do chair independence and succession planning … annual meetings...do chair independence and...

TRANSCRIPT

Do Chair Independence and SuccessionPlanning Influence CEO Turnover?

Christian von Drathen�

First Draft: September, 2013

This Draft: November, 2014

Abstract

There is widespread concern that corporate boards do not suffi-

ciently punish chief executive officers (CEOs) for poor performance.

Board effectiveness in ousting CEOs may be affected by chief execu-

tives who also chair the board or influence the succession planning

process. This article explores how chair independence and succes-

sion planning influence CEO turnover. I address endogeneity is-

sues using a trinomial probit regression system of CEO turnover that

models chair independence and succession planning endogenously.

I find that succession planning has a larger positive effect on CEO

turnover than suggested by previous research. I also find that chair

independence actually reduces the probability of succession plan-

ning because it creates a friction with the common relay succession

model. There is a negative overall effect of chair independence on

CEO turnover.�Jindal School of Management, The University of Texas at Dallas (UTD), 800 West

Campbell Road, Richardson, TX 75080, USA. Email: [email protected]. I thankUlf Axelson, Vicente Cuñat, Vassilis Hajivassiliou, Daniel Paravisini, Christopher Polk,Joel Shapiro and seminar participants at LSE for helpful comments and discussions. Allerrors are my own.

1

1 Introduction

There is widespread concern that corporate boards do not sufficiently pun-ish chief executive officers (CEOs) for poor performance. This may becaused by CEO entrenchment where boards retain chief executives whoshareholders would rather see fired. Board effectiveness in ousting CEOsmay be affected by chief executives who also chair the board (CEO duality)or influence the succession planning process. Empirical research showsthat CEO turnover is less sensitive to poor stock returns when firms havedual CEO-chairs (Dahya et al. (2002), Goyal and Park (2002)), and that thelikelihood of turnover decreases when firms have no succession plan andno heir apparent is available (Naveen (2006)). Accordingly, corporate gov-ernance rules were established to encourage boards to separate the chiefexecutive role from the chairperson1 and to introduce succession planningprocedures2. However, an important issue with these studies is that theygenerally rely on variation in corporate decision variables, which is un-likely to be random. In particular, endogeneity in chair independence andsuccession planning cannot be ruled out and standard regression resultsmay be biased.

In this article, I explore how chair independence and succession plan-ning affect CEO turnover by improving corporate governance and reduc-ing entrenchment. I address concerns regarding simultaneity and omit-ted variables in chair independence and succession planning by using a

1On December 16, 2009, the SEC announced a rule (SEC Release No. 33-9089; 34-61175; http://www.sec.gov/rules/final/2009/33-9089.pdf) that requires listed compa-nies to disclose the board leadership structure, including whether the firm has combinedthe CEO and chairperson position, and explain why such a leadership structure is appro-priate.

2On October 27, 2009, the SEC eliminated the ordinary business exclusion de-fense (SEC Release No. 33-9089; 34-61175; http://www.sec.gov/rules/final/2009/33-9089.pdf) employed by firms unable or unwilling to disclose their CEO succession plan-ning process to shareholders. In changing its prior view, the SEC recognized that inade-quate CEO succession planning represents an important business risk and flags a firm’sgovernance policy issue that goes beyond daily management of the firm. Successionplanning is considered "a key board function and a significant policy (and governance)issue . . . so that a company is not adversely affected by a vacancy in leadership."

2

trivariate probit system to estimate the effect on CEO turnover. Firms ex-ecute their succession plans by appointing an heir apparent to the boardof directors, usually a separate President, Chief Operating Officer, or ViceChair. I find that such succession planning increases the probability ofCEO turnover by at least 20%. When there are no succession candidatessome chief executives are retained even though shareholders may prefer tohave them replaced. Succession planning therefore seems to reduce CEOentrenchment by eliminating a friction to turnover.

The trivariate probit system permits a chair independence effect onsuccession planning and I find a significantly negative correlation. Thismay be caused by the common relay succession model, where CEO duality(no independence) coincides with an heir apparent (succession planning).The overall effect of chair independence is therefore negative and reducesthe likelihood of CEO turnover by 4%. This unexpected result may arisebecause the positive effect of improved monitoring by independent chairsis exceeded by the frictions arising from fewer relay successions. Chair in-dependence does not seem to reduce CEO entrenchment enough to com-pensate for the reduction in heirs apparent by barring relay successions.

I address concerns regarding unobserved managerial ability by select-ing samples of natural retirements and forced turnover. CEO ability can-not be directly observed, but corporate boards learn it over time untilit becomes a known quantity (Taylor (2010)). CEOs who survive boardscrutiny until retirement age are therefore likely to have high average abil-ity while CEOs who are forced to leave earlier most likely have low aver-age ability (Fee et al. (2010)). I find that coefficient estimates are consistentacross these samples and conclude that a bias caused by unobserved CEOability is unlikely.

This article supports corporate governance rule changes that enhancesuccession planning but provides no evidence for policies that promotechair independence.

The literature on CEO turnover is well established and rooted in corpo-rate governance theory. According to Jensen and Meckling (1976), Fama(1980), and Jensen and Ruback (1983), agency theory predicts that the

3

separation of corporate ownership from control encourages managers tomaximize private benefits and decrease shareholder value. Such manage-rial behavior is typically blamed on the unwillingness or inability of cor-porate boards to effectively exercise their role as shareholder representa-tives. Fama and Jensen (1983) show that ineffective corporate governanceemerges from boards dominated by firm managers. Weisbach (1988) ob-serves that manager-dominated boards are less likely to dismiss CEOs forpoor firm performance. Chair independence has come under particularscrutiny. Agency theory suggests that chair and CEO roles be separated inorder to increase board independence and enable better oversight. Con-sistent with agency theory, Goyal and Park (2002) and Dahya et al. (2002)show that chair independence increases the likelihood of turnover withrespect to firm performance.

Parrino (1997) suggests that firms evaluate trade-offs in turnover andsuccession decisions. The potential benefit of replacing a chief executivewith a successor increases with the expected improvement in match qual-ity between firm requirements and executive characteristics, but decreaseswith uncertainty in measuring these characteristics and fixed costs of CEOturnover. Taylor (2010) shows that corporate boards learn unobservableCEO ability over time until it becomes a know quantity. Vancil (1987) fo-cuses on CEO succession planning and finds that relay successions area common pattern. The firm selects an heir apparent several years be-fore the CEO’s anticipated retirement date, the heir apparent and outgo-ing chief executive work together until the CEO leaves, and the retiringCEO remains chairperson for a few years before also transferring chair-manship to the successor. Dual CEO-chairs are therefore a normal stageduring the common relay succession cycle. Naveen (2006) revisits succes-sion planning and finds that many U.S. firms use a relay process for insidesuccessions. The departing CEO’s age also plays an important role in topexecutive changes. Murphy (1999) documents that most CEO turnoverrelates to natural retirements.

This article is organized as follows. Section 2 develops testable hy-potheses. Section 3 discusses the empirical strategy. The sample and de-

4

scriptive statistics are presented in Section 4. Section 5 shows the mainresults, and Section 6 concludes.

2 Hypotheses

Corporate governance theory suggests that chair independence reducesCEO entrenchment and therefore has a positive effect on CEO turnover.Empirical research shows that succession planning also has a positive ef-fect on CEO turnover. However, chair independence is related to succes-sion planning and therefore has an indirect effect on CEO turnover as well:relay successions require both an heir apparent and a dual CEO-chair, whoremains as dependent chair after the turnover event. Since chair indepen-dence rules out the relay succession model, there may also be fewer heirsapparent and less CEO turnover. Any positive direct effect of chair in-dependence on CEO turnover could therefore be countered by a negativeindirect effect from less effective succession planning.

I motivate the test hypotheses for the effect of chair independence andCEO succession planning on turnover as well as their interaction. Thereare three hypotheses for testing how chair independence and successionplanning, both directly and indirectly, affect CEO turnover.

Direct Effects (DE)

Chair independence decreases entrenchment. The dual role of a CEO-chair creates conflicts of interest. Such conflict may arise because incen-tives to remain CEO are strong and can lead to entrenchment. As chair-person of the board, CEO-chairs may be able to influence the board intheir own turnover decisions as well as influence the board’s successionplanning process. Chief executives usually have superior information re-garding candidate ability. CEO entrenchment strategies to delay turnoverand succession may include, for example, downplaying candidate abilityor ousting an heir apparent. Separating the chairperson from the chiefexecutive role eliminates these conflicts of interest.

5

DE1: Chair independence makes CEO turnover more likely.

Succession planning facilitates inside successions. Firms engage insuccession planning in order to facilitate managerial successions. An heirapparent is typically a firm insider and designated successor to a retiringchief executive. The absence of an heir apparent leaves only other less suit-able inside or unknown outside successors, which might be more costlyand risky. Succession planning that produces an heir apparent shouldtherefore increase the probability of turnover.

DE2: Succession planning makes CEO turnover more likely.

Indirect Effects (IE)

Relay successions require CEO duality. Relay successions are char-acterized by chief executives taking the chairperson role and by boardsselecting an heir apparent prior to the management transition. The pro-motion of chief executives to dual CEO-chairs typically takes place beforethe appointment of the heir apparent. CEO duality usually precedes heirapparent in the relay succession cycle. Since chair independence rules outthe relay succession model there may also be fewer heirs apparent.

IE: Chair independence makes succession planning less likely.These three hypotheses provide tests for both the overall effect of chair

independence on CEO turnover (DE1) and the indirect effect through thesuccession planning channel (IE and DE2). These tests can be used todisentangle the direct and indirect effect of chair independence on CEOturnover and show which dominates.

3 Empirical Strategy

Measuring the effect of chair independence and succession planning onCEO turnover is a challenge. The firm’s decisions on chair independence,succession planning, and CEO turnover are made simultaneously. For

6

example, if a firm decides to use the common relay succession model(Vancil (1987)) then its succession planning, chair independence, and CEOturnover are affected at the same time: an heir apparent is selected, theincumbent becomes dual CEO-chair, and a target date is set to pass on theCEO title to the successor. Simultaneity can therefore lead to endogeneityand inconsistent estimates.

