dmm 2017 q4 report highlights - california iso 2017 q4 report highlights gabe murtaugh ... in the...

TRANSCRIPT

DMM 2017 Q4 Report Highlights

Gabe MurtaughSenior AnalystDepartment of Market Monitoring

Conference CallFebruary 21, 2018

• Real-time market performance– Higher prices in the 15-minute market– Large congestion revenue rights losses

• EIM market performance• Special issues and recommendations

– Wind and solar downward dispatch– Use of Aliso Canyon measures– Capacity procurement

Page 2

Outline

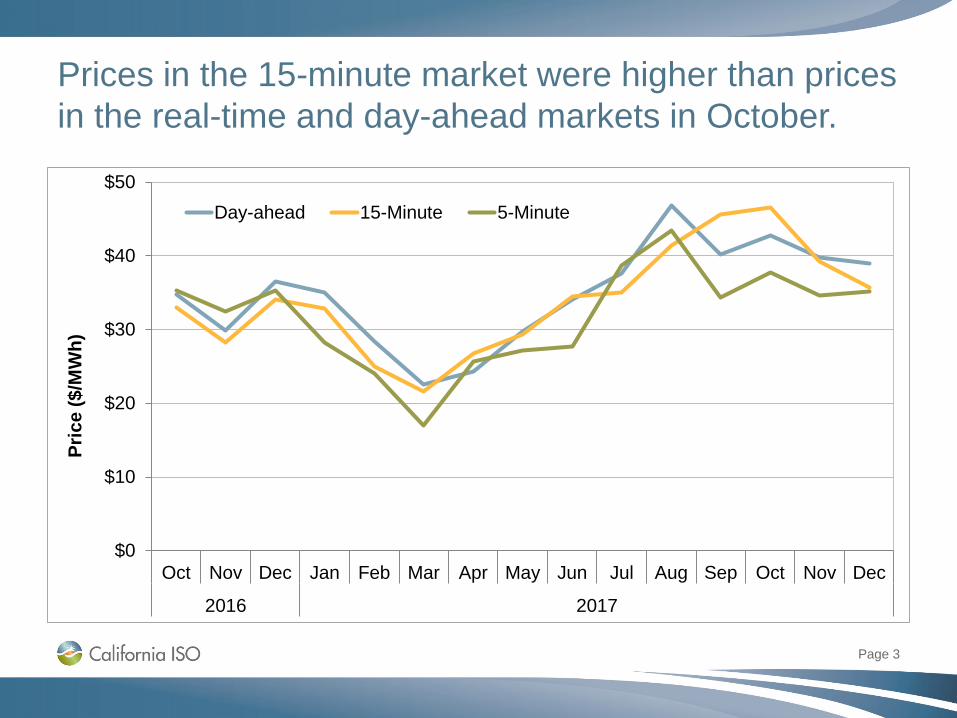

Prices in the 15-minute market were higher than prices in the real-time and day-ahead markets in October.

Page 3

$0

$10

$20

$30

$40

$50

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017

Pric

e ($

/MW

h)

Day-ahead 15-Minute 5-Minute

ISO prices continue to follow the net-load pattern. Net loads were lowest during the middle of the day.

Page 4

0

5,000

10,000

15,000

20,000

25,000

30,000

$0

$20

$40

$60

$80

$100

$120

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Aver

age

net s

yste

m lo

ad (M

W)

Pric

e ($

/MW

h)

Day-ahead 15-minute 5-minute Average net load

The power balance constraint was triggered more frequently in the 15-minute market this quarter.

