dictionary of terms, acronyms and ratios used …bank).pdf · ratings’ published reports and...

TRANSCRIPT

DICTIONARY OF TERMS, ACRONYMS AND RATIOS USED IN THE FINANCIAL SECTOR

FEBRUARY 13, 2014

Introduction

This list of terms, acronyms and ratios are compiled from those that are commonly used in Global Credit Ratings’ published reports and occasional research papers. The content of this dictionary is not intended to be comprehensive and/or complete, remains a work in progress and will be updated periodically as needed. \\ \\

Global Credit Rating Co. (Pty) Limited 107 Johan Avenue Sandton, 2146 Tel: +27 11 784-1771 Fax: +27 11 784-1770

Website: www.globalratings.net

Authorised and regulated by the Financial Services Board

Terms, Acronyms and Formulas (A-Z Selector)

A N

B O

C P

D Q

E R

F S

G T

H U

I V

J W

K X / Y

L Z

M Formulas

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 4

Account Formal record that represents, in words, money or other unit of measurement, certain resources, transactions or other events that result in changes to those resources and claims.

Accountant Person skilled in the recording and reporting of financial transactions.

Accounting Recording and reporting of financial transactions, including the origination of the transaction, its recognition, processing, and summarisation in the financial statements.

Accounting Period Period of time from one balance sheet to the next. Period of the income statement, usually one year.

Accounting Risk The risk that the integrity of the financial statements and related information cannot be upheld.

Advance A generic term for the ways in which a bank lends money, whether loan, overdraft, or discount.

Agreement A negotiated and usually legally enforceable understanding between two or more legally competent parties.

Amortisation The gradual reduction of an obligation over time as the net result of repayments, interest and fees.

Annual Report

Report to the stockholders of a company which includes the company's annual, audited balance sheet and related statements of earnings, stockholders' or owners' equity and cash flows, as well as other financial and business information.

Appetite Demand.

Appreciation An increase in value.

Arm’s Length A transaction in which the parties act independently and have no transaction favourable relationship with each other, or are not subject to undue influence or duress from another.

Arrears Bucket A non-performance classification, classified according to the number of days in arrears, i.e. 30, 60, 90 days.

Asset An item with economic value that an entity owns or controls.

Asset Quality The ability of a bank’s assets, especially its loans, to continue to perform according to its terms and generate net interest income for the bank.

A

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 5

Audit A careful review of financial records to verify their accuracy.

Audited Financial Statements Financial statements that have been audited by a certified auditor, stating that the financial statements present a true and fair picture of the entity’s financial condition.

Auditor Person who audits financial accounts and records kept by others.

Auditors' Report Written communication issued by an independent accountant or accounting firm, describing the character of his or her work and the degree of responsibility taken.

Back to Content (A-Z Selector)

Bad Debt All or portion of an account, loan, or note receivable considered to be uncollectible.

Balance Sum of debit entries minus the sum of credit entries in an account. If positive, the difference is called a debit balance; if negative, a credit balance.

Balance Sheet

Basic financial statements, usually accompanied by appropriate disclosures that describe the basis of accounting used in its preparation and presentation of a specified date the entity's assets, liabilities and owners’ equity. Also known as a statement of financial position.

Banking Environment The business and regulatory environment in which a bank operates.

Bankruptcy Legal process, governed by federal statute, whereby the debts of an insolvent person are liquidated after being satisfied to the greatest extent possible by the debtor’s assets.

Basel Basel Committee on Banking Supervision housed at the Bank for International Settlements.

Basis Points A basis point is 1/100th of a percentage.

Bond Long term debt.

Book value Total assets minus total liabilities. Book value also means the value of an asset as recorded on an entity’s books.

Breach A violation of a loan covenant or promise.

Breakeven point When revenue exactly equals expense.

Budget Financial plan that serves as an estimate of future cost, revenues or both.

B

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 6

Building society A type of deposit-taking financial institution that engages in long-term mortgage lending, primarily to finance owner-occupied residential mortgages/property.

Business cycle The sequence of recovery, upswing, peak, downturn, and recession during which business activity, as reflected by numerous economic indicators, predictably rises and falls.

Back to Content (A-Z Selector)

CAMEL

The acronym for the mainstream approach to credit analysis of financial institutions, referring to the five core elements of any credit assessment: Capital Adequacy, Asset Quality, Management (Competency), Earnings (Profitability) and Liquidity (Funding).

Cap A provision in a loan agreement that sets a limit on the interest rate which can be charged during the term of the loan.

Capital

Capital refers to the funds (e.g. money, loans, equity) which are available to carry on a business, make an investment, and generate future revenue. Capital also refers to physical assets which can be used to generate future returns.

Capital Adequacy A measure of the adequacy of an entity's capital resources in relation to its current liabilities and also in relation to the risks associated with its assets. An appropriate level of capital adequacy ensures that the entity has sufficient capital to support its activities and that its net worth is sufficient to absorb adverse changes in the value of its assets without becoming insolvent.

Capital and reserves Shareholders equity.

Capital at risk (CAR) The capital required to absorb unexpected losses.

Capital Reserves That portion of a company's profits not paid out as dividends to shareholders. They are also known as undistributable reserves.

Cash Funds that can be readily spent or used to meet current obligations.

Cash Flows Net of cash receipts and cash disbursements relating to a particular activity during a specified accounting period.

Certificate of Deposit (CD) Formal instrument issued by a bank upon which the deposit of funds may not be withdrawn for a specified time period.

Clean Opinion Audit opinion not qualified for any material scope restrictions. Also known as an unqualified opinion.

C

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 7

Collateral Asset provided to a creditor as security for a loan.

Contingent Assets Assets not recorded on an entity’s financial reports, but may be realised.

Contingent Liabilities Liabilities not recorded on an entity’s financial reports, but which might become due.

Convertible Bond A bond giving the investor the option to convert the bond into equity at a fixed conversion price or as per a pre-determined pricing formula.