Unobserved variables may also create endogeneity problems. For ex-ample, CEO ability is difficult to observe but influences chair indepen-dence and succession planning: a low ability chief executive is more likelyto face an independent chair and be replaced by an outside successor. Un-observed ability can therefore generate further inconsistency.

The empirical approach must therefore address endogeneity from bothsimultaneous and unobserved variables. This problem lends itself to si-multaneous systems estimation. My empirical strategy is therefore to esti-mate a recursive and fully observed system of seemingly unrelated regres-sion (SUR) equations.

Following this general approach, Naveen (2006) uses a bivariate probitregression to estimate the effect of one endogenous variable, successionplanning, on CEO turnover. However, the relay succession model is alsocharacterized by CEO duality, which is not part of her analysis. Therefore,I introduce a second endogenous variable, chair independence, in order tobetter incorporate the effect of relay successions.

The resulting recursive trivariate binary choice model can be specifiedas a system of SUR equations:

ChairIndt = 1[δ1Z1t + δ2Z2t + Xtγ1 + ε1t > 0] (1)

HeirAppt = 1[α2ChairIndt + δ2Z2t + Xtγ2 + ε2t > 0] (2)

Turnovert = 1[α3ChairIndt + β3HeirAppt + Xtγ3 + ε3t > 0] (3)

ε = (ε1, ε2, ε3)0 s N (0, Σ) (4)

Σ =

264 1 . .ρ12 1 .ρ13 ρ23 1

375 , (5)

7

where 1[�] is the indicator function, X is a matrix of controls, ρij reflects thecorrelation between the error terms εi and εj, and the dots refer to symmet-rical elements in the lower matrix part.

Stage one (Eq. 1) defines the endogenous binary choice variable chairindependence. If the chair of the board during year t is neither the currentnor a former CEO of the firm, then the chairperson is independent andChairIndt is set to 1. Z1 and Z2 are instruments.

Stage two (Eq. 2) defines the endogenous binary choice variable heirapparent. If the board of directors during year t includes a President, ChiefOperating Officer (COO), or Vice Chair who is not the current CEO, thenthe firm has a succession plan and HeirAppt is set to 1. Z2 is an instrument.

Stage three (Eq. 3) defines the endogenous binary choice variable CEOturnover. If the CEO changes during year t, then the firm experiences aCEO turnover event and Turnovert is set to 1.

The SUR system is recursive because in each stage the endogenousvariables of previous stages appear on the RHS: chair independence is anexplanatory variable for heir apparent, while both chair independence andheir apparent are explanatory variables for CEO turnover. The SUR sys-tem is also fully observed: the endogenous variables on the RHS (Eq. 2and Eq. 3) are actual observations and not estimates. This system permitscorrelation between the error terms in each stage (Eq. 5).

The SUR system can be estimated consistently using limited informa-tion maximum likelihood (LIML). Consistency requires identically but notindependently distributed errors in each stage, and homoskedasticity inthe final stage. Wilde (2000) shows that recursive multi-equation limiteddependent variable models do not require exclusion restrictions for pa-rameter identification3. Therefore all stages, except the final one, do notneed to be fully specified and can omit influential variables.

Wooldridge (2010)4 cautions against relying solely on nonlinearity inmultivariate probit models for parameter identification, and suggests to

3Wilde (2000) proves that a single varying exogenous regressor per equation is suffi-cient to eliminate problems with small variation identification in multi-equation probitmodels using endogenous indicator variables.

4p. 599

8

use exclusion restrictions. It is therefore conservative to use two instru-ments with three exclusion restrictions for the SUR system:

1. Post-SOX indicator. The Sarbanes-Oxley (SOX) act, enacted in July2002, enhances the oversight role of public company boards. It strength-ens non-executive director independence, particularly for audit com-mittees. SOX also increases chair independence and can be consid-ered an exogenous shock. However, the legislative scope does notcover succession planning and CEO turnover. The post-SOX indi-cator is therefore an instrument for chair independence and can beexcluded from the succession planning and CEO turnover equations.Any SOX effect on succession planning and CEO turnover is thus at-tributed to the chair independence channel.

2. Conditional candidate age indicator. Executives promoted to the ex-ecutive board are succession candidates well before their official se-lection as heir apparent (Naveen (2006)). Candidates for heir appar-ent are also usually younger than the incumbent CEO. Low candi-date age increases the likelihood of succession planning (heir appar-ent) and can be considered exogenous, after controlling for candidateavailability. However, it is not plausible that conditional candidateage has a direct effect on CEO turnover. Candidate age between 44and 52, conditional on candidate availability, is therefore an instru-ment for succession planning and chair independence that can beexcluded from the CEO turnover equation. Any candidate age effecton CEO turnover is accordingly attributed to the succession plan-ning and chair independence channel.

These exclusion restrictions deliver an identified model. I estimate theSUR system using simulated maximum likelihood methods based on theGHK algorithm5.

5The GHK algorithm was developed independently by Geweke (1989), Hajivassiliouand McFadden (1998), and Keane (1994). It is implemented in Stata for general condi-tional mixed processes with the user-written command cmp by Roodman (2011).

9

3.1 Unobserved Ability

The effect of managerial ability on board decisions could generally beeliminated by conditioning on it. However, it is difficult to directly ob-serve executive ability and there are no good proxies or instruments. Myempirical strategy is therefore to condition on managerial ability by select-ing samples where executive ability is likely to be similar.

Corporate boards receive various public and private signals in orderto learn unobservable managerial ability over time (Taylor (2010)). CEOsurvival is accordingly related to ability: chief executives surviving boardscrutiny long enough to enter natural retirement should have high aver-age ability, and those that are forced out sooner should have low averageability (Weisbach (1988), Fee et al. (2010)). I therefore select two samplesthat are likely to differ in CEO ability: natural retirements with high CEOability, and forced turnover with low CEO ability. If the regression coeffi-cients are robust for different levels of CEO ability then a bias caused byunobserved heterogeneity is unlikely.

4 Data

4.1 Sample Selection

The primary data source is BoardEx, which provides information on ex-ecutive management and non-executive board members by firm for thefiscal years from 1999 to 2008. The data set is merged with Compustat foraccounting and stock market information. The sample is restricted to non-financial U.S. firms6 with a minimum of $10 million in total assets wherethe chief executive is known at the beginning and end of each fiscal year.Interim successors, identified by either the title interim or acting chief ex-ecutive or by a CEO tenure of less than one year, are excluded. A turnoverevent occurs when the chief executive leaves the firm.

After selecting the initial sample I categorize CEO turnover further by

6SIC codes between 6000 and 6999 are excluded.

10

type. I select news articles from Factiva that contain the name of each de-parting chief executive during a two-year window around the turnoverdate to classify the likely cause of the departure. Forced turnover and nat-ural retirements are identified according to the classification used by Par-rino (1997). Forced turnover is selected with the following procedure: first,all turnover where a CEOs is reported to be fired is classified as forced.Second, all other turnover in which CEOs are under age 60 are reviewedfurther. If the report does not mention that: (i) the exit is health-related,(ii) the departing CEO either takes a new job in or outside the firm, leavesfor personal or other reasons unrelated to the firm, or (iii) the chief execu-tive departs in a natural retirement, then such turnover is also classified asforced. Retirement is natural when a CEO retires and announces it at leastsix months before leaving the firm.

Table 1 shows a panel data set with 25, 622 firm-years, 2, 250 firms,4, 665 chief executives, and 2, 790 CEO turnover events. Of these, 690 arenatural retirements and 1, 090 are forced CEO turnover.

Each turnover event typically comes with a succession. A relay succes-sion is a planned succession, characterized by an incoming CEO who waspreviously heir apparent and a departing CEO who stays on as chairper-son. An heir apparent is a firm insider with a tenure of at least one yearwho is either president, chief operating officer, or vice chairperson of thefirm prior to the transition. Chair independence is defined here as a chair-person who is neither the current nor a former chief executive. Relay suc-cession and chair independence are mutually exclusive: relay successionsby definition require a CEO who stays on as chairperson, and thereforethe chair is not independent.

4.2 Descriptive Statistics

Since the BoardEx database is not widely used in CEO turnover research,I report several key descriptive statistics for the sample.

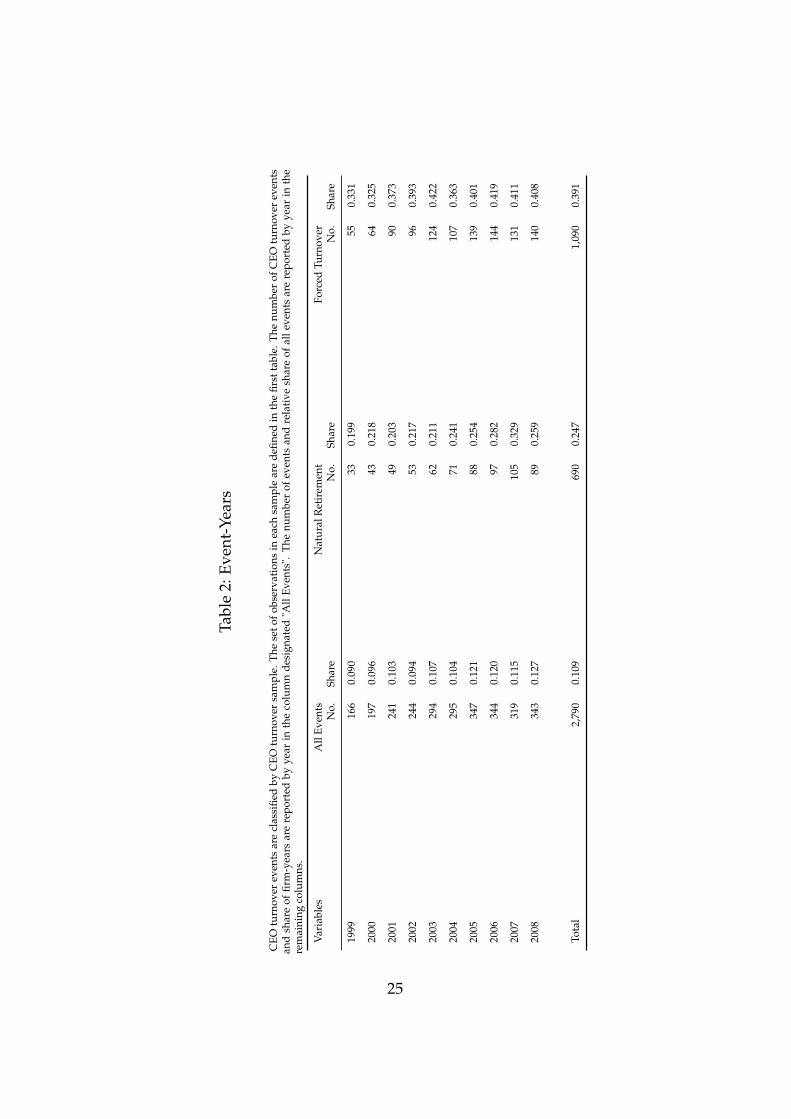

Table 2 reports the distribution of CEO turnover by year. The overallannual turnover rate is 10.9% and consistent with Parrino (1997), Naveen

11

(2006), and Fee et al. (2010). The average share of natural CEO retirementsis 24.7% and the average share of forced CEO turnover is 39.1%, the latterdisplaying an upward trend.

