Model 9660 was subsequently replaced with Model 9670 in 2006.Loan balance assumes a 30% down payment on the highest list price financed for 5 years with annual payments at a rate of 6.50%.

Source for equipment values: North American Equipment Dealers Association

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Res

ale

Val

ue a

s a

% o

f O

rigi

nal L

ist Pr

ice

Time Since Origination

2010 2009 2008 2007 2006 2005

Loan Balance

Model Year

7830 Tractor (1)

Model Year

9670 Combine (2)

Loan Balance

74

John DeerePower Systems

Engine Emissions and Technology

| Deere & Company | July 2012

Interim Tier 4 (IT4): • 50% Nitrogen Oxide (NOx) reduction• 90% Particulate Matter (PM) reduction

Final Tier 4 (FT4):• 80% NOx reduction

Tier 4 Engine Implementation

Final Tier 4

0

0.10

0.20

0.30

0.40

0.50

0 2.00 4.00 6.00 8.00 10.00 12.00

Tier 1

Tier 2

Tier 3

Interim Tier 4

NOx, g/kw-hr

PM

, g/

kw-h

r

76

| Deere & Company | July 2012

Final Tier 4Continuing Our Planned Building-Block Approach

Combines our customized selective catalytic reduction (SCR) system with our proven IT4 engine platform of cooled exhaust gas recirculation (EGR), diesel oxidation catalyst (DOC), and diesel particulate filter (DPF)

• An optimized solution – John Deere Integrated Emissions Control system– Meets Final Tier 4 emissions regulations– Uncompromised performance: power, torque, and responsiveness

• A fluid-efficient solution - maximum total fluid economy, not just fuel economy– Leverages the proven fuel efficiency of our PowerTech™ Plus engine platform– Low diesel exhaust fluid (DEF) dosing rates– Operate efficiently with low-sulfur diesel and B5-B20 blends

• A field-proven solution– Since 2005, our cooled EGR engines have a proven record of performance and durability– More than 5 million customer operating hours with our smart exhaust filter technology– Dedicated in-house aftertreatment team customizing our own SCR system

• An integrated vehicle solution– We design, manufacture, and service the engine, drivetrain, hydraulics, cooling, and electrical

systems• A fully supported solution

– John Deere’s proven worldwide dealer network is highly trained to provide service and support as well as increase productivity, reliability, and utilization of Deere machines

77

Farm Fundamentals

| Deere & Company | July 2012

U.S. Farm Cash ReceiptsOperating Cash Receipts and Government Payments

• Total cash receipts remain at historically high levels• Record levels expected for 2011

$0

$50

$100

$150

$200

$250

$300

$350

$400

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011F 2012F

$ Bill

ions

Government Payments Total Cash Receipts

Source: 1998 – 2010: USDA 13 February 20122011F – 2012F: Deere & Company Forecast as of 16 May 2012

79

| Deere & Company | July 2012

U.S. Farm Balance Sheet Strong

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

$0

$500

$1,000

$1,500

$2,000

$2,50019

7019

7119

7219

7319

7419

7519

7619

7719

7819

7919

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

11F

2012

F

$ Bill

ions

Farm Debt Farm Equity Debt to Equity Ratio (%) Debt to Asset Ratio (%)

Source: 1970 – 2010: USDA 13 February 20122011F – 2012F: Deere & Company Forecast as of 16 May 2012

80

| Deere & Company | July 2012

Corn, Soybeans, Wheat and Cotton PricesNearby Futures: 10 July 2007 – 10 July 2012

Source: Chicago Board of Trade – Corn, Soybeans & Wheat; Intercontinental Exchange – Cotton

1.002.003.004.005.006.007.008.009.00

7/10/07 7/10/08 7/10/09 7/10/10 7/10/11 7/10/12

Do

llars

Per

Bu

shel

Corn

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

7/10/07 7/10/08 7/10/09 7/10/10 7/10/11 7/10/12

Dol

lars

per

Bu

shel

Soybeans

2.00

4.00

6.00

8.00

10.00

12.00

14.00

7/10/07 7/10/08 7/10/09 7/10/10 7/10/11 7/10/12

Do

llars

per

Bu

shel

Wheat

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

7/10/07 7/10/08 7/10/09 7/10/10 7/10/11 7/10/12

Dol

lars

per

Pou

nd

Cotton

81

| Deere & Company | July 2012

Agricultural Growth – Energy2007 U.S. Energy Bill

• Significantly expanded mandatory levels of renewable fuels

Source: Energy Independence and Security Act of 2007

0

5

10

15

20

25

30

35

40

2008 2010 2012 2014 2016 2018 2020 2022

Gal

lons

(bi

llion

s)