Core Capital See primary capital.

Core Deposits That portion of a bank’s deposits that is relatively stable and has a predictable cost. Deposits fluctuate seasonally and cyclically, but even in adverse circumstances, deposits normally do not fall below some minimum level.

Cost of Funds The rate the bank pays to borrow funds that it re-lends to borrowers.

Corporate Governance The manner in which an entity is governed and decisions are undertaken.

County Risk

The range of risks emerging form the political, legal, economic and social conditions of a country that have adverse consequences affecting investors and creditors with exposure to the country, and may also include negative effects on financial institutions and borrowers in the county.

Covenant A clause in loan agreements that promises or obligates and/or restricts the borrower. If violated, a breach has occurred, which may cause the loan to become immediately due.

Credit

A contractual agreement in which a borrower receives something of value now, and agrees to repay the lender at some date in the future, generally with interest. The term also refers to the borrowing capacity of an individual or company.

Credit Bureau Provider of consumer credit information to credit providers.

Creditor Party that loans money or other assets to another party.

Credit Rating A rating accorded to the performance of either ultimate or timely payment of obligations.

Credit Rating Agency A party that provides an opinion on the credit quality of assets, debt securities and companies.

Credit risk

Risk that a party to a contractual agreement or transaction will be unable to meet their obligations or will default on commitments. Credit risk can be associated with almost any transaction or instrument such as swaps, repos, CDs, foreign exchange transactions, etc. Specific types

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 8

of credit risk include sovereign risk, country risk, legal or force.

Creditworthiness An assessment of a debtor’s ability to meet debt obligations.

Country Exposure Amount of an institution’s total investment and/or claims on borrowers in a specific county, direct as well as indirect.

Current Assets Asset that can be expected to turn into cash within a year or less.

Customer Deposits Deposits other than interbank deposits.

Back to Content (A-Z Selector)

Debt General name for money, notes, bonds, goods or services which represent amounts owed.

Debtor Party owing money or other assets to a creditor.

Default Failure to make loan payments on a timely basis or to comply with other terms/requirements as stipulated in the loan agreement.

Deferred An action that has been postponed until a future date.

Demand Deposit A deposit of funds that can be withdrawn without any advance notice.

Depreciation Expense allowance made for wear and tear on an asset over its estimated useful life.

Diversification

The principle that a portfolio in which assets are separated into different industry sectors, geographic regions and firms will embody less overall risk than one in which assets are concentrated into a few sectors, regions and firms.

Dividend A portion of the after-tax profits paid out to the owners of an entity as a return on their investment.

Back to Content (A-Z Selector)

D

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 9

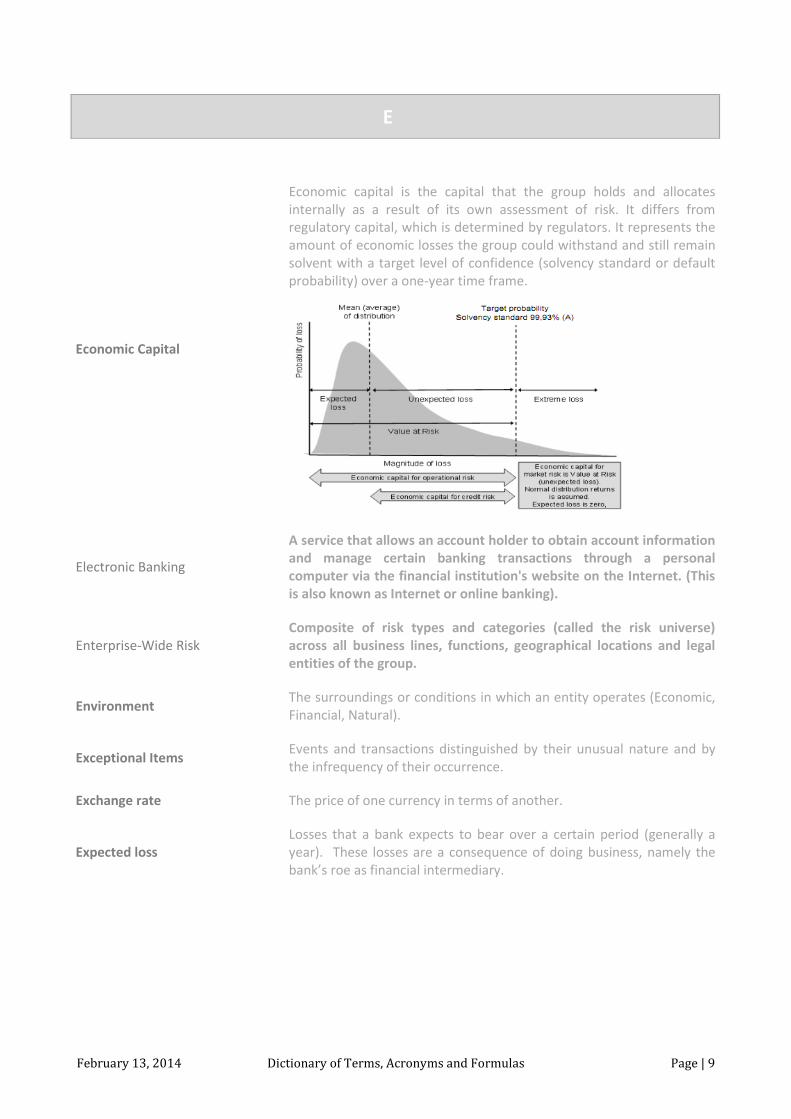

Economic Capital

Economic capital is the capital that the group holds and allocates internally as a result of its own assessment of risk. It differs from regulatory capital, which is determined by regulators. It represents the amount of economic losses the group could withstand and still remain solvent with a target level of confidence (solvency standard or default probability) over a one-year time frame.

Electronic Banking

A service that allows an account holder to obtain account information and manage certain banking transactions through a personal computer via the financial institution's website on the Internet. (This is also known as Internet or online banking).

