dla piper 2011 hospitality outlook...

TRANSCRIPT

JANUARY 2011

DLA PIPER2011 HOSPITALITY OUTLOOK SURVEY

DLA Piper LLP (US) 1

EXECUTIVE SUMMARY

Buoyed by the rebound of the US economy and an increasing number of hotel assets that traded hands in 2010, the bears have reversed course in dramatic fashion as the overwhelming majority of hospitality executives now hold a bullish view of the marketplace for 2011.

According to the DLA Piper 2011 Hospitality Outlook Survey, expectations for the continued recovery of the US economy and increased business travel have generated a renewed – and surprisingly robust – sense of optimism.

For the first time in three years, the overwhelming majority of respondents expect that hotel asset values will increase in the coming year, presenting the best buying opportunity since the recession. Seizing this opportunity, respondents believe that cash-heavy REITs and private equity investors will be the most active investors in 2011. Meanwhile, respondents are increasingly confident that their hotel debt will be refinanced or restructured in 2011.

On the operational side, guest input through the use of social media is playing an increasing role in hotel management as consumers more frequently rely on guest experiences, not brand loyalty, to make booking decisions.

HIGHLIGHTS OF DLA PIPER’S 2011 HOSPITALITY OUTLOOK SURVEY INCLUDE:

88 percent of respondents describe their 12-month outlook for the US hospitality industry as “bullish,” nearly tripling the bullish sentiment from 2010.

82 percent of respondents expect hotel asset values to rise during the next year, compared with only 20 percent of respondents in 2010.

9 out of 10 respondents believe that market conditions have created good buying opportunities for well-capitalized investors, led by opportunities in the upscale and luxury sectors.

Respondents expect REITs (51 percent) and private equity (40 percent) investors to dominate the US hospitality investment landscape in 2011.

37 percent of respondents expect that their hotel debt will be refinanced or restructured in 2011 – up from 31 percent in 2010.

69 percent of respondents report that TripAdvsior and other social media, including Twitter and Facebook, have changed the way they interact with guests.

Despite a heightened sense of bedbug paranoia among travelers across the country, the overwhelming majority of respondents (85 percent) report that fears over bedbugs did not negatively impact their operations in the past year.

The majority of respondents (65 percent) expect China to continue its dominance as the largest foreign investor in the US hospitality industry.

DLA Piper LLP (US) 2

VERBATIMS

Respondents were asked to share their thoughts on the following in an open forum for comment and feedback. The following represent select verbatims received from survey respondents.

Has the popularity of TripAdvisor and other social media websites (i.e., Twitter, Facebook, etc.) changed the way your organization interacts with guests? If so, please explain how.

We are monitoring and rewarding our management teams on achieving high performance on these sites. We know the consumer is using them to make travel purchase decisions.

More reliance on past guest experiences than on brand.

Making brands less important for travelers making booking decisions.

If you are not contacting your guests through these new direct sales portals, you are missing the boat.

Brands have less impact on relationship between guest and property.

Social media give us the chance to speak directly to our customers in an unvarnished and non-threatening environment. It is the booking engine of the future.

One more guest relations channel that must be monitored and managed. Social media is becoming full-time position at a hotel. Can’t afford not to monitor and respond to all comments.

Directing satisfied guests to TripAdvisor (or similar).

We spend a lot of time “managing” TripAdvisor.

It has raised awareness about service delivery, communication, and delivering on the promise made.

There is more accountability – whether to actual or perceived problems.

It can’t be ignored. Social media is replacing customer satisfaction surveys as the primary mechanism by which guests provide feedback, and it’s both instantaneous and shared with the world.

