do leverage, dividend policy and profitability influence the firm value

DESCRIPTION

Influence of firm value by leverageTRANSCRIPT

Electronic copy available at: http://ssrn.com/abstract=1158251

Do Leverage, Dividend Policy and Profitability influence the

Future Value of Firm? Evidence from India

By

Saurabh Ghosh∗

and

Arijit Ghosh**

Indira Gandhi Institute of Development Research

Gen. A.K. Vaidya Marg, Goregaon (East),

Mumbai-400065, India

Email: [email protected]

∗ Saurabh Ghosh is presently a Research Officer in Monetary Policy Department, Reserve Bank of India. **Arijit Ghosh is Doctoral Fellow in Indira Gandhi Institute of Development Research (IGIDR). Views expressed by the authors are their personal. The usual disclaimer applies.

Electronic copy available at: http://ssrn.com/abstract=1158251

Do Leverage, Dividend Policy and Profitability influence the

Future Value of Firm? Evidence from India

Abstract

This paper examines the effect of past dividend policy, leverage and profitability on the probability

of increase in future value of the firm (in terms of market to book value ratio (MBVR)) for an

emerging economy, India. We use fixed effect logit model to predict the probability of increase in

future value of the S&PCNX500 firms, from 1989-90 to 2001-02. We find that there is a non-linear

relation between leverage, profitability and probability of increase in future value of the firm.

Probability of increase in future value of firm reduces exponentially with the increase in leverage,

whereas, it increases with the raise in dividend payout and profitability of the firm. Among the

companies from different ownership groups, foreign standalone firms have larger probability to

create better future value than group-affiliated firms.

JEL Classification: G 32 G35 C23 C25

Keywords: Dividend Policy, Profitability, Firm Value, Logit Model, Panel Data

Do Leverage, Dividend Policy and Profitability influence the Future Value of Firm?

Evidence from India

1. Introduction With the ushering of economic liberalization in 1992, Indian stock market has

undergone several changes over the last decade. These include introduction of new

exchanges, massive computerization and electronic limit order book integrating the stock

exchanges across the nation, establishing of clearing corporation and subsequent

introduction of new derivative products in the market. Perhaps the most important among

these changes was the establishment of Securities and Exchange Board of India (SEBI) in

1992 as the market watchdog. SEBI, since it’s inception has strived in the direction of

narrowing the information gap between Indian corporations and investors, enforce better

corporate governance practices through guidelines, rules and regulations and through

active market for corporate control that has marked a new era in the Indian financial

arena. The investors reveled their confidence through their participation in the primary

and secondary market. Large number of new companies came to the primary market over

1993-96 and the market capitalization of S&PCNX 500 has increased considerably over

1990s. India has emerged as an emerging economy with largest number of companies

listed in its stock markets.

Over the last decade corporate governance has received considerable importance

in Indian financial market. With the initiation of market for corporate control and

activities in the merger and acquisition market, CEOs have assigned tremendous

importance for creating value for their firms. Accordingly companies from different

sectors (and/or ownership groups) have adopted different strategies to signal their earning

and growth potential over the years and thereby influence their stock prices. With this in

the background this paper attempts to analyze the factors that influenced the future value

of the companies listed in Indian stock markets and also how the effect of these factor

changes over different categories of firms.

The reminder of the paper is organized as follows. Section 2 gives a brief

overview of the literature. Data and the statistical specification used in this study are

described Section 3. Section 4 presents the empirical results and their interpretations.

Section 5 concludes the paper.

2. Background Literature

The well-developed and vibrant literature in modern corporate finance has its root

in the seminal paper by Franco Modigliani and Merton Miller (1958, 1963), (M-M

henceforth). This branch of finance started with the assumption of perfect information

and complete markets. It postulates that in a typical neoclassical market with perfect

competition, absence of agency costs, transaction and banking costs, the average cost of

raising fund for any firm is completely independent of its capital structure. With the same

set of assumptions M-M (1963) argued that the value of the firm is unaffected by the

dividend policy. However, over time many of these simplified assumptions were relaxed

and subsequent research showed capital structure does matter and there could exist

optimal dividend policy in the modified M-M framework.