Enterprise-Wide Risk Composite of risk types and categories (called the risk universe) across all business lines, functions, geographical locations and legal entities of the group.

Environment The surroundings or conditions in which an entity operates (Economic, Financial, Natural).

Exceptional Items Events and transactions distinguished by their unusual nature and by the infrequency of their occurrence.

Exchange rate The price of one currency in terms of another.

Expected loss Losses that a bank expects to bear over a certain period (generally a year). These losses are a consequence of doing business, namely the bank’s roe as financial intermediary.

E

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 10

Expected Shortfall Expected average loss for losses greater than value at risk (VAR).

Expense Cost incurred for a service used in the process of earning revenue.

Expenditure Payment, either in cash, by assuming a liability, or by surrendering an asset.

Exposure The extent to which a bank or institution is reliant on one or more counterparties as a result of trading transactions.

Exposure at Default (EAD) Quantification of the exposure at risk in case of a credit default.

Back to Content (A-Z Selector)

Facility The grant of availability of money at some future date in return for a fee.

Financial Institution An entity that focuses on dealing with financial transactions, such as investments, loans and deposits.

Financial Statements

Presentation of financial data including balance sheets, income statements and statements of cash flow, or any supporting statement that is intended to communicate an entity's financial position at a point in time and its results of operations for a period then ended.

Fixed asset Cannot be quickly turned into cash without interfering with business operation.

Fixed Deposit A deposit of funds in a bank under an agreement stipulating that the funds must be kept on deposit for a stated period of time at a predefined interest rate.

Forecast A calculation or estimate of future financial events.

Foreign Exchange Risk The risk that known or ascertainable currency cashflow commitments and receivables are uncovered and as a result have an adverse impact on the financial results and/or financial position due to movements in

F

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 11

exchange rates.

Franchise Business or banking franchise; a bank’s business.

Fraud Wilful misrepresentation by one person of a fact inflicting damage on another person.

Funding Acquisition of liabilities to match, cover or balance the particular asset or assets for which they are required.

Back to Content (A-Z Selector)

Guarantee An undertaking in writing by one person (the guarantor) given to another, usually a bank (the creditor) to be answerable for the debt of a third person (the debtor) to the creditor, upon default of the debtor.

Goodwill The difference between what an entity pays when it buys the asset/s of another entity and the book value of those assets.

Gross Risk See Inherent Risk

Back to Content (A-Z Selector)

Hedge

A risk management technique used to reduce the possibility of loss resulting from adverse movements in commodity prices, equity prices, interest rates or exchange rates arising from normal banking operations. Most often, the hedge involves the use of a financial instrument or derivative such as a forward, future, option or swap.

Hedging may prove to be ineffective in reducing the possibility of loss as a result of, inter alia, breakdowns in observed correlations between instruments, or markets or currencies and other market rates.

Hedging Action taken by the group to reduce or eliminate the possibility of loss resulting from adverse movements in commodity prices, equity prices, interest rates or exchange rates.

Back to Content (A-Z Selector)

G

H

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 12

ICAAP See Internal Capital Adequacy Assessment Process.

Illiquid Assets Broadly refers to loans or to other assets which are not easily convertible to cash, such as foreclosed assets and fixed assets.

Impairment An amount set aside for expected losses to be incurred by a creditor.

Income Inflow of revenue during a period of time.

Income Statement Summary of the effect of revenues and expenses over a period of time.

Industry Risk The risk that defaults will arise in an industry because of factors specifically affecting that industry.

Information Technology Risk

The risk associated with information technology has a strategic and an operational component. Information technology risk encompasses the strategic component, while the operational component is included in operational risk. This includes the risk of an uncoordinated, inefficient and/or under-resourced information technology strategy, as a result of which the group becomes progressively less competitive.

Inherent Risk Inherent risk is the product of the impact of the risk on the objective(s) and the likelihood of the risk occurring should no management actions/controls be in place to mitigate the risk.

Initial Public Offering (IPO) When a private company goes public for the first time.

Insolvency When an entity's liabilities exceed its assets.

Insurance and Assurance Risk

The risk that the underwriting process permits clients to enter risk pools with a higher level of risk than priced for, resulting in a loss to the business unit, bank or group.

Actuarial and statistical methodologies are used to price insurance risk. Underwriters align clients with this pricing basis and respond to any anti-selection by placing clients in substandard risk pools and price these risks with an additional risk premium and/or exclude certain claims, events or causes, or exclude clients from entering pools at all.

The failure to reinsure with acceptable quality reinsurers, beyond the level of risk appetite (excessive risk) mandated by the board of directors, risks underwritten by the short-term insurance and/or life assurance activities of the group, including catastrophe insurance (i.e. more than one insurance claim on the group arising from the same event), leading to disproportionate losses to the unit, bank or group.

Intangible Asset Asset having no physical existence such as trademarks and patents.

Interest Payment for the use or forbearance of money.

I

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 13

Interest Rate

The amount paid by a borrower to a lender in exchange for the use of the lender's money for a certain period of time. Interest is paid on loans or on debt instruments, such as notes or bonds, either at regular intervals or as part of a lump sum payment when the issue matures.

Interest Rate Risk

Interest rate risk in the banking book is the risk that earnings or economic value will decline as a result of changes in interest rates. The sources of interest rate risk in the banking book are:

repricing risk (mismatch risk) [timing differences in the maturity (for fixed-rate) and repricing (for floating-rate) of bank assets, liabilities and off-balance-sheet positions];

basis risk (imperfect correlation in the adjustment of the rates earned and paid on different instruments with otherwise similar repricing characteristics); and

yield curve risk (changes in the shape and slope of the yield curve); and embedded options risk (the risk pertaining to interest-related options embedded in bank products).

Interim Financial Statements Financial Statements that report the operations of an entity/business for less than one year.

Internal Audit Audit performed within an entity by its staff rather than an independent certified public accountant.