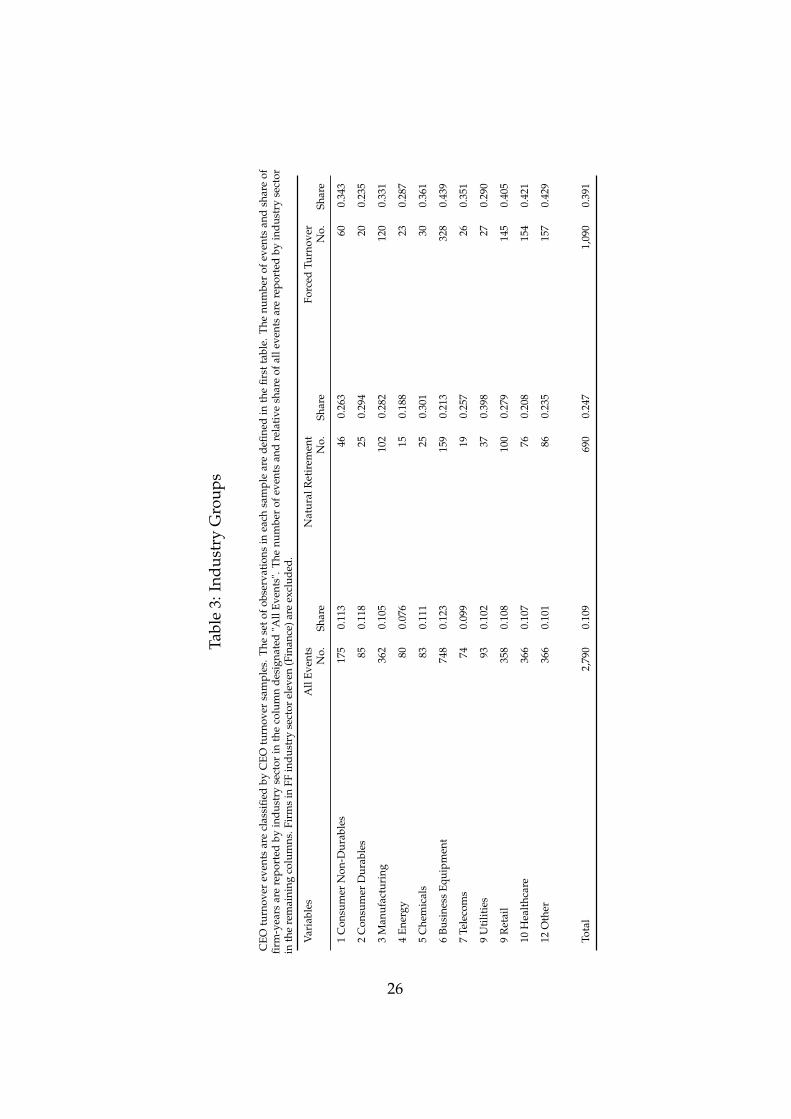

Table 3 illustrates the industry distribution of CEO turnover using theFama-French 12-industry classification system7. While the turnover ratevaries little across industry sectors, the proportion of natural retirementsand forced turnover varies considerably across sectors, this most likelyreflects differences in industry maturity and competition.

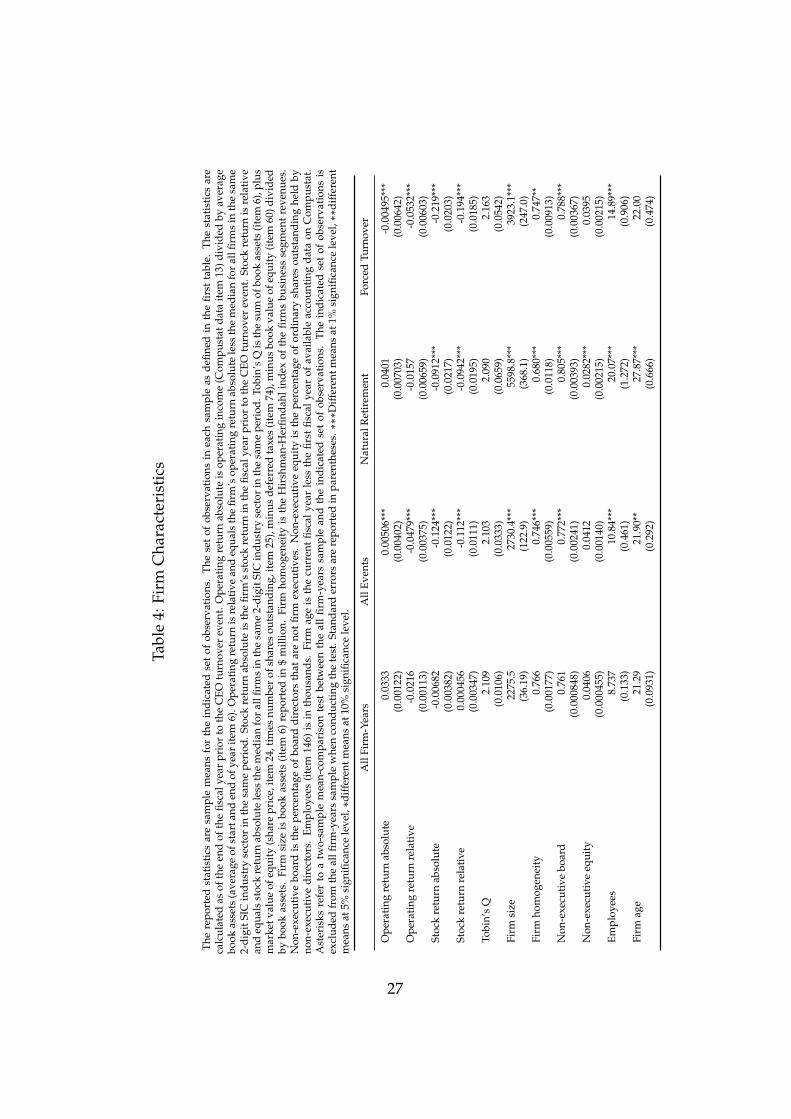

Table 4 presents firm characteristics. Turnover events are preceded bylow operating and stock returns. Firm size, age, and homogeneity, alongwith the proportion of non-executive board members are also correlatedwith CEO turnover.

Table 5 shows characteristics for incoming (Panel A) and outgoing CEOs(Panel B). The average CEO successor is 51.8 years old and replaces a 58.2year-old predecessors after a tenure of 7.7 years. Overall 28.4% of out-going chief executives have an independent chair of the board and 44.2%appoint an heir apparent. For natural retirements the average departureage is 59.4 years and CEO tenure is 7.2 years, 25.3% have an independentchairperson, and 44.9% have planned for their succession with an heir ap-parent. For forced turnover the average exit age is 54.8 years and tenureis 6.1 years, 34.2% have an independent chair, and 32.8% have an heir ap-parent.

Panel B also displays the succession type for departing chief execu-tives. Relay successions account for 23.3%, other inside successions for41.7%, and outside successions for 34.9% of all CEO turnover, respectively.Relay successions represent only 10.6% but outside successions accountfor 40.7% of forced turnover.

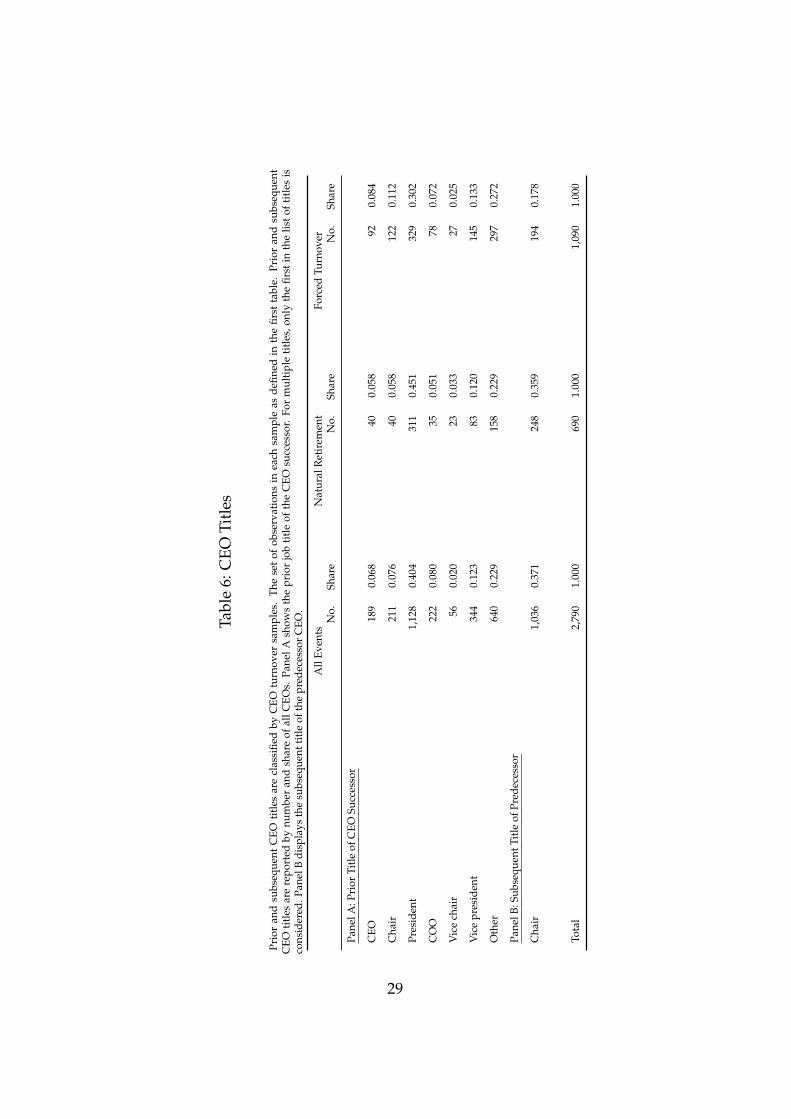

Table 6 presents the prior title of the incoming and subsequent tile ofthe outgoing CEO, respectively. Of the incoming CEOs 6.8% were CEOat another firm, while 7.6% were chairperson, 40.4% president, 7.8% chiefoperating officer, and 1.8% vice chair at the firm, respectively. Of the out-

