dfi - developmental role vs. sustainability by - adfiap · dfi - developmental role vs....

TRANSCRIPT

26 April 2012

PLENARY SESSION 3:DFIs and SME Development & Finance

35th ADFIAP ANNUAL MEETINGSIstanbul, Turkey

DFI - Developmental Role vs. Sustainability

by

Datuk Mohd Radzif Mohd YunusSME BANK MALAYSIA

2

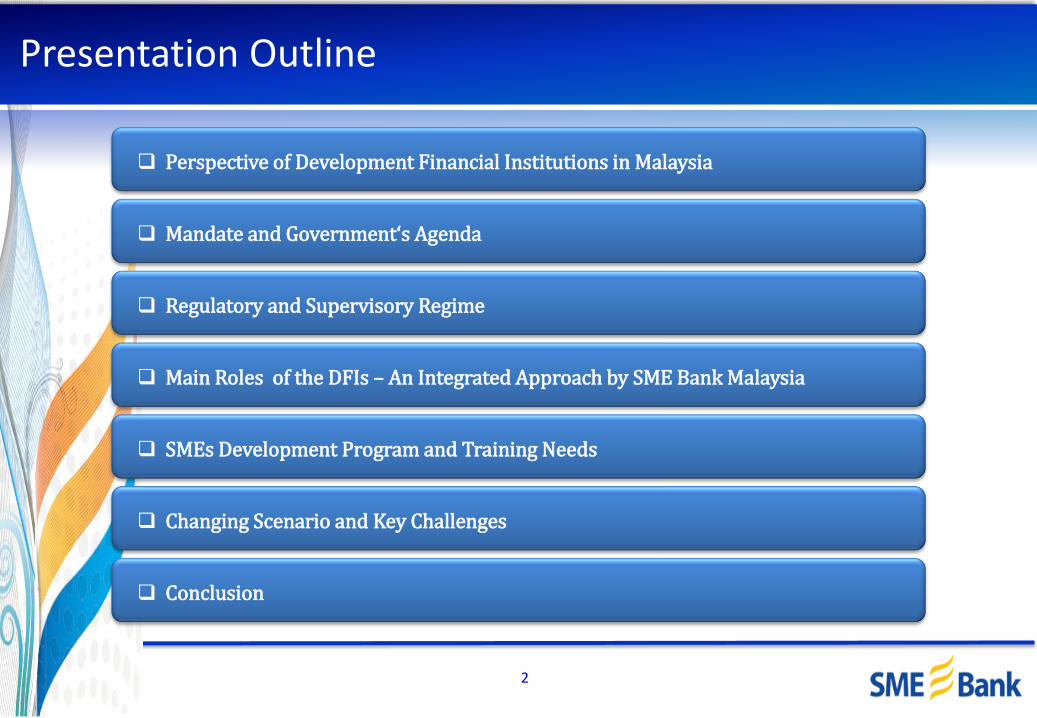

Presentation Outline

Perspective of Development Financial Institutions in Malaysia

Mandate and Government‘s Agenda

Regulatory and Supervisory Regime

Main Roles of the DFIs – An Integrated Approach by SME Bank Malaysia

SMEs Development Program and Training Needs

Changing Scenario and Key Challenges

Conclusion

3

Perspective of DFIs in Malaysia

DFIs are specialised FIs established by the Government with specific

mandate to develop and promote key sectors that are considered of

strategic importance to the overall socio-economic development

objectives of the country

The strategic sectors include agriculture, small and medium

enterprises (SMEs), infrastructure, maritime, export-oriented sector

as well as capital-intensive and high-technology industries

The are 13 DFIs in the country of which 6 are prescribed under the

Development Financial Institutions Act 2002 and supervised by the

Central Bank

Role and functions in providing focused financial and

development support to bolster human CAPITAL development, SOCIO-

ECONOMIC AGENDA and economic growth

4

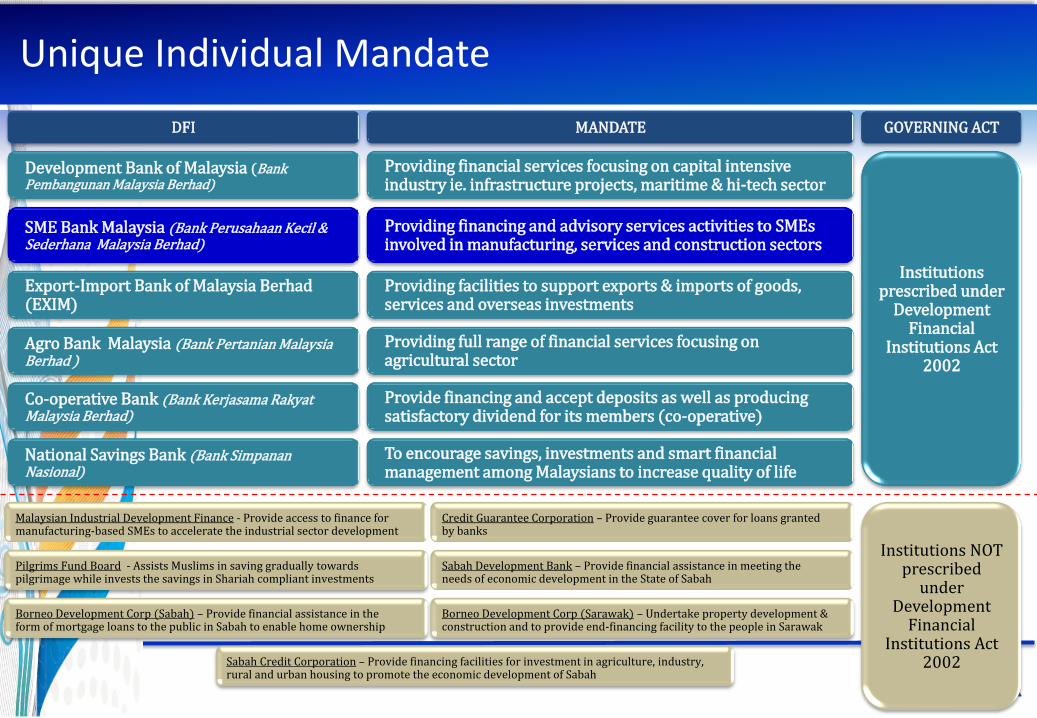

Unique Individual Mandate

DFI MANDATE

Development Bank of Malaysia (Bank Pembangunan Malaysia Berhad)

Providing financial services focusing on capital intensive industry ie. infrastructure projects, maritime & hi-tech sector

SME Bank Malaysia (Bank Perusahaan Kecil & Sederhana Malaysia Berhad)

Providing financing and advisory services activities to SMEs involved in manufacturing, services and construction sectors

Export-Import Bank of Malaysia Berhad (EXIM)

Providing facilities to support exports & imports of goods, services and overseas investments