Page 5

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%Ja

nFe

bM

ar Apr

May Jun

Jul

Aug

Sep Oct

Nov

Dec Jan

Feb

Mar Apr

May Jun

Jul

Aug

Sep Oct

Nov

Dec

2016 2017

Perc

ent o

f 15-

min

ute

inte

rval

s

Valid under-supply infeasibility (shortage)

Load bias limiter resolved infeasibility

Corrected or invalid infeasibility

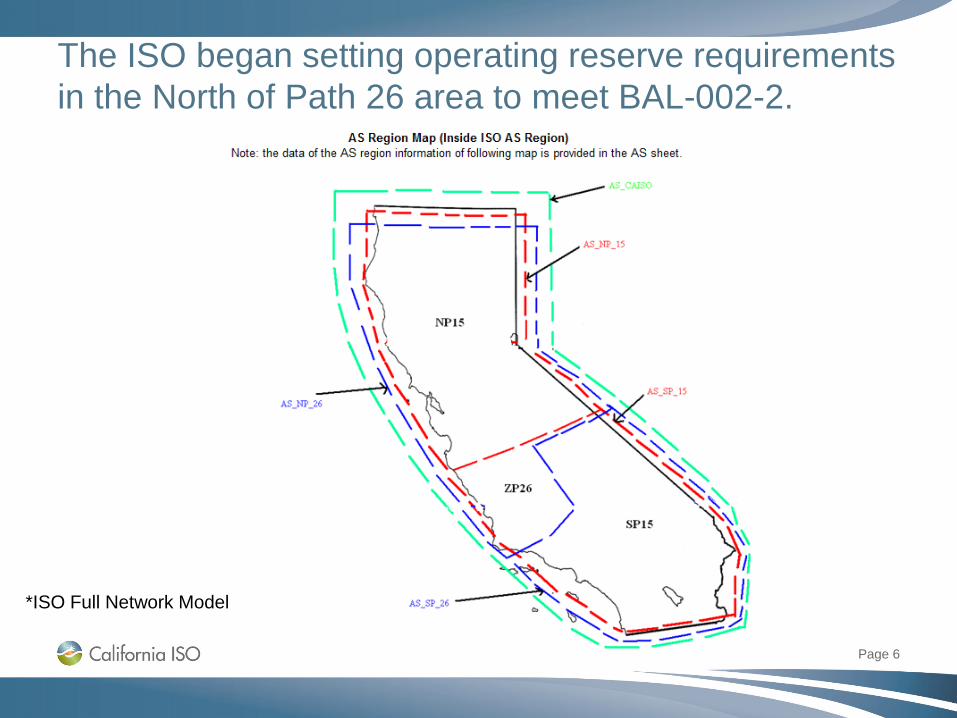

The ISO began setting operating reserve requirements in the North of Path 26 area to meet BAL-002-2.

*ISO Full Network Model

Page 6

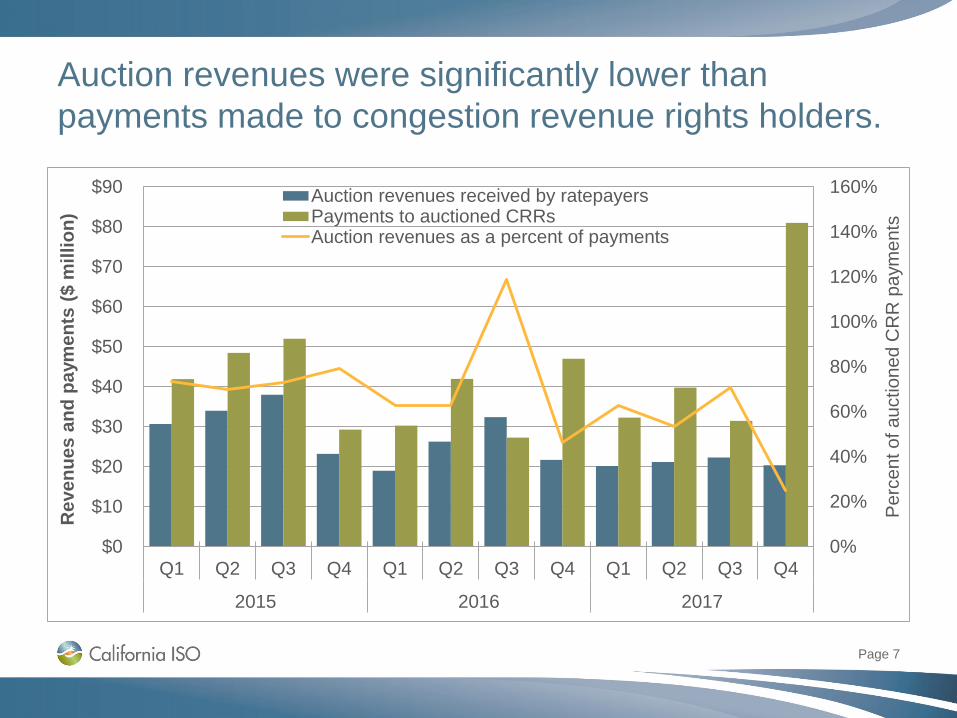

Auction revenues were significantly lower than payments made to congestion revenue rights holders.

