delegated asset management in the era of big data

TRANSCRIPT

Delegated Asset Management in the Era of Big Data∗

Ye Li† Chen Wang‡

May 31, 2018

Abstract

Taking advantage of big data, professional asset managers increasingly use nonlinear

techniques, such as machine learning, to forecast the full distribution of asset returns

rather than form a simple point estimate. We provide the first theoretical framework

that features this most general form of asset managers’ skill – the knowledge of true

probability distribution of asset returns. In contrast, investors face model uncertainty.

The equilibrium level of delegation depends on model uncertainty, and the cross-section

variation of asset returns are driven by a CAPM component and an alpha, which con-

stitutes of a model-uncertainty beta and an equilibrium price of uncertainty depending

on delegation. Interestingly, we show that even if delegation approaches 100% (e.g.,

driven by declining costs of asset management), the alpha of certain assets never dis-

appears because of investors’ model-hedging motive that increases in delegation and is

unique to our setup. Our model also resolves several puzzles in the literature of asset

management, such as delegation in spite of underperformance. We provide evidence

consistent with the model’s implications on delegation and asset pricing.

∗We would like to thank Andrew Ang, Nick Barberis, Patrick Bolton, Stefano Giglio, Lars Peter Hansen,Gur Huberman, Michael Johannes, Tano Santos, Jose A. Scheinkman, Andrei Shleifer, and Zhenyu Wangfor helpful comments. All errors are ours.†The Ohio State University. E-mail: [email protected]‡Yale School of Management. E-mail: [email protected]

1 Introduction

The era of big data is defined by exploding data sources and increasingly sophisticated

techniques for data processing. The asset management industry has been revolutionized by

such developments. For example, nonlinear models, such as machine learning, have gained

tremendous popularity. Equipped with these new toolkits, asset managers no longer operate

upon a simple return signal as traditionally modeled in the literature, but rather possess

superior knowledge of the full probability distribution of asset returns. This paper provides

a new analytical framework that accommodates this most general form of skill, and explores

its unique implications on delegation and the cross section of asset returns.

The model structure is simple. There are two types of agents: homogeneous managers

and homogeneous investors. The former observe the true probability distribution of asset

returns, but the latter do not, and they make decisions under model uncertainty (or “am-

biguity”) given by a set of possible probability distributions (“models”). Investors may pay

a fee and delegate part of their wealth to be allocated by managers, while manage the re-

tained wealth on their own under ambiguity.1 The equilibrium asset prices are determined by

equating the exogenous supply of assets to the aggregate demand of managers and investors.

We highlight that the difference between professional asset managers and ordinary

investors is on the knowledge of return distribution. Traditional models are nested as special

cases because they assume that managers observe a signal on realized returns, which is

essentially better knowledge of the first moment (i.e., expected asset returns). Our setup is

motivated by the fact that gathering and processing big data is increasingly a specialized

task. Accordingly, we assume that managers cannot directly inform investors their knowledge

of return distribution, as in reality, it is often difficult for managers to explain to investors

the economic rationale and statistical techniques behind investment strategies.2

We provide closed-form results on delegation and cross-section of asset returns by

solving a quadratic approximation of investors’ preference under model uncertainty.3 Our

approximation extends that of Maccheroni, Marinacci, and Ruffino (2013) into functional

1The fee may represent a concrete management fee, agency cost, screening cost, or the relative bargainingpower of investors over managers.

2Our setup is a special case of model uncertainty in a multi-agent environment studied by Hansen andSargent (2012) – one type of agents, managers, do not face model uncertainty, while the other type do andthey know that managers know the true return distribution.

3We assume smooth ambiguity aversion utility function proposed by Klibanoff, Marinacci, and Mukerji(2005) and examined by Epstein (2010) and Klibanoff, Marinacci, and Mukerji (2012).

1

spaces, and nests theirs as a special case. We also show that our solution of investors’

optimal portfolio nests current asset pricing models with ambiguity aversion as special cases,

and when delegation is unavailable and investors are ambiguity-neutral, our portfolio solution

collapse to the mean-variance portfolio of Markowitz (1959).

In out setup, a key feature of delegated allocation is that whichever probability model

is true, the manager knows it and dutifully allocates the delegated wealth according using

the corresponding efficient portfolio. Therefore, in investors’ mind, the return on the dele-

gated part of wealth is model-contingent.4 Mathematically, the delegated portfolio chosen

by managers is a mapping from the space of possible probability distributions to the space

of portfolio-weight vectors. Put in even simpler terms, investors view managers as portfolio

formation machines, with the knowledge of true return distribution as inputs and a vector of

portfolio weights as outputs.5 In contrast, investors’ retained wealth is only state-contingent

– its return is determined when a state of the world is realized, but the probability distribu-

tion is unknown. Investors’ own portfolio weights are recorded in a constant vector, chosen

to be robust to the whole set of possible distributions (“models”).

The model-contingent nature of delegation has two consequences. First, it improves

investors’ welfare. Investors’ optimal level of delegation depends on the model uncertainty

they face, the cross-model variation of efficient frontier, management fee, and preference

parameters, such as risk aversion and ambiguity aversion. We measure investors’ model un-

certainty by the Bayesian posterior from a latent factor model of stock returns that captures

key features of returns uncovered in the literature. Given the measured uncertainty, the

model-implied delegation has 19% correlation with its empirical counterpart.

This view on delegated asset management can easily explain several puzzles in the em-

pirical literature, such as delegation in spite of underperformance relative to indices. First,

asset managers can be skilled in knowing higher moments instead of the expected return.

Therefore, it is not necessary that ex post, we observe outperformance. Second, investors

cannot evaluate fund performances ex ante under rational expectation, so econometricians’

ex post performance measurements are based upon an information set different from in-

4In effect, we can treat ambiguity as an imaginary first stage where the probability distribution of assetreturns is randomly decided according to the investors’ prior over alternative probability models. Assetreturns are realized in the second stage. When making decisions, the investors cannot observe the first-stageoutcome (which probability model is true), but the fund managers can. In this way, delegated portfoliomanagement makes the market more complete by allowing investors to take model-contingent claims.

5We do not introduce frictions such as moral hazard, asymmetric information on managers’ type etc.

2

vestors’. The extent to which delegation improves welfare depends on the subjective set

of candidate probability models that investors entertain. We characterize conditions un-

der which delegation arises even though managers may underperform the market, deliver

negative alpha, or simply hold a portfolio proportional to the market portfolio.

The second consequence of model-contingent allocation through delegation is the in-

duced model-hedging motive of investors. Across candidate probability models, asset returns

vary with the delegation (i.e., frontier) return. Investors are averse to such cross-model co-

movement, and in their own allocation of retained wealth, they hedge such comovement by

overweighting assets that tend to move against the delegation return, and underweighting

assets that tend to move with the delegation return across candidate models.

Such a hedging motive has critical asset pricing implications. The equilibrium expected

returns of assets have a two-factor structure: a typical CAPM risk premium, and an model-

uncertainty premium (“alpha”). Alpha arises because asset returns’ cross-model comovement

with the frontier is priced in the cross section, and intuitively, the price of model uncertainty

depends on delegation. We would expected the alpha to disappear if the economy approaches

full delegation (e.g., driven by declining asset management fees), that is when rational-

expectation managers almost dominate the asset market, and investors’ participation is

almost zero. However, the alpha of certain assets never shrinks to zero. The more investors

delegate (and less wealth they manage on their own), the stronger model-hedging motive

they have. The increasing hedging motive counter-balances the decreasing fraction of wealth

managed by investors under model uncertainty, which sustains the alpha. Therefore, our

model offers an explanation on why certain investment strategies (e.g., “factors” in the stock

markets) still deliver alpha in spite of the growth of professional asset management.

We test the asset pricing implications of our model in the space of U.S. stock market

factors. We focus on factors rather than individual stocks because diversifiable (idiosyncratic)

risks should not matter for investors’ decisions under any probability distribution. First, we

test whether managers have better knowledge of return distribution. If they do, we should

observe their portfolio tilt towards factors with superior expected return. Every quarter,

we sort factors by the fund ownership (adjusted to match its theoretical counterpart in our

model). Factors with high fund ownership consistently outperform those with low fund

ownership. Parametric tests based on factor return prediction support this finding of factor

timing. A one standard deviation increase of fund ownership adds 1.76% (annualized) to a

3

factor’s future return, which translates to a 53% increase over the average factor return in

our sample. Next, we find that in spite of the strong growth of delegation in the past few

decades, the portfolio of factors with high fund ownership exhibits robust alpha, which is

consistent with our prediction that investors’ model-hedging motive sustains the alpha for

certain assets even though wealth managed under ambiguity declines and delegation rises.

Literature. Our paper fits into a broader literature of ambiguity and ambiguity aversion

(or “robustness” in Hansen and Sargent (2016)).6 Ambiguity (also called “Knightian uncer-

tainty”) is the lack of knowledge of probability distribution and can interpreted as model

uncertainty or uncertainty over specific parameters.7 Ellsberg paradox is one of the most

salient examples that demonstrate ambiguity-averse behavior. A version of it was noted con-

siderably earlier by John Maynard Keynes in his book ”A Treatise on Probability” (1921).

Widely cited as a fundamental challenge to the expected utility theory, ambiguity aversion

has been applied in various fields in economics and finance, especially asset pricing (See Gar-

lappi, Uppal, and Wang (2007), Kogan and Wang (2003), Maenhout (2004), Ju and Miao

(2012) among others). Epstein (2010) and Guidolin and Rinaldi (2010) review the literature.