DLA Piper LLP (US) 3

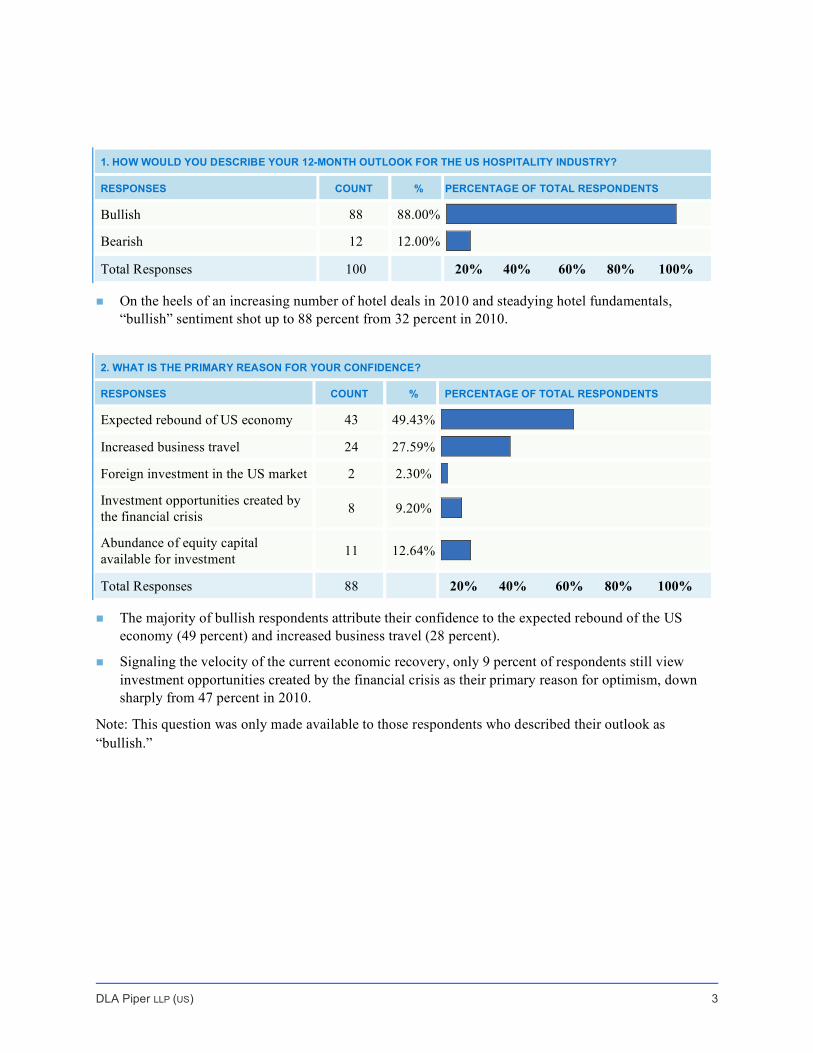

1. HOW WOULD YOU DESCRIBE YOUR 12-MONTH OUTLOOK FOR THE US HOSPITALITY INDUSTRY?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Bullish 88 88.00% Bearish 12 12.00% Total Responses 100 20% 40% 60% 80% 100%

On the heels of an increasing number of hotel deals in 2010 and steadying hotel fundamentals, “bullish” sentiment shot up to 88 percent from 32 percent in 2010.

2. WHAT IS THE PRIMARY REASON FOR YOUR CONFIDENCE?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Expected rebound of US economy 43 49.43% Increased business travel 24 27.59% Foreign investment in the US market 2 2.30% Investment opportunities created by the financial crisis

8 9.20%

Abundance of equity capital available for investment

11 12.64%

Total Responses 88 20% 40% 60% 80% 100%

The majority of bullish respondents attribute their confidence to the expected rebound of the US economy (49 percent) and increased business travel (28 percent).

Signaling the velocity of the current economic recovery, only 9 percent of respondents still view investment opportunities created by the financial crisis as their primary reason for optimism, down sharply from 47 percent in 2010.

Note: This question was only made available to those respondents who described their outlook as “bullish.”