7Definition of Fama-French 12-industry classification available athttp://mba.tuck.dartmouth.edu/pages/faculty/ken.french/

12

going CEOs 37.1% stay on as chairperson.There is a close relationship between chair independence, succession

planning and CEO turnover.Figure 1 presents the proportion of firms that have an independent

chairperson, i.e. a chair who is neither the current nor a former CEO.This figure shows that chair independence is strongly correlated with CEOturnover. The increase in chair independence around CEO turnover re-flects the fact that departing dual CEO-chairs do not always become non-executive chairperson.

Figure 2 displays the share of firms that plan CEO successions by ap-pointing an heir apparent. It shows that succession planning is stronglycorrelated with CEO turnover, particularly for natural retirements. Theshare of heirs apparent increases before the CEO turnover period and de-creases afterwards. This reflects that most firms only install one heir ap-parent who either becomes the next chief executive or typically leaves.

5 Results

The multivariate results are presented in three parts. First, I present a stan-dard probit regression of CEO turnover on exogenous covariates. Second,I display a "naïve" probit regression of CEO turnover that adds chair inde-pendence and succession planning but erroneously treats these endoge-nous variables as exogenous. Third, I show my main result: a trinomialprobit regression system of CEO turnover that models chair independenceand succession planning endogenously. These approaches produce signif-icantly different results and show that treating endogenous variables asexogenous can lead to large errors.

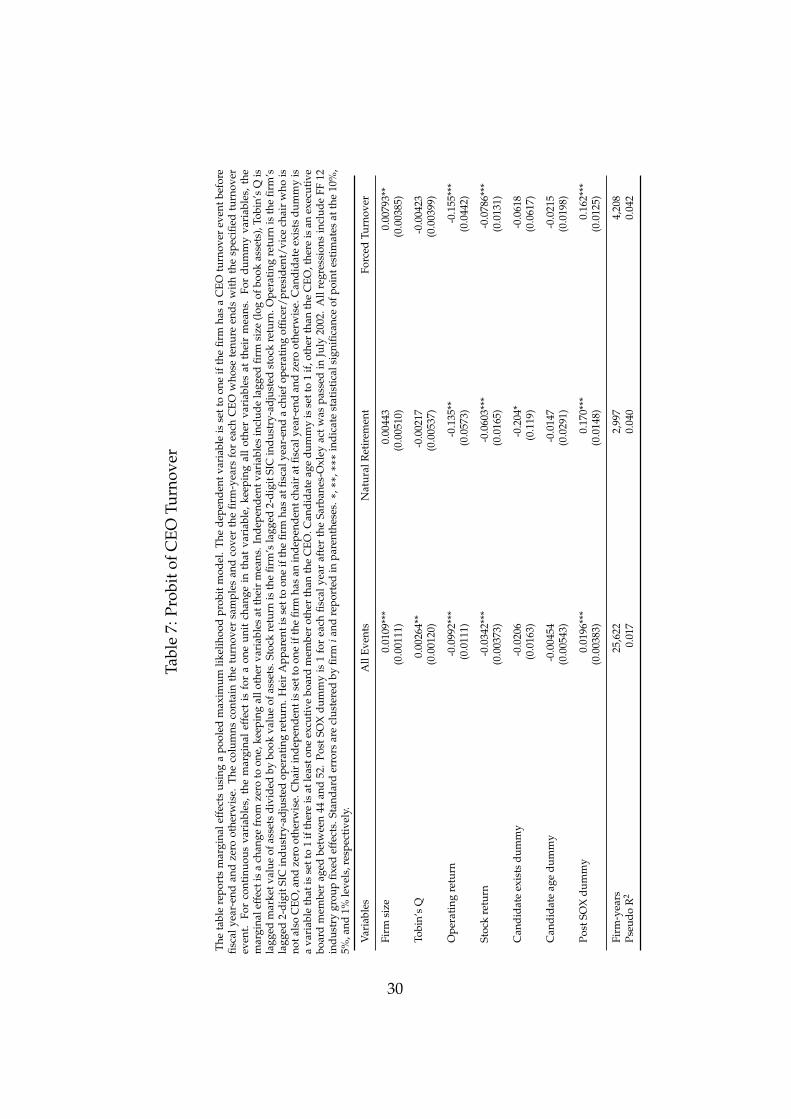

5.1 Standard Probit Regression

Table 7 shows the marginal effects for a standard probit regression of CEOturnover on exogenous variables. Industry-adjusted operating and stockreturns are significantly negative. This is consistent with the relative per-

13

formance evaluation hypothesis where firm performance measured rel-ative to industry benchmarks reveals CEO ability and untalented chiefexecutives are replaced. The post-Sarbanes-Oxley (SOX) dummy is alsosignificant, indicating that after 2002 CEO turnover increased.

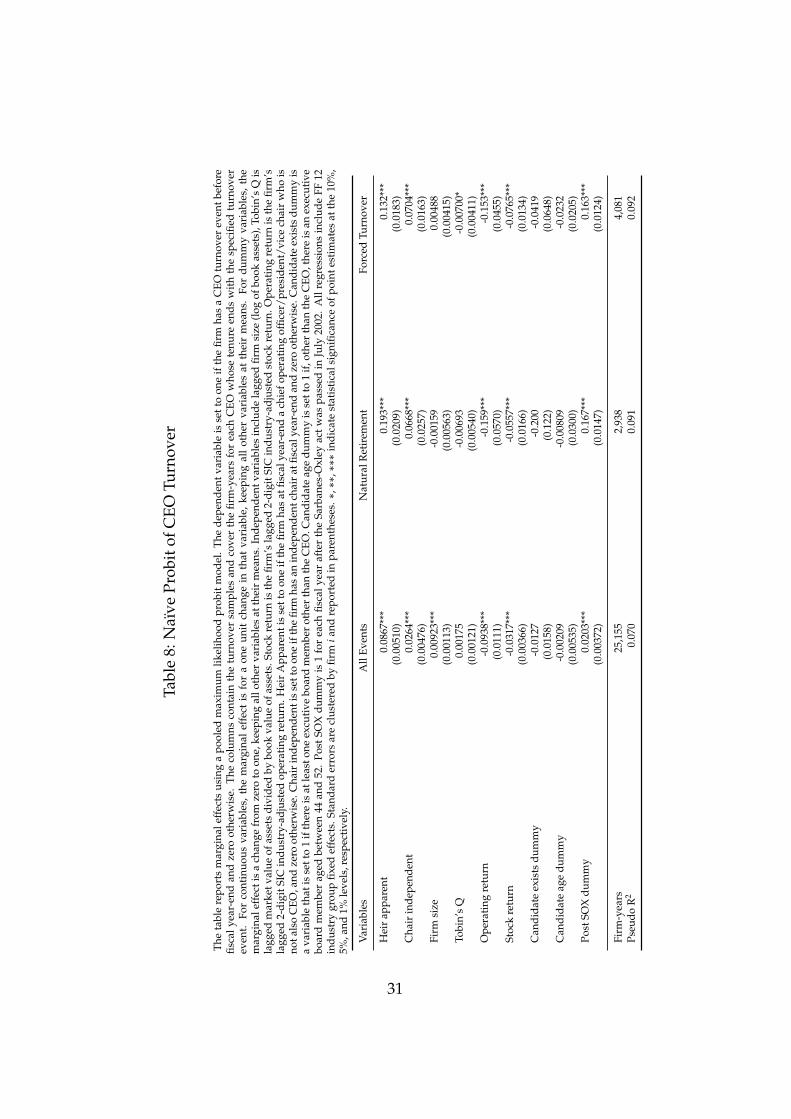

5.2 Naïve Probit Regression

Next, I analyze a naïve regression that ignores the endogeneity in chair in-dependence and succession planning. Firms most likely determine chairindependence and succession planning simultaneously but ignoring si-multaneity usually leads to inconsistent estimates. In order to explore theseverity of this issue it is instructive to compare these results with the morerobust methods further on.

Table 8 displays the marginal effects for a probit regression of CEOturnover on several exogenous variables, as well as on the endogenousvariables succession planning and chair independence. Succession plan-ning (heir apparent) seems to have a highly significant effect that increasesthe probability of CEO turnover by 19.3% for natural retirements, 13.2%for forced turnover, and 8.7% overall. Chair independence also appearsto have a highly significantly effect that increases the likelihood of CEOturnover by 6.7% for natural retirements, 7.0% for forced turnover, and2.6% overall.

The naïve regression results rely on the assumption that successionplanning and chair independence are exogenous, which is not plausible. Ifthese variables are functions of other variables then these estimates couldbe inconsistent. It is therefore better to use a model that is flexible enoughto deal with endogenously determined variables.

5.3 Trivariate Probit Regression System

I use a system of recursive, fully observed, and seemingly unrelated re-gressions (SUR) in order to estimate a model with endogenous variables.The SUR model includes three stages: the first stage is a standard probit

14

regression for chair independence (Eq. 1); the second stage is a bivariateprobit for succession planning (heir apparent) on chair independence (Eq.2); and the third stage is a trivariate probit for CEO turnover on chair in-dependence and succession planning (Eq. 3). For better identification Iimpose one exclusion restriction on the second stage and two on the thirdstage.

