determinants of tax morale in japan and turkey · 2017-05-27 · determinants of tax morale in...

TRANSCRIPT

Recep Tekeli Policy Research Institute 1

1 Determinants of Tax Morale in Japan and in Turkey

The Determinants of Tax Morale: the Effects of Cultural Differences and Politics

Recep Tekeli1

Abstract: In this paper we analyze the tax morale in two OECD countries; Turkey and Japan, using data from the fifth wave of World Values Surveys. Using Survey data for comparative analysis we can see the differences in several factors affecting Tax Morale between Japan and Turkey We empirically test what shapes tax morale by using Ordered Probit model. We have followed the literature but used additional variables to see what determines the notion “intrinsic motivation to pay taxes i.e tax morale”. Most of our findings are in line with the earlier works in tax morale literature. Our findings also indicate significantly higher tax morale in Japan than in Turkey, controlling in a multivariate analysis for additional variables.

Keywords: Tax morale; Tax compliance

JEL classification: H26; H30

1. Introduction

Why do people pay taxes? This question recently has started to be pronounced more often and

attracted increased attention in the tax (non)compliance literature over the last few years. It is

supposed that nobody likes to pay taxes but governments can still generate tax revenues. One

possible answer among the scholars is to force people to pay their taxes by establishing a

deterrence policy.

In line with the economics-of-crime approach, Allingham and Sandmo’s (1972) model shows

that the extent of tax evasion is negatively correlated with the probability of detection and the

degree of punishment. However, because of the empirical and experimental findings, their

seminal model has attracted many criticisms by researchers (see, e.g., Graetz and Wilde 1985;

Alm et al. 1992; Frey and Feld 2002). These deterrence models predict a comparatively high

incidence of tax evasion; even in many countries, the actual level of deterrence is found to be

too low to explain the high degree of tax compliance.(see Torgler, Schneider and Shaltegger,

2010:294; Torgler and Shaltegger, 2006:396)2

1 Faculty of Economics and Administrative Sciences, Department of Public Finance, University of Adnan Menderes, Nazilli, Turkey ([email protected]). The Research Grant by Higher Education Council of Turkey (YÖK) is greatly appreciated. I would like to thank Policy Research Institute at Ministry of Finance, Japan for granting Visiting Scholar position and Policy Research Institute staff. Also I would like to thank to participants at the workshop where this paper was presented. 2 Torgler Schneider and Shaltegger (2010:294) and Torgler and Shaltegger (2006:396) quoting from several researchers report that there is a considerable gap between the amount of risk aversion that is required to guarantee such compliance and the effectively reported degree of risk aversion. For example, in the United States and Switzerland, the estimated Arrow–Pratt measure of risk aversion is between 1 and 2, but approximately a value of 30 would explain the observed compliance rate in these countries. Also, they argued that a higher level of income declaration is reported in tax compliance experiments than the expected utility model would predict.

Recep Tekeli Policy Research Institute 2

2 Determinants of Tax Morale in Japan and in Turkey

In the tax compliance literature this seemed to be a “puzzle”, or in other words, it is indeed an

avenue to study further for the scholars. To resolve this puzzle of tax compliance, many

researchers have tried to link tax morale to the high degree of tax compliance (e.g., Schwartz

and Orleans 1967; Lewis 1982; Roth et al. 1989; Alm et al. 1992, 1999; Pommerehne et al.

1994; Frey 1997; Frey and Feld 2002; Feld and Tyran 2002; Torgler 2001 and Torgler and

Schneider 2009). In this perspective, Torgler, (2003:290) argued that Erard and Feinstein’s

work (1994) “demonstrates the relevance of integrating moral sentiments into the models to

provide a reasonable explanation of actual compliance behavior”. Also while reviewing the

tax compliance, Andreoni et al. (1998:852) suggest that “adding moral and social dynamics to

models of tax compliance is as yet a largely undeveloped area of research” (see Torgler

Schneider and Shaltegger 2010:294)

Following Torgler’s researches into the field of tax morale, rather than treating tax morale as

a black box, or a residuum, many papers have analyzed which factors shape or maintain tax

morale (see Torgler and Schneider 2007; Torgler and Murphy 2004; and Torgler Schneider

and Shaltegger 2010). In addition, this puzzle concerns policymakers because they need to

know the driving forces of tax morale and the possibility that it influences willingness to pay

taxes so that they can design efficient tax system.

In the literature, tax morale is defined as “a moral obligation to pay taxes”, or “a belief in

contributing to society by paying taxes”. It is also defined as “the existence of an intrinsic

motivation to pay taxes” (Torgler 2003; Torgler 2004; Torgler and Schneider 2009;

Cummings et al 2009; Torgller 2005). This is not an output variable like the size of shadow

economy; it measures individual attitude not individual behavior (Torgler 2004; Torgler and

Schneider 2009). Tax morale is also closely linked to the term taxpayer ethics by Alm and

Torgler (2006:228) and Torgler and Schneider (2007a:10; 2007b:444) and used the definition

by Song and Yarbrough (1978:443) that, “the norms of behaviour governing citizens as

taxpayers in their relationship with the government”. Torgler and Murphy(2004:301) defines

the concept as “tax morale can generally be understood to describe the moral principles or

values individuals hold about paying their tax” 3

3 Tax morale is sometimes related to the term tax culture. Although it is not well conceptually organized yet, tax culture is defined as all residual factors that have not been considered to explain the behavior of tax compliance. In this aspect, Nerre (2008:155) defines tax culture as follows: “A country-specific tax culture is the entirety of all relevant formal and informal institutions connected with the national tax system and its practical execution, which are historically embedded within the country’s culture, including the dependencies and ties resulting from their ongoing interaction.”

Recep Tekeli Policy Research Institute 3

3 Determinants of Tax Morale in Japan and in Turkey

Why Tax Morale is Important?

German scholars in the 1960s (e.g. Schmölders, 1970 and Strümpel, 1969) “tried to bridge

economics and social psychology by emphasizing that economic phenomena should be

analyzed from a perspective larger than the traditional neoclassical point of view (e.g., Lewis,

1979, 1982)” (see Torgler and Schneider 2007b:444).

In this respect, Torgler and Schneider (2007a:10-11) argue that values and attitudes can affect

individual behavior: Apart from sanctions, Spicer and Lundstedt (1976) argued that a set of

attitudes and norms might have affect on the choice between tax compliance and evasion.

Lewis (1982) points out that “it could be that tax evasion is the only channel through which

taxpayers can express their antipathy … we can be confident in our general prediction that if

tax attitudes become worse, tax evasion will increase” (p. 165, 177).” (excerpted from Torgler

and Schneider 2007a:10-11). Therefore, we can state that values and attitudes can affect

individual’s behavior.

Tax noncompliance is actually inevitable fact in all societies (see Cowell, 1990; Schneider

and Enste (2000, 2002); Schneider 2003; Alm et al. 2004; Schneider 2005; Schneider et al

2010 ). Schneider (2005:598) argues that most societies attempt to control shadow economic

activities “through measures such as punishment and prosecution, or by relying on economic

growth or education. Gathering statistics about who is engaged in shadow economy activities

and the frequencies with which these activities occur and magnitudes, is important”.

Schneider (2005:600) defines the shadow economy as: “ The shadow economy includes all

market-based legal production of goods and services that are deliberately concealed from

public authorities”: to avoid payment of taxes and social security contributions, to avoid

having to meet certain legal labor market standards, such as minimum wages, and to avoid

complying with certain administrative procedures. While the shadow economy is estimated

generally it was not dealt with typical economic activities that are illegal and fit the

characteristics of traditional crimes such as gambling, burglary, robbery, drug dealing,

prostitution etc. The informal household economy, which consists of all household services

and production, is not included either (see Schneider 2005; Schneider et al 2010).

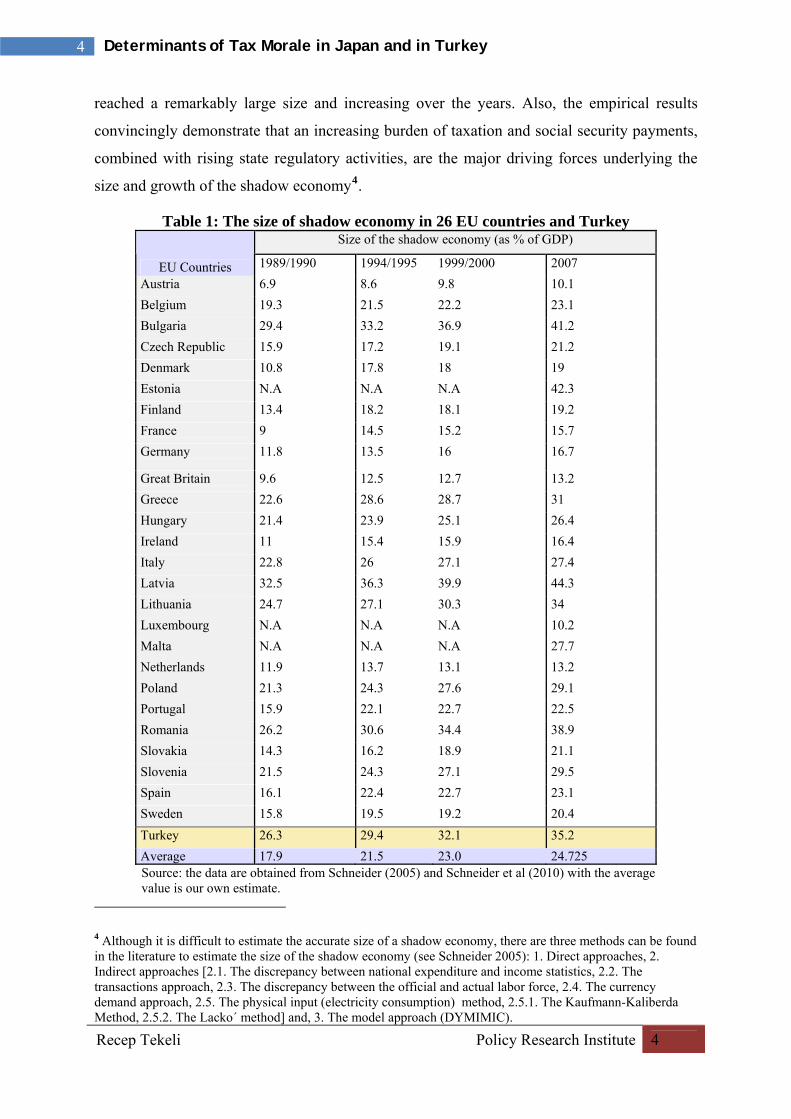

Schnieder (2005) and Schneider et al (2010) have provided estimates of the size of the

shadow economies for developing, transition and highly developed OECD countries over the

periods of time using the MIMIC/DYMIMIC and the currency demand approach. The first

conclusion from these results is that for all countries investigated the shadow economy has