Academic literature over the last decade has documented the effect of different

strategic factors influencing the firm values for the developed countries. Rappaport

(1981, 1987) has used value creation literature for corporate mergers and acquisition and

underlined the importance of growth rate, operating profit, income tax rate and fixed

capital investment as the major factor influencing the firms’ value. Recently some of the

studies concentrated on emerging market to analyze the factors that influenced the firms’

value in this market. Ben Naceur and Goaied (2002) investigated value creation process

for Tunisian stock exchange using a random probit model with unbalanced panel data. It

considered that the managers’ succeeded creating value to its share holders if the market

value of the share exceeds the book value of the corporation and vice versa. The authors

considered three main determinants of value creation: financial policy, profitability and

dividend policy.

In the modified M-M framework, literature has shown that firm’s performance

depends on the capital structure (or financial policy). Ross (1977) argued that more

leverage would signal the investors about the improved firm prospect and influence the

firm’s value in future. Increase in dividend payout increases the investors’ income at

present and signal the expected future cash flow for the corporation. Profitability is

undoubtedly one of the major factors determining the firm value. Ben Naceur and Goaied

(2002) argued that while profitability and debt have positive effect on the probability of

crating future value, the pay-out have reverse effect on the same.

India has one of the most developed stock markets in the world with large number

of domestic and international players investing in Indian stock market. With maximum

number of companies listed in the Indian stock exchanges from different industries and

different ownership groups (e.g. business affiliated firms, Indian standalone, foreign

standalone) and with the emphasis on corporate governance practices, India has become

an important and interesting destination for such studies. Among the available studies in

this area, Sahu (2002) used a sample of companies listed in BSE to explain the abnormal

stock returns by dividend stability and found no statically significant result. Another

study by Tuli and Mittal (2001) used 101 Indian firms and found price earning ratio is

significantly influenced by variability of market price and dividend pay out ratio.

However, the authors did not find any significant effect of industry and ownership pattern

on price to earning ratio.

This papers aims at determining the factors influencing the probability of future

firm value for Indian corporations after controlling for the industry and time specific

effects. In particular this study attempts to answer the following questions:

1. How the probability of future value creation is affected by firm’s

profitability, financing pattern and the dividend pay-out policy?

2. Whether the firms belonging to business groups have different effect on

probability of value creation?

3. Data

The primary source of the data for this paper is PROWESS database, compiled

by Center for Monitoring the Indian Economy (CMIE). This dataset is similar to the

COMPUSTAT database in USA. We have selected the firms that are presently included

in S&PCNX 500 index. The accounting and stock price data for these companies are

extracted for the year 1989-90 to 2001-02 from Prowess dataset for this study1.

Variable Description

Market to book value ratio (MBVR) is defined as the ratio of closing price of the

equity to book value of equity at the end of the financial year. MBVR is the dependent

variable for the OLS regression. For the logit model the dependent variable is a binary

series, which takes the value 1 if price to book value ratio is greater than one (i.e., market

perceived that future value of the firm is going to increase) and zero otherwise.

The other variables of interest include those representing Leverage Policy,

Dividend Policy and Profitability that have key bearing on the firms’ future value

creation. While the ratio of total amount of long-term debt to total amount of equity

capital (LEVERAGE) is included to proxy the leverage policy of the corporation, the ratio

of total dividend to total earning of the firm (PAY_OUT) is included to capture the

dividend policy of the same. The profitability of a company, on the other hand, is

captured by the ratio of net profit to net worth of the firm, which is also known as return

on equity (ROE).

To control for the size of the firm we consider total assets (ASSET) of the firm as a

proxy variable. To control for the differenced arising due to the firms belonging to

different business groups this paper considers different dummy variables. If the firm is

1 Among the large number of listed companies, those included in S&PCNX 500 are often considered for empirical studies for their liquid nature and representative characteristics.

private Indian standalone then the dummy, D_PVT_IND, take the value one and zero

otherwise. If, on the other hand, a firm is private foreign standalone then the dummy,

D_PVT_FOR, take the value one and otherwise zero. Indian companies differ considerably

access the industries. So industry dummies were used to control for industry specific

heterogeneity. Since 1990, Indian economy has undergone several changes, which have

their influence on the corporate valuation. So time dummies were also included to control

for the time trend. All the nominal variables are deflated by GDP deflator and expressed

at constant price of 1987-88.

(Insert Table-1 here)

Table 1 shows the mean values and the standard deviations (in parenthesis) of the

variables under consideration under six different cases (namely, all firms, large firms,

small firms, group-affiliated firms, Indian standalone firms and foreign standalone firms).

