dish tv india limited · investment rationale 4 1 poised to be the largest media company in india 2...

TRANSCRIPT

1

2

Dish TV India LimitedInvestor Presentation

Disclaimer

Some of the statements made in this presentation are forward-looking statements and are based on the current beliefs, assumptions, expectations, estimates, objectives and projections of the directors and management of Dish TV India Limited about its business and the industry and markets in which it operates.

These forward-looking statements include, without limitation, statements relating to revenues and earnings. The words “believe”, “anticipate”, “expect”, “estimate", "intend”, “project” and similar expressions are also intended to identify forward looking statements. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond the control of the Company and are difficult to predict.

Consequently, actual results could differ materially from those expressed or forecast in the forward-looking statements as a result of, among other factors, changes in economic and market conditions, changes in the regulatory environment and other business and operational risks. Dish TV India Limited does not undertake to update these forward-looking statements to reflect events or circumstances that may arise after publication.

3

Investment rationale

4

Poised to be the largest Media Company in India1

Significant merger synergies to be realised. Maiden dividend declared in 2Q FY192

At an inflection point; on course to deliver strong growth and margins3

Forthcoming, powerful integration of in-house OTT with DTH to increase urban stickiness

4

Aiming to be debt free in around two years 5

Annuity business with significant Free Cash Flow potential5

Buffered from disruptive technologies; supremacy amongst semi-urban and rural consumers

3

Poised to be the largest media company in India

5

Total Revenues (Rs Bn.)Year ending 31 March 2018

66.962.4

57.250.3

37.6

29.623.7 23.3 23.0

15.4 12.9

0

25

50

75

ZeeEntertainment

Enterprises

Dish TV India Ltd Tata Sky Network 18Media &

Investments

AirtelDigital TV

Sun TVNetwork

PVR D.B.Corp JagranPrakashan

HathwayCable &

Datacom

Den Networks

EBITDA (Rs Bn.)Year ending 31 March 2018

21.0 20.819.7 18.2

14.2

5.8 5.6 4.3 3.5 2.8 1.9

(4)

4

12

20

Sun TVNetwork

ZeeEntertainment

Enterprises

Dish TV India Ltd Tata Sky AirtelDigital TV

JagranPrakashan

D.B.Corp PVR HathwayCable &

Datacom

Den Networks Network18Media &

Investments

Source: Annual reports & company filings

Significant merger synergies to unfold

6

SAMPLE

TEXTSAMPLE

TEXT

~1100 mnCapexsynergies

~700 mnInterest cost synergies

Revenue synergies

Content & administrative cost synergies

Backend services & call centre synergies

~3300 mnabove EBITDA level synergies

5100 mnMerger

synergies

Already realised in 1H FY 19

Supremacy amongst semi-urban and rural consumers

7

Dish easiest to reach /

Most economical

for TV viewing

Distributed row houses

Growing penetration of wireless broadband

Unfeasible to lay fibre/

wired broadband

Negligible requirement

for unlimited

broadband

Larger family size

Inconvenient-Watching

linear TV on mobile screens

India outside big cities

Dish TV India has majority of its subscribers outside top-towns and cities

8

Indian TV Industry

The Indian TV industry

9Source: TV industry size: FICCI-KPMG 2017; Households: BARC India Universe Update 2018; Distribution Industry: MPA Report 2017

AnalogCable28%

Digital Cable39%

Market share - Distribution Industry

DTH33%

2020 INR 821 Bn.TV subscription revenuesCAGR of 8%(2017-2020P)

TV Industry to gain from increasing TV and Pay -TV penetration

Broadcasting Industry

Multiple broadcasters, having 300 pay channels, 577 FTA channels, producing content in more than

15 languages

Total households (in Mn.)

Total TV households (in Mn.)

TV penetration (of total HH’s)

C&S Penetration (of TV HH’s)

2018 2020

298 311

197

66%

83%

220

71%

84%646

702

821

665

761

920

2017

2018

2020P

TV Industry Size (INR Bn.)

