demystifying planned giving the cultivation process: ways to engage let’s begin the conversation...

TRANSCRIPT

Demystifying Planned Giving

THE CULTIVATION PROCESS:Ways to Engage

Let’s Begin the Conversation

Clyde W. Kunz, CFRE

Planned Giving Roundtable of Southern Arizona

Strengthening our community by promoting charitable gift planning

Course Objectives

Identify good planned gifts candidates Understand their profile & which types of gifts

likely “match” which donors Generate ideas for cultivating candidates Learn ideas for starting the conversation! Understand ways to used planned gifts

(i.e., for endowment-building) Develop strategies for ongoing

appreciation of planned gift donors

Demystifying Planned Giving 2011

Types of Planned Gifts

Bequests Beneficiary Designations Life income/split interest gifts Pooled Income fund Life Insurance Bargain Sale Gifts of Remainder Interest in a

Residence or Farm– a.k.a. Life EstateDemystifying Planned Giving 2011

Identifying Planned Gift Prospects Those with a multi-year history of giving to your

organization (at least 3 years+)

Those with a multi-year history of volunteerism with your organization

Those whose gifts are small in size, but consistent

Those whose life circumstances dictate changes

Demystifying Planned Giving 2011

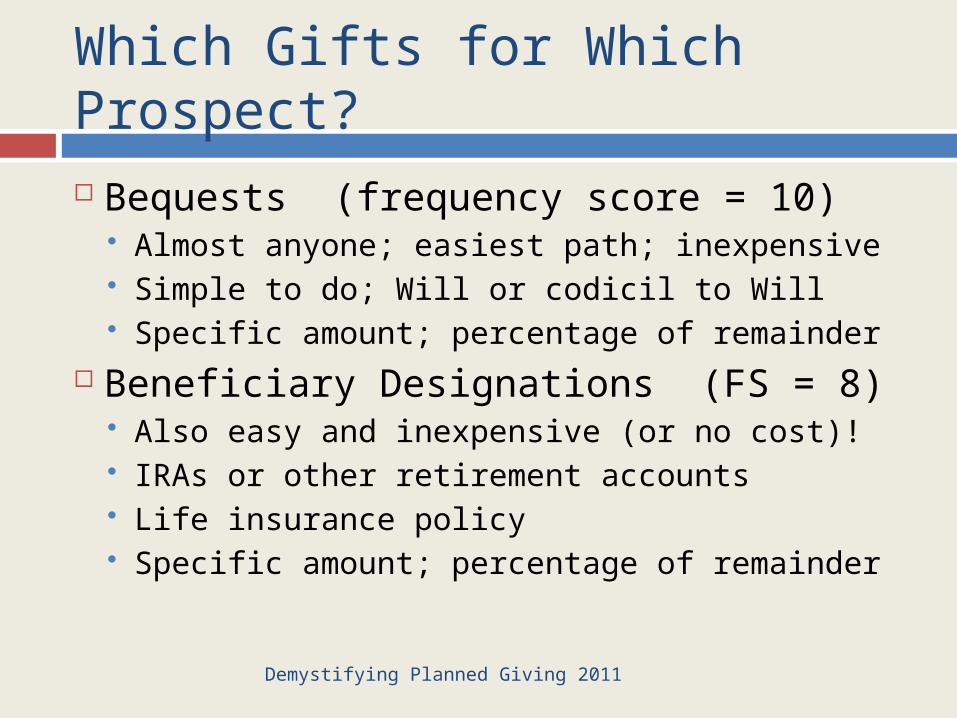

Which Gifts for Which Prospect? Bequests (frequency score = 10)

Almost anyone; easiest path; inexpensive Simple to do; Will or codicil to Will Specific amount; percentage of remainder

Beneficiary Designations (FS = 8) Also easy and inexpensive (or no cost)! IRAs or other retirement accounts Life insurance policy Specific amount; percentage of remainder

Demystifying Planned Giving 2011

Which Gifts for Which Prospect? Life Insurance (FS = 5)

Is insurance need still valid? Can make charity both the owner and the

beneficiary of policy (whole life only) Easy; inexpensive

Bargain Sale (FS = 1) Can be complicated Charity needs to have legal counsel May generate UBIT

