dfm konference 2002: strategisk ejendomsledelse

TRANSCRIPT

Effective Portfolio Management

SAS Radisson Koldingfjord - 30. January 2002

Joachim Wrang-Widén

DFM Konference 2002: Strategisk Ejendomsledelse

2© 2002 Andersen - Real Estate. All rights reserved.

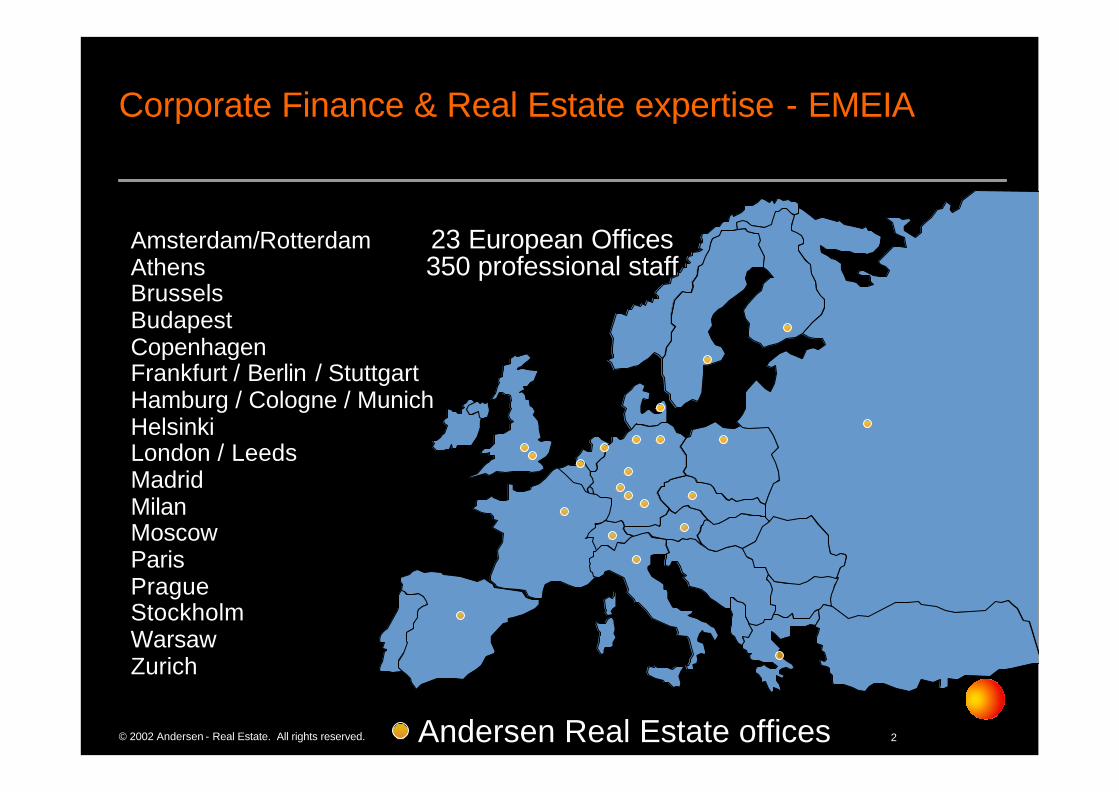

Corporate Finance & Real Estate expertise - EMEIA

Amsterdam/RotterdamAthens Brussels BudapestCopenhagenFrankfurt / Berlin / Stuttgart Hamburg / Cologne / MunichHelsinkiLondon / LeedsMadrid MilanMoscowParisPragueStockholmWarsawZurich

23 European Offices350 professional staff

Andersen Real Estate offices

3© 2002 Andersen - Real Estate. All rights reserved.

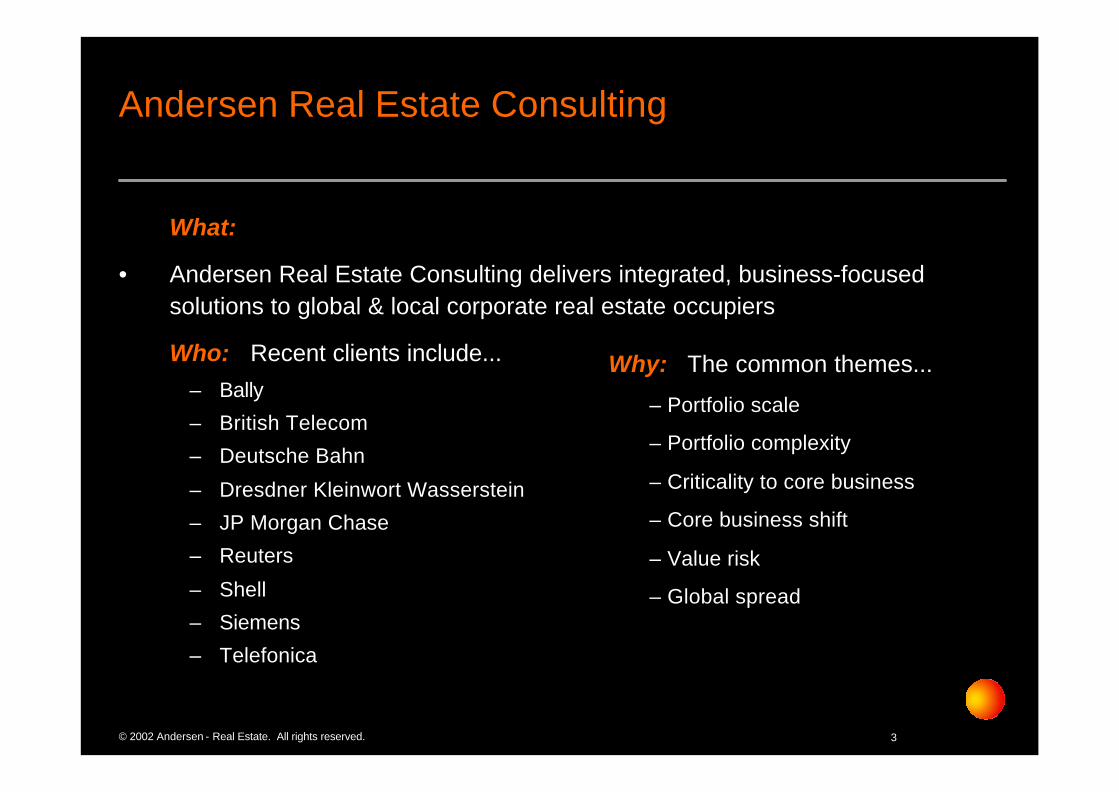

Andersen Real Estate Consulting

What:

• Andersen Real Estate Consulting delivers integrated, business-focused solutions to global & local corporate real estate occupiers

Who: Recent clients include...– Bally

– British Telecom

– Deutsche Bahn

– Dresdner Kleinwort Wasserstein

– JP Morgan Chase

– Reuters

– Shell

– Siemens

– Telefonica

Why: The common themes...

– Portfolio scale

– Portfolio complexity

– Criticality to core business

– Core business shift

– Value risk

– Global spread

4© 2002 Andersen - Real Estate. All rights reserved.

