does the sarbanes-oxley act reduce fraudulent financial

TRANSCRIPT

Does the Sarbanes-Oxley Act Reduce Fraudulent

Financial Reporting?

by

Szu-fan Chen

Submitted in Partial Fulfillment of the

Requirements for the Degree

Doctor of Philosophy

Supervised by Professor Jerold L. Zimmerman

Business Administration

William E. Simon Graduate School of Business Administration

University of Rochester

Rochester, New York

2014

ii

Biographical Sketch

The author was born in Taiwan, Republic of China. She attended the National Taiwan

University, and graduated with a Bachelor of Business Administration degree in Finance.

She began doctor studies in Accounting at the University of Rochester in 2008. She was

awarded a fellowship for doctoral student from 2008 to 2012 and received the Master of

Science in Business Administration from the University of Rochester in 2011. She

pursued her research in Accounting under the direction of Jerold L. Zimmerman.

iii

Acknowledgements

I am greatly indebted to Shane Heitzman, Joanna Wu, and Jerry Zimmerman for their

invaluable guidance in the development of this paper, and Charles Wasley, Edward

Owens, and Jaewoo Kim for stimulating discussions on this paper. I am also thankful to

Robert Novy-Marx, Jerry Warner, Ron Kaniel, Matt Gustafson, Michael Dambra,

Mengjie Huang, Ke Na, and workshop participants at the University of Rochester,

University of Minnesota, Drexel University, University of California-Riverside,

University of Hong Kong, Chinese University of Hong Kong, Hong Kong University of

Science and Technology, and National University of Singapore for helpful comments.

iv

Abstract

This paper investigates whether the Sarbanes-Oxley Act (SOX) achieves one of its main

goals of combating fraud. After accounting for the impact of SOX on fraud detection and

litigation, my findings imply a reduction of 100 basis points in the probability of fraud

commission after SOX. Further cross-sectional and time-series analyses show that this

reduction is attributable to the internal control provisions of SOX. I also find that

investors suffer smaller damages caused by frauds in the post-SOX period than in the pre-

SOX period. Although opponents of SOX argue that it reduces the competitiveness of US

companies while having little impact on fraud, my results suggest that SOX reduces

fraudulent financial reporting and increases investor protection. While this paper

investigates an important aspect of the direct benefits of SOX, it does not argue that SOX

is on net beneficial since it does not address the compliance costs of the regulation.

v

Contributors and Funding Sources

This work was supervised by a dissertation committee consisting of Professors Shane M.

Heitzman, Joanna Wu, and Jerold L. Zimmerman of the Department of Accounting. All

work for the dissertation was completed independently by the student. Graduate study

was supported by a fellowship for doctoral student from the University of Rochester.

vi

Table of Contents

Biographical Sketch ii

Acknowledgements iii

Abstract iv

Contributors and Funding Sources v

1. INTRODUCTION 1

2. LITERATURE REVIEW 6

2.1. The Prevention of Financial Statement Frauds 6

2.2. Measuring the Incidence of Financial Statement Frauds 7

2.3. The Costs and Benefits of SOX 9

3. HYPOTHESES 10

3.1. The Impact of SOX on the Probability of Fraud Commission 10

3.2. Cross-sectional Variation in the Impact of SOX 12

3.3. SOX-mandated Audits and Fraud Reduction 15

3.4. SOX and the Size of Damage Caused by Frauds 16

4. EMPIRICAL ANALYSES AND RESULTS 16

4.1. Change in the Probability of Fraud Commission after SOX 17

4.1.1. Research Design, Sample Selection and Descriptive Statistics 17

4.1.2. Change in the Probability of Fraud Commission 23

4.2. Cross-sectional Variation in Fraud Reduction 25

4.3. SOX-mandated Audits and Fraud Reduction 26

4.3.1. Research Design of Fraud Reduction after Section 404 Compliance 26

vii

4.3.2. Empirical Results of Fraud Reduction after Section 404 Compliance 29

4.4. Change in the Size of Damage after SOX 31

4.4.1. Sample Selection and Research Design 31

4.4.2. Regression Results 34

4.5. Additional Robustness Tests 36

5. CONCLUSION 38

Appendix A 40

Appendix B 43

Appendix C 47

References 49

viii

List of Figures

Figure 1: Impact of SOX on the Probabilities of Fraud Occurrence, Detection and

Litigation 55

Figure 2: Settlement Amount by Fraud Start Year 56

Figure 3: Number of Lawsuits by Filing Year 57

ix

List of Tables

Table 1: Descriptive Statistics 58

Table 2: Pearson/Spearman Correlation Matrix 61

Table 3: SOX and Fraud Commission 62

Table 4: Section 302 and 404 Compliance and Fraud Occurrence 64

Table 5: Lower Settlement Amount and the Timeliness of Fraud Detection 65

Table 6: Duration of Frauds 67

Table 7: Auditor Turnover 68

1

1. INTRODUCTION

After the Stock Market Crash of 1929, the United States government enacted the

Securities Act of 1933 and the Securities Exchange Act of 1934 to better protect investors

from misleading financial disclosures. As a result of the high-profile accounting scandals

in the early 2000s, Congress passed the Sarbanes-Oxley Act (hereafter SOX) in 2002 to

further deter fraudulent financial reporting by improving corporate internal controls and

financial disclosures. SOX imposed millions of dollars in annual compliance costs on

firms (Securities and Exchange Commission, 2009; hereafter SEC) and brought changes

to the governance practices of public firms. There is no shortage of studies documenting

both costs (e.g., Zhang, 2007; Iliev, 2010) and indirect benefits (e.g., Cohen, Dey, and

Lys, 2008; Jain, Kim, and Rezaee, 2006). There is, however, a noticeable lack of

empirical evidence about the impact of the regulation on fraudulent financial reporting,

likely due to the difficulty of measuring a change in fraudulent behavior. Without such

evidence it is difficult to evaluate the efficacy of securities regulations like SOX in

preventing fraud. This paper employs a novel research design to bridge this gap.

I focus on financial statement fraud at publicly-listed companies, the type of fraud

that SOX is intended to deter. Fraud is defined as the deliberate, material

misrepresentation of a firm’s financial condition. Because the commission of fraud is

unobservable unless it is detected and litigated, I deduce the commission of fraud from

the incidence of private securities lawsuits. My research design exploits the lag between

fraud occurrence and its later detection and litigation. As frauds caught after SOX are

detected and litigated by the same set of auditors and litigators, focusing on these frauds

2

effectively controls for SOX-induced differences in enforcement and litigation practices

that confound inferences obtained from a sample of detected frauds. I then partition these

frauds based on the start date of the fraud, i.e., the date when a firm issues the first of a

series of misstatements, and expect that the probability of committing fraud would be

lower after SOX than before SOX. The research design is explained in more detail in

Section 4.

To implement this research design, I obtain a list of private securities lawsuits

alleging frauds committed before SOX but detected and litigated after SOX from the

Stanford Securities Class Action Clearinghouse. To alleviate the concern that some

private lawsuits may not have merit, I rely on the outcome of a lawsuit to determine

whether or not the defendant is highly likely to have engaged in fraud (Choi, 2006; Dyck,

Morse, and Zingales, 2010).

My findings support the conjecture that SOX reduces fraud, consistent with the

intent of the Act. I find that, after accounting for SOX’s impact on the conditional

probabilities of fraud detection and litigation, the observed litigation risk falls by 20 basis

points after SOX. This reduction implies that the proportion of publicly-listed firms

engaging in fraud is lower by 100 basis points1 in the post-SOX period than in the pre-

SOX period. In other words, suppose the probability of fraud was x in the pre-SOX

period, then my result suggests that the post-SOX probability of fraud became (x – 1%).

Dyck, Morse, and Zingales (2013) estimate that the pervasiveness of fraud, x, is

1 The implication is based on Dyck et al.’s (2013) estimated detection rate. Section 4 provides a more

detailed explanation.

3

approximately between 5.6% and 14.5%, and hence my finding implies that the post-

SOX probability of fraud falls by 7% (= 1÷14.5) to 18% (= 1÷5.6).

