development of corporate governance regulations-the case of an emerging economy

DESCRIPTION

corporate governance in turkeyTRANSCRIPT

Development of Corporate Governance

Regulations: The Case of an Emerging

Economy Javed Siddiqui

ABSTRACT. This paper investigates the development

of corporate governance regulations in emerging econo-

mies, using the case of Bangladesh. In particular, the paper

considers three issues: What type of corporate governance

model may be suitable for an emerging economy such as

Bangladesh? What type of model has Bangladesh adopted

in reality? and What has prompted such adoption? By

analysing the corporate environment and corporate gov-

ernance regulations, the paper finds that, like many other

developing nations, Bangladesh has also adopted the

Anglo-American shareholder model of corporate gover-

nance. Analysis of behaviours of principal actors in the

Bangladeshi corporate governance scenario, using new

institutionalism as a theoretical foundation, then reveals

that such adoption may be prompted by exposure to

legitimacy threats rather than efficiency reasons.

KEY WORDS: corporate governance, emerging econ-

omies, regulations, institutional theory

Introduction

Ever since international financial agencies (IFAs)

such as the World Bank included corporate gover-

nance reforms as a development goal, significant

changes have taken place in the regulatory envi-

ronment guiding corporate governance in emerg-

ing economies1 (World Bank, 2002a). Developing

economies, in great need of external funds, have

been forced to open up their economies as part

of the IFA-sponsored globalisation process. The

IFAs have encouraged adoption of internationally

accepted accounting and corporate governance

practices as a prerequisite for obtaining loans. In

many cases, these agencies have prescribed models of

corporate governance that have been tested and

developed in developed economy conditions as a

‘‘powerful tool to battle against poverty’’ (World

Bank, 2007), and the socio-economic conditions of

the developing countries have been ignored (Uddin

and Choudhury, 2008).

Studies investigating adoption of donor-pres-

cribed regulatory reforms reveal that wholesale

embracement of such models by governments in

emerging economies has been a result of past failures

of indigenous economic and industrial polices, and

dependence on overseas assistance. Subsequently,

the role of IFAs in promoting such models has been

questioned (Reed, 2002). This sets the context for

this study.

The primary objective of this paper is to inves-

tigate the development of corporate governance

(CG) regulations in emerging economies, using

Bangladesh as a case. Like many other developing

economies, the Bangladesh corporate sector is char-

acterised by high ownership concentration, reluc-

tance of the corporate sector to raise funds through

the capital markets, lack of shareholder activism,

availability of bank financing, and poor enforcement

and monitoring of regulations. Also, the Bangladesh

government is dependent on IFAs for financing

various development projects, and there are in-

stances of donor influence in government policy

making (Sobhan, 2003).

In investigating the development of CG regula-

tions, this paper seeks to address three questions:

What type of CG model is conducive to Bangla-

desh’s current state of economic, legal and socio-

political environment? What type of CG reform has

Bangladesh adopted? And, what has prompted such

adoption? In doing so, the paper uses efficiency and

Journal of Business Ethics (2010) 91:253–274 � Springer 2009DOI 10.1007/s10551-009-0082-4

institutional perspectives (Zattoni and Cuomo,

2008) to investigate adoption of a particular brand of

CG reforms. Using new institutionalism (new

institutional sociology, hereafter NIS) as the con-

ceptual framework, this paper investigates the role of

different actors, namely, the professional bodies, the

private sector and the regulators, in the CG scenario

of Bangladesh. The influences of the IFAs on each of

these actors are investigated. By comparing the codes

developed by different regulatory bodies, the paper

attempts to identify isomorphic behaviour by dif-

ferent actors, and then use the NIS framework to

explain the potential reasons for such behaviour.

The findings suggest that, consistent with other

emerging economies, Bangladesh has also adopted the

Anglo-American shareholder model of CG, although

is not considered to be entirely suitable for emerging

economies, given the economic, legal and corporate

environment of these countries. An analysis of the

behaviour of the principal actors in the Bangladeshi

CG scenario indicates that the lack of self-regulation

by the professional bodies, and the absence of private-

sector rule-making bodies have created the scope for

the IFAs operating in Bangladesh to intervene with

policy-making decisions through private-sector

think-tanks. Thus, the decision for wholesale adop-

tion of IFA sponsored shareholder models have been

prompted by exposure to threats of legitimacy, rather

than efficiency perspectives.

The paper is organised as follows: the next section

presents a review of literature concerning CG reg-

ulations in emerging economies. Different CG

models are discussed. The following section exam-

ines the corporate environment for Bangladesh, and

seeks to identify the type of CG model that may be

suitable for such an environment. A subsequent

section then analyses different CG initiatives in

Bangladesh in an effort to determine the type of CG

model Bangladesh has adopted. This is followed by

section that attempts to explain and discuss the rea-

son for such adoption. Using agency and institu-

tional perspectives, the roles of different actors in the

Bangladeshi CG scenario are analysed.

CG models in developing economies

Donaldson and Preston (1995) identify two different

theories of corporation. The shareholder theory

emphasises that corporations are extensions of their

owners, who should be benefiting from it. There-

fore, the corporation should be accountable only to

the shareholders. On the other hand, the stake-

holder theory acknowledges corporation as a social

entity that has responsibility to a wider group of

stakeholders including shareholders, creditors, man-

agement, employees, the government and other

interested groups (Freeman and Reed, 1983). Sub-

sequent models of CG have been based on these two

views of the corporation. Whereas the Anglo-Saxon

models of CG have been embedded on the share-

holder theory, the European model has incorporated

the stakeholder version.

Letza et al. (2004) compare the two theories. The

shareholder model, or the principal agent model

(Jensen and Meckling, 1976), views that the purpose

of the corporation is to maximise shareholders’

wealth. According to this model, the main problem

of governance arises because of the agency rela-

tionship. Like the agency theory, the shareholder

model of CG is also a rational actor model, where

human beings are expected to be maximising their

own interest. As the model is based on assumptions

of strong market efficiency, a voluntary code of CG

is deemed to be sufficient, as managers in a strong

market would have enough incentives to install CG

mechanisms in their firms. The stakeholder model,

on the other hand, rejects the agency relationship as

the principal problem of CG. Rather, absence of

stakeholders’ involvement is viewed as the main

obstacle for ensuring efficient controls. Contrary to

the shareholder model, this model emphasises a

trust-based long-term relationship between firm and

stakeholders, protection of the rights of different

stakeholders, employee participation and business

ethics (Letza et al., 2004).

Zattoni and Cuomo (2008) apply efficiency and

institutional perspectives to investigate the global

diffusion of CG practices. The paper argues that, in

countries with poor protection of investors’ rights

(later referred to as civil right countries), the

potential benefits of adopting CG practices are

greater than in countries with strong protection of

investors’ rights (common law countries). The paper

also mentions that, under pressure from external

forces, governments may be forced to change gov-

ernance practices in order to legitimise the economic

system and attract foreign investments (p. 4). Using a

254 Javed Siddiqui

sample of 44 countries, the paper concludes that

issuance of codes in countries with poor investor

protection is prompted more by legitimisation rea-

sons rather than efficiency reasons. This is also

consistent with Enrione et al. (2006), who find such

countries to be late adaptors of CG regulations.

However, the paper did not comment on the types

of codes adopted by the sample countries.

The adoption of different type of codes of CG

was investigated by Rwegasira (2000) in an emerg-

ing economy context. The paper refers to stock-

holder and stakeholder models as ‘market-based’ and

‘institutionally based’ systems of governance. The

market-based system of governance is considered to

be more appropriate where company shares are

generally owned by dispersed owners, and the

managers are relatively free from close scrutiny and

control. Such systems are characterised by one-tier

board leadership structure. The institutionally based

system, on the other hand, relies on closer contact

between shareholders, managers, workers and sup-

pliers, and is hence synonymous with the stake-

holder model of CG. Rwegasira (2000) mentions

that this system of CG is more applicable to coun-

tries where banks are the primary sources of finance

for the companies. Such models are characterised by

the presence of a two-tier board structure: bankers

and other non-executive directors are members of

the supervisory or oversight board, whereas the

managers are members of the management board.

