developing dubai’s debt market to promote investment and

TRANSCRIPT

Developing Dubai’s debt marketto promote investment and growth

2 | Developing Dubai’s debt market to promote investment and growth

Developing Dubai’s debt market to promote investment and growth | 3

Content

Foreword

Acknowledgement

Executive summary

Rationale for having a local debt market

Financial sector assessment and overview of the debt market

Benchmarking analysis

References

10

11

12

22

24

33

52

4 | Developing Dubai’s debt market to promote investment and growth4 | Financial sector development for promoting investment and sustainable growth in Dubai

Developing Dubai’s debt market to promote investment and growth | 5

His Highness Sheikh Mohammed Bin Rashid Al Maktoum, Vice Presidentand Prime Minister of the UAE, and Ruler of Dubai

6 | Developing Dubai’s debt market to promote investment and growth

His Highness Sheikh Hamdan Bin Mohammed Bin Rashid Al Maktoum,Crown Prince of Dubai and Chairman of Dubai Executive Council

Developing Dubai’s debt market to promote investment and growth | 7

His Highness Sheikh Ahmed Bin Saeed Al Maktoum, President of Dubai CivilAviation and Chairman and Chief Executive of Emirates Airline and Group

8 | Developing Dubai’s debt market to promote investment and growth

The world's financial landscape has changedfundamentally over the last few years. Lessons drawnfrom the global financial crisis 2008 point to thepressing need to have an innovative financialarchitecture that is not only acting to provide adequatefinance to governments and businesses, but also to beeffective, timely and predictable in order to enhance thestability, wealth, social well-being, and environmentsustainability, hence secure long-term growth for thelocal economy.

One of the significant developments happened in theglobal financial market, however is the rise of capitaldebt markets. International reports suggest that globaldebt capital deals have increased rapidly over the lastfew years and totaled US$5.7 trillion in 2014.Furthermore, in addition to the US and other westerncountries, Australia and Japan, new players have enteredactively the said markets mostly from emerging markets.

If we look to Dubai, the last two decades haveconfirmed its position as a business capital of the UAE;thanks to its outstanding economic performance whichhas been the result of a deliberated policy aimed atintegrating Dubai into the world economy andtransforming it into an attractive regional andinternational hub for business and investment asunderpinned by Dubai Plan 2021. However, in its questto achieve this vision, the leadership of Dubai has placedthe continued development of the financial sector,including the debt capital market, high on its policyagenda given the important role it plays in facilitatingeconomic activity and promoting growth.

Precisely, in Dubai, further developing the local debtmarket both conventional and Islamic will have myriadadvantages for the domestic economy, especially in atime where demand is picking up in the run up to EXPO 2020 and given the continued investment oninfrastructure projects as well as the booming activitiesin the private sector. Also, we should start planningahead for new and better ways of financing thegrowing future needs expected to arise from public and private sectors without putting too much pressureon the domestic banks.

Hence, this second edition of policy report preparedjointly by ‘Dubai Economic Council’ and ‘Deloitte’ hascome at the right time, and succeeded in shedding thelight on the most important issues related to thedevelopment of the debt capital market in Dubai.

Saying that, we look forward to various entities fromboth public and private sector in Dubai and UAEbenefiting from this report in order to rationalize theirdecisions and maximize their gains when get involved inthe local debt markets.

Sheikh Ahmed bin Saeed Al Maktoum

10 | Developing Dubai’s debt market to promote investment and growth

We are delighted to announce the release of our secondreport in a series of publications aimed at encouraginginvestment in Dubai, titled “Developing Dubai’s debtmarket to promote investment and growth,” authored incollaboration between Deloitte Corporate Finance andthe Dubai Economic Council.

The report is being released at a time where debt capitalmarkets in particular can play a crucial role in enhancingthe financial sector through their role in diversifying thesources of financing for both the government and theprivate sector, in addition to attracting more foreigndirect investment.

A robust debt capital market offers an additional sourceof financing and can act as a source of stability to theeconomy by supporting growth across various economiccycles. The development of a deep and liquid debtmarket in Dubai is a continuous process, which will nodoubt require collaborative support from both theprivate and public sectors to ensure efforts areharmonised and steered towards promoting investmentand growth in Dubai.

This report clarifies the rationale for developing a localdebt market and presents an analysis of the factors thatare likely to provide the stimulus for the developmentand expansion of Dubai’s conventional and Islamic debtmarkets. The report also provides a benchmarking ofDubai with other regional and international financialhubs that have either proven successful in attractinginvestment, or are at the stage of developing their debtcapital markets and directly competing with Dubai. Thebenchmarking focuses on enhancing Dubai’s profile andcompetitiveness in areas of product innovation, marketinfrastructure and regulatory frameworks, which arefundamental factors for driving the development ofboth conventional and Islamic debt markets.

Finally, the report identifies potential gaps that couldimpact Dubai’s competitiveness and makes a number of policy recommendations that could support thedevelopment of the local debt market.

Foreword

H.E. Hani AI HamliSecretary GeneralDubai Economic Council

Humphry HattonCEOFinancial Advisory

Developing Dubai’s debt market to promote investment and growth | 11

The Dubai Economic Council (DEC) and DeloitteCorporate Finance Limited continue to share their visionand deploy their complementary comparative advantageto conceptualize, design and write the second edition oftheir annual reports on the financial sector in Dubai.

We would like to extend our gratitude to Her ExcellencySheikha Mona Abdullah Al Moalla, DEC Chief OperatingOfficer, Strategic Planning and Operations, for her role

in creating the motivating work environmentfor the staff and enabling the timely completion of thisreport. Dr. Abdulrazak Al Faris, DEC’s Deputy SecretaryGeneral for Economic Affairs, revised the report duringits various stages and provided valuable comments.Special thanks go to the Deloitte technical team: Messrs.David Stark, Panos Stavropoulos and Karim Labban andDEC technical team: Dr. Ali Al Sadik, Dr. MohamedTrabelsi, Ms. Dhuha Fadhel, Mr. German Gussakovskiyand Ms. Amal Al Iriani. We are also all grateful to Ms. AishaAl-Shaya and Mr. Buti Al Marri who took care of thelogistical and organizational issues.

We are grateful to Dubai Financial Market, Dubai IslamicEconomy Development Centre, Dubai InternationalFinancial Center, HSBC bank and Emirates NBD bank for participating at a closed-door seminar aimed atengaging stakeholders and experts to have their insightsand critical comments prior to the launch of the report,as well as the panel of experts; Dr. Magda Kandil,

Dr. Sayd Farook, Mr. Mohammed Ali Yasin, Mr. HussainAl Tajir and Mr. Chirag Shah who participated at thelaunch event of the report held on the 23rd November,2015. Dr. Ibrahim Elbadawi, DEC’s Director ofMacroeconomics & Forecasting and Mr. Rajeev Patel,Director at Deloitte supervised all stages of the projectand led the DEC-Deloitte joint team. Mr. Irfan AlHassani, Mr. Mohamed Al Sayed, Ms. Dana AlQatawneh and Ms. Nesrine Sabra helped in the mediaplan and invitation letters.

Last, but not least, we would also like to express oursincere gratitude to all 'other' DEC and Deloitte staffinvolved on this project in one way or another. We wishthem all continued success and let us keep up the goodwork.

Hani R. AI HamliSecretary GeneralDubai Economic Council

Humphry HattonCEOFinancial AdvisoryMiddle East Region

Acknowledgement

12 | Developing Dubai’s debt market to promote investment and growth

I. Purpose of the reportThe aim of this report is to identify factors that are likelyto provide the stimulus for the development andexpansion of Dubai’s conventional and Islamic debtmarkets. In view of this, we consider other financialhubs, both regional and international, that have eitherproven successful in attracting investments, or are at thestage of developing their debt capital markets anddirectly competing with Dubai. Markets selected as abenchmark are as follows:• Conventional debt markets: New York, London,

Singapore, Hong Kong, Riyadh and Manama; and• Islamic debt markets: Kuala Lumpur, London, Riyadh,

Doha and Manama.

In light of this, our report is broadly structured asfollows:1. Executive summary outlining the policy

recommendations emerging from the benchmarkinganalysis and focusing on:a. Supporting product innovation to increase market

liquidity;

b. Improving the underlying infrastructure to supportissuance and trading;

c. Enhancing the regulatory framework; andd. Developing the Islamic debt market, focusing on

key areas of infrastructure, regulation and productinnovation.

