determine the difference between internal and external reporting © dale r. geiger 20111

TRANSCRIPT

© Dale R. Geiger 2011 1

Determine the Difference Between Internal and External Reporting

Principles of Cost Analysis and Management

© Dale R. Geiger 2011 2

What Do Accountants Do?

© Dale R. Geiger 2011 3

Terminal Learning Objective

• Task: Determine the Difference Between Internal and External Reporting

• Condition: You are a cost advisor technician with access to PCAM course handouts, readings, and spreadsheet tools and awareness of Operational Environment (OE)/Contemporary Operational Environment (COE) variables and actors.

• Standard: with at least 80% accuracy:• Define the 4 characteristics of accounting information• Identify the difference between internal and external reporting• Classify GFEBS reports as internal or external

© Dale R. Geiger 2011 4

What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from Bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the User

© Dale R. Geiger 2011 5

What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from Bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the User

© Dale R. Geiger 2011 6

What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from Bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the User

© Dale R. Geiger 2011 7

What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the User

© Dale R. Geiger 2011 8

What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the User

© Dale R. Geiger 2011 9

What Do Accountants Do?

• Provide INFORMATION that is USEFUL to Decision Makers

• Information must be RELIABLE• Free from Bias• Verifiable

• Information must be RELEVANT• Will make a difference in the decision• Timely – frequency and lag time• Relevance is in the eye of the user

© Dale R. Geiger 2011 10

Who are the Users?

• Users may be INTERNAL or EXTERNAL• Internal users are:

• Managers and Leaders • What types of Decisions might they make?• What information might they need?

• External users are:• Investors, Creditors, Regulators and Legislators• What types of Decisions might they make?• What information might they need?

© Dale R. Geiger 2011 11

Who are the Users?

• Users may be INTERNAL or EXTERNAL• Internal users are:

• Managers and Leaders • What types of Decisions might they make?• What information might they need?

• External users are:• Investors, Creditors, Regulators and Legislators• What types of Decisions might they make?• What information might they need?

© Dale R. Geiger 2011 12

Who are the Users?

• Users may be INTERNAL or EXTERNAL• Internal users are:

• Managers and leaders • What types of decisions might they make?• What information might they need?

• External users are:• Investors, Creditors, Regulators and Legislators• What types of Decisions might they make?• What information might they need?

© Dale R. Geiger 2011 13

Who are the Users?

• Users may be INTERNAL or EXTERNAL• Internal users are:

• Managers and leaders • What types of decisions might they make?• What information might they need?

• External users are:• Investors, creditors, regulators, legislators and

citizens • What types of decisions might they make?• What information might they need?

© Dale R. Geiger 2011 14

External User Needs

• Examining an organization’s performance over time demands CONSISTENCY• Assures users that the information is prepared in

the same manner over multiple time periods• Deciding whether to fund competing

organizations or programs demands COMPARABILITY• Assures that the information from all organizations

is prepared according to the same set of principles

© Dale R. Geiger 2011 15

External User Needs

• Examining an organization’s performance over time demands CONSISTENCY• Assures users that the information is prepared in

the same manner over multiple time periods• Deciding whether to fund competing

organizations or programs demands COMPARABILITY• Assures that the information from all organizations

is prepared according to the same set of principles

© Dale R. Geiger 2011 16

External User Needs

• Examining an organization’s performance over time demands CONSISTENCY• Assures users that the information is prepared in

the same manner over multiple time periods• Deciding whether to fund competing

organizations or programs demands COMPARABILITY• Assures that the information from all organizations

is prepared according to the same set of principles

© Dale R. Geiger 2011 17

External User Needs

• Examining an organization’s performance over time demands CONSISTENCY• Assures users that the information is prepared in

the same manner over multiple time periods• Deciding whether to fund competing

organizations or programs demands COMPARABILITY• Assures that the information from all organizations

is prepared according to the same set of principles

© Dale R. Geiger 2011 18

External User Needs

• Examining an organization’s performance over time demands CONSISTENCY• Assures users that the information is prepared in

the same manner over multiple time periods• Deciding whether to fund competing

organizations or programs demands COMPARABILITY• Assures that the information from all organizations

is prepared according to the same set of principles

© Dale R. Geiger 2011 19

Consistent Combat Ship

16" guns

cruise missiles

landing gatesperiscope

ballistic missiles

flight deck

submersible hull

helicopter pad

torpedotubes

© Dale R. Geiger 2011 20

Check on Learning

• Which characteristic requires timely information?