Subscription revenues Advertising revenues

20%

33%17%

14%

16%

TV viewing in India

10

95%98%97%

Percentage of single TV households

Source: Percentage of single TV households: BARC

77% large and affluent joint families have single TV’s, implying co-viewing as a consumption pattern

79% of Indian households still have CRT TV’s

All India Urban Rural

Daily tune in on TV:566 Mn. Individuals

Daily time spent per individual03:44:28

(hh:mm:ss)

TV continues to remain the most popular form of entertainment Share of TV viewership universe across age groups

Adults(31-40 yrs)

Kids(2-14 years)

Youth(15-30 years)

Senior(>50 years)

Popular across age groups despite rising internet penetration

11Source: Share of TV viewership by, and across age groups: BARC

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000

51+ yrs

41-50 yrs

31-40 yrs

15-30 yrs

2-14 yrs

2017 2016

22%

Share of TV viewership universe by age groups(in Mn. impressions)

Contrary to popular perception, the youth contributes a massive 33% share of TV viewership, and has seen a growth of 22% in impressions over the year

Youth(15-30 years)

Mature41-50 years

Kids(2-14 years)

Senior(>50 years)

All India internet penetration- 30%

40.7

70.4

120

218

345

14.5 15.3 16.5 18.1 17.9

0

50

100

150

200

250

300

350

400

Dec-13 Dec-14 Dec-15 Dec-16 Dec-17

Broadband subscribers (in Mn.)

Wireless broadband subs (mn) Fixed broadband subs (mn)

12

Pay - TV in India

An overview of the Pay - TV Industry

TV households

197 Mn.

Pay -TV

163 Mn.

Cable Subs

109 Mn.

DTH Subs

54 Mn.

Non - Pay

34 Mn.

Free Dish

22 Mn.

13Source: TV & Pay – TV HH: BARC Universe Update 2018; Distribution by platform: MPA Report 2017; Free Dish subscriber base: MIB Annual Report, 2018

Asymmetry in the Pay - TV Industry

14Source: MPA Report 2017

Abysmally low content cost per subscriber per month in cable is an ARPU dampener for the entire Pay - TV industry

DTH maximized gains from Digitization (initiated in 2012). Majority of cable additions were conversion from Analog to Digital

Despite having only a 33% market share, DTH contributes >53% of subscription revenues earned by broadcasters

Cable DTH

Subscriber market share (%) 67% 33%

Content cost (INR Mn.) 50,938 56,982

Contribution towards subscription revenues of broadcasters 47% 53%

No deadline extension. TRAI Orders effective from February 1, 2019

Subscribers (in Mn.) 2011 2012 2013 2014 2015 2016 2017 2018

Net new additions by DTH 7.3 4.1 3.6 3.9 3.0 3.5 3.7 4.0

New digital additions by Cable 1.1 9.6 13.3 -1.5 9.7 13.5 10.2 6.9

Out of Which Analog seeding 0.0 7.6 11.5 0.0 8.2 12.1 9.0 5.8

Net new additions by Cable 1.1 2.0 1.9 -1.5 1.6 1.4 1.3 1.2

% of new additions by DTH 87% 67% 66% 100% 65% 72% 75% 78%

% of new additions by Cable 13% 33% 34% 0% 35% 28% 25% 22%

DTHCable

15

1,4391,131 1,064 997

103

DirecTV Charter Dish Comcast Netflix

Annual cost of Netflix 1/10th of Pay -TV cost in the US

Annual ARPU (USD) -2016

8054

3011 88 11 7 8 6

USA Australia Sweden Mexico Nigeria

Low cost of OTT vs Pay -TV drove adoption

Pay TV monthly ARPU OTT monthly fee

Source: Cost of OTT vs Pay –TV: Digital TV Research; Annual cost of Netflix : Marymaker Internet Trends Report 2017, : Cost of OTT vs Pay –TV: Digital TV Research & internal est.; Pricing of OTT services : Market Estimates

Emergence of OTT

The global OTT phenomenon

The India exception

600

180 210

Netflix Cable Pack DTH Basic packs

Pricing (per month) of OTT services vis-à-vis cable and DTH80

54

30

11 8 38 11 7 8 6 8

USA Australia Sweden Mexico Nigeria India

Cost of OTT vs Pay -TV per month (in USD) Pay TV monthly ARPU

OTT monthly fee

Low OTT costs compared to traditional Pay -TV platforms, led to higher adoption of OTT content globally

India is an exception to the global OTT phenomenon, with higher cost of OTT vs Pay -TV

16

IPTV as an offering

Reality check: Winning IPTV subscribers. Is it as easy as gaining telecom customers?

