department of revenue .bridgestone… · 2013-06-12 · department of...

TRANSCRIPT

\,,

STATE OF FLORIDA

DEPARTMENT OF REVENUE

.BRIDGESTONE/FIRESTONE, INC.

Petitioner,

v.

DEPARTMENT OF REVENUE

Respondent.

)))))))

))))

CASE NUMBER 92~2483

DcR Q3-'22.. FoF

FINAL ORDER

This cause came on before the Department of Revenue for

the purpose of issuing a final order. The Hearing Officer

assigned by the Division of Administrative Hearings submitted

a Recommended Order. A copy of the Recommended Order is

attached to this Final Order. Petitioner timely filed

Petitioner's Exception To·Recommended Order. Respondent

timely filed Respondent's Exceptions To Recommended Order And

Supporting Memorandum of Law; DOR's Reply To Petitioner's

Proposed Substituted Order And supporting Memorandum Of Law;

and DOR's Proposed Substituted Order. A copy of these

documents are attached to this Final Order.

Pursuant to Chapter 120, Florida Statutes, the Department

has jurisdiction of this cause.1.

At issue is whether a real property lease in "form," which

constituted part of a sale/leaseback transaction between The

Firestone Tire and Rubber Company, as predecessor to

Bridgestone/Firestone, Inc., and Firestone Real Estate

Leasing corporation (FIRELCO) should be treated as a mortgage

in "substance" not sUbject to the sales and use tax.

The Hearing Officer in his Recommended Order reconmended

that the Department enter a Final Order withdrawing the sales

and use tax assessment against Petitioner.

The Department, after a thorough review of the entire

record in this case, adopts the recommendation of the Hearing~-,

(\ Officer that a Final Order be entered withdrawing the'-......_/

assessment against Petitioner. However, the Department makes

certain rejections and modifications of the Hearing Officer's

statement of the Issue, Preliminary statement, Findings of

Fact, and Conclusions of Law.

statement of the Issue

The Department adopts and incorporates in this Final Order

the statement of the Issue as expressed in DOR's Proposed

substituted Order filed by Respondent.

In rejecting the Hearing Officer's statement of the Issue

the Department is in essence sUbstituting the word "mortgage"

2.

((

(~

for the term "financing statement" as used by the Hearing

Officer.

preliminary statement

Department adopts the Preliminary statement of DOR's

Proposed Substituted Order filed by Respondent. In rejecting

the Hearing Officer's Preliminary statement the Department is

again sUbstituting the word "mortgage" for the term

"financing statement" as used by the Hearing Officer. This

modification is made on the basis that the term "mortgage" is

given a statutory definition as expressed in s. 697.01, F.S.,

whereas the term financing arrangement" has no precise

meaning.

Findings of Fact

The Department adopts and incorporates in this Final Order

all of the Findings of Fact 1 through 12 in the Recommended

Order.

The Department modifies Finding of Fact 13 to correctly

identify FIRELCO rather than Firestone in line 2 as the

entity which had been assessed documentary stamp taxes, and

to identify FIRELCO rather than Firestone in lines 4 and 5 as

the party who received a notice of decision, and entered into

a closing agreement.

3.

The Department adopts and incorporates in this Final Order

Findings of Fact 14 through 29 in the Recommended Order.

Conclusions of Law

The Department adopts and incorporates in this Final Order

Conclusions of Law 30 through 32 in the Recommended Order.

The Department rejects Conclusions of Law 33 in the

Recommended Order and adopts Conclusion of Law 33 as it

appears in DOR's Proposed Substituted Order. The Department

rejects the Hearing Officer's conclusion because of the

interchangeable use of the terms "mortgage" and "financing

arrangement" rather than the use of the term "mortgage" which

is statutorily defined. Also, the Department takes exception

to the phrase "sale/leaseback agreement" finding that no

document was entered into evidence bearing that title.

Further, the Department takes exception to the Hearing

Officer's recommendation that the Department look to federal

income tax case law for additional guidance.

The Department adopts Conclusions of Law 34, 35, and 36 in

the Recommended Order.

The Department rejects Conclusions of Law 37, 38, and 39

in the Recommended Order because these conclusions suggest

the Department look to federal. income tax case law in

4.

()..,~-_./

administering the tax imposed in Chapter 212, Florida

statutes. In sUbstitution, the Department adopts a new

Conclusion of Law 37 as expressed in DOR's Proposed

substituted Order because Chapter 212, F.S., does not

"piggyback" federal income tax law as does Chapter 220,

Florida statutes.

Further, the cases construing what constitutes a

"mortgage" under s. 697.01, F.S., provides a better basis for

determining what constitutes a "lease" under Chapter 212,

F~S., than does federal income tax law. Upon these bases the

Department rejects the Hearing Officer's recommendation of

reliance on the principles, reasoning, and factual analysis

found in federal tax law and adopts the new Conclusion of Law

37 which appears in DOR's Proposed substituted Order.

The Department adopts and incorporates in this Final Order

the Hearing Officer's Conclusions of Law 40.

with the exception of a modification of the second

sentence the Department adopts and incorporates Conclusion of

Law 41 in this Final Order. The second sentence shall read:

While DOR is entitled to rely on such books and records to

the extent as allowed by law, it is apparent in Zero, the

taxpayer's "corporate books" carried an entry reflecting

rental payments to its parent corporation."

5.

RUling on Petitioner's Exception to Recommended Order

The Department rejects Petitioner's exception to the

Hearing Officer's Findings of Fact 13. First, the

Department restates what appears above in the modification of

Findings of Fact 13 that FIRELCO rather than Firestone should

be identified in this finding. Further, the question as to

whether the payment of documentary stamp tax on a document

other than the lease is to be considered as a bar to the same

tax on the lease was not before the Hearing Officer~

RUlings on Respondent's Exceptions to Recommended Order

The Department adopts Respondent's exception to the

Hearing Officer's Finding of Fact 13 and states that this

exception corrects a clerical error in that FIRELCO rather

than Firestone should have been identified as the entity

which had been issued an assessment for documentary stamp

tax. The Department adopts Respondent's exceptions to the

Hearing Officer's Conclusions of Law 33, 37, 38, 39. The

Department adopts Respondent's new Conclusion of Law 37.

conclusion

After a thorough review of the entire record, in which it

is determined that the document at issue was a mortgage, the

6.

Department notes that no finding in this matter concludes

that all similar agreements are to be characterized as

mortgages, and it reserves determination of the taxability

of future sale and leaseback transactions based on the facts

of such transactions and consideration of the applicable law.

Based upon the foregoing, it is ORDERED:

The recommendation of the Hearing Officer that the

assessment against Petitioner be rescinded or withdrawn is

sustained.

Notice of Rights

Any party to this Final Order has the right to seek

jUdicial review of the Final Order as provided in Section

120.68, Florida Statutes, by filing of a Notice of Appeal as

provided in Rule 9.110, Florida Rules of Appellate Procedure,

with the Clerk of the Department in the Office of General

Counsel, Post Office Box 6668, Tallahassee, Florida

32314-6668 and by filing a copy of the Notice of Appeal,

accompanied by the applicable filing fees, with the

appropriate District Court of Appeal. The Notice of Appeal

must be filed within 30 days from the date this final order

is filed with the Clerk of the Department.

7.

~,\. )'--./

o

DONE AND ENTERED IN TALLAHASSEE, LEON COUNTY, FLORIDA

this 5Y day of November ,1993.

certificate of Filinq

I HEREBY CERTIFY that the foregoing FINAL ORDER has beePhfiled in the official records of the Department this ~~=- _day of November, 1993.

copies furnished to:

L.H.FuchsExecutive DirectorDepartment of RevenueRoom 104Carlton BuildingTallahassee, Florida 32399-0100

Donald AlexanderHearing OfficerDivision of Administrative HearingsThe DeSoto Building1230 Apalachee ParkwayTallahassee, Florida 32399-1550

Jeffery M. Dikman, EsquireJarrell L. Murchison, EsquireDepartment of Legal AffairsThe Capitol - Tax sectionTallahassee, Florida 32399-1050

8.

