discontinued operations. academic resource center discontinued operations page 2 typical coverage of...

TRANSCRIPT

Discontinued operations

Academic Resource Center

Discontinued operations Page 2

Typical coverage of US GAAP

► Criteria for classification as non-current assets held for sale

► Criteria for classification as discontinued operations

► Valuation of discontinued operations

► Impact on depreciation

► Presentation of discontinued operations:

► Impact on comparative financial statements:

► Balance sheet presentation

► Income statement presentation

► Cash flow presentation

► Treatment when no longer qualified as a non-current asset held for sale

Academic Resource Center

Discontinued operations Page 3

Executive summary

► Under both IFRS and US GAAP, a discontinued operation represents a component of an entity that has been disposed of or is held for sale. In the 2010 edition of the AICPA’s Accounting Trends and Techniques, of the 500 companies surveyed, 44 companies discontinued or planned to discontinue the operations of a component of an entity.

► IFRS narrowly defines what qualifies as a discontinued operation. US GAAP more broadly defines discontinued operations and could include asset groups smaller than those allowed under IFRS. ASC 205-20-45-1 also requires that: “(a) the operations and cash flows of the component have been (or will be) eliminated from the ongoing operations of the entity as a result of the disposal transaction and (b) the entity will not have any significant continuing involvement in the operations of the component after the disposal transaction.” There is no similar requirement in IFRS.

Academic Resource Center

Discontinued operations Page 4

Executive summary

► There are differences in the presentation of discontinued operations:

► Balance sheet – IFRS does not require restatement of comparative information, while US GAAP does not provide any specific guidance on comparative information.

► Income statement – IFRS requires more extensive disclosures than US GAAP.

► Cash flows – IFRS 5.33 requires comparative disclosure of “the net cash flows attributable to the operating, investing and financing activities,” while US GAAP does not have a similar requirement.

Academic Resource Center

Discontinued operations Page 5

Primary pronouncements

US GAAP

► ASC 205-20, Discontinued Operations

► ASC 360, Property, Plant, and Equipment

IFRS

► IFRS 5, non-current Assets Held for Sale and Discontinued Operations

► IAS 36, Impairment of Assets

Academic Resource Center

Discontinued operations Page 6

Progress on convergence

► In September 2008, the Boards issued proposed amendments to ASC 205-20 and IFRS 5 to converge the definition of discontinued operations as well as the related disclosure requirements. The comment period on the ED ended in January 2009. In April 2010, the boards agreed that the ED should be republished. In the board meeting held on March 29, 2011, the IASB determined not to issue an ED until the FASB issues its ED and receives feedback.

► This project is not included as an active project in the IASB work plan as of March 2012.

Academic Resource Center

Discontinued operations Page 7

Criteria for classification as non-current assets held for sale

The following criteria must be met for a non-current asset (disposal group) to be classified as held for sale:

► The assets are available for immediate sale in their present condition.► Management commits to a plan to sell the assets.► Management is actively seeking a buyer.► The sale is probable and will generally occur within one year.► The selling price is reasonable in relation to the current value.► It is unlikely there will be any significant changes to the plan to sell the assets.

Similar

IFRSUS GAAP

Academic Resource Center

Discontinued operations Page 8

Criteria for classification as non-current assets held for sale

IFRS

► It must be “highly probable” the sale will occur within one year.

► IFRS 5, Appendix A, defines highly probable as “significantly more likely than probable.”

► IFRS 5.8 lists the criteria for a sale to be highly probable. Other than differences in terminology, there are no significant differences between US GAAP and IFRS.

US GAAP

► It must be probable the sale will occur within one year.

Academic Resource Center

Discontinued operations Page 9

Criteria for classification as discontinued operations

A discontinued operation is defined as a component of an entity that is held for sale or has been disposed. The definitions under both standards generally allow the inclusion of major lines of business and major geographic areas of operation.

Similar

IFRSUS GAAP

Academic Resource Center

Discontinued operations Page 10

Criteria for classification as discontinued operations

IFRS

► No similar requirement.

US GAAP

► More broadly defines what qualifies as a discontinued operation and could include asset groups smaller than those allowed under IFRS.

► ASC 205-20-45-1 requires that “(a) the operations and cash flows of the component have been (or will be) eliminated from the ongoing operations of the entity as a result of the disposal transaction and (b) the entity will not have any significant continuing involvement in the operations of the component after the disposal transaction.”

Academic Resource Center

Discontinued operations Page 11

Criteria for classification as discontinued operations Summary

IFRS

► Component of an entity held for sale or one that has been disposed.