Having identified the essential characteristics of the

two models, the paper then proceeds to comment on

the applicability of these models for Africa. Rwe-

gasira (2000) states that market-based systems have

got limited applicability in Africa.

The market-based system presupposes a low degree of

concentration of ownership, limited bank holdings…as

well as free flowing reliable and timely information

about the business and financial affairs of the company.

A number of these characteristics are not readily

realisable in Africa, at least for the time being.

(Rwegasira, 2000, p. 265)

The paper suggests that the institutionally based

system of CG may be a more preferred model for

Africa because of the low level of sophistication of

the stock markets and the investors, domination of

bank financing and high degrees of debt–equity

ratios. Also, most of the businesses in Africa tend to

be small or medium in size, making the banks even

more important stakeholders. The presence of bank

representatives on the board of directors would be

beneficial especially to the minority shareholders

who may not have the time and resources to

understand the complexity of the business. How-

ever, the paper pointed out that the success of such

models would depend on restructuring of banks and

financial institutions to accommodate better quality

staff and management. Paredes (2005) investigates

whether the US-styled stockholder model contrib-

utes to economic development for the emerging

economies. Consistent with Rwegasira (2000), the

paper identifies the lack of advanced markets as a

major factor that makes the stockholder model

inappropriate for the emerging economies. Paredes

states that emerging economies lack important

‘‘second-order institutions’’ such as experienced

investment bankers, lawyers, security analysts,

accountants and effective judicial systems that

‘‘enables markets to monitor’’ (Paredes, 2005, p. 36).

Paredes also points out that the shareholder system is

based on long-term pay-offs rather than short-term

benefits. However, the socio-political and economic

instability prevailing in many developing economies

makes it harder to predict future prospects.

Reed (2002) investigates adoption of CG models

in emerging economies. The paper states that, typi-

cally, emerging economies tend to adopt the Anglo-

Saxon (shareholder) model of CG [for example, India

(Mukherjee-Reed, 2002), South Africa (West, 2006)

and South Korea (Reed, 2002)], despite the fact that

such model is based on assumptions of efficient

markets and equity financing. The paper mentions

that many of these countries are formal British col-

onies, and share the common law system. This could

act as an incentive for adopting the Anglo-Saxon

model. Mukherjee-Reed (2002) investigates reasons

for India’s adoption of the Anglo-Saxon model of

CG. The paper compares the performance of the

Indian CG model with three basic claims made by

the Anglo-Saxon model: firstly, liberalisation will

result in increased corporate growth and profits;

secondly, sustained macro-economic growth will

facilitate overall level of opportunities, and benefits to

the society; and thirdly, the model will ensure

increased transparency in corporate dealings and

provide greater investor protection. The results

indicate that the effects of CG reforms in India have

Development of Corporate Governance Regulations 255

been less than promising. Especially, the reforms have

resulted in weakening of labour power, as indicated

by declining wage rates. Also, the reforms have failed

to improve levels of transparency and control by

shareholders (Mukherjee-Reed, 2002, p. 263). As

reasons for India’s adoption of the Anglo-Saxon

model, the paper mentions

The impetus for this shift (towards adoption of the

Anglo-Saxon model) has been a combination of global

political economy pressures and problems arising our

of the previous business house model of governance.

(Mukherjee-Reed, 2002, p. 266)

Therefore, the paper identifies the efficiency and

institutional perspectives (Zattoni and Cuomo,

2008) for adopting a particular model of CG.

However, apparently, the efficiency perspective does

not seem to explain the less than promising perfor-

mance of the CG model in India. As a source of

global political-economic pressure, the paper men-

tions that poor economic performance in 1991

forced the Indian government to turn to the Inter-

national Monetary Fund (IMF) and World Bank,

which initiated CG reforms in line with the Anglo-

Saxon model. Reed (2002) also acknowledges

dependence on external bodies (such as the World

Bank and the IMF) as one of the major reasons for

the dissemination of the shareholder model in

emerging economies.

As a condition of renegotiating loans, international

finance bodies imposed structural adjustment pro-

grammes on developing countries. These programmes

included a variety of features that induced a move to

an Anglo-Saxon model of governance. (Reed, 2002,

p. 230)

This is supported by Arnold (2005) who mentions

that IFAs such as the World Bank, the IMF and the

Asian Development Bank (ADB) could be regarded as

‘‘the new colonising influences arising from glob-

alisation of economic governance’’. Influences of

development agencies in accounting standard setting

in emerging economies are also reported by a number

studies [for example, Ashraf and Ghani (2005) in

Pakistan, Akhtaruddin (2005) and Mir and Rahaman

(2005) in Bangladesh, Ozcan and Cokgezen (2003) in

Turkey, Ahunwan (2002) in Nigeria and Uddin and

Tsamenyi (2005) in Ghana]. Uddin and Choudhury

(2008), investigating CG practices in Bangladesh,

question the role of the IFAs in development of CG

regulations in emerging economies.

Least developed countries (LDCs), sponsored and

advised by donor agencies, continue to focus on direct

transfers of governance models from Anglo-American

countries. The obsession with Western governance

models has led to insufficient regard for how tradi-

tional social structures, characterised by families, may

affect Western solutions in Bangladesh. Thus, the

paper encourages further research on CG issues in

traditional settings, which should take local pecu-

liarities and culture into consideration. (Uddin and

Choudhury, 2008, p. 1045)

Reed (2002) also points out that adoption of the

Anglo-Saxon model also has a legitimisation role. By

adopting this model, governments in developing

countries may try to send signals to the public that

the unpopular reforms (promoting globalisation and

free markets) are guided by efficient corporate

structures that will help generate condition for

economic growth and development. This is consis-

tent with Enrione et al. (2006) who suggest that late

adopters of CG codes tend to mimic established

practices for the sake of gaining legitimacy.

The Bangladesh corporate sector

Bangladesh is a South Asian country surrounded by

India and Myanmar. According to the United

Nation’s human development index, it is classified as

a least developed country (LDC).2 The corporate

environment in Bangladesh is characterised by

concentrated ownership structure, bank financing,

poor legal framework and lack of monitoring.

Table I presents the basic macro-economic data for

Bangladesh and its neighbours in South Asia. The

table indicates that Bangladesh significantly lags

behind its South Asian neighbours, all developing

nations, in terms of national income per capita. In an

effort to understand the nature of CG model that

may be suitable for Bangladesh, this section now

analyses the environment within which the corpo-

rate sector operates. In line with literature con-

cerning the suitability of different CG models [for

example, Paredes (2005), Rwegasira (2000)], a

number of attributes are analysed.

256 Javed Siddiqui

Ownership structure

Like many other developing countries, most com-

panies in Bangladesh are either family owned or

controlled by substantial shareholders (corporate

group or government). Company managements are

effectively just extensions of the dominant owners

(Farooque et al., 2007). They are closely held small

and medium-sized firms where corporate boards are

owner driven. Consequently, most of the companies

have executive directors, CEO and chairman from

the controlling family. Farooque et al. report that, on

average, the top five stockholders hold more than

50% of a firm’s outstanding stocks. Imam and Malik

(2007) analyse the ownership patterns of 219 com-

panies from 12 different industries listed on the Dhaka

Stock Exchange, the major stock exchange in the

country. It is reported that, on average, 32.33% of

the shares are held by the top three shareholders,

the results being even higher for real estate, fuel

and power, engineering, textile and pharmaceutical

sectors.

Shareholder involvement

Uddin and Choudhury (2008), investigating the

state of CG practices in Bangladesh, report that

Bangladeshi companies are reluctant to hold annual

general meetings (AGMs) even though this is a

statutory requirement. When AGMs are held, these

are characterised by domination by a small group of

people, poor attendance and discussion of trivial

matters. This is supported by a CG survey conducted

by the Bangladesh Enterprise Institute (BEI, 2003).

The perception of AGMs amongst the non-banking

listed companies surveyed seems to be a combination of

a necessary evil and a statutory requirement. Generally,

shareholder demands concentrate either on higher

dividends or trivial concerns like better quality food

and gifts at the AGM and transportation allowances.