This paper contributes to the literature of asset pricing theories by offering an al-

ternative decomposition of equilibrium expected return, and show that the price of model

uncertainty depends on the endogenous level of delegation. Moreover, we identify a set of

assets (or factors) whose CAPM alpha is robust to the growth of professional asset man-

agement industry. The empirical study in our paper show strong results of factor timing by

institutional investors, which contributes to the empirical asset pricing literature.

There are many ways to formalize ambiguity and ambiguity aversion.8 We adopt the

smooth ambiguity averse utility function proposed by Klibanoff, Marinacci, and Mukerji

(2005) because it separates ambiguity from ambiguity aversion (the attitude towards ambi-

guity). We show that our results hold even when investors are not ambiguity-averse but face

ambiguity. In contrast to existing literature on asset pricing under ambiguity, in our setup,

6Another related literature studies the “uncertainty shock” and its implications on macroeconomics, forexample Bloom (2009) among others.

7See Knight (1921) for Knight’s well-known distinction between risk (situations in which all relevant eventsare associated with a unique probability assignment) and uncertainty (situations in which some events donot have an obvious probability assignment).

8Camerer and Weber (1992), and Wakker (2008) have an explicit focus on defining ambiguity, ambiguityaversion, and how to best model such preferences, with a special focus issues of axiomatization of the resultingcriteria and preferences.

4

ambiguity-neutral investors cannot simply perform Bayesian model-averaging (i.e., operate

upon a probability distribution that averages over candidate probabilities for each state of the

world). This is precisely because delegation makes return on wealth both state-contingent

and model-contingent. Therefore, we are the first to show that delegation arises endoge-

nously due to agents’ model uncertainty, and at the same time, delegation fundamentally

changes how model uncertainty enters into agents’ decision.

Since Jensen (1968), a large literature has documented that active portfolio managers

fail to outperform passive benchmarks or to deliver “alpha” to investors.9 Fama and French

(2010) find that the aggregate portfolio of actively managed U.S. equity mutual funds is

close to the market portfolio, and very few funds produce sufficient benchmark-adjusted

returns to cover their costs. Nevertheless, the asset management sector has been growing

dramatically in the past few decades. This paper proposes an alternative perspective to

understand these puzzling findings by highlight investors’ model uncertainty in decision

making. We characterize explicitly the conditions under which fund managers underperform,

deliver negative alpha after fess, and hold portfolio proportional to the market portfolio.

2 Model

2.1 Model setup

Consider a two-period economy where agents make decisions on in the first period, and asset

returns are realized in the second and final period. There are N risky assets, whose returns

are stacked in a vector r = riNi=1, and one risk-free asset that delivers a risk-free return rf .

Define Ω as the set of states of the world, so the vector of asset returns is a mapping from

state space to real numbers, r : Ω 7→ RN .

There are a unit mass of homogeneous investors, and a unit mass of homogeneous fund

managers. To simplify the exposition, we assume that each investor is matched with one

fund manager, but we show that our results can be extended to more general settings.

Model uncertainty and preference. A representative investor is endowed with one unit

of wealth. She chooses δ, which is the fraction of wealth invested in the fund. We specify the

9See Barras, Scaillet, and Wermers (2010), Carhart (1997), Del Guercio and Reuter (2014), Fama andFrench (2010), Gruber (1996), Malkiel (1995), Wermers (2000), among others.

5

delegation return later after laying out the investor’s information set, belief, and preference.

The investor also chooses her own allocation of retained wealth, wo (“o” for “own”), a column

vector of portfolio weights on the N risky assets. The investor does not know the return

distribution, so she has to form her own portfolio under ambiguity or model uncertainty.

Throughout this paper, ambiguity and model uncertainty are used interchangeably.

Model uncertainty is given by ∆, a non-singleton set of candidate probability distribu-

tions of r (“models”). For a probability measure Q ∈ ∆, the investor assigns a prior π (Q),

which is the subjective probability that Q is the true model.

The investor’s preference is represented by the smooth ambiguity-averse utility function

in Klibanoff, Marinacci, and Mukerji (2005) (“KMM”). The purpose of using this specifica-

tion is to obtain a clean separation between ambiguity itself and the aversion to ambiguity.10

Utility is defined over the value of her terminal wealth, rδ,wo,wd , whose subscripts show the

dependence on the delegation level δ, the investor’s own portfolio wo, and the delegated

portfolio chosen by the fund manager wd (“d” for “delegated”):

V(rδ,wo,wd

)=

∫∆

φ

(∫Ω

u(rδ,wo,wd

)dQ (ω)

)dπ (Q) (1)

φ (·) and u (·) are strictly increasing functions and twice continuously differentiable. Con-

cavity of u (·) and φ (·) represent risk and ambiguity aversion respectively.

Delegation as model-contingent allocation. Fund managers’ preference is not modeled.

A representative manager does not make any decision other than constructing an efficient

portfolio under his knowledge of P , the true probability distribution of r. We may think of

a fund manager as a portfolio formation machine that creates a vector of portfolio weights

wd that achieves the efficient frontier (more details on wd later).

To access this “machine”, the investor pays an exogenous proportional fee ψ. In a

richer setting, ψ can be determined by the competition between fund managers, a manager’s

cost of effort or business operation, agency cost, and the his bargaining power relative to the

investor.

What can a fund manager offer? From the investor’s perspective, for any candidate

10Epstein (2010) has drawn the attention to the fact that KMM framework may imply counterintuitivebehaviors, but Klibanoff, Marinacci, and Mukerji (2012) have replied that those Ellsberg-style thoughtexperiments do not pose difficulty for the smooth ambiguity model.

6

model Q ∈ ∆, if Q is the true model, the fund manager delivers the corresponding efficient

portfolio wd (Q). In other words, what the investor has in mind is that with a chance of

π (Q), Q is the true model (i.e., Q = P ), and since the manager knows which model is true,

the delegated portfolio is the efficient portfolio under Q.

Delegation creates a model-contingent allocation of wealth. This can be clearly seen

as we write out the investor’s terminal wealth, i.e., the total return,

rδ,wo,wd = (1− δ)[rf + (r− rf1)T wo

]+ δ

[rf + (r− rf1)T wd (Q)

]= rf + (r− rf1)T

[(1− δ) wo + δwd (Q)

], Q ∈ ∆. (2)

The investor’s own portfolio is a N -dimensional vector, wo ∈ RN . In contrast, from the

investor’s perspective, the delegated portfolio is a mapping from the model space to real

numbers, r :∆ 7→ RN . When δ > 0, the total return rδ,wo,wd , is a mapping from the state

space and the model space, i.e., Ω × ∆, to R. This model-contingent property inherits

from the delegated portfolio wd (Q). If δ = 0, i.e. no delegation, the portfolio return is

rf + (r− rf1)T wo, which just a mapping from the state space Ω to R.

Under model uncertainty, asset managers improve investors’ ex ante welfare by offering

a technology to make model-contingent asset allocation. As in Segal (1990), we may treat

the model uncertainty as an imaginary first stage where the probability model has not yet

been drawn, so ambiguity can be understood as a type of market incompleteness. The

imaginary economy has two stages: (1) investors choose wo and δ but they cannot bet on

the realization of first-stage “states”, i.e, which probability model is true; (2) the probability

model is determined and observed by fund managers who allocate the wealth delegated

by investors. Asset management service reduces market incompleteness by offering model-

contingent allocations.

This is a very general view on delegated asset management and the skills of fund

managers. Typical models in the literature assume that fund managers observe predictive

signals. This is nested in our setup. Return signals simply bring a better estimate of

expected return and narrow the variance. Fund managers possess the knowledge of more

general aspects of return distribution. For example, Busse (1999) shows that mutual fund

managers are able to time market volatility, and Chen and Liang (2007) show the same for

7

hedge funds.11 Jondeau and Rockinger (2012) investigate further the economic value added

by forecasting up to the fourth moments of returns, which they call “distribution timing”.

We are the first to characterize fund managers’ skills in this most general form. As the

asset management industry increasingly leverages on big data and nonlinear data processing

techniques, such as pattern recognition by machine learning, it is important to model asset

management under this generic specification of managers’ knowledge on return distribution.

As will be shown later, this setup help resolve puzzles, such as delegation under negative

alpha and underperformance relative to indices, and generates a rich set of asset pricing

implications that are consistent with new evidence we provide on factor timing and alpha

evolution.

2.2 A quadratic approximation

To solve the investor’s delegation and portfolio allocation in closed forms, we approximate

the utility function in a quadratic fashion by extending the results of Maccheroni, Marinacci,

and Ruffino (2013) (“MMR”) into functional spaces. In this paper, we adopt their technical

regularity conditions. MMR’s approximation does not allow agents’ wealth to be model-

contingent. Model-contingent allocation through delegation is the key in our model. We will

show that our approximation nests MMR’s as a special case.

First, we define the certainty equivalent.

Definition 1 A representative investor’s certainty equivalent is defined by

C(rδ,wo,wd

)= υ−1

(∫∆

φ

(∫Ω

u(rδ,wo,wd

)dQ (ω)

)dπ (Q)

), (3)

where υ is a composite function υ = φ u.

Accordingly, we write the investor’s delegation and portfolio selection problem as follows:

maxwo,δ

C(rδ,wo,wd

)− ψδ

(4)

where the return on wealth, rδ,wo,wd , is both state- and model-contingent (Equation (2)).

11In line with the evidence, Ferson and Mo (2016) provide a framework to evaluate portfolio performancein both market timing and volatility timing.

8

The quadratic form is similar to the mean-variance preference but incorporates both

risk and ambiguity. The risk aversion and ambiguity aversion are defined in a small neigh-

borhood of the total return on wealth around rf .