2. A brief overview of the rationale for having a localdebt market;

3. Assessment of the financial sector and overview ofrecent developments in Dubai’s debt market; and

4. Analysis of key benchmarking criteria, results andlatest developments in peer markets.

Executive summary

Developing Dubai’s debt market to promote investment and growth | 13

II. Rationale for having a local debt market A sound and well-functioning financial system can helpsustain long-term economic growth as it allows formobilising savings to more productive sectors in theeconomy and promoting financial stability. Additionally,a deep and liquid financial system with diverseinstruments can offer resilience against shocksemanating from volatile markets.

Whilst the UAE has come a long way with thedevelopment of its financial system, the case fordeveloping the local debt market is stronger due to a number of factors, including:

• The robust fundamentals and economic growth of the UAE are supporting increased demand frominternational investors for high-quality papers issuedby the Government and large corporates;

• The continued investment in infrastructure and otherdevelopmental projects increase the need for diversesources of funding with long-term maturities;

• The development of the local debt market will helpdiversify the existing funding of Government RelatedEntities (GREs) and large corporates, which arecurrently heavily dependent on bank financing. Thiscan also reduce the systemic risk within the economyand provide banks with further flexibility in terms ofcomplying with central bank regulations that limit theexposure of banks to no more than 100% of theircapital base;

• A local debt market can facilitate the sterilisation oflarge capital inflows, and improve the implementationof the country’s monetary policies. It can also helpmitigate exchange rate risks by providing analternative source of multi-currency financing withouthaving to resort to foreign sources of capital; and

• The latest efforts and initiatives to establish Dubai as a global Islamic financial centre will increase demandfrom investors for high quality Islamic papers, whichcan be partially met by issuing local currency Sukuk.

• A deep and liquid local debt market will provide themonetary authority with better tools to address thedivergent business cycles between the economies ofthe UAE and the US, to which the UAE Dirham isbeing pegged, especially in a time of low oil pricesthat causes market liquidity to dry up.

A deep and liquid local bond market isfundamental for the development ofDubai’s financial sector. This couldfurther promote financial stability andsupport economic growth in Dubai and the UAE.

14 | Developing Dubai’s debt market to promote investment and growth

III. Financial sector assessment Overview of the Financial Development Index’s resultThe Financial Development (FD) index published by the International Monetary Fund (IMF) was used in this report as an indicator to assess the development of the financial sector in the UAE compared to otherbenchmarks. The ranking in the index is largely derivedfrom two sub-indices, namely: • The Financial Institutions (FI) index; and• The Financial Market (FM) index.

The chart below sets out the ranking of the UAE undereach of the three indices, compared to the ranking ofthe other benchmarking countries. A higher score wouldindicate a more developed financial sector.

The UAE appears to be lagging behind global financialcentres, such as Malaysia, UK, Singapore, USA, andHong Kong but is well positioned compared to some of the other regional financial centres, such as Bahrainand Qatar.

The ranking of regional financial centres on the sameindex has remarkably improved compared to the UAEover recent years. This highlights the need to cope with the growth of these financial centres by furtherdeveloping the UAE’s financial sector and local debtmarket.

Overview of historical debt issuanceThe UAE remains the largest bond market in the GCC in terms of issuance with around USD 19 billion of newbond issuances in 2013, representing a 41% marketshare of total new issuances in the GCC.

In addition, Dubai accounted for about 72% of the totalbond issuances in the UAE in 2014 and has become theworld leader in the Islamic bond industry overcomingother Islamic debt markets with a USD 36.7 billionnominal value of listed Sukuk in 2014.

Nevertheless, the UAE lags behind other GCC countriesin terms of total debt issuances (rather than bondissuance only) given that the central bank of UAE doesnot currently issue other type of debt products, such as treasury bills, notes and Sukuk denominated in local currencies.

Source: The Financial Development Index published by the International Monetary Fund, 2015

FM FI

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

HKG USA SGP UK MYS KSA BHR UAE

Score

FD

QAT

Developing Dubai’s debt market to promote investment and growth | 15

IV. Reaching the next levelTo enable Dubai to further develop its conventional and Islamic debt markets a benchmarking analysis wasconducted to identify challenges and improvementopportunities. Whilst Dubai currently surpasses itsregional neighbours Riyadh and Manama with regardsto conventional debt market maturity, furtheropportunities for development exist to enable it tocompete with leading financial hubs, such as New York,London, Signapore and Hong Kong. The underlyingdevelopment areas include strengthening the protectionof investors’ rights, developing the underlying tradinginfrastructure and framework to accommodatederivatives, targeting retail investors and establishing an effective benchmark yield curve.

With regards to the maturity of its Islamic debt marketDubai ranks similarly with its regional neighbours,Riyadh and Doha, whilst Kuala Lumpur represents the leading market, followed by Bahrain and London.Dubai could further develop key areas, such as disputeresolution and bankruptcy regulation for Sharia’acompliant products, development of a Sharia’acompliant repurchase agreement and introduce aplatform to allow retail investors to access the primarySukuk market.

In order to assess Dubai’s competitive position within debt markets, we have conceptualised thefollowing framework, which was used as part of thebenchmarking analysis covering the following areas of product innovation, supporting infrastructure and the effectiveness of the regulatory framework, which we considered as the fundamental factors in thedevelopment of the conventional and Islamic debtmarkets.

Enhancing Dubai’s profile andcompetitiveness in areas of productinnovation, market infrastructure andregulatory frameworks is fundamental forthe development of both conventionaland Islamic debt markets

Government initiativesand guarantees

Credit rating

Investor protection

Securitisation

Derivatives

Green bonds

Trading platforms

Clearing and settlement

Investor base

Benchmark yield curve

Information disclosure database

Registration and approval process

Maker incentives

Infrastructure

Regulatoryframework

Productinnovation

DevelopingDubai's debt

market

Productinnovation

Infrastructure

Regulatoryframework

Islamic debtmarket

16 | Developing Dubai’s debt market to promote investment and growth

The tables below summarise how Dubai ranks againstthe benchmark markets under the three main areas ofproduct innovation, infrastructure and regulatoryframework.

Dubai’s conventional debt market is more maturecompared to its regional neighbours, Riyadh andManama in the areas of product innovation andinfrastructure. Compared to more developed cities, such as New York, London, Singapore and Hong Kong,Dubai is less developed with regards to the use of derivatives and green bonds, an effective benchmarkyield curve is under-developed, and the registration andapproval process for bond issuances is relatively longer.

Additionally, the current regulatory framework providesless protection to investors, primarily due to limitationsin the current bankruptcy and dispute resolutionregulations.

In the areas of clearing and settlement infrastructure,Dubai ranks on par with New York, London, Singaporeand Hong Kong, whilst with regards to the use ofcovered bonds and the supporting regulatoryframework, it ranks higher than New York andSingapore. Dubai also ranks on par with Hong Kong inthe areas of maturity of trading platforms, but slightlybehind New York, London and Singapore mainly due to the lack of a derivatives trading platform.

Category Dubai New York London Singapore Hong Kong Riyadh Manama

Product innovation

Covered bonds Welldeveloped

Under-developed

Welldeveloped

Under-developed Not available* Not available* Not available*

Derivatives Under-developed

Welldeveloped

Welldeveloped Adequate Adequate Under-

developedUnder-

developed

Government bond derivatives Not available* Welldeveloped

Welldeveloped

Welldeveloped

Welldeveloped Not available* Not available*

Green bonds Not available* Adequate Adequate Under-developed

Under-developed Not available* Not available*

Infrastructure

Trading platforms Adequate Welldeveloped

Welldeveloped

Welldeveloped Adequate Adequate Adequate

Clearing and settlement Welldeveloped

Welldeveloped

Welldeveloped

Welldeveloped

Welldeveloped Adequate Adequate

Investor base Adequate Welldeveloped

Welldeveloped Adequate Adequate Under-

developed Adequate

Benchmark yield curve Under-developed

Welldeveloped

Welldeveloped Adequate Adequate Under-

developedUnder-

developed

Database for information disclosure Adequate Welldeveloped

Welldeveloped Adequate Well

developedUnder-

developedUnder-

developed

Registration and approval process Adequate Welldeveloped

Welldeveloped

Welldeveloped

Welldeveloped Adequate Adequate

Regulatory framework

Credit rating Adequate Welldeveloped

Welldeveloped

Welldeveloped

Welldeveloped

Under-developed Adequate

Investor protection Under-developed

Welldeveloped

Welldeveloped

Welldeveloped Adequate Under-

developedUnder-

developed

Source: The ratings applied for each of the benchmark markets are illustrative and directional based on qualitative research and notpurely based on quantitative indicators

*product not used

Conventional debt market benchmarking

Developing Dubai’s debt market to promote investment and growth | 17

In terms of maturity of the Islamic debt market Malaysiais the most developed, whilst Dubai ranks on par withRiyadh and Doha with regards to product innovation,supporting infrastructure and the regulatory framework.Dubai has recently announced a number of initiatives,such as the development of a Sharia’a compliantrepurchase agreement, a platform to allow retailinvestors access to the primary Sukuk market and the

UAE announced plans for the establishment of a Sharia’a board to oversee standards, which ifimplemented could allow Dubai to overtake Riyadh,Doha, London and Manama and also bring the city onpar with Kuala Lumpur. In addition, London and KualaLumpur have a more developed dispute resolution andbankruptcy regulatory framework when compared toDubai.