Agro Bank Malaysia (Bank Pertanian Malaysia Berhad )

Providing full range of financial services focusing on agricultural sector

Co-operative Bank (Bank Kerjasama Rakyat Malaysia Berhad)

Provide financing and accept deposits as well as producing satisfactory dividend for its members (co-operative)

National Savings Bank (Bank Simpanan Nasional)

To encourage savings, investments and smart financial management among Malaysians to increase quality of life

GOVERNING ACT

Institutions prescribed under

Development Financial

Institutions Act 2002

Pilgrims Fund Board - Assists Muslims in saving gradually towards pilgrimage while invests the savings in Shariah compliant investments

Sabah Development Bank – Provide financial assistance in meeting the needs of economic development in the State of Sabah

Malaysian Industrial Development Finance - Provide access to finance for manufacturing-based SMEs to accelerate the industrial sector development

Credit Guarantee Corporation – Provide guarantee cover for loans granted by banks

Borneo Development Corp (Sabah) – Provide financial assistance in the form of mortgage loans to the public in Sabah to enable home ownership

Borneo Development Corp (Sarawak) – Undertake property development & construction and to provide end-financing facility to the people in Sarawak

Sabah Credit Corporation – Provide financing facilities for investment in agriculture, industry, rural and urban housing to promote the economic development of Sabah

Institutions NOT prescribed

under Development

Financial Institutions Act

2002

5

SME Bank Malaysia: Mission and Vision

To support Government’s Economic Agenda in

developing SMEs as an engine of growth

To be a full fledged specialized financial institution to nurture the

small medium industry and enterprise for nation building

6

Government’s Agenda – 10MP and ETP

SME Growth vs. GDP Growth (2001-2011)

In efforts to promote Malaysia as a high-

income nation by 2020, the Government targets to grow SME industry’s

contribution to the nation’s GDP to 40% in

2020.

