do you know how assuris protects your clients? - ce corner ce revised aug 2017.pdf · 2 . take the...

TRANSCRIPT

CE MODULE: Understanding Assuris Protection

CE CREDITSThe Assuris Complimentary Continuing Education Course

for Financial Advisors is accredited for one credit hour by

Advocis, AIC, CSF, ICM and IIROC.

INSTRUCTIONSThis is a “read-and-learn” program. The examination component

is composed of 20 multiple-choice questions. The questions

are based on material found in the course. Certificates will

be issued electronically. After carefully reading this material, be

sure to visit www.cecorner.ca in order to take the examination.

LEARNING OBJECTIVESUpon successfully completing this course, financial advisors will be able to:1. Understand how Assuris protects a variety of insurance

benefits, including Death Benefit, Health Expense, Monthly

Income and Cash Value, as well as Accumulated Value

products offered through life insurance companies.

2. Describe to clients in simple terms how Assuris protects

their benefits.

3. Calculate Assuris protection for different benefits.

4. Provide clients with appropriate sources of information,

as well as know where to turn to get additional information

if required.

Assuris’ MissionAssuris’ mission is to protect policyholders if their life insurance company should fail.

AssurisIn the event that a life insurance company fails, Assuris protects policyholders by minimizing the loss of benefits and ensuring a quick transfer of policies to a solvent company, where their protected benefits will continue to be honoured.

Founded in 1990, Assuris is an independent, industry-funded not-for-profit compensation association, designated by the federal Minister of Finance under the Insurance Companies Act of Canada and specified in the Quebec Règlement d’application de la Loi sur les assurances.

Every life insurance company authorized to sell insurance policies in Canada is required, by the federal, provincial and territorial regulators, to become a member of Assuris. There are approximately 75 members. A complete member list is available at www.assuris.ca.

Do you know how Assuris protects your clients?If a life insurance company fails, financial advisors need to be

able to provide reassurance and peace of mind to their clients.

This continuing education (CE) module will help advisors gain the

knowledge to reassure their clients both at the point of sale and in

times of uncertainty.

2 TAKE THE QUIZ AT WWW.CECORNER.CA

Corporate StructureAssuris is governed by an independent Board of Directors. All directors serving on the Assuris’ board are independent of the members. Board directors are chosen for their knowledge and experience in the industry, as well as their professional expertise and their management of insolvencies.

Assuris’ corporate structure includes an Industry Advisory

Committee (IAC), consisting of seven representatives from the members; three representing Large Members and four representing Small Members. These represen-tatives are elected by the members at the Annual General Meeting.

The IAC provides an important link between the in-dependent Board of Directors and the members. The representatives are consulted on all strategic issues of importance to the industry.

Assuris’ FundingAssuris maintains a minimum Liquidity Fund level of100 million dollars with a target of 200 million dollars. This provides immediate cash to meet Assuris’ obligations in any future insolvency. In the event of a failure, Assuris will assess members for the necessary funds to cover the cost of providing Assuris protection to policyholders. Assuris’ assessment system has the financial capacity to raise sufficient funds to deal with any failure.

Past InsolvenciesThere have been four insolvencies in the life insurance industry in Canada. Working in

CE MODULE: UNDERSTANDING ASSURIS PROTECTION

partnership with regulators, the industry and the accounting and actuarial professions have been critical in developing Assuris’ expertise.

Shortly after Assuris came into being in 1990, we were called upon to deal with three insolvencies between 1992 and 1994. In addition to financial support, Assuris quickly developed expertise to resolve the unique and largely unprecedented issues in a life insurance company insolvency affecting Canadian policyholders. In those cases, all the Canadian policies were transferred to solvent life insurance companies.

In February 2012, the fourth insolvency occurred when Union of Canada Life Insurance was declared insolvent.

Union of Canada LifeOn February 2, 2012, Union of Canada Life Insurance sought court protection under the Winding-up and Restructuring Act (WURA). Assuris worked closely with the court-appointed liquidator, Grant Thornton Limited, to ensure policyholders were transferred to another life insurance company. Union of Canada Life Insurance had approximately 22,000 policies, 99% of which were fully covered by Assuris. Of the remaining 1% of policyholders who incurred some losses, all retained at least 95% of their benefits. Through this most recent insolvency, Assuris acquired additional experience in identifying risks and protecting life insurance policyholders.