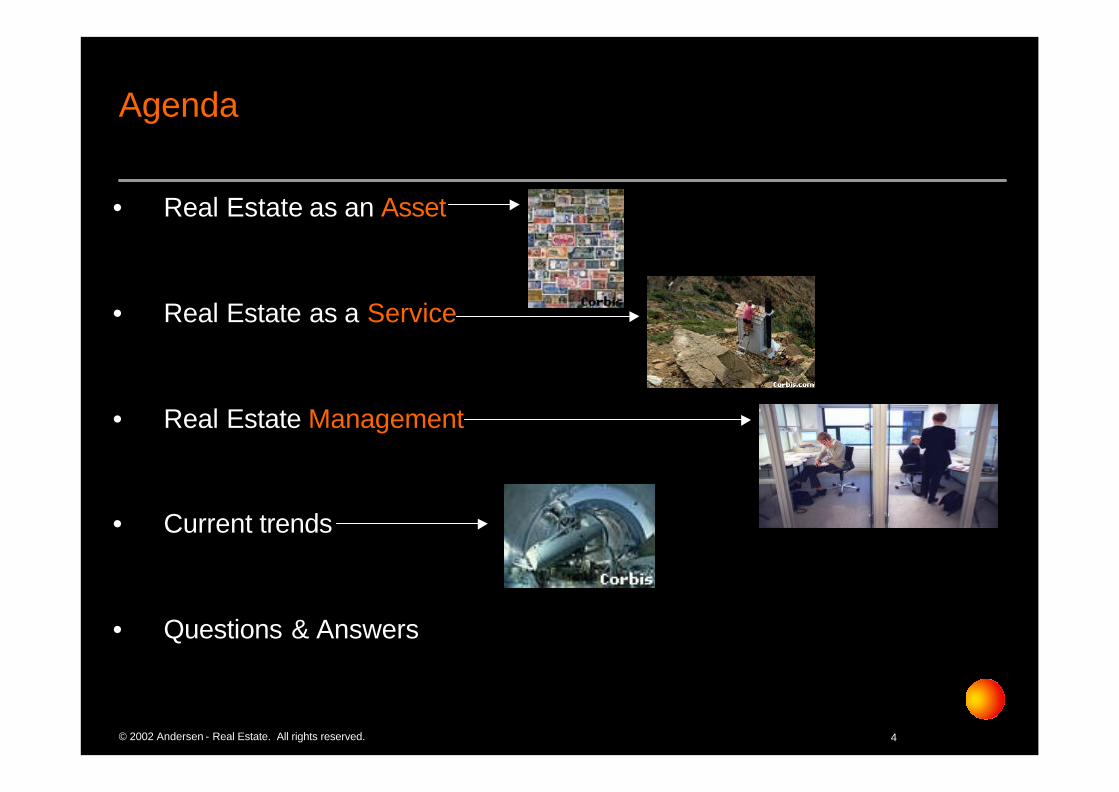

Agenda

• Real Estate as an Asset

• Real Estate as a Service

• Real Estate Management

• Current trends

• Questions & Answers

5© 2002 Andersen - Real Estate. All rights reserved.

Caveats

• Each saving is company specific– Difficult to generalise results– Client confidentiality

• Processes can be selected in general but implementation is an individual solution-dependent issue

• Presentation based on:– Practical experience through working with clients– Client opinions & views– Andersen research– Andersen & external surveys

6© 2002 Andersen - Real Estate. All rights reserved.

Real Estate as an Asset – Asset Management

• Many corporates typically have c. 40 % of their balance sheet in real estate

• Real estate costs are frequently the 2nd largest cost item – normally 25 % or more

• Real Estate as Asset:– Regardless of freehold or leasehold, it will be on your Balance sheet !– Changing Accounting Principles!

– Critical production factor (recruitment, physical etc.)

– Underpin corporate solidity (rating institutes, collateral for loans etc.)

How Why When

7© 2002 Andersen - Real Estate. All rights reserved.

”Property Forum” – Conference Autumn 2001

• 300 corporate real estate managers

• Interactive questionnaire session

• Main conference focus on real estate’s contribution to:

– shareholder value

– economic value added

– corporate efficiency

8© 2002 Andersen - Real Estate. All rights reserved.

To use your handset simply point towards To use your handset simply point towards the screen and press the key corresponding the screen and press the key corresponding to your choice. There is no send key. If to your choice. There is no send key. If you make a mistake press the C button you make a mistake press the C button and reand re--enter your selection.enter your selection.

9© 2002 Andersen - Real Estate. All rights reserved.

70%70%

22%22%

8%8%

?? ...an occupier ...an occupier

?? ...a service provider or ...a service provider or

?? ...neither ...neither

Are you…Are you…

10© 2002 Andersen - Real Estate. All rights reserved.

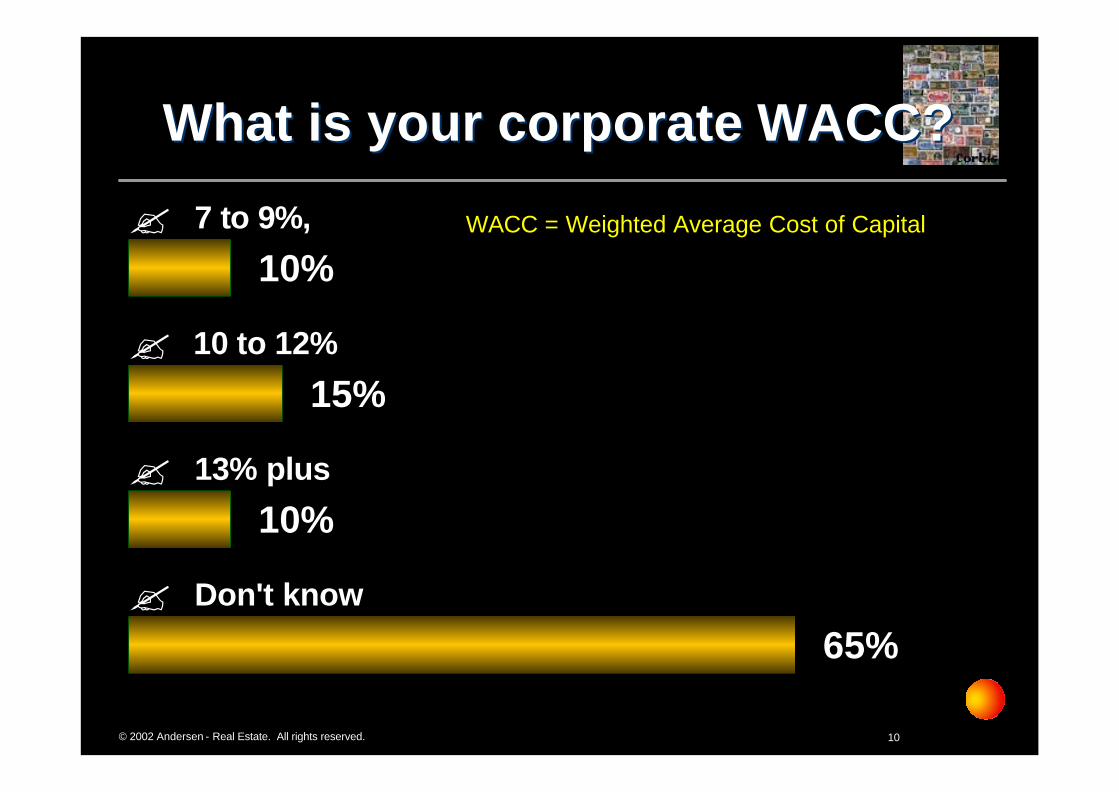

10%10%

15%15%

10%10%

65%65%

?? 7 to 9%, 7 to 9%,

?? 10 to 12% 10 to 12%

?? 13% plus 13% plus

?? Don't know Don't know

What is your corporateWhat is your corporate WACCWACC? ?