► Separate major parts of business or geographic area of operation.

► No similar requirement.

► No similar requirement.

► A single coordinated disposal plan.

US GAAP

► Component of an entity held for sale or one that has been disposed.

► Operations and cash flows can be clearly distinguished.

► Operations and cash flows will be eliminated from ongoing operations.

► No significant continuing involvement in the operations.

► No similar requirement.

Convergence: Based on tentative decisions to date, the Boards have decided to adopt a common definition as currently defined under IFRS. The Boards have also agreed on certain disclosures required if an entity retains continuing involvement with a discontinued operation after the disposal date.

Academic Resource Center

Discontinued operations Page 12

Example 1 – criteria for classification as a discontinued operationThe Copper Mining Company (CMC) is a fully integrated copper company. CMC has three separate operating segments. The mining segment mines the copper and had revenues of $1.0 billion and a net negative cash flow of $0.2 billion. The industrial segment smelts the copper into ingots and had revenues of $1.2 billion and a net cash flow of $0.2 billion. The distribution segment sells the copper ingots to third parties and had revenues of $1.5 billion and a net cash flow of $0.3 billion.

Criteria for discontinued operations example

Management of CMC has received an unsolicited offer from a competitor for its industrial segment, which it believes reflects the fair value of these operations. The competitor wants to complete the purchase in the next three months. CMC’s Board of Directors has authorized management’s plan to immediately sell its industrial segment to this competitor and retain the remaining two segments. As part of the proposed purchase, the competitor requires CMC to agree to process all its copper ore through its smelters for the next five years at a cost of 4 cents per ton. This is slightly less than CMC’s current cost of smelting the ore. The competitor also requires that CMC’s management continues to manage the industrial segment for six months after the sale. This will allow the competitor to hire its own management team to run the smelting operations. As is currently the case, CMC’s distribution segment would then sell the copper ingots to third parties.

Academic Resource Center

Discontinued operations Page 13

Criteria for discontinued operations example

Example 1 (continued):

► Does CMC’s industrial segment qualify as a discontinued operation under US GAAP? Explain your answer.

► Does CMC’s industrial segment qualify as a discontinued operation under IFRS? Explain your answer.

Academic Resource Center

Discontinued operations Page 14

Example 1 solution:

US GAAP:

The requirements for classification of the industrial segment as a non-current asset held for sale have been met as stated in the discussion above. The operations and cash flows of the industrial segment are clearly distinguishable from the rest of the operations. However, it appears CMC will have significant continuing involvement in the operations of the industrial segment after the disposal date. Therefore, this plan would not qualify for accounting as a discontinued operation.

Criteria for discontinued operations example

Academic Resource Center

Discontinued operations Page 15

Example 1 solution (continued):

IFRS:

The requirements for classification of the industrial segment as a non-current asset held for sale have been met:► The assets are available for immediate sale in their present condition.► Management has committed to a plan to sell the assets.► It has a buyer.► The sale is probable and likely will occur within one year.► The selling price is reasonable in relation to the current value.► It is unlikely there will be any significant changes to the plan to sell the assets.

The single coordinated plan involves the sale of a component of CMC, which represents a major separate line of business and, therefore, would qualify as a discontinued operation.

Criteria for discontinued operations example

Academic Resource Center

Discontinued operations Page 16

Valuation of discontinued operations

A non-current asset held for sale or a disposal group held for sale should be remeasured at the lower of its carrying value or fair value less selling costs. Any resulting gain or loss will be included in the income or loss of the discontinued operations.

Similar

IFRSUS GAAP

Academic Resource Center

Discontinued operations Page 17

Impact on depreciation

Both US GAAP and IFRS specify that assets held for sale should not be depreciated. Similar

IFRSUS GAAP

Academic Resource Center

Discontinued operations Page 18

Presentation – impact on comparative financial statements

Disclosure of relevant information regarding the discontinued operations is required. Similar

IFRSUS GAAP

Academic Resource Center

Discontinued operations Page 19

PresentationBalance sheet

Assets and liabilities of discontinued operations must be shown separately. Similar

IFRSUS GAAP

Academic Resource Center

Discontinued operations Page 20

PresentationBalance sheet

IFRS

► Does not require restatement of comparative information.

US GAAP

► No specific guidance on whether comparative information needs to be restated.

