dental industry association of canada (diac) · 1 dental industry association of canada (diac)...

TRANSCRIPT

1

DENTAL INDUSTRY ASSOCIATION OFCANADA (DIAC)

ASSOCIATION CANADIENNE DE L'INDUSTRIE DENTAIRE

TWENTY-SECOND ANNUALFUTURE OF DENTISTRY SURVEY REPORT

FINAL REPORT

August 5, 2018Submitted by:

Table of Contents

1. Introduction............................................................................................................1

2. Study Methodology.................................................................................................32a. Survey Method ..................................................................................................................................32b. Identification of Survey and Sampling Bias...........................................................................52c. Questionnaire Design .....................................................................................................................82d. Sample Size ..................................................................................................................................... 112e. Actual Response Rate .................................................................................................................. 122f. Regional Analysis........................................................................................................................... 123. Executive Summary...............................................................................................13

A. Respondent Profile ...............................................................................................14A.1 Practice Type ................................................................................................................................. 14A.2 Years in Practice ........................................................................................................................... 14A.3 Location of Practice ..................................................................................................................... 15A.4 Owner or Associate...................................................................................................................... 16A.5 Practice Affiliation ………………………………………………………………….18A.6 Years After Graduation To Set-up Practice ........................................................................ 23A.7 Number of Dentists in Practice ............................................................................................... 23A.8 Number of Operatories in the Practice ................................................................................ 25A.9 Chairside Days Spent In Practice Per Year ......................................................................... 28A.10 Average Patients Treated Per Day ...................................................................................... 29A.11 Hygiene Days............................................................................................................................... 30A.12 Demographic Shift in the Practice Profile ........................................................................ 31B. Product Purchases and Usage................................................................................35B.1 Dental Equipment ........................................................................................................................ 35B.2 Sundries/Consumable Products............................................................................................. 45B.3 Dental Laboratory Products..................................................................................................... 53C. Financing ..............................................................................................................58C.1 Leasing.............................................................................................................................................. 58C.2 Capital Financing .......................................................................................................................... 61

D. Marketing and Customer Service ..........................................................................63D.1 Relative Value of Marketing Vehicles ................................................................................... 63D.2 Suggested Service Improvements ......................................................................................... 67D.3 Internet ........................................................................................................................................... 70E. Continuing Education ............................................................................................75E.1 Interest in Continuing Education Topics............................................................................. 75E.2 Type of Study Club ....................................................................................................................... 77E.3 Suggestions for Improvement of CE Opportunities ........................................................ 77F. General Trends In Dentistry ...................................................................................78F.1 Percentage of Procedures Refer to Specialist .................................................................... 78F.2 Patient Information ..................................................................................................................... 81F.3 Practice Promotion ...................................................................................................................... 85APPENDIX A — Detailed Surveyed Tabulations..........................................................91

APPENDIX B — Survey Questionnaire Contents .......................................................147

APPENDIX C — Archive ...........................................................................................169

1

1. INTRODUCTIONIn October 2018, the Dental Industry Association of Canada (DIAC) retained the firm of EricP. Jones & Associates Inc. to assist with the design and administration of its 22nd AnnualSurvey (2018) of Canadian dentists. Given the diversity of DIAC membership, the study wasdeveloped to meet a variety of objectives covering the following broad areas:Product Purchases and Usagea) To determine current ownership and/or planned purchase of various types of dentalequipment.b) To determine current and anticipated future purchase sources and ordering methodsfor dental consumables/sundries.c) To determine current and anticipated future usage trends for specific dentalprocedures.d) To determine anticipated future usage trends for specific dental laboratory productcategories.Financinga) To determine anticipated financing sources and/or use of leasing options forequipment, practice purchase or office expansion.b) To determine dentist’s main influence on financing decisions.Marketing and Customer Servicea) To evaluate the value of specific marketing vehicles to the dentist as a source of newproduct information.b) To determine dentists’ Internet usage level and their rating of its value as a source ofinformation.c) To evaluate how dental dealers, manufacturers and laboratories could improve theirservice to their customer base.d) To determine if areas of unfilled need exist or if there are specific services dentistswould like to see offered by dealers, manufacturers or laboratories.

2

Continuing Educationa) To determine dentists’ level of interest in various Continuing Education Topics.b) To determine how current CE opportunities could be improved.c) To determine how many dentists currently belong or plan to join a Study Club and whattypes of Study Clubs dentists belong to.General Trends in Dentistry1. To determine current and future anticipated percentages for different proceduresdentists refer to a specialist.2. To determine who is currently placing the majority of implants.3. To determine dentists’ opinions on where patients are obtaining information aboutdental procedures and the main changes in their patient base.4. To determine dentists’ current or future usage of practice promotion methods such asasking for referrals, promoting new technologies, newsletters/direct mail, social media,etc.5. To determine dentist’s opinions on the top challenge they intend to address in 2018 andtheir three key metrics for success.6. To determine a profile of the breakdown of solo practices, Multi-practices (Grouppractice) Or Corporate Dentistry; the intention to join one of these organizations (orremain in solo practice); and the perceived benefits and drawbacks of such amembership.As with the previous studies conducted, the objective of this year’s survey was to gain abroad overview understanding of the issues and attitudes defining the purchase dynamicsin dental offices; the perceived value of marketing vehicles employed by dentalmanufacturers, dealers and laboratories; and the identification of important issues facingall Canadian dentists decision makers within the practice today and into the future (i.e.,within a two year horizon). The study is intended to assist dental manufacturers, dealers,laboratories and service providers as they develop new products and implement marketingprograms to address the needs of dentist decision makers in Canada.

3

2. STUDY METHODOLOGY

(a) Survey MethodThe 2018 survey was administered in an online format for the third year. Prior to 2016, thesurvey was also issued as a 6-page printed insert (with postage paid reply envelope)polybagged with the February 2015 issue of CDA Essentials for English speaking dentistsacross Canada (approximate count 16,000) and Spectrum Quebec for primarily Frenchspeaking dentists in Quebec (approximate count 4,200). This split was necessitated by twofactors: the CASL opt-in process in 2014 and the fact that l’Ordre des dentists du Quebecwas no longer a member of the CDA. In combination, DIAC’s coverage in Quebec throughthe CDA (whether polybagged with magazine or by email) had dropped to approximately635 potential dentist respondents - meaning that DIAC was not communicating with 2786dentists from the province of Quebec via its former CDA channels.As with the print version of the survey, access to the Quebec dentist population via OralHealth/Scott’s Directories at that time was severely restricted by CASL opt-in and l’Ordredes dentists du Quebec leaving the CDA. Oral Health/Scott’s Lists online list coverage wasdown 30% across the country in 2015 due to the CASL opt-in requirement. In this case, theimpact was more widespread across Canada with the email address list shrinking by 2308contacts from 7546 to 5238. There was also a noticeable drop in Quebec counts from 1689to 989, along with sizeable drops in BC and ON in terms of absolute numbers. On apercentage basis, every province and territory in the country showed a noticeable dropsince 2014.For the 2018 survey, email lists from Oral Health/Scott’s and Palmeri Publishing were utilized.Oral Health/Scott’s was used for English-speaking dentists (6206 GPs and Specialists) outsideQuebec and the Palmeri Publishing List used in Quebec only (due to its stated wider coveragenumbers – 1600 GPs and Specialists - in the province during the initial project planning period).

While email list counts vary constantly, an approximate total of 7730 dentists were repeatedlyreached over the survey period as per the following provincial breakdown.

The CDA’s most recent (as of December 31, 2017) counts of licensed dentists will be used forthe purposes of comparing the email reach to the overall estimated number of practicing dentistsin total, province by province across the county. This chart is supplied below the Email Listcounts chart.

4

All Dentists EmailBC 987AB 664SK 145MB 176ON 3829QC 1600NB 89NS 142PE 28NL 60NT / NU /YUKON 10

Grand Total 7730

All Practicing Dentists

BC 3,478AB 2,533SK 473MB 722ON 10,027QC 4,386NB 339NS 552PE 78NL 206NWT / NT /YUKON

75

Grand Total 20327A total of six emails were sent to English-speaking dentists across Canada (outside ofQuebec) distributed via the Oral Health/Scott’s Lists (linking to the English surveytabulations via the web link www.surveymonkey.com/r/DIAC2018) and four bi-lingualemails with links to the French language version of the survey were distributed by PalmeriPublishing into Quebec. Both Oral Health/Scott’s and Palmeri confirmed that their on-goingopt-in methods meet CASL standards per routine.

5

The availability of the online version was promoted in English via an initial email invitationand five subsequent email reminders along with the previously mentioned PalmeriPublishing coverage to practitioners in Quebec (one invitation and three reminders).In addition, a press release campaign was launched to dental media and dental associationsacross the country prior to the initial email, with some of the contacted media andassociations agreeing to run the release. There were free insertions of a DIAC survey adwith a link to online survey in the CDA Oasis e-newsletter in French and English over thesurvey period with a link to the online survey. Oral Health and Palmeri Publishing alsoplaced the DIAC ad on their magazine home pages over the period as unsold space wasavailable, with Oral health running the add periodically in their weekly Wednesday e-newsletter at no charge. All respondents were offered a chance to enter a draw for a GrandPrize of a $5000 travel voucher, three $500 second prizes along with ten consolation prizesof $100 travel vouchers. To qualify for the draw, completed surveys had to be received byJune 6, 2018.For 2018, an additional contest was run offering the first 100 respondents to submit acompleted survey a $10 Starbucks electronic gift card. Subsequent contests were run forapproximately two weeks per tradeshow (PDC, ODA and JDIQ), offering the first 30respondents to submit a completed survey by a specific due date during that tradeshowperiod a $10 Starbucks electronic gift card. These programs dramatically increased interestand promotional impact for the survey as evidenced by increased response around thespecific EBlasts dealing with each tradeshow (all EBlasts offered national coverageirrespective of the location of the tradeshow).Given the six well-spaced email messages for the English online version (initial emailMarch 1; and follow up reminders April 17, May 8 and May 22; and final Last Chance onJune 4) and four email messages for the French online version (initial email March 1;reminders April 17 and May 15; and final Last Chance on June 4), this allowed ample timefor response.(b) Identification of Survey and Sampling Bias1. As illustrated in EXHIBIT 1, the pattern of survey response on a percentage basis forthis year did vary from the national overall breakdown of dentists by province suppliedas the Oral Health/Scott’s mailing list totals. However, there are still some similaritiesto past results. In past years, Ontario’s percentage of response has historically beenlower than that province’s overall proportion of Canadian dentists, resulting in theremaining regions being slightly higher. While once again in 2018, the percentage ofOntario (41.5%) respondents was lower than the overall total number of dentists(42.9%) in the province, the difference is almost indistinguishable as it was last year.The same situation applied in Quebec where the province accounted for 14.1%(compared to 15.8% in 2017) of overall survey response as opposed to 20.1% of the

6

0% 10% 20% 30% 40% 50%NWT/NT/YKBritish ColumbiaAlbertaSaskatchewanManitobaOntarioQuebecNew BrunswickPEINova ScotiaNewfoundland Actual Distribution% of Survey Response

total number of dentists across Canada. However, the actual number of responsescontinues to grow in the province year over year. Correspondingly, the opinions ofWestern (36.1% of response as opposed to 31.7% of total dentists) and Atlantic Canada(8.3% of respondents as opposed to 5.3% of total dentists) respondents will haveslightly more impact on overall results than their total populations might warrant.However, given the relatively small base of 414 respondents, these variances are wellwithin statistical means. It will require at least another year or two of experience andtracking to determine what may be now occurring in terms of response patterns.DENTAL INDUSTRY ASSOCIATION OF CANADA

EXHIBIT 1

% of Survey Response by Province vs Actual Distribution(2018)

Given these variances and the far smaller base of respondents, the following chartillustrates the relative response rates to actual distribution of dentists across the countryas per the CDA Practicing Dentist counts. While there is some variance between respondentand actual percentages with the on-line survey administration in 2018, this chart illustratesthat there have always been variances up and down, province by province over the historyof the survey. The variances for 2018 are no more or less than what has been experiencednormally and still indicate a good reading of overall dentist opinion.

