delårsrapport januari-mars 2013 - cisionmb.cision.com/main/509/9414862/122948.pdfis never less than...

TRANSCRIPT

Delårsrapport januari-mars 2013

S 1/18

Q1 Interim Report January-March 2013 May 15, 2013 from Rederi AB TransAtlantic (publ)

Report Q1 2013, January - March

page 2/18

Interim Report 2013, January - March First quarter 2013

Net revenues amounted to SEK 685 M (861)

Result before capital costs, EBITDA, amounted to SEK -18 M (-15)

Result before tax amounted to SEK -138 M (-132)

Result after tax amounted to SEK -137 M (-132)

Earnings per share after tax amounted to SEK -1.2 (-1.2)

Significant events during the quarter

Viking Supply Ships implements, with effect from July 1, 2013, a new organizational structure to centralize all support functions as well as operational management at the head office in Copenhagen.

Swedish Maritime Administration decided not to extend the charter contracts for AHTS icebreakers Tor Viking and Balder Viking. The vessels will be available for contracts after Q1 2014 and Q1 2015 respectively.

Viking Supply Ships entered into a time charter contract for one of its AHTS icebreaker vessels with a major oil company.

Viking Supply Ships completed a tap issue of SEK 87 M (tranche 2) under the existing bond agreement.

The company works with lending banks to ensure a stable short and long-term financing. TransAtlantic has received waivers for the first quarter, 2013, in conjunction with the Group failing to fulfill some of the loan agreements on financial key figures.

Key figures

January-March

2013 2012

Net sales, SEK M 685 861 Operational result before tax, SEK M ¹ -138 -151 Result before tax, SEK M -138 -132 Result after tax, SEK M -137 -132 Earnings per share after tax, SEK -1.2 -1.2 Shareholders’ equity, SEK/share 16.6 21.1 Return on equity, % -27.9 -21.8 Return on capital employed, % -6.3 -6.9 Equity/asset ratio at balance day, % 34.2 36.1

1. Operational result: Earnings before tax, restructuring costs and acquisition effects.

-40%

-30%

-20%

-10%

0%

10%

Q22011

Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Return on capital employed and sharholders' equity, %

Capital employed Shareholders' equity

-400

-200

0

200

400

600

800

1 000

Q22011

Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Net sales and operational proft, SEK M

Net sales Operational profit/loss

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

0

100

200

300

400

500

600

Q22011

Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Liquidity and equity/assets ratio

Liquidity, SEK M Equity/assets ratio, %

Report Q1 2013, January - March

page 3/18

CEO’s statement

Profit before tax before restructuring cost

for the first quarter amounted to

SEK -138 M which is unsatisfactory. Profit

before tax for the group is split into

SEK -76 M (-88) for Viking Supply Ships

and SEK -62 M (-63) for Industrial

Shipping.

As stated in the 2012 Annual Report that was

published during the first quarter, the Group’s

liquidity is strained and exposed to risks. As we

have previously communicated, initiatives to

strengthen the company’s profitability and liquidity

have been initiated and we also continue to work

proactively with lenders to ensure a stable short and

long-term financing.

In addition, the company’s Board of Directors in

April unanimously decided to seek shareholders’

approval for a capital increase through a rights issue

of SEK 150 M. This is in order to improve the

funding structure, liquidity and ultimately the

operational performance of the Industrial Shipping

division in an even quicker fashion than earlier

planned. RABT will seek approval for this rights

issue at an extraordinary shareholders meeting,

date to be announced later.

Industrial Shipping The market situation has deteriorated both in terms

of volumes and rates during the first quarter and as

Industrial Shipping’s customers experience lower

demands from the European market, the volumes

decrease for TransAtlantic. This effect is

compounded by the strengthening of the Swedish

krona. We currently see no signs of recovery for the

remainder of the year. This calls for deeper actions

in order to get a competitive structure and every

stone is turned in order to streamline the

organization while still maintaining focus on

customers and commercial incentives. The division

has recently appointed Birna Ödefors as new CCO

and we believe her experience and background will

be of great benefit for further developing Industrial

Shipping to become significantly more dynamic and

competitive.

Viking Supply Ships Viking Supply Ships (VSS) has started to centralize

all support functions as well as operational

management at the headquarters in Copenhagen.

This means that the Kristiansand office will proceed

as a commercial office and the VSS Gothenburg

office will be closed. The reorganization will be

implemented by July 1, 2013.

During the quarter, Viking Supply Ships completed a

tap issue of SEK 87 M (tranche 2) under the existing

bond agreement. We also announced that the

Swedish Maritime Administration decided to not

extend the charter contracts for AHTS icebreakers

Tor Viking and Balder Viking and that one of these

vessels quickly entered into a time charter contract

with a major oil company.

The quarter was characterized by positioning in the

spot market and sales activities towards longer term

contracts. We believe Viking Supply Ships to be well

positioned in its market with a growing number of

opportunities for longer term contracts in VSS’ areas

of expertise.

Viking Supply Ships cost structure is competitive,

while that of Industrial Shipping needs to be

improved in order to react to deteriorating market

conditions.

For the RABT group, the next quarter will continue

to be challenging because of the same underlying

market conditions as in recent quarters. The key is

to try to offset a deteriorating market in Industrial

Shipping with operational and structural savings as

well as market share gains.