Recep Tekeli Policy Research Institute 4

4 Determinants of Tax Morale in Japan and in Turkey

reached a remarkably large size and increasing over the years. Also, the empirical results

convincingly demonstrate that an increasing burden of taxation and social security payments,

combined with rising state regulatory activities, are the major driving forces underlying the

size and growth of the shadow economy4.

Table 1: The size of shadow economy in 26 EU countries and Turkey Size of the shadow economy (as % of GDP)

EU Countries 1989/1990 1994/1995 1999/2000 2007

Austria 6.9 8.6 9.8 10.1

Belgium 19.3 21.5 22.2 23.1

Bulgaria 29.4 33.2 36.9 41.2

Czech Republic 15.9 17.2 19.1 21.2

Denmark 10.8 17.8 18 19

Estonia N.A N.A N.A 42.3

Finland 13.4 18.2 18.1 19.2

France 9 14.5 15.2 15.7

Germany 11.8 13.5 16 16.7

Great Britain 9.6 12.5 12.7 13.2

Greece 22.6 28.6 28.7 31

Hungary 21.4 23.9 25.1 26.4

Ireland 11 15.4 15.9 16.4

Italy 22.8 26 27.1 27.4

Latvia 32.5 36.3 39.9 44.3

Lithuania 24.7 27.1 30.3 34

Luxembourg N.A N.A N.A 10.2

Malta N.A N.A N.A 27.7

Netherlands 11.9 13.7 13.1 13.2

Poland 21.3 24.3 27.6 29.1

Portugal 15.9 22.1 22.7 22.5

Romania 26.2 30.6 34.4 38.9

Slovakia 14.3 16.2 18.9 21.1

Slovenia 21.5 24.3 27.1 29.5

Spain 16.1 22.4 22.7 23.1

Sweden 15.8 19.5 19.2 20.4

Turkey 26.3 29.4 32.1 35.2

Average 17.9 21.5 23.0 24.725 Source: the data are obtained from Schneider (2005) and Schneider et al (2010) with the average value is our own estimate.

4 Although it is difficult to estimate the accurate size of a shadow economy, there are three methods can be found in the literature to estimate the size of the shadow economy (see Schneider 2005): 1. Direct approaches, 2. Indirect approaches [2.1. The discrepancy between national expenditure and income statistics, 2.2. The transactions approach, 2.3. The discrepancy between the official and actual labor force, 2.4. The currency demand approach, 2.5. The physical input (electricity consumption) method, 2.5.1. The Kaufmann-Kaliberda Method, 2.5.2. The Lacko´ method] and, 3. The model approach (DYMIMIC).

Recep Tekeli Policy Research Institute 5

5 Determinants of Tax Morale in Japan and in Turkey

The size and development of shadow economies of 26 EU countries is shown in Table 1. The

average shadow economy size was 17.9% in 1989/90 and increased to 24.75% in 2007. In

Turkey the size of shadow economy shows a significant increase. The lowest shadow

economies have Austria, Luxembourg and Britain with the size of shadow economy around

10 to 13 percent in 2007. The highest shadow economies among 26 EU countries have

Romania with 38.9, Bulgaria 41.2 Estonia 42.3 and Latvia 44.3 percent. These countries’

sizes of shadow economy are above Turkey’s size in 2007 i.e 35.2% (see Graph 1).

Source: see the fourth column in Table 1.

Note: Graph is prepared by using shadow economy estimates of Schneider et al (2010)

Recep Tekeli Policy Research Institute 6

6 Determinants of Tax Morale in Japan and in Turkey

In Graph 2 above and Table 2 below the size of the shadow economy of 27 OECD countries

are shown. The lowest shadow economies have the USA, Switzerland, and Austria with an

average size of shadow economy varies from 9 to 10%. Japan also shows a low level of

shadow economy with 12.1%. The countries with the highest shadow economies among these

27 OECD countries are Turkey with 35.2%, Mexico with 31.3 %, Greece with 31% and South

Korea with 29.4%.

Table 2: The size of shadow economy in OECD countries (including Japan)

OECD Countries 2007 USA 9 Switzerland 9.1 Austria 10.1 Luxembourg 10.2 Japan 12.1 Great Britain 13.2 Netherlands 13.2 New Zealand 13.6 Australia 15 France 15.7 Ireland 16.4 Canada 16.6 Germany 16.7 Iceland 16.8 Denmark 19 Finland 19.2 Norway 20.2 Sweden 20.4 Portugal 22.5 Belgium 23.1 Spain 23.1 Italy 27.4 South Korea 29.4 Greece 31 Mexico 31.3 Turkey 35.2 Mean 18.8

The comparison of shadow economies in EU and OECD economies shows an important

phenomenon for some countries to deal with. The main problem in the shadow economy, or

black economy, is the fact that individuals are behaving dishonestly by providing false

Recep Tekeli Policy Research Institute 7

7 Determinants of Tax Morale in Japan and in Turkey

information. If so, what would lead citizens to behave more honestly, provide correct

information and improve the tax compliance rate? Some believe that tax morale is an answer

to this question (see Feld and Frey 2002). Also, Torgler and Schneider (2007b) argue that a

reduction of tax morale reduces the moral costs of behaving illegally and increases the

incentives to work in the black economy.

According to Alm, et al (2004), a negative correlation between the size of the shadow

economy, which is a measure of the extent of tax evasion, and tax morale indicates the extent

to which individuals’ revealed actions are related to their attitudes about paying taxes (Torgler

and Schneider 2009:230; Torgler and Schneider (2007b)). In this extent, a number of previous

studies have investigated the simple correlation between tax morale and the size of shadow

economy. For example, Alm and Torgler (2006:242) focusing on Europe and the United

States find a strong negative correlation (r=-0.460). Alm, Martinez-Vazquez, and Torgler

(2006) focused on transition countries and their results indicate a strong negative correlation

between both variables (-0.657) (see Torgler and Schneider, 2009:230). Torgler (2005)

investigates the correlation between the size of shadow economy and tax morale in Latin

America, and a strong negative correlation between both variables (-0.511) has been found.

Torgler and Schneider (2009) find a significant correlation between tax morale and the size of

shadow economy based on data from more than fifty countries. Their empirical results

strongly suggest that tax morale plays a significant role in determining the level of shadow

economy: higher tax morale leads to a smaller shadow economy. Also, the beta coefficients

show that its quantitative impact is comparable to other determinants.

It has been argued that if tax authority places a taxman under every bed it is highly likely to

achieve a high level of tax compliance rate but with high costs to the tax authority. Torgler

and Shaltegger (2006:397) argues that “even though taxation is enforced by law, there is a

moral dimension in paying taxes for many people”. For example, Slemrod (1992:7) “states

that methods that reinforce and encourage taxpayers’ devotion to their responsibilities as

citizens play an important role in the tax collection process” (excerpted from Torgler and

Shaltegger 2006:397).

If tax morale is thought to be an explanation for why tax compliance rates are so high, it

would be interesting to analyze what may shape tax morale among taxpayers. Next section

examines the magnitude and determinants of Tax Morale. Model and variables which are

considered to be important explaining tax morale are presented as well. Section 3 gives the

empirical results in Turkish and Japanese experience. Last section concludes the paper.

Recep Tekeli Policy Research Institute 8

8 Determinants of Tax Morale in Japan and in Turkey

2. Magnitude and Determinants of Tax Morale: 2.1 Magnitude

If tax morale is seen as an important factor to understand the puzzle of tax compliance and

plays a significant role in determining the levels of shadow economy, then it is necessary to

investigate the determinants of tax morale. Thus, this section focuses on the magnitude and

determinants of tax morale in the study countries: Turkey and Japan.

We define tax morale as “the intrinsic motivation to pay taxes” as defined by Torgler in his

papers. This is not physical output variable such as tax evasion or the size of shadow

economy. It measures an individual’s willingness to pay taxes, in other words, “the moral

obligation to pay taxes” or “the belief that paying taxes contributes to society”. Data for the

tax morale variable are extracted from the World Values Survey (WVS) (see Inglehart et al.,

2000). The World Value Survey is a worldwide investigation of socio-cultural and political

change, which includes the case of Turkey and Japan. There are so many variables for this

dataset and it covers quite a huge number of countries. They are based on representative

national samples of more than 1000 individuals. In the 2005 wave of the survey, a total of

1346 Turkish citizens and 1096 Japanese citizens agreed to participate in the study.

Data from these surveys can be accessed by researchers interested in how views change with

time and across countries. The World Values Surveys have produced comparative data on

what people value, what their beliefs are, what they want out of life and the facts of life. In the

survey, our main concern is the question number 200 which is about the attitudes toward

cheating on taxation. This attitude was measured with the 10 different scales, where the value

of one (1) indicates that cheating on taxation is never justifiable and the value of ten (10)

means it is always justifiable. This dataset has been regularly surveyed. The first one was

carried out in 1981 for European Value Survey. The second wave was completed in 1990-

1991, the third one was carried out in 1995-1996, the fourth one took place in 1999-2001, and

the fifth and last one took place in 2005/2007. As the last one is the most recent one which we

can access, we use the last wave for the analysis.