Corn-Based Starch Ethanol Advanced Biofuels

82

| Deere & Company | July 2012

Uses of U.S. Corn Crop 2010-2021Bus

hels

(m

illio

ns)

Source: USDA Agricultural Projections to 2021, February 2012

83

20.0%

23.0%

26.0%

29.0%

32.0%

35.0%

38.0%

41.0%

0

5,000

10,000

15,000

20,000

25,000

Feed & residual Ethanol & By-Products for fuel Food, Seed, & Industrial (Less Ethanol) ExportsEthanol & By-Products for Fuel as % of Total Corn Usage

|

0%

10%

20%

30%

40%

50%

60%

70%19

92

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

E

2012

P

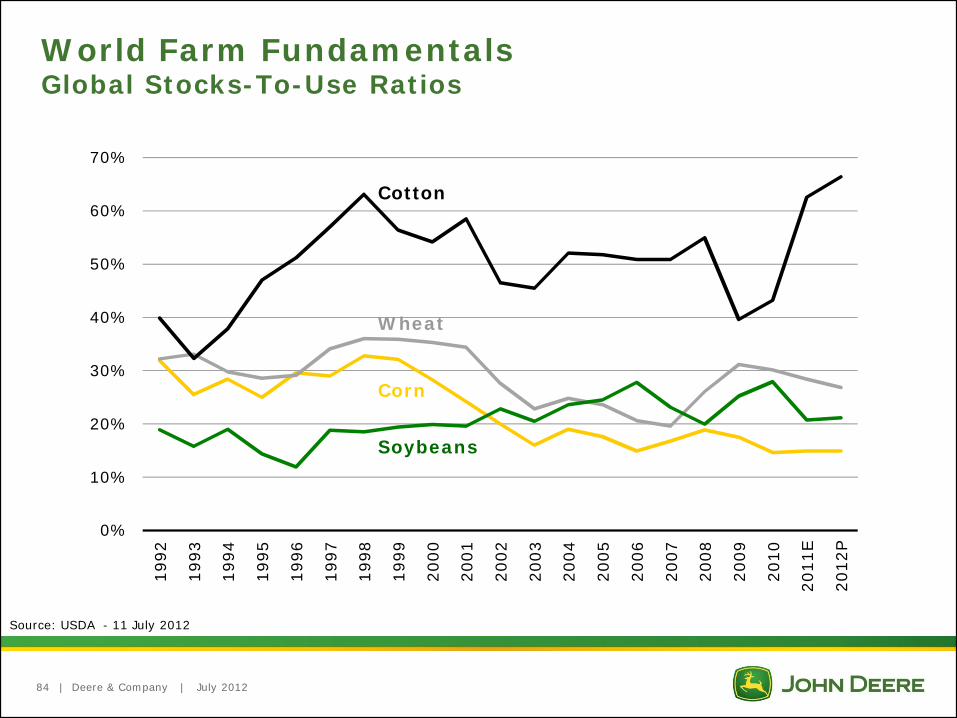

World Farm FundamentalsGlobal Stocks-To-Use Ratios

Source: USDA - 11 July 2012

