developing process flows 18 july -2013

TRANSCRIPT

Developing Process Developing Process FlowsFlows-- MurabahaMurabahaFlowsFlows MurabahaMurabaha

Developing Process FlowsDeveloping Process Flows

Four Pre-Requisites

a) Strong Commitment towards Islamic Bankinga) Strong Commitment towards Islamic Banking

a) Full Product Knowledge

a) Market Knowledge

b) Customer’s Business Processes

Developing Process Flows

Strong Commitment Towards Islamic Banking:

Developing Process Flows

g g

• It is the most important factor behind developing Shariah Compliantprocess flowsprocess flows.

• A less competent but strongly committed personnel is likely to ensurestrong Shariah Compliancestrong Shariah Compliance.

• Less Committed person will take Shariah Compliance a formality andt ibilitnot a responsibility.

• RM/RO has additional responsibility of Shariah Compliance over andb hi l RM/ROabove his role as an RM/RO.

Developing Process Flows

Strong Commitment Towards Islamic Banking:

Developing Process Flows

g g

• RM/RO must understand that he is responsible for passing Halalincome to all the Deposit Holders of the Bankincome to all the Deposit Holders of the Bank.

• If someone is not convinced about the principles of Islamic Bankingthan he must leave the job as Strong commitment to the cause is thethan he must leave the job as Strong commitment to the cause is themost important pre-requisite for a front staff.

Product KnowledgeProduct Knowledge

Product Knowledge:

• Strong Command over the Product Manuals and policies.

• Sequential flow of Murabaha Events must be knownSequential flow of Murabaha Events must be known

Product Knowledge

Sequential Flow of Transaction Documents

Product Knowledge

q

Placement of Order Form:

• Before the dispatch of goods from supplier

• Before or at the time of placing Order with supplier

• Order Form represents a situation where customer wants to purchasesome assets and have not yet acquired possession of the asset.

• Misconception that Order Form is placed only when disbursement isp p yrequired by Customer.

Product Knowledge

Sequential Flow of Murabaha Events

Product Knowledge

q

Placement of Order Form:

Example:

Al-Noor Traders-Dealer of Pesticides

Date of Order Form: 20th January 2012Date of Dispatch note : 17th January 2012Date of Dispatch note : 17 January 2012Declaration date: 20th January 2012

Res lt The Order form as s bmitted after the reciept of goods bResult: The Order form was submitted after the reciept of goods bythe customer therefore the transaction is Invalid

Product KnowledgeSequential Flow of Murabaha Events

Timing of Disbursement

Product Knowledge

g

• Must be done at the time when payment is required by supplier.

• It is a misconception that disbursement must be done before thedispatch of goods but indeed disbursement may be done before orafter the dispatch of goods as per the transaction termsafter the dispatch of goods, as per the transaction terms.

• In reality the disbursement may be done before or after the dispatchof goods as per the transaction termsof goods, as per the transaction terms.

• Eg Some suppliers of Macter requires payment upfront whereas somerequire payment after the delivery of goods therefore in formal casesrequire payment after the delivery of goods therefore in formal casesdisbursement was made upfront whereas in later case thedisbursement was made after the receipt of goods.

Product Knowledge

Sequential Flow of Murabaha Events

Product Knowledge

q

Execution of Declaration and Murabaha Contract

• Must be executed at the time of reciept of goods and before theconsumption/sale of the goods.

• Purchase Evidences must be attached with the Declaration andMurabaha Contract

• If in case invoices are not available at the time of delivery than Goodsreceipt evidence along with the name of supplier and amount ofpurchase will be taken, however invoices/bills will be taken as soon asthey are received.

Product Knowledge

Sequential Flow of Murabaha Events

Product Knowledge

q

Execution of Declaration and Murabaha Contract

• In case of sugar cane declaration was used to be executed after 7 to 8d f i f L i l d hdays of reciept of sugar canes. Later on it was revealed that sugarcane is directly put into the crushing machine therefore all theprevious transactions were in valid.

• For future transactions MBL’s representative was placed at the factoryto ensure declaration and Murabaha Contract before putting sugarcanes into the crushing machine.

Market Knowledge

Market Knowledge:

Market Knowledge

Market Knowledge:

• Types of Suppliers- Organized or Un-organized e.g. Seeds, phuttill li d b i d f b kare usually supplied by unorganized farmers, brokers.

• What is meant by Cash in the market? In leather market usuallypayment is made after quality testing. This mode of payment is usuallyconsidered cash in the market but in actual it is a credit sale.

• General Delivery terms in the market e.g. Suppliers provide freedeliveries in case of large orders.,

• Point of risk transfer? Shell usually provides Patrol in its own carrierand assumes risk of oil till they are off-loaded.

Market Knowledge

Market Knowledge:

Market Knowledge

Market Knowledge:

• Type of documentation prevailing in the market e.g. In AgriI k Bill ll i b b ’Inputs market Bills are usually not given by growers but customer’sself made bill is usually signed by the growers.