Confederation LifeOn August 11, 1994, the liquidation of Confederation Life began. In Canada alone, it had obligations to 260,000 individual policyholders and another 1.5 million people who participated in group insurance plans. In the end, Assuris partnered with the regulator and the liquidator to leverage lessons learned in previous insolvencies. The result was full recovery for policyholders and a final cost to Assuris of only $5 million for expenses incurred.

Sovereign LifeOn January 18, 1993, a winding-up order was granted against Sovereign Life, based in Calgary. At the time, Sovereign Life had 249,000 policyholders, 96% of whom were 100% protected by Assuris coverage. Of the remaining 4% who incurred some loss, all retained at

Assuris will react quickly to minimize disruption to

policyholders and ensure that they are protected in

the event of a failure.

CE MODULE: UNDERSTANDING ASSURIS PROTECTION 3TAKE THE QUIZ AT WWW.CECORNER.CA

least 90% of their benefits. To facilitate transferring adjusted policy benefits to solvent life insurers, Assuris introduced the concept of proportional reinsurance. Assuris also established a life insurance company subsidiary to reinsure policy liabilities and maximize recoveries from the residual assets of Sovereign Life.

Les CoopérantsOn January 3, 1992, Les Coopérants, headquartered in Montreal, was ordered into liquidation under the Winding-up and Restructuring Act. At the time Les Coopérants was declared insolvent, it had individual insurance contracts with 222,000 policyholders and group insurance certificate holders numbering 600,000. To protect policyholder interests, Assuris successfully established the precedent that policyholders should receive priority in the liquidation of a life insurance company. Assuris’ support also included guaranteeing that all policyholder benefits would be fully protected.

Assuris is ReadyIn order to be prepared to protect policyholders of a failed company, Assuris has developed a resolution contingency plan. Assuris will react quickly to minimize disruption to policyholders and ensure that they are protected, in the event of a failure.

Assuris has also put in place a communications contin-gency plan that outlines the steps to reassure and provide information to policyholders if their life insurance company should fail. This includes having information ready and posted online on a life insurance company being declared insolvent. Financial advisors will also be able to download a sample letter from Assuris’ website to personalize and send to their clients.

DetectionOver the years, we have developed and strengthened

our detection of solvency risks. As a result, we have well-established detection processes, which are the key to identifying potentially troubled companies at an early stage. Each year, we receive from the members the same regulatory filings as received by the regulators.

These include:• annual regulatory filings• financial statements• the appointed actuary’s report• the Dynamic Capital Adequacy testing report

Through mutual trust and information sharing, Assuris works in partnership with federal and provincial regulators to identify a potentially troubled company at an early stage. This ensures minimal disruptions to policyholders in the event of a failure.

ResolutionAssuris’ mission is to protect policyholders if their life insurance company should fail. Assuris does not intervene or prevent potential insolvencies. Assuris’ aim is to assist the regulators with early intervention to ensure that policyholders are protected. In the event of a failure, Assuris works with the liquidator to ensure a timely transfer of policies.

Assuris protects policyholders by continuing their covered benefits under the original terms of the policy rather than by cancelling the policy and paying cash compensation. This avoids any interruption in the provision of benefits to the consumer. It also ensures that policyholders who may no longer be insurable retain their benefits.

Assuris protects policyholders by continuing their covered benefits under

the original terms of the policy.

What You Need To Know • Policyholders are protected by Assuris • Where to get more information

4 CE MODULE: UNDERSTANDING ASSURIS PROTECTION TAKE THE QUIZ AT WWW.CECORNER.CA

Assuris ProtectionInsurance ProductsInsurance companies are constantly introducing new products. Instead of having to determine how the protection would apply for each specific product, Assuris protection is applied to the guaranteed benefits.

If a member fails, Assuris works with the liquidator to transfer the policies to a solvent company. Assuris guarantees that policyholders will retain at least 85% of the insurance benefits they were promised.

Insurance benefits include: • Death Benefit• Health Expense• Monthly Income• Cash Value, including Segregated

Fund Guarantees

Deposit-Type ProductsDeposit-type products are also transferred to a solvent company. For these products, Assuris guarantees that policyholders will retain 100% of their Accumulated Value up to $100,000. Deposit-type products include accumulation annuities, universal life overflow accounts, Guaranteed Interest Annuities (GIAs) (or Guaranteed Investment Certificate [GIC] type products) and dividend deposit accounts.

Adding Benefits TogetherAssuris protection is applied to all benefits of a similar type. For policyholders with more than one policy with the failed company, all similar benefits are added together before Assuris protection is applied.