Definition 2 At risk free return rf , the local absolute risk aversion γ is defined as

γ = −u′′ (rf )

u′ (rf )(5)

and marginal-utility-adjusted local ambiguity aversion θ is defined as

θ = −u′ (rf )φ′′ (u (rf ))

φ′ (u (rf ))(6)

Before the quadratic representation of investors’ preference, we introduce notations:

• Define Q as the “average model”. For an event A ⊂ Ω, Q (A) =∫A⊂∆

Q (A) dπ (Q).

• Define q as the Radon-Nikodym derivative of Q w.r.t. Q, i.e., q (ω) = dQ(ω)

dQ(ω)for ω ∈ Ω.

q and Q are used interchangeably to represent a candidate probability model in ∆.

• Let Rw = (r− rf1)T w denote the excess return of portfolio w.

• Let RwQ = EQ

[(r− rf1)T w

]denote the expectation of excess return of w under Q.

• Given Q ∈ ∆, let EQ (X) and σ2Q (X) denote the expectation and variance of any

random variable X respectively, and µXQ and ΣXQ denote the vector of expectation and

the matrix of covariance of any random vector respectively.

• GivenQ ∈ ∆, the covariance of two random variablesX and Y is denoted by covQ (X, Y ).

Quadratic Preference. Using the Taylor expansion in the functional space, we approxi-

mate the certainty equivalent as in Proposition 1. The proof uses the generalized Frechet

derivatives in the Banach spaces. Details are provided in the Appendix.

Proposition 1 (Quadratic Preference) The smooth ambiguity-averse preference over the

state- and model-contingent return, rδ,wo,wd, i.e. mappings from Ω×∆ to R, can be repre-

9

sented by the certainty equivalent, which has the following expansion:

C(rδ,wo,wd

)=rf + (1− δ)2Rwo

Q− (1− δ)2

2

(γσ2

Q

(Rwo)

+ θσ2π

(Rwo

Q

))+

δEπ

(R

wd(Q)Q

)− δ2

2

[γEπ

(σ2Q

(Rwd(Q)

))+ θσ2

π

(R

wd(Q)Q

)]− (θ + γ) (1− δ) δcovπ

(Rwo

Q , Rwd(Q)Q

)+R

(wo,wd

),

(7)

where R(wo,wd

)is a high-order term that satisfies lim(wo,wd)→0

R(wo,wd)‖(wo,wd)‖2 = 0.

If portfolios are diversified such that their matrix norm are close to zero, the residual

term can be ignored. We shall use the second-order approximation to represent preference.

The local quadratic approximation allows us to understand the investor’s preference

in a very intuitive manner. As previously defined, Rwo

Qis the expected excess return to her

own portfolio wo under the average model Q. An increases in Rwo

Qleads to higher utility,

but the sensitivity, (1− δ)2, decreases in the level of delegation δ. σ2Q

(Rwo)

is the variance

of excess return to the own portfolio under the average model Q. As a measure of risk

it decreases utility. The sensitivity to risk increases in γ, the parameter of risk aversion.

σ2π

(Rwo

Q

)measures model uncertainty. It is the cross-model variation of the mean excess

return, because Rwo

Q denotes the expected return on the investor’s retained wealth under a

particular model Q. The sensitivity to ambiguity increases in θ, the parameter of ambiguity

aversion. As δ increases, and thus, the retained wealth decreases, both sensitivities to risk

and ambiguity decline.

The delegation return enters into the utility in an intuitive manner. Eπ

(R

wd(Q)Q

)is

the expected excess return of the delegated portfolio, averaged over models under the prior

π,

Eπ

(R

wd(Q)Q

)=

∫Q∈∆

EQ

[(r− rf1)T wd (Q)

]dπ (Q) ,

where Rwd(Q)Q is the expected excess return of delegated portfolio if Q is the true model.

Utility increases in the cross-model average of expected return to delegation. σ2π

(R

wd(Q)Q

)measures the ambiguity in delegation return. It is a cross-model variance of expected excess

return, so it reduces utility, and its sensitivity increases in the level of delegation δ and

ambiguity aversion θ. Eπ

(σ2Q

(Rwd(Q)

))measures the risk in delegation return averaged

over models, because σ2Q

(Rwd(Q)

)is the variance of delegation return under a particular Q.

10

Intuitively, the sensitivity to delegation risk increases in risk aversion γ.

The terms discussed so far can be summarized into two categories. First, averaging

over models, what are the expected returns and return variances (“risk”). Second, the cross-

model mean and variance of the expected returns under a prior π over the model space ∆

(“ambiguity”). The quadratic approximation intuitively shows how the these statistics enter

into utility, and how the utility sensitivities depend on risk aversion, ambiguity aversion, and

the level of delegation.

The last term in the quadratic form deserves more attention. It is the cross-model co-

variance between the expected delegation return and the expected return on retained wealth.

Investors do not treat the delegation return and their own investment opportunity set sepa-

rately, but instead, they want to hedge the cross-model uncertainty. Specifically, if an asset

tends to deliver a higher expected return under models where the expected delegation return

is low, then investors would like to invest more in this assets. As long as δ is smaller than

one, even if the fund manager selects the efficient portfolio under each model, the investor

still faces the uncertainty that the delegation return varies across models, and thus, hedges

such uncertainty in her own allocation of retained wealth. covπ

(Rwo

Q , Rwd(Q)Q

)captures this

cross-model hedging motive.

This hedging term has a utility sensitivity that increases in both risk aversion γ and

ambiguity aversion θ. Holding γ and θ constant, the sensitivity is maximized at δ = 12.

Intuitively, the investor cares the most about the comovement between the delegation per-

formance and the return on her retained wealth, when she divides wealth 50/50. As will

be shown later, this hedging motive has critical implications on the equilibrium expected

returns of risky assets.

Our quadratic approximation nests MMR’s solution (when δ = 0, i.e., no delegation)

and the standard mean-variance preference (when δ = 0 and θ = 0, i.e., no delegation and

no ambiguity aversion) as special cases.

Corollary 1 Without delegation, i.e., δ = 0, the approximation degenerates to the quadratic

approximation of smooth ambiguity utility by Maccheroni, Marinacci, and Ruffino (2013):

C(rf + (r− rf1)T

[(1− δ) wo + δwd (Q)

])≈ rf +Rwo

Q− γ

2σ2Q

(Rwo)− θ

2σ2π

(Rwo

Q

). (8)

If δ = 0 and θ = 0, the quadratic form degenerates to the standard mean-variance utility

11

under the average model Q:

rf +Rwo

Q− γ

2σ2Q

(Rwo)

. (9)

Later, we show that the investor’s optimal portfolio choice wo nests MMR’s solution

of optimal portfolio and the mean-variance portfolio of ? as special cases.

Delegated portfolio. To derive the solution to the investor’s problem and equilibrium

asset pricing implications, we need to specify the delegated portfolio. In line Corollary 1,

the investor informs her risk aversion to the fund manager, and the manager forms the

mean-variance efficient portfolio given his knowledge of the true probability distribution of

r:

maxwd

(µrQ − rf1

)Twd − γ

2

(wd)T

ΣrQ

(wd)

where, as previously defined, µrQ and Σr

Q are the mean vector and covariance matrix of r

under probability measure Q. The delegated portfolio is model-contingent, wd : ∆ 7→ RN :

wd (Q) =(γΣr

Q

)−1 (µrQ − rf1

). (10)

What generates delegation is ambiguity, not the aversion. Even ambiguity-neutral

investors will choose to hire fund managers who deliver efficient allocations.

Even without ambiguity aversion (i.e., under linear φ (·)), as long as φ′ (·) > 0, the

investor always achieves higher utility by delegating asset allocation to a fund manager who

achieves efficient allocations for each candidate model (i.e., maximizing u (·) for each Q).

Under Gaussian asset returns and CARA u (·) with absolute risk aversion γ, wd (Q) is the

exact maximizer of u (·) for any given Q. Therefore, if the management fee ψ is equal to

zero, the optimal level of delegation is δ = 1.

2.3 Investor optimization

Investor portfolio choice. We solve the optimal level of delegation δ and portfolio wo

by maximizing the quadratic approximation given by Equation (7). Proposition 2 gives the

investor’s choice of own portfolio of risky assets, wo. Details are provided in the Appendix.

Proposition 2 (Investor portfolio under ambiguity & delegation) Given the optimal

12

level of delegation δ, the investor’s own portfolio of risky assets is given by

woδ =

(γΣr

Q+ θΣ

µrQπ

)−1

(µrQ− rf1

)− (θ + γ)

(δ

1− δ

)covπ

(µrQ, R

wd(Q)Q

)︸ ︷︷ ︸

ambiguity hedging demand

. (11)

If the investor could not delegate, i.e., δ = 0, and thus, has no access the model-

contingent allocation, her portfolio would be

wo0 =

(γΣr

Q+ θΣ

µrQπ

)−1 (µrQ− rf1

),

where the subscript “0” represent “zero” delegation. This is also MMR’s solution of ambi-

guity investor’s portfolio problem. ΣrQ

measures risk, the covariance matrix of asset returns

under the average model Q. It enters into the optimal portfolio scaled by γ, the parameter of

risk aversion. In contrast, ΣµrQπ is the cross-model covariance matrix of expected asset return

vector µrQ. It measures ambiguity. The optimal portfolio’s sensitivity to Σ

µrQπ depends on θ,

the parameter of ambiguity aversion. If θ = 0, the optimal portfolio becomes the standard

formula by ? under the average model, i.e.(γΣr

Q

)−1 (µrQ− rf1

). Without delegation,

ambiguity-neutral investors use Bayesian model averaging.