DLA Piper LLP (US) 4

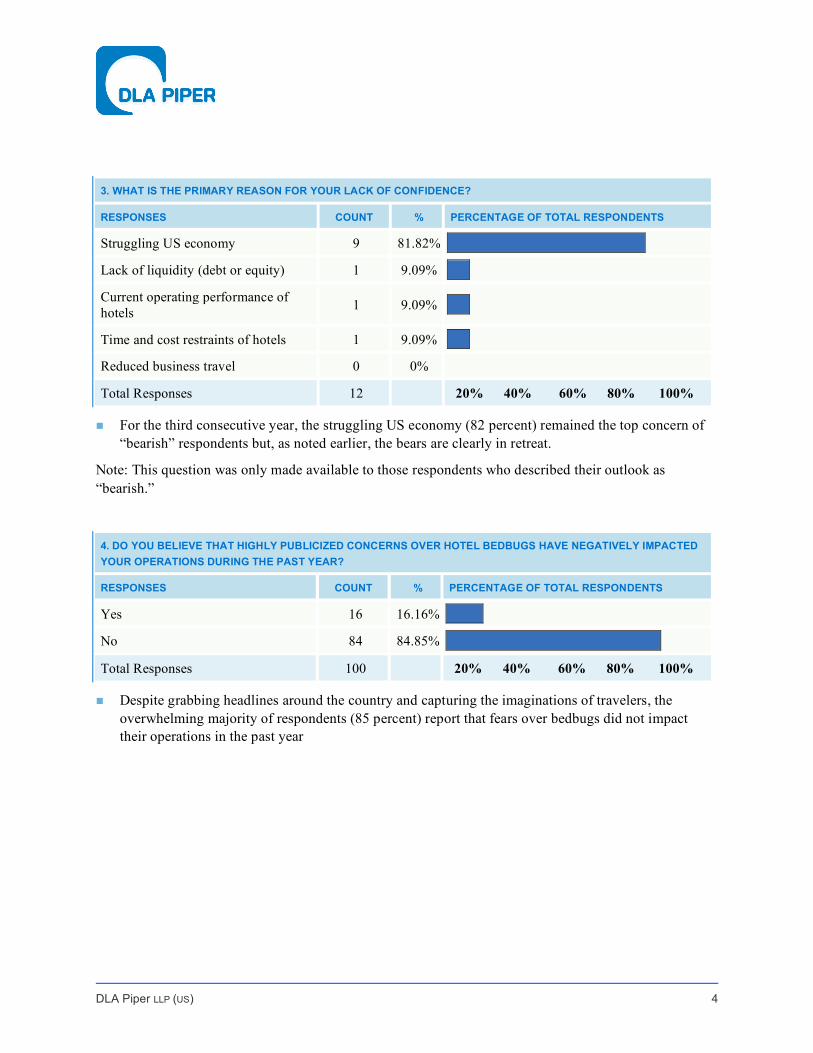

3. WHAT IS THE PRIMARY REASON FOR YOUR LACK OF CONFIDENCE?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Struggling US economy 9 81.82% Lack of liquidity (debt or equity) 1 9.09% Current operating performance of hotels

1 9.09%

Time and cost restraints of hotels 1 9.09% Reduced business travel 0 0%

Total Responses 12 20% 40% 60% 80% 100%

For the third consecutive year, the struggling US economy (82 percent) remained the top concern of “bearish” respondents but, as noted earlier, the bears are clearly in retreat.

Note: This question was only made available to those respondents who described their outlook as “bearish.”

4. DO YOU BELIEVE THAT HIGHLY PUBLICIZED CONCERNS OVER HOTEL BEDBUGS HAVE NEGATIVELY IMPACTED

YOUR OPERATIONS DURING THE PAST YEAR?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Yes 16 16.16% No 84 84.85% Total Responses 100 20% 40% 60% 80% 100%

Despite grabbing headlines around the country and capturing the imaginations of travelers, the overwhelming majority of respondents (85 percent) report that fears over bedbugs did not impact their operations in the past year