The main incentive for attendance is the meal served at

an attractive hotel and, surprisingly, trading activity

increases prior to AGMs to reflect that interest. There

are, in reality, a very limited number of people going to

AGMs who actually understand the financial statements

being presented and, consequently, have little to con-

tribute in terms of relevant inputs. (BEI, 2003, p. 33)

Reaz and Arun (2006), investigating the state of

CG in the banking sector, also have similar con-

clusions regarding shareholder involvement in the

Bangladesh corporate sector.

The capital market

The capital market in Bangladesh is still in primitive

stage. The country has two stock exchanges: the

TABLE I

Comparative economic, financial and capital market indicators as of December 31, 2006

Bangladesh India Pakistan Sri Lanka

Population (million) 158.6 1079 152 19

GDP per capita (US $) 470 620 600 1010

Number of stock exchanges 2 4 2 1

Market capitalisation (% GDP) 7.5 91.5 28.8 33.3

Number of companies registered 1327 N/A N/A N/A

Number of companies listed 325 4700 671 237

Number of chartered accountants 727 130,000 3700 2700

Presence of second-tier accountants None None 1 1

Number of commercial banks 49 88 28 19

Source: ADB quarterly economic update, December 2006, Economic Survey India, 2006, Securities and Exchange

Commission of Sri Lanka, South Asian Federation of Accountants website www.esafa.org; Wikipedia list of banks http://

en.wikipedia.org; South Asian Federation of Exchanges website www.safe-asia.com. Number of companies listed data for

Bangladesh, India, Pakistan, and Sri Lanka are for Dhaka Stock Exchange, Mumbai Stock Exchange, Karachi Stock

Exchange and Colombo Stock Exchange, respectively.

Development of Corporate Governance Regulations 257

Dhaka Stock Exchange (DSE) and the Chittagong

Stock Exchange (CSE). Although the Dhaka Stock

Exchange was set up in the early 1950s, the capital

market in Bangladesh has not flourished in com-

parison with its South Asian counterparts. Table I

presents the market capitalisation statistics for the

major bourses in South Asia. It shows that market

capitalisation to GDP ratio for Bangladesh is only

7.5%, whereas it is much higher in other South

Asian countries. A survey conducted by the Ban-

gladesh Enterprise Institute (BEI, 2003) reports that

the capital market does not seem to offer adequate

incentives for companies to go public.

Bank financing is readily available as result of excess

liquidity and extensive competition in the banking

sector due to the fact that new private bank licenses

had been issued mostly on a political basis; banks

therefore are reluctant to enforce additional require-

ments or strict conditions in lending. This phenome-

non is substantiated by our survey which revealed that

equity requirement had been the prime motivator for

only 10% of the public companies interviewed – the

remaining companies had cited reasons like tax

advantages and legal compulsion, for going public.

(BEI, 2003)

Bank loans are easily available as result of excessive

liquidity (discussed later in this section). Competition

in the banking sector also has resulted in lenient

conditions for credit. As a consequence, companies

still prefer debt financing to enlisting with stock ex-

changes. The ADB quarterly economic update on

Bangladesh (ADB, 2006) identifies poor CG, lack of

quality shares and inadequate and irregular partici-

pation of the institutional shareholders as major

reasons for the stagnant capital market. This is sub-

stantiated by the low number of companies listed in

Bangladesh stock exchanges (Table I).

The second-order institutions

Despite having a very large population, the number

of auditors in Bangladesh is surprisingly low, even

compared with its neighbours.3 A recent World

Bank report (2003) suggests that the auditing pro-

fession does not attract the best quality students, and

the job does not really differentiate between an

MBA and a professional auditor. Karim and Moizer

(1996) identified that audit fees in Bangladesh are

significantly low. The Company Act (1994) requires

that all public limited companies must have their

annual reports audited by professional chartered

accountants (members of the Institute of Chartered

Accountants of Bangladesh).

The Bangladesh Enterprise Institute (BEI, 2003),

in its report on the state of CG in Bangladesh,

identified the dismal state of the auditing profession

in Bangladesh.

The auditing function would seem to represent a

vicious circle; auditors are not perceived as indepen-

dent, and do not provide quality audits, therefore,

companies and shareholders are not willing to pay high

fees for an audit. The low fee structure, in turn, does

not provide an incentive to provide quality personnel

and audits. (BEI, 2003, p. 62).

Also, Bangladesh lacks the presence of any sec-

ond-tier accountancy bodies to cater to the needs of

the corporate world, although neighbouring coun-

tries have similar institutions.4 This means that a vast

majority of accountants working in the corporate

sector do not possess any accounting qualifications.

In addition to this, the other second-order institu-

tions, such as the judiciary, suffer from lack of skills

and proper training, especially in dealing with cor-

porate cases (BEI, 2003).

Legal structure

Bangladesh is a former British colony, and has

inherited the common legal system. The Companies

Act 1994 (revised after 81 years from Companies

Act 1913, when Bangladesh was part of British

India) defines the structure of the firms, including

the composition of the board of directors, appoint-

ment of the CEO, appointment and remuneration of

the auditors etc. The financial sector is also regulated

by the Banking Companies Act (1994) and the

Insurance Act (1973). However, the problem with

the legal environment has always been its poor

implementation (BEI, 2003). Uddin and Hopper

(2003), examining the success of privatisation of

state-owned companies in Bangladesh, also identi-

fied the lack of legal enforcement as a major prob-

lem. A World Bank study on the state of financial

accountability and governance in Bangladesh (World

258 Javed Siddiqui

Bank, 2002b) identifies that the sharing of respon-

sibility by a number of government agencies com-

plicates enforceability of corporate regulations.

Responsibility for enforcement is shared among the

Registrar of Joint Stock Companies, the Securities and

Exchange Commission, the professional accountancy

bodies, and the judiciary. The involvement of several

bodies in corporate accountability complicates enforce-

ment and reduces overall effectiveness. (World Bank,

2002b, p. 83).

Economic dependence on IFAs

After its independence in 1971 from Pakistan,

Bangladesh inherited a private-sector-dominated

economy. The new government was committed to

socialism. This, along with the ownership vacuum

created by West Pakistani owners of the industries,

who fled the country during the liberation war,

resulted in nationalisation of almost all major

industries. To fill this vacuum, bureaucrats, with no

prior management experience of training to run

commercial enterprises, were charged with running

these public-sector enterprises. The relative lack of

experience of these new managers led to poor per-

formance of these public-sector entities. This, cou-

pled with poor economic performance and change

in the government, allowed IFAs such as the World

Bank and the IMF to start intervening in economic

policy making in Bangladesh. Like other emerging

economies, donor agencies started sanctioning loans

against conditions of privatisation and open market

economy. A number of donor-aided financial sector

reforms projects were undertaken [for example, the

Financial Sector Adjustment Credit (FSAC) project

and the Financial Sector Reforms Programme

(FRSP), financed by the World Bank]. Among other

things, The FSAC, introduced in the early 1990s,

aimed at strengthening the capital market (CPD,

2003). This is consistent with Reed (2002) who

reports that structural adjustment programmes

imposed by international financial institutions work-

ing in emerging economies tend to promote glob-

alisation, free market economy and development of

capital markets. The World Bank and the Asian

Development Bank were instrumental in the

development of accounting standards in Bangladesh

(Mir and Rahaman, 2005). The influence of the

World Bank and other IFAs in structural adjustments

reforms in Bangladesh has also been investigated by

Uddin and Hopper (2003) and Akhtaruddin (2005).

Uddin and Hopper (2003), investigating the effect of

the World-Bank-initiated privatisation policy, ques-

tions the World Bank’s focus on profitability ‘‘to the

neglect of employment conditions, including trade

union and individual rights; social returns; and

financial transparency and accountability to external

constituents’’ (Uddin and Hopper, 2003, p. 769). It

is interesting to note that all these factors mentioned

by Uddin and Hopper as not considered by policies

imposed by the World Bank are actually consistent

with the stakeholder model of CG.