33% 33% 34% 35% 36% 37% 38% 38% 39% 40%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Total SME contribution to GDP (2011-2020)

SME Bank will provide funding

assistance to businesses

that are in the Development and Growth

stage

5.1

6.0e

e: estimate

7

The Master Plan charts the policy direction of SMEs in all sectors through the year 2020 towards achieving a high income nation in line with the New Economic Model (NEM)

Phase I: new SME Development Framework and broad policies and strategies to achieve the NEM goals;

Phase II: Master Plan is to look into the specific action plans and the monitoring mechanism

Government’s Agenda - SME Master Plan (2012-2020)

Innovation and technology adoptionAccess to

financing

Intensify formalisation

Access to market

Legal and regulatory environment

Infrastructure

Human capital and entrepreneurship development

Increase business formation

Expand number of high growth and innovative firms

Raise productivity

Focus Areas

Strategic Goals

8

Regulatory and Supervisory Regime

Legal and Governance

Banking Principles

Capitalisation and Funding

Reporting and

Prudential Standards

Maintenance of absolute minimum capital

Capital adequacy framework

Maintenance of reserve fund

Annual funding requirement

Best practices for the management of credit risk

Guidelines on management of IT environment

Guidelines on Introduction of New Products

Guidelines on classification of impaired loans & provisioning

Companies Act 1965

Development Financial Institution Act 2002

Anti-Money Laundering and Anti-Terrorism Financing Act 2001

Corporate Governance related Guidelines

A state to balance sustainable development impact and financial stability, hence applies sound banking principles

Sound and prudent financial management has allowed considerable leeway to cross subsidise its advisory role

9

Main Roles – Integrated Approach by SME Bank

MEDIUMSMALLMICRO

Small Medium Enterprises (SMEs)

DevelopmentBanking

High Impact Developmental Program Through

Synergized Approach of Financial Assistance

and Intervention

Financial assistance

serves as enabler

for SMEs, as

engine of growth, to

move up the value

chain and create

viral effect to

the economy

Hand-holding

approach from

the entry point

to inculcate business

acumen and propel

SME business

to the next level

Financing Intervention

10

SME Development Program – Training Needs

Based o the Survey conducted – More than 50% of the respondents faced the

major 8 problems

Result on TNA Survey revealed that – Modules related to management and human

resources are most needed by the SMEs, beside the subject on marketing and finance

Entrepreneur development and continued investment in human capital remain as the most critical elements in building the capacity and capability of SMEs

0.0%

50.0%

100.0%

Insufficient Working Capital Ineffective Debtor Control

Tough Competition Ineffective Marketing Strategies

Improper Book Keeping High Production Cost

Lack of Admin Staff Improper Inventory Control

Incompetent Sales Personnel Low Staff Discipline

Low Productivity Difficulty in Getting Cusomer

High Product Rejection Rate

Common Problems Faced by SMEs

1 3 5 7 9 11 132 4 6 8 10 12

1 2

3 4

5 6

7 8

9 10

11 12

13

0.0%

50.0%

100.0%

Self Motivation and Satisfaction Working Capital and Cash Management

Public Relations Personnel Management

Labour Act Credit Control

Book Keeping and Accounting Marketing and Strategy

Cost Management Financial Analysis

Quality Improvement Sales Technique and Skills

Inventory Management

Type of Training Modules Preferred by SMEs

1 3 5 7 9 11 132 4 6 8 10 12

1 2

3 4

5 6

7 8

9 10

11 12

13

Training Need Analysis (TNA) Survey Conducted - 100 respondents of new and existing entrepreneurs

