development proposal of 9 st marys street, …

TRANSCRIPT

DEVELOPMENT PROPOSAL OF

9 ST MARYS STREET, ANNAPOLIS MARYLAND

by

Jonathan Bullock

A practicum thesis submitted to Johns Hopkins University in conformity with

the requirements for the degree of Master of Science in Real Estate

Baltimore, Maryland

August, 2010

(notice of copyright is optional)

© 2010 Jonathan Bullock

All Rights Reserved

2

Table of Contents

Executive Summary ........................................................................................................................ 4

Market Analysis ............................................................................................................................... 5

Annapolis Overview ................................................................................................................... 6

Demographics ............................................................................................................................. 7

Employment ................................................................................................................................ 8

Site Analysis..................................................................................................................................... 8

Land Use Regulation ................................................................................................................ 10

Historic District ......................................................................................................................... 11

Building Design ............................................................................................................................. 12

Development Budget ................................................................................................................. 13

Debt Financing........................................................................................................................... 15

Feasibility and Valuation Analysis ................................................................................................ 16

Multi-Family Apartment ........................................................................................................... 17

Office ........................................................................................................................................ 19

Retail ......................................................................................................................................... 22

Mix Use: Retail & Office .......................................................................................................... 24

Feasibility & Valuation Summary ............................................................................................ 27

Mixed-Use Development Plan ....................................................................................................... 28

Ground Floor Retail .................................................................................................................. 28

Offices Suites ............................................................................................................................. 32

Entitlements ............................................................................................................................... 33

Mixed-Use Financial Analysis ...................................................................................................... 35

3

Development Budget ................................................................................................................ 36

Debt Financing .......................................................................................................................... 36

Construction Loan ................................................................................................................ 37

Permanent Loan ................................................................................................................... 38

Initial Equity Requirements & Returns ..................................................................................... 38

Rehabilitation Tax Credit .......................................................................................................... 39

Ground Lease ............................................................................................................................ 40

Profitability Analysis ................................................................................................................. 42

Equity Distribution .................................................................................................................... 43

Sensitivity Analysis ................................................................................................................... 44

Development Schedule................................................................................................................... 45

Conclusion...................................................................................................................................... 47

References ..................................................................................................................................... 48

Appendices .................................................................................................................................... 51

4

Executive Summary:

This proposal analyzes and supports the valuation, feasibility, and development opportunity of

9 St. Marys Street, located in Annapolis Maryland. The proposal begins with a broad market

analysis that identifies the prominent trends and drivers that exist in the Annapolis market area.

Next the analysis will drill down on the subject site through a site analysis followed by an

overview of the land use regulation and the associated challenges that encumber the property.

Incorporating the indentified zoning limitations, the proposed site and building design will then

be evaluated followed by the establishment of the proposed development budget.

The second part of the analysis derives the highest and best use for the site through a detailed

valuation of apartments, office, retail, and a mixed-use product with ground floor retail and

second floor office suites. Current market information was utilized from market reports and

comparable properties in the area and modeled using Argus DCF Valuation. James Graaskamps

single financial feasibility analysis will then be used to derive the use that yields the highest

supported property value.

The final section will entail a detailed analysis of the proposed end use, identifying the targeted

market the use looks to fill, followed by a comprehensive analysis of the various challenges as

well as feasible solutions to mitigate the risks. A detailed financial analysis will then test various

debt and equity structures providing viable alternative solutions including ground leases,

incorporation of rehabilitation tax credits, and the benefit of pursuing a public-private partnership

with the city. The end product will portray a distinctive sense of place that will compliment the

surrounding uses and act as a catalyst in pursuing the city’s goals of rebranding the city dock

5

area1. The space will offer unique features that accentuate the architectural craftsmanship that

inspired the design.

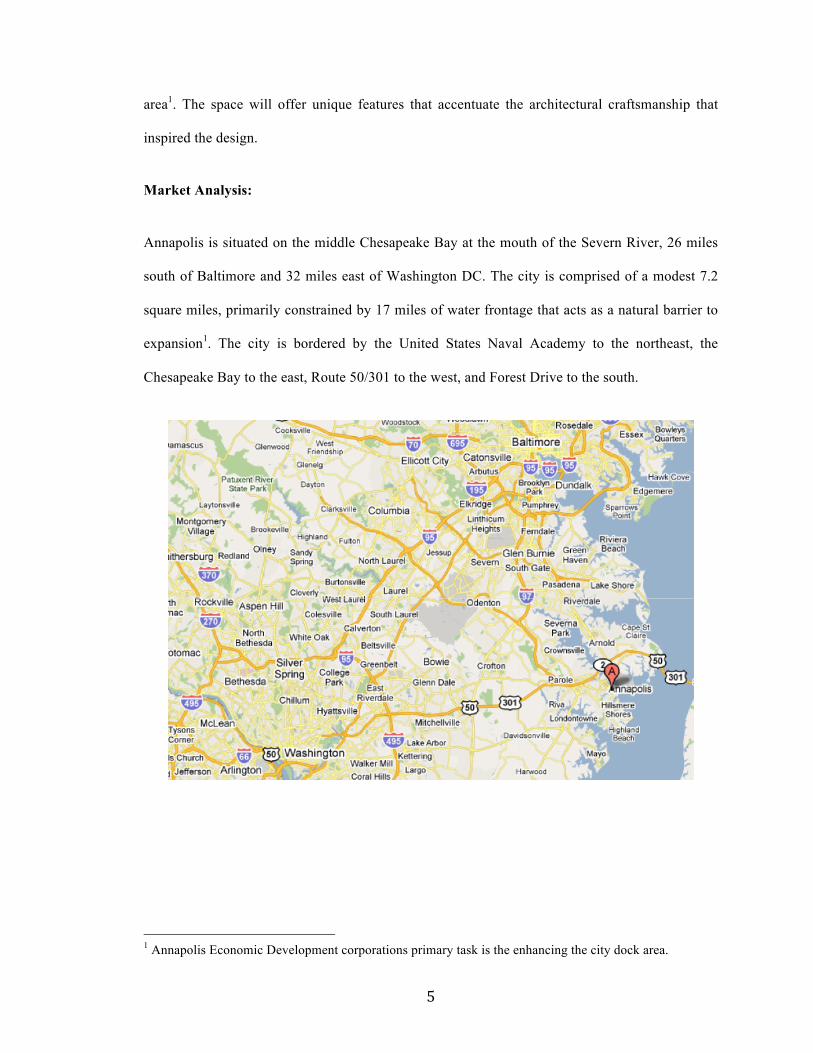

Market Analysis:

Annapolis is situated on the middle Chesapeake Bay at the mouth of the Severn River, 26 miles

south of Baltimore and 32 miles east of Washington DC. The city is comprised of a modest 7.2

square miles, primarily constrained by 17 miles of water frontage that acts as a natural barrier to

expansion1. The city is bordered by the United States Naval Academy to the northeast, the

Chesapeake Bay to the east, Route 50/301 to the west, and Forest Drive to the south.

1 Annapolis Economic Development corporations primary task is the enhancing the city dock area.

6

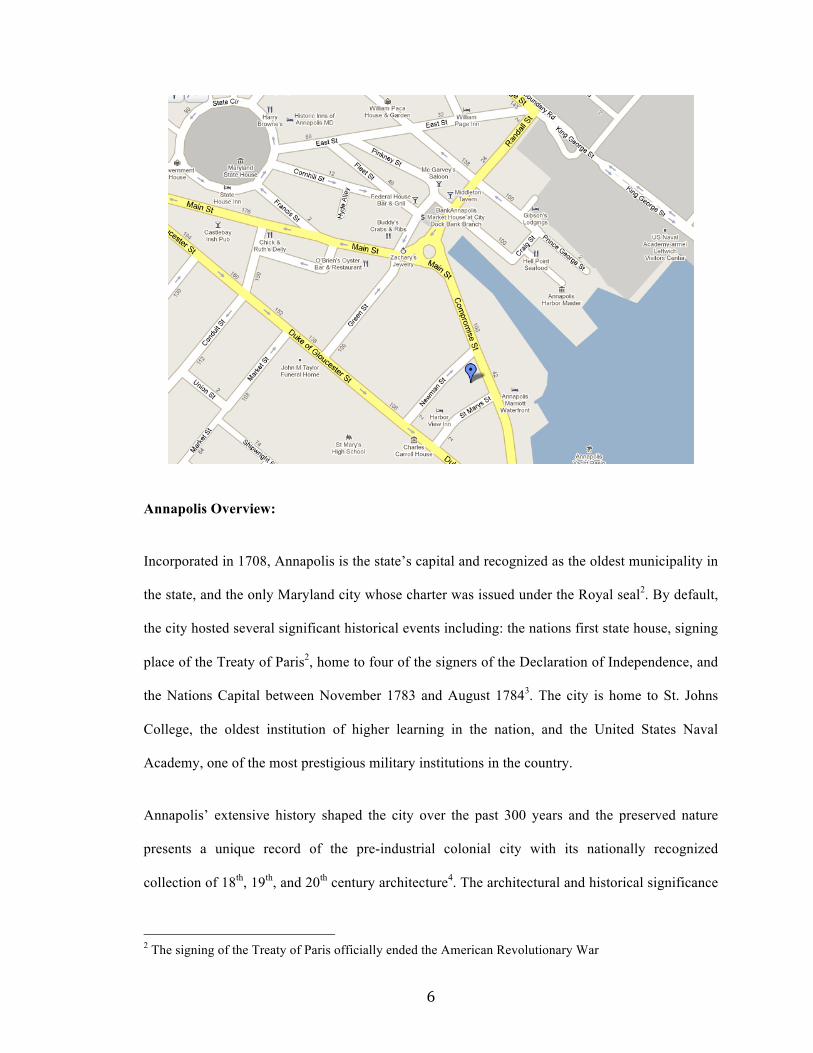

Annapolis Overview:

Incorporated in 1708, Annapolis is the state’s capital and recognized as the oldest municipality in

the state, and the only Maryland city whose charter was issued under the Royal seal2. By default,

the city hosted several significant historical events including: the nations first state house, signing

place of the Treaty of Paris2, home to four of the signers of the Declaration of Independence, and

the Nations Capital between November 1783 and August 17843. The city is home to St. Johns

College, the oldest institution of higher learning in the nation, and the United States Naval

Academy, one of the most prestigious military institutions in the country.

Annapolis’ extensive history shaped the city over the past 300 years and the preserved nature

presents a unique record of the pre-industrial colonial city with its nationally recognized

collection of 18th, 19th, and 20th century architecture4. The architectural and historical significance

2 The signing of the Treaty of Paris officially ended the American Revolutionary War

7

led to its designation as a National and Historic Landmark District in 19655. Additionally,

Annapolis’ Main Street was designated by the state’s Main Street Maryland Program, one that

selects communities that have committed to improve economy, appearance, and image of

traditional downtown business districts. In 2008, the American Planning Association named

Annapolis’ Main Street as one of the Ten Great Streets in America6. With such deep historical

roots, the ongoing preservation of a national treasure is essential to ensure the character of the

city is passed on to future generations and will prove to play a significant role in structuring this

proposal.

Demographics:

The 2000 census provided that Annapolis consisted of 35,838 residents, not including the

approximated 4,300 Naval Academy residents or the estimated 700 student that attend St. Johns

College. Policy Map estimated population of 36,711 as of 2009 and projects 37,222 residents in

2014, resulting in an estimated 1.39% growth rate. The population correlates into a total of

15,888 households bearing an average household size of 2.277, excluding the Naval Academy and

St Johns College residents. The estimated age distribution as of 2009 provided 13% over 65 years

of age, 63% between 18 and 64, 23% under 18, and 7% under 5 years of age8. The city’s median

household income as of 2008 was $72,173, 2.4% above the state’ median income of $70,482 and

38% above the national average of $52,1759.

Employment:

The presence of the state capital and Anne Arundel County seat provides a strong contingency of

government employees. Additionally, the city’s estimated 4.5 million visitors annually translates

into employment demand in the tourism and maritime industries10. A 2009 Claritas estimate

8

provides that the top five employment centers represents 53% of the employment in the City, and

include:

1) Health Care and Social Assistance 11.26%

2) Educational Service 11.19%

3) Retail Trade 10.72%

4) Accommodation and Food Service 9.94%

5) Professional, Scientific, & Technical Services 9.89%

The relatively educated population with 38.7% of citizens holding a bachelor’s degree or higher,

compares favorably to the state’s average of 31.4% and the nation’s average of 24.4%. As a result

of the presence of the Government and educated population, Annapolis faired the recent

economic recession relatively well yielding an unemployment rate of 6.2% in May 2010

compared to the state’s 7%.

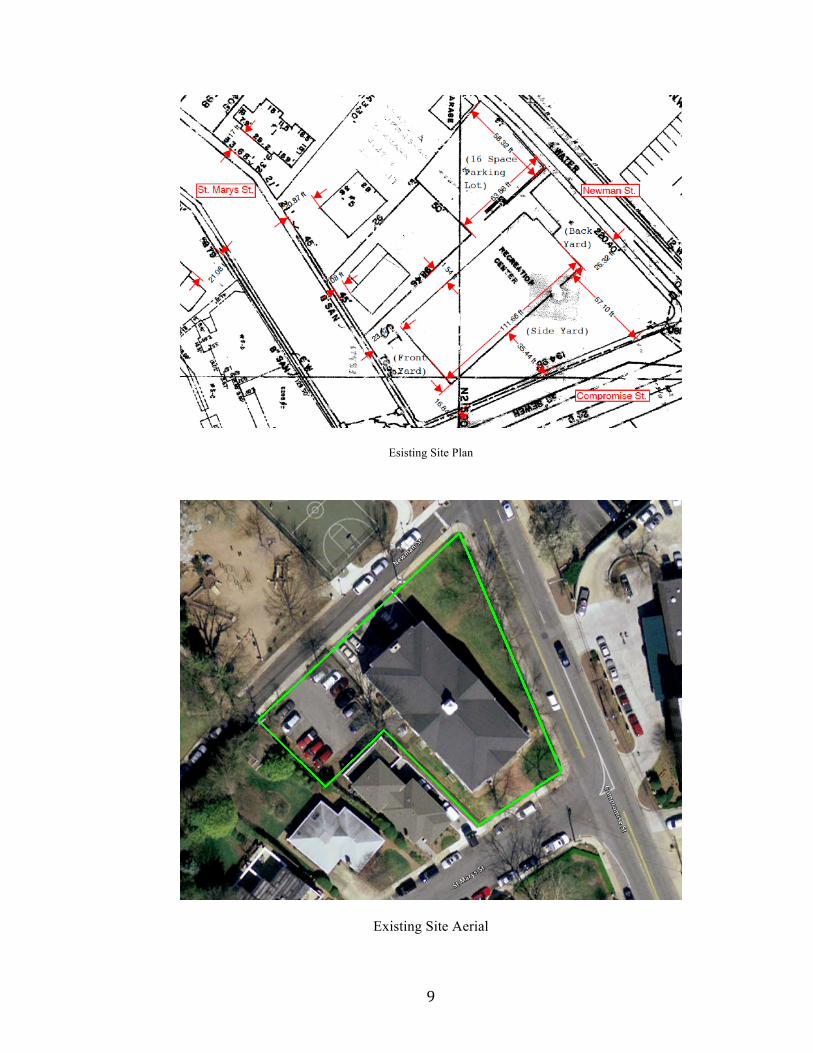

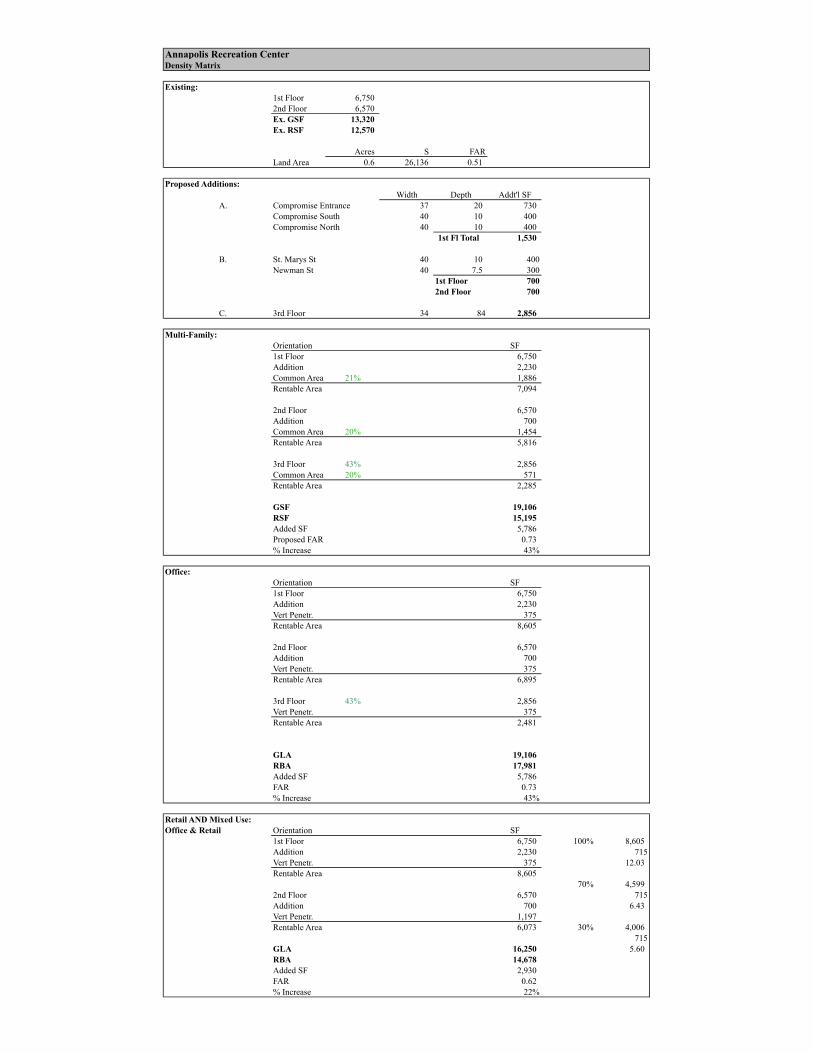

Site Analysis:

The site consists of 0.6 acres bordered by St. Marys Street to the south, Compromise Street to the

east, Newman Street to the north, and historic residential single-family dwellings to the west. A

small 16-space parking lot is located in the northwest west property corner with an additional 6-

spaces along the north side of the building.

9

Esisting Site Plan

Existing Site Aerial

10

The existing 13,320 SF structure was built in 1942 as a United Services Organization (USO),

used to bridge the social gap between enlisted soldiers and the general public. Over time, the

demand for the Annapolis USO subsided, and the US Government deemed the site obsolete in

1976 when the deed was transferred fee simple, to the City of Annapolis for a sum of $1.00.

The City of Annapolis converted the two story brick building into a recreation center for the

benefit of Annapolis residents. The first floor contains low 8-foot ceilings3 and is divided into

various meeting and activity rooms, while the second floor consists of a basketball court with 19-

foot vaulted ceilings that run the length of the building. The site remained the city’s primary

recreation center for over 30 years, accumulating numerous stories of note, including the former

Annapolis Mayor Roger “Pip” Moyers role as the basketball coach.

As the community grew, the demand for recreational facilities outgrew the potential of the

downtown center. As a result, the city commissioned the construction of a larger center, with a

wider range of services. In the spring of 2010, the 80,000 SF Roger “Pip” Moyer Community

Recreation Center was opened, deeming the downtown site obsolete.

Land Use Regulation Overview:

The city’s zoning is based on Euclidean zones, where parcels are designated specific permitted

uses to ensure compatibility among neighboring properties. Euclidean zones also enable planners

to ‘guide’ future development by implementing growth initiatives into the comprehensive plan.

The city’s current comprehensive plan was adopted in October 2009 and provides valuable

insight into the city’s goals over the next 10 years. The plan is designed around three primary

principles: 1) preserving and enhancing community character, 2) maintaining a vibrant economy,

and 3) promoting ‘green’ Annapolis11.

3 Renovations in mid 1990’s reduced first floor ceilings to add stability to second floor court. Proposed plan would revert first floor to 9-foot ceilings.

11

The site is currently zoned C-1 or Conservation Residential with the goal of encouraging the

conservation of educational, cultural, and the historical character of the old city12. The uses

permitted by-right in the C-1 zone include public and private schools, single family homes,

museums, art galleries, and religious institutions. Uses subject to special exception approval

expand the options to include multi-family apartments consisting of more than six units. In order

to conform with the retail, office, and mixed use options, rezoning will be required to either C2

Conservation Business, or C2A Special Conservation Business.

Rezoning in a Euclidean zone requires the applicant to prove the property meets the change or

mistake rule. A ‘change’ means the character of the neighborhood has changed significantly since

the last comprehensive plan to justify a change in zoning. A case could be made in favor of the

subject parcel providing that a change has occurred in the immediate neighborhood since the

building was vacated. The ‘mistake’ aspect relates to parcels that were improperly zoned based

on surrounding uses. One could argue that the 2009 comprehensive plan’s proposed

“recreational” use for the site subject mistakenly depicts the best use of the property.

Historic District:

In addition to the potential requirement for rezoning, the city’s historical significance is protected

by a historic overlay. The overlay takes precedence over the regulations dictated in the general

zoning code, essentially requiring the applicant to conform to two sets of parameters. Although

the 1942 structure is not itself considered historic, “it is a contributing resource to the Annapolis

National Register Historic District and therefore undertakings are in accordance with the Historic

Preservation Commission Design Guidelines, strict interpretation”13. As a result, the permitted

density in the C1 zone of 2.0 FAR, is overridden by the overlay restricting the structure from being

razed and further providing that additions must not change the historic context of the structure.

12

The Historic Preservation Commissions Design Guidelines are based on four primary preservation

goals: 1) preserving and enhancing the city’s historic urban form, 2) preserving and enhancing

individual historic streetscapes, 3) facilitating compatible landscape and site design, and 4)

preserving and protecting historic buildings, materials, and elements14. The ordinance encourages

respectable contemporary design that follows the design principles of existing neighboring

buildings, and respects the scale, proportions, order, rhythms, and materials of the prevailing

historic context15. Perhaps most applicable to this proposal, the guidelines require that new

building or addition ‘visually relate’ to the contributing historic buildings in its immediate

neighborhood rather than buildings in the historic district in general16. Such highly defined design

standards will warrant the consultation of local architects that possess high success rates with

similar projects. Allocating additional funds to secure a highly regarded local architect will assist

in mitigating the entitlement risk, while also providing a feasible final design that maximizes

density and streamlines the historical review and permitting processes.

Building Design:

The proposed building design will take a conservative approach to ensure compliance with the

historic overlay and general zoning code. Site constraints resulting from the non-symmetrical lot

size, required setbacks, presence existing trees protected by the Historic Preservation Commission,

and the buildings orientation towards the western of the property line, all played a role in

determining permitted density. As a result, the proposal models three modest additions with the

goal of maximizing density while preserving and balancing the building from an aesthetic point

of view.

The first proposed addition will reflect a seven-foot extension to the existing gable portrayed on

the north side of the structure. The south side will mirror the two-story addition, balancing the

13

structure and resulting in a combined total of approximately 1,400 SF4. The impact on the interior

will allow common elements to be concentrated towards the north and south sides of the building,

dedicating the buildings core to the specified end use. The second proposed addition runs the

length of the Compromise Street side of the building with the intent of complimenting the

Georgian architecture, while also softening the institutional characteristics. The first component

portrays the proposed main entrance, accomplished by extending the existing gable twenty feet.

To either side, ten-foot extensions, limited to one-story5 will run the remaining length of the

structure. The ten-foot depth was limited as a result of the narrow lot conditions on the southeast

property corner, and the proximity of existing trees. The second proposed addition results in an

additional 1,600 rentable square feet to the first floor6, while drastically improving the buildings

curb appeal. From an ingress and egress point of view, the entrance on Compromise Street

provides users with an additional access point providing improved circulation throughout the

building. The proposed entrance will also minimize traffic to the current main entrance on St.

Marys Street, comprised of historic single-family homes. The proposed additions are considered

to be within the limitations dictated under the historic preservation guidelines as well as the city’s

zoning regulation. As a result, the existing 13,320 GSF structure will be increased by 22% to

16,250 GSF, reflecting an increased FAR of 0.62 versus the existing 0.51. Details of calculations

are provided in Appendix A.

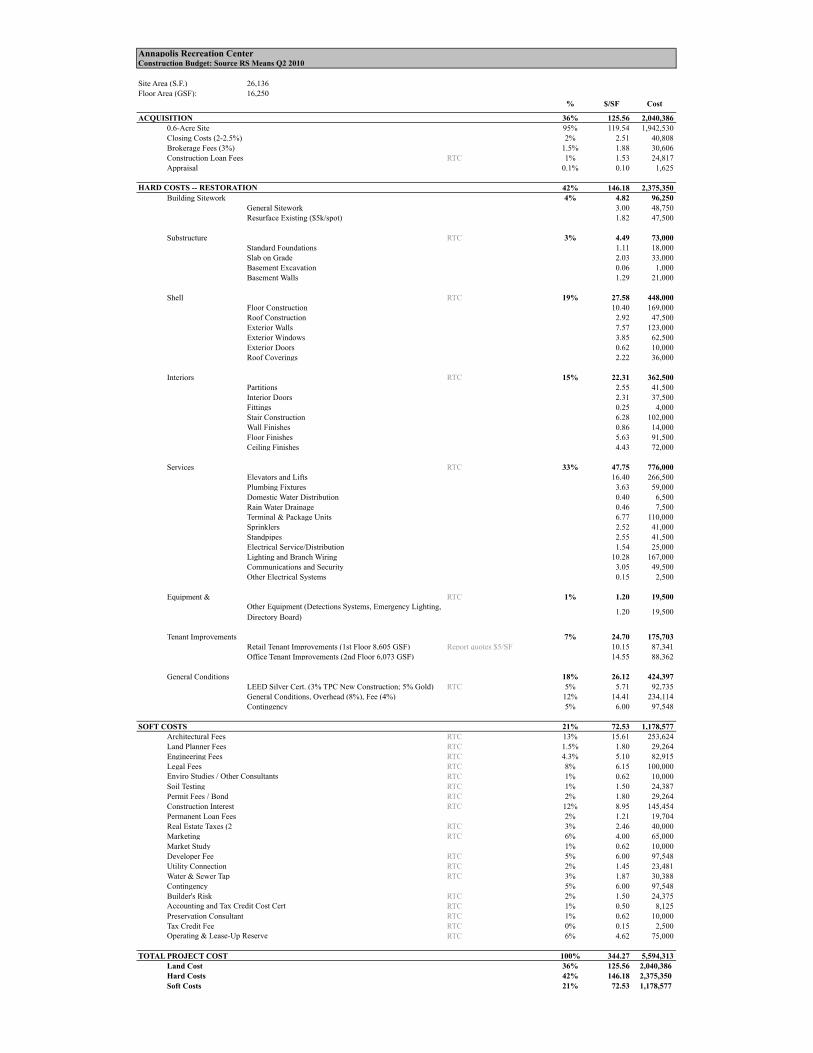

Development Budget:

The extent of the renovation work required to deliver the proposed end product has been derived

from take-offs of plans provided by the city, conversations with a city engineers, and a thorough

inspection of the structures exterior. Repeated requests to gain access to the building interior were

4 Range of increased PGI between $28,680 (Apt) and $46,774 (Mix-Use). 5 Original proposal to the city portrayed a two-story addition running the length of the east side. Upon review by the Historic Preservation Commission concern was raised regarding proposed additions impact in altering the buildings historical context. 6 Range of increased PGI between $32,436 (Apt) and $51,117 (Mix-Use)

14

denied by the mayor’s office. As a result, the renovation work of the existing 13,320 SF structure

has been modeled to reflect the associated construction risk and has been based on modified new

construction figures of $143 per SF17, while proposed additions will be based on $100 per SF. To

better gauge the accuracy, conversations with John Fitzgerald, Regional Director of Development

for Archon Group, provided a hard cost estimate of $100 per SF for renovations while David

Smith, Development Manager for Forest City Enterprises, estimated base building costs of $135

per SF for adaptive reuse projects.

Hard cost line items of note include a 5% allocation of the total project costs to achieve LEED

Existing Building certification, keeping in line with the comprehensive plans goal of creating a

‘green’ environment. Additional hard costs include a general conditions budget of 12%

accounting for overhead and the general contractors. A 5% contingency of hard costs acts as an

additional buffer for potential cost overruns.