Assuris provides separate protection for individual, group, registered and non-registered benefits, individual Tax-Free Savings Accounts (TFSAs) and group TFSAs.

The chart below is available at www.assuris.ca. It can be a great resource when you explain to your clients how their policies are protected.

Benefits Protection

or

85%whichever is higher

Death Benefits $200,000

Health Expense $60,000

Monthly Income $2,000/month

Cash Values $60,000

Benefit Protection

Accumulated Value up to $100,000

IndividualRegistered

IndividualNon-Registered

GroupRegistered

GroupNon-Registered

Individual Tax-Free Savings Account

Group Tax-Free Savings Account

Death Benefit x x

Health Expense x x

Monthly Income x x x x

Cash Values x x x x

Accumulated Values x x x x x x

CE MODULE: UNDERSTANDING ASSURIS PROTECTION 5TAKE THE QUIZ AT WWW.CECORNER.CA

Structure of ProtectionAssuris protection applies separately to each member. To be eligible for Assuris protection, the policy must be issued from a member in Canada to a Canadian citizen or resident. At the time of failure, the policy needs to be in force. Please note that Fraternal Benefit Societies are not members of Assuris.

When checking the list of members on the Assuris website, it is important to look for the company that has underwritten the policy and not the brand names.

For benefits unique to the life insurance industry, Assuris protection applies regardless of the value of the policy. For example, a policy with a $1,000,000 death benefit, on transfer, would be protected for $850,000 (85% of $1,000,000).

CurrencyPolicies are protected regardless of the currency. For example, a Canadian policy issued in U.S. dollars is protected by Assuris in the event of a failure. The policy would simply be converted to Canadian dollars.

HOW ASSURIS PROTECTION WORKSBenefits ProtectedAssuris protection applies to the benefits under products issued by a member, including:

Insurance Products• Life Insurance• Critical Illness• Health Expense

• Disability Income• Long-Term Care• Annuities

Deposit Type Products• Accumulation Annuities • TFSAs

Assuris protection also applies to guaranteed amounts under individual segregated funds policies.

Four Steps to Determine Protection1. CONFIRM YOUR CLIENT’S POLICY

WAS ISSUED IN CANADA BY A MEMBER.Assuris protection applies separately to each

member, regardless of its affiliation with

another member.

2. CONFIRM YOUR CLIENT WAS A CANADIANCITIZEN OR RESIDENT WHEN THE POLICY WASISSUED AND THAT THE POLICY IS STILL IN FORCE.

3. IDENTIFY YOUR CLIENT’S GUARANTEED BENEFITSAND APPLY THE APPROPRIATE PROTECTION.For benefits unique to the life insurance industry,

Assuris guarantees that policyholders will

recover at least 85% of their promised benefits.

Below certain dollar values, Assuris provides

100% protection.

For accumulated value benefits, Assuris

guarantees that policyholders will recover

100% of their promised benefits up to $100,000.

4. ADD TOGETHER ALL SIMILAR BENEFITS.Assuris provides separate protection for individual,

group, registered and non-registered benefits,

individual Tax-Free Savings Accounts (TFSAs)

and group TFSAs.

Assuris protection is applied to all benefits of a

similar type. For policyholders with more than

one policy with the failed company, all similar

benefits are added together before Assuris

protection is applied.

Refer to the last table on page 4 to help

understand how benefits are added together.

6 CE MODULE: UNDERSTANDING ASSURIS PROTECTION TAKE THE QUIZ AT WWW.CECORNER.CA

Their advisor sat down with them and told them about Assuris. He then illustrated for them what their protection would be on Janet’s term policy of $300,000 in the event their life insurance company failed.

Janet and Craig felt better knowing the policy was protected.

Whole Life A few years later, Janet and Craig bought a house and were doing well in their respective careers. One day, Janet came home to tell Craig that they were going to be parents. After sharing the news with their close friends and family, they called their financial advisor to look over their finances. With the help of their advisor, they decided to buy a whole-life policy with a death benefit of $500,000. After a few years, the cash value of the whole-life policy had built up to $20,000.

Payout Annuity When Janet’s mother and father moved to a nursing home, Janet and Craig helped them buy a payout annuity to help supplement their income.

For quarterly or annual payments, the protection is proportional (e.g., annual payments are protected at $24,000 per year or 85%, whichever is higher, and quarterly payments are protected at $6,000 per quarter or 85%, whichever is higher).