..,. ~ '.-)

Linda Lettera, EsquireGeneral CounselDepartment of Revenue201 Carlton BuildingTallahassee, Florida 32399-0100

Benjamin K. Phipps, EsquireFine Jacobson Schwartz Nash & BlockPost Office Box 1351Tallahassee, Florida 32302

Attachments:

Hearing Officer's Recommended OrderDOR's Proposed Substituted OrderRespondent's Exceptions to Recommended Order and Supporting

Memorandum of LawPetitioner's Exception to Recommended OrderDOR's Reply to Petitioner's Proposed Substituted Order and.

Supporting'Memorandum of Law

9.

\

STATE OF FLORIDADEPARTMENT OF REVENUE

BRIDGESTONE/FIRESTONE, INC.,

Petitioner,

vs.

DEPARTMENT OF REVENUE,

Respondent.

DOAH CASE NO. 92-2483

DOR'S PROPOSED SUBSTITUTED ORDER

Pursuant to notice, the above matter was heard before the

Division of Administrative Hearings by its duly designated

Hearing Officer, Donald R. Alexander, on April 29 and 30, 1993,

in Tallahassee; Florida. The Hearing Officer entered his

recommended "order on August 10, 1993. DOR and Petitioner timely

r-\() took exceptions to the recommended order. This proposed.'-......-0'-

substituted order solely reflects the exceptions taken by DOR.

APPEARANCES

For Petitioner: Benjamin K. Phipps, EsquirePost Office Box 1351Tallahassee, Florida 32302

For Respondent: "Leonard F. Binder, EsquireJarrell L. Murchison, EsquireDepartment of Legal AffairsThe Capitol-Tax SectionTallahassee, Florida 32399-1050

STATEMENT OF THE ISSUE

The ultimate issue is whether a real property lease in

"form," which constituted part of a sales/leaseback transaction

between The Firestone Tire and Rubber Company, as predecessor to

Bridgestone/Firestone, Inc., and Firestone Real Estate Leasing

Corporation should be treated as a mortage in "substance" not

subject to the sales and use tax.

Although DOR has adopted the recommendation of the Hearing

Officer that this particular sales/leaseback transaction is not

subject to the sales and use tax, this order should not be

construed as broadly applying to sales/leaseback transactions in

general. The Hearing Officer's findings of fact were based upon

the unique facts ana circumstances of this case, including

specific provisions contained in the pertinent documentation at

issue. The determination of whether any other sales/leaseback

transaction would be taxable for sales and use tax would

similarly depend upon the unique facts and circumstances in the

particular transaction.

PRELIMINARY STATEMENT

This matter began after an audit was conducted by

o Respondent, Department of Revenue (DOR), of the taxes paid by

Petitioner, Bridgestone/Firestone, Inc., during the period June

1, 1985, through December Xi, 1985-:-The-prLl.cTpaTIs'sue 'in the

,audit is whether a trartsaction between the predecessor of

Petitioner and Firestone Real Estate Leasing Corporation should

be treated as a mortgage or as a true lease. On the premise that

the transaction was a lease, DOR has proposed to make a, ,

substantial assessment on petitioner. After various informal

appeals were unsuccessful, Petitioner filed its petition for

formal hearing challenging the proposed assessment. The parties

have agreed that the total amount of taxe$, interest and

penalties in dispute are $l j 004,848.27.

The matter was referred by respondent to the Division of

Administrative Hearings on April 23, 1992, with a request that a

- 2 -

( hearing officer be assigned to conduct a formal hearing. By

notice of hearing dated May 11, 1992, a final hearing was

scheduled on September 22, 1992, in Tallahassee, Florida. At the

parties' request, the matter was rescheduled to December 1, 1992,

and then again to March 2, 1993. By agreement of the parties,

the matter was again rescheduled to April 15 and 16, 1993, and

finally to April 29 and 30, 1993, at the same location.

At final hearing, Petitioner presented the testimony of Dr.

William A. Hillison, a professor at the Florida State University

(FSU) school of business and accepted as an expert in the

analysis of financial transactions from accounting standards;

Donald J. Weidner, a professor and dean of the FSU school of law

and accepted as an expert in factors to be considered in making a

~ determination as to whether a transaction is a sale or a

mortgage; David F. Seele, petitioner's tax comptroller; and

Donald T. Allen, supervisor of pet~tioner's tax department.

Also, it offered petitioner's exhibits 1-7. All 8xhibits were

received in evidence except exhibit 6. Respondent presented the

testimony of Richard Unen, a DOR tax auditor; Peter J. Steffens,

DOR revenue opportunity research administrator; and Joseph R.

Boyd, a Tallahassee attorney and board certified in real property

law. Also, it offered Respondent's exhibits 1-10 and 11A-11J.

All exhibits were received in evidence.

~

The transcript of hearing (four volumes) was filed on May

26, 1993. Proposed findings of fact and conclusions of law were

originally due on June 26, 1993. By 9greement of the parties,

this time was extended to July 2, 1993, and the parties timely

filed their proposed orders on that date.

- 3 -

o

FINDINGS OF FACT

Based upon all of the evidence, the following findings of

fact are determined. With the exception of certain relatively

minor changes to paragraphs 13 and 29 below, all of the findings

of fact made by the Hearing Officer are adopted verbatim below:

A. Background

1. Petitioner, Bridgestone/Firestone, Inc. (petitioner or

Firestone), is a foreign corporation doing business in Florida.

During the relevant time period, it owned more than one thousand

retail outlets throughout the country, including thirty-nine in

Florida, which sold tires and provided additional automotive

services. Petitioner was then known as The Firestone Tire and

Rubber Compani.

2. Respondent, Department of Revenue (DOR), is the state

agency charged with the responsibility of enforcing the Florida

Revenue Act of 1949, as amended. Among other things, DOR

performs audits on taxpayers to insure that all taxes due have

been correctly paid. To this end, a routine audit was performed

on petitioner covering the audit period from June 1, 1985,

through December 31, 1988.. .

3 .. During th~ course of the audit, a DOR field auditor

reviewed a transaction that had occurred on October 22, 1985,

between Firestone and Firestone Real Estate Leasing Corporation

(FIRELCO) . In very broad terms, the agreement provided for the

usale of a substantial number of assets (land and buildings) to

FIRELCO and a leaseback of the assets ,by Firestone. After

concluding that this agreement was a lease arrangement between

- 4 -

B. The Transaction and its Genesis

4. In 1979 Firestone hired as president an executive from

outside the company for the first time. Previously, only members

of the Firestone fa~ily. or career Firestone employees had.held

that position. Deciding that Firestone should de-emphasize its

manufacturing operat~ons and concentrate on its retail

operations, the ne~ president quickly closed seven tire plants

and opened a number of new retail outlets with an emphasis on

stores in the Sunbelt states. A decision was also made to

,~~ finance this expansion by using the real estate as collateral.

- 5 -

o 5. The first group of stores was paid for by selling them

to a real estate investment trust (REIT) known as One Liberty

Firestone. This form of financing had been recommended for

several reasons by Merrill Lynch, Firestone's investment banker.

First, it gave Firestone "access to the public market". Second,

o

it allowed Firestone to use off-balance sheet financing, that is,

it removed the debt associated with the financing from

Firestone's balance sheet and thus improved its debt-equity

ratio. Finally, Firestone retained operations of the stores

through a lease with the REIT. For financial reporting and state

and federal tax purposes, the transaction was treated as a true

sale. The payments by Firestone to the REIT were treated as rent

on the books of both corporations.

6. Because Firestone had -lost the benefit of the

appreciation of the value of the stores under the REIT form of

financing, it decided to find a better form of financing for its

next acquisition of retail outlets. After considering several

alternatives, Firestone's then treasurer, Jack Rooney, and its

manager of domestic financing, Suzanne Palmer, concluded that the

new financing must meet several objectives, including retaining

of appreciation in value of the new properties, using the lowest

cost of financing available, continuing off-balance sheet

financing so that the assets and debt would not be carried on

Firestone's balance sheet, and using the real estate as security

for the financing. To meet these objectives, Rooney and Palmer

selected a sale/leaseback form of tra~saction to be structured so

that (a) it could be reported off-balance sheet, (b) it would be

- 6 -

(~ financed through the sale of commercial paper (unsecured" -_/

promissory notes), and (c) the control of the properties would be

retained by Firestone. To get the lowest rate possible for the

commercial 'paper, it was necessary to have the issuance of the

paper backed by a letter of credit issued by a bank with a very

high rating. Ultimately, the Canadian Imperial Bank of Commerce

(bank) was chosen. A credit agreement was prepared which set

forth the obligations of the bank with respect to the issuance of

the letter of credit. A depository agreement was also prepared

naming Manufacturers Hanover Trust Company as the depository

agent to handle the issuance and payment of the commercial paper

as it was issued and reissued. The agreement was designed to

protect the interest of the commercial paper note holders.

o 7 . In addition to the foregoing documents, a security

agreement was created which provided the security for the bank by

giving it an interest in the flow of funds to repay the debt, and

ultimately gave it an indirect interest in the real estate. This

was accomplished through the assignment of the lease and all

rents to the bank.

