documentary credit.docx

DESCRIPTION

Documentary Credit.docxTRANSCRIPT

Letter of Credit

Introduction

Banks, as we know, lend money to the public, for various purposes. Like

purchase of a home, a car, or other consumer durables etc. They also extend loans to

Industries that manufacture various goods, and machineries, and also to service

industries that provide various services, like a salon, internet kiosk, etc., to the

community.

Banks play a vital role in the development process of any nation, by providing

finance for different activities related to trade and commerce. This includes both

domestic and international trade and commerce.

One of the ways in which commercial banks facilitate international trade and

commerce, is by way of extending a non funded financing facility or mechanism

called the Documentary Credit (DC), or the Letter of Credit (LC).

This mechanism to facilitate international trade was developed under the

auspices of the International Chamber of Commerce, Paris. The rules and regulations

etc., governing the Documentary Credits, and the transactions there under, are

contained in what is known as the Uniform Customs and Practices for Documentary

Credits.

1 | P a g e

Letter of Credit

Meaning

Documentary Credit is an International trade procedure in which the credit

worthiness of an importer is substituted by the guarantee of a bank for specific

transaction. Under documentary credit arrangement (also called as letter of credit

arrangement) a bank (usually in the importer’s country) undertakes to pay for a

shipment, provided the exporter submits the required documents (such as clean bill of

lading, certificate of insurance, certificate of origin) within a specific period.

Definition

A Documentary Credit (DC), or Letter of Credit (LC), (they are one and the

same), is a legally binding undertaking given by a Bank on behalf of its customer, in

favor of a third party, to make payment to him (the third party), the stated sum of

money against submission of the required documents, as per the terms of the

Documentary Credit.

2 | P a g e

Letter of Credit

Mechanism of Letter of Credit

Letter of Credit is usually subject to the Uniform Customs and Practice for

Documentary Credits, International Chamber of Commerce Publication No. 600

(UCP 600).The mechanism of letter of credit is as follows :

1. Availability of Letter of Credit

Under UCP 600, an LC can be made available with:

a. Payment

Payment at sight against compliant documents.

b. Negotiation

Payment with or without recourse to the beneficiary or bona

fide holder against compliant documents presented under the credit.

c. Acceptance by a Drawee Bank

Payment at a future determinable date against compliant

documents. A tenor draft is normally required for presentation under

an acceptance credit and is drawn on the acceptance bank rather than

the issuing bank.

d. Usance Credit

Payment at a future determinable date against compliant

documents. A tenor draft is normally required (but not mandatory) for

presentation under a usance credit and is drawn on the Issuing Bank.

Usance credit is available by Negotiation, Acceptance and Deferred

3 | P a g e

Letter of Credit

Payment. A tenor draft is not required for presentation under a deferred

payment credit.

2. Parties in Letter of Credit Transaction

a. LC Applicant:

LC Applicant is normally the buyer under the sales contract and

the party that initiates the request to the Issuing Bank to issue an LC on

its behalf. The LC Applicant normally maintains banking facilities

with the Issuing Bank.

b. LC Beneficiary:

LC Beneficiary is normally the seller under the sales contract

and the party who will receivepayment under the LC if it can fulfill all

the terms and conditions of the credit.

c. Issuing Bank:

An Issuing Bank (or LC opening bank) is the bank that issues

the LC in favour of a seller at the request of the LC applicant. The

Issuing Bank is normally located in the applicant’s country with

established banking relationship with the applicant.

By issuing an LC, the Issuing Bank undertakes to pay the

beneficiary the value of the draft and/or other documents if all the

terms and conditions of the LC are complied with.

d. Advising Bank

An Advising Bank (or sometimes known as notifying bank) is

the bank that advises the LC beneficiary that there is an LC issued in

his favour. Advising Bank is normally located in the seller’s country

4 | P a g e

Letter of Credit

and is either appointed by the Issuing Bank or LC applicant. Its

primary responsibility is to authenticate the LC to ensure that the LC

comes from genuine source.

e. Confirming Bank:

A Confirming Bank (normally also the Advising Bank) is the

bank that adds its own undertaking to pay the LC beneficiary if all

terms and conditions of the credit are complied with. Such undertaking

is in addition to that given by the Issuing Bank at the request of the

Issuing Bank.