Gothenburg, May 15, 2013

Henning E. Jensen, CEO

Report Q1 2013, January - March

page 4/18

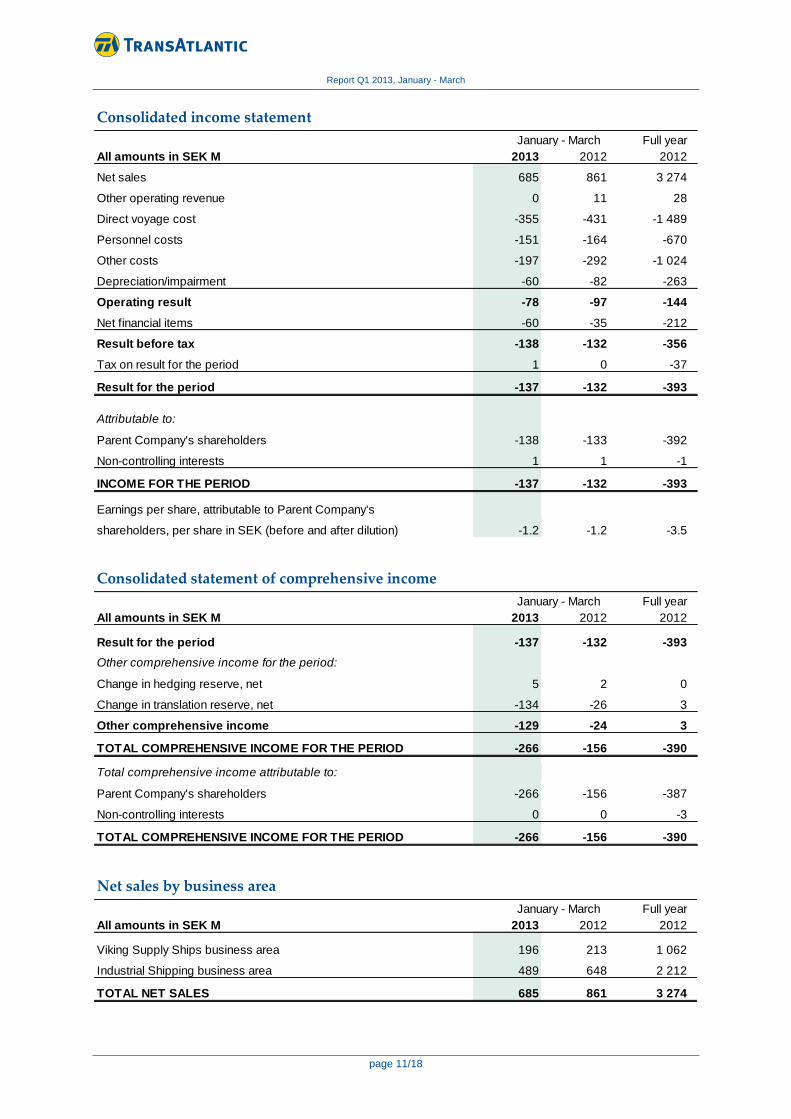

Consolidated earnings for January-March Consolidated net sales for the quarter amounted to SEK 685 M (861). The Group reported a result after tax of

SEK -137 M (-132), of which restructuring costs and acquisition effects amounted total SEK - M (19). The result

before tax amounted to SEK -138 M (-132).

Group

Full Year

SEK M 2013 2012 2012

Net sales 685 861 3 274

Result before capital costs, EBITDA -18 -15 120

Operating result -78 -97 -143

Result before tax -138 -132 -356

Profit margin -20.2% -15.3% -10.9%

Profit before tax by business area

Viking Supply Ships business area -76 -88 -119

Industrial Shipping business area -62 -63 -208

Total operational result -138 -151 -327

Restructuring items - 19 -35

Acquisition effects - - 6

Result before tax -138 -132 -356

Tax 1 0 -37

Result -137 -132 -393

SEK per share

Result after current tax -1.2 -1.2 -3.2

Result after full tax -1.2 -1.2 -3.5

For further information, please see tables on page 11-17.