WACC = Weighted Average Cost of Capital

11© 2002 Andersen - Real Estate. All rights reserved.

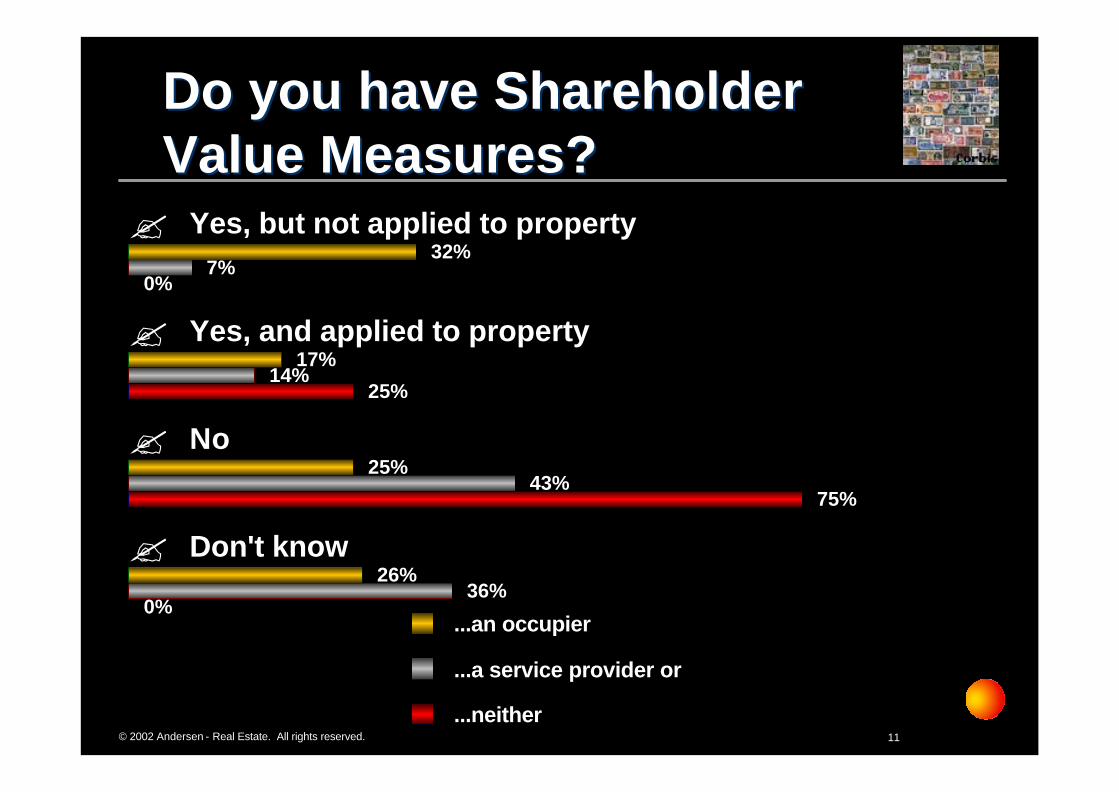

32%32%7%7%

0%0%

17%17%14%14%

25%25%

25%25%43%43%

75%75%

26%26%36%36%

0%0%

?? Yes, but not applied to property Yes, but not applied to property

?? Yes, and applied to property Yes, and applied to property

?? No No

?? Don't know Don't know

...an occupier

...a service provider or

...neither

Do you have Shareholder Do you have Shareholder Value Measures?Value Measures?

12© 2002 Andersen - Real Estate. All rights reserved.

74%74%60%60%

66%66%

26%26%35%35%

17%17%

0%0%5%5%

17%17%

?? Yes Yes

?? No No

?? Don't know Don't know

...an occupier

...a service provider or

...neither

Have you carried out any reviews of your Have you carried out any reviews of your real estate tenure strategy, or portfolio wide real estate tenure strategy, or portfolio wide analysis (as opposed to single units or analysis (as opposed to single units or assets) in the last 12 months?assets) in the last 12 months?

13© 2002 Andersen - Real Estate. All rights reserved.

34%34%35%35%

30%30%

14%14%17%17%

15%15%

25%25%18%18%

23%23%

23%23%22%22%

19%19%

4%4%8%8%

13%13%

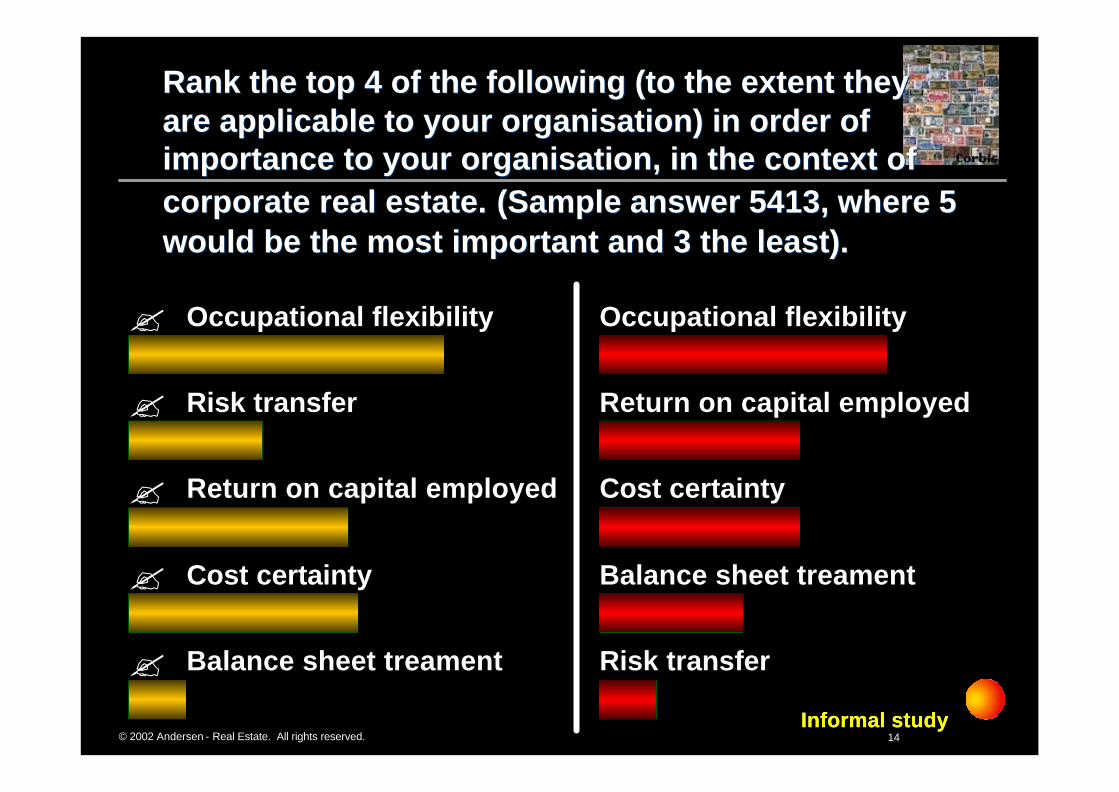

?? Occupational flexibility Occupational flexibility

?? Risk transfer Risk transfer

?? Return on capital employed Return on capital employed

?? Cost certainty Cost certainty

?? Balance sheet treament Balance sheet treament...an occupier

...a service provider or

...neither

Rank the top 4 of the following (to the extent they Rank the top 4 of the following (to the extent they are applicable to your organisation) in order of are applicable to your organisation) in order of importance to your organisation, in the context of importance to your organisation, in the context of corporate real estate.corporate real estate. (Sample answer 5413, where 5(Sample answer 5413, where 5would be the most important and 3 the least).would be the most important and 3 the least).