DLA Piper LLP (US) 5

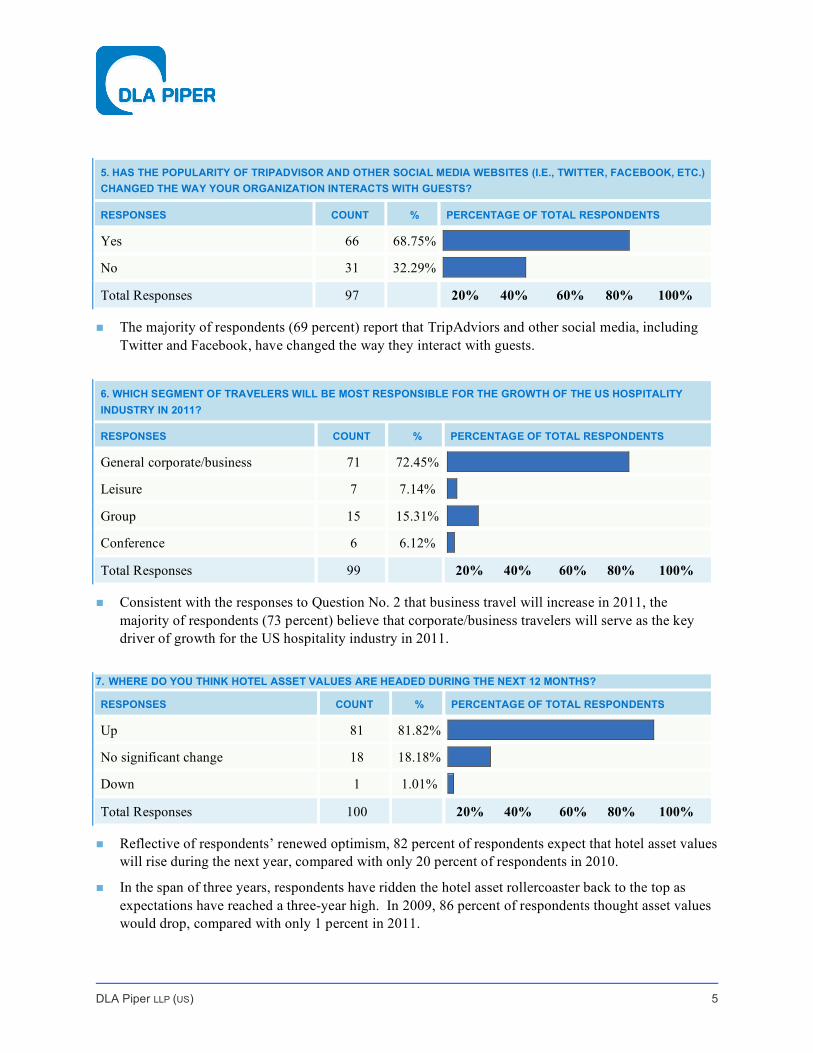

5. HAS THE POPULARITY OF TRIPADVISOR AND OTHER SOCIAL MEDIA WEBSITES (I.E., TWITTER, FACEBOOK, ETC.)

CHANGED THE WAY YOUR ORGANIZATION INTERACTS WITH GUESTS?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Yes 66 68.75% No 31 32.29% Total Responses 97 20% 40% 60% 80% 100%

The majority of respondents (69 percent) report that TripAdviors and other social media, including Twitter and Facebook, have changed the way they interact with guests.

6. WHICH SEGMENT OF TRAVELERS WILL BE MOST RESPONSIBLE FOR THE GROWTH OF THE US HOSPITALITY

INDUSTRY IN 2011?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

General corporate/business 71 72.45% Leisure 7 7.14% Group 15 15.31% Conference 6 6.12% Total Responses 99 20% 40% 60% 80% 100%

Consistent with the responses to Question No. 2 that business travel will increase in 2011, the majority of respondents (73 percent) believe that corporate/business travelers will serve as the key driver of growth for the US hospitality industry in 2011.

7. WHERE DO YOU THINK HOTEL ASSET VALUES ARE HEADED DURING THE NEXT 12 MONTHS?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Up 81 81.82% No significant change 18 18.18% Down 1 1.01% Total Responses 100 20% 40% 60% 80% 100%

Reflective of respondents’ renewed optimism, 82 percent of respondents expect that hotel asset values will rise during the next year, compared with only 20 percent of respondents in 2010.

In the span of three years, respondents have ridden the hotel asset rollercoaster back to the top as expectations have reached a three-year high. In 2009, 86 percent of respondents thought asset values would drop, compared with only 1 percent in 2011.