Telecom IPTV

Capex requirement Low Front loaded

Physical Infrastructure requirement Low High

Ground Task force Negligible Huge

Overall cost of delivery Low Extremely high per home

Distribution/reaching the last mile

Through local shops/ retail stores Through existing operators having access to homes

Pricing High existing data and voice costs supported aggressive undercutting by new entrant

Traditional C&S prices are too low to be susceptible to undercutting

Consumer experience/ novelty in offering as compared to existing service

Free voice and cheap data Nil ( Change in pipes only)

Potential reach of new technology Pan India Densely populated tier 1 cities

Potential consumers Data starved & aspiring mobile customers

Select consumers having extremely high data requirements

17

IPTV as an offering – An oversimplification of market thesis

IPTV as a threat to DTH – An oversimplification of market thesis! Have we seen this before?

• Mandatory digitization of Analog cable signals (Digital Addressable Systems), started in 2012, was perceived to be a threat to DTH

• DTH had the following advantages over Analog:

• DAS, on the other hand, had the potential to even out all these advantages as follows:

Value proposition DTH DAS

Video Quality Digital Digital

Number of channels High High

Pick and choose channels Available Available

HD channels Available Available

Value proposition DTH Analog

Video Quality Digital Analog

Number of channels Higher Lower

Pick and choose channels Available Not available

HD channels Available Not available

18

IPTV as an offering – An oversimplification .. (continued)

IPTV as a threat to DTH – An oversimplification of market thesis

• However, in reality, DTH emerged stronger than ever before post the event:

DTH Supremacy

19

Increased capacity & content throughput

VDSP Model

Consulting

eSolutionWeb Building

Web Design

Extremely efficient, low cost, video

delivery platform

Consumption of bandwidth

heavy content likely to

increase going forward.

SD HD UHD

Declining transponder

costs – an opportunity

Consolidation in cable &

implementation of the Tariff

Order to ensure a level playing field for DTH

Impact of changes in environment on DTH: mobility/fixed line

20

1.7

5.5

0.93

0.25

0.77

0.11

14.7%14.0%

11.4%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Siti Hathway Den

India broadband uptake as % home passed

Broadband Homes Passed Broadband Subscribers Uptake as (%) homes passed

8281,375

4,642

20,092

66.1%

237.6%

332.8%

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

350.0%

0

5000

10000

15000

20000

25000

Dec -14 Dec -15 Dec -16 Dec -17

Wireless data usage and growth

Wireless data usage (in million GB per year) Growth (YoY In %)

Exponential growth in data consumption on mobile has restricted the need for data through fixed line

21

Impact of changes in environment on DTH: FTTH

Fibre not a game changer!

FTTH Value addition to consumer experience

High speed There are no specific applications which need 1Gbps connectivity and till these applications evolve customers would not necessarily jump onto the Very High Speed broadband.

Data volume Marginal utility of data is negligible

Bundling of data Virtual Data Service Providers or VDSP would be an equally effective substitute to services like FTTH which promise bundled data. Existing last mile service providers like DTH companies would become VDSP’s to offer data benefits to existing subscribers in partnership with their respective mobile service providers on revenue share basis. A win-win for both!

Exponential growth in data consumption on mobile has restricted the need for data through fixed line

Price FTTH also requires corresponding ONTs and Routers/ Wi-Fi devices at home, which add significantly to the costs. These costs cannot be justified if the applications used do not have a need to use 1000 Mbps. Thus price to the end consumer would never be lower than wireless data.

With ARPU’s at 3$ , the DTH industry is not ripe for price disruption. IPTV through FTTH would also not offer any incremental benefit to the consumer thus restricting scope for any disruption.

Global FTTH adoption trends show it has not been disruptive in any of the markets in US or EU, nor has it grown at extraordinary rates having run into a series of hurdles.

22

Impact of changes in environment on DTH: FTTH

Fibre not a game changer .. even when compared to existing fixed line broadband

Global FTTH adoption trends show it has not been disruptive in any of the markets in US or EU, nor has it grown at extraordinary rates having run into a series of hurdles.

3.48

3.19 3.14 3.102.89 2.85 2.79

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Jio Giga fiber 7 Star Digital Spectranet Airtel Atria convergencetechnology

You broadband Hathway

NETFLIX ISP LEADER BOARD - OCTOBER 2018

Current speed Mbps

Source: Netflix ISP speed Index, October 2018

Impact of changes in environment on DTH: new regulations

23

Consulting

eSolutionWeb Building

Web Design

New Tariff Regulations

Creation of a level playing field vis-a-vis

cable

Network Carriage Fees to provide revenue

stability

Transparency in content deals

End of irrational carriage fee revenues as carriage gets

restricted to niche channels.