A simple comparison between pre- and post-SOX periods is not sufficient to rule

out the possibility that changes in the variable of interest are due to other concurrent

events around the passage of SOX. While all publicly listed firms have to comply with

SOX, the impact of the Act is not the same for all firms. Hence, the alternative

explanations could be ruled out by examining the cross-sectional variation in the

reduction of fraud between firms less affected by SOX and those more affected. As the

implementation time is not the same for all provisions of SOX, another way of ruling out

the alternative explanations is to examine whether provisions implemented earlier have

different impact on fraud than those implemented later. Accordingly, I further analyze

both the cross-sectional and the time-series variations in the risk of fraud.

Prior literature uses the cross-sectional variation in the economic consequences of

SOX to firms to identify the impact of the Act (e.g., Chhaochharia and Grinstein, 2007;

Gao, Wu, and Zimmerman, 2009; Hochberg, Sapienza, and Vissing-Jørgensen, 2009).

Similarly, my research method exploits three firm characteristics related to the level of

changes in a firm’s internal controls after SOX: size, age, and business complexity. First,

in order to meet the same standard of effective internal controls under SOX, small firms

had to adopt control procedures and activities more like those in large firms (ACSPC,

2006). Second, since recently-listed firms are more likely than seasoned firms to have

internal control weaknesses (Doyle, Ge, and McVay, 2007) and the former tends to have

more intense scrutiny from the SEC than the latter (Feroz, Park, and Pastena, 1991;

4

Beneish, 1997; Beneish, 1999), recently-listed firms are more motivated than seasoned

firms to change their internal controls after SOX. Last, as firms with more business lines

spend more on SOX-mandated reporting of internal controls (Zhang, 2007), these firms

are also likely to improve the integrity and accuracy of their financial statements. I

predict and find that the post-SOX reduction in fraud is much greater for smaller, less

seasoned firms and firms with more business lines.2

In addition to the cross-sectional variation in the reduction of fraud, SOX induces

time-series variations as well. In November, 2004, large firms were required to comply

with Section 404 of SOX, which involves external auditors’ attestation to management’s

evaluation of internal controls. For small firms the compliance deadline was eventually

postponed beyond the sample period in this paper. Prior studies find that external auditors

play an important role in the discovery of fraud (Dyck et al., 2010) and internal control

weaknesses (e.g., Doyle, et al., 2007; Bedard, Hoitash, and Hoitash, 2009). Hence I

expect that, by increasing external auditors’ liabilities, Section 404 would have a greater

impact on fraud than other SOX provisions implemented earlier. I find that the decline in

the risk of fraud is greater after Section 404 than before. This finding further supports the

hypothesis that the reduction in fraud is due to SOX rather than other concurrent events

around the passage of SOX or market forces (Ball, 2009).

Finally, I investigate whether SOX affects another key dimension of litigated fraud

cases: the severity of fraud. The legal liability provisions of SOX are intended to deter

large frauds, although ex ante it is unclear whether the marginal increase in managers’

2 However, a distinct cost-benefit analysis is beyond the scope of this paper.

5

liabilities deters financial reporting fraud (Ribstein, 2002). There could also be fewer

large frauds if SOX prevents damages from accumulating over time through tighter

internal controls, which by definition facilitates timely fraud detection. To explore the

influence of SOX on fraud damages, I use the settlement amount of a lawsuit to measure

the size of the damage caused by the alleged fraud.

I find evidence that damages decline after SOX. More specifically, the average

settlement amount declines immediately after SOX. Moreover, Section 404 compliance

does not induce a further decline in the average settlement amount, which is distinct from

my findings of the time-series change in the risk of new frauds. Because my sample

period includes both the market crashes in the early 2000s and the 2007-2008 financial

crises, market fluctuations alone cannot explain the reduction in the settlement amount.

Overall, the results indicate that managers avoid committing large frauds after SOX, but

the evidence is not sufficient to attribute the change to SOX.

This paper contributes to the literature in several ways. First, it provides a new

empirical design to measure the frequency of fraud that overcomes the partial

observability problem that is common in fraud studies. My research method imposes

fewer restrictions on the data and is more easily applied than other empirical models on

fraud (e.g., Wang, 2011; Zakolyukina, 2013). Second, this study adds to the set of

information required to determine whether the large costs to comply with SOX are

justified given the estimated change in the likelihood and size of frauds. Third, I find

some evidence that the post-SOX fraud reduction is positively related to a firm’s internal

6

control modifications. My findings offer insights into the mechanisms through which

SOX affects fraudulent financial reporting.

The rest of the paper proceeds as follows: Section 2 reviews related literature and

my contribution to prior studies. Section 3 provides a discussion of the impact of SOX

and develops hypotheses. Section 4 discusses the research design, sample selection, and

the results of empirical tests. Section 5 concludes the paper.

2. LITERATURE REVIEW

2.1. The Prevention of Financial Statement Frauds

The Securities Act of 1933 and the Securities Exchange Act of 1934 were enacted

to prevent frauds in the sale of securities. Stigler (1964) and Jarrell (1981) use stock

prices and returns to examine the impact of the Securities Act of 1933. Neither finds

evidence that fewer overpriced (or fraudulent) securities are issued after the regulation

came into effect. Benston’s (1969) survey of existing literature finds little support for

widespread frauds and misrepresentation of financial statements prior to the Securities

Act of 1933 and the Exchange Act of 1934. Benston (1973) further shows that the

Exchange Act of 1934 did not reduce frauds or the risk of stock returns. Although these

studies do not find a negative impact of securities rules on fraud, their research designs

were not sufficiently sophisticated to support the hypothesis that the securities laws in

1933 and 1934 do not prevent frauds (Seligman, 1983). Moreover, the early studies could

not exclude the impact of the state securities statutes adopted in the period immediately

7

preceding the passage of the 1933 and 1934 Securities Acts. My paper overcomes these

difficulties by examining both the cross-sectional and the time-series impacts of SOX.

The most important difference between SOX and prior securities regulations is that

the former prescribes particular corporate practices. Statement on Auditing Standards No.

99 lists three conditions generally present at the occurrence of frauds: incentive,

opportunity, and the rationalization of fraud commission. All of these are addressed in

SOX.3 The efficacy of these provisions is, however, an empirical question. Proponents of

SOX believe it prevents fraud by strengthening corporate governance and auditor

independence (Rezaee, 2005). Critics claim that the substance of the provisions in SOX is

not new and hence it is questionable that the regulation would change the risk of frauds

(Young, 2006). For example, the major concepts of SOX were first introduced in the

Treadway Commission Report in 1987, including independent audit committee and the

establishment of a system of internal controls. If on average firms voluntarily followed

the recommendations in the Treadway Commission Report before SOX, SOX would not

affect frauds significantly. If, on the other hand, by balancing the costs and benefits firms

did not choose to fully follow the recommendations before SOX, then the legislation is

likely to have an observable effect on fraud risk.

2.2. Measuring the Incidence of Financial Statement Frauds

Accounting scandals over the last two decades have spurred academic studies on

the risk of financial reporting fraud. A major challenge to researchers, however, is how to

3 For example, SOX increases criminal penalties to discourage accounting manipulations; it strengthens

internal audit procedures to reduce opportunities of accounting manipulation; it also requires additional

officer and director certifications of financial statements to enhance managers’ integrity and ethics.

8

measure the risk of fraud. Studies on the factors of the risk of frauds have tried various

proxies for frauds, including financial restatements (e.g., Burns and Kedia, 2006; Efendi

et al., 2007), SEC legal actions (e.g., Beneish, 1999; Dechow, Ge, Larson, and Sloan,

2011), and private litigation (e.g. Dyck et al., 2010). Financial restatement is a poor proxy

for financial reporting fraud, both because it includes unintentional errors (Hennes, Leone,

and Miller, 2008) and because it excludes the other important type of frauds: the

omission of material financial information. Seligman’s (1983) discussion of Benston

(1969) points out that failing to include the latter type of frauds leads to misleading

conclusions regarding to the frequency of frauds. In contrast, private litigation appears to

be a better proxy because it includes both the omission and the misstatement of financial

information and covers more fraud cases than SEC legal actions. Cox and Thomas (2003)

find in a sample of lawsuits settled in the 1990’s that 55 percent of SEC enforcement

actions produced a parallel private lawsuit but only 15 percent of private lawsuits

accompanied an SEC action. Karpoff, Koester, Lee, and Martin (2013) further show that

compared to the SEC Accounting and Auditing Enforcement Releases (AAERs), the

Stanford Private Securities Litigation database has a smaller omission rate of cases

prompting SEC actions. Although the majority of private lawsuits did not go to trial and

so were technically “alleged” frauds, legal studies suggest that the settlement amount

could indicate the merits of the lawsuit (e.g., Grundfest, 1995; Choi, 2006).