Page 7

0%

20%

40%

60%

80%

100%

120%

140%

160%

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2015 2016 2017

Per

cent

of a

uctio

ned

CR

R p

aym

ents

Rev

enue

s an

d pa

ymen

ts ($

mill

ion)

Auction revenues received by ratepayersPayments to auctioned CRRsAuction revenues as a percent of payments

Payments for the flexible ramping capacity product were low in the fourth quarter.

Page 8

$0.00

$0.04

$0.08

$0.12

$0.16

$0.20

$0.24

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017

Paym

ents

per

MW

h lo

ad ($

/MW

h)

Tota

l pay

men

ts ($

mill

ion)

California ISO PacifiCorp EastPacifiCorp West NV EnergyPuget Sound Energy Arizona Public ServicePortland General Electric Payments per MWh of load

The ISO discussed issues with the flexible ramping capacity with the Market Planning and Performance meeting on Feb 20:http://wwwpub.oa.caiso.com:21083/Documents/AgendaandPresentation-MarketPerfomanceandPlanningForum-Feb202018.pdf

Prices in all energy imbalance markets continue to mirror patterns in the ISO.

Page 9

$0

$20

$40

$60

$80

$100

$120

$140

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Aver

age

hour

ly p

rice

($/M

Wh)

PacifiCorp West, Puget Sound Energy, and Portland General ElectricPacifiCorp EastNV Energy and Arizona Public ServiceSouthern California Edison

Energy imbalance market participants are failing the sufficiency test less often than last year.

Page 10

0%

10%

20%

30%

40%

50%

60%

Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017

Perc

ent o

f hou

rs

California ISO PacifiCorp East PacifiCorp WestNV Energy Puget Sound Energy Arizona Public ServicePortland General Electric

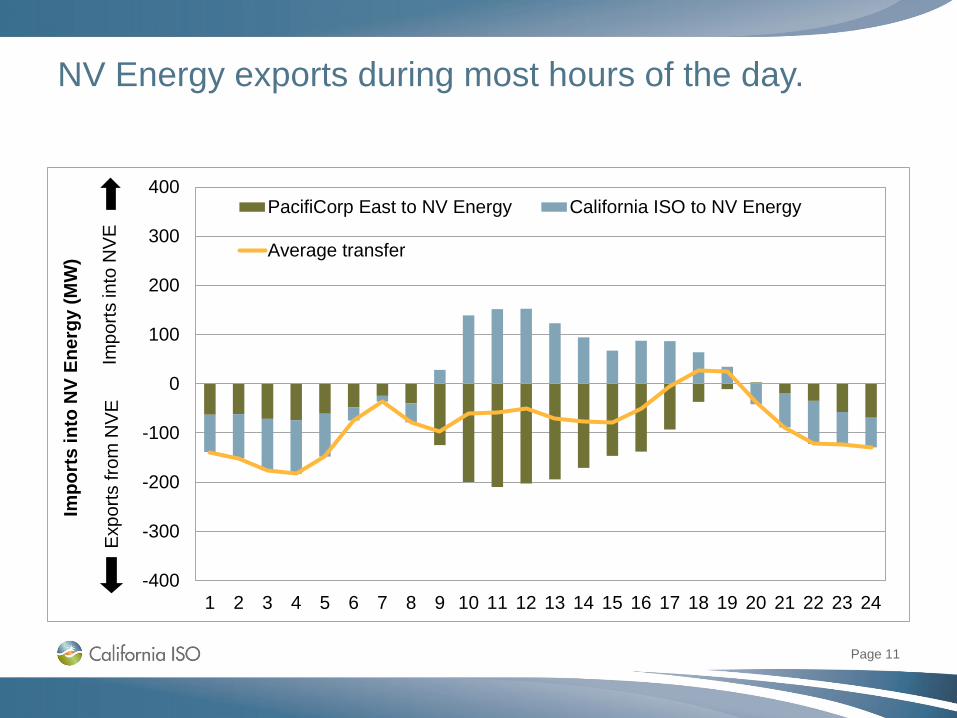

NV Energy exports during most hours of the day.