Demystifying Planned Giving 2011

Which Gifts for Which Prospect? Gifts of Remainder Interest in a Residence

or Farm– a.k.a. Life Estate (FS = 3) Gives donor a HUGE tax deduction in year of

donation Have to think about end-of-life issues

Pooled Income Fund (FS = 1) Similar to a mutual fund for donors Incurs administrative fees; spread over the donor

pool Can benefit higher-end donors to the detriment of

smaller donors.Demystifying Planned Giving 2011

Which Gifts for Which Prospect? Life income/split interest gifts

Charitable Gift Annuities (CGA) (FS = 9) Simple contract Low cost Guarantees income Good place to “park” appreciated assets May require an outside administrator

Demystifying Planned Giving 2011

Which Gifts for Which Prospect? Life income/split interest gifts

Charitable Remainder Trusts (CRT) (FS = 7) Rule of thumb: $200,000+ Give donor more control Good place to “park” appreciated assets Requires legal counsel to set up Requires administration Requires additional tax filing

Demystifying Planned Giving 2011

Which Gifts for Which Prospect? Life income/split interest gifts

Charitable Lead Trusts (FS = 1) Very rare For very large estates ($2M+) Used as a way to pass assets between

generations A good place to “park” appreciated assets Definitely requires legal counsel

Demystifying Planned Giving 2011

PRACTICE!

An elderly couple

Have moderate size investments in highly-appreciated stocks

Do not have sufficient income to meet their monthly needs.

Demystifying Planned Giving 2011

PRACTICE!

A young business professional and her husband

High income, but have a young family

Want to support the organizations on whose boards they both serve, but want the flexibility to modify those gifts if the organizations don’t hold their interest in the long-term

Demystifying Planned Giving 2011

PRACTICE!

A 60-something couple with many assets; do not need additional income; just sold a business for several milllion dollars

Recently moved into their lovely, but smaller “last home”

Children are working professionals; live across the country; have been ‘taken care of’ through assets in the couple’s stock portfolio

Demystifying Planned Giving 2011

PRACTICE!

An elderly couple with many assets; do not need income

Have a developmentally-disabled adult

child for whom they provide care

Demystifying Planned Giving 2011

PRACTICE!

A 50-something board member with a business he wants to donate; business is valued at $1.5 million

Still owes approximately $750,000 on a

mortgage loan on the building in which the business is housed

Plans to focus on his other business, which is where his passion now lies

Demystifying Planned Giving 2011

PRACTICE!

An elderly gentleman with modest assets

Lives comfortably with income from pension fund, social security, and annual distributions from an IRA to which he contributed over many years.

Children are grown and do not need his

financial assistance

Demystifying Planned Giving 2011

Talking About Planned Gifts

Passion for Mission “You have been volunteering with us for so long; I

don’t know what we’ll do when you’re gone!” “We appreciate your gifts to our annual fund so

much; have you ever considered a gift through your estate that might continue to provide support for the X program you care about so much?”

Peer Pressure: “A number of our other volunteers (donors) have chosen to remember the agency through their estate plans. Could I provide you with some information about that as well?”

Demystifying Planned Giving 2011

Talking About Planned Gifts

Creating a Legacy: “Can you give the full names of all 4 of your

grandparents? Your 8 great-grandparents?” “Who’s going to miss you when you’re gone?” “After you’ve taken care of your family’s needs,

would you consider…….?” When you die, everything you have accumulated

in your life will go one of three places: Your family - The government - Charities you care

about Pick any two!

Demystifying Planned Giving 2011

How Planned Gifts Are Used

As Part of a Campaign Make sure that using planned gifts for that

purpose is approved Consider “adding” a planned gift option to a

campaign as a way to broaden participation

To Build Endowment Donors may assume their gift goes to

endowment Make sure they understand how to restrict their

giftDemystifying Planned Giving 2011

Donor Giving Options

Donor

Cash Assets

Restricted (endowment)

UnrestrictedUnrestricted

Deferred/

planned

Deferred/

plannedCurrent Current

Demystifying Planned Giving 2011

Recognizing Planned Gifts

Donor Recognition “Club” or “Society” Annual or semi-annual event Program book listing / donor wall listing

Ongoing Planned Giving Information Planned giving newsletters Seminars / speakers

Other Lapel pin, desk set, etc.

Demystifying Planned Giving 2011