7

10-Year Comparison of Survey Response to Actual Dentist Distribution

By ProvinceActual

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Distribution% % % % % % % % % % %Newfoundland 1.7 1.5 0.3 1.0 0.3 1.2 1.4 1.9 0.9 1.2 .9Nova Scotia 3.1 4.5 5.3 4.3 4.6 2.7 4.0 5.3 2.7 4.6 2.4PEI 0.6 0.6 0.9 0.7 0.9 0.2 0.3 1.4 0.3 1.0 0.3New Brunswick 2.2 1.2 3.1 2.6 2.5 3.2 2.9 2.4 2.4 1.5 1.5Quebec 19.6 22.1 19.1 18.0 19.9 23.0 12.4 14.4 15.8 14.1 19.2Ontario 34.7 34.1 33.7 34.1 35.0 35.2 42.2 36.5 41.8 41.5 43.8Manitoba 6.4 4.5 4.3 5.2 7.4 4.6 3.5 5.8 2.1 1.9 3.2Saskatchewan 2.5 0.9 2.8 2.3 2.5 2.0 3.8 3.4 1.8 2.2 2.1Alberta 11.8 12.7 10.0 11.8 10.4 10.5 15.6 13 20.3 13.1 11.1British Columbia 16.5 16.6 20.1 19.3 16.3 17.1 13.3 14.9 11.6 18.7 15.2NWT/NT/YK 0.8 1.2 0.3 0.7 0.3 0.2 0.6 1.0 0.3 0.2 0.3

10-Year Comparison of Survey Response to Actual Dentist Distribution

By Region

Actual2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Distribution% % % % % % % % % % %Atlantic Canada 7.6 7.8 9.6 8.6 8.3 7.3 8.6 11.0 6.3 8.3 5.1Quebec 19.6 22.1 19.1 18.0 19.9 23.0 12.4 14.4 15.8 14.1 19.2Ontario 34.7 34.1 33.7 34.1 35.0 35.2 42.2 36.5 41.7 41.5 43.8Western Canada 38.0 35.9 37.5 39.3 36.9 34.4 36.2 38.1 36.2 36.1 31.9

8.3%14.1%

41.5%36.1%

5.1%19.2%

43.8%31.9%

Atlantic CanadaQuebecOntario

Western Canada

0% 10% 20% 30% 40% 50%Actual Distribution% of Survey Response

8

2. As with last year, non-response was not a problem with this survey falling withinexpected norms. Most dentists answered the survey fully. The only exceptions tended tobe on financial questions, which normally experience far higher non-response rates inmost surveys. In addition, open-ended questions routinely tend to result in much lowerresponse rates, particularly in an on-line as opposed to a hand-written environment.However, they are the only way of capturing opinion without biasing the response byproviding pre-determined lists of possible answers. Relevant non-response rates will benoted in the executive summary where applicable.3. Given the on-line administration methodology for 2018, it can be expected there will besome difference in the demographic make-up of respondents and its impact on theirresponses. For example, as by definition, these on-line respondents are predisposed tousing computers and working on-line, there may be variances in their responses tocomputer-oriented questions as compared to past years. These possible variances willbe noted as they occur.(c) Questionnaire DesignA questionnaire covering the key issues was developed by DIAC under the guidance of EricP. Jones & Associates Inc. As the primary purposes of this study were to measure allCanadian dentists' opinions regarding the future direction of dentistry along with thefurther development of a standard respondent profile based on their current purchasebehaviour, a mix of closed and open-ended questions were included. Open-ended questionsare an excellent way to collect “opinions”. Quite often, new factors or responses that greatlyinfluence market behaviour are uncovered.The questionnaire was specifically designed to avoid biasing response by mentioningspecific manufacturers, brands, dealers or suppliers. This data was captured, whereapplicable, through the use of open-ended questions. Specific brand data was not requestedgiven the constraints of questionnaire size.New Questions Added for 2017-2018 SurveyTwo new questions were added to the section of the survey aimed at those practicing in aMulti-practice (Group practice) or Corporate Dentistry environment as follows:

Do you feel as part of a group practice you can offer a higher standard of care thanthat of a sole practitioner?___ YES ___ NO ___ Don’t Know Do you believe your patients "feel" better serviced or less serviced compared to thatof a sole practitioner?___ Better serviced ___ Less serviced ___ Don’t Know

9

Questionnaire Review - 2017A major review and re-consideration of the survey objectives and questionnaire itself wasundertaken in 2017. As such, there were major changes made to all sections of the surveyfor 2017. New questions and response options were added or revised. In addition, it wasdecided to retire certain sections of the questionnaire entirely beginning in 2017. The finalreporting and analysis sections for these question areas will be placed in a new Appendix ofthe report moving forward to be called APPENDIX C – Archive. Changes were as follows:Questions Retired to Archive as Part of 2017 Review

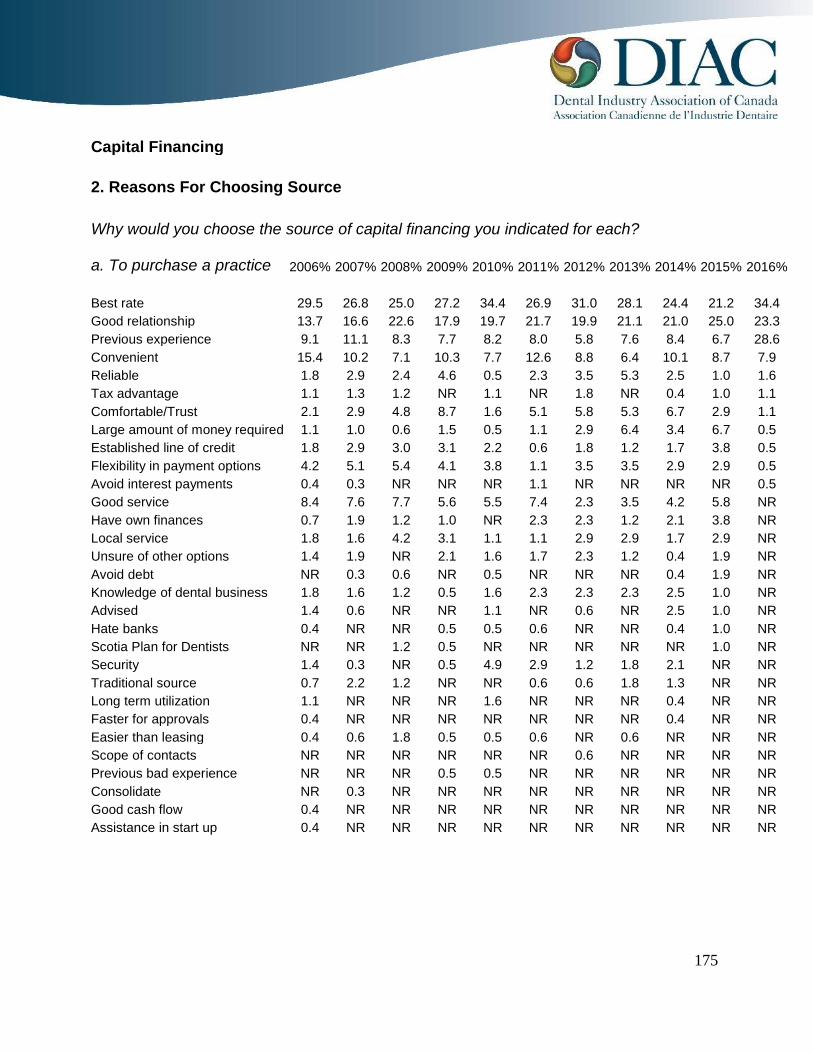

The response options for the questions “Who would you approach for capitalfinancing for each of the following (please specify source if applicable)?” AND “Whywould you choose each of those sources you indicated above?” were changedcompletely from “to purchase a practice, expand a practice or to add new equipment”to “To join a group practice, To join a dental service organization, To expand a multi-practice organization”. As past results are not comparable to those using the newresponse options, the original question analysis will be archived and a new analysisstarted in its place.

Question “What are the main changes you are seeing in your patient base?” wasremoved and that past analysis will be archived. Question “Reasons Patients Are Not Accepting Treatment Plans” was removed andthat past analysis will be archived. Question “Do you have computer terminals in your operatories?” AND “If plan to

purchase, when?” was revised to “What stage of ‘digitization’ has your office reachedcurrently?” with response options:

o Fully paperlesso Not paperlesso In transition to paperlessAND “Which areas of your office are digitized? (Please check off all that apply)” withresponse options:o Chartingo X-Rayo In the operatorieso In the Private OfficeAs past results are not comparable to those using the new response options, theoriginal question analysis will be archived and a new analysis started in its place.

Question on Internet Connection “Do you have an Internet/Email connection: At theFront Desk, in the operatories, in the Private Office?” was removed and that pastanalysis will be archived.

Questions “Do you currently belong to a Study Club? (YES, NO, No, but plan to joinone)” AND “If YES, what type of Study Club(s) do you belong to?” was revised to

10

“What type of Study Club(s) do you belong to? (Please check off all that apply)” withresponse options:o Implanto C&Bo Endodontico Periodontico Orthodontico Don’t Belong to a Study Clubo Other (please specify)As past results are not comparable to those using the new response options, theoriginal question analysis will be archived and a new analysis started in its place

Questions “If you visit the Exhibit Floor at conventions, please rate the following from1 to 5 (with 1 being Not Valuable and 5 being Extremely Valuable) regarding theirinfluence on your decision.”; “How long do you spend on the Exhibit Floor on average(hours per day)?”; “Would you still attend a Convention if there was no Exhibit Floor?”and “If you don’t visit the Exhibit Floor, what are your main reasons for not visiting?”were all removed and that past analysis will be archived.

Question “Do you have or ever, worked with Practice Consultants?” AND “If Yes, whatdid they help you with?” were removed and that past analysis will be archived.