14© 2002 Andersen - Real Estate. All rights reserved.

?? Occupational flexibility Occupational flexibility

?? Risk transfer Risk transfer

?? Return on capital employed Return on capital employed

?? Cost certainty Cost certainty

?? Balance sheet treament Balance sheet treament

Rank the top 4 of the following (to the extent they Rank the top 4 of the following (to the extent they are applicable to your organisation) in order of are applicable to your organisation) in order of importance to your organisation, in the context of importance to your organisation, in the context of corporate real estate.corporate real estate. (Sample answer 5413, where 5(Sample answer 5413, where 5would be the most important and 3 the least).would be the most important and 3 the least).

Occupational flexibilityOccupational flexibility

Return on capital employedReturn on capital employed

Cost certaintyCost certainty

Balance sheet treamentBalance sheet treament

Risk transferRisk transfer

Informal studyInformal study

15© 2002 Andersen - Real Estate. All rights reserved.

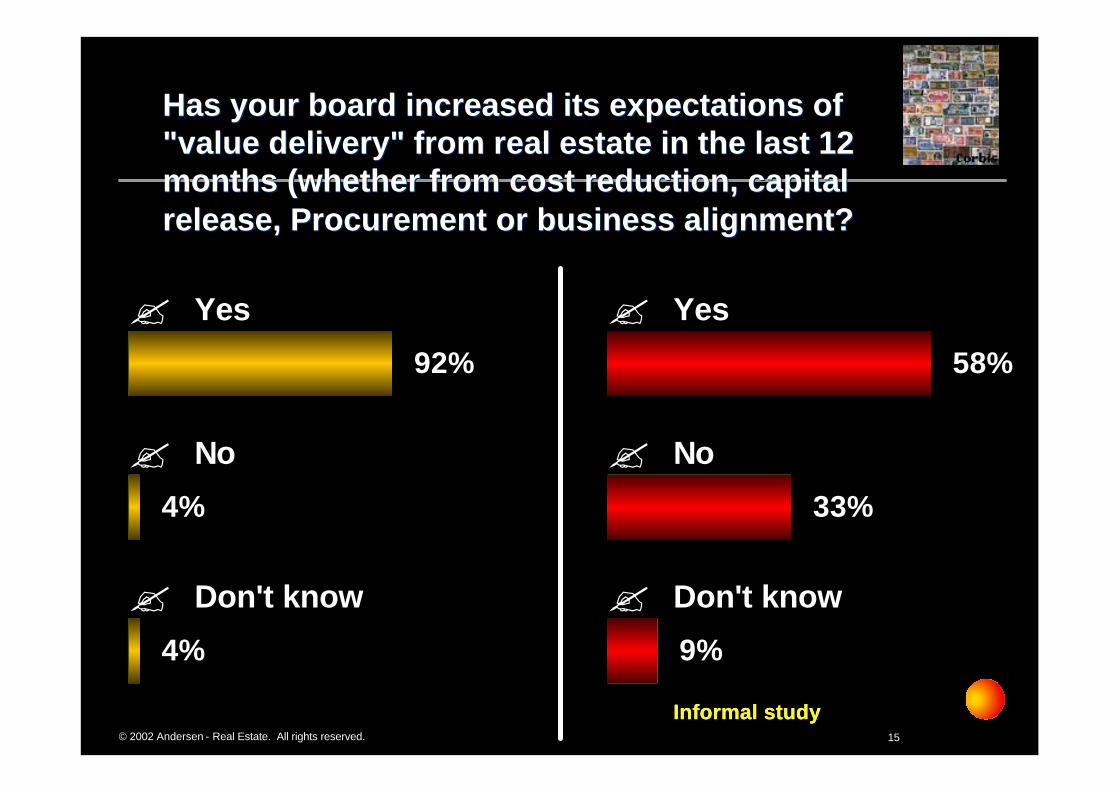

92%92%

4%4%

4%4%

?? Yes Yes

?? No No

?? Don't know Don't know

Has your board increased its expectations ofHas your board increased its expectations of"value delivery" from real estate in the last 12 "value delivery" from real estate in the last 12 months (whether from cost reduction, capital months (whether from cost reduction, capital release, Procurement or business alignment?release, Procurement or business alignment?

58%58%

33%33%

9%9%

?? Yes Yes

?? No No

?? Don't know Don't know

Informal studyInformal study

16© 2002 Andersen - Real Estate. All rights reserved.