Soft costs were derived from research and conversations with various industry professionals, and

resulted in an estimated $73 per SF. Line items of note include a 13% architectural fee,

corresponding with the typical range from 5-16% of total hard costs18. The premium accounts for

the anticipated elevated level of involvement required to conform with the restriction set forth in

the historic overlay zone. Engineering fees of 4.25% were averaged based on the typical range of

2.5-6% for new projects19. Similar to architectural fees, the allocation provides for the additional

services required to achieve the proposed design. Accounting for the anticipated level of

involvement with the entitlements process, conversations with Ben Wechsler20 resulted in a

$30,000 line item for a land planner. Mr. Wechsler’s expectation of local opposition in response

to the rezoning process resulted in an estimated legal fees line item of $100,000. Construction

interest was derived from the construction draw scheduled detailed in Appendix G and was based

on 6.5% interest only loan over an 18-months construction period. Real estate taxes are currently

assessed at $0.635 per $100 of the assessed value resulting in an annual tax approximately

15

$20,000. Upon endorsement by the city, lenders, and equity investors, a formal market study will

be commissioned to support of the intended use accounting for a $10,000 allocation. Lastly, a 5%

developer fee has been applied to compensate for the complexity and risk of delivering the

project.

Acquisition costs will vary based on the derived value detailed in the following section, however

the associated costs are based on constant percentages and costs per square foot. Anticipated costs

include an allocation of 2% of the land cost for closing costs, brokerage fees of 1.5%,

construction loan fees of 1%, permanent loan fees of 75bps, and an appraisal quoted at $0.10 per

SF.

Debt Financing:

Debt assumptions were provided by Sandy Spring Bank21 and represent the current environment

of the capital market. The quoted terms were based on the proposed sites details, including the

projects financials and development budget. The funding limitations are based on four primary

constraints: loan-to-value, loan-to-cost, debt service coverage ratio, and equity requirements.

Sandy Spring Bank provided that current underwriting criteria derives funding limitations based

on the least of the following:

• Maximum LTV range: 60-75%

• Maximum LTC range: 75-85%

• Minimum DCR range: 1.25-1.35

• Minimum Equity Requirement: 20% (other banks range from 10-20%)

For the purposes of this proposal we will assume a maximum loan-to-value of 65%, maximum

loan-to-cost of 80%, a minimum debt coverage ratio of 1.25, and a minimum equity requirement

of 20%.

16

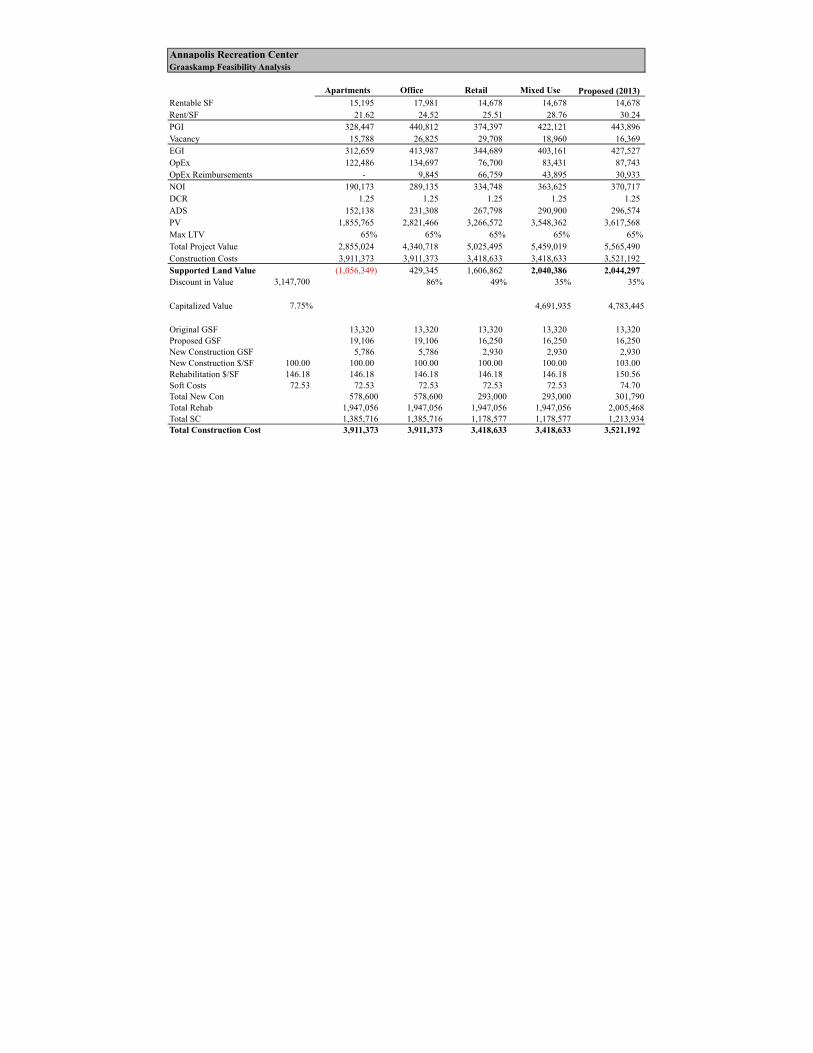

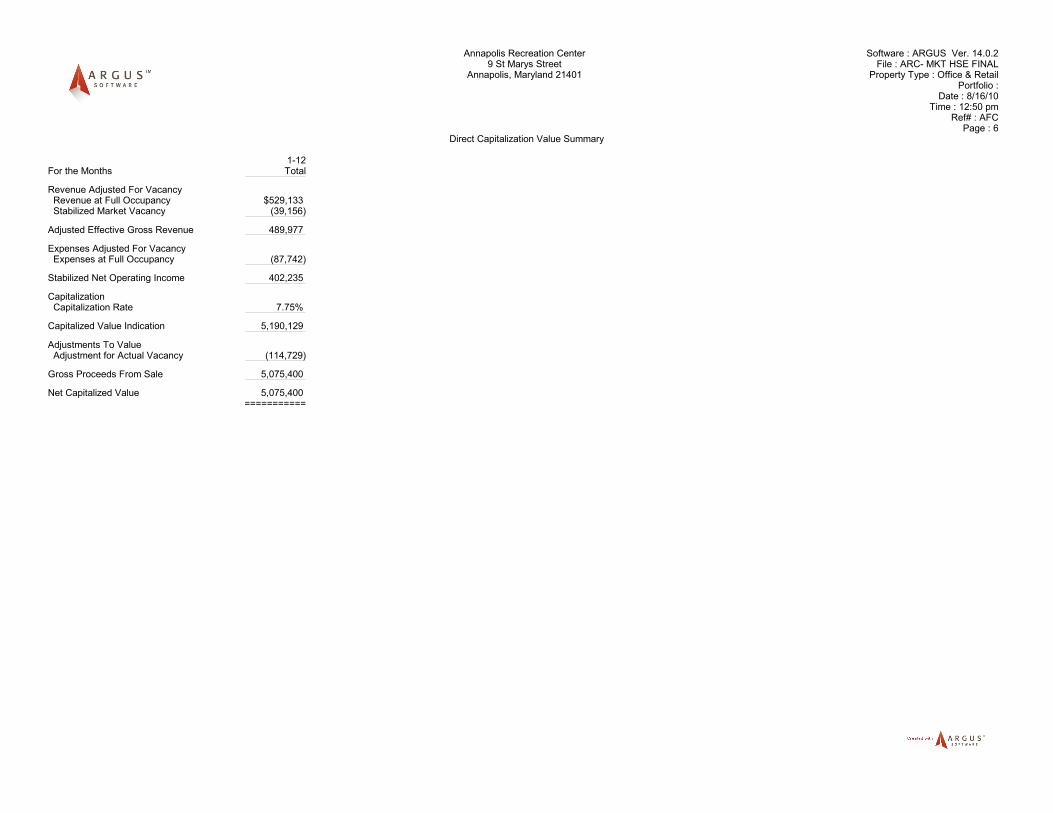

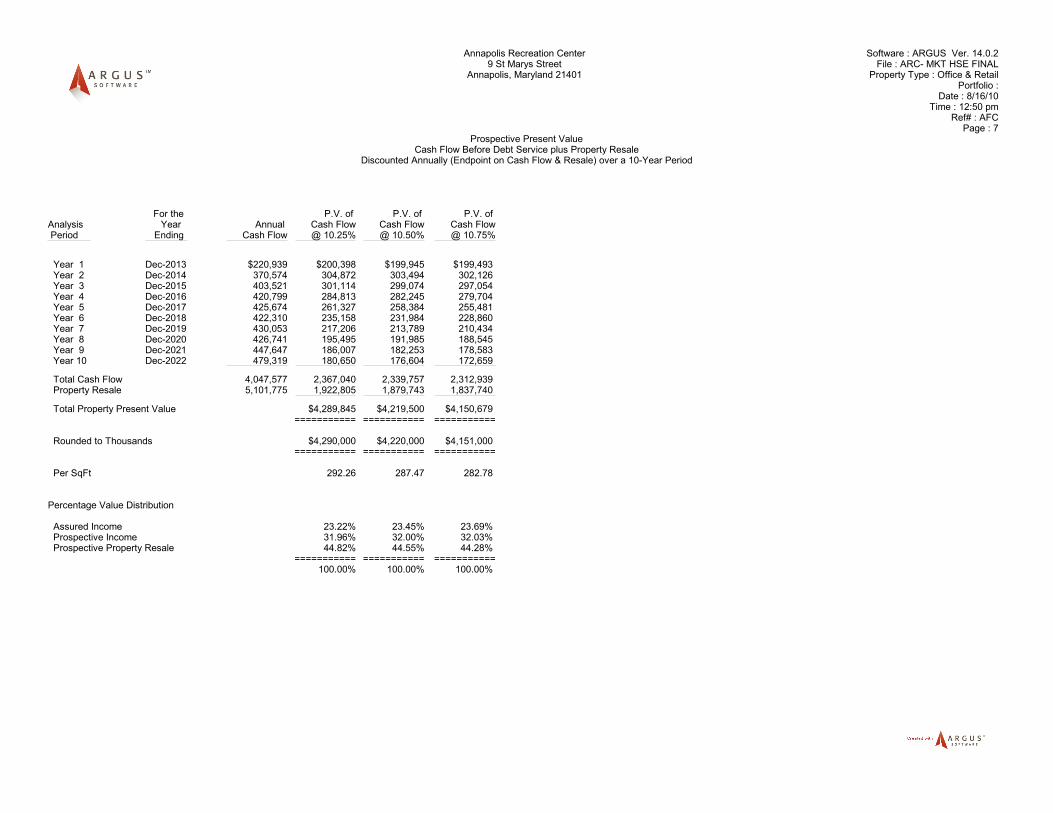

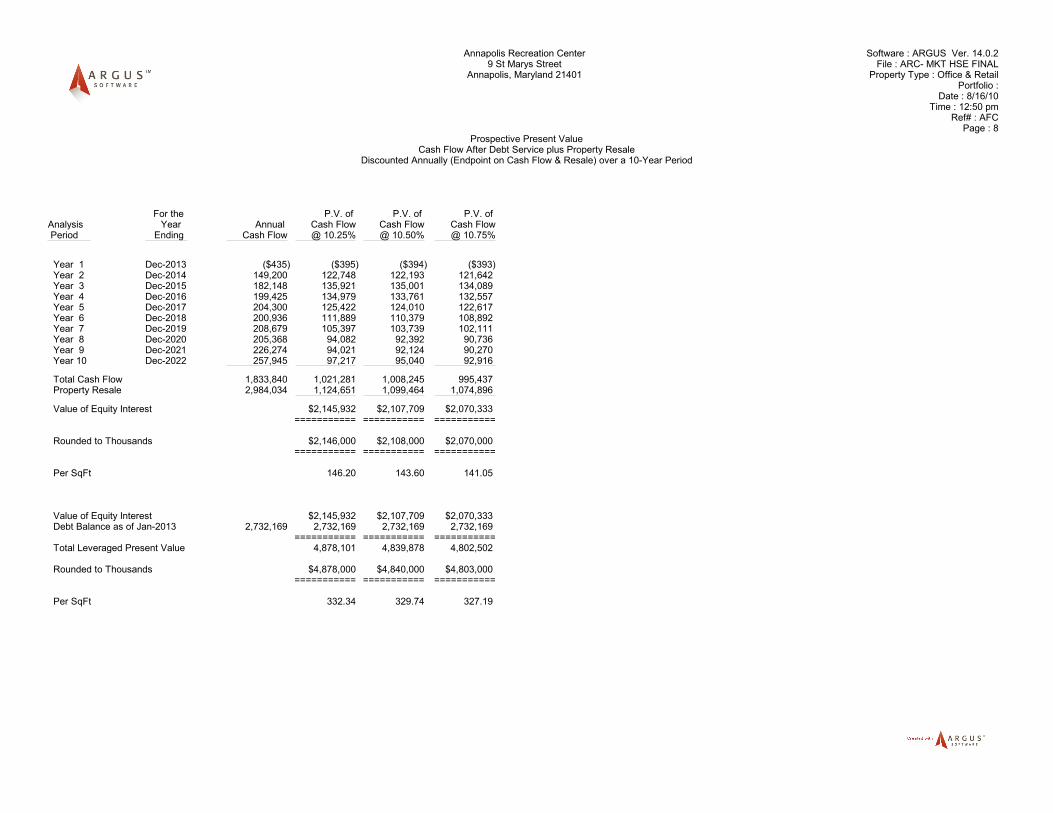

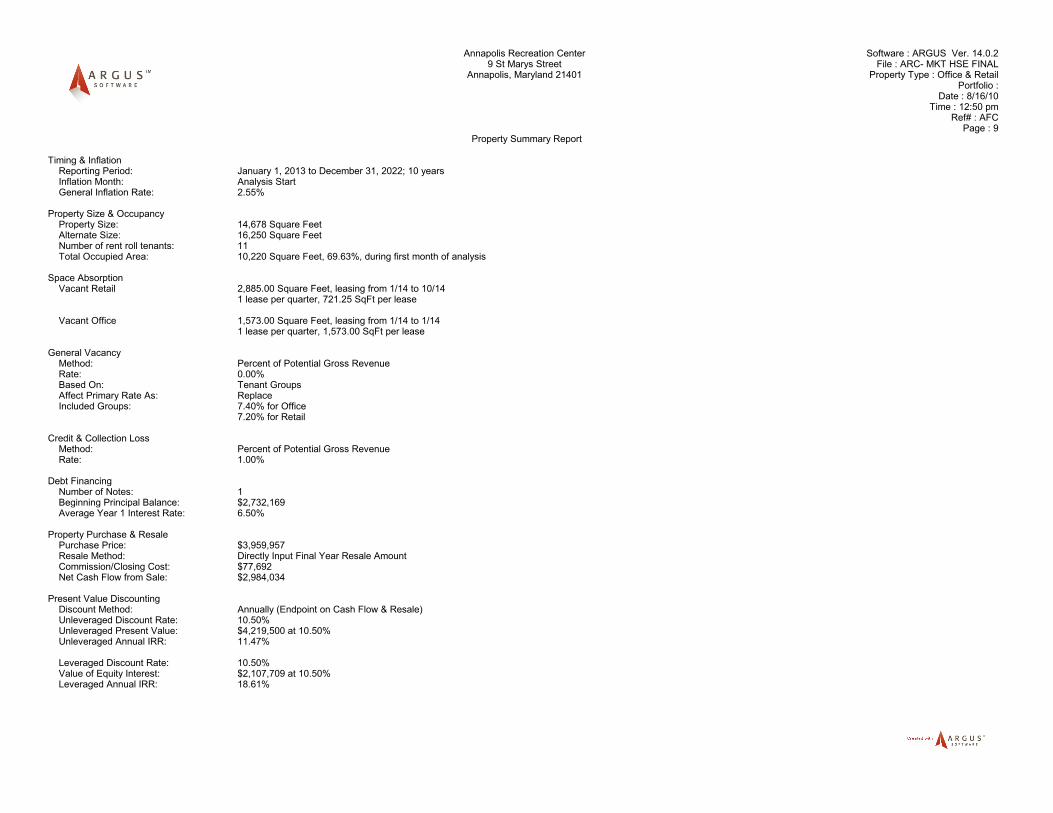

Feasibility and Valuation Analysis:

The use determined to support the highest derived property value will be considered the highest

and best use supported by the current market conditions. Considering the city is not actively

marketing the property, the value was initially based on the $3,147,700 assessed value provided

by the Maryland Department of Assessment and Taxation as of July 1, 2010. This value will be

challenged using James Graaskamp’s “backdoor approach” of the Simple Financial Feasibility

Analysis (SFFA). The backdoor approach utilizes current income potential, financing

assumptions, and estimated construction costs to derive a supported property value22.

The backdoor approach starts with the anticipated rentable square feet (RBA) that is multiplied by

market supported achievable rent per RBA to derive the potential gross income. Subtracting

market vacancy allowance provides the effective gross income. Operating expenses are then

subtracted to derive an estimated net operating income (NOI). Dividing the NOI by the debt

service coverage ratio provides the maximum annual debt service. Next, the debt service, interest

rate, and amortization period are used to establish the present value. Dividing the present value by

the maximum loan-to-value establishes the total project cost. Lastly, subtracting estimated

construction costs from the total project cost results in the supported purchase price for the land

and existing structure.

To further reduce valuation risk7, each use was initially modeled in Argus to provide more

accurate projections for items such as blended rental rates, accurate rentable space, and operating

expense reimbursements. Market assumptions for multi-family and retail uses were derived

primarily from REIS reports as of March 28, 2010, and June 28, 2010 for the office product.

Costar first quarter 2010 reports were also utilized to verify market information for the retail and

office uses. Preferred primary data was derived from recent sales and lease comparables, where 7 Risk that lack of current market data exists to accurately value the project.

17

averages were utilized to derive inputs for the financial analysis. Where recent sales and lease

comparables were absent, the Annapolis/Crofton submarket data was utilized.

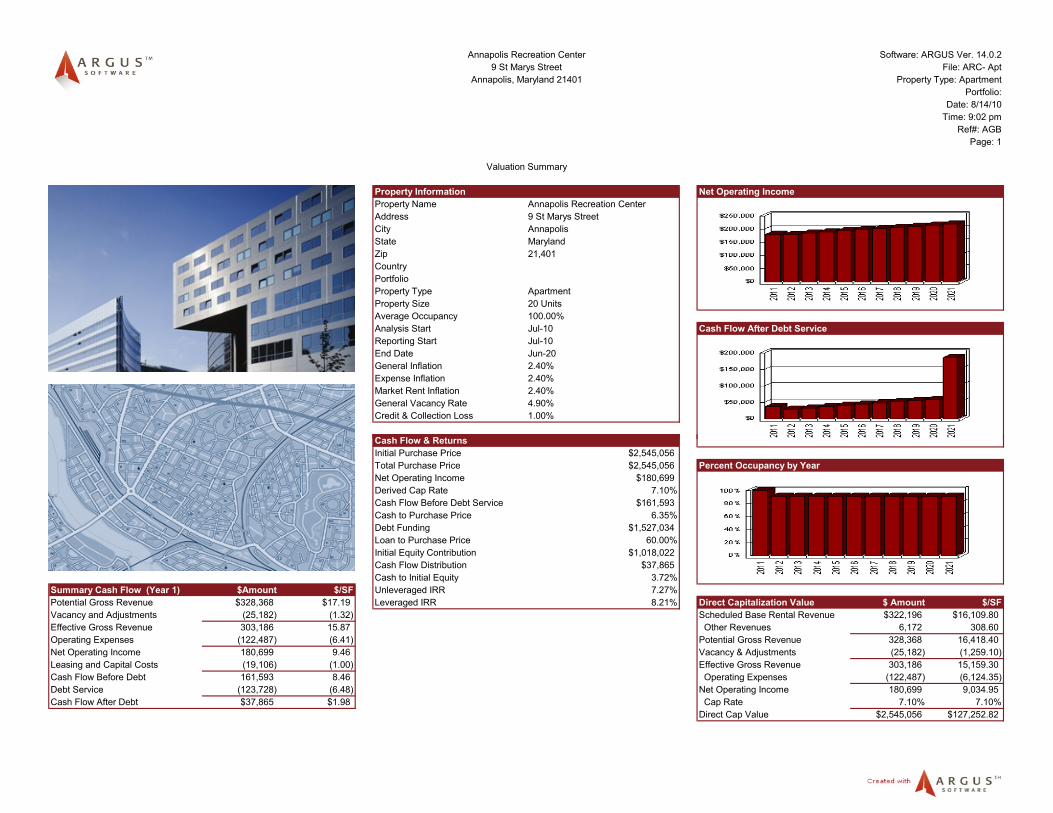

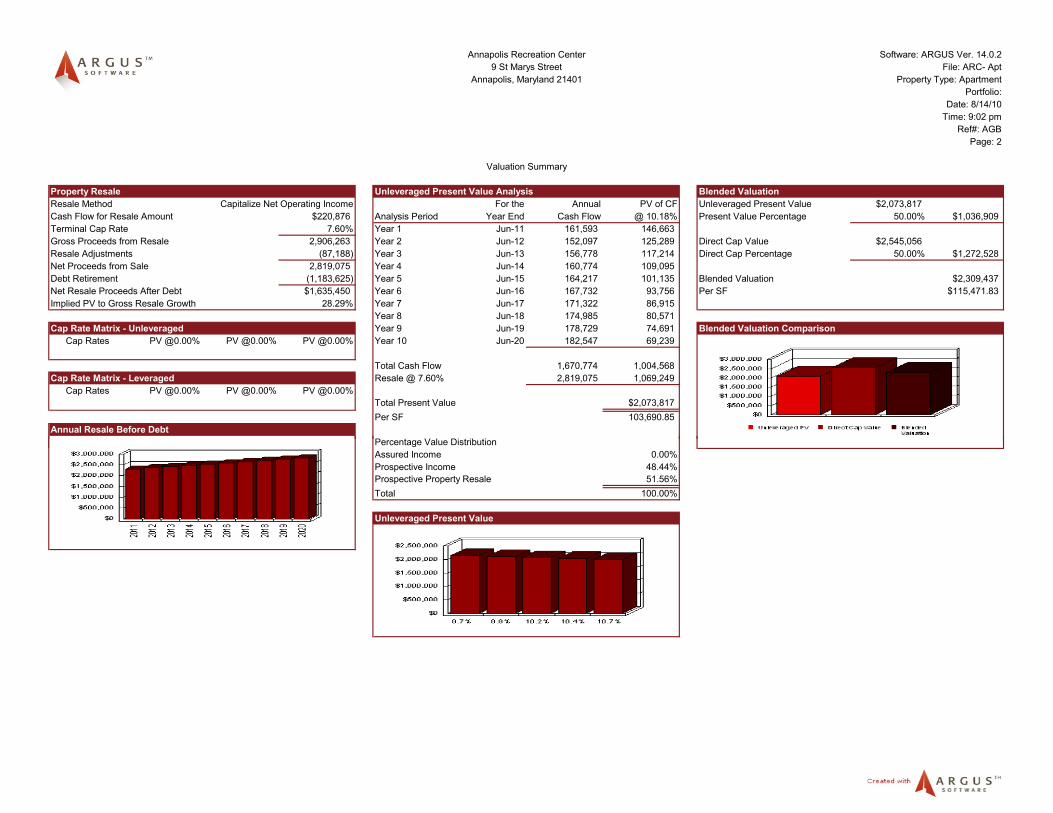

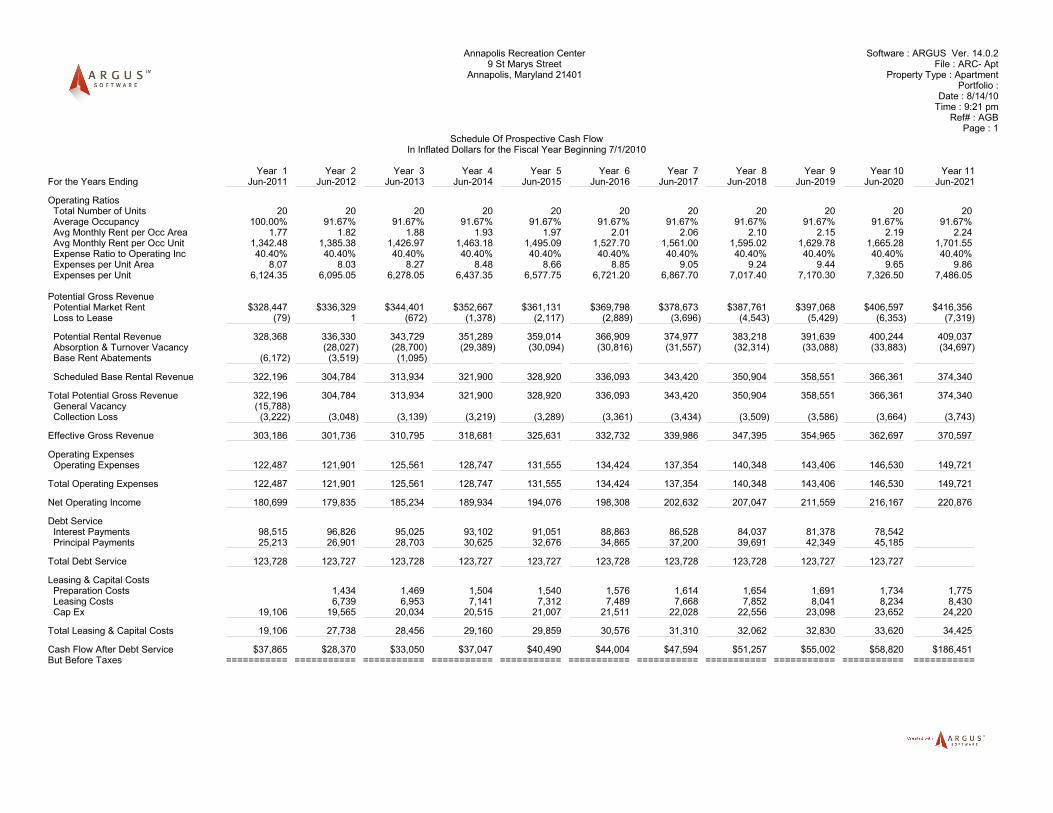

Multi-Family Apartments:

Detailed in Appendix A, the first floor will consist of 7,094 RBA after accounting for a 21%

common area factor. The second floor will yield 5,816 RBA after factoring in the proposed

additions and a 20% common area factor. To maximize potential gross income, the lofted second

floor has been modified to incorporate a third floor that will yield an additional 2,285 RBA after

factoring in 20% for common areas, and limited head room due to the roof pitch. Overall, the

building will produce a 15,195 RBA or 19,106 gross SF, correlating to a FAR of 0.738.

Market rents were derived from recent lease comparables where studios averaged 504 SF with

asking rent of $2.21 per SF, one-bedrooms average 706 SF at $1.89 per SF and two-bedrooms

averaged 1,174 SF at 1.47 per SF. The average vacancy of the three comparables was 4.9% with a

projected average vacancy rate between 2011 and 2014 of 3.75%23. For the purposes of this

analysis, a 4.9% vacancy rate will be applied. Annual concessions were identified through sales

comparables providing an average $313 per unit has been applied to the first year. A gradual

reduction to 5% over the following two-year period is intended to reflect the anticipated

improvements in the multi-family market.

Income growth of 2.4% was derived from REIS’ submarket five-year forecast. To ensure

projections are not inaccurately inflated over the holding period, expense growth has been

modeled to match income growth at 2.4%. Apartment market leasing assumptions also include a

65% renewal probability for each of the unit types, three-month downtime upon rollover, and unit

preparation costs of $200 per unit. Leasing commissions for new tenants reflect REIS

8 Estimation of floor area was determined through take-offs derived from plans acquired from the City of Annapolis

18

comparables of 3% and 1.5% for renewing leases. Recent sales comparable provided an average

operating expense ratio of 40.6% and capital expenditures of $1.00 per SF24. The assumptions

reveal a year one net operating income of $190,173.

Recent sale comparables provide an average going-in capitalization rate of 6.6% compared to

REIS’ 12-month rolling metro cap rate of 7.1% as of the first quarter of 201025. For the purposes

of this analysis, a 7.1% going-in capitalization rate was applied. A spread of 50bps has be applied

to derive a terminal capitalization rate of 7.6%. This spread reflects the reduction in value based

on the age of the structure and the erosion of income26. Applying the 7.1% capitalization rate to

the year one NOI reveals a suggested value of $2,545,056. Discounting the projected cash flows

and proceeds from reversion using a 10.18% rate, provides an unleveraged present value of

$2,073,817.