Table 9 shows the first stage, reporting the marginal effects of a probitregression for chair independence on exogenous covariates. Firm size hasa significantly negative correlation with chair independence since largerfirms are less likely to have an independent director chairing the board.Operating return has a significantly negative correlation with chair inde-pendence because underperforming firms are more likely to have an in-dependent chair. The insignificant coefficient for the natural retirementsample may reflect upward earnings management by retiring CEOs. Can-didate age between 44 and 52 (after controlling for candidate existence)has a significantly positive correlation with chair independence. Execu-tive board members within that age group are more likely to serve underan independent chairperson. Chair independence also increases signifi-cantly during the post-SOX years.

The candidate age dummy (after controlling for candidate existence)and the post-SOX dummy serve as instruments in the SUR model. Table 9shows that both are significantly correlated with chair independence andtherefore relevant instruments for the first stage.

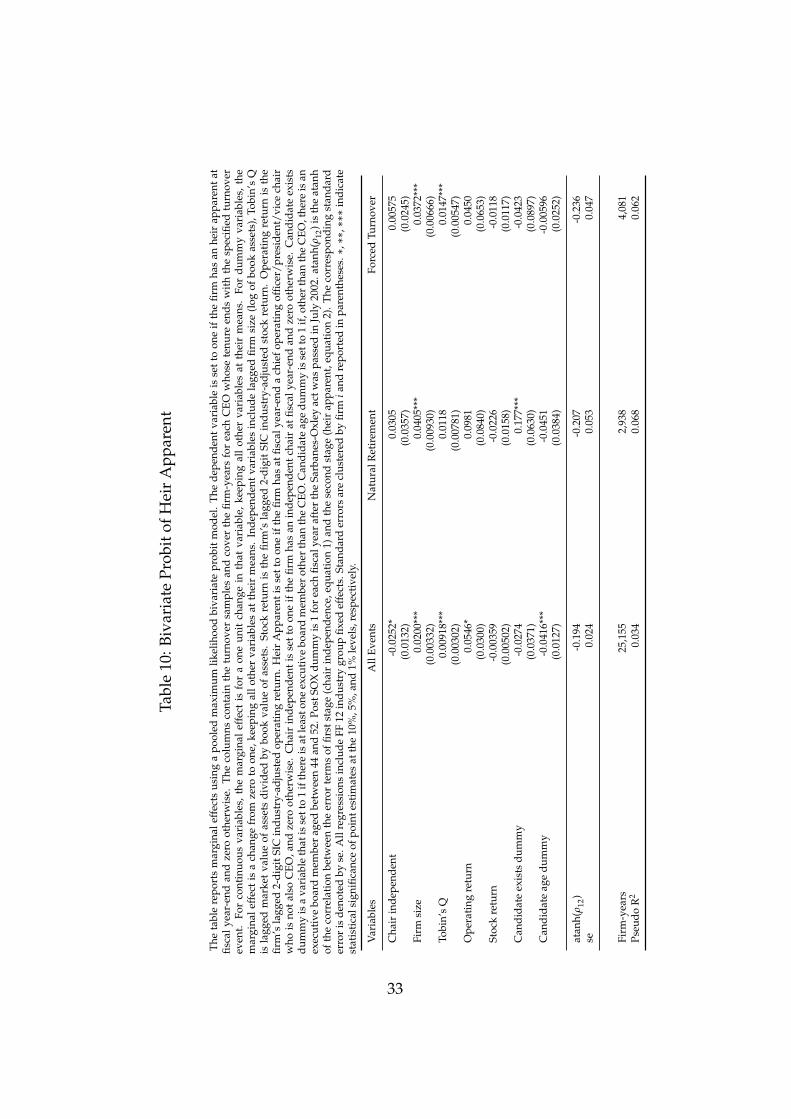

Table 10 presents the second stage, displaying the marginal effects ofa bivariate probit regression for succession planning (heir apparent) onchair independence and exogenous variables. Firm size is positively cor-related with succession planning; the larger a firm, the larger its internaltalent pool and the higher the likelihood of an internal heir apparent. To-bin’s Q is positively correlated with succession planning; the higher themarginal value of the firm, the higher the return to talent and the higherthe likelihood of an internal heir apparent.

Chair independence is weakly negatively correlated with successionplanning since independent chairs are less likely to appoint an heir appar-

15

ent from inside the firm. Chair independence is structurally incompatiblewith relay successions where the departing dual CEO-chair remains on theboard as a (dependent) chairperson. The test result is consistent with hy-pothesis IE that chair independence makes succession planning less likely.

The candidate age dummy (after controlling for candidate existence)is an instrument in the SUR model. Table 10 shows that it is significantlycorrelated with succession planning and therefore a relevant instrumentfor the second stage.

The SUR model uses fully observed dependent variables in all stagesand estimates the correlation between the respective error terms. Thisproperty makes it robust to omitted variable problems in all stages ex-cept the final. The regression estimates are consistent even if influentialvariables are omitted in the first stage. The correlation between the errorterms for the first (chair independence) and second (heir apparent) stageis reported as atanh(ρ12) and significantly negative. This shows that thereis an endogenous relationship between succession planning and chair in-dependence.

Table 11 presents the third and final stage. It presents the marginaleffects for a trivariate, recursive probit regression of CEO turnover on suc-cession planning (heir apparent), chair independence and exogenous vari-ables.

Succession planning (heir apparent) is significantly correlated with CEOturnover, increasing the likelihood of CEO turnover by 32.3% for naturalretirements, 22.0% for forced turnover, and 20.4% overall. Firms that havean heir apparent are much more likely to fire a chief executive. Withoutan heir apparent in place, firms show a greatly reduced willingness to dis-miss the CEO, possibly due to the higher cost and risk of using an untestedsuccessor from inside or outside the company. These results are consistentwith hypothesis DE2 that succession planning makes CEO turnover morelikely.

Chair independence is significantly correlated with CEO turnover, de-creasing the likelihood of CEO turnover by 4.0% overall (the coefficientestimates are similar for both natural retirements and forced turnover but

16

less significant). Independent chairs are less likely to fire a CEO. Thesetest results are not consistent with hypothesis DE1 because chair indepen-dence makes CEO turnover less likely.

The explanation seems to be as follows: A relay succession alwayscomes with both an heir apparent and a dependent chair. Chair inde-pendence therefore rules out relay successions, and CEO turnover is nega-tively affected by fewer (relay) heirs apparent. Any positive effect for chairindependence on CEO turnover seems to be exceeded by the negative ef-fect from the succession planning (heir apparent) channel.

Industry-adjusted operating and stock returns are significantly nega-tive. This is again consistent with the relative performance evaluation hy-pothesis.

The correlation between the error terms for the first (chair indepen-dence) and second (heir apparent) stage is again atanh(ρ12), for the first(chair independence) and third (CEO turnover) stage is atanh(ρ13), and forthe second (heir apparent) and third (CEO turnover) stage is atanh(ρ23).The correlation is in all cases highly significant and shows that there is anendogenous relationship between chair independence, succession plan-ning, and CEO turnover.

When comparing these results with the naïve regressions above it seemsthat endogeneity indeed greatly influences the estimates for chair inde-pendence and the existence of an heir apparent. The correlation betweensuccession planning (heir apparent) and CEO turnover is approximatelytwice that suggested by the single-equation model. The correlation be-tween chair independence and CEO turnover changes sign and becomessignificantly negative. Clearly there is a substantial bias in the naïve single-equation regressions and renders them useless when endogeneity is present.

Succession planning seems to have an even larger effect on CEO turnoverthan suggested by previous research. Chair independence does not seemto sufficiently improve corporate governance. Instead, chair independencerules out the common relay succession model and appears to cause fric-tions that exceed its potential benefits.

17

6 Conclusion

There is extensive literature on the individual determinants of CEO turnover.However, only a few articles have examined more complex systems of cor-porate decision making and address endogeneity issues in observationaldata.

This paper analyzes how chair independence and succession planninginfluence CEO turnover. I use a recursive SUR system in order to provideconsistent estimates of decision variables that are determined simultane-ously with omitted variables. A new comprehensive data set permits theselection of a large sample.

The analysis shows that succession planning has an even larger effecton CEO turnover than suggested by previous research. Chair indepen-dence has a significantly negative effect on succession planning due tofrictions with the common relay succession model. Overall, chair inde-pendence makes CEO turnover less likely.

Subsamples of natural CEO retirements and forced turnover show thatthese results are not driven by unobserved hetherogeneity in CEO ability.

These results differ markedly from a naïve regression that ignores en-dogeneity in chair independence and succession planning, as well as demon-strating that great care must be exercised when analyzing the effect of en-dogenous corporate decision variables.

18

References

Dahya, J., J. McConnell, and N. Travlos (2002). The Cadbury Committee,Corporate Performance, and Top Management Turnover. Journal ofFinance 57(1), 461–483.

Fama, E. (1980). Agency Problems and the Theory of the Firm. Journalof Political Economy, 288–307.

Fama, E. and M. Jensen (1983). Separation of Ownership and Control.Journal of Law & Econonmics 26, 301.

Fee, C., C. Hadlock, and J. Pierce (2010). Managers Who Lack Style:Evidence from Exogenous CEO changes. Working paper, MichiganState University.

Geweke, J. (1989). Bayesian Inference in Econometric Models UsingMonte Carlo Integration. Econometrica, 1317–1339.

Goyal, V. and C. Park (2002). Board Leadership Structure and CEOTurnover. Journal of Corporate Finance 8(1), 49–66.

Hajivassiliou, V. and D. McFadden (1998). The Method of SimulatedScores for the Estimation of LDV Models. Econometrica, 863–896.

Jensen, M. and W. Meckling (1976). Theory of the Firm: Managerial Be-havior, Agency Costs and Ownership Structure. Journal of FinancialEconomics 3(4), 305–360.

Jensen, M. and R. Ruback (1983). The Market for Corporate Control: TheScientific Evidence. Journal of Financial Economics 11(1-4), 5–50.