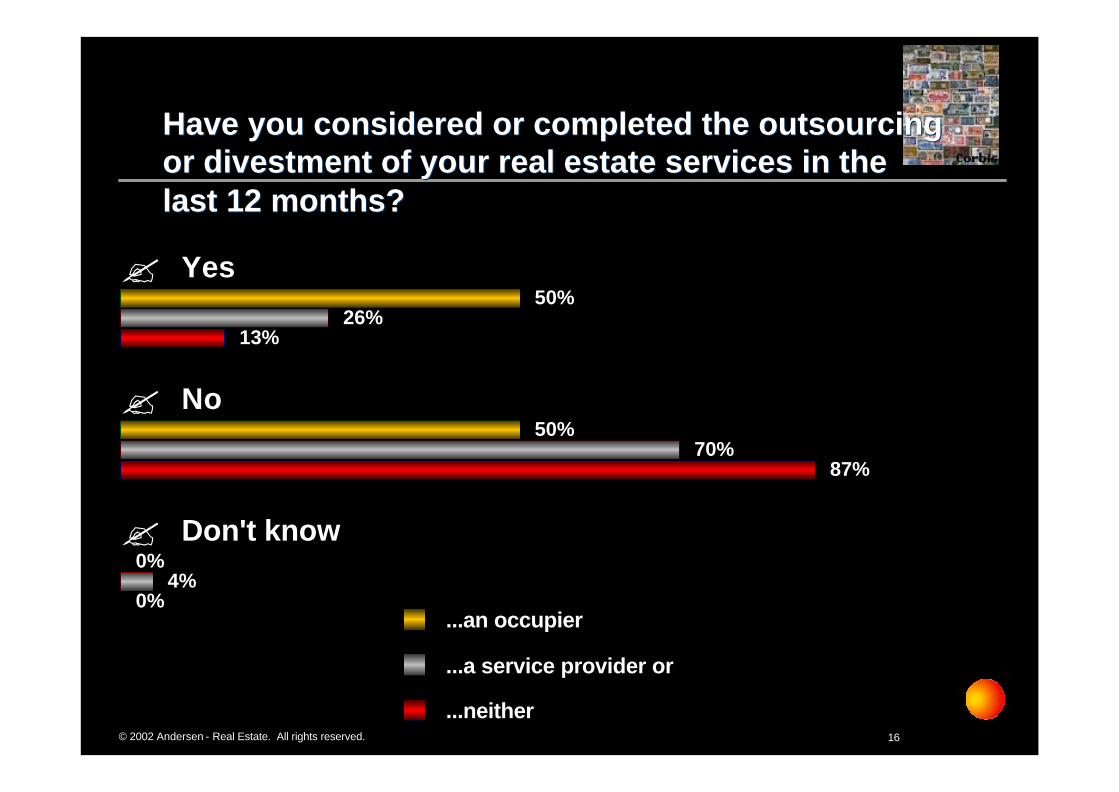

50%50%26%26%

13%13%

50%50%70%70%

87%87%

0%0%4%4%

0%0%

?? Yes Yes

?? No No

?? Don't know Don't know

...an occupier

...a service provider or

...neither

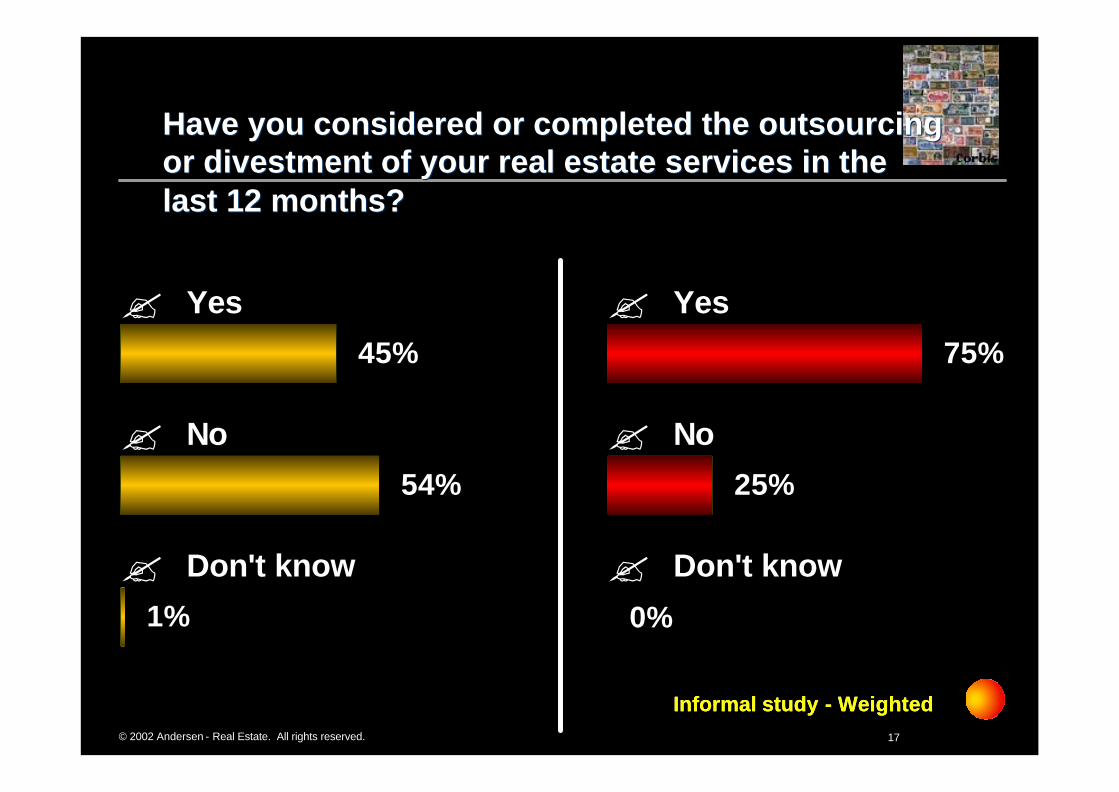

Have you considered or completed the outsourcingHave you considered or completed the outsourcingor divestment of your real estate services in the or divestment of your real estate services in the last 12 months?last 12 months?

17© 2002 Andersen - Real Estate. All rights reserved.

45%45%

54%54%

1%1%

?? Yes Yes

?? No No

?? Don't know Don't know

Have you considered or completed the outsourcingHave you considered or completed the outsourcingor divestment of your real estate services in the or divestment of your real estate services in the last 12 months?last 12 months?

75%75%

25%25%

0%0%

?? Yes Yes

?? No No

?? Don't know Don't know

Informal study Informal study -- WeightedWeighted

18© 2002 Andersen - Real Estate. All rights reserved.

Using Real Estate as Business Asset

•DKK 93 billion value

•DKK 178 billion annual turnover

•36,160 employees

•950 offices in 92 countries

•annual “real estate costs”: < 7 % or “no deal!”

•regional Service Providers with contracts tendered on a revolving basis

•in-house real estate team: Chief Financial Officer (!)

•Real estate outsourced to external Service Provider:

• advises & procures services from other suppliers

•manages relationships with suppliers & monitors performance

•Real Estate contributes to corporate success & growth!

•Real Estate used as strategic & tactical business tool

19© 2002 Andersen - Real Estate. All rights reserved.

• Contractors on clients:

”Clients are normally not very innovative.”

• Clients on contractors:

”Contractors are generally not very good or can’t

supply a complete service package that works 100%”

Real Estate as a Service:Corporate Requirements / Facility Management

20© 2002 Andersen - Real Estate. All rights reserved.

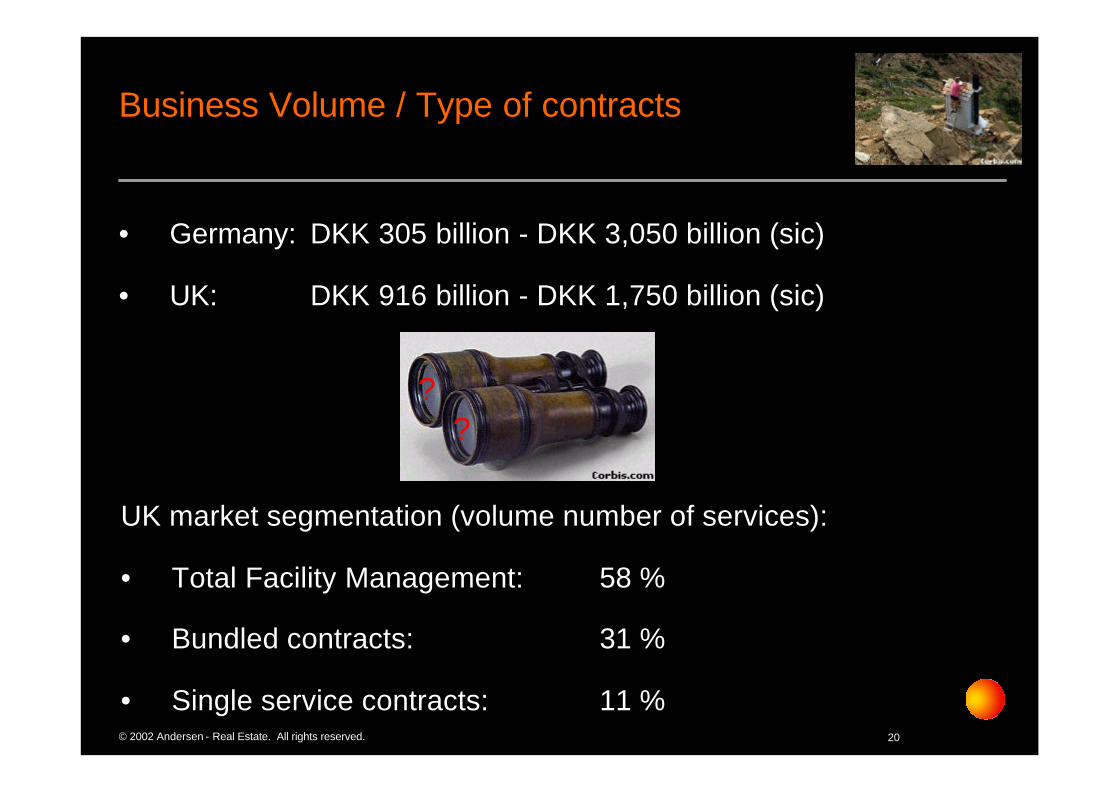

Business Volume / Type of contracts

• Germany: DKK 305 billion - DKK 3,050 billion (sic)

• UK: DKK 916 billion - DKK 1,750 billion (sic)

UK market segmentation (volume number of services):

• Total Facility Management: 58 %

• Bundled contracts: 31 %

• Single service contracts: 11 %

??