DLA Piper LLP (US) 6

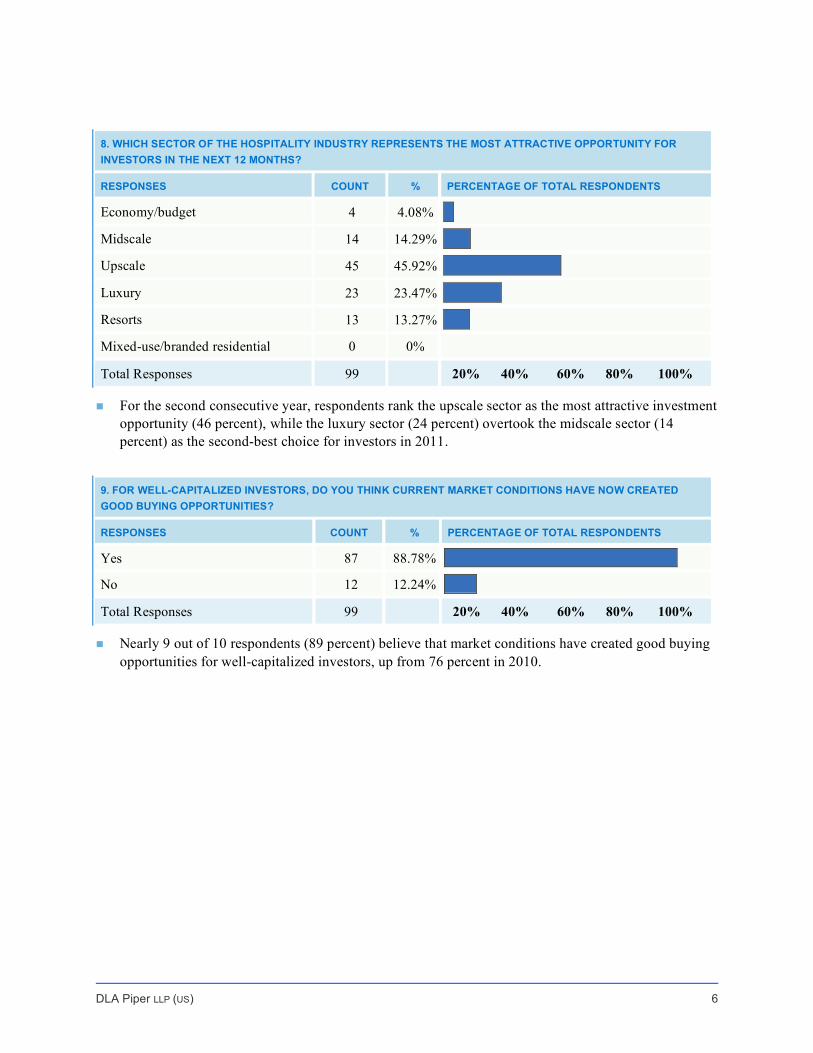

8. WHICH SECTOR OF THE HOSPITALITY INDUSTRY REPRESENTS THE MOST ATTRACTIVE OPPORTUNITY FOR

INVESTORS IN THE NEXT 12 MONTHS?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Economy/budget 4 4.08% Midscale 14 14.29% Upscale 45 45.92% Luxury 23 23.47% Resorts 13 13.27% Mixed-use/branded residential 0 0%

Total Responses 99 20% 40% 60% 80% 100%

For the second consecutive year, respondents rank the upscale sector as the most attractive investment opportunity (46 percent), while the luxury sector (24 percent) overtook the midscale sector (14 percent) as the second-best choice for investors in 2011.

9. FOR WELL-CAPITALIZED INVESTORS, DO YOU THINK CURRENT MARKET CONDITIONS HAVE NOW CREATED

GOOD BUYING OPPORTUNITIES?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Yes 87 88.78% No 12 12.24% Total Responses 99 20% 40% 60% 80% 100%

Nearly 9 out of 10 respondents (89 percent) believe that market conditions have created good buying opportunities for well-capitalized investors, up from 76 percent in 2010.