Meet Janet and CraigLet’s look at an example of a couple and their insurance products. Janet and Craig met in university and married shortly after Janet graduated.

Term LifeBeing responsible, they decided to get a term-life insurance policy for Janet, as Craig was finishing his master’s degree and dependent on Janet’s income. While on their honeymoon, they met a couple who was talking about the failure of an insurance company in the U.S.

When they got back, they contacted their financial advisor to find out if they should be worried about their life insurance company in Canada.

TERM-LIFE DEATH BENEFIT

PAYOUT ANNUITY MONTHLY INCOME BENEFIT

Sum Insured Assuris Protection Adjusted Benefit

$300,000 $200,000or 85%whichever is higher

$255,000

Sum Insured Assuris Protection Adjusted Benefit

$500,000Death Benefit

$200,000or 85%whichever is higher

$425,000

$20,000Cash Value

Under $60,000the Cash Value is fully protected

$20,000Cash Value

Payment Assuris Protection Adjusted Benefit

$3,000/mth $2,000/mth

or 85%whichever is higher

$2,550

WHOLE-LIFE DEATH BENEFIT & CASH VALUE BENEFIT

CE MODULE: UNDERSTANDING ASSURIS PROTECTION 7TAKE THE QUIZ AT WWW.CECORNER.CA

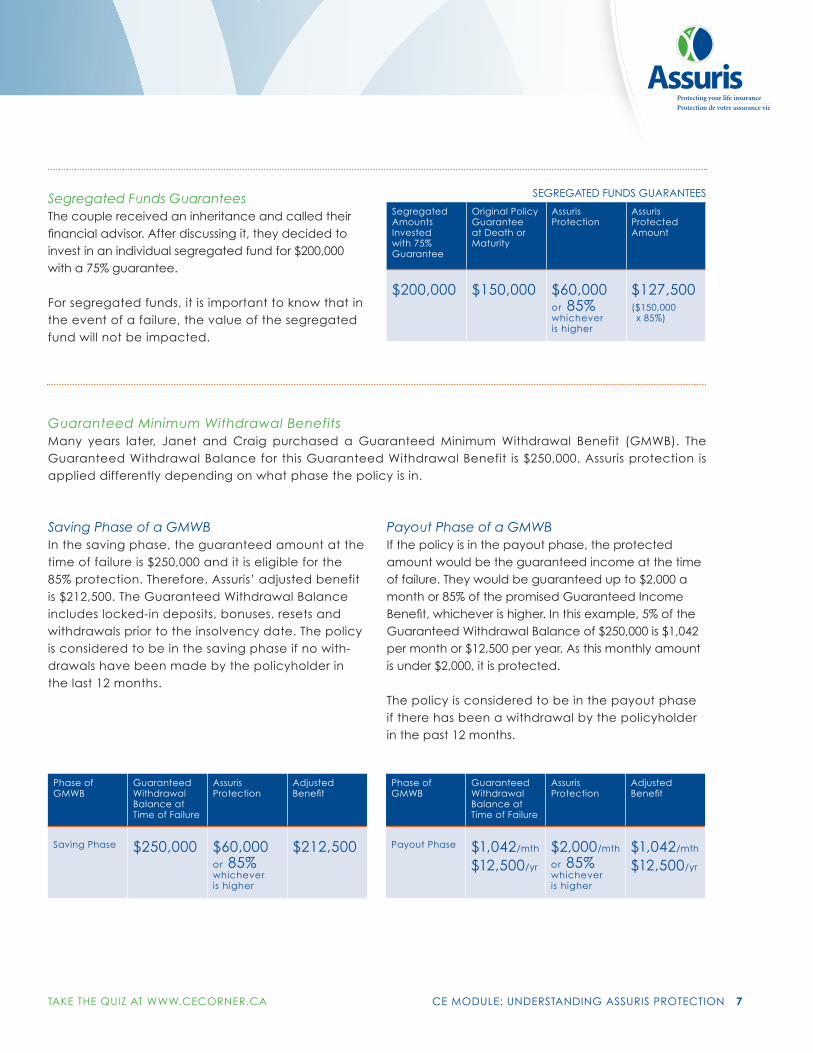

Saving Phase of a GMWBIn the saving phase, the guaranteed amount at the time of failure is $250,000 and it is eligible for the 85% protection. Therefore, Assuris’ adjusted benefit is $212,500. The Guaranteed Withdrawal Balance includes locked-in deposits, bonuses, resets and withdrawals prior to the insolvency date. The policy is considered to be in the saving phase if no with-drawals have been made by the policyholder in the last 12 months.