The above conceptual framework and summary of the benchmarking results are underpinned by detailedanalysis in the benchmarking analysis section of thisreport. The remainder of this executive summarypresents the key policy recommendations derived from the benchmarking results.

Category Dubai Kuala Lumpur Riyadh Doha London Manama

Product innovation

Sharia’a compliant repurchaseagreement

Not available(announced)

Under-developed Not available Not available Not available Under-

developed

Sharia’a compliant derivatives Under-developed

Under-developed

Under-developed

Under-developed

Under-developed

Under-developed

Green Sukuk Not available (UAEannounced plan) Well developed Not available Not available Not available Not available

Infrastructure

Secondary Sukuk trading platforms Adequate Well developed Adequate Adequate Adequate Adequate

Primary offering to retail investorsNot available

(underdevelopment)

Adequate Not available Not available Not available Under-developed

Regulatory framework

Dispute resolution and bankruptcyregulation

Under-developed Adequate Under-

developedUnder-

developed Well developed Under-developed

Sharia’a board to oversee standardsNot available

(announced plansat federal level)

Well developed Not available Not available Not availableNot available(announced

plans)

Primary sales of Sukuk to retailinvestors

Not available(announced byNasdaq Dubai)

Well developed Not available Not available Not available Adequate

Source: The ratings applied for each of the benchmark markets are illustrative and directional based on qualitative research and notpurely based on quantitative indicators.

Islamic debt market benchmarking

Following a qualitative benchmarkinganalysis against peer international andregional financial hubs, a number ofareas for improvement have beenidentified across both conventional and Islamic debt markets

18 | Developing Dubai’s debt market to promote investment and growth

V. Key policy recommendationsWe have identified a number of key policyrecommendations, which span the four key areas of our benchmarking analysis:a. Product innovation to meet market requirements

and increase liquidity;b. Infrastructure enhancements to support primary

market issuance and secondary trading forinstitutional and retail investors;

c. Formalisation of the regulatory framework to supportthe market; and

d. Development of the Islamic debt market focusing onkey areas of product innovation, infrastructure andregulation.

The policy recommendations below focus onimprovement opportunities for Dubai to enable furtherdevelopment and growth of its debt market.

Product innovation to increase liquidityProduct innovation can play an important role indeveloping markets, and recommendations couldinclude the following:•The introduction of derivatives on Dubai’s exchanges(e.g. interest rate swaps, Government bond forwardsand currency exchange swaps) may help support riskmanagement and increase market liquidity. The timingof introducing these products should be assessed toensure that the debt market has reached theappropriate size and adequate investor appetite ispresent. In addition, the appropriate regulatoryframework should be developed to regulate issuanceand trading of these products, supported further

through the development of an electronic tradingplatform.

• The introduction of appropriate regulation for theissuance and trading of green bonds, with a view toenable trading on its exchanges once debt market size and demand reach satisfactory levels.

Infrastructure enhancements to support issuanceand tradingThere are a number of key infrastructure enhancementsthat could be considered to support issuance andtrading: Trading platforms• In order to accommodate additional products, such

as derivatives, further development of the existingelectronic trading platforms may be required.

• Dubai Financial Market (DFM) may seek to increasemarket liquidity by accommodating Exchange TradedFunds (ETFs) and Real Estate Investment Trusts (REITs).

• NASDAQ Dubai may establish a platform to targetretail investors, allowing for the primary issuance andon-screen secondary trading of Government bonds, inline with the exchange’s recent announcement. TheDFM may shadow this approach and adopt a similarplatform to target retail investors, once justifiablematurity levels are reached.

• In attracting additional investors, Dubai may considerfurther developing the connectivity of the tradingplatforms on its exchanges to include directconnections with other platforms in the UAE, alongwith other regional markets.

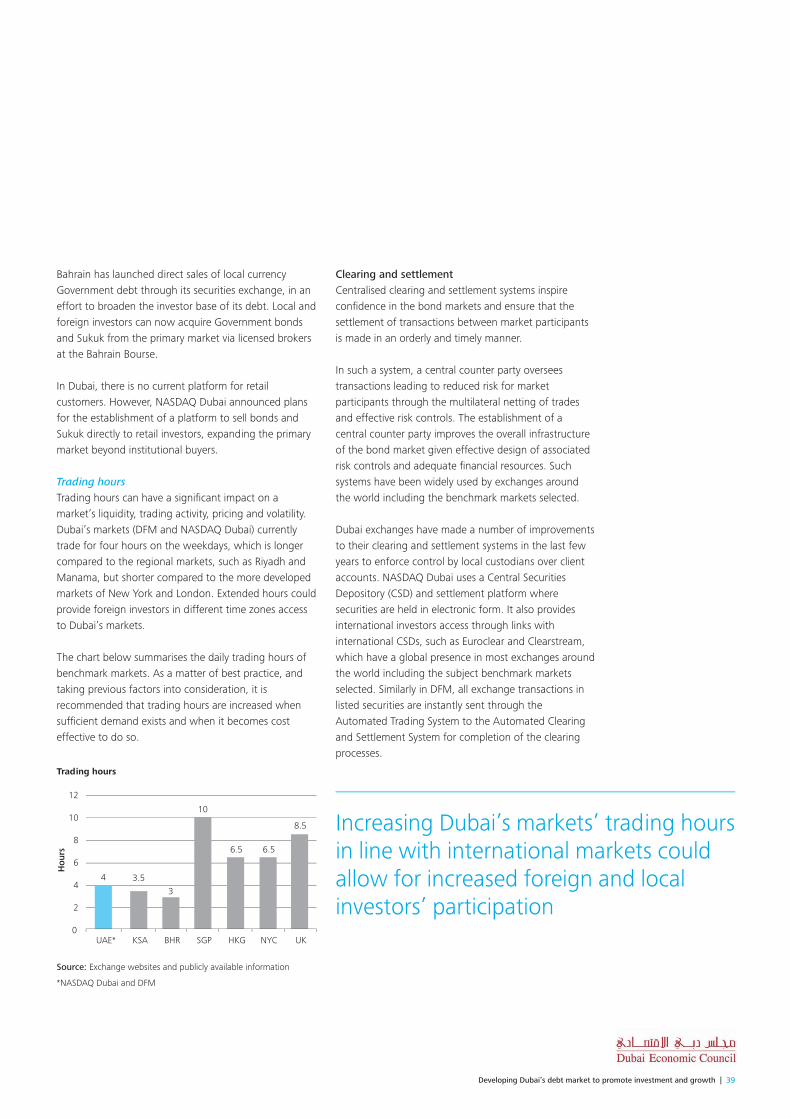

• Furthermore, the trading hours of Dubai’s exchangescould be extended, in line with international markets,to bolster trading activity during shoulder periods ofthe day and increase foreign investor participation.Market maturity and liquidity levels should be assessedin parallel with the additional costs associated withextending trading hours.

Clearing and settlement• To be in line with the more developed markets of

London and New York, Dubai may wish to considershortening the settlement cycle for Government bondsthereby providing the stimulus for increased activitylevels through faster execution and reducedsettlement risk.

The introduction of new debt productson Dubai’s exchanges, includingderivatives and green bonds canpromote liquidity and bolster demand in the debt market

Developing Dubai’s debt market to promote investment and growth | 19

Investor base• To further boost liquidity, the debt market’s investor

base may be widened by targeting a broader spectrumof investors, including foreign institutions, Islamicinstitutions and retail investors. The development ofadditional products and offerings, such as greenbonds, derivative products and Sharia’a compliantproducts, may be a further catalyst to attractingadditional investors to the debt market.

Benchmark yield curve• Dubai may consider issuing a wider range of

Government bond maturities in an effort to establish a more effective benchmark yield curve, furthersupporting market participants in pricing corporateissues more effectively across a wider range ofmaturities.

• The frequency of Government bond issues may also be increased. In addition, quasi-Governmentcorporations may be incentivised in order to galvanisethem to issue bonds and maintain an up to datebenchmark yield curve.