Pass through of content costs to

de-risk the business

Overall margin expansion

6

5

4

3

2

1

Impact of changes in environment on DTH: new pipes

24

New pipes- IPTV

Subscriber reach

Unlike Pan India footprint of satellite,

IPTV would be restricted to densely

populated tier-1 cities

Last mile

Direct to home versus dependence

on last mile operator in case of

IPTV

Wireline broadband

Limited uptake due to easy

availability of broadband

through wireless

Only 16% of rural viewers have access to internet.

~99% of the rural internet users access internet through their mobile devices.

25

1 + 1 = 11

Dish TV India – The Road Ahead

26

Short Term

FY 2020 – Cricketing action!

• World Cup + IPL to aid growth in revenues and profitability

• In the past:

• Merger synergies and operating leverage would be at play

• Tariff Order to reduce content outgo

World Cup FY2011 (Mn) Growth YoY FY 2015 (Mn) Growth YoY

Net Additions 2.8 Up 95.8% YoY 1.5 Up 87.5% YoY

Revenues 15,246 Up 32.2% YoY 27,816 Up 10.9% YoY

EBITDA 3,269 Up 100.0% YoY 7,331 Up 17.5% YoY

Dish TV India – The Road Ahead

27

Medium Term

FY 2020-2021 – Well positioned to address evolving video needs

• Constant increase in content throughput and capacity; strengthening ability to compete

• Technological innovations to enable subscribers to watch content anywhere, anytime.

• VDSP – Partnering with telcos and broadband players to offer exciting benefits to consumers.

• Emerging as a stronger alternative to bundled offerings

Long Term

FY 2022 – Established and unrivalled

• Leveraging the 23.6 million plus subscribers for competing benefits

• Overall margin expansion

• Solid and regular free cash flows

Consolidation to lead to value creation

28

Dish TV-Videocon

37%

Tata Sky27%

Airtel24%

Sun Direct11%

Reliance1%

Market Share (% of net subscribers)

Source: Market share - TRAI Data, September 2018 [69.45-6 mn]

Higher market share of the combined entity to create synergies

A combined entity with a significant presence across

India

Value creation through synergies

29

Leveraging strengths of

each company

Cost and financial synergies

Revenue synergies

Adopting best practises

Identifying the strengths of each brand

30

High top of the mind brand recall

Value for money offerings

Deep penetration in tier 2 and beyond markets

High brand loyalty in trade circles

Premium segment offerings like 4K

Reasonable presence in urban markets

Popular in regional content markets

Tailor made packages for regional audiences

Presence in key vernacular markets like Orissa and West Bengal

Co-existence of all three brands to target a higher market share while maintaining healthy competition and synergy in backend operations

Adopting best practises- Customer service

31

1 million home visits every month by field service

Faster, Better and Efficient Service model built on a service infrastructure no other DTH player can match

Adoption of the company owned service model for the entire entity

More than 4,000 distributors and around 470,000 dealers Mobile App for subscribers

Call centres across India supported by a large no. of agents

Targeting more than 450 owned service centres and 5,500 company

technicians

Adopting best practises - Backend and IT Operations

32

IVR for faster response

Optimising AHT for better customer experience

Cross utilising critical infrastructure for synergies

Inbound/outbound swap

Synergising backend operations to reap long term benefits and faster turnaround time for customer resolutions

Our core values

33

34

Entering the New Era

Reinvigorating the new entity

35

#JeetoSaareHeart

New leadership mix comprising of select professionals from both

entities

Separate sales teams with uniform structures

Fresh campaigns and branding initiatives. New Brand

Ambassador

Taking the lead in the industry with new customer centric packs-

‘Mera Apna Pack’

The beginning of the transformation into India’s most loved DTH brand!