Payout Phase of a GMWBIf the policy is in the payout phase, the protected amount would be the guaranteed income at the time of failure. They would be guaranteed up to $2,000 a month or 85% of the promised Guaranteed Income Benefit, whichever is higher. In this example, 5% of the Guaranteed Withdrawal Balance of $250,000 is $1,042 per month or $12,500 per year. As this monthly amount is under $2,000, it is protected.

The policy is considered to be in the payout phase if there has been a withdrawal by the policyholder in the past 12 months.

Segregated Funds Guarantees The couple received an inheritance and called their financial advisor. After discussing it, they decided to invest in an individual segregated fund for $200,000 with a 75% guarantee.

For segregated funds, it is important to know that in the event of a failure, the value of the segregated fund will not be impacted.

Guaranteed Minimum Withdrawal BenefitsMany years later, Janet and Craig purchased a Guaranteed Minimum Withdrawal Benefit (GMWB). The Guaranteed Withdrawal Balance for this Guaranteed Withdrawal Benefit is $250,000. Assuris protection is applied differently depending on what phase the policy is in.

Segregated Amounts Invested with 75% Guarantee

Original Policy Guarantee at Death or Maturity

AssurisProtection

AssurisProtected Amount

$200,000 $150,000 $60,000or 85%whichever is higher

$127,500($150,000 x 85%)

Phase of GMWB

Guaranteed Withdrawal Balance at Time of Failure

AssurisProtection

Adjusted Benefit

Saving Phase $250,000 $60,000or 85%whichever is higher

$212,500

Phase of GMWB

Guaranteed Withdrawal Balance at Time of Failure

AssurisProtection

Adjusted Benefit

Payout Phase $1,042/mth

$12,500/yr

$2,000/mth

or 85%whichever is higher

$1,042/mth

$12,500/yr

SEGREGATED FUNDS GUARANTEES

8 CE MODULE: UNDERSTANDING ASSURIS PROTECTION TAKE THE QUIZ AT WWW.CECORNER.CA

Visit Assuris’ Continuing Education website at www.cecorner.ca to take the quiz and receive one credit hour.

Accumulation Annuities (Deferred Annuities)Janet and Craig each purchase accumulation annuities ($75,000 and $125,000 respectively). All accumulation annuities were purchased with the same member. These are protected under Assuris’ Accumulated Value protection. On transfer, Assuris guarantees that policy-holders will retain 100% of the Accumulated Value up to $100,000. Janet’s policy is for $75,000; she is fully protected. Craig’s policy is for $125,000 and is there-fore protected for $100,000.

They also purchase a joint accumulation annuity from the same member for $50,000. However, the joint accumulation annuity is split evenly between each policyholder and added to the value of their individual benefits before Assuris protection is applied.

ACCUMULATED VALUE BENEFITS

JOINT DEFERRED ANNUITY

Example Accumulated Value

AssurisProtection

Protected Amount

Janet’s Policy $75,000 $100,000 $75,000

Craig’s Policy $125,000 $100,000 $100,000

Example Accumulated Value

AssurisProtection

Adjusted Benefit

Janet’s Policy $75,000under

$100,000fully protected

$75,000

Craig’s Policy $125,000 $100,000 $100,000

Joint Policy between Janet and Craig

$50,000split evenly

Janet’s policies=$100,000 ($75,000 + $25,000)

Craig’s policies=$150,000($125,000 + $25,000)

$100,000per policyholder

Janet

$100,000fully protected

Craig

$100,000

Talking to your clients about Assuris...As a financial advisor, part of helping your clients

build their overall financial plan includes a discussion

about their insurance options. It is also important to

help them become informed consumers by advising

them of the protection provided by Assuris.

Stay Informed• Assuris’ website provides the most complete, accurate and up-to-

date descriptions of Assuris protection. Visit www.assuris.ca.

• Assuris provides a free, bilingual brochure, which outlines basic

protection information. The brochure can be downloaded and

printed from the website (www.assuris.ca) or by emailing Assuris

to receive printed copies by mail.

• Email Assuris at [email protected].

• Follow us on Twitter: @Assuris

• Assuris’ Information Centre (toll-free: 1-866-878-1225) can answer any questions you or the client may have.