Another challenge arises from the partial observability of frauds. A fraud event is

not observed if it is never detected, which makes it difficult to separately examine the

commission and the detection of fraud. Wang (2011) employs a bivariate probit model to

9

separate the probability of fraud commission from the probability of fraud detection. Her

model includes ex-post factors affecting the detection of frauds and ex-ante detection

factors affecting the commission of frauds. This makes the model unsuitable for an event

study because a new regulation could affect both the ex-ante and ex-post detection

probabilities. Zakolyukina (2013) estimates the risk of frauds with a structural model.

The model, however, does not consider frauds involving intentional omission of material

information. Dyck et al. (2013) use a method conceptually similar to that in this paper.

They examine a sample of firms unexpectedly forced to change external auditors, a

setting where the probability of fraud commission is fixed while the likelihood of fraud

detection varies. The varying detection likelihood helps them estimate the level of fraud

pervasiveness.

2.3. The Costs and Benefits of SOX

Studies criticizing SOX focus on the increasing costs of complying with the internal

control provisions of SOX. Several studies show an increase in public firms’ audit and

accounting costs following the enactment of SOX (e.g., Asthana, Balsam, and Kim, 2009;

Eldridge and Kealy, 2005). The compliance costs are disproportionately large for small

public firms (American Electronics Association (“AeA”), 2005; Ferola, 2006). In

addition to the increase in audit and accounting fees, public firms’ legal fees and board

compensation have also soared since 2002 (Hartman, 2007). The costs of complying with

SOX motivate some firms to go private (Engel, Hayes, and Wang, 2007) or go dark

(Government Accountability Office (GAO), 2006; Leuz, Triantis, and Wang, 2008).

Bargeron, Lehn, and Zutter (2010) show a decline in corporate risk-taking after SOX and

10

interpret the finding as an adverse impact on firm value. In fact, the regulation was so

costly that shareholders perceive it as reducing firm value (Zhang, 2007).

Such a costly regulation also has benefits. Prior literature shows that it improves

investor confidence (Jain et al., 2006), promotes conservative financial reporting (Iliev,

2010), and helps reduce earnings management through accrual manipulation (Cohen et al.,

2008). These benefits are, however, indirect and difficult to quantify. Since SOX was

intended to combat fraud, it is important to understand by how much and through what

channels it affects fraudulent behavior. One contribution of this paper is to provide an

estimate of the change in the proportion of firms engaging in fraudulent financial

reporting. Multiplying the change in the fraud risk by a proxy for fraud damage would

then allow legislators to calculate the total benefit of SOX in terms of fraud reduction.

This paper abstains from a cost-benefit analysis, though, as finding an appropriate

estimate of the damage of fraud is beyond the scope of this paper.4

3. HYPOTHESES

3.1. The Impact of SOX on the Probability of Fraud Commission

In response to the spectacular frauds in the early 2000s, Congress enacted SOX to

restore investors’ confidence in the integrity of accounting report. Ex ante it was unclear,

however, whether more legislation was necessary and sufficient to fix the deficiencies in

4 Moreover, publicly-available estimates are controversial. The loss in a firm’s market value upon the

disclosure of the alleged fraud includes the impact of the difference between the reported and the actual

performance and the impact of the potential fraud. These impacts are difficult to disentangle. The

settlement amount is often a small proportion of the loss in market value and therefore could significantly

understate the damage of fraud. The difference between the stated and true accounting numbers is not

always available as many lawsuits allege misleading statements that do not affect the reported or forecasted

earnings.

11

the several levels of monitoring by directors, external auditors, and other stake holders.

Ribstein (2002) questions whether more regulations like SOX would prevent highly

motivated managers from engaging in frauds. Empirical data do not support the notion

that investors would benefit from the corporate governance mandates of SOX (Romano,

2005). Perino (2002) and Ball (2009) both question the efficacy of SOX in preventing

accounting frauds. Rice and Weber (2012) investigate the determinants of Section 404

reporting and find that Section 404 reporting does not reliably inform investors of

accounting improprieties in advance. The unreliability of Section 404 reporting may be

due to insufficient enforcement of SOX as firms failing to report internal control

weaknesses are not more likely to receive penalties (Rice, Weber, and Wu, 2013).

Several studies, on the other hand, indicate that SOX could reduce the agency

problem between insiders and outside shareholders by enhancing corporate controls and

monitoring. La Porta, Lopez-de-Silanes, and Shleifer (2006) find that the stock market

benefits from mandatory disclosures, consistent with Mahoney’s (1995) argument that

disclosure requirements reduce agency problems. Recent studies document evidence that

SOX not only mitigates agency problems for firms lobbying against the regulation

(Hochberg et al., 2009) but also reduces information asymmetry in the Chief Financial

Officer labor market (Wang, 2010). In addition, DeFond and Lennox (2011) find that

small auditors exit the market after SOX and argue that SOX improves audit quality. It is

therefore an empirical question whether SOX reduces the risk of fraud. This leads to my

first hypothesis:

12

H1: The probability that a firm engages in fraud declines in the post-SOX period

relative to the pre-SOX period.

3.2. Cross-sectional Variation in the Impact of SOX

The primary objective of SOX is to enhance corporate governance and internal

controls. By imposing the same requirements on all firms, however, SOX is not fully

scalable—it restricts firms from tailoring their spending on internal controls based on

firm characteristics.5 For example, Section 302 of SOX requires management to certify

the accuracy of financial reports and the effectiveness of internal controls; Section 404

requires managers and external auditors to report the adequacy of the firm’s internal

controls over financial reporting. These new rules provide powerful incentives to spend

on controls and fix weaknesses (Coates, 2007). Greenstone, Oyer, and Vissing-Jørgensen

(2006) find that firms more affected by new regulations also benefit more from the

compliance of the new rules and attribute the findings to agency problems before the

compliance of the new regulations. Hence, the more changes a firm adopts to comply

with SOX, the greater impact6 SOX should have on deterring financial statement frauds.

One way of testing the impact of SOX on fraud, therefore, is examining whether the

5 Although SOX also affects corporate governance in various dimensions, its impact on fraud through

changes in corporate governance is not as straight forward as its impact through changes in internal

controls. Romano (2005) discusses the lack of empirical evidence, prior to the enactment of SOX, that the

corporate governance mandates in SOX are associated with the risk of fraud. Moreover, since the optimal

governance structure is endogenously chosen by firms (e.g., Coles, Daniel, and Naveen, 2008), the relation

between corporate governance and the risk of fraud could be non-linear, making it difficult to interpret

empirical findings. Hence examining the effects of the governance provisions of SOX on fraud is beyond

the scope of this paper. 6 This “impact” is one-sided in the sense that it is only related to the change in frauds regardless of the costs.

Firms that did not voluntarily employ the practices prescribed by SOX could choose to do so either because

the costs outweigh the benefits or because there are agency problems. The former implies that SOX brings

net costs to these firms while the latter could imply that SOX brings net benefits. Which reason dominates

is not the focus of this paper and does not affect the analyses.

13

change in the risk of fraud is positively related to the amount of effort a firm puts forth to

comply with SOX. I discuss three firm characteristics likely associated with the cross-

sectional variation in the impact of SOX as follows.