Page 11

-400

-300

-200

-100

0

100

200

300

400

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Impo

rts

into

NV

Ener

gy (M

W)

PacifiCorp East to NV Energy California ISO to NV Energy

Average transfer

Impo

rts in

to N

VE

Exp

orts

from

NV

E

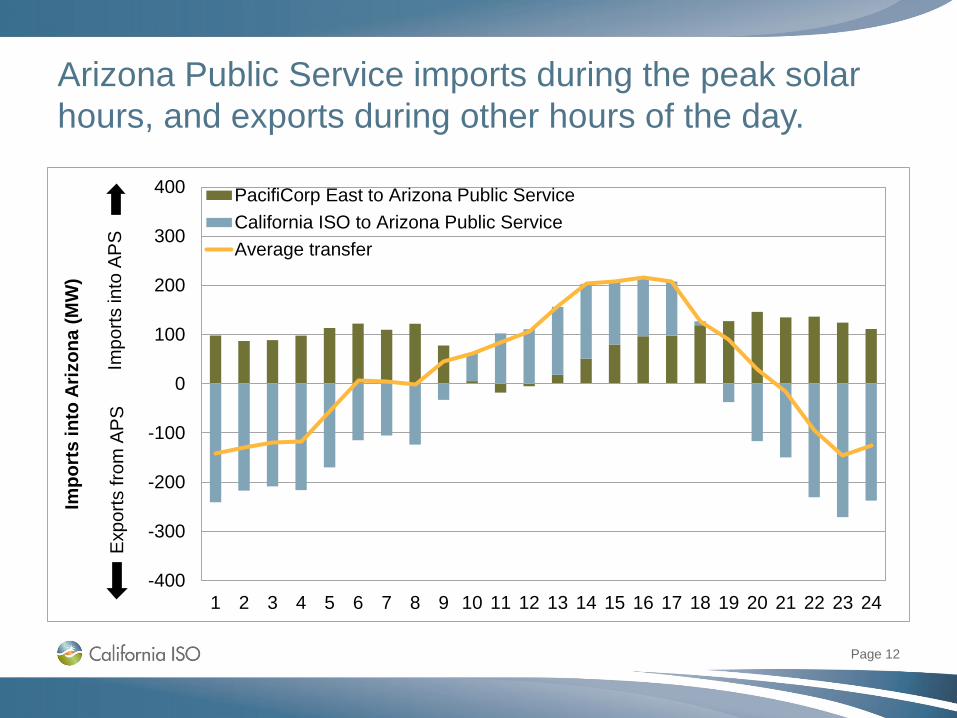

Arizona Public Service imports during the peak solar hours, and exports during other hours of the day.

Page 12

-400

-300

-200

-100

0

100

200

300

400

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Impo

rts

into

Ariz

ona

(MW

)

PacifiCorp East to Arizona Public ServiceCalifornia ISO to Arizona Public ServiceAverage transfer

Impo

rts in

to A

PS

Exp

orts

from

AP

S

PacifiCorp West exports during most hours of the day.

Page 13

-250

-200

-150

-100

-50

0

50

100

150

200

250

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Impo

rts

into

Pac

ifiC

orp

Wes

t (M

W)

ISO to PacifiCorp WestPacifiCorp East to PacifiCorp WestPuget Sound Energy to PacifiCorp WestPortland to PacfiCorp WestAverage transfer

Impo

rts in

to P

AC

WE

xpor

ts fr

om P

AC

W

Renewable downward dispatch increased from 2016, while curtailments continued to be very small.