The Confirming Bank will only confirm an LC upon

satisfactory evaluation on the conditions of the Issuing Bank and its

domicile country.

f. Nominated Bank:

A Nominated Bank is a bank authorised by the Issuing bank in

the credit to pay, negotiate, issue a deferred payment undertaking or

accept drafts under the LC. If the LC does not specify a Nominated

Bank, the LC is deemed as freely negotiable and any banks that receive

documents from the LC beneficiary are qualified to be a Nominated

Bank.

A Nominated Bank is not responsible to pay under the credit

unless it has added its confirmation to the credit. In such a case, it will

become a Confirming Bank.

g. Negotiating Bank:

A Negotiating Bank is the bank that examines the drafts and/or

documents presented by the LC beneficiary and gives values to such

drafts and/or documents. Negotiation could be in the form of

5 | P a g e

Letter of Credit

Purchasing or agreeing to purchase the drafts and/or documents

presented.

h. Reimbursing Bank:

A Reimbursing Bank is the paying agent appointed by the

Issuing Bank to honour claims submitted by the nominated or

negotiating bank.

6 | P a g e

Letter of Credit

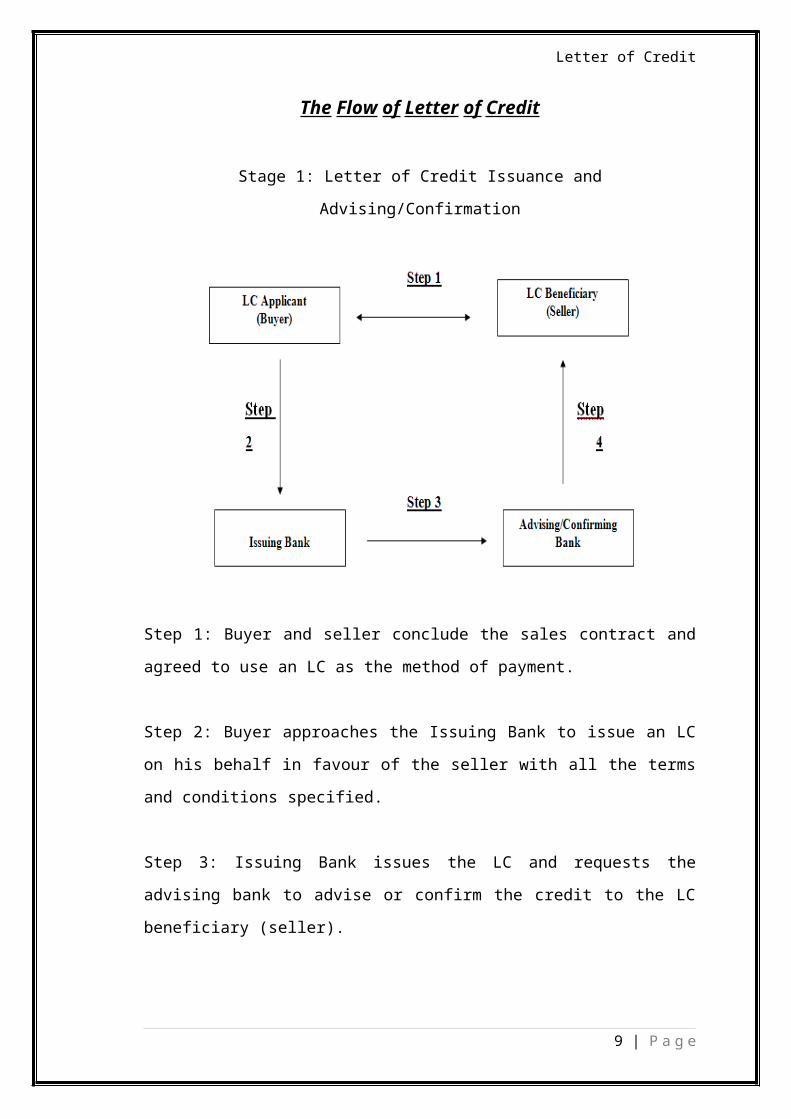

The Flow of Letter of Credit

Stage 1: Letter of Credit Issuance and Advising/Confirmation

Step 1: Buyer and seller conclude the sales contract and agreed to use an LC as the

method of payment.

Step 2: Buyer approaches the Issuing Bank to issue an LC on his behalf in favour of

the seller with all the terms and conditions specified.

Step 3: Issuing Bank issues the LC and requests the advising bank to advise or

confirm the credit to the LC beneficiary (seller).