DLA Piper LLP (US) 7

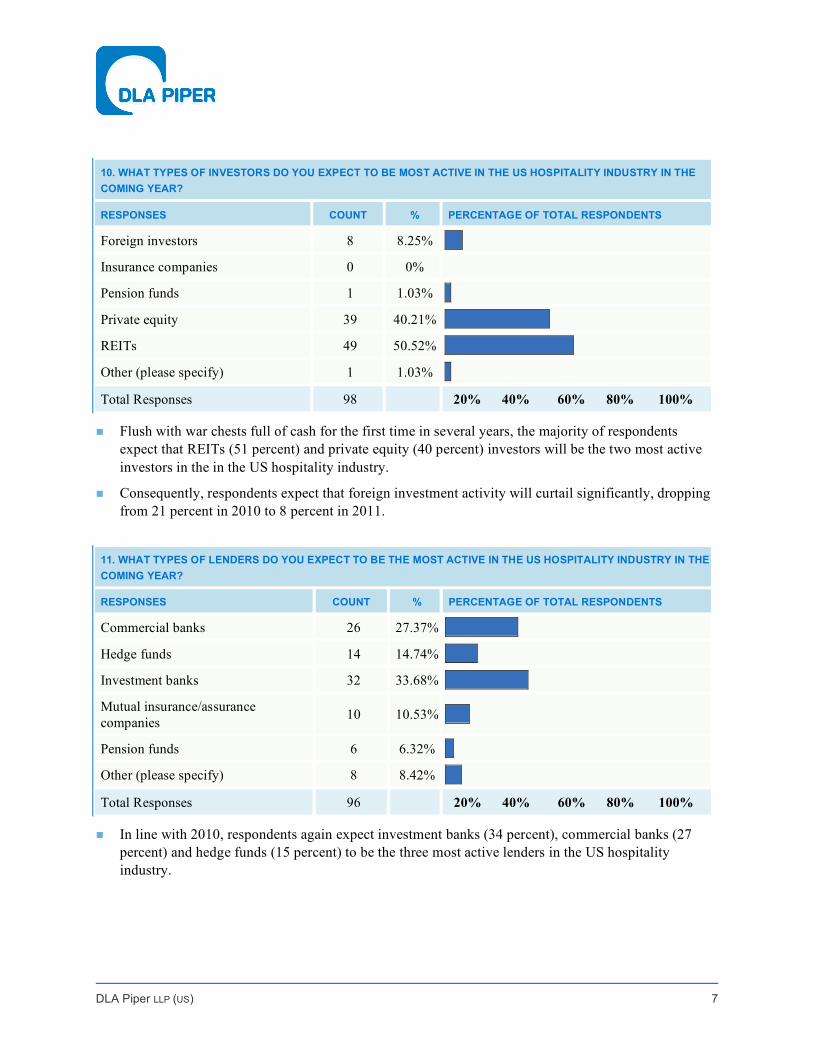

10. WHAT TYPES OF INVESTORS DO YOU EXPECT TO BE MOST ACTIVE IN THE US HOSPITALITY INDUSTRY IN THE

COMING YEAR?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Foreign investors 8 8.25% Insurance companies 0 0%

Pension funds 1 1.03% Private equity 39 40.21% REITs 49 50.52% Other (please specify) 1 1.03%

Total Responses 98 20% 40% 60% 80% 100%

Flush with war chests full of cash for the first time in several years, the majority of respondents expect that REITs (51 percent) and private equity (40 percent) investors will be the two most active investors in the in the US hospitality industry.

Consequently, respondents expect that foreign investment activity will curtail significantly, dropping from 21 percent in 2010 to 8 percent in 2011.

11. WHAT TYPES OF LENDERS DO YOU EXPECT TO BE THE MOST ACTIVE IN THE US HOSPITALITY INDUSTRY IN THE

COMING YEAR?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Commercial banks 26 27.37% Hedge funds 14 14.74% Investment banks 32 33.68% Mutual insurance/assurance companies

10 10.53%

Pension funds 6 6.32% Other (please specify) 8 8.42%

Total Responses 96 20% 40% 60% 80% 100%

In line with 2010, respondents again expect investment banks (34 percent), commercial banks (27 percent) and hedge funds (15 percent) to be the three most active lenders in the US hospitality industry.