The descriptive statistics reported in Table 1 shows that the value of a firm, in terms of

MBVR, is higher for the small firms and the foreign standalone firms. Large firms get

more leverage than any other category of firms. Profitability of the firm, in terms of ROE,

is higher for the Indian standalone companies. Table 2 shows the Pearson correlation

coefficient matrix between the variables of interest. It shows that MBVR has significant

negative correlation with leverage and size of the firm and positive correlation with

dividend policy and profitability of the firm. In the Appendix Figure 1 and 4 show that

with the ushering of economic liberalization there is a sharp rise in MBVR and ROE in

the year 1992, which have gradually decreased over the years. Figure 2 shows since post

liberalization period, the leverage has shown an increasing trend. However, dividend

payout policy does not depict any significant trend over this period.

4. Methodology & Results

So far we have done the univariate and bivariate analysis in the previous section.

To examine the factors effecting the future value creation of the firms listed in the Indian

stock exchange we first examine the effect of previous year’s leverage, dividend and

profitability on the MBVR of the company in a multivariate framework. The generic

form for this unbalanced panel model is as follows:

MBVRit = α + αt + β1LEVERAGEt-1 + β2(LEVERAGEt-1)2 + β3 PAY_OUTt-1 + β4 ROEt-1

+ β5(ROEt-1)2 + β6 LOG(ASSETt-1) + β7 D_PVT_INDit + β8 D_PVT_FORit +

+ ε∑=

+

22

18 )_(

kktk DINDβ it (1)

To account for the non-linearity in the relationship, the square of the previous

year’s leverage, pay out and profitability were also included in the regression. The

regression results based on the model specified in equation one is reported in Table 3

below.

(Insert table 3 here)

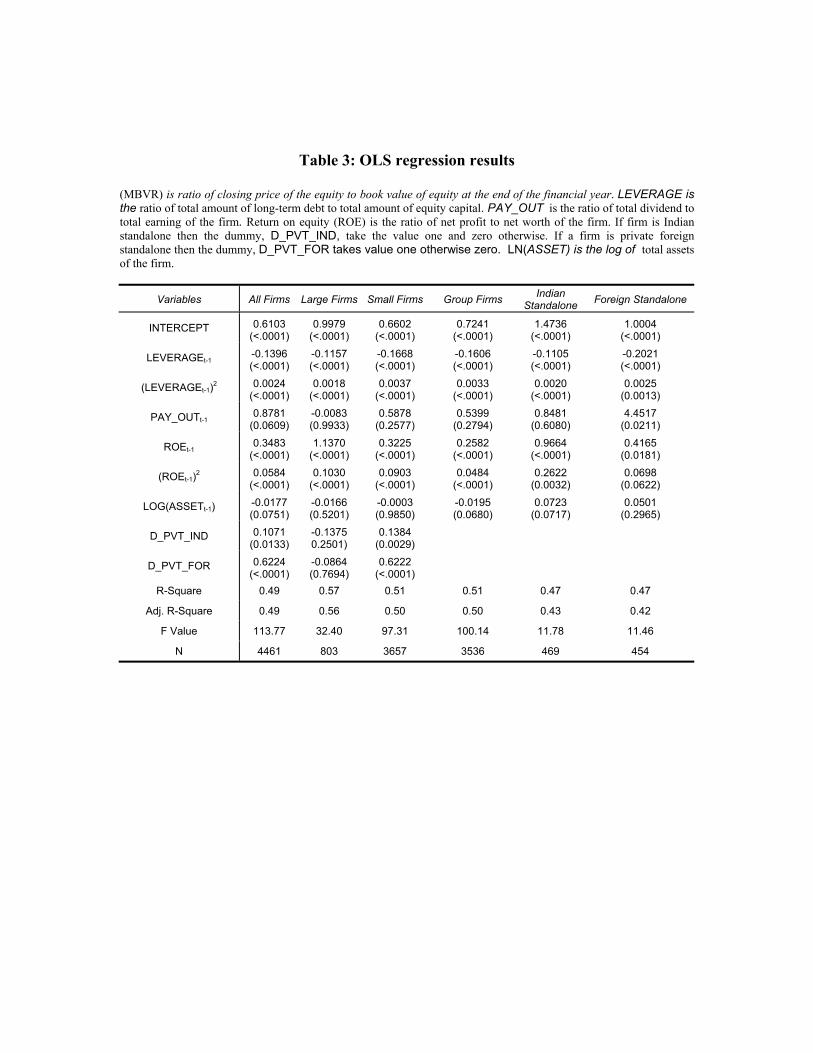

From Table 3, it appears that the previous year’s leverage has a negative effect (-