• Mahmmod cotton ginners makes the bill when phutti is accepted at• Mahmmod cotton ginners makes the bill when phutti is accepted attheir godown and suppliers signature is taken over the bill. Thisprocess was incorporated in their Murabaha process flow.

• Government regulations regarding the market e.g. Sales Taxpolicies for a particular market.

• Any other Market specific practice e.g. Mudda in Phutti Market;sale based on Delivery Orders in yarn market

Issues in Murabaha

Customer Business Practices

Issues in Murabaha

Following information must be obtained about customer’s

business practicesbusiness practices.

• Payment Terms with the suppliersM d f P S li Di I di• Mode of Payment to Supplier: Direct or Indirect

• Delivery Terms• Goods Receipt Evidences

P h E id• Purchase Evidences• Goods Identification method• Customer’s relationship with Suppliers• Inventory Holding Period

Payment Terms with Supplier

Payment terms of customer with its major supplier must be understoodb f d fti th P Fl f th t

Payment Terms with Supplier

before drafting the Process Flow of the customer.

Payment to suppliers can be made in the following different methods:

Full Advance Payment: Payment is made to supplier before the dispatchof goods

Impact on Disbursement:Disbursement is made at the time of placement of Order to supplierand before the dispatch of goods.

Eg. Fertilizer Companies usually delivers fertilizers after 1 to 6 monthsof receiving advance payment.

Payment Terms with Supplier

Partial Advance Payment: Partial advance payment is made at the time of

Payment Terms with Supplier

y p yOrder while partial payment is made after delivery of goods.

Impact on Disbursement:

This implies that partial disbursement will be made before the dispatch ofgoods while partial disbursement will be made after the dispatch of goods.

Implication on Profit Calculation: If first disbursement (eg Rs 5 Million) ismade on 1st Jan and 2nd Disbursement (eg Rs 10 Million) is made on 15thJanuary and maturity date is 30th Jan than profit calculation will include profiton Rs 5 million for 15 days and profit on Rs 15 million for 15 days. Thisprofit amount will be agreed at the time of execution of Murabaha Contract.

Payment Terms with Supplier

Credit Payment: Payment: Credit Payment is made to suppliers after certainnumber of days from the receipt of goods

Payment Terms with Supplier

number of days from the receipt of goods.

Eg. Iqbal Rice Mills, a rice processing unit, makes payment to its supplier after3 4 days of reciept of goods3-4 days of reciept of goods.

Iqbal rice mill was guided to provide Order Form at the time of placing orderwith supplier while disbursement was made after 3 4 days of execution ofwith supplier while disbursement was made after 3-4 days of execution ofDeclaration and Murabaha Contract.

Impact on timing of Order form:p g

Order form must be provided at the time of placing order with supplier andbefore the dispatch of goods

Impact on disbursement:

Disbursement will be made after the execution of murabaha contract andupon expire of the credit period even by supplier.

Payment Terms with Supplier

Implication on profit calculation:

Payment Terms with Supplier

p p

Profit will be calculated for the period between the disbursement date andmaturity date but agreed at the time of execution of murabaha contract i.e.before disbursement

The profit will be the calculated on the basis of expected disbursement

date and maturitydate and maturity

Payment Terms with Supplier

Cash Payment: Payment terms of “Cash” usually imply a credit period of

Payment Terms with Supplier

Cash Payment: Payment terms of Cash usually imply a credit period of1-7 days in most industries/markets.

This should be clearly determined at the time of PF development

P d i h ill b i f diProcess and sequence in such case will be same as in case of credit payment.

Spot Payment: Payment is made at the time of receipt of goods.

Impact on disbursement:Disbursement can be made on the date of receipt or goods

Mode of Payment

Mode of payment

Mode of Payment

1. Pay Order/Cross cheque (a/c payee only) /Online transfer within

MBL

� Th l ifi d di d f hi h h� These are classified as direct modes of payment , which ensures that funds are directly paid to the supplier only.

� Ideally Direct Payment should be made to ensure proper utilization of f dfunds.

� Eg. Purchases from Public limited companies

/ /2. Open cheque/Self Cheque/Cash

� These are indirect modes of payment where additional checks are required to ensure proper utilization of funds.

� A cash receipt acknowledgement from the supplier must be obtained in these cases

� E.g Phutti, surgical instruments, steel sheet

Mode of Payment

M d f p nt

Mode of Payment

Mode of payment

3. Payment in other accounts

� As per the market norms many supplier do not want payment at their company accounts but demand payments on the personal accounts of director/ manager/ employee for the company.g p y p y

� This mode can be acceptable but certified copy of the list of suchindividuals must be obtained from the supplier and incorporated inpp pthe process flow.

� Al Haye Medicos purchases medicines from different suppliers whoy p ppdemand payment in the personal accounts of directors/proprietorstherefore same was incorporated in their process flows.

Issues Related to Payment to Suppliers

Late presentation of cheque by supplier:

y pp

p q y pp

• Some time agent delivers cheque to the supplier but supplier presentsthe cheque late to the bankthe cheque late to the bank.