Page 14

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

20

40

60

80

100

120

140

160

Jan

Feb

Mar Apr

May Jun

Jul

Aug

Sep Oct

Nov

Dec Jan

Feb

Mar Apr

May Jun

Jul

Aug

Sep Oct

Nov

Dec

Perc

ent r

educ

tion

Meg

atw

att h

our (

thou

sand

s)

Economic downward dispatch (ISO)Self-scheduled curtailment (ISO)Economic downward dispatch (EIM)Wind and solar percent reduction (ISO)

2016 2017

Aliso adders were in place for a large number of days during the quarter.

Page 15

Many of the resources eligible for the Aliso adders did not include them in bids.

Page 16

0%

20%

40%

60%

80%

100%

23-O

ct24

-Oct

25-O

ct7-

Dec

8-D

ec9-

Dec

10-D

ec11

-Dec

12-D

ec13

-Dec

14-D

ec15

-Dec

16-D

ec17

-Dec

18-D

ec19

-Dec

20-D

ec21

-Dec

22-D

ec23

-Dec

24-D

ec25

-Dec

26-D

ec27

-Dec

28-D

ec29

-Dec

30-D

ec31

-Dec

Perc

ent S

oCal

Gas

min

imum

load

ca

paci

ty

Bid does not use scalar Bid uses scalar, not near capBid uses scalar, at or near cap

Page 17

$0.0

$0.5

$1.0

$1.5

$2.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2017

Bid

cos

t rec

over

y pa

ymen

ts ($

mill

ion) Excess bid cost recovery

payments due to Aliso scalars

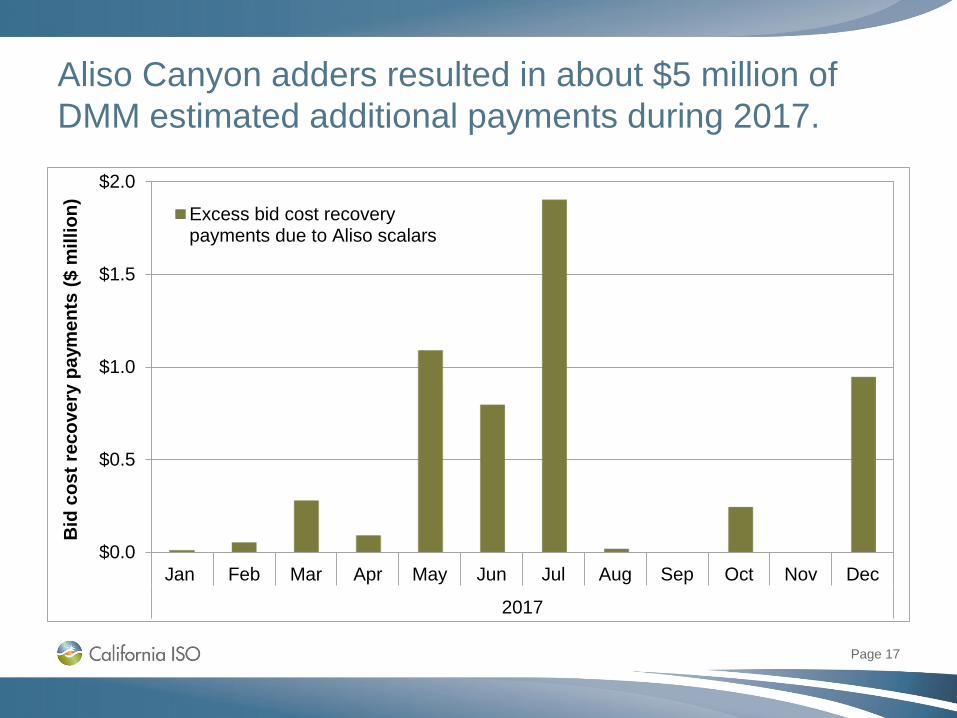

Aliso Canyon adders resulted in about $5 million of DMM estimated additional payments during 2017.