Applying Graaskamp’s SFFA backdoor approach to determine if the multi-family use supports

the acquisition of the property, we begin by multiplying the 15,195 rentable SF by the Argus

derived blended annual rental rate of $21.62 to derive a potential gross income of $328,447.

Subtracting the $15,788 vacancy allowance results in an effective gross income of $312,659. Less

operating expenses of $122,486 provides a net operating income of $190,173. Dividing the NOI

by the minimum 1.25 debt service coverage ratio, results in a maximum annual debt service of

$152,138. Incorporating the financial assumptions derives an estimated present value of

$1,855,765. Dividing the present value by a maximum loan-to-value of 65% reveals an estimated

total project cost of $2,855,024.

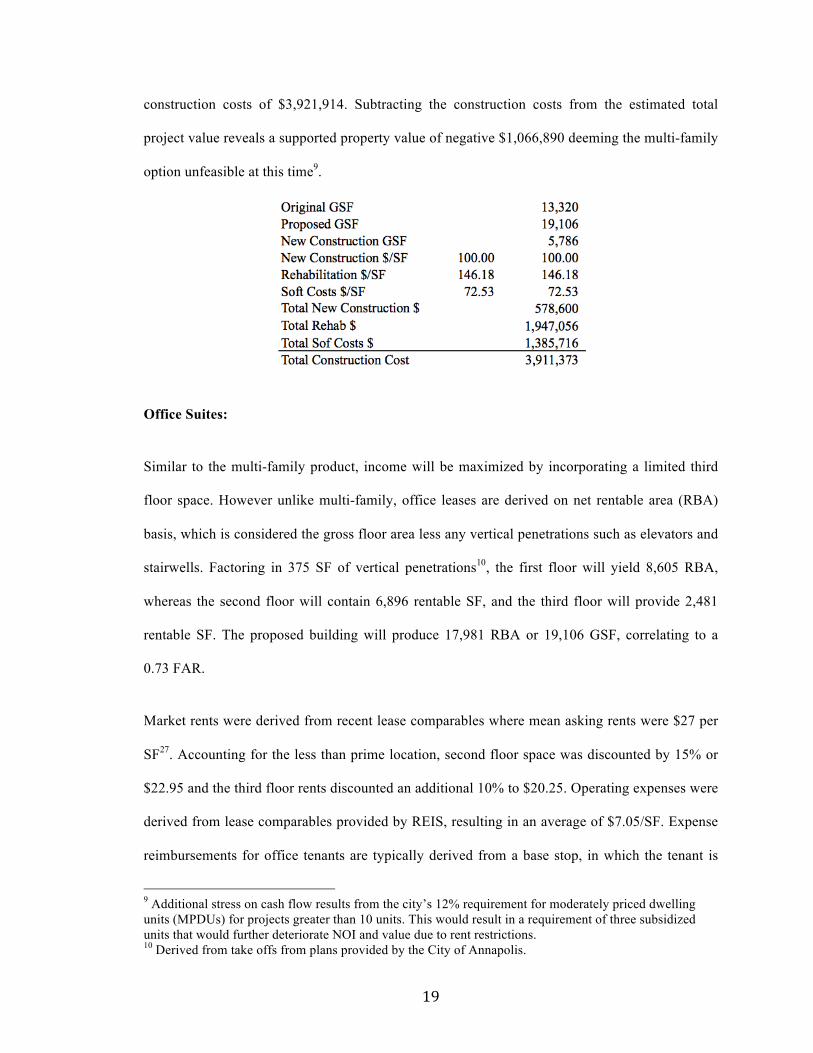

Illustrated below, new construction hard costs of $100 per SF were applied to the proposed 5,786

SF in new construction. Renovation hard costs of $146 per SF reflect the additional labor, time,

and risk, and were applied to the existing 13,320 SF. Soft costs of $73 per SF were applied to the

entire proposed 19,106 SF structure. The sum of the calculations reflects the total estimated

19

construction costs of $3,921,914. Subtracting the construction costs from the estimated total

project value reveals a supported property value of negative $1,066,890 deeming the multi-family

option unfeasible at this time9.

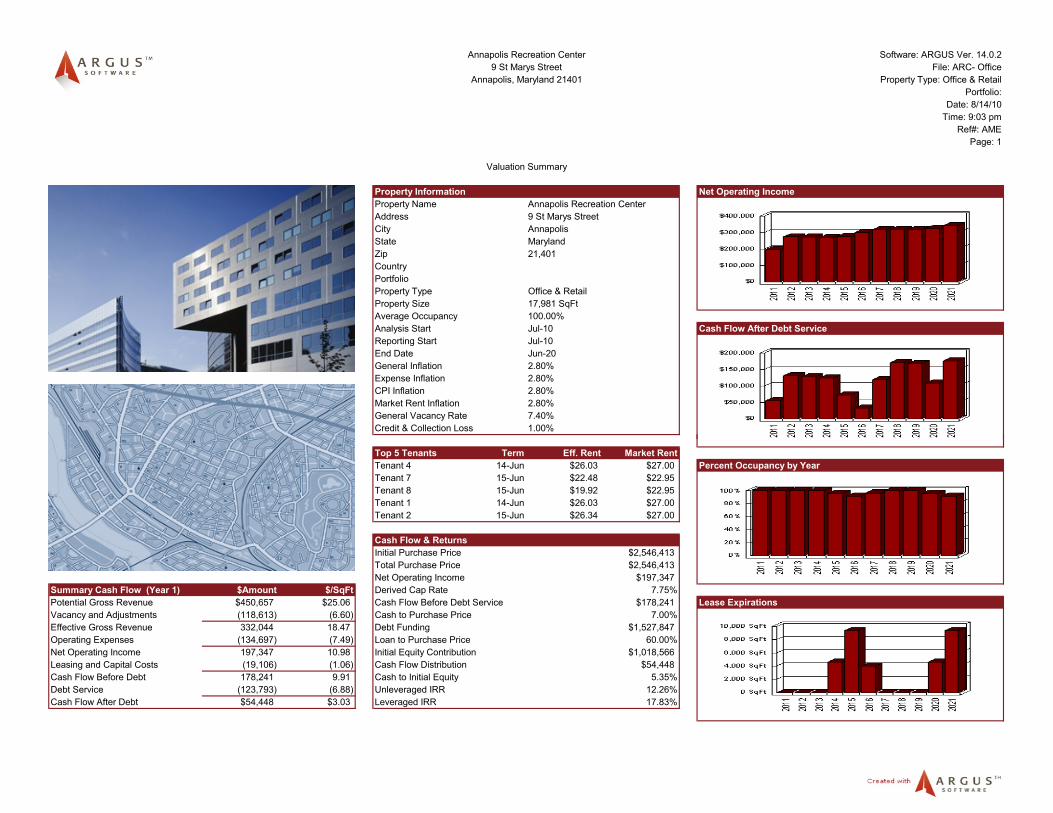

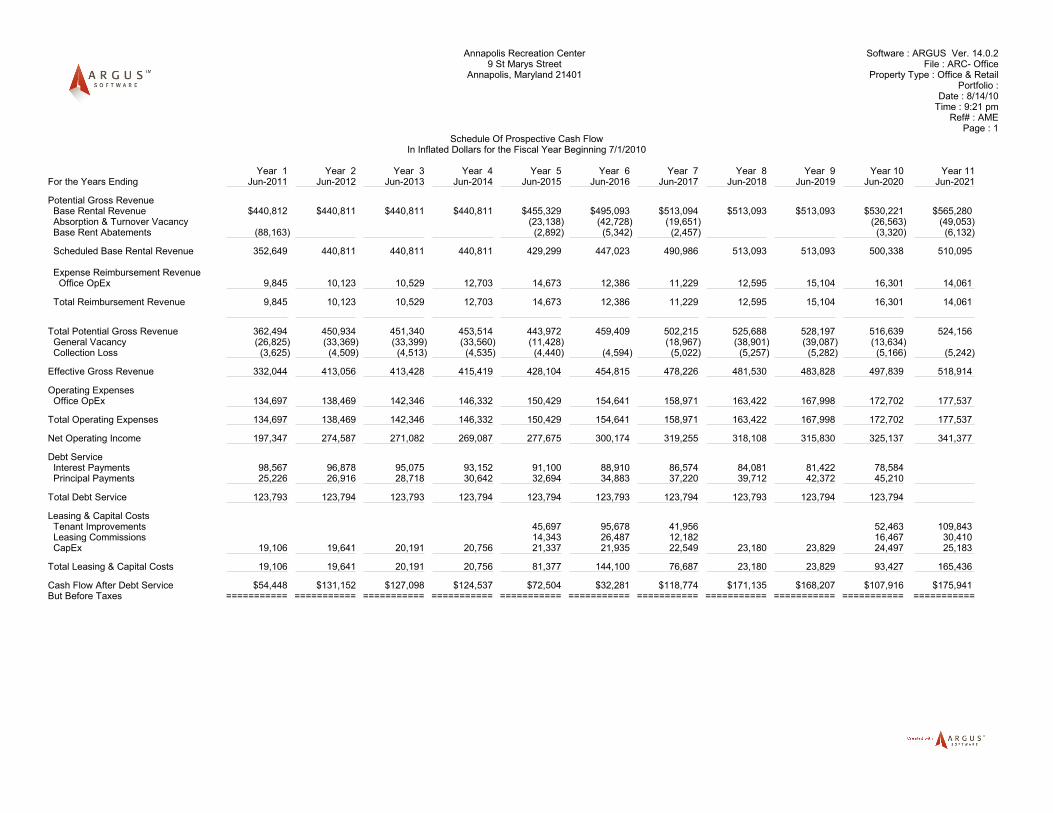

Office Suites:

Similar to the multi-family product, income will be maximized by incorporating a limited third

floor space. However unlike multi-family, office leases are derived on net rentable area (RBA)

basis, which is considered the gross floor area less any vertical penetrations such as elevators and

stairwells. Factoring in 375 SF of vertical penetrations10, the first floor will yield 8,605 RBA,

whereas the second floor will contain 6,896 rentable SF, and the third floor will provide 2,481

rentable SF. The proposed building will produce 17,981 RBA or 19,106 GSF, correlating to a

0.73 FAR.

Market rents were derived from recent lease comparables where mean asking rents were $27 per

SF27. Accounting for the less than prime location, second floor space was discounted by 15% or

$22.95 and the third floor rents discounted an additional 10% to $20.25. Operating expenses were

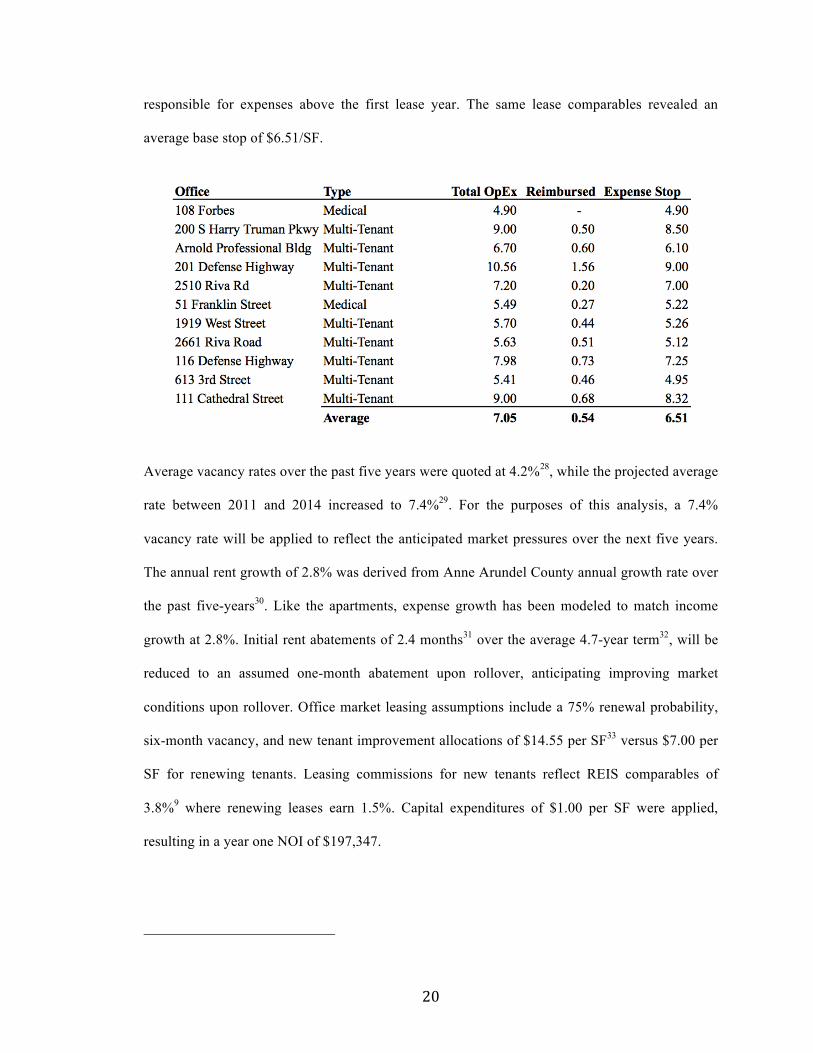

derived from lease comparables provided by REIS, resulting in an average of $7.05/SF. Expense

reimbursements for office tenants are typically derived from a base stop, in which the tenant is

9 Additional stress on cash flow results from the city’s 12% requirement for moderately priced dwelling units (MPDUs) for projects greater than 10 units. This would result in a requirement of three subsidized units that would further deteriorate NOI and value due to rent restrictions. 10 Derived from take offs from plans provided by the City of Annapolis.

20

responsible for expenses above the first lease year. The same lease comparables revealed an

average base stop of $6.51/SF.

Average vacancy rates over the past five years were quoted at 4.2%28, while the projected average

rate between 2011 and 2014 increased to 7.4%29. For the purposes of this analysis, a 7.4%

vacancy rate will be applied to reflect the anticipated market pressures over the next five years.

The annual rent growth of 2.8% was derived from Anne Arundel County annual growth rate over

the past five-years30. Like the apartments, expense growth has been modeled to match income

growth at 2.8%. Initial rent abatements of 2.4 months31 over the average 4.7-year term32, will be

reduced to an assumed one-month abatement upon rollover, anticipating improving market

conditions upon rollover. Office market leasing assumptions include a 75% renewal probability,

six-month vacancy, and new tenant improvement allocations of $14.55 per SF33 versus $7.00 per

SF for renewing tenants. Leasing commissions for new tenants reflect REIS comparables of

3.8%9 where renewing leases earn 1.5%. Capital expenditures of $1.00 per SF were applied,

resulting in a year one NOI of $197,347.

21

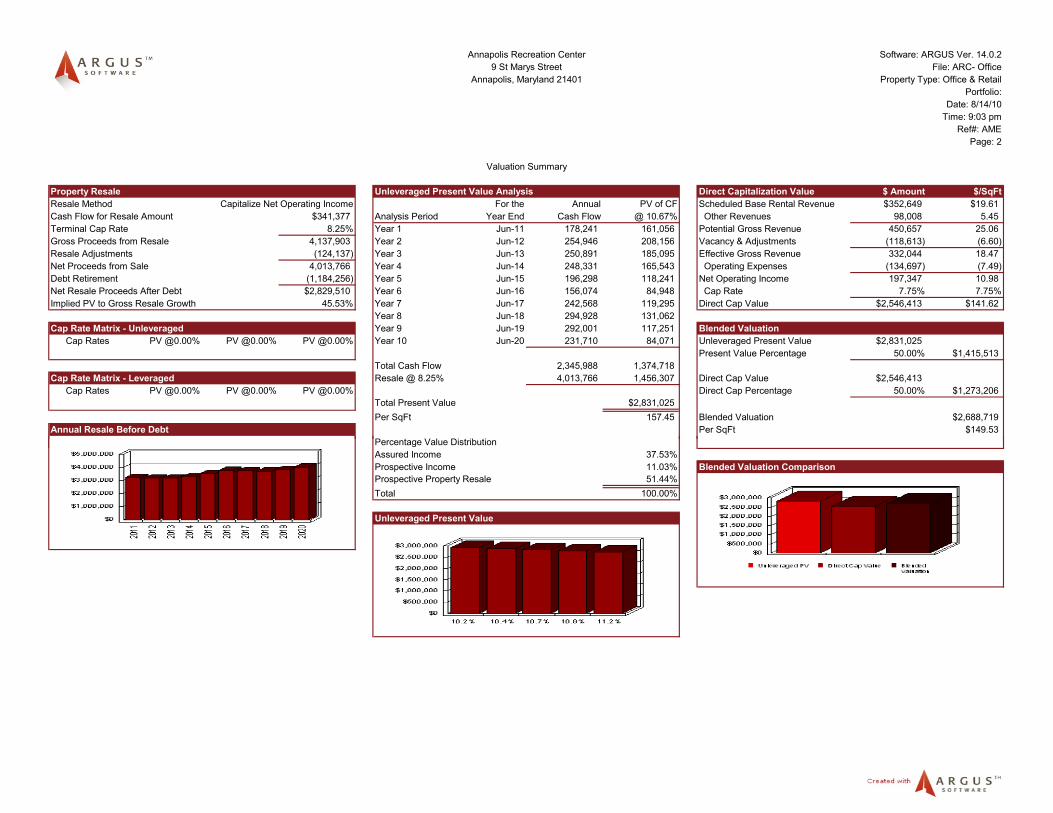

Average going-in capitalization rates from recent sale comparables are limited and evidenced by

one transaction, 108 Forbes Street that traded on March 1, 2010 for 7.7%, compared to the REIS

average 12-month rolling metro cap rate of 8.4%, as of the second quarter of 201011. For the

purposes of this analysis the 7.75% rate was applied. A 50bps spread was applied to the going-in

cap rate to derive the terminal capitalization rate of 8.25%. Applying the 7.75% capitalization rate

to the year one NOI reveals a suggested value of $2,546,413. Discounting the projected cash

flows and proceeds from reversion using a 10.67% rate, provides an unleveraged present value of

$2,831,025.

Applying Graaskamp’s SFFA backdoor approach to determine if the multi-family use supports

the acquisition of the property, we begin by multiplying the 17,981 rentable SF by the Argus

derived blended annual rental rate of $24.52 to derive a potential gross income of $440,812.

Subtracting the $26,825 vacancy allowance results in the effective gross income of $413,987.

Operating expenses of $134,697 less anticipated reimbursable expenses of $9,845 provides a net

operating income of $289,135. Dividing the NOI by the 1.25 minimum debt service coverage

ratio results in a maximum annual debt service of $231,308. Incorporating the financial

assumptions derives an estimated present value of $2,821,466. Dividing the present value by a

maximum loan-to-value of 65% reveals an estimated total project value of $4,340,718.

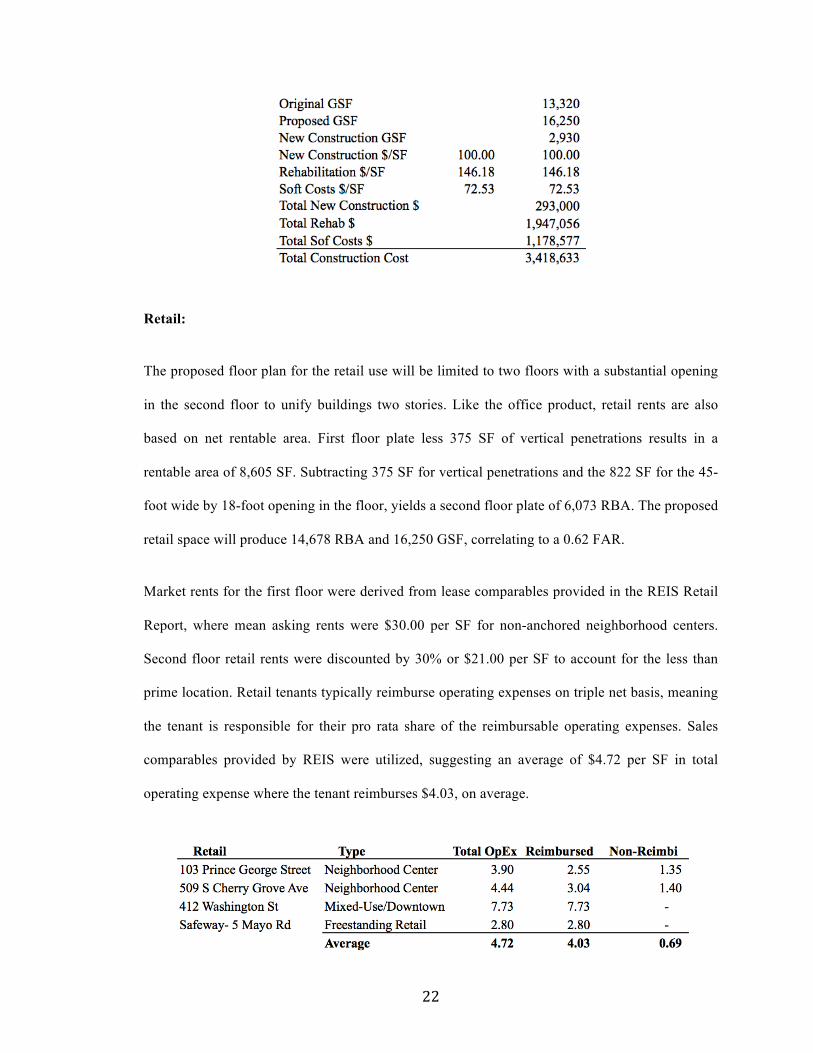

Illustrated below, new construction hard costs of $100 per SF were applied to the proposed 5,786

SF, while renovation hard costs of $146 per SF were applied to the existing 13,320 SF. Estimated

soft costs of $73 per SF were applied to the proposed 19,106 SF structure. The sum reflects total

estimated construction costs of $3,921,914. Subtracting construction costs from the estimated

total project value reveals a supported property value of $418,804 reflecting an 87% discount in

the assessed value.

22

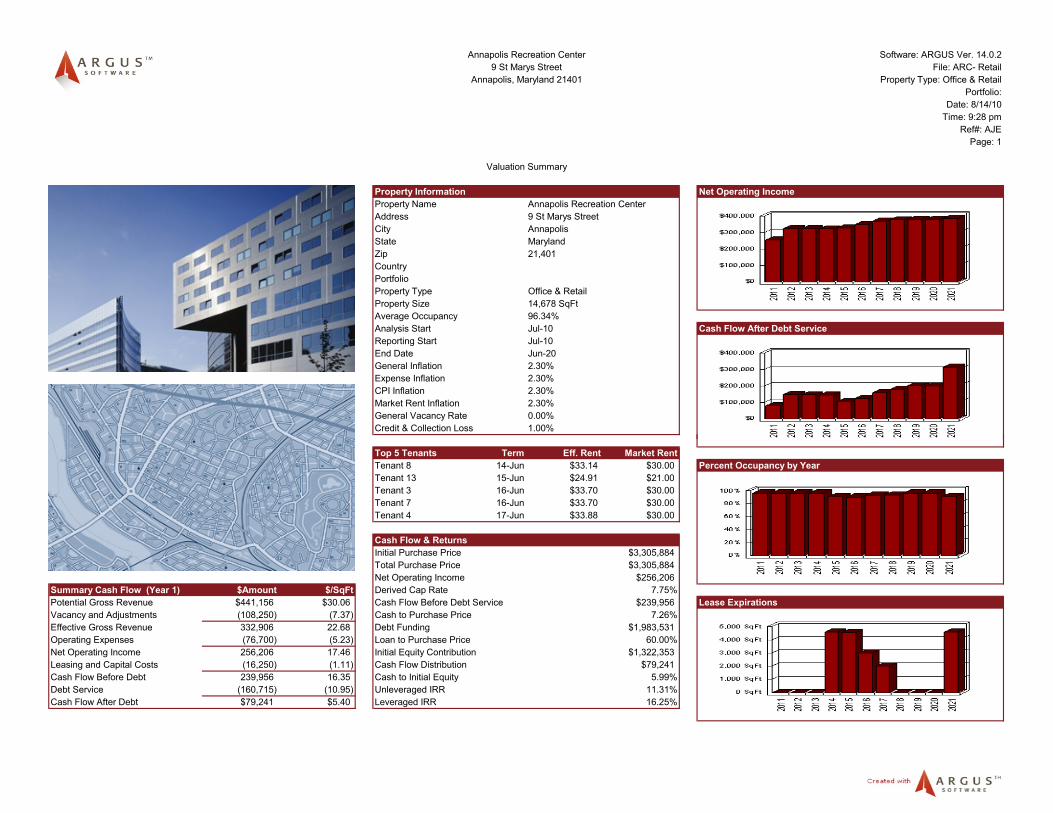

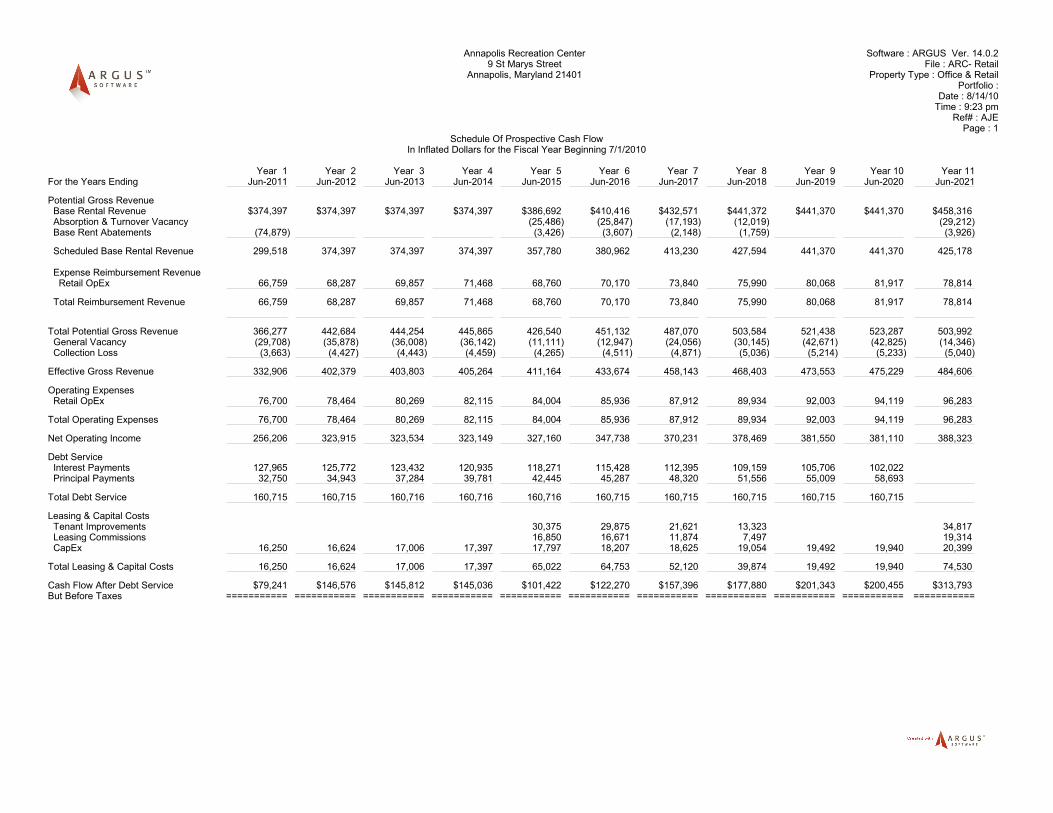

Retail:

The proposed floor plan for the retail use will be limited to two floors with a substantial opening

in the second floor to unify buildings two stories. Like the office product, retail rents are also

based on net rentable area. First floor plate less 375 SF of vertical penetrations results in a

rentable area of 8,605 SF. Subtracting 375 SF for vertical penetrations and the 822 SF for the 45-

foot wide by 18-foot opening in the floor, yields a second floor plate of 6,073 RBA. The proposed

retail space will produce 14,678 RBA and 16,250 GSF, correlating to a 0.62 FAR.

Market rents for the first floor were derived from lease comparables provided in the REIS Retail

Report, where mean asking rents were $30.00 per SF for non-anchored neighborhood centers.