• Dubai may also consider introducing an issuancecalendar for Government bonds including Sukuk,thereby providing investors with visibility over plannedissues, which could lead to improved markettransparency and investment levels.

Information disclosure database• Dubai may seek to introduce a database to capture

information with regards to issuers and trades, inparticular relating to Over the Counter (OTC) tradeswhere access to information is limited as compared to other trades executed. This may lead to increasedmarket transparency and better pricing of issues,culminating in stronger investor participation.

• To ensure the proper and effective safeguard of data,platforms that facilitate and promote the electronicsubmission of information and disclosures by issuersmay be introduced.

Registration and approval process• In line with other markets, such as London, Signapore

and Hong Kong, NASDAQ Dubai may considerreducing the admission time for issuers. In addition,

Dubai’s exchanges could consider adopting tailoredregistration and approval processes to cater fordifferent types of investors and issuances.

• In 2014, the UAE’s Securities and CommoditiesAuthority (SCA) introduced the debt securities issuanceprogramme to allow for a fast track process forregular issuers, in an effort to reduce the approvalcycle. The approval and admission process couldfurther be tailored based on the issuance rating (e.g.high vs. low quality), the type of investors (institutionalvs. retail) and the type of corporate bonds issued(plain vanilla vs. complex structures).

Market making incentives• DFM could further increase market liquidity by

providing incentives to market makers, to attract them on its exchange. In 2012, the SCA approvedmarket making regulations in an effort to increasemarket liquidity, however the DFM exchange currentlyhas no market makers appointed. In comparisonNasdaq Dubai has successfully incentivised marketmakers to join the exchange by offering a 100%rebate on trading and clearing fees to encourageparticipation and improve liquidity. DFM couldpotentially offer fee rebates to market makers as wellas consider adding flexibility to current market makingrequirements, which set limits on the number oftransactions and number of trading days in a security.

Formalise the regulatory frameworkA number of improvement opportunities have beenidentified to enhance the regulatory framework andfurther support the development of Dubai’sconventional debt market:

Developing the debt market’sinfrastructure is key to support efficienttrading and encourage issuers andinvestors’ participation

20 | Developing Dubai’s debt market to promote investment and growth

Credit rating• In 2014, the SCA announced that it is no longer

mandatory to obtain credit ratings from ratingagencies. Cancelling the requirement for mandatoryratings should be considered in the context ofencouraging issuers and making it more cost and time effective to offer bonds, against discouraginginvestors who seek to assess the credit risk of issuersby reverting to credit rating agencies.

• Whilst mandatory credit ratings might have lost some of its popularity in the aftermath of the globalfinancial crisis, the availability of credit ratings remainscritical to add transparency to the bond market andencourage investor participation by providing a vehiclefor credit risk assessment of issuers. This is renderedeven more important in a market dominated byprivately held corporates where investors have limitedaccess to the corporates’ financial information.

• Consequently, it is recommended that Dubai’sregulators and exchanges incentivise, or at the very least, encourage issuers to obtain credit ratings,even if this is not made mandatory. This can ensuresufficient transparency of information, in a marketdominated by family offices and privately heldbusinesses that have no obligations to publish theirstatutory accounts.

Investor protection • Appropriate reforms to existing bankruptcy laws in

Dubai could be made to ensure adequate investorprotection. In addition, there is a compelling case for more emphasis to be placed on restructuringmechanisms to provide for the fair and efficient

reorganisation of potentially distressed issuers,allowing for the issuer to plan for restructuring andresolution in advance. As a result, investors would beable to rationally assess the risk of investing in bonds,and the likelihood of a resolution, whether in part orin full, in the event of default.

• Further, Dubai may improve the efficiency of settlingdisputes by aligning arbitration regulation tointernational standards.

Other financial regulations and Governmentinitiatives• Dubai markets may benefit from aligning agendas

and efforts of various national regulatory authorities,paving the way for a coherent plan to drivedevelopment of the bond market. The achievability of this will be predicated on having a specific panelcomprising of government officials, regulatoryauthorities (including central bank representatives) and industry experts, addressing the variouschallenges and impediments to the development of a bond market, aligning respective priorities and agendas to achieve a harmonised plan.

• Dubai may also consider providing further protectionagainst lower-rated corporate issues to promote theseproducts in the debt market, orchestrated by settingup specialised third-party guarantee institutions thatrender such services.

• The introduction of a state pension schemes for boththe private and public sector could support anincrease in the establishment of pension funds.Pension funds could subsequently act as a vehicle fordeepening the debt market, as they are key investorsin debt products.

Develop the Islamic debt marketDeveloping further the Islamic debt market could play a considerable role in attracting further investment andestablishing Dubai as the leading global Islamic financialcentre. A number of policy recommendations have beenidentified to support this:

A well structured and bespoke regulatoryframework is recommended to promotemarket transparency and increaseinvestors’ confidence

Developing Dubai’s debt market to promote investment and growth | 21

Product innovation• New regulations and standards in respect of Sharia’a

compliant derivatives (such as currency and profit rateswaps) may be introduced in order to supportinvestors in hedging their positions. Such derivativescould ultimately be traded on NASDAQ Dubai and the DFM to ensure further transparency, but theintroduction of these instruments on the exchangeswould need to be timed appropriately to ensure thatthe market size and demand is adequate. In addition,the appropriate supporting infrastructure should bepresent to allow trading of such instruments.

• Introduction of a Sharia’a compliant repurchaseagreement, in line with NASDAQ Dubai’sannouncement, could support an active secondarymarket of Sukuk trading, which could also be adoptedby the DFM exchange in the future.

• Dubai could further develop the appropriateregulatory framework for green and sociallyresponsible investment Sukuk. Becoming the first city to issue a corporate green Sukuk may provideDubai with a distinct competitive advantage.

Infrastructure• Trading activity and liquidity levels on NASDAQ

Dubai’s Murabaha trading platform could beenhanced further through the introduction of aMurabaha index, or via publishing information onMurabaha trades in an attempt to provide marketparticipants with greater transparency. The existingMurabaha platform could be expanded to incorporateother Islamic products, such as Ijara.

• To boost liquidity, Dubai could continue the issuanceof Government Sukuk at various maturities and on a more frequent basis, as well as encourage stateowned and other corporations to issue Sukuk locallyrather than abroad.

• Implementation of the underlying platform to enableprimary sales of Sukuk to retail investors, in line withNASDAQ Dubai's announcement, with a similarplatform potentially to be implemented in the DFM in the future, could be considered.

Regulatory framework• Further developing the dispute resolution regulatory

framework for Islamic transactions, could supportmarket growth and further improve Dubai’s position in becoming the leading Islamic financial hub. DFSA’sarbitration knowledge and practices could potentiallybe utilised to support the drafting of such regulation.

• Collaboration with other leading Islamic hubs, such as Kuala Lumpur, London and GCC hubs could aid the standardisation of practices and further supportforeign investment. In addition, continued motivationby the Dubai authorities to support local entities toissue Sukuk in Dubai, rather than abroad, couldfurther support market liquidity.

• The establishment of a central supervisory Sharia’aboard to oversee and ensure transactions andproducts conform to Islamic standards, could reduce future disputes and increase transactions.

• Dubai may potentially implement a similar frameworkto Kuala Lumpur, to allow for Sharia’a Scholars thathold executive management positions to advise onlyone institution at any given time in a particular marketsegment, to avoid any potential conflicts of interest.

• NASDAQ Dubai may design and implement aframework to target retail investors, in line with recent announcements, allowing for access to primarySukuk issues and secondary online trading to increaseliquidity. A similar framework with appropriatechanges could potentially be adopted by the DFM.

Further developing Dubai’s Islamic debtmarket could play a considerable role inattracting investment and establishingDubai as the leading global Islamicfinancial centre

22 | Developing Dubai’s debt market to promote investment and growth

Rationale for having a local debt market

A vast body of economic literature supports the premisethat to sustain long-term economic growth, it isimperative to have a sound and well-functioningfinancial system. Such a system can yield several benefitsto the economy as it helps mobilise savings to moreproductive sectors, improves resource allocation,facilitates diversification and promotes bettermechanisms of risk sharing. It can also promote financialstability as deep and liquid financial systems with diverseinstruments, backed by a strong regulatory framework,can provide buffers against shocks emanating fromvolatile markets.

The UAE has come a long way with the development of its financial system by the establishment of severaldomestic and foreign banks* and by the establishmentof its two stock exchanges in Abu Dhabi and Dubai, inaddition to the offshore financial center DIFC. The UAE

also continues to improve and modernise its set of rulesand regulations in the banking sector with the aim ofachieving a resilient financial system that continues tofoster economic development.