Internal Capital Adequacy Assessment Process (ICAAP)

The process by which banks demonstrate that chosen internal capital targets are well founded and that these targets are consistent with their overall risk profile and current operating environment. The five main features of a rigorous process are:

board and senior management oversight;

sound capital assessment;

comprehensive assessment of risks;

monitoring and reporting; and

internal control review.

Internal Control System

An internal control system comprises the policies, procedures and activities within the group designed to:

ensure that risks are contained within the risk tolerances established by the risk management process; and

provide reasonable assurance of reliable and accurate information, ensure compliance with policies, procedures and laws, use resources efficiently, protect assets and achieve operational objectives.

Internal control is a process effected by the board of directors, senior management and all levels of staff in the group. The objectives of the internal control process are to provide reasonable assurance of:

efficiency and effectiveness of activities;

reliability, completeness and timeliness of financial and management information; and

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 14

compliance with applicable laws and regulations.

Internal Fraud

The risk of losses due to acts of a type intended to defraud, misappropriate property or circumvent regulations, the law or company policy, excluding diversity/discrimination events, which involves at least one internal party.

Investment Grade Credit ratings equal to or higher than "BBB-" (triple B minus).

Investment Risk

The risk of a decline in the net realisable value of investment assets arising from adverse movements in market prices or factors specific to the investment itself (e.g. reputation and the quality of management). Market prices are independent variables, which include interest rates, property values, exchange rates, and equity and commodity prices.

Issuer Risk The risk that a particular principal payment or set of payments due from an issuer or a listed instrument (e.g. corporate bond) will not be forthcoming as scheduled.

Issue versus Risk An issue (or event) has materialised or is in the process of doing so, while a risk has not yet materialised.

Islamic Banking

A type of banking practiced in some Islamic countries or countries with large Muslim populations. As Islam prohibits interest, various mechanisms for banking and finance have been devised which are deemed to conform to Islamic law.

Back to Content (A-Z Selector)

Journal A chronological record of business transactions.

Joint and Several Liability This is a legal term used to point that two or more entities are individually responsible, instead of being collectively responsible.

Judgment Clause

This relates to a provision regarding bank notes of hand or guarantees, and includes the authorisation of the borrowers or sureties given to the bank, to create a judgment lien, at any time after the completion of the legal instruments.

Judicial Lien It pertains to an interest in the holdings, which are gained from judicial or court orders.

Junior Debt The responsibilities of an issuing entity, for which quittance has contractually been considered, as a priority of miscellaneous liabilities of the same debtor.

Junk Bonds This is a recognised term for high-yield sureties with quality standings below investment grade.

J

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 15

Back to Content (A-Z Selector)

Key Risk Indicator (KRI) A management information indicator that provides continuous insight into the level of risk in the group/business.

Key Rate Duration This pertains to a measure of duration, which computes efficient or empirical duration by altering the market price for a particular maturity date on the yield curve, while keeping all other variables constant.

King III The King Report on Governance for South Africa 2010.

Knot Points It relates to the points that are on the yield curve for which there are discernible rates for traded instruments.

Back to Content (A-Z Selector)

Lease Conveyance of land, buildings, equipment or other assets from one person (lessor) to another (lessee) for a specific period of time for monetary or other consideration, usually in the form of rent.

Legal Risk

Legal risk arises from the necessity that the bank or group conducts its activities in conformity with the business and contractual legal principles applicable in each of the jurisdictions where it conducts its business. It is the possibility that a failure to meet these legal requirements may result in unenforceable contracts, litigation, fines, penalties or claims for damages or other adverse consequences.

It includes risk arising from inadequate documentation, legal or regulatory incapacity, insufficient authority of a counterparty and uncertainty about the validity or enforceability of an obligation in counterparty insolvency.

It comprises contravention, failure to prevent, detect or promptly correct violations of the terms and provisions of contractual agreements and related documents entered into with clients, counterparties, suppliers and other parties, including common-law and other applicable statutory liabilities.

Liability Debts or obligations owed by one entity (debtor) to another entity (creditor) payable in money, goods, or services.

Letter of Credit

A document issued by a bank (on behalf of the buyer or the importer), stating its commitment to pay a third party (seller or the exporter), a specific amount, for the purchase of goods by its customer, who is the buyer. The seller has to meet the conditions given in the document and

K

L

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 16

submit the relevant documents, in order to receive the payment. Letters of credit are mainly used in international trade transactions, wherein the customer and the supplier live in different countries.

Line of Credit

A pre-approved loan authorisation with a specific borrowing limit based on creditworthiness. A line of credit allows borrowers to obtain a number of loans without re-applying each time as long as the total of borrowed funds does not exceed the credit limit.

Liquid Assets Assets, generally of a short term, that can be converted into cash.

Liquidation The winding down of the business affairs and operations of a failed insured depository institution through the orderly disposition of its assets after it has been placed in receivership.

Liquidity The ability to service debt and redeem or reschedule liabilities when they mature, and the ability to exchange other assets for cash.

Liquidity Gap Discrepancy between incoming cash flows from the cover pool and interest or principal payments due on the privileged liabilities.

Liquidity Risk

Liquidity is the ability fund increases in assets and meet obligations as they become due, without incurring unacceptable losses.

There are two types of liquidity risk: market liquidity risk and funding liquidity risk. Market liquidity risk is the risk that the bank cannot easily offset or eliminate a position without significantly affecting the market price because of inadequate market depth or market disruption.

Funding liquidity risk is the risk that the bank will not be able to efficiently meet both expected and unexpected current and future cashflow and collateral needs without affecting either daily operations or the financial condition of the bank.

Liquidation Damages

A clause, which is commonly found in contracts, wherein the parties agree to pay a fixed amount, in case of any breach of the contractual provisions. The party, who violates the provisions, has to pay the amount to the aggrieved party.

Lock-in Period A guarantee given by the lender that there will be no change in the quoted mortgage rates for a specified period of time, which is called the lock-in period.