Step 4: Advising/confirming bank authenticates the LC and sends the LC to the LC

beneficiary.

7 | P a g e

Letter of Credit

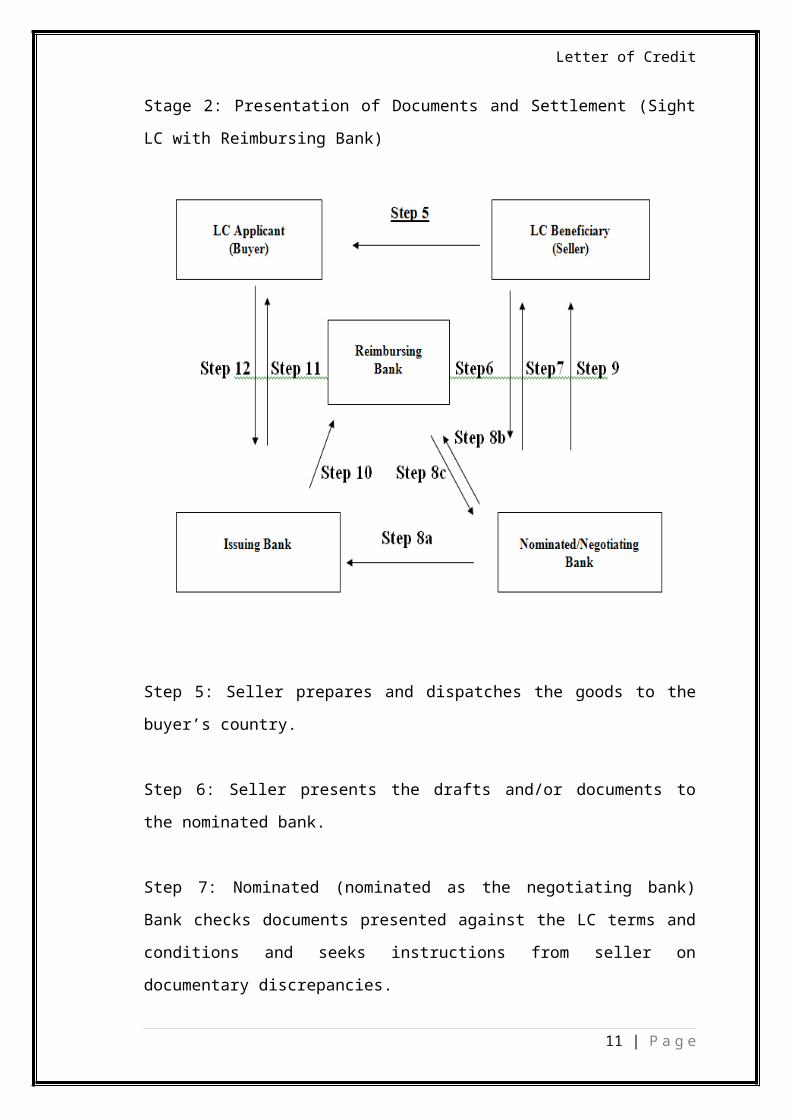

Stage 2: Presentation of Documents and Settlement (Sight LC with Reimbursing

Bank)

Step 5: Seller prepares and dispatches the goods to the buyer’s country.

Step 6: Seller presents the drafts and/or documents to the nominated bank.

Step 7: Nominated (nominated as the negotiating bank) Bank checks documents

presented against the LC terms and conditions and seeks instructions from seller on

documentary discrepancies.

Step 8a: Nominated Bank forwards the drafts and/or documents to the Issuing Bank.

Step 8b: If documents are free from discrepancies or discrepancies are supported by

seller’s indemnity, nominated bank claims reimbursement from the appointed

reimbursing bank.

8 | P a g e

Letter of Credit

Step 8c: Reimbursing Bank pays the nominated bank against a valid reimbursement

authority received from the Issuing Bank and statement from negotiating bank that the

documents complied with LC terms.

Step 9: Nominated Bank credits the net proceeds into the seller’s account.

Step 10: Issuing Bank checks documents presented against the LC terms and

conditions. If documents are free from discrepancies, Issuing Bank reimburses the

reimbursing bank.

Step 11: Issuing Bank presents documents to the buyer for payment.

Step 12: Once payment is received from the buyer, Issuing Bank releases documents

to the buyer for the latter to collect his goods.