Page 18

40% 80% 120% 160% 200% 240% 280% 320% 360% 400%0%

5%

10%

15%

20%

25%

Perc

ent o

f tra

ded

volu

me

Trade price as percent of next-day index price from prior day

110% 125%

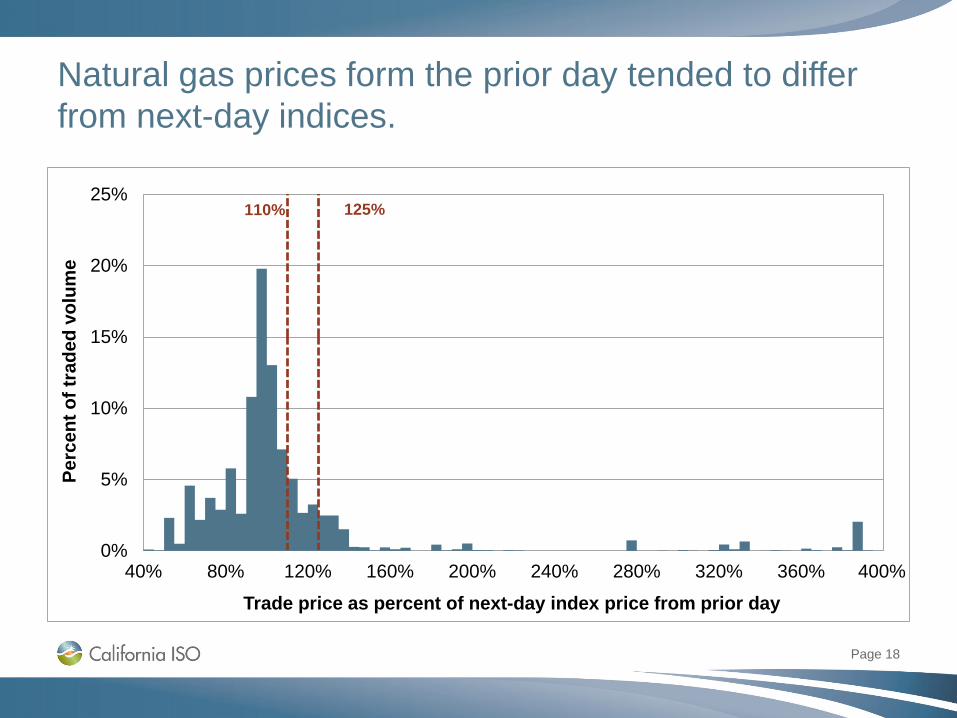

Natural gas prices form the prior day tended to differ from next-day indices.

Page 19

40% 60% 80% 100% 120% 140% 160%0%

10%

20%

30%

40%

50%

Perc

ent o

f tra

ded

volu

me

Trade price as percent of average at 8:30 a.m.

110% 125%

Average natural gas prices at 8:30 tended to reflect next-day indices.

• Metcalf received a designation for reliability must-run.

Page 20

Resource

CPM designation

(MW)

CPM deisgnation

datesPrice

($/kW-mon)Estimated cost

($ million)Local capacity

area Exceptional dispatch CPM triggerMANDALAY GEN STA. UNIT 3 119.4 10/24-11/22 $6.31 $0.73 System Higher loads in real-timeMANDALAY GEN STA. UNIT 2 215 12/05-2/02 $6.31 $2.67 SCE Local availabil ity for wildfireMANDALAY GEN STA. UNIT 1 215 12/05-2/02 $6.31 $2.67 SCE Local availabil ity for wildfireMANDALAY GEN STA. UNIT 3 130 12/05-2/02 $6.31 $1.61 SCE Local availabil ity for wildfire

Resource

CPM designation

(MW)Price

($/kW-mon)Estimated cost

($ million)Local capacity

area Exceptional dispatch CPM triggerMOSS LANDING POWER BLOCK 1 510 $6.19 $38.4 PG&E Material sub-area deficiencyENCINA UNIT 4 272 $6.31 $20.9 SDG&E Material sub-area deficiencyENCINA UNIT 5 273 $6.31 $21.0 SDG&E Material sub-area deficiency

Several procurements were made for capacity in the fourth quarter and for 2018.