#AlagHiView

Sharper customer focus with High Definition

36* Exclusive of taxes

Dish TV HD Add-Ons

English Movies & News HD – Rs. 101*

Hindi Entertainment HD - Rs. 133*

All Hindi HD - Rs. 197*

English Cricket HD - Rs. 57*

Tamil HD – Rs. 76*

Sharper than ever focus on boosting HD acquisition and recharges by maximising combined shelf and

retail visibility

Encouraging HD sampling through economical, must-

have HD bouquets

37

Financials

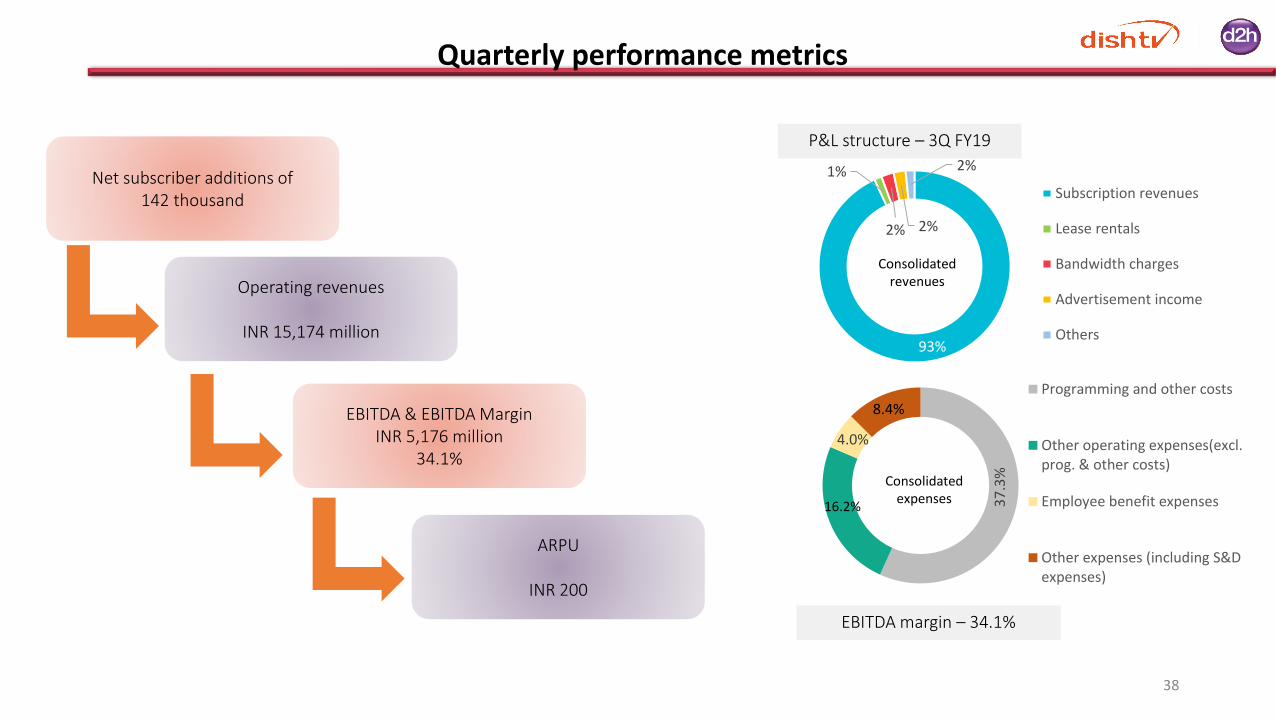

Quarterly performance metrics

38

Net subscriber additions of 142 thousand

EBITDA margin – 34.1%

Operating revenues

INR 15,174 million

EBITDA & EBITDA MarginINR 5,176 million

34.1%

ARPU

INR 200

93%

1%

2% 2%

2%

Subscription revenues

Lease rentals

Bandwidth charges

Advertisement income

Others

Consolidated revenues

37

.3%

16.2%

4.0%

8.4%

Programming and other costs

Other operating expenses(excl.prog. & other costs)

Employee benefit expenses

Other expenses (including S&Dexpenses)

Consolidated expenses

P&L structure – 3Q FY19

Quarter ended Quarter ended

INR Million Dec. 2018 Dec 2017

Operating revenues 15,174 16,143

Expenditure 9,999 11,165

EBITDA 5,176 4,978

EBITDA margin (%) 34.1 30.8

Other income 121 242

Depreciation 3,532 3,525

Finance cost 1,300 1,434

Profit / (Loss) before tax 464 261

Tax expense:

- Current Tax- Current Tax-prior years- Deferred Tax- Deferred Tax- prior years

18192

(1,281)(54)

101-

1,843-

Net Profit / (Loss) for the period 1,527 (1,683)

3QFY 2019 vs. 3QFY 2018Operating revenues break-up

(Rs. mn)

3QFY 2019

Summarized Consolidated P&L - Quarterly

14,126

189

324 300 236 Subscription revenues

Lease rentals

Bandwidth charges

Advertisement income

Teleport services, CPE &Other

39On March 22, 2018, Videocon D2h Limited had merged with and into Dish TV India Limited with the appointed date of the merger being October 1, 2017.