New Questions Added as Part of 2017 Review

An entirely new question “Do you currently offer financing options to our patients,such as 12 months Equal Monthly Payment plans, through any of the followingmethods?” was added to the questionnaire with response options:

o We offer in-house financing where we administer the process and assume thecredit risk

o We use a 3rd party financing provider like Health Smart Financialo We do not offer financing to our patients

An entirely new question was added “What are the three key metrics for success inyour practice? (please select up to three of the following)” to the questionnaire withresponse options:

o Financial/paying bills/overhead costs, etc.o Getting more patients/keeping busy/increasing patient visitso Staffing issueso Tracking referrals out of the practiceo Implementation of technologyo Other (Please specify)

Entirely new Questions “Is your practice: A solo practice, Multi-practice (Grouppractice) Or Corporate Dentistry?”; “In the next two years, do you intend to: Join amulti-practice (Group practice); Join a Corporate Dentistry Organization; Remain insolo practice?”; “Are you: An Owner of a multi-practice (Group practice), An Associatein a multi-practice (Group practice)?”; “Is your multi-practice (Group practice) /

11

Corporate Dentistry Organization: Regional, National, International?”; “How manyseparate Clinics/Locations are there in your multi-practice (Group practice) /Corporate Dentistry Organization: 2-4, 5 or more?”; “What do you feel are the keyadvantages of a multi-practice (Group practice) / Corporate Dentistry structure?”;“What do you feel are the main drawbacks of a multi-practice (Group practice) /Corporate Dentistry structure?” were added to the questionnaire.

An entirely new Question “How many operatories are you planning to add to yourpractice in the next 2 years?” was added to the questionnaire with response options:None, 1, 2, 3 or more.

An entirely new Question “Do you currently place the majority of your own implants?”was added to the questionnaire with response options: YES, NO but plan to do so inthe future, Plan to continue to have Specialist place, Other (please specify)”

New Response Options Added as Part of 2017 Review

“Electric Handpiece” was added to the list of response options for questions “Whichof the following equipment do you currently own and/or plan to buy in the next twoyears?”; “Concerning the equipment you plan to buy, which product would you buyfirst?” AND “Which product would you buy second?”

A new Practice promotion option “Free Service offering (e.g. a Free Whitening)” wasadded to the list for the question “Are you currently using, planning to use orconsidering any of the following in your practice? (Please check all that apply)”

Two new options (“Fluoride” and ‘Whitening”) were added to the current list ofoptions offered for the question “What are your practice’s patients asking you about?(Please check off all that apply)”

Questions Rephrased as Part of 2017 Review

Question “What are the top three challenges in your practice today?” was rephrasedas “What is the top challenge you intend to address in 2017?” The questions on Study Clubs “Do you currently belong to a Study Club?” and “If YES,

what type of Study Club(s) do you belong to?” were rephrased to the more direct“What type of Study Club(s) do you belong to? (Please check off all that apply)” alongwith a new response option “Don’t belong to a Study Club”.(d) Sample SizeTargeted survey response set beginning in 2016 was 150 completed surveys - given the on-line administration only and the far smaller overall dentist populations reached via thebaseline email address lists used (as opposed to mailing all dentists). In theory, 19 timesout of 20, the results from an overall sample of this size should vary by no more than +/- 8percentage points from what would have been found by surveying the entire population ofthe target market. This methodology and result are standards for the research industry.

12

(e) Actual Response RateA total of 414 dentists responded to the on-line survey (as opposed to 335 completing theonline survey in 2017 and 208 in 2016) within the time frame allotted. Response continuesto grow year-over-year since the initially targeted 150 on-line respondents expected for2016. The impact has been an increase in the overall accuracy of response from +/- 6.8% in2016 to +/- 4.69%. This 2018 result still provides a good reading of dental opinion acrossCanada.All respondents were dentists practicing in Canada. As illustrated in the section of thisreport covering the respondent profile, the study encompassed a diversity of generaldentists and specialists; solo and group practices and dentists practicing in all regions ofthe country.(f) Regional AnalysisSince the 2000 survey (with the exception of 2005 where response rates were too low), wehave added Regional Analysis on selected questions where noticeable variances occur. Thiswas accomplished by grouping respondents into four areas: West (B.C., Alberta,Saskatchewan and Manitoba), Ontario, Quebec and Atlantic Canada. These groupings werenecessary to ensure a sufficient number of respondents in each area to allow somereasonable level of accuracy. As the accuracy of response ranges +/- 10% to +/- 21%depending on the question, these analyses should be considered as “indications” ofbehaviour only. Regional analyses were not supplied for questions where there was littledifference between regional results and those for the country as a whole.

13

3. EXECUTIVE SUMMARY

OverviewTo allow a more systematic review of the results, the report will organize the questionsfrom the survey into logical groupings by study objective. The actual question from thesurvey will appear in its entirety. This will allow cross-referencing, if desired, back to theoriginal questionnaire form. Wherever possible, a comparison to the previous year’s surveyresults as well as five-year trends will be noted.Responses to the survey are presented in six different summaries as follows:A. Overall Respondent Profile

B. Product Purchases and Usage

C. Financing

D. Marketing and Customer Service

E. Continuing Education

F. General Trends in DentistryThe report is supplemented with three appendices: Appendix A contains the detailedtabulations of the survey: Appendix B supplies a copy of the full on-line 2018 questionnairelinked to the email announcements as outlined earlier in this report; and Appendix C nowcontains the analyses and raw results for those questions retired and archived.

14

A. Respondent Profile

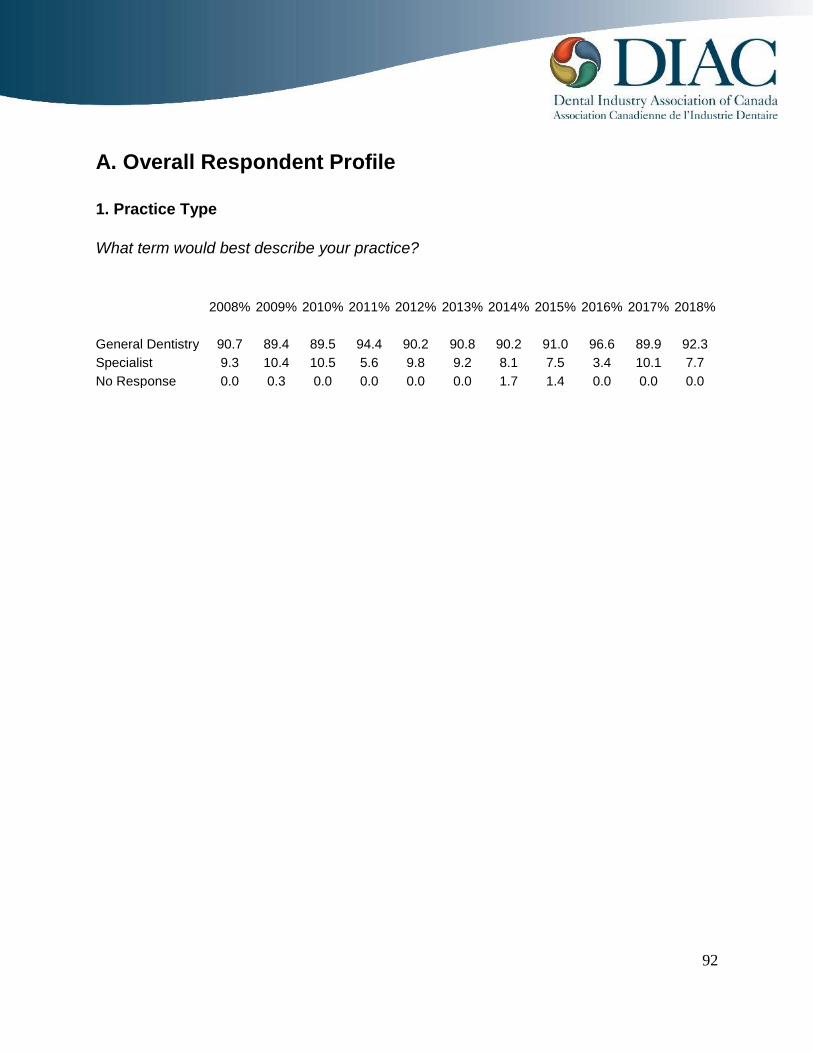

1. Practice Type

Which term would best describe your practice?

As expected, the vast majority of respondents were General Dentists (92%) in 2018 while8% were Specialists, returning to the usual Specialist rate as compared to the average overthe last decade.2. Years in Practice

How many years have you practiced dentistry?

GeneralDentistry

92%

Specialist8%

5 11 16 19 28200.2

0-3 years4-9 years10-15 years16-20 years21-25 years26 years or moreNo Response

15

The vast majority (83%) of respondents in 2018 had practiced dentistry for 10 or moreyears. Survey response therefore, continues to reflect the opinions and patterns of well-established practices. What is interesting is that the percentage of dentists who havepracticed for more than 20 years rose in 2018 to 48% (from 32% in 2017 and 18% in2016) despite the new on-line survey administration. In the past, these respondentsaccounted for 64.7% in 2015 and an average of 63% from 2009-2014. This is almostentirely due to the re-emergence of the “26 years or more” respondent now at 20% of totalresponse, after almost disappearing in 2016 at only 4.3%. However, this “26 years or more”respondent had previously accounted for as much as 57% of total response so perhaps thisreflects more of a balance.There have been corresponding large increase in the percentage of “21-25 years”respondents for 2018 (28% from 19% last year) leading to an overall aging of therespondent base. Of course, there have been corresponding decreases in the “10-15” (16versus 21% in 2017 and 37% in 2016) and “16-20” (19 versus 29% last year) groups. The“0-3” (5% both years) and“4-9” (11 versus13%) groups basically held their own. Ingeneral, the respondent base continues to be younger in terms of most of the past history ofthe survey, at least in terms of years in practice, but the trend continues once againtowards an older profile.On a regional basis, Atlantic respondents (29% less than 9 years) tended to have been inpractice a shorter length of time in 2018 as opposed to respondents from other regions. In2016, it was Quebec (77%) with the highest percentage below 15 years. This changed in2018 to an older demographic with Quebec respondents having a higher than averagepercentage of respondents in practice over 26 years (28% as opposed to 20% overall).Ontario and Western respondent profiles mirrored the overall averages.3. Location of Practice

Which type of area would best describe the location of your practice?As in previous years, the majority of respondents (62% as opposed to 56% last year and51% in 2016) described their location as Urban. The remaining respondents represent agood mix of response from Suburban (22% as opposed to last year’s 29%) and Rural (12%)practices.Response from Urban area dentists is slightly higher than the average of about 53% for theprevious 10 years. The percentage of response from Suburban areas is about even with theaverage of 24.9% from the last ten years. Response from Rural practices basically the sameas in 2017 and still below the average of 17.7% from the last 10 years. “Institutional”represented 3% of respondents (about the same as 4% in 2017, above the 1% of practicesfrom 2015 and 2016 (and compared to the average of 2.2% the last ten years).

16

Regionally, there were again significantly more Atlantic Rural (24%) respondents. This wasoffset overall by lower Rural responses in Quebec and Ontario. Ontario and Quebecrespondents considered themselves Suburban. Western Canada (67%) had by far thehighest percentage of Urban respondents, as it did in 2017.4. Owner or Associate

Are you an owner or associate?