Excess liquidity in the banking sector

The Bangladeshi banking sector is characterised by

presence of large number of commercial banks, ex-

cess liquidity in the banking sector and default cul-

ture. Due to recent deregulation in the banking

sector, there has been a significant growth in the

number of private commercial banks. The number

of banks in all now stands at 49 in Bangladesh. Out

of the 49 banks, four are Nationalised Commercial

Banks (NCBs), 28 local private commercial banks,

12 foreign banks and the other 5 are Development

Financial Institutions (DFIs). Table I indicates that,

compared with its neighbours, this number is high.

This has resulted in fierce competition in the

banking sector, resulting in greater ease in obtaining

loans from this sector (BEI, 2003).

However, the main problem in the Bangladeshi

banking sector is the presence of default culture

(Siddiqui and Podder, 2002). The total default loan

rate of all banks was 33.49% (of total loans) in 1997,

40.65% in 1998, 41.11% in 1999 and 34.92% in

2000. Recently, the non-performing loan came

down to 17% in 2004 (BSS, 2004). Younis (2005)

identifies information problems in the form of moral

hazard, adverse selection or monitoring cost of

commercial banks in selecting borrowers; the lack

of legal actions against defaulters (as a major portion

of the loans goes to influential businessmen, politi-

cians and insiders) and the government’s practice of

debt forgiveness as major reasons for nonpayment of

debt in Bangladesh. This is consistent with the BEI

Development of Corporate Governance Regulations 259

(2003), which reports presence of political interfer-

ence in lending decisions by banks. The Centre for

Policy Dialogue (2003) reports that the existence of

this default culture is not only having adverse impact

on profitability and liquidity, but also raising the cost

of lending substantially. This, in turn, means that

good borrowers are affected and in some cases, they

have been influenced not to repay bank loans.

State of corporate social responsibility, and labour

conditions

Belal and Owen (2007) investigates the extent of

corporate social reporting in Bangladesh. They

report that the key social issues of concern in the

corporate sector are child labour, equal opportunity

and workplace health and safety matters.5 Working

conditions and poor wage rates are issues of partic-

ular concern. In many instances workers are required

to work 12 h a day, sometimes throughout the

night, with 1 day’s holiday per month and com-

pulsory overtime (Milne, 2001). A further problem

lies in the issue of unpaid wages which often remain

outstanding for months, especially in the export-

oriented garments manufacturing sector (Frost,

2005).6 This results in frequent violence and anarchy

in the industrial sector.

From the above discussion, it is apparent that the

corporate sector in Bangladesh is characterised by

high ownership concentration, lack of shareholder

involvement, the reluctance of firms to raise capital

through the stock markets, high degree of bank

borrowing and eventual nonpayment of such

loans, and lack of quality manpower for operating

the second-order institutions. The socio-economic

environment is affected by unsatisfactory legal

enforcement and poor working conditions. In

addition, the Bangladesh corporate and economic

environment also suffers from lack of timely infor-

mation (Imam et al., 2001), and political instability

(CPD, 2003).7 This is consistent with Farooque

et al. (2007), who report that some of the institu-

tional features of Bangladesh include a less developed

capital market, an at least weak-form efficient stock

market, absence of an active market for corporate

control, generally concentrated ownership, high

reliance on bank financing and a passive managerial

labour market. It may be noted that these conditions

are not unique to Bangladesh. Rather, such condi-

tions prevail in many emerging economies; for

example, Ahunwan (2002) reports presence of

concentrated ownership, inefficient capital market,

unsophisticated legal system and lack of shareholder

activism in Nigeria; Rwegasira (2000) identifies low

degree of capital market sophistication, high own-

ership concentration and lack of economic and

political stability in Africa. Paredes (2005) men-

tioned that the prerequisites for efficient functioning

of the shareholders model include an efficient capital

market, competent manpower working in the

second-order institutions, sound legal structure

and long-term political stability. Also, shareholder

involvement and timeliness of financial reporting

were considered important prerequisites for success

of the shareholder model (Letza et al., 2004; Rwe-

gasira, 2000). It seems that all of these factors are

absent in Bangladesh, justifying the non-adoption of

the shareholder model of CG. Also, the poor

working conditions and unsatisfactory levels of loan

recovery make a case for representatives of workers

and banks to be present on the board of directors.

Therefore, it seems that the corporate environment

in Bangladesh is more conducive for the adoption of

a stakeholder-based model. This addresses the first

research question. The next section will analyse

what type of CG model Bangladesh has adopted, and

a subsequent section will attempt to analyse the

reasons for such adoption.

Corporate governance initiatives

in Bangladesh

CG reforms in Bangladesh are still in very initial stages.

So far, Bangladesh has failed to develop any recognised

code of CG. The only code of CG developed so far has

been through the Bangladesh Enterprise Institute

(BEI, 2004), a donor-funded private-sector think-tank

without any statutory power. The Bangladesh Bank

(BB), the central bank of Bangladesh, issued a number

of circulars relating to formulation of audit committees

(Bangladesh Bank, 2002), CG (Bangladesh Bank,

2003a) and appointment of the board of directors

(Bangladesh Bank, 2003b). These orders, though not

formally put together as a code, are applicable only for

banking companies. Recently, the Securities and

Exchange Commission (SEC) has issued an order

260 Javed Siddiqui

relating to CG (SEC, 2006), applicable only to com-

panies listed on the stock exchanges. These are the two

major regulations relating to CG in Bangladesh.

This section primarily compares the major CG

initiatives undertaken in Bangladesh so far. The

provisions of the BB circular (2002, 2003a, b), the

BEI code (2004) and the SEC order on CG (SEC,

2006) are compared. For the purpose of comparison,

a number of key features have been identified,

namely, the board of directors, the external auditors,

the audit committee and the basis of compliance.

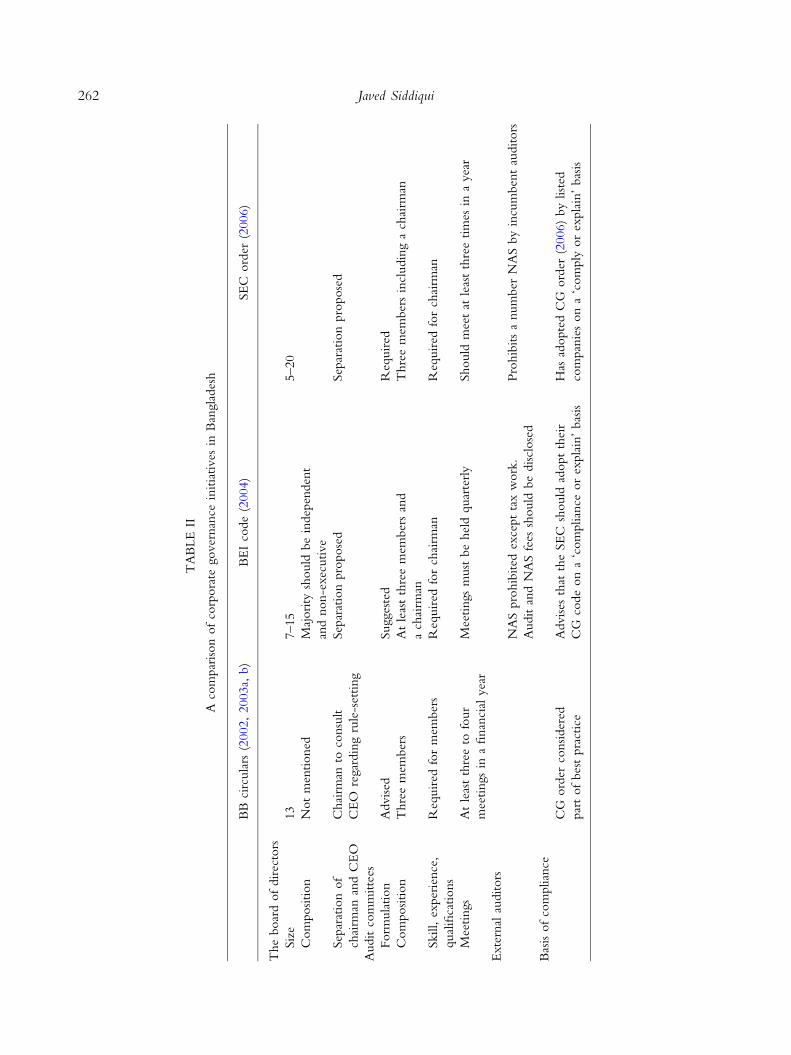

Table II presents a brief comparison.