DLA Piper LLP (US) 8

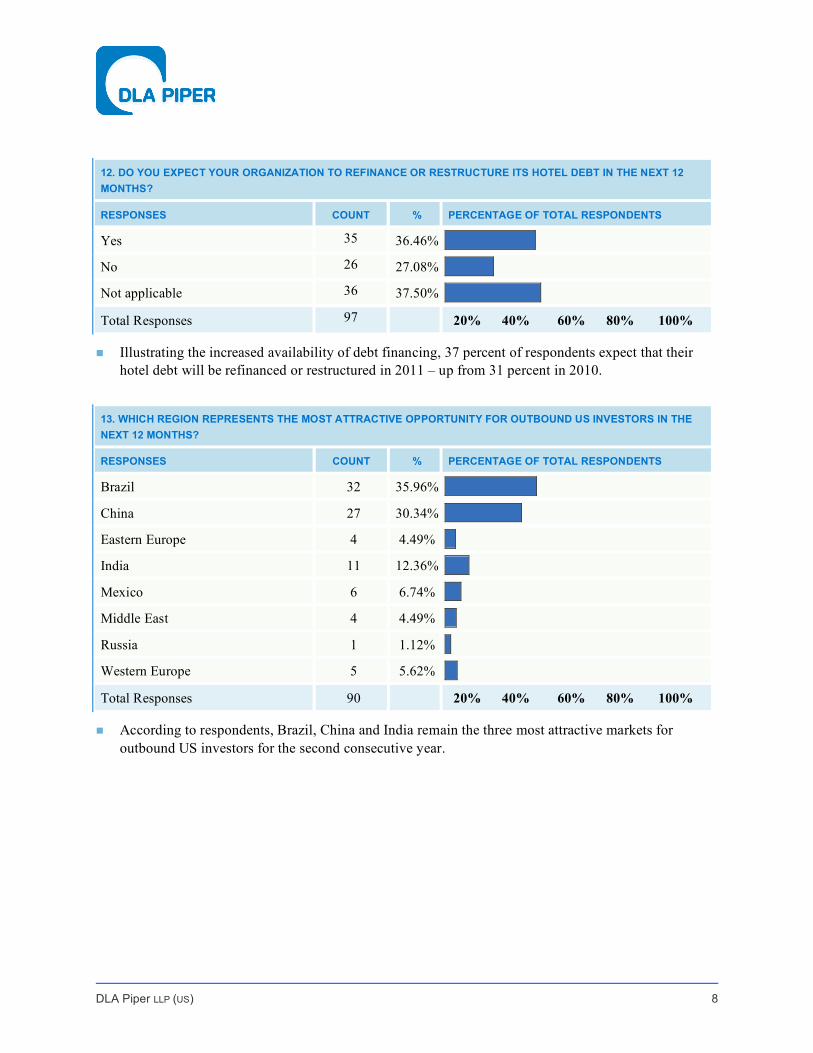

12. DO YOU EXPECT YOUR ORGANIZATION TO REFINANCE OR RESTRUCTURE ITS HOTEL DEBT IN THE NEXT 12

MONTHS?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Yes 35 36.46% No 26 27.08% Not applicable 36 37.50% Total Responses 97 20% 40% 60% 80% 100%

Illustrating the increased availability of debt financing, 37 percent of respondents expect that their hotel debt will be refinanced or restructured in 2011 – up from 31 percent in 2010.

13. WHICH REGION REPRESENTS THE MOST ATTRACTIVE OPPORTUNITY FOR OUTBOUND US INVESTORS IN THE

NEXT 12 MONTHS?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Brazil 32 35.96% China 27 30.34% Eastern Europe 4 4.49% India 11 12.36% Mexico 6 6.74% Middle East 4 4.49% Russia 1 1.12% Western Europe 5 5.62% Total Responses 90 20% 40% 60% 80% 100%

According to respondents, Brazil, China and India remain the three most attractive markets for outbound US investors for the second consecutive year.