The vast majority of respondents (72% as it was last year and as opposed to 77% in 2016and 79% in 2015) considered themselves owners of their practices. This is lower than the

62%

23%12% 3%0%10%20%30%40%50%60%70%

Urban Suburban Rural Institutional

Owner72%

Associate28%

17

average from the previous 10 years (78% from 2008-2017). A further 28% identifiedthemselves as associates, a record high and much higher than the average of 17% the last10 years. The percentage of Owners continues to trend downwards and the percentage ofAssociates upwards. This may be a function of the “younger dentist” demographic outlinedin the Years in Practice section earlier and may again reinforce the premise that there is arelationship between years in practice, ownership status and the profile of the surveyrespondent.When considering the profile of the respondents in each range based on years in practice, itis evident that the 0-3 range of years in practice is dominated by Associates withownership becoming more prevalent as years in practice increases. Then as the respondentages, they return to Associateship as an exit strategy.Owner vs Associate Breakdown by Individual Year in Practice Ranges*

0-3years

4-9years

10-15years

16-20years

21-25years

26 yearsor more

Owner 18% 64% 73% 83% 80% 69%Associate 82% 36% 27% 17% 20% 31%

Total 100% 100% 100% 100% 100% 100%

*All Respondents answered the questions.

18%64% 73% 83% 80% 69%

82%36% 27% 17% 20% 31%

0-3 years 4-9 years 10-15 years 16-20 years 21-25 years 26 years ormore

Associate Owner

18

This chart illustrates the divergence between Owner and Associate based on starting out inpractice, drawing very close on a percentage basis as they move through the mid-years, withincreasing ownership over 20 years in practice and finally illustrating the return of the olderdentist to Associateship as they exit the profession.

In addition, while not tracked by this survey, there is the trend acknowledged in the dentalresearch literature towards younger dentists joining group practices (whether independent ornational organizations) as an entry into the market and older dentists joining similarorganizations as an exit strategy.Regionally, Western dentists (77%) were far more likely to describe themselves as owners.Ontario (32%) had far more Associate respondents.5. Practice AffiliationAn entirely new set of questions was added to the 2017 survey around the area ofaffiliation of the respondent dentist, both today and projected over the next two years. Thiswas accomplished by separating those currently in solo practice, and intending to remainso, from the respondents who were in a multi-practice or group dentistry situation througha two stage set of questions. As this branching can be difficult to follow without seeing thetotal flow of the questions, the full set will be outlined here first. All respondents wereasked:“Is your practice:

A solo practice, Multi-practice (Group practice) Or Corporate Dentistry?”Respondents who stated they were currently in a solo practice based on their response tothe question above were then asked:“In the next two years, do you intend to: Join a multi-practice (Group practice); Join a Corporate Dentistry Organization; Remain in solo practice?”Those who had elected to remain in solo practice where then moved on to the questionsabout their own practice regarding years to set-up, number of other dentists in practice,number of operatories in the practice, etc. as per usual.

19

Respondents who stated they were currently in a multi-practice or group dentistrysituation, or intended to do so in the next two years, were then asked a set of subsidiaryquestions as follows:“Are you: An Owner of a multi-practice (Group practice), An Associate in a multi-practice (Group practice)?”“Is your multi-practice (Group practice) / Corporate Dentistry Organization: Regional, National, International?”“How many separate Clinics/Locations are there in your multi-practice (Group practice) /

Corporate Dentistry Organization: 2-4, 5 or more?”“Do you feel as part of a group practice you can offer a higher standard of care than that

of a sole practitioner? “ YES NO Don’t Know“Do you believe your patients "feel" better serviced or less serviced compared to that of a

sole practitioner?” Better serviced Less serviced Don’t Know“What do you feel are the key advantages of a multi-practice (Group practice) / Corporate

Dentistry structure?”“What do you feel are the main drawbacks of a multi-practice (Group practice) /Corporate Dentistry structure?”

20

Actual response for each of the questions was as follows:“Is your practice: A solo practice; Multi-practice (Group practice); Or CorporateDentistry?”

2017% 2018%

A solo practice 58.5 63.0Multi-practice (Group practice) 36.4 34.3Corporate Dentistry 3.9 1.9No response 1.2 0.7The majority (63%) of respondents stated they were in a solo practice, whileapproximately a third (34%) were in a group practice situation with a further 2% inCorporate dentistry. This paralleled the 2017 breakdown.Regionally, as with 2017, Quebec (53%) and (41%) Atlantic respondents were more likelyto be in group practice with Western dentists (68%) and Ontario (67%) in solo Practice.Those currently in a solo practice stated they intend to remain there (91 -100% across allRegions), just as strongly as last year. Only Ontario showed any interest in either joining aMulti-practice (3.6%) or Corporate Dentistry Organization (5.8%).“In the next two years, do you intend to: Join a multi-practice (Group practice); Join a

Corporate Dentistry Organization; Remain in solo practice?”2017%2018%

Join a multi-practice 4.1 1.9Join a Corporate Dentistry Org 4.1 3.5Remain a solo practice 91.8 94.6

Response Regarding Multi-Practices“Are you: An Owner of a multi-practice (Group practice); or An Associate in a multi-practice (Group practice)?”

2017% 2018%An Owner of a multi-practice 46.3 45.1An Associate in a multi-practice 53.7 54.9Response from those involved in Group Practice was fairly evenly split between thoseowning a group practice and those who were Associates in one. As in 2017, Quebec (55%)had a higher percentage of Owners while Atlantic (64%) and Ontario (59%) had a higherpercentage of Associate respondents.

21

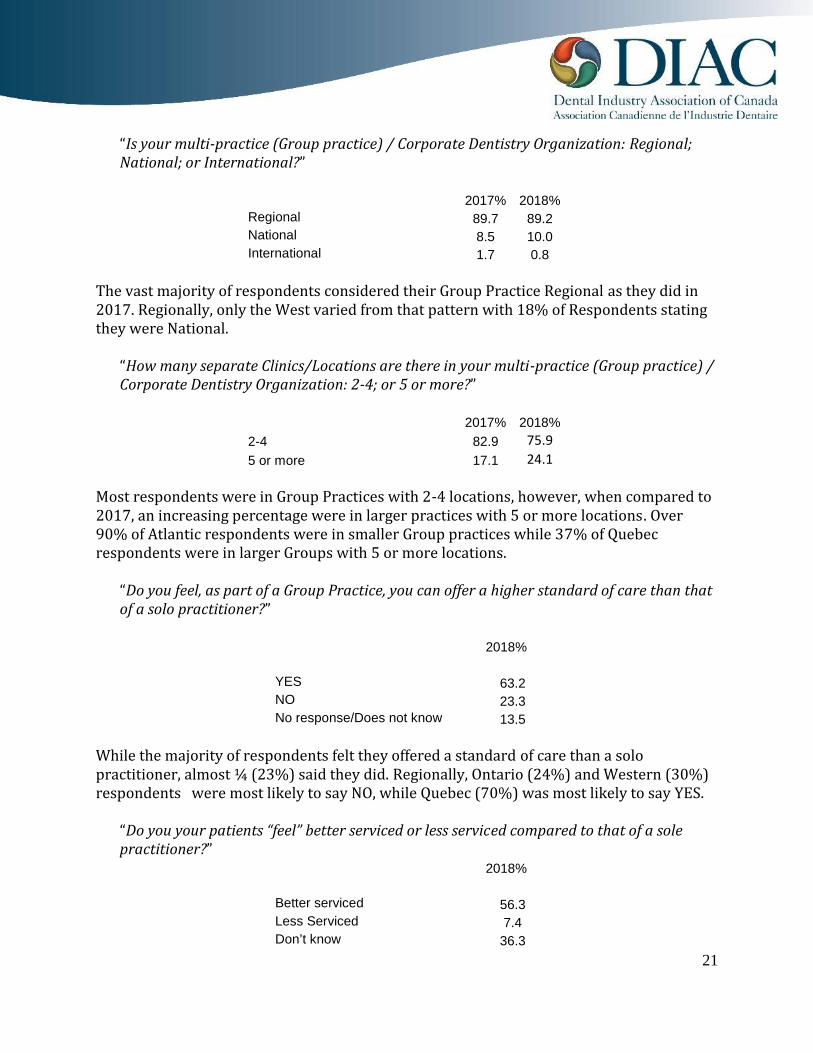

“Is your multi-practice (Group practice) / Corporate Dentistry Organization: Regional;National; or International?”

2017% 2018%Regional 89.7 89.2National 8.5 10.0International 1.7 0.8The vast majority of respondents considered their Group Practice Regional as they did in2017. Regionally, only the West varied from that pattern with 18% of Respondents statingthey were National.“How many separate Clinics/Locations are there in your multi-practice (Group practice) /

Corporate Dentistry Organization: 2-4; or 5 or more?”2017% 2018%

2-4 82.9 75.95 or more 17.1 24.1Most respondents were in Group Practices with 2-4 locations, however, when compared to2017, an increasing percentage were in larger practices with 5 or more locations. Over90% of Atlantic respondents were in smaller Group practices while 37% of Quebecrespondents were in larger Groups with 5 or more locations.“Do you feel, as part of a Group Practice, you can offer a higher standard of care than that

of a solo practitioner?”2018%

YES 63.2NO 23.3No response/Does not know 13.5While the majority of respondents felt they offered a standard of care than a solopractitioner, almost ¼ (23%) said they did. Regionally, Ontario (24%) and Western (30%)respondents were most likely to say NO, while Quebec (70%) was most likely to say YES.“Do you your patients “feel” better serviced or less serviced compared to that of a sole

practitioner?”2018%

Better serviced 56.3Less Serviced 7.4Don’t know 36.3

22

Similarly, while 56% of practitioners believed their patients felt better serviced and only7% less serviced, over 1/3 didn’t know.“What do you feel are the key advantages of a multi-practice (Group practice) / CorporateDentistry structure?”

2017% 2018%

Have associate support 51.1 57.1Buying Power 29.8 20.0Better hours for patients 6.4 12.4More schedule flexibility 5.3 2.9More variety in locations 2.1 NRReach more Patients 2.1 5.7Standardization 1.1 1.9Most respondents felt the support of their peers (57%) and buying power (20%) of theGroup Practice were still the primary benefits. However, there was a noticeable jump in thereadings for Better hours for patients and Reach more patients, which may relate toconcerns on patient volumes and level of business evidenced elsewhere in this report.“What do you feel are the main drawbacks of a multi-practice (Group practice) /

Corporate Dentistry structure?”2017% 2018%

Too many levels, too rigid 32.6 12.0Conflict with management style 20.0 29.0Too many staff 11.6 16.0Stress 10.5 2.0Less profit 7.4 5.0Consistency of Care 5.3 21.0Product demand 4.2 NRNone 3.2 9.0Standardization 2.1 2.0Patient Distribution 2.1 4.0Travel Required 1.1 NRThere was more diversity of opinion in terms of the drawbacks. The lack offlexibility/rigidity and stress (whether management style, staff or just stress itself) stillaccounted for most (65%) of the drawbacks stated. However, consistency of care wasmentioned by over 20% of respondents in 2018 (as compared to just 5% in 2017). Thisapplied across all Regions.

23

6. Years After Graduation to Set-up Your Practice

Interestingly enough, this year’s results have returned to historical norms, with 22% ofrespondents setting up their practices in the first year (26% in 2017, 29% in 2015, 32 % in 2013and a high of 44% in 2010). It would appear that 2016 was an anomaly in response. This samepattern of response applied across all Regions as it did last year with the exception of the Westwhere only 50% had set up by Year 3 (as opposed to 60% - 62% in the other Regions)..

If you are an owner, how many years after graduation did you buy/set-up your practice?