Nevertheless, a high-level benchmarking analysiscomparing the financial development of the UAE to that of other regional and international financial hubsindicates a number of development areas that the UAEcan address, in order to cope with the growth of otherpeer financial centres. A detailed assessment of theUAE’s financial sector is presented in the “financialsector assessment and overview of the debt market”section of this report.

One potential area of development that has beendiscussed extensively after the Asian crisis of the latenineties and was reinvigorated after the 2008 globalfinancial crisis, especially in the context of emergingmarkets, is the development of local debt markets.Specifically, the development of a deep local debtmarket can help achieve the following objectives: • Provide tools for the Government to finance large

fiscal deficits without having to resort to borrowingfrom domestic banks or tapping into foreign sourcesof capital which might expose the country toexchange rate risk or risks of “sudden stops” in capital inflows;

• Facilitate the sterilisation of large capital inflows, and improve the implementation of the country’smonetary policies;

• Provide an alternative to bank lending and offeringrelatively cheaper financing to large reputable firms.This can have a direct implication on lending to smalland medium-sized enterprises as more bank resources

Whilst the UAE has come a long waywith the development of its financialsystem, a number of additionaldevelopment areas that can beaddressed in order to cope with thegrowth of other peer financial centers

*According to the most recent statistics of the central bank of UAE, 51 local and

foreign banks with 1,184 branches are currently operating in the UAE.

Developing Dubai’s debt market to promote investment and growth | 23

can be utilised for other loan recipients other thanGovernment related entities and large firms;

• Promote market discipline and transparency throughimproving the quality and disclosure of information;and

• Enhance financial stability by having a more diversefinancial system compromised of capital marketsalongside banks. This system can better absorb shockscreated by banking crises by providing a substitute tobank finance.

In the context of Dubai and the UAE at large, the casefor a local debt market is strong due to a number offactors. These include:• The robust fundamentals and economic growth of the

UAE are increasing demand from internationalinvestors for high-quality papers issued by theGovernment and large corporates;

• The continued investment in infrastructure and otherdevelopmental projects increases the need for newsources of funding with long-term maturities. This canbe partially addressed through the issuance of long-term debt instruments;

• The development of the local debt market will helpdiversify the existing funding of GREs and largecorporates in the UAE, which are currently heavilydependent on bank financing. This in turn can reducethe systemic risk within the economy and providebanks with further flexibility in terms of complyingwith central bank regulations that limit the exposureof banks to no more than 100% of their capital base;

• A local debt market will help mitigate exchange raterisks by providing alternative sources of multi-currencyfinancing without having to resort to foreign sourcesof capital. It can also reduce the risk of “sudden stops”or reversals in international capital flows; and

• The latest efforts directed towards turning Dubai intoa global capital of an Islamic economy will createmore demand from investors for high quality papers,which can be partially met by issuing local currencySukuk.

• Moreover, the divergent business cycles of theeconomies of the UAE and the US, to which the UAEDirham is being pegged, could render the UAEmonetary policy more complicated in certain times.For example, the recent hike of the US interest ratewhich was followed instantaneously by a similar rise inthe UAE policy rate might have come in a time whenthe UAE economy is in need for a further expansionaryrather than a contractionary monetary policy to helpboost market liquidity which was markedly affected bythe falling oil prices since mid-2014. Hence, thedevelopment of a deep and liquid local debt marketcan help support market liquidity in the UAE despitethe diverging business cycles of the two economies,and in fact, it can also provide an effective tool forenhancing the transmission mechanism of monetary policy.

In the context of Dubai and the UAE atlarge, the case for developing the localdebt market to promote investment andgrowth is strong

24 | Developing Dubai’s debt market to promote investment and growth

Financial sector assessment andoverview of the debt market

Overview of the financial development indexThe Financial Development (FD) index published byInternational Monetary Fund (IMF) was used in thisreport as an indicator to assess the development of the financial sector in the UAE compared to otherbenchmarks.

Based on the IMF’s FD index of 2013, the UAE appearsto be lagging behind international financial centres, suchas Malaysia, UK, Singapore, USA, and Hong Kong but iswell positioned compared to some of the other regionalfinancial centres, such as Bahrain.

The ranking of the regional financial centres on thesame index has remarkably improved compared to theUAE over the recent years. This highlights the need tocope with the growth of these financial centres byfurther developing the UAE’s financial sector and localdebt market.

The decomposition of the FD index into its sub-components of the Financial Institutions (FI) andFinancial Market (FM) indices provides further insightsinto these numbers. For instance, the UAE ranks aheadof Saudi Arabia on the FI index but lags behind the restof the countries on the same measure. On the otherhand, the UAE ranks ahead of Bahrain but on par withQatar on the FM index. However, the substantial gapbetween the UAE and Saudi Arabia, as well as betweenthe UAE and the other global financial centers, suggeststhat further scope for improvement exists for the UAE.

FM FI

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

HKG USA SGP UK MYS KSA BHR UAE

Score

FD

QAT

Source: The Financial Development Index published by the International Monetary Fund, 2015

The financial development indicators in the UAE and selective regional and global economies in 2013

The UAE appears to be lagging behindinternational financial centres, but is wellpositioned compared to some of theother regional financial centres, such as Bahrain

Developing Dubai’s debt market to promote investment and growth | 25

The new Financial Development (FD) index of the IMFThe IMF’s new FD index provides a broader measure of the state of financial development in each of the 176 countries included in the sample covering theperiod 1980-2013. The index provides a far morecomprehensive measure of financial developmentincluding but not limited to; the percentage ofpopulation with bank accounts or private sector creditas a percentage of GDP. The index offers a compositescore capturing both financial institutions (FI), such asbanks, insurance companies, mutual funds and pensionfunds, and financial markets (FM), including stock andbond markets.

Moreover, the new FD index covers:• Depth - size and liquidity of markets; • Access - ability of individuals to access financial

services; and • Efficiency - ability of institutions to provide financial

services at low cost and with sustainable revenues and level of activities in capital markets.

In light of this, the IMF’s FD index offers the bestapproximate for the status of financial development,which allows for the benchmarking of the UAE’sfinancial development in comparison to other peerregional and international hubs.

The chart below shows the decomposition of the FDindex into its two main sub-components, FI and FMindices, constructed using weighted averages of keyindicators of depth, access and efficiency within eachindex.

The IMF’s Financial Development Index

FinancialDevelopment

Index (FDI)

FinancialMarkets

(FM)

FinancialInstitutions

(FI)

Efficiency(FIE)

Efficiency(FIE)

Depth(FID)

Access(FIA)

Depth(FMD)

Access(FMA)

Source: “Rethinking Financial Deepening: Stability and Growth in Emerging Markets,”IMF Staff Discussion Note, May 2015.

The UAE’s financial sector assessmentwas based on the IMF’s financialdevelopment index. This takes intoaccount the depth, access, and efficiencyof both financial institutions and financialmarkets development.

26 | Developing Dubai’s debt market to promote investment and growth

The Evolution of the Financial Development indices The UAE has maintained a stable pace in developing itsfinancial sector throughout the eighties and nineties.However, the development of the financial markets inthe UAE started to pick up in the late nineties, largelydriven by the rise of oil prices and global reforms thatfollowed the Asian crisis of the late nineties.

The development of financial markets in the UAEappears to have a strong correlation with the oil cycle asdepicted in the graph below. This is evident through theperiod from 2004 onwards, which witnessed a series ofboom and bust in oil prices. In parallel with rising oilprices, the Government followed an expansionary fiscalpolicy that helped in boosting economic activity andpumping more liquidity into the market.

Aided by an environment of low interest rates and withthe inauguration of the DIFC as the first offshorefinancial center in the region, the FD Index (and morespecifically the FM index) increased substantially throughthe second half of the 2000s. However, the globalfinancial crisis of 2008 and the subsequent drop in oilprices led to a sharp decrease in the FD and the FMindices before these two indices stabilised at an averagescore of 0.4 between 2011 and 2013.

Source: The Financial Development Index published by the International Monetary Fund, 2015

FM FI

0

20

40

60

80

100

120

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Score

USD

FD

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

S

WTI Spot oil prices

The evolution of the financial development in the UAE and global oil prices over the period 1988-2013

The development of financial markets in the UAE appears to have a strongcorrelation with changes in oil prices

Developing Dubai’s debt market to promote investment and growth | 27

Financial Market index in the UAEThe above graph shows a breakdown of the UAE’s FM index based on depth (FMD), access (FMA) andefficiency (FME). In addition, it shows the evolution of each index component over the period from 1980 to 2013.