Keane, M. (1994). A Computationally Practical Simulation Estimator forPanel Data. Econometrica, 95–116.

Murphy, K. (1999). Executive Compensation. Handbook of LaborEconomics 3, 2485–2563.

Naveen, L. (2006). Organizational Complexity and Succession Planning.Journal of Financial & Quantitative Analysis 41(03), 661–683.

19

Parrino, R. (1997). CEO Turnover and Outside Succession: A Cross-Sectional Analysis. Journal of Financial Economics 46(2), 165–197.

Roodman, D. (2011). Fitting Fully Observed Recursive Mixed-ProcessModels with CMP. Stata Journal 11(2), 159–206.

Taylor, L. A. (2010). Why are CEOs Rarely Fired? Evidence from Struc-tural Estimation. Journal of Finance 65(6), 2051–2087.

Vancil, R. F. (1987). Passing the Baton: Managing the Process of CEO Succession.Harvard Business School Press, Boston, MA.

Weisbach, M. (1988). Outside Directors and CEO Turnover. Journal ofFinancial Economics 20, 431–460.

Wilde, J. (2000). Identification of Multiple Equation Probit Models withEndogenous Dummy Regressors. Economics Letters 69(3), 309–312.

Wooldridge, J. M. (2010). Econometric Analysis of Cross Section and Panel Data, 2nd edition.MIT Press, Cambridge, MA.

20

7 Figures and Tables

21

Figure 1: Chair Independence by Period

0.1

.2.3

.4.5

Sha

re

5 4 3 2 1 0 1 2 3 4 5Event Year

Natural Retirement Forced Turnover

22

Figure 2: Heir Apparent by Period

.1.2

.3.4

.5S

hare

5 4 3 2 1 0 1 2 3 4 5Event Year

Natural Retirement Forced Turnover

23

Tabl

e1:

Sam

ple

Stat

isti

cs

The

sam

ple

incl

udes

allC

EOs

iden

tifie

dfr

omBo

ardE

xbe

twee

n19

99an

d20

08.

This

data

isth

enm

erge

dw

ith

Com

pust

atfo

rac

coun

ting

and

stoc

kpr

ice

info

rmat

ion.

The

data

seti

sre

stri

cted

tono

n-fin

anci

alfir

ms

inco

rpor

ated

inth

eU

.S.w

ith

am

inim

umof

US$

10m

illio

nin

tota

lass

ets

whe

reth

eid

enti

tyof

the

CEO

iskn

own

atth

ebe

ginn

ing

and

end

ofea

chfis

caly

ear.

Inte

rim

succ

esso

rs,i

dent

ified

byei

ther

the

titl

ein

teri

mor

acti

ngch

ief

exec

utiv

e,or

bya

CEO

tenu

reof

less

than

one

year

,are

excl

uded

.Atu

rnov

erev

enth

asoc

curr

edw

hen

the

iden

tity

ofa

chie

fexe

cuti

veat

fisca

lyea

r-en

ddi

ffer

sfr

omth

atat

the

begi

nnin

gof

afis

caly

ear.

The

natu

ralr

etir

emen

tan

dfo

rced

exit

subs

ampl

esar

eca

tego

rize

dac

cord

ing

toa

met

hod

desc

ribe

din

Parr

ino

(199

7).

No.

Shar

e

All

firm

-yea

rs25

,622

All

com

pani

es2,

250

All

CEO

s4,

665

CEO

Turn

over

Sam

ples

All

even

ts2,

790

1.00

0

Nat

ural

reti

rem

ent

690

0.24

7

Forc

edtu

rnov

er1,

090

0.39

1

24

Tabl

e2:

Even

t-Ye

ars

CEO

turn

over

even

tsar

ecl

assi

fied

byC

EOtu

rnov

ersa

mpl

e.Th

ese

tofo

bser

vati

ons

inea

chsa

mpl

ear

ede

fined

inth

efir

stta

ble.

The

num

ber

ofC

EOtu

rnov

erev

ents

and

shar

eof

firm

-yea

rsar

ere

port

edby

year

inth

eco

lum

nde

sign

ated

"All

Even

ts".

The

num

ber

ofev

ents

and

rela

tive

shar

eof

alle

vent

sar

ere

port

edby

year

inth

ere

mai

ning

colu

mns

.

Var

iabl

esA

llEv

ents

Nat

ural

Ret

irem

ent

Forc

edTu

rnov

erN

o.Sh

are

No.

Shar

eN

o.Sh

are

1999

166

0.09

033

0.19

955

0.33

1

2000

197

0.09

643

0.21

864

0.32

5

2001

241

0.10

349

0.20

390

0.37

3

2002

244

0.09

453

0.21

796

0.39

3

2003

294

0.10

762

0.21

112

40.

422

2004

295

0.10

471

0.24

110

70.

363

2005

347

0.12

188

0.25

413

90.

401

2006

344

0.12

097

0.28

214

40.

419

2007

319

0.11

510

50.

329

131

0.41

1

2008

343

0.12

789

0.25

914

00.

408

Tota

l2,

790

0.10

969

00.

247

1,09

00.

391

25

Tabl

e3:

Indu

stry

Gro

ups

CEO

turn

over

even

tsar

ecl

assi

fied

byC

EOtu

rnov

ersa

mpl

es.

The

seto

fobs

erva

tion

sin

each

sam

ple

are

defin

edin

the

first

tabl

e.T

henu

mbe

rof

even

tsan

dsh

are

offir

m-y

ears

are

repo

rted

byin

dust

ryse

ctor

inth

eco

lum

nde

sign

ated

"All

Even

ts".

The

num

ber

ofev

ents

and

rela

tive

shar

eof

alle

vent

sar

ere

port

edby

indu

stry

sect

orin

the

rem

aini

ngco

lum

ns.F

irm

sin

FFin

dust

ryse

ctor

elev

en(F

inan

ce)a

reex

clud

ed.

Var

iabl

esA

llEv

ents

Nat

ural

Ret

irem

ent

Forc

edTu

rnov

erN

o.Sh

are

No.

Shar

eN

o.Sh

are

1C

onsu

mer

Non

-Dur

able

s17

50.

113

460.

263

600.

343

2C

onsu

mer

Dur

able

s85

0.11

825

0.29

420

0.23

5

3M

anuf

actu

ring

362

0.10

510

20.

282

120

0.33

1

4En

ergy

800.

076

150.

188

230.

287

5C

hem

ical

s83

0.11

125

0.30

130

0.36

1

6Bu

sine

ssEq

uipm

ent

748

0.12

315

90.

213

328

0.43

9

7Te

leco

ms

740.

099

190.

257

260.

351

9U

tilit

ies

930.

102

370.

398

270.

290

9R

etai

l35

80.

108

100

0.27

914

50.

405

10H

ealt

hcar

e36

60.

107

760.

208

154

0.42

1

12O

ther

366

0.10

186

0.23

515

70.

429

Tota

l2,

790

0.10

969

00.

247

1,09

00.

391

26

Tabl

e4:

Firm

Cha

ract

eris

tics

The

repo

rted

stat

isti

csar

esa

mpl

em

eans

for

the

indi

cate

dse

tof

obse

rvat

ions

.Th

ese

tof

obse

rvat

ions

inea

chsa

mpl

eas

defin

edin

the

first

tabl

e.T

hest

atis

tics

are

calc

ulat

edas

ofth

een

dof

the

fisca

lyea

rpr

ior

toth

eC

EOtu

rnov

erev

ent.

Ope

rati

ngre

turn

abso

lute

isop

erat

ing

inco

me

(Com

pust

atda

tait

em13

)div

ided

byav

erag

ebo

okas

sets

(ave

rage

ofst

arta

nden

dof

year

item

6).O

pera

ting

retu

rnis

rela

tive

and

equa

lsth

efir

m’s

oper

atin

gre

turn

abso

lute

less

the

med

ian

for

allfi

rms

inth

esa

me

2-di

gitS

ICin

dust

ryse

ctor

inth

esa

me

peri

od.

Stoc

kre

turn

abso

lute

isth

efir

m’s

stoc

kre

turn

inth

efis

caly

ear

prio

rto

the

CEO

turn

over

even

t.St

ock

retu

rnis

rela

tive

and

equa

lsst

ock

retu

rnab

solu

tele

ssth

em

edia

nfo

ral

lfirm

sin

the

sam

e2-

digi

tSIC

indu

stry

sect

orin

the

sam

epe

riod

.Tob

in’s

Qis

the

sum

ofbo

okas

sets

(ite

m6)

,plu

sm

arke

tval

ueof

equi

ty(s

hare

pric

e,it

em24

,tim

esnu

mbe

rof

shar

esou

tsta

ndin

g,it

em25

),m

inus

defe

rred

taxe

s(i

tem

74),

min

usbo

okva

lue

ofeq

uity

(ite

m60

)div

ided

bybo

okas

sets

.Fi

rmsi

zeis

book

asse

ts(i

tem

6)re

port

edin

$m

illio

n.Fi

rmho

mog

enei

tyis

the

Hir

shm

an-H

erfin

dahl

inde

xof

the

firm

sbu

sine

ssse

gmen

tre

venu

es.

Non

-exe

cuti

vebo

ard

isth

epe

rcen

tage

ofbo

ard

dire

ctor

sth

atar

eno

tfir

mex

ecut

ives

.N

on-e

xecu

tive

equi

tyis

the

perc

enta

geof

ordi

nary

shar

esou

tsta

ndin

ghe

ldby

non-

exec

utiv

edi

rect

ors.

Empl

oyee

s(i

tem

146)

isin

thou

sand

s.Fi

rmag

eis

the

curr

ent

fisca

lyea

rle

ssth

efir

stfis

caly

ear

ofav

aila

ble

acco

unti

ngda

taon

Com

pust

at.

Ast

eris

ksre

fer

toa

two-

sam

ple

mea

n-co

mpa

riso

nte

stbe

twee

nth

eal

lfir

m-y

ears

sam

ple

and

the

indi

cate

dse

tof

obse

rvat

ions

.T

hein

dica

ted

set

ofob

serv

atio

nsis

excl

uded

from

the

allfi

rm-y

ears

sam

ple

whe

nco

nduc

ting

the

test

.Sta

ndar

der

rors

are

repo

rted

inpa

rent

hese

s.���D

iffer

entm

eans

at1%

sign

ifica

nce

leve

l,��

diff

eren

tm

eans

at5%

sign

ifica

nce

leve

l,�d

iffer

entm

eans

at10

%si

gnifi

canc

ele

vel.