Long Term Debt

An amount owed for a period exceeding one year, from the date of last balance sheet/accounting year. Otherwise known as funded debts, long term debts refers to those loans, which become due, after one year from the last balance sheet/accounting year. Such debts can be a bank loan, bonds, mortgage, debenture, or other obligations.

Loss Excess of expenditures over revenue for a period or activity.

Loss Given Default (LGD) This is an estimate of the amount of the exposure at default that will not be recovered. It also includes other costs such as legal costs.

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 17

Back to Content (A-Z Selector)

Margin The rate taken by the lender over the cost of funds, which effectively represents the entity’s profit and remuneration for taking the risk of the loan; also known as spread.

Market Risk The risk of loss (in both the banking and trading book) as a result of unfavourable changes in foreign exchange rates, interest rates, equity prices, credit spreads and commodity prices.

Maturity The term maturity is used to indicate the end of investment period of any fixed investment or security.

Maturity Date Maturity date is the date on which the investment or security attains maturity.

Monetary Policy A government’s policy towards the supply of credit.

Model Risk The risk that business decisions are made using model results that are incorrect. This includes the possibility of losing perspective of the limitations of models in general and the pitfalls related with their use.

Mortgage A debt instrument used in a real estate transaction where the property is the collateral for the loan. A mortgage gives the lender a right to take possession of the property if the borrower fails to pay off the loan.

Mortgage Loan A loan made by a lender to a borrower to finance real estate.

Back to Content (A-Z Selector)

Net Assets Excess of the value of securities owned, cash, receivables, and other assets over the liabilities of the company.

Net Income Excess or deficit of total revenues and gains compared with total expenses and losses for an accounting period.

Net Interest Margin Net interest margin is the net interest income divided by average interest earning assets.

Net Operating Loss A total loss that is calculated for a tax year and is attributed to business or casualty losses.

Non-investment Grade Credit ratings equal to or lower than "BB+" (double B plus).

M

N

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 18

Non-performing loan (NPL) When a borrower is overdue, typically 90 + days in arrears or as defined in the transaction documents.

Non-recourse Loan A loan which is secured by collateral and for which the borrower is not personally liable, is called a non-recourse loan.

Net Risk See residual risk.

Notching A movement in rating (up or down).

Nostro Account An account held at a foreign bank, used for the receipt and delivery of funds in settlement of trades.

NPL Ratio The ratio of non-performing loans and advances to total gross loans and advanced expressed as a percentage.

Back to Content (A-Z Selector)

Operational Risk The risk of loss resulting from inadequate or failed internal processes, people or systems or from external events. This includes legal risk, but excludes strategic risk and reputational risk.

Original Principal Balance The amount borrowed by any borrower is called the original principal balance.

Online (Internet) Banking The accessing of bank information, accounts and transactions with the help of a computer through the financial institution's website on the Internet is called online banking. It is also called e-banking.

Overdraft When the amount of money withdrawn from a bank account is greater than the amount actually available in the account, the excess is known as an overdraft, and the account is said to be overdrawn.

Origination Fee The charges a lender or creditor levies for processing a loan. It includes cost of loan document preparation, verification of the credit history of the borrower and conducting an overall appraisal.

Ordinary Dividends Dividends, which are a distribution of the profits of a company, are called ordinary dividends.

Ordinary Income Income, not qualifying as a capital gain, is called ordinary income.

Back to Content (A-Z Selector)

O

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 19

Past Due Item Any note or other time instrument of indebtedness that has not been paid on the due date.

Payee Payee is the person to whom the money is to be paid by the payer.

Payer Payer is the person who pays the money to the payee.

Performing An obligation that performs according to its contractual obligations.

Point-in-time Rating A credit rating based on point-in-time risk measures. Point-in-time measures assume the financial condition of the borrower will remain as it currently is. Compare with through-the-cycle rating.

Point of Sale (POS)

The term point of sale can refer to either:

the location at which a transaction takes place; or

systems that allow bank customers to effect transfers of funds from their deposit accounts and other financial transactions at retail establishments.

Political Risk

The exposure to a loss in cross-border lending, caused by political factors in a certain country, political factors which are, at least to some extent, under the control of the government but not under the control of an entity.

Portfolio A bank’s loan and investment assets.

Pre-paid Expense Cost incurred to acquire economically useful goods or services that are expected to be consumed in the revenue-earning process within the operating cycle.

Primary (Tier 1/I) Capital

Primary capital consists of issued ordinary share capital, hybrid debt capital, perpetual preference share capital, retained earnings and reserves. This amount is then reduced by the portion of capital that is allocated to trading activities and other regulatory deductions.

Principal Principal is basic amount which is invested to yield returns over a certain period of time at a given rate of interest.

Probability of Default (PD) Quantification of the likelihood of a borrower being unable to repay during a specific time horizon, usually 12 months.

Provision To set aside or deduct an amount from operating income to cover expected or identified loan losses.

Back to Content (A-Z Selector)

P

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 20

Qualified Opinion An auditor's opinion mentioned in his report which holds some reservations regarding the process of audit is called a qualified opinion.

Quality Spread The difference between the yields of government securities and non-government (public/private) securities, as a result of different ratings or quality, is called a quality spread.

Back to Content (A-Z Selector)

Rating Outlook A rating outlook indicates the potential direction of a rating over the medium term, typically a one to two year period.

Rating Watch Indicates that a rating is under review for possible change in the short-term, and the movement may be either positive or negative.

Recapitalisation

An internal reorganisation of an entity including a rearrangement of the capital structure by changing the kind of stock or the number of shares outstanding or issuing stock instead of bonds. It is distinguished from most other types of reorganisation because it involves only one entity and is usually accomplished by the surrender by shareholders of their securities for other stock or securities of a different type.

Refinance Refinance means clearing the current loan with the proceeds of a new one and using the same property for collateral.

Reference Asset An asset such as debt instrument which has a credit derivative is called as a reference asset.