Second floor retail rents were discounted by 30% or $21.00 per SF to account for the less than

prime location. Retail tenants typically reimburse operating expenses on triple net basis, meaning

the tenant is responsible for their pro rata share of the reimbursable operating expenses. Sales

comparables provided by REIS were utilized, suggesting an average of $4.72 per SF in total

operating expense where the tenant reimburses $4.03, on average.

23

Average vacancy rates over the past five years were quoted at 4.3%34, while the projected average

vacancy rate between 2011 and 2014 is anticipated to increase to 7.2%35. For the purposes of this

analysis, a 7.2% vacancy rate will be applied. The annual rent growth of 2.3% was derived from

the annualized five-year category for neighborhood shopping centers36. Expense growth has been

modeled to match income growth at 2.3%. Initial rent abatements of 2.4 months37 per lease term

were initially applied, reducing to one month upon rollover, in anticipation of better market

conditions upon rollover. Additional market leasing assumptions include a 75% renewal

probability, six-month downtime between leases, and $10.15 per SF38 for new tenant

improvement reducing to $5.00 per SF for renewing tenants. Leasing commissions for new

tenants reflect REIS comparables of 3.2% where renewing leases are modeled to earn 1.5%.

Annual reserves for capital expenditure were capped at $1.00 per SF resulting in a year one net

operating income of $256,206.

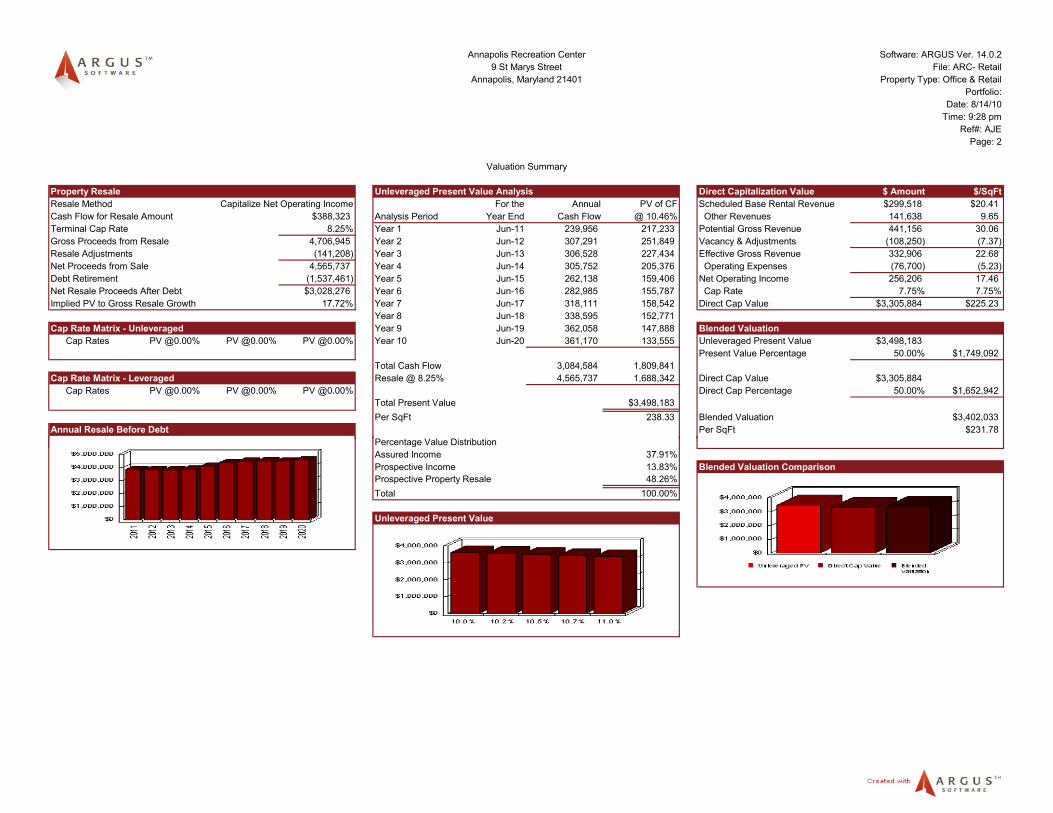

Average going-in capitalization rates of recent comparable sales provides a rate of 8.2%

compared to REIS’ average 12-month rolling metro cap rate of 7.3% as of the first quarter of

2010. For the purposes of this analysis the 7.75% rate was applied. A 50bps spread was applied to

the going-in cap rate to derive a terminal capitalization rate of 8.25%. Applying the 7.75%

capitalization rate to the year one NOI reveals a suggested value of $3,305,884. Discounting the

projected cash flows and proceeds from reversion using a 10.46% rate, provides an unleveraged

present value of $3,498,183.

Applying Graaskamp’s SFFA backdoor approach to determine if the retail use supports the

acquisition of the property, we begin by multiplying the 14,678 rentable SF by the Argus derived

blended annual rental rate of $25.51 to derive a potential gross income of $374,397. Subtracting

$29,708 for vacancy allowance results in the effective gross income of $344,689. Subtracting

total operating expenses of $76,700 less anticipated reimbursable expenses of $66,759 provides a

net operating income of $334,748. Dividing by the 1.25 debt service coverage ratio results in a

24

maximum annual debt service of $262,798. Incorporating the financial assumptions derives an

estimated present value of $3,266,572. Dividing the present value by a maximum loan-to-value

of 65% reveals an estimated total project value of $5,025,495.

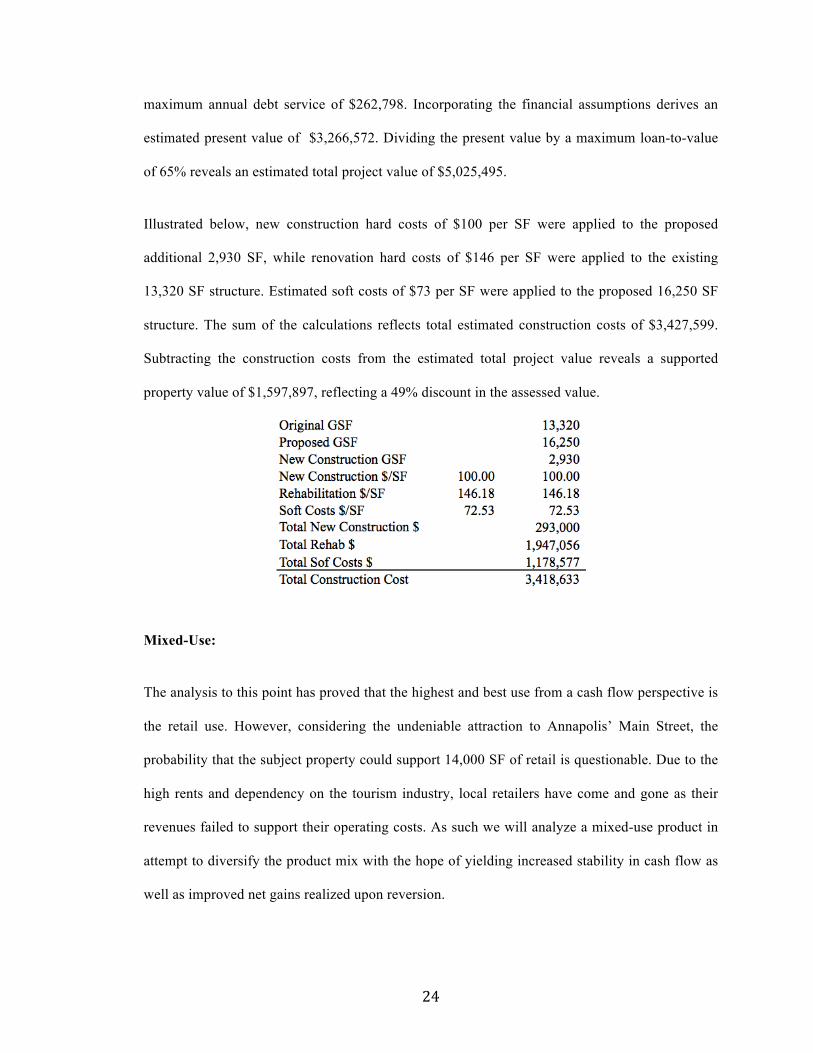

Illustrated below, new construction hard costs of $100 per SF were applied to the proposed

additional 2,930 SF, while renovation hard costs of $146 per SF were applied to the existing

13,320 SF structure. Estimated soft costs of $73 per SF were applied to the proposed 16,250 SF

structure. The sum of the calculations reflects total estimated construction costs of $3,427,599.

Subtracting the construction costs from the estimated total project value reveals a supported

property value of $1,597,897, reflecting a 49% discount in the assessed value.

Mixed-Use:

The analysis to this point has proved that the highest and best use from a cash flow perspective is

the retail use. However, considering the undeniable attraction to Annapolis’ Main Street, the

probability that the subject property could support 14,000 SF of retail is questionable. Due to the

high rents and dependency on the tourism industry, local retailers have come and gone as their

revenues failed to support their operating costs. As such we will analyze a mixed-use product in

attempt to diversify the product mix with the hope of yielding increased stability in cash flow as

well as improved net gains realized upon reversion.

25

The proposed floor plan for a mixed-use project will incorporate ground floor retail and office

suites on the second floor. Similar to the all retail product, a 45-foot long by 18-foot wide

opening will be cut into the center of second floor to expose the second floor lofted ceilings. Both

retail and office leases are based on net rentable area, resulting in a first floor net rentable area of

8,605 SF and a second floor net rentable area of 6,073 SF. The proposed mixed-use space will

produce 14,678 RBA and 16,250 GSF, correlating to a 0.62 FAR.

First floor retail rental rate remain at $30.00 per SF with triple net operating expense

reimbursements of $4.03 per SF and total expenses of $4.72 per SF. Vacancy for the retail portion

has been held constant at 7.2% and the average six-year term will remain. Initial rent abatements

of 2.4 months per lease term were applied, reducing to one month upon rollover in anticipation of

better market conditions. Both income and expenses have been modeled to grow at a constant

2.5%. Additional market leasing assumptions include a 75% renewal probability, six-month

vacancy, and new tenant improvements of $10.15 per SF in comparison to $5.00 per SF for

renewing tenants. Leasing commissions for new tenants reflect REIS comparables of 3.2% where

renewing leases earn 1.5%. Lastly, annual capital expenditures of $1.00 per SF were applied.

The second floor office rental rate has been modeled at $27.00 per SF with the assumption that

the unique open floor plan will attract premium rents. Operating expense reimbursements were

based on an expense stop, and are modeled to reflect $6.51 per SF, with total expenses of $7.05

per SF. The office vacancy rate coincides with the REIS report of 7.4%, as does the average term

of 4.7 years. Both income and expenses have been modeled to grow at a constant 2.5%. Initial

rent abatements of 2.4 months per term have been revised to one-month upon rollover. Additional

office market leasing assumptions include a 75% renewal probability, six-month vacancy, and

new tenant improvement of $14.55 per SF versus $7.00 for renewing tenants. Leasing

commissions for new tenants reflect REIS comparables of 3.8% where renewing leases earn

26

1.5%. Lastly, capital expenditure were modeled using $1.00 per SF annually resulting in a year

one net operating income of $275,433.

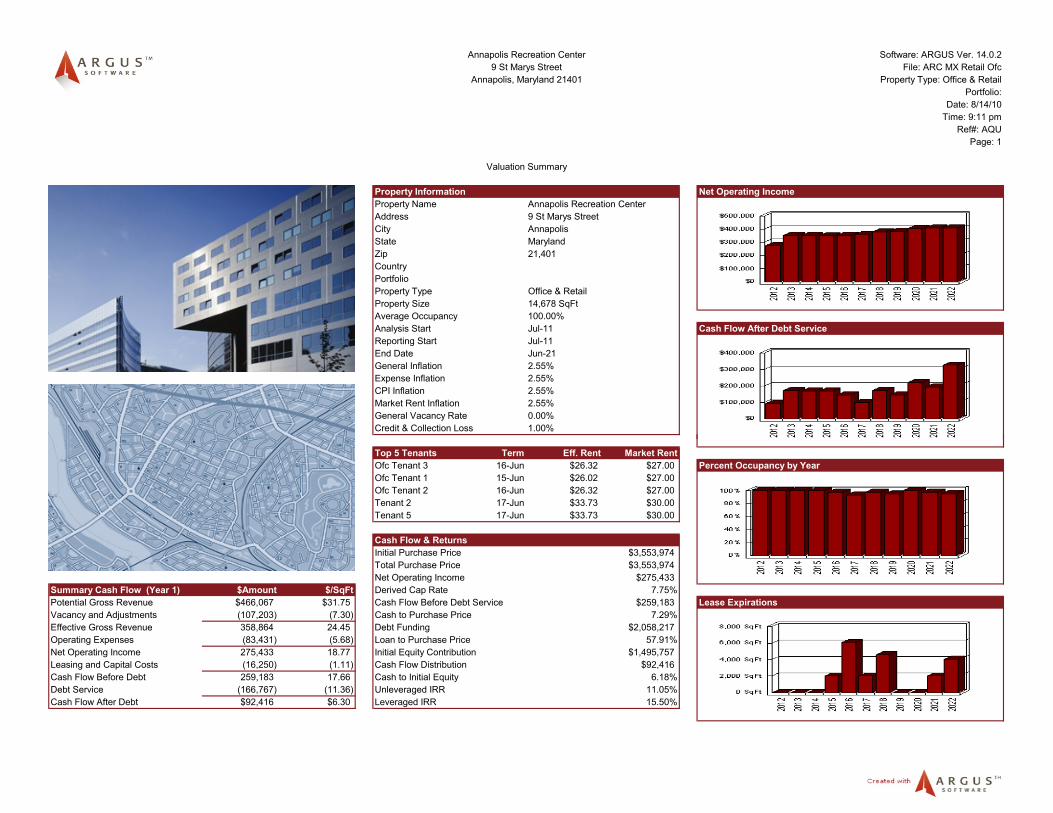

Derived going-in capitalization rates of 7.75% were utilized for both retail and office while a 50-

basis point spread provides a terminal capitalization rate of 8.25%. Applying the 7.75%

capitalization rate to the year one NOI reveals a suggested value of $3,553,974. Discounting the

projected cash flows and proceeds from reversion using a 10.5% rate, provides an unleveraged

present value of $3,685,658.

Applying Graaskamp’s SFFA backdoor approach, the 14,678 rentable SF is multiplied by the

Argus derived blended annual rental rate of $28.76 to derive a potential gross income of

$422,121. Subtracting $18,960 for vacancy allowance results in an effective gross income of

$403,161. Subtracting total operating expenses of $83,431 less reimbursable expenses of $43,895

provides a net operating income of $363,625. Dividing by the 1.25 debt service coverage ratio

results in a maximum annual debt service of $290,900. Utilizing the financial assumptions

suggests an estimated present value of $3,548,362. Dividing the present value by a maximum

loan-to-value of 65% reveals an estimated total project value of $5,459,019.

As illustrated below, new construction hard costs of $100 per SF were applied to the anticipated

2,930 GSF in additions, while renovation hard costs of $146 per SF were applied to the 13,320

SF existing structure. Estimated soft costs remain at $73 per SF and were applied to the proposed

16,250 SF structure. The sum of the calculations reflects total estimated construction costs of

$3,427,599. Subtracting the construction costs from the estimated total project value reveals a

supported property value of $2,031,420 reflecting a 35% discount in the assessed value.

27

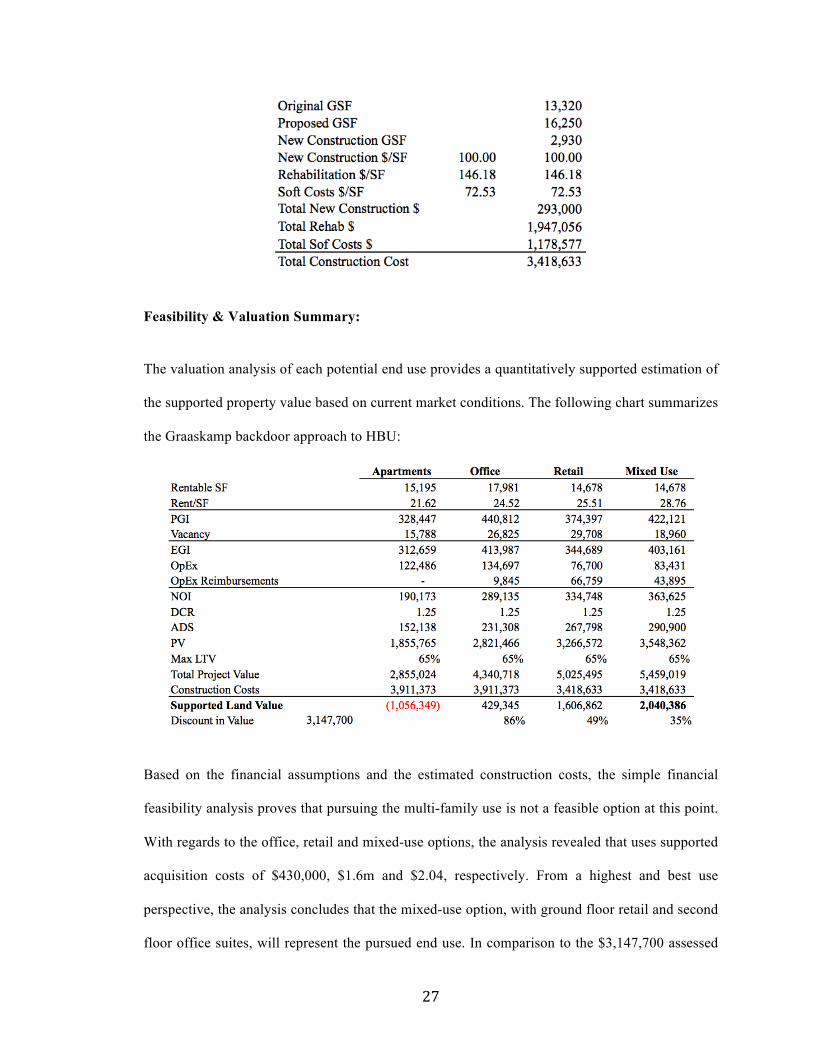

Feasibility & Valuation Summary:

The valuation analysis of each potential end use provides a quantitatively supported estimation of

the supported property value based on current market conditions. The following chart summarizes

the Graaskamp backdoor approach to HBU:

Based on the financial assumptions and the estimated construction costs, the simple financial

feasibility analysis proves that pursuing the multi-family use is not a feasible option at this point.

With regards to the office, retail and mixed-use options, the analysis revealed that uses supported

acquisition costs of $430,000, $1.6m and $2.04, respectively. From a highest and best use

perspective, the analysis concludes that the mixed-use option, with ground floor retail and second

floor office suites, will represent the pursued end use. In comparison to the $3,147,700 assessed

28

value, the supported property value reflects a 35% discount in value, accurately reflecting the

recent economic recession, where on average values of commercial real estate have reset between

30% and 40%39. The remainder of this proposal will focus on the viability of pursuing the mixed-

use product.

Mixed-Use Development Plan:

The pursued end use for the first floor will strive to fill a gap that has been present in the

Annapolis market for decades. For the majority of the city vast 300-year history and up until the

1950’s, the city dock area provided residents with essential goods and services generally

consumed by households. Since the 1950’s, the city’s dynamic has evolved to tailor more towards

tourists than residents. Commercial fishing boats that filled the city dock and provided residents

with fresh seafood, has since been replaced with parking lots and tourist targeted shops. The

closing of iconic 5,000 SF city dock market house resulted in the displacement of tenants, many

of which had occupied the space for decades. The intent of the city’s previous administration was

to renovate the building and lease the entire space to a national gourmet grocer. Fumbles in the

renovation work and disputes over details in the lease, resulted in the termination of the lease by

the tenant. To this day, the market house has not functioned to its potential with a large portion

vacant, portraying the inherent challenges that accompany real estate investing for businesses

whose core business is not real estate.

Ground Floor Retail:

Although a variety of tenants could potentially occupy the ground floor space, this proposal

targets a niche tenant group that aims to fill an essential gap in services. The proposed use will

take the form of a market house setting comprised of a variety of vendors providing fresh

produce, meats, and seafood. The target market would be residents and tourists, as well as the

29

large contingency of transient boater that pass through or spend the season in “America’s Sailing

Capital.”40

Opponents would argue the proposed use would ineffectively compete with the centrally located

city dock market house located two blocks to the north. To the contrary, the space would strive to

compliment the timeless essence of the existing market house. Recently awarded market house

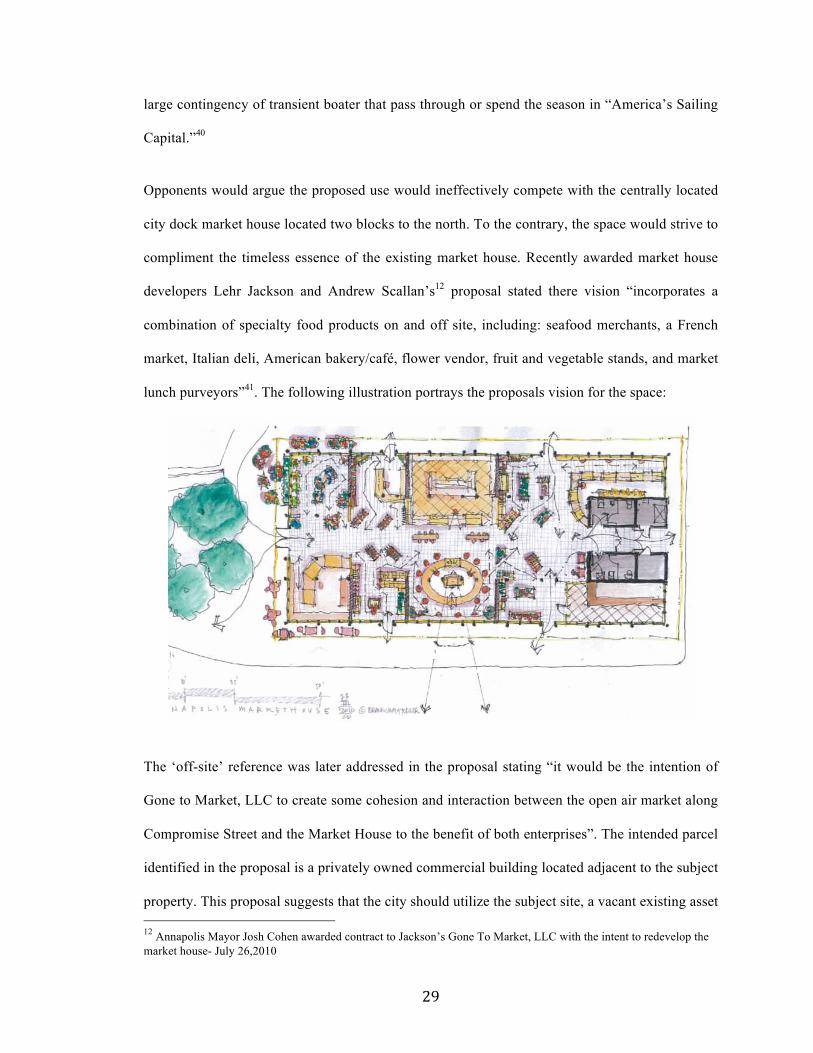

developers Lehr Jackson and Andrew Scallan’s12 proposal stated there vision “incorporates a

combination of specialty food products on and off site, including: seafood merchants, a French

market, Italian deli, American bakery/café, flower vendor, fruit and vegetable stands, and market

lunch purveyors”41. The following illustration portrays the proposals vision for the space:

The ‘off-site’ reference was later addressed in the proposal stating “it would be the intention of

Gone to Market, LLC to create some cohesion and interaction between the open air market along

Compromise Street and the Market House to the benefit of both enterprises”. The intended parcel

identified in the proposal is a privately owned commercial building located adjacent to the subject

property. This proposal suggests that the city should utilize the subject site, a vacant existing asset 12 Annapolis Mayor Josh Cohen awarded contract to Jackson’s Gone To Market, LLC with the intent to redevelop the market house- July 26,2010

30

controlled by the city. As a result, the city dock market house would focus on providing prepared

foods for residents and visitors, while the subject site would cater more towards providing fresh

produce, seafood, poultry and meat.

The closest grocery stores that service city residents are Groul’s Market and Giant Food located

1.4 miles and 3.1 miles from downtown. As a result, residents are required to drive outside the

city limits to fulfill their basic grocery needs, depriving the city of potential revenue. Further,

once the residents leave the city, they are more inclined to run additional errands outside city

limited, placing additional strain on revenues that could be realized by the city42. During a recent

conversation with Lehr Jackson, he stated that Main Street has changed over the last twenty years

to cater more towards the tourist contingency, than focusing on the basic needs of the residents.

As a result, the residents have been forced to leave the city limits to fulfill their basic needs43.

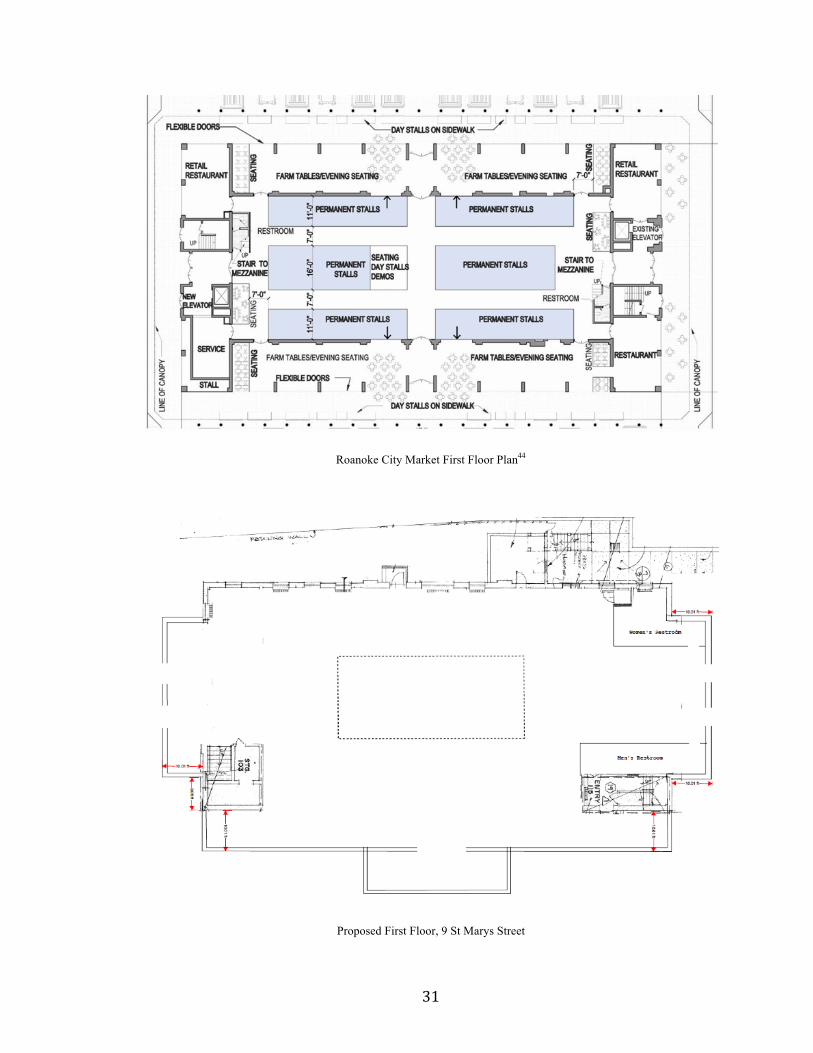

The proposed end product would be similar to Washington DC’s Eastern Market, Easton

Maryland’s Market Square, or Virginia’s Roanoke City Market. The site plan below illustrates

Roanoke City Market’s floor plan, one that shares similarities to the subject sites size and layout.

Permanent stalls line the length of the buildings core, with either end utilized for facilities,

storage, and access to the upper floors. Similar to this proposal, the center of the second floor

would be opened to reveal the vaulted ceilings while creating a sense of place for patrons.