Years After Graduation Buy/Set Up Practice2011-2018 Study Periods

7. Number of Dentists in the Practice

How many other dentists are there in your practice?Here too we continue at historical norms as it was in 2017. In 2016, there was a far lowerpercentage of respondents identifying themselves as sole practitioners (23%) as opposedto36% in 2015 (and an average of 40% the last seven years and much lower from theaverage of 45.7% recorded from 1997-2007). For 2018, we have 36% as sole practitioners.Correspondingly, the number of practices with one additional dentist was at 23% (asopposed to 49.5% in 2016) corresponding to the 29.5% seen in 2015 (and the average28.9% for the last 12 years). Those practices with two and three additional dentistsaccounted for 19% (16.8% in 2016) and 8% (7.2% in 2016) respectively.

44%

34%

35%

32%

29%

7%

26%

22%

41%

45%

45%

50%

46%

76%

49%

51%

11%

11%

11%

10%

13%

9%

12%

13%

5%

10%

10%

8%

12%

7%

12%

14%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%20112012201320142015201620172018Within the 1st year 2-5 years 6-9 years 10 years or more

24

The dramatic increase in the percentage of respondents (11% this year and 13% in 2017)with five or more dentists (including the respondent) in their practice continued in 2018.This was 3.4% in 2016 and an average of 6.3% the last 14 years. This may reflect the higherproportion of associates and a “younger” dentist base in recent overall respondent bases.Number of Additional Dentists in Practice (2018)

Atlantic had the highest percentage of sole practitioners (46%) and the second highest(15%) of large 4 or more dentist practices. Quebec (18%) trended towards larger practicesat the other end of the spectrum. Ontario tended to have the highest percentage ofpractices with two or fewer practitioners by far (83%). Historically, in 2015, the Maritimes(10%) were more likely to have five or more dentists in their practices than Quebec (9.3%),Ontario (3.4%) and the West (0%). In 2013, the West and Ontario were more likely to havefive or more dentists in their practice.

36%23% 19%

8% 11%

Sole Practitioner One Two Three Four or more

25

8. Number of Operatories in the PracticeIn 2016, it appeared was a definite trend towards respondents having more operatories intheir practices with 82% having four or more that year (as opposed to 64.1% in 2015).However, since that time the number of practices with four or more operatories hasdeclined each year with 64% this year and72% in 2017.

How many operatories do you have in your office?

1%11%

21%20%

18%26%

OneTwo

ThreeFourFive

More than Five

26

Yet, 2018 also saw an uptick in the number of respondents with three or fewer operatoriesat 33% (28% in 2017). As the following graph illustrates, practices with three or feweroperatories had been generally in steady decline since the survey began, a real drop of40.2% since 1997 (58% in 1997 versus 17.8% in 2016).Three or Fewer vs Four or More Operatories 1997-2018

The trend of those having more than five operatories in the practice (15.4% from 1997 to2010) had levelled off over the last five years staying in a range of 20-25%. For 2017, thisincreased to an all-time high of 30% but has returned to historical norms in 2018 at 26%.Five or More Operatories 1997-2016

58%36%41%

64%

0%10%20%30%40%50%60%70%80%90%

Three or Fewer OperatoriesFour or More Operatories

15%30%

0%5%10%15%20%25%30%35%

27

Quebec (48%) and Atlantic (47%) were the most likely to have five or more operatorieswhile the majority of Western practices (72%) had four or more. Ontario (38%) was mostlikely to have 3 or less.Number of Operatories Planning to Add in Next 2 Years“How many operatories are you planning to add to your practice in the next 2 years?”This was a new question added in 2017 with response options: None, 1, 2, 3 or more.

2017% 2018%

None 77.6 72.01 12.2 10.92 3.6 7.53 or more 3.0 6.3No Response 3.6 3.4

As with 2017, the majority of respondents (72%) were planning to stick with the statusquo. However, 28% were planning on adding at least one operatory (with increasingpercentages year-over-year planning on adding more than one).Number of Operatories Planning to Add in Next 2 Years

None72%

One11%

Two8%3 or more6% No Response3%

28

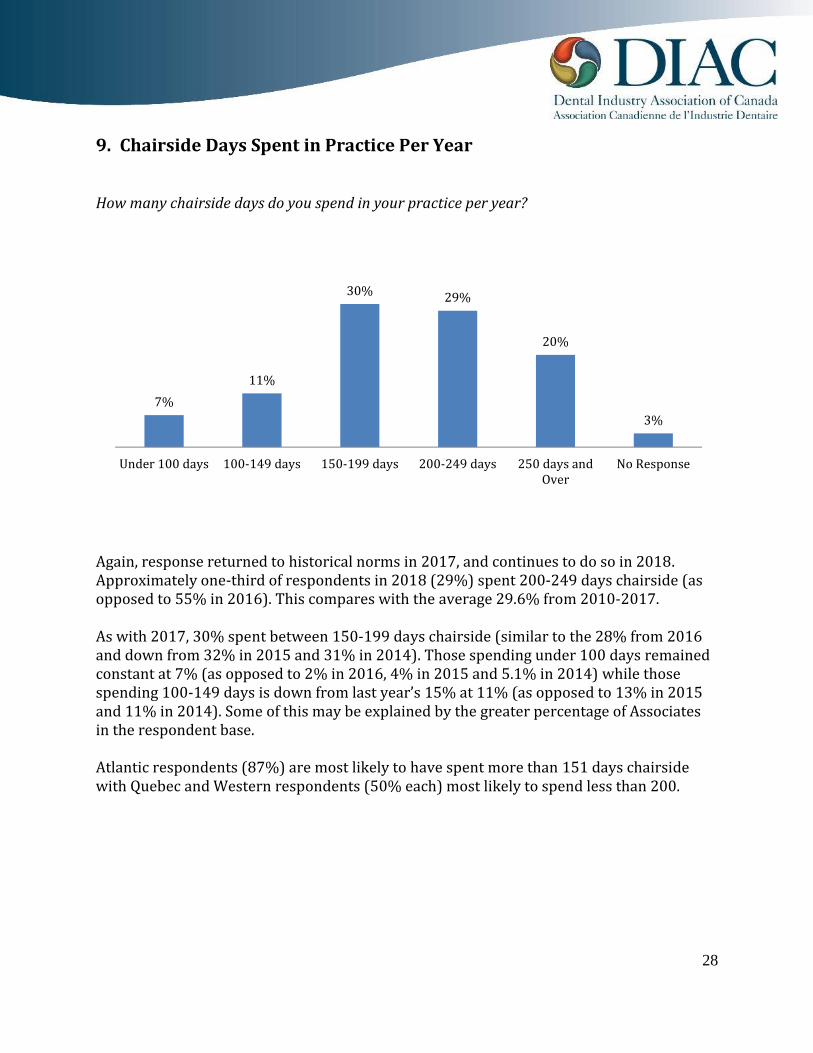

9. Chairside Days Spent in Practice Per Year

How many chairside days do you spend in your practice per year?

Again, response returned to historical norms in 2017, and continues to do so in 2018.Approximately one-third of respondents in 2018 (29%) spent 200-249 days chairside (asopposed to 55% in 2016). This compares with the average 29.6% from 2010-2017.As with 2017, 30% spent between 150-199 days chairside (similar to the 28% from 2016and down from 32% in 2015 and 31% in 2014). Those spending under 100 days remainedconstant at 7% (as opposed to 2% in 2016, 4% in 2015 and 5.1% in 2014) while thosespending 100-149 days is down from last year’s 15% at 11% (as opposed to 13% in 2015and 11% in 2014). Some of this may be explained by the greater percentage of Associatesin the respondent base.Atlantic respondents (87%) are most likely to have spent more than 151 days chairsidewith Quebec and Western respondents (50% each) most likely to spend less than 200.

7% 11%30% 29%

20%3%

Under 100 days 100-149 days 150-199 days 200-249 days 250 days andOver No Response

29

10. Average Patients Treated Per Day

In an average day, how many patients would you, as the dentist, treat?

Atlantic dentists have historically treated a slightly higher on average number of patientsper day than other regions. However, in 2018, Atlantic, Quebec and Ontario dentist wererelatively equal. Western respondents tended to treat more patients in the 15+ per dayranges.

Unlike last year, where a higher number ofspecialists responded, the GP/Specialist split onresponse has returned to historical norms. In 2017,comparisons were difficult as Orthodontists, forexample, treat a far higher number of patients perday than the average GP, while Oral Surgeons maytreat less. For 2018, it appears the trend towardstreating fewer patients per day has continued with89% of 2018 respondents stating they treated lessthan 15 patients a day (as opposed to 83% in 2017and an average of 78.6% over the last five years).

On an overall basis, dentists treated 11.3 patients inan average day comparable to the average of 12.5patients over the last ten years.

5 or less patients5%

6-10patients

62%

11-14 patients22%15-20 patients7%Over 20 patients5%

No Response0%

30

11. Hygiene Days

How many hygiene days do you have per week?

Despite a blip last year, those with three or more hygiene days per week has returned topast norms, levelled off again as it did the previous three years prior to 2017. Forty-sixpercent of respondents in 2018 had 5 or more hygiene days per week (as compared to 44% lastyear; 40% in 2016 and the average of 38.6% the last ten years), while 20% had 4 hygiene daysper week (slightly lower than the 23% in 2017 but in line with the average of 23.8% from2007-2016). The rates for those having one, two or three hygiene days per week hasreturned to historical norms of the 8% - 10% average over the last ten years.

8% 9% 10%20%

46%

7%1 day 2 days 3 days 4 days 5 or more days No Response

31

12. Demographic Shift in the Practice ProfileBeginning with the addition of a number of new questions in 2007-2008, an effort wasstarted to track the change, if any, in the “demographic profile” of the Canadian dentalpractice based on survey respondents’ answers. We now have ten years of data in manyprofile areas allowing some meaningful trend analysis over a period of time (as opposed tosingle year variances that may only be representative of a change in the mix of respondentsthat year or a short term shock to the marketplace). Beginning in 2016, a new dynamic hasbeen introduced with a change to on-line survey administration, yet many of the profilesgenerated remain the same: There are now more dentists per practice on average. The number of hygiene days per practice is increasing overall (with more days beingadded by those who only had one or two per week previously)We now see additional trends developing over the past few years: There are a growing percentage of respondents describing their location as Urban(now 62% as compared to 56% last year and 51% in 2016) (average of 53% overpast ten years). The drop off is in Suburban locations (falling to 22% from 29% lastyear and an average of 25% over the past 10 years) while Rural percentages havestayed relatively consistent over the past few surveys at 12% (but down from 17%average the past ten years). This result may be due to the growing number ofassociates answering the survey and/or a still “younger” demographic than surveysconducted earlier in the decade. There are still more operatories per practice then in the past but growth is slowingin the larger “4 or more operatory” practice. The percentage of those with “5 ormore operatories” has stabilized at around 26%. While only tracked for the past two years, there does seem to be a trend developingthat roughly 75% of respondents do not plan to add more operatories to thepractice over the next two years. However, it appears increasing percentages doplan to add 2 or 3 operatories, if they do move ahead with expansion. The trend towards treating fewer patients per day has continued with 89% treatingless than 15 patients a day. On average, dentists treated 11.3 patients a day in 2018as compared to the average 12.5 patients over the past 10 years.The trend for recent graduates to take longer to set up their practices has changed back tohistorical norms this year, perhaps been reinforced by a younger respondent demographic,more Urban practices reporting and a greater number of Associates responding.The percentage for newer graduates (0-3 years) setting up in practice within the first 3years has been dropping steadily since 2008, from around 40% at that time to 11% in2013. As might be expected, there was also a movement to a later set-up in the 4-9 years in