Regulatory Capital The total of primary, secondary and tertiary capital.

Reinvestment Risk The risk that arises from the fact that dividends or any yields may not be eligible for investment to earn the rate of interest.

Reserve Account An account which is maintained by depositing undistributed parts of profit for future needs is called as a reserve account.

Reserve Requirement Cash money or liquidity that a banks need to hold with the Reserve Bank (of its home country).

Residual Value The anticipated value that a company calculates, to sell its asset at the end of its full life.

Retained Earnings The accumulation of an entity’s profits less any dividends paid out.

Q

R

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 21

Repricing Repricing means a change in the rate of interest.

Repurchase Agreement (REPO) Agreement whereby an institution purchases securities under a situation that the seller will repurchase the securities within a certain time period at a certain price.

Reputational Risk

The risk of impairment of an entity’s image in the community or the long-term trust placed in it by its shareholders as a result of a variety of factors, such as performance, strategy execution, the ability to create shareholder value, or an activity, action or stance taken by the entity.

Residual Risk Residual risk is the product of the impact of the risk on the objective(s) and the likelihood of the risk occurring taking into consideration current management actions/controls in place to mitigate the risk

Return on Capital A measure which determines how a company will optimise its funds.

Revenues Sales of products, merchandise, and services; and earnings from interest, dividends, rents.

Revolving Credit

A credit agreement that allows a customer to borrow against a preapproved credit line when purchasing goods and services. The borrower is only billed for the amount that is actually borrowed plus any interest due.

Risk

The possibility of an outcome not occurring as expected. It can be measured and is not the same as uncertainty, which is not measurable. In financial terms, risk refers to the possibility of financial loss. It can be classified as credit risk, market risk and operational risk.

Risk Acceptance

Risk acceptance is used in risk management to describe an informed decision to accept the consequences and likelihood of a particular risk. In terms of best practice, risk can only be accepted if it can be illustrated that the risk is within set risk appetite limits.

Risk Appetite

The quantum of risk the group is willing to accept in pursuit of its business strategy. Risk appetite is expressed quantitatively as risk measures such as economic capital and risk limits, and qualitatively in terms of policies and controls.

Risk Avoidance Risk avoidance is used in risk management to describe an informed decision not to become involved in activities that lead to the possibility of the risk being realised.

Risk Identification The ongoing recognition and discernment of risk.

Risk Management Process of identifying and monitoring business risks in a manner that offers a risk/return relationship that is acceptable to an entity's operating philosophy.

Risk Management Framework An outline for the management of a risk more fully developed or described elsewhere.

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 22

Risk Management Process

Risk management is the identification, assessment, and prioritisation of risks, followed by coordinated and economical application of resources to minimise, monitor, and control the probability and/or impact of unfortunate events or to maximise the realisation of opportunities.

Risk Management Strategy

The strategies to manage risk include transferring the risk to another party, avoiding the risk, mitigating the risk by reducing the negative effect of the risk, and accepting some or all of the consequences of a particular risk (see transfer of risk, risk avoidance and risk mitigation).

Risk Measurement The evaluation of the magnitude of risk and its impact on the achievement of business objectives.

Risk Mitigation Risk mitigation is used in risk management to describe steps taken to control or prevent an issue or event hazard from causing harm and to reduce risk to a tolerable/acceptable level and within appetite levels.

Risk Monitoring The ongoing and systematic tracking and evaluating of risk management decisions and actions against strategies, risk appetite, policies, limits and key risk indicators.

Risk Reporting The communication of risk information in all phases of the risk management process, namely identification, measurement, management and monitoring.

Risk versus Issue A risk has not (yet) materialised, while an issue has materialised or is in the process doing so.

Risk-Weighted Assets (RWA)

Risk-weighted assets are determined by applying risk weights to balance sheet assets and off-balance-sheet financial instruments according to the relative credit risk of the counterparty. The risk weighting for each balance sheet asset and off-balance-sheet financial instrument is governed by the respective home authorities.

Back to Content (A-Z Selector)

Secondary (Tier 2/II) Capital Secondary capital is mainly made up of subordinated debt, portfolio impairment and 50% of any revaluation reserves and other specified regulatory deductions.

Secured Loan

A loan which is backed by a pledging of real or personal property (collateral) by the borrower to the lender. Unlike unsecured loans, which is backed by a mere promise by the borrower that he will repay the loan, in case of a secured loan, the lender can initiate legal action against the borrower to reclaim and sell the collateral (pledged property).

S

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 23

Securitisation The creation and issuance of tradable securities, such as bonds, that are backed by the income generated by an asset, a loan, a public works project or other revenue source.

Security Security is a risk management function consisting of physical security, information security and personnel integrity.

Settlement Full repayment of an obligation.

Settlement Risk

The risk that an organisation gives, but fails to receive, consideration from a counterparty during the settlement of a transaction. The settlement may be cash or securities.

Foreign exchange settlement risk is the risk of loss when a bank in a foreign exchange transaction pays the currency it sold but does not receive the currency it bought.

Short Term Current; ordinarily less than one year.

Short-term rating A credit rating based on the opinion of the ability to honour short term (less than a year) obligations.

Sovereign Risk The risk of default by the government of the country on its obligations.

Strategic Risk

The risk of an adverse impact on capital and earnings due to business policy decisions (made or not made), changes in the economic environment, deficient or insufficient implementation of decisions, or failure to adapt to changes in the environment.

Strategic risk is either the failure to do the right thing, doing the right thing poorly, or doing the wrong thing.

Subordinated Debt Refers to the status of the debt. In the event of the bankruptcy or liquidation of the debtor, subordinated debt only has a secondary claim on repayments, after other debt has been repaid.

Syndicated Loan

A very large loan extended by a group of small banks to a single borrower, especially corporate borrowers. In most cases of syndicated loans, there will be a lead bank, which provides a part of the loan and syndicates the balance amount to other banks.