Given δ > 0, the portfolio exhibits a hedging demand from covπ

(µrQ, R

wd(Q)Q

), the

cross-model comovement between the expected excess returns of assets, µrQ, and the expected

excess return from delegation, Rwd(Q)Q . The investor knows that whichever model is true, the

fund manager must know it and construct the efficient portfolio accordingly, but the true

model is still unknown. Therefore, the investor must design her own portfolio in a way that

is ”robust” to such ambiguity. The higher the ambiguity aversion is, the more sensitive the

investor’s portfolio choice to this covariance term.

Even if we shut down ambiguity aversion (θ = 0), we still have the hedging demand,

which is −γ(

δ1−δ

)covπ

(µrQ, R

wd(Q)Q

), depending on the risk aversion parameter. Fund man-

agers select the mean-variance efficient portfolio for investors for each model, but the in-

vestors still have allocate the retained wealth. To do that, they must consider all the proba-

bility models and make their own portfolio robust to the cross-model variation in investment

opportunity set and delegated return. This cross-model hedging motive compromises the

risk management within each particular probability model, and thereby, higher risk aver-

13

sion makes investors more cautious to the cross-model covariance between asset returns and

delegation return.

Let covπ

(µriQ , R

wd(Q)Q

)denote the i-th element of covπ

(µrQ, R

wd(Q)Q

). It represents the

covariance between asset i’s expected return, µriQ , and the delegation return. When the

expected delegation return comoves with asset i’s expected return, i.e. covπ

(µriQ , R

wd(Q)Q

)>

0, the investor reduces investment in asset i, and when the comovement is large, the investor

would rather take a short position in i as a hedge. When asset i’s expected return moves

against the expected delegation return, i.e. covπ

(µriQ , R

wd(Q)Q

)< 0, the investor demands

more of asset i as if buying an insurance against model uncertainty. This hedging motive

will have critical implications on the equilibrium cross-section of expected asset returns.

Optimal delegation. The optimal fraction of wealth delegated to fund managers depends

on structure of investors’ ambiguity and delegation fee ψ.

Proposition 3 (Optimal Delegation given wo) Given the optimal portfolio wo, the in-

vestor’s optimal delegation level δ is given by the first order condition:

δ =Eπ

(R

wd(Q)Q

)−Rwo

Q− (θ + γ) covπ

(Rwo

Q , Rwd(Q)Q

)− ψ

Eπ

(R

wd(Q)Q

)−Rwo

Q− (θ + γ) covπ

(Rwo

Q , Rwd(Q)Q

)+ θσ2

π

(R

wd(Q)Q

) . (12)

δ = 1, only if the investor is ambiguity-neutral (θ = 0) and delegation is free ψ = 0.

The solution is very intuitive. If the investor can do well on her own, (i.e. high Rwo

Q),

delegation decreases. If the expected return on retained wealth Rwo

Q comoves closely with the

expected return on delegated wealth Rwd(Q)Q across models (i.e. high covπ

(Rwo

Q , Rwd(Q)Q

)),

delegation also decreases. The investor are averse to the cross-model comovement, as re-

flected in the choice of wo. Delegation will increase if the delegation return is expected to be

high across models (i.e. high Eπ

(R

wd(Q)Q

)), and if it does not fluctuate much across prob-

ability models (i.e. low σ2π

(R

wd(Q)Q

)). Note that the investor’s own portfolio wo depends

on δ, so Equation (12) only implicitly defines δ. The next corollary solves δ explicitly as a

function of the investor’s ambiguity structure and management fee.

14

Corollary 2 (Optimal Delegation) The investor’s optimal delegation level δ is given by

δ =Eπ

(R

wd(q)Q

)− (θ + γ)B − C − ψ

Eπ

(R

wd(q)Q

)+ θσ2

π

(R

wd(q)Q

)− (θ + γ)2A− 2 (θ + γ)B − C

, (13)

where

A =covπ

(µrQ, R

wd(q)Q

)T (γΣr

Q+ θΣ

µrQπ

)−1

covπ

(µrQ, R

wd(q)Q

), (14)

B =covπ

(µrQ, R

wd(q)Q

)T (γΣr

Q+ θΣ

µrQπ

)−1 (µrQ− rf1

), (15)

C =(µrQ− rf1

)T (γΣr

Q+ θΣ

µrQπ

)−1 (µrQ− rf1

). (16)

The solution in Equation (13) depends on complicated structure of the investor’s model

uncertainty that involves the cross-model mean and variance of expected delegation return

(i.e., the expected returns on the mean-variance frontier of candidate models) and the cross-

model comovement of delegation return and asset returns.

In the empirical section, we estimate a representative investor’s model uncertainty and

calculate the model-implied delegation under this general solution. Specifically, we show

that our model-implied δ is highly correlated with the data counterpart. But next, we

shall proceed to derive comparative statics and explore more economic intuitions under a

particular but intuitive structure of ambiguity.

Comparative statics under simplified ambiguity. In order to derive intuitive compar-

ative statics, we will make the following assumptions to simplify the structure of investors’

ambiguity.

Assumption 1 The investor knows the covariance matrix, ΣrP , for any model Q ∈ ∆.

Under this assumption and the quadratic approximation of investor preference, the

model uncertainty is only about the expected returns, which is captured by the subjective

covariance matrix of expected returns, ΣµrQπ , under investors’ prior π over candidate models.

This assumption is very intuitive. If the investor’s model uncertainty is from estimation

errors, the diagonal of ΣµrQπ represents the square of standard errors of the expected return

estimator. Following this interpretation, it is reasonable to add the following assumption.

15

Assumption 2 The investor’s subjective belief of expected return is given by a normal dis-

tribution, whose covariance is proportional to the true return variance:

µrQ ∼ N

(µrQ, υΣr

P

). (17)

Since µrQ ∼ N

(µrQ, υΣr

P

), υ that parameterizes the level of model uncertainty, which

can be easily understood as “parameter uncertainty” or “estimation error” when the in-

vestor tries to estimated the expected excess returns. The normality assumption of the prior

over µrQ also brings technical convenience. As shown in Appendix C, we can apply the Is-

serlis’ theorem to dramatically simplify ambiguity investors’ optimal delegation and portfolio

choice.

N(µrQ, υΣr

P

)is the popular conjugate prior. υ can be understood as the inverse of the

size of estimation sample, based on which the investor calculates the covariance matrix of

her estimator of expected excess return. A large value of υ reflects large estimation errors. If

the investor has T observations of r and she assumes the independence across observations,

the method-of-moment estimator of the expected return is 1T

ΣTt=1r and its covariance is 1

TΣrP .

This case directly maps to the assumption ΣµrQπ = υΣr

P with υ = 1T

. It is natural to assume

that υ < 1, because 1T< 1 for any sample size larger than one.

Assumption 3 υ < 1.

These assumptions highlight the link between volatility and ambiguity. When assuming

the covariance of asset returns are known to investors, larger volatility means the expected

returns are harder to estimate (higher parameter uncertainty). This model suggests that

delegation should also relate to the potentially time-varying uncertainty induced by the

evolution of asset return volatility. The case of known covariance and unknown expected

returns echoes the observation by Merton (1980). Kogan and Wang (2003) also consider this

case in their discussion of portfolio selection under ambiguity.

Using these assumptions, we solve explicitly the optimal delegation as a function of the

exogenous parameters, and simplifies the formula of optimal portfolio choice (details in the

Appendix). The solution is summarized in the following proposition for comparative statics.

Proposition 4 (Comparative Statics) Under the three assumptions, the investor’s port-

16

folio is given by

wo = (ΣrP )−1

(µrQ− rf1

)[ 1

γ + υθ− υ

(γ + θ

γ + υθ

)(δ

1− δ

)2

γ

]. (18)

The optimal delegation decision is

δ =

υγN − ψ +

[1− γ

γ+υθ

(2υ(θ+γ)

γ+ 1)]Rwd

Q(1 + 2 θυ

γ

)υγN +

[1 + 4 θυ

γ− γ

γ+υθ

(2υ(θ+γ)

γ+ 1)2]Rwd

Q

, (19)

where the expected return to the delegated portfolio under the average model Q is

Rwd

Q=(µrQ− rf1

)T(γΣr

P )−1(µrQ− rf1

).12 (20)

We have the following results of comparative statics:

1 The optimal level of delegation δ increases in N , the number of risky asset, and γ, the

risk aversion: ∂δ∂N

> 0, ∂δ∂γ> 0.

2 The optimal level of delegation δ decreases in θ, the ambiguity aversion, υ the level of

ambiguity, and ψ, the management free: ∂δ∂υ< 0, ∂δ

∂θ< 0, ∂δ

∂ψ< 0.

3 Given the delegation level δ, wo decreases in ambiguity aversion θ, the level of ambiguity

υ, ambiguity, and risk aversion γ: ∂wo

∂υ< 0, ∂wo

∂θ< 0, ∂wo

∂γ< 0, given δ.

4 When, N < 1υ

[(γ + θ + γ

2υ

)ψ + (θ − γ)Rwd

Q

], wo ≥ 0 if and only if µr

Q≥ rf1.

After applying the Isserlis’ theorem to simplify δ and wo (details in the Appendix),

a new summary statistic N , the number of assets, shows up. Intuitively, as the number of

risky assets increases, the fund manager’s ability to construct efficient portfolios of a large

set of assets is more valuable, so the delegation level increases. Delegation also increases in

risk aversion, because when risk aversion is high, a little bit away from the efficient frontier

significantly decreases the investor’ utility.

12A simple calculation shows that the formula produces reasonable level of delegation. δ equals 49% under

the following calibration: N = 10, γ = 5, θ = 1, Rwd

Q= 0.04, ψ = 0.01 and υ = 0.01. δ increases to 99%,

when N increases to 1000.