8. To achieve Firestone's goal of off-balance sheet

financing, a separate, independent corporation named Firestone

Real Estate Leasing Corporation (FIRELCO) was created. All of

the stock of the corporation was owned by Case Western Reserve

University, located in Cleveland, Ohio. When initially

established, FIRELCO was a shell company with no assets, it had)

no working employees, and it had only,the minimum number of

directors required by law. It was not controlled by or related

- 7 -

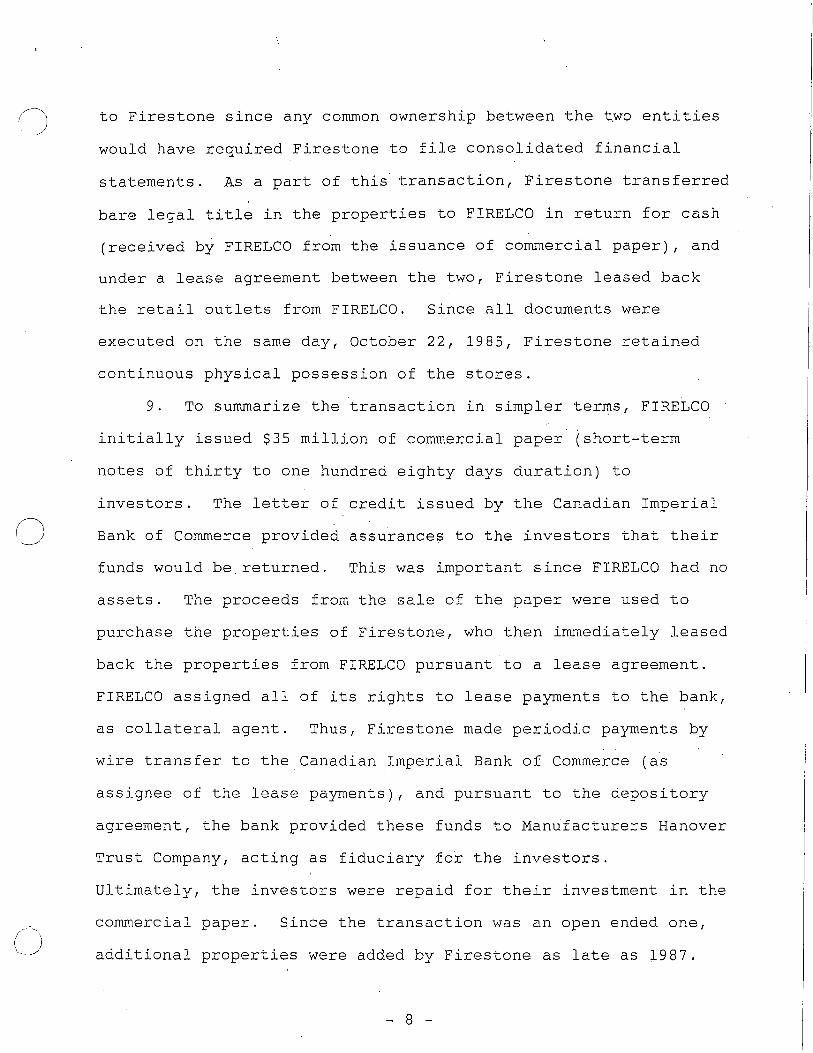

~ to Firestone since any common ownership between the two entities

would have required Firestone to file consolidated financial

statements. As a part of this transaction, Firestone transferred

bare legal title in the properties to FIRELCO in return for cash

(received by FIRELCO from the issuance of commercial paper), and

under a lease agreement between the two, Firestone leased back

the retail outlets from FIRELCO. Since all documents were

executed on the same day, October 22, 1985, Firestone retained

continuous physical possession of the stores.

9. To summarize the transaction in simpler terms, FIRELCO

initially issued $35 million of commercial paper' (short-term

notes of thirty to one hundred eighty days duration) to

investors. The letter of credit issued by the Canadian Imperial

.~ Bank of Commerce provided assurances to .the investors that their

funds would be returned. This was important since FIRELCO had no

assets. The proceeds from the sale of the paper were used to

purchase the properties of Firestone, who then immediately leased

back the properties from FIRELCO pursuant to a lease agreement.

FIRELCO assigned all of its rights to lease payments to the bank,

as collateral agent. Thus, Firestone made periodic payments by

wire transfer to the Canadian Imperial Bank of Commerce (as

assignee of the lease payments), and pursuant to the depository

agreement, the bank provided these funds to Manufacturers Hanover

Trust Company, acting as fiduciary for the investors.

Ultimately, the investors were repaid for their investment in the

commercial paper. Since the transaction was an open ended one,

additional properties were added by Firestone as late as 1987.

- 8 -

:~ .By the end of that year, FIRELCO had issued paper in excess of./

$150 million as a financing tool for Firestone.

10. By structuring the transaction in this manner,

Firestone was able to secure "virtually 100 percent financing"

for an interest rate on the commercial paper of less than that of

passbook savings. Also, it was able to secure off-balance sheet

financing; that is, it ended up with only cash on its books while

transferring the fixed assets (land and buildings) and

substantial debt to the books of FIRELCO, thus improving its

balance sheet. Finally, it was able to retain control of the

retail stores.

11. The sale/leaseback form of financing was fairly common

oin the 1980's and had a number of advantages over other types of

financing. First, it permitted the entity using that type of

financing to maintain a good debt to equity ratio since the debt

was shifted to the lessor. Also, commercial paper enjoyed a

lower interest rate than a long-term mortgage, thus allowing the

entity to realize savings in interest costs. In addition, unlike

the typical mortgage, this type of financing allowed the entity

to obtain 100 percent financing. Finally, the lessee was able to

retain control of all of its assets.

C. DOR's Audit and Conclusions

12. As a part of the audit, a DOR field auditor visited

Firestone's offices and examined all of the relevant documents

pertaining to the lease. At that time, the auditor was told by a

member of Firestone's tax department ~hat the payments made by()Firestone to FIRELCO were "rental payments".

- 9 -

In addition,

i,.:

- 10 -

lease itself. This constituted further evidence to DOR that the

Further, theseindicating the "monthly rent" paid by each store.

after having reached an agreement as to how the total transaction

assessed documentary stamp taxes on the assignment of rent.

Firestone's records contained a monthly rental schedule

14. In further support of its position, DOR relied upon the

was a "mortgage." Based on these considerations, the auditor

payments were characterized as rental payments in handwritten

notes maint.ained in petitioner's "real property files." Finally,

the Firestone representative nevei stated that the transaction

intangible personal property tax or documentary stamp tax on the

Firestone be liable for the sales tax associated with the lease

Tallahassee DOR personnel revealed that while FIRELCO had been

13. A subsequent review of Firestone's records by

payments. These taxes amounted to approximately $680,000.

recommended that the transaction be treated as a lease and that

would be apportioned to Florida, that Firestone had never paid

Exchange Commission (SEC) in which the reports referred to "rent

transaction was a lease and not a financing arrangement since

such taxes would be due on a mortgage.

various Form 10-K's filed by Firestone with the Securities and

as an "operating lease" as opposed to a capital or financing

payments for operating leases" and characterized the transaction

lease. Thus, DOR asserted that the assessment was correct since)

;/ the documents reviewed in the audit spoke of a "lease", "rental

portion of the transaction in 1987, and a notice of decision and~\

~~j ~losing agreement had been entered into by the DOR and FIRELCO

r~ payments" and the like, there was a representation by Firestone

that "rental paYments" were being made under the lease, and

Firestone had paid no documentary or intangible tax on the lease.

15. Finally, DOR offered the testimony of a board certified

real estate attorney who examined the one hundred eight page

lease and noted some twenty provisions which he opined would be

typically found in a lease agreement and not a mortgage. The

expert concluded that the lease in form was also a lease in

substance.