31

Roanoke City Market First Floor Plan44

Proposed First Floor, 9 St Marys Street

32

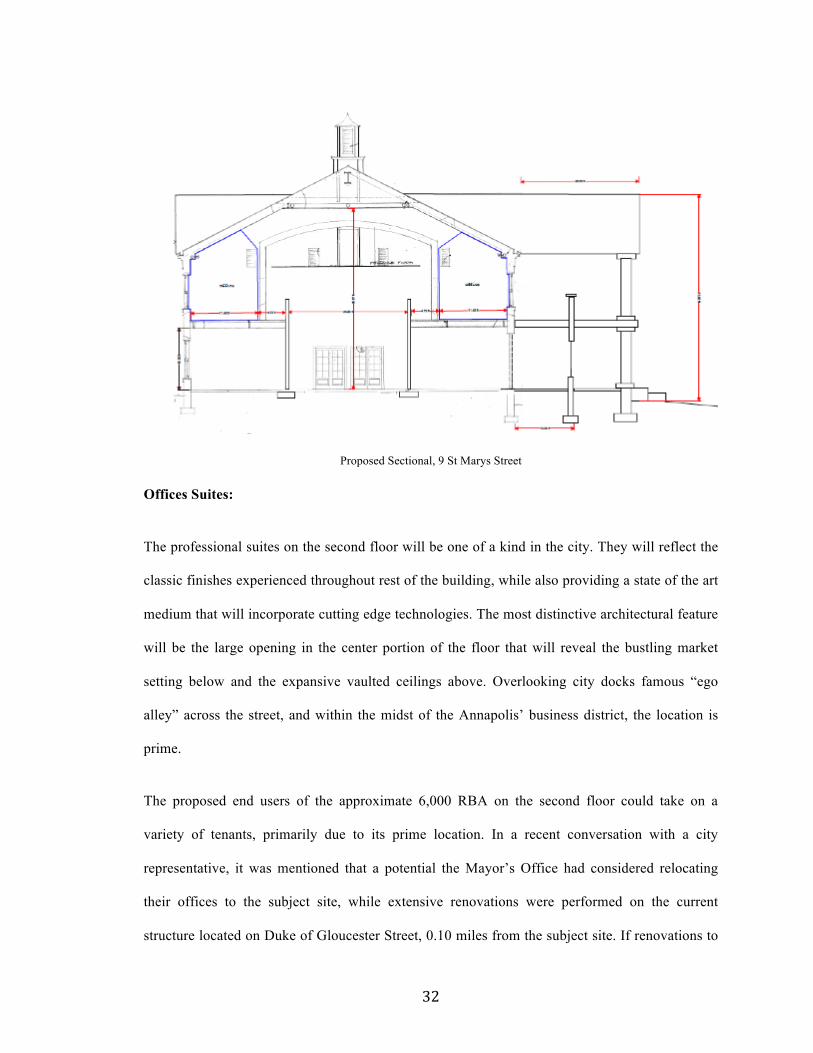

Proposed Sectional, 9 St Marys Street

Offices Suites:

The professional suites on the second floor will be one of a kind in the city. They will reflect the

classic finishes experienced throughout rest of the building, while also providing a state of the art

medium that will incorporate cutting edge technologies. The most distinctive architectural feature

will be the large opening in the center portion of the floor that will reveal the bustling market

setting below and the expansive vaulted ceilings above. Overlooking city docks famous “ego

alley” across the street, and within the midst of the Annapolis’ business district, the location is

prime.

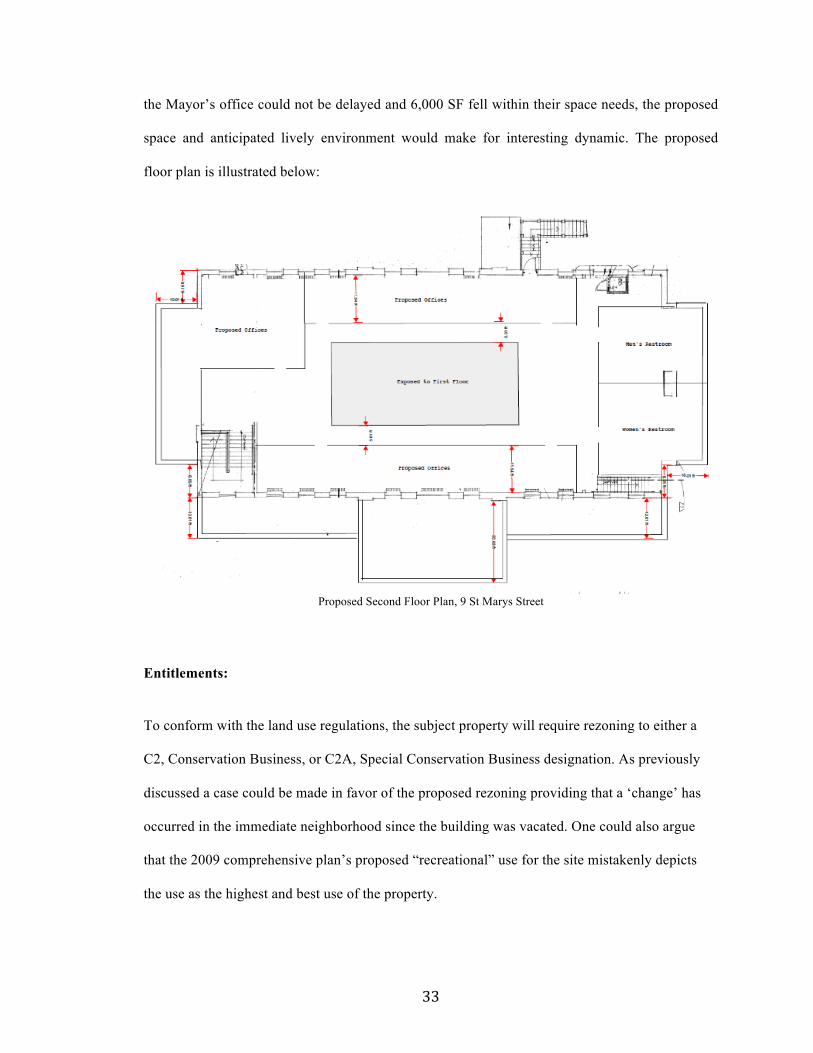

The proposed end users of the approximate 6,000 RBA on the second floor could take on a

variety of tenants, primarily due to its prime location. In a recent conversation with a city

representative, it was mentioned that a potential the Mayor’s Office had considered relocating

their offices to the subject site, while extensive renovations were performed on the current

structure located on Duke of Gloucester Street, 0.10 miles from the subject site. If renovations to

33

the Mayor’s office could not be delayed and 6,000 SF fell within their space needs, the proposed

space and anticipated lively environment would make for interesting dynamic. The proposed

floor plan is illustrated below:

Proposed Second Floor Plan, 9 St Marys Street

Entitlements:

To conform with the land use regulations, the subject property will require rezoning to either a

C2, Conservation Business, or C2A, Special Conservation Business designation. As previously

discussed a case could be made in favor of the proposed rezoning providing that a ‘change’ has

occurred in the immediate neighborhood since the building was vacated. One could also argue

that the 2009 comprehensive plan’s proposed “recreational” use for the site mistakenly depicts

the use as the highest and best use of the property.

34

Annapolis land use attorney, Ben Wechsler with Linowes & Blocher explained the subject

property’s location within the historic district, and the public context of the property, would likely

result in considerable community involvement and/or opposition. The process would require

various public meetings to the Planning Commission, addressing various issues and points of

contention identified by city staff, the Commission, and the residents. Once the Planning

Commission is satisfied that all requirements have been satisfied, a recommendation for approval

would be made to the Board of Appeals for a final decision during another public hearing. The

anticipated timeframe for approval on the city level would range from four to six months.

The primary risk pertains to the likelihood of the opposition appealing the Planning Commissions

decision and subsequently the Board of Appeals decision. In the event a compromise could not be

reached at the Board of Appeals level, the matter would be heard by the Anne Arundel County

Circuit Court, a process that could conservatively delay the project for nine to twelve months. In

the event the Circuit Courts decision was appealed the issue would require a final decision by the

Special Court of Appeals, providing additional delays in the range of six to twelve months. The

legal costs associated with such a full blown adversarial rezoning process would range from

$100,000 to $200,000 and the process could be drawn out over a five years period45.

To mitigate the associated entitlement risk, it’s the intent of this proposal to enter a public-private

partnership with the city. Doing so would permit the city to rezone the parcel through an

administrative process, as municipalities are not subject to their zoning regulations46. The project

could be incorporated as part of the recently established Annapolis Economic Development

Corporation (AEDC), with the primary task of promoting economic development efforts through

a partial privatization approach. Annapolis Mayor Josh Cohen stated in a recent article “The

AEDC I envision will be working with a lot of businesses, recruiting them, shepherding them

through the process, but they’re going to need the support of planning and zoning, permits and

inspections to make things happen.” The city’s intent is to have the AEDC running by fall 2010,

35

with the initial focus on revitalizing the historic waterfront area, located within the context of the

subject site. Engaging the AEDC to enter a public/private partnership and lobbying the concept to

the alderman and community through a series of design charettes would prove pivotal in gaining

support for the project and significantly reduce the associated entitlement risk in rezoning the

subject property.

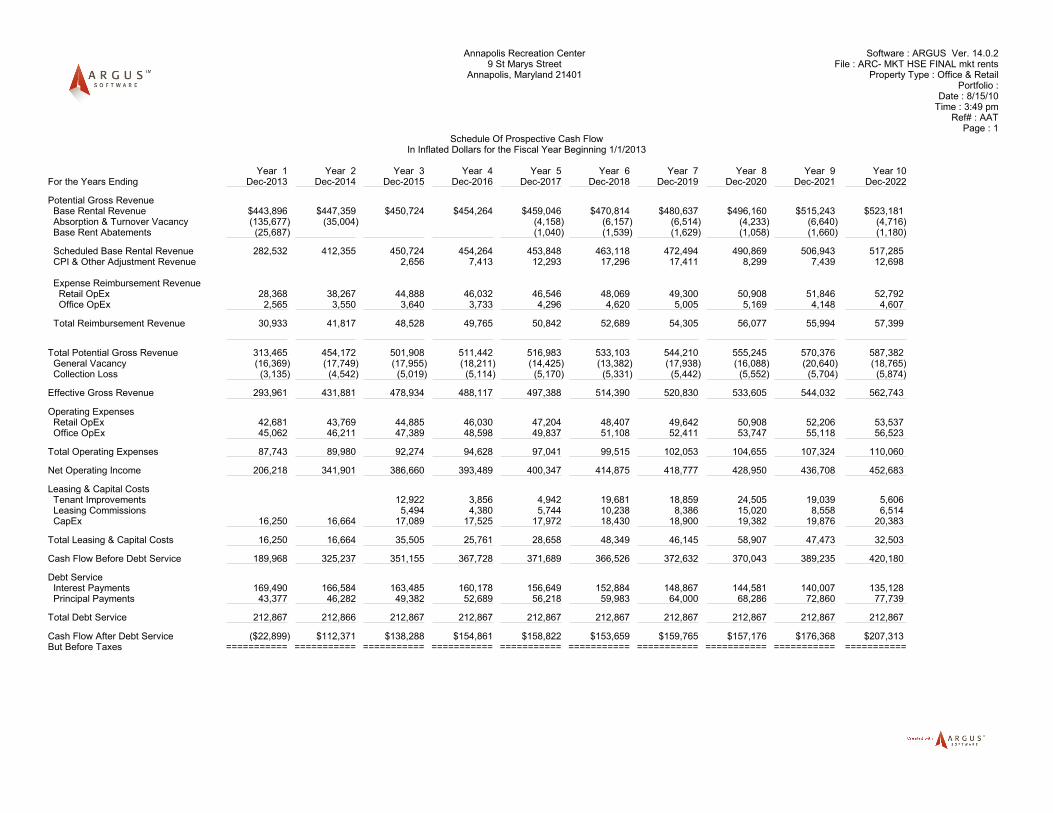

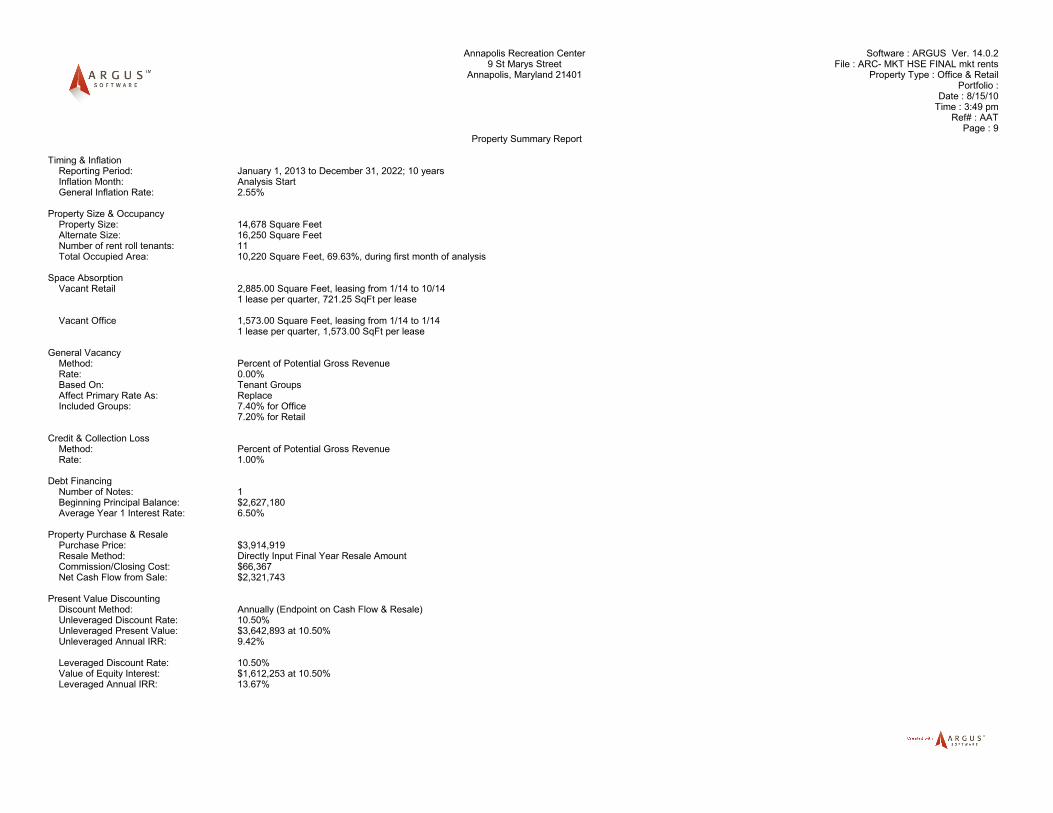

Mixed-Use Financial Analysis:

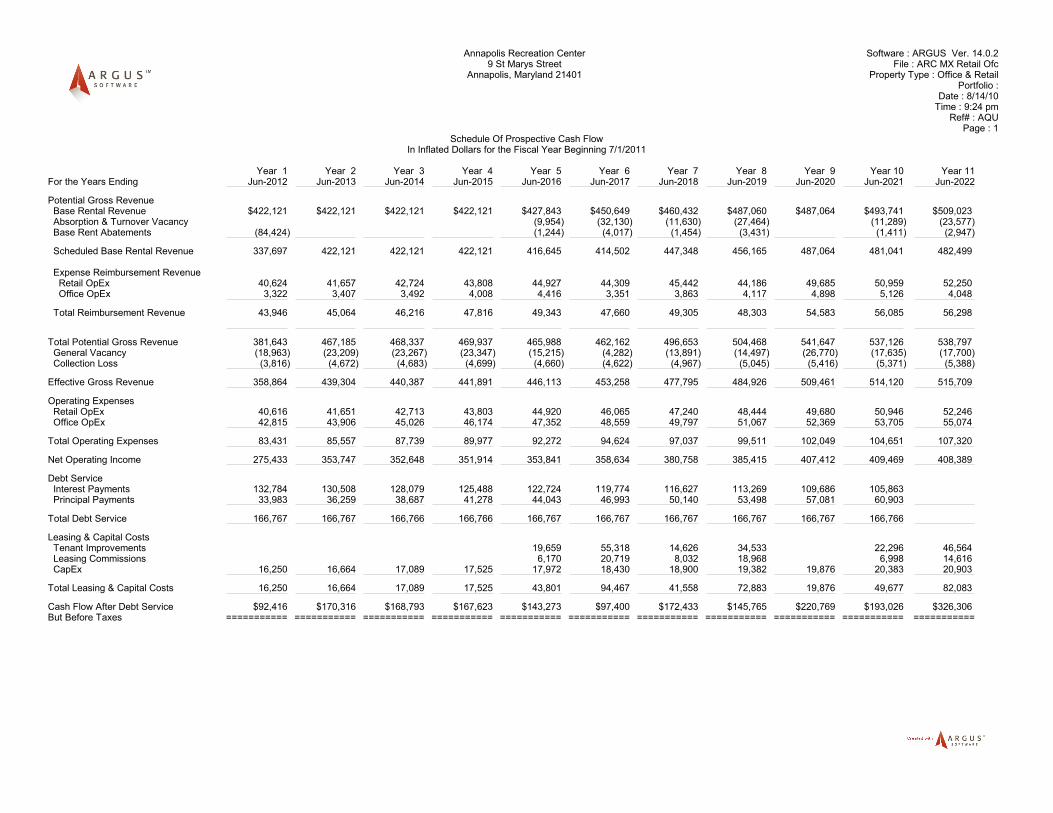

Many of the assumptions used in feasibility analysis will be utilized for the proposed end use.

Variations of note include the revised January 1, 2013 analysis start date that factors a 26-month

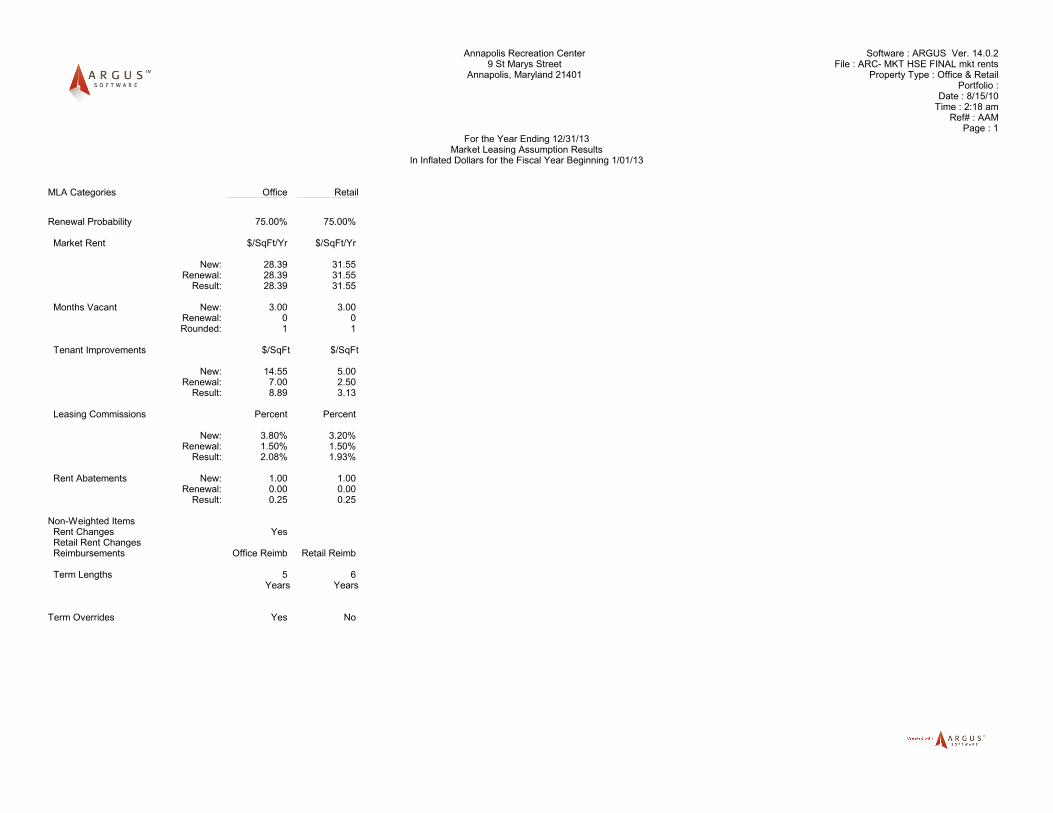

period for design, permitting and approvals, and an 18-month construction period. The income

and expense assumptions have accrued to reflect the 2.55% annual growth rate resulting in retail

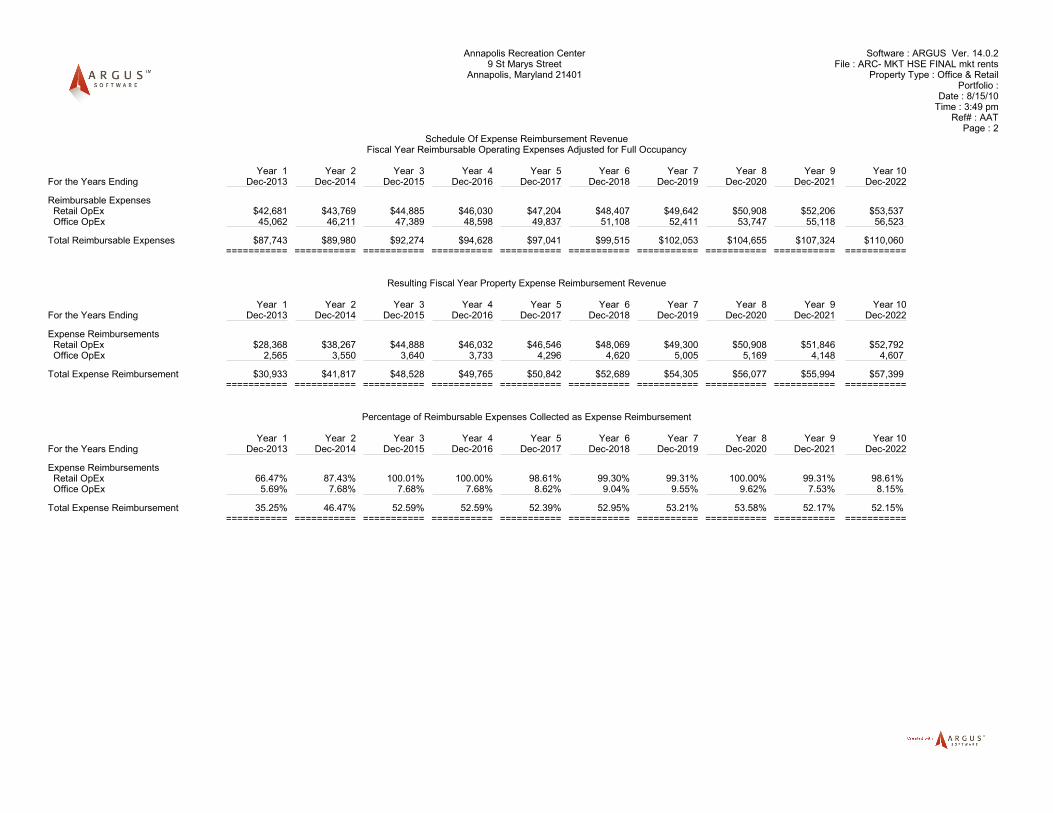

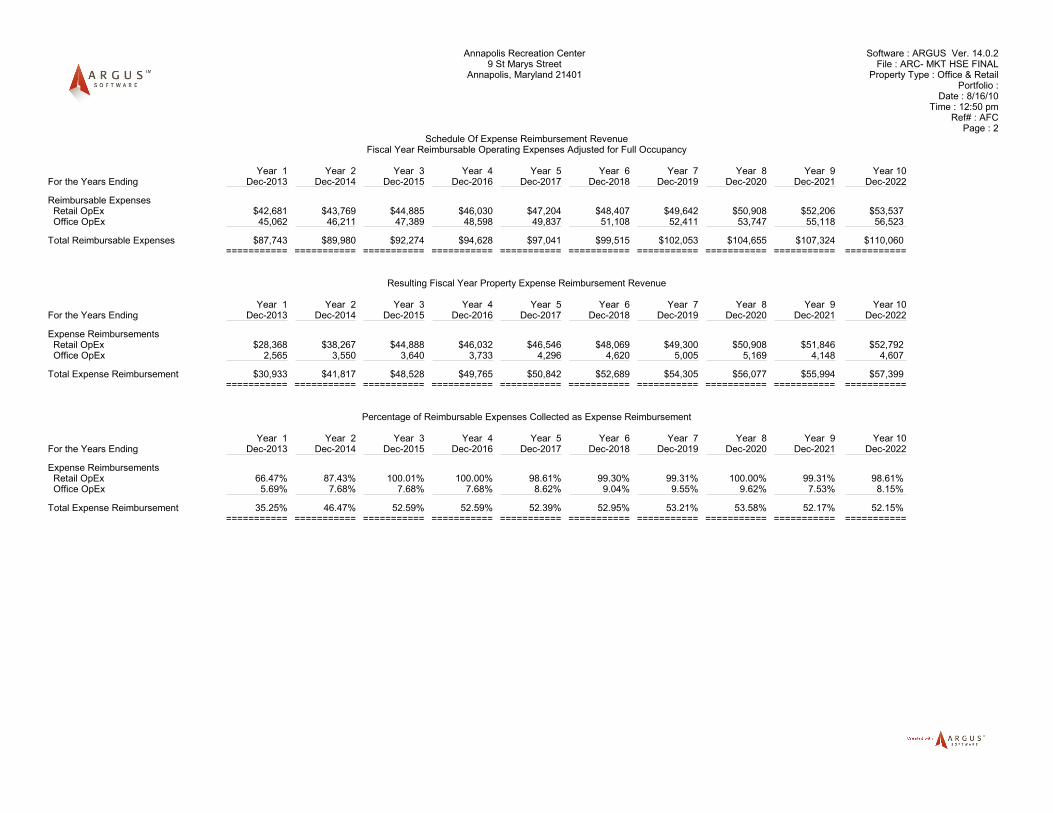

rents of $31.55 per SF and office rents of $28.39. Operating expenses for the retail portion were

inflated to $4.96 per SF with an average reimbursement of $4.24 per SF while office operating

expenses were modeled at $7.42 per SF with an average base stop of $6.85. Tenant improvement

allocations for the 1st floor of $10.15 per SF have been revised downward to $5.00 per SF to more

accurately represent the anticipated market place setting, while tenant improvements for the

office suites remain at $14.55 per SF.