Deere & Company | July 201284

Cotton

Wheat

Corn

Soybeans

| Deere & Company | July 2012

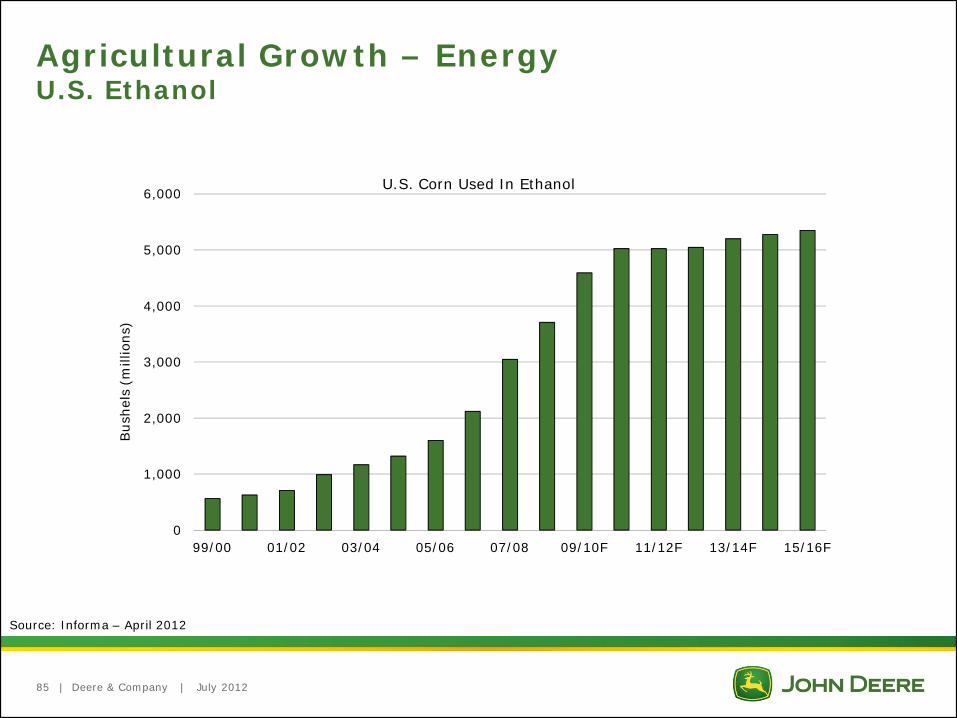

Agricultural Growth – EnergyU.S. Ethanol

U.S. Corn Used In Ethanol

Source: Informa – April 2012

85

0

1,000

2,000

3,000

4,000

5,000

6,000

99/00 01/02 03/04 05/06 07/08 09/10F 11/12F 13/14F 15/16F

Bus

hels

(m

illio

ns)

| Deere & Company | July 2012

Daily Ethanol Margin Per Bushel Corn GrindBased on Nearby Futures Prices (Excl ITDA*)

*Interest, Tax, Depreciation and Amortization (ITDA) totals ~$0.50 and is often disregarded in margin calculations because it does not influence short term production decisionsSource: Informa – July 2012

($0.50)