D. The Relevance of FASB 13

16. For financial reporting purposes, Firestone recorded the

transaction on its financial statements and other external

reports in accordance with generally accepted accounting(\~~ principles, the source of which includes, among other things, the

standards issued by the Financial Accounting Standards Board

(FASB). That board establishes accounting standards, which at

last count numbered one hundred fourteen, to be used by the

accounting profession in preparing financial statements. Among

them is FASB 13, which is applicable to this controversy and, at

the time the tra"nsaction occurred, governed. the accounting for

leases. Under FASB 13, a lease must be reported as a debt of the

"lessee" on its balance sheet if anyone of four conditions

exists. Put another way, a lease will not be reported as a debt~r{\,",,~

unless ~rl--fe~~Aof the following tests are met:

a. The lease transfers ownership of theproperty to the lessee.

b. The lease contains a bargain purchaseoption.

- 11 -

C~)

c. The lease term is equal to 75 percent ormore of the estimated life of the leased property.

d. The present value of the minimum leasepayments equals or exceeds 90 percent of thefair value of the leased premises.

As can be seen in the following discussion, none of these

criteria were met. Therefore, Firestone was obliged to report

the transaction as a lease in a footnote to its financial

statements. For Firestone to have recorded the transaction in

any other manner for financial reporting purposes would have

contravened FASB 13 and generally accepted accounting principles.

17. Under the terms of the lease agreement by Firestone and

FIRELCO, Firestone retained the option to repurchase all of the

leased properties at the end of a five year period for $137

million. Since the transfer of properties was not automatic, the

first criterion requiring that "the lease transfers ownership of

the property to the lessee" was not met.

18. Under the second criterion, "the lease (must) contain a

bargain purchase option." Since the purchase option in the lease

agreement was for the unamortized portion of the debt, which was

the book value, and a purchase at book value cannot be a bargain

purchase, this part of FASB 13 was not met.

19. Third, in order for the lease to be reported as a debt

on the books of Firestone, "the lease term (must be) equal to 75

percent or more of the estimated life of the leased property."

In this case, the lease called for a five year term. This is

,I

less than 75 percent of the estimated life of the improved real

\/~) property since new retail stores have a probable useful life of

35 years or more. Therefore, this part of the test was not met.

- 12 -

o

20. Finally, the lease called for the debt to be amortized

at the rate of 3 percent per year or a total of 15 percent over

the five year period of the lease. This left an unamortized debt

of 85 percent at the end of the five year term. This meant that

the minimum (and maximum) lease payments equaled only 15 percent

of the value of the property at the end of the lease term. Since

the fourth criterion requires that "the present value of the

minimum lease payments equals or exceeds 90 percent of the fair

value of the leased premises," the final part of the test was not

met.

21. Because none of the four tests of FASB 13 were met, the

transaction had to be recorded in a footnote, as a lease, rather

than on Firestone's balance sheet as a debt. This was consistent

with generally accepted accounting principles.' Therefore, in its

1984, 1985, 1986 and 1987 Form 10-K's, which are annual reports

filed with the SEC, Firestone reported the lease in footnotes,

and not as a balance sheet debt.

22. In 1988, or after the transaction occurred, FASB 98 was

issued. Had it not had prospective application only, the new

standard would have required this tr~n~action to be reported as a

debt or liability on the balance sheet of the financial

statements of Firestone.

E. An Analysis of the Transaction

23. Although a document may be cflled a lease on its face,

this in itself is not dispositive of the issue. Rather, in order

(~ to properly determine the true nature of the transaction, it is

necessary to examine the intention of the parties and the

- 13 -

substance of the agreement. In this case, the more credible and

persuasive evidence supports a finding that the sale/leaseback

agreement between Firestone and FIRELCO was a financing

transaction rather than a lease.

24. Initially, it is noted that a taxpayer can treat an item

one way for financial reporting purposes and another way for tax

purposes. A common example is depreciation, where a taxpayer can

properly use straight line depreciation for book purposes and

accelerated depreciation for tax purposes. Similarly, in cases

S11Ch as this, a taxpayer can report a transaction as a lease in

its financial statements but as a financing transaction for tax

purposes. Thus, in accordance with FASB 13, Firestone was

obligated to use such terms as "operating lease" and "rental

CJ payments" in its Form 10-K's filed with the SEC and to

characterize the transaction as a lease in the footnotes to its

financial statements. It could, however, treat the matter

C)

differently for tax purposes.

25. Firestone established that its tax returns were

prepared to reflect that no sale had occurred between Firestone

and FIRELCO, and therefore the retail stores continued to be

tieated as depreciable assets of Firestone for all tax purposes.

In doing so, Firestone relied upon advice from its tax counsel.

Further, the monthly payments made to the bank were treated as

principal and interest for all tax purposes, and not as rental

payments. In addition, for internal accounting purposes, the

transaction was treated in exactly th~ same way as for tax

reporting purposes, that is, with the real estate remaining on

- 14 -

(-) Firestone I s books as deprec iable as sets and with the payments

being treated as payments of principal and interest, and not

rent.

26. Although DaR's expert found some twenty provisions in

the agreement which are typically found in a lease, the greater

weight of evidence supports a finding that the sale/leaseback

here was used to effect a mortgage substitute through a deed

absolute with collateral documents. For example, sections 4.1-

4.4, 5.2, 6.1, 7.1, 7.3, 8.1, 8.2, 9.1, 9.2, 10.1, 11.1, 11.3,

11.8, 12.1-12.3, 13.1, 15.1-15.4, 18.1,23.3,24.1, 25.1, 28.1,

28.2,.30.1, 31.1, and 31.2 of the lease ~re clear indicia that in

reality the ~ransaction was a financing arrangement for

Firestone. Indeed, it was Firestone's primary aim in this

o transaction, as well as the intention of the parties, to raise

money so that Firestone could acquire new retail outlets. By way

of illustration, there are provisions in the lease which provide

that the rent is tied to FIRELCO's carrying costs and not a

reasonable return on the fair market of property (s. 4.1),

Firestone bears the burden of making all repairs to the property,

including major structural repairs (s. 5.2), the obligations of

the tenant continue even in the event of termination such as

condemnation (s. 6.2), the tenant must make all reports on the

property required by law (s. 7.1), FIRELCO must grant any

easements that Firestone determines are necessary (s. 8.2), in

the event of an insurable loss, the insurance proceeds go to the

tenant (s. 11.3), the landlord warrants that it will report to

the federal government that the tenant owns the property and

- 15 -

o

o

o

hence the tenant receives all federal tax benefits such as

depreciation (s. 17.2), ~pon transfer of title, the landlord's

liabilities are relieved and it has no liabilities under the

lease (s. 23.3), the tenant reserves the right to substitute any

retail properties and the replacement property can be no less

than the unamortized cost of the substituted property (s. 24.1),

and at the end of the lease, any accumulated equity in the

property is paid to Firestone as a management fee (s. 28.1).

27. In determining the practical business substance of the

transaction, it is also necessary to determine if the buyer is a

single purpose financing corporation, if the short and long term

risks and benefits associated with ownership pass to the so

called buyer, and if the seller's aim is to borrow money. In

this regard, the evidence shows that FIRELCO can properly be

called a single purpose financing corporation since it existed

only for the purpose of this transaction. That is, its sole

purpose was to facilitate the issuance of commercial paper, and

it was prohibited by the collateral documents from engaging in

any other business or corporate activity. Further, FIRELCO did

not enjoy any long or short-term benefits associated with

ownership of property, it did not assume possession of the

property, and the risks associated with ownership of the property

did not pass to the lessor but rather remained with Firestone.

Finally, as noted in the preceding paragraph, when it entered

into the transaction, Firestone's principal aim was to borrow

money. All of these considerations support a finding that the

practical business substance of the transaction was that of

financing new acquisitions for Firestone.