The board of directors

According to Bangladesh Bank (BB) circulars

(2003b) regarding banking companies, the board of

directors of bank companies should be constituted of

a maximum of 13 directors. According to the BEI

code (2004), the size of the board should be between

7 and 15. The SEC order (2006) suggests that the

number of board members should be not less than 5

and not more than 20.

BEI guideline says that companies should articu-

late and implement a nomination program to enable

a majority of board members to be non-executive

and independent directors. According to SEC, at

least one-tenth of the total number of the company’s

board of directors, subject to a minimum of one,

should be independent directors.

The guidelines of BEI suggest that the position of

the chairman and the CEO should be fulfilled by

different individuals since their functions are neces-

sarily separate. A strong, independent chairman pro-

vides the appropriate counterbalance and check to the

power of the managing director/CEO. The SEC

order states that the positions of the chairman and

CEO should preferably be filled by different indi-

viduals. Although BB guidelines do not mention

anything directly regarding this separation, it indicates

that the chairman should effect all necessary actions in

accordance with the set rules through the CEO.

Audit committees

BEI (2004) suggests forming a number of commit-

tees such as audit committee, nomination committee

and remuneration committee. SEC order (2006)

requires formulation of audit committees. According

to this order, the company should have an audit

committee as a sub-committee of the board of

directors. The audit committee should assist the

board of directors in ensuring that the financial

statements reflect a true and fair view of the state of

affairs of the company and in ensuring a good

monitoring system within the business. BB circular

(2002) advises banks to formulate audit committees

as a part of best practices.

Regarding the composition of audit committees,

BB circular mentions that there should be three

directors nominated by the board for a period of

3 years. BEI guidelines prescribe that there should be

at least three members and a chairman appointed by

the board. The chairman of the board should not be a

member of the committee. SEC states that in an AC

there should be three members selected by the board

of directors, one of whom would be the chairman.

BEI guidelines propose that majority of the members

along with the chairman should be independent

directors. BB did not cover this issue. SEC said that

AC should include at least one independent director.

BB states that the members of the AC should have

‘‘adequate understanding’’ of the role and responsi-

bilities of the committee, as well as the bank’s

business, operation and risks. BEI states the chairman

should be non-executive directors with professional

qualification and recent relevant financial experi-

ence. SEC pronounces that the chairman would

have to possess a professional qualification, and must

have knowledge, understanding or experience in

accounting or finance.

Regarding number of meetings, BB (2002)

requires audit committees to hold at least three to

four meetings in a financial year. This is consistent

with BEI (2004), which proposes that meetings must

be held quarterly, to monitor internal and external

audits. Also, the SEC (2006) prescribes that the audit

committees should meet at least three times in a year.

External auditors

BEI guideline suggests that external auditors should be

independent, well-qualified and free of conflicts of

interest. Except tax work, the audit firms should not

go for any non-audit services and if they perform any

Development of Corporate Governance Regulations 261

TA

BLE

II

Aco

mpar

ison

of

corp

ora

tegover

nan

cein

itia

tives

inB

angla

des

h

BB

circ

ula

rs(2

002,

2003a,

b)

BE

Ico

de

(2004)

SE

Cord

er(2

006)

The

boar

dof

dir

ecto

rs

Siz

e13

7–15

5–20

Com

position

Not

men

tioned

Maj

ori

tysh

ould

be

indep

enden

t

and

non-e

xec

utive

Sep

arat

ion

of

chai

rman

and

CE

O

Chai

rman

toco

nsu

lt

CE

Ore

gar

din

gru

le-s

etting

Sep

arat

ion

pro

pose

dSep

arat

ion

pro

pose

d

Audit

com

mitte

es

Form

ula

tion

Advised

Sugges

ted

Req

uir

ed

Com

position

Thre

em

ember

sA

tle

ast

thre

em

ember

san

d

ach

airm

an

Thre

em

ember

sin

cludin

ga

chai

rman

Skill,

exper

ience

,

qual

ifica

tions

Req

uir

edfo

rm

ember

sR

equir

edfo

rch

airm

anR

equir

edfo

rch

airm

an

Mee

tings

At

leas

tth

ree

tofo

ur

mee

tings

ina

finan

cial

yea

r

Mee

tings

must

be

hel

dquar

terl

yShould

mee

tat

leas

tth

ree

tim

esin

ayea

r

Exte

rnal

auditors

NA

Spro

hib

ited

exce

pt

tax

work

.

Audit

and

NA

Sfe

essh

ould

be

discl

ose

d

Pro

hib

its

anum

ber

NA

Sby

incu

mben

tau

ditors

Bas

isof

com

plian

ce

CG

ord

erco

nsider

ed

par

tof

bes

tpra

ctic

e

Advises

that

the

SE

Csh

ould

adopt

thei

r

CG

code

on

a‘c

om

plian

ceor

expla

in’

bas

is

Has

adopte

dC

Gord

er(2

006)

by

list

ed

com

pan

ies

on

a‘c

om

ply

or

expla

in’

bas

is

262 Javed Siddiqui

non-audit service, both audit and non-audit fees

should be disclosed to the shareholders. Consistent

with BEI (2004), SEC (2006) also prohibits a number

of non-audit services (NAS) by incumbent auditors.8

Basis of compliance

All three CG regulations are also similar in terms of

the bases of compliance. Although the BB circular

on CG makes it mandatory for the banking com-

panies to follow the rules relating to composition of

the board of directors, regarding the formulation of

audit committee, the BB is much more lenient,

mentioning this as a part of best practice, and

‘advising’ banks to formulate such committees

(Bangladesh Bank, 2002). The BEI code (2004)

advises that the SEC should adopt their CG code on

a ‘compliance or explain’ basis. Subsequently, the

SEC has made adoption of their CG order (2006) by

listed companies on a ‘comply or explain’ basis.

From the above discussion, it is apparent that,

despite the inappropriateness of the shareholder

model, as reported in the earlier section, Bangladesh,

like many other developing countries, has adopted

this model. The BB, BEI and SEC CG initiatives all

suggest a single-tier board structure where directors

are elected by the shareholders, the presence of

independent directors on the board and the separa-

tion of the chairman and the CEO. Consistent with

the Organisation for Economic Cooperation and

Development (OECD) guidelines for CG (1999 and

2004), all the CG regulations recommend an

extended role of the audit committees. Also, Ban-

gladesh Bank (2002, 2003a, b), BEI (2004) and SEC

(2006) are similar in terms of audit committee

composition, qualification of committee members,

presence of independent directors and frequency of

the meetings. The BEI (2004) and the SEC (2006)

also have similar views regarding auditor providing

non-audit services, as both actors seem to suggest a

blanket prohibition on a number of services.

Theorising development of CG regulations

The early developments in CG regulations have

been rooted on the basic assumptions of the agency

theory (Jensen and Meckling, 1976). Thus, the

agency-based notions of market efficiency, oppor-

tunism and self-interest-driven motivations for

disclosure are also essential attributes of the Anglo-

American model of CG (Roberts, 2004). However,

shareholder model has been developed, and tested in

developing economy settings, where the basic

assumptions of the agency theory hold. Paredes’

(2005) criteria for success of the shareholder model,

such as efficient contracting systems, sound eco-

nomic policies, efficient market and second-order

institutions, are all features of the agency theory. As

mentioned by Paredes, and as evident from the

discussion presented in the earlier section, such a

model does not work in developing economy set-

tings. Ozcan and Cokgezen (2003) consider agency

perspectives in explaining capital market reforms in

Turkey. The authors argue that economies in

emerging markets are subject to abuse by managers,

politicians and institutions. Therefore, the assump-

tions of the agency theory do not hold. Consistent

with Paredes, the paper finds that the Anglo-Saxon

open market models are not appropriate for

emerging economies.