• In this scenario order form will be accepted at the time of placingorder with the supplier but disbursement will be made on the dateorder with the supplier but disbursement will be made on the datewhen cheque will be presented for clearing.

• If goods are delivered before the presentation of cheque the• If goods are delivered before the presentation of cheque thedeclaration and murabaha contract must be executed before thedisbursement.

Issues Related to Payment to SuppliersPartial payment by customer:

• S m tim st m r m k s s m p m nt fr m is n s r s nd

y pp

• Some time customer makes some payment from is own sources andsome payment from the funds taken from the bank.

I hi b k d h ill h h hi f h• In this case bank and the customer will share the ownership of thegoods as per their proportionate share in the payment.

Thi hi i ill b fl d i h h d l f• This ownership ratio will be reflected in the schedule of assets.

• For e.g. if bank pays Rs 50. and customer pays Rs 50 to purchasewatch worth Rs 100, Than MBl’s ownership share in the watch will be50% while customers share will be 50%.

• Premier Agencies purchases medicines on daily basis. On anyparticular Order they usually involve their own funds and in case ofany shortfall funds from bank is also taken. The goods received areowned by both as per their proportion the payment.

Delivery Terms with SuppliersDelivery Terms with Suppliers

Delivery Terms

Delivery Terms help in determining the point where ownership transfersfrom supplier to client.

It must be understood at which point risk is transferred to the customer i.e.at which point customer bears the risk of loss / damage of the goods

Delivery Terms with Suppliers

Delivery Terms

Delivery Terms with Suppliers

Some of the common delivery terms are as follows.

Transit risk borne by supplier:

In this case ownership transfers to the customer after delivery of goods atcustomer premises. Therefore Declaration & the Murabaha Contract must bepexecuted after the delivery of the goods.

Transit risk borne by customer:y

In this case ownership of goods transfers to the customer immediately upondispatch from supplier premises.

Declaration and Murahabha contract can be executed while the goods are intransit.

Delivery Terms with SuppliersDelivery Terms with Suppliers

Example of Transit Risk borne by Customer:p y

For e.g. masood and company purchases diesel from caltex. Caltex deliversoil through its approved rented carriage whose rent is paid by masood andcompany.

It take 3 days for the diesel to be transported from Karachi to Faisalabad.M d d i d li i ti ti i di t lMasood and company receives delivery intimation, immediately upondispatch of goods from Karachi.

At that point Masood and Company declares the receipt of oil to the bankAt that point Masood and Company declares the receipt of oil to the bankand execute a Murabaha Contract by providing the detail of the dispatchedoil on its letter head accompanied by copy of delivery note if available.

Later on invoices are provided by the customer upon their receipt fromsupplier.

Delivery Terms with Suppliers

Place of Delivery

Delivery Terms with Suppliers

y

a) at customer godown.

b) some 3rd party processing unitb) some 3rd party processing unit

c) at the place of buyers of our customer

If goods are delivered at some 3rd party processing unit than it must beIf goods are delivered at some 3rd party processing unit than it must beincorporated in the process flow and the Declaration and MurabahaContract must be executed through physical inspection at the processingunit It must be ensured the Declaration and Murabaha Contract must beunit. It must be ensured the Declaration and Murabaha Contract must beexecuted before the stat of processing. Eg. Processing of yarn, Wet blueprocess of Hides, Cutting and molding of steel are usually outsources bym n mp ni smanu companies.

Delivery Terms with Suppliers

Place of Delivery

Delivery Terms with Suppliers

y

If goods are delivered directly to the buyer of our customer under theIf goods are delivered directly to the buyer of our customer, under therisk of the supplier, than murabaha cannot be offered as ownership wasnot transferred to the customer.

Eg. Central Trading, large sized trading unit based in Lahore, used todeliver the goods directly to their customers without taking the risk ofgoods Ignorance of this fact causes loss to the Bank in the form ofgoods. Ignorance of this fact causes loss to the Bank in the form ofCharity.

Delivery Terms with Suppliers

Timing of Delivery

Delivery Terms with Suppliers

Time taken by the supplier to deliver the goods after reciept ofOrder/Payment must be also be incorporated in the process flows to be ablet t Sh i h C lito ensure strong Shariah Compliance.

Some customers make full delivery of good in single while other delivers thed i l i l hgoods in multiple trenches

In cases where goods are delivered in multiple trenches MBL will not wait tillh l i f f ll d li f d b ill i l D l ithe completion of full delivery of goods but will execute partial Declaration

and Murabaha on the delivered lot immediately.

In cases of bulk supplies in multiples trenches a time interval may also bedefined for declaring the goods.

Goods Receipt Evidences

Goods Receipt Evidence

Goods Receipt Evidences

Timing of receipt of goods:Goods Receipt Evidence (G.R.E.) info V.s. Purchase Evidence (P.E.) info?p ( ) ( )

Misconception regarding invoice date and delivery date.