All

Firm

-Yea

rsA

llEv

ents

Nat

ural

Ret

irem

ent

Forc

edTu

rnov

er

Ope

rati

ngre

turn

abso

lute

0.03

330.

0050

6***

0.04

01-0

.004

95**

*(0

.001

22)

(0.0

0402

)(0

.007

03)

(0.0

0642

)O

pera

ting

retu

rnre

lati

ve-0

.021

6-0

.047

9***

-0.0

157

-0.0

532*

**(0

.001

13)

(0.0

0375

)(0

.006

59)

(0.0

0603

)St

ock

retu

rnab

solu

te-0

.006

82-0

.124

***

-0.0

912*

**-0

.219

***

(0.0

0382

)(0

.012

2)(0

.021

7)(0

.020

3)St

ock

retu

rnre

lati

ve0.

0004

56-0

.112

***

-0.0

942*

**-0

.194

***

(0.0

0347

)(0

.011

1)(0

.019

5)(0

.018

5)To

bin’

sQ

2.10

92.

103

2.09

02.

163

(0.0

106)

(0.0

333)

(0.0

659)

(0.0

542)

Firm

size

2275

.527

30.4

***

5598

.8**

*39

23.1

***

(36.

19)

(122

.9)

(368

.1)

(247

.0)

Firm

hom

ogen

eity

0.76

60.

746*

**0.

680*

**0.

747*

*(0

.001

77)

(0.0

0559

)(0

.011

8)(0

.009

13)

Non

-exe

cuti

vebo

ard

0.76

10.

772*

**0.

805*

**0.

788*

**(0

.000

848)

(0.0

0241

)(0

.003

93)

(0.0

0367

)N

on-e

xecu

tive

equi

ty0.

0406

0.04

120.

0282

***

0.03

95(0

.000

455)

(0.0

0140

)(0

.002

15)

(0.0

0215

)Em

ploy

ees

8.73

710

.84*

**20

.07*

**14

.89*

**(0

.133

)(0

.461

)(1

.272

)(0

.906

)Fi

rmag

e21

.29

21.9

0**

27.8

7***

22.0

0(0

.093

1)(0

.292

)(0

.666

)(0

.474

)

27

Tabl

e5:

CEO

Cha

ract

eris

tics

The

repo

rted

stat

isti

csar

esa

mpl

em

eans

for

the

indi

cate

dse

tof

obse

rvat

ions

.Th

ese

tof

obse

rvat

ions

inea

chsa

mpl

eas

defin

edin

the

first

tabl

e.T

hest

atis

tics

are

calc

ulat

edas

ofth

een

dof

the

fisca

lyea

rpr

ior

toth

eC

EOtu

rnov

erev

ent(

unle

ssst

ated

othe

rwis

e).

Pane

lAsh

ows

stat

isti

csfo

rth

eC

EOsu

cces

sor

and

Pane

lBfo

rth

epr

edec

esso

r.A

geis

inye

ars

atfis

caly

ear-

end.

Col

lege

issh

are

ofC

EOs

wit

hgr

adua

tede

gree

.MBA

issh

are

ofC

EOs

wit

hM

BAde

gree

.Org

aniz

atio

nalt

enur

eis

year

sin

sam

efir

mat

fisca

lyea

r-en

d.In

dust

ryte

nure

isye

ars

inpu

blic

U.S

.firm

insa

me

2-di

gitS

ICin

dust

ryse

ctor

atfis

caly

ear-

end.

Lead

ersh

ipte

nure

isye

ars

asC

EOor

ashe

irap

pare

ntat

fisca

lyea

r-en

d.C

hair

inde

pend

ence

isth

esh

are

ofch

airs

who

are

nott

hecu

rren

tor

afo

rmer

CEO

.Hei

rap

pare

ntis

shar

eof

CEO

sw

hoha

veat

leas

ton

ehe

irap

pare

nt.

Ast

eris

ksre

fer

toa

two-

sam

ple

mea

n-co

mpa

riso

nte

stbe

twee

nth

eal

lfirm

-yea

rssa

mpl

ean

dth

ein

dica

ted

seto

fob

serv

atio

ns.

The

indi

cate

dse

tof

obse

rvat

ions

isex

clud

edfr

omth

eal

lfirm

-yea

rssa

mpl

ew

hen

cond

ucti

ngth

ete

st.

Stan

dard

erro

rsar

ere

port

edin

pare

nthe

ses.���

Diff

eren

tmea

nsat

1%si

gnifi

canc

ele

vel,��

diff

eren

tmea

nsat

5%si

gnifi

canc

ele

vel,�

diff

eren

tmea

nsat

10%

sign

ifica

nce

leve

l.

All

Firm

-Yea

rsA

llEv

ents

Nat

ural

Ret

irem

ent

Forc

edTu

rnov

er

Pane

lA:C

EOSu

cces

sor

Age

55.0

551

.78*

**52

.41*

**52

.29*

**(0

.051

2)(0

.142

)(0

.269

)(0

.238

)C

olle

ge0.

799

0.84

2***

0.88

3***

0.86

1***

(0.0

0250

)(0

.006

91)

(0.0

123)

(0.0

105)

MBA

0.27

30.

324*

**0.

367*

**0.

339*

**(0

.002

78)

(0.0

0886

)(0

.018

4)(0

.014

3)O

rgan

izat

iona

lten

ure

13.3

17.

008*

**7.

515*

**6.

335*

**(0

.065

7)(0

.163

)(0

.357

)(0

.255

)Pa

nelB

:Pre

dece

ssor

Age

61.0

758

.23*

**59

.35*

**54

.84*

**(0

.086

7)(0

.168

)(0

.302

)(0

.227

)C

EOte

nure

7.99

27.

664*

**7.

230*

**6.

136*

**(0

.070

4)(0

.138

)(0

.264

)(0

.170

)O

rgan

izat

iona

lten

ure

15.9

813

.86*

**15

.19*

11.5

6***

(0.1

17)

(0.2

19)

(0.4

59)

(0.3

04)

Cha

irin

depe

nden

t0.

257

0.28

4***

0.25

30.

342*

**(0

.002

76)

(0.0

0871

)(0

.016

8)(0

.014

7)H

eir

appa

rent

0.28

90.

442*

**0.

499*

**0.

328*

**(0

.002

83)

(0.0

0940

)(0

.019

0)(0

.014

2)R

elay

succ

essi

on0.

0254

0.23

3***

0.22

9***

0.10

6***

(0.0

0098

3)(0

.008

01)

(0.0

160)

(0.0

0931

)O

ther

insi

desu

cces

sion

0.04

540.

417*

**0.

401*

**0.

487*

**(0

.001

30)

(0.0

0934

)(0

.018

7)(0

.015

1)O

utsi

desu

cces

sion

0.03

810.

349*

**0.

370*

**0.

407*

**(0

.001

20)

(0.0

0903

)(0

.018

4)(0

.014

9)

28

Tabl

e6:

CEO

Titl

es

Prio

ran

dsu

bseq

uent

CEO

titl

esar

ecl

assi

fied

byC

EOtu

rnov

ersa

mpl

es.

The

set

ofob

serv

atio

nsin

each

sam

ple

asde

fined

inth

efir

stta

ble.

Prio

ran

dsu

bseq

uent

CEO

titl

esar

ere

port

edby

num

ber

and

shar

eof

allC

EOs.

Pane

lAsh

ows

the

prio

rjo

bti

tle

ofth

eC

EOsu

cces

sor.

For

mul

tipl

eti

tles

,onl

yth

efir

stin

the

listo

fti

tles

isco

nsid

ered

.Pan

elB

disp

lays

the

subs

eque

ntti

tle

ofth

epr

edec

esso

rC

EO.

All

Even

tsN

atur

alR

etir

emen

tFo

rced

Turn

over

No.

Shar

eN

o.Sh

are

No.

Shar

e

Pane

lA:P

rior

Titl

eof

CEO

Succ

esso

r

CEO

189

0.06

840

0.05

892

0.08

4

Cha

ir21

10.

076

400.

058

122

0.11

2

Pres

iden

t1,

128

0.40

431

10.

451

329

0.30

2

CO

O22

20.

080

350.

051

780.

072

Vic

ech

air

560.

020

230.

033

270.

025

Vic

epr

esid

ent

344

0.12

383

0.12

014

50.

133

Oth

er64

00.

229

158

0.22

929

70.

272

Pane

lB:S

ubse

quen

tTit

leof

Pred

eces

sor

Cha

ir1,

036

0.37

124

80.

359

194

0.17

8

Tota

l2,

790

1.00

069

01.

000

1,09

01.

000

29

Tabl

e7:

Prob

itof

CEO

Turn

over

The

tabl

ere

port

sm

argi

nale

ffec

tsus

ing

apo

oled

max

imum

likel

ihoo

dpr

obit

mod

el.

The

depe

nden

tvar

iabl

eis

sett

oon

eif

the

firm

has

aC

EOtu

rnov

erev

entb

efor

efis

caly

ear-

end

and

zero

othe

rwis

e.Th

eco

lum

nsco

ntai

nth

etu

rnov

ersa

mpl

esan

dco

ver

the

firm

-yea

rsfo

rea

chC

EOw

hose

tenu

reen

dsw

ith

the

spec

ified

turn

over

even

t.Fo

rco

ntin

uous

vari

able

s,th

em

argi

nal

effe

ctis

for

aon

eun

itch

ange

inth

atva

riab

le,

keep

ing

all

othe

rva

riab

les

atth

eir

mea

ns.