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

7/10

/08

10/1

0/08

1/10

/09

4/10

/09

7/10

/09

10/1

0/09

1/10

/10

4/10

/10

7/10

/10

10/1

0/10

1/10

/11

4/10

/11

7/10

/11

10/1

0/11

1/10

/12

4/10

/12

7/10

/12

86

Market and Currency Volatility

|

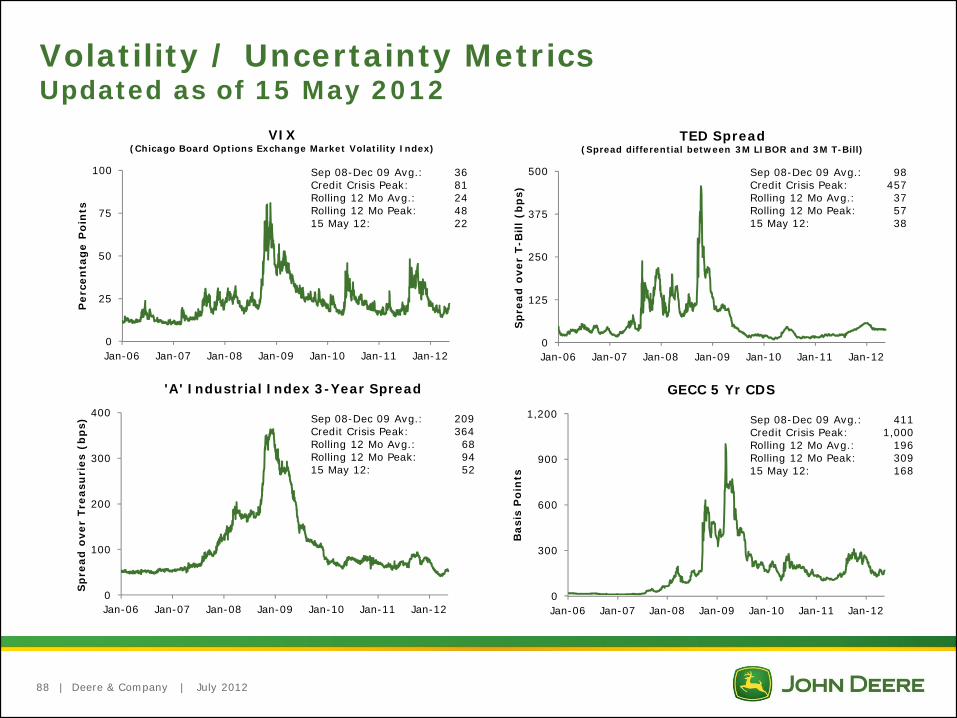

Volatility / Uncertainty MetricsUpdated as of 15 May 2012

Deere & Company | July 201288

Sep 08-Dec 09 Avg.: 36Credit Crisis Peak: 81Rolling 12 Mo Avg.: 24Rolling 12 Mo Peak: 4815 May 12: 22

Sep 08-Dec 09 Avg.: 411Credit Crisis Peak: 1,000Rolling 12 Mo Avg.: 196Rolling 12 Mo Peak: 30915 May 12: 168

Sep 08-Dec 09 Avg.: 209Credit Crisis Peak: 364 Rolling 12 Mo Avg.: 68Rolling 12 Mo Peak: 9415 May 12: 52

Sep 08-Dec 09 Avg.: 98Credit Crisis Peak: 457Rolling 12 Mo Avg.: 37Rolling 12 Mo Peak: 5715 May 12: 38

0

25

50

75

100

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Per

cen

tag

e P

oin

ts

VIX(Chicago Board Options Exchange Market Volatility Index)

0

125

250

375

500

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Sp

read

ove

r T

-Bill

(b

ps)

TED Spread(Spread differential between 3M LIBOR and 3M T-Bill)

0

100

200

300

400

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Sp

read

ove

r T

reas

uri

es (

bp

s)

'A' Industrial Index 3-Year Spread

0

300

600

900

1,200

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Bas

is P

oin

ts

GECC 5 Yr CDS

|

65

75

85

95

105

115

125

135

Ind

exed

Val

ue

EUR

GBP

AUD

JPY

CAD

BRL

Wea

ker

FCSt

rong

er F

C

Currency Movement Post Credit Crisis

Deere & Company | July 2012

FY 2008 FY 2009 FY 2010 FY 2011

89

FY 2007

Appendix

| Deere & Company | July 2012

Enterprise SVA Reconciliation to GAAP

Equipment Operations 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011Net Sales 11,077 11,703 13,349 17,673 19,401 19,884 21,489 25,803 20,756 23,573 29,466 Average Identifiable Assets

With Inventories at LIFO 8,743 6,229 5,965 6,482 7,248 7,546 8,092 9,652 9,647 9,196 11,516 With Inventories at Standard Cost 9,678 7,147 6,925 7,477 8,312 8,634 9,205 10,812 10,950 10,494 12,875

Operating Profit (46) 401 708 1,905 1,842 1,905 2,318 2,927 1,365 2,909 3,839 Percent of Net Sales -0.4% 3.4% 5.3% 10.8% 9.5% 9.6% 10.8% 11.3% 6.6% 12.3% 13.0%

Operating Return on AssetsWith Inventories at LIFO -0.5% 6.4% 11.9% 29.4% 25.4% 25.2% 28.6% 30.3% 14.1% 31.6% 33.3%With Inventories at Standard Cost -0.5% 5.6% 10.2% 25.5% 22.2% 22.1% 25.2% 27.1% 12.5% 27.7% 29.8%

SVA Cost of Assets (1,162) (858) (831) (897) (998) (1,036) (1,094) (1,284) (1,301) (1,259) (1,545) Equipment Operations SVA (1,208) (457) (123) 1,008 844 869 1,224 1,643 64 1,650 2,294

