dodd frank executive comp valcon

TRANSCRIPT

Executive Compensation and Risk in the Post-Dodd Frank Environment

Valcon 2011

Stephen M. BainbridgeWilliam D. Warren Distinguished Professor

UCLA School of Law

© Stephen M. Bainbridge 2011 22/24/11

© Stephen M. Bainbridge 2011 32/24/11

Loose money policy

Crisis Factors

Gov’t pro-home

ownership policy

Risk management failures

Consumer debt

Corporate governance

of Main Street firms

CorporateGovernanceof banks

© Stephen M. Bainbridge 2011 42/24/11

The Compensation Story

Take excess risks

producing non-

sustainable returns

© Stephen M. Bainbridge 2011 52/24/11

Apply to both Main Street and Wall Street

© Stephen M. Bainbridge 2011 6

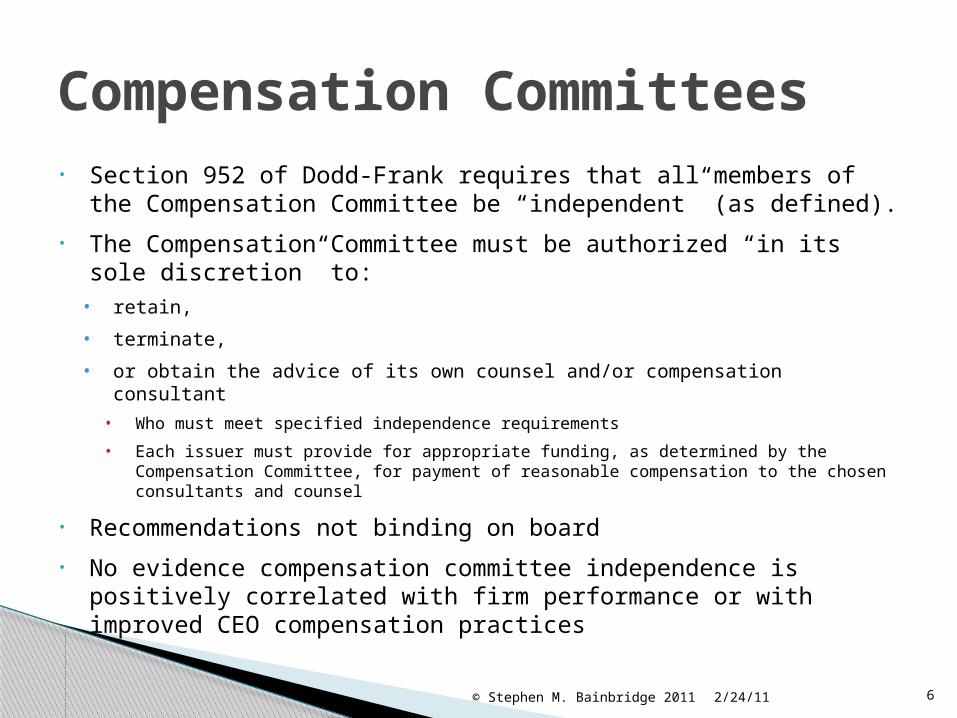

• Section 952 of Dodd-Frank requires that all members of the Compensation Committee be “independent” (as defined).

• The Compensation Committee must be authorized “in its sole discretion” to:• retain,

• terminate,

• or obtain the advice of its own counsel and/or compensation consultant

• Who must meet specified independence requirements

• Each issuer must provide for appropriate funding, as determined by the Compensation Committee, for payment of reasonable compensation to the chosen consultants and counsel

• Recommendations not binding on board

• No evidence compensation committee independence is positively correlated with firm performance or with improved CEO compensation practices

2/24/11

Compensation Committees

© Stephen M. Bainbridge 2011 7

New Compensation Disclosures Pay vs. Performance: Clear description of

relationship between executive compensation paid and the company’s financial performance.

Pay Equity DisclosureA. The median of the annual total compensation of

all the company’s employees except the CEO

B. The annual total compensation of the CEO, and

C. The ratio of (A) to (B)

Whether Compensation Committee has retained consultant, whether any conflicts of interest were identified, and if so, how addressed

2/24/11

© Stephen M. Bainbridge 2011 8

Clawing-Back Executive Compensation: SOX § 304

2/24/11

© Stephen M. Bainbridge 2011 92/24/11

Dodd-Frank § 954

New listed company manual provisions must require listed companies to disclose their policies for clawing back incentive-based compensation paid to current or

former executive officers in the event of a restatement of the company’s

financials due to material non-compliance with any federal securities law financial

reporting requirement

© Stephen M. Bainbridge 2011

Comparing SOX to Dodd-Frank

SARBANES-OXLEY ACT Dodd-Frank

Individuals Subject to Claw back Provision

CEOs and CFOs of public companies who restate earnings

Current and former executive officers of exchange listed companies

Standing to Enforce Claw back Provision

SEC only -- no private right of action Issuer (Shareholder derivative standing?)

Circumstances that Trigger Claw back Provision

An accounting restatement due to the material non-compliance of the issuer with any financial reporting requirement under the securities laws

A restatement of the company’s financials due to material non-compliance with any federal securities law financial reporting requirement

Conduct that Triggers Claw back Provision

Unspecified “misconduct” in preparing financial statements

No misconduct required – apparently strict liability

Forms of Compensation Recouped under Provision

Any bonus or other incentive or equity based compensation

Excess bonus or incentive compensation (Δ amt paid and would have been paid if correct)

Claw back - Duration The 12 month period following issuance of the financial statements including restatements

Three years prior to date of restatement

© Stephen M. Bainbridge 2011 11

§951: Say on Pay

2/24/11

© Stephen M. Bainbridge 2011 122/24/11

Comparative Risk Preferences re Pay

© Stephen M. Bainbridge 2011 132/24/11

Shareholder Empowerment

© Stephen M. Bainbridge 2011 14

Implications of New Environment Increase in shareholder power to influence

board composition and executive pay Increase in power of proxy advisers who

advise institutional shareholders on how to vote – or to whom such shareholders delegate vote decisions

More pressure on boards to accede to wishes of most vocal shareholders – including pressure to conform to rigid ideas about governance and compensation practices

2/24/11