- 16 -

28. In summary, FIRELCO was a single purpose financing

corporation totally lacking in economic substance. The various

deeds from Firestone to FIRELCO were "deeds absolute" and the

various other documents, that is, the credit agreement, security

agreement, depository agreement, purchase and sale agreement,

lease, and assignment of rents and lease, were "collateral

documents." In this regard, it should be not.ed that the parties

did not intend for the deeds absolute to embody the whole

agreement but rather for the agreement to include both the deeds

and the collateral documents together. No sale actually occurred

and FIRELCO held naked legal title for the sole purpose of

providing security. There was no economic substance to the lease

beyond insuring amortization of the debt. Further, the

c-J practicalities of the situation and specific provisions of the

lease insure that Firestone was at all times the actual owner of

the property. Firestone treated the transaction as a financing

()

arrangement for federal and state income tax purposes, for ad

valorem tax purposes, for state sales and documentary tax

purposes, and for internal accounting purposes. In compliance

with FASB 13, however, Firestone reported the transaction as a

lease for financial reporting purposes. Therefore, the

transaction is found to be in the nature of a mortgage or

financing arrangement.

F. Estoppel

29. During the field audit phase of this proceeding, a

Firestone employee initially characte~ized the payments made by

Firestone to FIRELCO as rental payments and did not refer to the

- 17 -

C)

document as a mortgage. As noted in an earlier portion of this

order, there. were also several documents shown to the auditor

which contained the words "lease", "rental payments" and the

like. At that point, the DOR auditor was inclined to treat the

"monthly rent" under the lease as constituting rent for sales tax

purposes and to make corresponding audit adjustments. Firestone

disagreed, however, with the auditor's preliminary analysis and

argued that the payments should be characterized as a "financing

arrangement" rather than a true lease. Firestone also furnished

the auditor with a copy of the opinion letter from its tax

counsel which concluded that the transaction was not a lease. In

determining whether to accept this assertion, the field auditor

contacted his .supervisor, and togeth~r they checked with the

assistant bureau chief of multi-state audits. The field auditor

testified at hearing that he knew this was a precedent setting

case, other taxpayers had taken the same position as Firestone,

and at that time he and his supervisor had already decided to

treat the transaction as taxable. That position was approved by

the assistant bureau chief. Based upon substantial competent

evidence, the Hearing Officer concluded that, before the field

audit was concluded and preliminary action taken, DOR was aware

of Firestone's position on this issue. Therefore, DOR does not

claim that during the audit it was misled as to Firestone's

position or that Firestone subsequently changed its position

after the audit was completed. Moreover, DOR suffered no

detriment by virtue of its reliance on Firestone's announced

position.

- 18 -

30.

CONCLUSIONS OF LAW

The Division of Administrative Hearings had

jurisdiction of the subject matter and the parties hereto

pursuant to Sections 120.57 and 120.575, Florida Statutes.

31. As provided for-in Subsection 120.575(2), Florida

Statutes, the agency's "burden of proof ... shall be limited to a

showing that an assessment has been made against the taxpayer

and the factual and legal grounds upon which the (agency) has

made the assessment II • See also, Department of Revenue v. Quotron

Systems, Inc., 615 So.2d 774, 776 (Fla. 3d DCA 1993). Once that

showing is made, the burden shifts to the taxpayer to demonstrate

by a preponderance of the evidence that the assessment is

incorrect.

32. In construing the taxing statutes, the undersigned is

obliged to honor the long-established principle that tax laws are

to be strongly construed in favor of the taxpayer and against the

government. See,~, Maas Brothers, Inc. v. Dickinson, 195

So.2d 193, 198 (Fla. 1967). The statutory authority for the

assessment is found in Subsection 212.031(1)(a), Florida

Statutes. That subsection reads in relevant part as follows:

(1) (a) It is declared to be the legislativeintent that every person is exercising ataxable privilege who engages in thebusiness of renting, leasing, or letting anyreal property .

On the theory that the transaction is a lease within the meaning

of the foregoing statute, and no taxes have been paid, DOR

C) proposed to tax Firestone, as the tenant, since by law a tenant

is liable for any sales tax not paid by its landlord.

- 19 -

33. The central issue in this proceeding is whether the

"lease" agreement executed by the parties is a lease or a

mortgage. In resolving this issue, it is helpful to refer nbt

only to relevant tax decisions, but also to real estate cases

arising un~er Subsection 697.01(1), Florida Statutes, which have

determined whether instruments not denominated as a mortgage are

nonetheles~ treated as such. As to this latter body of law, DOR

initially contended that it was irrelevant since the purpose of a

taxing statute is to raise revenues while section 697.01

ostensibly deals with due process rights in foreclosure and quiet

title actions. The Hearing Officer determined that while not

arising under chapter 212, these cases nonetheless provide

guidance in determining whether an instrument is in the na.ture of

n a lease or a mortgage. Therefore, the undersigned accepts the

o

Hearing Officer's recommendation and deems this body of

substantive law t? be persuasive in resolving the ultimate issue.

34. Subsection 697.01(1) reads in pertinent part as

follows:

(1) All. . instruments in writing convey-ing or selling property, either real orpersonal, for the purpose or with the intention of securing the payment of moneyshall be deem~d and. held mortgages.

In other words, .the statute provides that even though a

transaction is not necessarily denominated as a "mortgage", if it

was executed for the purpose of securing money, it shall be

treated as such. Cases arising under this statute discuss when a

"deed absolute", as was given in 'this case, will be deemed to be

a mortgage, and the facts and circumstances leading to such a

- 20 -

result. In making a determination when a deed absolute should be

considered in conjunction with other agreements, whether written

or oral, parole evidence is admissible and does not violate the

parole evidence rule because the deed absolute does not embody,

and was not intended to embody, the whole agreement of the

parties. In Markell, et al. v. Hilbert, et al., 140 Fla. 842,

o

o

192 So. 392 (1939), the supreme court stated the general rule on

this subject as follows:

It appears that this court, many years ago,. held generally, independent of this

statute (s. 697.01), that parole evidence isadmissible in equity to show that a deed ofconveyance, absolute upon its face, wasintended as a mortgage, and where it is shownthat such a conveyance has been executed tosecure the payment of money, equity will treatit as a mortgage. "The court looks at substancerather than form, makes inquiry and hearsevidence beyond the terms of the instrument tothe very heart of the transaction so as todetermine the intent of the parties and alladmissible evidence bearing upon this equitableprinciple is received and considered by thecourt, whether written or oral, as it is theintention of equity to promote justice andto prevent fraud and imposition.

Id. at 398.

Under the foregoing rule, all of the documents (including the

collateral documents) which have been introduced in this case~

and the relevant testimony of the witnesses, must be considered

in determining how the transaction is to be treated. In doing

so, there is no violation of the parole evidence rule.

35. In determining the facts and circumstances which will

govern whether the transaction is to be deemed a mortgage, the

primary rule of construction is the intention of the parties.

- 21 -

(~\ This intent is established not only from the face of the',--

instruments, but also from the situation of the parties and the

nature and object of the transaction. Boyette v. Carden, 347

So.2d 759 (Fla. 1st DCA 1977). In plainer terms, one must

examine substance rather than form. The rule in Florida is that

an instrument must be considered a mortgage, regardless of its

form, if, when taken alone or in connection with surrounding

facts, it appears to have been given for the purpose of securing

money. First Mortgage Corp. of Stuart v. deGive, 177 So.2d 741

(Fla. 2nd DCA 1965). See also, Watkins et ux. v. Burnstein, 152

Fla. 828, 14 So.2d 569 (1943)(deed and lease with option to

purchase considered a single transaction constituting a

mortgage); Thomas v. Thomas, 96 So.2d. 771 (Fla. 1957) (absence of

(/'1.~ __ a promissory note evidencing- debt did not prohibit transaction

from being classified as a mortgage); Sommer v. Pennisi, 48 Fla.

Supp. 2d 197 (15th Cir. Ct. 1990)(a recitation in a deed that it

represents an absolute conveyance and not a mortgage is not

determinative of the issue); Hialeah, Inc. v. Dade County, 490

So.2d 998 (Fla. 3rd DCA 1986) (where burdens and obligations of

ownership rest with the lessee, a sale/leaseback will be

consider~d a mortgage) .

36. Based upon the established facts that the

sale/leaseback was executed solely for the purpose of securing

money to finance Firestone's acquisitions, the parties intended

the transaction to be a financing arrangement for taxing

()purposes, and the burdens and obligations of ownership rested_

with the lessee, it is concluded that the sale/leaseback here was

- 22 -

(----"\ used to effect a mortgage substitute through a deed absolute with.. )"-/

collateral documents. In other words, when stripped of all legal

titles and denominations, the transaction must be deemed to be a

mort.gage.