21© 2002 Andersen - Real Estate. All rights reserved.

Outsourcing from a corporate occupierperspective

• Why outsource?

• solution competence within corporate

• process skills for procurement of outsourcing contract– structuring of contract - content, service levels, bonus & penalty clauses

• monitoring skills regarding outsourcing contract– service delivery, proactivity, responsiveness, cost-benefit

• offers staff career prospects otherwise not present

• how do you take care of outsourced staff ?

• Do we have IT infrastructure, databases & Management Information Systems that the Service Provider can use and report into ?

22© 2002 Andersen - Real Estate. All rights reserved.

Why do corporates outsource?

• The link between bundling of services, particularly within IT and maintenance

• Benefits in economies of scale

• Greater risk transfer

• Higher quality service standards & better value for money

23© 2002 Andersen - Real Estate. All rights reserved.

Market Direction

• Contracts and Bundling– IT & Telecommunications bundling becoming more popular – Total Facility Management contracts on the increase– Long term contracts more evident, often on a national basis– Corporate PFI style deals on the increase

• PRIME and STEPS

• British Telecom and BBC

• Fees & Payment– various methods of benchmarking/market testing of current services– greater delegation of authority to contractor

• Performance– introduction of staff and contract incentive schemes

24© 2002 Andersen - Real Estate. All rights reserved.

Outsourcing decision

• What services to outsource:– which skills / competencies are your “critical competitive advantage”– importance of delivery quality

• Structuring of contract– incentives & penalties– quality and performance and price– current staff & systems move over to new entity?

• Supplier side– any competent & capable service providers in the market?– one / several contracts?

©Castle Rock Entertainment 1996

25© 2002 Andersen - Real Estate. All rights reserved.

Contract arrangements

• Contracts normally > 3 years

• High contract set-up costs

• Required service levels normally reached 12-18 months into contract period

• Short-term contracts do not provide contractor time to “bed-in” -no time to cover the set-up costs

26© 2002 Andersen - Real Estate. All rights reserved.

Real Estate Management:How to measure and Add Value?

• Key Performance Indicators [KPI] are difficult to identify

• Clients increasingly have a corporate real estate strategy with different options – Slots- og Ejendomsstyrelsen :

– Decision Tree structure– Corporate score-card and the role of real estate to achieve this

• Boundary on what you actually can measure

• Appropriateness of measurability

• What to achieve?

• How to achieve?

27© 2002 Andersen - Real Estate. All rights reserved.

Benchmarking – Corporate Comments

Benchmarking less succesfull than initially hoped for:

1. Too many benchmarks have focused on individual services (e.g. cleaning, security) rather than management function per se

2. Multitude of various benchmarks

3. Even if you select a benchmark, how do you measure and do you have reliable, valid data?

4. How do you define an objective KPI?

5. Benchmarks should change – don’t use the same at t10 as at t0

28© 2002 Andersen - Real Estate. All rights reserved.

Benchmark Trends

• External benchmarks used as initial indicator

• Key Performance Indicators used for:– Management of suppliers– Show value generation of services / real estate management to internal users

• OPD (Occupier Property Databank) useful but clients now ”club together” with other occupiers (not necessarily in the same industry) to compare process, notcosts.

• Use multiple suppliers for same service to compare service levels and value for money

• Process benchmarking:– Process innovation– Performance measurement– Contract terms

29© 2002 Andersen - Real Estate. All rights reserved.

Outsourcing model - strategic corporatereal estate management

•DKK 778 billion value

•DKK 220 billion annual turnover

•144,000 employees

•4,274 banking centres in the US

•offices in 38 countries, active in 190 countries

•3 global regions - 1 Service Provider / region

•contracts tendered on a 3-5 year period

•in-house team: 4 for Europe (!)

•in-house team:

•selects Service Provider, procures services, manages relationships with Service Providers, monitors performance from Service Providers, in-house team advises business units & group management on strategy

• business units pre-planning future accommodation needs

30© 2002 Andersen - Real Estate. All rights reserved.

Current Trends

• Integrated approach to corporate real estate

• Increased focus on core business

• Corporate real estate as a valuable asset + service + function

• Private Finance Initiative = PFI

– Redistribution of capital from real estate into core business

– Total Outsourcing

31© 2002 Andersen - Real Estate. All rights reserved.