The general question to assess the level of tax morale in World Values Survey is that:

“Please tell me for each of the following statements whether you think it can always be justified, never be justified, or something in between”: V200. Cheating on tax if you have the chance.

1 2 3 4 5 6 7 8 9 10

never justified always justified

Recep Tekeli Policy Research Institute 9

9 Determinants of Tax Morale in Japan and in Turkey

The tax morale variable is generated by recoding this ten-point scale into a four point scale

(0,1,2, and 3), with the value 3 standing for “never justifiable”. As usual, the value of 0 is an

aggregation of the last 7 scale points (4-10), which were rarely chosen (ie, 0 = “always

justifiable” to 3 = “never justifiable”; original scores of 4-10 were recoded into 0 = “always

justifiable”).

We should point Elffers et al. (1987) that their findings indicate the differences between

actual evasion assessed and evasion reported in survey responses. This result shows that

subjective surveys are always prone to significant reporting errors. As argued by some

researchers, tax morale is also measured with subjective survey responses in WWS, thus the

measurement of tax morale is not free of bias (e.g. Torgler 2004; Torgler and Schneider 2007;

Torgler et al 2010). Because the available data from surveys are based on self-reports in

which respondents may tend to overstate their degree of compliance (Andreoni et al. 1998),

no objective or directly observable measure of tax morale is available. However, the degree of

honesty is expected to be higher because in the WWS the tax morale is defined less sensitive

than directly asking whether a person has evaded taxes. Moreover, the dataset is based on

wide-ranging surveys (based on more than two hundred questions) it was assumed to reduce

the probability of respondent suspicion and the framing effects of other tax context questions.

However, it can still be argued that a taxpayer who has evaded in the past will tend to excuse

this kind of behavior and report a higher degree of tax morale in the survey. As no sanctions

are involved in the survey many respondents might overstate their willingness to pay taxes or

degree of honesty.( see Torgler and Schneider 2007a; Torgler and Schneider 2007b; Torgler

and Shaltegger 2006) 5

On the other hand, it was further argued that the use of such a single question (single item

value) has the advantage of reducing problems of index construction complexity, especially in

regard to measurement procedure or low correlation between items (see Torgler and

Schneider 2007a; Torgler 2004; Torgler 2003; Alm and Torgler2006). According to Torgler

and Schneider (2007a:450) “tax morale is a multi-dimensional concept that requires a multi-

item measurement tool and the likelihood of a multi-item index being adversely affected by

random errors will produce more reliable measures. However, several previous studies have

found consistent results using single-item survey measurements and laboratory experiments

5 We should also indicate another disadvantage of working with survey data as argued by Alm and Torgler (2006:237-238) that “we cannot control for such traditional factors as the audit probability (because this is not known for each individual) and the fine rate (because this is identical for all individuals in a country)”.

Recep Tekeli Policy Research Institute 10

10 Determinants of Tax Morale in Japan and in Turkey

(e.g., Cummings et al. 2005; Alm and Torgler 2006)”. Despite these criticisms our approach

to measuring tax morale is consistent with the previous studies in this area (see Torgler, 2007;

Torgler and Schneider 2007a; Torgler 2004; Torgler 2003; Alm and Torgler2006).

Graph 3 provides a comparison of tax morale levels of 12 EU countries with the same method.

It shows the frequency of response for “tax cheating is never justifiable” with respect to the

total respondents and the EU average value for scaled response6. The descriptive analysis

reveals the percentage of individuals in each EU country stating that ‘tax evasion is never

justifiable’ (i.e., those with the highest level of tax morale) and the mean level of tax morale

among EU countries. Turkey with 80.50% shows a higher proportion of never justifiable

response than that of EU average (57%). The average score obtained for the tax morale

question across all EU countries in 2005/2007 was 2.2 (out of 10). The lowest level of tax

morale is observed for France and Norway.

6 Selected countries in WVS 2005 are: Bulgaria [2006], Finland [2005], France [2006], Germany [2006], Great Britain [2006], Italy [2005], Netherlands [2006], Norway [2007], Poland [2005], Romania [2005], Spain [2007], Sweden [2006] and Turkey [2007].

Recep Tekeli Policy Research Institute 11

11 Determinants of Tax Morale in Japan and in Turkey

Graph 4 provides a comparison of Tax Morale levels of 15 Asia Pacific Economic

Cooperation (APEC) Countries. It also shows that in 2005 the average number of people in

Japan stating that tax cheating is never justified was 82.90%, which was far above APEC

average of 61.80%. The average score obtained for the tax morale question across all APEC

countries in 2005/2007 was 2.1 (out of 10). The lowest level of tax morale is observed for

Malaysia and Thailand. As we can see there is a strong difference among APEC countries

with the highest tax morale.7

Table 3 shows the range of responses varied from 1.5 to 3.5. The country most opposed to tax

cheating is Japan with a mean score of 1.5 followed by South Korea and Indonesia. Malaysia

has the highest score at 3.5 implying that Malaysian has the least opposition to tax cheating.

7 APEC currently has 21 members, including most countries with a coastline on the Pacific Ocean. As Taiwan joined with full approval of mainland China under the name Chinese Taipei, the APEC uses the term Member Economies rather than member countries to refer to its members. Therefore we also used Member Economies rather than member countries. Selected countries/samples are Australia [2005], Canada [2006], Chile [2006], China [2007], Hong Kong, China [2005], Indonesia [2006], Japan [2005], Malaysia [2006], Mexico [2005], New Zealand [2004], Russian Federation [2006], South Korea [2005], Taiwan [2006], Thailand [2007], United States [2006], Viet Nam [2006] http://www.wvsevsdb.com/wvs/WVSAnalizeQuestion.jsp(04-07-2011)

Recep Tekeli Policy Research Institute 12

12 Determinants of Tax Morale in Japan and in Turkey

Table 3: Tax Morale in APEC Countries

APEC Countries cheating never justified mean score

Japan 82.90% 1.5 South Korea 74.20% 1.6 Indonesia 79.30% 1.6 Viet Nam 76.90% 1.7 Canada 66.10% 1.9 Chile 66.20% 1.9 Hong Kong 61.40% 1.9 Australia 63.90% 2 China 63.40% 2 Taiwan 61.90% 2 United States 63.80% 2.1 New Zealand 60.20% 2.2 Mexico 60.10% 2.6 Thailand 29.00% 2.8 Russian Federation 51.30% 3 Malaysia 26.90% 3.5

Mean 61.80% 2.1

Note: Data on tax cheating was not available for all OECD countries.

Recep Tekeli Policy Research Institute 13

13 Determinants of Tax Morale in Japan and in Turkey

Table 4 presents a basic descriptive analysis showing the percentage of individuals in each

OECD country saying that ‘tax cheating is never justifiable’ (that is, those with the highest

level of tax morale). Table 4 also presents the mean level of tax morale in Turkey and in

Japan in relation to other OECD countries.

Table 4: Tax Morale in OECD Countries

OECD Countries Never justifiable Mean Scores

France 47.90% 2.8 Norway 49.70% 2.3 Sweden 53.50% 2.2 Poland 55.10% 2.4 Finland 56.20% 2.1 Germany 56.60% 2.2 Great Britain 57.80% 2.3 Mexico 60.10% 2.6 New Zealand 60.20% 2.2 Netherlands 61.10% 2.3 Italy 61.50% 2.2 Switzerland 61.80% 2 United States 63.80% 2.1 Australia 63.90% 2 Spain 64.80% 2.1 Canada 66.10% 1.9 Chile 66.20% 1.9 South Korea 74.20% 1.6

Turkey 80.50% 1.3

Japan 82.90% 1.5 Mean 62.60% 2.1

First of all, it can be seen that in 2005 wave of WVS, the average number of people among all

OECD countries saying that tax cheating was never justified was 62.6 per cent. Further the

average score obtained for the tax morale question across all OECD countries was 2.1. When

comparing the Japanese and Turkish figures to those of the rest of the OECD, it can be seen in

Table 4 that both countries’ level of tax morale in 2005 and in 2007 (82.90 and 80.50 percent

respectively) was substantially well above the OECD average (62.60%).

In sum, the results for the magnitude of tax morale show that Japan and Turkey rank in the

highest as compared to other countries within their regions. Thus, this gives a task to explain

why tax morale is very high in these two countries; what determines tax morale and are there

any similarities between these two countries in the determination of tax morale level.

Recep Tekeli Policy Research Institute 14

14 Determinants of Tax Morale in Japan and in Turkey

The tax systems of the study countries

Although two countries with very different cultures and a different history and politics, a

comparison of tax morale and compliance between Turkey and Japan as a member of OECD

constitutes a good experiment since the tax systems themselves are broadly similar.

The elements of the personal income tax (PIT) systems in both countries are summarized in

Table 5. For the PIT (and Corporate Income Tax, CIT), the self-assessment are similar in both

countries although there are varying degrees of aggressiveness in tax enforcement. Both

countries rely on some form of tax withholding at source, the stamp payment system, official

assessment system and individual self-assessment and reporting of final tax liabilities. Tax

evasion seemed to be treated as more serious crime in Turkey than in Japan even though

general tax amnesty was conducted three times in the last decade (2003, 2008 and 2011) in

Turkey.