DLA Piper LLP (US) 9

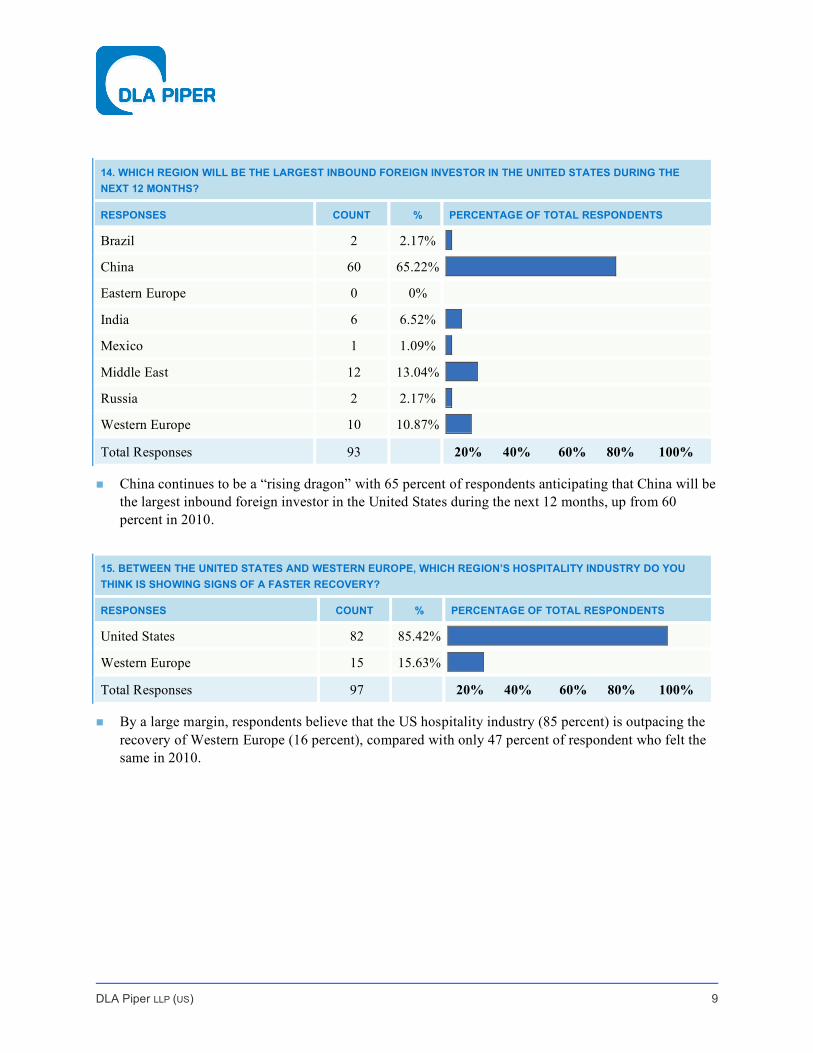

14. WHICH REGION WILL BE THE LARGEST INBOUND FOREIGN INVESTOR IN THE UNITED STATES DURING THE

NEXT 12 MONTHS?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

Brazil 2 2.17% China 60 65.22% Eastern Europe 0 0%

India 6 6.52% Mexico 1 1.09% Middle East 12 13.04% Russia 2 2.17% Western Europe 10 10.87% Total Responses 93 20% 40% 60% 80% 100%

China continues to be a “rising dragon” with 65 percent of respondents anticipating that China will be the largest inbound foreign investor in the United States during the next 12 months, up from 60 percent in 2010.

15. BETWEEN THE UNITED STATES AND WESTERN EUROPE, WHICH REGION’S HOSPITALITY INDUSTRY DO YOU

THINK IS SHOWING SIGNS OF A FASTER RECOVERY?

RESPONSES COUNT % PERCENTAGE OF TOTAL RESPONDENTS

United States 82 85.42% Western Europe 15 15.63% Total Responses 97 20% 40% 60% 80% 100%

By a large margin, respondents believe that the US hospitality industry (85 percent) is outpacing the recovery of Western Europe (16 percent), compared with only 47 percent of respondent who felt the same in 2010.

DLA Piper LLP (US) 10

METHODOLOGY

In January of 2011, DLA Piper distributed a survey via email to top executives within the hospitality industry, including CEOs, COOs, CFOs and other senior executives, which was completed by 101 respondents.

Question No. 2 was only made available to those respondents who described themselves as “bullish” in Question No. 1.

Question No. 3 was only made available to those respondents who described themselves as “bearish” in Question No. 1.

Due to rounding, all percentages used in all questions may not add up to 100 percent.

DLA Piper LLP (US) 11

CONTACTS

For a copy of the complete results for DLA Piper’s 2010 Hospitality Outlook Survey, please visit www.dlapiper.com and search “Hospitality and Leisure” or contact one of the following:

Sandra Kellman Global Co-chair and Head of Hospitality & Leisure Group US, DLA Piper T +1 312 368 4082 Brian Kiefer Media Relations, Greentarget T +1 312 252 4113