Jan-Mar

Report Q1 2013, January - March

page 5/18

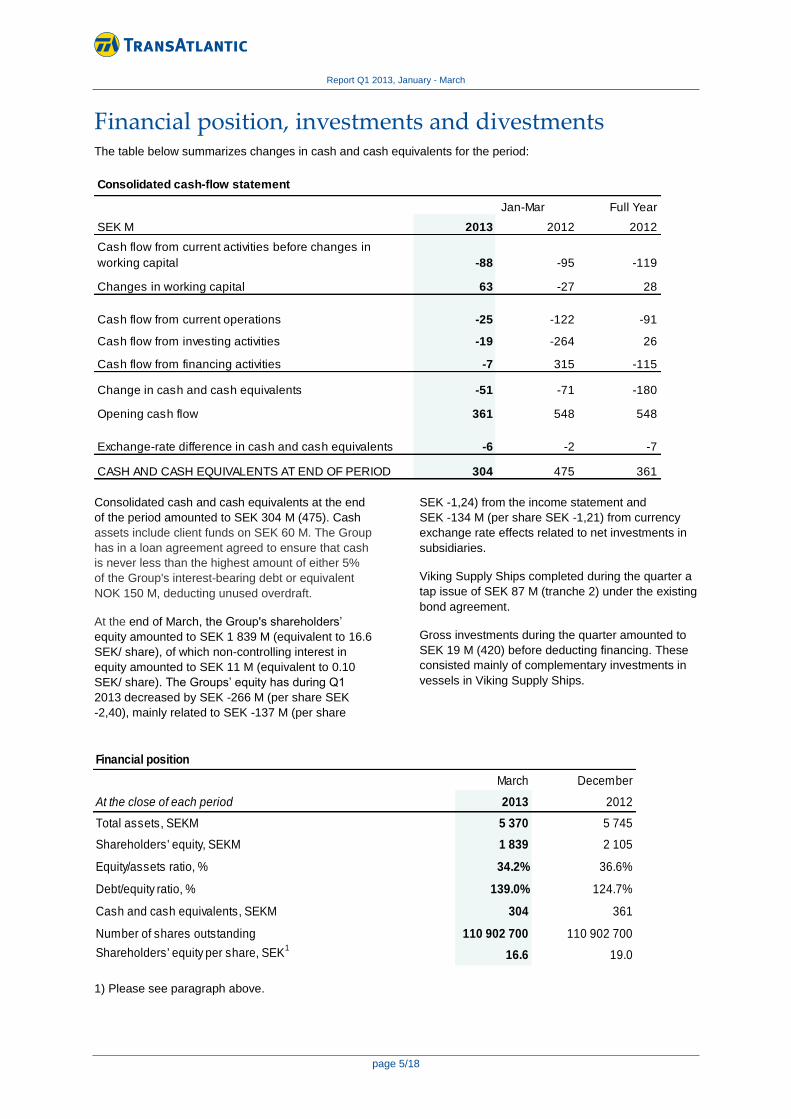

Financial position, investments and divestments The table below summarizes changes in cash and cash equivalents for the period:

SEK M 2013 2012 2012

Cash flow from current activities before changes in

working capital -88 -95 -119

Changes in working capital 63 -27 28

Cash flow from current operations -25 -122 -91

Cash flow from investing activities -19 -264 26

Cash flow from financing activities -7 315 -115

Change in cash and cash equivalents -51 -71 -180

Opening cash flow 361 548 548

Exchange-rate difference in cash and cash equivalents -6 -2 -7

CASH AND CASH EQUIVALENTS AT END OF PERIOD 304 475 361

Full Year Jan-Mar

Consolidated cash-flow statement

Consolidated cash and cash equivalents at the end

of the period amounted to SEK 304 M (475). Cash

assets include client funds on SEK 60 M. The Group

has in a loan agreement agreed to ensure that cash

is never less than the highest amount of either 5%

of the Group's interest-bearing debt or equivalent

NOK 150 M, deducting unused overdraft.

At the end of March, the Group's shareholders’

equity amounted to SEK 1 839 M (equivalent to 16.6

SEK/ share), of which non-controlling interest in

equity amounted to SEK 11 M (equivalent to 0.10

SEK/ share). The Groups’ equity has during Q1

2013 decreased by SEK -266 M (per share SEK

-2,40), mainly related to SEK -137 M (per share

SEK -1,24) from the income statement and

SEK -134 M (per share SEK -1,21) from currency

exchange rate effects related to net investments in

subsidiaries.

Viking Supply Ships completed during the quarter a

tap issue of SEK 87 M (tranche 2) under the existing

bond agreement.

Gross investments during the quarter amounted to

SEK 19 M (420) before deducting financing. These

consisted mainly of complementary investments in

vessels in Viking Supply Ships.

1) Please see paragraph above.

Financial position

March December

At the close of each period 2013 2012

Total assets, SEKM 5 370 5 745

Shareholders' equity, SEKM 1 839 2 105

Equity/assets ratio, % 34.2% 36.6%

Debt/equity ratio, % 139.0% 124.7%

Cash and cash equivalents, SEKM 304 361

Number of shares outstanding 110 902 700 110 902 700

Shareholders' equity per share, SEK1

16.6 19.0

Report Q1 2013, January - March

page 6/18

Industrial Shipping business area The first quarter was marked by a tough

market with excess capacity and further

reduced demand. The weak euro has

affected earnings negatively, while the

weak dollar has contributed to a positive

effect. The operational result for the

business for the first quarter is SEK -62

million (-63).

Despite the difficult market, the first quarter results

is in line with last year, though slightly worse than

expected. This means that despite an unimproved

result, costs have been cut and market shares are

won. Activities to further increase focus on

customers and sales are ongoing in parallel with

efficiency and cost-cutting measures which include

reflagging, bunker savings, changed crew policy

and consolidation of offices.

RoRo

Regular services have been conducted between

Finland and Sweden / Germany / Belgium with four

lines, TransLumi Line (TLL), TransBothnia Line

(TBL), TransFeeder North (TFN) and TransBothnia

Container Line (TBCL). TBCL, acquired in 2012,

has been integrated and further enhanced the

business area's offering in the Gulf of Bothnia. The

division's volumes declined during the quarter due

to the prevailing economic conditions. Focused

sales aktivities has resulted in new business that

has partially offset the volume decline within the

existing customer base.

Container

The container-based shipping route to England,

(TransPal Line) and feeder traffic to Germany

(TransFeeder South) experienced a mild winter but

economic conditions, combined with excess

capacity has affected the division lines negatively

through lower freight rates and lower volumes.

Bulk

The weak market with declining freight rates has persisted from the previous year in both large bulk and small bulk segments. The ice-classed vessels have not seen the premier freight rates, which have been customary in previous years, partly because of the late and relatively mild winter.

During the next quarter beneficial effects of

accelerated growth and cost improvement initiatives

is expected although the continued weak market

with low demand is likely to partially counteract the

impact of those initiatives.

Industrial Shipping

SEK M 2013 2012 2012

Net sales 489 648 2 212

Result before capital costs, EBITDA -44 -27 -125

Operational result -62 -63 -208

Profit margin -12.7% -9.7% -9.4%

January-March Full year

0

200

400

600

800

Q22011

Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Net Sales Industrial Shipping, SEK M

-80

-60

-40

-20

0

Q22011

Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Operational result, Industrial Shipping, SEK M