The UAE’s FM depth and efficiency indices have beenmoving very closely with the oil cycle.1 In particular, thesignificant improvement in FM efficiency through theperiod from 2004 to 2008 provided a remarkable boostto the UAE’s financial markets, as evidenced by theimproving, albeit swinging, FM depth index during thesame period.

However, the two sub-indices have plummeted in therecent years in the aftermath of the global financialcrisis, tightening liquidity, rising credit spreads andfalling oil prices. On the other hand, the FM accessindex has been historically very low till 2010 when the

number of debt issuers increased substantially pushingthe FM access index to a high level of 0.5 on a zero toone scaled index. Despite this remarkable improvement,accessing UAE’s FM remained stagnant throughout thefollowing years.

Source: The Financial Development Index published by the International Monetary Fund, 2015

The UAE’s FM index components

1980

2005

2006

2007

2008

2009

2010

2011

2012

2013

1999

2000

2001

2002

2003

2004

1993

1994

1995

1996

1997

1998

1987

1988

1989

1990

1991

1992

1981

1982

1983

1984

1985

1986

FMA FMD

0.00.1

0.20.3

0.5

0.6

0.4

0.70.8

0.9

1.0

Score

FM

FME

1 FM depth index is constructed using measures such as: stock market

capitalization to GDP; stock traded to GDP; international debt securities

Government (% of GDP); total debt securities of nonfinancial corporations

(% of GDP); and total debt securities of financial corporations (% of GDP).

FM efficiency is a proxy by the stock market turnover ratio (stocks

traded/capitalization). FM access is measured by the percent of market

capitalization outside of the top 10 largest companies and the total number

of issuers of debt (domestic and external, non-financial corporations and

financial corporations).

The financial market development in theUAE has slowed down in the aftermathof the global financial crisis. This was the result of tightening liquidity, risingcredit spreads and a significant decreasein oil prices.

28 | Developing Dubai’s debt market to promote investment and growth

Financial Institutions index in the UAEThe below graph presents a breakdown of the FI indexbased on the depth (FMD), access (FMA) and efficiency(FME) and shows the evolution of each component overthe period from 1980 to 2013 in the UAE.

There appears to be a slight progress in thedevelopment of the UAE’s financial institutions as the FI index increased slightly from an average score of 0.35in the period from 1980 to 2003 to an average score ofjust over 0.4 registered in 2013. However, a stabledecrease in the FI efficiency index from 1981 to 2013highlights the need to carefully consider and addressthis issue.

On the other hand, despite the improving depth andaccess measures of the UAE’s financial institutionsthroughout the latest decade, they remain far below theefficiency levels achieved by these institutions. In orderfor these indicators to improve, additional efforts shouldbe made to increase the share of non-bank financialinstitutions’ assets in the financial sector, and improvethe access to these institutions through theestablishment of more branches.

Source: The Financial Development Index published by the International Monetary Fund, 2015

The UAE’s FI index components

1980

2005

2006

2007

2008

2009

2010

2011

2012

2013

1999

2000

2001

2002

2003

2004

1993

1994

1995

1996

1997

1998

1987

1988

1989

1990

1991

1992

1981

1982

1983

1984

1985

1986

FIA FID

0.00.1

0.20.3

0.5

0.6

0.4

0.70.8

0.9

1.0

Score

FI

FIE

0.0

Despite the improving depth and access measures of the UAE’s financialinstitutions throughout the latest decade,they remain far below the efficiencylevels achieved by these institutions

Developing Dubai’s debt market to promote investment and growth | 29

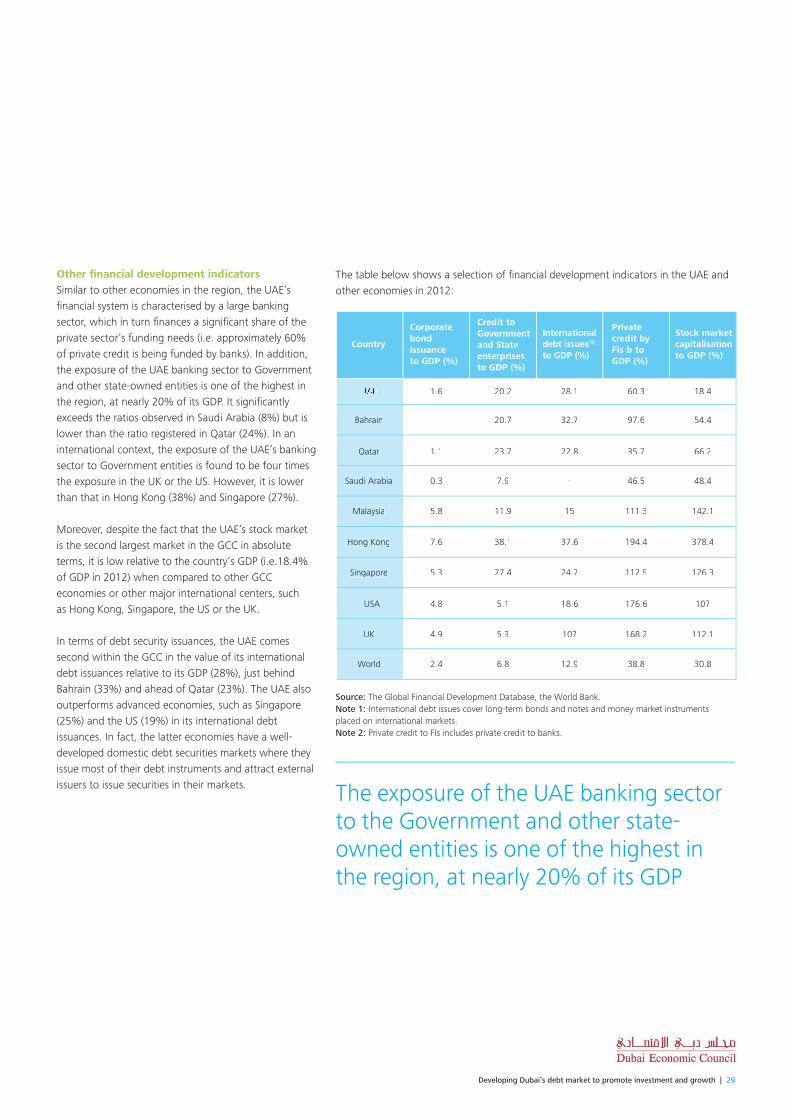

The table below shows a selection of financial development indicators in the UAE andother economies in 2012:

Source: The Global Financial Development Database, the World Bank. Note 1: International debt issues cover long-term bonds and notes and money market instrumentsplaced on international markets. Note 2: Private credit to FIs includes private credit to banks.

Corporatebondissuanceto GDP (%)

Country

UAE

Bahrain

Qatar

Saudi Arabia

Malaysia

Hong Kong

Singapore

USA

UK

World

1.6

-

1.1

0.3

5.8

7.6

5.3

4.8

4.9

2.4

20.2

20.7

23.7

7.9

11.9

38.1

27.4

5.1

5.3

6.8

28.1

32.7

22.8

-

15

37.6

24.7

18.6

107

12.9

60.3

97.6

35.7

46.5

111.3

194.4

112.5

176.6

168.2

38.8

18.4

54.4

66.2

48.4

142.1

378.4

126.3

107

112.1

30.8

Credit toGovernmentand Stateenterprises to GDP (%)

Internationaldebt issues(1)

to GDP (%)

Privatecredit byFIs b toGDP (%)

Stock marketcapitalisationto GDP (%)

Other financial development indicatorsSimilar to other economies in the region, the UAE’sfinancial system is characterised by a large bankingsector, which in turn finances a significant share of theprivate sector’s funding needs (i.e. approximately 60%of private credit is being funded by banks). In addition,the exposure of the UAE banking sector to Governmentand other state-owned entities is one of the highest inthe region, at nearly 20% of its GDP. It significantlyexceeds the ratios observed in Saudi Arabia (8%) but islower than the ratio registered in Qatar (24%). In aninternational context, the exposure of the UAE’s bankingsector to Government entities is found to be four timesthe exposure in the UK or the US. However, it is lowerthan that in Hong Kong (38%) and Singapore (27%).

Moreover, despite the fact that the UAE’s stock marketis the second largest market in the GCC in absoluteterms, it is low relative to the country’s GDP (i.e.18.4%of GDP in 2012) when compared to other GCCeconomies or other major international centers, such as Hong Kong, Singapore, the US or the UK.