Some of the common good receipt Evidences are as follows.External goods receipt/ delivery evidences : Delivery notes /Delivery Challan /Builty/ Truck Receipty / y/ p

Internal goods receipt evidences: Computerized inventorymanagement system/ goods receiving notes/ manual good receivesmanagement system/ goods receiving notes/ manual good receivesregister

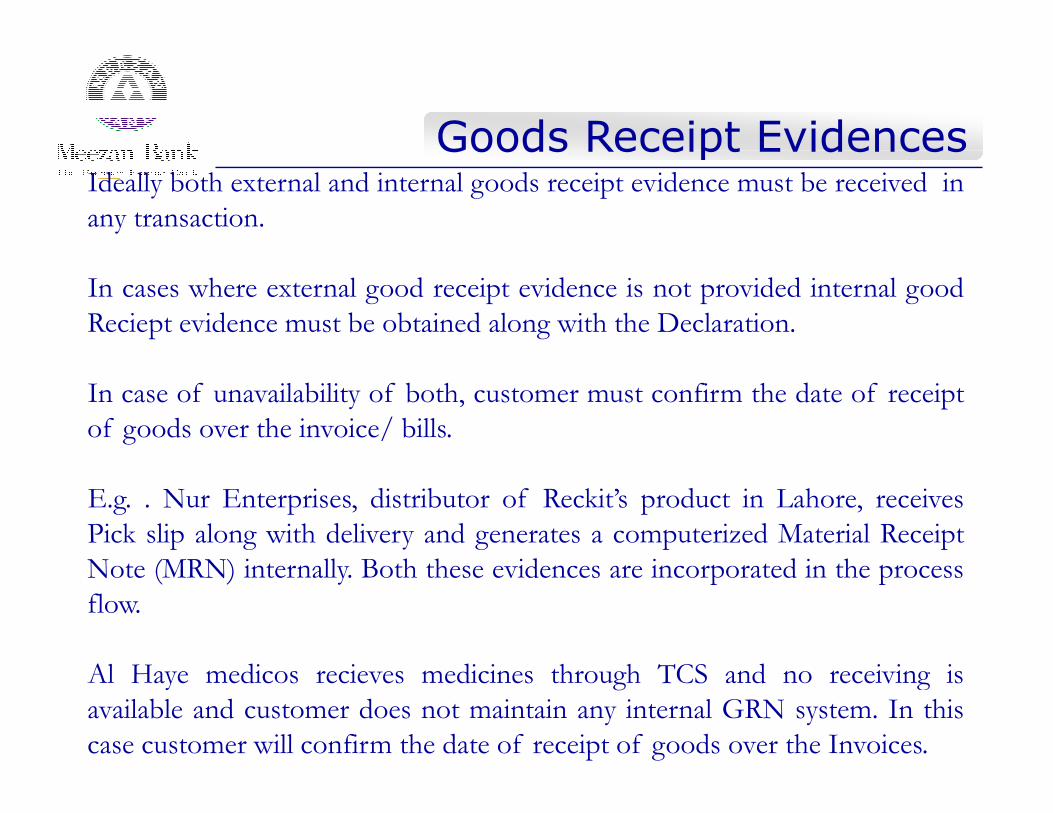

Goods Receipt EvidencesIdeally both external and internal goods receipt evidence must be received inany transaction.

Goods Receipt Evidences

In cases where external good receipt evidence is not provided internal goodReciept evidence must be obtained along with the Declaration.

In case of unavailability of both, customer must confirm the date of receiptof goods over the invoice/ bills.

E.g. . Nur Enterprises, distributor of Reckit’s product in Lahore, receivesPick slip along with delivery and generates a computerized Material ReceiptN (MRN) i ll B h h id i d i hNote (MRN) internally. Both these evidences are incorporated in the processflow.

Al Haye medicos recieves medicines through TCS and no receiving isavailable and customer does not maintain any internal GRN system. In thiscase customer will confirm the date of receipt of goods over the Invoices.

Purchase Evidences

Purchase Evidences

Purchase Evidences

Some of the common types of purchased evidences are as follows.1. Sales taxes invoice (Usually issued by public limited suppliers)2 Comp ter generated in oice / bills (Us all iss ed b Pri ate Ltd2. Computer generated invoice / bills (Usually issued by Private Ltd

Companies)3. Hand written bills over letter head of suppliers (Small scall

suppliers/Partnership concerns)suppliers/Partnership concerns)4. Katchi Purchi with signs of suppliers. ( Un-organized suppliers)

We must determined which types of purchase evidences are received by theyp p ycustomer and incorporate their nature in the process follows.

In case of katchi purchi or no evidences a transaction summary sheet will beobtained from the customer.

Purchase Evidences

Timing of purchases evidences

Purchase Evidences

a) Purchase evidences delivered along with the receipt of goods:

If purchase evidences are delivered after some days of receipt ofd h D l i h M b h b dgoods than Declaration the Murabaha contract must be executed on

the basis of available goods Receipt evidencesE.g. In Fertilizer Industry

b) Purchase evidence delivered after some days of receipt of goods.Customer will mention the PKR value of the goods over the goodreceipt evidences. Invoices will be provided to the bank as soon asthey are received by the Customer.E.g Usually in case of purchase from Limited companies the Invoicesare issued after 10 to 15 days of receipt of goods.