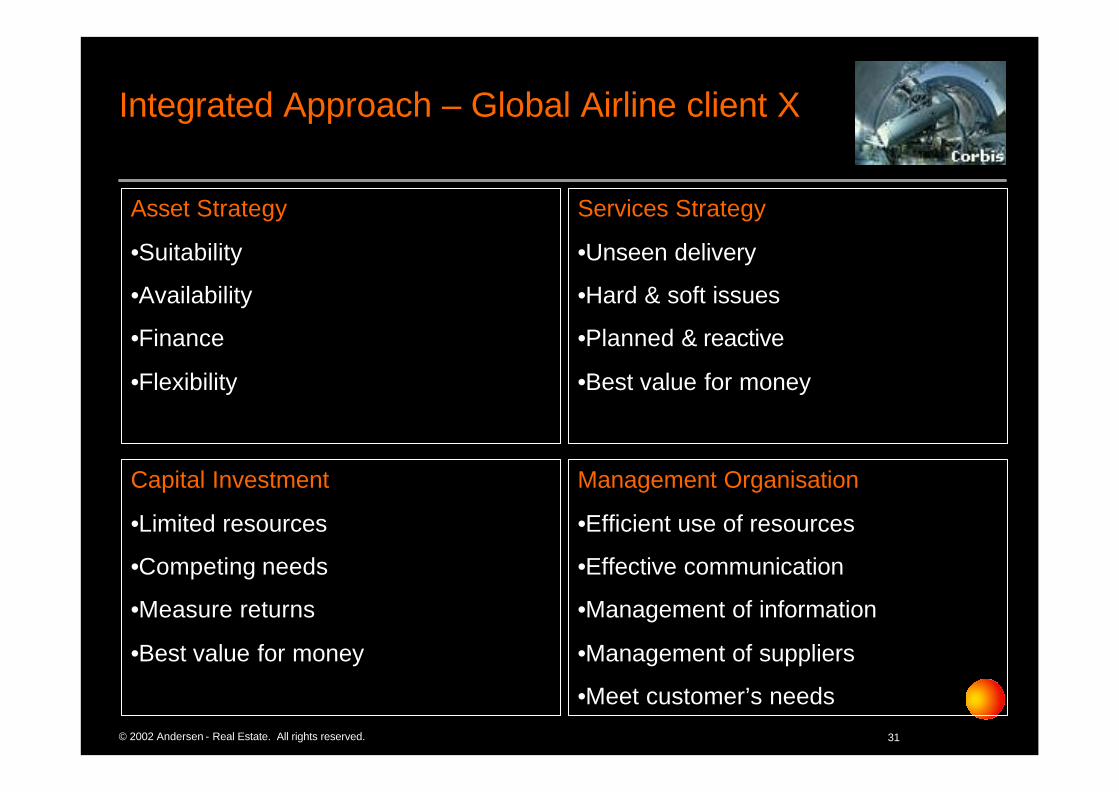

Asset Strategy

•Suitability

•Availability

•Finance

•Flexibility

Services Strategy

•Unseen delivery

•Hard & soft issues

•Planned & reactive

•Best value for money

Capital Investment

•Limited resources

•Competing needs

•Measure returns

•Best value for money

Management Organisation

•Efficient use of resources

•Effective communication

•Management of information

•Management of suppliers

•Meet customer’s needs

Integrated Approach – Global Airline client X

32© 2002 Andersen - Real Estate. All rights reserved.

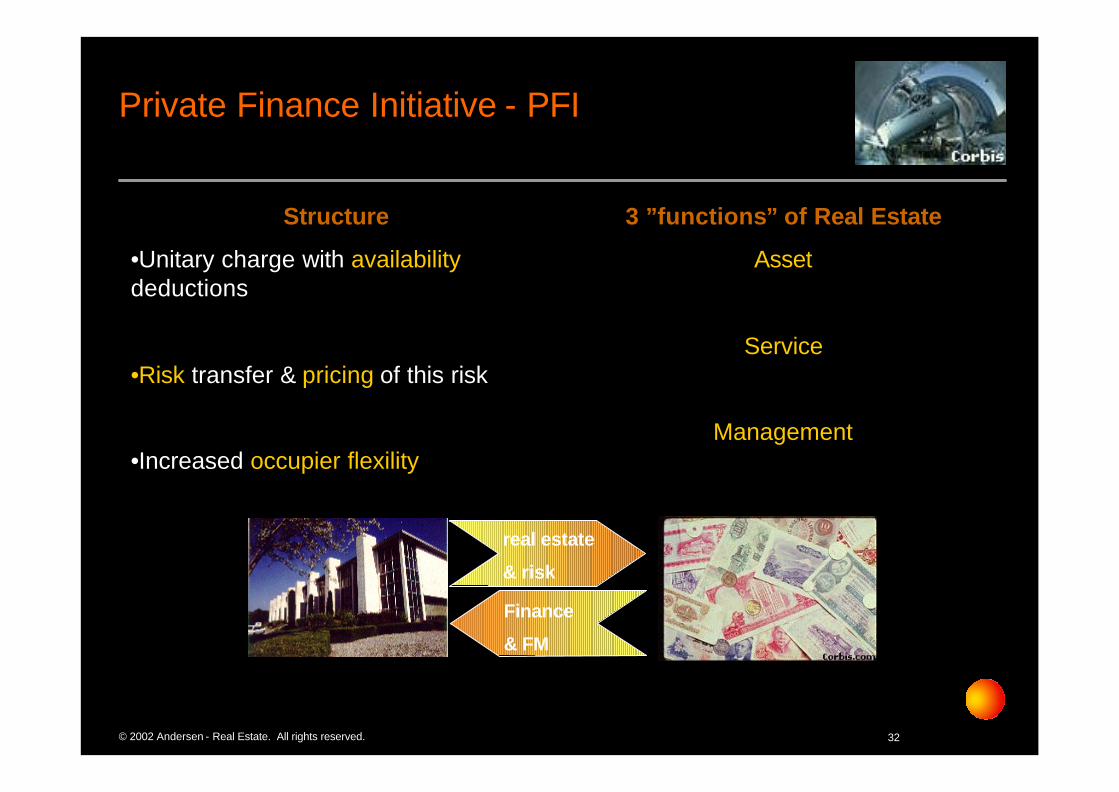

Private Finance Initiative - PFI

real estate

& risk

Finance

& FM

Structure

•Unitary charge with availabilitydeductions

•Risk transfer & pricing of this risk

•Increased occupier flexility

3 ”functions” of Real Estate

Asset

Service

Management

33© 2002 Andersen - Real Estate. All rights reserved.

What is Corporate PFI?

The concept - Corporate PFI - has evolved from UK

government initiatives driven by the need of corporates to;

- drive capital out of real estate to pursue value creating objectives

- transfer property related risks to organisations that are geared up and incentivised to manage those risks

- increase operating flexibility and liquidity

- link payments to performance levels in in both the provision of premises and supporting services

34© 2002 Andersen - Real Estate. All rights reserved.

What is Corporate PFI not?

Corporate PFI is not:

• a sale- & leaseback

• a serviced facility concept (e.g Regus, HQ etc.)

• a facilities management outsourcing (that function covers only part of the PFI structure)

•sale- & leaseback:–is one solution but fails on often required corporate need for flexibility–Normally does not offer the “profit element” for corporate

•serviced facility–normally doesn’t cope with multi-site & sector facilities

35© 2002 Andersen - Real Estate. All rights reserved.