11

DFIs – A Changing Scenario

• DFIs have been forced to become less dependent as Government face more budgetary constraints and development aid declines

• To use own financial strength to intermediate between the providers and users of capital

• To improve Balance Sheet to enhance attractiveness of capital

Government’s Budgetary Constraint

• Developmental role or development assistance is often non-recoverable but complements development banking, thus, both functions become mutually reinforcing

• The functions are bundled together since the skills required for assessing potential investments are similar to those required to address capacity building and other development needs

Complementary Function

12

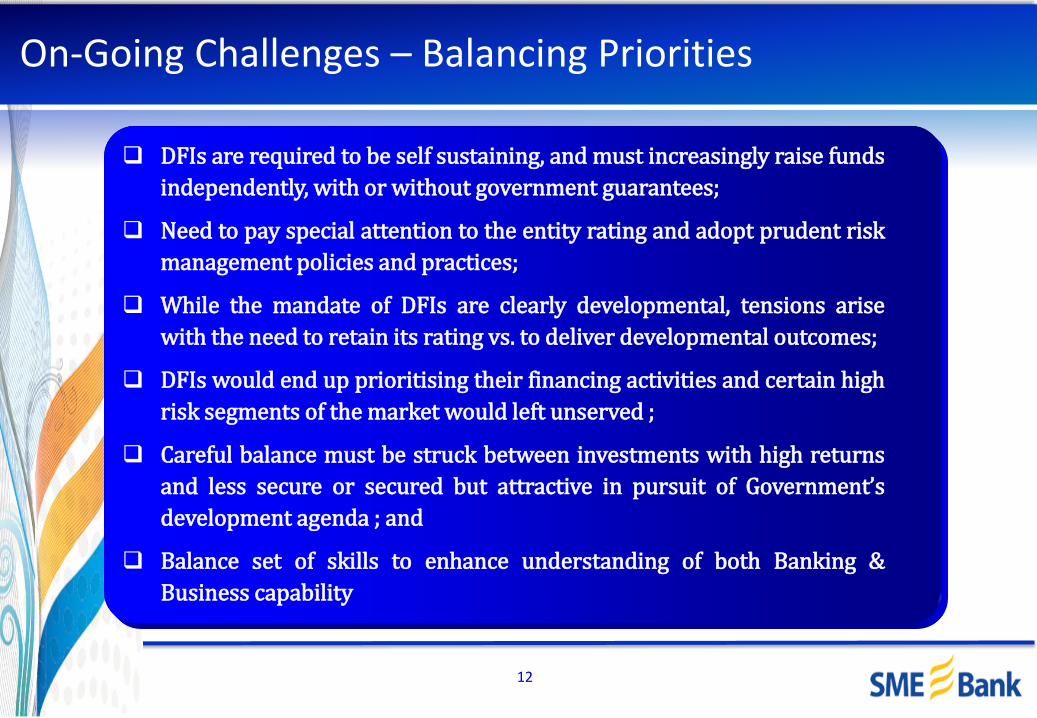

On-Going Challenges – Balancing Priorities

DFIs are required to be self sustaining, and must increasingly raise funds

independently, with or without government guarantees;

Need to pay special attention to the entity rating and adopt prudent risk

management policies and practices;

While the mandate of DFIs are clearly developmental, tensions arise

with the need to retain its rating vs. to deliver developmental outcomes;

DFIs would end up prioritising their financing activities and certain high

risk segments of the market would left unserved ;

Careful balance must be struck between investments with high returns

and less secure or secured but attractive in pursuit of Government’s

development agenda ; and

Balance set of skills to enhance understanding of both Banking &

Business capability

13

Conclusion – Developmental Role vs. Sustainability

For DFI to succeed within the rapidly changing environment, they must

meet a number of challenges for their effective management;

This requires sound governance and financial management, flexibility and

the ability to balance cost-effective intermediation and risk management

with outreach through smart partnerships, capacity building and

knowledge management;

DFIs need to sufficiently generate income through diversification of

income stream which could be used to cross subsidise its developmental

role