Report Q1 2013, January - March

page 7/18

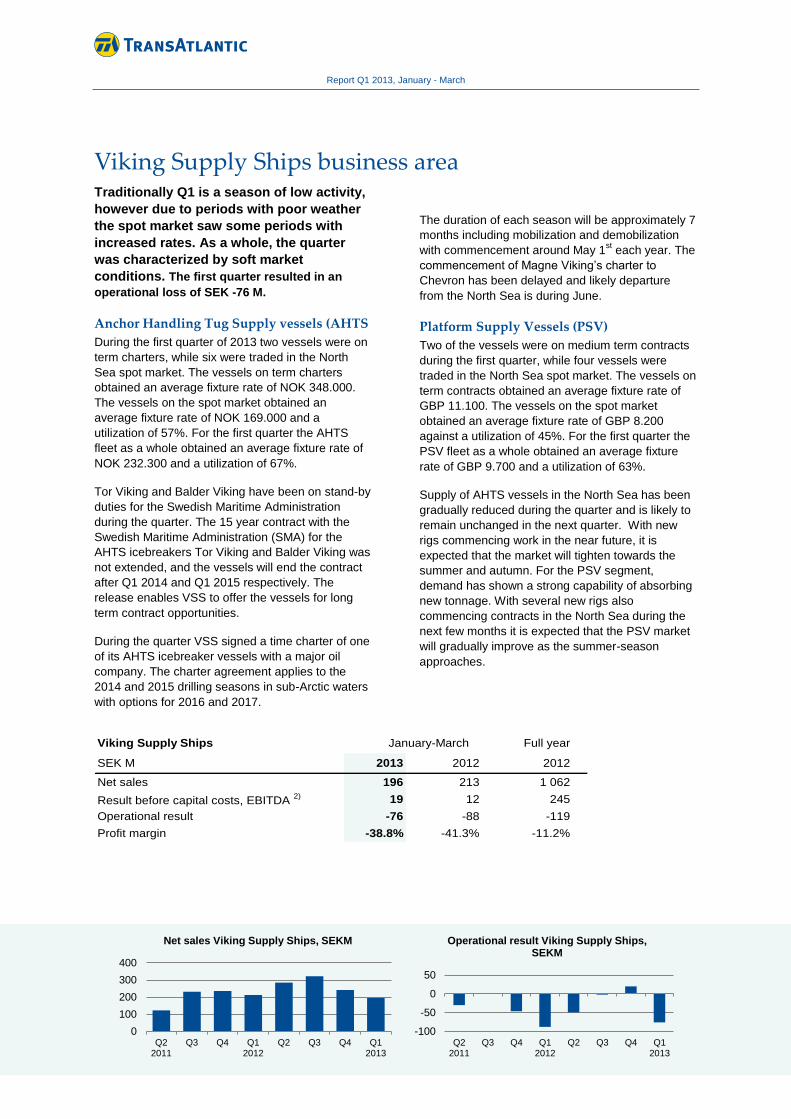

Viking Supply Ships business area Traditionally Q1 is a season of low activity,

however due to periods with poor weather

the spot market saw some periods with

increased rates. As a whole, the quarter

was characterized by soft market

conditions. The first quarter resulted in an

operational loss of SEK -76 M.

Anchor Handling Tug Supply vessels (AHTS

During the first quarter of 2013 two vessels were on

term charters, while six were traded in the North

Sea spot market. The vessels on term charters

obtained an average fixture rate of NOK 348.000.

The vessels on the spot market obtained an

average fixture rate of NOK 169.000 and a

utilization of 57%. For the first quarter the AHTS

fleet as a whole obtained an average fixture rate of

NOK 232.300 and a utilization of 67%.

Tor Viking and Balder Viking have been on stand-by

duties for the Swedish Maritime Administration

during the quarter. The 15 year contract with the

Swedish Maritime Administration (SMA) for the

AHTS icebreakers Tor Viking and Balder Viking was

not extended, and the vessels will end the contract

after Q1 2014 and Q1 2015 respectively. The

release enables VSS to offer the vessels for long

term contract opportunities.

During the quarter VSS signed a time charter of one

of its AHTS icebreaker vessels with a major oil

company. The charter agreement applies to the

2014 and 2015 drilling seasons in sub-Arctic waters

with options for 2016 and 2017.

The duration of each season will be approximately 7

months including mobilization and demobilization

with commencement around May 1st each year. The

commencement of Magne Viking’s charter to

Chevron has been delayed and likely departure

from the North Sea is during June.

Platform Supply Vessels (PSV)

Two of the vessels were on medium term contracts

during the first quarter, while four vessels were

traded in the North Sea spot market. The vessels on

term contracts obtained an average fixture rate of

GBP 11.100. The vessels on the spot market

obtained an average fixture rate of GBP 8.200

against a utilization of 45%. For the first quarter the

PSV fleet as a whole obtained an average fixture

rate of GBP 9.700 and a utilization of 63%.

Supply of AHTS vessels in the North Sea has been

gradually reduced during the quarter and is likely to

remain unchanged in the next quarter. With new

rigs commencing work in the near future, it is

expected that the market will tighten towards the

summer and autumn. For the PSV segment,

demand has shown a strong capability of absorbing

new tonnage. With several new rigs also

commencing contracts in the North Sea during the

next few months it is expected that the PSV market

will gradually improve as the summer-season

approaches.

Viking Supply Ships

SEK M 2013 2012 2012

Net sales 196 213 1 062

Result before capital costs, EBITDA 2) 19 12 245

Operational result -76 -88 -119

Profit margin -38.8% -41.3% -11.2%

January-March Full year

0

100

200

300

400

Q22011

Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Net sales Viking Supply Ships, SEKM

-100

-50

0

50

Q22011

Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Operational result Viking Supply Ships, SEKM

Report Q1 2013, January - March

page 8/18

Parent company

Earnings and financial position

The Parent Company’s result before tax for the

quarter amounted to SEK -40 M (67). The result

after tax for the period amounted to SEK -40 M (76).

The Parent Company’s total assets amounted to

SEK 2 567 M (2 607 on Dec 31, 2012). The

equity/assets ratio on the balance-sheet date was 74 %

(75 on Dec 31, 2012). Cash and cash equivalents at the

end of the period amounted to SEK 53 M (84).