The 2006 final report of the Advisory Committee on Smaller Public Companies

(ACSPC) to the SEC suggests that, to achieve the desired flexibility and the speed of

reaction to market changes, small firms have to frequently modify their operating

practices and reporting processes. Accordingly, a small firm has more authority

concentrated in top management and a lower demand for well-established processes than

a large firm. The direct involvement of top managers in small firms can provide

sufficiently strong controls even without static controls and procedures (the Committee of

Sponsoring Organizations, 1992; “COSO”).7 This explains why small firms have a

different optimal system of internal controls than large firms. After SOX was passed,

however, the SEC and PCAOB imposed a universal definition of effective internal

controls and identified as suitable for compliance purposes only one internal control

framework—the COSO framework. Auditors also tend to apply a one-size-fits-all

approach to the SOX-mandated audit of internal controls (ACSPC, 2006). These

universal requirements8 led to small firms’ adoption of the types of control activities

optimal for large firms, such as better segregation of duties and more detailed control

7 More specifically, the COSO framework states: “For example, direct involvement by the CEO and other

key managers in a new marketing plan, and retention of authority for credit sales, significant purchases and

draw downs on lines of credit, can provide strong control over those activities, lessening or obviating the

need for more detailed control activities. Direct hands-on knowledge of sales to key customers and careful

review of key ratios and other performance indicators often can serve the purpose of lower level control

activities typically found in large companies.” 8 The COSO guidance for small firms was not published until mid 2006, so small firms followed the same

guidance as large firms at the beginning of SOX compliance.

14

activities. The greater change SOX imposed on small firms is evidenced by these firms’

disproportionately higher compliance costs (AeA, 2005) and greater percentage increase

in audit fees after SOX (SEC, 2009). The preceding arguments indicate that the impact of

SOX on fraud would be greater for small firms than for large firms.

H2: The reduction in the probability of fraud commission in the post-SOX period is

greater for smaller firms.

SOX requires firms and their auditors to conduct additional review and assessment

of the effectiveness of internal controls. The scope of documentation and testing of

internal controls under SOX would increase in a firm’s number of business lines (Zhang,

2007). The number of business lines is also positively related to the probability that a

firm encounters material control weaknesses (Ashbaugh-Skaife, Collins, and Kinney,

2007; Doyle et al., 2007). The impact of SOX-mandated changes in internal controls is

therefore likely to be greater the more complex a firm’s business. My second cross-

sectional hypothesis is as follows stated in the alternative form.

H3: The reduction in the probability of fraud commission in the post-SOX period is

greater for firms with more complex operations.

The impact of SOX could also vary by firm age, which is defined in this paper as

the length of time a firm is traded on a public market. The longer a firm is publicly traded,

the more likely it has identified and remediated internal control weaknesses to comply

with securities regulations (Doyle et al., 2007). Thus to meet the same standard of

effective internal controls imposed by SOX, young firms had to implement more changes

to their internal controls in place relative to old firms. Additionally, the SEC tends to

15

scrutinize young firms more than old firms because the former are more pressured to

meet earnings expectations and hence more motivated to manipulate earnings (Beasley,

1996; Desai, Hogan, and Wilkins, 2006; Feroz et al., 1991; Beneish, 1997; Beneish,

1999). As SOX raises the SEC’s budget to review more publicly-listed firms, I expect

that the impact would be greater for young firms than for old firms. If SOX achieves its

goal of discouraging opportunistic behavior and enhancing the accuracy and reliability of

financial reports, the impact of SOX would be greater for younger firms, leading to a

greater reduction in fraud.

H4: The reduction in the probability of fraud commission in the post-SOX period is

greater for younger firms.

3.3. SOX-mandated Audits and Fraud Reduction

External auditors play an important role in identifying internal control deficiencies

that were not detected by managers (Hammersley, Myers, and Shakespeare, 2008). Ge

and McVay (2005) and Ashbaugh-Skaife et al. (2007) find that dominant audit suppliers

are more able than small auditors to uncover and require management to disclose

weaknesses in internal controls. Dyck et al. (2010) also find that auditors identify more

frauds after SOX came into effect. By requiring auditors to attest to management’s report

of internal control over financial reporting, Section 404 of SOX is more likely to deter

frauds than other provisions of SOX. Hence I expect that the post-SOX reduction in fraud

would be more pronounced after firms start to comply with Section 404 of SOX.

H5: There is a greater reduction in new frauds in the post-Section-404 period than in

the pre-Section-404 period when managers only have to comply with Section 302.

16

3.4. SOX and the Size of Damage Caused by Frauds

In addition to reducing the probability of fraud commission, SOX is intended to

reduce the magnitude of the damage caused by accounting frauds. SOX is likely to lower

fraud damages for two reasons. First, the SEC’s 2009 survey finds that on average SOX

improves the quality of the surveyed firms’ internal controls, which should increase the

likelihood of timely detection of frauds. Timelier discovery of fraud shortens the duration

of fraud and reduces the number of defrauded investors (Cox and Thomas, 2004). Ceteris

paribus, the fewer investors affected, the smaller total damages. Second, legislators

increased the criminal liability and added the clawback provision to SOX in an attempt to

reduce managers’ incentive to commit large frauds. If these provisions achieve the

desired goals, there would be fewer large frauds, causing a decline in the average size of

damage. I predict that the implementation of SOX would be associated with a reduction

in the damage of frauds but do not identify which of the two previously-mentioned

reasons causes the reduction.

H6: The damage to investors from fraudulent financial reporting declines after SOX

compliance.

4. EMPIRICAL ANALYSES AND RESULTS

In this section I discuss the research design and the results of empirical tests of each

hypothesis. First I test whether the risk of fraud declines after SOX, which is followed by

examinations of the cross-section and time-series variation in the reduction of fraud.

Then I analyze the change in the size of damage caused by frauds after SOX and explore

the possible reasons for the change.

17

4.1. Change in the Probability of Fraud Commission after SOX

I use the same sample and similar regression models to test H1 to H4. In this

subsection, I first explain the research design together with the sample selection and

descriptive statistics of H1 to H4, and then discuss the results of empirical tests.

4.1.1. Research Design, Sample Selection and Descriptive Statistics

The change in the probability of fraud is unobservable but can be inferred from the

change in an observable variable: the probability of private securities litigation, P(L).

This observable probability is the product of two probabilities: the probability that a fraud

was committed, P(C), and the conditional probability that the fraud was detected and

litigated, P(L|C).9 As Figure 1 shows, Fraud A and Fraud B differ by the timing of fraud

commission, detection and litigation. A comparison of frauds A and B would thus

involve joint tests of the influence of SOX on P(C) and P(L|C). Because SOX cannot

affect fraud commission in the pre-SOX period, frauds A and C should be associated with

the same P(C). Similarly, for frauds B and C, SOX would have affected P(L|C) in the

same way because the frauds are discovered and litigated under the same set of securities

regulation, with the same systems of internal controls, and by the same group of auditors

and litigators. In other words,

Fraud A: P(L) = P(L|C)pre-SOX * P(C)pre-SOX,

9 More precisely, P(L|C) is also a joint probability and can be decomposed into the probability of detection

conditional on the commission of frauds, and the probability of litigation conditional on the commission

and detection of frauds. Since the main purpose of the research design is to control for SOX’s impact on the

detection and litigation of fraud, for brevity and without loss of generality I use P(L|C) to represent the

product of the above two conditional probabilities. Also note that the extension of the statute of limitations

pursuant to SOX could potentially delay the litigation after detection, but it does not affect the period of

time between fraud commission and detection. Moreover, private lawsuits are on average filed within four

months after the end of the class action period, much shorter than the one-year statute of limitation before

SOX and three-year limitation after SOX.

18

Fraud B: P(L) = P(L|C)post-SOX * P(C)post-SOX,

Fraud C: P(L) = P(L|C)post-SOX * P(C)pre-SOX.

It is apparent from the above equations that the difference between P(L) of Fraud B

and P(L) of Fraud C, ∆P(L), equals to P(L|C)post-SOX times the difference between P(C)pre-

SOX and P(C)post-SOX. In other words, by comparing Frauds B and C I can control for the

impact of SOX on P(L|C) and infer how SOX changes the unobservable P(C) from the

change in the observable P(L).