Table 5: Features of the tax system in the study countries Tax feature Turkey Japan Self reporting/assessment Yes Yes Withholding Yes Yes Stamp payment Yes Yes Official assessment Yes Yes Tax rates (%) PIT: 15, 20, 27, 35

CIT: 20 PIT: 10, 20, 30, 37 CIT: 22-30

The respective computations of the PIT and CIT bases are similar. In Japan, PIT and CIT are

taxed separately as in Turkey. The PIT base consists of wages and salaries as well as earnings

from interest and dividends (but these are taxed at the source). The marginal rate for PIT is

capped at 35 percent in Turkey, lower than the top rate in Japan (37 percent). The corporate

tax rates in Japan varies from 34.5 %(30% effective) for ordinary companies with large scale

to 25 %(effective 22%) for small size corporate and cooperative associations and public

service corporation. However in Turkey there is a basic corporate tax rate of 20 % applied to

all size corporations.

Both countries have some form of administrative and judicial penalties imposed for failure to

file if taxes are owed. Administrative penalties consist of interest and a penalty up to the tax

owed/evaded. Judicial penalties also can be imposed for tax evasion/fraud. In Japan there is a

delinquent tax fee at the rate of 14.6% per annum and substantial additional tax imposed at the

rate of 35% of the tax amount as a penalty for evasion. In case of fraud additional tax is

imposed at the rate of 40% of the tax amount (see Table 6). There is a judicial penalty

imposed against tax crimes in connection with the assessment and collection of tax.

Recep Tekeli Policy Research Institute 15

15 Determinants of Tax Morale in Japan and in Turkey

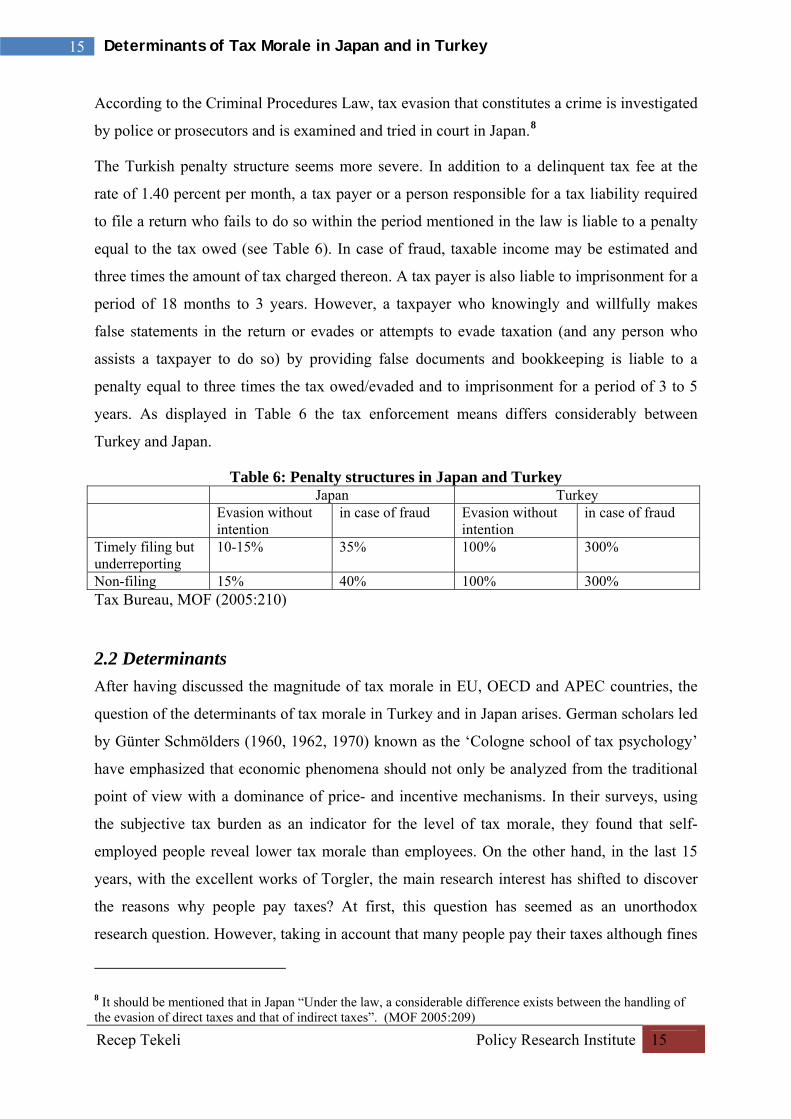

According to the Criminal Procedures Law, tax evasion that constitutes a crime is investigated

by police or prosecutors and is examined and tried in court in Japan.8

The Turkish penalty structure seems more severe. In addition to a delinquent tax fee at the

rate of 1.40 percent per month, a tax payer or a person responsible for a tax liability required

to file a return who fails to do so within the period mentioned in the law is liable to a penalty

equal to the tax owed (see Table 6). In case of fraud, taxable income may be estimated and

three times the amount of tax charged thereon. A tax payer is also liable to imprisonment for a

period of 18 months to 3 years. However, a taxpayer who knowingly and willfully makes

false statements in the return or evades or attempts to evade taxation (and any person who

assists a taxpayer to do so) by providing false documents and bookkeeping is liable to a

penalty equal to three times the tax owed/evaded and to imprisonment for a period of 3 to 5

years. As displayed in Table 6 the tax enforcement means differs considerably between

Turkey and Japan.

Table 6: Penalty structures in Japan and Turkey Japan Turkey Evasion without

intention in case of fraud Evasion without

intention in case of fraud

Timely filing but underreporting

10-15% 35% 100% 300%

Non-filing 15% 40% 100% 300% Tax Bureau, MOF (2005:210)

2.2 Determinants

After having discussed the magnitude of tax morale in EU, OECD and APEC countries, the

question of the determinants of tax morale in Turkey and in Japan arises. German scholars led

by Günter Schmölders (1960, 1962, 1970) known as the ‘Cologne school of tax psychology’

have emphasized that economic phenomena should not only be analyzed from the traditional

point of view with a dominance of price- and incentive mechanisms. In their surveys, using

the subjective tax burden as an indicator for the level of tax morale, they found that self-

employed people reveal lower tax morale than employees. On the other hand, in the last 15

years, with the excellent works of Torgler, the main research interest has shifted to discover

the reasons why people pay taxes? At first, this question has seemed as an unorthodox

research question. However, taking in account that many people pay their taxes although fines

8 It should be mentioned that in Japan “Under the law, a considerable difference exists between the handling of the evasion of direct taxes and that of indirect taxes”. (MOF 2005:209)

Recep Tekeli Policy Research Institute 16

16 Determinants of Tax Morale in Japan and in Turkey

and audit probability are low, the question seemed not only reasonable but also crucial for the

design of a country’s efficient tax system (Erard and Feinstein, 1994). (see Torgler and

Shaltegger 2006)

The results indicate that the high level of tax compliance cannot be explained entirely by the

level of enforcement (Graetz and Wilde, 1985). It is a long way before a person becomes a tax

evader. For example, Elffers (2000) sees the process of tax evasion as a staircase with three

different steps. First, taxpayers have to be seized by a will ‘not to comply’. Some researchers

have argued that many taxpayers do not even think of tax evasion and hence do not even

search for ways to cheat at taxes. In Long and Swingen’s words (1991:130) some taxpayers

are “simply predisposed not to evade”. Some researchers findings indicate that there are

individuals who always comply (Alm 1999). In a second step, Elffers (2000:187) goes on to

argue that not everyone with “an inclination to dodge his taxes is able to translate his intention

into action”, because many individuals do not have the opportunity or the knowledge and

resources to evade. In the last step, you can find taxpayers that feel inclined ‘not to comply’

and check for the opportunity to evade taxes. Elffers’s argument is that this is the phase where

standard economic theory works, where taxpayers evaluate the expected value of tax evasion.

Thus, the focus has been on the lower level (willingness step) where attitudes regarding tax

evasion (i.e. tax morale) play an essential role. (see Torgler 2003:290)

2.2.1 Model and Variables

The empirical analysis in this paper focuses on tax morale which is influenced by a variety of

factors. In empirical analysis social, demographic and economic factors as well as national

pride or religiosity play a role in determining tax morale in a society. Also, “there is the

institutional arrangement in which the government works. Here, the extent of democratic

participation (possibilities) by taxpayers as well as the level of institutional and political trust

are decisive. Tax morale is driven by the acceptance of government decisions.” (see Torgler

and Shaltegger (2006:397). Following discussions explain the variables and indicate the

expectations of the coefficient signs.

Elffers (2000), as already discussed above, argues that it is important that people remain at the

lower level of the staircase to tax evasion. Thus, it might be interesting to focus on the

“willingness step”, which means that attitudes regarding tax evasion play an essential role.

Thus, the empirical analyses focus on the attitudes regarding tax evasion which is simply

defined as tax morale and data on Japan and Turkey from 2005 World Values Surveys are

Recep Tekeli Policy Research Institute 17

17 Determinants of Tax Morale in Japan and in Turkey

evaluated (see Inglehart et al., 2000). Our main model for predicting tax morale in the study

countries has the following structure:

where TM denotes the individual degree of tax morale in a respected country; Our key

independent variables TRUST denotes individual’s trust in authority; PRIDE denotes pride of

individual; POL is individual’s political and pro-democratic attitudes, HAPPY denotes

individual’s well being (happiness) and X is a vector of variables which denotes numerous

socioeconomics and control variables such as age, gender, marital status, education,

awareness, employment and occupational status. Our choice of independent variables is in

line with the literature. Torgler and Shaltegger (2006) discuss the studies using the factors to

explain the determinants of tax morale in various countries. In Tale 7 summary of survey

studies in different regions are presented with the variables and signs.