Number of shares

Share distribution on March 31, 2013 is presented

below:

Number of Series A shares 7 271 842

Number of Series B shares, listed 103 630 858

Total number of shares 110 902 700

See also Changes in Group’s shareholders’ equity,

page 14.

Report Q1 2013, January - March

page 9/18

Other Corporate tax

The general situation for the Group is that taxes

payable are highly limited. Accordingly, recognized

corporate tax mainly comprises deferred tax. The

recognized net deferred tax asset for the Swedish

operations amounted by the end of the quarter to

SEK 74 M (74, on Dec 31, 2012). The recognized

deferred tax liability for the operations outside

Sweden amounted to SEK -11 M (-18, on Dec 31,

2012).

Transactions with closely related parties

Kistefos has, through an extended consulting

contract, been compensated for their management

work by the SEK 2 M paid for the period January-

March 2013.

TransAtlantic has during the quarter extended the

lease for a container ship, TransAlrek, owned by a

German shipping company, in which TransAtlantic's

Vice Chairman Folke Patriksson has a minority

interest via his company Enneff Rederi AB. The

agreement is on market terms and will run until

2014 with a quarterly rent for 2013 of SEK 3 M.

Vessel operations for three of the Group's Dutch-

owned ships is operated by an external company,

partly owned by Felix Feleus, who is also the CEO

of TransAtlantic Netherlands BV. Fees for vessel

operations are on commercial terms and amounted

to SEK 246 T for the three vessels during the

quarter. Agreement has been terminated and

ceased as of the end of March. There were no

other significant transactions.

Risks and uncertainties

TransAtlantic is a Group characterized by a high

degree of international operations, thereby exposed

to a number of operational and financial risks.

TransAtlantic works actively to identify, assess and

manage these risks. Risk management is included

as an element of the ongoing reviews of the

operations. The company’s liquidity is strained.

Accordingly, the company has defined and initiated

tangible measures to strengthen the company’s

profitability and liquidity. In parallel, active efforts are

in progress with banks to secure short and long-

term stable financing.

The 2012 Annual Report (page 20) includes a report

on the relevant risks facing TransAtlantic.

Accounting policies

This interim report, for the Group, was prepared in

accordance with the application of IAS 34 Interim

Financial Reporting and applicable rules in the

Swedish Annual Accounts Act and for the Parent

Company, in accordance with the Swedish Annual

Accounts Act and the Swedish Financial Reporting

Board’s recommendation FRF 2 Accounting for

Legal Entities. Unless otherwise noted, the same

accounting policies for both the Group and the

Parent Company have been applied as those used

in the most recent Annual Report.

The revised IAS 19, Employee Benefits, entered

into force on January 1, 2013, with retrospective

application. The biggest change is the option to

defer actuarial gains and losses using the corridor

approach disappears, they should on a current

basis instead be included in other comprehensive

income. Pension liabilities have been restated

accordingly and included debt has been reduced by

about SEK 2 M, with corresponding positive impact

on equity capital.

Viking Supply Ships will publish a separate report

which is demanded due to the issued bond. Some

values in that report are not comparable since there

are different acquisition values and depreciation

plans in VSS and the Group. VSS has from Q3 in

2011 been built through Group-internal transfers of

vessels and operations at then current marketing

prices, why disparities have arisen.

Number of employees

The number of employees in the Group at the end

of the year was 879 (2012-03-31: 967).

Events after the close of the reporting period

Birna Ödefors, currently Managing Director at CMA

CGM, has been appointed new CCO of

TransAtlantic, effective June 15, 2013.

Viking Supply Ships Ltd entering into a contract with

BP UK for two Platform Supply Vessels.

The Board of Directors decided to seek

shareholders’ approval for a capital increase

through a rights issue of SEK 150 M in order to

strengthen its short term funding and liquidity.

TransAtlantic was awarded a two-year contract

jointly with Outokumpu Stainless Oy and

Outokumpu Chrome Oy for transportation of both

import and export cargoes to and from the plant in

Tornio.

The Annual General meeting was held on April 24,

2013 at the Hotel 11, Eriksberg, Gothenburg,

Sweden.

Rederi AB TransAtlantic appointed Tomas

Bergendahl as CFO, effective from July 15, 2103.

Report Q1 2013, January - March

page 10/18

Press and analyst conference

In conjunction with the publication of the Q1-report

2013, an earnings call will take place on May 15,

2013 at 01.00 pm (GMT + 1) with TransAtlantic’s

CEO, Henning E. Jensen. In connection with the

conference, a presentation will be available at the

company’s website, www.rabt.se. Please see

Investor Relations/Q1 Report 2013.

This information is such that TransAtlantic is obligated to publish in accordance with the Swedish Securities Act

and/or the Swedish Financial Instruments Trading Act. This report has been prepared in both Swedish and

English versions. In case of variations in the content between the two versions, the Swedish version shall govern.

This report was submitted for publication at 8:30 a.m. on May 15, 2013.

The Board of Directors and the CEO confirm that the year-end report gives an accurate summary of the

Company’s and the Groups’ activities, position and results and describes the noteworthy risks and uncertainty

faced by the Company and companies that are includes within the Group.

Gothenburg, May 15, 2013

The Board of Directors of Rederi AB TransAtlantic

For further information, please contact Head of Corporate Communications Carina Dietmann +46 (0) 31-763 2334.

Financial calendar 2013 February 26 Year-end report 2012

April 24 Annual General Meeting

May 15 Interim report January – March

August 7 Interim report January-June

October 30 Interim report January – September

The Year-end report is available in its entirety on the company’s website.