Annual performance metrics

40

Dish TV India Limited’s first set of merged financials for FY18

Combined subscriber base of 23 million

EBITDA margin – 28.4% #

Operating revenues*

INR 62,377

Adjusted EBITDA & Margin*INR 19,690

31.6%

ARPU

INR 201

91%

3%

3%

1% 2%

Subscription revenues

Bandwidth income

Advertising income

Lease rent

Other income

Consolidated revenues

36%

18%

5%

13%

Programming and other costs

Other operating expenses(excl.prog. & other costs)

Employee benefit expenses

Other expenses (including S&Dexpenses)

Consolidated expenses

P&L structure – FY18

* Presuming FY 18 financials represented 12 months each of Dish TV and d2h. * Adjusted EBITDA is EBITDA adjusted for merger expenses to the tune of Rs. 840 million booked in FY18 that have been excluded while calculating Adjusted EBITDA# Merged financials for FY18 basis 12 months of Dish TV and 6 months of d2h

Yearended

Yearended

INR Million Mar. – 2018 Mar. – 2017

Operating revenues 46,342 30,144

Expenditure 33,181 20,464

EBITDA 13,160 9,680

EBITDA margin (%) 28.4 32.1

Other income 542 615

Depreciation 10,717 6,908

Financial expenses 3,964 2,292

Profit / (Loss) before tax (979) 1,095

Current TaxCurrent Tax-prior periodDeferred Tax

53(30)

(166)

9820

(708)

Deferred Tax- prior period 13 -

Net Profit / (Loss) for the period (849) 821

FY 2018 vs. FY 2017Operating revenues break-up

(INR Mn.)

FY 2018

Summarized Consolidated P&L- Annual

42,167

1,225

1,375

670 905

Subscription revenues

Lease rentals

Bandwidth charges

Advertisement income

Teleport services, CPE &Other

41Financials of Dish TV India Limited for the year ended March 31, 2018 represent 12 months financial performance of Dish TV India Limited and 6 months financial performance of Videocon d2h Limited. Financial numbers for FY18 are thus not comparable with FY17. Presuming FY18 financials had represented 12 months each, operating revenues and EBITDA of the Company would have been Rs. 62,377 million and Rs. 19,690 million respectively.

INR Million Sept. 2018 (Unaudited)

Equity and liabilities

Equity

(a) Equity share capital 1,841

(b) Other equity 66,008

Equity attributable to owners of Holding Company 67,849

(c) Non-controlling interest (277)Liabilities(1) Non-current liabilities

(a) Financial liabilities

(i) Borrowings 20,139

(ii) Other financial liabilities 0

(b) Provisions 419

(c) Other non-current liabilities 557(2) Current liabilities

(a) Financial liabilities

(i) Borrowings 2,334

(ii) Trade payables 10,631

(iii) Other financial liabilities 12,370

(b) Other current liabilities 21,290(c) Provisions(d) Current tax liabilities (net)

30,058229

Total Equity & Liabilities 1,65,600

Consolidated Balance Sheet

42

INR Million Sept. 2018 (Unaudited)Assets(1) Non-current assets

(a) Property, plant & equipment 34,615(b) Capital work in progress 7,471(c) Goodwill 62,754(d) Other intangible assets 22,106(e) Financial assets

(i) Investments 1,500(ii) Loans 153(iii) Other financial assets 94

(f) Deferred tax assets (net) 6,080(g) Current tax assets (net) 1,111(h) Other non-current assets 2,210

(2) Current assets(a) Inventories 467(b) Financial assets

(i) Investments(ii) Trade receivables(iii) Cash and cash equivalents(iv) Bank balances other than (iii) above(v) Loans(vi) Other financial assets

(c) Other current assets

01,6011,0821,440

7315,080

7,762

Total assets 1,65,600

43

Thank You