• Which characteristic requires verifiable information?

• Why would users demand consistency?

© Dale R. Geiger 2011 21

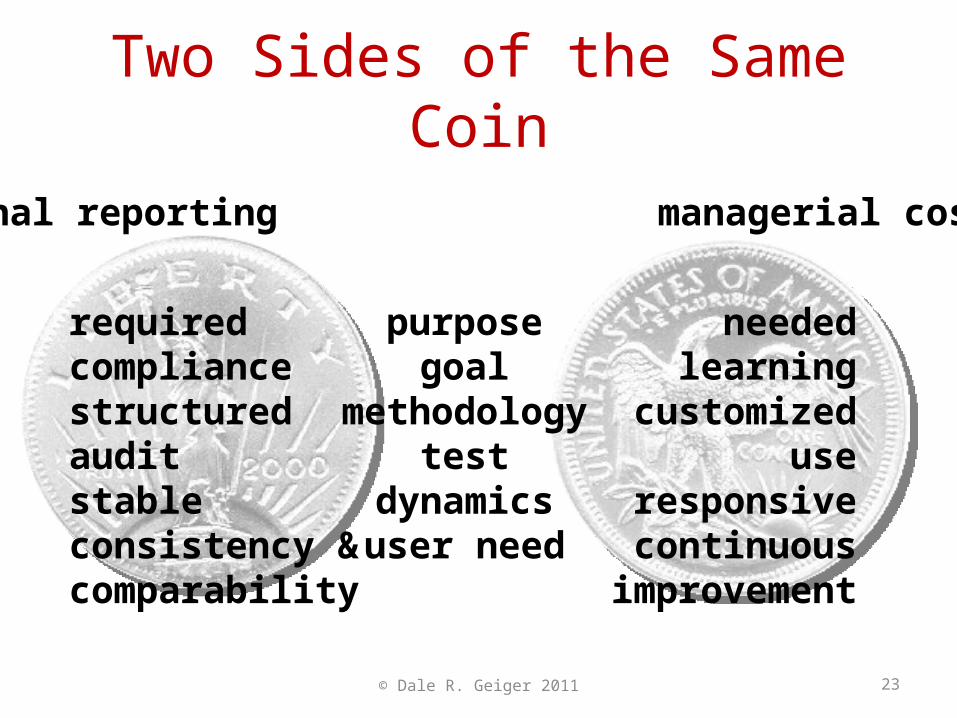

Two Sides of the Same Coin

requiredcompliancestructuredauditstableconsistency &comparability

purposegoal

methodologytest

dynamicsuser need

neededlearning

customizeduse

responsivecontinuous

improvement

external reporting managerial costing

© Dale R. Geiger 2011 22

Two Sides of the Same Coin

requiredcompliancestructuredauditstableconsistency &comparability

purposegoal

methodologytest

dynamicsuser need

neededlearning

customizeduse

responsivecontinuous

improvement

external reporting managerial costing

© Dale R. Geiger 2011 23

Two Sides of the Same Coin

requiredcompliancestructuredauditstableconsistency &comparability

purposegoal

methodologytest

dynamicsuser need

neededlearning

customizeduse

responsivecontinuous

improvement

external reporting managerial costing

© Dale R. Geiger 2011 24

Two Sides of the Same Coin

requiredcompliancestructuredauditstableconsistency &comparability

purposegoal

methodologytest

dynamicsuser need

neededlearning

customizeduse

responsivecontinuous

improvement

external reporting managerial costing

© Dale R. Geiger 2011 25

Two Sides of the Same Coin

requiredcompliancestructuredauditstableconsistency &comparability

purposegoal

methodologytest

dynamicsuser need

neededlearning

customizeduse

responsivecontinuous

improvement

external reporting managerial costing

© Dale R. Geiger 2011 26

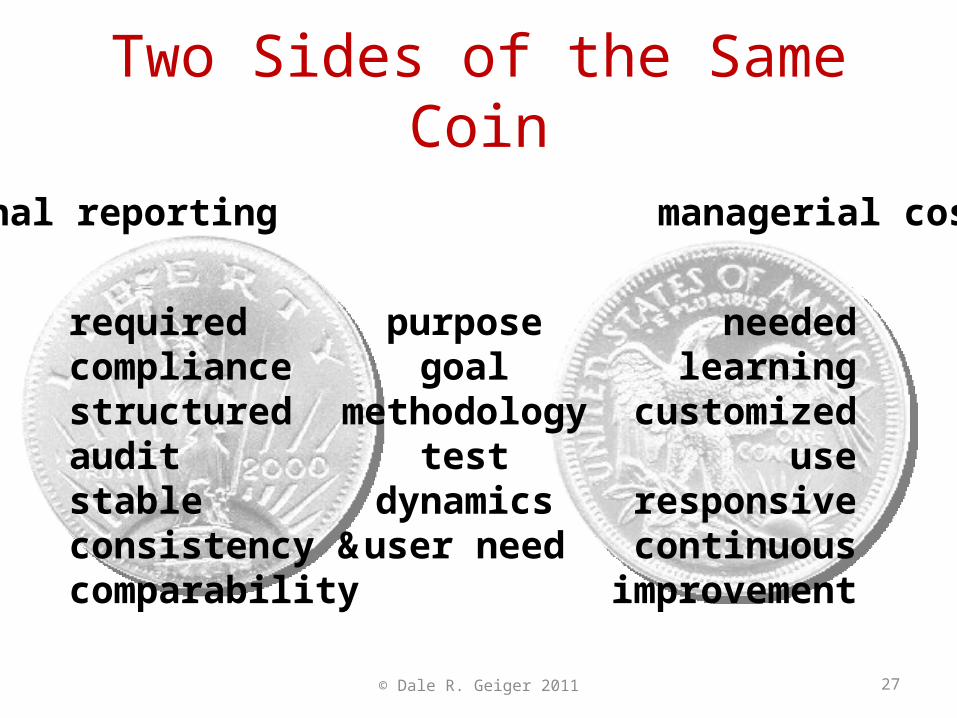

Two Sides of the Same Coin

requiredcompliancestructuredauditstableconsistency &comparability

purposegoal

methodologytest

dynamicsuser need

neededlearning

customizeduse

responsivecontinuous

improvement

external reporting managerial costing

© Dale R. Geiger 2011 27

Two Sides of the Same Coin

requiredcompliancestructuredauditstableconsistency &comparability

purposegoal

methodologytest

dynamicsuser need

neededlearning

customizeduse

responsivecontinuous

improvement

external reporting managerial costing

© Dale R. Geiger 2011 28

Example

External Report: Tax Return • Why?• How?• Test of success?• Dynamics?