Report Q1 2013, January - March

page 11/18

Full year

All amounts in SEK M 2013 2012 2012

Net sales 685 861 3 274

Other operating revenue 0 11 28

Direct voyage cost -355 -431 -1 489

Personnel costs -151 -164 -670

Other costs -197 -292 -1 024

Depreciation/impairment -60 -82 -263

Operating result -78 -97 -144

Net financial items -60 -35 -212

Result before tax -138 -132 -356

Tax on result for the period 1 0 -37

Result for the period -137 -132 -393

Attributable to:

Parent Company's shareholders -138 -133 -392

Non-controlling interests 1 1 -1

INCOME FOR THE PERIOD -137 -132 -393

Earnings per share, attributable to Parent Company's

shareholders, per share in SEK (before and after dilution) -1.2 -1.2 -3.5

Consolidated income statement

January - March

Full year

All amounts in SEK M 2013 2012 2012

Result for the period -137 -132 -393

Other comprehensive income for the period:

Change in hedging reserve, net 5 2 0

Change in translation reserve, net -134 -26 3

Other comprehensive income -129 -24 3

TOTAL COMPREHENSIVE INCOME FOR THE PERIOD -266 -156 -390

Total comprehensive income attributable to:

Parent Company's shareholders -266 -156 -387

Non-controlling interests 0 0 -3

TOTAL COMPREHENSIVE INCOME FOR THE PERIOD -266 -156 -390

Consolidated statement of comprehensive income

January - March

Full year

All amounts in SEK M 2013 2012 2012

Viking Supply Ships business area 196 213 1 062

Industrial Shipping business area 489 648 2 212

TOTAL NET SALES 685 861 3 274

Net sales by business area

January - March

Report Q1 2013, January - March

page 12/18

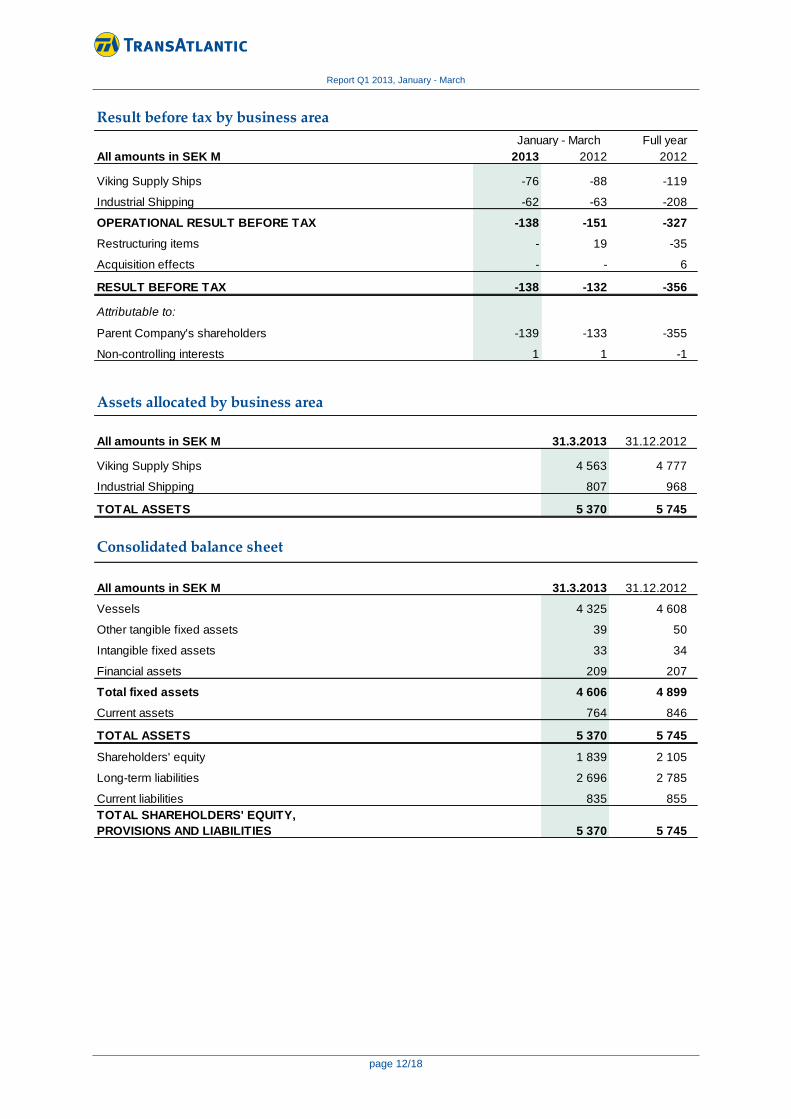

Full year

All amounts in SEK M 2013 2012 2012

Viking Supply Ships -76 -88 -119

Industrial Shipping -62 -63 -208

OPERATIONAL RESULT BEFORE TAX -138 -151 -327

Restructuring items - 19 -35

Acquisition effects - - 6

RESULT BEFORE TAX -138 -132 -356

Attributable to:

Parent Company's shareholders -139 -133 -355

Non-controlling interests 1 1 -1

Result before tax by business area

January - March

All amounts in SEK M 31.3.2013 31.12.2012

Viking Supply Ships 4 563 4 777

Industrial Shipping 807 968

TOTAL ASSETS 5 370 5 745

Assets allocated by business area

Consolidated balance sheet

All amounts in SEK M 31.3.2013 31.12.2012

Vessels 4 325 4 608

Other tangible fixed assets 39 50

Intangible fixed assets 33 34

Financial assets 209 207

Total fixed assets 4 606 4 899

Current assets 764 846

TOTAL ASSETS 5 370 5 745

Shareholders' equity 1 839 2 105

Long-term liabilities 2 696 2 785

Current liabilities 835 855

TOTAL SHAREHOLDERS' EQUITY,

PROVISIONS AND LIABILITIES 5 370 5 745

Report Q1 2013, January - March

page 13/18

The valuation of financial assets and liabilities in the balance sheet are based on aquisition value or fair value.