Systemic Risk Risk associated with the general health or structure of the financial system which would have serious adverse effects on economic conditions or financial stability.

Back to Content (A-Z Selector)

Tertiary (Tier 3/III) Capital Tertiary capital means:

T

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 24

accrued current-year uncapitalised net profits derived from trading activities; and

capital obtained by means of unsecured subordinated loans, subject to such conditions as may be prescribed.

Through-the-cycle Rating A credit rating based on through-the-cycle risk measures. Through-the-cycle measures evaluate the financial condition of the borrower over a longer term, incorporating a full economic (or business) cycle.

Time Deposit

A time deposit (also known as a term deposit) is a money deposit at a bank that cannot be withdrawn for a certain "term" or period of time. When the term is over it can be withdrawn, or it can be held for another term. The longer the term, the better the yield on the money. Generally, there are significant penalties for early withdrawal.

Transfer of Risk Transfer of risk is used in risk management to describe the shifting of the burden of the risk to another party. Insurance is a common example of risk transfer.

Trading Book

This comprises positions in financial instruments and commodities, including derivative products and other off-balance-sheet instruments that are held with trading intent or to hedge other elements of the trading book. It includes financial instruments and commodities that:

are held for short-term resale; or

are held with the intention of benefiting from price variations; or

arise from broking and market making; or

are held to hedge other elements of the trading book.

Treasury Bill Short-term obligation that bears no interest and is sold at a discount.

Treasury Note Intermediate-term obligation that matures one to five years from issuance and bears interest.

Back to Content (A-Z Selector)

Unaudited Financial Statements (or Management Accounts)

Financial statements which have not undergone a detailed audit examination by an independent certified accountant.

Underwriting Risk When an investment banker buys the balance or all of the new shares that a company is issuing, the risk that the price will go down before they are sold, or that investors will not want to buy them.

Unexpected Loss (UL)

Losses that may exceed the expected loss within a certain period (e.g. one year) and within a specified confidence level (i.e. 99,93%). Unexpected loss is the difference between value at risk and expected loss.

U

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 25

Unqualified Opinion A word used to depict a suggestion letter concomitant with scrutinised financial statements.

Ursury Laws The jurisprudences setting up the uttermost permissible rates of interest that can be charged on certain types of credit extensions to particular kinds of borrowers.

Use Test

Requirement that the components of advanced approaches for the calculation of regulatory capital should not be used merely for the calculation of regulatory capital. Instead they should play an essential role in how a bank measures and manages risk in its business.

Back to Content (A-Z Selector)

Value at Risk (VaR)

Formally, this is the probabilistic bound of losses over a given period (the holding period) expressed in terms of a specified degree of confidence (the confidence interval). Put more simply, VaR is the worst-case loss expected over the holding period within the probability set out by the confidence interval. Larger losses are possible, but with a lower probability.

Variance This is a stats-related word which measures the distribution of information, like rates or costs around the mean.

Variance Swap This relates to an OTC fiscal derivative which enables a person to speculate on or hedging jeopardies connected with unpredictability of some underlying product (e.g. exchange/interest rate or stock index).

Back to Content (A-Z Selector)

V

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 26

Waiver In banking terms, a waiver is relinquishing the rights. Sometimes also considered to be the exemption or settlement of a part of debt.

Warehouse Lines of Credit Warehouse line of credit is a facility provided to the borrower to get a warehouse mortgage portfolio for future security.

Wholesale Banking Wholesale banking is a term used for banks which offer services to other corporate entities, large institutions and other financial institutions.

Withdrawals Removing of funds from a bank account is called as making a withdrawal.

Without Recourse A term which signifies that the buyer is responsible for non-performance of an asset or non-payment of an instrument, instead of the seller.

Working Capital In banking terms, working capital is defined as the difference between current assets and current liabilities.

Write-off The total reduction in the value of an asset.

Back to Content (A-Z Selector)

Year-on-year (y-o-y or y/y) Year-on-year. Used to compare change over a 12-month period.

Yield Curve Yield curve is a graph or a curve that shows the relationship between maturity dates and yield.

Yield The returns earned on a stock or a bond, as per the effective rate of interest on the effective date, is called a yield in the banking terms.

Yield Curve Risk Yield curve risk is the huge risk involved in a fixed income instrument, due to major fluctuations in the market rates of interest.

Yield-to-maturity (YTM) The average annual yield that an investor receives because he holds it for life or till the maturity date is called as the yield to maturity.

Back to Content (A-Z Selector)

W

Y

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 27

Z-score Z score is a measure, used in the banking field, to determine the difference between a single data point and a normal data point.

Zero Balance Zero balance is when the total outstanding balance is paid and there are no new charges or cash advances during a billing cycle.

Zero Coupon Yield Curve Zero coupon yield curve is also called as spot yield curve, and is used to determine discount factors.

Back to Content (A-Z Selector)

Z

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 28

Back to Content (A-Z Selector)

Term Formula Explanation

Capital Adequacy Ratio (CAR) Tier I Capital + Tier II Capital / Risk-Weighted Assets

Determines the bank's capacity to meet its current l iabilities and other

risks such as credit risk and operational risk. A CAR below the minimum

statutory level indicates that the bank is not adequately capitalised to

expand its operations.

Net advances to Customer deposits + Short-Term Funding Net Advances / Customer Deposits + Short-Term FundingIndicates the percentage of the total deposits locked into non-liquid

assets. A high figure denotes low liquidity.

Liquid Assets to Total Funding Liquid Assets + Marketable Debt Securities / Deposits & Market FundingMeasures a bank's funding match to short term investments and

whether they could be coverted quickly to cover redemption.

Bad Debt Charge to Total Operating Income Bad Debt Charge (income statement) / Operating IncomeMeasures the burden that uncollectable debt is placing on the bank's

operating efficiency.

Cost Ratio Opereating Expenses / Total Operating Income Measures a bank's margin after paying funding sources.