32

practice group, who have shown a tendency to delay until their 4th to 9th years in practice,although a far higher percentage of this group were able to set up in their first three years.As we move up the scale in terms of years in practice, we see that noticeably higherpercentages of these “older” groups were able to set up their own practice within 3 years ofactually joining the profession (50 – 65% of those over 20 years in practice).In 2014, we saw what appeared to be a switch back to historical norms with 40% of the 0-3year in practice respondents setting up in practice. However, on closer inspection, this wasa direct result of the older demographic profile of the new online respondents. In 2015, weagain saw a decline in the 0-3 results down to 29.4% setting up in their first three yearsand corresponding drops in those with longer times in dentistry. In 2016, 0-3 year resultsbasically stabilized at around 30%. At the same time, fewer and fewer dentists who havebeen practicing dentistry for 4-9 or 10-15 years were able to set up within the first threeyears, as the trend moved out over time. As the respondents length of time in the industrygrows, so too does the likelihood that they were able to set up their practice within theirfirst three years in the industry. In 2017, we saw a return to historical norms with a moreeven distribution of response as it was in 2015 and earlier. In 2018, the same historicalpattern remains but with a return to the decline in the 0-3 results (down to 22.7%) settingup in their first three years and corresponding drops in 4-9 and 10-15 years in dentistry.Length of Years to Set-up Practice by Years in Practice 2018

23%30% 24%

54% 50% 49%34% 38%

19% 20% 11%6%23% 10% 8%

0%10%20%30%40%50%60%70%80%90%

0-3 4 to 9 10 to 15 16 to 20 21 to 25 26+

10th Year & Over4th to 9th YearFirst 3 years

Years in Practice

Years to Setup Practice

33

Years to Set-up Practice Years in Practice2018 0-3 4 to 9 10 to 15 16 to 20 21 to 25 26+First 3 years 22.7 29.8 24.3 41.0 50.0 48.94th to 9th Year 0.0 34.0 37.9 19.2 19.8 10.710 Year & Over 0.0 0.0 6.1 23.1 10.3 8.32017 0-3 4 to 9 10 to 15 16 to 20 21 to 25 26+First 3 years 29.0 38.6 39.1 47.9 42.9 53.34th to 9th Year 0.0 27.2 36.2 16.7 12.7 17.710 Year & Over 0.0 0.0 5.8 15.6 11.1 8.9

2016 0-3 4 to 9 10 to 15 16 to 20 21 to 25 26+First 3 years 33.3 18.8 35.5 56.5 57.7 44.44th to 9th Year 0.0 24.9 44.7 29.0 7.6 22.210 Year & Over 0.0 0.0 5.3 4.8 7.7 33.3

2015 0-3 4 to 9 10 to 15 16 to 20 21 to 25 26+First 3 years 29.4 36.1 26.3 21.0 35.7 52.24th to 9th Year 0.0 36.1 29.0 42.1 38.0 16.310 Year & Over 0.0 0.0 18.4 10.5 19.0 7.7

2014 0-3 4 to 9 10 to 15 16 to 20 21 to 25 26+First 3 years 40.0 46.7 44.0 42.1 45.8 60.44th to 9th Year 0.0 23.3 35.3 31.7 31.4 13.710 Year & Over 0.0 0.0 2.9 13.2 10.4 5.52013 0-3 4 to 9 10 to 15 16 to 20 21 to 25 26+First 3 years 11.1 34.2 45.7 42.0 52.9 55.44th to 9th Year 0.0 43.8 23.0 38.7 25.5 10.910 Year & Over 0.0 0.0 8.6 9.7 9.8 8.32012 0-3 4 to 9 10 to 15 16 to 20 21 to 25 26+First 3 years 18.2 29.2 33.4 34.4 51.2 58.84th to 9th Year 0.0 41.8 30.0 18.8 13.9 18.210 Year & Over 0.0 0.0 13.3 15.6 11.6 5.62011 0-3 4 to 9 10 to 15 16 to 20 21 to 25 26+First 3 years 22.2 41.9 12.5 47.3 50.0 64.24th to 9th Year 0.0 23.3 45.8 16.8 34.2 10.810 Year & Over 0.0 0.0 4.2 11.1 7.9 2.42010 0-3 4 to 9 10 to 15 16 to 20 21 to 25 26+First 3 years 45.5 50.0 25.1 56.3 55.3 58.74th to 9th Year 0.0 17.9 47.0 15.6 23.4 13.010 Year & Over 0.0 0.0 6.3 9.4 8.5 8.5

34

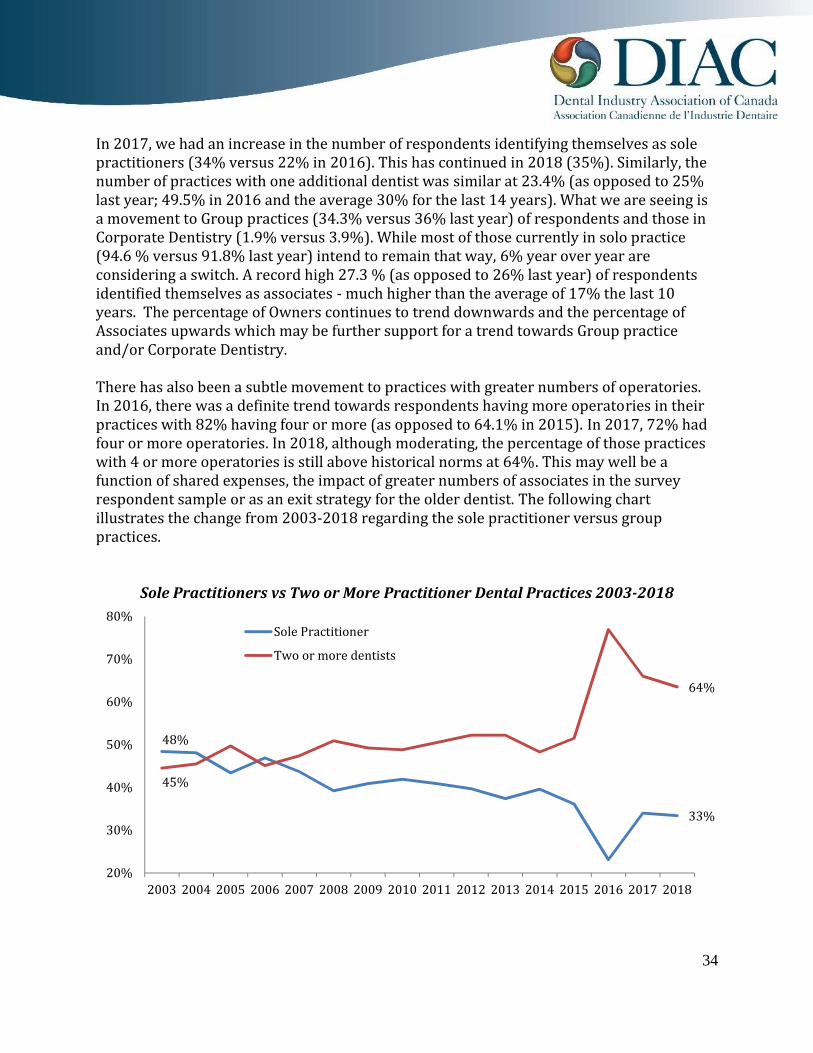

In 2017, we had an increase in the number of respondents identifying themselves as solepractitioners (34% versus 22% in 2016). This has continued in 2018 (35%). Similarly, thenumber of practices with one additional dentist was similar at 23.4% (as opposed to 25%last year; 49.5% in 2016 and the average 30% for the last 14 years). What we are seeing isa movement to Group practices (34.3% versus 36% last year) of respondents and those inCorporate Dentistry (1.9% versus 3.9%). While most of those currently in solo practice(94.6 % versus 91.8% last year) intend to remain that way, 6% year over year areconsidering a switch. A record high 27.3 % (as opposed to 26% last year) of respondentsidentified themselves as associates - much higher than the average of 17% the last 10years. The percentage of Owners continues to trend downwards and the percentage ofAssociates upwards which may be further support for a trend towards Group practiceand/or Corporate Dentistry.There has also been a subtle movement to practices with greater numbers of operatories.In 2016, there was a definite trend towards respondents having more operatories in theirpractices with 82% having four or more (as opposed to 64.1% in 2015). In 2017, 72% hadfour or more operatories. In 2018, although moderating, the percentage of those practiceswith 4 or more operatories is still above historical norms at 64%. This may well be afunction of shared expenses, the impact of greater numbers of associates in the surveyrespondent sample or as an exit strategy for the older dentist. The following chartillustrates the change from 2003-2018 regarding the sole practitioner versus grouppractices.Sole Practitioners vs Two or More Practitioner Dental Practices 2003-2018

48%33%45%

64%

20%30%40%50%60%70%80%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Sole PractitionerTwo or more dentists

35

B. Product Purchases and Usage

B.1 Dental Equipment

1. Stage of Office Digitization and Areas Digitized

What stage of ‘digitization’ has your office reached currently?

2017% 2018%

Fully paperless 37.3 32.7Not paperless 37.0 33.7In transition to paperless 25.7 33.7

The former questions “Do you have computer terminals in youroperatories?” AND “If plan to purchase, when?” asked in previoussurveys were revised in 2017 to new questions reflecting theimpact of digitization on the dental office.Respondents in 2017 and 2018 were now asked “What stage of‘digitization’ has your office reached currently?” with suppliedresponse options: Fully paperless, Not paperless, and In transitionto paperless. This was then augmented with a second question“Which areas of your office are digitized? (Please check off all thatapply)” with supplied response options: Charting, X-Ray, In theoperatories, and In the Private Office.In 2018, response was evenly split between Fully paperless(33%); Not paperless (34%) and In transition to paperless (34%).As with 2017, the overall trend is towards the paperless officewith 63% -66% either there now or moving there.

36

Which areas of your office are digitized? (Please check off all that apply)

2017% 2018%

X-Ray 84.5 86.7In the operatories 64.2 66.4In the Private Office 60.3 61.6Charting 52.8 53.4As might be expected, X-Ray was once again the top area digitized today but all areas wereover 50% (and increasing). Charting was the least likely to be digitized today at 53%.

32.7

33.7

33.7

Stage of "Digitization - 2018%

Fully paperlessNot paperlessIn transition to paperless

87% 66% 62% 53%

X-Ray In the operatories In the Private Office Charting

37

2. Utilization of Clinical Portion of Practice Management Software

For those with the applicable systems, are you utilizing the clinical portion of your practicemanagement software (i.e., in the operatory for the charting of treatment)?In 2016, almost three-quarters of respondents (73.9%) stated they were currently usingthe clinical portion of their practice management software. This was a real departure frompast results as compared to the 45% reported in 2015 (with a previous all-time high of45.5% in 2013 and up from 37.9% last year and the original 14.9% back in 2000). In 2017,this dropped back a bit to 59%, still higher than historical numbers and probably more inkeeping with a slower increase in adoption shown over the past decade,In 2018, those currently using declined at bit at 57% but those planning to use continuedits climb to 32% (above the ten-year average of 28.2%). Those stating they don’t plan touse the clinical portion of their practice management software continued to decline at 11%(compared to 16% last year).The higher percentages of Use and Plan to Use over the past few years are undoubtedly theresult of the on-line survey administration methodology (respondents predisposed to theuse of computerization) as well as the possible “younger” overall demographic of therespondent base.