Goods Identification Method

Good identification method

Goods Identification Method

Identification of goods at the time of sale is a must for a valid Sale.

Customer’s business process and storage facility must be visited to determinethe method of identification of goods

Some of the common method goods identification are:1. Separate stacking of goods (Bags of seeds can be stacked seperately)2 Lot no identification in schedule of assets (Purchase of cotton by large2. Lot no identification in schedule of assets (Purchase of cotton by large Corporate units)3. Bag no.4 C l f ki4. Color of packing5. Designating separate area for MBL’s goods (Hides, skins)6. Tank no. (separate allocation of tank for patrol/oil purchase)

Example of Separate StackingExample of Separate Stacking

Identification by Inventory CardIdentification by Inventory Card

Customer Supplier Relationship

Buyer – Seller

Customer Supplier Relationship

y

Agent/Broker – Principal

Parent – Subsidiary

• Majority holding• Minority holdingMinority holding

E.g. US Apparel purchases goods from US Denim, which was a majority holding subsidiary of US Apparel The transaction wasmajority holding subsidiary of US Apparel. The transaction was put into charity.

E.g. Indus Dying purchases goods from Fashion Net, Minority holding subsidiary of Indus Dying The same is incorporated inholding subsidiary of Indus Dying. The same is incorporated in the process flow.

Things to Remember

� Acceptance of Order Form means a financial commitment to thet h t d d P t i t O d F t

Things to Remember

customer, where customer can demand Payment against Order Form atany time

� B k d d/ Bl k O d F h ld b d i� Back-dated/ Blank Order Form should not be accepted in any case.

� RM should submit the Order Form (either Hard Copy / email ScannedA d l b h d f h d f f dCopy) to CAD immediately (by the end of the day) after receipt of Order

Form from the customer.

�� Upon reciept of Order Form, limit of the customer must beearmarked/blocked in the system. This is built in T24 system.

� Customer must be asked to sign and stamp over the copies of Purchaseevidences provided to the Bank.

Things to Remember

� Minimum Inventory Holding period means the minimum time duringhi h h i l di ill i i i i i l f

Things to Remember

which that particular commodity will remain in its original form atcustomer’s premises.

� A mm mi t k i th t r I t r h ldi p ri d p r th� A common mistake is that average Inventory holding period as per thebalance sheet is calculated which is not required as we are interested inonly the inventory holding period of the purchased goods and averageinventory holding period reflects the inventory holding of all the rawy g p y gmaterials

� If it is not possible to obtain Invoices in the name of bank than itsJ ifi i b i d i h flJustification must be mentioned in the process flow.

� If formal Invoices are not issued by supplier than its justification mustl b bt i d i th flalso be obtained in the process flow.

Things to Remember

� During Physical Inspection MBL’s owned goods must be clearlyidentified before signing Murabaha Contract

Things to Remember

identified before signing Murabaha Contract� In case of Physical Inspection Murabaha Contract must be executed

during physical inspection but if not possible during physical inspectionthen at most at the same day provided that it must be ensured thatthen at most at the same day provided that it must be ensured thatgoods are not consumed/sold.

� RM must communicate the acceptance of Murabaha Contract to thecustomer only after MBL signs on customer’s offer to Purchase merelycustomer only after MBL signs on customer s offer to Purchase merelysubmission of Purchase evidences does not concludes Murabahatransaction automatically.

� If the procurement cycle of the customer changes with the passage of� If the procurement cycle of the customer changes with the passage oftime and/or change in economic conditions, RM should get theMurabaha Process Flow revised and approved from PDSC so as toincorporate the change in procurement cycle.p g p y

Things to RememberThings to Remember

�� RM should get the Murabaha Process Flow accepted from the customer.RM should explain each and every step of the Process Flow to thecustomer so as to avoid any mistake in the execution of the Murabahatransactions.

� RM should remain in constant touch with the customer even afterapproval of PF to be aware regarding changes PF ground realities.

Case StudiesCase Studies

Case Studies for MurabahaCase Studies for Murabaha

Some case studies of Murabaha Financing are as follows and will be coveredin detail in the presentation:p

1. Novatex2. Nishat Power2. Nishat Power3. Abdullah Textile Mills

Novatex Limited

NOVATEX LTD.

Company Background:

NOVATEX LTD.

Company Background:

Novatex is the leading manufacturer of Pet Resin and pre-forms. Major Rawmaterial of Novatex is PTA, which is procured from Lotte Pakistan.

Background of the Procurement Cycle:

Customer own around 9 specially designed containers for delivery of PTAfrom Lotte Pakistan to customer’s premises.

Delivery of PTA is round the clock at Novatex premises and PTA is receivedy pin specially designed containers mostly in BULK form.

PTA is directly decanted to the storage area from the containers where it isy gmixed with the previously procured PTA.