Table 7: Literature: Determinants of Tax Morale (excerpted from Torgler and Shaltegger 2006:415)

Dependent Variable Tax Morale

Regions Europe North and Latin America

Transition, Asian Countries and Australia

Independent Variables Age + + + Gender (female) + + + Education (-/+) (+) + Married + + (+) Self-employed - (+) - Income - - - Financial Satisfaction + + + Church Attendance + + +(Asia) Religious + + (-/+) Trust in Government + + + Trust in Legal System + + Trust in court/legal system

+

Trust in the president + Trust public officials + + Pride + + Direct democracy +(Switzerland) +USA Pro-democratic attitudes

+ + +

Local autonomy + Notes: Summary of survey studies in different regions. Tendencies: +: significant positive coefficient, (+), (-), positive, respectively negative coefficient sign without being (consistently) significant, (±) positive and negative sign of the coefficient without being (consistently) significant.

i

k

kiiiiXHAPPYPOLTRUSTTM

133i21

PRIDE

Recep Tekeli Policy Research Institute 18

18 Determinants of Tax Morale in Japan and in Turkey

Dependent Variable

The dependent variable in our study is Tax Morale (TMi). The general question to assess level

of tax morale from the World Values Survey 2005– and for which has been used in several

previous research studies is already described above.

The WVS has been broadly used by researchers and the applied econometric method is

Ordered Probit models. The tax morale variable is scaled dependent variable and hence the

ordered probit models help to analyze the ranking information of this variable (Torgler 2006).

Following Cummings et al (2009:451-452) answers of “don’t know” and missing values were

not coded and were dropped from the sample. In the model the estimated equation has a non-

linear form and only the sign of the coefficient can be directly interpreted, not its coefficient

as in ordinary regression equation. Calculating the marginal effects is therefore a method to

find the quantitative effect of independent variable has on tax morale9. The marginal effect

indicates the change in the share of taxpayers (or the probability of) belonging to a specific

tax morale level (i.e. 0,1,2,3) when the independent variable increases by exactly one unit. We

will present only the marginal effects for the highest value - i.e. tax evasion is never justified-

from the ordered probit estimation.10

Table 8: Tax Morale

Country Justifiable:

cheating on taxes Japan (2005)

Turkey (2007)

Never justifiable 82.90% 80.50% 2 6.00% 12.50% 3 4.50% 4.00% 4 2.60% 1.10% 5 2.20% 1.10% 6 0.10% 0.20% 7 0.30% 0.20% 8 0.40% 0.10% 9 0.10% 0.10%

Always justifiable 0.90% 0.30% Total 1075

(100%) 1341

(100%) Mean 1.5 1.3

Standard Deviation 1.32 0.97

9 Bruin (2006) offers the “margin” command to find the marginal effect of a specific variable in the regression. 10 The empirical results on the tax morale can be given on request from the author.

Recep Tekeli Policy Research Institute 19

19 Determinants of Tax Morale in Japan and in Turkey

Table 8 shows the frequency of response for “tax cheating is never justifiable” with respect to

the total respondents, the average value and standard deviation for scaled response. Japan

shows a higher proportion of never justifiable response than that of Turkey. Although mean

response in Japan is slightly higher than that in Turkey, the mean scores appeared to be

basically the same; 1.5 for Japan and 1.3 for Turkey. On a scale from 1 to 10, it does not seem

like much of a difference. The Japanese sample had the highest percentage (82.90%) response

for that position but both countries had responses for the “never justifiable” position above

eighty percent.

Independent Variables

Our independent variables are described below.

TRUST: There is no doubt that the socio-demographic and the socio-economic background

of individuals affect tax morale. Torgler (2001) argued that there were a number of key

factors that seemed to be important for understanding tax morale. Two of these factors

included the relationship taxpayers had with their Government (ie, whether they trusted them

or not), and taxpayers’ moral rules and sentiments. Torgler (2005) confirmed that these

concepts predicted levels of tax morale in Latin America as well as in other countries (see

also Torgler and Murphy 2004). In order to see whether these variables were important in

understanding tax morale in the study countries, three questions that most closely measured

these concepts were chosen from the World Values Survey and used as predictors of tax

morale: trust in the government, trust in the legal system and trust in the parliament.

Trust in the government has been measured as follows:

Could you tell me how much confidence you have in the government in your capital: is it a great deal of confidence, quite a lot of confidence, not very much confidence or none at all? (1= “a great deal” to 4= “none at all”).

The other variables used to explore the relationship taxpayers had with authority are trust in

the legal system and trust in the parliament. Trust in the legal system was measured in the

World Values Survey as follows:

Could you tell me how much confidence you have in the legal system: is it a great deal of confidence, quite a lot of confidence, not very much confidence or none at all? (1= “a great deal” to 4= “none at all”).

Trust in the parliament was measured in the World Values Survey as follows:

Could you tell me how much confidence you have in the Parliament: is it a great deal of confidence, quite a lot of confidence, not very much confidence or none

Recep Tekeli Policy Research Institute 20

20 Determinants of Tax Morale in Japan and in Turkey

at all? (1= “a great deal” to 4= “none at all”).

These three variables allow us to analyze trust at the constitutional level, thereby focusing on

how the relationship between the State and its citizens is established, and also allow us to

analyze trust more closely at the current politico-economic level (see Alm and Torgler

2006:236). Torgler and Murphy (2004:309) see the relationship between taxpayers and the

State as “a relational contract or psychological contract, which involves strong emotional ties

and loyalties”. If citizens/taxpayers trust their government, representatives and justice system,

because the State is seen to be acting in a trustworthy manner, taxpayers/citizens might be

more willing to comply with their tax obligations.

The tax authority cannot achieve compliance rate completely; they would have to place a

taxman under every bed. In this respect, trust especially plays an important role where

detection and punishment are achieved by high cost. This might indicate that trust is an

important institution, which influences citizens’ incentive to commit themselves to obedience.

The findings by Scholz and Lubell (1998) from America and by Murphy (2004) from

Australian experience have led Torgler and Murphy (2004:310) to indicate that trust is an

important institution, which influences citizens’ incentives to commit themselves to

obedience. If this is indeed the case, one would therefore expect that those who have more

trust in the legal system, government and/or in Parliament might also have higher levels of tax

morale.

Furthermore, Torgler and Shaltegger (2006:410) assert that “trust is not an attitude that can be

demanded by the government, taxpayers bestow trust on their government or they don’t”. In

similar arguments, Torgler (2004:243) points out that “trust can only be created if the

government acts in line with citizens’ needs and desires…”.

In the lights of above arguments, the following hypothesis is going to be tested:

Hypothesis 1. The more extensive the citizens’ trust in the government, in the parliament and the legal system (justice or the court), the higher the tax morale.

We expect that trust in the government, the legal system and the parliament has a strong

impact on tax morale. In other words the willingness to pay taxes is highly influenced by the

positive treatments of taxpayers by the authorities.

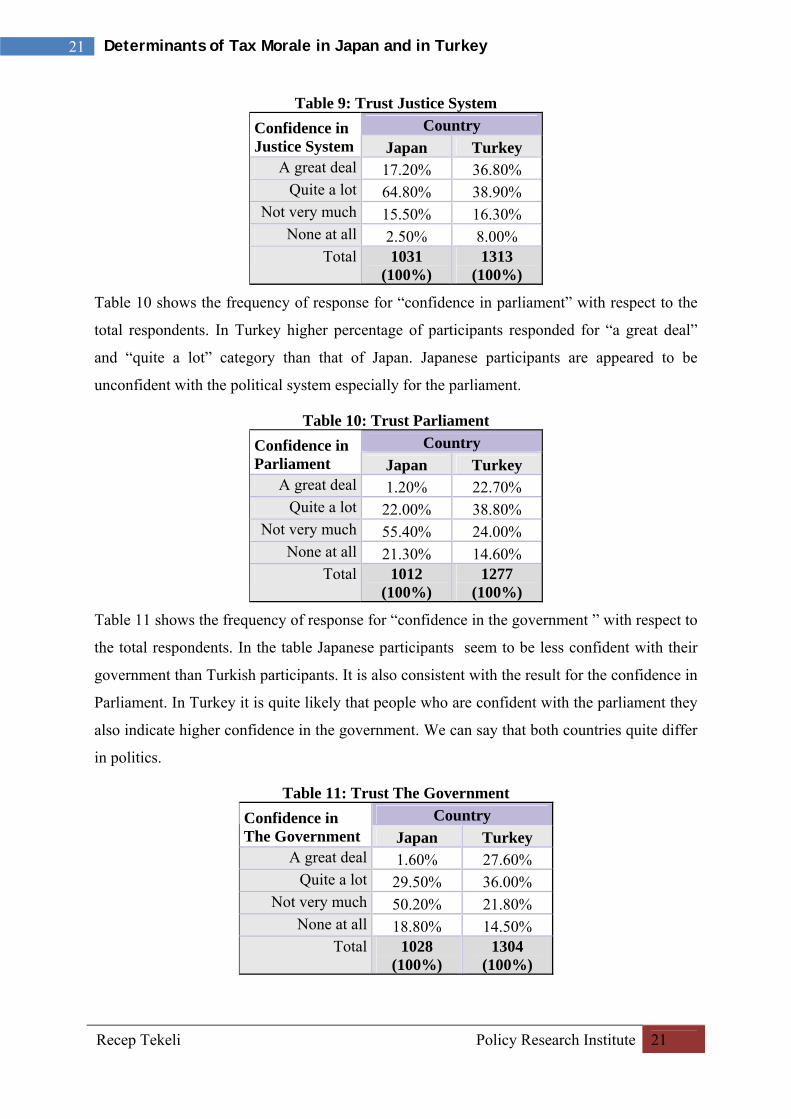

Table 9 shows the frequency of response for “confidence in Justice System” with respect to

the total respondents. In Japan participants have higher confidence in justice system than in

Turkey. In Turkey 24.3% of respondents are not confident with justice system while 18% of

respondents are not confident with their justice system in Japan.