17

Note that we can interpret N as the number of risk factors instead of primitive risky

assets. Suppose there are infinite number of assets, whose returns are spanned by N risk

factors and their own idiosyncratic shocks. By law of large numbers, the investor can always

diversify away the idiosyncratic shocks at zero cost no matter what the underlying prob-

ability model is, provided that all the candidate probability measures are not point-mass.

Effectively, the portfolio selection problem is defined on the N risk factors. More sources of

risk (large N) motivates the investor to hire fund managers.

Holding constant the number of assets, delegation decreases in ambiguity aversion (θ)

and the level of ambiguity (υ), because the investor has to pay more attention to hedging

against the model uncertainty induced by cross-model variation in the delegation return,

which reduces benefits of delegation. A more uncertain environment tends to reduce delega-

tion.

The comparative statics on investor’s portfolio choice are derived conditional on the

delegation decision. The investor becomes more conservative in holding risky assets, when

facing more ambiguity, or under higher ambiguity aversion or risk aversion.

In reality, most investors hold long positions, while professional asset managers may

take short positions. In the model, the aggregate portfolio of ambiguity investors takes

all long positions, if under their average model, the expected excess returns are all positive

(µrQ≥ rf1). This result requires N to be lower than an upper bound given by the parameters.

As time goes, the number of assets tends to increase, so investors may hold aggregate short

positions in at least some of the risky assets. However, historic data accumulates, υ, the

estimation error or parameter uncertainty, tends to decrease, which raises the upper bound

of N . If we interpret N as the number of factors that generate undiversifiable risks, N is

likely to be a single-digit number. The upper bound of N that guarantees wo ≥ 0 when

µrQ≥ rf1 is equal to 272 under the following calibration: γ = 5, θ = 1, Rwd

Q= 0.04, ψ = 0.01

and υ = 0.01.

2.4 Cross-section asset pricing

We characterize the equilibrium expected returns on risky assets and their CAPM alpha.

First, we show that when delegation is unavailable, our model produces results that nest key

theoretical findings in the literature of asset pricing under ambiguity. Next, we show that

adding delegation significantly changes the reults.

18

Ambiguity gives rise to an ambiguity premium in the expected return, and the price

of ambiguity depends on the equilibrium level of delegation. In contrast to the existing

literature, such ambiguity premium does not disappear when investors are not ambiguity

averse. Also, if we consider a sequence of economy with increasing levels of delegation all

the way to 100%, the asset market equilibrium does not converge to CAPM (the equilibrium

when δ is exactly 100%). Such discontinuity suggests that in spite of the growth of asset

management industry, there shall always be deviation from CAPM and alpha to be earned.

The key economy mechanism behind these results is ambiguity investors’ motive to hedge

against model uncertainty.

To characterize the equilibrium expected return, we define the market portfolio m,

which is equal to the exogenous supply of risky assets. Market clearing conditions implies:

m = δwd (P ) + (1− δ) wo. (21)

Equilibrium without delegation. We first study the case when delegation is impossible.

Recall that wo0 is the “zero-delegation portfolio”, that is the ambiguity investor’s portfolio

when delegation is unavailable,

wo0 =

(γΣr

Q+ θΣ

µrQπ

)−1 (µrQ− rf1

)(22)

When δ = 0, using the market clearing condition, m = wo0, we solve the results under the

general form of ambiguity without imposing the three simplification assumptions.

Proposition 5 (Ambiguity Premium without Delegation) When delegation is unavail-

able (δ = 0), the equilibrium expected excess returns of risky assets are

µrP − rf1 =λmβ

Pr,m + λwo

0βπµrQ,m, (23)

if investors’ average model is the true model, i.e., Q = P , where we define

• market price of risk, λm = γσ2P (Rm), the risk beta, βPr,m = covP (r,Rm)

σ2P (Rm)

,

• market price of ambiguity, λwo0

= θσ2π

(RmQ

), the ambiguity beta, βπµrQ,m =

covπ(µrQ,RmQ )

σ2π(Rm

Q ).

19

Equation (23) decompose the expected excess return into two components. When the

ambiguity investors are the only market participants, the expected excess returns compensate

them for both their risk exposure and ambiguity exposure. The first component λmβPr,m is

exactly the standard CAPM beta multiplied by the market price of risk. The second term

λwo0βπµrQ,m is the product of the ambiguity beta and price of ambiguity.

The ambiguity beta measures the cross-model comovement between the expected asset

returns and the expected market return (i.e. the return of zero-delegation portfolio). If asset

i’s expected return comoves with the expected market return (i.e. βπµriQ ,m

> 0), the asset must

deliver a higher average return through λwo0βπµriQ ,m

> 0 in order to attract investors’ capital to

clear the market. If asset i’s expected return moves against the expected market return (i.e.

βπµriQ ,m

< 0), then it serves as hedge against model uncertainty from the ambiguity investor’s

perspective, and thus, it affords a discount in the average return via λwo0βπµriQ ,m

< 0.

Note that the assumption of Q = P is important. Investors face model uncertainty, so

they cannot evaluate the expected returns of risky assets under the true model P . Instead,

they examine the expected returns by averaging over candidates models, i.e., µrQ

. Only under

the assumption that Q = P , does investors’ average expected return µrQ

coincide with the

expected return under the true model µrP , and thus, can we solve µr

P from the optimality

condition of investors’ portfolio choice.

Ambiguity generates CAPM alpha as in Maccheroni, Marinacci, and Ruffino (2013).

In their paper, they analyze a special case where an ambiguity investor’s portfolio choice

when one asset is pure risk (whose distribution is known) while the other asset’s return is

ambiguous. Using the constrained robust approach, Kogan and Wang (2003) derive the sim-

ilar two-factor structure of equilibrium expected returns. Garlappi, Uppal, and Wang (2007)

extend the findings in Kogan and Wang (2003) using multiple-prior-preference approach. In

those models and here, if we shut down ambiguity aversion by setting θ equal to zero, the

price of ambiguity, λwo0

= θσ2π

(R

wo0

Q

), becomes zero, and the model degenerates to CAPM.

Corollary 3 (CAPM without delegation) When delegation is unavailable (δ = 0), if

investors are not ambiguity-averse (θ = 0), the equilibrium excess returns of risky assets are

µrP − rf1 = λmβ

Pr,m, (24)

if investors’ average model is the true model, i.e., Q = P .

20

If the investor is ambiguity-neutral, the investor’s utility function can be written as

V (r) =

∫∆

∫Ω

u (r) dQ (ω) dπ (Q) =

∫Ω

u (r)

[∫∆

dQ (ω) dπ (Q)

]=

∫Ω

u (r) dQ (ω)

which is simply the expected utility given the average probability model Q. Our quadratic

approximation becomes the standard mean-variance utility as shown previously, so if Q = P ,

we rediscover CAPM. It is critical that u (r) can be taken out of the integral operator∫

∆

because u (r), or equivalently r, only depends on the state ω, but not on the model Q. This is

in turn because delegation is unavailable, so ambiguity investors cannot make their portfolio

return model-contingent. Next, we will show that when delegation is available, the economy

still deviates from CAPM even when investors are not ambiguity-averse.

Equilibrium with delegation. When delegation is available, the market portfolio is a

mixture of fund managers’ portfolio and investors’ portfolio, i.e., m = δwd (P ) + (1− δ) wo,

the market clearing condition. To derive intuitive results and streamline the exposition, we

adopt the three assumptions to simplify the ambiguity structure. In the Appendix, we show

that the results hold under the general form of ambiguity. Here, to solve the expected returns

under the true model, µrP , we do not need to assume assume Q = P because µr

P already shows

up in fund managers’ portfolio (details in the Appendix). Substituting investors’ portfolio

in Equation (18) into the market clearing condition, we have the results.

Proposition 6 (Ambiguity Premium with Delegation) Under the simplified ambigu-

ity, the equilibrium expected excess returns of risky assets are

µrP − rf1 =

(λm

1

δ

)βPr,m +α, (25)

where λm and βPr,m are defined in Proposition 5. The CAPM alpha is

α =

(1

1 + υθ/γ

)[2υ

(1 +

θ

γ

)−(

1− δδ

)](µrQ− rf1

). (26)

Moreover, even when investors are not ambiguity-averse (θ = 0), the CAPM alpha still exists

and equals to

α =

(2υ + 1− 1

δ

)(µrQ− rf1

). (27)

21

The price of risk, λm1δ, decreases in the level of delegation. Therefore, the model

implies a declining market premium as the asset management sector grows, i.e., δ increase,

due to lower management fee or variation in the structure of investors’ model uncertainty.

α can be interpreted as compensation for ambiguity, and it increases in υ, the level of

ambiguity. When υ is small, which tends to be the case under the previous interpretation of

υ as the inverse of sample size, α decreases in µrQ− rf1, the expected excess returns under

investors’ average probability model Q. Intuitively, when the scenarios are better on average,

investors demand less compensation for ambiguity.

Interestingly, even when investors are ambiguity-neutral, the economy still deviates

from CAPM. This contrasts Corollary 3 that CAPM alpha disappears when θ = 0. In

equation (11), the cross-model covariance term is multiplied by both the ambiguity aversion

θ and the risk aversion γ. Through delegation, investors’ wealth becomes model-contingent,

so they have to make their own portfolio robust to the cross-model variation in the investment

opportunity set and the delegation return. This cross-model hedging motive compromises the

risk management within each particular model, and thereby, higher risk aversion contributes

to a stronger aversion to model uncertainty. Delegation induces such hedging motive, and

thus, links the required compensation for ambiguity to investors’ risk aversion.