0.14) on the MBVR of the company, which is significant at one per cent level. This effect

however decreases with the increases in leverage, which appears from the positive

coefficient of the square of LEVERAGE-t-1 term. For the Indian corporations the previous

years pay-off (0.87) and return on equity (0.35) have positive influence on the

corporations’ MBVR. Moreover the square term of ROE has a positive coefficient

implying that ROE influences MBVR at an increasing rate. The log of assets and the

dummies for group companies were all significantly different from zero at ten per cent

levels. The significance of these coefficients prompted separate analysis of the future

value creation across different groups and size2. The results reported in table 3

substantiate conclusions of the pooled model as the signs of the independent variables

coefficients as they are obtained in the pooled model. However, the previous year’s

payout significantly affects MBVR for the all firms sample and especially for the sample

of foreign standalone companies.

2 Companies with total asset more than median of total asset is considered as large size and others are considered as small. The asset size however differs considerable across the broad classification. To account for it ln(asset) was included as a control variable in these sub-groups.

This paper also attempts to model the probability of increase in the future value of

the firm. The binary variable (Y) takes value 1 if MBVR is greater than one (i.e., if the

market value of the firm is greater than the book value), otherwise zero. The logistic

model is as follows:

ee

ititt

ititt

X

X

itit XYob εβαα

εβαα

+′++

+′++

+==

1)|1(Pr (2)

where Xit are the same explanatory variables used in equation (1). This model

aims to predict how the probability of improvement of the future value of the firm

influenced by the previous year’s dividend and leverage policy and profitability of the

firm. The empirical results of the logit model is reported in the table-4 below

The coefficient of lagged value of leverage (-O.44) and its square term (0.007)

imply that as the leverage of the firm increases, the probability of raise in future firm’s

values declines at a decreasing rate. The negative influence of leverage on the probability

of future value creation was observed across the ownership groups and size. The

profitability of the firm (as apparent from the coefficient of ROE) increases the

probability of increase in future value creation. Point to note is, this increase is higher for

foreign standalone firms as compare to Indian standalone or group-affiliated firms.

Unlike the OLS model, the dividend payout did not significantly explain the chance of

future value creation. Neither in the pooled model nor in the size and ownership group

specific regression the coefficient of payout was significantly different from zero at 10

per cent level.

This paper analyzed the accounting factor that influence the probability of

increase in future market valuation of the firms’ listed in Indian stock exchange after

controlling for the time and industry specific effects. The empirical results indicate that

the increase in leverage has a negative impact on the chance of future value increase of

the firm. It could be because more reliance on credit increases the conflict of interest

between shareholders and creditors, giving more control to the managers/promoter, which

in turn have a negative influence on the future valuation. Alike Naceur and Goaied

(2002), we found previous year’s profitability positive influences future firm’s value, as

increase in profitability might have signaled better quality of management. However, the

pay-off did not significantly influence the probability of future MBVR increase in the

pooled model as well as the models across ownership group and size. This finding could

be because of the fact that the dividend payment the future performance varied

considerably across firms listed in Indian stock exchange.

5. Conclusion

This paper investigates the value creation process of the firms listed in the Indian

stock market and their dependence on the accounting variables. It used an unbalanced

logit model and found that the increase in profitability has a positive influence on the

probability of creating future value and the relation is stronger for foreign standalone

firms as compared to private Indian standalone or business group owned firms. Leverage,

one the other hand, has negative impact on the chances of increase in future value of the

corporation and this relation was uniform across size and ownership group. It could be

because of the potential conflict of interest between the equity holders and the creditors

that got reflected in the stock prices. The dividend pay-off policy of the firm, however,

could not significantly influence the probability of future value creation of the firms

listed in Indian stock market.

Reference:

Ben-Naceur, Samy and Mohamed Goaied (2002), “The Relationship between Dividend Policy, Financial Structure, Profitability and Firm Value”, Applied Financial Economics, 12(12), 843-49.