Recep Tekeli Policy Research Institute 21

21 Determinants of Tax Morale in Japan and in Turkey

Table 9: Trust Justice System

Country Confidence in Justice System Japan Turkey

A great deal 17.20% 36.80% Quite a lot 64.80% 38.90%

Not very much 15.50% 16.30% None at all 2.50% 8.00%

Total 1031 (100%)

1313 (100%)

Table 10 shows the frequency of response for “confidence in parliament” with respect to the

total respondents. In Turkey higher percentage of participants responded for “a great deal”

and “quite a lot” category than that of Japan. Japanese participants are appeared to be

unconfident with the political system especially for the parliament.

Table 10: Trust Parliament

Country Confidence in Parliament Japan Turkey

A great deal 1.20% 22.70% Quite a lot 22.00% 38.80%

Not very much 55.40% 24.00% None at all 21.30% 14.60%

Total 1012 (100%)

1277 (100%)

Table 11 shows the frequency of response for “confidence in the government ” with respect to

the total respondents. In the table Japanese participants seem to be less confident with their

government than Turkish participants. It is also consistent with the result for the confidence in

Parliament. In Turkey it is quite likely that people who are confident with the parliament they

also indicate higher confidence in the government. We can say that both countries quite differ

in politics.

Table 11: Trust The Government

Country Confidence in The Government Japan Turkey

A great deal 1.60% 27.60% Quite a lot 29.50% 36.00%

Not very much 50.20% 21.80% None at all 18.80% 14.50%

Total 1028 (100%)

1304 (100%)

Recep Tekeli Policy Research Institute 22

22 Determinants of Tax Morale in Japan and in Turkey

PRIDE: Although pride is a widespread phenomenon, pride and its effect on tax cheating or

tax evasion have not been discussed very much in economic literature. However, many results

are provided in recent literature. Boulding (1992:93) states that “The dynamics which governs

the creation, destruction, and distribution of various forms of pride and shame in society are

very little understood, yet nothing perhaps is more crucial to the understanding of the overall

dynamics of a particular society than the marked differences which exist among societies in

this regard’’ (excerpted from Torgler 2004:243 also see Torgler and Shaltegger 2006:412).

Everybody could be proud of own country. Pride produces a sense of group identification

which can be found in international games such as the FIFA/FIBA World Cup. Tyler (2000)

“argues that pride influences people’s behaviour in groups, organizations and societies. It

gives a basis for encouraging cooperative behavior” (see Torgler 2004:243; Torgler and

Shaltegger 2006:412). To analyze the effects of pride on tax cheating (or tax morale) it can be

hypothesized that people who are proud to be citizens of their country are more loyal, better

identified with the state and have thus a higher tax morale.

The question that measures national pride is:

How proud are you to be . . .? (specific nationality, e.g., ‘Japanese, Turkish, Korean, Dutch etc.’) (1 = very proud, 4 =not at all proud).

Hypothesis 2. The greater the citizens’ national pride, the higher the tax morale.

Table 12 shows the frequency of response for “how proud of nationality ” with respect to the

total respondents. Turkey shows a higher proportion of “very proud” response than that of

Japan. Almost 40 percent of participants in the survey are responded “not proud” of Japan,

while only 3.5 percent of participants responded for “not proud” of own country in Turkey.

Table 12: Pride.

Country How proud of nationality Japan Turkey

Very proud 22.20% 81.30% Quite proud 38.80% 15.10%

Not very proud 35.10% 2.90% Not at all proud 3.80% 0.60%

Total 1030 (100%)

1264 (100%)

POLITICAL ATTITUDES: Because of political attitudes (both partisan and ideological

positions) and/ or a general distrust of political institutions and a lack of confidence in their

own country’s institutions, tax payers might less comply with their own country’s taxes. For

Recep Tekeli Policy Research Institute 23

23 Determinants of Tax Morale in Japan and in Turkey

example, Penas and Penas (2008:3) argued that “Individuals who defend the limitation of

government’s revenues and hence a protection of parts of their own income and wealth from

taxation are probably more likely to cheat on their taxes”. Although political disaffection and

lack of confidence in the political process, politicians, and democratic institutions (Montero

and Torcal 2006:6) might affect tax morale, there are other political attitudes which affect tax

morale i.e. ideological biases (being left or right in politics). (see Penas and Penas 2008)

We test political attitudes by a variable ideology, which is the self-placement in a left-right

ideological scale from 1 (left) to 10 (right). It was measured as follows:

How would you place yourself in a political scale? (1=extreme left, 10=extreme right)

We do not expect a priori sign on the coefficient of this variable.

Table 13 shows the frequency of response for “self positioning in political scale” with respect

to the total respondents. In Japan, participants’ answer is indicating the center in political

scale(52.7%) but in Turkey participants are appeared to be skewed to the centre right in

politics (see the mean score is 6.2) as many people are conservatives and traditional values are

still highly respected.

Table 13: Ideology

Country Self positioning in political scale Japan Turkey

Left 2.40% 7.90% 2 2.20% 3.90% 3 9.00% 7.00% 4 9.70% 6.00% 5 27.10% 12.90%6 25.60% 18.80%7 9.50% 7.70% 8 10.30% 13.50%9 2.10% 6.60%

Right 2.00% 15.70%Total 863

(100%)1143

(100%)Mean 5.5 6.2

It might also be interesting to analyze whether a pro democratic attitude has a positive effect

(if any) on tax morale. In general, democracy offers citizens the possibility to express their

preferences. In a democratic countries citizens are able to better monitor and control

politicians and thus to reduce the asymmetry of information between them and their

Recep Tekeli Policy Research Institute 24

24 Determinants of Tax Morale in Japan and in Turkey

representatives. Torgler and Shaltegger (2006:413) shows that a higher pro democratic

attitude leads to higher tax morale in Latin America and in transition countries as well. As

observed in transition countries, a move toward more democracy might help to enhance tax

morale and civic virtue over time. (see Torgler and Shaltegger 2006 :413)

The degree of democratization might influence citizens’ tax morale and thus we have built a

variable that measures individuals’ support for democratic government (Pro-Democracy). The

question is:

Would you say that our country is governed by a democratic political system? (1= none at all (not democratically governed), 10=country is completely governed by a democracy).

Hypothesis 3. A stronger pro democratic attitude leads to a higher tax morale.

Satisfaction with the way democracy works could also be a measure of political disaffection.

If tax payers are politically discontent then they might less comply with taxes. For example,

Feld and Frey (2007) argue that tax morale is boosted if political processes perceived as fair

and legitimate.

Table 14 shows the frequency of response for “democraticness in own country” with respect

to the total respondents. Majority of respondents in Japan believes that their county is being

governed democratically. Percentage of participants who believe the country is not

democratic at all is higher in Turkey (26.50%) than that of Japan (7%). So in Turkey the level

of democracy is believed to be lower than in Japan.

Table 14: Democraticness

Country Democraticness in own country Japan Turkey

Not at all democratic 0.80% 6.90% 2 0.60% 4.20% 3 3.00% 7.10% 4 2.60% 8.30% 5 8.00% 11.20% 6 23.00% 16.50% 7 24.90% 15.50% 8 24.50% 13.80% 9 9.30% 7.70%

Completely democratic 3.10% 8.80% Total 998 (100%) 1277 (100%)Mean 6.9 6

Recep Tekeli Policy Research Institute 25

25 Determinants of Tax Morale in Japan and in Turkey

HAPPINESS: Frey and Stutzer (2002) summarize that the extent of happiness may influence

many important economic decisions e.g. consumption activities, work behavior, investment

behavior and political behavior. In this respect, it might also be interesting to analyze whether

the citizens’ happiness (i.e. individual’s well being) affect the tax morale or not. Recent

literature on happiness is developing, but in tax morale research there are not many results

provided. Only one exception is the study by Torgler (2004) who has included the happiness

variable in order to consider the fact that in some Asian countries such as India and the

Philippines many citizens have a low living standard. Here we assume that one’s happiness

level affects the moral attitude towards tax compliance. Thus we would like to find an answer

to whether happier people are more likely to report honestly, or not?

In the WVS happiness was measured by this question:

Taking all things together, would you say you are: very happy (4), quite happy (3), not very happy (2), not at all happy (1)

Hypothesis 4. Tax morale increases with individual’s well being.

Table 15 shows the frequency of response for “ feeling of happiness” with respect to the total

respondents. In both countries 85-90% per cent of participants were happy with the current

life. However, in Turkey the proportion of “not all happy” responses are higher than in Japan.

Table 15: Happiness Country Feeling of

happiness Japan Turkey Very happy 29.20% 37.40% Quite happy 60.50% 48.90%

Not very happy 9.20% 9.40%

Not at all happy 1.10% 4.30% Total 1066 (100%) 1345 (100%)

CONTROL VARIABLES:

In addition to the main independent variables discussed above we also use additional

independent variables as controls to more fully explore what factors might determine tax

morale in the study countries. Further control variables are age, gender, education, awareness,

marital status, economic and occupation status and religiosity. Each of these variables and

expected coefficient are discussed below:

Recep Tekeli Policy Research Institute 26

26 Determinants of Tax Morale in Japan and in Turkey

1. Age. We will use age as a continuous variable and also treat age as a categorical variable

(three classes are formed in the survey: 18-29, 30-49, 50+ with 18-29 as the reference group)

Do older people have higher tax morale than younger ?