Academic Resource Center

Discontinued operations Page 21

Example 2a – balance sheet presentation example

Company A has met all the requirements for accounting for a discontinued operation under both US GAAP and IFRS in its 2012 comparative financial statements. Indicate the minimum required disclosure for discontinued operations by placing an X in the chart below. If the disclosure is not mandatory, place an NR (not required) in the chart.

Balance sheet presentation example

US GAAP IFRS

2012 2011 2012 2011

Cash

Total assets

Total liabilities

Net assets

Academic Resource Center

Discontinued operations Page 22

Example 2a solution:

Both US GAAP and IFRS require that assets and liabilities of discontinued operations be shown separately on the balance sheet. IFRS does not require restatement of comparative information on the balance sheet. US GAAP does not provide any specific guidance on whether comparative information on the balance sheet needs to be restated.

Balance sheet presentation example

US GAAP IFRS

2012 2011 2012 2011

Cash NR NR NR NR

Total assets X NR X NR

Total liabilities X NR X NR

Net assets NR NR NR NR

Academic Resource Center

Discontinued operations Page 23

PresentationIncome statement

The results of discontinued operations must be shown separately from continuing operations.

Comparative information must be restated.

Similar

IFRSUS GAAP

Revenue, pretax income (loss) and any gain (loss) on remeasurement for discontinued operations must be disclosed.

Similar

Similar

Academic Resource Center

Discontinued operations Page 24

PresentationIncome statement

IFRS

► Requires disclosure of expenses, income taxes on operations and income taxes on gains (losses) on remeasurement related to discontinued operations.

US GAAP

► Requires disclosure of the total tax income related to discontinued operations.

Academic Resource Center

Discontinued operations Page 25

Example 2b – income statement presentation

Using the information from the previous example, indicate the minimum required disclosure for discontinued operations by placing an X in the chart. If the disclosure is not mandatory place an NR (not required) in the chart.

Income statement presentation example

US GAAP IFRS

2012 2011 2012 2011

Revenue

Expenses

Pretax income

Income tax on operations

Remeasurement gain or loss

Income tax on remeasurement

Net interest income (expense)

Total income taxes

Academic Resource Center

Discontinued operations Page 26

Example 2b solution:

Both US GAAP and IFRS require the results of discontinued operations be shown separately from continuing operations on the income statement. Comparative information on the income statement must be restated. Both require disclosure of revenue, pretax income (loss) and gain (loss) on remeasurement for discontinued operations. US GAAP requires disclosure of the total income tax related to discontinued operations. IFRS requires disclosure of expenses, income taxes on operations and income taxes on gains (losses) on remeasurement related to discontinued operations.