NOVATEX LTD.NOVATEX LTD.

Problems:Problems:

Following issues were faced in offering Murabaha Financing

1. Identification of goods - Mixing of PTA with previously procuredPTA

2. Constant Usage of goods from the storage area

3 Timing of signing of Murabaha Contract3. Timing of signing of Murabaha Contract

4. Customer’s unwillingness on placing Muqaddam for signing ofM b h C t tMurabaha Contract

NOVATEX LTD.

Problems:

NOVATEX LTD.

1. Identification of goods2. Timing of signing of Murabaha Contract

Solution

� Specially designed Murabaha Contract drafted for signing ofSpec a y des g ed u aba a Co t act d a ted o s g g oMurabaha Contract before consumption i.e. mixing of MBL goodswith customer’s own stock

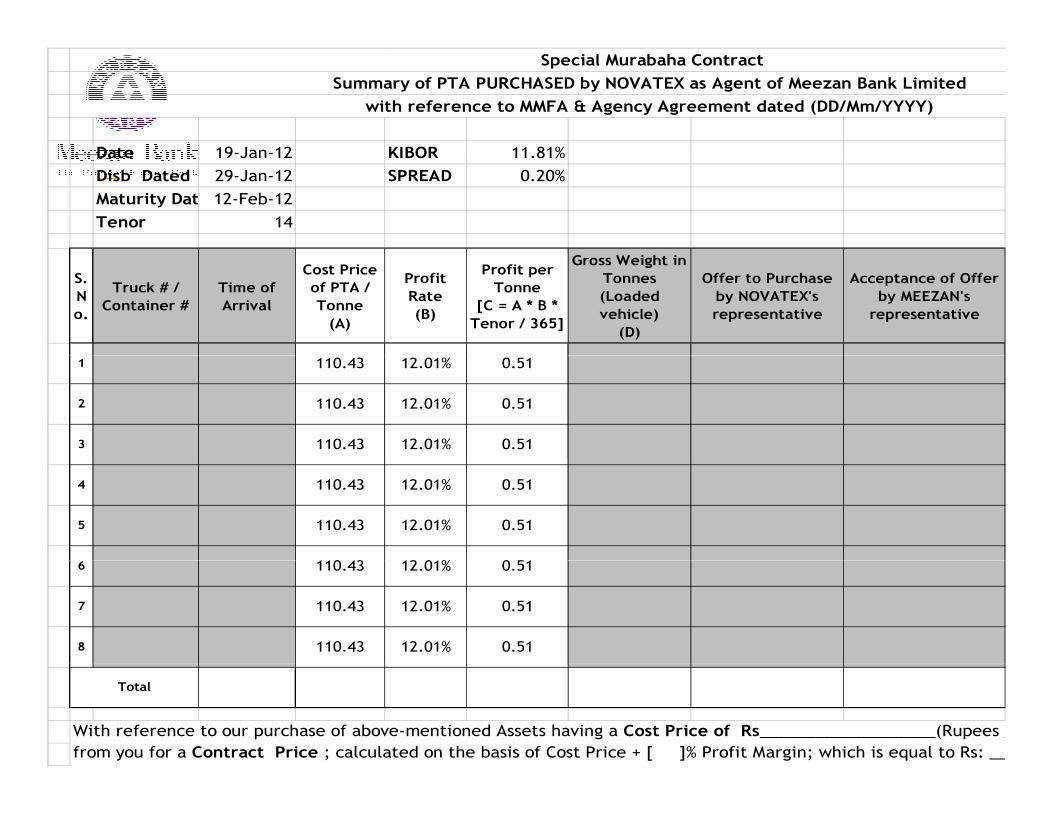

� Murabaha is executed for each Truck on per Tonne basis i.e. Cost perTonne, Profit per Tonne and Sale Price per Tonne of PTA is agreedfor each Truckfor each Truck.

NOVATEX LTD.

Problems

NOVATEX LTD.

1. Identification of goods2. Timing of signing of Murabaha Contract

Solution (Continued…)

� Customer’s authorized representative offer to purchase (by signingCusto e s aut o ed ep ese tat ve p (by s g gthe respective row of ‘Special Murabaha Contract’) PTA from MBL,loaded in a specific vehicle.

� MBL’s representative accept the offer by countersigning respectiverow of ‘Special Murabaha Contract’.

Date 19 Jan 12 KIBOR 11 81%

Special Murabaha ContractSummary of PTA PURCHASED by NOVATEX as Agent of Meezan Bank Limited

with reference to MMFA & Agency Agreement dated (DD/Mm/YYYY)

Date 19-Jan-12 KIBOR 11.81%Disb Dated 29-Jan-12 SPREAD 0.20%Maturity Dat 12-Feb-12Tenor 14

S. No.

Truck # / Container #

Time of Arrival

Cost Price of PTA / Tonne

(A)

Profit Rate (B)

Profit per Tonne

[C = A * B * Tenor / 365]

Gross Weight in Tonnes (Loaded vehicle)

(D)

Offer to Purchase by NOVATEX's representative

Acceptance of Offer by MEEZAN's

representative

1 110.43 12.01% 0.51

2 110.43 12.01% 0.51

3 110.43 12.01% 0.51

4 110.43 12.01% 0.51

5 110.43 12.01% 0.51

110 43 12 01% 0 516 110.43 12.01% 0.51

7 110.43 12.01% 0.51

8 110.43 12.01% 0.51

With reference to our purchase of above-mentioned Assets having a Cost Price of Rs___________________(Rupees _from you for a Contract Price ; calculated on the basis of Cost Price + [ ]% Profit Margin; which is equal to Rs: __

Total

NOVATEX LTD.