I test my first hypothesis based on the model 5 in Kim and Skinner (2012)10

for

securities litigation risk:

( )

(1)

I define SOX_START as a dummy variable that equals 1 for firm-year observations

in the litigation sample if a lawsuit involves frauds committed in the post-SOX period

and in the non-litigation sample if the fiscal year ends after SOX. A negative coefficient

on SOX_START would be consistent with my hypothesis that SOX reduces fraud. The

10

Wang (2011) uses a bivariate probit model with partial observability to estimate the probability of fraud

commission and the probability of detection and litigation of frauds but does not examine the impact of

SOX. I do not use her model for several reasons. First, it is not clear whether her model is suitable for my

study because her model uses variables after the commission of frauds, which makes it hard to properly

define the time dummy of SOX_START for sued firms and non-sued firms. Second, because her model

imposes significant data restrictions, I would not be able to obtain a large enough sample size to test my

hypotheses other than H1. Third, my main research question is whether the probability of fraud commission

has changed instead of estimating the level of the likelihood of fraud commission and detection.

Nonetheless my test results of H1 remain unchanged if I use Wang’s model and my current definition of

the SOX_START dummy.

19

post-SOX period is defined as the period after August 29, 2002 for the following reasons.

First, although frauds committed before the passage of SOX could be affected by the

expected influence of the Act, it only took Congress two months to pass the final bill

after Sen. Sarbanes’ bill was passed in the Senate Banking Committee. The period is even

shorter after the details of the final bill were made public. Hence the early influence of

SOX is likely very limited. Second, SOX was signed into law on July 30, 2002 but the

implementation started later. The rules related to accelerated filing of insider trading

reports (Section 403) and certifications of internal controls (Section 302) went into effect

on August 29, 2002. Accordingly I use August 29, 2002 to separate the pre- and post-

SOX periods, although the one month difference does not change the empirical results. I

control for variables that are statistically significantly related to the risk of litigation in

Kim and Skinner’s (2012) model 511

and provide the definitions of these variables in

Appendix A.

My litigation sample includes a list of securities class action lawsuits filed between

August 29, 2002 and December 31, 2008 from the Stanford Securities Class Action

Clearinghouse.12

The sample period ends at the end of 2008 because most of the lawsuits

filed afterwards are not yet resolved. I retain securities lawsuits classified as “classic”13

by the Stanford database and brought by common unit or shareholders against US firms

11

Due to the unavailability of institutional investor data I do not include this variable. 12

Karpoff et al. (2013; KKLM hereafter) discuss potential problems with the Stanford database. I use the

settlement amount as a proxy for the size of frauds, which is not affected by the event identification

problem discussed in KKLM. The Stanford database omits violations to securities regulation if there is no

lawsuit filed against the perpetrators. These omissions most likely involve very small firms. My empirical

results are robust to the exclusion of very small firms. I also confirm that there are no duplicate lawsuits

arising from the same instance of financial misstatements. 13

“Classic” includes lawsuits alleging misleading forward-looking statements and SEC filings. Other types

are: IPO allocation, mutual fund, and analyst.

20

listed on NYSE, American Exchange, and NASDAQ. Merger and acquisition lawsuits

alleging misleading proxy statements are excluded because these cases are not directly

comparable to lawsuits alleging misleading statements of a firm’s current performance

and future prospects. To avoid the confounding effect of frivolous lawsuits, I follow

Dyck et al. (2010) and exclude lawsuits that were dismissed or settled under $3 million.14

The final litigation sample includes 267 lawsuits that were filed15

between August

29, 2002 and the end of 2008 and that have the requisite COMPUSTAT and CRSP data.

Among these lawsuits, 93 involve pre-SOX frauds and the rest involve post-SOX frauds,

and the earliest class action period starts in 1998. My non-litigation sample includes

exchange-listed US firms that are not sued for violation of securities rules between 1998

and 2008 and that have the requisite COMPUSTAT and CRSP data over the same period.

There are 8,372 firms (46,821 firm-year observations) in the non-litigation sample, 6,840

14

In the appendix I discuss and explain the reason why the absolute amount of settlement is preferable to

size-adjusted settlements when determining the merits of a lawsuit. Nonetheless, as a robustness check I

consider two sized-adjusted measures: a settlement divided by firm market value 10 days before and 10

days after the end of the class action period. Inferences are unchanged using cutoff points between 0.1%

and 1% for either one of the two size-adjusted measures, and using cutoff points of $1 million or $2.5

million for the absolute amount of the settlement. Some firms might settle frivolous lawsuits for more than

$3 million. Although the number of such cases is not likely to be large, these cases would still reduce the

power of my empirical tests. 15

The end of the class action period is usually the earliest date that investors learn of the bad news, whereas

the filing date of the first complaint represents the date that investors determine that the bad news is

allegedly due to fraudulent misconducts rather than unintentional mistakes. Hence both dates can be used

as a proxy for the date that the fraud was detected, but only the latter can be used as a proxy for the

litigation date of the fraud. Using the end of the class action period would increase the number of frauds

classified as frauds detected and litigated before SOX, causing a potential bias against me finding

significant results. Nonetheless, because the average lawsuit in my sample is filed shortly (around two

months) after the end of the class action period, my litigation sample does not change much by using either

date. The untabulated results show that inferences are unchanged using the end of the class period instead

of the filing date.

21

firms (20,235) in the pre-SOX period and 5,832 (26,586) in the post-SOX period.16

Also

following Kim and Skinner (2012), I winsorize all continuous variables at the 1% and

99% level.

I report the descriptive statistics of the litigation sample and the non-litigation

sample in Panel A of Table 1. Similar to Kim and Skinner’s (2012) findings, firms in the

litigation sample are on average larger, have greater historical growth, higher future

growth potential and lower tangible assets, and are more likely to have raised capital in

the past two years. Firms are also more likely to be sued if they have larger abnormal

returns, more skewed returns, or more volatile returns. In the litigation sample, 45% of

firms are in the electronics, retail, biotech, and computer industries, whereas in the non-

litigation sample only 27% of firms are in these industries.

My research design has two implicit assumptions. First, frauds litigated after SOX

but committed before SOX (Fraud C in Figure 1) resemble frauds litigated and

committed before SOX (Fraud A in Figure 1) in most aspects other than the likelihood of

detection and litigation due to a change in the regulation. To examine the validity of this

assumption, I obtain a list of lawsuits filed between January 1,1998 and August 29, 2002

with the same selection criteria as discussed earlier (276 cases). If the characteristics of

the 276 cases of Fraud A are similar to those of the 93 cases of Fraud C, it would be

reasonable to assume that Fraud A and Fraud C are drawn from the same distribution of

fraud commission. As Panel B of Table 1 shows, these two groups of frauds only differ in

16

All of my results hold after excluding firms in the financial service and utility industries. I report results

including these industries to account for the surge of frauds in the early 2000s involving utility companies

and another surge of frauds in the late 2000s involving financial companies.

22

terms of the length of the class action period, firm size, the proportion of lawsuits

involving restatement, and the amount of equity issuance. Because all of these frauds

were committed in the pre-SOX period, those detected later, i.e., in the post-SOX period,

have longer class action periods than those detected earlier. Firms engaging in Fraud C

are on average slightly larger, issue slightly less equity, and are more likely to involve

financial restatements. The difference in RESTATE indicates that Fraud C could be

associated with a higher likelihood of detection17

, but the differences in other factors

suggest that the timing of fraud detection and litigation is not significantly related to a

fundamental difference in the nature of frauds.