Internal Report: Checkbook• Why?• How?• Test of success?• Dynamics?

© Dale R. Geiger 2011 29

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 30

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 31

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 32

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 33

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 34

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

© Dale R. Geiger 2011 35

Research: System Uses at 59 Federal Organizations

1 2 3 4 5 6 7 8

9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24

25 26 27 28 29 30 31 32

33 34 35 36 37 38 39 40

41 42 43 44 45 46 47 48

50 51 52 53 54 55 56 57

58 59

mgmt control

pricingOH allocation

reqr costing

BLM PBS

VMSS

WVA

FGIS

Check on Learning

• What are the basic uses for Cost Accounting systems?

• Should all cost systems be the same?• Why or why not?

© Dale R. Geiger 2011 36

What about GFEBS?

• General Fund Enterprise Business System• Used Army-wide• Permits real-time posting of financial

transactions• Reports costs according to Budget-relevant

and non-Budget-relevant Cost Objects• Are GFEBS reports internal or external?

© Dale R. Geiger 201137

Unit Cost Report

© Dale R. Geiger 2011 38

Unit Cost Report

This report shows the actual and planned quantities and actual and

planned (average) unit cost for various SKFs (Statistical Key Figures)

such as Headcount.

© Dale R. Geiger 2011 39

Discussion Questions

• Who would use this report? • How might they use it?• If you were the Senior Leader of this

organization, would you be surprised that your cost per headcount was $78,919.20?

• What would you want to know about that number?

• Would this be an internal or external report for you?

© Dale R. Geiger 2011 40

Check on Learning

• What characteristics would identify a report as internal to an organization?

• What characteristics would identify a report as external to an organization?

© Dale R. Geiger 2011 41

© Dale R. Geiger 2011 42

Conclusion

• Needs for internal cost information are as varied as the organizations themselves

• External cost reports:• Facilitate comparison of organizations by external

users• Are unlikely to meet internal management

information needs