For

dum

my

vari

able

s,th

em

argi

nale

ffec

tis

ach

ange

from

zero

toon

e,ke

epin

gal

loth

erva

riab

les

atth

eir

mea

ns.I

ndep

ende

ntva

riab

les

incl

ude

lagg

edfir

msi

ze(l

ogof

book

asse

ts),

Tobi

n’s

Qis

lagg

edm

arke

tval

ueof

asse

tsdi

vide

dby

book

valu

eof

asse

ts.S

tock

retu

rnis

the

firm

’sla

gged

2-di

gitS

ICin

dust

ry-a

djus

ted

stoc

kre

turn

.Ope

rati

ngre

turn

isth

efir

m’s

lagg

ed2-

digi

tSIC

indu

stry

-adj

uste

dop

erat

ing

retu

rn.H

eir

App

aren

tis

sett

oon

eif

the

firm

has

atfis

caly

ear-

end

ach

iefo

pera

ting

offic

er/p

resi

dent

/vic

ech

air

who

isno

tals

oC

EO,a

ndze

root

herw

ise.

Cha

irin

depe

nden

tis

sett

oon

eif

the

firm

has

anin

depe

nden

tcha

irat

fisca

lyea

r-en

dan

dze

root

herw

ise.

Can

dida

teex

ists

dum

my

isa

vari

able

that

isse

tto

1if

ther

eis

atle

asto

neex

cuti

vebo

ard

mem

ber

othe

rth

anth

eC

EO.C

andi

date

age

dum

my

isse

tto

1if

,oth

erth

anth

eC

EO,t

here

isan

exec

utiv

ebo

ard

mem

ber

aged

betw

een

44an

d52

.Po

stSO

Xdu

mm

yis

1fo

rea

chfis

caly

ear

afte

rth

eSa

rban

es-O

xley

act

was

pass

edin

July

2002

.A

llre

gres

sion

sin

clud

eFF

12in

dust

rygr

oup

fixed

effe

cts.

Stan

dard

erro

rsar

ecl

uste

red

byfir

mia

ndre

port

edin

pare

nthe

ses.�,��

,���

indi

cate

stat

isti

cals

igni

fican

ceof

poin

test

imat

esat

the

10%

,5%

,and

1%le

vels

,res

pect

ivel

y.

Var

iabl

esA

llEv

ents

Nat

ural

Ret

irem

ent

Forc

edTu

rnov

er

Firm

size

0.01

09**

*0.

0044

30.

0079

3**

(0.0

0111

)(0

.005

10)

(0.0

0385

)

Tobi

n’s

Q0.

0026

4**

-0.0

0217

-0.0

0423

(0.0

0120

)(0

.005

37)

(0.0

0399

)

Ope

rati

ngre

turn

-0.0

992*

**-0

.135

**-0

.155

***

(0.0

111)

(0.0

573)

(0.0

442)

Stoc

kre

turn

-0.0

342*

**-0

.060

3***

-0.0

786*

**(0

.003

73)

(0.0

165)

(0.0

131)

Can

dida

teex

ists

dum

my

-0.0

206

-0.2

04*

-0.0

618

(0.0

163)

(0.1

19)

(0.0

617)

Can

dida

teag

edu

mm

y-0

.004

54-0

.014

7-0

.021

5(0

.005

43)

(0.0

291)

(0.0

198)

Post

SOX

dum

my

0.01

96**

*0.

170*

**0.

162*

**(0

.003

83)

(0.0

148)

(0.0

125)

Firm

-yea

rs25

,622

2,99

74,

208

Pseu

doR

20.

017

0.04

00.

042

30

Tabl

e8:

Naï

vePr

obit

ofC

EOTu

rnov

er

The

tabl

ere

port

sm

argi

nale

ffec

tsus

ing

apo

oled

max

imum

likel

ihoo

dpr

obit

mod

el.

The

depe

nden

tvar

iabl

eis

sett

oon

eif

the

firm

has

aC

EOtu

rnov

erev

entb

efor

efis

caly

ear-

end

and

zero

othe

rwis

e.Th

eco

lum

nsco

ntai

nth

etu

rnov

ersa

mpl

esan

dco

ver

the

firm

-yea

rsfo

rea

chC

EOw

hose

tenu

reen

dsw

ith

the

spec

ified

turn

over

even

t.Fo

rco

ntin

uous

vari

able

s,th

em

argi

nal

effe

ctis

for

aon

eun

itch

ange

inth

atva

riab

le,

keep

ing

all

othe

rva

riab

les

atth

eir

mea

ns.

For

dum

my

vari

able

s,th

em

argi

nale

ffec

tis

ach

ange

from

zero

toon

e,ke

epin

gal

loth

erva

riab

les

atth

eir

mea

ns.I

ndep

ende

ntva

riab

les

incl

ude

lagg

edfir

msi

ze(l

ogof

book

asse

ts),

Tobi

n’s

Qis

lagg

edm

arke

tval

ueof

asse

tsdi

vide

dby

book

valu

eof

asse

ts.S

tock

retu

rnis

the

firm

’sla

gged

2-di

gitS

ICin

dust

ry-a

djus

ted

stoc

kre

turn

.Ope

rati

ngre

turn

isth

efir

m’s

lagg

ed2-

digi

tSIC

indu

stry

-adj

uste

dop

erat

ing

retu

rn.H

eir

App

aren

tis

sett

oon

eif

the

firm

has

atfis

caly

ear-

end

ach

iefo

pera

ting

offic

er/p

resi

dent

/vic

ech

air

who

isno

tals

oC

EO,a

ndze

root

herw

ise.

Cha

irin

depe

nden

tis

sett

oon

eif

the

firm

has

anin

depe

nden

tcha

irat

fisca

lyea

r-en

dan

dze

root

herw

ise.

Can

dida

teex

ists

dum

my

isa

vari

able

that

isse

tto

1if

ther

eis

atle

asto

neex

cuti

vebo

ard

mem

ber

othe

rth

anth

eC

EO.C

andi

date

age

dum

my

isse

tto

1if

,oth

erth

anth

eC

EO,t

here

isan

exec

utiv

ebo

ard

mem

ber

aged

betw

een

44an

d52

.Po

stSO

Xdu

mm

yis

1fo

rea

chfis

caly

ear

afte

rth

eSa

rban

es-O

xley

act

was

pass

edin

July

2002

.A

llre

gres

sion

sin

clud

eFF

12in

dust

rygr

oup

fixed

effe

cts.

Stan

dard

erro

rsar

ecl

uste

red

byfir

mia

ndre

port

edin

pare

nthe

ses.�,��

,���

indi

cate

stat

isti

cals

igni

fican

ceof

poin

test

imat

esat

the

10%

,5%

,and

1%le

vels

,res

pect

ivel

y.

Var

iabl

esA

llEv

ents

Nat

ural

Ret

irem

ent

Forc

edTu

rnov

er

Hei

rap

pare

nt0.

0867

***

0.19

3***

0.13

2***

(0.0

0510

)(0

.020

9)(0

.018

3)C

hair

inde

pend

ent

0.02

64**

*0.

0668

***

0.07

04**

*(0

.004

76)

(0.0

257)

(0.0

163)

Firm

size

0.00

923*

**-0

.001

590.

0048

8(0

.001

13)

(0.0

0563

)(0

.004

15)

Tobi

n’s

Q0.

0017

5-0

.006

93-0

.007

00*

(0.0

0121

)(0

.005

40)

(0.0

0411

)O

pera

ting

retu

rn-0

.093

8***

-0.1

59**

*-0

.153

***

(0.0

111)

(0.0

570)

(0.0

455)

Stoc

kre

turn

-0.0

317*

**-0

.055

7***

-0.0

765*

**(0

.003

66)

(0.0

166)

(0.0

134)

Can

dida

teex

ists

dum

my

-0.0

127

-0.2

00-0

.041

9(0

.015

8)(0

.122

)(0

.064

8)C

andi

date

age

dum

my

-0.0

0209

-0.0

0809

-0.0

232

(0.0

0535

)(0

.030

0)(0

.020

5)Po

stSO

Xdu

mm

y0.

0203

***

0.16

7***

0.16

3***

(0.0

0372

)(0

.014

7)(0

.012

4)

Firm

-yea

rs25

,155

2,93

84,

081

Pseu

doR

20.

070

0.09

10.

092

31

Tabl

e9:

Prob

itof

Cha

irIn

depe

nden

ce

The

tabl

ere

port

sm

argi

nale

ffec

tsus

ing

apo

oled

max

imum

likel

ihoo

dpr

obit

mod

el.

The

depe

nden

tvar

iabl

eis

sett

oon

eif

the

firm

has

anin

depe

nden

tcha

irat

fisca

lye

ar-e

ndan

dze

root

herw

ise.

The

colu

mns

cont

ain

the

turn

over

sam

ples

and

cove

rth

efir

m-y

ears

for

each

CEO

who

sete

nure

ends

wit

hth

esp

ecifi

edtu

rnov

erev

ent.

For

cont

inuo

usva

riab

les,

the

mar

gina

leff

ecti

sfo

ra

one

unit

chan

gein

that

vari

able

,kee

ping

allo

ther

vari

able

sat

thei

rm

eans

.For

dum

my

vari

able

s,th

em

argi

nale

ffec

tis

ach

ange

from

zero

toon

e,ke

epin

gal

loth

erva

riab

les

atth

eir

mea

ns.I

ndep

ende

ntva

riab

les

incl

ude

lagg

edfir

msi

ze(l

ogof

book

asse

ts),

Tobi

n’s

Qis

lagg

edm

arke

tva

lue

ofas

sets

divi

ded

bybo

okva

lue

ofas

sets

.Sto

ckre

turn

isth

efir

m’s

lagg

ed2-

digi

tSIC

indu

stry

-adj

uste

dst

ock

retu

rn.O

pera

ting

retu

rnis

the

firm

’sla

gged

2-di

git

SIC

indu

stry

-adj

uste

dop

erat

ing

retu

rn.H

eir

App

aren

tis

sett

oon

eif

the

firm

has

atfis

caly

ear-

end

ach

iefo

pera

ting

offic

er/p

resi

dent

/vic

ech

air

who

isno

tals

oC

EO,

and

zero

othe

rwis

e.C

hair

inde

pend

ent

isse

tto

one

ifth

efir

mha

san

inde

pend

ent

chai

rat

fisca

lyea

r-en

dan

dze

root

herw

ise.

Can

dida

teex

ists

dum

my

isa

vari

able

that

isse

tto

1if

ther

eis

atle

ast