Utilization of Clinical Portion of Practice Management Software 2006-2018

28%

57%

31% 32%42%

11%0%10%20%30%40%50%60%70%80%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018Currently Using Planning To Use Don't Plan To Use

38

Western (60%) and Ontario respondents (56%) were slightly more inclined to use theclinical portion while Atlantic (52%) and Quebec (47%) practitioners were less inclined.The majority of this year’s respondents who stated they plan to eventually use the clinicalportion of their software, plan to use it “soon” (50%) or when more productive (50%).Of those who don’t plan on using the clinical portion of their software, the most commonreason given was overwhelmingly “satisfied with current system” (85%) followed byReliability (5%) and Not Flexible Enough (5%). “Paper is easier” (41% in 2015 and the topreason for all but one of the past twelve years) was not mentioned in 2018 (although thatmay be the “current system”). Popular answers from previous surveys like retiring andCost were also not mentioned at all, again illustrating the impact of the new surveyadministration methodology.3. Dental Equipment Currently Owned and/or Plan to Buy

Which of the following equipment do you currently ownand/or plan to buy in the next two years?Respondents were first asked to identify whether theyowned particular types of equipment today. Multipleresponses were allowed and, in fact, most respondentsindicated more than one category. A new responseoption “Electric Handpiece” was added back into thelist of options in 2017 (was removed in 2011) for allquestions in this section. For the 2011 survey year,Caries Detection was removed replaced by DigitalImpression System and Cone Beam ComputedTomography.In general, 2018 respondents were more likely toselect more items, either as owning now or planningto purchase in the future.

39

Dental Equipment Own Today

1 Formerly worded as Integrated Office System2 Formerly worded as Office Management SystemThe same items had consistently ranked as the top three owned (albeit not always in thesame order) in surveys from 1998 to 2016. This year, the Electric Handpiece re-added in2017 was second highest at 71%, otherwise the order was the same as the previous twoyears. Digital Radiography (82%) was again the top item (same as 80% last year, 69% in2015, 63% in 2014 and representing a steady increase in ownership from 2.6% in 2000),followed by Electric Handpiece, then by a tie between Integrated Clinical & ManagementComputerized System (67%) (63% last year, 66% in 2016 and 56% in 2015) and Intra-OralCamera (67%) (63% last year, 72 % in 2016 and steadily increasing in ownership from34.6% in 2000).Office Management-only Computerized System (51%) was fifth (an average of 50% the lastten years). This was followed by Laser (Soft Tissue Management) (43%) (year-over-yearsteady increases from 10.4% in 2007) and Interactive Patient Education System at 28%. Ofthe two new categories introduced in 2011, Digital Impression System ownership stayedthe same at 21% (up from 6.2% in 2011). Cone Beam Computed Tomography was also upat 11% ownership (up from 2.5% in 2011). Laser (Hard and Soft Tissue Mgt) was thelowest at 9% in keeping with historical trends.

82%71%67%67%51%43%27%21%16%11%9%

Digital RadiographyElectric HandpieceIntegrated Clinical & Mgt Computer Sys1Intra-Oral CameraOffice Mgt-only Computerized System2Laser (Soft Tissue Mgt)Interactive Patient Education SystemDigital Impression SystemChair Side Cad-Cam (fixed restorations)Cone Beam Computed TomographyLaser (Hard and Soft Tissue Mgt)

40

Dental Equipment Plan to Buy

Respondents were then asked to identify the pieces of equipment they planned to buywithin the next two years. Again, multiple responses were allowed. Again this year, the topchoice was Digital Impression System at 35% (up from 30% last year and. Up from the 26%average over the past 7 years). Electric Handpiece took a huge jump from 11% last year to29% and second place this year. Otherwise the order of popularity in items was much thesame as in 2017. Interactive Patient Education System is now third at 20% (17% in 2016).Cone Beam Computed Tomography (19%) was fourth most popular.Chair Side CAD-CAM has remained around its historical norm at 16% followed by Laser(Soft Tissue Management) (16%). Laser (Hard and Soft Tissue Mgt) jumped to 16% from8% last year, followed by Intra-Oral Camera (13% as it was in 2017 and 2016). IntegratedClinical & Management Computerized System was next at 10% (9% in 2016). DigitalRadiography continues to trend down from a high of 31% in 2007 and is now at 10%. Ofcourse, this also reflects the on-going growth in actual ownership for this equipment. OfficeManagement-only Computerized System was the final choice at 6% (3% last year), againbecause of actual current ownership.

35%29%20%20%16%16%16%13%10%10%6%

Digital Impression SystemElectric HandpieceInteractive Patient Education SystemCone Beam Computed TomographyChair Side Cad-Cam (fixed restorations)Laser (Soft Tissue Mgt)Laser (Hard and Soft Tissue Mgt)Intra-Oral CameraIntegrated Clinical & Mgt Computer Sys.1Digital RadiographyOffice Mgt-only Computerized System2

41

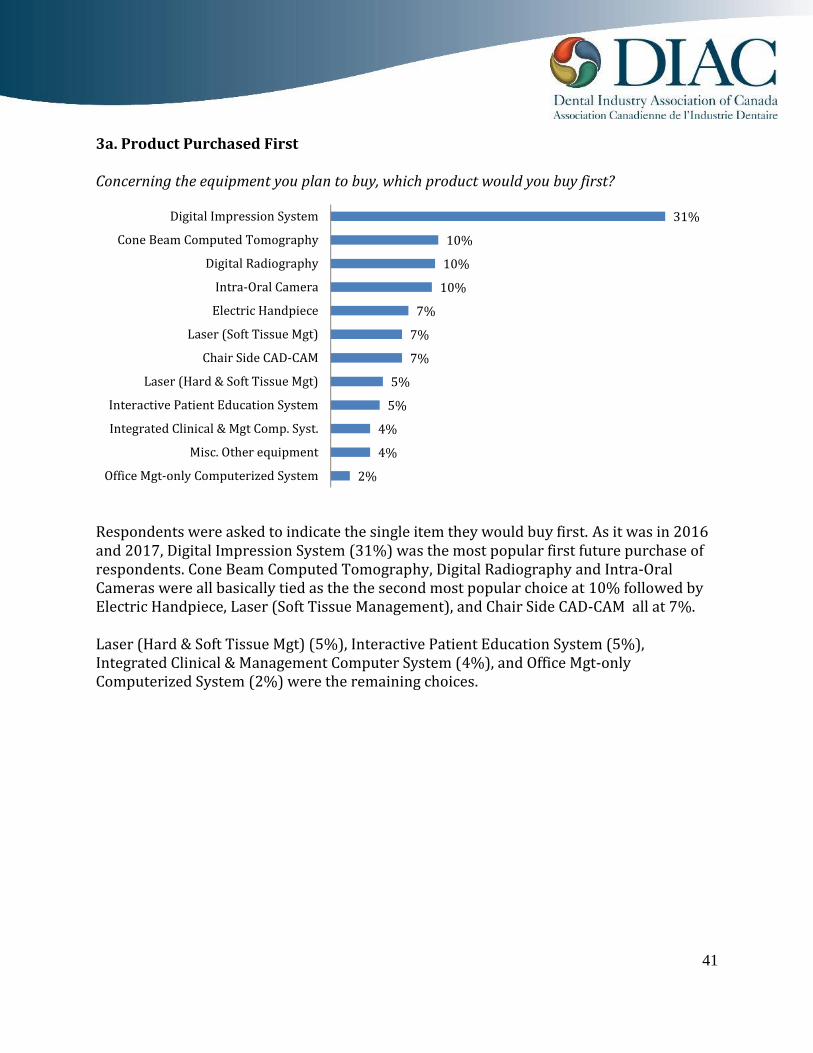

3a. Product Purchased First

Concerning the equipment you plan to buy, which product would you buy first?

Respondents were asked to indicate the single item they would buy first. As it was in 2016and 2017, Digital Impression System (31%) was the most popular first future purchase ofrespondents. Cone Beam Computed Tomography, Digital Radiography and Intra-OralCameras were all basically tied as the the second most popular choice at 10% followed byElectric Handpiece, Laser (Soft Tissue Management), and Chair Side CAD-CAM all at 7%.Laser (Hard & Soft Tissue Mgt) (5%), Interactive Patient Education System (5%),Integrated Clinical & Management Computer System (4%), and Office Mgt-onlyComputerized System (2%) were the remaining choices.

31%10%10%10%7%7%7%5%5%4%4%2%

Digital Impression SystemCone Beam Computed TomographyDigital RadiographyIntra-Oral CameraElectric HandpieceLaser (Soft Tissue Mgt)Chair Side CAD-CAMLaser (Hard & Soft Tissue Mgt)Interactive Patient Education SystemIntegrated Clinical & Mgt Comp. Syst.Misc. Other equipmentOffice Mgt-only Computerized System

42

3b. Product Purchased Second

Which product would you buy second?

Respondents were then asked to indicate the single item they would buy second. As hasbeen the case with past surveys, a significantly lower number (approximately 41%) ofrespondents answered this question versus a 62% response rate for the product theywould purchase first. However, as with 2016 and 2017, significantly more respondentsoverall specified a product for both parts of this question as opposed to previous years.The most popular “second purchase choice” in 2018 was Digital Impression System (16%)(18% in 2017 and 11.3% in 2016). Electric Handpiece jumped to second place at 14% (9%in 2017). Chair Side CAD-CAM was again third at 13% (12% in 2017 and up from anaverage of 6.5% the previous ten years), followed by Interactive Patient Education System(12%) (14% in 2017). Cone Beam Computed Tomography (2015’s first place and secondin 2016) were at a rounded 9% as was Laser (Soft Tissue Management), followed by Intra-Oral Cameras (7.3%) (11% in both 2016 and 2017) and Laser (Hard and Soft TissueManagement) (6.5%). Integrated Clinical & Management Computerized System (5%),Digital Radiography (4% and continuing a downward trend since it was number one withan average of 20.7% from 2007-2009), Misc. Other equipment (3%) and OfficeManagement-only Computer (2%) were the remaining choices.

16%14%13%12%9%9%7%7%5%4%3%2%

Digital Impression SystemElectric HandpieceChair Side CAD-CAMInteractive Patient Education SystemLaser (Soft Tissue Mgt)Cone Beam Computed TomographyIntra-Oral CameraLaser (Hard & Soft Tissue Mgt)Integrated Clinical & Mgt Comp. Syst.Digital RadiographyMisc. Other equipmentOffice Management-only Computer

43

4a. Preferred Equipment Service Provider

Who is your preferred equipment service provider?

The vast majority of respondents in 2018 preferred a Full Service Dealer (86%)(comparable to the average of 85% for the last nine years), while 9% preferred anIndependent Technician (also the same average as the last nine years) and 5% favoured theManufacturer (continuing an upward trend over the six years previous to 2017 growingfrom 1.9% in 2011).Atlantic (94%) and West (89%) were more likely to use a Full Service Dealer than otherregions. Ontario (11%) returned to being the top region using an Independent Technicianas it had been nine out of the ten years prior to 2017 and the top region using theManufacturer (7%). After a 19% reading in 2017 for Quebec use of an IndependentTechnician, this reading reverted back to historical norms in 2018 at 7%.