9 | P a g e

Letter of Credit

Essentials of Letters of Credit

1. Inexpensive means of payment in domestic and international trade

Letters of credit (L/C) have long served as a convenient, inexpensive

means of payment in domestic and international trade. L/Cs may serve as

guaranties, securing performance obligations with a bank,s commitment to pay

upon presentation of a draft, default notice or other documents specified by the

L/C. L/Cs have long been governed by Article 5 of the Uniform Commercial

Code. The L/C is intended to assure the vendor of payment before the goods

leave its warehouse.

2. What is a Letter of Credit?

An L/C may be broadly defined as an undertaking by an issuer, the

bank, to pay a third party, the vendor who is the beneficiary for the account of

the banks customer, the debtor, when the vendor submits documents specified

by the L/C. If the vendor submits proper documents before the credit expires,

the bank will pay the L/C, and the debtor must reimburse the bank. An L/C

may be either revocable or irrevocable. An irrevocable L/C can be modified

only with the consent of the vendor. A revocable L/C can be modified by the

bank without the vendors consent. L/C s come in two varieties: commercial

L/Cs, commonly used to pay for goods, and "standby L/Cs, which secure

performance by assuring payment after default. Under either type, the credit of

the bank is substituted for the credit of the debtor in favor of the vendor.

3. Essential Principles Governing Law

Within the United States, Article 5 of the Uniform Commercial Code

(UCC) governs L/Cs. Article 5 is founded on two principles: (1) the L/C,s

independence from the underlying business transaction, and (2) strict

compliance with documentary requirements.

10 | P a g e

Letter of Credit

4. The Independence Doctrine

L/Cs are purely documentary transactions, separate and independent

from the underlying contract between the debtor and the vendor. The bank

honoring the L/C is concerned only to see that the documents conform with

the requirements in the L/C. If the documents conform, the bank will pay, and

obtain reimbursement from the debtor. The bank need not look past the

documents to examine the underlying sale of merchandise. The letter of credit

is independent from the underlying transaction and, except in rare cases of

fraud or forgery, the issuing bank must honor conforming documents. Thus,

vendors are given protections that the issuing bank must honor its demand for

payment (which complies with the terms of the L/C) regardless of whether the

goods conform with the underlying sale contract.

5. Strict Compliance

The bank may insist upon strict compliance with the requirements of

the L/C. In the absence of conformity with the L/C, the vendor cannot force

payment and the bank pays at its peril. The question remains, how strict

compliance? Some courts insist upon literal compliance, so that a misspelled

name or typographical error dooms the vendors demand for payment. Other

courts require payment upon substantial compliance with documentary

requirements. Careful vendors should remember that the bank may insist upon

strict compliance with all documentary requirements. If the documents do not

conform, the bank should give the vendor prompt, detailed notice, specifying

all deficiencies.

11 | P a g e

Letter of Credit

Forms of Letters of Credit

1. Commercial Letters of Credit

This form of L/C is commonly used when the contract involves sale of

goods. Many exporters require payment by letter of credit. Typically, the

buyer applies to his bank, which opens a letter of credit in favor of the

exporter, payable upon presentation of the sellers draft, bill of lading and other

shipping documents specified in the credit. When the goods are shipped, the

seller delivers those documents to the bank and collects full payment. The

bank holds the documents and usually takes a security interest, pending

reimbursement by its customer, the buyer. The transaction involves three

relationships: (1) the letter of credit, which obligates the bank to pay the

beneficiary upon presentation of the documents; (2) the reimbursement

agreement between the bank and its customer, which obligates the beneficiary

to reimburse the bank and pay a fee; and (3) the underlying contract for the

sale of goods.

2. Standby Letters of Credit

A standby L/C is customarily used in non-sales transactions. This form

of L/C assures payment in case of nonperformance. Under the commercial

L/C, the vendors right to payment is conditioned upon submitting certain

documents; with standby L/Cs, a vendor draws down on the L/C only when

the vendor establishes that the debtor has defaulted. For the commercial L/C,

payment is expected; for the standby L/C, payment should be the exception.

12 | P a g e

Letter of Credit

The Parties, Rights and Obligations

1. Issuing Bank

When an issuer receives a draft and demand for payment, it must

decide to honor or dishonor within three banking days under the UCC. The

bank must examine the documents with reasonable care. If the documents

conform, the bank must pay, and be reimbursed by its customer, the debtor.