In terms of debt security issuances, the UAE comessecond within the GCC in the value of its internationaldebt issuances relative to its GDP (28%), just behindBahrain (33%) and ahead of Qatar (23%). The UAE alsooutperforms advanced economies, such as Singapore(25%) and the US (19%) in its international debtissuances. In fact, the latter economies have a well-developed domestic debt securities markets where theyissue most of their debt instruments and attract externalissuers to issue securities in their markets. The exposure of the UAE banking sector

to the Government and other state-owned entities is one of the highest inthe region, at nearly 20% of its GDP

30 | Developing Dubai’s debt market to promote investment and growth

Private external financingThe structure of private external financing (as illustratedin the chart) suggests that the private sector in the UAEis still heavily reliant on bank loans to finance theircapital structure, especially when compared to othereconomies within the region and across the globe.

However, there was a temporary exception to this trendin 2011 and 2012 due to a surge in bond issuances byseveral corporates, driven by the tightening of banklending in the domestic market, and by investors aimingto benefit from a globally low interest rate environment. As banks resumed lending in 2013, encouraged by afavorable economic setting, private firms increased theirborrowing from banks, which increased to 65% of theirtotal external financing.

Source: Global Financial Stability Report, IMF, Statisticalappendix, 2014

*UAE used, as rating for Dubai is not available

Structure of Private External Financing in selectiveeconomies in 2013

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

USUKQATKSAUAE* OMA

Equity Loans Bonds

65% 62%

10% 4%

20%30%

21%

49%

51%

29%

44%

15%

82%

32% 36%

46%

Source: Global Financial Stability Report, IMF, Statisticalappendix, 2014

Structure of Private External Financing in the UAE during2010 - 2013

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

201320112010 2012

Equity Loans Bonds

29%

61% 58%

32%

65%

40%38%

71%

1%

1%2%

3%

The private sector in the UAE is heavilyreliant on bank financing

Developing Dubai’s debt market to promote investment and growth | 31

Source: Bloomberg and Kuwait Financial Center “Markaz”

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

UAE Other GCC

58%

42%

33%

67%

68%

32%

40%

60% 59%

41%

2012 201320102009 2011

Overview of recent developments in the debtmarketIssuance of conventional bonds and Islamic Sukuk inthe GCCThe UAE has been the first issuer of conventional bondsand Sukuk in the GCC for many years. In 2013, newissuances made by the UAE accounted for nearly 41% oftotal new issuances in the GCC with nearly USD 19billion of bond and Sukuk issuances. However, whenaccounting for issuances of treasury bills, notes, bondsand Sukuk denominated in local currencies and issuedby GCC central banks, the share of UAE in the total debtissuances of GCC countries drops significantly as thecentral bank of UAE does not issue these types ofpapers.

Bond issuances in the UAE Bond issuances by corporates, including sovereignbonds, banks and other financial corporations, accountfor the majority of debt issuances in the UAE, withnearly 96% of total issuances made by banks, financialand non-financial corporations.

Source: Bank of International Settlements

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1 2015Q4 2014 Q2 2015

Sovereign bondsBanksOther financial corporationsNon-financial corporations

4%

32%

37%

27%

4%

35%

35%

5%

36%

33%

26% 26%

The UAE has been the first and largestissuer of conventional bonds and Sukukin the GCC for many years

Issuance of conventional bonds and Islamic Sukuk, 2013 Bond issuance by entity type in the UAE

32 | Developing Dubai’s debt market to promote investment and growth

On the other hand, issuances in Dubai representedabout 72% of total bond issuances in the UAE in 2014,of which issuances by banks and DIFC corporatescomprised approximately 74% as opposed to 26%issuances by the Government and GREs.

Moreover, approximately 58% of these new issuanceswere denominated in USD followed by CHF (22%) andEUR (17%), while the issuances in AED represented just0.2% of the total debt issuances.

Sukuk issuances On the Sukuk issuances, recent statistics suggests thatDubai has become the world leader in the Islamic bondindustry overcoming all its rivals with a USD 36.7bnnominal value of listed Sukuk in 2014. NASDAQ Dubaiaccounts for most of the Sukuk listings (93%), with avery small percentage listed on DFM. The UAEGovernment or related entities were involved in 56% oftotal Sukuk listings in Dubai, while Saudi Arabian issuersaccounted for 22% and Indonesian issuers 16%.1

Bond issuances in Dubai by sector in 2013

26%

74%

Banks and DIFC corporates

Government and GREs

Source: Bloomberg

Issuances in Dubai by currency

2.1%

21.9%

17.0%

58.8%0.2%

AED

CHF EUR Other USD

UK and Ireland

USD 25bn eachDubai

USD 36.7bnMalaysia

USD 26.6bn

Dubai has become the world leader in the Islamic bond market with USD 36.7bn nominal value of listedSukuk in 2014

Source: Bloomberg

Sukuk issuance levels in 2014

Developing Dubai’s debt market to promote investment and growth | 33

OverviewThe benchmarking analysis performed compared Dubaiagainst global financial hubs in order to identify gapsand improvement opportunities in conventional andIslamic debt markets. The key benchmarks selected forthe conventional debt market include global financialhubs that share similar characteristics with Dubai, butare perceived as more established. The benchmarksselected for the Islamic debt market are those that havebeen developing an Islamic finance capability over thelast few years and are in direct competition with Dubai.The benchmarks selected include:• Conventional debt markets: New York, London,

Singapore, Hong Kong, Riyadh and Manama; and• Islamic debt markets: Kuala Lumpur, London, Riyadh,

Doha and Manama.

The adjacent diagram summarises the key factors andareas that were considered in the analysis performed.

Support product innovation to increase marketliquidityThe development of new debt products enables thedebt market to function efficiently by providing issuerswith a range of alternative instruments to raise capitaland offer investors the option to manage theirinvestment portfolios more effectively. In addition, newinnovative and diversified products, such as hedginginstruments could support both investors and issuers inmanaging risk more effectively and thus further supportmarket liquidity.

Benchmarking analysis

Government initiativesand guarantees

Credit rating

Investor protection

Securitisation

Derivatives

Green bonds

Trading platforms

Clearing and settlement

Investor base

Benchmark yield curve

Information disclosure database

Registration and approval process

Maker incentives

Infrastructure

Regulatoryframework

Productinnovation

DevelopingDubai's debt

market

Productinnovation

Infrastructure

Regulatoryframework

Islamic debtmarket

A four pillar framework analysis wasfollowed to benchmark the developmentof Dubai’s conventional and Islamic debtmarkets against peer global and regionalfinancial hubs

34 | Developing Dubai’s debt market to promote investment and growth

This section provides an overview of the differentproducts in the conventional debt market within Dubaiand the benchmarked jurisdictions.

Based on current levels of development, the Dubai debtmarket appears to have adequate debt instruments inplace considering the current state and size of themarket, with the potential of including derivativeproducts on its exchanges. Dubai compares relativelywell compared to other cities in the region with regardsto the variety of products available. Singapore, HongKong, London and New York offer a wider variety ofproducts with some derivatives traded on theirexchanges, however, debt market size is higher withgreater investor demand.

The table below summarises the debt products on offerin benchmark markets.

Product innovation benchmarking

Dubai is well positioned compared toother cities in the region with regards tothe variety of debt products available inthe market

Products Dubai New York London Singapore Hong Kong Riyadh Manama

Covered bonds Welldeveloped

Under-developed

Welldeveloped

Under-developed Not available* Not available* Not available*

Derivatives

Interest rate swapAvailable but

not onexchange

Available onexchange

Available onexchange

Available butnot on

exchange

Available onexchange

Available butnot on

exchange

Available butnot on

exchange

Interest rate futures contractAvailable but

not onexchange

Available onNYSE

Euronext

Available onexchange

Available onexchange

Available onexchange

(OTC clear)

Available butnot on

exchange

Available butnot on

exchange

Currency swapAvailable but

not onexchange

Available onexchange

Available onexchange

Available butnot on

exchange

Underdevelopment-

Centralclearing by the

OTC Clearexchange

Available butnot on

exchange

Available butnot on

exchange

Currency future/forwardAvailable but

not onexchange

Available onexchange

Available onexchange

Forwardavailable onexchange

Underdevelopment-

Centralclearing by the

OTC Clearexchange

Available butnot on

exchange

Available butnot on

exchange

Government derivatives

Government bond futures contract Notavailable

Available onNYSE

Euronext

Availableon ICE

exchange

Available on exchange

Available on exchange

Notavailable

Notavailable

Green bonds

Green bonds Notavailable

Available onexchange but

furtherdevelopmentof regulation

required

Available onexchange but

furtherdevelopmentof regulation

required

Available onexchange but

furtherdevelopmentof regulation

required

Available onexchange but

furtherdevelopmentof regulation

required

Not available

Notavailable

*product not used

Developing Dubai’s debt market to promote investment and growth | 35

Covered bondsFollowing the global financial crisis in 2007, demand forcovered bonds was higher than Asset Backed Securities(ABS) and commercial and residential mortgagesecurities due to the perceived lower risk.