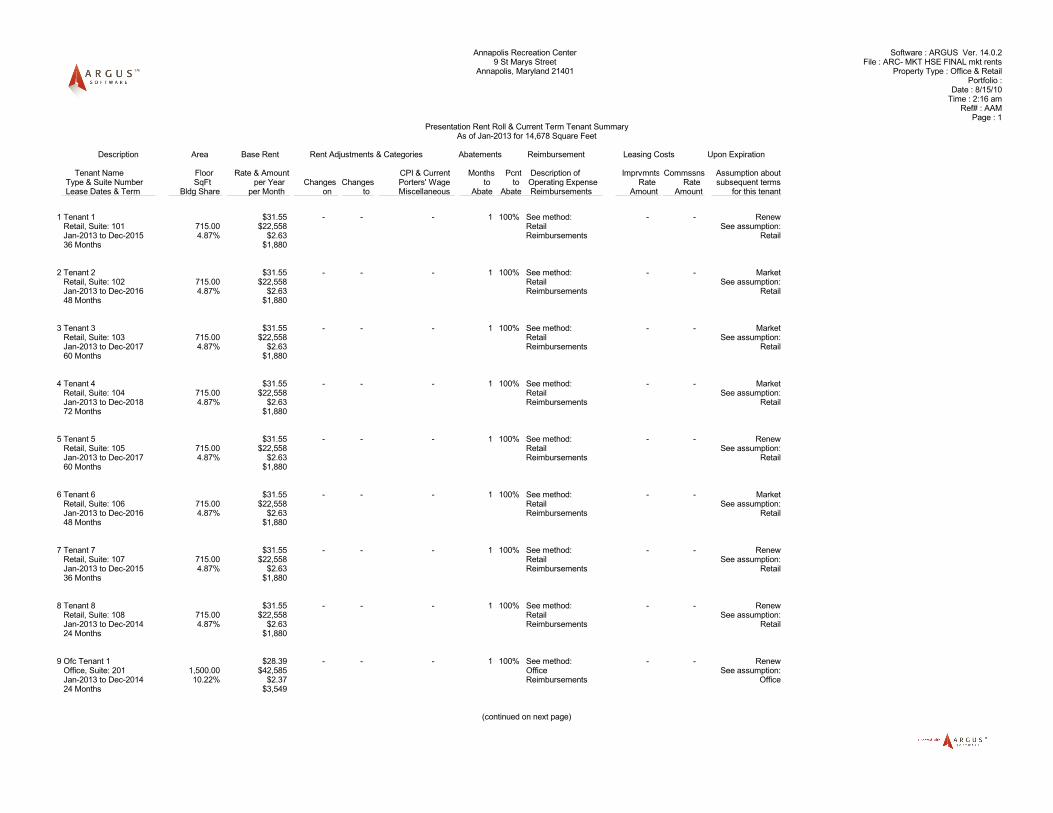

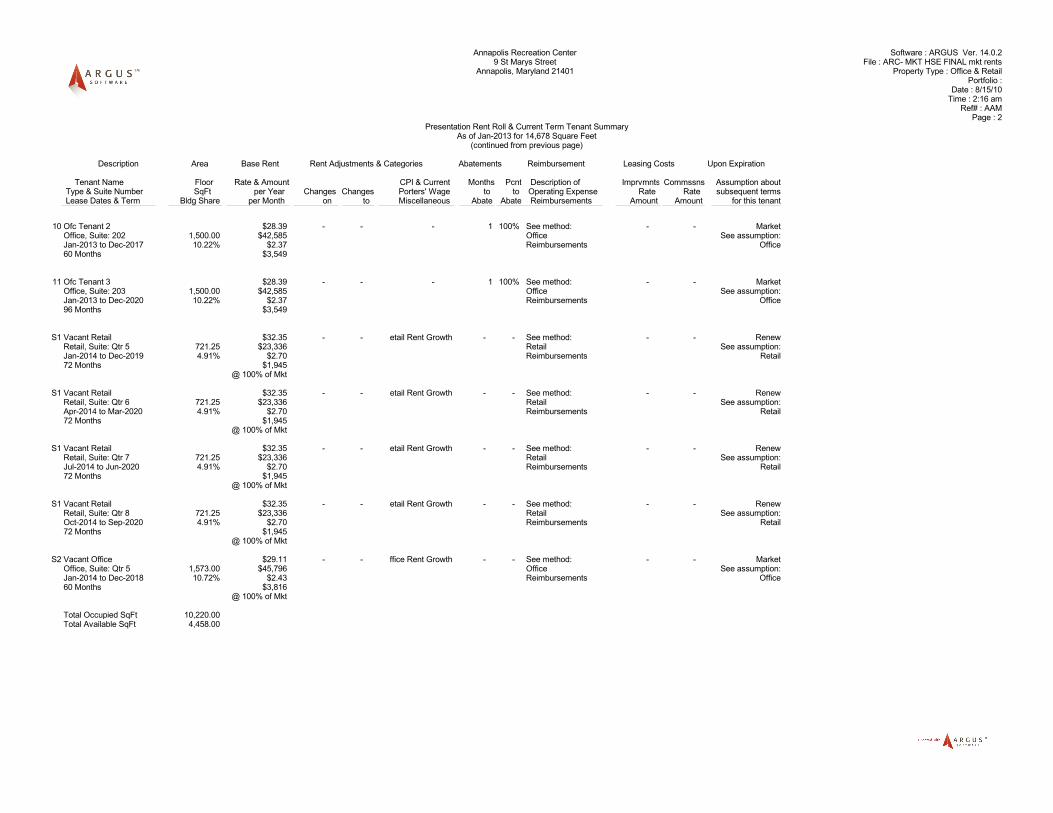

Incorporating the market house component affected the rent roll reflecting the reduced space

requirements of vendors, resulting in a total of twelve tenants each averaging 715 SF47. The office

suites will be comprised of four tenants each averaging 1,500SF. To address the associated

leasing risk, or the risk that forecasted absorption volume will not be realized, 70% or 10,274 SF

will be preleased, while and the remaining space will be absorbed over the course of the first two

years of the analysis. The market space has been modeled to absorb four tenants at a rate of one

lease per quarter beginning January 2014, while the office suites will absorb one tenant on a

quarterly basis beginning the same time. To further stabilize the projected cash flows, tenant lease

36

terms have been staggered to moderate the rollover impact on cash flow for any given year. The

remaining assumptions reflect the data provided in the valuation and feasibility analysis for the

mixed-use model.

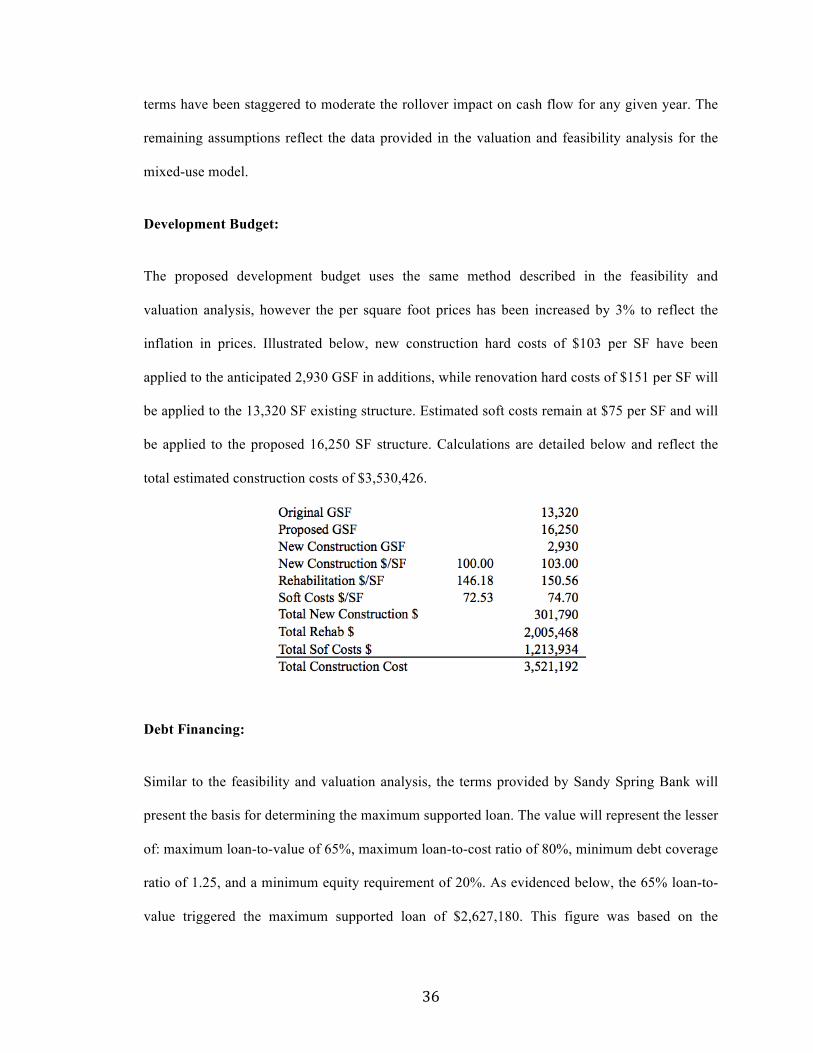

Development Budget:

The proposed development budget uses the same method described in the feasibility and

valuation analysis, however the per square foot prices has been increased by 3% to reflect the

inflation in prices. Illustrated below, new construction hard costs of $103 per SF have been

applied to the anticipated 2,930 GSF in additions, while renovation hard costs of $151 per SF will

be applied to the 13,320 SF existing structure. Estimated soft costs remain at $75 per SF and will

be applied to the proposed 16,250 SF structure. Calculations are detailed below and reflect the

total estimated construction costs of $3,530,426.

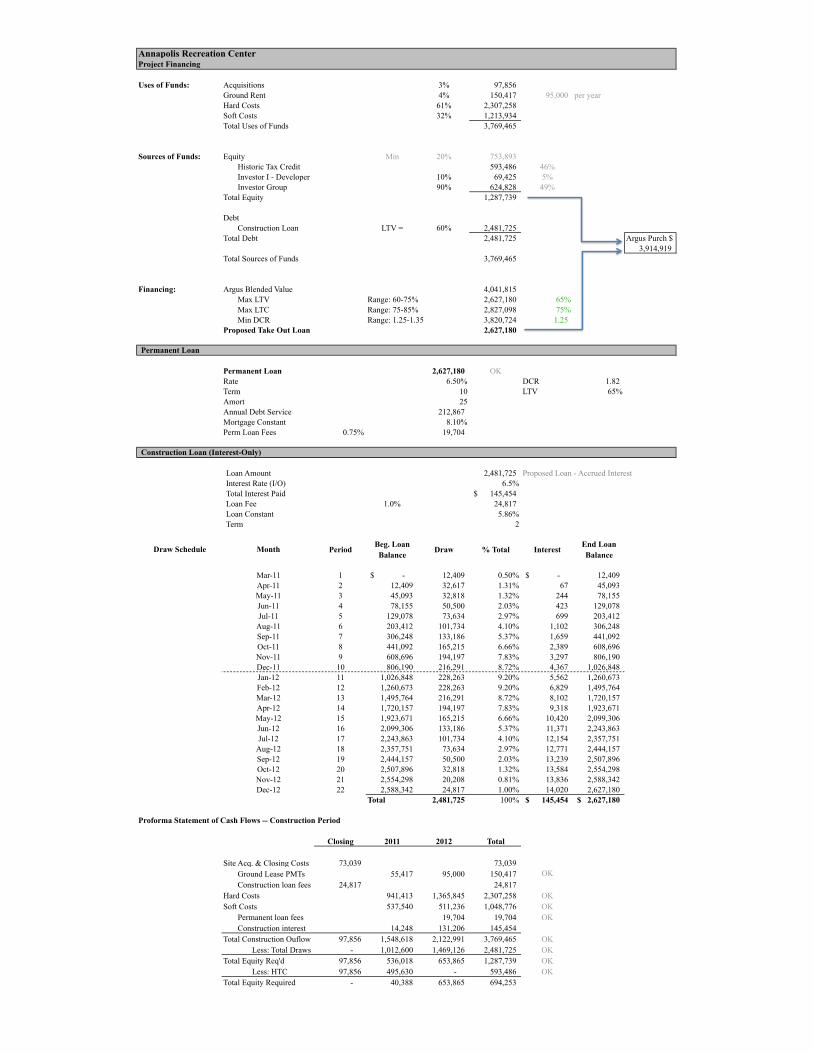

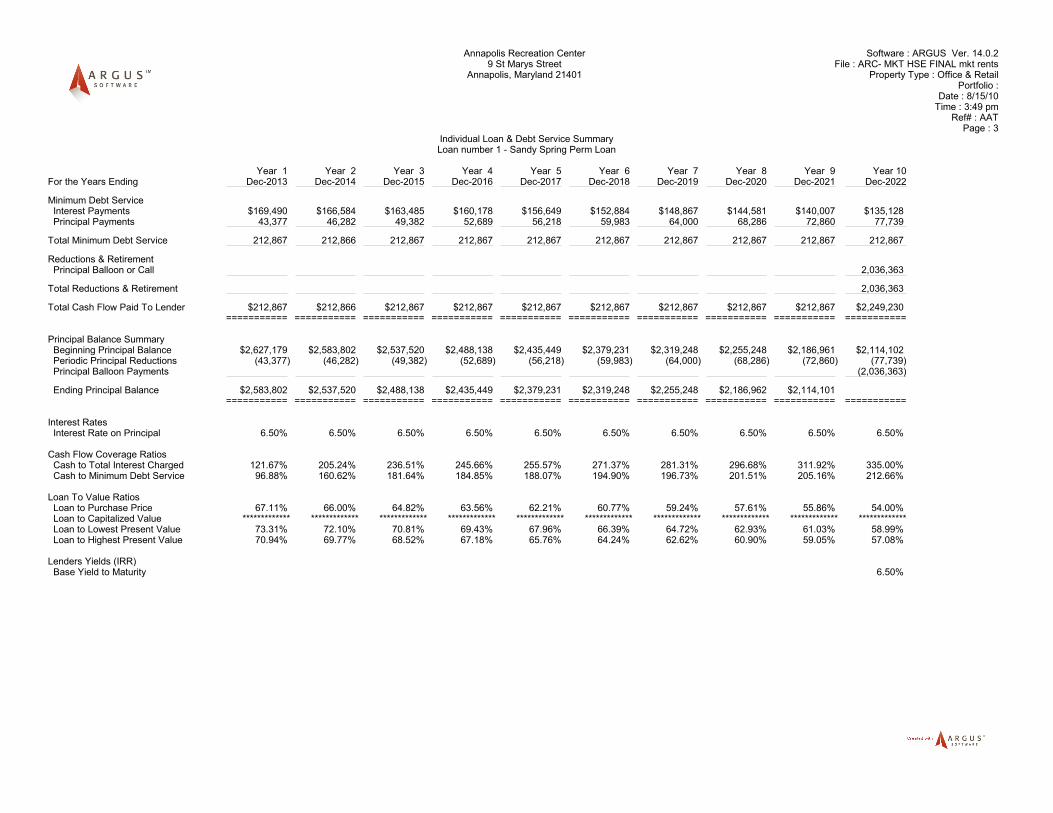

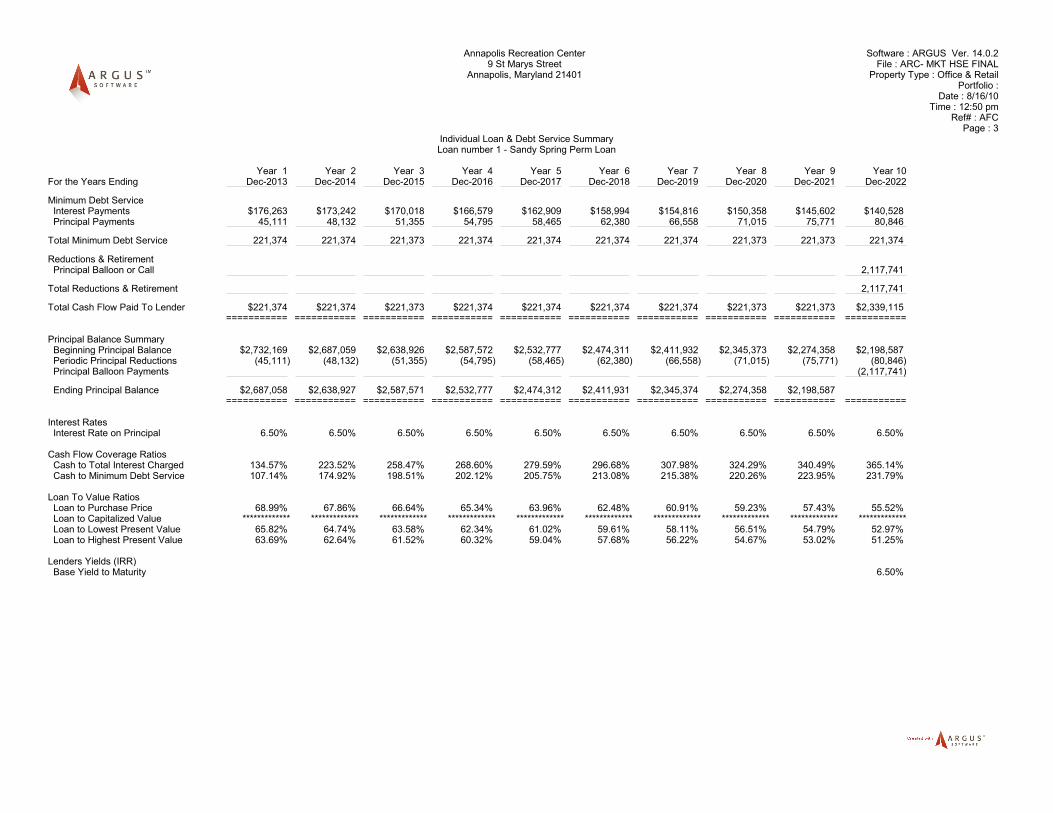

Debt Financing:

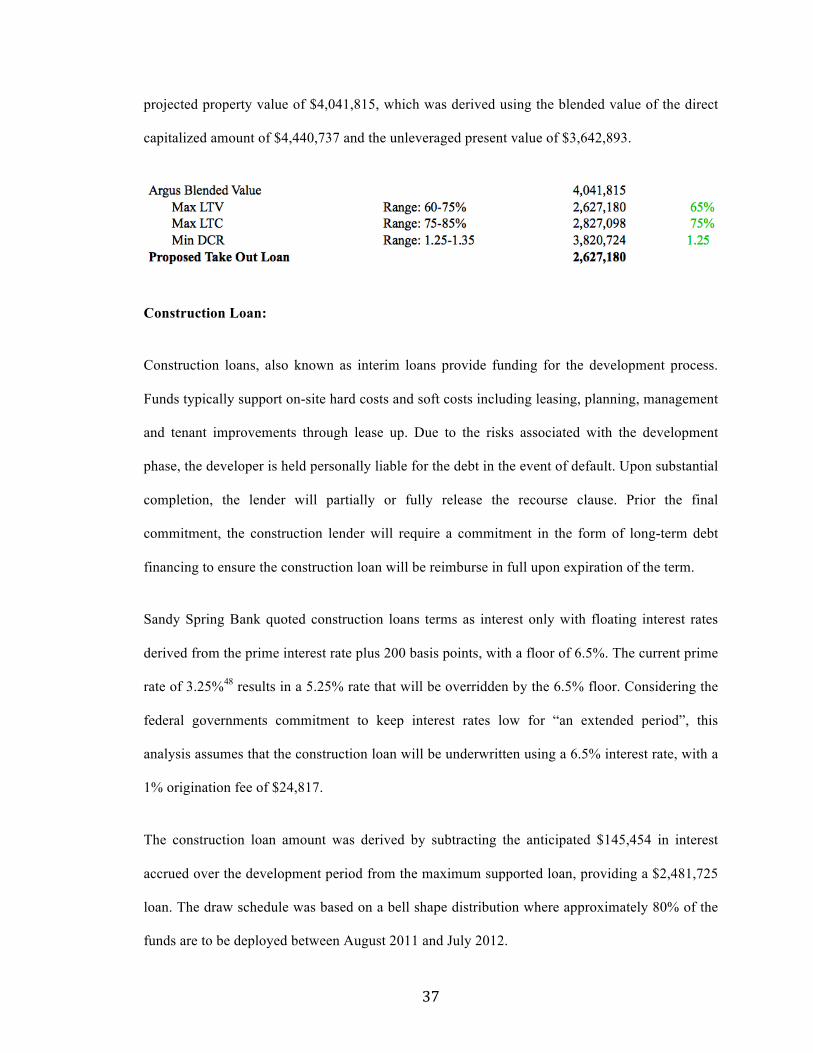

Similar to the feasibility and valuation analysis, the terms provided by Sandy Spring Bank will

present the basis for determining the maximum supported loan. The value will represent the lesser

of: maximum loan-to-value of 65%, maximum loan-to-cost ratio of 80%, minimum debt coverage

ratio of 1.25, and a minimum equity requirement of 20%. As evidenced below, the 65% loan-to-

value triggered the maximum supported loan of $2,627,180. This figure was based on the

37

projected property value of $4,041,815, which was derived using the blended value of the direct

capitalized amount of $4,440,737 and the unleveraged present value of $3,642,893.

Construction Loan:

Construction loans, also known as interim loans provide funding for the development process.

Funds typically support on-site hard costs and soft costs including leasing, planning, management

and tenant improvements through lease up. Due to the risks associated with the development

phase, the developer is held personally liable for the debt in the event of default. Upon substantial

completion, the lender will partially or fully release the recourse clause. Prior the final

commitment, the construction lender will require a commitment in the form of long-term debt

financing to ensure the construction loan will be reimburse in full upon expiration of the term.

Sandy Spring Bank quoted construction loans terms as interest only with floating interest rates

derived from the prime interest rate plus 200 basis points, with a floor of 6.5%. The current prime

rate of 3.25%48 results in a 5.25% rate that will be overridden by the 6.5% floor. Considering the

federal governments commitment to keep interest rates low for “an extended period”, this

analysis assumes that the construction loan will be underwritten using a 6.5% interest rate, with a

1% origination fee of $24,817.

The construction loan amount was derived by subtracting the anticipated $145,454 in interest

accrued over the development period from the maximum supported loan, providing a $2,481,725

loan. The draw schedule was based on a bell shape distribution where approximately 80% of the

funds are to be deployed between August 2011 and July 2012.

38

Permanent Loan:

Permanent, or take out loans from Sandy Spring Bank base the interest rate on 5-year treasuries

plus a 400-450bps spread, with a 6.5% floor. Currently, 5-year treasury notes are yielding

1.457%49 plus a 450bps spread provides a suggested rate of 5.96%, which would be overridden

by the 6.5% floor. Although the rate won’t be locked in until construction nears completion, this

analysis assumes an interest rate of 6.5%. Permanent loan fees due at origination were quoted

between 50-100bps, where for the purpose of this analysis a 75bps or $19,704 fee has been

applied. Lastly the loan will be amortized over a 25 years period with a term of 10 years.

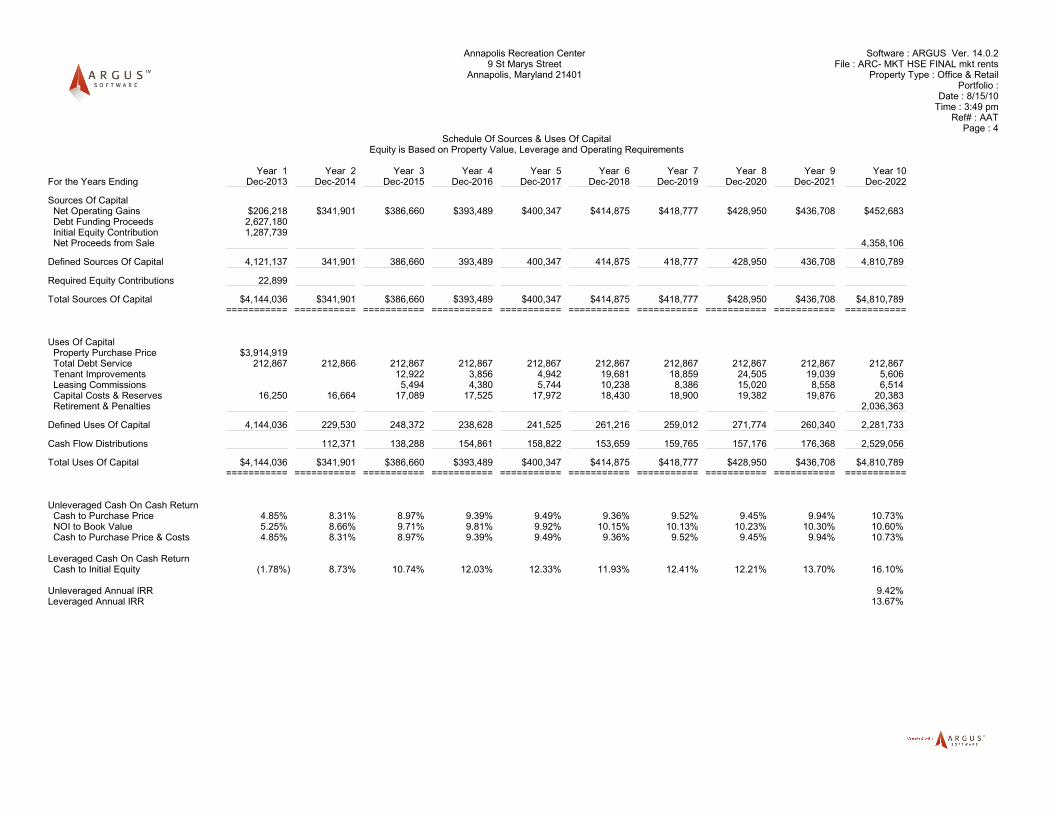

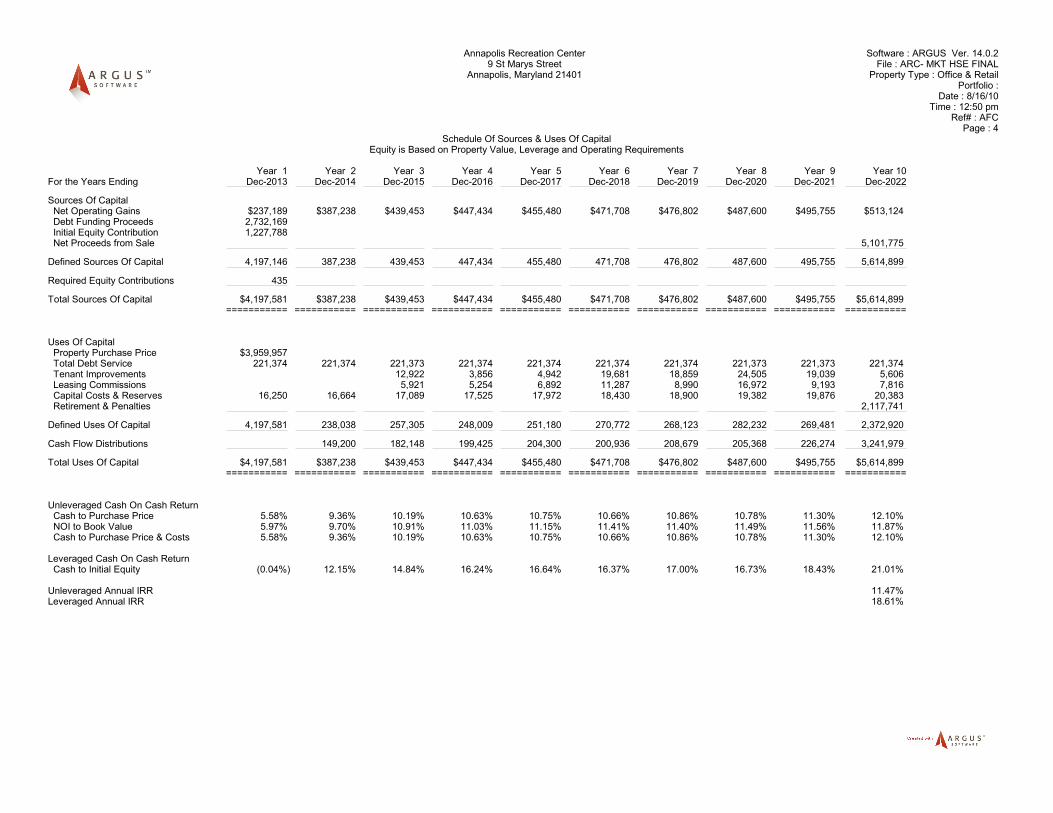

Initial Equity Requirement & Returns:

The initial projected development budget of $5.53m accounts for the derived $2.03m acquisition

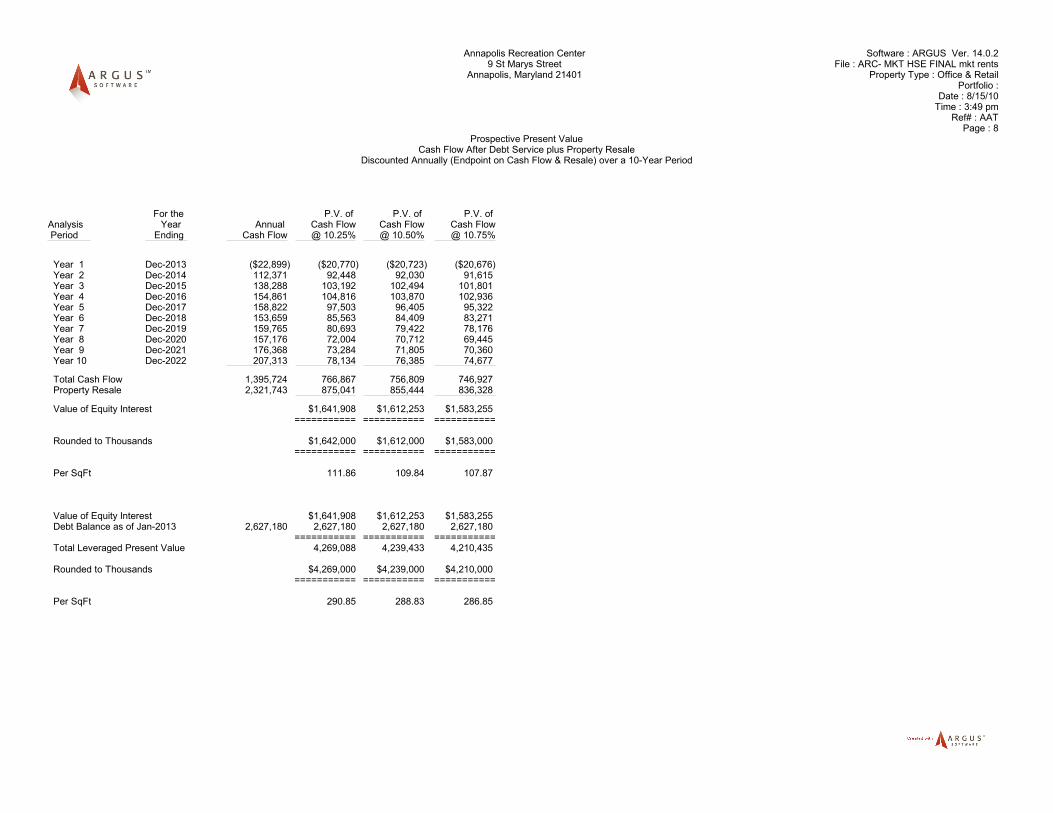

cost, hard costs of $2.3m, and $1.2m in related soft costs. Applying the $2.48m construction loan

reveals a funding gap of $3.05m. Running the discounted cash flow to determine the assets

performance over a 10-year hold period reveals leveraged internal rate of return of 5.24%.