Failure to honor within three banking days constitutes dishonor. If the

documents do not conform, the bank should give the beneficiary prompt,

detailed notice, specifying all deficiencies.

2. Vendor

The vendor is entitled to payment upon submission of proper

documents. By presenting its draft and demand for payment, the vendor

represents that all conditions of the L/C have been complied with.

3. Debtor

The debtor must reimburse the bank when the bank honors conforming

drafts and demands, i.e. the debtor unconditionally agrees to reimburse the

bank.

13 | P a g e

Letter of Credit

Types of Letter of Credit

Import/export Letter of Credit

It is said to the credit which buyer assigns i so that he imports a

product to his own country and in general this credit is in another country and

its value is export value.

Revocable Letter of Credit

In this type of credit buyer and the bank which has established the LC,

are able to manipulate the letter of credits or make any kinds of corrections

without informing the seller and getting permissions from him. This type of

LC is not used a lot.

Irrevocable LC

In this type of LC, any kinds of change and manipulations from the

buyer part and the establisher bank require the permission and satisfaction of

seller part. According to the last rules of international business room, return

ability or none return ability, the credit will be none returnable.

Confirmed LC

They are the guaranties that buyer will be given so that, the buyer will

give the guaranty from his own bank to any other valid bank that the seller

will desire it.

Unconfirmed LC

This type of letter of credit, does not acquire the other bank's confirmation.

14 | P a g e

Letter of Credit

Transferrable LC

It is said to the credit that the seller can give a part or parts of credit

(Completely) to the person or persons he decides. This type of credit is a

benefit for seller.

Untransferable LC

It is said to the credit that seller cannot give a part or completely right

of assigned credit to somebody or to the persons he wants. In international

commerce, it is required that the credit will be untransferable.

Usance LC

It is kind of credit that won't be paid and assigned immediately after

checking the valid documents but paying and assigning it requires an indicated

duration which is accepted by both of the buyer and seller. In reality, buyer

will give an opportunity to the seller to pay the required money after taking the

related goods and selling them.

At Sight LC

It is a kind of credit that the announcer bank after observing the

carriage documents from the seller and checking all the documents

immediately pays the required money.

Red Clause LC

In this kind of credit assignment seller before sending the products can

take the pre-paid and parts of the money from the bank. The first part of the

credit is to attract the attention acceptor bank. The reason why it named so, is

that the first time this credit is established by the assigner bank, to take the

attention of the offered bank, the terms and conditions were written by red ink,

from that time it became famous with that name.

15 | P a g e

Letter of Credit

Back to Back LC

In this type of LC consisted of two separated and different types of LC.

First one is established in the benefit of the seller that is not able to provide the

corresponding goods for any reasons. Because of that reason according to the

credit which is opened for him, neither credit will be opened for another seller

to provide the desired goods and sends it.

Back-to-back L/C is a type of L/C issued in case of intermediary trade.

Intermediate companies such as trading houses are sometimes required to open

L/Cs by supplier and receive Export L/Cs from buyer. SMBC will issue a L/C

for the intermediary company which is secured by the Export L/C (Master

L/C). This L/C is called "Back-to-back L/C".

16 | P a g e

Letter of Credit

ICC’s New Rules on Documentary Credits

ICC’s new rules on documentary credits, which are used for letter of credit

transactions worldwide, were approved by the ICC Commission on Banking

Technique and Practice on 25 October 2006. UCP 600 is the first revision of the rules

since 1993 and represents more than three years of work by the commission. The

implementation date is 1 July 2007.

UCP 600 contains significant changes to the existing rules, including:

A reduction in the number of articles from 49 to 39;

New articles on “Definitions” and “Interpretations” providing

more clarity and precision in the rules;

A definitive description of negotiation as “purchase” of drafts of documents;

The replacement of the phrase “reasonable time” for acceptance or refusal of

documents by a maximum period of five banking days.

UCP 600 also includes the 12 Articles of the eUCP, ICC’s supplement to the

UCP governing presentation of documents in electronic or part-electronic form.

The UCP were first published by ICC in 1933. Revised versions were issued

by the ICC in 1951, 1962, 1974, 1983 and 1993. Written into virtually every letter of

credit, the UCP are accepted worldwide. They are the most successful private rules

for trade ever developed and illustrate the importance ICC attaches to self-regulation.