The second implicit assumption of my design is that frauds detected and litigated

after SOX are subject to similar likelihood of detection and litigation but differ in the

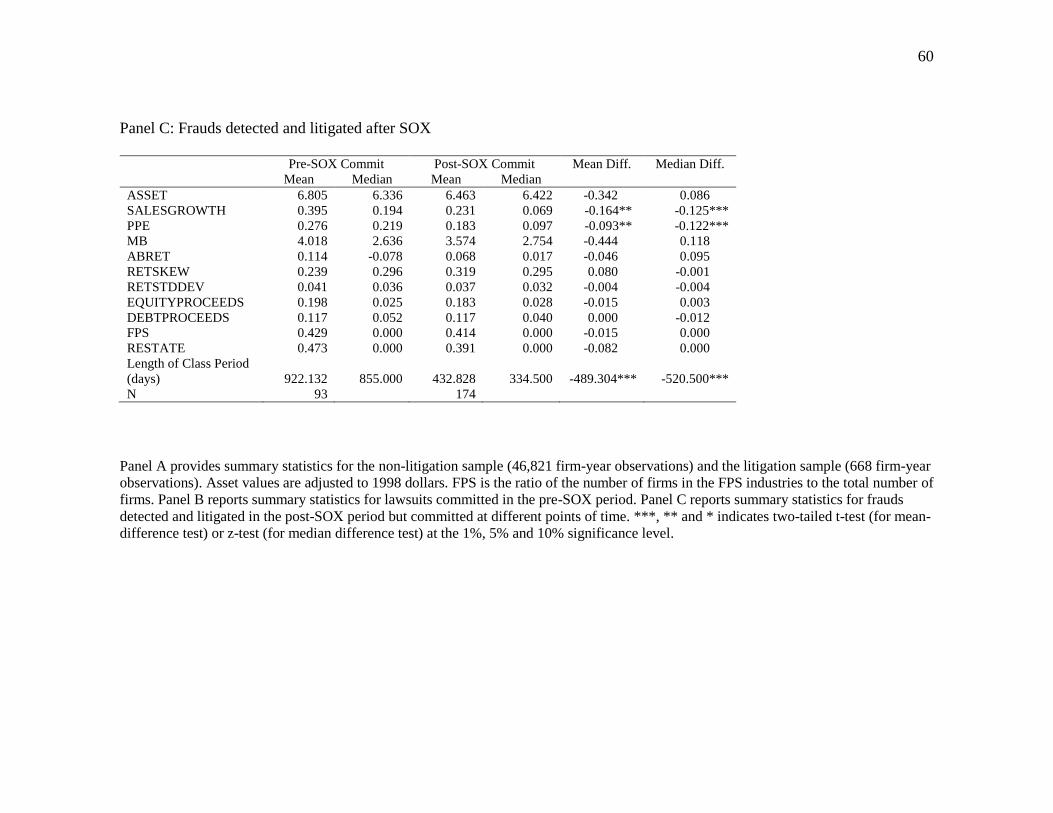

probability of commission. A univariate comparison of these frauds is shown in Panel C

of Table 1. The mean and median differences in ABRET, RETSKEW and RETSTDDEV,

and RESTATE, factors associated with the probability of fraud detection and litigation

identified in prior studies (e.g., Kim and Skinner, 2012; Wang, 2011), are not statistically

significant. On the other hand, factors affecting the incentive and motivations of

committing frauds, such as SALESGROWTH and PPE, are significantly different for

frauds committed before and after SOX. The results support my assumption that the

17

Unreported results show that both Fraud B and Fraud C are more likely to involve financial restatements

than Fraud A. This is consistent with prior literature that there is an increase in the incidence of financial

restatement after SOX (e.g., GAO, 2006). It is possible that the length of the class action period represents

some other aspects of the fundamental differences among lawsuits. As discussed in subsection 4.5, my

inferences do not change after controlling for the duration of fraud.

23

timing of fraud occurrence does not affect the likelihood of fraud detection and

litigation.18

The correlation matrix reported in Table 2 shows that the signs of the correlations

between private litigation risk and the control variables identified in model (1) are

consistent with those reported in Kim and Skinner (2012). The correlations between

Length of the Class Period (days) and most of the determinants of private litigation risk

are not statistically significant, indicating that the difference in the length of class action

period between Fraud B and C would not have a significant impact on the results.

4.1.2. Change in the Probability of Fraud Commission

Using my research design, I present the estimation results of model (1) in Column 1

of Table 3. The coefficient on SOX_START in Column 1 is significantly negative with a

marginal effect of -0.002. This result indicates that the probability of fraud commission in

fact declines after SOX. The area under the ROC curve is 0.74, which indicates that the

discrimination ability of the model is acceptable (Hosmer and Lemeshow, 2000). The

coefficients on the control variables are largely significant with expected signs and the

point estimates are similar to those reported in Kim and Skinner (2012).

Given an estimated value of P(L|C), I can deduce the amount of change in P(C)

from the -0.002 decline in P(L). Dyck et al. (2013) estimate that the annual average P(L|C)

is around 0.275, so the observed reduction in litigation risk implies that the probability of

18

Panel C of Table 1 also shows that frauds committed before SOX has a longer class action period than

frauds committed after SOX. If most of the frauds are detected and litigated shortly after commission, then

frauds committed before SOX (Fraud C) would have a detection and litigation date closer to the beginning

of my sample period than frauds committed and detected after SOX (Fraud B). This would work against me

finding significant results if the detection and litigation likelihood is higher in the later years of my sample

period due to firms’ Section 404 compliance. As discussed in footnote 14, I address the difference in the

duration of frauds in the robustness test.

24

fraud commission declines by 0.01 (= 0.002/0.275). As discussed in the introduction, the

economic significance of this 100 basis points decline in P(C) depends on the total

damages of frauds. Even though I do not have an estimate of these damages, they are

likely to be substantial as implied in prior studies on the market value loss following the

exposure of frauds (e.g., Cornerstone’s annual securities litigation studies) and the

spillover effects of frauds (e.g., Gleason, Jenkins, and Johnson, 2008; Akhigbe, Martin,

and Whyte, 2005).

The implications of my results are different from those in prior studies (e.g., PwC

2008 securities litigation survey), which find an insignificant change in the incidence of

private securities lawsuits after SOX. Unlike my paper, these studies do not control for

the impact of SOX on P(L|C). Moreover, they use the lawsuit filing date rather than the

fraud commission date in their analyses of fraud commission. To illustrate the difference

between my study and prior studies, I estimate a regression model by replacing

SOX_START in model (1) with SOX_FILE, a dummy variable for frauds filed in the

post-SOX period. The litigation sample includes lawsuits filed between 1998 and 2008.

This regression therefore compares the difference in Prob(SUED) based on whether a

lawsuit was filed before or after SOX, rather than whether the alleged fraud was

committed before or after SOX. Column 2 of Table 3 presents the estimation results of

this regression. The positive coefficient on SOX_FILE indicates that after SOX public

firms are exposed to a greater litigation risk. The marginal effect of SOX_FILE is 0.0056,

indicating a 0.56% increase in the joint probability of fraud commission, detection and

litigation. The area under ROC curve is 0.7565, so the model’s ability to discriminate is

25

acceptable. The coefficient estimates are similar to those in Kim and Skinner (2012).

Since this regression essentially compares Fraud A in Figure 1 with Fraud B and Fraud C,

the increasing litigation risk can reflect an increase in P(L|C), an increase in P(C), or both.

Thus one cannot infer from the regression results how SOX changes the commission of

fraud. The different results in Columns 1 and 2 of Table 3 show the importance of

controlling for the change in P(L|C) when testing the impact of SOX on fraud.

In sum, my findings support the hypothesis that the probability of fraud commission

declines after SOX. To explore whether this change in fraud is attributable to SOX, next I

examine the cross-sectional variation of the change.

4.2. Cross-sectional Variation in Fraud Reduction

I augment Model (1) with additional variables to test the cross-sectional variation in

the fraud reduction as follows:

( )

(2)

I use the same proxy for business complexity as in Ashbaugh-Skaife et al. (2007),

SEGMENTS, defined as the average number of four-digit SIC industries for each firm in

the pre-SOX period. H2 predicts that the post-SOX fraud reduction is greater as business

complexity increases, so I expect that would be negative. I define AGE as the natural

log of one plus the number of years a firm has price information on CRSP by the time

SOX was passed. AGE is 0 if a firm does not have price information before SOX. H3

26

predicts that the reduction in fraud is larger for younger firms, so would be positive.

H4 predicts that the smaller the firm, the larger the post-SOX reduction in fraud. Because

is included as a control variable, I use the interactive term

to test H4, which predicts to be positive.

The control variables include SOX_START, SEGMENTS, AGE, ASSET, and other

determinants of litigation risk in model (1). The sample used to estimate model (2) is the

same as the sample used to estimate model (1).