The valuation of FX derivatives and interest rate derivatives are based on fair value. The balance items

"Current assets" includes derivatives by SEK 5 M (0), "Long-term liabilities" by SEK 41 M (43) and

"Current liabilities" by SEK 0 M (2). Valuation of other financial assets and liabilities items in the balance sheets

are based on aquisition value.

The input used in the valuation of financial instruments base the three level classification:

Level 1, fair values based on market values, where the instruments are traded on an active market, are

available. Level 2, no market values based on an active market are available, valuations are instead based

on measurements of discounted cash flows. Level 3, at least one variable is based on own assessments.

The fair value valuation of the Group´s FX- and intrerest rate instruments are based on input according to level 2.

Valuation of financial assets and liabilities

Assessment of fair value of financial instruments

Full year

MSEK 2013 2012 2012

Cash flow from operations before changes in working

capital -88 -95 -119

Changes in working capital 63 -27 28

Cash flow from current operations -25 -122 -91

Cash flow from investing activities -19 -264 26

Cash flow from financing activities -7 315 -115

Changes in cash and cash equivalents -51 -71 -180

Cash flow at beginning of period 361 548 548

Exchange-rate difference in cash and cash equivalents -6 -2 -7

CASH AND CASH EQUIVALENTS AT END OF PERIOD 304 475 361

Consolidated cash-flow statement

January - March

Report Q1 2013, January - March

page 14/18

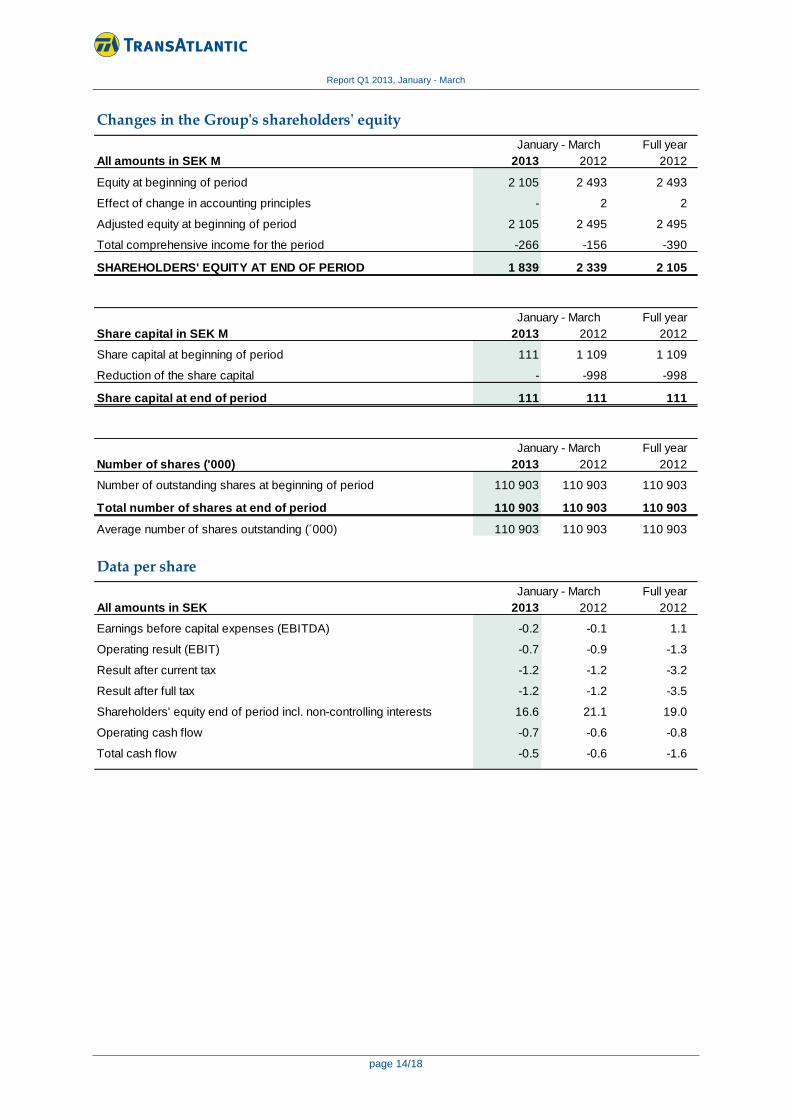

Full year

All amounts in SEK M 2013 2012 2012

Equity at beginning of period 2 105 2 493 2 493

Effect of change in accounting principles - 2 2

Adjusted equity at beginning of period 2 105 2 495 2 495

Total comprehensive income for the period -266 -156 -390

SHAREHOLDERS' EQUITY AT END OF PERIOD 1 839 2 339 2 105

Full year

Share capital in SEK M 2013 2012 2012

Share capital at beginning of period 111 1 109 1 109

Reduction of the share capital - -998 -998

Share capital at end of period 111 111 111

Full year

Number of shares ('000) 2013 2012 2012

Number of outstanding shares at beginning of period 110 903 110 903 110 903

Total number of shares at end of period 110 903 110 903 110 903

Average number of shares outstanding (´000) 110 903 110 903 110 903

January - March

Changes in the Group's shareholders' equity

January - March

January - March

Data per share

Full year

All amounts in SEK 2013 2012 2012

Earnings before capital expenses (EBITDA) -0.2 -0.1 1.1

Operating result (EBIT) -0.7 -0.9 -1.3

Result after current tax -1.2 -1.2 -3.2

Result after full tax -1.2 -1.2 -3.5

Shareholders' equity end of period incl. non-controlling interests 16.6 21.1 19.0