Following the sell-out event in October this year, Understanding the UCP 600,

presented by Chair of the UCP 600 Drafting Group Gary Collyer, will take place on

26 January, at the Prince de Galles hotel, Paris.

17 | P a g e

Letter of Credit

Role of UPC 600 for Documentary Credits

UCP 600 is the latest version of the rules that govern letters of credit

transactions worldwide. UCP 600 is prepared by International Chamber of

Commerce’s (ICC) Commission on Banking Technique and Practice. Its full name is

2007 Revision of Uniform Customs and Practice for Documentary Credits, UCP 600,

and (ICC Publication No. 600). The ICC Commission on Banking Technique and

Practice approved UCP 600 on 25 October 2006. The rules have been effective since

1 July 2007.

UCP 500 was the rules that had been in implementation before UCP 600.

There are several significant differences exist between UCP 600 and UCP 500. Some

of these differences are as follows;

• The number of articles reduced from 49 to 39 in UCP 600;

• In order to reach a standard meaning of terms used in the rules and prevent

unnecessary repetitions two new articles have been added to the UCP 600.

These newly added articles are Article 2 “Definitions” and Article 3

“Interpretations”. These articles bring more clarity and precision in the rules;

• A definitive description of negotiation as “purchase” of drafts of documents;

• New provisions, which allow for the discounting of deferred payment credits;

• The replacement of the phrase “reasonable time” for acceptance or refusal of

documents by a maximum period of five banking days.

The Uniform Customs and Practice for Documentary Credits (UCP 600)

establishes an international standard of letter of credit practice. This set of rules for

the issuance and use of Letters of Credit for bankers went into effect July 1, 2007 in

consultation with bankers, the International Chamber of Commerce and other

interested parties from around the world. In other words, UCP 600 are the latest

revision of the Uniform Customs and Practice that govern the operation of letters of

credit. Historically, the UCP have been revised about every ten years to keep up with

changing business and banking practices as well as changes in technology.

18 | P a g e

Letter of Credit

Although the UCP defines rights and obligations of the various parties in a

letter of credit transaction, it is not law and any given letter of credit is subject to the

UCP only to the extent indicated in the letter of credit itself. The latest revision of

UCP is the sixth revision of the rules since they were first promulgated in 1933. The

current version is the result of year of effort by the International Chamber of

Commerce's Commission on Banking Techniques and Practices.

History of UCP

First uniform rules published by ICC in 1933. Revised versions were issued in

1951, 1962, 1974, 1983 and 1993.

1933 – Uniform Customs and Practice for Commercial Documentary Credits

1951 Revision - Uniform Customs and Practice for Commercial Documentary Credits

1962 Revision - Uniform Customs and Practice for Documentary Credits

1974 Revision – Uniform Customs and Practice for Documentary Credits

1983 Revision – Uniform Customs and Practice for Documentary Credits

1993 Revision – Uniform Customs and Practice for Documentary Credits

Currently majority of letters of credit issued everyday is subject to latest

version of the UCP. This widely acceptance is the key sign that shows the importance

of the UCP, which are the most successful private rules for trade ever developed.

19 | P a g e

Letter of Credit

Legal Acts Regulating the Payment by Documentary Credit

The advantage of payment by documentary credit over other forms of payment

on the basis of an analysis of its main features and some issues that surround it. The

success of the application of payment by credit is directly linked to the level of the

development of its respective legal framework. International payment relations

areregulated both by normative acts of certain states as well as customs and practices

in business dealings. Moreover, the universality of banking operations causes the

unification of international payment. To this end the International Chamber of

Commerce elaborated “The Uniform Customs and Practice for Documentary Credits”

(hereinafter referred as Uniform Customs and Practice). This entered into force on 1

January 1994. It is a reflection of the progressive achievements made in the payment

relations of the banking sector. The latter caused the wide application of this form of

payment in export-import operations.