37. Although the Hearing Officer recommended reliance upon

federal income tax law for additional guidance, DOR rejects this

recommendation of law. Chapter 212, Fla. Stat., does not

"piggyback" federal income tax law, as does Chapter 220, Fla.

Stat. The case law construing what constitutes a "mortgage"

under §697.01, Fla. Stat. provides a better basis for determining

what constitutes a "lease" under Chapter 212 than federal income

tax law.

38. DOR initially cited Greenhut Construction Co. v. Knot~,

!:-J 247 So.2d 517 (Fla. 1st DCA 1971) and its progeny. DOR initially

raised the issue of estoppel and argued that Firestone was

equitably estopped from denying that the document in question was

a lease. For estoppel to apply in this case, the following facts

must be present:

(a) Firestone must have made a representationto DOR that the transaction was a lease;

(b) DbR relied on th~t repr~sentation;and

(c) Firestone later made a change in positionas to the nature of the transaction which wasdetrimental to DOR, caused by the representation and reliance thereon.

The evidence showed that during the course of the field audit,

and before any prelim~nary action was taken, DOR was fully aware

of Firestone's position as to the nature of the transaction.

Since no change in position occurred after the audit was

- 23 -

:~ completed and the assessment made, and DOR suffered no detriment,

the Hearing Officer determined that the claim of estoppel would

not lie. DOR accepts this recommendation.

EECOMHENDATION

Based on the foregoing findings of fact and conclusions of

law, it is

ORDERED that the sales and use tax assessments discussed

herein, which issued against petitioner are now withdrawn.

DONE AND ENTERED this

1993, in Tallahassee, Florida.

day of

(JLARRY H. FUCHSExecutive Director

CERTIFICATE OF FILING

I HEREBY CERTIFY that the foregoing Final Order has been

filed in the official records of the Department of Revenue I this

____day of ___________ 1 1993.

JUDY LANGSTONAGENCY CLERK

NOTICE OF RIGHTS

Any party to this Order has the right to seek judicial

review of the Order pursuant to Section 120.68, Fla. Stat., by

the filing of a Notice of Appeal pursuant to Florida Rule of

Appellate Procedure 9.110, with the Clerk of the Department in

(~ the Office of the General Counsell P.O. Box 6668, Tallahassee,

Florida 32314-6668, and by filing a copy of the Notice of Appeal

- 24 -

/~ accompanied by the applicable filing fees with the appropriate-"~~

District Court of Appeal. The Notice of Appeal must be filed

within 30 days from the date this Order is filed with the Clerk

of the Department.

COPIES FURNISHED:

Donald AlexanderHearing OfficerDivision of Administrative HearingsThe DeSoto Bldg.1230 Apalachee ParkwayTallahassee, FL32399-1550

(~

Linda Lettera, EsquireGeneral CounselRobert G. Parsons, EsquireAssistant General CounselDepartment of Revenue204 Carlton BuildingTallahassee, FL 32301

Benjamin K. Phipps, EsquireP. O. Box 1351Tallahassee, FL 32302

Jeffrey M. Dikrnan, EsquireJarrell L. Murchison, EsquireDepartment of Legal AffairsThe Capitol-Tax SectionTallahassee, FL 32399-1050

- 25 -

STATE OF FLORIDADIVISION OF ADMINISTRATIVE HEARINGS

BRIDGESTONE/FIRESTONE, INC.,

Petitioner,

vs.

DEPARTMENT OF REVENUE,

Respondent.

CASE NO. 92-2483

RECOMMENDED ORDER

Pursuant to notice, the above matter was heard before the

Division of Administrative Hearings by its duly designated

Hearing Officer, Donald R. Alexander, on April 29 and 30, 1993,

in Tallahassee, Florida.

APPEARANCES

For Petitioner:

For Respondent:

Benjamin K. Phipps, EsquirePost Office Box 1351Tallahassee, Florida 32302

Leonard F. Binder, EsquireJarrell L. Murchison, EsquireDepartment of Legal AffairsThe Capitol-Tax SectionTallahassee, Florida 32399-1050

STATEMENT OF THE ISSUE

The. ultimate issue .is whether a sales/leaseback agreement

between The Firestone Tire and Rubber Company, as predecessor to

Bridgestone/Firestone, Inc., i and Firestone Real Estate Leasing

Corporation should be treated as a. financing a.greement and is

thus not subject to the sales and use tax.

PRELII1INP-..Rf STATE:r.:rr.:J.'TT

This matter began after an audit was conducted by

respondent, Department of Revenue (DOR), of the taxes paid by

petitioner, Bridgestone/Firestone, Inc., during the period June

1, 1985, through December 31, 1988. The principal issue in the

audit is whether a transaction between the predecessor of

petitioner and Firestone Real Estate Leasing Corporation should

be treated as a financing arrangement or a lease. On the premise

that the transaction was a lease, DOR has proposed to make a

substantial assessment on petitioner. After various informal

appeals were unsuccessful, petitioner filed its petition for

formal hearing challenging the proposed assessment. The parties

have agreed that the total amount of taxes, interest and

penalties in dispute are $1,004,848.27.

The matter was" referred by respondent to the Division of

Administrative Hearings on April 23, 1992, with a request that a

hearing officer be assigned to conduct a formal hearing. By

notice of hearing dated May II, 1992, a "final hearing was

scheduled on September 22, 1992, in Tallahassee, Florida. At the

parties' request, the matter was rescheduled to December 1, 1992,

and then again to March 2, 1993. By agreement of the parties,

the matter was again rescheduled to April 15 and 16, 1993, and

finally to April 29 and 3D, 1993, at the same location.

At final hearing, petitioner presented the testimony" of Dr.

William A. Hillison, a professor at the Florida State University

(FSU) school of business and accepted as an expert in the

analysis of financial transactions from accounting standards;

Donald J. Weidner, a professor and dean of the FSU school of law

and accepted as an expert in factors to be considered in making a

determination as to whether a transaction is a sale or a

2

(~) mortgage; David F. Seele, petitioner's tax comptroller; and

Donald T. Allen, supervisor of petitioner's tax department.

Also, it offered petitioner's exhibits 1-7. All exhibits were

received in evidence except exhibit 6. Respondent presented the

testimony of Richard Unen, a DaR tax auditor; Peter J. Steffens,

DaR revenue opportunity research administrator; and Joseph R.

Boyd, a Tallahassee attorney and board certified in real property

law. Also, It offered respondent's exhibits 1-10 and 11A-11J.

All exhibits were received in evidence.

The transcript of hearing (four volumes) was filed on May

26, 1993. Prop?sed findings of fact and conclusions of law were

originally due on June 26, 1993. By agreement of the. parties,

this time was extended to July 2, 1993, and the parties timely

c) filed their proposed orders on that date. b ruling on each

proposed finding has been made in the Appendix attached to this

Recommended Order.

FINDINGS OF FACT

Based upon all of the evidence, the following findings of

fact are determined:

A. Background

1. . Petitioner, Br idgestone IF ires tone , Inc. cpeti tioner or

Firestone), is a foreign corporation doing business in Florida.

During the relevant time period, it owned more than one thousand

retail outlets throughout the country, including thirty-nine in

Florida, which sold tires and provided additional automotive

Rubber Company.(Jservices. Petitioner was then known as The Firestone Tire and

3

"-""I./

2. Respondent, Department of Revenue (DOR), is the state

agency charged with the responsibility of enforcing the Florida

Revenue Act of 1949, as amended. Among other things, DOR

performs audits on taxpayers to insure that all taxes due have

been correctly paid. To this end, a routine audit was performed

on petitioner covering the audit period from June I, 1985,

through December 31, 1988.