This model-hedging motive also creates an equilibrium discontinuity. Consider a se-

quence of economies with increasing levels of delegation, which may be due to declining man-

agement fees or changes in the structure of investors’ ambiguity. Surprisingly, the limit of

this sequence is not CAPM. However, when δ is precisely equal to one, we have m = wd (P ),

and exactly the CAPM equilibrium

µrP − rf1 = βPr,mλm, (28)

where λm = Rwd

P = RmP .

Corollary 4 (Equilibrium Discontinuity with Delegation) As δ approaches 100%, the

equilibrium does not converge to the CAPM equilibrium:

limδ→1

α = 2υ

(1 + θ/γ

1 + υθ/γ

)(µrQ− rf1

). (29)

22

Even when investors are not ambiguity averse (θ = 0), we have

limδ→1

α (δ) =2υ(µrQ− rf1

). (30)

The ambiguity alpha is equal to zero only if ambiguity disappears, i.e., υ = 0, or the expected

returns of risky assets under investors’ average model coincides with those under the true

model, i.e., µrQ

= µrP . However, when δ = 100%, we have the exact CAPM equilibrium given

by Equation (28).

Even if fund managers, who behave as standard mean-variance agents, almost take over

the whole market, the equilibrium still deviates from CAPM. Therefore, we may observe an

increasing share of wealth delegated to professionals, CAPM alpha never goes away for

many assets. This result contributes to the literature of empirical asset pricing. The asset

management sector has grown dramatically in the past few decades in the U.S. stock market

(French (2008)). However, many “anomalies”, such as value premium, are still alive. It

is hard for asset pricing models to rationalize the “anomalies”. It is even more difficult to

reconcile the stationarity of ”anomaly” premia with a period of secular growth of professional

asset management that exploits such anomalies. This paper offers an alternative view based

on delegation under model uncertainty.

As δ increases, the standard risk premium approaches the CAPM counterpart. How-

ever, unless ambiguity disappear or investors fully refrain from the market, the ambiguity

premium never disappears. As approaches 100%, the model-hedging component of wo ex-

plodes. When investors delegate a larger share of their wealth to fund managers, they

become more sensitive to the cross-model variation of asset returns and delegation returns,

and therefore, hedge more. This hedging motive arises from the model-contingent allocation

through delegation.

2.5 Delegation and fund performance

The evidence on mutual funds underperformance suggests that investors might be better off

by refraining from delegation and holding the market portfolio instead. Therefore, it poses

a challenge to rationalize the existence of the active portfolio management industry.

By taking an ambiguity perspective on delegation, this paper shifts the focus from

ex post performance to ex ante welfare improvement, and reconciles the evidence on fund

23

performance with the growth of active asset management. The econometrics in ex post

measurement of performance assumes “large sample” and investors’ rational expectation.

However, investors face model uncertainty in reality, and cannot rely on such measurements

ex ante. Moreover, delegation arises the improvement in ex ante welfare from the access to

model-contingent allocation provided by asset managers. It is valuable no matter whether

funds outperform the market index or delivers alpha ex post. Next, we characterize the

conditions under which delegation arises in spite of underperformance or alpha.

Fund underperforming the market. Let us consider investing in the market index, and

compare the expected delegation return and the market return under the simplified structure

of ambiguity. Substituting the investor’s portfolio (equation (18)) into the expected market

excess return under P , we have

RmP = δR

wd(P )P + (1− δ)Rwo

P

= (µrP − rf1)T (γΣr

P )−1

[(µr

P − rf1) δ +(µrQ− rf1

)((1− δ) γ − δ2υ (θ + γ)

γ + υθ

)].

The expected excess return of the fund manager’s portfolio is

Rwd(P )P = (µr

P − rf1)T (γΣrP )−1 (µr

P − rf1)

The difference, Rwd(P )P −Rm

P , is equal to

(1− δ) (µrP − rf1)T (γΣr

P )−1

[(µr

P − rf1)−(µrQ− rf1

)(γ − ( δ1−δ

)2υ (θ + γ)

γ + υθ

)]. (31)

Proposition 7 (Underperformance) Under the three simplification assumptions, fund

managers underperform the market if

N∑i=1

wdi (P ) (µri

P − rf ) < κN∑i=1

wdi (P )

(µriQ− rf1

),

where wdi (P ) is the fund managers’ portfolio weight on asset i.

κ =γ −

(δ

1−δ

)2υ (θ + γ)

γ + υθ(32)

24

, increasing in θ and υ, and decreasing in γ.

Whether the fund managers underperform or outperform the market depends on the

comparison between the weighted average of assets’ expected returns under true model and

the weighted average of assets’ expected returns under the investors’ average model (scaled by

κ). Because ambiguity investors also participate in the market, fund managers’ performance

depends on their relative (to ambiguity investors) aggression in risk- and ambiguity-taking. If

investors have in mind a high-return market (i.e. high µrQ

), then they can be more aggressive

and beat fund managers by taking on more exposure to risk and ambiguity.

Next, holding constant∑N

i=1 wdi (P ) (µri

P − rf ) and∑N

i=1 wdi (P )

(µriQ− rf1

), and as-

suming both are positive, we see a higher κ leads to underperformance. As shown in the

Appendix, κ increases in θ and υ, and decreases in γ. The model implies the fund man-

agers are more likely to underperform the market when ambiguity investors have lower risk

aversion, higher ambiguity aversion, and face more ambiguity. This is consistent with the

comparative statics of wo. Under higher values of θ and υ, stronger motive to hedge the

cross-model comovement between the investment opportunity set and the delegation return,

which motivates investors to take more extreme direct positions. A decrease in γ also moti-

vates investors to increase direct holdings of risky assets.13

Investors delegate in spite of the underperformance, because they do not know the

probability distribution of the market return, and thus, cannot evaluate under the rational

expectation, whether fund managers are expected to under- or over-perform the market

index. Instead, investors delegate to maximize ex ante wealth under ambiguity.

Delegation without Alpha. Another commonly used performance metric is “alpha”. It is

defined as the average of residuals from regressing fund return on the market excess return.

Let us assume that µrQ

= µrP . In this case, investors’ portfolio is proportional to fund

managers’ portfolio (and the market portfolio)

wo = (ΣrP )−1 (µr

P − rf1)

[1

γ + υθ− υ

(γ + θ

γ + υθ

)(δ

1− δ

)2

γ

]. (33)

13This result echoes the observation made by De Long, Shleifer, Summers, and Waldmann (1990) thatirrational investors’ willingness to earn a risk premium may outweigh their inadequate knowledge of returndistribution and allow them to accumulate more wealth that rational investors (on average, by law of largenumbers).

25

Therefore, CAPM holds. A regression of fund managers’ excess returns on the market excess

returns will find exact zero alpha. In other words, fund managers basically holds the market

portfolio (up to a scaling factor).14

Proposition 8 (Zero Alpha Delegation) Under the three simplification assumptions and

given µrQ

= µrP , CAPM holds and the delegated portfolio delivers zero gross alpha and negative

alpha after fees.

Why investors invest a significant share of wealth in actively managed funds, in spite

of their underperformance and negative alpha after fees. This paper argues that under

ambiguity, they choose to delegate in order to improve ex ante welfare. Delegation essentially

provides access to achieve model-contingent allocation. In the investor’s mind, the delegated

wealth is optimally allocated on the efficient frontier under each probability model.

Ex post, econometricians cannot back out ambiguity investors’ optimal delegation

choice by simply looking at fund performance and asset returns, because ambiguity investors

do not have rational expectation. Data is generated only from true probability model, but

when making delegation and investment decisions, investors have to consider many the al-

ternative scenarios given the finite sample and their limited econometric skills.

Another interesting implication is that even if fund manager knows the true model,

this may not help them to generate “market risk-adjusted return”. This result challenges the

traditional approach of fund performance measurement: an asset management firm could be

“active” in acquiring the knowledge of true probability model, but this effort is not likely to

be compensated if we only look at the market-adjusted performance.

3 Evidence

In this section, we examine the empirical implications of the model. We use data from the

U.S. stock market, and consider investors’ investment opportunity set as a set of stock-market

factors instead of individual stocks, because idiosyncratic risks can be diversified away at

zero cost so they should not matter for investors’ evaluation of both risk and ambiguity.

First, we show that active fund managers exhibit knowledge of factor returns. Specifi-

cally, we show that at factor level, current ownership by active fund managers predicts future

14This scenario mirrors the empirical observation in the U.S. stock market that on average the fundmanagers hold the market portfolio (Lewellen (2010)).

26

factor returns. In other words, by having a better knowledge of expected factor return, active

fund managers are able to perform factor timing.

Second, we examine the model prediction that as the delegation level grows, CAPM

alpha does not disappear for a set of factors. We plot the faction of wealth in the U.S.

stock market managed in delegated portfolios, and the rolling-window CAPM alpha of a set

factors with high fund ownership. The former exhibits a stronger upward trend, but in spite

of this, the latter fluctuates and stays above zero consistently.

Finally, we simulate investors’ ambiguity by fitting a latent factor model of returns

to the commonly used size and book-to-market sorted portfolios. The model incorporate

time-varying expected return and time-varying covariance matrix. Ambiguity, measured by

the Bayesian posterior uncertainty, is directly plugged into the optimal delegation level in

the model. The model-implied delegation has a 19% correlation with the detrended data.

3.1 Data and variable construction

Factor construction. We consider the most widely studied stock-market factors docu-

mented by the empirical asset pricing literature. The factors are divided into two categories:

accounting-based and return-based. Accounting-based factors include value (“HML”), ac-

cruals (“ACR”), investment (“CMA”), profitability (“RMW”), and net issuance (“NI”).