Despite the fact that Uniform Customs and Practice has a recommending

nature and represents the unofficial codification of the rules for business, a majority of

banks throughout the world carry out payment by documentary credit. It should also

be noted that the Uniform

Customs and Practice serves as a basis for relevant national legislation in many

countries. The Uniform Customs and Practice provides the definition of the credit and

determines its type, rules and means of its application, obligations and the liability of

banks. It also lays down the requirements of the documents presented on the basis of

credit as well as the rules on their presentation. If a bank applies the Uniform Customs

and Practice then the provisions there from are considered binding both for the bank

and the clients. The legal framework for payment by credit is Article 876 of the Civil

Code. It provides only the definition of the documentary (commercial) credit, but it

has been supplemented by “the Rules of Georgia on Non-Cash Payment” approved by

Order No. 220 of the President of the National Bank of Georgia of 2 September,

1999.5 These rules stipulate the following forms of payment: payment orders, credits,

payment-collection orders, cheques and collection order. Another legal act regulating

payment relations is the “Interim Instruction on Opening the Settlement,

Correspondent, Currency, Budgetary, Current and other Accounts (Temporary, Cash

Service) in the Banking Institutions of Georgia” approved by Order No. 222 of the

20 | P a g e

Letter of Credit

President of the National Bank of Georgia of 2 September 1999. We should

distinguish between forms of payment and settlement documents. The latter can have

the same designation as a respective form of payment (e.g. a payment order, credit or

cheque), although they have an accounting and informational function.

21 | P a g e

Letter of Credit

Legal Construction of Payment by the Credit

According to the Civil Code of Georgia, by opening a credit, the credit

institution (issuing bank) undertakes, at the request and instruction of a customer (the

purchaser of credit), to pay the money to a third person (the remittent8 ) under the

order of this person against a said document, or pay drafts presented by a remittent,

accept drafts, or assign another bank with this transaction, if the credit terms are

fulfilled. The customer undertakes to pay the agreed commission. Thus, a

documentary credit is a bank’s fixed obligation to pay to the buyer a definite sum of

money within an agreed time frame (or authorise another bank (the nominated bank)

to make such payment), in the case of the timely presentation of appropriate

documents, certifying the shipment of cargo (the rendering of service) and the exact

fulfilment of the terms of the credit. For making payments by credit it is not the

movement of goods as such but more the documents that bear the principal

importance. It is according to the documentation that the control over the movement

of goods, works or services is carried out.

The payment operation on the basis of documentary credit can be described as

follows:

1. The form of payment for the supplied goods (rendered service) shall be

defined in the contract between the exporter and the importer. If the payment

is made on the basis of documentary credit, the parties determine the type of

credit, the expiry date and the place of its fulfilment, the authorised banks etc.;

2. At the request and instruction of a customer (creditor), the issuing bank shall

open the credit. The application on opening the credit shall include

information such as the name of a remittent and the amount of the credit; the

place and means for its use; goods on paying of which the credit was opened;

documentation to be presented to the bank; the expirydate for shipment and

the presentation of documentation;

3. The next stage is to notify the exporter by sending an advice that the credit is

open. Further more the issuing bank sends the credit (advice, notification on

22 | P a g e

Letter of Credit

the opening of the credit) to the exporter, usually through a service bank

(advising bank) of an exporter, which in its turn carries out the notification

procedure;

4. The advising bank retains a copy of the advice because it is authorised to

receive from the exporter documents stipulated by the credit and to carry out

an examination of them. The advising bank at the same time may be

categorized as a nominated bank, i.e. a bank, that is authorized to pay under

the credit;

5. Upon receipt of the credit (advice), the exporter examines its compliance with

the terms of credit as settled in the concluded contract. If there is no evidence

of non-compliance, it starts the fulfillment of obligations (e.g. the shipment of

cargo);

6. After receiving the transport documents from the carrier, the exporter presents

them together with other documents listed in the credit to the nominated bank.

The credit also stipulates a specified period of time, after the date of shipment,

during which the presentation of documents must be made. If no such period is

stipulated, banks will not accept documents presented to them twenty-one

days after shipment.9 In any event, documents must be presented not later than

the expiry date of the credit;

7. Furthermore, the nominated bank examines the documents no later than seven

banking days after receiving them;

8. The issuing bank withdraws the amount from the importer’s account or (in

accordance with the terms of the credit) and withdraws it from the special

account on which the money was deposited in advance. After examination of

the documents the issuing bank transfers the money to the nominated bank;

9. Finally, the nominated bank transfers the money to the exporter;

23 | P a g e

Letter of Credit

10. From the moment of receiving the documents from the issuing bank, the

importer is deemed to be the owner of the goods. In this case, the credit is not

only a form of payment but also it performs the function of being an

instrument for securing the performance of the payment obligation. Here, it

should also be noted that the above scheme of payment by credit is of a

general nature and may vary according to the particular type of credit issued.