Accounting for the fact that equity investors could earn 6% in stock market50, and mezzanine and

hard money investors require returns ranging from 12-25%51, the project as structured is deemed

unfeasible at this time.

Alternative Financing Strategies:

At this point, we will reassess and explore alternative options to reduce the equity requirement,

increase projected returns, and ultimately present a viable development option for the subject site.

Specifically, we will analyze and incorporate the following two concepts: 1) federal and state

rehabilitation tax credits, and 2) supplementing a ground lease in place of purchasing the

property.

39

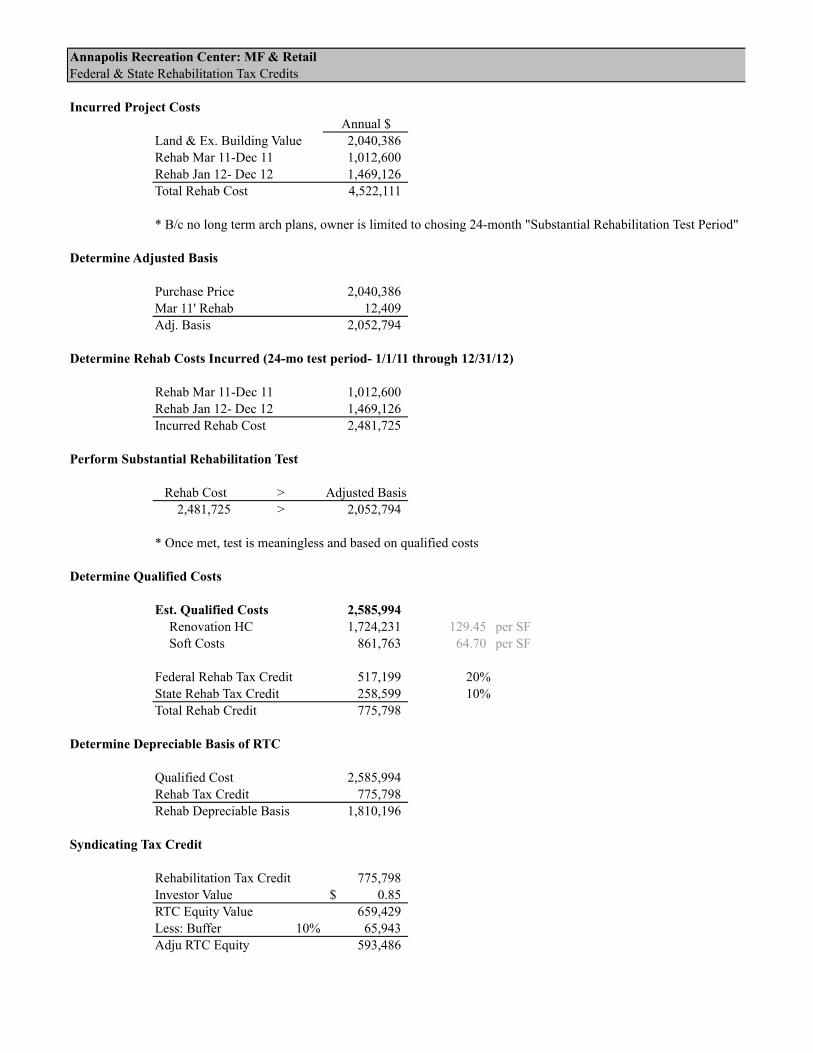

Rehabilitation Tax Credits:

The benefit of the subject property being within a designated historic district is it qualifies for the

20% Federal Rehabilitation Tax Credit and an additional 10% credit from the state of Maryland.

The cumulative 30% tax credit is applied to the “qualified rehabilitation costs” which include:

hard construction costs incurred for rehabilitation of existing structure, tenant improvements,

construction contingency, architectural and engineering fees, environmental remediation,

appraisal and market study, permit and bond fees, insurance, accounting and tax credit cost

certification, legal fees, preservation consultant, tax credit fees, financing fees, construction

interest, and the developer fee52 (Detailed in Appendices 2 & 5).

Isolating the qualified costs in the proposed development budget results in an estimated qualified

rehabilitation cost of $2,585,994. Applying the 20% Federal tax credit accounts for a $517,199

credit, while the 10% state credit will account for $258,599, providing a total tax credit of

$775,798. The tax credit can be applied as a reduction in the recipients annual tax liability, or as

up front equity to the project, with the final decision based on the alternative that creates the

highest value to the developer.

If the credit were applied to reduce tax liability, once the rehabilitation work is completed and

certified by the National Parks Service, the total credit amount would be applied on an annual

basis, dollar-for-dollar, over a five-year period. The other option reflects the intent of this

proposal and involves the developer selling the credit to a tax credit investor, who in turn uses the

credit to offset alternative tax liabilities. In exchange, the developer realizes the proceeds as

additional equity to the project. To compensate for the risk associated with acquiring the ‘future

benefits’ of the credit, tax credit investors are currently paying $0.85 on the dollar53 providing an

equity value of $659,423. To account for the inclusion of potentially unqualified costs, the equity

value has been reduced by a 10% resulting in a total equity value of $593,486.

40

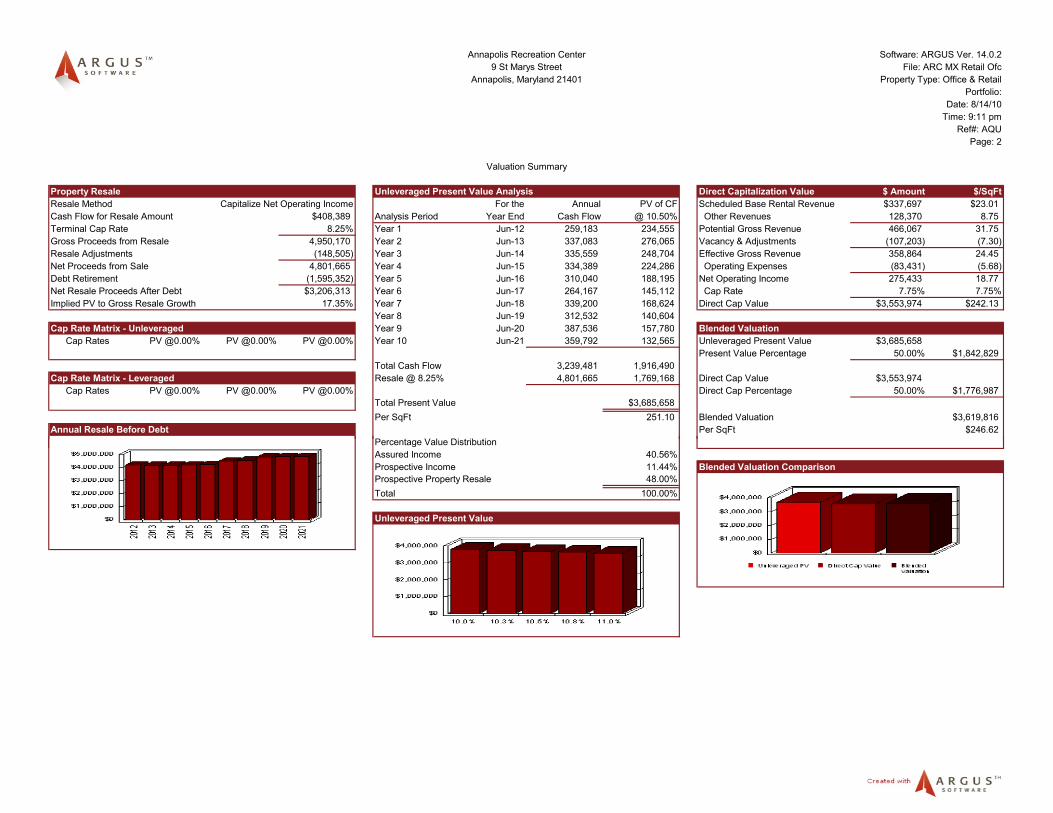

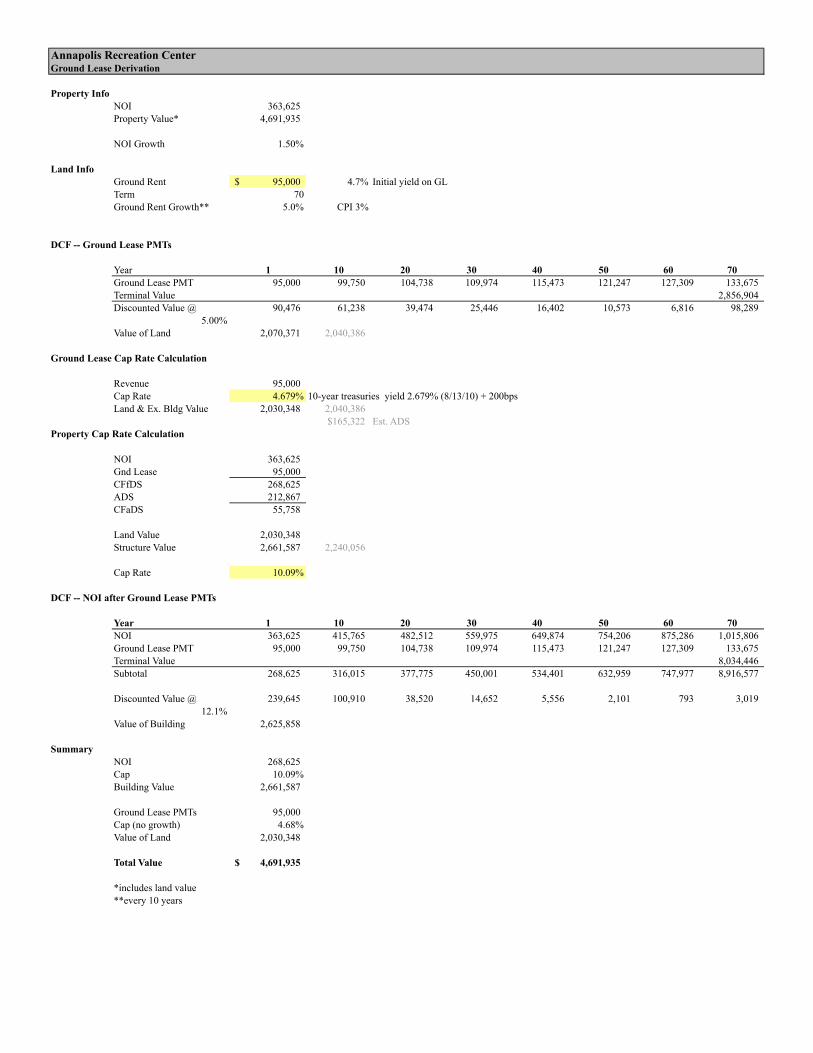

Ground Lease:

To further reduce the equity requirement, the acquisition cost of the property has been replaced

with a long-term ground lease. Detailed in Appendix F, the projection analyzes the expected NOI

and annual growth rate in conjunction with the derived $2.03m property value as the basis for

supporting the derived annual ground lease payment. Project data derived from the Argus

discounted cash flow portrayed in Appendix H, results in a year one NOI of $363,62513 with a

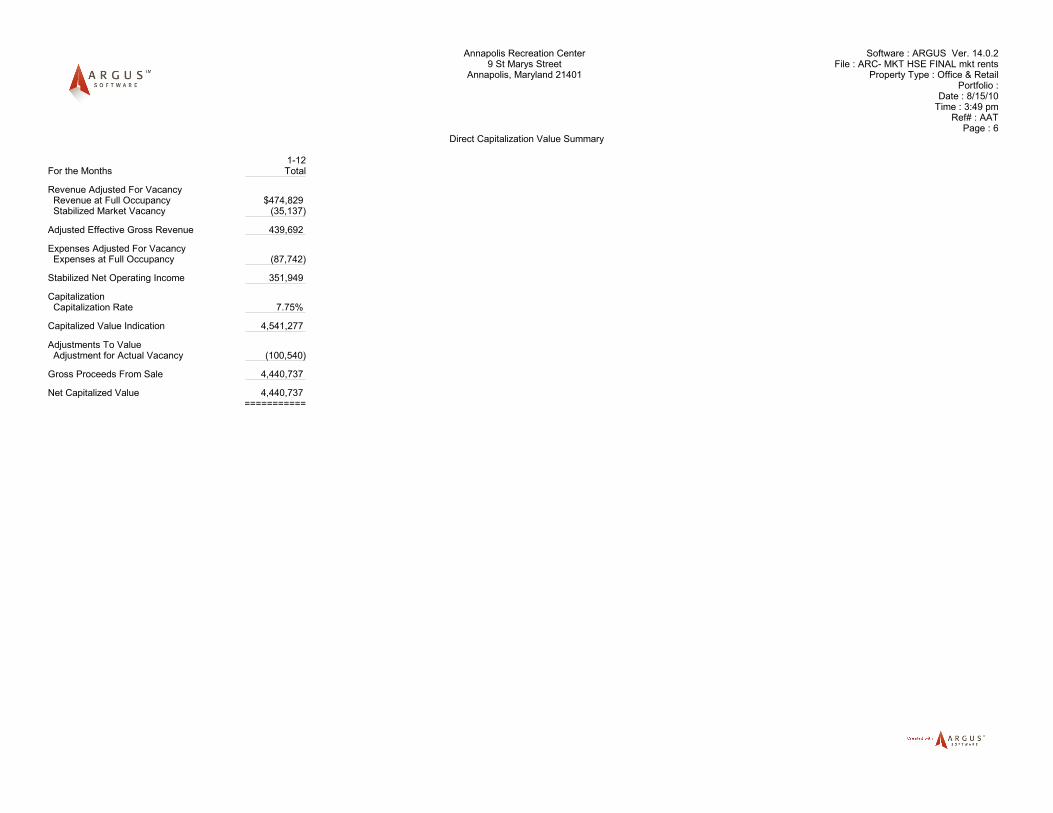

projected annual growth of 1.5%. Capitalizing the NOI at a going in rate of 7.75% provides an

assessed property value of $4.7m in 2013. The derived annual ground lease payment of $95,000

was backed into assuming a renewable 70-year term, where the land rent has been modeled to

grow in increments of 5% every ten years. The modest growth rate is intended to reflect the long-

term average inflation rate of 3%54 with a risk premium 200bps premium. Modeling the

anticipated payments over the term and capitalized in the 70th year derives a terminal value of

$2,856,904. Accounting for the time value of money, the cash flows and reversionary ground

lease value are discounted at 5%14 to derive a $2,070,371 present value of the existing land and

building, corresponding with the derived $2,031,420 property value. Capitalizing the $95,000

ground lease payment at 4.68%15, reflects the city’s anticipated return, and results in a present

value of $2,030,348.

The accuracy of the ground lease payments is then verified by incorporating the NOI into the

projection above to derive a value of the structure. Assuming a nominal annual growth rate of

1.5% over the 70-year lease term, a terminal value is derived by capitalizing the 70th year NOI

using a 10.09%. Next, the annual subtotals are discounted by 11.6% to derive the structures

present value of $2,661,587. To prove the validity of the calculations, we ensure the sum of the

13 Adjusted NOI omits absorption & turnover vacancy, base rent abatements, and credit loss 14 Discount rate = Risk Free Rate (10yr T-Bills) + Investments Risk Premium 15 Total return = risk free rate (2.68%) + risk premium (200 bps)

41

present value of the property and the proposed building reflects the direct capitalize value of

$4.7m.

The ground lease arrangement provides an annual obligation of $95,000 for the leasehold interest

in the property versus the estimated annual debt service of $170,000 16 associated with acquiring

the fee simple interest. The resulting impact reduces the equity requirement by the assessed value

of the property. Applying the ground lease payment to the discounted cash flow model however,

reveals that the vast majority of the cash flow after debt service is consumed by the ground lease

obligation. As a result, the preferred returns to the equity investors are severely constrained,

presenting a risk that investors may seek alternative investments.

An alternative strategy reflected in the final analysis partitions the available annual cash flows

using a 60/40 split. Under this arrangement, the city would be entitled to 60% of the annual net

cash flow to satisfy the ground lease obligation, while the remaining 40% will be reserved for

distribution to equity investors. Instances where available cash flow insufficiently covers the

ground lease payments, the unpaid balance would carry over to subsequent years. Upon reversion,

the cumulative unpaid ground lease balance would be reimbursed from the net sales proceeds. As

modeled, other than the first year where net cash flow are projected to be negative, the cash flow

allocations in the second year are projected to cover 71% of the annual payment increasing to

98% by year four.

From the city’s perspective, the asset currently doesn’t produce any economic benefit to the city,

and it would not be unreasonable to assume the 60% distribution in exchange for a steady long-

term revenue source. Additionally, the city would reap the various indirect benefits such as the

increased sales and property tax revenue, job creation, rebranding of the city dock area, and the

elimination of a blighted vacant property. As a partner in the project, the city would also benefit

16 Assumes 100% financing at 6.5% amortized over 25 years.

42

from providing an essential service to the community that currently doesn’t exist, while also

recapturing lost revenues spent outside the city. Lastly, the ground lease option preserves the

ownership and equity interest that the city has vested in the asset. With a cost basis of $1.00, the

city will realize benefit from the annual rent payments return, while retaining the fee simple

interest in the asset.

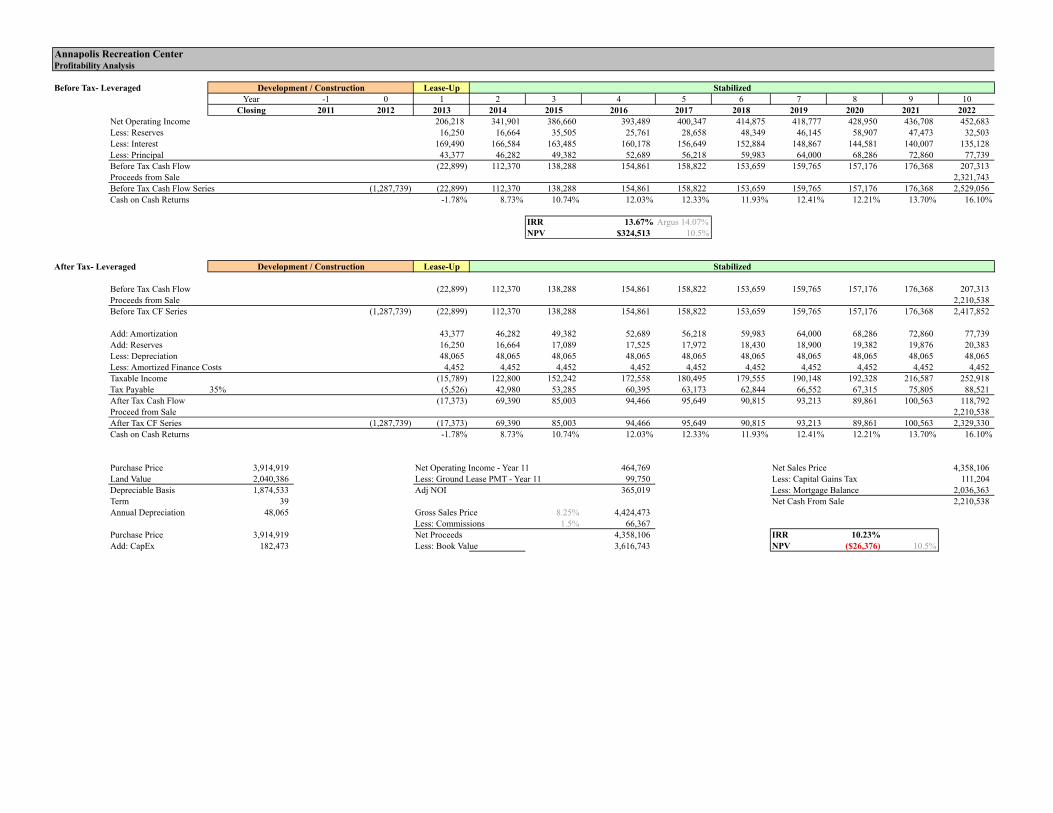

Profitability Analysis:

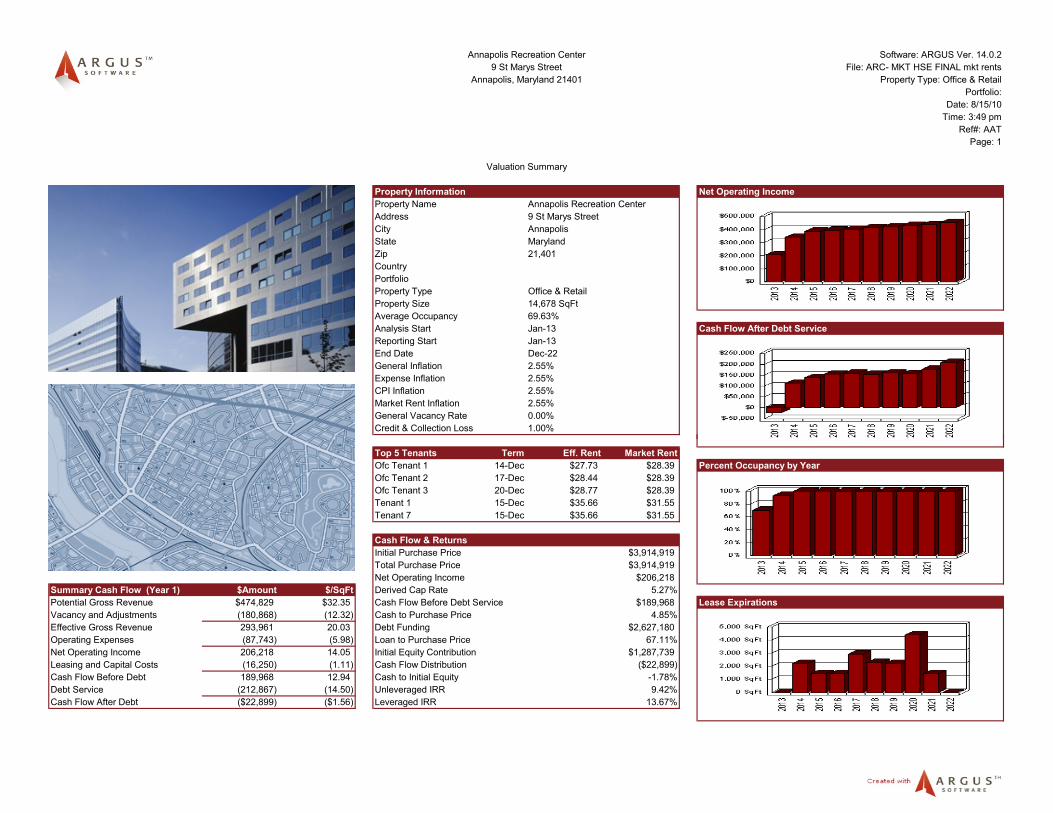

Pursuing a ground lease through a public-private partnership reduces the equity requirement to

$1.3m. Applying the $593,486 equity value of the rehabilitation tax credit reduces the cash equity

requirement to $694,253. The revised stabilized discounted cash flow detailed in Appendix H

incorporates the market assumptions detailed previously as well as the $2,627,180 loan provided

by Sandy Spring Bank. Modeled based on a 10-year hold period commencing January 2013, the

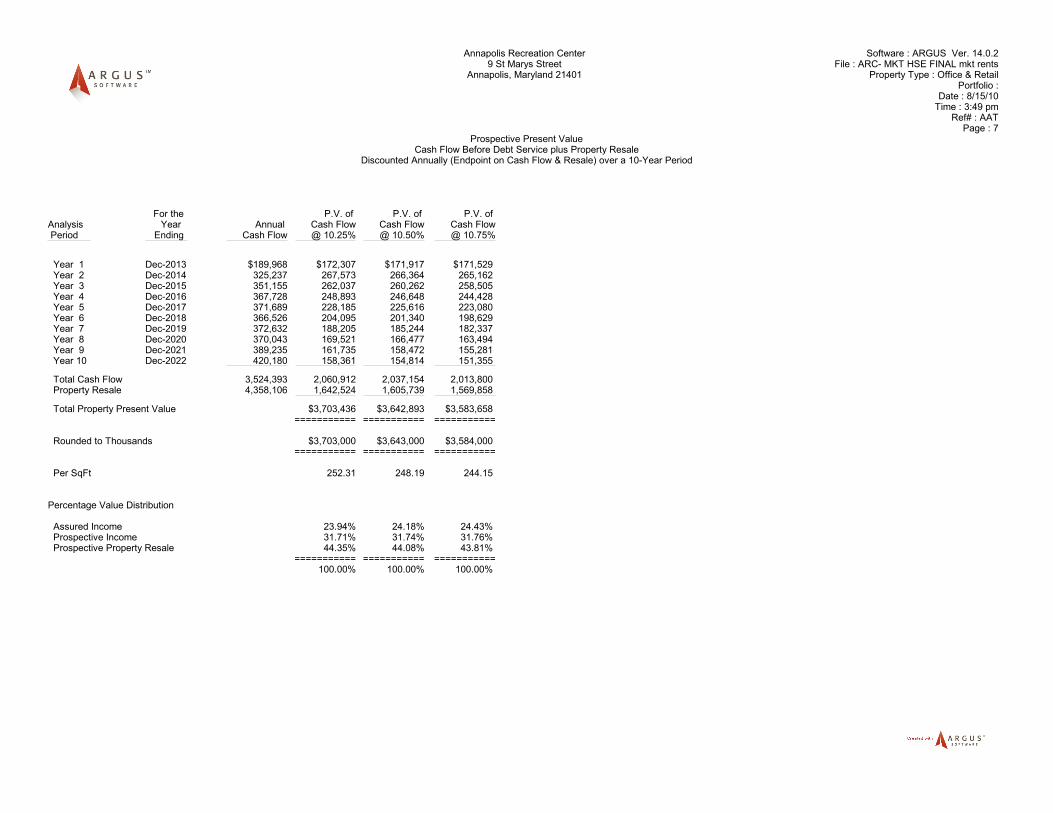

property provides a positive net present value of $324,513, an unleveraged internal rate of return

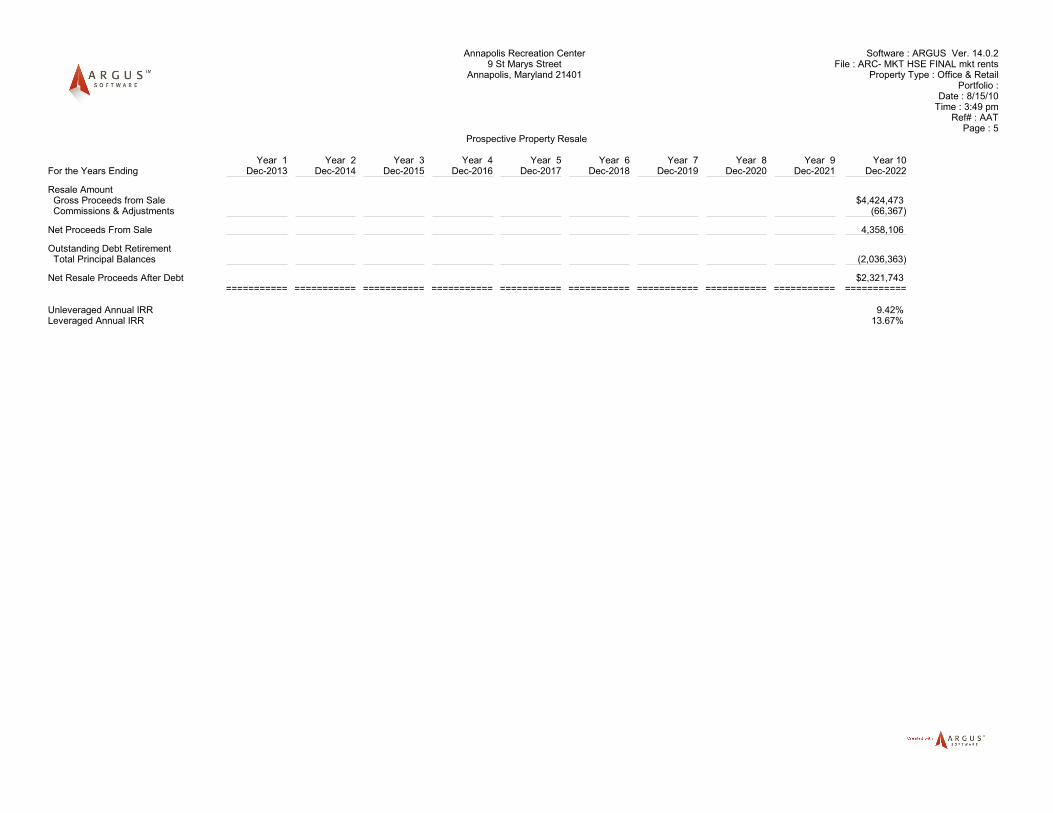

of 9.42%, and leveraged internal rate of return of 13.67%, reflecting the role of positive leverage.