The apparent shortcomings of the agency theory

in explaining CG in developing countries have

forced different authors to use other theoretical

foundations, and the new institutional sociology

(NIS) framework has been a popular choice (for

example, Enrione et al., 2006; Yoshikawa et al.,

2007 etc.). NIS explains why different organisations

structure themselves in a similar manner. Suchman

(1995) states that the principal difference between

the early management theories, where enterprise was

viewed as a rational system, and the NIS, lies in the

introduction of the concept of organisational legiti-

macy. The paper considers legitimacy as ‘‘a gener-

alised perception or assumption that the actions of an

entity are desirable, proper, or appropriate within

some socially constructed system of norms, values,

beliefs, and definitions’’ (Suchman, 1995, p. 574).

Organisations may seek legitimacy for a number of

reasons. Parsons (1960) mentions that legitimacy

leads to persistence, as stakeholders are likely to

provide resources to organisations that appear

desirable, proper and appropriate. Jepperson (1991)

argues that legitimacy extends creditability to the

organisation, as it involves explaining what the

organisation is doing and why. This is supported by

Meyer and Rowan (1991), who mention that

Development of Corporate Governance Regulations 263

organisations that lack legitimacy are generally

deemed as unnecessary and irrational. DiMaggio

(1988) mentions that attainment of organisational

legitimacy is imperative if an organisation wants

active support from its stakeholders.

DiMaggio and Powell (1983), in their seminal

paper on institutional isomorphism, identified three

mechanisms through which institutions become

similar: coercive isomorphism, mimetic isomor-

phism and normative isomorphism. According to

them, coercive isomorphism generates from political

influence and problems of legitimacy; mimetic iso-

morphism is a result of a standard response to

uncertain environments; and normative isomor-

phism is associated with professionalism. DiMaggio

and Powell (1983, 1991) state that coercive iso-

morphism may arise due to formal or informal

pressures. Sometimes, organisations are subject to a

common legal environment such as tax regulations,

company law requirements, antipollution provisions

etc. Organisations are forced to change their struc-

tures in response to these regulations, and this may

lead to an isomorphic organisational structure

throughout the industrial field. The paper also

acknowledges that direct imposition of regulations

may also come from outside government, such as

professional bodies, or other interested parties. Also,

sometimes, organisations tend to imitate each other.

DiMaggio and Powell (1983) point out that such

mimetic behaviour is likely to happen when the

organisation operates in an uncertain environment,

when the organisational goals are not clearly defined

or when organisational technology is poorly

understood.

Yoshikawa et al. (2007) adopt the institutional

approach to investigate CG developments in Japan.

Based on multiple case studies, the paper concluded

that the Japanese system of CG neither fully con-

verges nor fully diverges from the Anglo-American

model (discussed later in this paper). The paper then

offered a NIS-based explanation for such develop-

ments. It was found that, in defence of legitimacy,

the Japanese government had to eventually revise the

commercial code. Enrione et al. (2006) investigated

the institutionalisation of CG codes using the NIS

approach. The paper argues that institutionalising

processes generally lead to convergence. The paper

used Greenwood et al.’s (2002) six stages of insti-

tutional change to investigate the development of

codes of CG. The paper identifies that, since the

development of the OECD principles of CG

(OECD, 1999), countries around the world have

used this as a benchmark. Consistent with Seal

(2006), the authors argue that such isomorphism

generates due to problems of legitimacy, as the

legitimacy of the governance system is defined as

‘‘conformity to widespread global practises’’ (Enri-

one et al., 2006, p. 967). The paper states that early

adopters of CG regulations have tended to use

economic rationale for such initiative. On the other

hand, late adopters generally tend to mimic the ac-

cepted global practices for the sake of legitimacy.

This is consistent with DiMaggio and Powell’s

(1983) notion of mimetic isomorphism.

Actors in corporate governance

The Bangladeshi CG scenario is dominated by the

presence of a few professional accountancy groups

who are supposed to self-regulate their members, a

number of civil society bodies which are expected to

be sources of normative pressure, and the regulatory

bodies. For the purpose of this paper, this section

will attempt to analyse the behaviour of three dif-

ferent major actors in the Bangladeshi CG scenario:

one professional accountancy body, one civil society

research organisation and one regulatory authority,

using the NIS as a theoretical foundation.

Self-regulation: the Institute of Chartered Accountants

of Bangladesh (ICAB)

The auditing profession in Bangladesh is character-

ised by very low levels of audit fees, poor percep-

tions regarding audit quality and lack of demand for

audited financial accounts. At present, the Institute

of Chartered Accountants of Bangladesh (ICAB) is

the only professional association for chartered

accountants. The ICAB is responsible for developing

the codes of ethics for its members, as well as self-

regulating them. The ICAB has its code of pro-

fessional ethics, and preserves the right to take

disciplinary actions, including cancellation of mem-

bership against members violating said code. The

ICAB code includes concepts of independence,

integrity and professional conduct. However, despite

264 Javed Siddiqui

having such power, the ICAB has very rarely dis-

ciplined its members for violation of its bylaws and

code of ethics.9 In recent years, the SEC fined a

number of audit firms on charges of concealing

material information.10 However, the ICAB failed

to take any disciplinary action against the audit firms.

The lack of actions against members have raised

questions regarding the effectiveness of ICAB as a

professional body, and users have expressed their

concern regarding the quality of financial reports

audited by the members of this association (BEI,

2003). This perception has created problems of

legitimacy for the association.

The apparent failure of ICAB to be perceived as a

legitimate body for professional accountants in

Bangladesh has created the scope for intervention

into its activities by other independent actors. Like

many other developing countries, Bangladesh is also

heavily dependent on overseas assistance. Such

assistance mainly comes in the form of soft loans

from IFAs such as the World Bank, the ADB, the

Department for International Development (DFID)

etc., making these organisations hugely influential in

government policy-making process in Bangladesh.

These IFAs have an interest in promoting free

market economy around the world, and develop-

ment of capital markets is one of the preconditions

for such an economy. As the accountancy profession

has a strong role to play in ensuring development of

capital markets, the IFAs have an active interest in

the activities of this profession. The World Bank, in

a number of reports (2002b, 2003), has acknowl-

edged the poor state of accounting and auditing

profession in Bangladesh, and has identified the need

for assistance in the sector. In 1999, the World Bank

advanced a US $200,000 loan to the Bangladesh

Government for the development of accounting and

auditing standards in Bangladesh. The majority of

this fund was channelled to the ICAB through the

SEC. Mir and Rahaman (2005) investigated the

international accounting standards adoption process

in Bangladesh. The paper commented that most of

the accounting standards developed by the ICAB,

and labelled as ‘Bangladesh Accounting Standards’

were actually ‘‘carbon copies of the International

Accounting Standards’’ (Mir and Rahaman, 2005,

p. 826). Drawing on institutional theory, the paper

noted that such isomorphism was prominent in

developing economies, as adoption of international

accounting standards would result in cost savings.

Also, adoption of International Accounting Stan-

dards (IAS) provides these countries, heavily depen-

dent on external assistance, with legitimacy with

their donor agencies. This is consistent with

DiMaggio and Powell (1983), who pointed out that

conformity or isomorphism is a function of external

dependence. Pfeffer and Salancik (1978) also

acknowledge that acquiescence is the most probable

response to institutional pressure when organisa-

tional dependence on the source of such pressure is

high.

The above discussion indicates the lack of self-

regulation in the accountancy profession in Bangla-

desh. Such lack of self-regulation leads to lack of

legitimacy, as the market tends to believe that the

auditors do not act in a socially acceptable manner.

According to Meyer and Rowan (1991), such

organisations would be deemed as unnecessary. To

regain such legitimacy, the ICAB then has to be seen

as acting in a manner that is acceptable to its stake-

holder groups. However, it might be noted that,

although the institute is externally dependent on

donors for funds for implementation of its projects,

the Company Law (1994) has given the members of

this profession the right to operate in a monopoly.

Therefore, although the ICAB has a severe legiti-

macy problem, for it to survive in an economy

characterised by a weak capital market and poor

demand for audited financial statements, it does not

really have to respond to legitimacy threats, as the

market would not have gone for voluntary or

higher-quality audit services anyway. So far, the

ICAB has not taken any initiative on CG, other than

holding a number of seminars for its members. This

is unusual compared with developed economies, as

accountancy and auditing bodies are considered to

be a major stakeholder group in the CG models.