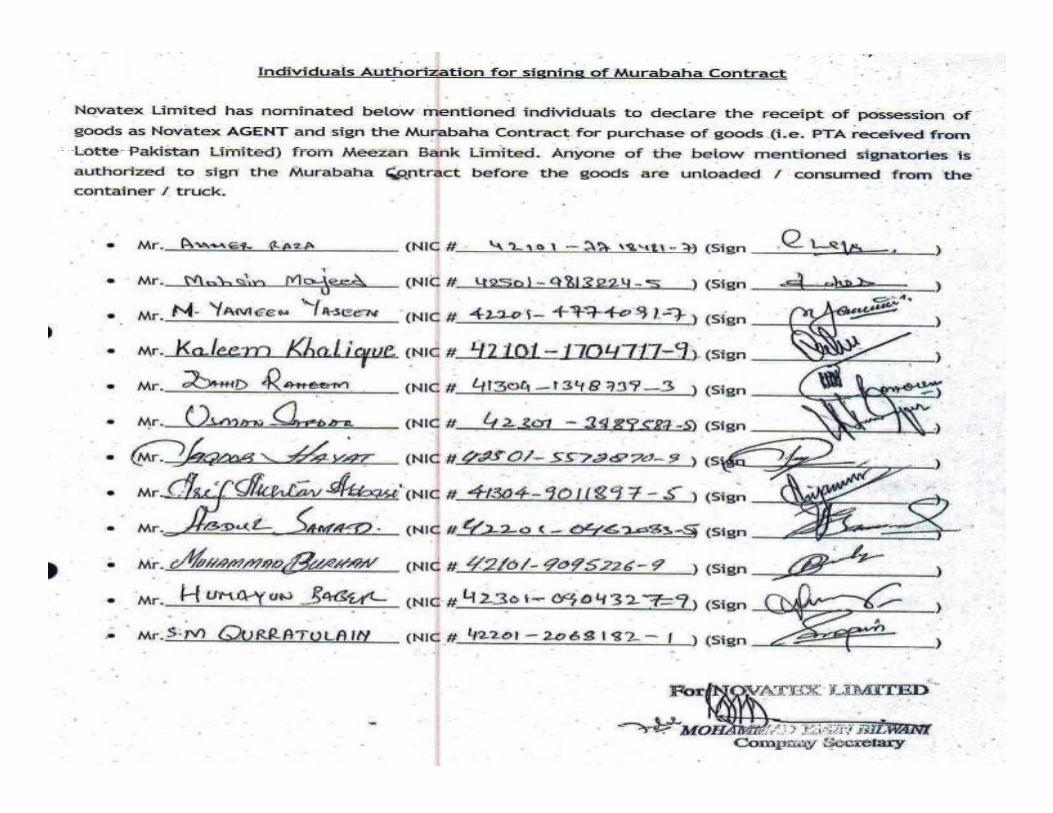

3. Novatex’s unwillingness on placing Muqaddam for signing of Murabaha

NOVATEX LTD.

g p g q g gContract

Nomination of factory personnel for signing of ‘Offer to Purchase’

Novatex nominated 10 different factory personnel (of different shifts) forsigning of ‘Offer to Purchase’ Murabaha goods from Bank on Novetex’ss g g o u aba a goods o a o Novete sbehalf.

Novatex Ltd.

3. Novatex’s unwillingness on placing Muqaddam for signing of

Novatex Ltd.

Murabaha Contract (Continued….)

Agency Agreement with customer’s representatives

� MBL signed Agency Agreement with 10 different customer’srepresentatives of factory (of different shifts) for performingfollowing activitiesg

� Write Truck #, Gross Weight, Time and Actual Weight� Signing of ‘Acceptance of Offer’

� Their names were placed on the Notice board near decanting station

Ni h t P Li it dNi h t P Li it dNishat Power LimitedNishat Power Limited

Nishat Power Ltd.

Company Background:

Nishat Power Ltd.

Nishat Power Limited (NPL) is contributing economical power to thenational grid. Major Raw material of NPL is Furnace Oil which is procuredfrom PSO, Oilco etc.

Background of the Procurement Cycle:

The procurement of Furnace Oil is being made through Different supplierson Advance / Credit Payment

When the oil tankers arrive they are weighed on Weigh Bridge at NPL. Ay g g gweight receipt is generated and issued to the tanker driver.