Modigliani, Franco and Merton Miller (1958), "The Cost of Capital, Corporation Finance, and the Theory of Investment." American Economic Review, 48, 261-97. Modigliani, Franco and Merton Miller (1963), "Corporate Income Taxes and the Cost of Capital." American Economic Review, 53, 433-43. Rappaport, A. (1986) Linking Competitive Strategy and Shareholder Value Analysis. The Journal of Business Strategy, 3, 58-67 Rappaport, A. (1987) Corporate Performance Standards and Shareholder Value. The Journal of Business Strategy 4, 28-38. Ross. S (1977). The Determination Of Financial Structure The Incentive Signaling Approach. Bell Journal of Economics. 8, 23-40 Sahu, Chinmoy (2002), “An Empirical Test of Stable Dividend Hypothesis”, Finance India, 16(2), 613-26. Tuli, Nishi and, R K Mittal (2001), “Determinants of Price-Earnings Ratio”, Finance India, 15(4), 1235-50.

Table 1: Descriptive statistics (MBVR) is ratio of closing price of the equity to book value of equity at the end of the financial year. LEVERAGE is

the ratio of total amount of long-term debt to total amount of equity capital. PAY_OUT is the ratio of total dividend to total earning of the firm. Return on equity (ROE) is the ratio of net profit to net worth of the firm. ASSET total assets

of the firm.

Variable All Firms Large Firms Small Firms Group Firms Indian

Standalone Firms

Foreign Standalone Firms

MBVR 3.137 (5.993)

2.133 (3.537)

3.349 (6.372)

2.833 (5.659)

2.850 (5.119)

5.776 (8.255)

LEVERAGE 1.726 (4.140)

3.057 (7.151)

1.441 (3.063)

1.973 (4.470)

1.247 (3.094)

0.319 (0.484)

DIVIDEND PAY OFF 0.023 (0.029)

0.025 (0.028)

0.023 (0.029)

0.024 (0.030)

0.024 (0.026)

0.020 (0.023)

PROFITABILITY (ROE) 0.138 (0.367)

0.095 (0.449)

0.148 (0.346)

0.133 (0.372)

0.168 (0.283)

0.148 (0.397)

SIZE 13.795 (75.556)

66.395 (170.110)

2.500 (2.248)

16.639 (84.509)

3.632 (9.212)

2.146 (6.210)

Table 2: Pearson Correlation Matrix. (MBVR) is ratio of closing price of the equity to book value of equity at the end of the financial year. LEVERAGE is

the ratio of total amount of long-term debt to total amount of equity capital. PAY_OUT is the ratio of total dividend to total earning of the firm. Return on equity (ROE) is the ratio of net profit to net worth of the firm. ASSET total assets

of the firm.

MBVR LEVERAGE POLICY DIVIDEND POLICY PROFITABILITY SIZE

MBVR 1.000

LEVERAGE -0.158 (<.0001) 1.000

PAY-0FF 0.028 (0.060)

-0.093 (<.0001) 1.000

ROE 0.074 (<.0001)

-0.210 (<.0001)

0.124 (<.0001) 1.000

SIZE -0.042 (<.0001)

0.076 (<.0001)

-0.011 (0.450)

-0.021 (0.155) 1.000

Table 3: OLS regression results (MBVR) is ratio of closing price of the equity to book value of equity at the end of the financial year. LEVERAGE is the ratio of total amount of long-term debt to total amount of equity capital. PAY_OUT is the ratio of total dividend to total earning of the firm. Return on equity (ROE) is the ratio of net profit to net worth of the firm. If firm is Indian standalone then the dummy, D_PVT_IND, take the value one and zero otherwise. If a firm is private foreign standalone then the dummy, D_PVT_FOR takes value one otherwise zero. LN(ASSET) is the log of total assets of the firm.

Variables All Firms Large Firms Small Firms Group Firms Indian Standalone Foreign Standalone

INTERCEPT 0.6103 (<.0001)

0.9979 (<.0001)

0.6602 (<.0001)

0.7241 (<.0001)

1.4736 (<.0001)

1.0004 (<.0001)

LEVERAGEt-1 -0.1396 (<.0001)

-0.1157 (<.0001)

-0.1668 (<.0001)

-0.1606 (<.0001)

-0.1105 (<.0001)

-0.2021 (<.0001)

(LEVERAGEt-1)2 0.0024 (<.0001)

0.0018 (<.0001)

0.0037 (<.0001)

0.0033 (<.0001)

0.0020 (<.0001)

0.0025 (0.0013)

PAY_OUTt-1 0.8781

(0.0609) -0.0083 (0.9933)

0.5878 (0.2577)

0.5399 (0.2794)

0.8481 (0.6080)

4.4517 (0.0211)