Partitioning the IRR reveals a relatively balanced distribution where 24% accounts for assured

value, 32% is devoted to prospective income, and the remaining 44% is based on the proceeds

realized from reversion. Leveraged cash on cash returns, or the cash flow after debt service

divided by the initial equity investment increases from negative 1.78% in year one to 12.33% in

year five and 16.1% in year ten. The negative return in year one primarily reflects the allocation

of $136,000 for vacancy and absorption turnover and $26,000 in base rent abatements.

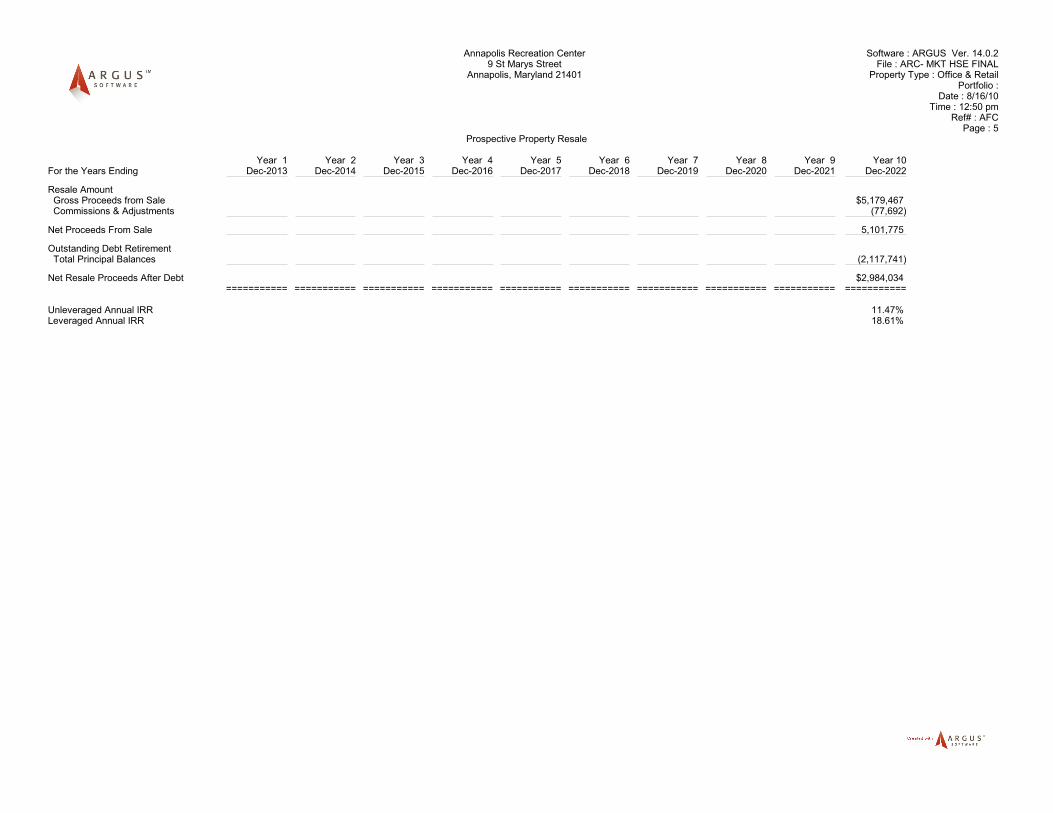

Accounting for the ground lease obligation, reversionary value was based on a modified year

eleven NOI, reduced by the $99,750 ground lease obligation. Capitalized using an 8.25% terminal

capitalization rate reveals a projected gross sales price of $4,424,473.

43

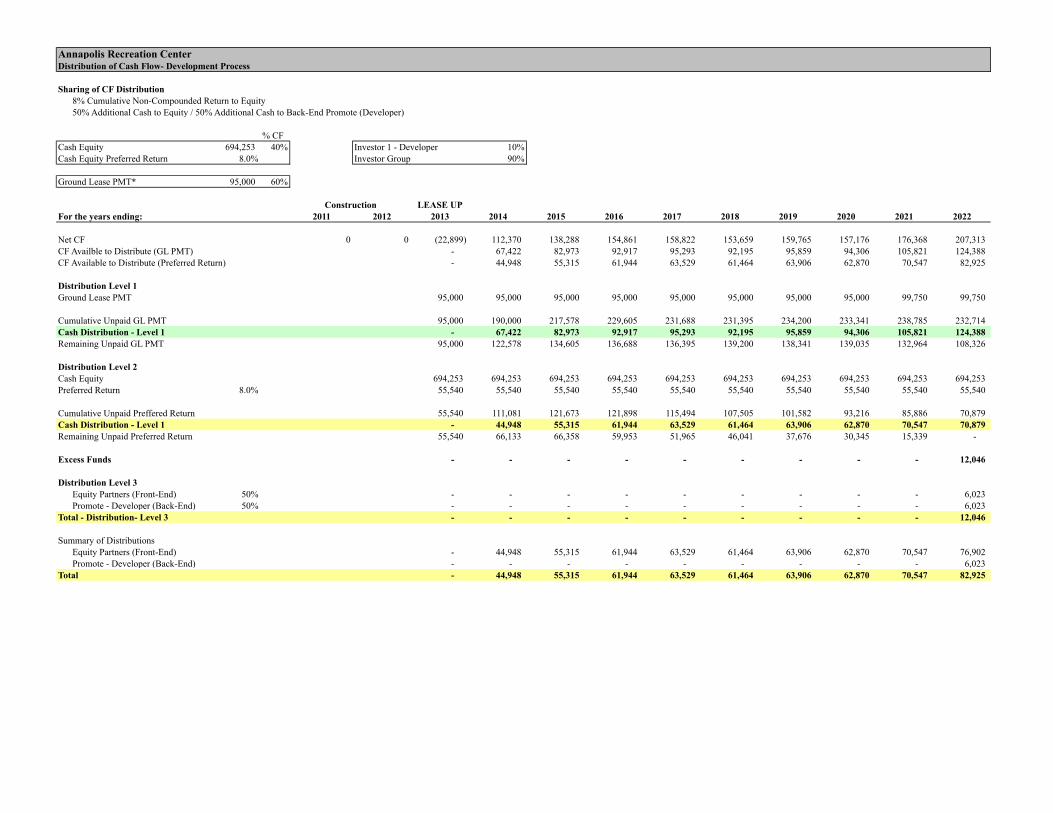

Equity Distribution:

The $1,287,739 equity component is comprised of three components: the rehabilitation tax credit

equity of $593,486 accounts for 46%, the developer’s 5% contribution of $69,525, and the

investor groups $624,828 accounts for the remaining 49%. The nominal contribution by the

developer is predicated on the equity contribution realized through the tax credit.

Detailed in Appendix J, the equity investors are entitled to 40% of the net cash flow. The equity

obtained from the tax credit has been excluded from distribution, resulting in total cash equity for

distribution of $694,253. Distributions are allocated on a pari-passu basis where the developer

accounts for 10% and the investor group accounts for the remaining 90%. Annual cash flow

distributions are based on two distribution levels. The first level reflects an annual 8% cumulative

non-compounding return to the equity, equating to $55,540. In the event of cash flow shortages,

unpaid preferred returns carry over to subsequent years. Once cash flows are sufficient enough to

cover the preferred return and the accumulated unpaid preferred returns, the second distribution

level is applied. The excess funds are split 50/50 between the equity partners (front end) and the

developer as a back-end promote.

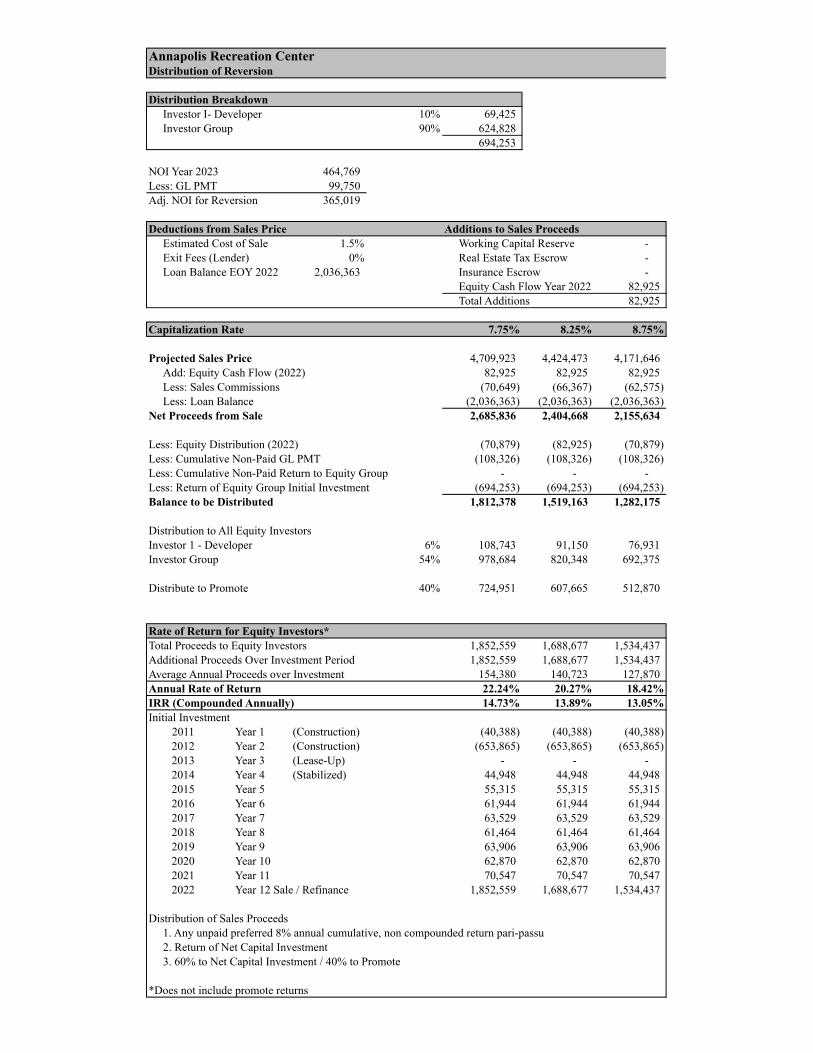

Upon reversion, the sales commission and the outstanding loans balance are deducted from the

gross sales price. The remaining net sales proceeds are distributed in three levels. First, any

unpaid cumulative preferred return and/or unpaid cumulative ground lease payments are

reimbursed. As illustrated in Appendix K, the city will be reimbursed the $108,326 in outstanding

ground lease payment. Once the city has bee compensated, their participation in the equity

distribution has been fulfilled and the remainder will be distributed among the equity partners.

The second distribution returns the investors net capital investment. The third level distributes the

remaining balance of $1.52m, split 60/40, where the equity partners receive 60% distributed pari-

passu, and the developer receives the remaining 40%.

44

The return analysis has been based on the assumption that $40,388 in equity will be deployed in

2011 and the remaining $653,865 in 2012. Projected average annual returns to the equity

investors reflect 20.27% correlating to an annually compounded internal rate of return of

13.89%17. Considering the limited risk and modest equity requirements associated with the

project, the projected returns are considered to be in line with equity investors’ expectations.

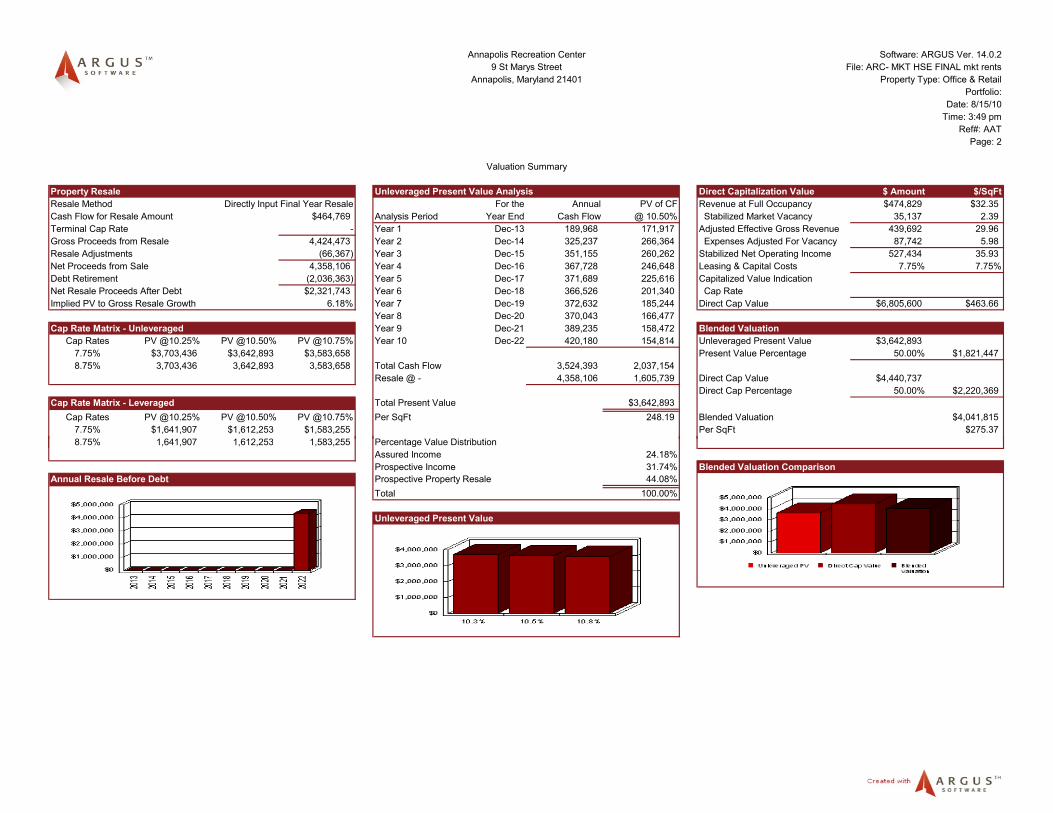

Sensitivity Analysis:

A sensitivity analysis has been incorporated in the equity distribution from a sale in 2022, where

the underwritten 8.25% terminal capitalization rate was tested using at 7.75% and 8.75% rate. In

the event the property traded for a 7.75%, average annual returns to equity would increase by

200bps or 22.24%. The annually compounded internal rate of return would reflect and increase of

84bps to 14.73%. If market conditions caused the property to trade at an 8.75% terminal

capitalization rate, the annual rate of return would decrease by 200bps to 18.42% and the internal

rate of return would be revised downward 84bps to13.05%.

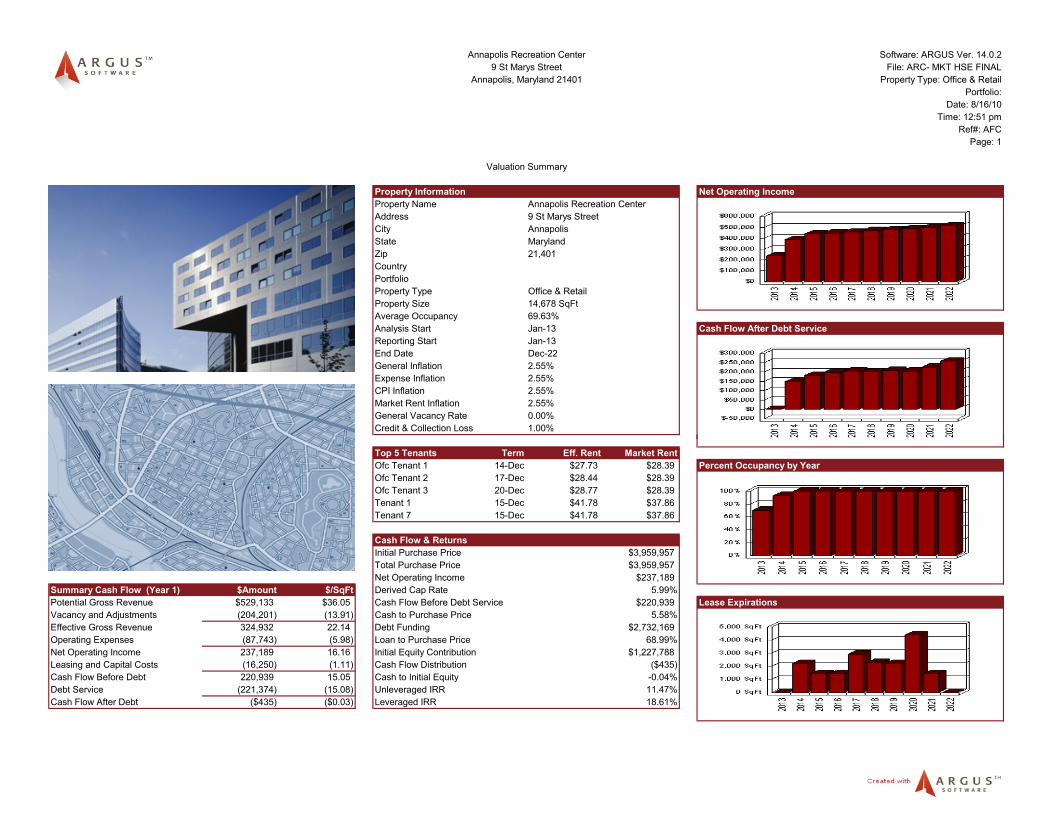

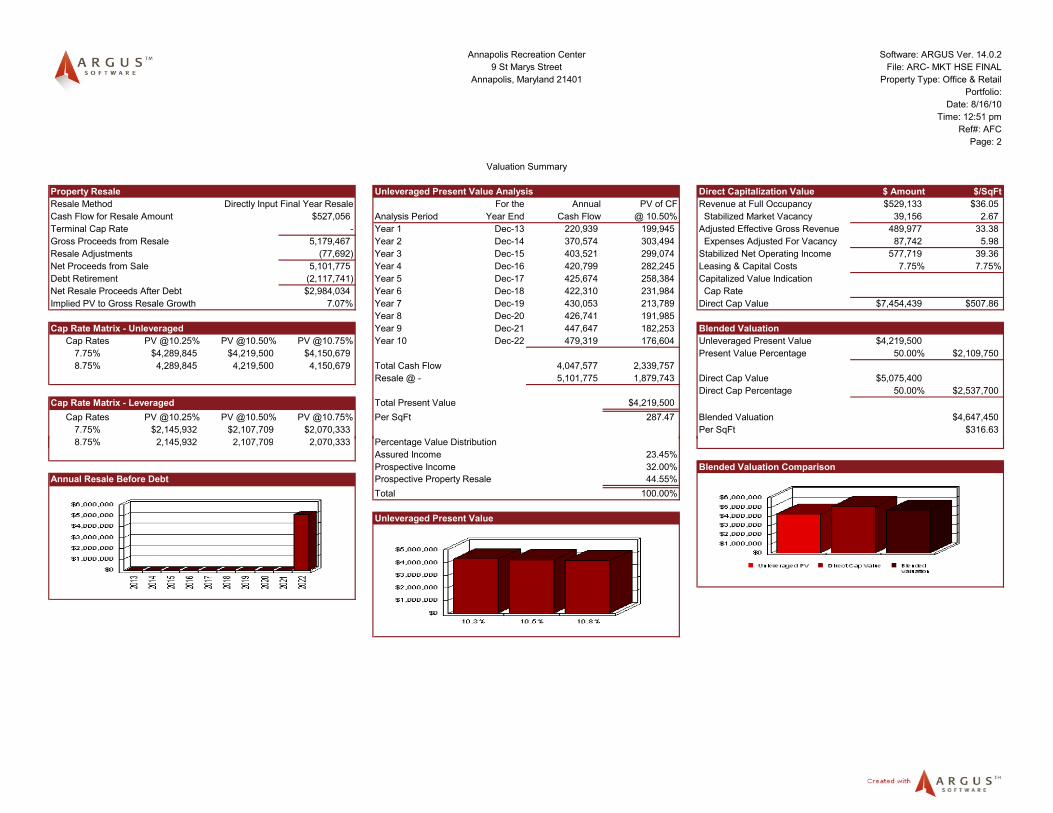

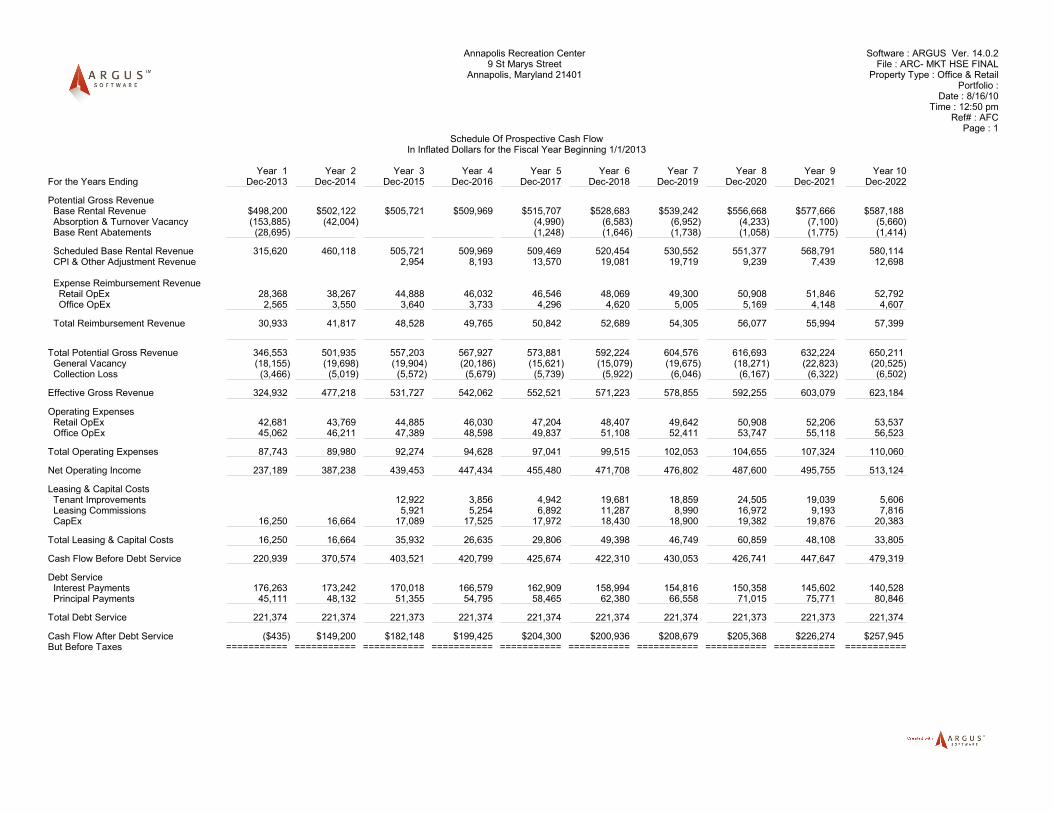

A second sensitivity test incorporates a reference made in a recent interview with Mayor Josh

Cohen, where the monthly debt service payment on the city dock market house was quoted at

$20,00055. Assuming the figure is accurate, Graaskamps SFFA was used to derive a supported

rent of $45 per square foot. Deducting 20% for the city dock market house’s prime location,

provides a suggested current rent of $36.00 per SF in 2010 dollars. Accounting for the time value

of money provides a suggested rent in 2013 of $37.86 per SF. The discounted cash flow detailed

in Appendix L illustrates the effect of the increased first floor rent only, holding all other

assumption constant. Leveraged returns increase nearly 500bps over the baseline, to 18.67%

assuming a 10-year hold and reversionary value accounting for the ground lease obligation. The

primary benefit is reflected in the net cash flows available for distribution to service the ground

17 Does not account for promote return

45

lease obligation and the equity investors. Other than the first two years of the analysis, projected

net cash flows available for distribution will cover the annual combined obligations of 150,54018.

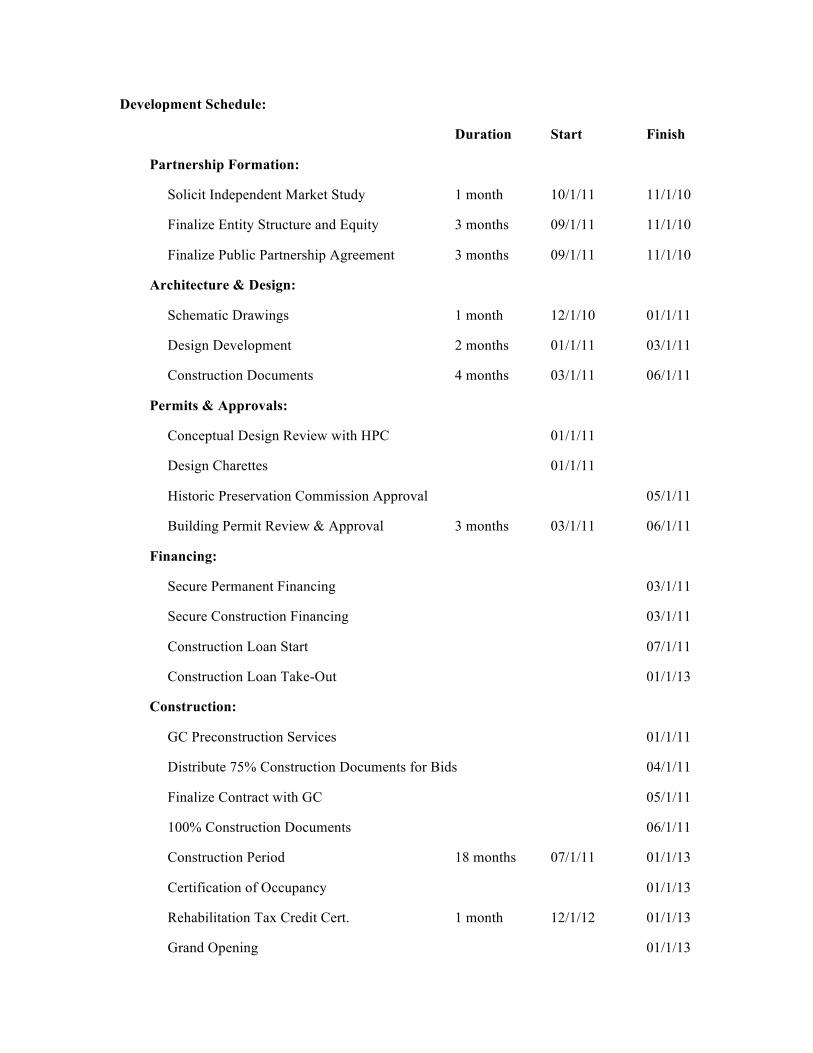

Development Schedule:

Appendix M outlines the development schedule for the proposed project. Project milestones are

broken into five categories: partnership formation, design, permits and approvals, financing, and

construction.

Upon the commitment by City of Annapolis to support the project as outlined, a formal market

study will be commissioned to verify the assumptions outlined above. Next, a limited liability

corporation will be formed as the primary entity for the project. Formal commitments from equity

partners and term agreements regarding expected distributions and assumed liability would then

be formalized. At the same time, partnership agreements with the City of Annapolis and/or the