Financial ServicesNet Income 262 330 309 345 584 364 337 203 373 471Average Equity 2,115 2,177 2,265 2,227 2,466 2,524 2,355 2,732 3,064 3,194Return on Equity 12.40% 15.20% 13.60% 15.50% 23.70% 14.40% 14.30% 7.40% 12.20% 14.70%Operating Profit Continuing 416 504 466 491 521 553 493 242 499 725Change in Allowance for Doubtful Receivables 16 17 -8 -12 15 17 -4 68 -14 - SVA Income Continuing 432 521 458 479 536 570 489 310 485 725Average Equity Continuing Operations 2,115 2,177 2,163 2,110 2,424 2,524 2,355 2,732 3,064 3,194Average Allowance for Doubtful Receivables 161 160 165 150 148 167 183 195 232 - SVA Average Equity 2,276 2,337 2,328 2,260 2,572 2,691 2,538 2,927 3,296 3,194Cost of Equity -437 -431 -414 -410 -457 -480 -430 -458 -420 -492SVA Continuing Operations 44 69 79 90 59 -148 65 233SVA Discontinued Operations -11 25 - - - - - - Financial Services SVA (5) 90 44 69 79 90 59 (148) 65 233

Deere & Company - Enterprise SVA (462) (33) 1,052 913 948 1,314 1,702 (84) 1,715 2,527

(millions of dollars unless stated otherwise)

91

| Deere & Company | July 2012

Equipment Ops SVA Reconciliation to GAAP

Equipment Operations 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001Net Sales 5,848 5,723 6,479 7,663 8,830 9,640 11,082 11,926 9,701 11,169 11,077 Average Identifiable Assets

With Inventories at LIFO 5,585 5,765 5,449 5,551 6,187 6,502 6,682 7,672 7,724 8,069 8,743 With Inventories at Standard Cost 6,702 6,846 6,442 6,494 7,131 7,488 7,703 8,711 8,739 9,039 9,678

Operating Profit 16 77 242 847 1,006 1,125 1,402 1,476 272 693 (46) Percent of Net Sales 0.3% 1.3% 3.7% 11.1% 11.4% 11.7% 12.6% 12.4% 2.8% 6.2% -0.4%

Operating Return on AssetsWith Inventories at LIFO 0.3% 1.3% 4.4% 15.3% 16.3% 17.3% 21.0% 19.3% 3.5% 8.6% -0.5%With Inventories at Standard Cost 0.2% 1.1% 3.8% 13.0% 14.1% 15.0% 18.2% 16.9% 3.1% 7.7% -0.5%

SVA Cost of Assets (804) (821) (773) (780) (856) (898) (924) (1,045) (1,049) (1,085) (1,162) SVA (788) (744) (531) 67 150 227 477 431 (776) (392) (1,208)

Equipment Operations 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011Net Sales 11,703 13,349 17,673 19,401 19,884 21,489 25,803 20,756 23,573 29,466 Average Identifiable Assets

With Inventories at LIFO 6,229 5,965 6,482 7,248 7,546 8,092 9,652 9,647 9,196 11,516 With Inventories at Standard Cost 7,147 6,925 7,477 8,312 8,634 9,205 10,812 10,950 10,494 12,875

Operating Profit 401 708 1,905 1,842 1,905 2,318 2,927 1,365 2,909 3,839 Percent of Net Sales 3.4% 5.3% 10.8% 9.5% 9.6% 10.8% 11.3% 6.6% 12.3% 13.0%

Operating Return on AssetsWith Inventories at LIFO 6.4% 11.9% 29.4% 25.4% 25.2% 28.6% 30.3% 14.1% 31.6% 33.3%With Inventories at Standard Cost 5.6% 10.2% 25.5% 22.2% 22.1% 25.2% 27.1% 12.5% 27.7% 29.8%

SVA Cost of Assets (858) (831) (897) (998) (1,036) (1,094) (1,284) (1,301) (1,259) (1,545) SVA (457) (123) 1,008 844 869 1,224 1,643 64 1,650 2,294

(millions of dollars unless stated otherwise)

92

| Deere & Company | July 2012

2009 OROA Reconciliation to GAAPEquipment Operations

Equipment Operations2009, as Reported

Exclude Goodwill Impairment &

Voluntary Employee-Separation

2009, as Adjusted

Net Sales 20,756 20,756 Average Identifiable Assets

With Inventories at LIFO 9,647 9,647 With Inventories at Standard Cost 10,950 10,950

Operating Profit 1,365 380 1,745 Percent of Net Sales 6.6% 8.4%

Operating Return on AssetsWith Inventories at LIFO 14.1% 18.1%With Inventories at Standard Cost 12.5% 15.9%

(millions of dollars unless stated otherwise)

93