Full ServiceDealer

86% IndependentTechnician9%Manufacturer5%

44

4b. Preferred Equipment Service Provider – Service Contract or As Needed

Do you prefer a service contract, to have service as needed or other?

In 2016, there was almost a 50/50 split on the question of preferring a service contract orto have service as needed. For 2017 and 2018, response appears to have returned tohistorical norms. In 2015, over sixty percent (62.4%) (up from 60.1% in 2014, 59.5% in2013 and 61% in 2012 and an average of 57.3% from 2007-2011) of respondents overallpreferred to have service as needed, while 32.7% preferred a service contract (the exactsame average as the previous four years and similar to the average of 34.3% from 2007-2010). For 2018, a new all-time high of 64% of respondents preferred service as neededwhile 36% preferred a service contract.Quebec (56%) respondents were more likely to have a service contract again this year. Ineight of the last nine years, Quebec respondents have been most likely to have a servicecontract. On the other hand, Atlantic (65%), Western (59%) and Ontario (57%)respondents were more likely to have service as needed.

to haveservice asneeded63.9%

a servicecontract36.1%

45

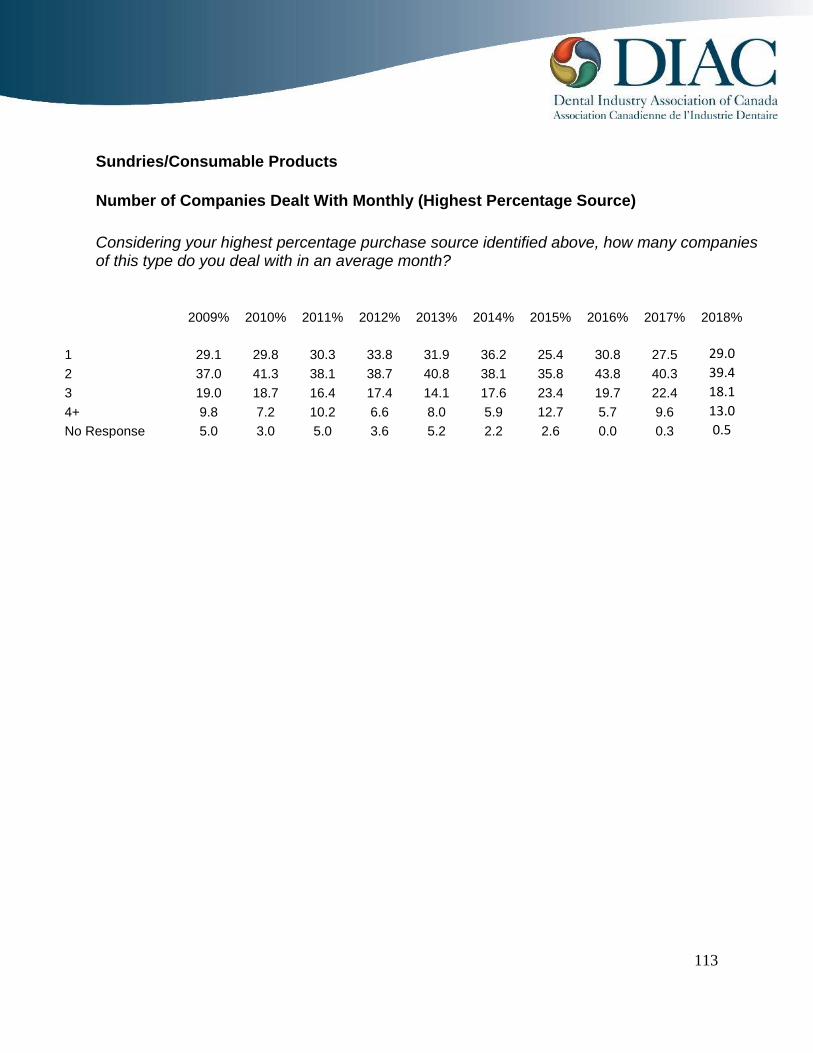

B.2 Sundries/Consumable Products

Source for Sundry/Consumable Purchases

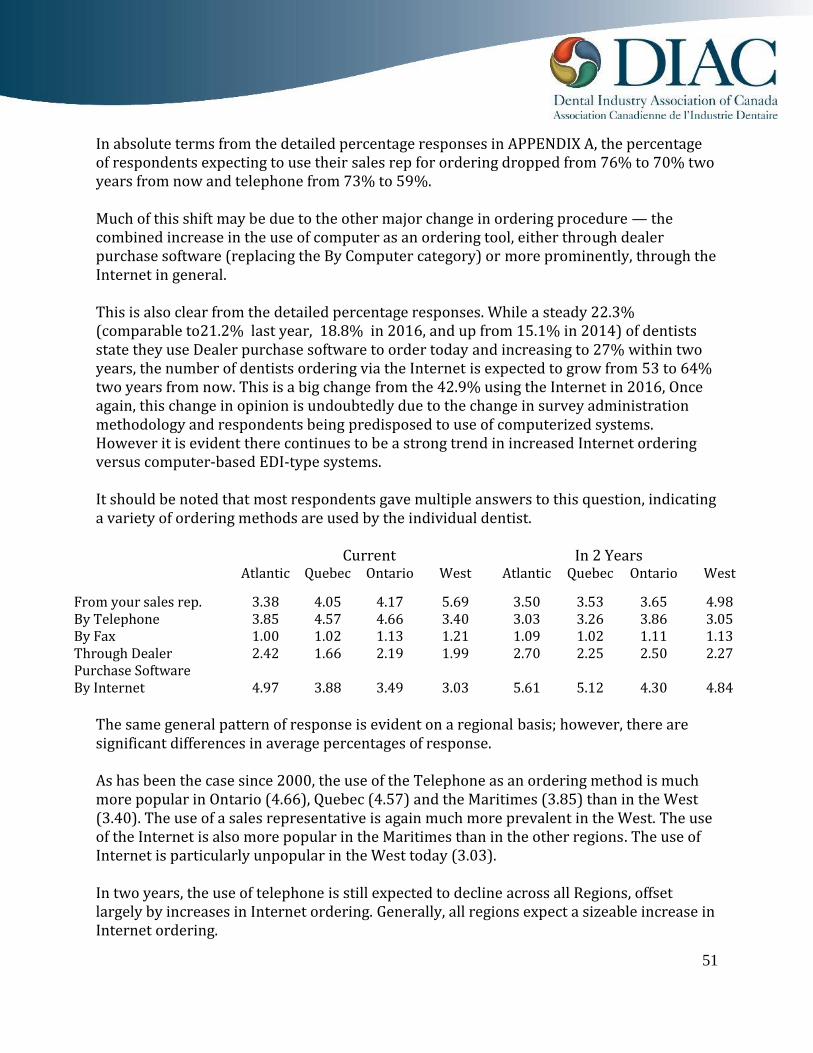

Preferred Source

What approximate percentage of your current sundries/consumables (e.g., paper products,impression material, amalgam, restoratives, cements, diamonds, etc.) purchases do you makefrom the following sources? What would you expect these percentages to be two years fromnow?Respondents were asked to state the percentage of their sundries/consumables theypurchased from particular sources today and what they expected those percentages to betwo years from now. The detailed percentage breakdown of response in 10% ranges bysource is provided in the APPENDIX attached to this report. However, the average responseby source (0out of 10) is a more valuable indication of dentist buying habits.

Average Response by Source for Sundries/ConsumablesCurrent2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018Full Service Dealer 9.11 9.19 9.13 9.09 8.77 8.92 9.06 9.07 8.99 9.22 9.17 9.02 8.99Consumables Only Dealer NR NR NR NR NR 1.98 2.11 1.98 2.07 2.11 1.87 2.09 2.07Grey Market Dealer NR NR NR 1.14 1.24 1.38 1.19 1.19 1.22 1.18 1.21 1.25 1.22Cooperative Buying Group 1.26 2.25 2.27 2.23 1.13 1.17 1.15 1.21 1.15 1.09 1.09 1.16 1.15Mail Order 2.20 2.15 2.20 1.96 1.49 1.34 1.27 1.38 1.31 1.20 1.27 1.21 1.31Direct From Manufacturer 1.86 1.80 1.78 1.84 1.68 1.66 1.69 1.65 1.70 1.61 1.61 1.80 1.70

46

In 2 Years2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018Full Service Dealer 8.72 8.81 8.76 8.80 8.50 8.67 8.81 8.82 8.71 8.93 8.26 8.65 8.71Consumables Only Dealer NR NR NR NR NR 2.01 2.12 1.99 2.09 2.22 2.08 2.13 2.09Grey Market Dealer NR NR NR 1.17 1.27 1.39 1.19 1.23 1.22 1.16 1.22 1.28 1.22Cooperative Buying Group 1.33 2.37 2.37 2.45 1.23 1.25 1.23 1.21 1.18 1.20 1.29 1.29 1.18Mail Order 2.31 2.26 2.36 2.01 1.52 1.40 1.34 1.47 1.35 1.20 1.42 1.33 1.35Direct From Manufacturer 2.06 1.94 1.88 1.96 1.78 1.75 1.75 1.71 1.81 1.67 2.08 1.88 1.81These results show the general pattern of preference by type of supply outlet since the2005 study. For the 2011 survey, Consumables Only Dealer was added to the list ofresponse categories and Other Authorized Dealer removed as a category. In 2007, Co-operative was added, while Grey Market Dealer was added as a new response category forthe 2009 survey. Buying Group and Co-operative were merged into one category in 2010(Please note: results from 2007 to 2009 for “Cooperative Buying Group” have inflatedvalues as they have been combined for year-to-year comparison purposes). This year, asthey have since 1998, the Full Service Dealer accounts for the majority of current productpurchases. In general, the same pattern of response as in previous years applies to 2018 forcurrent purchases.The second part of the question regarding respondents expected preferred source in twoyears’ time both confirms the Full Service Dealers dominance and still presents the sameinteresting paradox as outlined earlier in previous reports (although the types of sourcehave varied as the options provided have varied).Although the rating for Full Service Dealer has returned to historical norms in 2017 (andcontinues to do so in 2018), when comparing the individual survey response (currentversus expected future source in any given year) over the years, it would appear that somesmall percentage of dentists expect to be utilizing a source other than Full Service Dealer intwo years (it would appear the significant drop in the 2016 reading for Full Service Dealerswas in fact an anomaly, possibly due to the smaller respondent count and the differentsurvey administration methodology that year). The results for Cooperative Buying Group,Mail Order and Direct from Manufacturer (a significant increase) show an expectedincrease in share in two years. Yet, in terms of their actual current buying behaviour, aconsistently large share of dentists buy from Full Service Dealers with correspondingsmaller shares for Consumables Only Dealers, Cooperative Buying Group, Mail Order andDirect from Manufacturer. The paradox is why some respondents continue to feel (evenwith the new demographic profile) they will change purchase source in the future and yetdo not do so. The answer may lie later in this section where they continue to give “price” asthe driving force behind a desire to change when asked for their reason. The factor ofpurchases from multiple sources should also be kept in mind.

47