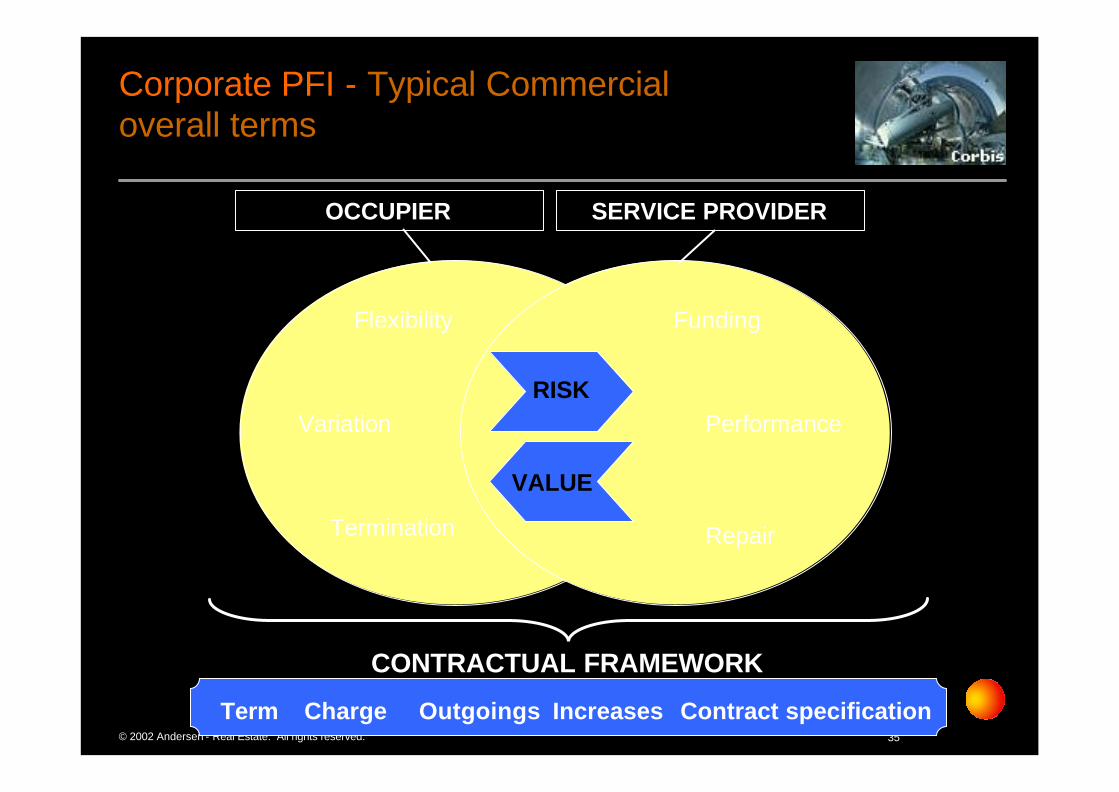

Corporate PFI - Typical Commercialoverall terms

Flexibility

Variation

Termination

Funding

Performance

Repair

OCCUPIER SERVICE PROVIDER

RISK

VALUE

CONTRACTUAL FRAMEWORK

Term Charge Outgoings Increases Contract specification

Flexibility

Variation

Termination

Funding

Performance

Repair

36© 2002 Andersen - Real Estate. All rights reserved.

Corporate PFI - Why do it?What the occupiers say….

• Operational flexibility– ability to reduce accommodation without financial penalty or overhead– flexibility to leave selection of hand back properties until future– ability to re-acquire in future not lost

• Reduce operating costs– Service Providers have economies of scale and focus– corporate PFI ‘price’ is much lower than traditional UK lease– Property risk transferred in price competitive bidding environment– Property upside is in part retained

• Release capital for core business– future value uncertainty for investment in operational property assets – core business generates much higher return than property assets– increase shareholder value added

37© 2002 Andersen - Real Estate. All rights reserved.

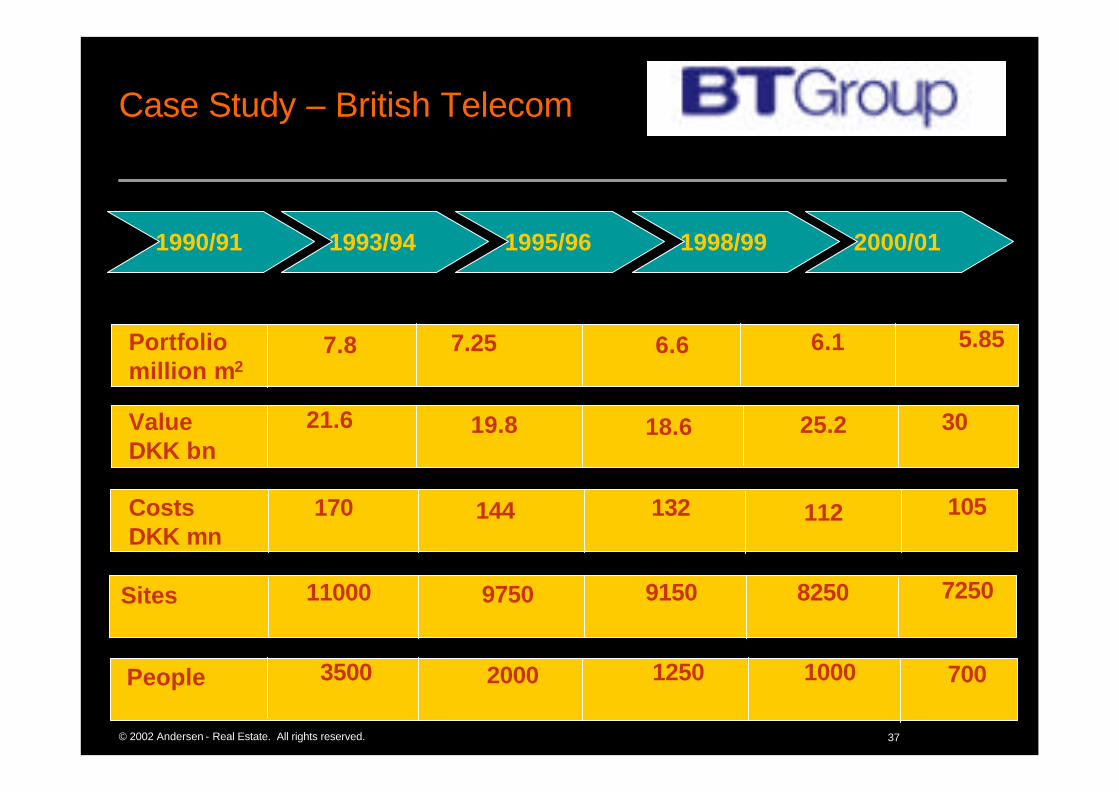

Case Study – British Telecom

1998/991995/961993/941990/91 2000/01

Portfolio million m2

5.856.16.67.257.8

Costs DKK mn

170 144 132 112 105

9750Sites 11000 9150 8250 7250

People 3500 2000 1250 1000 700

Value DKK bn

19.8 18.6 25.2 3021.6

38© 2002 Andersen - Real Estate. All rights reserved.

• Release capital for core business investment

• Achieve operational flexibility

• Achieve rapid solution

• Transfer property risk out of BT

• Reduce Real Estate related overheads

• Outsource non-core activities

• Went to market with ‘total solution requirements’ - corporate PFI

• Tight time-cost-quality balance for data management

• Re-engineering operational businesses’ entire approach to corporate real estate

• One supplier for real estate solutions

Objectives Approach

• Realign real estate structure to match future strategic needs of the BT Group.

• New internal real estate organisation acting as an Informed Client Unit only.

• Occupying businesses more focussed on their “real” cost and responsibilities.

• Positive financial solution, without ‘giving away’ value or future options with estate.

• Innovative and highly “tailored” solution, on a market-leading scale.

Successes & Deliverables

Case Study - British Telecom

DKK 29 billion transaction (!) – advised by Andersen

39© 2002 Andersen - Real Estate. All rights reserved.

Conclusion 1 [2]

• Using Real Estate as Asset:– WPP with cost reductions of DKK 180 million

• Real Estate as Service:– Bank of America organisation several hundred to 4 people + outsourcing– Right service at right time in right place at right price

• Real Estate Management as value adding / releasing function:– British Telecom releasing DKK 29 billion for core business

Viewing Real Estate in an integrated fashion as integral part of the corporate:

– Global Airline Client X releasing capital, better facilities at lower cost with higher flexibility

40© 2002 Andersen - Real Estate. All rights reserved.

Conclusion 2 [2]

• Shareholder value focus gaining ground

• Corporates increasingly view real estate as a valuable asset + service + function

• Real estate is expected to ”deliver value” to corporate = increased pressures for efficiency & effectiveness of real estate as asset + service + function

• Financial markets offer more options today compared to 90’s

• Innovative corporates increasingly look for ”total solutions” (e.g. PFI) that cover several areas

41© 2002 Andersen - Real Estate. All rights reserved.

42© 2002 Andersen - Real Estate. All rights reserved.

Andersen - Real Estate Denmark

• Joachim Wrang-Widén

• Office: +45-35 25 27 14

• Telefax: +45-35 25 20 19

• Mobile: +45-22 20 27 14

• E-mail: [email protected]

Midtermolen 1

DK-2100 Copenhagen

43© 2002 Andersen - Real Estate. All rights reserved.