Return-based factors include momentum (“MOM”), short-term reversal (“STR”), long-term

reversal (“LTR”), betting-against-beta (“BAB”), idiosyncratic volatility (“IVOL”), and to-

tal volatility (“TVOL”).

To construct each factor, we use monthly and daily returns data of stocks listed on

NYSE, AMEX, and Nasdaq from the Center for Research in Securities Prices (CRSP). We

include ordinary common shares (share codes 10 and 11) and adjust delisting by using CRSP

delisting returns. We obtain accounting data from annual COMPUSTAT files to compute

some of the firm characteristics. We follow the standard convention and lag accounting

information by six months (Fama and French (1993)). If a firm’s fiscal year ends in December

in year t, we assume that this information is available to investors at the end of June in year

t+ 1.

We construct each factor the typical HML-like fashion by independently sorting stocks

into six portfolios by size (“ME”) and a factor characteristic. We use NYSE breakpoints

– median for size, and 30th and 70th percentiles for the factor characteristic. We compute

27

value-weighted returns and other characteristics on the six portfolios. A factor’s return is

the value weighted average return of the two high-characteristic portfolios minus that of the

two low-characteristic portfolios. We rebalance accounting-based factors annually at the end

of each June, and rebalance the return-based factors monthly.

Fund ownership: δ in data. Quarterly institutional ownership data are from Thompson

Financial CDA/Spectrum holdings database for the period of 1980Q1–2017Q4. Mutual

funds characteristics (e.g., investment objectives) are obtained from the CRSP survivorship-

bias-free mutual fund database. We apply filters to holdings data that are standard in

the literature: (1) we pick the first vintage date (“FDATE”) for each fund-report date

(FUNDNO-RDATE) pair to avoid stale information; (2) we adjust shares held by a fund for

stock splits to account for corporate events that happen between report date (“RDATE”)

and vintage date (“FDATE”).

To map institutional investors in data to asset managers in our model, we exclude

funds with investment objective codes (“IOC”) of International, Municipal Bonds, Bond

& Preferred, Balanced respectively. For the main results, we stick with this definition of

institutional investors. As a robustness check, we further narrow down the definition of

institutional investors to active domestic equity funds by utilizing investment objective code

from CRSP, Lipper, Strategic Insight, and Wiesenberger. The results using this narrower

definition of institutional investors, not tabulated, are very similar to our main results.

We calculate the share of institutional ownership by summing up the stock holdings of

all institutions for each stock in each quarter. Stocks that are on listed in CRSP, but without

any reported institutional holdings, are assumed to have zero fund ownership. Table 1 reports

summary statistics of monthly returns and quarterly fund ownership for all factors.

Fund ownership at factor level. Our model is built upon the assumption that asset

managers have superior probability models of factor returns. A direct implication from

this assumption is that all else equal, the variation of wd, the portfolio allocation by fund

managers across factors, should predict future factor returns – asset managers respond to

the variation of expected factor returns over time.

Ideally, we would like to treat each factor as an asset and compute the weight for

each factor as the fraction of total dollar amount invested by funds. However, factors are

comprised of numerous stocks and different factors have overlapping stock compositions.

28

For example, stock A could be in the long leg of value and short leg of momentum. The

exact dollar amount of stock A attributed to each factor cannot be exactly identified, which

complicates our portfolio weight calculation.

Instead of calculating the exact weights of factors in fund portfolio, we calculate the

relative over/underweight of each factor. Specifically, we measure the funds’ exposure to

each factor by the spread of institutional ownership (“INST”) between the long leg and

short leg.

INSTi,t = INST longi,t − INST shorti,t (34)

where INST ji,t, j = long, short is the value-weighted average of the institutional ownership

of all constituent stocks in long/short leg of factor i. The intuition is simple. If institutional

investors genuinely have superior knowledge of the true return distribution, when they over-

weight certain factors, all else equal, the subsequent performance of these factors shall be

stronger, and vice versa.

3.2 Asset pricing implications

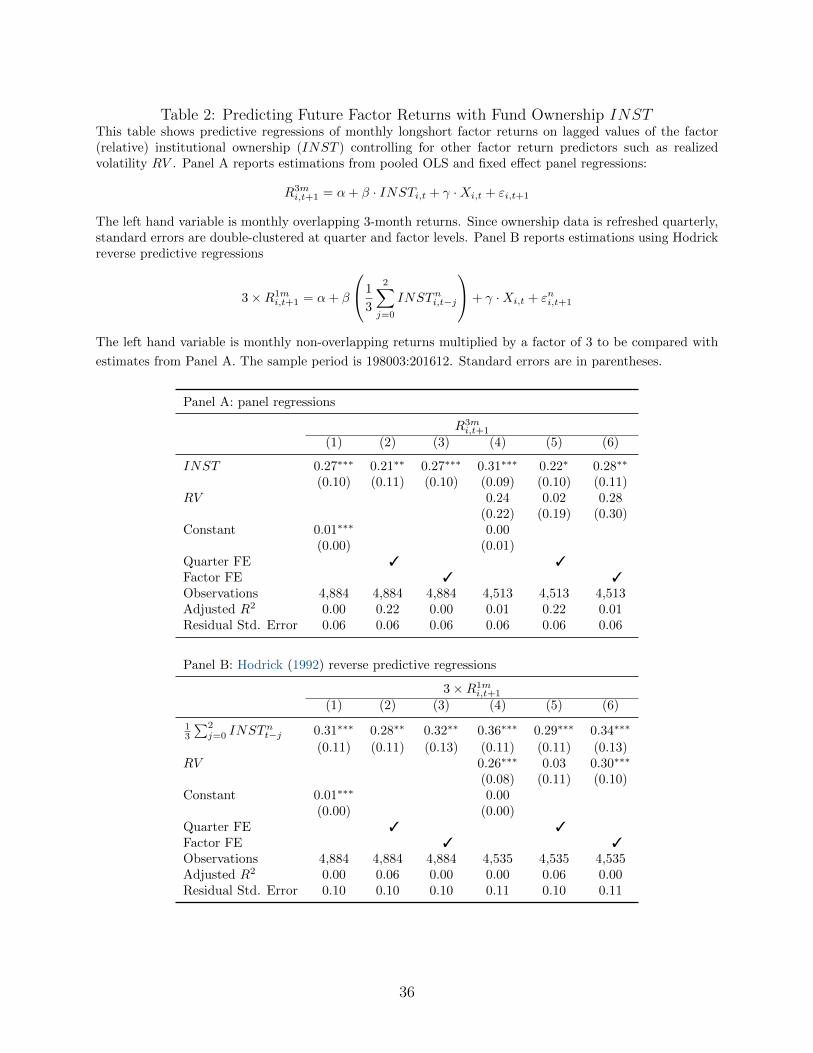

Factor timing: parametric test. From institutional investors’ relative portfolio weights

on each factor (INST ), we could empirically test whether fund managers have superior

knowledge of return distributions. Specifically, we estimate the following model: for factor

i,

Et[Ri,t+1] = α + β · INSTi,t + γ ·Xi,t + εi,t+1 (35)

where i = HML,ACR,CMA,RMW,NI,MOM,STR,LTR,BAB, IV OL, TV OL and

Xi,t includes control variables such as factor volatility (realized or from GARCH models).

Our main prediction is that the factors will outperform in following periods when the such

factors’ (relative) institutional ownership INST is high.

Since factor institutional ownership (INST ) is available quarterly, we set the returns

to future 3-month returns. To increase the statistical power, we use monthly overlapping

returns and pool all factors together to estimate a panel predictive regression. In Table 2

Panel A, we report the results of panel regression using pooled OLS and various fixed effect

models. RVi,t is the realized volatility of factor i estimated using previous 36-month sample

29

of factor returns. Standard errors are double-clustered at quarter and factor levels.

As typical in the literature of return predictability, we address the concern over biased

standard errors due to overlapping observations. Specifically, we follow the suggestion of Ho-

drick (1992) and run the following “reverse” regression to test the factor return predictability

of INST at three-month horizon.

3×Ri,t+1m = α + β

(1

3

2∑j=0

INSTi,t−j

)+ γ ·Xi,t + εi,t+1 (36)

On the left-hand side is the Ri,t+1m, the future one-month return multiplied by 3 so that it is

comparable in magnitude with quarterly returns. Results are reported in Panel B of Table

2.

Our key prediction is confirmed in all specifications. In the both panels, the factor

predictive of INST is positive and significant, robust to alternative standard errors and

various fixed effects. The coefficients estimated using panel regressions and Hodrick reverse

regressions are very close. Moreover, the predictability we document is economically mean-

ingful. For example, the coefficient 0.31 in the first column of Panel B implies that, when

the institutional ownership of one factor rises by one standard deviation, future factor re-

turn increase by 44 bps in the following quarter (1.76% annualized). Given the average

annual factor return of 3.31% in our sample, an one standard-deviation change in INST is

associated with 53% increase of expected factor return. The evidence of factor timing by

fund managers lends substantial support to our model setup, the key assumption that asset

managers possess superior knowledge of return distribution.