ROEt-1 0.3483

(<.0001) 1.1370

(<.0001) 0.3225

(<.0001) 0.2582

(<.0001) 0.9664

(<.0001) 0.4165

(0.0181)

(ROEt-1)2 0.0584 (<.0001)

0.1030 (<.0001)

0.0903 (<.0001)

0.0484 (<.0001)

0.2622 (0.0032)

0.0698 (0.0622)

LOG(ASSETt-1) -0.0177 (0.0751)

-0.0166 (0.5201)

-0.0003 (0.9850)

-0.0195 (0.0680)

0.0723 (0.0717)

0.0501 (0.2965)

D_PVT_IND 0.1071 (0.0133)

-0.1375 0.2501)

0.1384 (0.0029)

D_PVT_FOR 0.6224 (<.0001)

-0.0864 (0.7694)

0.6222 (<.0001)

R-Square 0.49 0.57 0.51 0.51 0.47 0.47

Adj. R-Square 0.49 0.56 0.50 0.50 0.43 0.42

F Value 113.77 32.40 97.31 100.14 11.78 11.46

N 4461 803 3657 3536 469 454

Table 4: Logit Model

(MBVR) is ratio of closing price of the equity to book value of equity at the end of the financial year. LEVERAGE is the ratio of total amount of long-term debt to total amount of equity capital. PAY_OUT is the ratio of total dividend to total earning of the firm. Return on equity (ROE) is the ratio of net profit to net worth of the firm. If firm is Indian standalone then the dummy, D_PVT_IND, take the value one and zero otherwise. If a firm is private foreign standalone then the dummy, D_PVT_FOR takes value one otherwise zero. ASSET total assets of the firm.

Variable All Firms Large Firms Small Firms Group Firms Indian Standalone

Foreign Standalone

INTERCEPT 2.7600 (<.0001)

4.2975 (<.0001)

3.6718 (<.0001)

2.8716 (<.0001)

3.3319 (0.0102)

1.7466 (0.0635)

LEVERAGEt-1 -0.4360 (<.0001)

-0.5412 (<.0001)

-0.5455 (<.0001)

-0.4940 (<.0001)

-0.2410 (0.0422)

-0.3466 (0.1855)

(LEVERAGEt-1) 2 0.0072 (<.0001)

0.0076 (<.0001)

0.0142 (<.0001)

0.0102 (<.0001)

0.0047 (0.1803)

-0.0109 (0.1208)

PAY_OUTt-1 0.1380

(0.9186) -3.3405 (0.3194)

-0.7560 (0.6159)

-0.5285 (0.7196)

3.5130 (0.4677)

-16.3592 (0.1716)

ROEt-1 0.7577

(0.0015) 2.4710

(0.0153) 2.0384

(<.0001) 0.6067

(0.0203) 1.4478

(0.2860) 5.3722

(0.0023)

(ROEt-1)2 0.1106 (0.0043)

0.2200 (0.0282)

1.9982 (<.0001)

0.0829 (0.0115)

10.9652 (0.0007)

20.3404 (0.0023)

LOG(ASSETt-1) 0.0079

(0.8062) -0.0644 (0.4948)

0.1003 (0.0558)

0.0171 (0.6258)

0.0842 (0.5473)

-0.2233 (0.3070)

D_PVT_IND 0.2314 (0.0755)

-1.0167 (0.0155)

0.4163 (0.0045)

D_PVT_FOR 1.1884 (<.0001)

-1.6773 (0.1886)

1.3467 (<.0001)

Log likelihood 1805.28 319.90 1369.90 1416.72 143.90 99.44

Likelihood Ratio 38.00 31.00 31.00 36.00 33.00 24.00

Annexure

Figure 1

Price-Book Value Ratio Trend

0

2

4

6

8

10

12

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Year

P-B

Rat

io

(PBVR) is ratio of closing price of the equity to book value of equity at the end of the financial year.

Figure 2

Leverage Trend

0

0.5

1

1.5

2

2.5

3

3.5

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Year

Leve

rage

LEVERAGE is the ratio of total amount of long-term debt to total amount of equity capital.

Figure 3

Dividend Payout trend

0

0.005

0.01

0.015

0.02

0.025

0.03

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Year

Div

eden

d Pa

yout

PAY_OUT is the ratio of total dividend to total earning of the firm.

Figure 4

ROE trend

0

0.05

0.1

0.15

0.2

0.25

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Year

RO

E

Return on equity (ROE) is the ratio of net profit to net worth of the firm.