Operating cash flow -0.7 -0.6 -0.8

Total cash flow -0.5 -0.6 -1.6

January - March

Report Q1 2013, January - March

page 15/18

Full year

2013 2012 2012

Earnings before capital expenses (EBITDA) SEK M -18 -15 120

Operating result (EBIT) SEK M -78 -97 -143

Shareholders' equity SEK M 1 839 2 337 2 105

Net indebtedness SEK M 2 556 2 916 2 623

Operating cash flow SEK M -79 -69 -94

Total cash flow SEK M -51 -71 -180

Return on capital employed % -6.3 -6.9 -2.7

Return on shareholders' equity % -27.9 -21.8 -17.1

Equity/assets ratio % 34.2 36.1 36.6

Debt/equity ratio % 139.0 127.7 124.7

Profit margin % -20.2 -15.3 -10.9

Key data

January - March

Full year

All amounts in SEK M 2013 2012 2012

Net sales 283 292 1 247

Other operating revenue 0 11 18

Direct voyage costs -136 -135 -486

Personnel costs -42 -44 -166

Other costs -147 -147 -695

Depreciation/impairment -1 -1 -3

Operating result -43 -24 -85

Net financial items 3 91 -126

Result before tax -40 67 -211

Tax on result for the year 0 9 -67

RESULT FOR THE PERIOD -40 76 -278

Other comprehensive income - - -

TOTAL COMPREHENSIVE INCOME FOR THE PERIOD -40 76 -278

Parent Company income statement

January - March

Report Q1 2013, January - March

page 16/18

All amounts in SEK M 31.3.2013 31.12.2012

Tangible fixed assets 3 3

Intangible fixed assets 22 23

Financial fixed assets 2 819 2 793

Total fixed assets 2 844 2 819

Current asstes 620 647

TOTAL ASSETS 3 464 3 466

Shareholders' equity 2 567 2 607

Provisions 7 7

Longterm liabilities 593 584

Current liabilities 297 268

TOTAL SHAREHOLDERS' EQUITY,

PROVISIONS AND LIABILITIES 3 464 3 466

Parent Company balance sheet

Full year

All amounts in SEK M 2013 2012 2012

Shareholders' equity at beginning of period 2 605 2 883 2 883

Effect of change in accounting principles 2 2 2

Adjusted equity at beginning of period 2 607 2 885 2 885

Total comprehensive income for the period -40 76 -278

SHAREHOLDERS' EQUITY AT END OF PERIOD 2 567 2 961 2 607

January - March

Changes in Parent Company's shareholders' equity

Report Q1 2013, January - March

page 17/18

Definitions Capital employed

Interest-bearing liabilities and shareholders’ equity.

Debt/equity ratio

Interest-bearing liabilities minus cash and cash

equivalents divided by shareholders’ equity.

Disinvestment

Divestment of fixed assets.

Dividend yield

Dividend per share divided by the closing share

price at year-end.

Earnings per share

Profit after financial items less 1) current tax, 2) tax

on profit for the year (current and deferred tax) in

accordance with the consolidated income

statement.

EBIT

Earnings before interest and taxes, corresponding

to operating profit/loss.

EBITDA

Earnings before interest, taxes, depreciation and

amortization, corresponding to profit/loss before

capital expenses and tax.

Equity/assets ratio

Shareholders’ equity divided by total assets.

Equity per share

Equity divided by the number of shares outstanding.

Hedging

A general term for financial measures taken to avoid

undesirable effects on earnings due to variations in

interest rates, exchange rates, etc.

IFRS

International Financial Reporting Standards – an

international accounting standard used by all listed

companies. Some older standards included in IFRS

include IAS (International Accounting Standards).

Interest coverage ratio

Operating profit/loss before depreciation plus

interest income divided by interest expense.

Net indebtedness

Interest-bearing liabilities less cash and cash

equivalents.

Operating cash flow

Profit/loss after financial income/expense adjusted

for capital gains/losses, depreciation/amortization

and impairment.

Operating profit/loss (before tax)

Profit/loss before tax and before restructuring costs.

Operational profit/loss per business area

Profit/loss after financial items and before Group-

wide expenses and central/Group-wide net financial

income/expenses.

Operating profit/loss

Profit/loss before financial items and tax, and before

restructuring costs.

Profit margin

Profit after financial items divided by net sales.

Return on equity

Profit after financial items less tax on profit for the

year, divided by average shareholders’ equity.

Return on capital employed

Profit before depreciation and amortization (EBIT)

divided by average capital employed.

Restructuring costs

Includes revenues and expenses of a non-recurring

nature, such as capital gains/losses from the sale of

vessels, impairment of vessels and costs related to

personnel cutbacks.

Share of interest-bearing capital

Equity and deferred tax (including minority share)

divided by total assets.

Total cash flow

Cash flow from operating activities, investing

activities and financing activities

Report Q1 2013, January - March

page 18/18

Rederi AB TransAtlantic (RABT) is a leading Swedish

shipping company with headquarters in Gothenburg,

Sweden, and additional offices in Europe. TransAtlantic is

organized into two business areas: Industrial Shipping and

Viking Supply Ships. Viking Supply Ships, which is active in

offshore and icebreaking, is also a wholly owned subsidiary

of RABT. The Industrial Shipping business area consists of

three divisions: Bulk, Container and RoRo. The Group has

about 800 employees and generated sales of SEK 3,274 M

in 2012. The company’s Series B shares are listed on the

NASDAQ OMX Stockholm, Small Cap segment.

www.rabt.com

Rederi AB TransAtlantic (publ) Visiting address: Lindholmsallén 10 Box 8809, SE-402 71 Gothenburg, Sweden Tel: +46 31–763 23 00 E-mail: [email protected] www.rabt.com