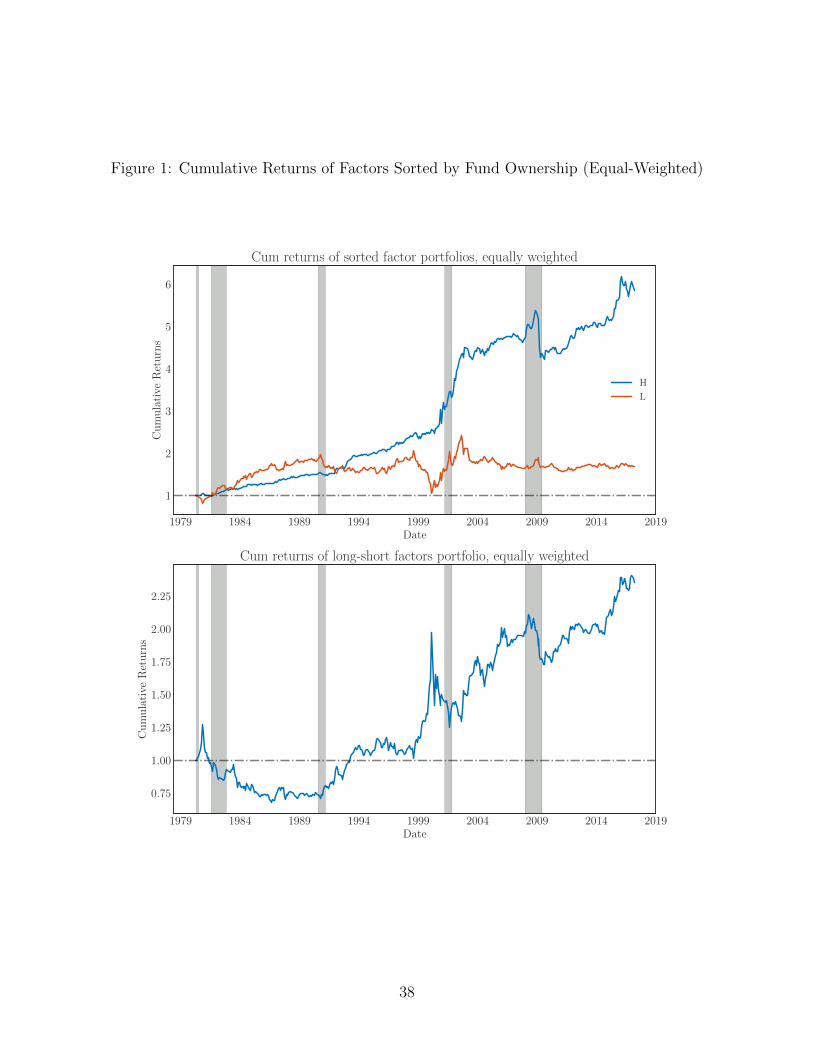

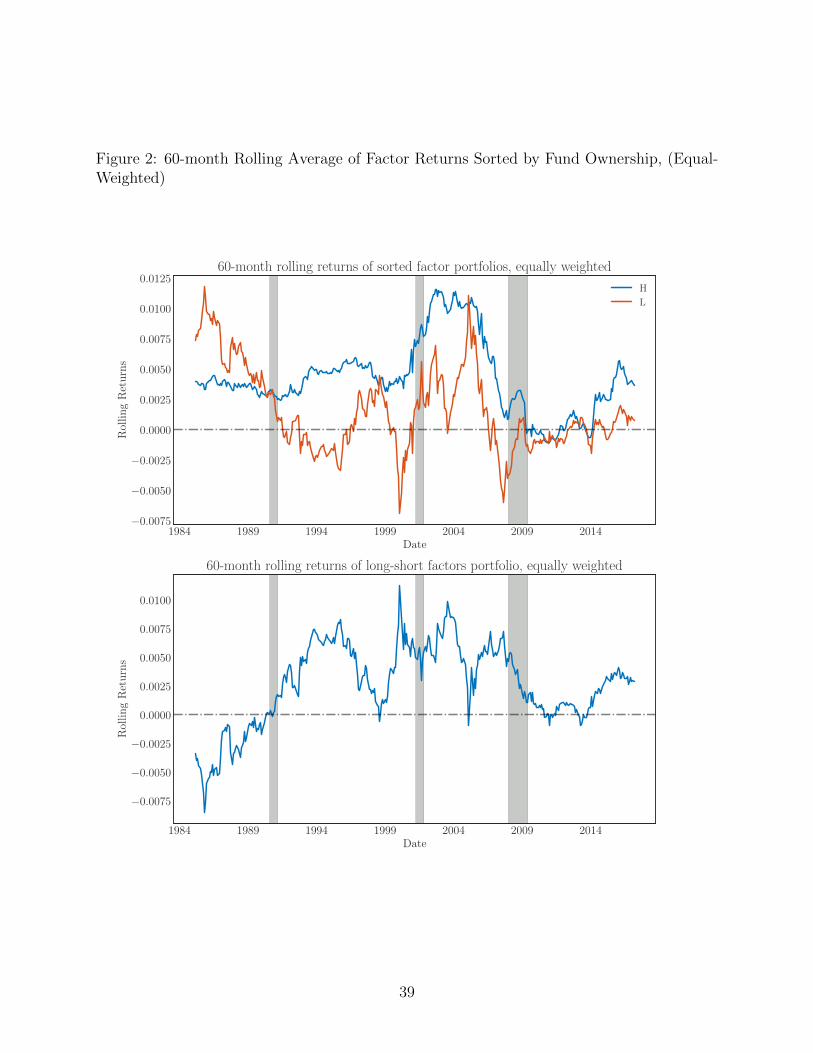

Factor timing: nonparametric test. We also implement a trading strategy that exploits

the information advantage of the institutional investors, which serve as a nonparametric test

of our model setup. The strategy formed as follows. At the end of each quarter, we rank all

factors based on their respective INST . We go long the top 4 factors and short the bottom

4 factors for the following 3 months, weighting each factor equally. For comparison, we also

form an “M” portfolio by equally weighting the factors with medium INST . The portfolio

is rebalanced quarterly.

The performances of high INST , low INST factors, and that of long-short factor

portfolio are plotted in Figure 1 (cumulative returns) and Figure 2 (rolling average returns).

30

Factors with high fund ownership consistently outperform factors with low fund ownership

since 1991. The fact that this pattern only started to appear in the 1990s suggests that

asset management industry may benefit from the exploding research efforts devoted to stock-

market factors in the academia and the developments of data processing techniques, including

financial econometrics, around the same time.

So far, we have only focused on the first moment of factor returns. In Table 3, we

report various moments and statistics of returns of factor portfolios sorted by fund ownership.

Factors with high fund ownership exhibit higher mean return, lower volatility, and smaller

skewness. These statistics all vary monotonically in fund ownership, suggesting that asset

managers tend to invest in a set of factors with a particular and superior statistical profile

(e.g., higher Sharpe ratio). Asset managers also tend to hold stocks with higher kurtosis

relative to the rest of the market, which seems to imply that ambiguity investors refrain

from factors with more extreme returns while asset managers are more willing to take on

such exposure probably due to their superior knowledge of probability distribution.

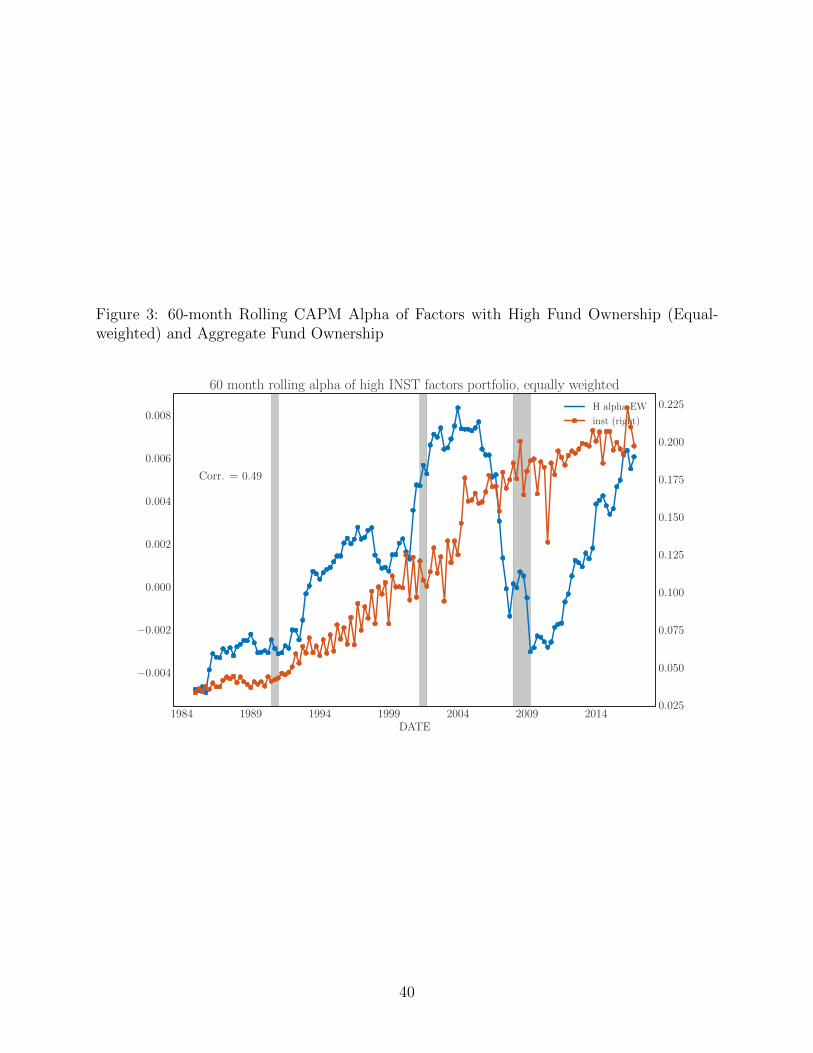

The robust alpha. In Corollary 4, we show that even if the level of delegation approaches

100%, the equilibrium does not converge to CAPM in the sense that there exists a set of