Covered bonds - similar to ABS - use a pool of assets as collateral, however in addition to the claim overcollaterised assets, the investor has a claim over otherassets held by the issuing entity. Nevertheless, theliability of covered bonds remains on the issuer’s balancesheet even if the assets covering the bond aretransferred to another entity. Covered bond holdershave priority over assets in the event of an issuerdefault.

The UK covered bond market was established in 2003with the issuance of a relevant regulatory framework. Inthe US, regulation for covered bonds was introduced in2008, however market activity gained momentum in2010. Regulation in the US does not currently permit USentities to issue covered bonds to US investors, withonly foreign entities permitted to target US investors.

In January 2014, the UAE financial market regulatorSCA, issued new regulations on the issuance, listing andtrading of covered bonds, to support the developmentof the local debt market. The new regulations define therequirements to obtain a license to issue covered bonds,and prescribe disclosure requirements for issuers.Singapore set up a regulatory framework for coveredbonds in 2014, however some market participants notea lack of detail in the framework.2

Riyadh announced in 2015 that it was planning todevelop a securitisation platform to increase alternativesfor issuers with lower credit ratings, whilst Hong Konghas not yet introduced regulation for covered bonds.

DerivativesTraditionally, derivatives in the American and Europeanmarkets have been traded over the counter butfollowing the global financial crisis, the majority ofmarkets agreed on improved regulation to monitor thissegment, shifting towards electronic trading platforms(primarily for standardised derivatives) in order toincrease transparency.

However, given the costs involved in shifting to anelectronic platform, less developed markets have yet to adapt such a platform.

A number of derivative products, such as interest rateswaps, currency swaps and interest rate future contractsare offered by banks in the GCC, however, theseinstruments are not traded on their respectiveexchanges, unlike more developed markets such as New York and London, whilst Singapore only hasinterest rate and currency futures on its exchange.

Hong Kong is currently developing a platform to enabletrading and clearing of currency swaps and futures onthe “OTC clear” exchange.

Government bonds future contractsDerivatives, such as interest rate futures andGovernment bond futures are used by a number ofcountries to support investors in hedging their positionsand ultimately, attracting further investment andcreating liquidity.

Derivatives such as interest rates,currency swap and future contracts areoffered by banks in the GCC but nottraded on the exchange due to lack ofdemand

36 | Developing Dubai’s debt market to promote investment and growth

Unlike more developed conventional debt markets,Government bond futures have not been issued bydeveloping markets, such as Dubai, Riyadh and Manamaprimarily due to the lack of demand.

Singapore offers Government bond futures (5-year USD100,000 face value at 3% coupon rate) which aretraded on Singapore’s exchange. Similarly, Hong KongGovernment futures are available on the Hong KongFutures Exchange.

Green bondsCorporate green bonds recorded growth in 2013,primarily in the European and the American market.Total green bonds global issuance during 2014amounted to USD 36.6 billion and may potentially reachUSD 50 billion in 2015.1

In 2015, the London Stock Exchange (LSE) launched aplatform and framework for the issuance and trading ofgreen bonds, whereby the issuer is required to receivethird party clearance with a specific qualification toverify the nature of the bonds. The first Indian Greenbond was listed on the LSE one month after the bourseannounced the opening of the platform.

Hong Kong’s first green bond (USD 300m) was issued inJuly 2015 on the Hong Kong exchange, whilst the firstAsian Pacific green bond was listed on the Singaporeexchange in 2014, potentially signaling the emergenceof the green bond market in Asia.

The key area of focus in the development of the Greenbond market would be to standardise what constitutesa Green bond issue and transparency on how proceedsare used. For example, leading regulators mayencourage the assurance of a green bond issue byexternal third party certifiers and develop an effectiveregulatory framework with regards to monitoring andreporting on where the proceeds are deployed.

In the GCC demand for green bonds has yet to reachsubstantial levels so as to justify the introduction of suchinstruments and regulations.

Improving the underlying infrastructure tosupport issuance and tradingAn efficient market infrastructure can be assessedthrough the following main pillars:• Trading platforms: The availability of efficient trading

platforms lowers trading costs and price volatility,reduces market fragmentation, facilitates order flow,improves price discovery and ensures widedissemination of information.

• Clearing and settlement: Reliable clearing andsettlement systems allow for cost and time efficientexecution of transactions.

• Investor base: A wide and diverse investor base leadsto increased liquidity and inspires confidence, allowingfor a broader range of products to cater for investorrequirements.

• Benchmark yield curve: The ability to develop abenchmark yield curve from Government bondissuances can facilitate the efficient pricing of creditrisk for investors and corporates.

Development of the global Green bondmarket would require standardisation of what constitutes a Green bond andmarket transparency on how proceedsare used

Developing Dubai’s debt market to promote investment and growth | 37

• Information disclosure database: An efficientplatform and database for information disclosure ofissuers and trades can enhance transparency in themarket, and in turn, encourage both local and foreigninvestor participation.

• Registration and approval process: A time efficientregistration and approval process supported by aneffective regulatory environment could furtherpromote fast and efficient bond issuance levels.

Trading platforms ETM, OTC and ETP platforms Different trading platforms facilitate the issuance ofboth public and private placements of trades. The mostcommonly used platforms include the Exchange TradedMarkets (ETM), Over the Counter (OTC) and ElectronicTrading Platforms (ETP).

Whilst ETMs are commonly used in developed markets,emerging markets primarily use OTC platforms given thedynamics of the transactions and investors within themarket. Bond transactions in Dubai and Hong Kong arelargely executed through OTC platforms as they aretypically large and tend to be traded by institutionalinvestors who prefer to negotiate directly with thecounterparties.

ETPs are becoming increasingly popular for transactionsinvolving more standardised and low risk corporatebonds, such as investment grade bonds. Developedmarkets, such as New York and London have a fullyautomated electronic trading platform that allows bondtrading for institutional and retail investors whileoffering trading platforms for non-conventionalproducts, such as derivatives. Manama, Dubai andRiyadh have taken steps towards the implementation ofETPs in their respective bond markets. The Bahrainbourse recently implemented the Automated TradingSystem (“ATS”) platform that allows electronic execution

of transactions. Riyadh is in the process of implementingthe X-stream INET Trading platform by NASDAQ to allowelectronic trading of Sukuk and conventional bonds,whilst NASDAQ Dubai has implemented the sametechnology.

The ETP, with its combination of electronic trading andcentralised price dissemination, can provide bonddealers with a more complete and efficient platform forcost competitive trade execution. It can also lead tomore effective price discovery and greater access by awider range of investors.

The introduction of an ETP will need to be in parallelwith enhanced market liquidity, as such platforms haverelatively high implementation and maintenance relatedcosts, and as such, economies of scale through largetransaction volumes will need to be achieved in order tojustify such costs.

Other steps towards developing the marketinfrastructure and increasing market liquidity mightinclude the introduction of new platforms or expandingthe current platforms to allow:• Connectivity with other regional and international

markets and brokers’ systems;• Introduction of derivative products; • Access to retail investors; and• Efficient trading hours.

The availability and efficiency ofelectronic trading platforms can supportincreased market liquidity

38 | Developing Dubai’s debt market to promote investment and growth

ConnectivityConnectivity between domestic, regional andinternational platforms could offer easier andautomated access to various stakeholders includingbrokers, dealers, issuers, and local and foreign investorsas witnessed in the developed market. These marketshave expanded their infrastructure to accommodateconnecting systems with other exchanges andplatforms. For example, the New York Stock Exchange(NYSE) offers the option to connect directly through theFIX gateway to all NYSE Euronext markets (Amsterdam,Belfast, Brussels, Chicago, Lisbon, London, New York,Palo Alto, Paris and San Francisco). It also offersconnection to Bloomberg’s Trade Order ManagementSystem (TOMS) and InterDealer, which gives access tocross-asset trading platforms across the NYSE.

On the other hand the DFM operates an order-drivenautomated screen-based trading system where investorscan place their orders through DFM’s accreditedbrokers, who then place these orders on the exchange’ssystem. The system automatically matches buy and sellorders of a particular security based on price andquantity requirements similar to the trading systemimplemented in Riyadh where brokerage firms’ systemsare also connected directly with the exchange (Tadawul)system.

Platforms for derivative productsThe availability and ability of platforms to accommodateother non-conventional products, such as derivatives isalso key in driving market liquidity in order to meetinvestor demand. This is primarily witnessed in New York where the NYSE offers direct access to a wideinternational network of derivative exchanges andclearing houses through the Intercontinental Exchange(ICE).