Column 3 of Table 3 displays the results from estimating model (2). The coefficient

on SOX_START*SEGMENTS is negative and statistically significant, consistent with

H2 that the post-SOX reduction in fraud is more pronounced for complex firms than for

firms with simpler operations. The post-SOX fraud reduction is smaller as AGE and

ASSET increase, consistent with H3 and H4 that younger and smaller firms enjoy more

fraud reduction benefits than older or larger firms. These results suggest that firms with

weaker controls benefit more from SOX implementation.

The coefficients on the control variables have signs that are largely consistent with

expectations. The Cox-Snell pseudo R2 of 0.083 suggests that the predictive ability of

model (2) is slightly better than model (1), whose R2 is 0.078. The area under the ROC

curve at 0.75 indicates that the discrimination ability of model (2) is acceptable.

4.3. SOX-mandated Audits and Fraud Reduction

4.3.1. Research Design of Fraud Reduction after Section 404 Compliance

To test H5, first I identify the compliance date of Section 404, which varies by firm

size as discussed below. On June 5, 2003, SEC issued the first rule (SEC Release No.33-

27

8238) that sets June 15, 2004 as the compliance date of Section 404 for accelerated filers,

defined as firms whose public float is above $75 million by the end of the latest second

fiscal quarter. On February 24, 2004, SEC extended the compliance date for accelerated

filers to November 15, 2004 (SEC Release No. 33-8392). Hence for firms classified as

accelerated filers before 2004 the full impact of Section 404 on frauds would manifest

after November 15, 2004.

Before November 15, 2004 and since as early as mid 2003, Section 404 could have

affected frauds through the expectation of the rule’s impact and the audit already

commenced. Because this period is very close to the passage of SOX, it is difficult to

separate the impact of Section 302 and the early influence of Section 404. There are also

other provisions of SOX that came into effect before November 15, 2004. For example,

in early 2003 the SEC adopted a rule that requires publicly-listed firms to comply with

the audit committee requirements mandated by SOX (SEC Release No. 33-8220). A time

dummy variable for this period therefore measures the aggregate influence of these rules

and the early influence of Section 404, although this period is referred to as the “Section

302 period” for brevity. Nonetheless, in this period the early influence of Section 404

should be small because the majority of the accelerated filers would not have finished the

Section 404 review and audit of their internal controls by their auditors.

Firms not classified as accelerated filers before 2004 must comply with Section 404

once their public float exceeds $75 million. To account for their varying compliance

dates I perform a separate test of H5 for these firms. Firms that never became accelerated

filers by 2009 were permanently exempted by the Dodd-Frank Act of 2010 from the

28

auditor attestation requirement of Section 404(b) of SOX. Accordingly, I only test the

influence of Section 404 audit on frauds for non-accelerated filers that became

accelerated filers between 2005 and 2008.19

For these firms the Section 302 and Section

404 periods are separated based on each firm’s compliance date of Section 404.

I classify a firm as a non-accelerated filer if (a) its reported market value is under

$75 million in the second quarter of each fiscal year, and (b) it was not classified as an

accelerated filer in the previous year.20

Once a firm becomes an accelerated filer, it only

exits the accelerated filer status if its market value of equity falls below $50 million (SEC

Release No. 33-8644). Following this classification, I identify 3,154 firms that were

accelerated filers by November 15, 2004 (“early accelerated filers”) and 675 firms that

first issued Section 404 management report on internal controls in their 10-K reports after

November 15, 2005 (“late accelerated filers”). I then estimate the following logit model

on each of the previous samples to test H5:

( ) (3)

302START is a dummy variable that equals 1 for frauds committed between the

date SOX was passed and the compliance date of Section 404, and for non-sued firms if

their fiscal years are within this period. 302START measures the influence of the

provisions of SOX that came into effect in this period as well as the early influence of

19

Gao et al. (2009) show that some non-accelerated filers stay small to avoid Section 404 compliance. It is

unlikely that firms simultaneously engage in fraud to inflate stock prices and decrease firm value to avoid

SOX compliance. Nonetheless, this would also bias my results toward finding no impact of SOX. 20

I use market value instead of public float because COMPUSTAT does not have the latter information.

Since the regulation defines the accelerated filer status based on a firm’s public float, which in most cases

is lower than its market value, the smallest accelerated filers are potentially misclassified as non-

accelerated filers. The erroneous exclusion of very small accelerated filers could bias my conclusion toward

finding small or no impact of SOX if the post-SOX fraud reduction is greater for small firms.

29

Section 404. The sign of the coefficient on 302START represents the direction of this

aggregate influence on litigation risk. 404START is a dummy variable that equals 1 for

frauds committed after November 15, 2004 and for non-sued firm-year observations after

the same date. A negative coefficient on 404START would indicate that the litigation risk

in the Section 404 period is lower than in the pre-SOX period. Unless the probability of

fraud detection and litigation declines after SOX, negative coefficients on 302START

and 404START would indicate a declining probability of fraud commission over the

post-SOX period. H5 predicts that Section 404 has a greater impact on the risk of fraud

than other provisions implemented before Section 404, so the coefficient on 404START

would be more negative than the coefficient on 302START. The control variables include

all variables except for SOX_START in model (1).

4.3.2. Empirical Results of Fraud Reduction after Section 404 Compliance

I report the estimation results of model (3) for early accelerated filers in Column 1

of Table 4. The coefficients on 302START and 404START are negative and statistically

significant, indicating that the probability of fraud commission is lower in Section 302

and Section 404 periods than in the pre-SOX period. The Wald χ2 test rejects the null

hypothesis that the coefficient on 302START is less than or equal to the coefficient on

404START, consistent with H5 that the post-SOX fraud reduction is greater in the

Section 404 period than in the Section 302 period. Moreover, the marginal effect of

404START is -0.9%, much larger than the marginal effect of 302START at -0.13%. The

results suggest that Section 404 is more important than Section 302 in terms of fraud

prevention. The marginal effect of 404START at -0.9% is only smaller in magnitude than

30

the marginal effects of the standard deviation of stock returns at 1.2%, which illustrates

the economic importance of Section 404 compliance relative to other litigation and fraud

risk factors.

Next, I use model (3) to test H5 for late accelerated filers. Column 2 of Table 4

presents the results of the multivariate regression. Similar to the results in Column 1, the

coefficients on 302START and 404START are negative and significant, indicating that

the risk of fraud is lower in both periods than in the pre-SOX period. The coefficient on

404START is again lower than the coefficient on 302START and the difference is

statistically significant at the 0.05 level. In addition, if I change the dates when the firms

became accelerated filers to one year ahead or after the actual dates, I cannot find a

significant influence of Section 404 on the probability of litigation (results are not

reported). This robustness check provides support for my argument that Section 404 of

SOX contributes to the fraud reduction after SOX.21

For completeness, I estimate a similar model as the one in Column 3 of Table 3 to

test whether P(L|C) is higher in both the Section 302 and the Section 404 period. Instead

of replacing SOX_START in model (1) with SOX_FILE, I replace 302START and

404START in model (3) with 302FILE and 404FILE, dummy variables for frauds filed

21

Column 2 of Table 4 also shows a significantly negative coefficient on the FPS dummy, which suggests

that, in this sample, firms in industries other than biotech, electronics, computer and retail are more likely

to be sued for misleading financial statements. I examine the industry distribution and find that

transportation (SIC codes 4011-4731) and services (SIC codes 7000-7361, 7380-7997, and 8111-8744)

industries in this sample also have relatively higher proportion of firms engaging in fraudulent financial

reporting (results not reported). The insignificance of the coefficient on PPE could also be related to the

industry distribution in this particular sample. The transportation industry has a high ratio of tangible assets

to total assets (75%) while the services industry has much less tangible assets (39%), so the relation

between PPE and litigation risk declines substantially. Despite the different industry distribution in this

sample than other samples, the area under the ROC curve is 0.87, indicating that using this sample the

model’s ability to discriminate is excellent.