3. During the course of the audit, a DOR field auditor

reviewed a transaction that had occurred on October 22, 1985,

between Firestone and Firestone Real Estate Leasing Corporation

(FIRELCO) . In very broad terms, the agreement provided for the

sale of a substantial number of assets (land and buildings) to

FIRELCO and a leaseback of the assets by Firestone. After

(J concluding that this agreement was a lease arrangement between

,the two corporations, DOR issued a notice of decision on February

19, 1992, wherein it proposed to assess petitioner $1,233,942.67

in unpaid taxes, interest and penalties. Of this amount,

Firestone did not contest $229,094.67. Therefore, $1,004,848.27

is in dispute. In the notice of decision, DOR concluded that

"the "sale/leaseback agreement between Bridgestone/Firestone, Inc.

and Firestone Real Estate Leasing Corporation is a lease of real

property rather than a mere financing arrangement, and the

transaction is subject to the sales and use tax." Petitioner

then filed its request for hearing contending generally that DOR

had misunderstood the true nature of the transaction, the

agreement was a financing arrangement rather than a leasing

(~ arrangement for both federal and state tax purposes, and the

4

._---------------_._----

payments under the lease should not be subject to the commercial

rental tax as DOR has proposed. Accordingly, petitioner has

asked that the assessment be rescinded or withdrawn.

B. The Transaction and its Genesis

4. In 1979 Firestone hired as president an executive from

outside the company for the first time. Previously, only members

of the Firestone family or career Firestone employees had held

that position. Deciding that Firestone should de-emphasize its

manufacturing operations and concentrate on its retail

operations, the new president quickly closed seven tire plants

and opened a number of new retail outlets with an emphas is on

stores in the Sunbel t states. A decision was also made to

finance this expansion by using the real estate as collateral.

to a real estate investment trust (REIT) known as One Libertyo 5 . The first group of stores was paid for by selling them

Firestone. This form of financing had been recommended for

several reasons by Merrill Lynch, Firestone's investment banker.

First, .it gave Firestone "access to the public market". Second,

it allowed Firestone to use off-balance sheet financing, that is,

it removed the debt associated with the financing from

Firestone's balance sheet and thus improved its debt-equity

ratio. Finally, Firestone retained operations of the stores

through a lease with the REIT. For financial reporting and state

and federal tax purposes, the transaction was treated as a true

sale. The payments by Firestone to the REIT were treated as rent

on the books of both corporations.

6. Because Firestone had lost the benefit of the

appreciation of the value of the stores under the REIT form of

5

financing, it decided to find a better form of financing for its

next acquisition of retail outlets. After considering several

al ternatives, Firestone's then treasurer, Jack Rooney, and its

manager of domestic financing, Suzanne Palmer, concluded that the

new financing must meet several objectives, including retaining

of appreciation in value of the new properties, using the lowest

cost of financing available, continuing off-balance sheet

fincmcing so that the assets and debt would not be carried on

Firestone's balance sheet, and using the real estate as security

for the financing. To meet these objectives, Rooney and Palmer

selected a sale/leaseback form of transaction to be structured so

that (a) it could be reported off~balance sheet, (b) it would be

financed through the sale of commercial paper (unsecured

(~ promissory notes), and (c) the control of the properties would be,,-,-./

retained by Firestone. To get the lowest rate possible for the

commercial paper , it was necessary to have the issuance of the

paper backed by a letter of credit issued by a bank with a very

high rating. Ultimately, the Canadian Imperial Bank of Commerce'

(bank) was chosen. A credit agreement was prepared which set

forth the obligations of the bank with respect to the issuance of

the letter of credit. A depository agreement was also prepared

naming Manufacturers Hanover Trust Company as the depository

agent to handle the issuance and payment of the commercial paper

as it was issued and reissued. The agreement was designed to

protect the interest of the commercial paper note holders.

,7. In addition to the foregoing documents, a security

agreement was created which provided the security for the bank by

6

---_._--~-~~~---~----~~~~~_. -~~----~--~------

giving it an interest in the flow of funds to repay the debt, and

ultimately gave it an indirect interest in the real estate. This

was accomplished through the assigrunent of the lease and all

rents to the bank.

8. To achieve Firestone's goal of off-balance sheet

financing, a separate, independent corporation named Firestone

Real Estate Leasing Corporation (FIRELCO) was created. All of

the stock of the corporation was owned by Case Western Reserve

University, located in Cleveland, Ohio. When initially

established, FIRELCO was a shell company with no assets, i thad

no working employees, and it had only the minimum. number of

directors required by law. It was not controlled by or related

to Firestone since any common ownership between the two entities

~) would have required Firestone to file consolidated financial\ .

'---_.. /

statements. As a part of this transaction, Firestone transferred

bare legal title in the properties to FIRELCO in return for cash

(received by FIRELCO from the issuance of commercial paper), and

under a lease agreement between the two, Firestone leased back

the retail outlets from FIRELCO. Since all documents were

executed on the same day, October 22, 1985, Firestone retained

continuous physical possession of the stores.

9 • To summarize the transaction in simpler terms,

FIRELCO initially issued $35 million of commercial paper (short-

term notes of thirty to one hundred eiahtv- ... days duration) to

investors. The letter of credit issued by the Canadian Imperial

Bank of Con®erce provided assurances to the investors that their

(~ funds would be returned. This was important since FIRELCO had no

7

assets.

-------_.,-.--_._----------~

The proceeds from the sale of the paper were used to

purchase the properties of Firestone, who then immediately leased

back the properties from FIRELCO pursuant to a lease agreement.

FIRELCO assigned all of its rights to lease payments to the bank,

as collateral agent. Thus, Firestone made periodic payments by

wire transfer to the Canadian Imperial Bank of Commerce (as

assignee of the lease payments), and pursuant to the depository

agreement, the bank provided these funds to Manufacturers Hanover

Trust Company, acting as fiduciary for the investors.

Ultimately, the investors were repaid for their investment in the

commercial paper. Since the transaction was an open ended one,

addit.ional properties were added by Firestone as late as 1987.

By the end of that year, FIRELCO had issued paper in excess of

I~ $150 million as a financing tool for Firestone.

10. By structuring the transaction in this manner,

Firestone was able to secure "virtually 100% financing" for an

interest rate on the commercial paper of less than that of

passbook savings. Also, it was able to secure off-balance sheet

financing; that is, it ended up with only cash on its books while

transferring the fixed assets (land and buildings) and

substantial debt to the books of FIRELCO, thus improving its

balance sheet.

retail stores.

Finally , it was able to retain control of the

11. The sale/leaseback form of financing was fairly common

in the 1980's and had a number of advantages over other types of

financing. First, it permitted the entity using that type of

financing to maintain a good debt to equity ratio since the debt

8

was shifted to the lessor. Also, commercial paper enjoyed a

lower interest rate than a long-term mortgage, thus allowing the

entity to realize savings in interest costs. In addition, unlike

the typical mortgage, this type of financing allowed the entity

to obtain 100% financing. Finally, the lessee was able to retain

control of all of its assets.

c. DaR's Audit and Conclusions

12. As a part of the audit, a DaR field auditor visited

Firestone's offices and examined all of the relevant documents

pertaining to the lease. At that time, the auditor was told by a

member of Firestone I s tax department that the pa.yments made by

Firestone to FIRELCO were "rental payments". In addition,

Firestone's records contained a monthly rental schedule

payments were characterized as rental payments in handwritten() indicating the "monthly rent" paid by each store. Further, these

notes maintained in petitioner's "real property files." Finally,

the Firestone representative never stated that the transaction

was a "mortgage." Based on these cons idera tions, the auditor

recommended that the transaction be treated as a lease and that

Firestone be liable for the sales tax associated with the lease

payments. These taxes amounted to approximately 5680,000.

13. A subsequent review of Firestone's records by

Tallahassee DaR personnel revealed that while Firestone had been

assessed documenta.ry ste.mp taxes on the assignment of rent

portion of the transaction in 1987, and a notice of decision and

closing agreement had been entered into by the parties after

I~) having reached an agreement as to how the total transaction would

9

be apportioned to Florida, it had never paid intangible personal

property tax or documentary stamp tax on the lease itself. This

constituted further evidence to DOR that the transaction was a

lease and not a financing arrangement since· such taxes would be

due on a mortgage.

14. In further support of its position, DOR relied upon the

various Form 10-K' s filed by Firestone with the Securities and

Exchange Commission (SEC) in which the reports referred to "rent

payments for operating leases" and characterized the transaction

as an "operating lease" as opposed to a capital or f inanc ing

lease. Thus, DOR asserts the assessment is correct since the

documents reviewed in the audit spoke of a "lease", "rental

payments" and the like, there was a representation by Firestone

that "rental payments" were being made under the lease, and

Firestone had paid no documentary or intangible tax on the lease.