Tittle (1980) argues that older people (aged greater than 65) are more sensitive to the threat of

sanctions (both social and financial) from others in the society. Although the findings of the

tax compliance studies show that the impact of age on compliance is still uncertain, some

researchers have found that older taxpayers are more compliant (see Torgler 2006:88 and

Torgler and Murphy 2004). It has been suggested that this is because older people while aging

have acquired more material goods, have obtained greater status in their community, and have

a stronger dependency on the reactions from others (Torgler and Murphy 2004:312). Thus, the

potential costs of sanctions from others increase for this group (see Torgler 2006:88). Here we

are concerned whether this sensitivity to sanction among older taxpayers also affects level of

tax morale or not.

On the other hand, it can be argued that elderly people might be more experienced in tax

matters, which might reduce their tax compliance. But we do not expect that happens for two

reasons. First one is elder’s attachment to the community; If they have been living for a

certain period of time in the same place they are more attached to the community

(Pommerehne and Weck- Hannemann, 1996) (see Torgler and Schneider, 2005). Therefore,

attachment might have a positive effect on tax morale. Second one is as older people are

generally not subject to income taxes, they might have a different attitude towards tax

compliance (or higher tax morale). (Torgler 2004)

Table 16: Age.

Country Age Group Japan Turkey

15-24 7.00% 20.70% 25-34 16.50% 31.60% 35-44 17.40% 21.80% 45-54 20.80% 14.20% 55-64 21.50% 6.20%

65 and more years 16.70% 5.50% Total 1096

(100%) 1346

(100%) Mean 48.1 36.5

Table 16 shows the frequency of response for “age group” with respect to the total

respondents. While more than 50 percent of participants are in the first two categories of age

Recep Tekeli Policy Research Institute 27

27 Determinants of Tax Morale in Japan and in Turkey

(lower age groups ) in Turkey, in Japan 23.5% of participants are in lower age categories.

Also, percentage of elders in Japan is much higher than in Turkey.

2. Gender (categorical variable: 1= male (the reference group), 2=otherwise)

Do gender differences affect the level of tax morale? Social psychological research suggests

that women are more compliant and less self-reliant than men (e.g. Tittle 1980). Differences

in tax morale levels may be due to differences in gender values or to lower female labour

participation rates. Some researchers in the tax compliance literature found that women are

more compliant than counterpart (see Torgler 2004; Torgler 2006; Torgler and Schneider

2005, Torgler and Valev 2006)

Torgler and Valev (2006:5) concludes from Dollar et al (2001) paper that there is an evidence

of a higher presence of women parliamentarians had a statistically significant negative impact

on corruption. Swammy et al (2001) also find that if women participation in parliament, in

government ministers and in the labor force increases, then corruption will decrease.

Experimental research findings indicate that gender may influence various behaviors such as

charitable giving, bargaining, and household decision making. Strong differences between

men and women are also observed in accident involvements, alcohol and drug abuse. The

criminology literature actually gives a basis to explain possible gender differences. (Torgler

and Valev 2006:5)

Table 17 shows the frequency of response for “gender” with respect to the total respondents.

In Japan female respondents are higher than in Turkey. In Turkey almost equal percentage of

gender participated in the survey. Survey sample also represents the national distribution of

sex in Turkey. In 2007 census, female comprises 49.88% of total populations while male

comprises 50.12% of total populations.

Table 17: Gender

Country Sex Japan Turkey

Male 44.10% 50.20% Female 55.90% 49.80%

Total 1096 (100%)

1346 (100%)

Recep Tekeli Policy Research Institute 28

28 Determinants of Tax Morale in Japan and in Turkey

3. Marital status [married (in the reference group), single, living together, divorced,

separated, widowed)

Do married people have different levels of tax morale than others? An individual’s marital

status might influence his/her behavior. It was argued that married people are more compliant

than others, especially compared to singles because they are more constrained by their social

networks (Torgler and Murphy 2004; Torgler and Schneider, 2005). The argumentation for

this is stated by Tittle (1980:111) as: “A long tradition in sociology, extending back to

Durkheim, postulates that proneness toward rule breaking varies inversely with the extent to

which individuals are involved in social networks with constraining content”. Tittle (1980)

found significant differences among the different marital status, with the greatest evidence for

the singles, followed by the separated or divorced. (see Torgler 2004; Torgler 2006).

In the tax compliance literature Torgler (2006:89) stated that “some studies have found that

non-compliance is more common and of greater magnitude among married taxpayers (see

Clotfelter, 1983; Feinstein, 1991)”. This is due to the tax system. If dual incomes are treated

as one (as in the US), “being thus taxed in a higher bracket than two separate incomes,

compliance might be lower (Hays 2000)” (see Torgler 2006:89). However this is not the case

in the study countries and there is still further evidence needed to clearly understand the

correlation between tax morale and marital status.

Table 18 shows the frequency of response for “marital status” with respect to the total

respondents. In Japan higher percentage of participants are responded for “married” category

than in Turkey. In Turkey the proportion of single/never married category is much higher than

that of Japan. Divorce rate seems to be lower in Turkey than in Japan. Living together as a

married couple does not seem to be common life style in Turkish society.

Table 18: Marital status.

Country Marital status Japan Turkey

Married 72.80% 66.40% Living together as married 1.70% 0.10%

Divorced 3.00% 1.40% Separated 0.60% 0.20% Widowed 4.70% 2.30%

Single/Never married 17.20% 29.60% Total 1090

(100%) 1346

(100%)

Recep Tekeli Policy Research Institute 29

29 Determinants of Tax Morale in Japan and in Turkey

Table 19: Educational level

Country Highest educational level attained Japan Turkey No formal education - 8.30%

Inadequately completed elementary education - 3.80%

Completed (compulsory) elementary education 8.20% 36.60%

Incomplete secondary school: technical/vocational type/(Compulsory) elementary education and basic vocational qualification

1.30% 2.60%

Complete secondary school: technical/vocational type/Secondary, intermediate vocational qualification

11.50% 6.90%

Incomplete secondary: university-preparatory type/Secondary, intermediate general qualification

4.00% 3.30%

Complete secondary: university-preparatory type/Full secondary, maturity level certificate

48.00% 26.70%

Some university without degree/Higher education - lower-level tertiary certificate

1.90% 1.00%

University with degree/Higher education - upper-level tertiary certificate

25.10% 10.80%

Total 1072 (100%)

1346 (100%)

4. Education [continuous variable for higher educational level attained: 1= low (never gone

to the school), 10 = higher education)]

Do more educated people have higher tax morale level than less educated people? “Education

is related to taxpayer’s knowledge about the tax law. Better educated taxpayers are supposed

to know more about tax law and fiscal connections, and thus would be in a better position to

assess the degree of compliance (see Lewis, 1982)” (see Torgler, 2006:89). Therefore

educated taxpayers might be more aware of the public services and benefits. If this

assumption is correct, then, we might expect that better educated taxpayers would be more

compliant with their tax obligations. This assumption, however, cannot be automatically

accepted because the degree of knowledge involving evasion or avoidance opportunities

might increase with the education level. Hence we might expect that better educated taxpayers

may be less compliant because they better understand opportunities for tax evasion and

avoidance and might be better aware of how the State uses tax revenues (see Torgler 2006:89;

Recep Tekeli Policy Research Institute 30

30 Determinants of Tax Morale in Japan and in Turkey

Torgler and Murphy 2004; Torgler and Schneider 2005). Thus, as the effect of education on

tax compliance is not clear, further empirical results are needed to distinguish which effects

are stronger.

Table 19 shows the frequency of response for “highest educational level attained” with

respect to the total respondents. One interesting result from the table is that 8.3% of

participants have not attained any formal education in Turkey. Percentage of participants

attained higher education level is higher in Japan than in Turkey; 25.1% of participants in

Japan have graduated from the university, while 10.80% of participants hold a university

diploma in Turkey.

Current literature on tax morale has only used formal education as a proxy of such awareness.

Therefore, Torgler and Shaltegger (2006:409) suggested that future studies should take a look

at informal education such as time spent for reading a newspaper to investigate whether

awareness affects tax morale or not. Hence we also constructed a variable to measure such

awareness to see its effect on tax morale.

Awareness is a categorical variable. It was measured by following question:

People use different sources to learn what is going on in their country and the world.

For each of the following sources, please indicate whether you used it last week or did

not use it last week to obtain information: Daily newspaper? (categorical variable:

1=yes, 2=no)

Table 20 shows the frequency of response for “ information source ” with respect to the total

respondents. In Japan 90.1 percent of participants used a daily newspaper as information

source while in Turkey 58.60% of participants used a daily news paper which is quite lower

than Japanese rate.

Table 20: Awareness.

Country

Information source: Daily newspaper Japan Turkey Used last week 90.10% 58.60%

Not used last week 9.90% 41.40% Total 1080 (100%) 1343 (100%)

5. Economic class [we used scale of incomes: 1=low income, 10=high income].

Do the levels of tax morale vary with the level of tax payers’ income? Although some

research into tax morale has also shown that a person’s economic situation can affect their

level of tax morale, the effects of income on tax morale are difficult to assess theoretically

Recep Tekeli Policy Research Institute 31

31 Determinants of Tax Morale in Japan and in Turkey

(Torgler 2004; Torgler and Schneider 2005:237; Torgler and Shaltegger 2006:410). This is

because, as argued by Torgler and Murphy (2004:31), “the findings have been mixed. The

findings have also been found to depend on an individual’s risk preference and the

progression of the income tax schedule” 11.