31

before and after Section 404 compliance. The estimation results of this regression, using

the sample of early accelerated filers, are presented in Column 3 of Table 4. The

coefficients on 302FILE and 404FILE are positive and significant, indicating that

litigation risk is higher in both sub-periods after SOX than before SOX. Following the

same reasoning in subsection 4.1.2, the results suggest that the higher litigation risk after

SOX is due to an increase in P(L|C). Negative coefficients on 302START and

404START would therefore imply a reduction in P(C). In the rest of the paper I follow

this interpretation without further distinguishing between the observed litigation risk and

the inferred probability of fraud commission.

Overall, the regression results in Table 4 are consistent with H5 that the post-SOX

fraud reduction is larger after firms’ compliance with Section 404.

4.4. Change in the Size of Damage after SOX

4.4.1. Sample Selection and Research Design

The actual damages of securities frauds are rarely specified in the lawsuit. There are

two possible measures of the size of damage: loss of a firm’s market value after the

disclosure of the alleged fraud, and the settlement amount of a lawsuit. Although the loss

of a firm’s market value is theoretically equivalent to the actual damages to investors,

empirical models using the market value change often overstate the damages by a large

amount.22

The settlement amount, on the other hand, has to be approved by the federal

court to be fair, adequate and reasonable. Hence I use the settlement amount to measure

the size of the damage and estimate the following model to test H3:

22

Cone and Laurence (1994) find that the overstatement can be as large as $270 million.

32

(4)

I define SETTLE as the natural log of the total settlement amount23

of a lawsuit. To

examine the impact of different provisions of SOX, I include two dummy variables:

SEC302 for frauds committed after SOX and before November 15, 2004, and SEC404

for frauds committed afterwards. SEC302 measures the influence of Section 302 plus the

early influence of Section 404 before firms began to issue Section 404 audit. SEC404

measures the full impact of Section 404 audit. H6 predicts that the coefficients on

SEC302 and SEC404 are negative but does not predict whether the coefficients would be

different. I use SEC302 and SEC404 instead of one dummy variable for the entire post-

SOX period to show the time-series change in settlement amount after SOX.

I control for other determinants of settlement amount following Cox and Thomas

(2004). I measure firm size (ASSET) as the natural log of a firm’s total assets measured

at end of the first fiscal year after the filing date of the lawsuit. Larger companies have

deeper pockets, so I expect a positive sign for ASSET. I define FINDISTRESS as the

change in Book-to-Market ratio from the filing date of a lawsuit to the date that the final

order is entered. Cox and Thomas (2004) use this term as a measure of financial

23

The dependent variable is not adjusted for inflation because the independent variables include firm size

(ASSET) and provable losses (LOSS).

33

distress.24

Theoretically, if the book value declines more than the market value, the

company would be less able to afford large settlements. The expected sign for this term is

negative. LOSS is a measure of the amount by which a firm’s market value is inflated by

the issuance of misleading accounting information. I use the improved two-trader model

in Finnerty and Pushner (2003) to more accurately measure the market value inflation.

Appendix B provides the details of the model. I expect LOSS to be positively related to

the total provable losses to investors and hence positively related to the size of the dollar

settlements. I define LENGTH as the number of months in the class action period, which

measures the number of damaged investors, and expect a positive sign for this term. ICW

is an indicator of whether a fraud case involves the firm’s or its auditor’s disclosure of

internal control weaknesses. HARD is a dummy variable that equals 1 if the lawsuit

involves an SEC legal action or financial restatements, and zero otherwise. Private

attorneys use ICW and HARD to support their claim that the alleged accounting

irregularities were committed intentionally or with severe recklessness. I expect that ICW

and HARD are positively related to the settlement amount.

My sample includes lawsuits filed between 1996 and 2008 that have available stock

returns and accounting data. I manually collect the information of whether each case

involves a firm’s disclosure of internal control weaknesses, SEC legal actions, and

financial restatements. I exclude lawsuits not brought by common unit or shareholders,

not involving allegations of Rule 10b-5 violations, and settled for less than $3 million.

24

Their measurement period for this term ends at the settlement of the suit. Although I do not have the

settlement date for every case in my litigation sample, for 704 lawsuits that I do have both the settlement

date and the finalized date, the settlement date on average is within six months prior to the finalized date.

The average length of the interval between the filing date of a suit and the finalized date is 3.5 years. Hence

my measurement period does not differ significantly from the period used in Cox and Thomas (2004).

34

The final sample includes 570 cases against US firms listed on the three national stock

exchanges from 1996 to 2008.

4.4.2. Regression Results

Figure 2 presents the change in the average and median settlement amount25

by the

commencement year of fraud. The average settlement amount increased sharply right

before the dotcom bubble burst, descended afterwards, and then rose again in the sub-

prime mortgage crisis period. Despite the surge in the 2006 to 2007 period, the average

settlement amount trended downward over time. In contrast, there is little change in the

median settlement amount. The different trends between the mean and median settlement

amount indicate that the reduction in the mean settlement amount is mainly due to fewer

large alleged frauds after SOX.

I report the multivariate regression results in the first column of Table 5, Panel A.

The coefficients on SEC302 and SEC404 are significantly negative, but the difference

between these coefficients is not statistically significant (p-value is greater than 0.9). The

average settlement amount of frauds committed after SOX is lower than before SOX by

around 40% (=exp(0.34)-1). These estimates indicate that the average settlement amount

declines shortly after the enactment of SOX, but somewhat surprisingly Section 404 does

not lead to any further change in the size of the settlement. This is different from my

earlier findings that the risk of fraud falls more following firms’ Section 404 compliance.

The coefficients on most of the other variables have signs consistent with expectation.

The settlement amount is positively related to firm size, the estimated amount of market

25

The values are adjusted to 1998 dollars. The nominal settlement amount shows the same pattern.

35

value inflation due to fraud, and the existence of ineffective internal controls, SEC

actions, and financial restatements. The coefficient on LENGTH is not statistically

significant mainly because LOSS has incorporated the impact of the number of investors

affected by fraud. Similar to the findings in Cox and Thomas (2004), the coefficient on

the measure of financial distress is not significantly different from zero. My inferences

are robust to the exclusion of lawsuits settled above $1 billion as shown in the second

column of Table 5, Panel A.

My hypothesis does not distinguish between possible reasons why SOX discourages

large frauds. Nonetheless, because the length of class action period is readily available, I

also explore whether the decline in the size of fraud damages is a result of timelier fraud

detection. If timelier detection of fraud contributes to the reduction in settlement amount

after SOX, the duration of fraud should be shorter when the settlement amount declines.

Table 5, Panel B shows the number of days in the class action period for frauds

committed before SOX, during the Section 302 period, and during the Section 404 period.

On average frauds starting in the pre-SOX period last for 435 days. In the Section 302

period, the duration of fraud becomes longer when the settlement amount declines over

the same period. These findings do not support the conjecture that earlier detection of

fraud is the reason why the size of damage drops after SOX. In the Section 404 period,

again the duration of fraud and the average settlement amount does not move in the same

direction. The length of the class action period drops to 350 days but the average

settlement amount does not change. The results are consistent with the hypothesis that

SOX discourages managers from committing large frauds, although the evidence is not

36

sufficient to rule out competing hypotheses that other 2002 events contribute to the

decline in the size of damage.

4.5. Additional Robustness Tests

One assumption in my research design is that frauds with different duration share

similar probabilities of detection and litigation. Table 6 shows the number and percentage

of frauds that were caught and litigated within the specified number of years since their

commission. On average 23% of frauds were discovered and litigated in the same year of

commission, 42% were caught and litigated in the following year, and this percentage

declines as the duration increases. These numbers indicate that the conditional

probabilities of fraud detection and litigation vary with the duration of frauds.

To check the robustness of my results to different durations of pre- and post-SOX

frauds, I repeat the estimation of the litigation risk regressions using a group of old frauds,

i.e., those litigated two years after commission. The untabulated results show that the

average marginal effect of SOX_START remains the same. Another way of examining

the impact of fraud duration is controlling for the duration directly in the regression. For

firms that are not sued in my sample period, I assume that the duration of fraud exceeds

the length of the sample period. My results are qualitatively similar after including a

duration factor (untabulated). In sum, different durations of pre- and post-SOX frauds do

not affect my inferences regarding the impact of SOX on the risk of fraud.