15. Finally, DOR offered the testimony of a board certified

real estate attorney who examined the one hundred eight page

lease and noted some twenty provisions which he opined would be

typically found in a lease agreement and not a mortgage. The

expert concluded that the lease in form was also a lease in

substance.

D. The Relevance of FASB 13

16. For financial

the transaction on its

reporting purposes,

financial statements

Firestone

and other

recorded

external

reports in accordance with generally accepted accounting

principles, the source of which includes, among other things, the

c=~\ standards issued by the Financial Accounting Standards Board

10

(FASB.) . That boa;rd establishes accounting standards, which at

last count numbered one hundred fourteen, to be used by the

accounting profession in preparing financial statements. Among

them is FAS~ 13, which is applicable to this controversy and, at

the time the transaction occurred, governed the ac'counting for

leases. Under FASB 13, a lease must be reported as a debt of the

"lessee" on its balance sheet if anyone of four conditions

C)

exists.

unless

Put another way, a lease will not~ reported

all four of the following tests are met:!'

a. The lease transfers ownership of theproperty to the lessee.

b. The lease contains a bargain purchaseoption.

c. The lease term is equal to 75% or more ofthe estimated life of the leased property.

d. The present value of the minimum leasepayments equals or exceeds 90% of the fairvalue of the leased premises.

as a debt

As can be seen in the following discussion, none of these

criteria were met. Therefore, Firestone was obliged to report

the transaction as a lease in a footnote to its financial

statements. For Firestone to have recorded the transaction in

any other manner for financial reporting purposes would have

contravened FASB 13 and generally accepted accounting principles.

17. Under the terms of the lease agreement by Firestone and

FIRELCO, Firestone retained the option to repurchase all of the

leased properties at the end of a five year period for $137

million. Since the transfer of properties was not automatic, the

first criterion requiring that "the lease transfers ownership of

the property to the lessee" was not met.

11

-----~--~~- ~- -- - ----- -------~--~-----~------

18. Under the second criterion, "the lease (must) contain a

bargain purchase option." Since the purchase option in the lease

. agreement was for the unamortized portion of the debt, which was

the book value, and a purchase at book value cannot be a bargain

purchase, this part of FASB 13 was not met.

19. Third, in order for the lease to be reported as a debt

on the books of Firestone, "the lease term (must be) equal to 75%

or more of the estimated life of the leased property." In this

case, the lease called for a five year term. This is less than

75% of the estimated life of the improvedieal property since new

retail stores have a probable useful life of 35 years or more.

Therefore, this part of the test was not met.

20. Finally, the lease called for the debt to be amortized

(~ at the rate of 3% per year or a total of 15% over the five year

period of the lease. This left an unamortized debt of 85% at the

end of the five year term. This meant that the minimum (and

maximum) lease payments equaled only 15% of the value of the

property at the end of the lease term. Since the fourth

criterion requires that "the present value of the minimum lease

payments equals or exce.eds 90% of the fair value of the leased

premises," the final part of the test was not met.

21. Because none of the four tests of FASB 13 were met, the

transaction had to be recorded in a footnote, as a lease, rather

than on Firestone's balance sheet as a debt. This was consistent

with generally accepted accounting principles. Therefore, in its

1984,1985,1986 and 1987 Form 10-K's, which are annual reports

filed with the SEC, Firestone reported the lease in footnotes,

and not as a balance sheet debt.

12

22.

issued.

In 1988, or after the transaction occurred, FASB 98 was

Had it not had prospective application only, the new

standard would have required this transaction to be reported as a

debt or liability on the balance

statements of Firestone.

E. An Analysis of the Transaction

sheet of the financial

23. Although a document may be called a lease on its face,

this in itself is not dispositive of the issue. Rather, in order

to properly determine the true nature of the transaction, it is

necessary to examine the intention of the parties and the

substance of the agreement. In this case, the more credible and

persuasive evidence supports a finding that the sale/leaseback.

agreement between Firestone and FIRELCO was a financing

transaction rather than a lease.

24. Initially, it is noted that a taxpayer can treat an

item one way for financial reporting purposes and another way for

tax purposes. A common example is depreciation, where a taxpayer

can properly use straight line depreciation for book purposes and

accelerated depreciation for tax purposes. Similarly, in cases

such as this, a taxpayer can report a transaction as a lease in

its financial statements but as a .financing transaction for tax

purposes. Thus, in accordance with FASB 13, Firestone was

obligated to use such terms as "operating lease" and "rental

payments" in its Form 10-K's filed with the SEC and to

characterize the transaction as a lease in the footnotes to its

financial statements. It could, however, treat the matter

(--) differently for tax purposes."..~

13

25. Firestone established that its tax returns were

prepared to reflect that no sale had occurred between Firestone

and FIRELCO, and therefore the retail stores continued to be

treated as depreciable assets of Firestone for all tax purposes.

In doing so, Firestone relied upon advice from its tax counsel.

Further, the monthly payments 'made to the bank were treated as

principal and interest for all tax purposes, and not as rental

payments. In addition, for internal accounting purposes, the

transaction was treated in exactly the same way as for tax

reporting purposes, that is, with the real estate remaining on

Firestone I s books as depreciable assets and with the payments

being treated as payments of principal and interest, and not

rent.

26. Although DaR's expert found some twenty provisions in

the agreement which are typically found in a lease, the greater

weight of evidence supports a finding that the sale/leaseback

here was used to effect a mortgage substitute through a deed

absolute with collateral documents. For example, sections 4.1-

4 . 4, 5. 2, 6. 1, 7. 1, 7. 3 , 8. 1, 8. 2, 9. 1, 9. 2, 10. 1 , 11. 1 , 11. 3 ,

11.8, 12.1-12.3, 13.1, 15.1-15.4, 18.1, 23.3, 24.1, 25.1, 28.1,

28.2 1 30.1, 31.1, and 31.2 of- the lease are -clear indicia that in

reality the transaction was a financing arrangement for

Firestone. Indeed, it was Firestone's primary aim in this

transaction, as well as the intention of the parties, to raise

money so that Firestone could acquire new retail outlets. By way

of illustration, there are provisions in the lease which provide

C-\ that the rent is tied to FIRELCO' s carrying costs and not a

14

()

(J

reasonable return on the fair market of property (s. 4.1),

Firestone bears the burden of making all repairs to the property,

including major structural repairs (s. 5.2), the obligations of

the tenant continue even in the event of termination such as

condem~ation (s. 6.2), the tenant must make all reports on the

property required by law (s. 7.1), FIRELCO must grant any

easements that Firestone determines are necessary (s. 8.2), in

the event of an insurable loss, the insurance proceeds go to the

tenant (s. 11.3), the landlord warrants "that it y.,rill report to

the federal government that the tenant .owns the property and

hence the tenant receives all federal tax benefits such as

depreciation (s. i7.2), upon transfer of title, the landlord's

liabilities are relieved and it . has no liabilities under the

lease (s. 23.3), the tenant reserves the right to substitute any

retail properties and the replacement property can be no less

than the unamortized cost of the substituted property (s. 24.1),

and at the end of the lease, any accumulated equity in the

property is paid to Firestone as a management fee (s. 28.1).

27. In determining the practical business substance of the

transaction, it is also necessary to determine if the buyer is a

single purpose financing corporation, if the short and long term

risks and benefits associated with ownership pass to the so

called buyer, and if the seller's aim is to borrow money. In

this regard, the evidence shows that FIRELCO can properly be

called a single purpose financing corporation since it existed

only for the purpose of this transaction. That is, its sale

purpose was to facilitate the issuance of commercial paper, and

15

it was prohibited by the collateral documents from engaging in

any other business or corporate activity. Further, FIRELCO did

not enjoy any long or short-term benefits associated with

ownership of property, it did not assume possession of the

property, and the risks associated with ownership of the property

did not pass to the lessor but rather remained with Firestone.

Finally, as noted in the preceding paragraph, when it entered

into the transaction, Firestone I s principal aim was to borrow

money. All of these considerations support a finding that the

practical business substance of the transaction was that of

financing new acquisitions for Firestone.

28. In summary, FIRELCO was a single purpose f inanc ing

corporation totally lacking in economic substance. The various

C~)deeds from Firestone to FIRELCO were "deeds absolute" and the

various other documents, that is, the credit agreement, security

agreement, depository agreement, purchase and sale agreement,

lease, and assignment of rents and lease, were "collateral

documents." In this regard, it should be noted that the parties