The risk of oil is transferred to NPL at the time when the oil is dumpedpfrom the oil tanker into the Storage Tank at NPL; before dumping of oil, therisk is borne by the supplier.

Nishat Power Ltd.

Background of the Procurement Cycle: (Continued….)

Nishat Power Ltd.

There are 3 storage tanks at NPL’s plant, each having capacity of 10,000metric tons of furnace oil. Additionally, there are two ‘day tanks’ and twobuffer tanks. Day tanks have capacity of 500 metric tons each, while buffertanks have capacity of 200 metric tons each.

The furnace oil is pumped from storage tanks to buffer tanks, from where itis treated for impurities and then pumped to day tanks for ultimateconsumption.p

Nishat Power Ltd.

Problems

Nishat Power Ltd.

Problems

Oil procured on any day is first decanted in the Storage tanks of thecustomer The decanted oil may (or may not ) pumped to the buffer tankcustomer. The decanted oil may (or may not ) pumped to the buffer tank.

Chances of consumption, i.e. pumping of oil from Storage tank to buffertank of Oil procured on MBL’s behalf is possibletank, of Oil procured on MBLs behalf is possible

Murabaha Contract cannot be executed on per container basis as the risk ofthe goods transfers to the buyer after the oil is decanted in customer’sthe goods transfers to the buyer after the oil is decanted in customer sstorage tank

Nishat Power Ltd.

Solution

Nishat Power Ltd.

Solution

Keeping in view the working capacity of NPL, which is 1000 metric tons per d MBL’ RM ill l t th d il t k t k th t th iday, MBL’s RM will evaluate the daily stock to make sure that there is sufficient stock of oil already owned by NPL available for current production of NPL (that is minimum 2000 MT, which is sufficient for 2 d ) b f d i f MBL’ ildays) before decanting of MBL’s oil.

MBL’s RM will then identify the storage tank of NPL with minimum level of il ffi i f d ioil sufficient for current production.

Nishat Power Ltd.

Solution (Continued…)

Nishat Power Ltd.

( )

Oil is then dumped in the storage tank as identified above, thereby creating Shirkat ul Milk of oil in the tank. NPL will be allowed to utilize oil from the Shirkat ul Milk of oil in the tank. NPL will be allowed to utilize oil from thetank up to its share in the tank till the Murabaha Contract is signed.

The customer will provide the stock report in the next morning The stockThe customer will provide the stock report in the next morning. The stock report will show present status of oil in Storage Tank as identified by the RM initially and the additions of MBL’s oil during last day and quantity used by NPL during this periodNPL during this period.

Nishat Power Ltd.

Solution (Continued….)

Nishat Power Ltd.

The customer will sign a Declaration for receipt of oil as MBL’s agent,mentioning the percentage holding of Furnace Oil of MBL in the StorageTank and subsequently sign the Murabaha Contract for purchase of the samequantity.

Following points should be taken care of while signing of MurabahaContract and Schedule of Asset� The Schedule of Assets along with the Murabaha Sale Contract must

include the accurate percentage of oil owned by MBL. Quantity ofp g y Q yOil should be mentioned as percentage of the total oil, in metrictons, present in the tank.

� Number of Storage Tank Identified for Decanting should bementioned on Murabaha Contract.

Abd ll h T til Mill LtdAbd ll h T til Mill LtdAbdullah Textile Mills LtdAbdullah Textile Mills Ltd

Abdullah Textile Mills

Company Background:

Abdullah Textile Mills

Abdullah Textile Mills is a spinning unit, established in 1991 with installed capacity of 234 spindles & 400 rotors. The Company is engaged in manufacturing of ring spun cotton yarn ranging from 10/S to 72/S . The company Factory is located at Abdullah Nagar Chak No 85/15-l, District Khanewal It purchases cotton bales and cotton waste from local market.

Problem:

Abdullah Textile usually make advance payment to supplier on the basis of y p y ppmarket rate of Cotton Bales.

Abdullah Textile Mills

During the transit of cotton bales from supplier to Abdullah Textile the

Abdullah Textile Mills

PKR value of the bales decreases because weight of the bales drops as a result of drying of moisture during the transit.

Therefore the problem is that exact value of goods purchased is determined only after the second weight at customer’s premises.

Solution:

Average deterioration of weight as a result of drying of moisture is g g y gdetermined which comes out to be 20%.

Abdullah Textile Mills was required to give Order form for 20% less value q gthan the Ordered Quantity i.e Order form of Rs 80,000 against order of Rs 100,000.

Abdullah Textile Mills

Upon delivery of bales, when the value of delivered lot is finalized after

Abdullah Textile Mills

weighing, Ownership ratio of MBL is specified over the lot which will be represented in the Schedule of Assets.

MBL will sell its ownership share in the lot of bales to the customer through Murabaha Contract.

For example: If Order form of Rs 80,000 was given for the Order of Rs 100,000 and after second weight at customer’s godown the value of the goods is Rs 90,000 than MBL share in the goods will be 80,000/90,000= g g88.8%.

Thank You