Private actors: the civil society

According to Whittington (1993), regulation tends

to switch from self-regulation to private regulation.

The absence of self-regulation in Bangladeshi cor-

porate sector would then create a scope for the

development of private regulations. However, there

have not been any attempts by the professional

accountancy and business bodies in Bangladesh to

Development of Corporate Governance Regulations 265

initiate any private regulatory initiatives in CG.

Nevertheless, there are a number of civil society

think-tanks that have from time to time provided

guidance on CG in Bangladesh, the Bangladesh

Enterprise Institute (BEI) being the most prominent.

The BEI conducted the first major study on CG in

Bangladesh in 2002. The project, funded by the

DFID and the Commonwealth Secretariat, com-

pared the existing CG practices in South Asian

countries. The Bangladesh chapter of the report

reviewed the corporate and legal environments, the

state of the accounting and auditing profession,

the role of the regulatory bodies and the role of the

‘pressure’ groups (BEI, 2003). The report identified

that, due to a number of reasons, including lack of

proper knowledge, lack of proper monitoring and

lack of quality audit services, disclosures made in the

annual reports of Bangladeshi companies were, in

many cases, inaccurate and incomplete. The report

also identified the common concern of the stake-

holder groups regarding the truth and fairness of

audited financial statements (BEI, 2003, p. 24). The

report commented that government-funded regula-

tors, such as the SEC, the Bangladesh Bank and the

Registrar of Joint Stock Companies (RJSC),

remained largely ineffective due to lack of capacity

and qualified personnel. The ICAB’s role in regu-

lating the accounting and auditing profession was

referred to as ‘‘seriously called into question’’ (BEI,

2003, p. 27). The report also identified that there

was a dearth of pressure groups in Bangladesh. The

financial media lacks qualified and experienced

journalists, and there is no association or group that

joins the shareholders together.

Having identified the lack of governance in the

corporate sector in Bangladesh, and lack of legiti-

macy of the professional and regulatory bodies,

the BEI set about developing a code of CG in

Bangladesh (BEI, 2004). It is important to note that

the BEI is strictly a private-sector entity with no

statutory or regulatory power. Also, unlike the

Cadbury Code (1992) or the Combined Code

(FRC, 2003) in the UK, the BEI code has not been

adopted by any stock markets.11 Nevertheless, the

BEI code is the first comprehensive set of CG

guidelines in Bangladesh. Surprisingly, even though

the BEI is an independent private-sector body, the

BEI’s taskforce on CG included members from the

Bangladesh Government and other important regu-

latory agencies, including the Chairman of the SEC.

Like BEI (2003), the CG codes were also developed

by BEI under a project funded by the DFID and the

Commonwealth Secretariat. Consistent with CG

codes in other parts of the world [for example, the

OECD guidelines (1999) and the Combined Code

(2003) in the UK], the BEI CG code (2004)

incorporated notions of independent directors on

the board, separation of the chairman and the CEO

and the formulation of audit committees. It is

mentioned that the BEI code was developed in

consultation with the OECD code of CG (1999).

The BEI code is discussed in detail in a later section

of this paper.

Once the CG code was developed, BEI then

undertook another project to strengthen CG prac-

tices in Bangladesh. The objective of this project was

to ‘‘inject CG practices as a microeconomic policy

instrument to complement other microeconomic

policy instruments and macro-economic reform

policies, particularly financial sector reform’’.12

Under this project, the BEI has been regularly

organising CG training and awareness programmes

in different private, public and professional institu-

tions. The project is funded by The Netherlands

embassy in Bangladesh, and the Commonwealth

Secretariat.

The above discussion indicates that, in the absence

of private-sector regulatory bodies in Bangladesh,

think-tanks such as BEI have made significant con-

tributions in the development of CG guidelines. In a

recent speech, the BEI chief claimed that the BEI has

‘‘acted as a catalyst in the development of CG in

Bangladesh’’ (ICGN, 2006). It may be noted that all

the BEI CG initiatives, including the CG code, have

been funded by different donor agencies. The BEI has

no source of revenue of its own, and is financially

dependent on these projects. This is different from

private-sector regulatory initiatives in other coun-

tries.13 The resource dependence of the BEI on dif-

ferent aid agencies may be seen as providing scope for

different donor agencies to influence the BEI’s policy

making and research. As BEI has demonstrated that it

has significant influence on government-level policy

making, the donors might use such organisations as

‘catalysts’ to pass on policies to the Government.14

Also, the donor-funded BEI CG awareness pro-

grammes would also make such policies more

acceptable to the private and public sectors.

266 Javed Siddiqui

Government regulators: the Securities and Exchange

Commission

The primary government regulator in the Bangla-

desh CG scenario is the Securities and Exchange

Commission of Bangladesh (SEC). Established in

1993, the SEC’s objective is to ‘‘protect the inves-

tors, promote and develop capital markets in Ban-

gladesh, and regulate the securities market’’ (Hossain

et al., 2005). The SEC is funded by the government,

and its chairman and three members in the board are

also recruited by the government.

In 1996, the Bangladeshi capital market went

through a major turmoil. Between July and

November, the all share price index in Dhaka Stock

Exchange (DSE) went up by 265%. The relatively

inexperienced Bangladeshi investors rushed to the

market. However, such rise was short lived, as the

index went down from 3648 in November 1 to 486

points in April (SEC, 1997). Investigations later

revealed a scam involving a group of investors.

Association of members of SEC and DSE were also

reported (The Daily Star, 1999). The stock market

crash resulted in huge lack of confidence, and for

years investors stayed away from investing in the

capital market (BEI, 2003). This is consistent with

Ozcan and Cokgezen (2003), who report that cap-

ital market failures in emerging economies often

have long-term destabilising effects with wide-

spread painful outcomes. Solaiman (2006) recently

reviewed the development of capital markets in

Bangladesh. On the 1996 stock market crash, the

paper commented:

The disaster came as a blow to investors and regulators

alike. The government became more concerned about

the market, which prompted the authorities to bring

about further reforms in securities regulation. (Solai-

man, 2006, p. 203)

Immediately after the stock market turmoil, the

government undertook a number of reform pro-

grammes to restore investors’ confidence. The SEC

went through a number of major changes: it was

entrusted as the final rule-making authority for

capital markets; its organogram was revised to

incorporate two new members; considerable staff

was recruited; and a new investors’ education pro-

gramme was introduced. However, despite such

measures, the SEC still suffers from lack of highly

skilled professionals, as noted by the BEI report

(2003):

The Corporate Accounts does not have the capacity to

review the half-yearly accounts of the listed compa-

nies. The SEC, like other regulators dealing with

corporate accounts, has to depend to a large extent on

the performance of the auditors of these companies, of

which much has been said elsewhere in the report.

Likewise, the Commission does not have a full time

corporate lawyer on board. The surveillance and

investigations units are also not adequately staffed or

trained. Therefore, the quality of the monitoring

activities of the SEC remains open to question. (BEI,

2003, p. 57)

In 1999, the Asian Development Bank (ADB)

initiated a US $1.07 million project to strengthen

the capacity of SEC so that it can perform its reg-

ulatory functions. The ADB, in its technical assis-

tance report to the Government of Bangladesh

(ADB, 2000), mentioned that the stock market had

not recovered from the 1996 crash, and that good

CG by the companies listed in the stock exchanges

was essential. The purpose of the ADB technical

assistance was to ‘‘develop a CG structure needed to

build confidence and trust of the public and share-

holders’’ (ADB, 2000). Under the project, the ADB

aimed to develop a CG manual that would be dis-

tributed at the workshops and training sessions

conducted by the SEC. Also, members of the SEC,

DSE, CSE, and ICAB would be provided training

regarding CG. However, although the project

completed in 2002, the CG manual was not devel-

oped. Nevertheless, under the project, members of

the SEC staff were provided training regarding CG,

which helped the SEC to finally come up with a CG

order in 2006 (SEC, 2006). Compared with the BEI

code, the SEC order is much more specific in terms

of contents, and does not offer detailed explanation

of the rules.