One of the principal advantages of documentary credit is its diversity.

It enables the parties, by taking into account existing circumstances, to select

the form that best meets their requirements.

24 | P a g e

Letter of Credit

Risks in Letters of Credit

Although letters of credit are a balanced payment method in terms of risk

issues for both exporters and importers, each letters of credit party bears some amount

of risk. As we have explained before letters of credit transactions are handled by

banks. This responsibility makes the banks one of the parties that bears risks in a letter

of credit transaction.

Risks in letters of credit can be discussed under four groups; general risks in

letters of credit, risks to the applicant, risks to the beneficiary and risks to the banks.

General Risks in Letters of Credit:

1. Country Risk: (Political Risk)

The first risk factor that can be mentioned in the general risks

group is the country risk or the political risk. Let us assume that we are an

exporter located in a country X and we have a customer from the country

Y. Our customer, which is from the country Y, opened a L/C in favor of

us. We have checked the L/C conditions and they seem workable. We have

produced and shipped the order as per the L/C and transmit the required

documents to the issuing bank before the expiry date. The issuing bank

found our presentation complying and informed us that they will be

honoring our payment claim at the maturity date. However, before the

maturity date due Country Y has changed its export regime, which makes

it impossible for the issuing bank to honor our presentation. This

illustrative is a good example of a country risks. Other examples of

country risks are mass riots, civil war, boycott, sovereign risk and transfer

risk.

2. Fraud Risk

25 | P a g e

Letter of Credit

As we have described before all conditions stated in a letter of

credit must be connected to a document, otherwise banks will disregard

such a condition. In addition, banks deal with only documents but not

goods, services or performance to which the documents may relate. This

feature of the letters of credit is the source of the fraud risk at the same

time. As an example, a beneficiary of a certain letter of credit transaction

can prepare fake documents, which looks complying on their face, to make

the presentation to the issuing bank. As the documents are complying on

their face, the issuing bank may honor the presentation and in this case, the

applicant must pay to the issuing bank for the goods it will never be

receiving. Beneficiaries of L/Cs bear also fraud risks. This happens if an

applicant issues a counterfeit letter of credit. In this case, the beneficiary

never receives its payment for the goods it has shipped.

3. Risks to the Applicant

In a letter of credit transaction, main risk factors for the applicants

are non-delivery, goods received with inferior quality, exchange rate risk

and the issuing bank's bankruptcy risk.

4. Risks to the Beneficiary

In a letter of credit transaction, main risk factors for the

beneficiaries are unable to comply with letter of credit conditions,

counterfeit L/C, issuing bank's failure risk and issuing bank's country risk.

5. Risks to the Banks

Every bank in a L/C transaction bears risks more or less. The risk

amount increases as responsibility of the bank increases.

26 | P a g e

Letter of Credit

Conclusion

Banks, as facilitators of international trade and commerce have been served

well by the mechanism of the Documentary Credit. The beauty of these credits is that

they provide appropriate protection, as required, by the seller, buyer, the seller's Bank,

and the buyer's Bank, while extracting their share of responsibility under the

transaction.

The DCs have acted as a sort of bridge between buyers and sellers of goods

and services, based in different countries, bringing them together, through the agency

of the Banks.

Since they came into being in 1933, DCs have no doubt played a significant role in

cross border trade, overcoming the barriers of language, customs and practices,

currencies, etc. And last, but not the least, they are an important source of business

and revenues to the Commercial Banks, and are expected to grow even more in

importance, in the coming years.

It could be concluded that documentary credit is a reliable and convenient

instrument of international settlement. However, we have to agree with those views

expressed in legal literature that this type of payment is complicated and expensive.

The application of credit in export-import operations is complicated both in legal as

well as economic terms. If several banks participate in a settlement by credit,

ultimately the purchaser of the credit will have to reimburse the costs of all the

authorized banks. Usually, the cost for each operation, such as the opening of credit,

sending a letter of advice, confirmation, the examination of documents envisaged by

the credit to name but some of the procedures is determined in the form of a fixed

interest on the amount of credit for any operation.

It is also noteworthy that the advantage of credit is directly linked with the

relevant experience of the participating banks in this field and with the existence of a

wide network of correspondent banks. Under these circumstances operations are less

complicated.

27 | P a g e

Letter of Credit

Bibliography

Personal Notes of SYJC.

Documentary Credit Operations Book.

28 | P a g e