ROaE Net Income (Adj.) / Average Common Shareholder's Equity Measures a bank's ability to build equity through retained earnings.

ROaA Net Income (Adj.) / Average Total AssetsMeasures how a bank is managing its assets to optimise its

profitability.

Liquidity

Net Advances to Customer Deposits Net Advances / Customer Deposits

Measures the relative portion of a bank's loan portfolio that is funded

by customer deposits. This ratio aids analysis of the role deposits play

as a funding source.

Capitalisaton

Internal Capital Generation Measures how quickly a bank is able to generate equity capital.

Leverage Ratio

Net Income / Shareholder's Equity

Total Capital & Reserves / Total assetsA measure of the solvency of a bank, this ratio helps a bank assess its

ability to meet obligations and absorb unexpected losses.

Net Interest Margin Net Interest Income / Average Earning Assets

Measures a bank's margin after paying funding sources and how

successful a bank's investment decisions are compared to its debt

situation.

Non-Interest Income to Total Operating Income Other Income / Operating IncomeMeasures the proportion of a bank's total income that have been

generated by non-intrest related activities.

Profitability

Total Loan Loss Reserves to Gross Advances Total Loan Loss Reserves / Gross AdvancesIndicates the propotion of the total portfolio that has been set aside but

not charged off.

Bad Debt Charge to Gross Advances Bad Debt Charge (income statement) / Average Gross Advances (Adj.) Measure the proportion of loans that is estimated to be uncollectable.

Liquid Assets to Total Assets Liquid Assets + Marketable Debt Securities / Total AssetsMeasures the extent to which liquid assets can support a bank's asset

base.

Asset Quality

Gross Non-Performing Loans Ratio Impaired Loans / Gross Loans Measures the value of delinquent loans from the total loan portfolio.

Net Advances to Total Funding Net Advances / Total Funding (excl. equity)Measures the percentage of funding that is tied up in loans. The higher

the ratio, the less l iquid a bank is.

Formulas

February 13, 2014 Dictionary of Terms, Acronyms and Formulas Page | 29

ALL GCR CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS, TERMS OF USE OF SUCH RATINGS AND DISCLAIMERS. PLEASE READ THESE LIMITATIONS, TERMS OF USE AND

DISCLAIMERS BY FOLLOWING THIS LINK:HTTP://GLOBALRATINGS.NET/UNDERSTANDINGRATINGS. IN ADDITION, RATING SCALES AND DEFINITIONS ARE AVAILABLE ON GCR’S PUBLIC

WEB SITE AT WWW.GLOBALRATINGS.NET/RATINGSINFORMATION. PUBLISHED RATINGS, CRITERIA, AND METHODOLOGIES ARE AVAILABLE FROM THIS SITE AT ALL TIMES. GCR'S

CODE OF CONDUCT, CONFIDENTIALITY, CONFLICTS OF INTEREST, COMPLIANCE, AND OTHER RELEVANT POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE

UNDERSTANDING RATINGS SECTION OF THIS SITE.

CREDIT RATINGS ISSUED AND RESEARCH PUBLICATIONS PUBLISHED BY GCR, ARE GCR’S OPINIONS, AS AT THE DATE OF ISSUE OR PUBLICATION THEREOF, OF THE RELATIVE FUTURE

CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. GCR DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL

AND/OR FINANCIAL OBLIGATIONS AS THEY BECOME DUE. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: FRAUD, MARKET LIQUIDITY RISK,

MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND GCR’S OPINIONS INCLUDED IN GCR’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT.

CREDIT RATINGS AND GCR’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND GCR’S PUBLICATIONS ARE NOT AND

DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL OR HOLD PARTICULAR SECURITIES. NEITHER GCR’S CREDIT RATINGS, NOR ITS PUBLICATIONS, COMMENT ON THE

SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. GCR ISSUES ITS CREDIT RATINGS AND PUBLISHES GCR’S PUBLICATIONS WITH THE EXPECTATION AND

UNDERSTANDING THAT EACH INVESTOR WILL MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING OR SALE.

Copyright © 2013 Global Credit Rating Co (Pty) Ltd. INFORMATION PUBLISHED BY GCR MAY NOT BE COPIED OR OTHERWISE REPRODUCED OR DISCLOSED, IN WHOLE OR IN

PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT GCR’S PRIOR WRITTEN CONSENT. Credit ratings are solicited by,

or on behalf of, the issuer of the instrument in respect of which the rating is issued, and GCR is compensated for the provision of these ratings.

Information sources used to prepare the ratings are set out in each credit rating report and/or rating notification and include the following: parties

involved in the ratings and public information. All information used to prepare the ratings is obtained by GCR from sources reasonably believed by it to

be accurate and reliable. Although GCR will at all times use its best efforts and practices to ensure that the information it relies on is accurate at the time,

GCR does not provide any warranty in respect of, nor is it otherwise responsible for, the accurateness of such information. GCR adopts all reasonable

measures to ensure that the information it uses in assigning a credit rating is of sufficient quality and that such information is obtained from sources that

GCR, acting reasonably, considers to be reliable, including, when appropriate, independent third-party sources. However, GCR cannot in every instance

independently verify or validate information received in the rating process. Under no circumstances shall GCR have any liability to any person or entity

for (a) any loss or damage suffered by such person or entity caused by, resulting from, or relating to, any error made by GCR, whether negligently

(including gross negligence) or otherwise, or other circumstance or contingency outside the control of GCR or any of its directors, officers, employees or

agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such

information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits)

suffered by such person or entity, as a result of the use of or inability to use any such information. The ratings, financial reporting analysis, projections,

and other observations, if any, constituting part of the information contained in each credit rating report and/or rating notification are, and must be

construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. Each user of the

information contained in each credit rating report and/or rating notification must make its own study and evaluation of each security it may consider

purchasing, holding or selling. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR

FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY GCR IN ANY FORM OR

MANNER WHATSOEVER.