The above section discussed the role of different

actors in the Bangladesh CG scenario. The discus-

sion indicates that international financing bodies

exercise significant levels of influence on all the

actors involved in the CG scenario in Bangladesh.

The next section will present a comparison between

different CG initiatives in Bangladesh.

Development of Corporate Governance Regulations 267

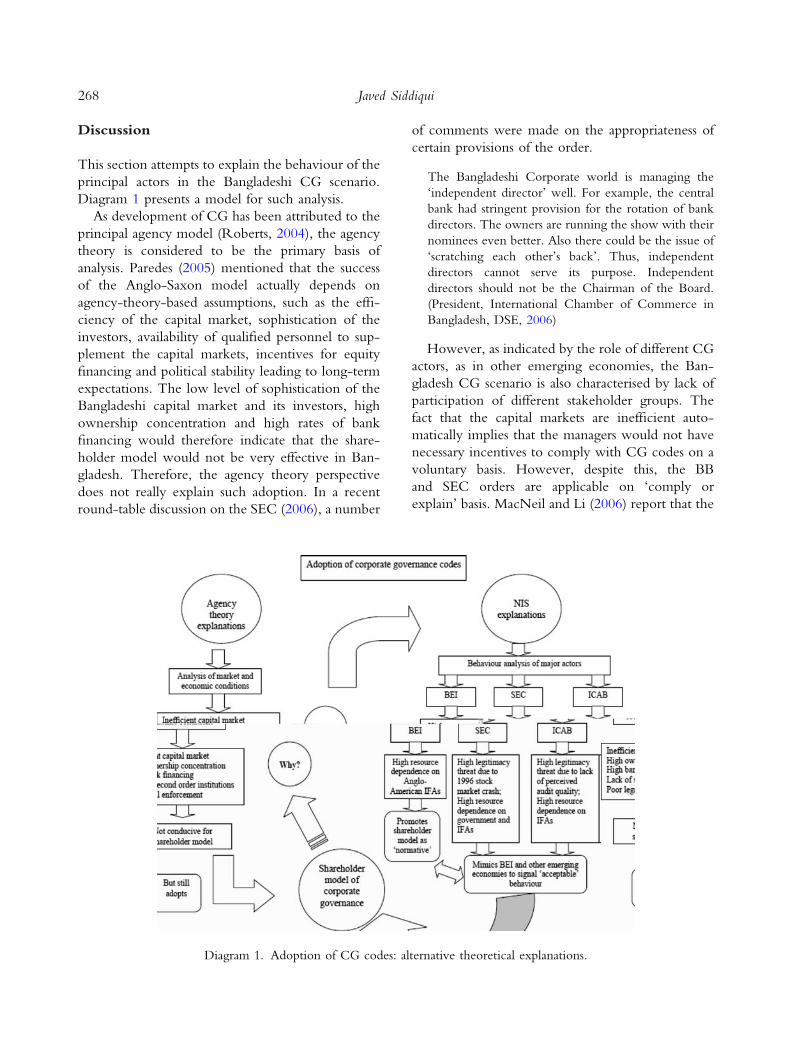

Discussion

This section attempts to explain the behaviour of the

principal actors in the Bangladeshi CG scenario.

Diagram 1 presents a model for such analysis.

As development of CG has been attributed to the

principal agency model (Roberts, 2004), the agency

theory is considered to be the primary basis of

analysis. Paredes (2005) mentioned that the success

of the Anglo-Saxon model actually depends on

agency-theory-based assumptions, such as the effi-

ciency of the capital market, sophistication of the

investors, availability of qualified personnel to sup-

plement the capital markets, incentives for equity

financing and political stability leading to long-term

expectations. The low level of sophistication of the

Bangladeshi capital market and its investors, high

ownership concentration and high rates of bank

financing would therefore indicate that the share-

holder model would not be very effective in Ban-

gladesh. Therefore, the agency theory perspective

does not really explain such adoption. In a recent

round-table discussion on the SEC (2006), a number

of comments were made on the appropriateness of

certain provisions of the order.

The Bangladeshi Corporate world is managing the

‘independent director’ well. For example, the central

bank had stringent provision for the rotation of bank

directors. The owners are running the show with their

nominees even better. Also there could be the issue of

‘scratching each other’s back’. Thus, independent

directors cannot serve its purpose. Independent

directors should not be the Chairman of the Board.

(President, International Chamber of Commerce in

Bangladesh, DSE, 2006)

However, as indicated by the role of different CG

actors, as in other emerging economies, the Ban-

gladesh CG scenario is also characterised by lack of

participation of different stakeholder groups. The

fact that the capital markets are inefficient auto-

matically implies that the managers would not have

necessary incentives to comply with CG codes on a

voluntary basis. However, despite this, the BB

and SEC orders are applicable on ‘comply or

explain’ basis. MacNeil and Li (2006) report that the

Diagram 1. Adoption of CG codes: alternative theoretical explanations.

268 Javed Siddiqui

application of CG codes on ‘comply or explain’ basis

is ineffective even in developed economies. Also, the

lack of participation of different stakeholder groups

in the preparation of CG codes has resulted in the

lack of corporate social reporting in Bangladesh

(Belal and Owen, 2007), and even the ICAB has

failed to protect its own interest (as evidenced by a

suggested ban on NAS). Another discussant in the

DSE round-table discussion (2006) summed up the

inappropriateness of the CG codes in Bangladesh.

The CG practices we are discussing were developed in

OECD countries. These might not be applicable in

our country because of the difference in culture and

value system. (former vice president, ICAB, DSE,

2006)

Therefore, it is apparent that the agency theory is

not sufficient in explaining the adoption of the Anglo-

American model of CG in Bangladesh. Diagram 1

then explores whether NIS can be used as a theoretical

basis for such behaviour. From the institutional per-

spective, it may be worth noting that, although the

professional and regulatory bodies suffer from prob-

lems of legitimacy, their exposure to threats of legiti-

macy may have been different. The accountancy body,

the ICAB, has severe problems of legitimacy, arising

from public perceptions of lack of independence. This

may have resulted in lower audit fees as clients are not

willing to pay more for poor quality audit work.

Nevertheless, the Company Law (1994) still ensures

that public limited companies must have their financial

statements audited by members of the ICAB. This

grants the ICAB a right to operate in a monopoly.

As the ICAB enjoys a superior lobbying power com-

pared with the other accountancy body, the Institute

of Cost and Management Accountants of Bangladesh

(ICMAB) (see Mir and Rahaman, 2005), ensures that,

although it is reluctant to self-regulate its members, its

self-regulatory power will not be challenged by any

other professional bodies. This, coupled with the poor

demand for audited financial information, probably acts

as an incentive for the ICAB not to regulate its mem-

bers. Therefore, although the organisation has severe

problems of legitimacy, its legitimacy threat is low, as

the professional body has been granted a monopoly and

does not necessarily have to be seen to be acting in a

socially acceptable manner to earn revenues.

The regulatory body, the SEC in this case, is

financially dependent on the government. Also, the

top posts are filled by the government. Therefore,

the government exercises a significant influence on

this body. The 1996 stock market collapse created

sever problems of legitimacy for the SEC, and it has

not recovered from such problems of legitimacy so

far. However, although the legitimacy problems for

the ICAB and the SEC may be similar, their expo-

sure to legitimacy threats is different. Whereas the

ICAB does not have to depend on public perception

and confidence for its earning, the SEC, financed by

the Government of Bangladesh, has to face a dif-

ferent scenario. The Government of Bangladesh

heavily relies on overseas assistance, and donors tie

up such assistance with different development goals.

One such development goal is the promotion of

capital markets as a means for ensuring a free market

economy. Therefore, the Government of Bangla-

desh, the SEC’s financiers, would be keen to restore

their legitimacy with the IFAs by proving that they

are behaving in an acceptable manner. This is con-

sistent with Seal (2006), who mentions that CG

reforms are considered to be collectively sanctioned

norms that organisations are expected to comply

with. Thus, the adoption of the apparently successful

shareholder model may provide the SEC, and the

Government of Bangladesh, with its much-needed

legitimacy which will ensure continued support of

the financing agencies. As the SEC, a new organi-

sation with a reputation for failure (for the 1996