Income statement presentation example

US GAAP IFRS

2010 2009 2010 2009

Revenue X X X X

Expenses NR NR X X

Pretax income X X X X

Income tax on operations NR NR X X

Remeasurement gain or loss X X X X

Income tax on remeasurement NR NR X X

Net interest income (expense) NR NR NR NR

Total income taxes X X NR NR

Academic Resource Center

Discontinued operations Page 27

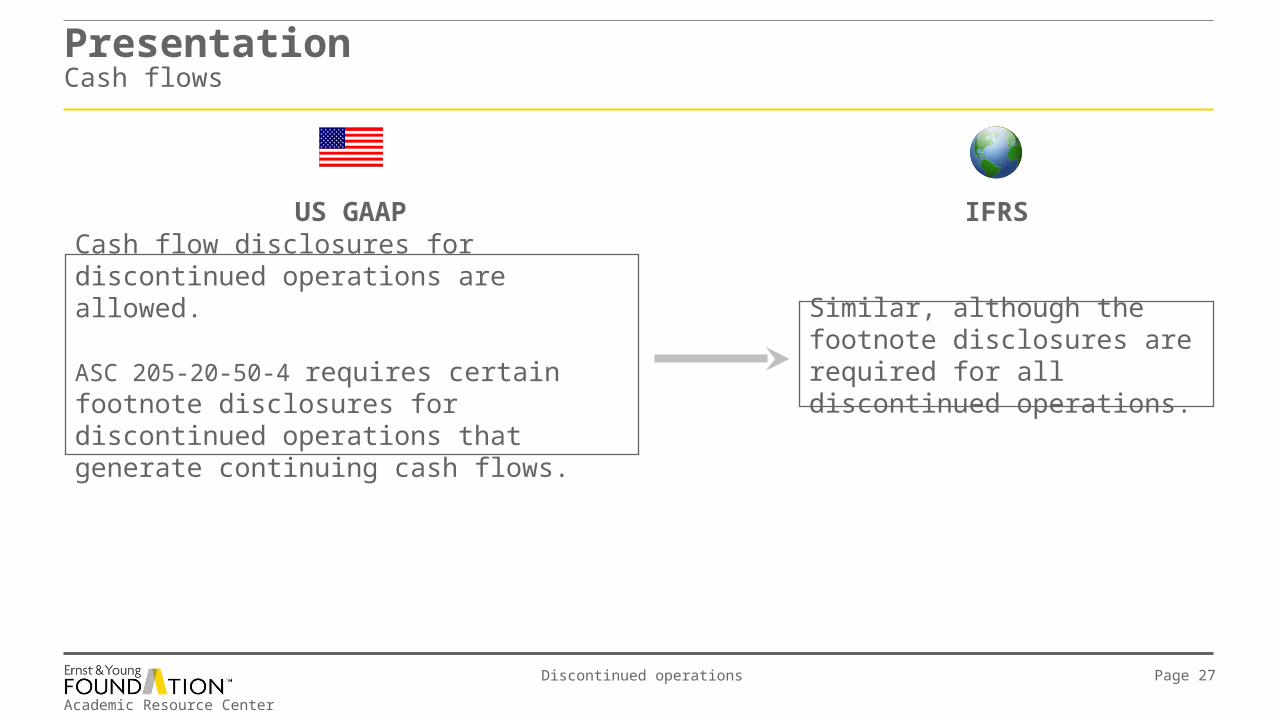

PresentationCash flows

Cash flow disclosures for discontinued operations are allowed.

ASC 205-20-50-4 requires certain footnote disclosures for discontinued operations that generate continuing cash flows.

Similar, although the footnote disclosures are required for all discontinued operations.

IFRSUS GAAP

Academic Resource Center

Discontinued operations Page 28

PresentationCash flows

IFRS

► Requires disclosure of “the net cash flows attributable to the operating, investing and financing activities of discontinued operations. These disclosures may be presented in either the notes or on the face of the financial statements.

► Restatement of comparative information for prior periods is also required.

US GAAP

► No similar requirement for cash flow disclosures of discontinued operations.

► ASC 230-10-45-24 states that “An entity that nevertheless chooses to report separately operating cash flows of discontinued operations shall do so consistently for all periods affected, which may include periods long after sale or liquidation of the operation.”

Academic Resource Center

Discontinued operations Page 29

Example 2c – cash flows presentation

Using the information from the previous example, indicate the minimum required disclosure for discontinued operations by placing an X in the chart below. If the disclosure is not mandatory, place an NR (not required) in the chart.

Cash flows presentation example

US GAAP IFRS

2010 2009 2010 2009

Cash flows attributable to:

Operating activities

Investing activities

Financing activities

Net cash flows

Academic Resource Center

Discontinued operations Page 30

Example 2c solution:

IFRS requires disclosure of “the net cash flows attributable to the operating, investing and financing activities of discontinued operations. These disclosures may be presented in either the notes or on the face of the financial statements.” Restatement of comparative information for prior periods is also required. US GAAP does not have a similar requirement for cash flow disclosures of discontinued operations.

Cash flows presentation example

US GAAP IFRS

2012 2011 2012 2011

Cash flows attributable to:

Operating activities NR NR X X

Investing activities NR NR X X

Financing activities NR NR X X

Net cash flows NR NR NR NR

Academic Resource Center

Discontinued operations Page 31

Treatment when no longer qualified as a non-current asset held for sale

A non-current asset held for sale should be reclassified to assets held and used. The value of these operations should be recorded at the lesser of:►The original carrying amount adjusted for any depreciation (amortization) expense that would have been recognized had the discontinued operation been continuously classified as a continuing operation.► Its current fair value.

IFRSUS GAAP

Similar except recoverable amount is used instead of fair value.

Academic Resource Center

Discontinued operations Page 32

Treatment when no longer qualified as a non-current asset held for sale

IFRS

► The original carrying amount must also be adjusted for any revaluations had the discontinuing operation been continuously classified as a continuing operation.

US GAAP

► Does not specify that revaluations must be considered when determining the original carrying amount. However, since these operations are being valued at the lesser of the adjusted original cost or the current fair value, it is likely to result in the same valuation. Therefore, this difference is not significant.

Academic Resource Center

Discontinued operations Page 33

Ernst & Young LLP

Assurance | Tax | Transactions | Advisory

About Ernst & YoungErnst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 152,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global and of Ernst & Young Americas operating in the US.

© 2012 Ernst & Young Foundation (US). All Rights Reserved.SCORE No. MM4120C.