If the country has a progressive income tax schedule, taxpayers with a higher income earn a

higher income return by evading [i.e. a higher marginal tax rate makes tax evasion more

profitable]. On the other hand, taxpayers with a lower income might have lower social

“stakes” or restrictions but they are less in the position to take these risks because of a high

marginal utility loss (wealth reduction) if they are caught and penalized (See Torgler 2006:90;

Torgler and Schneider 2005:232). Also, as argued by Alm and Torgler (2006:237) that “a

rational choice theory of crime predicts that individuals in lower income classes are more

likely to engage in criminal activities due to their lower opportunity costs”. As a result we do

not expect the sign of coefficient on income variable in a priori. Here we will give more

evidence which effects are stronger.

Table 21: Incomes.

Country Scale of incomes Japan Turkey

Lower step 14.80% 22.90% second step 13.80% 26.60%

Third step 13.50% 14.10% Fourth step 11.40% 14.80%

Fifth step 9.10% 3.20% Sixth step 9.20% 7.50%

Seventh step 7.80% 1.30% Eigth step 5.80% 5.80%

Nineth step 7.30% 1.90% Tenth step 7.30% 1.90%

Total 1000 (100%) 1321 (100%)Mean 4.7 3.3

Table 21 shows the frequency of response for “scale of incomes” with respect to the total

respondents. Almost half of the participants fall into the first two low income scales in Turkey,

while in Japan about one third of the participants fall into first two low-scales of income

categories. Also percentage of participants who fall into higher income scales is higher in

11 For example, Jackson and Milliron (1986) argue that if the relationship between income level and compliance is not linear but curvilinear, then using linear models might produce biased estimates, and hence causing the difference in the empirical findings.

Recep Tekeli Policy Research Institute 32

32 Determinants of Tax Morale in Japan and in Turkey

Japan than in Turkey. It also shows the consistent feature that the mean value score for

response in Japan is higher than in Turkey.

6. Occupation status (full time employed (in the reference group), part time employed, selfemployed, unemployed, housewife, student, retired, other).

Does the occupation status of individual influence tax morale? The standard argument is that

self-employed taxpayers would have more opportunity to evade their taxes than taxpayers

who have their taxes deducted each payday by their employers (Torgler and Murphy

2004:313) 12 . Torgler (2006:90) concluded from Vogel’s survey in Sweden that “self-

employed taxpayers are more likely to think that large parts of taxes were used for

meaningless purposes, that the government had made a great number of unnecessary social

reforms, that they have had less benefit from government programs than the average taxpayer,

and that the burden of taxes was too high”. Also Lewis (1982) argued that self-employed have

higher compliance costs and hence taxes become more visible for them. Torgler and

Shaltegger’s (2006:409-10) survey findings show that the coefficient of occupation status is

not significant but in the transition countries the coefficient is mostly significant with a

negative sign. They argue that in these countries self-employed individuals might feel the

financial restriction much more, as the compliance costs and taxes become more visible.

Although, it is not easy to make a clear prediction about the influence of occupation status on

tax morale, in line with the findings of Schmölders (1960) in Europe and Torgler and

Shaltegger (2006:409-10) survey findings, we would expect that self-employed Turks and

Japanese would have a lower level of tax morale than those employed by others.

Table 22: Employment status.

Country Employment status. Japan Turkey

Full time 38.40% 22.20% Part time 15.50% 2.70%

Self employed 11.60% 14.50% Retired 9.90% 9.10%

Housewife 17.90% 34.60% Students 2.80% 8.40%

Unemployed 1.60% 6.10% Other 2.40% 2.40% Total 1055 (100%) 1346 (100%)

12 We should emphasize the difference between tax morale and tax evasion. As in Torgler (2006), here the arguments are related to tax evasion and not tax morale.

Recep Tekeli Policy Research Institute 33

33 Determinants of Tax Morale in Japan and in Turkey

Table 22 shows the frequency of response for “employment status” with respect to the total

respondents. Percentage of unemployed participants is higher in Turkey (6.1%) than in Japan

(1.6%). Because of the substantial young generation in Turkey, students’ proportion is higher

in Turkey than in Japan. Also one conclusion can be drawn from the table is that one third of

participants in Turkey is housewife indicating that women’s participation in the workforce is

quite low.

7. Religiosity

Does the religion make any differences to the levels of tax morale? To answer this question

we used religiosity as an additional independent variable that was analyzed in this study. In

his earlier studies Torgler (2001) argued that moral sentiments were important for

understanding tax morale. In the same vein Torgler and Murphy (2004:310) stated that “There

are many behavioral norms and moral constraints that are strongly influenced by religious

motivations”.

It was argued that religion might influence people’s habits and might have the function to

economize and simplify people’s actions. According to Torgler (2003:295) religion forms

habits of thought common to all human beings. While analyzing the question why morality

and religion are tied together, Margolis (1997) suggested that religion includes the belief in

the right behavior which has two components: “the performance of rituals, which is important

in a society and serves to bind society together, and right behavior in the secular sense of what

is fair and just” (see Torgler 2003:298 and Torgler 2006: 85).

According to Torgler (2006:84) and Torgler and Schneider (2007:449) religious organizations

provide moral social constitutions for a society and, to a certain extent, act as ‘‘supernatural

police’’ that enforce accepted rules. This is because religion can act as a sanctioning system

that “legitimizes and reinforces social values and may also inhibit illegal behavior (Hirschi

and Stark, 1969).” (see Torgler and Schneider 2007:449)

A negative correlation between religious membership and crime (less violent and non violent)

has been reported in criminology literature (see, Torgler and Schneider 2007:449; Alm and

Torgler 2006:237). Thus, in many religions, as religiosity affects the degree of rule breaking,

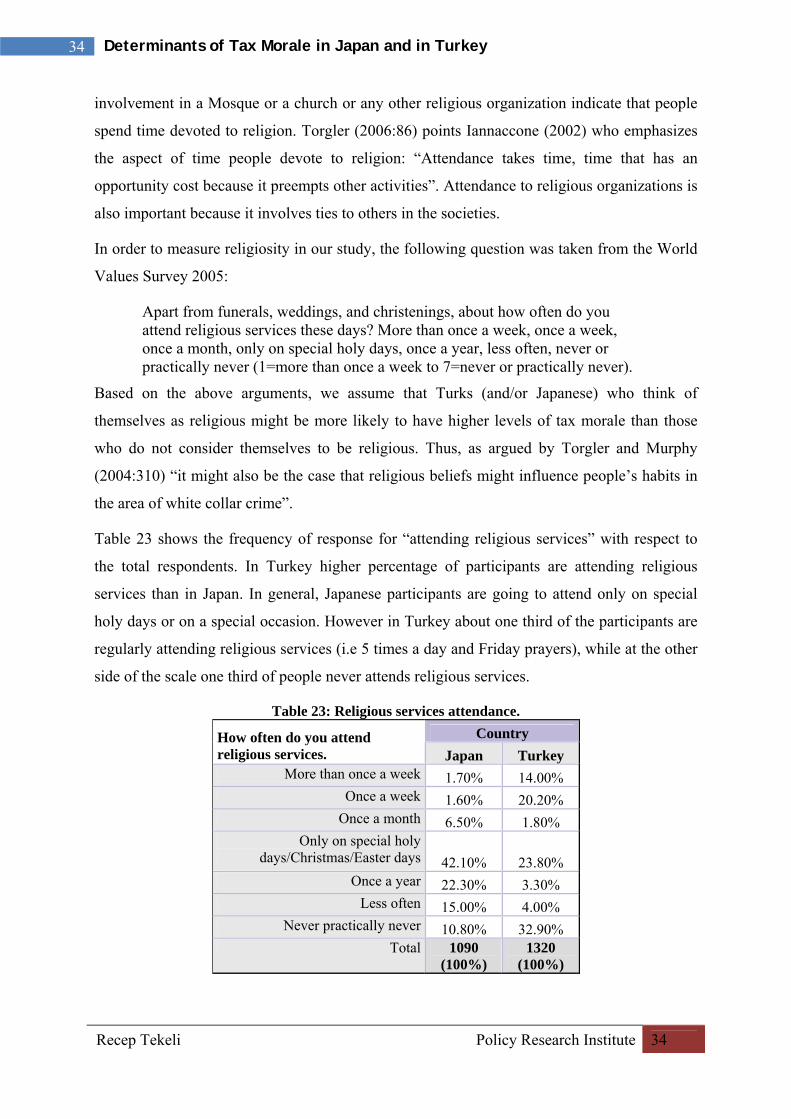

we might assume that it can be a restriction on tax evasion. The degree of religiosity could be

measured directly by asking. However, we include religiosity proxied by frequency of

religious service attendance. This is because it approximately shows how much time

individuals devote to religion. The frequency of religious service attendance and the

Recep Tekeli Policy Research Institute 34

34 Determinants of Tax Morale in Japan and in Turkey

involvement in a Mosque or a church or any other religious organization indicate that people

spend time devoted to religion. Torgler (2006:86) points Iannaccone (2002) who emphasizes

the aspect of time people devote to religion: “Attendance takes time, time that has an

opportunity cost because it preempts other activities”. Attendance to religious organizations is

also important because it involves ties to others in the societies.

In order to measure religiosity in our study, the following question was taken from the World

Values Survey 2005:

Apart from funerals, weddings, and christenings, about how often do you attend religious services these days? More than once a week, once a week, once a month, only on special holy days, once a year, less often, never or practically never (1=more than once a week to 7=never or practically never).

Based on the above arguments, we assume that Turks (and/or Japanese) who think of

themselves as religious might be more likely to have higher levels of tax morale than those

who do not consider themselves to be religious. Thus, as argued by Torgler and Murphy