determinants of asset backed security prices in crisis periods william perraudin & shi wu...

TRANSCRIPT

Determinants of Asset Backed Security Prices in Crisis Periods

William Perraudin & Shi Wu

Comments by:

Stephen SchaeferLondon Business School

Conference on:

Liquidity: Pricing and Risk ManagementBank of England, June 23-24, 2008

Liquidity: Pricing and Risk Management: Imperial College - Bank of England 2

Models of Credit Pricing

• Credit pricing models currently unsuccessful in explaining level of spreads (structural models)

intensity models simply calibrate to market spreads

• Wide dispersion in prices / spreads even within rating:

relative to dispersion explained by models

but … data quality often poor

• This paper asks:

what explains deviations of spreads / prices from the rating category average?

Liquidity: Pricing and Risk Management: Imperial College - Bank of England 3

What does the paper do?

• Large sample of prices on Home Equity Loan (HEL) and Manufactured Housing Loan (MHL) ABS

• Fits average credit spread curves by credit rating category

• Attempts to explain deviations from average pricing

Liquidity: Pricing and Risk Management: Imperial College - Bank of England 4

Dispersion in Credit Pricing

• Studies of corporate debt (e.g., Collin-Dufresne, Goldstein & Martin, 2001) have also found high level of unexplained variation in prices

• Understanding the nature and source of this variation is an interesting and important question

Liquidity: Pricing and Risk Management: Imperial College - Bank of England 5

Methodology

• Uses transition matrix approach to fit time-homogeneous, rating-specific credit spread term structures to large sample of prices HEL and MHL

• Asks whether deviations from average pricing by credit category can be explained in terms of proxies for:

risk premia

liquidity

deviation between market and rating agency assessment of collateral quality (“disagreement”)

Liquidity: Pricing and Risk Management: Imperial College - Bank of England 6

1. Rating Transition Model

• Approach (as in Jarrow, Lando & Turnbull, 1997) employs risk-neutral transition matrix

• Presented as “interpolation technique” however model makes behavioural assumptions:

based on no-arbitrage condition

… but this implies pricing errors that are zero or, realistically, small while in crisis period they are substantial

• Minimising squared price errors sacrifices fit in spread at short maturities for fit at long maturities

Liquidity: Pricing and Risk Management: Imperial College - Bank of England 7

2. Default Risk for Given Rating May Change over Time

Source: Moody’s KMV – “Credit Risk matters”, Fall 2007

Equal estimated default probability for “A” in 2001 and “B” in 2007 . .

• Assumption of time-homogeneous transition matrix but evidence that default probability for given credit rating category declined substantially after 2001 recession

Liquidity: Pricing and Risk Management: Imperial College - Bank of England 8

3. Modelling Prices Using of Spreads

• Spreads (e.g., to Treasury curve) useful descriptive tool but may be difficult to use in pricing models because:

interest rate risk and credit risk are fundamentally linked (negative correlation between credit spreads and Treasury rates – “low duration” puzzle)

convenience yield in Treasury rates – particularly in crisis periods – means not clear which rate should be used as proxy for riskless

Liquidity: Pricing and Risk Management: Imperial College - Bank of England 9

US$ 5-Year Swap Spread

0

20

40

60

80

100

120

4. What is the appropriate riskless benchmark for measuring spreads?

• Paper uses Treasury rate but potential problem of (time-varying) convenience yield on Treasuries

“Decomposing Swap Spreads”, Feldhütter & Lando (J. Fin. Economics, forthcoming)

August 2006 – December 2007

June 07

Liquidity: Pricing and Risk Management: Imperial College - Bank of England 10

Results – what explains the residuals?

• Risk premia

limited significance of Fama-French SMB & HML factors

perhaps noisy beta estimates; 30 day moving window regression estimates

• “Disagreement” between market and rating agency

sub-rating category dummies significant

suggests sub-ratings are significant but not clear why “disagreement”

• Liquidity

appears that issue size is significant

Liquidity: Pricing and Risk Management: Imperial College - Bank of England 11

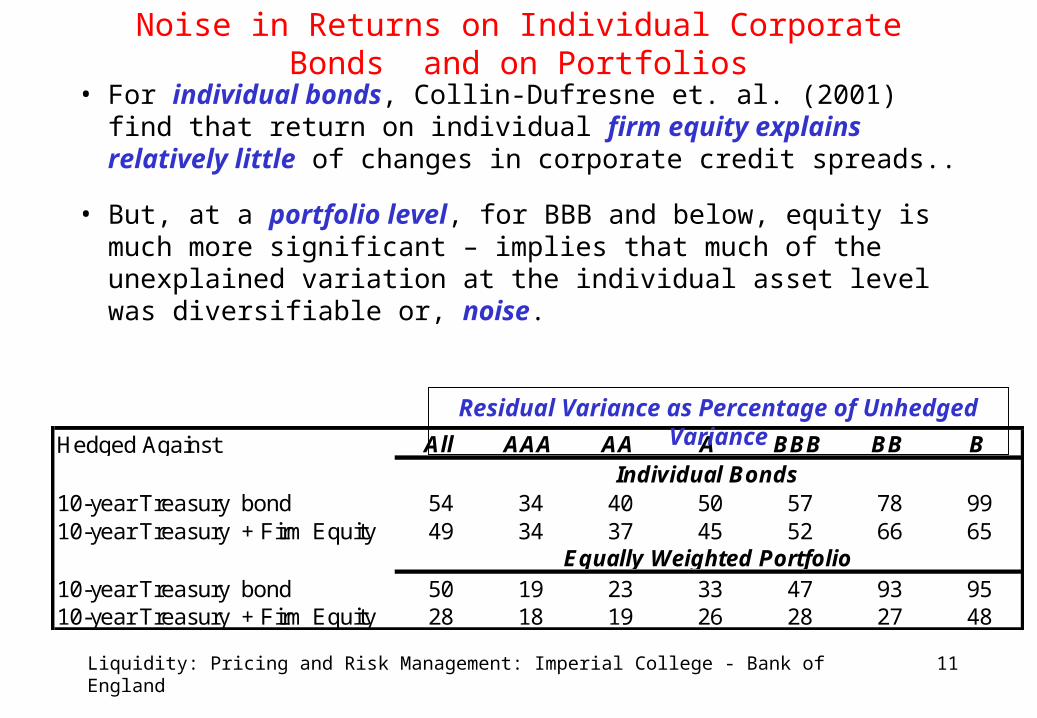

Noise in Returns on Individual Corporate Bonds and on Portfolios

• For individual bonds, Collin-Dufresne et. al. (2001) find that return on individual firm equity explains relatively little of changes in corporate credit spreads..

• But, at a portfolio level, for BBB and below, equity is much more significant – implies that much of the unexplained variation at the individual asset level was diversifiable or, noise.

Hedged Against All AAA AA A BBB BB B

10-year Treasury bond 54 34 40 50 57 78 9910-year Treasury + Firm Equity 49 34 37 45 52 66 65

10-year Treasury bond 50 19 23 33 47 93 9510-year Treasury + Firm Equity 28 18 19 26 28 27 48

Individual Bonds

Equally Weighted Portfolio

Residual Variance as Percentage of Unhedged Variance

Liquidity: Pricing and Risk Management: Imperial College - Bank of England 12

Summary – Pricing in the Crisis

• Currently difficult to understand either level or cross-sectional variability in credit spreads in crisis.

• High level of some spreads is particularly difficult to understand

may be less to do with detailed characteristics of instrument

.. and more to do with fact that many of the holders (e.g., hedge funds) were leveraged and their need to undertake forced sales as a result of falls in collateral values.